Embed Size (px)

Citation preview

1

Income Shocks and Household Risk-Coping Strategies: The

Role of Formal Insurance in Rural Vietnam

Development Economics Research Group (DERG)

University of Copenhagen (UoC)

Central Institute for Economic Management (CIEM)

Ministry of Planning and Investment (MPI) of Vietnam

Centre for Agricultural Policy (CAP)

Institute of Policy and Strategy for Agriculture and Rural Development (IPSARD)

Ministry of Agriculture and Rural Development (MARD) of Vietnam

Specific Authors:

Carol Newman*

Fiona Wainwright*

Nguyen Le Hoa**

Bui Thi Uyen**

Le Vu Ngoc Kien**

Luu Duk Khai***

Prepared under the Agriculture and Rural Development (ARD) Programme

Royal Embassy of Denmark of Vietnam

* Department of Economics, Trinity College Dublin and DERG/UoC

** CAP / IPSARD

*** CIEM

2

1. Introduction

A fundamental problem facing rural households in many developing countries is how

to maintain satisfactory levels of consumption in the face of adverse income shocks.

These shocks can affect a household’s welfare by negatively impacting on household

income, existing household wealth and the health of household members. This in-

depth study considers the various strategies rural households in Vietnam employ to

cope with adverse income shocks. We categorise shocks as either idiosyncratic (for

example, injury, illness, death, divorce, etc.) that affect an individual household or

income earner only, or spatially covariant (for example, a flood which affects all

households in a particular location) that can affect entire communities. In many cases

the former type of shock can be insurable in formal financial markets, while the latter

are generally non-insurable in a formal way due to supply-side constraints.

Using panel data from rural households in Vietnam, we explore the impact of adverse

income shocks on households based on a subjective measure of risk-coping ability

and supplement this analysis with an investigation of the consumption smoothing

ability of households. We also explore the extent to which savings stocks in the form

of liquid assets (livestock holdings, grain stores, savings and borrowings) are used as

a form of self-insurance or risk-coping strategy and the role that formal insurance

plays in reducing the need for self-insurance instruments.

In developing countries, exposure to risk remains a significant cause of poverty for

poor farmers (Fafchamps, 2009). The nature of the shock will have implications for a

household’s ability to cope and its consequences (Dercon, 2002). For example,

spatially covariant shocks, and, in particular, weather related events such as rainfall,

can negatively impact on human welfare.1 There is also much evidence to support the

detrimental effect that the occurrence of idiosyncratic income shocks can have on a

household (Morduch, 2004; Townsend, 1994; Udry, 1991). In addition to having an

impact on a household’s ability to cope, the nature of the shock is also important for

understanding the strategies households use to cope with its adverse consequences.

Idiosyncratic shocks can be insured informally at a community level, or, if available,

via formal insurance contracts with a third-party insurer. Recent literature suggests

that the lack of formal insurance, both in terms of market availability and actual take-

up, is one of the key drivers of persistent levels of poverty in developing countries

(Morduch, 2002). Spatially covariant shocks are more difficult to insure collectively

and formal insurance contracts are extremely rare for reasons of moral hazard and

adverse selection.2

Consequently, households living in risky environments must

develop alternative strategies to reduce the impact of shocks on their livelihoods

(Dercon, 2002).

1 For example, Alderman et al (2006) find that detrimental weather can impact on the nutrition and

height of children while Jacoby and Skoufias (1997) find that weather related events can affect school

attendance and enrolment. In contrast, Deaton (1997) finds that spatially covariant shocks in certain

villages in Cote d’Ivoire explain little of the variation in household income. 2 As well as supply side constraints Cole et al (2010) find that credit constraints and trust are significant

barriers to the uptake of rainfall insurance in India.

3

Alderman and Paxson (1994) distinguish between risk-management and risk-coping

strategies whereby the former attempt to affect how risky the income generating

process is (‘income smoothing’) while the latter deal with the consequences of income

risk, i.e. income shocks, after the event (‘consumption smoothing’). A considerable

body of literature on savings and consumption smoothing explores the concept of

precautionary savings (Zeldes, 1989; Kimball, 1990; Deaton, 1991, 1992; Udry, 1994).

The evidence suggests that in rural populations where credit constraints are binding,

inefficient savings behaviour is likely to occur.3 The savings of many poor households

appear to be a pre-emptive response to income shocks rather than a long term

investment decision. In addition to accumulating savings stores for precautionary (and

other inter-temporal) motives, evidence also suggests that risk-averse households

accumulate other forms of liquid assets for self-insurance purposes, which under

severe credit constraints they may be forced to sell to smooth consumption.4

In this paper we explore the extent to which rural households in Vietnam cope with

adverse income shocks. Our data come from the Vietnamese Access to Resources

Household Survey for 2006, 2008 and 2010 and include detailed information on

households’ financial resources, access to and purchase of formal insurance, and the

incidence of idiosyncratic and spatially covariant shocks. We distinguish between

spatially covariant and idiosyncratic shocks and also consider the extent to which

formal insurance contracts and precautionary savings instruments help households to

cope. Our primary hypothesis is that in the absence of formal insurance contracts for

spatially covariant risk transfer, a risk-averse household engages in precautionary

savings strategies to buffer against forms of spatially covariant risk while formally

insuring against forms of idiosyncratic risk. In addition to forms of household savings

(for example, formal savings instruments, informal savings and ROSCAs), this paper

also considers other forms of asset accumulation in the form of livestock holdings and

crop stores as precautionary saving strategies against spatially covariant risk, as well

as borrowing.

The remainder of the paper is organised as follow. Section 2 provides some relevant

background on Vietnam highlighting the vulnerability of households to adverse

income shocks and the state of development formal financial markets (credit, savings

and insurance) in terms of their ability to help households cope with such shocks.

Section 3 outlines the empirical approach used to explore these issues while Section 4

describes the data. Section 5 discusses the empirical findings and Section 6 concludes.

2. Vietnamese Background and Context

2.1 Vulnerability to shocks

Macroeconomic instability, high inflation and underdeveloped legal systems can have

a significant negative impact on the value of household resources. In developing

countries, however, other types of risk are also common leading to extremely variable

3 Udry (1994) found evidence of precautionary savings in rural villages of northern Nigeria where he

showed that these households saved significantly in anticipation of transitory shocks. Deaton (1992)

found that significant savings were made in anticipation of income shocks in Cote d’Ivoire. 4 Rosenzweig and Wolpin (1993) provide evidence that farmers sell bullocks when faced with an

unfavourable crisis in Icrisat villages in India. Fafchamps et al (1998) find that livestock transactions in

the West African semi-arid tropics are responsive to income fluctuations while Lim and Townsend

(1998) find that the most effective approach to risk-coping at the household level is by self-insurance

through in-kind saving (for example, building up grain reserves and drawing them down as required).

4

incomes particularly for the most vulnerable groups. For example, adverse

movements in agricultural prices, unstable employment opportunities, or natural

disasters can all have a profound effect on households, particularly those relying on

agriculture for subsistence and their livelihoods.

In Vietnam households and individuals are particularly exposed to adverse income

shocks with those involved in agriculture the worst affected. According to a recent

UN report, Vietnam is one of the top ten countries in the world affected most by

natural disasters. Data from the Vietnamese Ministry of Agriculture and Rural

Development show that the total damage caused by natural disasters annually is about

1.5 percent of GDP, affecting 9,000 people and causing the death of 466 people. The

agricultural sector suffers more than all others.5 Between 1990 and 2008, Vietnam

experienced 194 extreme weather events. In 2008, there were 515 deaths, over

230,000 ha of rice and crops were completely destroyed, 1 million units of livestock

died, 54,000 ha of aquaculture property was damaged and 4,700 houses collapsed or

were swept away. In total, the total damage caused by natural disasters in 2008 was

estimated at over 11,500 billion VND.6 Agricultural production and rural areas were

affected the most.

Aside from weather related events, crop insects and animal diseases are also common

given the hot and humid tropical climate in Vietnam. In addition, given that most

Vietnamese farmers are smallholders, the knowledge and resources to prevent the

spread of disease are low. The Highly Pathogenic Avian Influenza (HPAI) was first

discovered in Vietnam in mid-2003. Since then, the country has endured 5 waves of

outbreaks with various government and international agency responses (Magalhaes et

al., 2006; Agrifood Consulting International, 2006). Over 51 million units of poultry

were destroyed with the total damage estimated at approximately 10,000 billion VND.

Other common diseases affecting livestock include New Caste, Gumboro, and Fowl

cholera. According to the National institute of Animal husbandry, approximately 40

to 53 percent of poultry is infected by New caste disease annually while 27-32 percent

are infected by Gumboro and a further 14-15 percent by Fowl cholera. The death rate

of free-range chickens from hatching to adulthood is 47 percent with costs for

veterinary medicine accounting for up to 10-12 percent of total costs.7 A recent

research report into the competitiveness of livestock in Vietnam found that livestock

disease occurred in all provinces investigated (12 in total) between 2008 and 2010.

The highest infection rate was in Long An with disease evident in approximately 70

percent of communes.8

Nguyen (2003) estimates that between 5 and 10 percent of Vietnam’s population is at

risk of poverty. Oxfam, using participatory poverty monitoring in rural communities

between 2005 and 2010, found that exposure to risk and adverse income shocks

increase the vulnerability of households, particularly the rural poor.9 Aside from price

volatility and natural disasters, the most common problem cited by farmers as

affecting livelihoods is the inability to work due to health problems. Moreover, when

asked about the risks and challenges anticipated in the coming 12 months, inability to

5 http://vnexpress.net/gl/xa-hoi/2007/10/3b9fb183/

6 Số liệu của Tổng cục Thống kê

7 http://www.vcn.vnn.vn/PrintPreview.aspx?ID=5616

8 LIFSAP: Livestock competitiveness and food safety project, report 2010

9 Participatory poverty monitoring in rural communities in Vietnam – Oxfam, Action aid, 2005-2010

5

work is cited as the most common concern. For the poor who lack capital, land and

education, labour is the most valuable asset and so the risk of ill-health which

prevents them from working and requires expensive health treatment is of particular

concern. Nguyen (2003) identifies five distinct groups of households that are

particularly vulnerable to risks of this kind. They include, female-headed households,

ethnic-minority households, landless households, poor households, and households

located in the Red River Delta area.

In summary, Vietnamese households are particularly exposed to significant adverse

income shocks and the most vulnerable groups in society are most affected. These

shocks range from weather related events and crop and livestock disease to

macroeconomic factors such as inflation and price instability. For the poorest

households health related risk is also of particular concern.

2.2 Formal coping mechanisms

Households can cope with adverse income shocks in a variety of ways. The optimal

form of risk coping is through insurance contracts that cover households income

losses in the event of an adverse shock. Vietnam’s insurance market is one of the

fastest growing markets in the world. Between 2000 and 2009, the Vietnamese life

insurance sector increased from US$51.12 million to US$671 million, and the non-life

sector from US$126 million to US$763 million (Business Monitor International Ltd.,

2010).10

According to the Vietnam Insurance Association, there are more than

120,000 insurance agents operating in Vietnam. The sector, however, is still small in

size and only a limited range of insurance products are available. The total value of

insurance premiums in Vietnam accounted for less than 2 percent of GDP in 2005,

compared to 9.5 percent in the US, 8.7 percent in the EU and 10.5 percent in Japan

suggesting that there is significant scope for growth in this sector in the future.

Health insurance products have developed particularly rapidly in Vietnam. The

percentage of patients (in-patient and out-patient) with health insurance or a free

health care certificate increased rapidly from 37.4 percent in 2004 to 66.7 percent in

2010.11

User fees for health care services were introduced in 1988 resulting in

significant increases in out-of pocket expenditure on health by households.

Compulsory health insurance schemes were instituted to redress the issues of access

by the poor but the main participants in health insurance plans are the better off

households (Wagstaff and Nguyen 2002).

Agriculture insurance, covering risks related to agricultural production, has the

potential to make a significant impact on the risk coping ability of rural farmers given

the dependence of the Vietnamese population on agriculture and the high degree of

exposure to agriculture related risk. However, agricultural insurance markets are

virtually undeveloped in Vietnam.

Approximately 1 percent of farmers are insured to protect against damage to crops,

0.24 for cattle, 0.1 percent for swine and 0.04 percent for poultry. Up to 2008, two

insurance companies provided agricultural insurance on a small scale: Baoviet and

Groupama. However, these businesses were found to be unprofitable and so only

10

Vietnam Insurance Report Q1 2010, Business Monitor International Ltd. 11

VHLSS 2010 -GSO

6

existed for a short time.12

In response, the Prime Minister issued Decision 315/QD-

TTg on the pilot provision of agriculture insurance in 20 provinces and cities across

Vietnam from 1st July 2011. Under the Decision, agricultural insurance will cover

paddy, livestock and poultry, and aquaculture. The State will pay the full insurance

premium for the poor and farming households and 80 percent of the insurance

premium for the nearly poor farming households. In addition, an exemption of 60

percent will be given to other farming households and 20 percent for agricultural

organisations.13

2.3 Informal coping mechanisms

While insurance markets exist in Vietnam, like many developing countries they are

not well developed and so many households must rely on other coping mechanisms.

Nguyen (2003) finds that the main risk-coping strategies adopted by households in

Vietnam are self-insurance strategies including selling assets, withdrawing savings,

borrowing from relatives and friends, or using credit. She also finds evidence however,

that Vietnam’s current safety net system fails to protect the most vulnerable groups.

