Embed Size (px)

DESCRIPTION

stock and investment

Citation preview

7/24/2015 India Strategy: Getting on track!– Detailed Report

http://www.motilaloswal.com/site/rreports/HTML/635721163512170886/index.htm 1/85

India Strategy | Get on Juneplease !track 2015

India StrategyFY03‐08:25% CAGR

FY93‐96:45% CAGR

FY96‐03:1% CAGR

FY93‐FY15:14% CAGR

FY08‐15:8% CAGR

FY15‐17E:20% CAGR

Getting on track!Research Team ([email protected])

7/24/2015 India Strategy: Getting on track!– Detailed Report

http://www.motilaloswal.com/site/rreports/HTML/635721163512170886/index.htm 2/85

ContentsIndia Strategy ‐ Getting on track! ................................................................................................. 1‐721QFY16 Highlights & Ready Reckoner ...................................................................................... 73‐85Sectors & Companies ............................................................................................................... 86‐3201. Automobiles

Amara Raja BatteriesAshok LeylandBajaj AutoBharat ForgeEicher MotorsExide IndustriesHero MotoCorpMahindra & MahindraMaruti Suzuki IndiaTata MotorsTVS Motor

2. Capital GoodsABBBHELBharat ElectronicsCrompton GreavesCummins IndiaHavells IndiaLarsen & ToubroSiemensThermaxVoltas

3. CementACCAmbuja CementGrasim IndustriesIndia CementsRamco CementShree CementUltraTech Cement

4. ConsumerAsian PaintsBritannia IndustriesColgate PalmoliveDabur IndiaEmamiGodrej Consumer ProductsGSK ConsumerHindustan UnileverITCJyothy LabsMaricoNestle IndiaPidilite IndustriesRadico KhaitanUnited Spirits

5a. Financials ‐ BanksAxis BankBank of BarodaBank of IndiaDCB BankFederal BankHDFC BankICICI BankIndian BankIndusInd BankKotak Mahindra BankPunjab National BankState Bank of IndiaUnion Bank

87‐101919293949596979899

100101

102‐115106107108109110111112113114115

116‐126120121122123124125126

127‐144130131132133134135136137138139140141142143144

145‐163150151152153154155156157158159160161162

Yes Bank5b. Financials ‐ NBFC

Bajaj FinanceDewan HousingHDFCIDFCIndiabulls HousingLIC Housing FinanceM & M Financial ServicesPower Finance CorporationRepcoRural ElectricficationShriram Transport

6. HealthcareAlembic PharmaAurobindo PharmaBioconCadila HealthcareCiplaDivi’s LaboratoriesDr Reddy’s Labs.Glenmark PharmaGSK PharmaIPCA LaboratoriesLupinSanofi IndiaSun PharmaceuticalsTorrent Pharma

7. MediaD B CorpDish TVHathway CableHT MediaJagran PrakashanPVRSiti CableSun TV NetworkZee Entertainment

8. MetalsHindalcoHindustan ZincJSW SteelNalcoNMDCSesa SterliteSAILTata Steel

9. Oil & GasBPCLCairn IndiaGAILGujarat State PetronetHPCLIOCIndraprastha GasMRPLOil IndiaONGCPetronet LNGReliance Industries

163164‐176

166167168169170171172173174175176

177‐194181182183184185186187188189190191192193194

195‐207199200201202203204205206207

208‐222215216217218219220221222

223‐239228229230231232233234235236237238239

10. Real EstateDLFGodrej PropertiesIndiabulls Real EstateMahindra LifespacesOberoi RealtyPhoenix MillsPrestige Estate ProjectsSobha Developers

11. RetailJubilant FoodShoppers StopTitan Company

240‐252245246247248249250251252

253‐258256257258

259‐274264265266267268269270271272273274

275‐283280281282283

284‐297288289290291292293294295296297

298‐316298299300301302303304305306307308309310311312313314315316

12. TechnologyCognizant TechnologyHCL TechnologiesHexaware TechnologiesInfosysKPIT TechnologiesMindtreeMphasiSPersistent SystemsTCSTech MahindraWipro

13. TelecomBharti AirtelBharti InfratelIdea CellularReliance Communication

14. UtilitiesCESCCoal IndiaJSW EnergyNHPCNTPCPower Grid Corp.PTC IndiaRattanindia PowerReliance InfrastructureTata Power

15. OthersArvindBata IndiaCastrol IndiaConcorCoromandel InternationalDynamatic TechGateway DistriparkGujarat Pipavav PortInfo EdgeInox LeisureJain IrrigationJust DialKaveri SeedsMonsanto IndiaSintex IndustriesTata ElxsiTTK PrestigeUPLV‐Guard Industries

Note: All stock prices and indices for companies as on 30 June 2015, unless otherwise statedInvestors are advised to refer through disclosures made at the end of the Research Report.

7/24/2015 India Strategy: Getting on track!– Detailed Report

http://www.motilaloswal.com/site/rreports/HTML/635721163512170886/index.htm 3/85

India Strategy | Getting on track!

India StrategyBSE Sensex: 27,574 S&P CNX: 8,329

Getting on track!Inflation, INR, Deficits well in control now; Govt spending to drive capexrecovery; Earnings to rebound in FY16/17

1QFY16 PREVIEW: Another quarter of decline! Worst is likely over! |1QFY16 performance of MOSL Universe: Third consecutive quarter of PATde‐growth

Motilal Oswal values yoursupport in the AsiamoneyBrokers Poll 2015 for IndiaResearch, Sales and Tradingteam. We request your ballot.

Our bottom‐up estimates indicate a 1% YoY decline in aggregate PAT for theMOSL Universe (ex‐RMs). Sales would remain flat and EBITDA would growmoderately (4%). The fall in global commodities, delay in revival of theinvestment cycle and muted rural consumption continue to impact growth ofcorporate India.Only seven sectors are expected to witness double‐digit PAT growth—Media(36%), Telecom (23%), Capital Goods (18%), Private Banks (17%), Consumer(14%), Oil (11%) and Retail (11%). Six sectors would likely report PAT de‐growth—Healthcare (‐1%), Auto (‐7%), Real Estate (‐11%), PSU Banks (‐27%),Cement (‐33%) and Metals (‐52%).Nifty PAT (ex‐BPCL) is likely to remain flat YoY—an improvement over 11% de‐growth in 4QFY15. Sales would marginaly decline (‐1%) in 1QFY16 (v/s ‐6% in4QFY15).About one‐fourth of the Nifty constituents would report >15% YoY PAT growth;however, this would be offset by PAT de‐growth in more than one‐third of theconstituents. Cyclicals and domestic‐facing companies would contribute to PATde‐growth (14 out of 17 PAT de‐growth companies are cyclical).Top PAT growth companies would be Maruti (77%), Tata Power (63%), Cipla(+41%), ONGC (+41%), Idea (+36%), Yes Bank (+29%), Indusind Bank (+24%) andBharti Airtel (+21).Top PAT de‐growth companies would be Punjab National Bank (‐58%), CairnIndia (‐57%), Bank of Baroda (‐44%), NMDC (‐42%), Ambuja Cement (‐40%),Grasim (‐38%), Hindalco (‐38%) and Tata Motors (‐31%).

Exhibit 1: PAT de‐growth in 1QFY16; expect rebound in 2H

39

22 25 24 26

10 14 125

1914

7 7 916 13

MOSL UniverseQuarterly PAT Growth

16 YoY (%) LPA: 10%22

30

2 18 6

‐6 ‐8 ‐1

‐14‐9

Source: Company, MOSL

July 2015 1

7/24/2015 India Strategy: Getting on track!– Detailed Report

http://www.motilaloswal.com/site/rreports/HTML/635721163512170886/index.htm 4/85

India Strategy | Getting on track!

FY16‐17 ESTIMATES: Expect recovery in 2HFY16 | Government‐led capexand low inflation to lead recovery

Delay in domestic recovery and global commodity fall continue be theheadwinds for earnings growth. Other factors such as muted rural consumption,continuing asset quality woes in PSU banks and adverse cross currencymovements continue to pull down the aggregate growth of corporate India.However, we believe government‐led capital spending and favorable inflationleading to lower rates will create conducive environment for earnings growthrecovery.Our bottom‐up estimates suggest aggregate PAT of the MOSL Universe (ex‐RMs)to rebound to 17%/23% in FY16/FY17. Sales growth would increase moderatelyto 9% in FY16 before jumping to 13% in FY17.Expect Sensex EPS to grow 15% to 1,561 in FY16 and 22% to 1,907 in FY17. Sincethe last preview, three‐fourths of the Sensex companies would see an EPS cut—led by Tata Steel, Sun Pharma, Hindalco, Tata Motors, Coal India and GAIL. Topupgrade drivers are Maruti, NTPC, ONGC and Bajaj Auto.One‐third of the Sensex companies would contribute more than two‐thirds ofFY16 Sensex EPS expansion. Key contributors to the EPS expansion would beONGC, Tata Motors, ICICI Bank, HDFC Bank, Tata Steel and Reliance Ind, M&M,Axis Bank, HDFC and SBI.

PROFIT POOL: Oil share halves, Technology doubles; Public sector dwarfed| Profit Pool analysis FY03‐15: Some interesting trends from the past

India Inc PerforMeter

CAGR %

FY03‐FY15

FY03‐FY08

FY08‐FY15

FY15‐17E

PAT

16

27

9

20

Sensex

20

39

9

??

We expect a pick‐up in earnings growth for corporate India from the second halfof FY16; this could well be the beginning of the new earnings cycle. While ourEPS CAGR for the next two years is 20%, the earnings cycle has seen higher andlonger‐duration growth.

In Phase‐1 (FY03‐08) of our FY03‐15 analysis, PAT CAGR was 27%; it was only 9%

in Phase‐2 (FY08‐15).

We present some trends to draw from the last 13 years of earnings cycle andpick where reversion to mean can lead to a change in growth trends.#1 PUBLIC v/s PRIVATE SECTOR: The ultimate case study of value migration#2 CYCLICALS: Change in PAT orbit#3 OIL & GAS: PAT share halves to 17% in the best era of crude prices#4 FINANCIALS: Private sector cashes in on public banks' slip#5 CONSUMER: Only a foul‐weather friend? Not quiteBased on the above, we expect some of the following potential themes to playout going forward:#1 FY15‐17 PAT GROWTH: Expect acceleration in growth from 2HFY16, CAGR of

20% over FY15‐17.#2 PRIVATE BANKS, CONSUMER: Two large profit pools, which can only get

bigger and better (thereby creating several growth opportunities).#3 OIL & GAS: Reforms can normalize earnings, resulting in significant growth.#4 CEMENT: Early‐bird cyclical turnarounds?#5 CAPITAL GOODS: Book‐to‐bill ratio on the rise; govt spending to trigger

growth.

July 2015 2

7/24/2015 India Strategy: Getting on track!– Detailed Report

http://www.motilaloswal.com/site/rreports/HTML/635721163512170886/index.htm 5/85

India Strategy | Getting on track!

