Embed Size (px)

Citation preview

Indian Advance Pricing Agreement Regime The Game Changer2012

Disclaimer:The information contained in this document has been compiled or arrived at from discussions with various stakeholders, industry experts and other sources believed to be reliable, but no representation or warranty is made to its accuracy, completeness or correctness. The information contained in this document is published for the knowledge of the recipient but is not to be relied upon as authoritative or taken in substitution for the exercise of judgment by any recipient. This document is not intended to be a substitute for professional, technical or legal advice or opinion and the contents in this document are subject to change without notice. Whilst due care has been taken in the preparation of this report and information contained herein, Grant Thornton does not take ownership of or endorse any findings or personal views expressed herein or accept any liability whatsoever, for any direct or consequential loss howsoever arising from any use of this document or its contents or otherwise arising in connection herewith

Contents

1 Foreword

3 Introduction

2 Backdrop

4 APA Framework and Rules in India

5 Types of APAs

6 Practical Considerations for Implementing an APA

7 APA Process

8 Critical Analysis of an APA

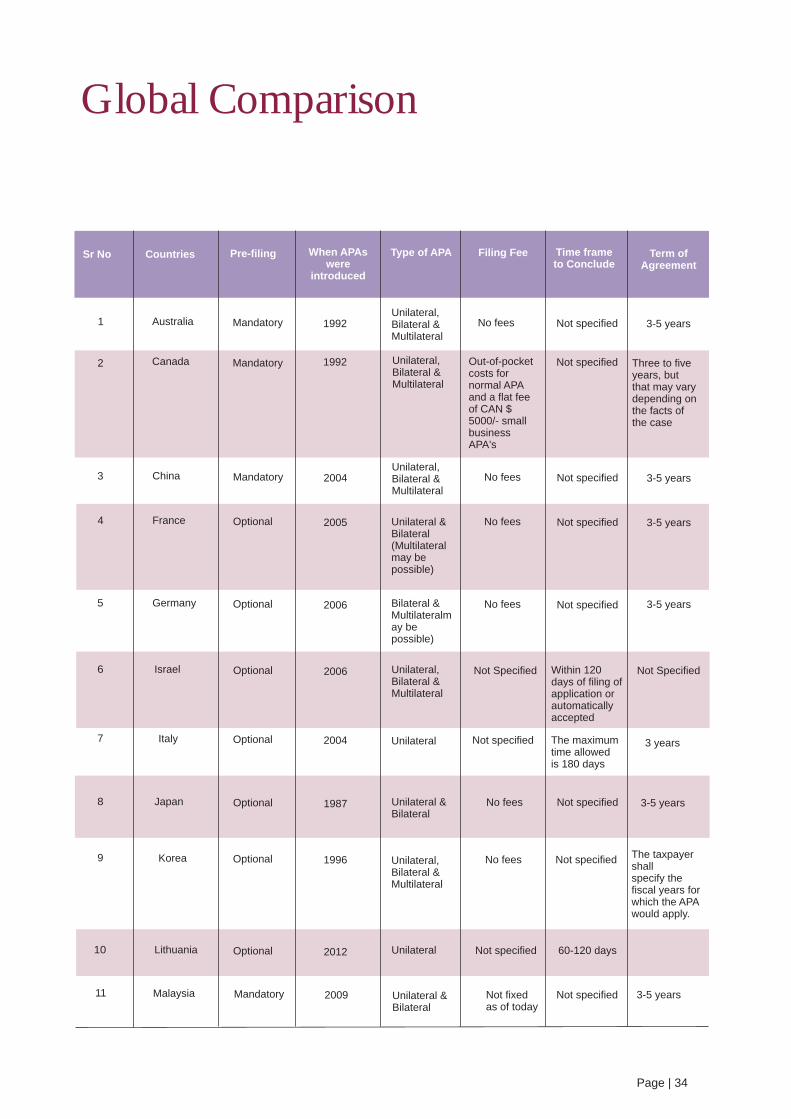

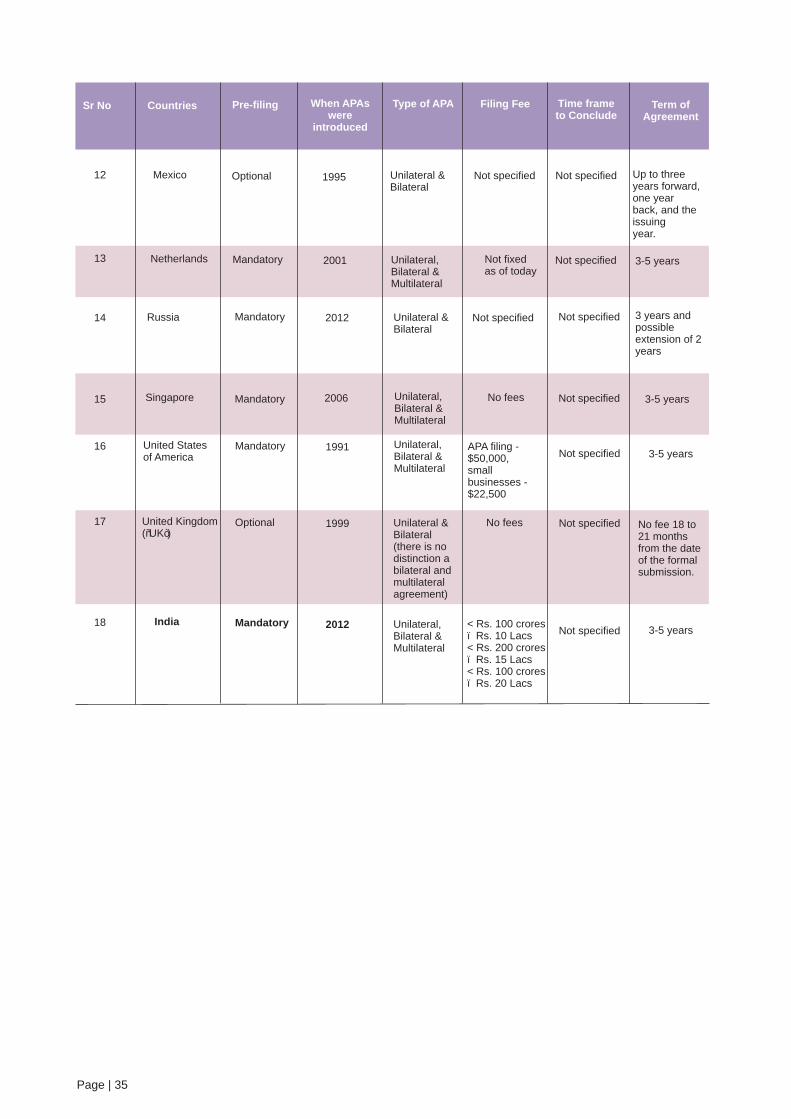

9 Global Comparison

10 Our Expert Advisors

11 Abbreviations

12 Annexures- Rules & Forms

Foreword

Karishma R Phatarphekar

Partner & Practice LeaderTransfer Pricing ServiceGrant Thornton India LLP

The introduction of Indian APA Rules is a silver lining to the aggressive transfer pricing audit regime in India and may indeed be the game changer in the Indian transfer pricing landscape. It aims to reduce a lot of litigation time and cost of the taxpayer and tax authorities if adopted in the right spirit. I believe that the APA regime should stand the test of time since the APA authorities has been assertive on implementing this in a fair, pragmatic and positive manner.

Page | 1

Advance Pricing Agreement (“APA”) was showcased as a part of the proposed Direct Taxes Code

(“DTC”) way back in 2009 and was again mentioned in the DTC 2010. However, with the uncertainty

surrounding the introduction of DTC, APA introduction also got deferred. For a highly litigious transfer

pricing regime of India, this uncertainty regarding the fate of APA raised a lot of concern amongst large

taxpayers. In a much appreciated move, the Ministry of Finance introduced the APAs in the Finance Act

2012.

The APA program finally became a reality in India. The APA rules have heralded the beginning of the

much awaited dispute avoidance mechanism in the Indian transfer pricing environment. Given the recent

Indian transfer pricing audit scenario, the introduction of APAs is a much needed regime against the

aggressive industry wide positions adopted by the tax authorities.

The Indian APA Rules are indeed at par with the Global APA Rules. The rules fairly touch upon most of

the issues that warrant consideration in an APA regime. It is indeed heartening to note that bi-lateral and

multi-lateral agreements are provided for. Pre-filing consultations have been provided for and are

mandatory in nature. I believe that the pre-filing consultations will help the APA authorities to gauge the

basic issues involved, time frame needed to conclude the APA, the kind of expert APA team (experts in

economic, statistics, law etc) required for concluding the APA, any additional information required etc.

With all such per hand information with the APA authorities, we expect the APA process to be smooth

and not very time consuming.

To screen out the non so serious players a graded fee depending on the value of the international transaction has been prescribed. The process and application has been clearly laid out and also allows for onsite visits by the tax authorities to the business premises of the taxpayer to get a better practical insight into the function asset and risk analysis. The rules also provide for option of renewal, amendment and withdrawal. Though roll backs are not explicitly enabled once the APA is concluded it will definitely have a precedence value in case of pending litigation.

APA Backdrop

Transfer pricing, in simple parlance, is an art of pricing (i.e. arm’s length price) cross-border transactions

entered into between two or more companies of the same multinational group (referred to as related

parties/associated enterprises). Since its inception, transfer pricing has emerged as the biggest area of tax

dispute for Multinational Corporations (“MNCs”). Therefore, it is important to understand and acknowledge

that the practice of transfer pricing has direct and significant impact on the tax revenue of a country.

For the revenue authorities around the world, transfer pricing is considered as a very important issue which

requires detailed examination, documentation requirements and thorough understanding of tax rules

prevailing in different countries and international organisations like OECD. The Indian scenario of transfer

pricing is also not much different. The transfer pricing adjustments in the recent sixth audit cycle in India

alone amounted to INR 44,000 crore (approximately USD 9.78 billion) which is more than the aggregate

income adjustments by tax authorities in audits of previous four years.

India has the highest number of litigations over transfer pricing, where MNCs have been charged of reducing

their tax liability by transferring profits to group companies abroad.

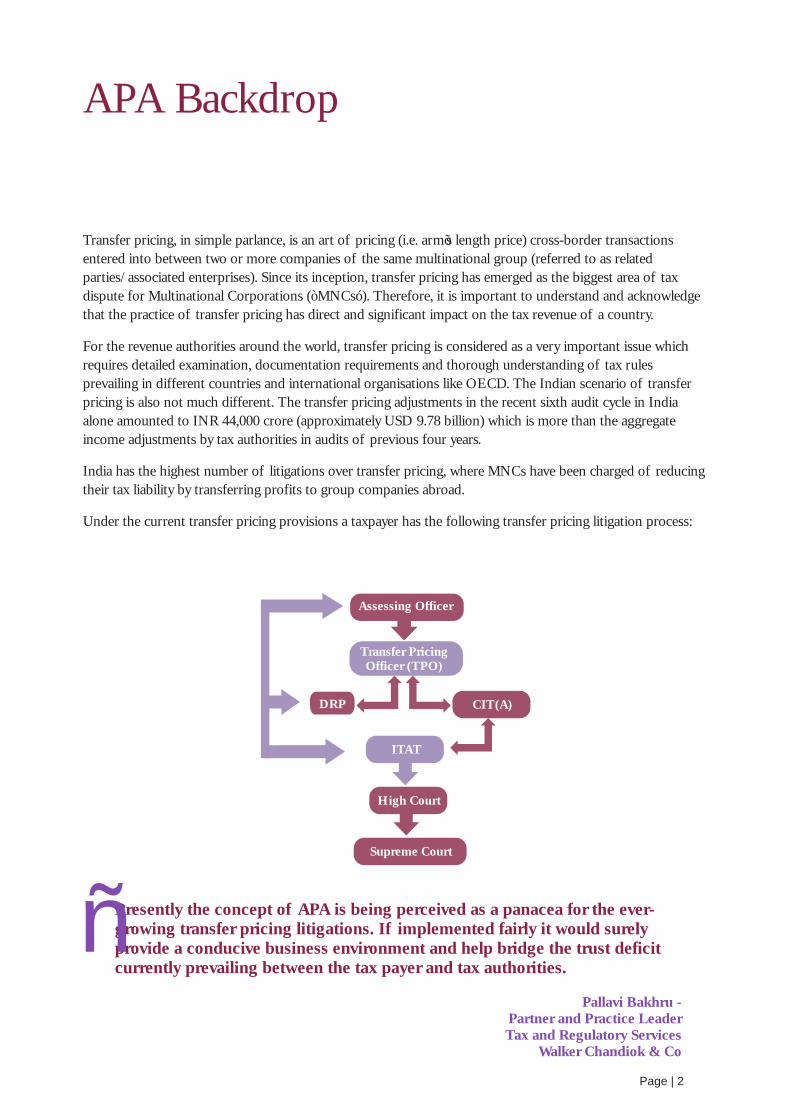

Under the current transfer pricing provisions a taxpayer has the following transfer pricing litigation process:

DRP

Transfer Pricing Officer (TPO)

Assessing Officer

CIT(A)

ITAT

High Court

Supreme Court

Presently the concept of APA is being perceived as a panacea for the ever-growing transfer pricing litigations. If implemented fairly it would surely provide a conducive business environment and help bridge the trust deficit currently prevailing between the tax payer and tax authorities.