Research by VASS and Oxfam finds that many poor households reduce consumption

in order to cope with income shocks. This is particularly the case for poor households

who are more likely to reduce the quantity and quality of their meals and healthcare

expenses than non-poor households. Non-poor households are more likely to reduce

social expenses (funerals, weddings, etc.) or rely on savings when faced with adverse

income shocks reducing the need to cut down on food and healthcare expenditure.

Selling assets such as livestock is also common among wealthier households.

Social support from communities and organisations is also important for the poor in

overcoming adverse income shocks. A long tradition and culture of risk sharing exists

in small communities in Vietnam. This includes support from friends and relatives but

also support from mass organisations such as the Women’s Union, Farmers’

Association, Veterans’ Association, and the Youth Union.

2.4 Government coping mechanisms

Government support to help individuals and communities cope with risks is provided

through various social protection policies. These policies cover three circles: the outer

circle includes measures for capacity building in risk mitigation and the reduction of

vulnerability such as vocational training, career orientation, agriculture extension,

support for poverty reduction, etc; the next inner circle includes prevention and

mitigation measures through insurance mechanisms including social insurance,

medical insurance and others; the innermost circle includes protection measures

through direct social support extended to those affected by risks through Decree

67/CP, and covers shocks relating to natural disasters and diseases.14

Vietnam’s public safety net covers a broad range of areas, including social protection,

hunger eradication, poverty reduction, social insurance, health insurance, and

employment and unemployment services. Initiatives are also carried out to assist

elderly people living alone, children in especially difficult circumstances, disabled

12

http://www.taichinhvietnam.com/taichinhvietnam/modules.php?name=News&file=article&sid=159 13

http://www.vietlaw.gov.vn/LAWNET/ 14

Participatory poverty monitoring in rural communities in Vietnam, Synthesis report, round 2, 2008-

2009

7

people, victims of natural calamities, and periodically starving people. In principle,

this safety net is designed by the government to help social beneficiaries, especially

those in vulnerable groups, with below minimum standards of living. In practice,

however, their effectiveness is unclear as they tend to be poorly funded and largely

reliant on scarce local resources. For example, in 1999 almost 1 million people were

eligible for such assistance but only 20 percent of them actually received an allowance

(MOLISA 1999b). Pensions and other employment-related social insurance payments

are provided only to workers in the formal sector (Nguyen, 2003).

3. Empirical Approach

Economy theory suggests that in risky environments, where no insurance markets

exist, households will accumulate precautionary savings and assets in order to protect

themselves against income and wealth variability. Precautionary savings, however,

are inefficient in the sense that they divert resources from productive investments and

from consumption. If risk can be insured through formal insurance contracts, then risk

averse households will choose to purchase insurance to protect themselves against

future income variability. In many developing countries formal insurance markets are

not well developed and will only offer insurance products that cover certain types of

risk and mainly risk that is idiosyncratic in nature. Aggregate or spatially covariant

risks, such as flooding or pest and livestock disease, are rarely insurable in formal

markets. Theory suggests that households will save and purchase insurance in order

to smooth consumption over time and so the realization of adverse income shocks

should not affect consumption levels between one period and the next but households

with insurance will precautionary save less than those without given that the

uncertainty associated with income due to idiosyncratic risks is eliminated.

Our empirical investigation focuses on: the extent to which households manage to

cope with adverse income shocks and whether this is reflected in their consumption

smoothing ability; the role of precautionary saving as a coping mechanism; and

whether formal insurance reduces the need for precautionary saving. We use three

separate empirical investigations to explore these issues. First, we use a subjective

measure of coping ability to analyse the determinants of households’ ability to cope

when faced with adverse income shocks. We exploit the panel dimension to our data

by using a fixed effects linear probability model that controls for time invariant

household heterogeneity. Time varying household characteristics are also included as

control variables. The key explanatory variables of interest are the different types of

income shocks and the severity and persistence of these shocks.

Second, we consider the extent to which households smooth consumption over time in

the face of income shocks of different types and consider whether consumption

smoothing ability varies depending on the presence of savings and formal insurance.

We first estimate parameters for a standard household consumption equation which

can be used to predict consumption levels that are consistent with consumption

smoothing. We then test the extent to which actual and predicted consumption levels

are statistically different. We analyse the extent to which deviations from permanent

consumption levels are attributable to shocks and explore whether these deviations are

correlated with savings and insurance instruments. To obtain parameters for the

general consumption function that represents households’ consumption smoothing

preferences we estimate a fixed effects regression of consumption on income, wealth

8

and other relevant explanatory factors that are consistent with the permanent income

hypothesis including age, education level of the household head, household size, etc.,

only using households that were not exposed to any shocks. The following model is

estimated separately for each region.

2

0 1 2 3 4 5

6 7 8

it it it it it it

it it it i it

lnCons ln Income lnWealth lnCredit Age Age

Education Sex Size u e

(1)

We use the estimated coefficients from equation (1) to predict household consumption

in each period using the observed data on each explanatory variable in that period.

Income reported lost due to adverse shocks in each period is added back in order to

capture the true ceteris paribus predicted level of consumption. If households manage

to smooth consumption then the estimated level of consumption, which takes into

account changes in observable consumption determinants should be the same as the

actual observed level of consumption in that period. We use a simple t-test to test for a

statistically significant difference between the two measures. Failure to reject the null

hypothesis will provide evidence of consumption smoothing. This test is performed

across different household groupings according to the category of shocks suffered,

whether savings or formal insurance are present and household income levels.

The second stage of our empirical investigation explores the mechanism of

consumption smoothing invoked by the household. There is ample evidence that

households across the developing world accumulate savings and liquid assets as a

form of precautionary saving (Fafchamps, 2009; Deaton, 1992; Deaton, 1991). As

discussed in Fafchamps et al (1998) and Newman et al (2011) households will choose

a portfolio of liquid assets which will depend on the individual returns to each type of

asset as well as the variance and co-variances of returns. In this paper we consider a

variety of different liquid asset types including formal and informal savings, livestock

holdings, crop stores and forms of borrowings (including formal and informal loans).

We expect households to allocate total savings (including any precautionary

component) across a range of different assets to buffer against unexpected income

shocks.

Identifying a causal relationship between the occurrence of an adverse income shock

and the depletion of the stock of liquid assets is complicated given that the effect of

the shock may be difficult to separate from other factors that may deplete household

liquid assets. For example, households that suffer the death of a family member may

have already begun depleting liquid asset stocks if that household member required

medical treatment for some time in advance of his or her death. The relationship

between shocks and the depletion of liquid assets can be identified using a panel

fixed-effects approach under certain assumptions. Our data facilitate the

disaggregation of overall shocks into their exogenous (spatially covariant) and

idiosyncratic components. Exogenous spatially covariant shocks are further

disaggregated into 1) economic (for example, crop price changes, key input price

changes/shortages) and 2) natural (for example, floods, typhoons, droughts etc)

components while our raw data motivate the classification of idiosyncratic shocks as 3)

insurable (for example, illness, injury or death of household member) and 4)

uninsurable (for example, crime/theft, divorce, family disputes etc). By their nature,

idiosyncratic shocks may be correlated with unobserved household characteristics that

affect a household’s financial decision making. Using a fixed effects estimation

9

procedure will eliminate any time invariant unobserved heterogeneity while the

inclusion of control variables for wealth, income, education and other household

characteristics attempt to capture any remaining time varying heterogeneity. The full

household level fixed effects model we estimate is given by:

ittiit

itititititit

ititit

ititititit

ev

dTransdNatdFreeInsdIdioIdInsdIdioI

dTransdFreeInsdIns

dIdioUdIdioIdEcondNata

9

1098

765

4321

'

δZ

(2)

Where 1

n

it itiA a

represents the aggregate household liquid asset value under

consideration adjusted to 2010 present values, itdNat ,

itdEcon , itdIdioI and

itdIdioU

are dummy variables indicating spatially covariant natural and economic and

idiosyncratic insurable and uninsurable shocks respectively, itZ represents a vector of

time variant household characteristics (including wealth levels which act as a proxy

for time variant household risk aversion), t represent time dummies,

iu

is a

household specific fixed effect and it

is the household random error term. We

assume that regional differences which control for insurance supply side variations

and asset pricing variations across regions (including variance/co-variances of asset

returns) are subsumed within the household fixed effect while the time dummies

control for average changes in asset values over time.

Our model also includes the binary variable, itdIns , which indicates whether the

household made any insurance claims on insurance contracts purchased (either

voluntary or compulsory) during the time period. The model also includes an

interaction term, itit dInsdIdioI * , capturing the effect on household liquid asset levels

of those households suffering an idiosyncratic and insurable shock and making an

insurance claim. We also include interactions between itdFreeIns , which captures

whether the household claimed insurance from state provided free insurance policies,

and the incidence of insurable idiosyncratic shocks. Our hypothesis is that the

estimated coefficients on both level and interaction terms should be significant with

the interaction term signalling the degree to which insurance serves to ease the

depletion of the liquid asset under financial stress.

Our analysis is further extended to consider the extent to which other risk-coping

strategies may serve to lessen the depletion of liquid assets. We consider public and

private transfers through the dummy itdTrans as an alternative way to smooth

consumption in the face of an adverse income shock.15

Government aid programs may

also act as an important safety net for those households suffering spatially covariant

natural shocks and this effect is captured through the interaction term it itdNat * dTrans .

15

While anecdotal evidence suggests that the Vietnamese government provides assistance via transfer

payments to households severely affected by natural disasters, the majority of public transfers in our

data are in the form of pensions and transfers from children. If households expect transfers in the event

of an income shock then they could be viewed as safety-nets that act as a substitute for insurance. It is

not clear whether this is the case for our sample of households, although given that there are no

insurance products available to protect against income losses associated with natural disasters it is

unlikely that the safety-net component of transfers will affect our results.

10

If external transfers help to lessen the depletion of liquid asset holdings in the event of

an adverse idiosyncratic or natural shock we would expect the coefficient on these

interaction terms to be positive and statistically significant.

4. Data

The data are taken from the Vietnam Access to Resources Household Survey

(VARHS) for 2006, 2008 and 2010 (CIEM et al, 2007; 2009; 2011). This survey was

carried out in rural areas of 12 provinces of Vietnam in the summer of each year

producing a balanced panel of 2,045 households spread over 161 districts and 456

communes.16

The survey was conducted during the same three month period each

year to ensure consistency and facilitating reasonable comparisons across time. The

VARHS explores issues surrounding Vietnamese rural households’ access to

resources and the constraints that these households face in managing their livelihoods.

Along with detailed demographic information on household members, the survey

includes sections on household assets, savings, credit (both formal and informal),

formal insurance, shocks and risk-coping, informal safety nets and the structure of

social capital. The full set of explanatory variables used in this analysis is described in

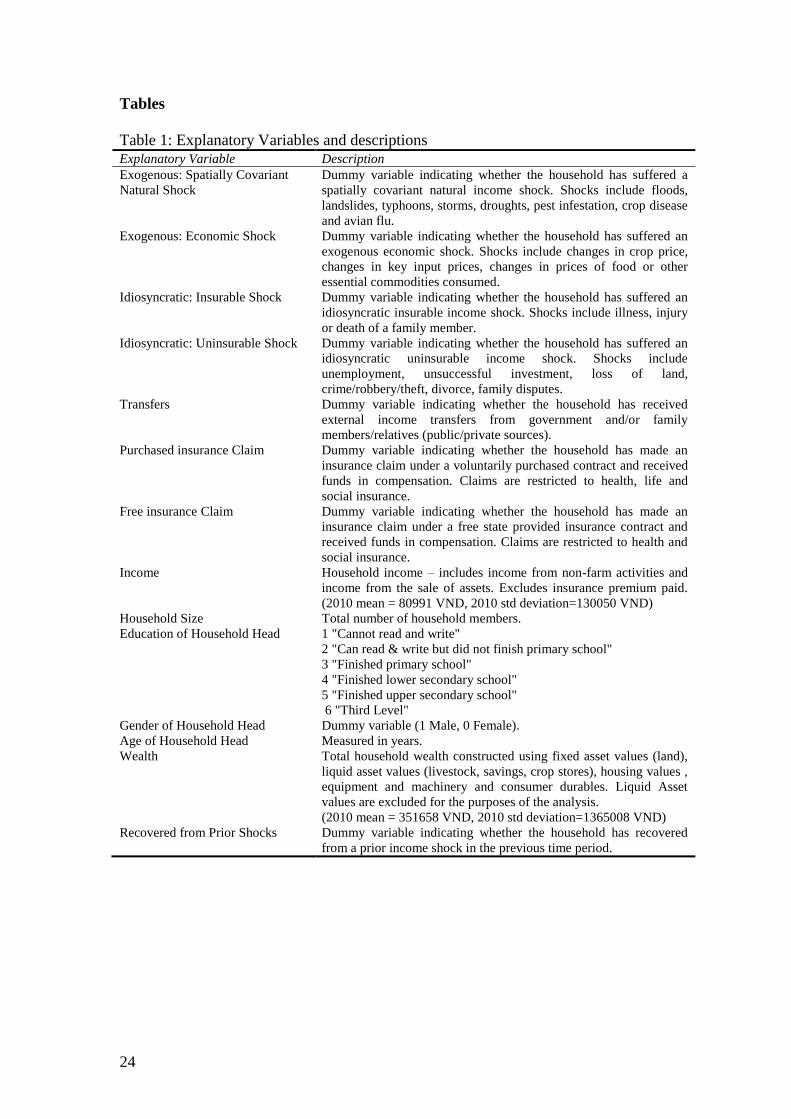

Table 1.

