Embed Size (px)

Citation preview

ed-TH / sa- MA

Shrinking Universe

Cut our coal benchmark price forecast to US$55 per ton

Paris climate agreement is negative for thermal coal

Meanwhile, currently natural gas is competitive vs. thermal coal price

Stock price correction is a de-rating process and NOT an opportunity to buy

Cut our coal benchmark price to US$55 per ton. We cut our long-term coal benchmark price to US$55 per ton from US$67 previously. Current low crude oil and gas prices will exert more pressure on coal price and demand, as natural gas, which is more environmentally friendly than coal, is trading at a minor disparity vs. coal for the first time. This is would potentially accelerate energy substitution from coal to gas after the Paris climate deal on Dec 2015, which was participated by 200 countries. Moreover, we also believe the current pollution issue in China coastal area will put environmental issues in the government's top priority via pushing ultra low emission energy mix going forward. This means thermal coal energy mix will continue to drop ahead, and our thesis that thermal coal import peaked in 2014 and will continue to drop ahead remains intact.

Insignificant supply cuts. Amid the coal demand downtrend, we see insignificant supply cuts by major coal miners from both Indonesia and Australia. Indonesia's largest coal miners have indicated that production volume could drop next year. However, the official production target has not been released yet. We cut our FY16 and FY17 thermal coal stocks earnings by 10% and 15% on average respectively, mainly on production cuts as miners will not lower their strip ratios to reduce cash cost at the current coal price level, to preserve their reserves.

No positive catalyst for coal stocks. Stock price tumbled 50% on average last year and we believe it was part of coal stocks' valuation de-rating amid the structural changes in the coal sector and NOT an opportunity to buy coal stocks. Low coal price in the long run also casts uncertainties on miners' long-term earnings, cash flows and coal reserves' economic feasibility. Our top Fully Valued call remain HRUM with lower target price of Rp450 on lower ASP and production volume outlook.

JCI : 4,523.98

Analyst William Simadiputra +62 2130034939 [email protected]

STOCKS

Source: DBS Vickers Tambang Batubara Bukit Asam: Indonesia largest coal miners with 1.99bn ton of coal reserves. Main coal mining concession located in Tanjung Enim, south Sumatera

Adaro Energy: Indonesia second largest coal producer. It also has subsidiaries that operate in the mining contracting, barging and ship loading business

Indo Tambangraya Megah: One of the largest coal mining company Banpu. Coal consession located in Kalimantan, Indonesia

Harum Energy: Ninth largest coal producers in Indonesia combined coal reserves life of 7 years

DBS Group Research . Equity 18 Jan 2016

Indonesia Industry Focus

Thermal Coal Sector

Refer to important disclosures at the end of this report

Price Mkt Cap Target Price Performance (%)

Rp US$m Rp 3 mth 12 mth Rating

Tambang Batubara 4,465 736 5,100 (30.8) (60.1) HOLD Adaro Energy 449 1,027 505 (29.8) (52.5) HOLD Indo Tambangraya 5,425 438 6,100 (46.4) (63.8) HOLD Harum Energy 670 130 450 (25.6) (61.4) FULLY

Industry Focus

Thermal Coal Sector

Page 2

Cut our coal benchmark price to US$55 per ton.

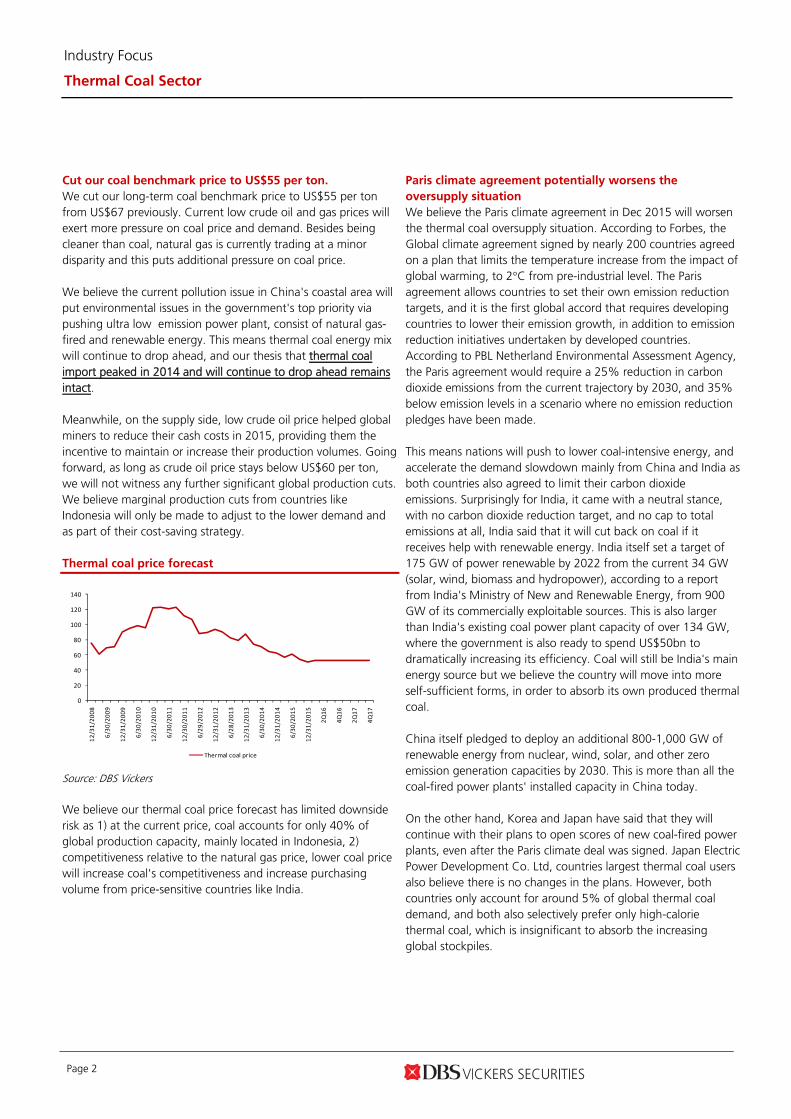

We cut our long-term coal benchmark price to US$55 per ton from US$67 previously. Current low crude oil and gas prices will exert more pressure on coal price and demand. Besides being cleaner than coal, natural gas is currently trading at a minor disparity and this puts additional pressure on coal price. We believe the current pollution issue in China's coastal area will put environmental issues in the government's top priority via pushing ultra low emission power plant, consist of natural gas-fired and renewable energy. This means thermal coal energy mix will continue to drop ahead, and our thesis that thermal coal import peaked in 2014 and will continue to drop ahead remains intact. Meanwhile, on the supply side, low crude oil price helped global miners to reduce their cash costs in 2015, providing them the incentive to maintain or increase their production volumes. Going forward, as long as crude oil price stays below US$60 per ton, we will not witness any further significant global production cuts. We believe marginal production cuts from countries like Indonesia will only be made to adjust to the lower demand and as part of their cost-saving strategy. Thermal coal price forecast

0

20

40

60

80

100

120

140

12/31/2008

6/30/2009

12/31/2009

6/30/2010

12/31/2010

6/30/2011

12/30/2011

6/29/2012

12/31/2012

6/28/2013

12/31/2013

6/30/2014

12/31/2014

6/30/2015

12/31/2015

2Q16

4Q16

2Q17

4Q17

Thermal coal price

Source: DBS Vickers We believe our thermal coal price forecast has limited downside risk as 1) at the current price, coal accounts for only 40% of global production capacity, mainly located in Indonesia, 2) competitiveness relative to the natural gas price, lower coal price will increase coal's competitiveness and increase purchasing volume from price-sensitive countries like India.