Pallavi Bakhru - Partner and Practice Leader Tax and Regulatory Services

Walker Chandiok & Co

“

Page | 2

Additionally, in order to avoid double taxation, Mutual Agreement Procedure (“MAP”) is proved to be an

effective method where the Revenue Authorities of two separate nations together try to resolve a dispute.

Under MAP an agreement would be reached between the tax authorities that reduce double taxation or

conflicting taxation. Here disputes are resolved through Competent Authorities (“CA”) of contracting state.

MAP is an important argument decree mechanism that exists regardless of remedies offered in domestic tax

laws. Though there are number of inherent advantages under MAP but it is just an optional method in India

and often argued as a lengthy procedure which on an average takes 2-3 years to resolve disputes. Again MAP

is a mechanism available subsequent to audits and transfer pricing TP adjustments when compared to an APA,

which is more progressive and proactive.

To overcome all these bottlenecks of transfer pricing audits, APA and its provisions in India is a positive

development and welcome move by the government.

As per the Indian APA Rules, the regular audit of the covered transactions under the APA shall not be

undertaken by the TPO once an APA is concluded. TPO having the jurisdiction over the assessee shall carry

out the compliance audit of the agreement for each of the year covered in the agreement. The TPO shall

submit the compliance audit report, for each year covered in the agreement, to the Director General of

Income Tax (“DGIT”) (International Taxation) in case of unilateral agreement and to the competent

authority in India, in case of bilateral or multilateral agreement, mentioning therein his findings as regards

compliance by the assesseeassesse with terms of the agreement.

Against such backdrop, APAs have globally served as an effective mechanism to address transfer pricing issues

all over the world. Many countries have implemented APAs in order to provide certainty to taxpayers, thereby

reducing transfer pricing audits and litigation. This paper is in support of the introduction of the APA Rules

by the Government of India.

Accordingly, we believe that this paper will provide useful and practical insights and prove helpful for the

taxpayers to understand the APA regime and if it is appropriate for them to consider it for their related party

transactions.

Page | 3

Introduction

As per the Indian Rules, APA is an agreement between the Central Board of Direct Taxes and any person, which determines, in advance, the arm’s length price or specifies the manner of the determination of arm’s length price (or both), in relation to an international transaction.

What is an APA

Once an APA has been entered into with respect to an international transaction, the arm’s length price with respect to that international transaction, for the period specified in the APA, will be determined only in accordance with the APA.

An (APA) (or “arrangements”) as referred to by the OECD in its 2010 transfer pricing guidelines is –

“An arrangement that determines, in advance of controlled transactions, an appropriate set of criteria for the determination of the transfer pricing for those transactions over a fixed period of time”.

The Internal Revenue Service (“IRS”) defines an APA as: “An APA is an agreement between a taxpayer and the Service in which the parties set forth, in advance of controlled transactions, the best Transfer Pricing Method (“TPM”) within the meaning of Sec. 482 of the Code and the regulations. The agreement specifies the controlled transactions or transfers (covered transactions), TPM, APA term, operational and compliance provisions, appropriate adjustments, critical assumptions regarding future events, required APA records, and annual reporting responsibilities.”

The IRS which has collectively more APA experience than any other taxing authority further describes the APA Programme as:

“The Advance Pricing Agreement (APA) Program is designed to resolve actual or potential transfer pricing

disputes in a principled, cooperative manner, as an alternative to the traditional adversarial process. An APA is

a binding contract between the IRS and a taxpayer by which the IRS agrees not to seek a transfer pricing

adjustment for a covered transaction if the taxpayer files its tax return for a covered year consistent with the

agreed transfer pricing method.”

The inherent idea of an APA is to increase the efficiency of tax administration by encouraging taxpayers to

present before the tax authorities all the facts relevant to a proper transfer pricing analysis and to work

towards a mutual agreement. APA reduces the burden of compliance by giving taxpayers greater certainty

regarding their transfer pricing methods, promoting their issues and by allowing them for discussion and

resolution in advance before the tax authorities.

Creativity and flexibility often are important to reach an agreement. The regulations which vary in different

countries often do not provide clear guidance for special circumstances and under the best method rule one

should require special provisions if needed to reach a fair and reliable result. Further, often two or more

approaches to certain issues are possible, and there is no clear basis for preferring one approach over another.In this case, the tax authorities can give the taxpayer its preferred treatment of some issues in return for

getting its own preferred treatment of other issues. Also, in this case the tax authorities might (in the interest

of efficient tax administration) works with a reasonable approach proposed by the taxpayer rather than

independently develop another approach that might be equally reasonable.

Page | 4

Characteristics of an APA

An APA normally requires agreement on these major items:

choosing a transfer pricing method

selecting comparable uncontrolled companies or transactions (comparables)

deciding on the years over which comparables’ results are analyzed (the “analysis window”) and related matters;

adjusting the comparables’ results because of differences with the tested party; constructing a range ofarm’s length results

critical assumptions

testing results during the APA period and consequences of being outside the arm’s length range.

Scope and objective of an APA

APA can be applied for various international transactions, like purchase or sale of raw materials, finished

goods, providing services, financing arrangements, transfer and use of tangible/intangible assets, etc.

However, considering the time and resources required for concluding an APA, it is generally preferred to enter

into an APA in respect of complex/high value transactions. Certain jurisdictions also exclude routine

transactions from the scope of the APA.

Also, applying for an APA for transactions is generally left to the discretion of the taxpayer. Though it is not

the statutory obligation for a taxpayer to cover all the related party or inter-company transaction in an APA,

however, considering the scope of APA it is generally recommended to disclose all the inter-company

transactions proposed to be entered into by the taxpayer to the relevant tax authorities so that both the parties

may discuss and come to a consensus to include such transactions. This is more due to the fact that the APA

proposals are independent in nature and binding only on the person in whose case the agreement has been

entered into and only in respect of the transaction in relation to which the agreement has been entered into.

The scope of an APA also states the time period for which the APA shall remain in force. Generally an APA

is entered into for duration of three to five years and may be renewed/re-negotiated upon completion of the

originally agreed term. Under the Indian APA Rules, the APA term could be up to a period of five years with

an option for renewal.

At this point it is important to mention that since APA is a type of agreement between the taxpayer and the

tax authorities with a futuristic point of view i.e., it is to be applied for controlled transactions over a future

period of time, however, the negotiated position under an executed APA can be applied to prior years which

are not covered by the terms of an APA. This is known as roll-back of an APA. The Indian APA Rules do not

enable roll back of APAs.

Since the rules are issued the APA authorities have been discussing this in general with the taxpayers

and may consider issuing a guidance paper in the form of FAQ’s shortly.

Page | 5

Hence, an APA is an agreement that sets transfer price of the covered transactions prospectively between the

taxpayer and tax authorities. APA process follows a consultative and collaborative approach between the

taxpayer and the tax authorities. The taxpayer and tax authority also mutually agree on the transfer pricing

method to be applied and its application for a certain period of time.

APA programs are designed so taxpayers can willingly determine real or possible transfer pricing disputes in

an honourable, supportive manner, against the traditional audit process. APAs have been introduced with an

objective of lessening the burden of compliance by giving taxpayers greater certainty regarding their transfer

pricing approaches. Further, the tax outcomes of the international transactions are also brought out, hence,

giving an effective tool for management of the tax risks for both the taxpayer and the tax authorities.

Given the above, we hope that the advent of the APA rules bring a level of certainty on basic transfer pricing

disputes on issues such as use of data not available in the public domain, selection of comparables and non-

contemporaneous data. Further, we hope that APAs will also be useful for highly litigious issues such as

valuation of shares, corporate guarantees, inter-corporate loans, royalty, intangibles, etc, on which at present

there is no statutory guidance.

27

who wish to have tax and financial reporting certainty and elimination of double taxation who have complex transactions where differing views are likely to arise in respect of transfer pricing who wish to avoid the possibility of dedicating significant resources to an extensive transfer pricing

audit

The ensuing chapters provide a holistic understanding of APA’s which includes:

The APA scheme is ideal for taxpayers:

APA Rules could be the game changer in the decade long Indian transfer pricing regulations. It is definitely an opportune time for the taxpayer to discuss and evaluate whether APA is suitable for its business.

APA framework and rules in India types of APAs practical considerations for implementing an APA critical analysis of an APA APA Process when is the right time to consider APA; and a comparative overview of APA regimes in major jurisdictions where an APA scheme exists

Page | 6

The objective of pre-filing consultation is to enable amongst other things, both parties to:

Timeframe to conclude an APA, broadly can also be mutually agreed upon during the pre-filing

consultation.

Types of APAs available: The APA Scheme has enabled companies to not only opt for Unilateral APA, but

also for Bilateral and Multilateral APAs. However, in case of a unilateral APA, the APA rules require the

taxpayers to explicitly mention in the application the reasons for entering into a unilateral APA instead of a

bilateral or a multilateral agreement. Bilateral and multilateral APAs would be routed through the Competent

Authority (“CA”) and it is imperative that the Associated Enterprises (“AE”) have initiated APA in their own

country.

determine the scope of the agreement

identify transfer pricing issues

determine the suitability of international transaction for the agreement

discuss broad terms of the agreement

APA Framework and Rules in India

While the Finance Act had put the bare-shell structure of the APA regime in place, the detailed rules were

awaited. The much awaited APA scheme has been finally notified by the government by amending the

Income-tax Rules, 1962 (‘Principal Rules’) and inserting Rules 10F to 10T and 44GA in the Principal Rules.

(The relevant legislation and the detailed APA Rules in this regard have been enclosed as Annexure I to this

report)

The key characteristic features of APA as proposed in India are as under:

Applicability: The APA Rules are applicable to all “persons” undertaking international transactions or

contemplating to undertake international transactions.

Threshold: No threshold limit has been prescribed in the APA Rules. All the taxpayers entering or

proposing to enter into an international transaction have an option to enter into an APA.

Pre Filing Consultation: This is a mandatory requirement in the process and not an option provided to the

taxpayer. Additionally it involves a mandate of providing a lot of detailed information, with an option to keep

the name of the taxpayer and its related entities ‘anonymous’. Taxpayers/ representatives can request for a

pre-filing consultation with the DGIT. While the pre-filing consultation is neither binding on the Board nor

the taxpayer to enter into an APA.

APA team: As rolled out by the APA Rules, the APA team in India would comprise of not only the

designated income-tax officers under this regime but also include experts in economic, statistics, law or any

other field as may be nominated by the DGIT. This is a positive and welcome step taken by the revenue to

deal with the complex transfer pricing issues being faced globally which require an overall insight into the

global business practices.

Page | 7

Discussion

Discussion

Agreement

Unilateral

Bilate

ral/

Mul

tiiate

ral

Agreement

Outside IndiaIndia

Tax authorities including experts from economics, statistics, law etc.