Exhibit 2: FY03‐15 India Inc PAT performance: Sector‐wise highlightsSector PAT (INR b) PAT CAGR (%) ROE (%)(No of Companies) FY03 FY08 FY15 FY17E FY03‐15 FY03‐08 FY08‐FY15 FY15‐17E FY03 FY08 FY15 FY17EAuto (11) 21 85 292 492 24 32 19 30 19 26 22 23Capital Goods (12) 15 80 99 174 17 40 3 32 12 25 10 14Cement (14) 7 97 60 146 20 69 ‐7 56 8 30 6 12Consumer (15) 48 75 209 304 13 9 16 21 38 35 33 37Financials (31) 141 341 951 1,395 17 19 16 21 30 14 15 16

Banks‐Private (10) 25 90 376 540 26 30 23 20 18 11 15 17Banks‐PSU (10) 87 192 313 491 11 17 7 25 25 18 10 13NBFC (11) 29 58 263 363 20 15 24 18 48 14 18 19

Healthcare (14) 17 51 169 280 21 25 19 29 25 21 20 22Media (11) 3 5 21 46 18 10 24 47 25 7 14 22Metals (9) 27 303 295 283 22 62 0 ‐2 15 26 10 9Oil & Gas (12) 265 529 638 1,004 8 15 3 25 25 19 10 13Real Estate (10) 1 91 26 47 30 142 ‐16 35 13 30 4 7Retail (3) 0 2 10 15 41 61 28 23 7 24 22 23Technology (11) 39 159 548 692 25 32 19 12 36 32 27 25Telecom (4) ‐4 133 110 129 L to P L to P ‐3 8 ‐3 22 8 8Utilities (10) 67 173 346 457 15 21 10 15 12 14 14 17Others (25) 6 23 62 107 21 29 15 31 15 17 15 20MOSL (192) 653 2,146 3,836 5,569 16 27 9 20 20 20 14 16

MOSL Univ. PAT Share (%)FY03 FY08 FY15 FY17E3 4 8 92 4 3 31 5 2 37 3 5 522 16 25 254 4 10 1013 9 8 94 3 7 73 2 4 50 0 1 14 14 8 540 25 17 180 4 1 10 0 0 06 7 14 12‐1 6 3 210 8 9 81 1 2 2

100 100 100 100

Source: Company, MOSL

ECONOMICS: A strong macro at early stage of recovery to create a virtuousinvestment cycle | Revenue buoyancy on growth to accelerate fiscalcorrection

Tax‐GDP ratio increased by around 400bp in the previous upcycle between FY02to FY08. The current phase of fiscal consolidation is being achieved on the backof expenditure compression and increased tax effort. However, a repeat of taxbuoyancy seen in the previous upcycle would allow accelerated reduction infiscal deficit to as low as 2% by FY20.Higher revenue, besides fiscal correction, would allow a jump in governmentexpenditure. Together with an expenditure switch towards capex spend awayfrom subsidy this would act as a big booster to investments in general.While many private infrastructure companies came up in the previous cycleploughing sizable investments in the economy; the winners of the current cycleare likely to be those well positioned to benefit from the direction of theeconomy that the government is seeking to give in the next five years.The fiscal discipline and macro stability should bring in its wake a revision in therating of India several notches higher than the current investment grade,particularly when the criteria laid out by S&P in its Sep‐14 rating outlookupgrade have all been satisfied by a comfortable margin and countries withcomparable macro parameters and credit history enjoy much higher ratings.On the inflation front, government has taken a multitude of measures to ensurethat the backbone of food inflation is broken through a series of interventionaimed at curbing prices, providing subsidy and other forms of support, improvedco‐ordination with the states and smoothing the supply chain to ensure higherfood availability. Other drivers of inflation viz., global commodity and foodprices, rural wage have all eased.

July 2015 3

7/24/2015 India Strategy: Getting on track!– Detailed Report

http://www.motilaloswal.com/site/rreports/HTML/635721163512170886/index.htm 6/85

India Strategy | Getting on track!

The structural decline in inflation can take rates and bond yields to a level evenlower than the low point of previous cycle particularly when net marketborrowing by the government is slated to decline releasing a good deal offinancial savings to be channelized into other forms of investments.After the bouts of volatility during late 2013, INR has returned to stability toemerge as one of the best performing currencies. The external stabilityparameters have also strengthened on the back of increased capital flows.Greenshoots of a capex recovery on the back of higher public spend towardsinfrastructure are visible already with CMIE capex data, recovery of IIP capitalgoods and sectors facing the focus areas of the government showing anuptrend. However, the biggest silver lining comes from a marked improvementin credit quality and some decline in the indebtedness of infra companies thatmakes them lendable again. With interest rate cycle headed south and selectivepush from the government this indeed is a more surefooted recipe forinvestment recovery.

Exhibit 3: Revenue buoyancy of 400bp in FY02‐08 economic upcycle – an equivalent jump now would take deficit to new low

Fiscal deficit to GDP (%)

14

12

10

8

6

4

2

0

6.0

11.9

10.3

A period ofstagnation on fiscalmanagement

Gross tax to GDP (%)14.1

9.98.0

6.0

Rising revenuehelped to correctthe deficit

Post crisis

10.0Expanding tax netkept collectionsteady and helpedcorrect deficit too

5.8

4.1

As corporate profitand buoyancy recoverstax collections wouldspike and deficit toreach new low

2.5 2.0

Source: Government, MOSL

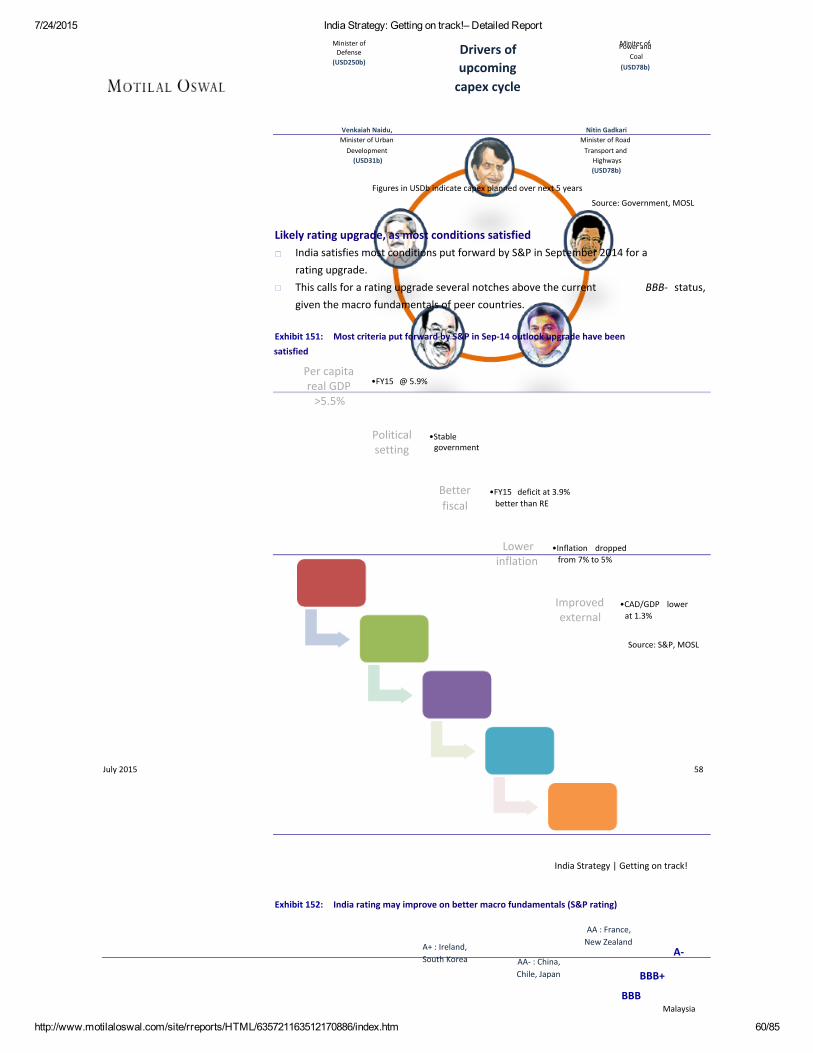

Exhibit 4: Government would be a significant catalyst for coming capex cycle

ManoharParikkar

Minister ofDefense

(USD250b)

Suresh PrabhuMinister of Railways

(USD94b)

Drivers ofupcomingcapex cycle

Piyush GoyalMiniter ofPower and

Coal(USD78b)

Venkaiah Naidu,Minister of UrbanDevelopment(USD31b)

Nitin GadkariMinister of RoadTransport and

Highways(USD78b)

Figures in USDb indicate capex planned over next 5 years

Source: Government, MOSL

July 2015 4

7/24/2015 India Strategy: Getting on track!– Detailed Report

http://www.motilaloswal.com/site/rreports/HTML/635721163512170886/index.htm 7/85

India Strategy | Getting on track!

Exhibit 5: Credit quality has improved noticeably

4.0

3.0

2.0

1.0

0.0

Credit ratio Modified credit ratio (RHS)1.2

1.1

1.0

0.9

0.8

Exhibit 6: Indebtedness of infra cos. on a decline now

1.2

1.0

0.8

0.6

0.4

0.2

0.0

Net Debt to Equity (x) D/E (x)1.40

1.20

1.00

0.80

0.60

0.40

0.20

0.00

Source: RBI, Government, MOSL Source: RBI, Government, MOSL

MARKETS & FLOWS: Indian equities have delivered positive returns for 3consecutive years

Indian equities have delivered positive returns for three consecutive years, andpositive returns in five out of the last six years.Sectoral performances have been very divergent in CY15YTD. Telecom was thetop performer with 14% return and significantly outperformed the Nifty (1%return); it was followed by Capital Goods (+13%) and Healthcare (+13%). PSUBanks (‐22%) and Metals (‐13%) were the top underperformers.Lupin was the best‐performing Sensex stock (32% return) for CY15, followed byMaruti Suzuki (21%) and HUL (21%). Hindalco, Tata Steel, Sesa Sterlite, HeroMotocorp, SBI, ITC, ICICI Bank, GAIL and Tata Motors were the topunderperformers (delivering negative returns of 10‐30%).Valuations of Indian equities are near the long‐term averages; need growth topick‐up. The Sensex trades at 16.9x P/E (slightly above its long‐period average of16.2x) and near its 10‐year average P/B of 2.8x.Domestic MFs have turned big buyers in Indian equities for 14 consecutivemonths. DII (ex MFs) have also turned net buyers by pumping in USD1.3b inthree months after 13 months of outflows.FIIs invested another USD6.2b in the first half of CY15 compared with USD16.2bin CY14. However, FIIs have been net sellers in recent months.FII holding in BSE‐200 companies is at an all‐time high of 25.6% compared withDII at 10.9%. FIIs have bought USD 169b in 23 years. Since Jan 2000, FIIs boughtUSD158b compared with DIIs’ USD8.8b. We expect this trend to stabilize asdomestic flows have turned positive now.Financial savings to increase; higher share toward equities likely.

STRATEGY:ECONOMIST:

Rajat Rajgarhia ([email protected])Dipankar Mitra ([email protected])

Sources of exhibits in this section include RBI, CMIE, Bloomberg, IMF, UN, Rogers International, Industry, Companies, and MOSL database

July 2015 5

7/24/2015 India Strategy: Getting on track!– Detailed Report

http://www.motilaloswal.com/site/rreports/HTML/635721163512170886/index.htm 8/85

India Strategy | Getting on track!

1QFY16 PREVIEW Another quarter of decline! Worst is likely over!1QFY16 performance of MOSL Universe: Third consecutive quarter of PATde‐growth

Our bottom‐up estimates indicate a 1% YoY decline in aggregate PAT for the MOSL

Universe (ex‐RMs). Sales would remain flat and EBITDA would grow moderately (4%).