Paris climate agreement potentially worsens the

oversupply situation

We believe the Paris climate agreement in Dec 2015 will worsen the thermal coal oversupply situation. According to Forbes, the Global climate agreement signed by nearly 200 countries agreed on a plan that limits the temperature increase from the impact of global warming, to 2°C from pre-industrial level. The Paris agreement allows countries to set their own emission reduction targets, and it is the first global accord that requires developing countries to lower their emission growth, in addition to emission reduction initiatives undertaken by developed countries. According to PBL Netherland Environmental Assessment Agency, the Paris agreement would require a 25% reduction in carbon dioxide emissions from the current trajectory by 2030, and 35% below emission levels in a scenario where no emission reduction pledges have been made. This means nations will push to lower coal-intensive energy, and accelerate the demand slowdown mainly from China and India as both countries also agreed to limit their carbon dioxide emissions. Surprisingly for India, it came with a neutral stance, with no carbon dioxide reduction target, and no cap to total emissions at all, India said that it will cut back on coal if it receives help with renewable energy. India itself set a target of 175 GW of power renewable by 2022 from the current 34 GW (solar, wind, biomass and hydropower), according to a report from India's Ministry of New and Renewable Energy, from 900 GW of its commercially exploitable sources. This is also larger than India's existing coal power plant capacity of over 134 GW, where the government is also ready to spend US$50bn to dramatically increasing its efficiency. Coal will still be India's main energy source but we believe the country will move into more self-sufficient forms, in order to absorb its own produced thermal coal. China itself pledged to deploy an additional 800-1,000 GW of renewable energy from nuclear, wind, solar, and other zero emission generation capacities by 2030. This is more than all the coal-fired power plants' installed capacity in China today. On the other hand, Korea and Japan have said that they will continue with their plans to open scores of new coal-fired power plants, even after the Paris climate deal was signed. Japan Electric Power Development Co. Ltd, countries largest thermal coal users also believe there is no changes in the plans. However, both countries only account for around 5% of global thermal coal demand, and both also selectively prefer only high-calorie thermal coal, which is insignificant to absorb the increasing global stockpiles.

Industry Focus

Thermal Coal Sector

Page 3

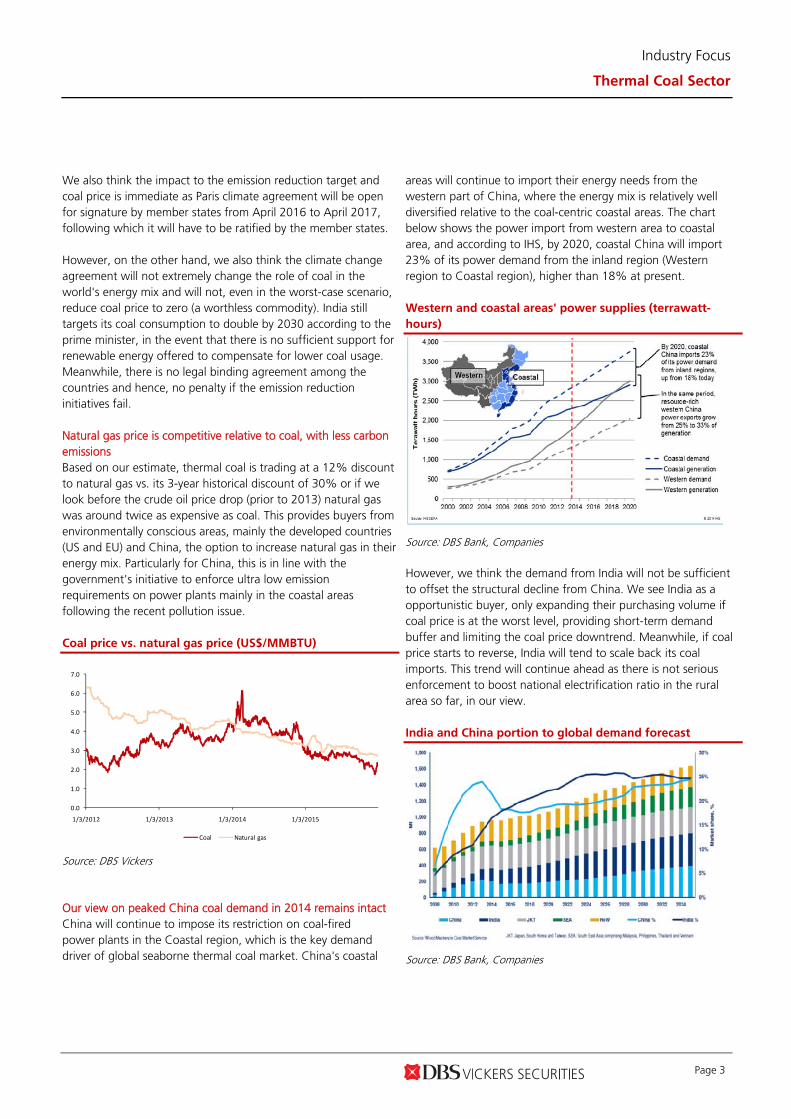

We also think the impact to the emission reduction target and coal price is immediate as Paris climate agreement will be open for signature by member states from April 2016 to April 2017, following which it will have to be ratified by the member states. However, on the other hand, we also think the climate change agreement will not extremely change the role of coal in the world's energy mix and will not, even in the worst-case scenario, reduce coal price to zero (a worthless commodity). India still targets its coal consumption to double by 2030 according to the prime minister, in the event that there is no sufficient support for renewable energy offered to compensate for lower coal usage. Meanwhile, there is no legal binding agreement among the countries and hence, no penalty if the emission reduction initiatives fail. Natural gas price is competitive relative to coal, with less carbon emissions Based on our estimate, thermal coal is trading at a 12% discount to natural gas vs. its 3-year historical discount of 30% or if we look before the crude oil price drop (prior to 2013) natural gas was around twice as expensive as coal. This provides buyers from environmentally conscious areas, mainly the developed countries (US and EU) and China, the option to increase natural gas in their energy mix. Particularly for China, this is in line with the government's initiative to enforce ultra low emission requirements on power plants mainly in the coastal areas following the recent pollution issue. Coal price vs. natural gas price (US$/MMBTU)

0.0

1.0

2.0

3.0

4.0

5.0

6.0

7.0

1/3/2012 1/3/2013 1/3/2014 1/3/2015

Coal Natural gas

Source: DBS Vickers Our view on peaked China coal demand in 2014 remains intact China will continue to impose its restriction on coal-fired power plants in the Coastal region, which is the key demand driver of global seaborne thermal coal market. China's coastal

areas will continue to import their energy needs from the western part of China, where the energy mix is relatively well diversified relative to the coal-centric coastal areas. The chart below shows the power import from western area to coastal area, and according to IHS, by 2020, coastal China will import 23% of its power demand from the inland region (Western region to Coastal region), higher than 18% at present. Western and coastal areas' power supplies (terrawatt-

hours)

Source: DBS Bank, Companies However, we think the demand from India will not be sufficient to offset the structural decline from China. We see India as a opportunistic buyer, only expanding their purchasing volume if coal price is at the worst level, providing short-term demand buffer and limiting the coal price downtrend. Meanwhile, if coal price starts to reverse, India will tend to scale back its coal imports. This trend will continue ahead as there is not serious enforcement to boost national electrification ratio in the rural area so far, in our view. India and China portion to global demand forecast

Source: DBS Bank, Companies

Industry Focus

Thermal Coal Sector

Page 4

Moreover, in Indonesia, the domestic demand as per government's blueprint, alongside Indonesia's 35,000-MW power plant project, is also expanding below the initial target. Indonesia's power plant project, despite appearing promising, faces multiple challenges in reality, such as land acquisition, and limited financing options that offer the combination of long-term tenure and competitive financing cost. We also do not see any significant improvements on the land acquisition stage as most of the project participants have said that it has unlimited risks relating to the land ownership, given the lack of coordination between central and local government, weak law enforcement (mainly on land ownership) and complications on underground execution. Going forward, we see the execution risk remaining intact as we do not see any meaningful progress in the phase one power plant projects (first 12,000 MW roll-out). This is seen in Batang projects, a prolonged delay power plant projects is a joint venture between Adaro Energy, J Power and Itochu, faces land acquisition hurdle in the past three years. The remaining land is only 13 hectares, or 1% of the total land required to build the power plant. Our view on peaked China coal demand in 2014 remain

intact The current level of coal price only accommodates around 40% of global thermal coal output capacity (see chart) which is dominated by Indonesia. This reflects Indonesia's open pit mining characteristics which have a lower cash cost structure relative to underground mines. Big-four coal miners under our coverage, ADRO, PTBA and ITMG, are still posting positive cash margins and earnings so far. Cash cost for global seaborne thermal coal supply (2015)

Source: DBS Vickers

We see further significant supply cut potential as being minimal in 2016; supply cuts will be made only to adjust for the lower demand, not to increase coal price. In this prisoner dilemma circumstances, taking the case study in Indonesia, miners implemented cost-saving strategies via 1) lowering strip ratio resulting in lower equipment workload and hauling distances, lower cash cost, and 2) renegotiating mining contracting rate as contractors like Pamapersada enjoyed margin expansion on strengthening USD trend, and 3) only focus on mines in the most profitable concession. Besides Indonesia, other countries have also successfully lowered their cash costs (see chart) in 2015, and this indicate that global miners are still able to at least maintain their production volume. We believe crude oil price, which dropped by 40% (WTI crude oil price) in the 2015 downtrend, is the key factor of miners' cost changes last year. These dynamics also confirm our thesis that crude oil and coal price correlate from the cost perspective; and lower crude oil price incentivises miners to boost production. Miners' cost changes in 2015