Board Approval

DG InternationalTaxation

CompetentAuthority

APA Team (APA directorand APA officers)

Taxpayer

Competent Authority

Associated Enterprise(AE)

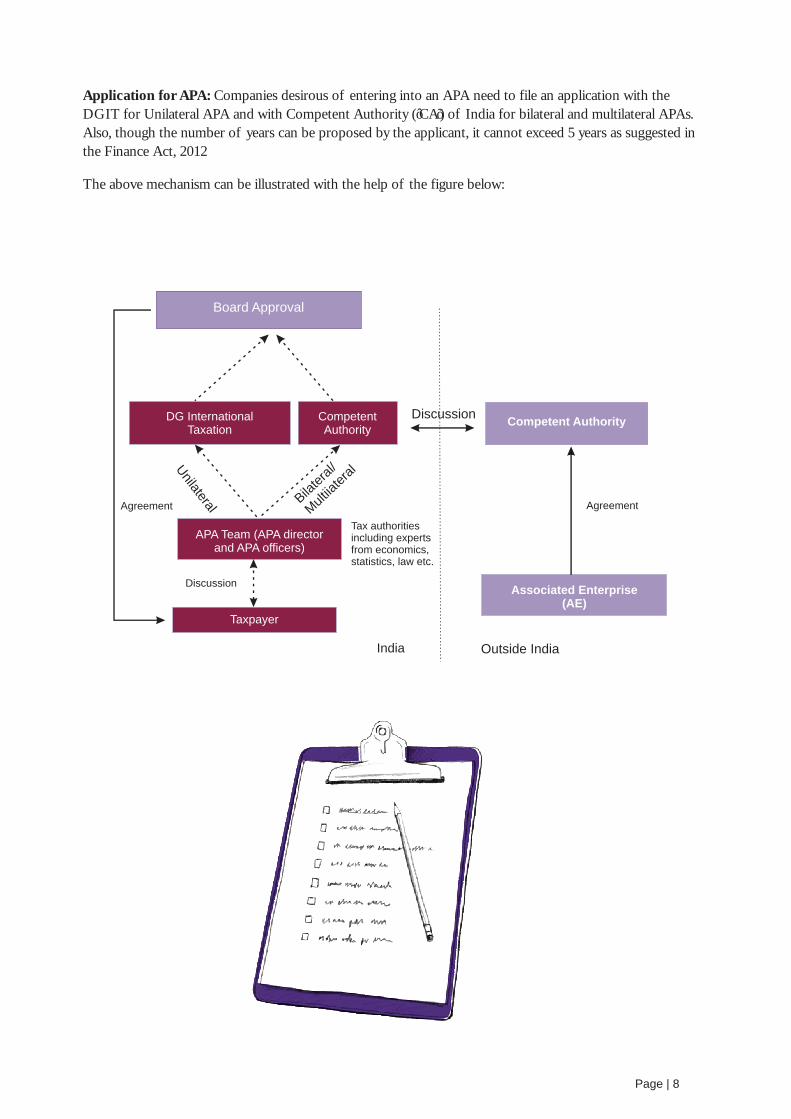

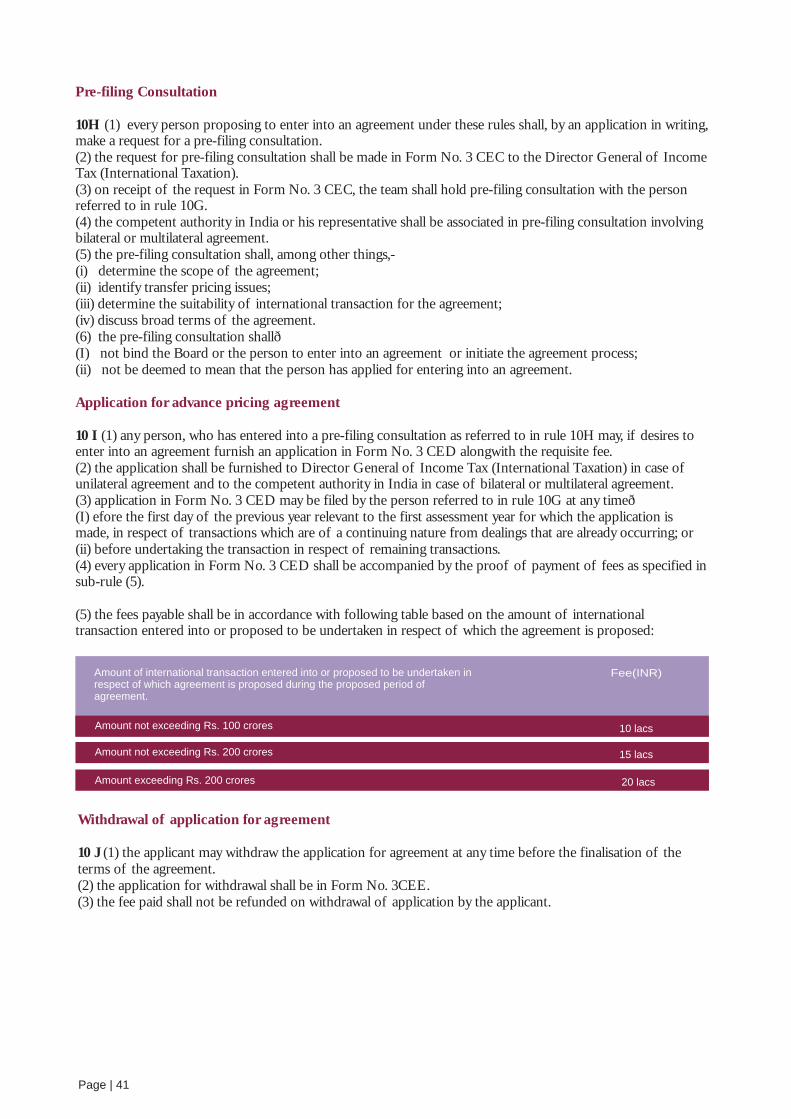

Application for APA: Companies desirous of entering into an APA need to file an application with the

DGIT for Unilateral APA and with Competent Authority (‘CA’) of India for bilateral and multilateral APAs.

Also, though the number of years can be proposed by the applicant, it cannot exceed 5 years as suggested in

the Finance Act, 2012

The above mechanism can be illustrated with the help of the figure below:

Page | 8

Fee payable: In order, to screen out the non serious players a graded fee from INR 1 million to 2 million depending on the value of the international transaction has been prescribed. The prescribed application filing fee thresholds are as follows:

Amount of international transaction entered into or proposed to be undertaken in respect of which APA is proposed

Fee (USD)

Transaction amount INR 1000 mn (USD 20mn)

20,000

Transaction amount between INR 1000 & INR 2000 mn (USA 20mn TO USD 40mn)

30,000

Transaction amount exceeding INR 200 mn (USD 40mn)

0.04

Timing of application: Applicants desirous of entering into an APA are required to file their applications

within the following timelines:

holding meetings with applicant

calling for additional documents/ information/material from the applicant

visiting applicant’s business premises

making inquiries as may deems fit in the circumstances of the case

in case of continuing / existing transactions since the application is to be filed before the first day of the

relevant previous year, the first year for which a taxpayer may be able to apply for an APA would be FY

2013-14in case of remaining transactions (i.e. new or proposed) any time before undertaking the transactions

If the application is allowed in the preliminary processing phase, the main processing of applications would be

conducted by the APA team in the following manner:

Procedure: Prior to the main processing of the application there is step of preliminary processing of

application which includes vetting the application for any deficiencies (defect in application, relevant

document not attached or application not in accordance with understanding reached in the pre-filing

consultation).

In case there is any defect in the proposed application, the DGIT or CA would require the taxpayer to remove

such deficiency within stipulated time, barring which the application would be rejected and correspondingly

the fee received would also be refunded.

1 USD has been converted at 54 INR

Fee (INR million)

1

1.5

40,000

Tax authorities visit to business premise needs to be looked at positively, as this will help gain full business understanding on a practical basis and ensure effective resolution – this has been a global experience.

Page | 9

In case of a bilateral or multilateral APA, the applicant shall not be entitled to be part of the discussion

between the competent authority of India and the competent authority of the other country/ countries. Also

the applicant shall convey acceptance or otherwise of the agreement within 30 days of it being

communicated. If the agreement is not acceptable the applicant could continue with the unilateral option or

withdraw the application.

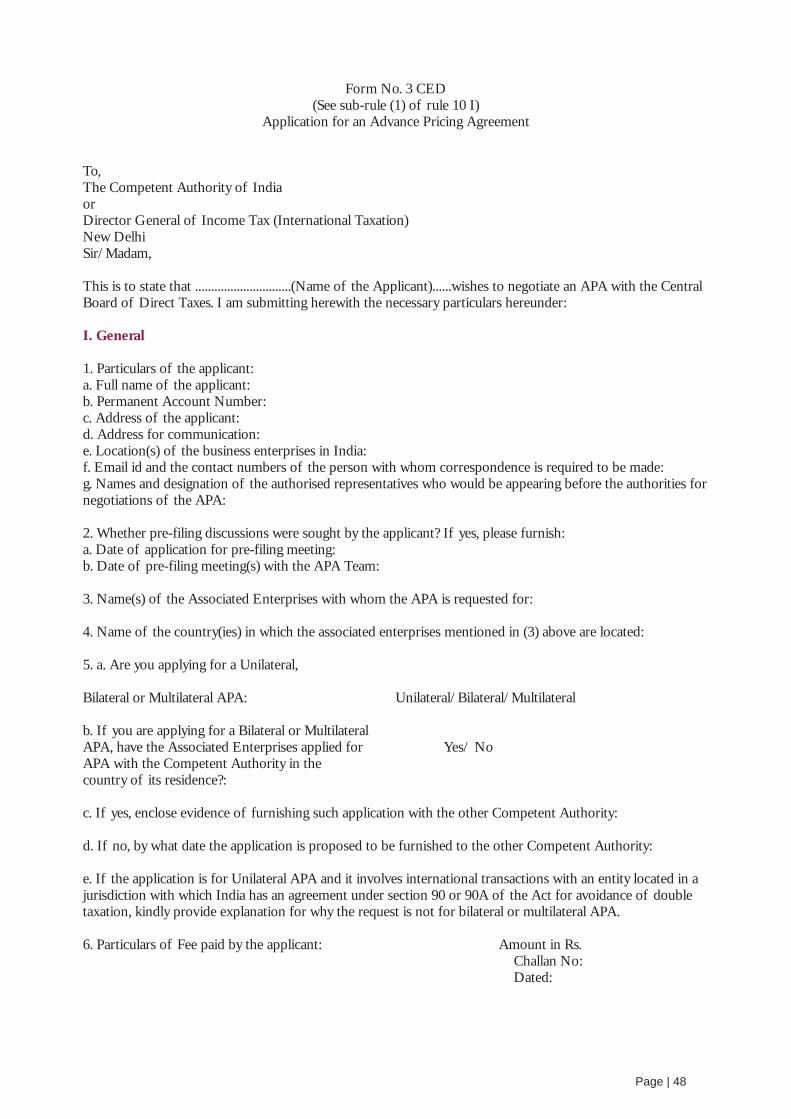

Particulars Form No.