[INSERT TABLE 1 ABOUT HERE]

Information on income shocks are gathered by asking households to rank the shocks

suffered in order of importance and to provide an associated monetary loss in terms of

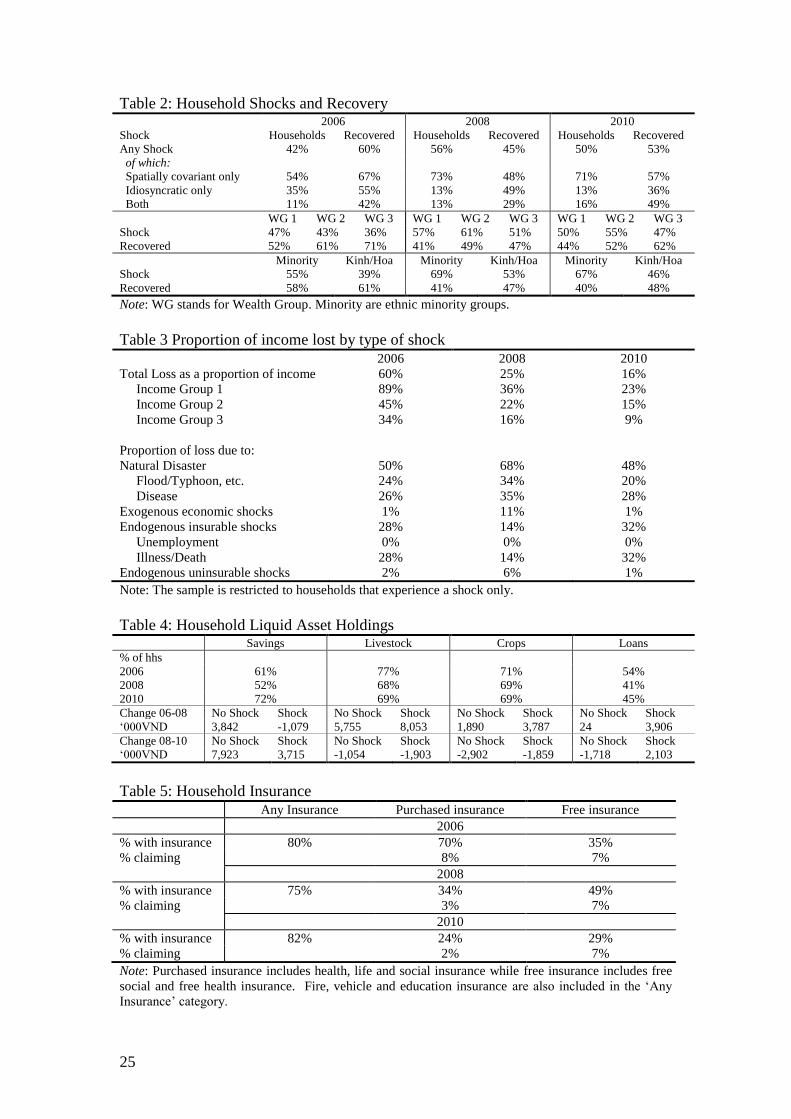

Vietnamese Dong (VND). Table 2 provides a more detailed breakdown of income

shocks and their sub-categories.

[INSERT TABLE 2 ABOUT HERE]

We find that that 42 per cent of households suffered an adverse income shock

between 2004 and 2006, 56 per cent between 2006 and 2008 and 50 per cent suffered

between 2008 and 2010. At a disaggregated level, in 2008 we find that 13 per cent of

households suffered an idiosyncratic shock only (down from 35 per cent in 2006)

while 73 per cent suffered an exogenous spatially covariant shock only thus providing

some support toward the dominance of spatially covariant over idiosyncratic shocks.

In 2010, spatially covariant shocks also dominate idiosyncratic shocks by 71 per cent

to 13 per cent, respectively. In 2006, 60 per cent of households report that they fully

recovered from the income shocks compared with 45 per cent and 53 per cent in 2008

and 2010, respectively, suggesting that households’ ability to cope has fallen over the

sample period. Recovery is less likely where households experience both spatially

covariant and idiosyncratic shocks.17

Disaggregating the household shock and recovery data across wealth groups reveals

that in all years, households in the wealthiest group suffer the least from income

shocks. Wealthier households are also more likely to recover from income shocks.

16

The survey was developed by the Development Economics Research Group, Department of

Economics, University of Copenhagen and the Institute of Labour Studies and Social Affairs, Hanoi

Vietnam. 17

Households are asked whether they have fully recovered from the effects of the adverse shock(s)

suffered during the current timeframe and this measure is therefore subjective.

11

These data suggest that while income shocks are problematic for households in all

wealth groups, recovery is more difficult for poorer households. We also find that a

greater proportion of ethnic minority households suffer from shocks and also

experience a greater number of shocks in all years. They also find it more difficult to

recover from the shocks suffered. Further analysis of the differences across

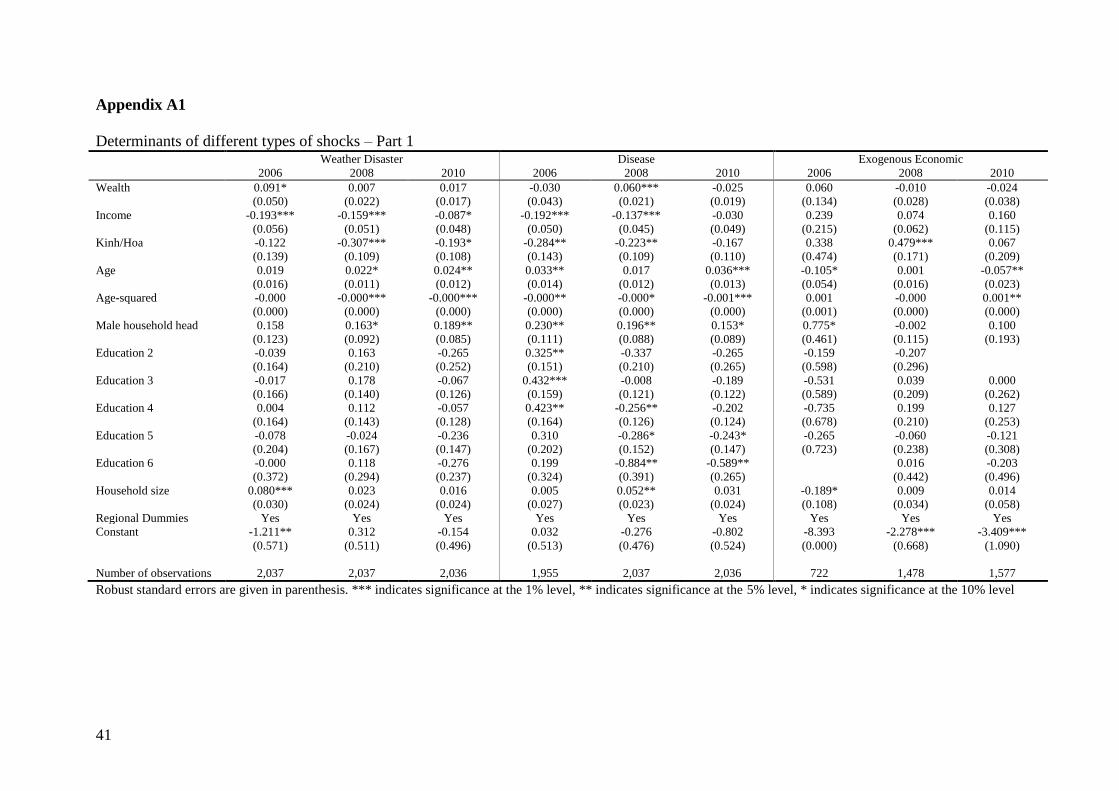

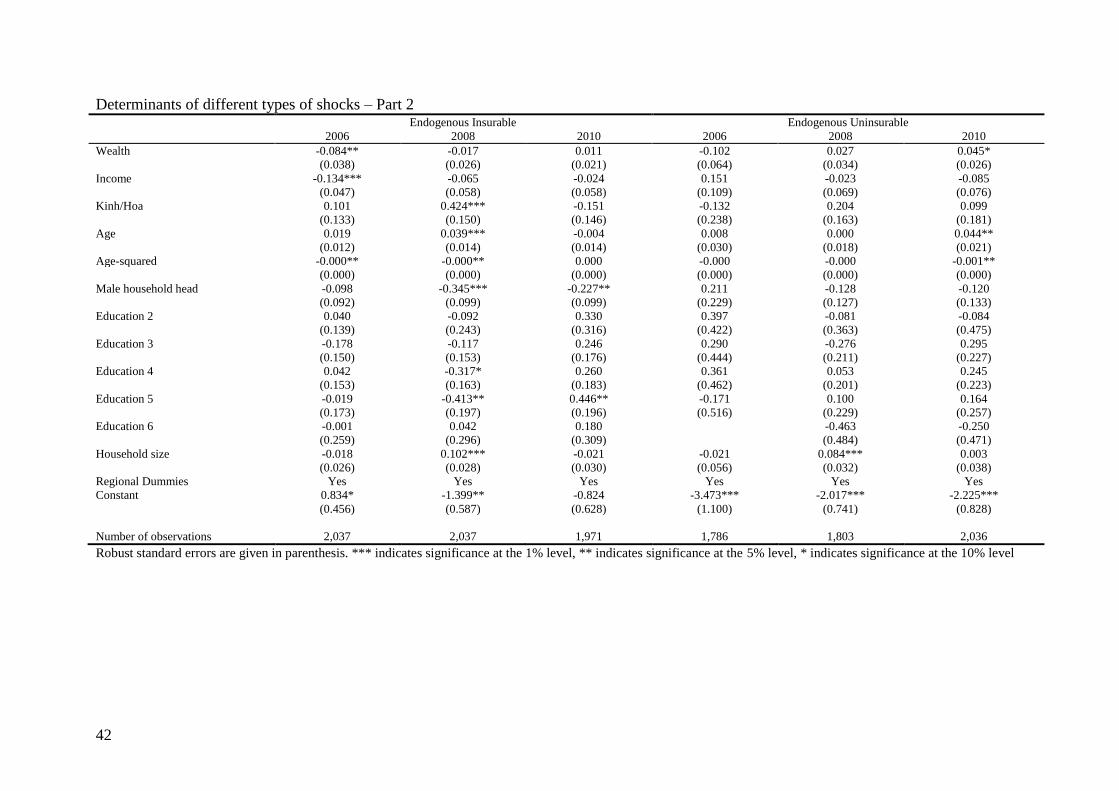

households in the incidence of shocks is provided in Appendix A1 where the

probability of each type of shock is regressed against a series of household

characteristics. The results suggest that low-income households and ethnic minorities

are the most vulnerable, particularly to the occurrence of natural disasters.

The extent of the losses to household income as a result of shocks varies considerably

over time. As revealed in Table 3, the size of losses fell from 60 percent of income in

2006 to 15 percent of income in 2010. In all cases, however, households in the lowest

income group suffer the greatest proportional losses. Natural disasters are the most

significant type of shock suffered followed by illness or death of a family member.

[INSERT TABLE 3 ABOUT HERE]

Table 4 describes the liquid asset holdings of households and how they are

accumulated or depleted for households that experience shocks. We find that the

proportion of households with savings increased between 2006 and 2010 from 61 per

cent to 72 per cent of households.18

The proportion of households with other types of

liquid asset holdings is relatively similar in each year while the proportion of

households with loans fell between 2006 and 2010.

[INSERT TABLE 4 ABOUT HERE]

Table 4 also details the change in the average value of different types of liquid asset

holdings of households between 2006 and 2008 and between 2008 and 2010,

disaggregated by whether the household experienced a shock or not. Households that

suffered a shock between 2006 and 2008 reduced their savings by an average of 1

million VND while households that did not suffer a shock increased their savings

levels. In contrast, between 2008 and 2010, all households increase their savings

levels on average, but households suffering from shocks increase their stock of

savings by less than those not suffering. We also find that the amount of loans

outstanding increases for households that suffer shocks which suggests that

households may turn to credit in times of financial stress.

In recent years, the Vietnamese formal insurance sector has experienced substantial

growth in terms of market penetration (see Section 2).19

The raw data reveal that

insurance is held by 82 per cent of households in 2010 (see Table 5). This includes all

types of insurance, voluntary and compulsory. Of those 24 per cent of households

hold purchased insurance contracts that insure them against the types of idiosyncratic

risks considered in our empirical analysis (health, life and social) and 29 percent of

households hold free insurance provided by the government (health and social).