Source: DBS Vickers

Forecast cut on lower production volume, ASP

Lower benchmark price translates into lower ASP Our new coal benchmark price translates into lower ASP. ADRO and ITMG's ASPs were lowered by 5% and 4% to US$48 per ton and US$57 per ton respectively. We assume that PTBA's ASP will drop by only 1% (vs. guidance's flat ASP) as 48% of its sales will be domestic, where the ASP outlook is relatively flat this year. Domestic coal price tend to be better than international price as this is part of the government's energy mix blueprint to support domestic coal miners' business going concern and the coal price itself. We believe amid the current thermal coal price downtrend situation, buyers or traders prefer shorter coal price contracts as they expect lower coal price ahead. However, we expect

Industry Focus

Thermal Coal Sector

Page 5

companies' ASPs relative to Newcastle benchmark price to narrow as buyers try to find better coal pricing by benchmarking other coal price indices. Production volume cut We cut our FY16 and FY17 earnings forecasts for our coal coverage on lower ASP. Moreover, we also cut our PTBA and ADRO coal production by 4% and 4% to 47m ton and 19.8m ton respectively as we believe both companies will need to cut their productions to stay profitable. We further cut ITMG coal production by 15% to 25m ton, as we adjust our coal benchmark price forecast and its ASP and ITMG need to do so in order to stay in healthy margin. Our earnings forecast is in line with our view that Indonesia coal miners will only marginally cut their production given that they have successfully lowered their operational cost mainly on lower fuel cost and mining contracting rate. We are currently 12% below the consensus forecast as we believe consensus has not fully accounted for the low thermal coal price in the next two years, at least, and the implication to companies' financial performance. Overall, our lower production assumption is based on our view that the coal miners have little more room to reduce their costs via lowering their strip ratios. Miners who have successfully

lowered their strip ratios in the last three years, have seen lower cash costs. However, we believe implementing such a strategy in the coming years will put miners' reserves at risk as shorter coal hauling means some of the reserves will not be feasibly mineable in the near future. This lead to our production cut assumption is the best option to miners to maintain profitability and reserves simultaneously. Slightly lower profitability, thanks to production cuts and efficiencies Our new forecast implies a slight profitability contraction as production cuts, focus on the most profitable concession and continuous efficiencies will limit the negative impact on the lower ASP assumption. On the other hand, we believe the low crude oil price does not fully translate into steeply lower cash cost per ton as a steep drop in crude oil price does not translate into lower national industrial fuel price and coal production cost. We estimate the industrial fuel price to drop around 15% this year, translating into 5% lower cash cost per ton in FY16 (30% of fuel cost component assumption). On the mining contracting rate, we believe there will only be a minimal cut mainly for large coal companies such as ADRO and PTBA, thanks to their bargaining power.

Industry Focus

Thermal Coal Sector

Page 6

ITMG earnings revision summary

2015F 2016F 2017F

Old New Changes Old New Changes Old New Chang

es Revenue (US$mn) 1,672 1,672 0% 1,752 1,393 -21% 1,657 1,117 -33% Gross profit (US$mn) 317 317 0% 290 224 -23% 254 177 -30% EBITDA (US$mn) 230 230 0% 198 163 -18% 172 146 -15% Net profit (US$mn) 144 144 0% 120 94 -22% 99 80 -19%

Production volume (mn ton) 27.5 27.5 0% 29.5 25.0 -15% 30 23.0 -22% ASP (US$ per ton) 60.9 60.9 0% 59.5 56.6 -5% 57 49.5 -14% Cash cost per ton (US$/ton) 39.09 39.09 0% 39.6 36.9 -7% 38 31.76 -16%

Source : Company, DBS Vickers ADRO earnings revision summary

2015F 2016F 2017F

Old New Changes Old New Changes Old New Changes Revenue (US$mn) 2,820 2,820 0% 2,666 2,423 -9% 2666 2,191 -18% Gross profit (US$mn) 618 618 0% 594 538 -10% 603 461 -24% EBITDA (US$mn) 605 605 0% 565 528 -7% 578 474 -18% Net profit (US$mn) 196 196 0% 173 154 -11% 178 126 -29%

Production volume (mn ton) 52.5 52.5 0% 49.0 47.0 -4% 46.5 44.5 -4% ASP (US$ per ton) 50.8 50.8 0% 51.0 48.0 -6% 53.5 45.2 -15%

Source : Company, DBS Vickers PTBA earnings revision summary

2015F 2016F 2017F

Old New Changes Old New Changes Old New Changes Revenue (US$mn) 14,276 14,276 0% 14,276 13,998 -2% 14790.6 13,998 -5% Gross profit (US$mn) 3,802 3,802 0% 3,924 2,816 -28% 3869.5 3,192 -18% EBITDA (US$mn) 2,382 2,382 0% 2,469 1,728 -30% 2317.4 2,045 -12% Net profit (US$mn) 1,848 1,848 0% 1,917 1,363 -29% 1835.0 1,631 -11%

Production volume (mn ton) 22.0 18.5 -16% 20.5 19.8 -4% 22.8 21.8 -4% ASP (US$ per ton) 716.0 716.0 0% 692.0 684.4 -1% 689 679.0 -1% Cash cost per ton (US$/ton) 632.00 632.00 0% 625.00 607.00 -3% 620 607.00 -2% Source : Company, DBS Vickers

HRUM earnings revision summary

2015F 2016F 2017F

Old New Changes Old New Changes Old New Changes Revenue (US$mn) 285 285 0% 228 183 -20% 228 183 -20% Gross profit (US$mn) 50 65 30% 37 27 -28% 32 26 -20% EBITDA (US$mn) 19 34 77% 20 16 -22% 22 21 -8% Net profit (US$mn) 6 15 165% 10 7 -29% 11 10 -11%

Production volume (mn ton) 5.0 5.0 0% 4.0 3.5 -13% 4 3.5 -13% ASP (US$ per ton) 57.0 57.0 0% 57.0 52.3 -8% 57.0 52.3 -8% Op. cash cost per ton (US$/ton) 36.00 36.00 0% 36.00 34.00 -6% 36 34.15 -5% Source : Company, DBS Vickers

Industry Focus

Thermal Coal Sector

Page 7

Valuation: De-rating reflects structural changes in the

sector What happened in 2015 Coal stock price dropped by 55% on average last year. We believe the combination of weak quarterly financial results and weak outlook on overall commodity price performance in 2015. We see the stock price correction as a sign of stock valuation de-rating on the structural changes in the coal sector, instead of cyclical stock price correction. This also reflects market awareness that the commodity stocks, particularly coal mining stocks, will suffer another painful year. Coal stocks performance in 2015

‐50%

‐64%‐60%

‐39%

‐70%

‐60%

‐50%

‐40%

‐30%

‐20%

‐10%

0%

ADRO PTBA ITMG Jakmine Index

Series1

Source: DBS Vickers We also do not see the recent share price correction as an opportunity to buy coal mining stocks as we see no positive catalysts for the next twelve months. Miners have not published their 2016 operational guidance but majorly clued 'difficult' year will still persist. Moreover, after our earnings forecast update, inputting the lower ASP and the implication on overall mining activities, coal stock valuation do not show major discount as good entry point, in our view. Currently coal stocks are trading at their historical low PE multiple (see chart, -2SD), but we see this as fair. Historical multiple is not an appropriate comparison, in our view, given the different circumstances the coal miners face today vs. five years ago. Current coal price is also 40% lower than its five-year average level and there are implications on the coal miners operational and earnings performance, which we believe should be translated into their stock valuation and performance. As such, we do not see stock price reaching double-digit multiples unless coal price at least recover to above US$67 per ton level, or to our prior thermal coal forecast.