The fall in global commodities, delay in revival of the investment cycle and muted

rural consumption continue to impact growth of corporate India.

Only seven sectors are expected to witness double‐digit PAT growth—Media (36%),

Telecom (23%), Capital Goods (18%), Private Banks (17%), Consumer (14%), Oil (11%)

and Retail (11%). Six sectors would likely report PAT de‐growth—Healthcare (‐1%),

Auto (‐7%), Real Estate (‐11%), PSU Banks (‐27%), Cement (‐33%) and Metals (‐52%).

Nifty PAT (ex‐BPCL) is likely to remain flat YoY—an improvement over 11% de‐growth

in 4QFY15. Sales would marginaly decline (‐1%) in 1QFY16 (v/s ‐6% in 4QFY15).

About one‐fourth of the Nifty constituents would report >15% YoY PAT growth;

however, this would be offset by PAT de‐growth in more than one‐third of the

constituents. Cyclicals and domestic‐facing companies would contribute to PAT de‐

growth (14 out of 17 PAT de‐growth companies are cyclical).

Top PAT growth companies are Maruti (77%), Tata Power (63%), Cipla (+41%), ONGC

(+41%), Idea (+36%), Yes Bank (+29%), Indusind Bank (+24%) and Bharti Airtel (+21).

Top PAT de‐growth companies would be Punjab National Bank (‐58%), Cairn India (‐

57%), Bank of Baroda (‐44%), NMDC (‐42%), Ambuja Cement (‐40%), Grasim (‐38%),

Hindalco (‐38%) and Tata Motors (‐31%).

Aggregate PAT to decline 1% YoY; sales to remain flatMOSL Universe’s (ex‐RMs) sales and EBITDA would grow marginally (1% each).Aggregate PAT would decline 1% YoY.

1QFY16 would be the third consecutive quarter of PAT de‐growth. Suchconsecutive PAT de‐growth was last witnessed in Sep‐09.Several domestic cyclicals like Auto, Cement and PSU Banks would de‐grow.Global sectors such as Metals and Healthcare would continue to report PATdecline; Technology would report one of the lowest PAT growth (7% YoY).Large sectors that would report growth include Consumer, Private Banks,NBFCs, Utilities, Oil and Technology.

EBITDA margins (ex‐Financials & RMs) would expand ~70bps YoY to 20%, nearits LPA of 20.2%—despite Cap Goods, Cement, Metals well below the LPA level.This quarter would see continued impact of fall in global commodities and aconsequent negative WPI impact.

MOSL Universe Quarterly PATGrowth YoY (%) LPA: 10%

Exhibit 7: PAT de‐growth in 1QFY16; expect rebound in 2H

39

22 25 24 26

10 14 125

1914

7 7 9

2230

16 13 16

2 18

‐6 ‐8 ‐1

6

‐14 ‐9

Source: Company, MOSL

July 2015 6

7/24/2015 India Strategy: Getting on track!– Detailed Report

http://www.motilaloswal.com/site/rreports/HTML/635721163512170886/index.htm 9/85

India Strategy | Getting on track!

Exhibit 8: Sales to remain muted during 1H

27 26

1722 21

25 2621 23

19

MOSL UniverseQuarterly Sales Growth

YoY (%) LPA: 13%1619

913

1014 14 12 14

6 5 51 0

‐5

4

‐6 ‐4

Source: Company, MOSL

Exhibit 9: 1QFY16 EBITDA margin (ex‐Financials& RMs) would expand 70bps to 20%; shows signs of bottoming out

23.222.3 MOSL Universe EBITDA

Margin LPA: 20.2%20.722.1 22.2 22.022.1 21.8

20.021.419.320.7 20.620.4

19.7 19.919.619.9 19.6 19.419.419.1 19.0 18.819.2 19.319.1 19.0 19.018.8 18.718.6

FY09 FY10 FY11 FY12 FY13 FY14 FY15 FY16

Source: Company, MOSL

Exhibit 10: 1QFY16 PAT margin (ex‐Financials & RMs) to expand 50bps to 10.5%

14.7

13.3 12.3

MOSL Universe PAT MarginLPA: 11.3%

10.9 11.0

13.112.6 12.6 11.012.2 12.211.911.9 10.410.511.8 11.4 10.011.2 11.1 10.810.5 10.310.7 10.210.310.110.610.010.210.5

9.4

FY09 FY10 FY11 FY12 FY13 FY14 FY15 FY16

Source: Company, MOSL

July 2015 7

7/24/2015 India Strategy: Getting on track!– Detailed Report

http://www.motilaloswal.com/site/rreports/HTML/635721163512170886/index.htm 10/85

India Strategy | Getting on track!

Exhibit 11: Sector‐wise 1QFY16 performance of the MOSL Universe

Sector

(No of companies)

High growth sectorsMedia (9)

Telecom (4)Others (18)Capital Goods (10)

Private Banks (8)Med/Low growth sectorsConsumer (15)

Oil Excl. RMs (9)Retail (3)

NBFC (11)Utilities (10)Technology (11)

PAT de‐growth sectorsHealthcare (14)Auto (11)

Real Estate (8)PSU Banks (6)Cement (7)

Metals (9)MOSL Excl. RMs (163)

MOSL Ex Oil & Metals (145)Sensex (30)Sensex Ex Oil & Metal (24)

Nifty Ex BPCL (49)Nifty Ex Oil & Metal (41)

Sales

Mar‐ Var % Var %15 YoY QoQ

1,13154

418171291

1983,371388

1,43342

120658729

2,990306

1,130

48273167

1,0667,492

4,9934,8122,955

5,5643,660

815

7110

18‐18

‐136

167

14

0123

821

‐61

7‐16

‐17

‐138

4‐4

‐39

3126

2310

‐345

‐38‐2

‐6‐20

‐71

‐20‐5

0‐3

EBITDA

Mar‐ Var % Var %15 YoY QoQ

38715

1522925

16684183

2784

111188178

61673

167

1618525

1521,845

1,4161,135809

1,4031,051

1618

15147

181112

68

141910

‐94‐1

‐40

‐14

‐294

957

38

‐921

64

‐60

‐676

217

‐513

03312

8‐17‐18

21

‐21‐6

1‐5

Net Profit PAT DeltaEBITDAMargin

Chg bpYoY

Mar‐ Var % Var %Share % Share %

15 YoY QoQ

1686

301718

9653058

1662

6897

140

2444683

65711

42943

735612455

737556

1936

231818

171014

1111

997

‐25‐1‐7

‐11‐27‐33

‐52‐1

354

01

‐1328

106

‐60

‐364

24‐11

‐2‐10

162140

09

‐25

24

17‐2

70

181

322

10566

180

71015

2659

161

4100

36323

773737

18863096

2233

75105128

‐1,093‐7

‐88

‐10‐284‐76

‐629100

22267

2354550

‐3827885

35416

‐155292‐102

‐220‐177‐64

‐388‐83

‐240

‐45381

4513640

8933

Source: Company, MOSL

Mixed bag in terms of sectoral performance: Share of global commodities inaggregate PAT to increase, led by Oil & Gas; Metals drag

Overall, seven sectors would report double‐digit PAT growth and six sectorswould report PAT de‐growth.Financials would report PAT de‐growth of 1%, a first, primarily driven by poorperformance of PSU banks

PSUs will account for a 37% share in the sector’s profits in 1QFY16 v/s 49%in 1QFY15

Technology would continue to report mid‐single digit growth (7%) for thesecond consecutive quarter; Healthcare would continue to witness negativegrowth (‐3% YoY)Capital Goods would report 18% growth after 11 consecutive quarters of PATdecline, thus giving indication of early signs of revival in investment cycle.Auto, Cement and Metals would continue to report PAT de‐growth.Sectors with record PAT:

Consumer and Telecom would report multi‐quarter high PAT numbersMetals would report its lowest PAT in eight years

Share of commodities in the aggregate PAT would increase in 1QFY16—areversal from the last few quarters, primarily led by Oil. Metals would continueto drag

8July 2015

7/24/2015 India Strategy: Getting on track!– Detailed Report

http://www.motilaloswal.com/site/rreports/HTML/635721163512170886/index.htm 11/85

India Strategy | Getting on track!

Exhibit 13: Contribution of global businesses^ would reduceExhibit 12: MOSL Universe ex‐Global Commodities PAT gr (%) to 48% in 1QFY16 and to 45% by FY16‐end

MOSL Universe Ex Global Commodities PAT growth (%)18

151212 10

63 3

45

‐2

44

Global business PAT Share (%)Others PAT share (%)

5556

5255

48

45

Source: Company, MOSL ^ Global businesses include IT, Healthcare, Metals, Oil (ExRMs), JLR Source: Company, MOSL

Exhibit 14: Sectoral quarterly PAT trend (INR b)FY12 FY13 FY14 FY15 FY16E

Jun Sep Dec Mar Jun Sep Dec Mar Jun Sep Dec Mar Jun Sep Dec Mar Jun Sep Dec MarAuto 50 52 63 80 56 50 47 76 50 71 81 77 89 74 75 59 83 94 99 103Capital Goods 23 28 34 65 26 27 28 60 17 22 26 55 15 20 22 44 18 25 31 57Cement 19 12 16 23 25 19 16 20 19 11 11 18 17 14 9 15 11 10 14 20Consumer 33 36 38 38 40 42 46 44 45 48 52 49 50 54 58 55 58 64 69 66Financials 129 151 163 193 179 180 190 205 202 182 194 213 223 213 209 222 221 239 265 291

Private Banks 42 45 52 57 54 57 67 71 70 72 80 85 82 85 95 100 96 101 113 119PSU Banks 51 65 71 91 80 74 71 73 75 52 52 64 78 63 48 52 57 63 72 87NBFC 36 41 40 45 45 49 51 60 57 58 61 64 62 65 66 69 68 74 79 84

Healthcare 20 22 21 23 22 28 28 31 34 41 45 43 45 52 33 37 44 54 54 61Media 4 4 4 3 4 5 5 4 5 5 6 5 5 5 8 6 7 7 9 8Metals 90 72 63 72 78 57 45 78 62 61 61 76 68 74 63 34 25 34 34 50Oil & Gas 56 38 284 367 ‐251 342 217 403 95 203 137 346 187 153 71 247 207 209 211 222

Oil & Gas Ex RMs 150 178 139 139 154 173 166 133 139 174 175 165 149 149 95 134 166 155 153 171Real Estate 6 6 5 6 5 4 6 4 5 4 4 5 5 4 5 5 5 4 9 6Retail 2 2 2 2 2 2 3 2 2 2 2 3 2 3 2 3 2 3 3 3Technology 66 67 80 82 89 91 95 95 104 119 127 132 130 135 142 140 140 144 152 159Telecom 16 15 15 16 12 11 6 6 13 12 12 18 20 24 24 22 25 24 25 27Utilities 42 41 42 50 50 47 50 48 50 51 52 50 50 51 48 58 56 62 56 62Others 12 10 10 11 12 10 10 11 12 11 13 14 14 12 14 16 17 16 18 20MOSL Univ Excl RMs 661 696 696 802 753 745 741 817 760 814 862 922 885 883 808 848 877 935 990 1,103

Comparable Universe, excludes Coal India, Just Dial, Prestige Estate, Bharti Infratel, Alembic Pharma, Vedanta due to merger, RattanIndiaPower, Hathway and Repco Home Fin. Source: Company, MOSL

Sector

July 2015 9

7/24/2015 India Strategy: Getting on track!– Detailed Report

http://www.motilaloswal.com/site/rreports/HTML/635721163512170886/index.htm 12/85

India Strategy | Getting on track!