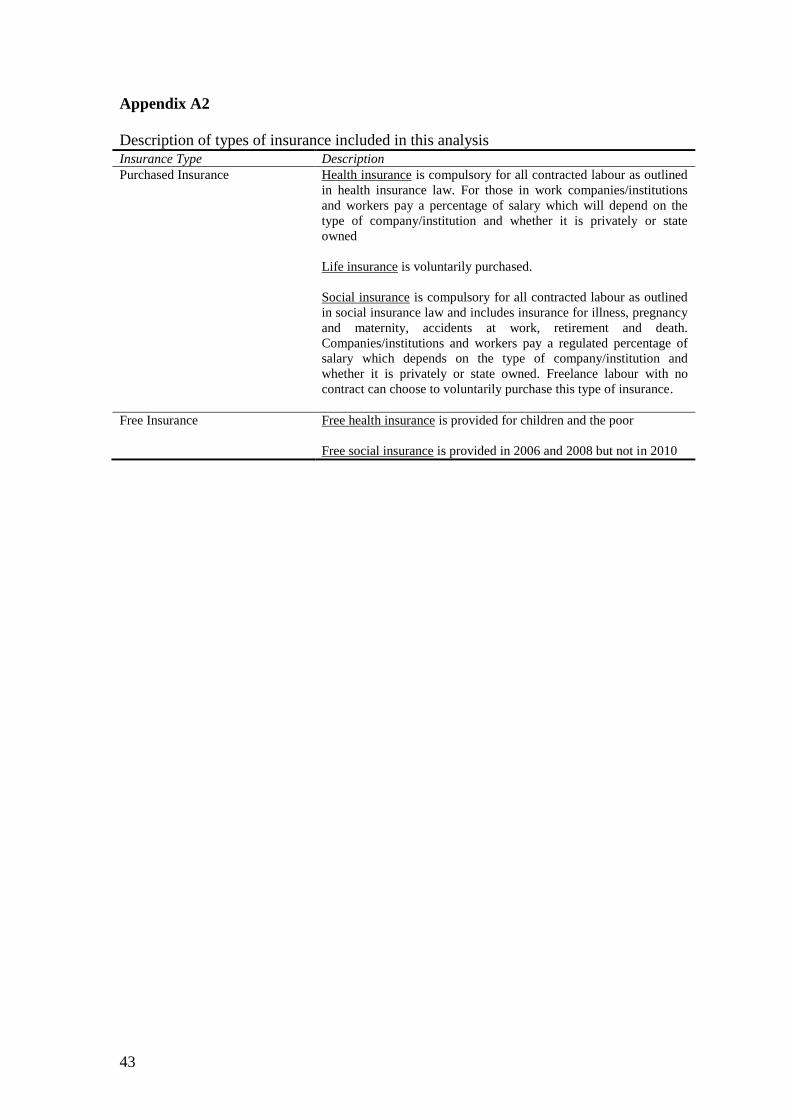

Appendix A2 provides a brief description of each type of insurance. While over time

the uptake of insurance has increased between 2006 and 2010, the proportion of

18

In 2008 only 52 per cent of households had savings which may reflect that difficult year that many

rural households in Vietnam had in 2008 due to the food price crisis and inflation which followed. 19

The Knowledge Centre forecast formal insurance market growth of 12% between 2007 and 2011.

12

contracts which are voluntarily purchased is much lower in 2010 compared with 2006.

This is most likely due to the introduction of other types of risk coping mechanisms

by the Vietnamese government during the time period (see Section 2).20

[INSERT TABLE 5 ABOUT HERE]

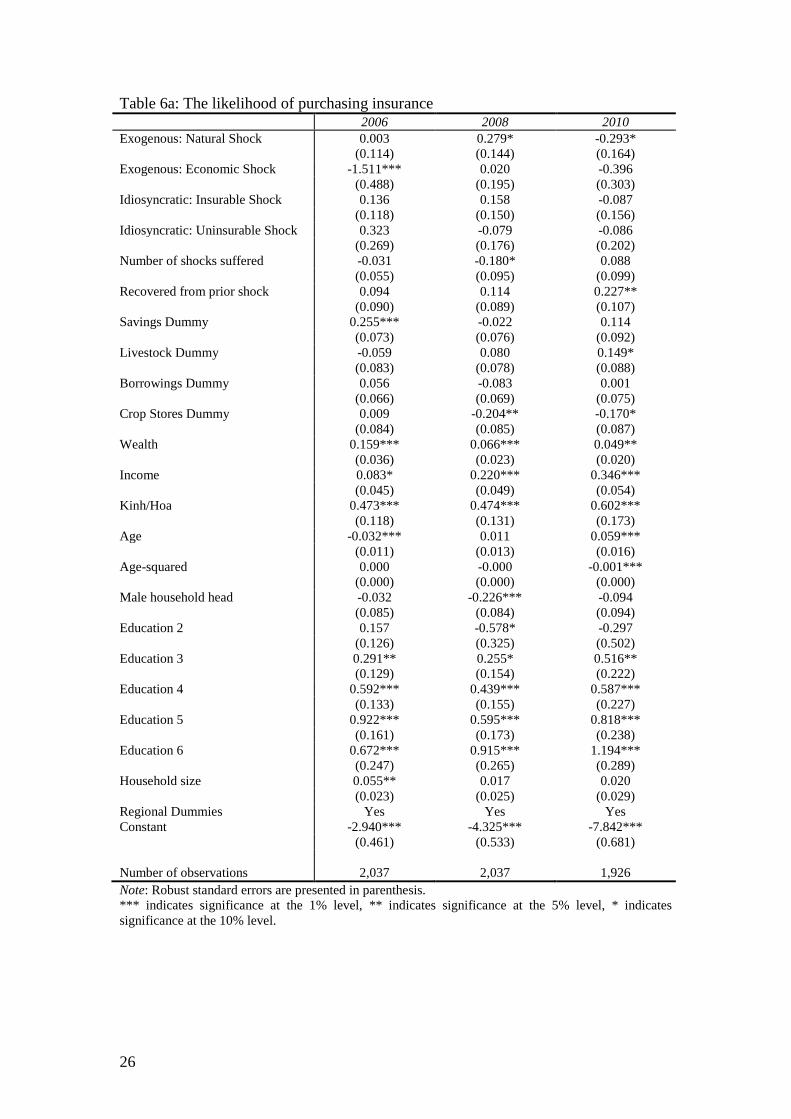

As a guide to the profile of households holding purchased insurance, we also estimate

a simple probit model of purchased insurance participation and free insurance held for

each year of our data. The results for purchased insurance are presented in Table 6a

and for free insurance in Table 6b.21

Although subject to potential endogeneity bias

with respect to unobserved heterogeneous risk aversion (and other factors), the results

suggest that the probability of a household holding formal insurance is correlated with

the education level of the household head, household wealth and income.22

There is

also evidence that ethnicity plays an important role with households of Kinh or Hoa

origin much more likely to hold purchased insurance. The level of savings of the

household is also highly correlated with the likelihood of purchase of insurance in

2006. Overall, the consistency over the years of the correlation between insurance and

education, wealth, income and ethnicity, suggests that information or financial

constraints may exclude some households from insurance markets.23

This should be

borne in mind when interpreting our later findings.

[INSERT TABLES 6a AND 6b ABOUT HERE]

The results for free insurance, presented in Table 6b, are the opposite to what is found

for purchased insurance. Poorer households are less likely to have free insurance as

are households of Kinh or Hoa ethnicity. Male headed households are also less likely

to have free insurance. We also find a negative association between education and

free insurance but a positive association between household size and the incidence of

holding free insurance. These results are consistent with Vietnamese policy of

providing social safety nets to the poorest and most vulnerable groups as discussed in

Section 2.

5. Empirical Results

The summary statistics presented in Section 4 help to motivate the central research

questions of this paper concerning household risk-coping mechanisms and their

effectiveness. As discussed in Section 3, there are three parts to our empirical

investigation of these issues. First, we estimate a fixed effects linear probability model

of households’ ability to cope with shocks. The measure used is the households self

reporting of whether they recovered from the shock suffered. Second, we focus on

consumption responses to adverse shocks to gain an understanding of the extent to

which households manage to smooth their consumption over time and whether this

20

It should be noted that insurance against spatially covariant risk (for example, rainfall insurance) is

not available to households in our sample. 21

The Knowledge Centre forecast formal insurance market growth of 12% between 2007 and 2011. 22

This result is consistent with the findings of Cole et al (2010) in relation to rainfall insurance in India. 23

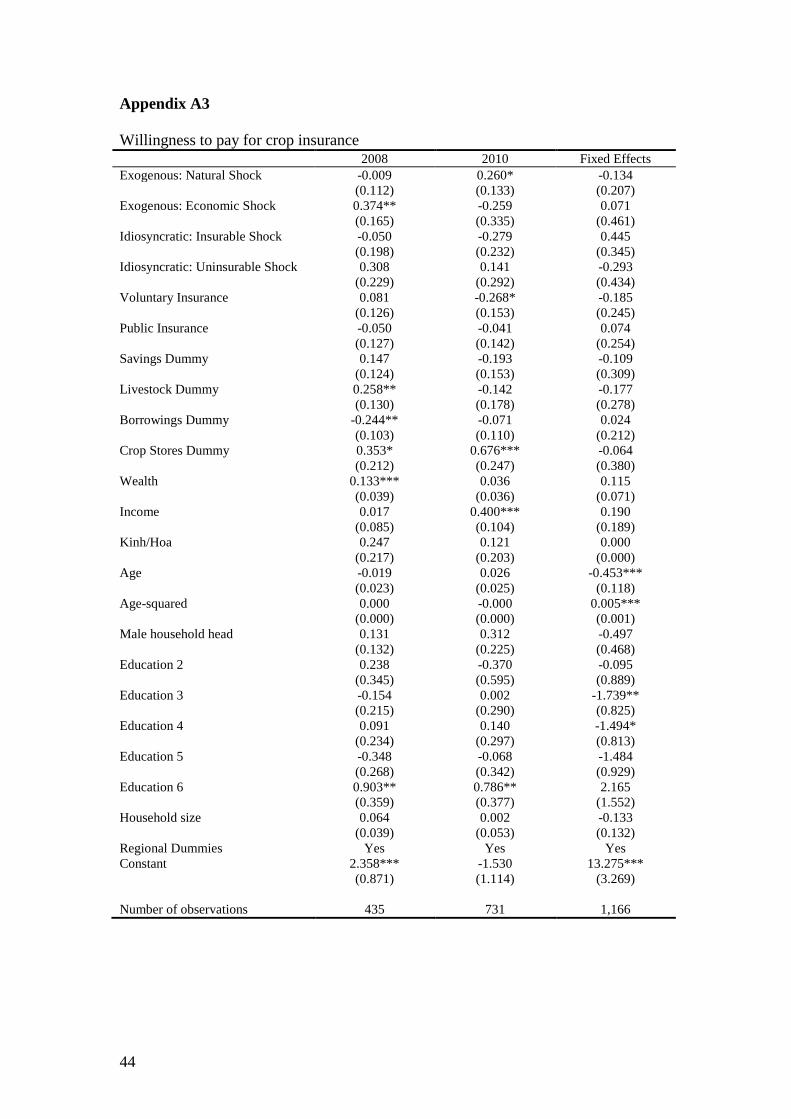

When households were asked whether they were willing to pay for crop insurance specifically wealth

and income were found to be the most important determining factors. Results are presented in

Appendix A3.

13

relates to their holdings of liquid assets and formal insurance. Third we examine the

depletion of household liquid assets in response to adverse income shocks to

determine whether these assets serve precautionary or self-insurance purposes. Taken

together, these steps should help us to gain a clearer understanding of the important

risk-coping strategies within rural Vietnam and their effectiveness.

5.1 Ability to Cope

The results of the fixed effects linear probability model of the likelihood of recovery

from an adverse income shock are presented in Table 7. We consider whether the

household holds liquid assets in the form of savings, livestock, crops stores and loans

together with other relevant wealth controls. The baseline model presented in column

(1) shows that income and wealth are strong predictors of a household’s ability to

recover from the shocks they suffer. The greater the level of borrowing of households

the less likely they are to recover from a shock suggesting that indebted households

find it more difficult to cope. There is no evidence to suggest that insurance plays a

role in the recovery process.

[INSERT TABLE 7 ABOUT HERE]

In column (2) the number of shocks suffered by the household is included. As is

consistent with the literature we find that the more shocks a household suffers the less

likely they are to recover. In column (3) the type of shock is added to the model.

Households that experience a natural shock, such as a weather related incident appear

to have fewer problems recovering. This suggests that coping mechanisms for

households that experience spatially covariant shocks may be better developed than

those for other types of shocks. It may be the case that external factors (for example,

government transfers) help to alleviate the adverse impacts of natural shocks. This

issue is explored further in the empirical section.