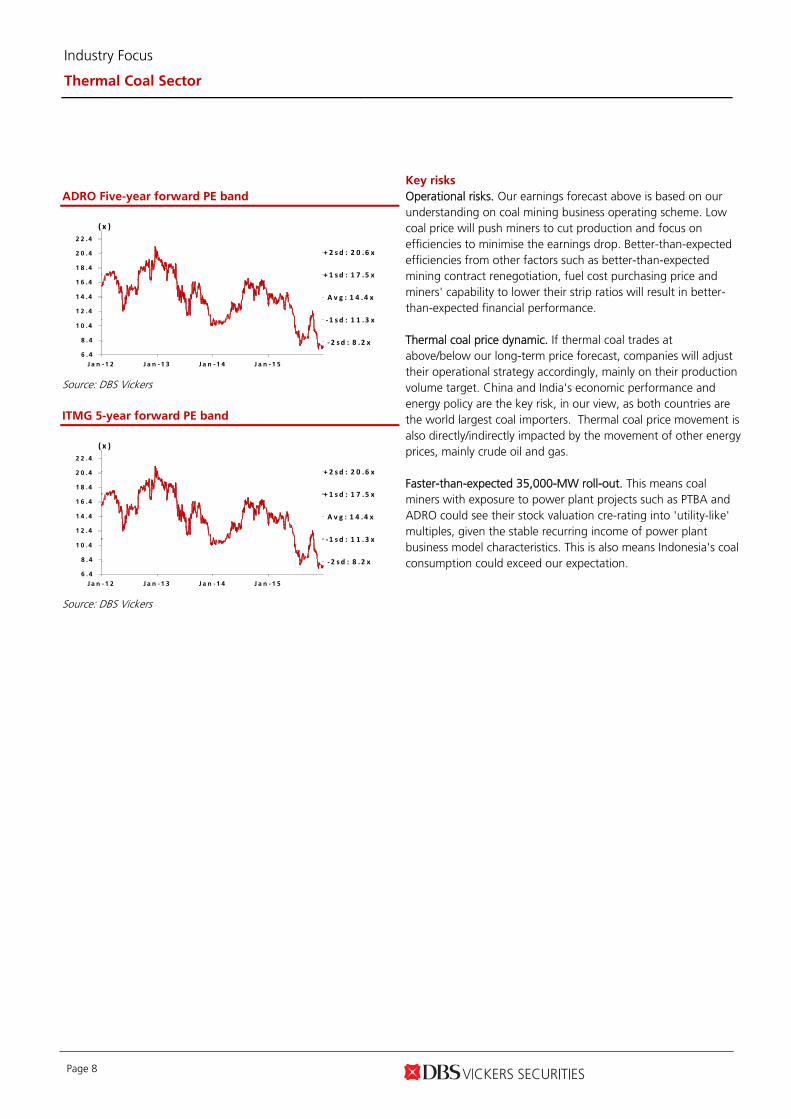

What we think in 2016 In the next twelve months, power plant catalyst is not a strong angle to push coal stocks in our view, as it will be more about multi-year construction and operational refinement before it will be truly profitable and coal stocks could be re-rated as utility company. HRUM remain our Fully Valued call for Indonesia coal sector since we believe it will be the worst impacted coal miners if the coal price to stay low at current level. We do not have HRUM historical PE band since HRUM was on negative earnings in FY14. ITMG looks quite attractive at this point as it dividend yield has reach double digits of 12%. However, we are concerned about ITMG's capability to pursue its dividend payment consistently. We do not doubt management's shareholder return policy, but are instead worried about how ITMG manage its profitability and production amid its depleting coal reserves simultaneously. On ADRO, we like its low cash cost structure (operational and financial cost) and initiative on power plant projects. However, on the other hand, we believe ADRO is not immune to production cuts in order to stay profitable in the next two years. Moreover, we see weak earnings momentum to still persist in the next two years. PTBA's overall performance is good and its mine mouth power plant project means PTBA is not exposed to the land acquisition issue like what other power plant players face nowadays. However, we believe PTBA will achieve lower-than-targeted production and sales volume if efficiencies remain the management's focus. PTBA Five-year forward PE band

A v g : 1 4 .4 x

+ 1 s d : 1 7 .5 x

+ 2 s d : 2 0 .6 x

‐1 s d : 1 1 .3 x

‐2 s d : 8 .2 x

6 . 4

8 . 4

1 0 .4

1 2 .4

1 4 .4

1 6 .4

1 8 .4

2 0 .4

2 2 .4

J a n -1 2 J a n -1 3 J a n -1 4 J a n -1 5

( x )

Source: DBS Vickers

Industry Focus

Thermal Coal Sector

Page 8

ADRO Five-year forward PE band

A v g : 1 4 .4 x

+ 1 s d : 1 7 .5 x

+ 2 s d : 2 0 .6 x

‐1 s d : 1 1 .3 x

‐2 sd : 8 .2 x

6 . 4

8 . 4

1 0 .4

1 2 .4

1 4 .4

1 6 .4

1 8 .4

2 0 .4

2 2 .4

J a n -1 2 J a n -1 3 J a n -1 4 J a n -1 5

( x )

Source: DBS Vickers

ITMG 5-year forward PE band

A v g : 1 4 .4 x

+ 1 s d : 1 7 .5 x

+ 2 s d : 2 0 .6 x

‐1 s d : 1 1 .3 x

‐2 sd : 8 .2 x

6 . 4

8 . 4

1 0 .4

1 2 .4

1 4 .4

1 6 .4

1 8 .4

2 0 .4

2 2 .4

J a n -1 2 J a n -1 3 J a n -1 4 J a n -1 5

( x )

Source: DBS Vickers

Key risks Operational risks. Our earnings forecast above is based on our understanding on coal mining business operating scheme. Low coal price will push miners to cut production and focus on efficiencies to minimise the earnings drop. Better-than-expected efficiencies from other factors such as better-than-expected mining contract renegotiation, fuel cost purchasing price and miners' capability to lower their strip ratios will result in better-than-expected financial performance. Thermal coal price dynamic. If thermal coal trades at above/below our long-term price forecast, companies will adjust their operational strategy accordingly, mainly on their production volume target. China and India's economic performance and energy policy are the key risk, in our view, as both countries are the world largest coal importers. Thermal coal price movement is also directly/indirectly impacted by the movement of other energy prices, mainly crude oil and gas. Faster-than-expected 35,000-MW roll-out. This means coal miners with exposure to power plant projects such as PTBA and ADRO could see their stock valuation cre-rating into 'utility-like' multiples, given the stable recurring income of power plant business model characteristics. This is also means Indonesia's coal consumption could exceed our expectation.