Application for a pre-filing meeting

Application for an APA

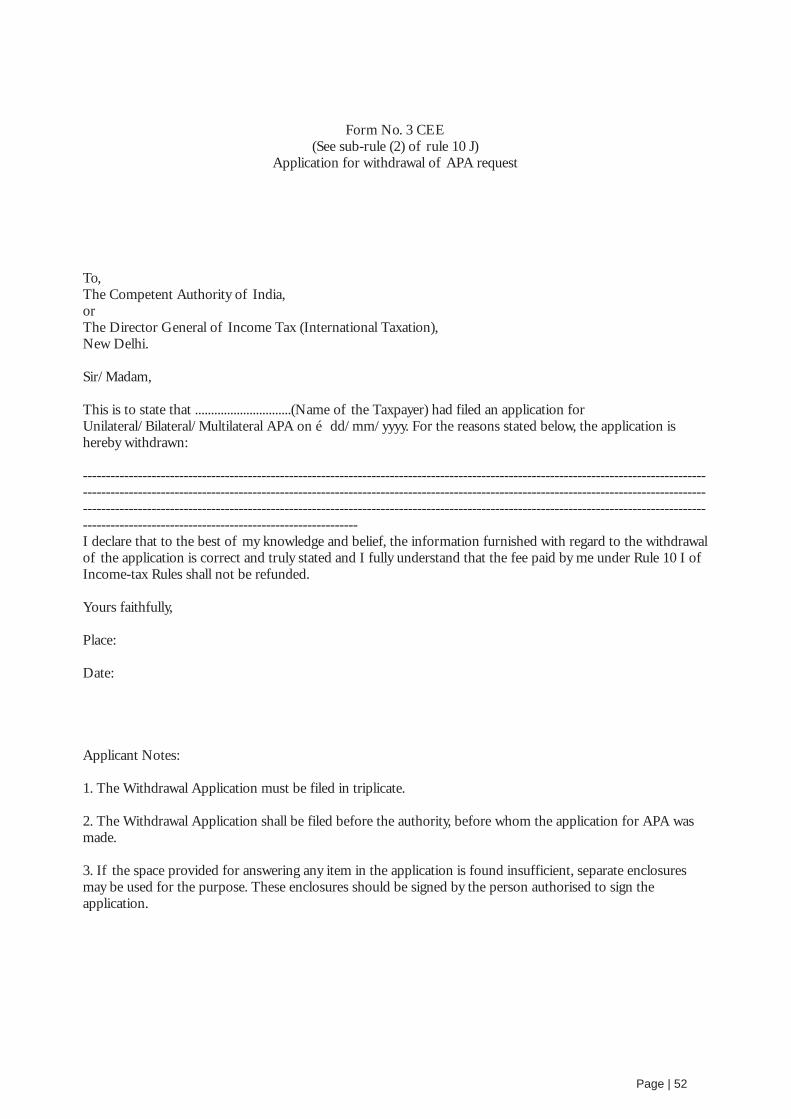

Application for withdrawal of APA request

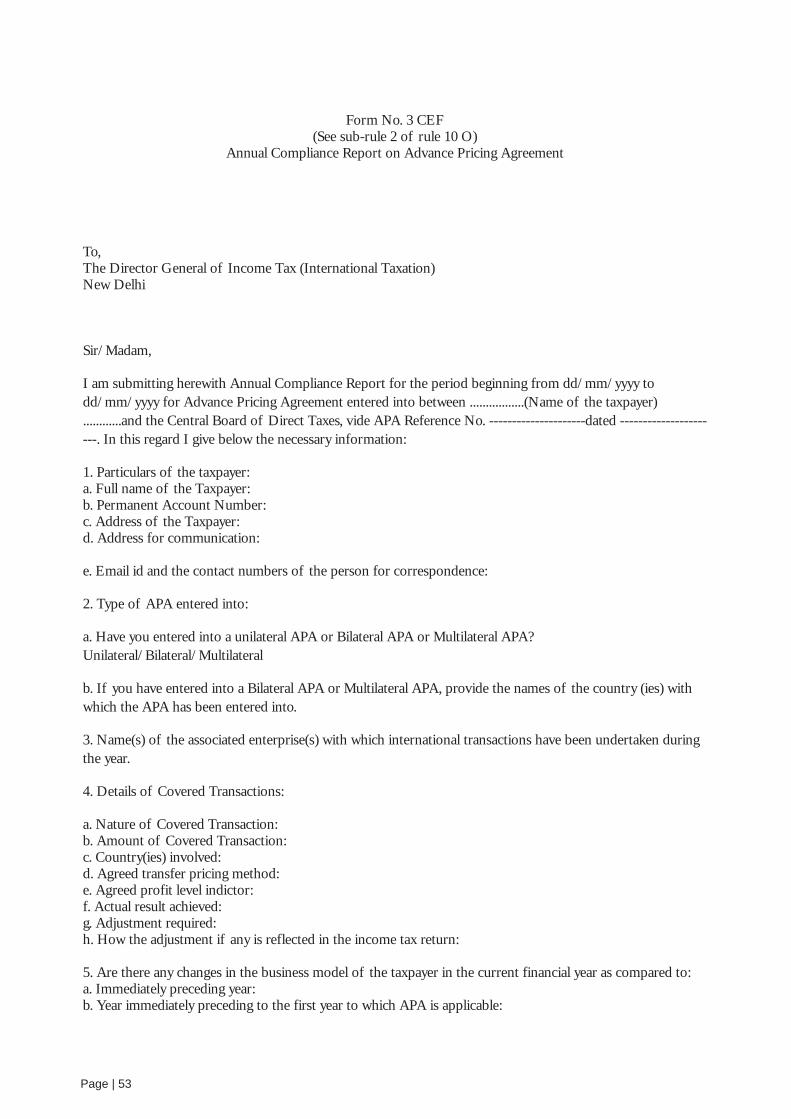

Annual Compliance Report on APA

3CEC

3CED

3CEE

3CEF

The prescribed forms in this regard have been enclosed as Annexure II to this report.

international transactions coveredagreed transfer pricing methodology, if anydetermination of arm’s length price, if anydefinition of relevant termscritical assumptions time period of APAother conditions, if any, not covered in the Income Tax Act or in the Income Tax Rules

change in lawchanges in critical assumptions or failure to meet conditions by the applicant or by the Board

furnished in quadruplicate to DGIT for each of the years covered in the agreement. One copy each would be sent by the DGIT to the CA India, to the Commissioner of Income Tax who has the jurisdiction over the income-tax assessment of the taxpayer and one copy to the TPO having the jurisdiction over the taxpayer.filed within thirty days of the due date of filing the income tax return for that year, or within ninety days of entering into an agreement, whichever is later.

Withdrawal: Applicants can withdraw their applications any time before the finalisation of the terms of the

APA. However, the fee which has been paid would not be refunded if the APA is withdrawn at the discretion

of the applicant himself.

Forms prescribed: The following forms are prescribed for the APA Scheme:

Page | 10

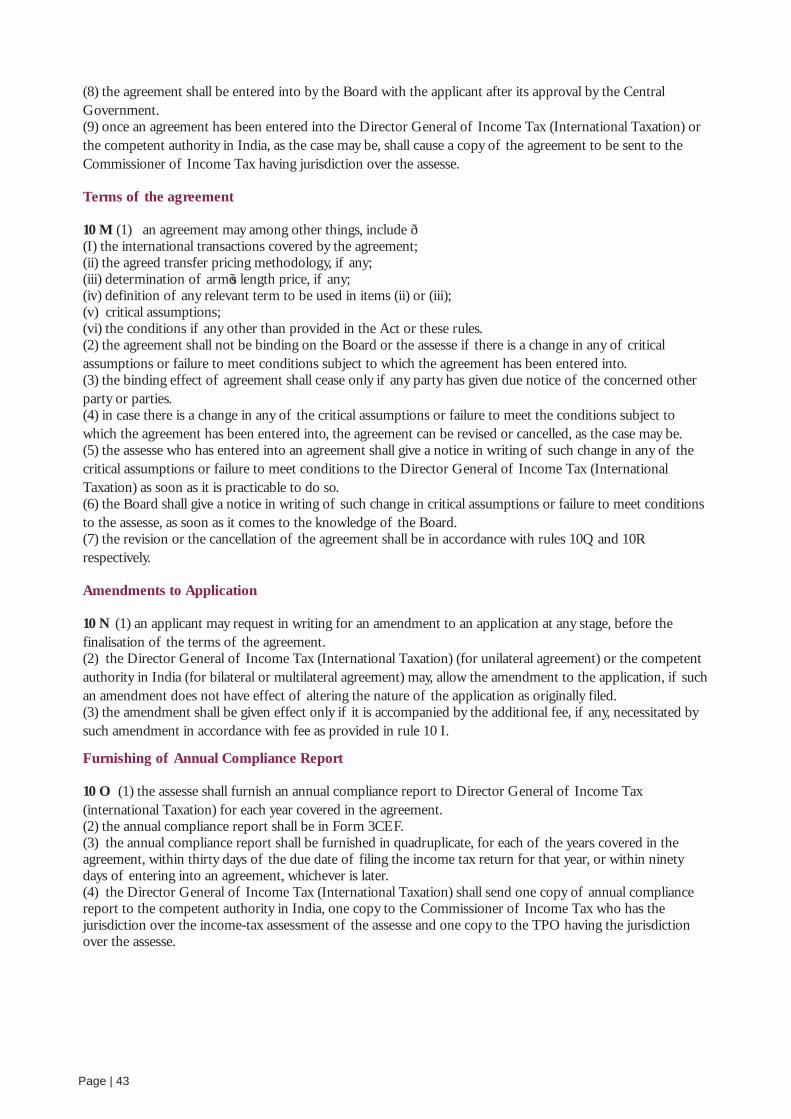

APA, agreement and terms: The APA would be entered into by the Board and the taxpayer after getting

approval from the Central Government. An APA would cover the following points:

Critical assumptions: Means critical and significant factors and assumptions that if changed would annul

the APA. This is the most crucial aspect in an APA and needs to be carefully agreed and drafted.

Binding effect of APA: APA would not be binding in case of any changes in critical assumptions or failure

in meeting conditions set under APA. Also, the binding effect of APA would cease in the following cases:

Annual Compliance Report: An annual compliance report has to be:

Amendments to Application: The APA scheme provides for the amendment of the application by the

taxpayer at any time before the finalization of the agreement, in case allowed by the DGIT / CA on account

of non-changing of material facts and payment of additional fees if required.

Revision of APA: An APA can be revised under any of the following circumstances:

Cancellation of APA: An APA can be cancelled in case of the following:

Renewal of APA: The renewal of APA is permitted under the new APA rules requiring all other listed

processes of fees, application, etc. other the pre-filing consultation required in case of the original filing.

change in critical underlying assumptionschange in such law other than that which renders it non-bindingrequest from CA in the other country

The revision order is required to be in writing citing reasons of revision required and the following

additional noteworthy features:

revisions can be initiated by the Board / DGIT/ CA/ taxpayeropportunity of being heard to be providednon-agreement by the taxpayer on the proposed revisions may result in cancellation of the APA

negative findings of the compliance audit by the TPOfailure in timely filing of annual compliance report or filing with material errors non-agreement by the taxpayer on the proposed revisions may result in cancellation of the APAon account of fraud or misrepresentation of facts

The order of cancellation is required to have the following essential features:

in writing with reasonsopportunity of being heard to be providedformal communication to the concerned Assessing Officer and the TPO

The rules do mention that the annual compliance audit is not meant to be a regular TP audit

Compliance Audit of the APA: The TPO having jurisdiction over the applicant is authorized to carry out

the compliance audit of the APA for each of the year covered in the agreement and is required to furnish his

report within six months from the end of the month in which the annual compliance report is received by

him. It is provided that such covered transactions under the APA scheme would not be audited by the TPOs

under the routine transfer pricing assessment procedure.

The compliance audit under the APA scheme is not a general feature seen globally and should be restricted to

purely a monitoring procedure than a verification audit procedure.

Page | 11

Certain aspects not covered under the regime: While the overall regime adapts most of the global best

practices, the following are concerns are expressed by tax payers:

Rollbacks not explicitly enabled: Roll back of APA is also a concept which is in application in most of the

jurisdictions. It refers to the use of the methodology agreed in the APA in the years where audit for prior

years are open. Methodology agreed in the APA can be used as guidance in the open years. By providing that

APAs for on-going transactions need to be filed in advance of relevant previous years, it is implied that there

are no roll backs provided in the scheme. In India although roll back of APA is not formally enabled, we

understand that if facts are similar it may have persuasive value in courts.

No time frame to conclude: Although no time lines have been clearly given in the APA Rules, a time-line

should also be proposed internally for completion of an APA to be effective for the taxpayer. We understand

that during the pre-filing consultations this is one aspect the applicant can gain mutual understanding with the

team. Of course in case of bilateral or multilateral APAs it is not in the complete control of the Indian CA &

APA team.

Lack of firewall provisions to protect taxpayer information: Confidentiality of the tax-payers information

is also a critical issue. The information shared by a tax-payer while negotiating an APA may contain the group

policy, pricing policy, future business predictions, revenue model which are of strategic importance to the

MNE group. The income tax act does protect taxpayer information from being shared in the public domain.

However, if an APA is not concluded then whether the information would be shared with the regular audit

team is a concern to be addressed.

We understand that details sought in an APA application are anyway called for during documentation

compliance or transfer pricing audits. If there is something non-routine and confidential taxpayers can

discuss this during the PFC and obtain some comfort.

I expect the Tax Authorities to adopt a realistic, business minded approach and arrive at an optimum Advance Pricing Agreement (APA) in reasonable time -an approach where more and more companies will be encouraged to enter into APA and pay predictable taxes. This will definitely lead to higher economic activity in the country, generating more employment and wealth, and thus boost the overall tax revenue.