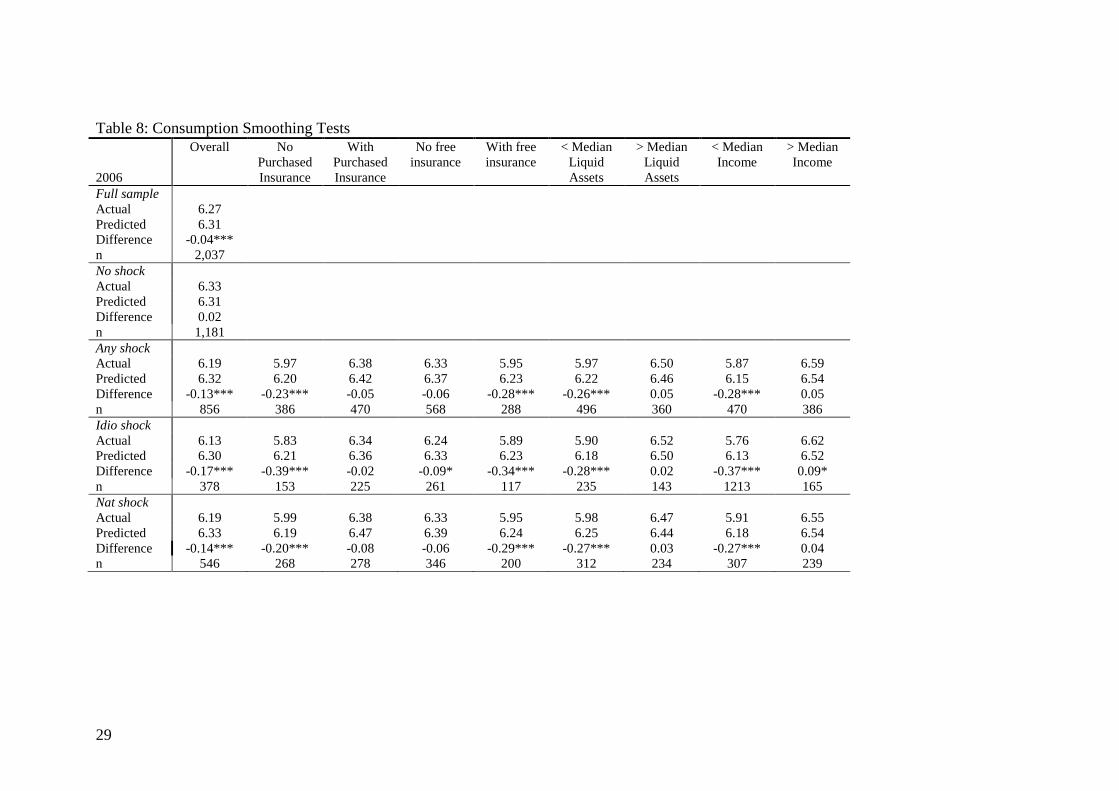

5.2 Consumption Smoothing

On the basis of subjective responses to coping with income shocks, 54 per cent of

households indicate reducing consumption is the most important risk-coping

mechanism. In addition, 25 per cent of households report that they increase

borrowings and sell assets. If coping mechanisms are operating effectively, be they

formal or informal, then households should smooth consumption over time regardless

of whether they suffer an income shock or not. To test whether this is the case, first, a

general consumption function is estimated separately for each region using the panel

of households that suffered no shocks over the sample period.24

The estimated

coefficients are used to predict consumption for 2006, 2008 and 2010 using the

observed data on the explanatory variables in each year.25

The mean levels of (log)

actual and predicted food expenditure and the difference between them are presented

in Table 8 along with t-tests of the significance of the difference between them.

Failure to reject the null hypothesis provides evidence of consumption smoothing.

Significantly positive (negative) differences indicate that the estimated value is

significantly lower (higher) than the actual suggesting that actual observed

consumption is higher (lower) than expected. Households are also grouped by

24

Results available on request. 25

For the estimated consumption calculation, income earned is adjusted for the realised shock amount

in order to generate a more accurate consumption prediction based on ceteris paribus effects.

14

category of shocks, the presence of formal insurance and other liquid savings

instruments and income.

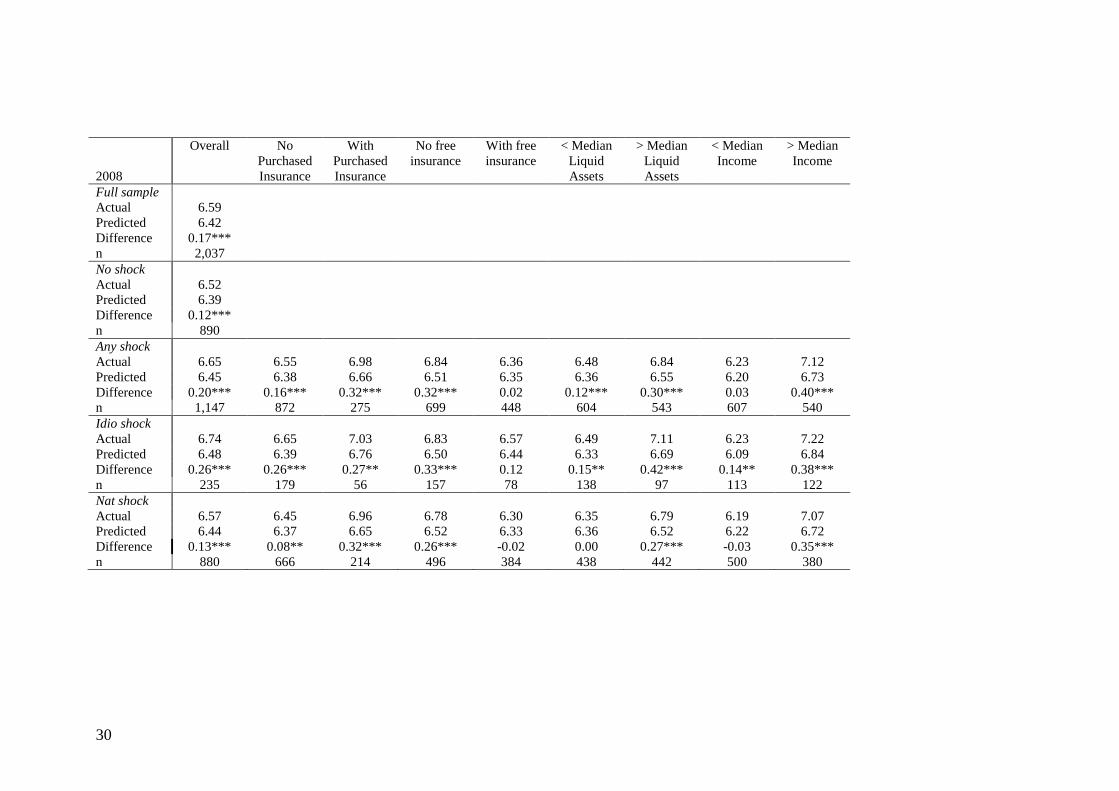

[INSERT TABLE 8 ABOUT HERE]

We first consider the consumption patterns of households in 2006 and find that overall

households consume less than predicted by our model. The difference between actual

and predicted consumption levels is particularly high for households that suffer

shocks, both idiosyncratic and natural shocks. However, households with purchased

insurance that suffer shocks (all types) manage to smooth consumption. In contrast,

households with free insurance do not manage to smooth consumption which is likely

picking up an income effect.

The extent of the difference between actual and predicted consumption levels in 2006

is also correlated with the level of liquid asset holdings of the household. We find that

households with above median liquid assets smooth consumption when faced with

idiosyncratic shocks. Coupled with our findings for insurance this suggests that both

purchased insurance and precautionary saving serve as a buffer against unexpected

income losses. We find a similar result for income suggesting that even when the level

of income is controlled for households earning higher incomes manage to smooth

consumption in the face of income shocks to a greater extent than those on lower

income levels. This suggests that the poorest households remain the most vulnerable

to risk.

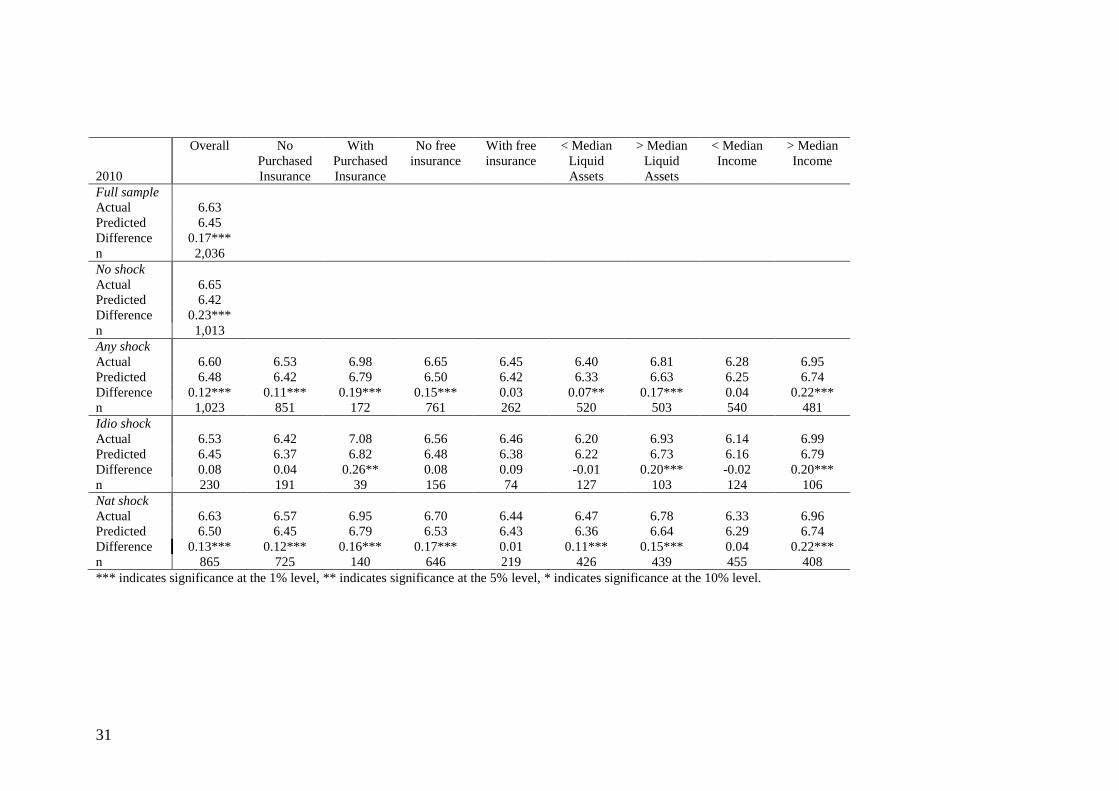

The results for 2008 and 2010 suggest that all households smooth consumption, even

when faced with idiosyncratic and natural shocks. However, the difference between

actual and predicted consumption levels is lower for households with no insurance

and for households with below median liquid asset holdings and income. The

difference is also lower for households with free insurance. This is most likely

correlated with an income effect as in both 2008 and 2010 households with below

median income and with free insurance that suffer shocks barely manage to smooth

consumption.

Overall, our results suggest that Vietnamese households manage to smooth

consumption over time, even in the face of idiosyncratic and natural shocks. This is

particularly the case in the more recent years of the sample. There is some evidence to

suggest that household’s ability to smooth consumption is somewhat correlated with

insurance and savings instruments, particularly in the case of idiosyncratic shocks.

The extent to which households deplete their stock of liquid assets and the role that

insurance plays in this is explored further in the third stage of our empirical analysis.

5.3 Total Liquid Assets

We now turn our attention away from consumption responses toward asset responses

in the face of income shocks. To explore this aspect of risk coping we estimate the

model presented in equation (2). For each asset class under consideration (total liquid

assets, savings, livestock, crop stores and loans), we use fixed effects estimation to

regress the level of household asset holdings (expressed in million VND) in each year

against our measures of exogenous spatially covariant and idiosyncratic shocks

together with income controls, wealth controls and household composition changes.

All value variables are adjusted to 2010 present values. Income shocks are

15

disaggregated by exogenous natural and economic and idiosyncratic, insurable and

uninsurable. We also include a dummy variable to control for external public and

private transfers together with a dummy variable to control for actual formal

insurance claims and free insurance claims. We focus explicitly on the types of

insurance claims that closely align with our category of idiosyncratic insurable shocks,

i.e. health, social and life insurance.

First, we determine whether households suffering any type of income shock

experience a statistically significant reduction in asset levels. Second, we disaggregate

the income shock measure into its exogenous and idiosyncratic components to explore

how each specific category of shock influences asset levels over time. Third, we

interact insurance claims and transfers with the incidence of shocks to establish

whether they help to reduce the impact of shocks on asset depletion. We also

disaggregate our results by wealth group to establish the extent to which the poor are

particularly vulnerable.26

Controls for income, household size, gender of household

head, age of the household head and age squared (to capture any lifecycle effects),

wealth (net of liquid assets), recovery from prior shocks (to control for persistence)

and time dummies (to control for average changes in asset values over time) are

included.

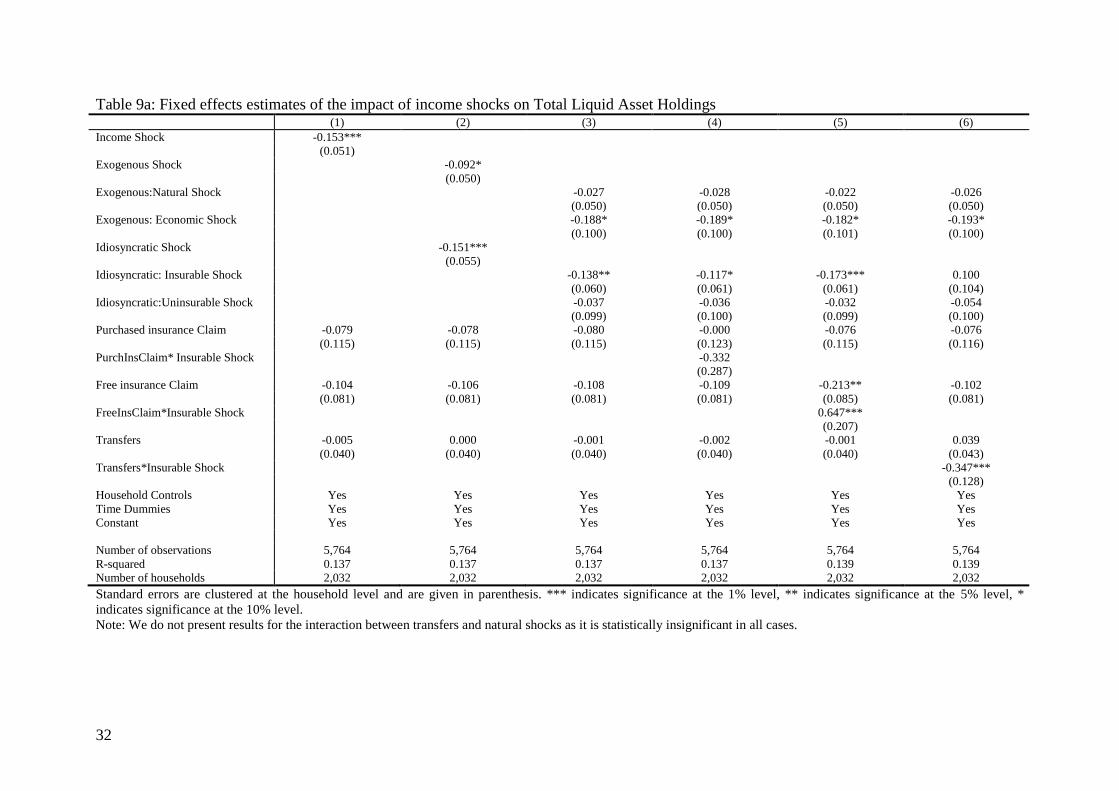

We first consider whether a household’s stock of total liquid assets (including all

savings, livestock and crops stores) is responsive to adverse income shocks. The

results are presented in Table 9a.