Industry Focus

Thermal Coal Sector

Page 9

Company Guides

ASIAN INSIGHTS VICKERS SECURITIES ed: TH / sa: MA

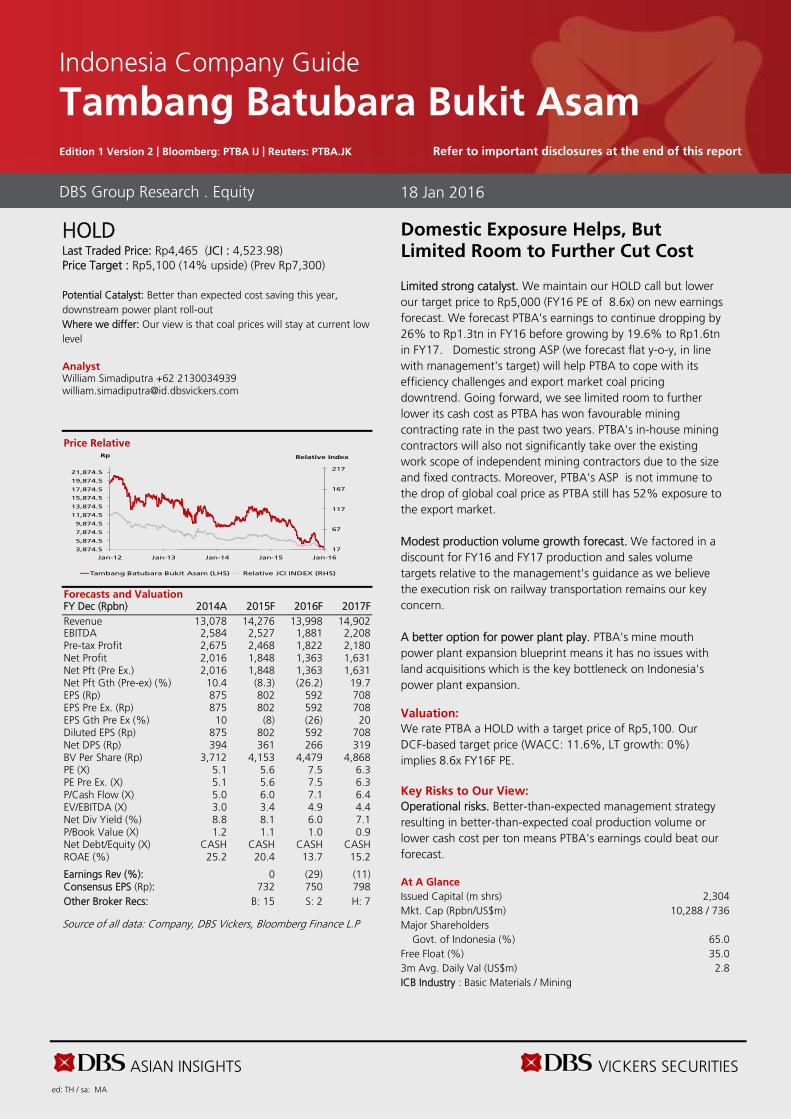

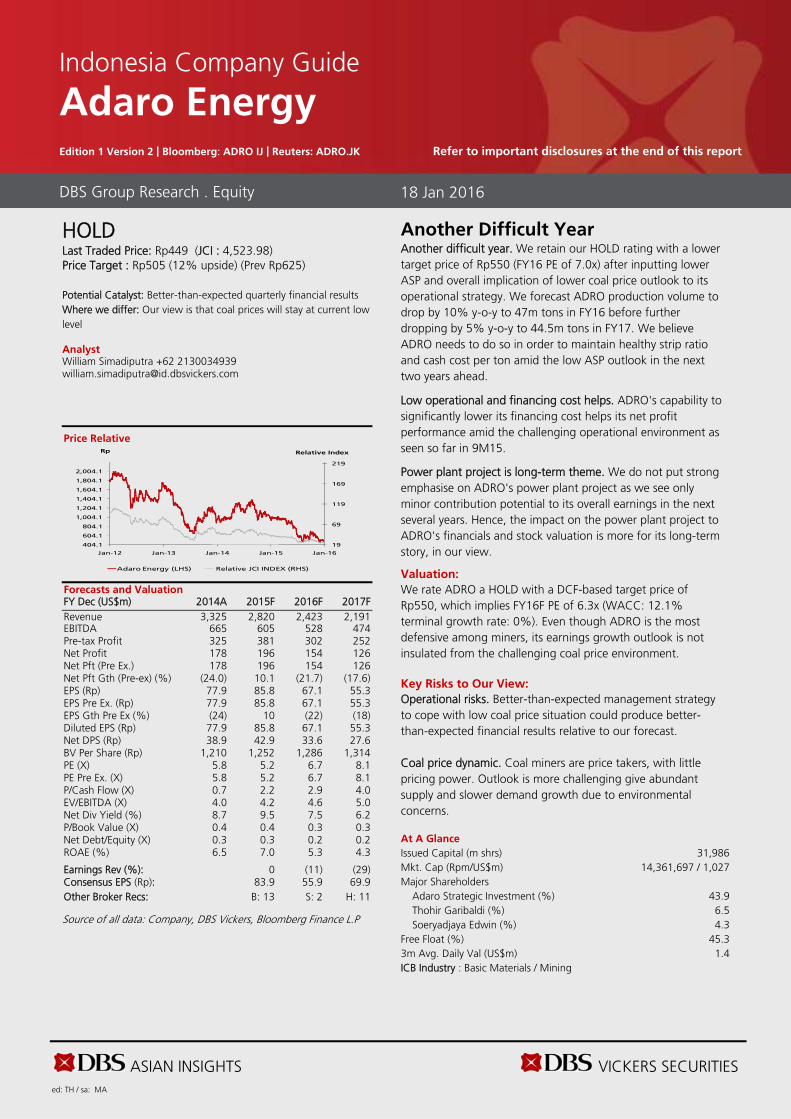

HOLD Last Traded Price: Rp4,465 (JCI : 4,523.98) Price Target : Rp5,100 (14% upside) (Prev Rp7,300) Potential Catalyst: Better than expected cost saving this year, downstream power plant roll-out Where we differ: Our view is that coal prices will stay at current low level

Analyst William Simadiputra +62 2130034939 [email protected]

Price Relative

Forecasts and Valuation FY Dec (Rpbn) 2014A 2015F 2016F 2017F Revenue 13,078 14,276 13,998 14,902 EBITDA 2,584 2,527 1,881 2,208 Pre-tax Profit 2,675 2,468 1,822 2,180 Net Profit 2,016 1,848 1,363 1,631 Net Pft (Pre Ex.) 2,016 1,848 1,363 1,631 Net Pft Gth (Pre-ex) (%) 10.4 (8.3) (26.2) 19.7 EPS (Rp) 875 802 592 708 EPS Pre Ex. (Rp) 875 802 592 708 EPS Gth Pre Ex (%) 10 (8) (26) 20 Diluted EPS (Rp) 875 802 592 708 Net DPS (Rp) 394 361 266 319 BV Per Share (Rp) 3,712 4,153 4,479 4,868 PE (X) 5.1 5.6 7.5 6.3 PE Pre Ex. (X) 5.1 5.6 7.5 6.3 P/Cash Flow (X) 5.0 6.0 7.1 6.4 EV/EBITDA (X) 3.0 3.4 4.9 4.4 Net Div Yield (%) 8.8 8.1 6.0 7.1 P/Book Value (X) 1.2 1.1 1.0 0.9 Net Debt/Equity (X) CASH CASH CASH CASH ROAE (%) 25.2 20.4 13.7 15.2 Earnings Rev (%): 0 (29) (11) Consensus EPS (Rp): 732 750 798 Other Broker Recs: B: 15 S: 2 H: 7

Source of all data: Company, DBS Vickers, Bloomberg Finance L.P

Domestic Exposure Helps, But Limited Room to Further Cut Cost Limited strong catalyst. We maintain our HOLD call but lower our target price to Rp5,000 (FY16 PE of 8.6x) on new earnings forecast. We forecast PTBA's earnings to continue dropping by 26% to Rp1.3tn in FY16 before growing by 19.6% to Rp1.6tn in FY17. Domestic strong ASP (we forecast flat y-o-y, in line with management's target) will help PTBA to cope with its efficiency challenges and export market coal pricing downtrend. Going forward, we see limited room to further lower its cash cost as PTBA has won favourable mining contracting rate in the past two years. PTBA's in-house mining contractors will also not significantly take over the existing work scope of independent mining contractors due to the size and fixed contracts. Moreover, PTBA's ASP is not immune to the drop of global coal price as PTBA still has 52% exposure to the export market. Modest production volume growth forecast. We factored in a discount for FY16 and FY17 production and sales volume targets relative to the management's guidance as we believe the execution risk on railway transportation remains our key concern. A better option for power plant play. PTBA's mine mouth power plant expansion blueprint means it has no issues with land acquisitions which is the key bottleneck on Indonesia's power plant expansion. Valuation:

We rate PTBA a HOLD with a target price of Rp5,100. Our DCF-based target price (WACC: 11.6%, LT growth: 0%) implies 8.6x FY16F PE. Key Risks to Our View:

Operational risks. Better-than-expected management strategy resulting in better-than-expected coal production volume or lower cash cost per ton means PTBA's earnings could beat our forecast. At A Glance Issued Capital (m shrs) 2,304 Mkt. Cap (Rpbn/US$m) 10,288 / 736 Major Shareholders Govt. of Indonesia (%) 65.0 Free Float (%) 35.0 3m Avg. Daily Val (US$m) 2.8 ICB Industry : Basic Materials / Mining

DBS Group Research . Equity 18 Jan 2016

Indonesia Company Guide

Tambang Batubara Bukit Asam Edition 1 Version 2 | Bloomberg: PTBA IJ | Reuters: PTBA.JK Refer to important disclosures at the end of this report

17

67

117

167

217

3,874.5

5,874.5

7,874.5

9,874.5

11,874.5

13,874.5

15,874.5

17,874.5

19,874.5

21,874.5

Jan-12 Jan-13 Jan-14 Jan-15 Jan-16

Relative IndexRp

Tambang Batubara Bukit Asam (LHS) Relative JCI INDEX (RHS)