Exhibit 15: Sectoral quarterly PAT growth trend (%)

FY16EFY12 FY13 FY14 FY15

Jun Sep Dec Mar Jun Sep Dec Mar Jun Sep Dec Mar Jun Sep Dec Mar Jun Sep Dec Mar

‐7Auto 7 4 30 52 12 ‐3 ‐25 ‐5 ‐12 41 71 2 79 4 ‐24 ‐7 27 32 75

12 ‐4 ‐18 ‐8Capital Goods 4 1 4 30 ‐33 ‐21 ‐6 ‐9 ‐13 ‐6 ‐16 ‐19 18 24 42 30

Cement 5 73 53 15 28 63 ‐2 ‐14 ‐26 ‐44 ‐33 ‐11 ‐10 26 ‐12 ‐16 ‐33 ‐25 44 32

14 18 19 19Consumer 15 19 17 22 24 15 23 18 13 17 12 11 11 12 11 13

‐1 12 27 31Financials 1 18 13 57 39 19 16 6 13 1 2 4 10 17 8 417 18 19 20Private Banks 31 28 27 29 30 27 28 25 29 26 20 20 18 19 19 17

PSU Banks ‐22 9 6 124 56 14 0 ‐19 ‐6 ‐30 ‐27 ‐12 4 21 ‐9 ‐18 ‐27 1 51 669 15 20 22NBFC 17 23 11 18 23 20 29 34 26 18 20 6 10 11 7 9

Health Care 15 4 8 8 9 27 35 34 57 50 58 42 34 25 ‐25 ‐14 ‐3 4 62 6432 36 15 36Media 14 8 ‐8 ‐34 ‐2 8 22 25 26 12 21 13 ‐5 3 31 17

4Metals 14 2 ‐12 ‐24 ‐13 ‐22 ‐29 8 ‐20 8 37 ‐3 9 22 ‐55 ‐64 ‐55 ‐46 46

Oil & Gas 60 ‐84 61 96 PL 812 ‐24 10 ‐138 ‐41 ‐37 ‐14 97 ‐25 ‐48 ‐29 10 36 197 ‐10

Oil & Gas Ex RMs 43 25 ‐11 9 3 ‐3 19 ‐4 ‐10 1 6 24 8 ‐14 ‐46 ‐19 11 4 60 28

Real Estate ‐4 ‐10 ‐37 ‐8 ‐5 ‐31 11 ‐29 ‐6 ‐10 ‐34 20 8 ‐2 16 ‐11 ‐17 14 94 2911 7 32 29Retail 68 17 13 52 6 14 22 24 15 5 ‐12 12 ‐6 24 5 ‐27 7 7 13Technology 20 13 24 26 35 35 19 15 17 30 34 39 25 13 11 6

25 1 1 24Telecom ‐26 ‐38 ‐30 ‐13 ‐26 ‐25 ‐57 ‐58 10 13 95 170 53 91 99 2612 21 16 6Utilities 8 6 13 3 18 14 19 ‐4 2 9 4 4 0 1 ‐8 16

18 39 25 25Others 30 ‐10 ‐1 ‐6 ‐1 1 8 ‐4 2 13 26 30 20 8 11 14

‐1 6 22 30MOSL Univ Excl RMs 14 12 5 19 14 7 7 2 1 9 16 13 16 8 ‐6 ‐8Comparable Universe, excludes Coal India, Just Dial, Prestige Estate, Bharti Infratel, Alembic Pharma, Vedanta due to merger, RattanIndiaPower, Hathway and Repco Home Fin. Source: Company, MOSL

Sector

Distribution of PAT growth to improve slightlyNearly one‐fifth (21%) of the companies would report >30% PAT growth,roughly same as in the previous quarter. Companies reporting >15% growthwould increase to 22% from 17% in 4Q.Less than one‐third of the companies would report PAT de‐growth, a welcomechange from nearly 40% in 4Q.

Exhibit 16: Broadbasing of high PAT growth companies

Earnings Growth >30% >15‐30% >0‐15% <0% Ex RMs (%)

55 36 34 25 15 24 26 20 ‐8 ‐15 ‐15 ‐11 23 42 26 22 24 9 13 11 4 18 11 8 5 0 ‐2 8 13 10 17 7 ‐7 ‐9 ‐1 6 2231

11 17 14 14 13 1321 24 23 26 25 24 31 26 28 263011 32 35 31 27 30 27 34 35 3939 39 42 40 36 37 44 3711 15 42 41 42 4011 19 181419 19 24 9 9 10 20 18 1819 23 2214 1426 2723 2813 24 19 2721 28 262517 16 18 21 22 2417 2311 18 16 1322 2418 23 172218 2122 10

18 262114 16 1524 25 18 22 18 16 221060 54 19 21 22 1719 16 1852 48 5144 45 41 43 39 4438 32 39 3535 30 3226 27 21 21 24 25 25 27 26 24 20 26 24 20 19 26 18 20 21 26

PAT Growth Ex RMs (%)

Source: Company, MOSL

July 2015 10

7/24/2015 India Strategy: Getting on track!– Detailed Report

http://www.motilaloswal.com/site/rreports/HTML/635721163512170886/index.htm 13/85

India Strategy | Getting on track!

Nifty PAT would remain flat; de‐growth in sales to continueWhile Nifty PAT (ex‐BPCL) is likely to remain flat YoY, it marks an improvementover 11% de‐growth in 4QFY15. Sales would marginaly decline (‐1%) in 1QFY16(v/s ‐6% in 4QFY15).Cyclicals and domestic‐facing companies would contribute to PAT de‐growth (14out of 17 PAT de‐growth companies are cyclical)Most of the top PAT growth companies—Tata Power (+63%), Idea (+36%), Cipla(+41%), ONGC (+41%)—were aided by lower base.Top PAT growth companies would be Maruti (77%), Tata Power (63%), Cipla(+41%), ONGC (+41%), Idea (+36%), Yes Bank (+29%), Indusind Bank (+24%) andBharti Airtel (+21).Top PAT de‐growth companies would be Punjab National Bank (‐58%), CairnIndia (‐57%), Bank of Baroda (‐44%), NMDC (‐42%), Ambuja Cement (‐40%),Grasim (‐38%), Hindalco (‐38%) and Tata Motors (‐31%).

38 LPA: 15%

3

‐10‐14‐20‐24

12 1124

716

7 8

‐3 ‐4

1015 11 18

216

‐9‐110

6

Exhibit 17: 1Q Nifty PAT to remain flat YoY—an improvement from de‐growth in 3Q/4Q, but significantly below LPA of 15%

36 37 45 5129

44

207

‐6

23 2630 30

23 24 21 21 23 28 2533

13 14

FY05 FY06 FY07 FY08 FY09 FY10 FY11 FY12 FY13 FY14 FY15 FY16

Source: Company, MOSL

Exhibit 18: Nifty sales to de‐grow 1% in 1QFY16—the third consecutive quarter of de‐growth

2226 30 24 32 30 31

19 1914

19 2231 31 31 37 31 31

17

8

‐2

27 2521 19 22

2521 23

LPA: 18%

19 1612 8 5 2

13 14 12 154

‐1 ‐1

3

‐6

18

9

‐8 ‐6

FY05 FY06 FY07 FY08 FY09 FY10 FY11 FY12 FY13 FY14 FY15 FY16

Source: Company, MOSL

Exhibit 19: Expect 1QFY16 Nifty (ex‐RMs) EBITDA margin to improve and move above LPA of 25.4%

31.3

30.230.3 30.5

29.527.8

28.9

27.1 26.226.0 25.7

25.9 25.4

LPA: 25.4%

26.225.4 25.225.3 25.4 25.525.0 25.0

24.7 24.324.024.3 25.3 23.6 23.6 25.123.122.7 23.323.6 23.9 24.823.824.1 23.4 23.222.523.0 22.8 22.322.5

27.726.9

27.0 26.6

FY05 FY06 FY07 FY08 FY09 FY10 FY11 FY12 FY13 FY14 FY15 FY16

Source: Company, MOSL

July 2015 11

7/24/2015 India Strategy: Getting on track!– Detailed Report

http://www.motilaloswal.com/site/rreports/HTML/635721163512170886/index.htm 14/85

India Strategy | Getting on track!

Exhibit 20: 1QFY16E performance of Nifty companies (INR b)Sales EBITDA PAT

Jun‐15 Var % YoY Jun‐15 Var % YoY Jun‐15 Var % YoYHigh PAT Growth (12) 1,205 11 458 18 202 31Maruti Suzuki 132 16 22 62 13 77Tata Power 95 9 26 46 4 63Cipla 33 23 7 33 4 41ONGC 235 8 133 6 67 41Idea Cellular 89 17 32 29 10 36Yes Bank 10 40 9 41 6 29IndusInd Bank 10 22 9 16 5 24Bharti Airtel 238 4 85 10 13 21HDFC Bank 63 22 46 20 27 20Axis Bank 39 17 35 20 20 18Bajaj Auto 59 11 11 22 9 17NTPC 202 12 43 31 24 17Med/Low PAT Growth (20) 2,444 ‐3 613 11 400 8Asian Paints 36 8 6 15 4 14Hero MotoCorp 69 ‐1 8 16 6 13TCS 258 17 73 14 57 12Kotak Mahindra Bank 17 15 11 13 6 12GAIL 140 5 12 15 7 12Power Grid Corp. 46 18 40 19 13 12ICICI Bank 51 15 51 13 30 12Hind. Unilever 85 11 15 16 11 12Reliance Inds. 752 ‐22 89 18 62 10Larsen & Toubro 109 5 12 7 8 9Wipro 124 11 28 9 22 7Dr Reddy’ s Labs 38 9 9 12 6 6Coal India 190 7 47 11 43 6ITC 93 0 33 1 23 5Infosys 141 10 38 9 30 4Bosch 26 10 5 7 3 2HDFC 20 16 20 2 14 1HCL Technologies 97 16 23 3 19 1State Bank 138 4 92 5 34 1Zee Entertainment 13 22 3 ‐10 2 0Negative PAT Growth (17) 1,915 ‐4 332 ‐21 134 ‐37Tech Mahindra 62 22 9 1 6 ‐5BHEL 45 ‐12 2 ‐21 2 ‐8Lupin 32 ‐2 8 ‐21 6 ‐10Vedanta 172 1 43 ‐24 17 ‐14Mahindra & Mahindra 93 ‐6 11 ‐20 7 ‐20Ultratech Cement 61 7 10 ‐4 5 ‐27ACC 30 0 3 ‐24 2 ‐27Sun Pharma 67 6 17 ‐8 10 ‐28Tata Motors 636 ‐2 95 ‐14 37 ‐31Hindalco 255 6 22 7 4 ‐38Grasim Industries 14 ‐3 1 ‐17 1 ‐38Ambuja Cements 25 ‐8 4 ‐38 2 ‐40NMDC 19 ‐45 12 ‐50 11 ‐42Bank of Baroda 33 0 24 ‐2 8 ‐44Cairn India 27 ‐39 14 ‐57 12 ‐57Punjab National Bank 40 ‐8 28 ‐10 6 ‐58Tata Steel 304 ‐16 27 ‐36 0 PLNIFTY Ex BPCL (49) 5,564 ‐1 1,403 3 737 0Note: For Financials, Sales represents Net Interest Income, and EBITDA represents Operating Profit

Company PAT Contbn(%)

27211911124313

5411811242813163402350

1810121101510021210

100

EBITDA marginJun‐15 Var (bp)

38 22616 46127 68822 16257 ‐10436 32586 10689 ‐46436 21174 ‐7890 23819 16721 30325 30417 10712 17328 ‐5866 ‐1168 70

86 6899 ‐13818 8612 39711 2323 ‐3224 5025 9736 1627 ‐2218 ‐51

100 ‐1,27423 ‐29867 3221 ‐75017 ‐36815 ‐3114 ‐43

26 ‐61225 ‐82912 ‐20916 ‐18310 ‐31526 ‐41015 ‐2239 98 ‐124

14 ‐70463 ‐65073 ‐13752 ‐2,17470 ‐1369 ‐279

25 89Source: Company, MOSL

July 2015 12

7/24/2015 India Strategy: Getting on track!– Detailed Report

http://www.motilaloswal.com/site/rreports/HTML/635721163512170886/index.htm 15/85

India Strategy | Getting on track!