[INSERT TABLE 9a ABOUT HERE]

Column (1) reveals that shocks have a negative impact on the accumulation of total

liquid assets. Insurance claims and external transfers have no significant effect.

Disaggregating the income shock into its exogenous and idiosyncratic components

(Column 2) we find that both types of shock have a negative impact on the value of

liquid asset. A further breakdown of the type of shock (Column 3) reveals that both

exogenous economic and idiosyncratic insurable shocks serve to deplete total liquid

asset values over time, providing some evidence in support of our primary hypothesis

that household total liquid assets may serve precautionary savings purposes.27

Interacting formal insurance claims with idiosyncratic insurable shocks (Column 4)

has no significant effect on the level of liquid assets. The interaction between free

insurance claims and idiosyncratic insurable shocks (Column 5) has a positive and

significant effects indicating that while households that suffer these shocks deplete

their liquid asset savings those that receive free insurance transfers do so to a less of

an extent. This suggests that government safety nets play some role in supporting

households that are exposed to shocks of this kind. In Column 6, transfers (public and

private) are interacted with idiosyncratic insurable shocks. The interaction term is

negative and significant suggesting that households that experience shocks and are in

receipt of transfers deplete their savings to a greater extent than other households: in

26

Interpreting the results of such a disaggregation should be done with care given that households are

sampled from rural areas and so are on average poorer than the general population. As such the wealth

groups should be interpreted relative to the sample used rather than the population as a whole. 27

We cannot disentangle the precise amount of total liquid assets which was originally intended to

serve precautionary savings purposes from the amount serving other inter-temporal purposes.

16

other words, the availability of transfers does not prevent households from depleting

their liquid asset savings.

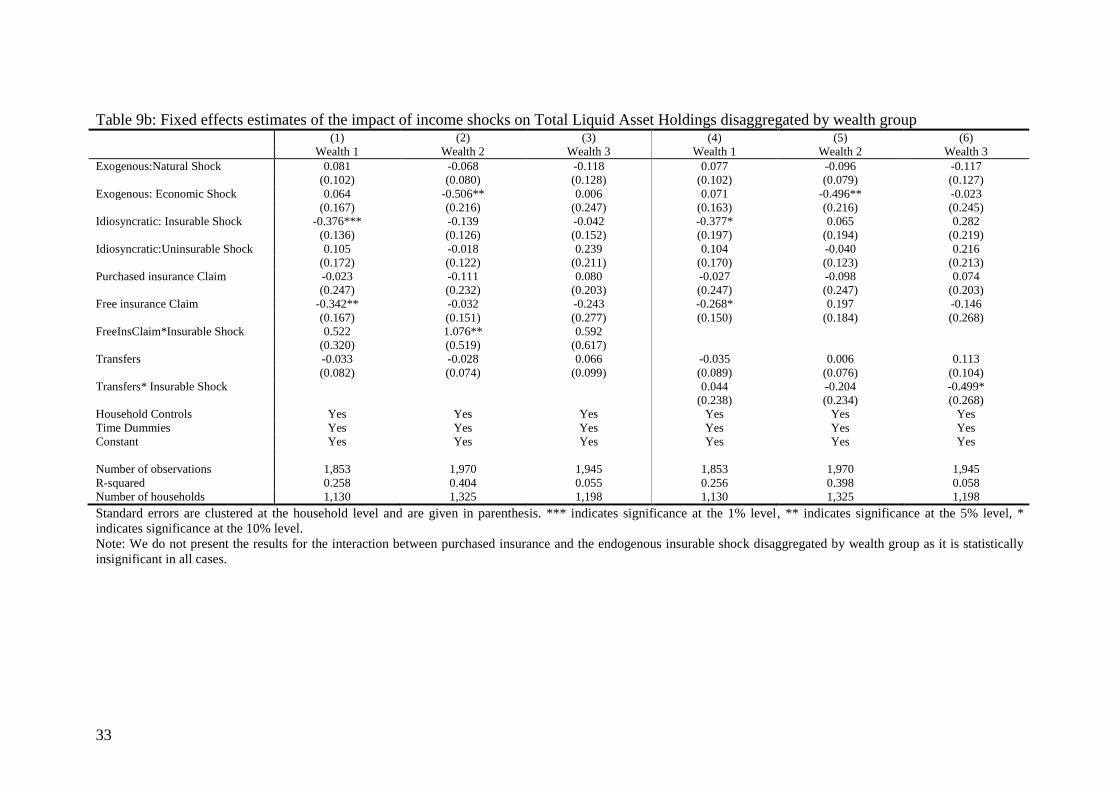

Disaggregating our sample into three wealth groups and running the model separately

for each group we find that exogenous economic shocks are important for the middle

wealth group while idiosyncratic insurable shocks are most problematic for the lowest

wealth group (see Table 9b). Free insurance claims, however, only benefit the middle

wealth group suggesting that while on aggregate free insurance is serving a social

safety net function it may not be reaching the poorest groups. We also find in Column

(6) that the interaction between idiosyncratic shocks and transfers is only negative and

significant for the wealthiest group. This suggests that wealthier households that

suffer idiosyncratic shocks might draw on many different mechanisms for coping

including depleting assets and relying on transfers from others.

INSERT TABLE 9b HERE

5.4 Livestock Holdings

To understand whether livestock serves as a buffer against adverse shocks we

estimate a fixed effects regression of livestock holdings values against our exogenous

spatially covariant and idiosyncratic shock measures. The results are presented in

Table 10.

[INSERT TABLE 10 ABOUT HERE]

There is no evidence to suggest that livestock acts as a buffer against overall income

shocks (Column 1). Disaggregating income shocks into their exogenous and

idiosyncratic components we find a negative and significant relationship between

idiosyncratic shocks and the value of livestock holdings (Column 2). There is no

evidence to suggest, however, that livestock acts as a buffer against spatially covariant

shocks. These findings support the partial equilibrium effects discussed in Fafchamps

et al (1998) whereby if livestock markets are not perfectly integrated then it is

difficult for this asset class to act as a buffer stock in the case of exogenous spatially

covariant shocks. In such closed market situations, net sales of livestock must sum to

zero at the commune/village level. Idiosyncratic insurable shocks, on the other hand,

facilitate the use of livestock as a risk-coping mechanism and we see some evidence

that this is the case (Column 3). Turning our attention to formal insurance effects, we

find that insurance claims are negatively related to total livestock values (Columns 1

to 6). The interaction between whether the households makes an insurance claim with

whether the household suffered an idiosyncratic insurable shock, however, is

statistically insignificant. We also find no evidence that free insurance or external

transfers act in any way to preserve livestock holdings.

Overall, our results provide some support for the hypothesis that livestock plays an

important role in consumption smoothing where idiosyncratic insurable shocks occur

but not for exogenous spatially covariant shocks (Rosenzweig and Wolpin (1993) find

a similar result).28

5.5 Financial Savings

28

The results do not vary across wealth group and so they are not included.

17

We estimate a similar model of the responsiveness of a household’s total stock of

savings to exogenous spatially covariant and idiosyncratic shocks. We also consider a

disaggregation of the total stock of savings into cash/gold stores. The results

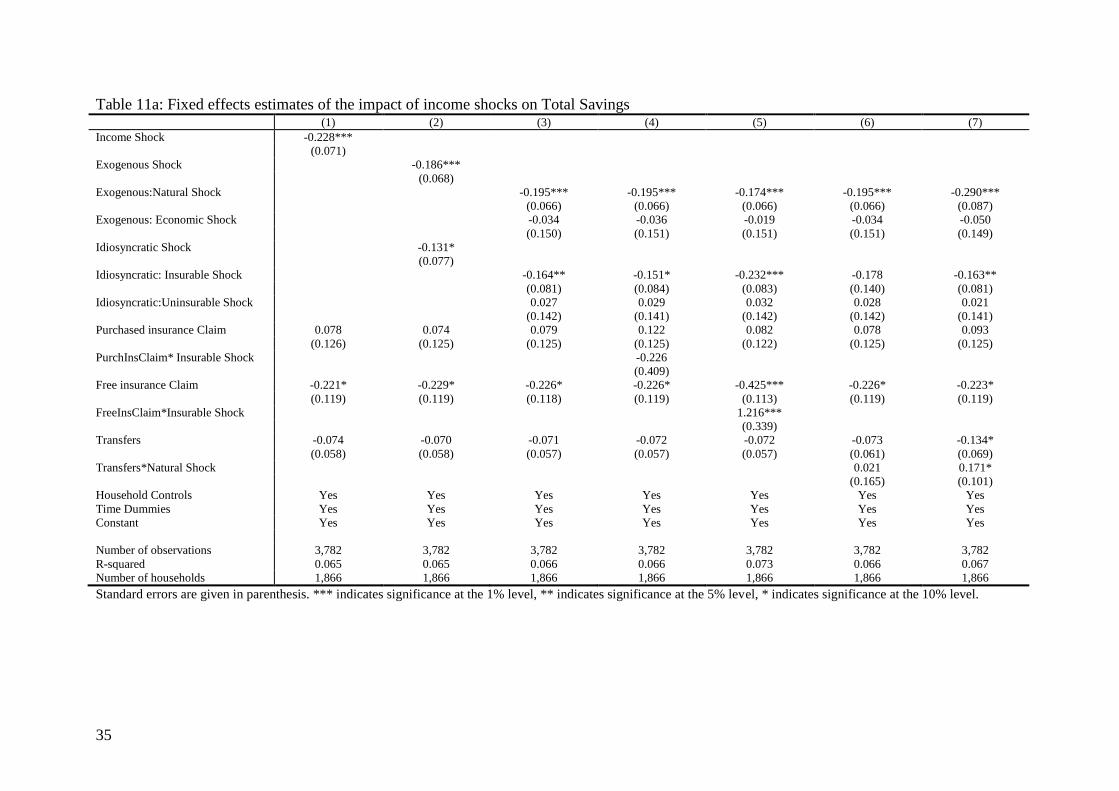

pertaining to total savings stocks are presented in Table 11a.

[INSERT TABLES 11a AND 11b ABOUT HERE]

We find that the occurrence of an income shock depletes a household’s stock of total

savings over time (Column 1). Disaggregating income shocks by type we find that

while both exogenous spatially covariant and idiosyncratic shocks are important

(Column 2), spatially covariant natural shocks have the greatest impact (Column 3).

Also of note is the average negative effect on savings of households in receipt of free

insurance claims which suggests that these households are experiencing particular

financial difficulty. When the occurrence of free insurance claims is interacted with

idiosyncratic shocks (Column 5) we find that they serve to deplete the impact of

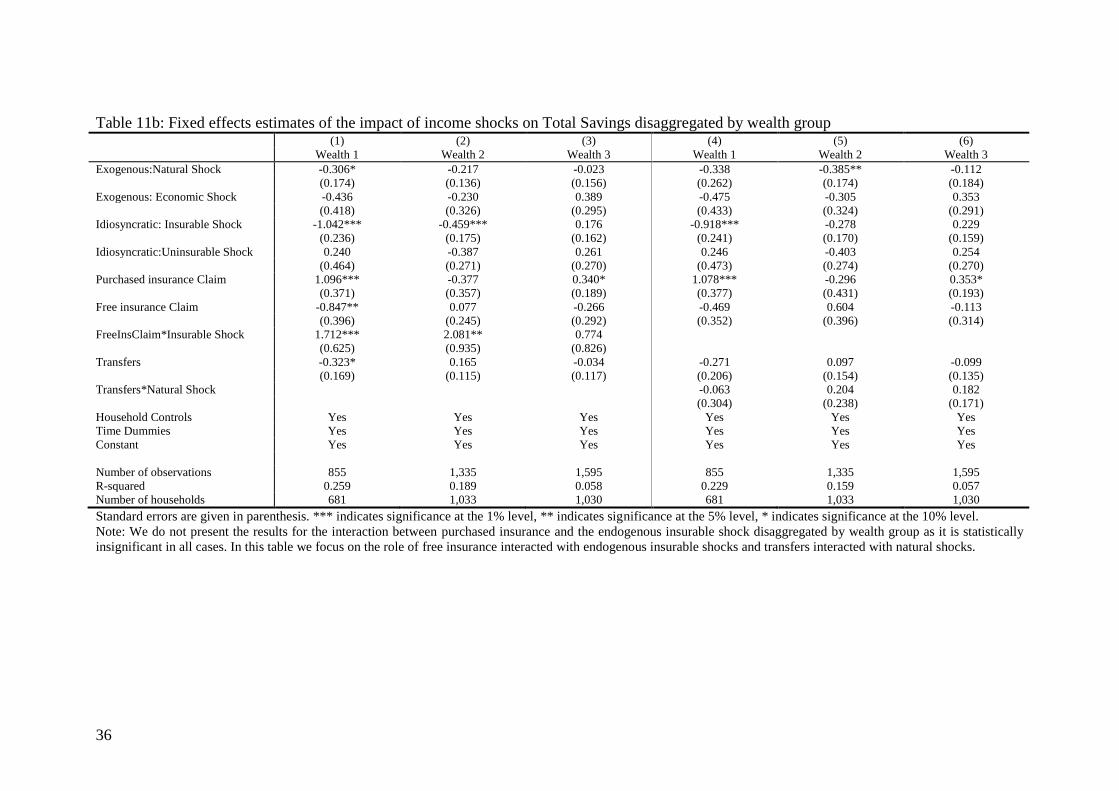

idiosyncratic shocks on household savings. When disaggregated by wealth group

(Table 11b) we find that this effect holds for the first and the second wealth group but

is of a greater magnitude for the latter. This adds further evidence to our claim that

social safety nets are important for households when faced with adverse income

shocks. We do not find any evidence that purchased insurance claims reduces the

impact of shocks on household savings.