ASIAN INSIGHTS VICKERS SECURITIES Page 11

Company Guide

Tambang Batubara Bukit Asam

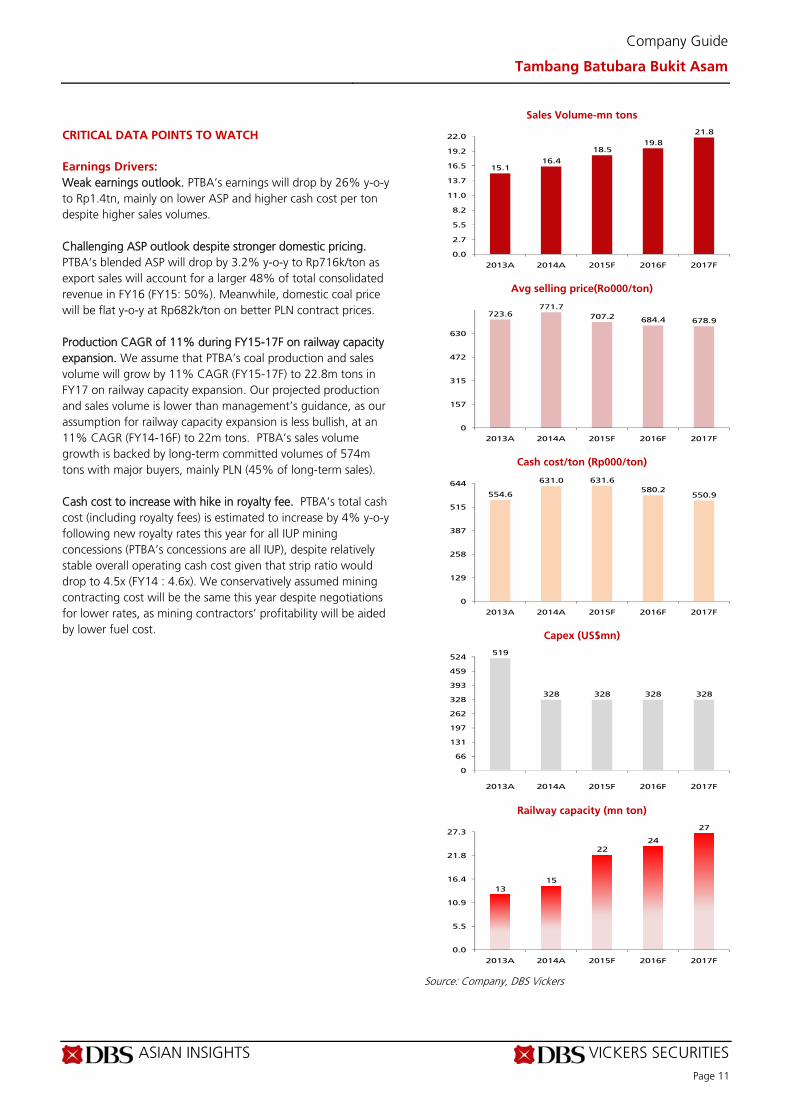

CRITICAL DATA POINTS TO WATCH

Earnings Drivers:

Weak earnings outlook. PTBA’s earnings will drop by 26% y-o-y to Rp1.4tn, mainly on lower ASP and higher cash cost per ton despite higher sales volumes. Challenging ASP outlook despite stronger domestic pricing. PTBA’s blended ASP will drop by 3.2% y-o-y to Rp716k/ton as export sales will account for a larger 48% of total consolidated revenue in FY16 (FY15: 50%). Meanwhile, domestic coal price will be flat y-o-y at Rp682k/ton on better PLN contract prices. Production CAGR of 11% during FY15-17F on railway capacity expansion. We assume that PTBA’s coal production and sales volume will grow by 11% CAGR (FY15-17F) to 22.8m tons in FY17 on railway capacity expansion. Our projected production and sales volume is lower than management’s guidance, as our assumption for railway capacity expansion is less bullish, at an 11% CAGR (FY14-16F) to 22m tons. PTBA’s sales volume growth is backed by long-term committed volumes of 574m tons with major buyers, mainly PLN (45% of long-term sales). Cash cost to increase with hike in royalty fee. PTBA’s total cash cost (including royalty fees) is estimated to increase by 4% y-o-y following new royalty rates this year for all IUP mining concessions (PTBA’s concessions are all IUP), despite relatively stable overall operating cash cost given that strip ratio would drop to 4.5x (FY14 : 4.6x). We conservatively assumed mining contracting cost will be the same this year despite negotiations for lower rates, as mining contractors’ profitability will be aided by lower fuel cost.

Sales Volume-mn tons

Avg selling price(Ro000/ton)

Cash cost/ton (Rp000/ton)

Capex (US$mn)

Railway capacity (mn ton)

Source: Company, DBS Vickers

15.116.4

18.519.8

21.8

0.0

2.7

5.5

8.2

11.0

13.7

16.5

19.2

22.0

2013A 2014A 2015F 2016F 2017F

723.6771.7

707.2 684.4 678.9

0

157

315

472

630

2013A 2014A 2015F 2016F 2017F

554.6

631.0 631.6

580.2550.9

0

129

258

387

515

644

2013A 2014A 2015F 2016F 2017F

519

328 328 328 328

0

66

131

197

262

328

393

459

524

2013A 2014A 2015F 2016F 2017F

1315

2224

27

0.0

5.5

10.9

16.4

21.8

27.3

2013A 2014A 2015F 2016F 2017F

ASIAN INSIGHTS VICKERS SECURITIES Page 12

Company Guide

Tambang Batubara Bukit Asam

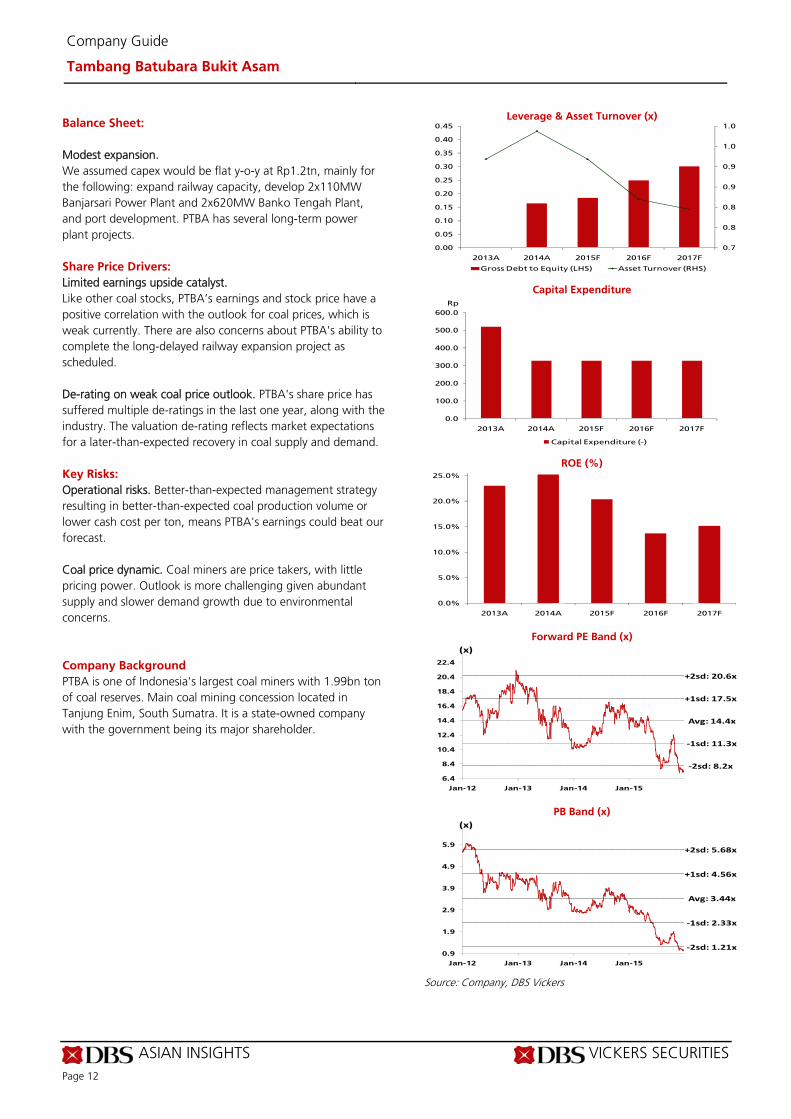

Balance Sheet:

Modest expansion. We assumed capex would be flat y-o-y at Rp1.2tn, mainly for the following: expand railway capacity, develop 2x110MW Banjarsari Power Plant and 2x620MW Banko Tengah Plant, and port development. PTBA has several long-term power plant projects.

Share Price Drivers:

Limited earnings upside catalyst. Like other coal stocks, PTBA’s earnings and stock price have a positive correlation with the outlook for coal prices, which is weak currently. There are also concerns about PTBA's ability to complete the long-delayed railway expansion project as scheduled. De-rating on weak coal price outlook. PTBA's share price has suffered multiple de-ratings in the last one year, along with the industry. The valuation de-rating reflects market expectations for a later-than-expected recovery in coal supply and demand.

Key Risks:

Operational risks. Better-than-expected management strategy resulting in better-than-expected coal production volume or lower cash cost per ton, means PTBA's earnings could beat our forecast. Coal price dynamic. Coal miners are price takers, with little pricing power. Outlook is more challenging given abundant supply and slower demand growth due to environmental concerns.