M K NarayanaswamySenior Director – Accounting and Taxation,

Sanofi India Limited

“

Page | 12

Types of APA

Some countries allow for only unilateral APAs while some others allow for bilateral and multilateral APAs.

Taxpayers generally wish to enter into bilateral or multilateral APAs to ensure avoidance of double taxation.

Indian APA rules cover all three types of APA’s i.e. unilateral APA, bilateral APA and multilateral APA. This

chapter aims to give a brief analytical heads up on the types of APAs.

Unilateral APAs

The arrangement solely between a taxpayer and a home country tax administration is referred to as

“unilateral APA”. The Indian APA Rules define uUnilateral APAs as agreement between the Board and the

applicant which is neither a bilateral nor multilateral agreement.

A unilateral APA is an one sided APA i.e the pricing is agreed with tax administration of home country while

in the related parties jurisdiction, the related party will still have to undergo the routine litigation process. If

associated enterprises (“AE”) jurisdiction raises a transfer pricing adjustment with respect to a transaction or

issue covered by the unilateral APA, then the unilateral APA can be treated as the taxpayer’s filing and

therefore eligible for MAP and adjustable, as opposed to an irreversible settlement.

Considering the above, it is evident that the unilateral APAs do not reliably eliminate double taxation issue or

might even create taxation gaps and therefore are less preferred by the taxpayers. The below figure

encapsulates the unilateral APA process.

Types of APAS

Unilateral APAs

Multilateral APAs

Bilateral APAs

Solely between a taxpayer and a tax authority

single mutual agreement between the CA of

tax administrations and taxpayers

More than one bilateral mutual agreement

Page | 13

Board Apporval

DG International Taxation

APA Team

Tax Payer

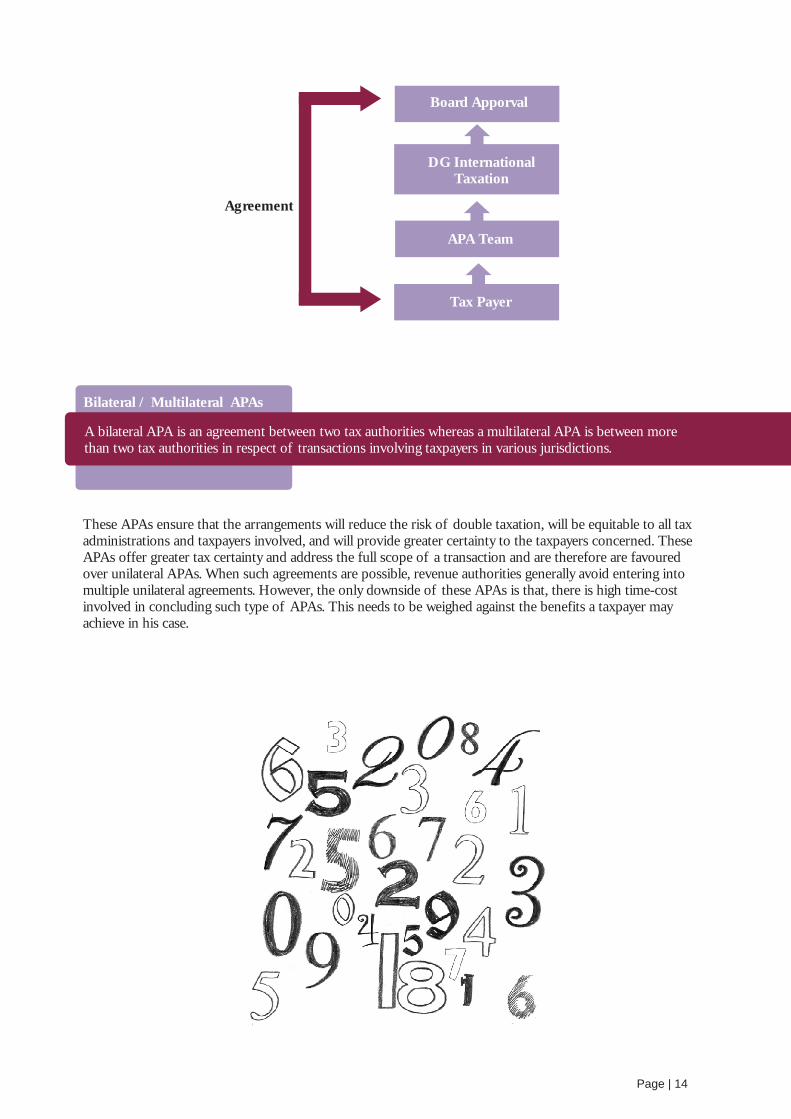

Bilateral / Multilateral APAs

A bilateral APA is an agreement between two tax authorities whereas a multilateral APA is between more than two tax authorities in respect of transactions involving taxpayers in various jurisdictions.

Agreement

These APAs ensure that the arrangements will reduce the risk of double taxation, will be equitable to all tax administrations and taxpayers involved, and will provide greater certainty to the taxpayers concerned. These APAs offer greater tax certainty and address the full scope of a transaction and are therefore are favoured over unilateral APAs. When such agreements are possible, revenue authorities generally avoid entering into multiple unilateral agreements. However, the only downside of these APAs is that, there is high time-cost involved in concluding such type of APAs. This needs to be weighed against the benefits a taxpayer may achieve in his case.

Page | 14

MAP-APA

MAP APAs are governed by the mutual agreement procedure of the applicable double tax agreement, Article 25 of the OECD Model Tax Convention, and are administered at the discretion of the relevant tax administrations. The guidelines provide that if a taxpayer does not request a MAP APA, then the reason should be reviewed, and wherever possible, tax authorities should encourage the taxpayer to request a MAP APA if the circumstances are suitable. The negotiation of MAP APAs requires the consent of the relevant competent authorities. In some cases the taxpayer might voluntarily take the initiative by making simultaneous requests to the affected competent authorities. The willingness to enter into MAP APAs will depend on the particular policy of a country and how it interprets the mutual agreement article of its bilateral treaties. The desire of the taxpayer for certainty of treatment is therefore not, in isolation, sufficient to execute MAP APAs.

The fact that a taxpayer may be under audit or examination should not prevent the taxpayer from requesting a MAP APA in respect of prospective transactions. The audit or examination and the mutual agreement procedure are separate processes and generally can be resolved separately. Audit or examination activities would not normally be suspended by a tax administration whilst the MAP APA is being considered, unless it is agreed by all parties that the audit or examination should be held in abeyance because the obtaining of the MAP APA would assist with the completion of the audit or examination.

Though the MAP process may provide more certainty and entail cost savings to the taxpayer, it is to be noted that it might not always be possible to apply a single transfer pricing methodology to a wide variety of facts and circumstances, transactions and countries likely to be the subject of a multilateral MAP APA. Therefore, care needs to be taken by all the participating jurisdictions to ensure that the methodology, even after such adaptation, represents a proper application of the arm’s length principle in the conditions found in their country.

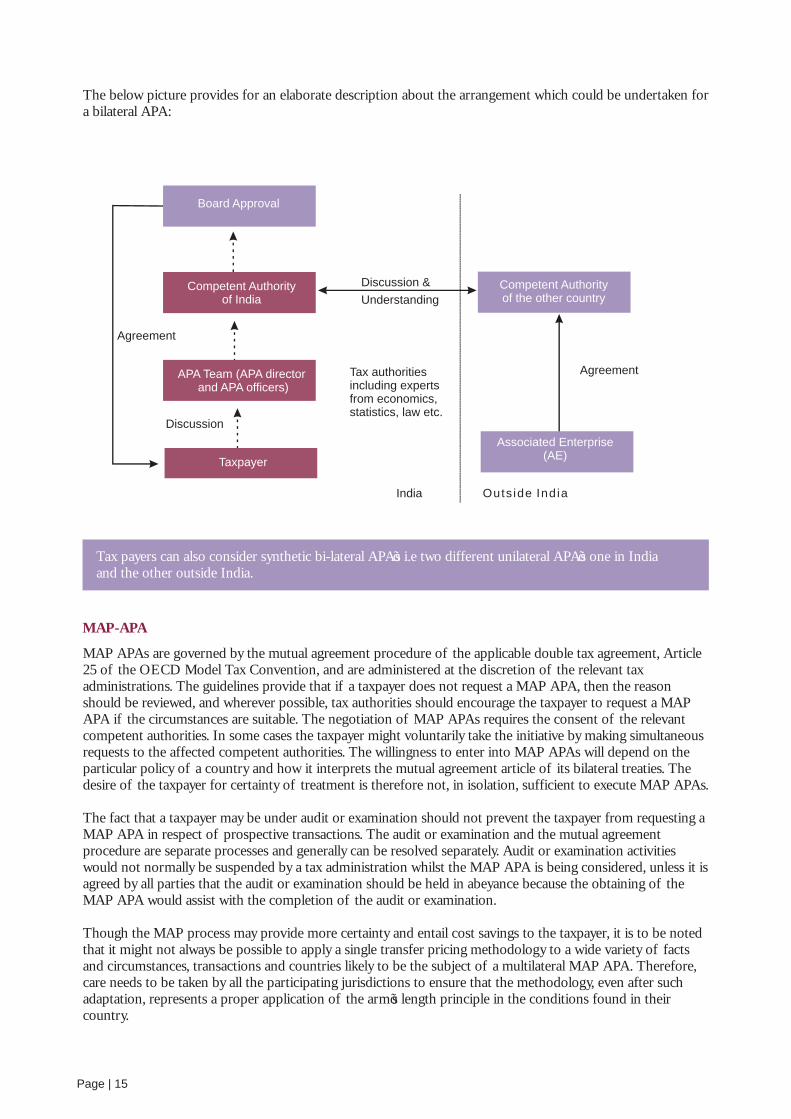

The below picture provides for an elaborate description about the arrangement which could be undertaken for a bilateral APA:

Board Approval

Competent Authorityof India

APA Team (APA director and APA officers)

Taxpayer

Agreement

Discussion

Discussion &

Understanding

Tax authorities including experts from economics, statistics, law etc.

India

Competent Authority of the other country

Board Approval

Associated Enterprise(AE)

Competent Authorityof India

Outs ide Ind ia

Agreement

Tax payers can also consider synthetic bi-lateral APA’s i.e two different unilateral APA’s one in India and the other outside India.

Page | 15

Choice of APA’s

Across the globe in some tax jurisdictions, multiple provisions and rules exist for choice of APA and its applicability. In certain countries unilateral APAs are only available when the bilateral treaty network is not available. In such cases, the regional tax authority may issue a unilateral decision with future effect. In some regions bilateral APAs are the rule and unilateral APAs are the exception only in special cases: where there is no treaty, where a large number of countries are involved, thus making a multilateral APA impractical, or where small businesses are involved.

In the interest of ‘sound tax administration’ and the elimination of any double taxation potential, taxpayers as well as the tax administrations prefer bilateral/multilateral APAs over unilateral APAs. However, bilateral/multilateral APAs tend to take a longer time to conclude as more than one tax administration is engaged in the process. In such cases, the tax administrations may choose to provide a unilateral APA to the taxpayer. While there can be situations where a unilateral APA might be preferable over a bilateral/multilateral APA, such situations are limited. More often than not, it would be in the interest of the tax authorities as well as the taxpayers to enter into bilateral/multilateral APAs for the reasons discussed above.

Though unilateral APAs may be useful in certain circumstances, such as covering issues or transactions where no applicable tax convention exists, they may prove to have limited utility where both tax administrations actively review the type of transactions being covered. Also in certain jurisdictions a unilateral APA is granted if the taxpayer shows ‘sufficient justification’.

In cases where global trading is conducted on a fully integrated basis (i.e. the trading and risk management of a book of financial products takes place in a number of different locations, usually at least three), a multilateral, and not a bilateral, APA has becomes necessary. However, in some cases where a bilateral APA has been sought and the treaty is not appropriate, or where a treaty is not applicable, the competent authorities of some countries may nevertheless conclude an arrangement using the executive power conferred on the heads of tax authorities. Considering the above, the choice of APA’s proves significance wherein critical and complex transactions are involved.