Some interesting sectoral trends in 1QFY16 earnings

Key PAT growth sectorsAll Capital Goods companies (except BHEL and Voltas) would report PAT growth.Except L&T (9%), all companies would report double‐digit PAT growth.All Consumer and Retail companies (except United Spirits) would report PATgrowthAll Pvt Banks and NBFCs (except DCB Bank) would report PAT growth

Key PAT de‐growth sectorsAll PSU Banks (except SBI and Indian Bank) would report PAT de‐growthAll Metal companies would report PAT de‐growthAll Cement companies (except India Cement and Ramco Cement) would reportPAT de‐growth

Exhibit 22: 1QFY16 sectoral PAT growth (%)

3623 18

14 11 11

Exhibit 21: 1QFY16 sectoral sales growth (%)

15 1412

10 8 8 7 7 63

1 1 09 7

‐1 ‐1 ‐1 ‐7 ‐11

‐33‐52

‐6‐13

Source: Company, MOSL Source: Company, MOSL

Exhibit 23: 1QFY16 sectoral EBITDA margin (%)

36.5 32.528.6 27.9

24.4 23.7

Exhibit 24: 1QFY16 sectoral PAT margin (%)

19.2

21.3 20.0 19.414.9 14.8 14.7

14.8 14.7 14.29.3 8.4

12.0 12.0 11.6 10.57.3 7.3 6.7 6.1

5.4 4.0

Source: Company, MOSL Source: Company, MOSL

July 2015 13

7/24/2015 India Strategy: Getting on track!– Detailed Report

http://www.motilaloswal.com/site/rreports/HTML/635721163512170886/index.htm 16/85

India Strategy | Getting on track!

Other sectorhighlights

AUTOSAfter an initial spurt last year post elections, demand recovery is losingmomentum, with no improvement in the underlying economic environment.M&HCV volumes continued to recover in 1QFY16 (third consecutive quarter ofrecovery, after nine quarters of decline), with ~15% YoY growth; PV volumeswere up by ~7%. However, other segments witnessed muted demand, with 2Wand LCVs volumes flat YoY.Margins for our auto OEM (ex JLR) coverage universe are expected to expand180bp YoY (50bp QoQ) to 11.5%, driven primarily by AL (+460bp) and MSIL(+460bp), partially offset by MM (‐210bp). EBITDA is likely to grow ~31% YoY(~2.2% QoQ) for our coverage universe (ex JLR), translating into ~19% growth inPAT. While AL is expected to report its fourth consecutive quarter of PAT atINR1.4b (v/s ~INR479m loss in 1QFY15), TVS PAT is likely to grow ~46% and EIMPAT 54%. MM’s PAT is estimated to decline by ~20% YoY. We expect margins toimprove over the next two years, driven by demand recovery‐led discountmoderation, soft commodity prices and operating leverage.

Exhibit 25: EBITDA margin (ex JLR) recovery to continue fromtroughs of 4QFY14 Exhibit 26: Auto aggregate PAT growth constrained by JLR

18

15

127

9‐3

6 ‐25‐5 ‐12

430

52

1241

2 4

‐7‐24

‐7

Aggregate (excld JLR) Aggregate (incl JLR) Auto PAT growth YoY (%) Auto Ex JLR PAT growth YoY (%)

112

71 79

Source: Company, MOSL Source: Company, MOSL

Exhibit 27: Market share of BJAUT to improve in FY16, driven by CT‐100 launchEconomy ‐ MS (%)

Lack of self‐start (SS) option in Platina hurt Bajaj Autoas SS grew tp ~50% of Economy segment

CT100 & Platina Self 40Start launch

34

30

25 25 24 2521

27

33

Source: Company, MOSL

CAPITAL GOODSManagements are expected to guide for cautious optimism, as improvedbusiness sentiment is yet to result in increased tenders, leading to slower paceof order finalization. For 1QFY16, we expect 2% revenue growth and EBITDA

14July 2015

7/24/2015 India Strategy: Getting on track!– Detailed Report

http://www.motilaloswal.com/site/rreports/HTML/635721163512170886/index.htm 17/85

India Strategy | Getting on track!

margins improving 80bp to 9%. Order inflows for 1QFY15 would be muted, asordering activity from domestic customers is yet to pick up.Project executing companies are restructuring their balance sheets and infusingcapital to prepare for the next level of growth.ABB continues to invest in localization initiatives, Voltas continues to bidcautiously. For Cummins, exports would remain the key growth driver, whichwould support operating leverage (current capacity utilization ~50‐55%). Thereremains a sense of guarded optimism on the near term outlook.

Exhibit 28: Revenue to witness muted growth led byconstrained execution

Sales (INR b) Growth (%) YoY

Exhibit 29: EBITDA margin to improve by 80bps YoY

EBITDA Margin (%)

Source: Company, MOSL Source: Company, MOSL

Exhibit 30: Capital Goods revenues flat led by constrained execution; BTB stable at 3.1x

Capital Goods Sales growth (%) BTB (X)

2.9 3.0 3.1 3.12.9 2.8

2.62.3 2.3

11 17

2.2 2.22.1

6

‐5 ‐2

2.3 2.3 2.4

0

2.32.6

15 19 16 0

‐4 ‐1 ‐4 ‐4 ‐7‐13 ‐7

Source: Company, MOSL

July 2015 15

India Strategy | Getting on track!

7/24/2015 India Strategy: Getting on track!– Detailed Report

http://www.motilaloswal.com/site/rreports/HTML/635721163512170886/index.htm 18/85

CEMENTDemand momentum slowly improved within 1QFY16 after decline in April, 2‐3%growth in May and a mixed bag trend in June (0‐5%) based on regional intensityof rainfall (lower rainfall in the north led to better volumes than west in June).Overall, north and east are expected to post relatively better volume growth in1QFY16 v/s west and south (south showing weakest volume trend with near‐double digit de‐growth). We estimate ~1.5% YoY growth for the industry, whileMOSL cement universe to grow by ~3.4% YoY (+5.5% QoQ) due to multipleinstance of new capacity commencement viz. Shree Cement, JK Lakshmi andDalmia Bharat. Effective utilizations stood at ~70% (‐3pp YoY, ‐1pp QOQ).Cement prices (ex‐south) are down 4‐8% QoQ in 1QFY16—the west and thenorth were worst affected, with 7‐8% decline QoQ (though select pockets sawINR10‐30/bag uptick during June). East and central regions posted 3‐4%QoQ dipin average prices, while production discipline in south continues to hold pricesQoQ. We are factoring in INR150‐200/ton (~4%) QoQ drop in realizations ofMOSL coverage universe, including largely flattish (0‐1% QoQ dip) for southernplayers. We are factoring in for INR10/INR17 per bag (5%/9%) YoY rise inrealizations in FY16/FY17.Sharp decline in realization would hurt profitability by INR150‐200/ton (4ppQoQ dip in margins). Cost should remain flattish amidst (a) 3‐4% QoQ decline inimported coal and pet coke prices, (b) 2.7% rise in rail freight and ~3% dieselcost , (c) rise in packaging cost as crude revived, and (d) marginal positiveoperating leverage QoQ.We expect MOSL universe EBITDA/ton at INR660 in 1QFY16 (‐INR189 QoQ, ‐INR117 YoY) with southern players likely to post EBITDA/ton of INR900‐1,200(~1pp QoQ dip in margins). We factor in for EBITDA/ton of INR818/1,096 per tonin FY16/FY17 as against ~INR727 in FY15.

Exhibit 32: MOSL universe cement volumes to grow 4.7% YoYin 1QFY16

Aggregate Vol (m ton)

13.810.49.4 8.4

4.0 3.32.7 1.9 1.50.4(2.0)

Volume growth (%)

9.15.3 4.4 4.7

Exhibit 31: Volume growth trend (%) signifies weakness incement demand in 1QFY16 (%)

15

10

5

0

‐5

‐10

MOSL Universe IIP data

6.1

(5.8)

35 34 36 42 38 35 37 41 38 36 37 43 42 38 39 41 44

Source: Company, MOSL Source: Company, MOSL

CONSUMERWe expect our Consumer universe to post 7.5% revenue growth and 13.8% PATgrowth in 1QFY16. Broadly, consumption trends continue to remain sluggishacross categories and geographies (rural growth>urban despite incrementalpressure on rural wage growth, given lower salience in overall revenue

July 2015 16

India Strategy | Getting on track!

7/24/2015 India Strategy: Getting on track!– Detailed Report

http://www.motilaloswal.com/site/rreports/HTML/635721163512170886/index.htm 19/85

contribution). We expect clear trends in rural to emerge only post monsoonsand a possible pick‐up in government spending.1QFY16 should see continued benefit of raw material easing. While competitiveintensity has picked up marginally in certain HPC categories, organized playershave been proactive in pre‐empting and tackling competition. However, webelieve the price cuts/discounts have not yet changed the volume trajectorymateriall. We expect EBITDA to grow at 12% in 1QFY16 for our coverage.

Exhibit 33: EBITDA to grow 12% in 1QFY16 aided primarily byRM softening Exhibit 34: Consumer ex‐ITC PAT growth healthy

Sales Growth (%)

21.1

20.219.8

20.5 20.520.2

EBITDA margins (%)

21.3

20.4 20.5

21.621.3 21.3

26

17

1012

19

10

24Consumer Ex ITC PAT grw YoY (%)

16

9

18

9

58 9

12

1921

21.0 21.2 21.2

19.3 20.3 15.0 16.7 16.4 13.6 10.6 10.3 11.0 11.1 14.6 12.3 7.8 6.6 7.5

Source: Company, MOSL Source: Company, MOSL

FINANCIALSPSU banks: PSU banks’ PPP/PAT is expected to grow 0%/‐27% YoY on account oflower balance sheet growth and continued asset quality troubles. Higher‐than‐expected NPAs (especially relapse from RL) will be a drag on earnings. Over thelast year, Indian banks, mainly PSUs, have sold ~INR600b worth assets to ARCs;we believe write‐downs and resultant MTM provisioning for the same (as perRBI guidelines) would begin over the next one/two quarters. SBIN remains ourtop pick to play revival in Indian economy.Private sector banks: For private banks, healthy core operating performanceand one off income (repatriation of capital) will help to manage earnings. Weexpect PPP and PAT growth of ~18% YoY and ~17% YoY. Our top picks areHDFCB, AXSB, YES and DCBB in private sector.