Natural shocks also lead to a significant depletion of savings by households, however,

when transfers are interacted with natural shocks (Column 7 of Table 11a) we find

that those households in receipt of transfers deplete their savings to a lesser extent.

We interpret this result as providing some evidence regarding the importance of

external transfers in times of natural disaster, notwithstanding that the magnitude of

this assistance appears not to fully compensate for the total financial loss incurred by

the household.

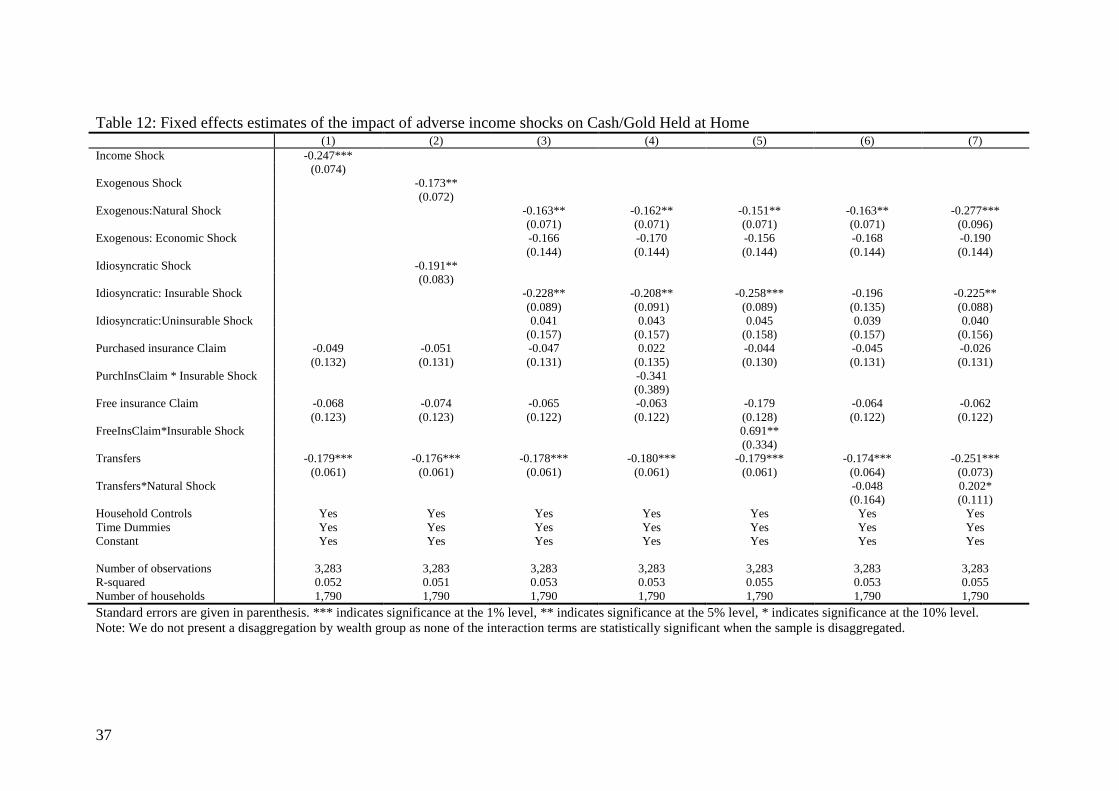

Disaggregating total savings into its various components also reveals some interesting

findings, particularly for cash/gold held at home (see Table 12). We find that both

natural disasters and idiosyncratic insurable shocks deplete households’ stock of

cash/gold held at home.29

As for the total stock of saving, we find that transfers

feature significantly as a risk-coping mechanism in the face of natural disasters

although there is still a shortfall in terms of financial loss for the household. Free

insurance claims are also important in easing the depletion of cash/gold in the face of

idiosyncratic insurable shocks but we do not find the same effect for purchased

insurance. The complementarity between purchased insurance and savings

instruments suggests that insurance markets may be incomplete. We find no

significant evidence that either formal or informal savings serve as important risk-

coping mechanisms for the household.30

[INSERT TABLE 12 ABOUT HERE]

5.6 Crop storage

29

It possible that natural disasters such as flooding might physically destroy the stock of cash and gold

held by households. We cannot tell from our data whether or not this is the case. 30

The results for formal and informal savings are not presented but are available on request.

18

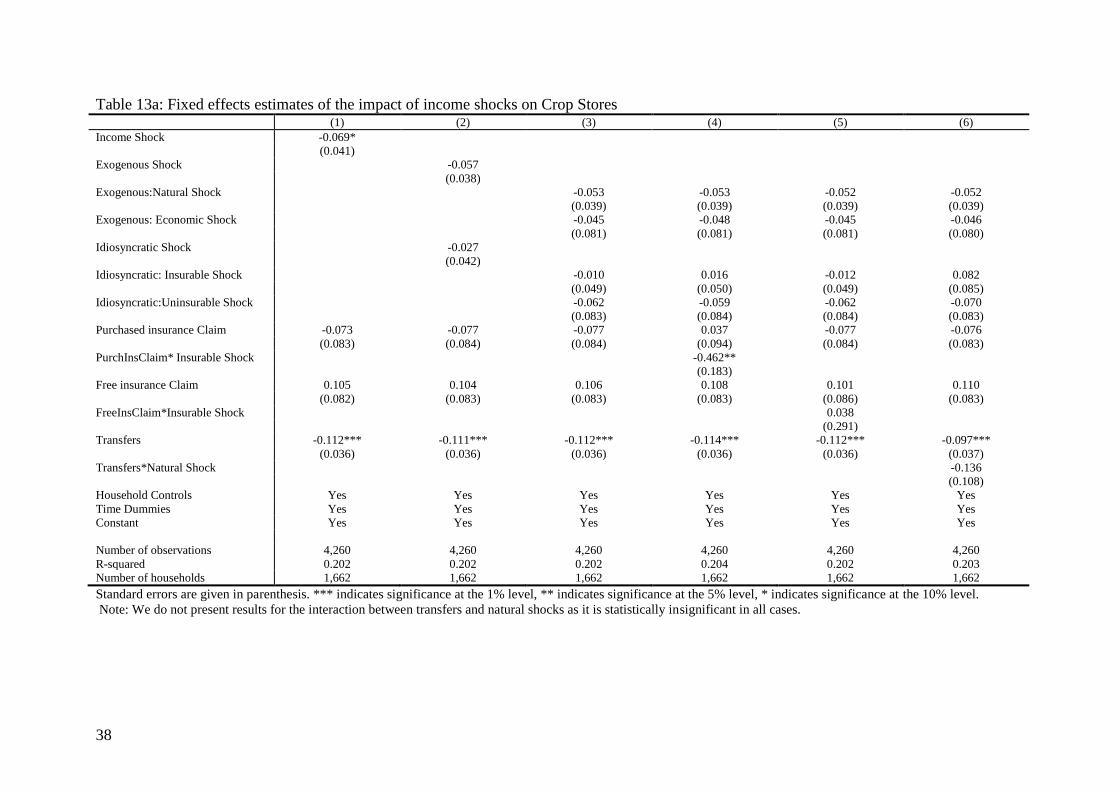

Crop stores in the form of rice, maize, potatoes etc., may also act as a form of

precautionary saving.31

Results of the impact of exogenous spatially covariant and

idiosyncratic shocks on the store of crops are presented in Table 13a.

[INSERT TABLES 13a AND 13b ABOUT HERE]

The results indicate that total crop stores are somewhat responsive to shocks (Column

1) but this result is not robust to the disaggregation of spatially covariant and

idiosyncratic shocks into their constituent components. Disaggregating by wealth

group (Table 13b) we find that for middle wealth groups (Column 3), idiosyncratic

uninsurable shocks serve to deplete household crop stores. There is no evidence that

insurance claims or transfers serve as a buffer against asset depletion. One possible

explanation for this is that for households that suffered an idiosyncratic uninsurable

shock, risk-coping may simply require that more harvest is consumed in the home to

offset the financial loss incurred. Households in the wealthiest group that make

insurance claims also deplete their stores of crops which once again suggests that in

times of financial stress wealthier households rely on a variety of different risk coping

mechanisms. There is also some evidence to suggest that wealthier households that

experience idiosyncratic insurable shocks also benefit from free insurance claims to

the extent that they reduce the need for households to deplete their crop stores. It

should be noted that these households are only wealthy relative to the sample of rural

households included in the survey and should not be considered representative of the

population of wealth households in Vietnam as a whole.

Overall, we find some evidence that crop stores are drawn down in times of financial

stress from uninsurable exogenous and idiosyncratic losses and thus appear to serve

precautionary savings purposes. Given that anecdotal evidence suggests that rural

Vietnamese households do not have the means to store large quantities of their crops

(due to the small scale of their production and a lack of storage facilities), it is not

surprising that we find very little evidence that crop stores are used as a risk-coping

mechanism for the poor.

5.7 Household Borrowing

Finally, we turn our attention to rural credit markets and test whether the existence of

credit instruments (or negative assets) serve as a risk-coping mechanism for rural

Vietnamese households. According to Dercon (2002), credit and insurance markets in

developing economies are typically absent or incomplete, either for good theoretical

reasons or as a result of bad policy (for surveys, see Bell (1988) or Besley (1994,

1995)). Typically, consumption loans are also rare. We use a fixed effects estimation

to regress the total outstanding household loan amounts against measures of spatially

covariant and idiosyncratic shocks to determine whether the household resorts to

borrowing to facilitate consumption smoothing when faced with adverse income

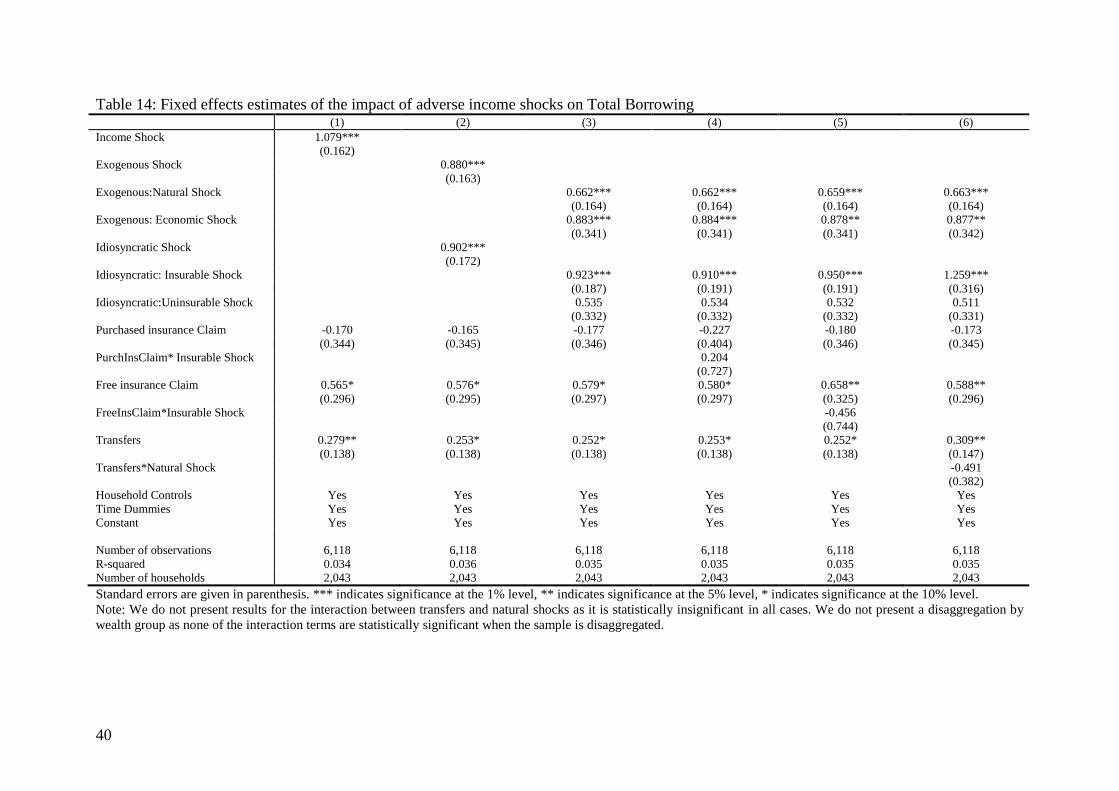

shocks. The results are presented in Table 14.