Indian APA Rules offer all three options i.e unilateral APA, bilateral APA and multilateral APA. The rules provided for taxpayers to provide reasons in writing if a unilateral APA is opted for. It may also be possible to convert a unilateral APA application that is not yet concluded into a bilateral APA. Conversion of bilateral to unilateral is anyway provided for in the rules.

Page | 16

Advance pricing agreement is a welcome move by the Government as it promises certainty of transfer prices and likely eliminates/reduce litigation. This would significantly free up the time of CFOs/ Tax Directors for business instead of tax matters. The mutual agreement procedure (MAP) under the Tax Treaties has been a rather prolonged and convoluted process going upto 3 years for a closure. As against this, although APA is also expected to initially take a long time, it would be a one-time investment and companies cap reap benefits on renewals after the expiry of the 5 year period. Renewals are generally understood to happen at a much faster pace thus crunching the overall time spent on the APA process.

Madhusoodhana Y R

Head - Global Tax and Trade,

Intel India

“

Practical Considerations for Implementing an APA

Type of transactions to be considered: Covered Transactions

As per Section 92CC(1) of the Income-tax Act, 1961, “The Board, with the approval of the Central Government, may enter into an advance pricing agreement with any person, determining the arm’s length price or specifying the manner in which arm’s length price is to be determined, in relation to an international transaction to be entered into by that person”. As such, all the international intercompany transactions entered with Associated Enterprises (“AEs”) are covered within the purview of an APA.

The taxpayer could decide the intercompany transactions in respect of which they would like to negotiate and enter into an APA. There is no requirement that all AEs or all intercompany transactions must be covered under an APA. However, it is important to fully disclose all the intercompany transactions proposed to be entered into by the taxpayer to the tax authorities’ APA team. In certain cases, if tax authorities are of the view that it would be important to include certain other intercompany transactions (originally proposed by the taxpayer to be excluded) for various reasons, the tax authorities may discuss with the taxpayer and mutually agree to include such transactions.

An APA should ideally cover complex / high value transactions considering the time and cost linked in concluding an APA.

The APA rules define covered transactions as the international transaction or transactions for which agreement has been entered into.

When is it right to enter into an APA

There are numerous aspects that the taxpayer should consider while deciding upon entering into an APA. The key determining aspects are highlighted below:

Certainty vs. Flexibility

Transfer pricing in India is heavily litigated in the last six concluded audits and taxpayers have been looking forward to clear answers to their arm’s length woes. In this regard, one of the benefits that the taxpayer can achieve through an APA is certainty.

While an APA provides a high degree of certainty over the APA term (a maximum of 5 years), there is a trade-off one has to accept vis-a-vis flexibility. Once a taxpayer enters into an APA, it does take away the ability to make fundamental changes to the transfer pricing method. Making any material changes on the key assumptions underlying the APA would make the APA subject to annulment by the Board.

Time & Cost

The APA process is a time consuming process and can take significantly longer time and resources as compared to a transfer pricing audit through the regular channel. Mature APA jurisdictions like Japan and USA also take a minimum of 14 months going all the way up to 3 years in some cases to conclude a unilateral APA. Bilateral / Multilateral APAs, would take even longer given the level of complexity just by virtue of having more than two tax administrations involved.

Page | 17

From an Indian perspective, the APA Rules define persons eligible to apply for APA rules as any person who has undertaken an international transaction; or is contemplating to undertake an international transaction.

The Rules have not prescribed any monetary limit with respect to the related party transaction value. However, there is pre-filing consultation and preliminary screening process involved prior to determining whether a formal application needs to be made.

Involvement of the taxpayer in the APA process

A taxpayer is exhaustively and significantly involved during an APA process. This may include, and is not limited to, taxpayers’ discussions with tax authorities, assisting tax authorities in onsite inspections of taxpayer’s premises which enables a deeper insight into the taxpayer’s business and accordingly the pricing of the transactions proposed to be covered under an APA. Importantly, the taxpayer is expected to be effectively involved in regular communication with its associated enterprises, ensuring effective information flow to tax authorities.

Further, the taxpayer should not expect to be involved in any internal discussions of tax authorities or correspondence. Where requested, the taxpayer should be prepared to attend meetings between officials and to provide any requested information or explanations in a timely manner.

From an Indian perspective too, the Rules do not permit taxpayers to be part of internal discussion of tax authorities

It is important for revenue authorities to encourage the involvement of taxpayer in the entire APA process. In case of bilateral / multilateral APAs, it would be advisable that the revenue authorities keep the taxpayer updated and informed about the progress of any discussion with any foreign tax authority and ensure confidentiality in respect of any information obtained from the taxpayer. It is also important that taxpayer and its associated enterprises in the other country provide consistent position to their respective competent authorities.

As such, the taxpayer should consider the time frames bearing in mind that an APA is a one-time process that can cover up to five years (another factor to consider is that roll backs are not permitted in India). While on one hand it can take a long time to conclude an APA, on the other, it might be a better option considering the timelines involved in pursuing normal channels of dispute resolution (litigation) in India.

Information Control

While negotiating an APA, one of the requirements would be to share a lot of information / documentation which could at times be confidential / trade secret. This involves not only the past positions of taxpayer, but also future plans and forecasts. On the other hand, if the taxpayer opts to go with the regular tax audit cycle, the information requirements are limited to the issues involved for the year under audit. Taxpayer should accordingly evaluate its option to go for an APA. In an APA situation the taxpayer is in control of information as compared to in a defense situation where information is demanded.

Eligibility Criteria

Various jurisdictions follow different practices for admission of an APA request. Some adopt a monetary threshold for accepting an APA while some focus on the degree of complexity involved in the transfer pricing issues proposed to be covered through APAs. For example, China requires the annual amount of related party transactions proposed to be covered under the APA should be over RMB 40 million. On the other hand, United Kingdom focuses on the degree of complexity involved in the transfer pricing issues proposed to be covered (however, there have been some recent changes in this regard; this criteria has been relaxed in the latest revised draft APA manual of the HMRC).

Page | 18

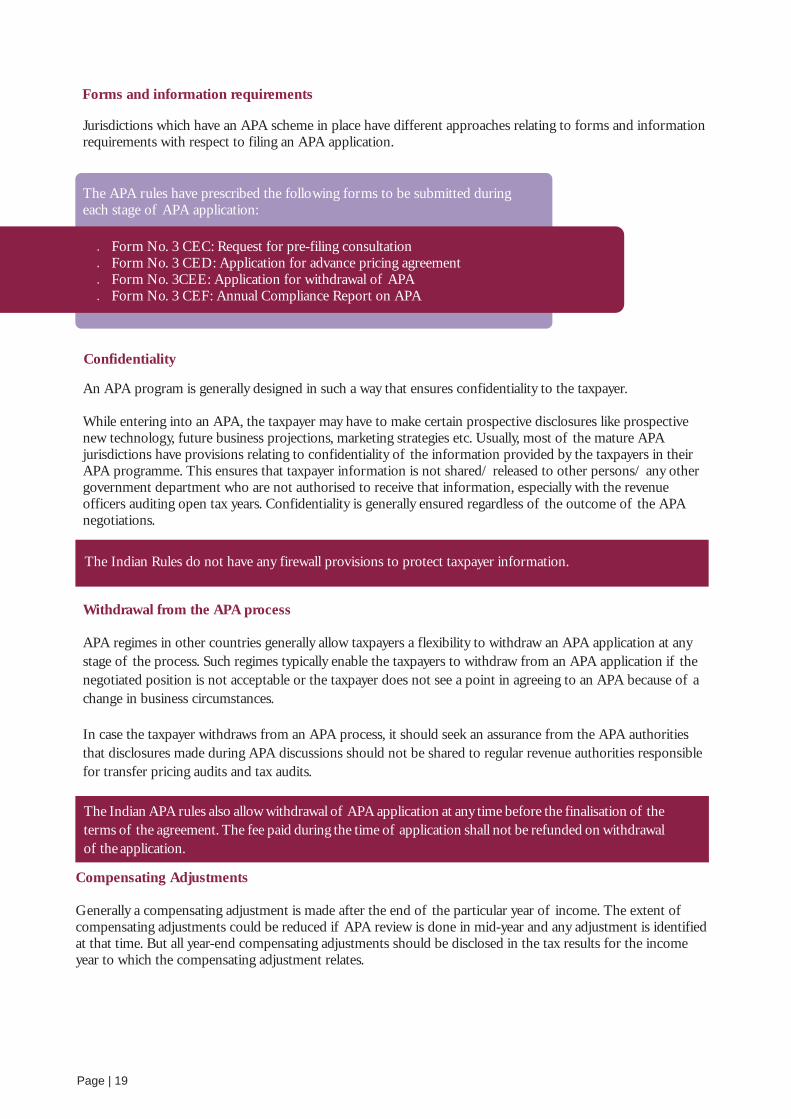

Forms and information requirements

Jurisdictions which have an APA scheme in place have different approaches relating to forms and information requirements with respect to filing an APA application.

Form No. 3 CEC: Request for pre-filing consultationForm No. 3 CED: Application for advance pricing agreementForm No. 3CEE: Application for withdrawal of APAForm No. 3 CEF: Annual Compliance Report on APA

An APA program is generally designed in such a way that ensures confidentiality to the taxpayer.

While entering into an APA, the taxpayer may have to make certain prospective disclosures like prospective new technology, future business projections, marketing strategies etc. Usually, most of the mature APA jurisdictions have provisions relating to confidentiality of the information provided by the taxpayers in their APA programme. This ensures that taxpayer information is not shared/ released to other persons/ any other government department who are not authorised to receive that information, especially with the revenue officers auditing open tax years. Confidentiality is generally ensured regardless of the outcome of the APA negotiations.

The Indian Rules do not have any firewall provisions to protect taxpayer information.

The APA rules have prescribed the following forms to be submitted during each stage of APA application:

Withdrawal from the APA process

APA regimes in other countries generally allow taxpayers a flexibility to withdraw an APA application at any

stage of the process. Such regimes typically enable the taxpayers to withdraw from an APA application if the

negotiated position is not acceptable or the taxpayer does not see a point in agreeing to an APA because of a

change in business circumstances.

In case the taxpayer withdraws from an APA process, it should seek an assurance from the APA authorities

that disclosures made during APA discussions should not be shared to regular revenue authorities responsible

for transfer pricing audits and tax audits.

The Indian APA rules also allow withdrawal of APA application at any time before the finalisation of the

terms of the agreement. The fee paid during the time of application shall not be refunded on withdrawal

of the application.

Page | 19

Confidentiality

Compensating Adjustments

Generally a compensating adjustment is made after the end of the particular year of income. The extent of compensating adjustments could be reduced if APA review is done in mid-year and any adjustment is identified at that time. But all year-end compensating adjustments should be disclosed in the tax results for the income year to which the compensating adjustment relates.

Compensating adjustments are not recognised by most OECD member countries, on the grounds that the tax return should reflect the actual transactions. Where compensating adjustments are permitted (or required) in the country of one associated enterprise but not permitted in the country of the other associated enterprise, double taxation may result as corresponding adjustment relief may not be available if no primary adjustment is made. The mutual agreement procedure is available to resolve difficulties presented by compensating adjustments, and revenue authorities are encouraged to use their best efforts to resolve any double taxation which may arise from different country approaches to such year-end adjustments.The above issue of double taxation is eliminated in the case of bilateral/multilateral APAs where the tax authorities provide an upfront buy-in to the covered international transactions.

Fees

Out of all the countries which have APA scheme in place, only few countries have some form of APA fee

requirement. The main purpose of charging a fee is to effectively conclude an APA within a reasonable period of

time. The APA fee arrangements may vary from fixed fees payable at the time of application to an APA scheme, or

variable fee arrangements based on certain actual costs like travel and accommodation costs incurred by the

revenue authorities in processing an APA application. In India a graded fee is prescribed.

Time frame for an APA Process

The time frame for an APA process depends on the type of APA entered into, i.e., whether it is a unilateral APA or

bilateral/multilateral APA. Further, the time frame varies on a case-to-case basis depending on the complexities

involved and needs significant amount of time and analysis before an APA is agreed and concluded between the

taxpayer and revenue authorities.

Generally a unilateral APA may take upwards of 14 months and bilateral/multilateral APA may take up to 36-48

months for completion. There would be need for the taxpayer and revenue authorities to discuss and agree a

proposed time frame for completion of APA at the initial stage of filing an APA application. Regular monitoring

of the progress against the agreed time frame by both, the taxpayer, and, by revenue authorities, may help in

ensuring timely conclusion of an APA process.