Exhibit 35: Higher opex and provisions would be a drag onPSU bank’s profitability; healthy growth in profitability forPrivate banks to continue (PAT growth % YoY)

Private Banks

29.3

‐5.9

‐29.7 ‐26.8

25.820.0 19.7

‐12.1

18.0

3.5

PSU Banks

20.6

18.6

18.6

‐8.9

17.1

‐18.3

16.8

Exhibit 36: Share of PSUs in sector profits will be down to37% in 1QFY16 vs 49% in 1QFY15

PVT Banks PAT Share (%) PSU Bank PAT Share (%)

42 40 43 49 42 33 34 3755 59 58 61 60 56 52 51 52

58 60 57 51 58 67 66 6345 41 42 39 40 44 48 49 48‐26.8

Source: Company, MOSL

July 2015

Source: Company, MOSL

17

India Strategy | Getting on track!

7/24/2015 India Strategy: Getting on track!– Detailed Report

http://www.motilaloswal.com/site/rreports/HTML/635721163512170886/index.htm 20/85

NBFCs: We expect the NBFCs under our coverage to deliver 8.8% YoY PATgrowth. For retail NBFCs, the quarter would be marred by seasonal weakness,translating into lower growth and margin contraction. However, timely onset ofmonsoon and sharper focus on recoveries would lead to above trend‐lineperformance on asset quality. Improving macroeconomic environment, stableliquidity, easing wholesale rates and reduction in repo rate by the RBI are thekey positives. While incremental data points indicate bottoming‐out of thecycle, growth and asset quality outlook is expected to improve gradually forNBFCs. Top picks are IDFC and MMFS.

Exhibit 37: PAT growth for NBFCs universe expected at 8.8%

28.8

23.420.3

32.1

24

15.718.8

6.79.4 10.9

5.78.7 8.8

Source: Company, MOSL

HEALTHCAREWe estimate 14.2% growth in sector revenue in 1Q, supported by strongperformance in domestic market. However, weak quarter in US for few large capcompanies is likely to pull down overall EBITDA margins to 23.7% (‐180bp). PATis expected to remain flat, mainly on account of higher deprecation during thequarter. We believe Cipla, Cadila, Torrent Pharma and Alembic Pharma arelikely to deliver strong operational performance in 1Q.Slow pace of approvals in US and increased pricing pressure is expected toimpact larger players like – Sun Pharma, Lupin and Dr Reddy’s. However, Cipla islikely to benefit from gNexium supply to its partner Teva (sole gneric player). Indomestic business, all large cap companies are expected to post double digitgrowth aided by price increase undertaken in April and continued traction inspecialty therapies. According to NPPA, Indian pharma companies are allowedto take 3.6% price hike on NLEM products and 10% price hike on Non NLEMproducts from April 2015.In Mid Caps, apart from IPCA, most of the other companies are expected tobenefit from recent surge in ANDA approvals for their US filings. Alembic andTorrent are expected to deliver strong US numbers on account of gAbilifylaunch. Aurobindo and Glenmark are also likely to benefit from recent druglaunches in US market. Cadila would continue to gain from price hike in HCQ andexpected to report good growth in US.We expect Sun pharma to post muted numbers in 1Q on the back of (1) Ongoingsupply constrains at Halol plant, (2) Lack of approvals in US, (3) Price erosion insome of the Taro products and (4) Difficulties in Ranbaxy merger.

July 2015 18

India Strategy | Getting on track!

7/24/2015 India Strategy: Getting on track!– Detailed Report

http://www.motilaloswal.com/site/rreports/HTML/635721163512170886/index.htm 21/85

The INR depreciated 8% YoY against the USD in 1QFY16 (63.5 v/s 59 in 1QFY15).Hence, 1QFY16 net sales of export‐oriented companies may be higher thanwitnessed in the last 2‐3 quarters.However, emerging market currency crisis will affect companies such as DrReddy’s, Torrent Pharma and Glenmark in our coverage. Similarly, somenegative impact of Euro depreciation would be visible in companies such asAurobindo, Torrent Pharma and Cipla, which have a higher proportion of Eurosales in the overall revenue.

Exhibit 38: Healthcare: EBITDA Margin to contract by 180bp

EBITDA Margin (%)

22.9

20.722.1 22.4

23.0

21.3

23.023.7 24.2 24.0

25.526.4

24.0 23.7

21.6 22.0

19.4

*4QFY15(excluding sun pharma): 21% Source: Company, MOSL

MEDIAWe expect 14% aggregate PAT growth in 1QFY16 but 23% growth ex‐ZEE.Earnings growth is expected to be divergent. Among the print companies, DBcorp is expected to see pressure on its advertising revenue led by continuedweakness in demand from key segments. This coupled with increased launchand start‐up expenses are expected to keep PAT under pressure. Printcompanies (ex‐DB Corp) are also expected to see a flat bottom‐line YoY. Benignnewsprint prices will provide some solace. While ZEE’s earnings would beimpacted by increased &TV and sports losses. Earnings are expected to remainflat for SUNTV led by likely escalation in content costs. Pay TV operators (DISHTVand HATH) are expected to report improved profitability in the form of lowerlosses in the case of Hathway. Dish too is expected to continue its PAT +vestreak after its PAT turnaround in 4Q.We expect our universe ad revenue growth to recover to 9% YoY vs 7% each in4QFY15 and FY15. ZEE would be the only media company to report more than20% ad growth on the back of its new channel launch. Our industry interactionsindicate that growth remained soft for most of 1QFY16, with likely pick‐up in 2H.

July 2015 19

India Strategy | Getting on track!

7/24/2015 India Strategy: Getting on track!– Detailed Report

http://www.motilaloswal.com/site/rreports/HTML/635721163512170886/index.htm 22/85

Exhibit 39: Media: Quarterly PAT (INR b)7.4

4.3 4.75.3 5.8

4.6

5.94.8 4.9

5.6 5.35.8

6.4

Source: Company, MOSL

METALSAlthough steel demand is gradually improving with single digit growth, thecontinuous pressure of imports has been shrinking market for domestic mills.Post a poor 4QFY15, we expect our Metals coverage universe to post anotherweak quarter, with aggregate EBITDA declining 32% YoY (growing 7% QoQ)amidst lower metal prices (ex‐Zinc) and persisting imports.We have cut EBITDA estimates for steel companies by 3‐10% on lowerrealizations.While LME aluminum was largely unchanged QoQ (at USD1,800/ton), spotpremiums came under significant pressure.Zinc prices were supportive in the quarter, up 5% QoQ / 6% YoY to USD2,192.Volumes would be up ~30% YoY, but due to more than tripling of royalty YoY(due to DMF), we expect EBITDA to increase by just 12% YoY for Hindustan Zinc.We cut our LME (aluminum) assumption from USD1,900/ton to USD1,800/tonfor FY16, and from USD1,950/ton to USD1,900/ton for FY17. Thus, our EBITDAestimates for Hindalco and Nalco are cut by 5% for FY16 and by 25% for FY17.Our target prices are cut from INR206 to INR179 for Hindalco, and from INR77 toINR72 for Nalco. For Vedanta, we cut our EBITDA estimates for FY16 and FY17 by1%, and trim our target price from INR209 to INR177 on lower aluminum LMEand spot aluminum/zinc premiums, offset by higher INR/USD assumptions.

Exhibit 41: Steel sales volume to increase

SAIL

9.4

2.4

3.2

2.3

Tata Steel

7.8

2.6

2.6

2.0

8.9

3.1

3.0

2.0

8.9

3.1

3.0

2.1

SAIL

9.7

3.1

3.5

2.4

JSW Steel

8.5

2.9

2.8

2.1

8.8

3.1

2.9

2.1

JSPL

8.7

3.0

2.9

2.1

9.4

3.1

3.2

2.4

9.3

3.0

3.3

2.1

Exhibit 40: India steel – EBITDA/ton (INR)

Average

20,000

15,000

10,000

5,000

0

JSW Steel

Tata Steel

JSPL

Source: Company, MOSL Source: Company, MOSL

July 2015 20

India Strategy | Getting on track!

7/24/2015 India Strategy: Getting on track!– Detailed Report

http://www.motilaloswal.com/site/rreports/HTML/635721163512170886/index.htm 23/85

OIL & GASIncluding DBTL, expect 1QFY16 under recoveries at INR91b (‐68% YoY). Whilethe DBTL component will be compensated by government, sharing of non‐DBTLand kerosene subsidy is not yet clear.Regional benchmark, Reuters Singapore GRM was up 40% YoY but down 6%QoQ to average at USD8.1/bbl led by higher gasoline cracks.In petchem, polymer (PE, PP, PVC) as well as polyester (POY, PSF) spreads wereup YoY and QoQ, however polyester QoQ increase was marginal.OMC’s demonstrate pricing power by tweaking marketing margins, lower QoQ.While upstream PSU’s are expected to report strong numbers led by almost nilsubsidy, still await clarity on long term subsidy sharingRIL’s standalone PAT is expected to be up 10% YoY to ~INR62b led by higherpetchem margin and GRM, partly negated by lower E&P profits.

Exhibit 43: Reuters Singapore GRM was up 40% YoY but down6% QoQ to average at USD8.1/bbl

Reuters Singapore GRM (USD/bbl)

120

105

90

75

60

45

30

15

0

109876543210

1QFY04 1QFY06 1QFY08 1QFY10 1QFY12 1QFY14 1QFY16

Exhibit 42: Diesel into over recovery zone post deregulation

Diesel (under)/over recovery (INR/ltr)

Brent crude price (USD/bbl) ‐ RHS6

3

0

(3)

(6)

(9)

(12)

(15)

Jun‐12 Dec‐12 Jul‐13 Jan‐14 Aug‐14 Feb‐15

Source: Bloomberg, MOSL Source: Bloomberg, MOSL

REAL ESTATEEconomic recovery overhang delays realty pick‐upOver 1QFY16, the BSE Realty index underperformed the broader index by ~14%, asthe muted macro outlook and slow pace of on‐ground recovery continued as majoroverhangs. Affordability remains a dampener in most markets, led by (a) higherprice, (b) mismatch in product proposition, and (c) delay in economic revival.Investor participation is weak and the end‐consumers’ decision making time is yet tocontract. Prices are range‐bound and time correction is underway.

Launch momentum slow; presales to weakenLaunch momentum was slow in 1QFY16; developers continue to wait for approvalsunder new regulations (Mumbai, Chennai) or demand pick‐up. Select launches byGodrej Properties (Prime, Icon in Mumbai), Sobha Developers (Dream Acres inBangalore), Lodha (Central in Thane, Mumbai) did well. Broader presalesmomentum is slow in all market including Bangalore. QoQ, we expect lower presalesfor our coverage universe.

July 2015 21

India Strategy | Getting on track!

7/24/2015 India Strategy: Getting on track!– Detailed Report

http://www.motilaloswal.com/site/rreports/HTML/635721163512170886/index.htm 24/85

The NCR market showed marginal improvement on the residential front, withapproval for Dwarka Expressway expected to drive demand. DLF’s Camellia wouldpost stable momentum. Discount schemes and innovative offerings are in full swing.Developers like Tata Housing resorted to online property auctions and sales tooffload inventory. Operating cash flows for most companies would remain sub‐normal, resulting in rise in gearing levels.

PE activities strong; commercial market picking up graduallyThough private equity (PE) players remain upbeat on Indian real estate, the quarterwitnessed the exit of key PE players like ASK group and Milestone in certain projects.The commercial asset class is showing positive signs towards recovery in the NCRand Bangalore markets, with rentals picking up and demand outpacing supply.