[INSERT TABLE 14 ABOUT HERE]

31

Park (2005) finds that the joint nature of production and savings decisions limits the income loss

associated with risk-coping, and the desire to store grain can explain why subsistence households are

frequently net purchasers but rarely net sellers of grain.

19

We find that total household loan amounts are positively and significantly responsive

to adverse income shocks, indicating that households increase borrowing in times of

financial hardship (Column 1). We disaggregate income shocks into their constituent

components and find that both exogenous and idiosyncratic shocks are associated with

higher levels of borrowing (Column 2). A further disaggregation of income shocks

suggests that all types of shocks, with the exception of endogenous uninsurable

shocks, significantly increase household borrowing (Column 3). It appears that rural

Vietnamese households resort to increasing their borrowings in times of financial

stress. We do not find any evidence that formal insurance claims, free insurance

claims or external transfers help to ease households’ debt burden. Disaggregating by

wealth group we find that the reliance on credit in times of financial hardship is most

characteristic of wealthier households who are more likely to have access to credit

than poorer households.32

6. Conclusion

In this paper, we examine the consequences of risk on the behaviour of Vietnamese

households by examining the ability of households to recover from adverse income

shocks through examining their consumption and asset depletion responses. We find

that households in rural Vietnam manage to smooth consumption in the face of

adverse income shocks and an important mechanism for smoothing consumption is

the use of precautionary saving. Households deplete their total stock of liquid assets in

response to exogenous economic shocks and idiosyncratic insurable shocks. Financial

savings, particularly cash and gold held at home, act as important buffers in the face

of spatially covariant natural shocks. Free insurance plays an important role in easing

the depletion of savings in response to idiosyncratic shocks while external transfers

are important for risk-coping in the face of natural disasters. Of particular note is the

fact that borrowing is increased when households are faced with idiosyncratic and

spatially covariant shocks.

These findings provide evidence for the importance of savings and insurance

instruments for the ability of households to consumption smooth where income risks

prevail. Savings for precautionary purposes may lead to lower welfare outcomes in

the long run given that they result in lower levels of consumption and use up

resources that could be put to more productive uses. This is exacerbated by the fact

that the uncertainty associated with income shocks may lead households to save

excessively in these forms. While our results suggest that the presence of free

insurance instruments reduces the need to draw down some forms of precautionary

savings in the event of adverse income shocks, there is strong evidence to suggest that

insurance markets do not fully cover idiosyncratic risks.

We find evidence that the poorest households and ethnic minorities are the most

vulnerable groups. The baseline model presented in this paper reveals that income and

wealth are strong predictors of the ability of households to recover from the shocks

they suffer. The greater the level of borrowing of households the less likely they are to

recover from a shock suggesting that indebted households find it more difficult to

cope. Free state-provided insurance is of greater benefit to the middle wealth group

32

The disaggregation by wealth group is not presented due to space constraints but the results are

available on request.

20

but does also act as a buffer for some poor households. There is a clear need for

government to ensure that social safety nets protect the most vulnerable in society.

Households that experience a natural shock, such as a weather related incident, appear

to have fewer problems recovering. This suggests that coping mechanisms for

households that experience spatially covariant shocks may be better developed than

those for other types of shocks. We find that natural shocks lead to a significant

depletion of savings by households but when transfers are interacted with natural

shocks we find that those households in receipt of transfers deplete their savings to a

lesser extent. This provides some evidence regarding the importance of external

transfers in times of natural disaster, notwithstanding that the magnitude of this

assistance appears not to fully compensate for the total financial loss incurred.

While government transfers help households to overcome the damage associated with

natural disasters, this comes at a substantial cost to the state. Few households have

access to agricultural insurance to protect against losses due to natural shocks and so

there is significant scope for the development of agricultural insurance products in

order to reduce the variability in income for farmers living in vulnerable areas, and to

reduce the cost government support schemes for these households.

In July 2011, the Vietnamese government introduced a pilot agricultural insurance

product in 20 provinces and cities across Vietnam.33

This programme aims to promote

the development of the agricultural insurance market by supporting 60 percent of the

premiums for households and 20 percent for organisations involved in agricultural

production. Moreover, poor households will receive support of between 80 and 100

percent of premiums.

Incentivizing the take-up of agricultural insurance is an important step forward,

however, many obstacles remain. For example, agricultural insurance is associated

with very high-risks and difficulties in calculating the types of risks that can be

insured, monitoring the incidence of insured events and calculating claims, represent

significant barriers. The Government also has an important role to play in creating the

legal transparency and competitive environment necessary for private insurance

companies to provide agricultural insurance. Close coordination between insurance

companies, credit institutions and farmer’s organisations will facilitate this process. It

is also important that agricultural insurance schemes are directed toward the

mitigation of risk for farmers rather than toward achieving social goals directly. If the

market operates effectively then it will lead to less variability in income for those

farmers affected, more profitable outcomes and reductions in poverty. In the interim,

however, the support programs currently in place play an important role in helping

households to cope. It is important that these support programs are maintained and

reorganised in a way that they reach the most vulnerable.

33

Decision 315/QD-TTg

21

References

Alderman, H. (1998). ‘Saving and Economic Shocks in Rural Pakistan’, Journal of

Development Economics, vol. 51(2), pp. 343–66.

Alderman, H., Hoddinott, J. and Kinsey, B. (2006). ‘Long-term Consequences of

Early Childhood Malnutrition’, Oxford Economic Papers, vol. 58(3), pp. 450-74.

Alderman, H. and Paxson, C. (1994). ‘Do the poor Insure? A Synthesis of the

Literature on Risk and Consumption in Developing Countries’, International

Economics Association, Moscow Meeting, Proceedings, Vol.4.

Bell, C. (1988). ‘Credit Markets, Contracts and Interlinked Transactions’, in Chenery,

H. and T.N. Srinivasan (eds), Handbook of Development Economics, vol. 1,

Amsterdam: North-Holland.

Besley, T. (1994). ‘Savings, Credit and Insurance’, in J. Behrman and T.N. Srinivasan

(eds), Handbook of Development Economics, vol. IIIA, Amsterdam: North-Holland.

Besley, T. (1995). ‘Nonmarket Institutions for Credit and Risk Sharing in Low-

Income Countries’, Journal of Economic Perspectives, vol. 9(Summer), pp. 115–27.

Briys, E. (1986). ‘Insurance and Consumption: The Continuous-Time Case’, Journal

of Risk and Insurance, vol. 53, pp. 718-723.

CIEM, DOE-University of Copenhagen, ILSSA, IPSARD (2007). Characteristics of

the Vietnamese Rural Economy: Evidence from a 2006 Rural Household Survey in 12

Provinces of Vietnam. Hanoi: Statistical Publishing House.

CIEM, DOE-University of Copenhagen, ILSSA, IPSARD (2009). Characteristics of

the Vietnamese Rural Economy: Evidence from a 2008 Rural Household Survey in 12

Provinces of Vietnam. Hanoi: Statistical Publishing House.

CIEM, DOE-University of Copenhagen, ILSSA, IPSARD (Forthcoming 2011).

Characteristics of the Vietnamese Rural Economy: Evidence from a 2010 Rural

Household Survey in 12 Provinces of Vietnam. Hanoi: Statistical Publishing House.

Cole, S., Giné, X., Tobacman, J., Topalova, P., Townsend, R. and Vickery, J. (2010).

‘Barriers to Household Risk Management: Evidence from India.’ Federal Reserve

Bank of New York Staff Report Number 373.

Deaton, A. (1991). ‘Savings and Liquidity Constraints’, Econometrica, vol. 59(5), pp.

1221–48.

Deaton, A. (1992). ‘Household Saving in LDCs: Credit Markets, Insurance and

Welfare’, Scandinavian Journal of Economics, vol. 94(2), pp. 253–73.

Deaton, A. (1997). The Analysis of Household Surveys: A Microeconomic Approach,

Baltimore: Johns Hopkins University Press.

22

Dercon, S. (2002). ‘Income Risk, Coping Strategies and Safety Nets’ World Bank

Research Observer, vol. 17(2), pp. 141-66.

Dionne, G. (2000). Handbook of Insurance, New York: Kluwer Academic Publishers.

Dionne, G and L. Eeckhoudt, (1984). ‘Insurance and Saving: Some Further Results’,

Insurance: Mathematics and Economics, vol. 3(2), pp. 101-110.

Fafchamps, M. (2009). ‘Vulnerability, Risk Management, and Agricultural

Development’, CEGA Working Paper Number AfD-0904.

Fafchamps, M., Czukas, K., and Udry, C. (1998). ‘Drought and Saving in West-

Africa: Are Livestock a Buffer Stock’, Journal of Development Economics, vol.

55(2), pp. 273–305.

Gollier, C. (1994). ‘Insurance and Precautionary Capital Accumulation in a

Continuous-Time Model’, Journal of Risk and Insurance vol. 61(1), pp. 78-95.

Jacoby, H. and Skoufias, E. (1997). ‘Risk, Financial Markets and Human Capital in a

Developing Country’, Review of Economic Studies, vol. 64(3), pp. 311–36.

Kimball, M. (1990). ‘Precautionary Saving and the Marginal Propensity to Consume’,

NBER Working Paper Number 3403.

Lim, Y. and Townsend, R., (1998). ‘General Equilibrium Models of Financial

Systems: Theory and Measurement in Village Economies.’ Review of Economic

Dynamics, vol. 1(1), pp. 59-118.

Morduch, J. (2004). ‘Consumption Smoothing Across Space: Tests for Village-Level

Responses to Risk’, In Dercon, S. (ed.), Insurance against Poverty, Oxford University

Press.

Morduch, J. (2002). ‘Micro-insurance: the next revolution’, In Banerjee, A. Benabou

R. and Mookherjee, D. (eds.) What we have learned about poverty? Oxford

University Press.

Newman, C., Tarp, F. and Van den Broeck, K. (2011). ‘Social Capital and Savings

Behaviour: Evidence from Vietnam.’ IIIS Discussion Paper Number 351.

Nguyen, Q.N. (2003). ‘Responses to poverty and risks in Vietnam: How effectively

does Vietnamese public safety net target vulnerable populations’ Research and

Development, Bank for Foreign Trade of Vietnam.

Park, A. (2006). ‘Risk and Household Grain Management in Developing Countries’,

The Economic Journal, vol. 116(514), pp.1088-115.

Rosenzweig, M. and Wolpin, K. (1993). ‘Credit Market Constraints, Consumption

Smoothing, and the Accumulation of Durable Production Assets in Low-income

Countries: Investment in Bullocks in India’, Journal of Political Economy, vol.

101(2), pp. 223–44.

23

Townsend, R. (1994). ‘Risk and Insurance in Village India’, Econometrica, vol.

62(3), pp. 539–91.

Udry, C. (1991). ‘Credit Markets in Northern Nigeria: Credit as Insurance in a Rural

Economy’, World Bank Economic Review, vol. 4(3), pp. 251–71.

Udry, C. (1994). ‘Risk and Insurance in a Rural Credit Market: An empirical

Investigation of Northern Nigeria’, Review of Economic Studies, vol. 61(3), pp. 495–

526.

Ventura, L. and Eisenhauer, J. (2005). ‘The Relevance of Precautionary Saving’,

German Economic Review, vol. 6(5), pp. 23-35.

Zeldes, S. (1989). ‘Optimal consumption with stochastic income: deviations from

certainty equivalence’, Quarterly Journal of Economics, vol. 104(2), pp. 275-298.

24

Tables

Table 1: Explanatory Variables and descriptions Explanatory Variable Description

Exogenous: Spatially Covariant

Natural Shock

Dummy variable indicating whether the household has suffered a

spatially covariant natural income shock. Shocks include floods,

landslides, typhoons, storms, droughts, pest infestation, crop disease

and avian flu.

Exogenous: Economic Shock Dummy variable indicating whether the household has suffered an

exogenous economic shock. Shocks include changes in crop price,

changes in key input prices, changes in prices of food or other

essential commodities consumed.

Idiosyncratic: Insurable Shock Dummy variable indicating whether the household has suffered an

idiosyncratic insurable income shock. Shocks include illness, injury

or death of a family member.

Idiosyncratic: Uninsurable Shock Dummy variable indicating whether the household has suffered an

idiosyncratic uninsurable income shock. Shocks include

unemployment, unsuccessful investment, loss of land,

crime/robbery/theft, divorce, family disputes.

Transfers Dummy variable indicating whether the household has received

external income transfers from government and/or family

members/relatives (public/private sources).

Purchased insurance Claim Dummy variable indicating whether the household has made an

insurance claim under a voluntarily purchased contract and received

funds in compensation. Claims are restricted to health, life and

social insurance.

Free insurance Claim Dummy variable indicating whether the household has made an

insurance claim under a free state provided insurance contract and

received funds in compensation. Claims are restricted to health and

social insurance.

Income Household income – includes income from non-farm activities and

income from the sale of assets. Excludes insurance premium paid.

(2010 mean = 80991 VND, 2010 std deviation=130050 VND)

Household Size Total number of household members.

Education of Household Head 1 "Cannot read and write"

2 "Can read & write but did not finish primary school"

3 "Finished primary school"

4 "Finished lower secondary school"

5 "Finished upper secondary school"

6 "Third Level"

Gender of Household Head Dummy variable (1 Male, 0 Female).

Age of Household Head Measured in years.

Wealth

Total household wealth constructed using fixed asset values (land),