Company Background

PTBA is one of Indonesia's largest coal miners with 1.99bn ton of coal reserves. Main coal mining concession located in Tanjung Enim, South Sumatra. It is a state-owned company with the government being its major shareholder.

Leverage & Asset Turnover (x)

Capital Expenditure

ROE (%)

Forward PE Band (x)

PB Band (x)

Source: Company, DBS Vickers

0.7

0.8

0.8

0.9

0.9

1.0

1.0

0.00

0.05

0.10

0.15

0.20

0.25

0.30

0.35

0.40

0.45

2013A 2014A 2015F 2016F 2017F

Gross Debt to Equity (LHS) Asset Turnover (RHS)

0.0

100.0

200.0

300.0

400.0

500.0

600.0

2013A 2014A 2015F 2016F 2017F

Capital Expenditure (-)

Rp

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

2013A 2014A 2015F 2016F 2017F

Avg: 14.4x

+1sd: 17.5x

+2sd: 20.6x

‐1sd: 11.3x

‐2sd: 8.2x

6.4

8.4

10.4

12.4

14.4

16.4

18.4

20.4

22.4

Jan-12 Jan-13 Jan-14 Jan-15

(x)

Avg: 3.44x

+1sd: 4.56x

+2sd: 5.68x

‐1sd: 2.33x

‐2sd: 1.21x0.9

1.9

2.9

3.9

4.9

5.9

Jan-12 Jan-13 Jan-14 Jan-15

(x)

ASIAN INSIGHTS VICKERS SECURITIES Page 13

Company Guide

Tambang Batubara Bukit Asam

Key Assumptions

FY Dec 2013A 2014A 2015F 2016F 2017F Sales Volume-mn tons 15.1 16.4 18.5 19.8 21.8 Avg selling 724 772 707 684 679 Cash cost/ton (Rp000/ton) 555 631 632 580 551 Capex (US$mn) 519 328 328 328 328 Railway capacity (mn ton) 12.8 14.8 22.0 24.0 27.0

Income Statement (Rpbn)

FY Dec 2013A 2014A 2015F 2016F 2017F Revenue 11,209 13,078 14,276 13,998 14,902 Cost of Goods Sold (7,746) (9,056) (10,474) (11,182) (11,710) Gross Profit 3,464 4,022 3,802 2,816 3,192 Other Opng (Exp)/Inc (1,311) (1,712) (1,570) (1,260) (1,341) Operating Profit 2,153 2,310 2,231 1,556 1,851 Other Non Opg (Exp)/Inc 0.0 0.0 0.0 0.0 0.0 Associates & JV Inc 74.9 146 146 153 163 Net Interest (Exp)/Inc 234 219 91.3 113 166 Exceptional Gain/(Loss) 0.0 0.0 0.0 0.0 0.0 Pre-tax Profit 2,461 2,675 2,468 1,822 2,180 Tax (607) (656) (617) (455) (545) Minority Interest (28.1) (3.0) (3.3) (3.3) (3.5) Preference Dividend 0.0 0.0 0.0 0.0 0.0 Net Profit 1,826 2,016 1,848 1,363 1,631 Net Profit before Except. 1,826 2,016 1,848 1,363 1,631 EBITDA 2,322 2,584 2,527 1,881 2,208 Growth Revenue Gth (%) (3.3) 16.7 9.2 (1.9) 6.5 EBITDA Gth (%) (36.5) 11.3 (2.2) (25.6) 17.4 Opg Profit Gth (%) (40.1) 7.3 (3.4) (30.3) 18.9 Net Profit Gth (Pre-ex) (%) (37.0) 10.4 (8.3) (26.2) 19.7 Margins & Ratio Gross Margins (%) 30.9 30.8 26.6 20.1 21.4 Opg Profit Margin (%) 19.2 17.7 15.6 11.1 12.4 Net Profit Margin (%) 16.3 15.4 12.9 9.7 10.9 ROAE (%) 23.0 25.2 20.4 13.7 15.2 ROA (%) 15.0 15.2 11.9 8.0 8.7 ROCE (%) 15.9 16.5 13.5 8.4 9.0 Div Payout Ratio (%) 45.0 45.0 45.0 45.0 45.0 Net Interest Cover (x) NM NM NM NM NM

Source: Company, DBS Vickers

Downtrend in ASP trend on export sales ASP drag, despite solid domestic coal pricing

ASIAN INSIGHTS VICKERS SECURITIES Page 14

Company Guide

Tambang Batubara Bukit Asam

Quarterly / Interim Income Statement (Rpbn)

FY Dec 3Q2014 4Q2014 1Q2015 2Q2015 3Q2015 Revenue 3,229 3,422 3,277 3,235 3,990 Cost of Goods Sold (2,277) (2,467) (2,506) (2,292) (2,740) Gross Profit 952 955 771 942 1,250 Other Oper. (Exp)/Inc (179) (217) (226) (114) (145) Operating Profit 458 459 359 534 905 Net Interest (Exp)/Inc (7.9) (35.6) (29.7) (31.6) (65.3) Exceptional Gain/(Loss) 0.0 0.0 0.0 0.0 0.0 Pre-tax Profit 556 530 463 636 952 Tax (129) (103) (122) (182) (242) Minority Interest (0.8) 7.40 (0.1) 0.38 0.82 Net Profit 426 434 341 455 710 Net profit bef Except. 426 434 341 455 710 EBITDA 402 663 0.0 0.0 0.0 Growth Revenue Gth (%) (3.1) 6.0 (4.2) (1.3) 23.4 EBITDA Gth (%) (48.2) 65.0 nm nm nm Opg Profit Gth (%) (37.0) 0.2 (21.7) 48.6 69.5 Net Profit Gth (Pre-ex) (%) (31.3) 1.9 (21.6) 33.5 56.3 Margins Gross Margins (%) 29.5 27.9 23.5 29.1 31.3 Opg Profit Margins (%) 14.2 13.4 11.0 16.5 22.7 Net Profit Margins (%) 13.2 12.7 10.4 14.1 17.8

Balance Sheet (Rpbn)

FY Dec 2013A 2014A 2015F 2016F 2017F Net Fixed Assets 2,803 3,988 4,165 4,320 4,453 Invts in Associates & JVs 0.0 0.0 0.0 0.0 0.0 Other LT Assets 2,394 3,408 4,733 5,966 7,200 Cash & ST Invts 3,344 4,039 3,706 3,870 4,081 Inventory 902 1,033 1,195 1,276 1,336 Debtors 1,428 1,439 1,571 1,541 1,640 Other Current Assets 806 905 905 905 905 Total Assets 11,677 14,812 16,276 17,877 19,616 ST Debt 0.0 467 0.0 0.0 0.0 Creditor 472 546 631 674 705 Other Current Liab 1,789 2,561 2,561 2,561 2,561 LT Debt 0.0 962 1,791 2,600 3,409 Other LT Liabilities 1,865 1,605 1,605 1,605 1,605 Shareholder’s Equity 7,437 8,554 9,570 10,320 11,217 Minority Interests 114 117 117 117 117 Total Cap. & Liab. 11,677 14,812 16,276 17,877 19,616 Non-Cash Wkg. Capital 875 271 479 486 614 Net Cash/(Debt) 3,344 2,610 1,916 1,270 671 Debtors Turn (avg days) 48.4 40.0 38.5 40.6 39.0 Creditors Turn (avg days) 14.8 20.8 20.8 21.6 21.9 Inventory Turn (avg days) 39.8 39.6 39.4 41.0 41.4 Asset Turnover (x) 0.9 1.0 0.9 0.8 0.8 Current Ratio (x) 2.9 2.1 2.3 2.3 2.4 Quick Ratio (x) 2.1 1.5 1.7 1.7 1.8 Net Debt/Equity (X) CASH CASH CASH CASH CASH Net Debt/Equity ex MI (X) CASH CASH CASH CASH CASH Capex to Debt (%) N/A 22.9 18.3 12.6 9.6 Z-Score (X) 4.7 3.8 3.6 3.4 3.2

Source: Company, DBS Vickers

9M15 results showed PTBA's successful efficiency effort mainly on lower mining contracting rate