Exhibit 44: Quarterly Trend in Presales value (INR b)Presales (INR b)

FY11 FY12 FY13 FY14

NCR Centric developers 102.6 90.9DLF 59.4 52.9Unitech 43.2 38.1Mumbai Centric developers 79.1 39.6IBREL 48.4 19.5HDIL 20.7 10.6ORL 10.1 9.5

Bangalore Centric developers 32.4 46.8Sobha 10.9 17.4PEPL 13.8 20.6Purva 7.6 8.8Brigade

Diversified 16.9 18.9MAHLIFE 7.0 6.0GPL (own stake) 10.0 12.8

66.3

38.228.138.7

30.0‐

8.7

68.222.2

31.114.97.9

18.84.414.4

1Q 2Q

FY15

3Q 4Q

21.5

19.81.721.8

5.54.012.3

21.26.3

10.11.33.5

4.22.51.7

FY15 YoY, %

46.9

38.68.352.1

20.314.117.7

86.621.0

43.714.214.3

17.77.010.7

‐36

‐22‐641

‐4889247

‐23‐39

‐15‐45‐29

‐3316‐47

55.8 6.5 11.1 7.9

40.7 3.1 9.2 6.515.1 3.4 1.9 1.439.7 10.0 8.3 12.0

30.7 5.6 4.0 5.25.6 3.0 3.3 3.83.4 1.4 1.0 3.0

75.7 21.4 23.2 20.923.4 4.8 5.6 4.3

36.3 13.1 12.9 7.616.0 3.5 4.7 4.813.4 2.5 4.1 4.2

16.3 4.1 3.9 5.43.7 0.5 0.9 3.112.6 3.6 3.0 2.3

TECHNOLOGYWe expect aggregate reported USD revenue growth of 2.6% QoQ across top tierIT companies in 1QFY16, with TCS leading organic growth at 4.1% QoQ in CCterms. Energy segment at WPRO and Telecom at TECHM will drag theperformance across those two companies. Tier II IT companies are expected tofare in a similarly polarized fashion, with aggregate growth estimated at 2.4%QoQ. PSYS, KPIT, CYL and MPHL all face specific headwinds to their portfolio.While INR appreciation of ~2.%+ QoQ along with relatively stable globalcurrencies is a tailwind to margins, wage hikes at TCS, INFO and WPRO, andgrowth issues in TECHM will offset the impact from the same. Only HCLT in tier‐Ishould see expansion in margins.Across tier I, our aggregate estimate for PAT growth is 7% YoY, led by TCS (12%).TECHM should lag with YoY decline of 5% due to lower margins. Tier II ITuniverse is expected to report a PAT growth of 12% YoY, led by HEXW (+41%YoY) and MTCL (+18% YoY). KPIT is expected to lag (‐17% YoY).

July 2015 22

India Strategy | Getting on track!

7/24/2015 India Strategy: Getting on track!– Detailed Report

http://www.motilaloswal.com/site/rreports/HTML/635721163512170886/index.htm 25/85

Exhibit 45: WPRO, TECHM to lag peers; expect TCS, CTSH tobenefit from 1Q seasonality

9

7

5

3

1

‐1

4.13.02.7

0.8(0.1)

TCS Infosys Wipro

Exhibit 46: Tier‐II IT performance impacted by several clientspecific issues during the quarter

Persistent Systems Hexaware KPIT Tech.Mindtree Mphasis

8.57.8 5.6

5.0 4.2 4.1 3.64.0 1.4 1.51.2 0.3 0.1 0.90.60.5

‐0.4

‐3.4

2QFY15

‐3.2‐5.6

3QFY15 4QFY15 1QFY16E

Source: Company, MOSL Source: Company, MOSL

Exhibit 47: Ex‐TECHM, CC YoY revenue growth is not expected Exhibit 48: Technology growth is expected to be one of theto witness deceleration lowest ever

3QFY15 4QFY15 1QFY16ETechnology PAT grw YoY (%)

35 35

20

13

24 2619

30

15 17

3439

25

13 11

6 7

TCS INFO WPRO HCLT TECHM CTSH

Source: Company, MOSLSource: Company, MOSL

TELECOMYoY earnings rebound to remain strong, with PAT for Bharti/Idea growing21%/36% YoY. PAT growth for Bharti Infratel should remain healthy at 16%.We expect ~19/29% YoY India mobile EBITDA growth for Bharti/Idea supportedby wireless traffic growth and continued momentum in data business. VoiceRPM is likely to be under pressure

Exhibit 49: Telecom: Quarterly PAT (INR b)

Bharti (India) Idea

19.4

13.98.9

2.3

2.1

2.4

2.5

2.3

2.5

10.8

3.8

2.9

14.8

4.9

3.6

14.0

4.5 4.7 5.9

4.7

7.3

4.6

7.6

4.7

7.7

5.1

9.4

23.8

Bharti Infratel

21.8 23.025.6 25.5 24.7

15.8

9.9

5.42.8 4.1 5.6

Source: Company, MOSL

July 2015 23

India Strategy | Getting on track!

7/24/2015 India Strategy: Getting on track!– Detailed Report

http://www.motilaloswal.com/site/rreports/HTML/635721163512170886/index.htm 26/85

UTILITIESIn April‐May 2015, all‐India generation grew 3% YoY, led by similar 3% YoYgrowth in coal generation, while gas based generation de‐grew by 14% YoY.Generation growth for the month of April stood at 0.3% YoY, while on set ofsummer led to rather better generation of 6% YoY in the month of May 2015.Coal project PLF has remained range‐bound at ~63%.Power demand stood flat YoY for the period April‐May 2015, comprising ofdemand de‐growth in the month of April to the tune of 3.5% YoY offset by 2.3%YoY improvement in demand in May 2015. Subdued demand growth is partlyled by poor DISCOMs financials, while our interaction with industry indicatesreal slowdown too impacting demand. Over the same period, power supplyincreased by 1.1% YoY, leading to base deficit of 2.3%, vs 4.1% YoY.We expect Utilities companies in our coverage to report revenue growth of 7.2%YoY and PAT growth of 8.7% YoY in 1QFY16. Aggregate PAT would be negativelyimpacted by de‐growth in PAT for JSW energy, and higher losses for RattanIndiaPower. However, NTPC (up 17% YoY), Powergrid (up 12% YoY), Coal India (up 6%YoY) and Tata Power (up 63% YoY) would report robust PAT growth.

Exhibit 51: Monthly generation appears flattish

All India Generation (BUs)27

13

4 6 6 7

0 16 7

05

1216

7

1113

4

Gr (YoY, %)

14 11

6

Exhibit 50: Coal project PLFs remain range‐bound

Coal Generation (BUs) PLF (%)

10

3

‐7

6

0

Source: CEA Source: CEA

Exhibit 52: Power demand remain muted (BUs)

FY142.3%

FY15 YTDFY16 Gr (%)

Exhibit 53: Base deficit remains subdued (%)12

9

6

3

YTD FY16 FY13 FY14 FY15

‐3.5%

0April May June July Aug Sept Oct Nov Dec Jan Feb Mar

Source: CEA

2.22.4

Apr May Jun Jul Aug Sep Oct Nov Dec Jan Feb Mar

Source: CEA

July 2015 24

India Strategy | Getting on track!

7/24/2015 India Strategy: Getting on track!– Detailed Report

http://www.motilaloswal.com/site/rreports/HTML/635721163512170886/index.htm 27/85

Exhibit 54: Peak deficit too trends lower (%)

16

13

10

7

4

1

‐2

3.52.3

YTDFY16 FY13 FY14 FY15

Exhibit 55: ST prices cool remain soft (INR/unit)

Apr May Jun Jul Aug Sep Oct Nov Dec Jan Feb Mar

Source: CEA Source: IEX

July 2015 25

India Strategy | Getting on track!

7/24/2015 India Strategy: Getting on track!– Detailed Report

http://www.motilaloswal.com/site/rreports/HTML/635721163512170886/index.htm 28/85

Intra‐sector 1QFY16 earnings divergence (%)Sectors Sector

Growth (%)

+30% Growth 15‐30% growth 0‐15% growth ‐ve earnings

growth (%)

Earnings

momentum

High growth sectors

Media 36

Telecom

Capital Goods

Banks ‐ Private

23

18

17

PVRL: 152%, SUNTV: 40%

DITV: LP

IDEA: 36%

SIEM: 878%, BHE: 117%,

TMX: 54%

JAGP: 27% Z: 0%

BHARTI: 21%,

BHIN: 16%

ABB: 28%, CRG: 14%, HAVL: 11%,

KKC: 19% LT: 9%

YES: 29%, IIB: 24%, FB: 15%, KMB: 12%,

HDFCB: 20%, ICICIBC: 12%

AXSB: 18%

PIDI: 30%,

DABUR: 26%,

SKB: 19%,

CLGT: 16%

DBCL:‐15%,HTML:‐49%, 3 1 1 4HATH:Loss,SCNL:Loss

RCOM: ‐4% 1 2 0 1

VOLT: ‐6%,

BHEL: ‐8%

DCBB: ‐3%

3 2 3 2

0 4 3 1

Medium/Low growth sectors

Consumer 14 JYL: 59%, GCPL: 52%,

BRIT: 48%, UNSP: LP

Retail

NBFC

11

9

SHOP: 335%,

JUBI: 51%

MRCO: 14%, APNT: 14%,

RDCK: 13%, HUVR: 12%,

HMN: 6%, ITC: 5%,

NEST: 1%

TTAN: 3%

4 4 7 0

2 0 1 0

Utilities 9

Oil & Gas

(Ex Rms)

Technology

7

7

MMFS: 27%, RECL: 9%, POWF: 7%,

IHFL: 25%,BAF: 24%, SHTF: 4%, HDFC: 1%,

LICHF: 20%,DEWH: 18%, IDFC: 1%

REPCO: 18%

TPWR: 63% PTCIN: 28%, CESC: 14%, PWGR: 12%, JSW: ‐24%,

NTPC: 17% COAL: 6%,NHPC: 3%, RTPOW: Loss

RELI: 0%

HPCL: 1399%, ONGC: 41%, GUJS: 25%, GAIL: 12%, RIL: 10%, IOCL: ‐9%,BPCL : ‐11%,

MRPL: LP OINL: 18% PLNG: 4% IGL: ‐13%, CAIR: ‐57%

HEXW: 41% TELX: 21%, TCS: 12%, WPRO: 7%, PSYS: ‐3%,

MTCL: 18% MPHL: 6%, INFO: 4%, TECHM: ‐5%,

HCLT: 1% KPIT: ‐17%

ALPM: 126%, CDH: 50%,

CIPLA: 41%, GLXO: 36%

MSIL: 77%, BHFC: 54%,

EIM: 54%, TVSL: 46%,

AL :LP

IBREL: 60%,

OBER: 54%

TRP: 25%,

DIVI: 21%

AMRJ: 19%,

BJAUT: 17%

GPL: 22%,

PEPL: 21%

0 6 5 0

1 2 5 2

3 2 3 4

5 31 2

PAT degrowth sectors

Healthcare ‐1

Autos ‐7

GNP: 10%, DRRD: 6%, SANL:‐3%,LPC:‐10%,4 2

ARBP: 6%, BIOS: 1% SUNP:‐28%,IPCA:‐78%

HMCL: 13%, MM: ‐20%,

EXID: 8% TTMT: ‐31% 5 2

PHNX: 5%

4 4

2 2

Real Estate ‐11

Banks ‐ PSU ‐27

Cement ‐33

Metals ‐52

Earnings momentum:

SOBHA: ‐5%,2 2 1 3DLFU: ‐14%,

MLIFE: ‐81%

INBK: 4%, BOB: ‐44%, 00SBIN: 1% UNBK: ‐48%, 2 4

BOI: ‐49%, PNB: ‐58%

TRCL: 234% UTCEM/ACC: ‐27%,1 0GRASIM: ‐38%, 0

6SRCM:‐79%ACEM:‐40%,

ICEM: Loss

HZ: ‐3%, VEDL: ‐14%,

NACL:‐18%,HNDL:‐38%, 0 0 0 9NMDC:‐42%,JSTL:‐90%,

JSP: PL, SAIL: PL,

TATA: PL

Represents number of companies in each of the growth brackets; PL: Profit to Loss; LP: Loss to Profit

July 2015 27

India Strategy | Getting on track!