There are specific countries like UK, Israel, Lithuania which provide for time frame to conclude an APA.

India Rules do not provide for a time frame to conclude an APA.

Page | 20

When an APA arrangement nears completion, tax authorities may agree (on the request of the taxpayer) to

extend the APA beyond the period for which it was originally agreed upon. Such an extended arrangement is

termed as a renewal of an APA.

A request to renew an APA should be made bearing in mind the need for sufficient lead time required by the

taxpayer and by revenue authorities to review and evaluate the renewal request and to reach an agreement. It

may be helpful to commence the renewal process well before the existing APA completion date.

Renewal of an APA

Indian Rules do not provide for a time frame to conclude an APAThe processing and evaluation of renewal application is generally similar to an initial APA application process.

However, the necessary level of details may be reduced; particularly if there have not been material changes in

the facts and circumstances of the case.

Renewal of an APA is not automatic and depends on the consent of all the parties concerned and subject to

the taxpayer demonstrating, among other things, compliance with the terms and conditions of the existing

APA. The methodology and terms and conditions of the renewed APA may differ from those of the previous

APA.

The Indian APA Rules provide for renewing of an APA. The request for renewal of an APA has to be

made as a new application, using the same procedure as outlined for in the APA rules except for pre

filing consultation.

Roll-back of an APA

An APA is generally prospective in nature, that is, it addresses the transactions which occur in future. But, APA

may address the prior year issues/transactions that are either in the course of dispute between the taxpayer and the

competent revenue authorities or which are under audit review. The final agreement discussed and agreed in an

APA may be applied or rolled back to the transaction(s) in the prior period.

Taxpayers may request the revenue authorities to consider for rollback, along with the initial filing of an APA

application. However, the revenue authorities may also propose that similar transfer pricing method as agreed

under an APA should be rolled back to prior years. Approval of other country's revenue authorities is required if

the roll back is for a bilateral APA.

Though rollbacks for APA are not formally enabled, it seems that a successfully concluded APA will have high precedence value for pending litigation cases or pending mutual agreement proceedings if the facts are similar for these cases as well.

Vaishali Mane

Client Service Director

Transfer Pricing Services

“Grant Thornton India LLP

Page | 21

The Indian APA Rules does not enable for roll back of APA, but a concluded APA could have

precedence value for open litigation issues for most taxpayers.

Kudos to the Indian Government for introducing the APA scheme, a beacon of hope for corporate India and MNCs to arrest the thousands of crores of Rupees locked up in transfer pricing controversies. An open and cooperative approach from Revenue as well as the taxpayers in implementing the APA process shall be the defining corner stones of success which would be a departure from the defensive approach in vogue for decades in India.

Fatema Hunaid

Client Service DirectorTransfer Pricing Service

“

Public Reporting

Some countries like Japan, Australia and USA which are mature APA jurisdictions prepare and publish APA

annual reports of their APA schemes which include statistics as to the types of APA applications received &

processed and also inventory of work-in-progress.

Taxpayers, on the other hand, are also required to submit, within a specified period of time, all reports

demonstrating compliance with the rules of APA on a yearly basis called APA Annual Report. The APA Annual

Report substitutes the formal transfer pricing documentation which the taxpayer is required to comply with under

regular transfer pricing legislation and thereby reduces the taxpayer's cost and time involved in maintaining the

annual mandatory transfer pricing documentation for the international transactions required under the Indian

transfer pricing legislation.

Grant Thornton India LLP

Indian government can also consider some form of public reporting.

Page | 22

APA Process

The below diagram depicts the lucid stages involved in an APA process. The APA process is exhaustive in nature.

The below APA process would usually be adopted by a taxpayer, however it should not be considered as a

yardstick approach. The taxpayer will have to dedicate copious amount of time and resources in the entire APA

process for a successful outcome.

Phase 1 : Feasibility studyDetermine suitability of an APA

Phase 2 : Pre-filing Consultation Understand the perspective of the department on basic issues

Phase 3 : APA Application File a written APA application and preliminary screening

Phase 4 : Negotiation Negotiations between the taxpayer and tax administrator

Phase 5 : Execute APA formal agreement of APA executed which is binding on taxpayer and tax administrator

Phase 6 : Annual APA Compliance Report File and annual compliance report in relation to the implementation of the APA

Phase 7 : Compliance Audit TPO to carry compliance Audit for each covered year

Phase 8 : APA Renewal Extending the APA beyond the period originally provided (new APA)

Page | 23

We expect the APA regime to layout clear criteria’s or ground rules for admitting APA application, time bound decisions and transparency in decision making from the authorities.

Priya MurliBayer Cropscience India LimitedHead of Taxation

“

An APA may not be suitable for everyone and in every situation. Thus, a feasibility study needs be undertaken.

A feasibility study aims to objectively and rationally uncover, the strengths and weaknesses of the existing

business model or proposed venture, evaluate the opportunities and threats and ultimately draw up the

prospects for success. The feasibility study should also aim to analyse which transaction or group of

transaction the taxpayer should cover while entering into an APA. In its simplest terms, the feasibility study

should encapsulate the objective, type of transaction to be covered, cost-benefit (economic) analysis and the

risk threshold. This will enable a company to decide if an APA is feasible or not.

As mentioned above, the feasibility study should detail the primary objective for entering into an APA. The

objective could be to determine certainty in case of high risk / high value transfer pricing issue or ensure

certainty before starting a new line of business; expansion etc. or another objective could be to eliminate risk

of double taxation (bilateral/multilateral APA).

Once the objective is decided, the next step would be to determine the economic benefit for entering into an

APA vis-à-vis the current litigation options available. The economic analysis would entail undertaking a cost-

benefit-risk analysis. The taxpayer will have to determine an appropriate threshold limit in terms of time,

resource and money that it would want to invest in an APA process. In case where the taxpayer has gamut of

international transaction, the taxpayer will also need to analyse the economic feasibility in terms of which

transaction or group of transaction should be covered. Analysing all these factors, would help the taxpayer to

determine the benefits and savings that are expected from an APA as compared to the time-cost and effort

involved in procuring an APA and the acceptable risk tolerance benchmarks.

One more important factor one needs to consider is the outcome of the APA may not always be the same as

expected. In the process of filing for an APA one will have to disclose a lot of confidential information.

Therefore, while undertaking the feasibility study; an evaluation of this risk also should not be ignored.

Once it makes economic sense for entering into an APA, one has to also determine which transactions should

be covered and also undertake a detailed transfer pricing analysis for the covered transaction. This would

enable in anticipating the transfer pricing methodology and benchmarks for the covered transactions.

Thus a feasibility study should analyse the pros and cons and simultaneously with the help of the transfer

pricing analysis determine the economic benefit for entering into an APA. If the economic benefit outweigh

costs and the acceptable risks, then it is feasible to enter in to an APA.

Pre-filing Consultation (PFC)

PFC allows taxpayers to discuss the suitability of an APA before deciding to pursue it. The PFC would be

fruitful if the taxpayer is given a chance to discuss the case directly with the Board personnel who would be

processing the case.

It is understood that, the pre-filing conferences can be held on a named or anonymous basis also. An

anonymous pre-filing conference provides the taxpayers the opportunity to discuss the facts and issues of the

case with the board. During the discussion, the taxpayer can determine the openness of the Board to the

issues of the taxpayer, without the fear of inviting an audit if the taxpayer decides not to proceed with an

APA.

It is pertinent to note that the taxpayer should file the pre-filing submission to the APA office one week prior

to the meeting. This would enable the APA team and the taxpayer to be equally prepared for a productive

meeting.

Feasibility Study

Page | 24

determine the scope of the agreement;identify transfer pricing issues;determine the suitability of international transaction for the agreement;discuss broad terms of the agreement.

As per the Indian APA Rules the pre filing consultation aims to achieve the following:

The PFC may conclude with a written understanding as the APA application needs to adhere to broad terms agreed during the PFC.

The pre filing discussions however do not bind a taxpayer or the tax administration to the APA process.

Usually like other countries, it is expected that the taxpayer would get only one chance for the pre-filing

meeting. However, if the level of complexities is high then there can be more than one pre-filing meeting. The

tax authorities can also suggest in the pre-filing meeting what further information may be required to be filed

while submitting the formal APA application.

Page | 25

Thus a pre-filing meeting would give the taxpayer a fair perspective on the receptivity of the APA Board. The taxpayer can then decide whether it would want to formally apply for an APA. Also based on the pre filing discussion, the taxpayer can accordingly strategise its submission approach, transfer pricing methodology to be adopted etc. to ensure smooth processing of APA. There is no fee for the PFC.

As per the Indian APA rules; the pre filing submission should include the following (details provided in annexure)

Pre filing application to contain

Define RPT to be covered

Value of IT – Prior 3 yrs TP audit

Brief profile of the business

Brief profile of the business

Proposed TPMSpecify the type of APA

FAR profile Proposed TPMProposed TPM Why other TPM not suitable

Define profit level indicators

Brief profile of the business

Type of any 3rd party benchmark

Define critical assumptions

APA application

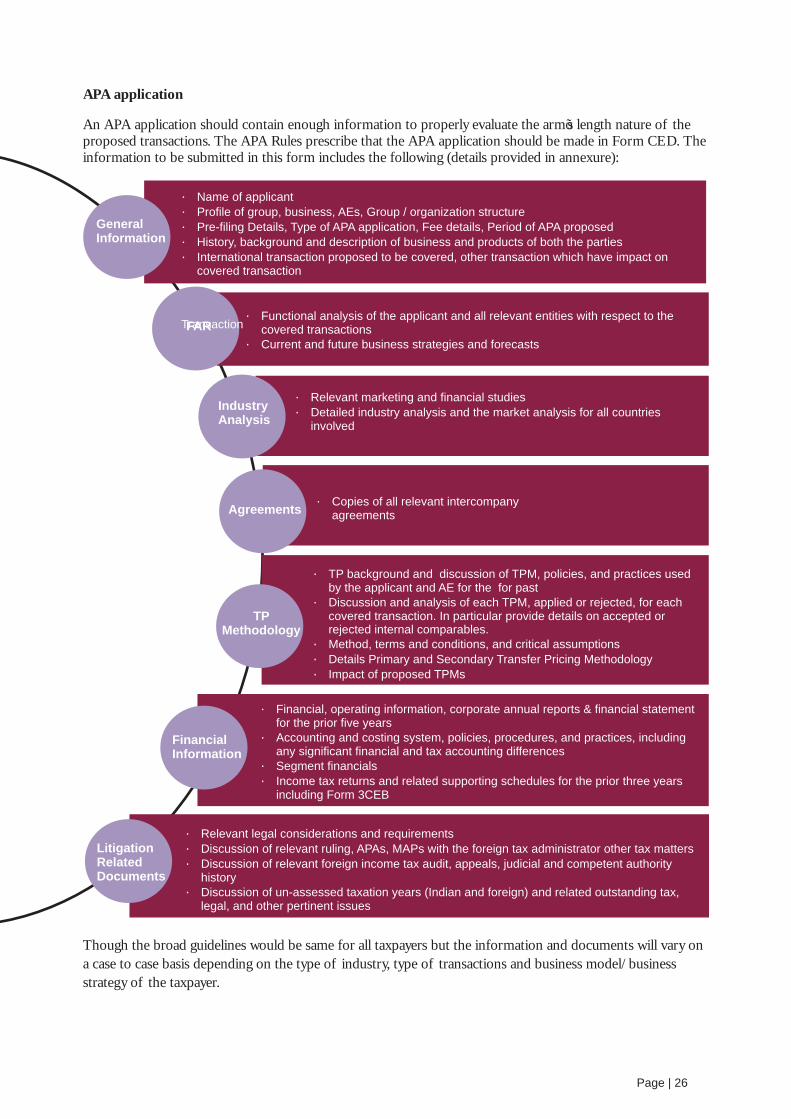

An APA application should contain enough information to properly evaluate the arm’s length nature of the proposed transactions. The APA Rules prescribe that the APA application should be made in Form CED. The information to be submitted in this form includes the following (details provided in annexure):

Page | 26

Though the broad guidelines would be same for all taxpayers but the information and documents will vary on

a case to case basis depending on the type of industry, type of transactions and business model/business

strategy of the taxpayer.