7/24/2015 India Strategy: Getting on track!– Detailed Report

http://www.motilaloswal.com/site/rreports/HTML/635721163512170886/index.htm 29/85

FY16‐17 estimates Expect recovery in 2HFY16Government‐led capex and low inflation to lead recovery

Delay in domestic recovery and global commodity fall continue be the headwinds for

earnings growth. Other factors such as muted rural consumption, continuing asset

quality woes in PSU banks and adverse cross currency movements continue to pull

down the aggregate growth of corporate India.

However, we believe government‐led capital spending and favorable inflation leading

to lower rates will create conducive environment for earnings growth recovery.

Our bottom‐up estimates suggest aggregate PAT of the MOSL Universe (ex‐RMs) to

rebound to 17%/23% in FY16/FY17. Sales growth would increase moderately to 9% in

FY16 before jumping to 13% in FY17.

Expect Sensex EPS to grow 15% to 1,561 in FY16 and 22% to 1,907 in FY17. Since the

last preview, three‐fourths of the Sensex companies would see an EPS cut—led by

Tata Steel, Sun Pharma, Hindalco, Tata Motors, Coal India and GAIL. Top upgrade

drivers are Maruti, NTPC, ONGC and Bajaj Auto.

One‐third of the Sensex companies would contribute more than two‐thirds of FY16

Sensex EPS expansion. Key contributors to the EPS expansion would be ONGC, Tata

Motors, ICICI Bank, HDFC Bank, Tata Steel and Reliance Ind, M&M, Axis Bank, HDFC

and SBI.

FY16 Earnings cut—‘Murphy still at Work’Since March 2014, earnings have seen a 13% downgrade and earnings growthhas been cut by 2pp.Earnings cuts were driven by factors such as fall in commoditiy prices, delay inrevival of investment cycle, muted rural consumption, continued asset qualityissues at PSU banks and adverse cross currency movements that impact globalbusinesses.

Exhibit 56: Corporate earnings have seen a 13% downgradesince March 2014…

FY16 EPS (INR)

21.4

17.5

FY16 EPS Growth YoY (%)

19.9

2pp cut in FY16EPS growth since

Mar 2014

Exhibit 57: … driven by

#1

#2

#3

#4

Fall in commodity prices

Delay in revival of the investment cycle

Muted rural consumption

Persisting asset quality issues , esp. with the PSU banks

Adverse cross currency movements

Factors specific to companies

Source: MOSL

18.4

15.3

1,793

Mar 14

1,875

Sep 14

1,761

Dec 14

1,662

Mar 15

1,561

June 15

#5

#6

Source: MOSL, Company

#1 – Fall in commodity prices led to severe downgradesSince Apr‐14, global commodities (represented by CRB commodity index) havefallen ~15% (one‐year fall of ~14%). Oil, during a similar period, has correctedby ~44% (one‐year fall of 45%)

July 2015 27

India Strategy | Getting on track!

7/24/2015 India Strategy: Getting on track!– Detailed Report

http://www.motilaloswal.com/site/rreports/HTML/635721163512170886/index.htm 30/85

Global cyclicals contributed 31.6% of total Nifty earnings in the Mar‐14 preview.However, a 21% cut in earnings estimates has brought down the global cyclicalsearnings contribution to 28.2% (a drop of 334bp)Major cuts were led by Tata Steel (63%), Cairn India (61%), NMDC (46%),Hindalco (27%), Coal India (21%) and ONGC (18%)

Exhibit 59: … led to unprecedented revision in estimates inglobal cyclical since March 2014

FY16E revision (%)

15.4

FY16E growth rate (%)

11.5 17.0

Exhibit 58: Fall in global commodities …

105

95

85

75

65

55

74

64

CRB Commodity Index (USD)Rogers Intl. Comm. Index (USD)

‐12.1

‐20.7

Nifty ex RMs Global cyclicals

‐7.0

Nifty ex globalcyclicals

Source: MOSL, CompanySource: MOSL, Bloomberg

Exhibit 60: Earnings cut was led by Tata Steel (63% cut in PAT estimates), Cairn India (61%)and NMDC (46%)

FY16E revision (%)

‐27

‐46

‐63Tata Steel

‐61

Cairn India

‐21 ‐18

NMDC Hindalco Coal India ONGC

Note: Global cyclicals include Metals, Energy (ex RMs) and Coal India Source: MOSL, Company

#2 ‐ Delay in revival of the investment cycleManufacturing IIP has remained weak (average of 2.3% post 2014 genrealelections). However, IIP has shown resilience at ~4% since Jan‐15.Projects completed (as a % of projects under implementation) remains at lowlevels of 4.1%; this has impacted the virtuous cycle of cash flow generation inthe system.Project execution remains sluggish due to regulatory, financing and viabilityconstraints.This has led to steep cuts in our estimates for Cement and Capital Goods; ACCleads the pack with 49% cut in FY16 estimates, followed by Grasim (41%),Ultratech (33%), L&T (22%), BHEL (20%) and Ambuja (18%).

July 2015 28

India Strategy | Getting on track!

7/24/2015 India Strategy: Getting on track!– Detailed Report

http://www.motilaloswal.com/site/rreports/HTML/635721163512170886/index.htm 31/85

Exhibit 61: Manufacturing IIP remains at baseline levels (%YoY, 3mma)

Manufacturing IIP % YoY 3mma10

8

6

4

2

0

‐2

Manufacturing IIP averagepost Modi govt. is 2%

Exhibit 62: Weak execution results sub‐optimal number ofprojects completed (as % of projects under implementation)(ttm)

15.0%

12.0%

9.0%

6.0%

3.0%

Projects completed had consistently remainedat 7%+ of projects under implementation

Projects Completed ttm, as % of Prj under Impl

Execution impacted given regulatory,financing and viability constraints

Average 6.4%

Source: MOSL, Govt. Source: MOSL, CMIE

Exhibit 63: Slow domestic recovery and lower capacity utilization result in steep cuts inFY16 earnings

FY16E revision (%)

‐22

‐33‐41

‐49

ACC Grasim Inds UltratechCement

L&T

‐20 ‐18

BHEL Ambuja Cem

Source: MOSL, Company

#3 – Muted rural demand and growthMSP price increase was a mere 3% during FY16; this was post a new low of 2% inFY15.Rural wage growth has also moderated steeply from ~10% in FY14 to 6% in FY15Forecast of poor monsoons in 2015, following a deficit rain in 2014, also has animpact on rural demand.

Exhibit 65: … along with this, rural wage growth hasmoderated and is the lowest in almost a decade

Simple avg wage rate for all rural occupations (%)

NDA‐II Avg:2%

7

2 3 9 8

12

19

16

19

Exhibit 64: Second successive year of very low hike in MSP(%)…

UPA‐IAvg: 9%

10 NDA‐I6 6

2

27 UPA‐IIAvg: 12%

1916

12

7

18

86

8

4 3 3 10

6

Source: MOSL, Govt.

July 2015

Source: MOSL, Govt.

29

India Strategy | Getting on track!

Exhibit 66: FY15 Volumes estimate for 2Ws and Tractor has

7/24/2015 India Strategy: Getting on track!– Detailed Report

http://www.motilaloswal.com/site/rreports/HTML/635721163512170886/index.htm 32/85

seen downgrades…2Ws

2.1%

0.0% ‐4.0% ‐3.3%

TractorExhibit 67: …also reflecting in FY16 earnings revision

FY16E revision (%)

‐6.5%

‐11.0%

Sep‐14 Dec‐14 Mar‐15

Source: MOSL, SIAM, Company

‐28M&M

‐17‐15

Hero Moto Bajaj Auto

Source: MOSL, Company

Exhibit 68: HUVR volume growth has been sub‐5% in the past two years, with 30‐35%volumes from rural India

HUL Volume growth (%)13.0

9.3

6.8

3.34.8

4.04.8

8.0

Source: MOSL, Company

#4 ‐ Asset quality issues: Lower credit growth and asset quality leading tohuge cute in estimates

Credit growth stands at a four‐year low at 10% in FY15 v/s an average creditgrowth of ~15%.Weaker‐than‐expected domestic recovery leading to continued rise in stressloans for PSU banks.Slippages are likely to go up as the banks are likely to grapple with the norestructuring forbearance windowGNPA’s jumped from 2.2% of loan book in FY11 to 4.6% of the loan book inFY15. We expect GNPAs to up further in 1HFY16.

Exhibit 70: ... leading to downgrades in earnings estimatessince Mar‐14

FY16E revision (%)

Exhibit 69: Credit growth remains weak while GNPAs &restructured loans are near highs…

GNPA

21.519.6

Restructured Loans

17.0

6.2

3.0

17.5

7.1

4.9

System credit growth

8.4

10.0

4.5

8.8

9.7

15.9

7.3

3.9

14.0

7.2

3.8

13.9

7.5

4.44.12.2

3.5

3.0

‐21

4.6

‐41

BOI PNB

‐18

BOB

Source: MOSL, Company

30

Source: MOSL; Company

July 2015

India Strategy | Getting on track!

#5 – Tech: Adverse cross currencies and weak global demand restricts PAT

7/24/2015 India Strategy: Getting on track!– Detailed Report

http://www.motilaloswal.com/site/rreports/HTML/635721163512170886/index.htm 33/85

growthMajor global currencies like EUR, GBP, JPY and AUD have all depreciated 8‐18%since 1QFY15; however, INR has depreciated by only ~5% . This impacted USDrevenues of companies cutting revenue estimates by 400‐600bp in FY15/16across top‐tier IT companiesWeakness in specific segments in global markets has led many IT companies toguide for muted growth. This follows a disappointing growth in 4QFY15.Contribution of Technology to overall PAT seems to have peaked at 14.3% inFY15. We estimate PAT growth of only 9% in FY16, lowest ever for the sector.

Exhibit 71: Major global currencies depreciated 10‐18% v/s USD since 1QFY15 (%) …

18.6% 18.3%17.3%

8.1%

5.4%

EUR GDP AUD JPY INR

Source: MOSL, Bloomberg

Exhibit 72: … resulting in PAT growth to come down to 9%

45

28

47 Technology PAT growth (%)

23% CAGR PAT 3227growth

1916 18 17 15

Exhibit 73: Technology contribution may have peaked at14.2% in FY15

Technology PAT as % of MOSL PAT universe

10.4

7.9 7.46.7 7.4

8.3 8.5 8.4 8.4

12.914.3

13.2 12.4

1116

9

Source: MOSL, Company Source: MOSL, Company