General Information

Industry Analysis

FAR

Agreements

TP Methodology

Financial Information

Litigation Related Documents

Name of applicant

Profile of group, business, AEs, Group / organization structure

Pre-filing Details, Type of APA application, Fee details, Period of APA proposed

History, background and description of business and products of both the parties

International transaction proposed to be covered, other transaction which have impact on covered transaction

Transaction Functional analysis of the applicant and all relevant entities with respect to the

covered transactions Current and future business strategies and forecasts

Relevant marketing and financial studies

Detailed industry analysis and the market analysis for all countries involved

Copies of all relevant intercompany agreements

TP background and discussion of TPM, policies, and practices used by the applicant and AE for the for past

Discussion and analysis of each TPM, applied or rejected, for each covered transaction. In particular provide details on accepted or rejected internal comparables.

Method, terms and conditions, and critical assumptions

Details Primary and Secondary Transfer Pricing Methodology

Impact of proposed TPMs

Financial, operating information, corporate annual reports & financial statement for the prior five years

Accounting and costing system, policies, procedures, and practices, including any significant financial and tax accounting differences

Segment financials

Income tax returns and related supporting schedules for the prior three years including Form 3CEB

Relevant legal considerations and requirements

Discussion of relevant ruling, APAs, MAPs with the foreign tax administrator other tax matters

Discussion of relevant foreign income tax audit, appeals, judicial and competent authority history

Discussion of un-assessed taxation years (Indian and foreign) and related outstanding tax, legal, and other pertinent issues

The deficiency letter shall be served to the taxpayer before the expiry of one month from the date of receipt of the application.

On receipt of the deficiency letter the taxpayer will have to remove the deficiency or modify the application within a period of fifteen days (maximum 30 days) from the date of service of the deficiency letter.

Based on the modified application, the DGIT or the competent authority in India, as the case may be, if satisfied with the modified application may pass an order for the application to be further processed. In case they are not satisfied then the application shall not be allowed to be proceeded. However, no order will be passed without providing an opportunity of being heard to the applicant and if an application is not allowed to be proceeded with, the fee paid by the applicant shall be refunded.

Negotiations between taxpayer and tax administration

Once the APA application is received by the tax administration, it would study and evaluate the application in detail. If the tax administration requires any additional information or documents then it would send a notice to the taxpayer to provide the same. In addition to the written information requests, the tax administration could also request for onsite visits.

After understanding and gathering all the required information the tax administration would then arrange for negotiation meetings with the taxpayer. In case of unilateral APAs, the tax administration will arrange negotiations and discussions with the taxpayer. For bilateral APAs, the tax administration will first arrange negotiations with the taxpayer and then enter into discussion rounds with the relevant competent authorities.

In the negotiation phase the tax administration and the taxpayer would mutually reach to a conclusion on the transfer pricing of the covered transactions. In complex transactions, the negotiation meetings could be more than one meeting.

The tax administrator should share with the taxpayer its findings/conclusion after the negotiations. Once the negotiation proceedings are done the next step in the APA process would be drafting of an APA.

Page | 27

For a bilateral, similar submission must also be filed simultaneously with the other tax administration involved.

A well drafted APA documentation pack would ensure smooth processing of the application. It would also give the tax administration upfront clarity on the issue and thereby reduce the time and effort involved in processing of the APA.

As per the Indian APA Rules, every application filed by the taxpayer should be complete respects and accompanied by requisite documents. The DGIT or Competent Authority in India shall issue a deficiency letter if:

any defect is noticed in the application, or any relevant document is not attached, or application is not in accordance with understanding reached in pre-filing consultation

This step is unique compared to APA regimes of other mature tax administrations.

Preliminary Screening

The APA application should be filed before the first day of the previous year relevant to the first assessment

year for which the application is made, in respect of transactions which are of a continuing nature from

dealings that are already occurring; or before undertaking the transaction in respect of remaining transactions.

Draft and Execute APA

The formal agreement is based on the negotiation carried out between the taxpayer and the tax authorities. In the case of a unilateral APA, the tax authorities and the taxpayer in the course of negotiation may have agreed on a methodology or outcome, and it is then up to the tax authorities to draft an appropriate agreement that recognizes this particular outcome. However, in the case of a bilateral/multilateral APA, a similar process would be followed where the relevant tax authorities agree on a TPM or outcomes. While drafting the APA the tax authorities may take into account many basic assumptions like:

corporate shareholding structure; constant conditions regarding market conditions, market shares, revenue volumes, and sales prices (e.g. no

significant changes due to new technology); constant conditions regarding regulatory law, customs, import and export restrictions, and international

payment transactions; constant function and risk allocation; constant business model; constant conditions regarding exchange rates and interest rates; no material changes in the tax framework of the other state; and any other critical assumptions

details of the taxpayer type of APA entered into name(s) of the associated enterprise(s) with which international transactions have been undertaken

during the year. details of Covered Transactions including nature, amount, agreed TPM, agreed PLI, actual result

achieved, adjustment required details of any changes in the business model details of any changes in the Functional and Risk Profile of the taxpayer and the associated enterprises transfer pricing methodology agreed upon in the APA details of Critical assumptions agreed upon in the APA and changes thereof, if any: details of any changes in the organisational structure of the taxpayer / group details of other terms and conditions agreed upon in the APA

The APA authorities could consider using a standard template of an APA agreement like the US IRS.

Annual APA Compliance Report

Page | 28

The tax authorities will draft the formal agreement in a manner consistent with the laws of that country relating to contractual arrangements and having regard to provisions in the tax law. It is imperative that the taxpayer should consult with its advisers as to the appropriateness of the agreement proposed by the tax authorities. This formal agreement will be binding on both the taxpayers and tax authorities. If any tax demand is raised as a result of the normal TP audit process on any subject matter of the APA, the same should not be enforced till the execution of the APA.

The taxpayer is also required to prepare and file an annual compliance report in relation to the implementation of the APA to the tax authority for each year of the APA. The Indian APA Rules require the following information to be furnished in the annual compliance report:

Compliance Audit

The TPO having the jurisdiction over the taxpayer will carry out the compliance audit of the agreement for each of the year covered in the agreement. The TPO will have to furnish the compliance audit report within six months from the end of the month in which the annual compliance report is referred to him.

While undertaking the compliance audit, the TPO may require the assessee to substantiate compliance with the terms of the agreement, including satisfaction of the critical assumptions, correctness of the supporting data or information and consistency of the application of the transfer pricing method. The TPO may also ask the assessee to submit any information, or document, to establish that the terms of the agreement has been complied with.

The TPO shall submit the compliance audit report, for each year covered in the agreement, to the DGIT in case of unilateral agreement and to the competent authority in India, in case of bilateral or multilateral agreement, mentioning therein his findings as regards compliance by the assesse with terms of the agreement. The DGIT shall forward the report to the Board in a case where there is finding of failure on part of assesse to comply with terms of agreement and cancellation of the agreement is required.

APA Renewal

When an existing APA is drawing to a close of its term, the parties agree to enter into further discussions or negotiations with a view to extending the APA beyond the period originally provided. Any such extended arrangement is concluded as a new APA.

The taxpayer may have to file an application along with supporting evidence to confirm that there have not been any major changes to the facts and conditions in the existing APA, and that the taxpayer has been in full compliance with the provisions and requirements of the APA. After receiving the application, tax authorities will review and evaluate the application documents, and negotiate with the taxpayer to draft the new APA.

The renewal of APA would result in benefits to all parties involved in the negotiation process. In particular, the tax certainty is extended for the agreed further term and, therefore, the voluntary compliance objectives are enhanced. Also far less time and resources are required to renew an APA than were required for the initial APA, this will result in reduced cost for the taxpayer.

As per the Indian Rules, similar procedure for renewal is to be followed excluding pre-filing consultation.

Page | 29

The compliance audit is not expected to be in the name of a regular TP audit.

Critical Analysis of an APA

The APA process as per the Indian APA Rules is consistent with the process adopted by other countries with the only difference that the Indian Rules do not enable for Roll back of APAs

Presently the concept of APA is being perceived as a vaccine for the ever-growing transfer pricing litigations.

APA provides a reasonable degree of certainty relating to tax outcome of the international transaction(s)

entered into by the taxpayer by determining in advance the transfer pricing methodology to be applied in

respect of the international transaction(s) covered by an APA. An APA may thus be helpful in minimising

transfer pricing audits, delivering a particular tax outcome based on the terms of the agreement, and often

substantially reducing compliance costs over the duration of the APA. This enables a more efficient and

effective management of transfer pricing compliance requirements by bringing fairness, simplicity and

efficiency which may otherwise lead to become litigation issues. Thus, from the perspective of a taxpayer, an

APA can be a mechanism for efficient handling of tax risks associated with international transactions. And

from the perspective of tax authorities, an APA can similarly be a mechanism for quality administration of the

transfer pricing legislation. Hence, APA results in win-win situation for both the parties involved i.e. taxpayer

and tax administrator.

APA, in particular a bilateral or a multilateral, can be an effective tool in potentially eliminating double

taxation. A pre-determined pricing strategy which is acceptable to all the tax jurisdictions will result into

optimal allocation of income among the jurisdictions involved with-out the risk on an income being double

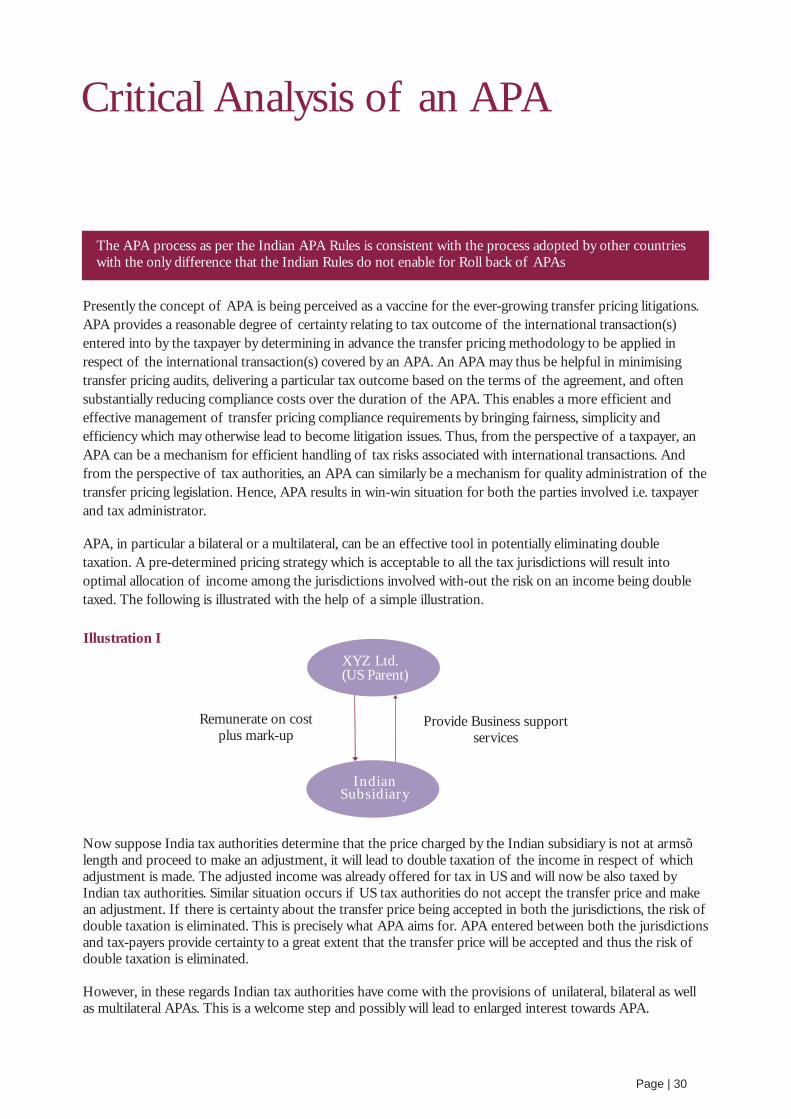

taxed. The following is illustrated with the help of a simple illustration.

XYZ Ltd.(US Parent)

Remunerate on cost plus mark-up

Provide Business support services

Indian Subsidiary