ASIAN INSIGHTS VICKERS SECURITIES Page 15

Company Guide

Tambang Batubara Bukit Asam

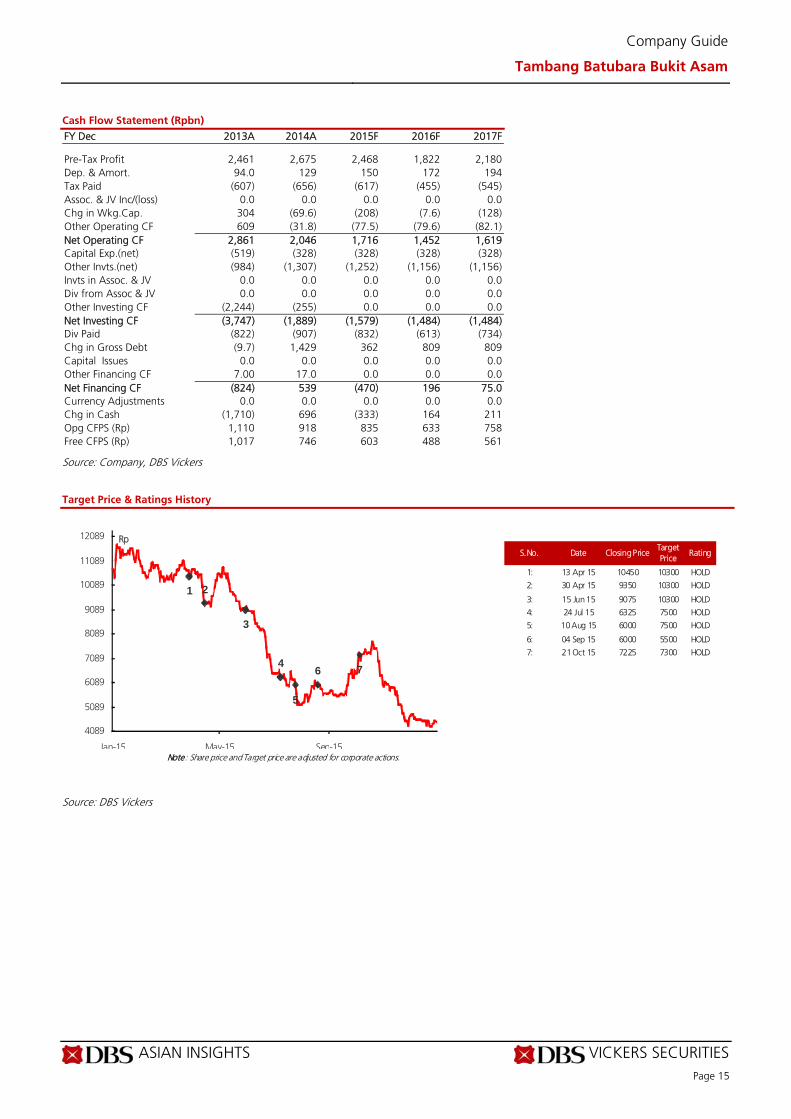

Cash Flow Statement (Rpbn)

FY Dec 2013A 2014A 2015F 2016F 2017F Pre-Tax Profit 2,461 2,675 2,468 1,822 2,180 Dep. & Amort. 94.0 129 150 172 194 Tax Paid (607) (656) (617) (455) (545) Assoc. & JV Inc/(loss) 0.0 0.0 0.0 0.0 0.0 Chg in Wkg.Cap. 304 (69.6) (208) (7.6) (128) Other Operating CF 609 (31.8) (77.5) (79.6) (82.1) Net Operating CF 2,861 2,046 1,716 1,452 1,619 Capital Exp.(net) (519) (328) (328) (328) (328) Other Invts.(net) (984) (1,307) (1,252) (1,156) (1,156) Invts in Assoc. & JV 0.0 0.0 0.0 0.0 0.0 Div from Assoc & JV 0.0 0.0 0.0 0.0 0.0 Other Investing CF (2,244) (255) 0.0 0.0 0.0 Net Investing CF (3,747) (1,889) (1,579) (1,484) (1,484) Div Paid (822) (907) (832) (613) (734) Chg in Gross Debt (9.7) 1,429 362 809 809 Capital Issues 0.0 0.0 0.0 0.0 0.0 Other Financing CF 7.00 17.0 0.0 0.0 0.0 Net Financing CF (824) 539 (470) 196 75.0 Currency Adjustments 0.0 0.0 0.0 0.0 0.0 Chg in Cash (1,710) 696 (333) 164 211 Opg CFPS (Rp) 1,110 918 835 633 758 Free CFPS (Rp) 1,017 746 603 488 561

Source: Company, DBS Vickers

Target Price & Ratings History

Source: DBS Vickers

S.No. Date Closing PriceTarget Price

Rating

1: 13 Apr 15 10450 10300 HOLD

2: 30 Apr 15 9350 10300 HOLD

3: 15 Jun 15 9075 10300 HOLD

4: 24 Jul 15 6325 7500 HOLD

5: 10 Aug 15 6000 7500 HOLD

6: 04 Sep 15 6000 5500 HOLD

7: 21 Oct 15 7225 7300 HOLD

Note: Share price and Target price are adjusted for corporate actions.

1 2

3

4

5

6 7

4089

5089

6089

7089

8089

9089

10089

11089

12089

Jan-15 May-15 Sep-15

Rp

ASIAN INSIGHTS VICKERS SECURITIES ed: TH / sa: MA

HOLD Last Traded Price: Rp449 (JCI : 4,523.98) Price Target : Rp505 (12% upside) (Prev Rp625) Potential Catalyst: Better-than-expected quarterly financial results Where we differ: Our view is that coal prices will stay at current low level Analyst William Simadiputra +62 2130034939 [email protected]

Price Relative

Forecasts and Valuation FY Dec (US$m) 2014A 2015F 2016F 2017F Revenue 3,325 2,820 2,423 2,191 EBITDA 665 605 528 474 Pre-tax Profit 325 381 302 252 Net Profit 178 196 154 126 Net Pft (Pre Ex.) 178 196 154 126 Net Pft Gth (Pre-ex) (%) (24.0) 10.1 (21.7) (17.6) EPS (Rp) 77.9 85.8 67.1 55.3 EPS Pre Ex. (Rp) 77.9 85.8 67.1 55.3 EPS Gth Pre Ex (%) (24) 10 (22) (18) Diluted EPS (Rp) 77.9 85.8 67.1 55.3 Net DPS (Rp) 38.9 42.9 33.6 27.6 BV Per Share (Rp) 1,210 1,252 1,286 1,314 PE (X) 5.8 5.2 6.7 8.1 PE Pre Ex. (X) 5.8 5.2 6.7 8.1 P/Cash Flow (X) 0.7 2.2 2.9 4.0 EV/EBITDA (X) 4.0 4.2 4.6 5.0 Net Div Yield (%) 8.7 9.5 7.5 6.2 P/Book Value (X) 0.4 0.4 0.3 0.3 Net Debt/Equity (X) 0.3 0.3 0.2 0.2 ROAE (%) 6.5 7.0 5.3 4.3 Earnings Rev (%): 0 (11) (29) Consensus EPS (Rp): 83.9 55.9 69.9 Other Broker Recs: B: 13 S: 2 H: 11

Source of all data: Company, DBS Vickers, Bloomberg Finance L.P

Another Difficult Year Another difficult year. We retain our HOLD rating with a lower target price of Rp550 (FY16 PE of 7.0x) after inputting lower ASP and overall implication of lower coal price outlook to its operational strategy. We forecast ADRO production volume to drop by 10% y-o-y to 47m tons in FY16 before further dropping by 5% y-o-y to 44.5m tons in FY17. We believe ADRO needs to do so in order to maintain healthy strip ratio and cash cost per ton amid the low ASP outlook in the next two years ahead.

Low operational and financing cost helps. ADRO's capability to significantly lower its financing cost helps its net profit performance amid the challenging operational environment as seen so far in 9M15.

Power plant project is long-term theme. We do not put strong emphasise on ADRO's power plant project as we see only minor contribution potential to its overall earnings in the next several years. Hence, the impact on the power plant project to ADRO's financials and stock valuation is more for its long-term story, in our view.

Valuation:

We rate ADRO a HOLD with a DCF-based target price of Rp550, which implies FY16F PE of 6.3x (WACC: 12.1% terminal growth rate: 0%). Even though ADRO is the most defensive among miners, its earnings growth outlook is not insulated from the challenging coal price environment. Key Risks to Our View:

Operational risks. Better-than-expected management strategy to cope with low coal price situation could produce better-than-expected financial results relative to our forecast. Coal price dynamic. Coal miners are price takers, with little pricing power. Outlook is more challenging give abundant supply and slower demand growth due to environmental concerns. At A Glance Issued Capital (m shrs) 31,986 Mkt. Cap (Rpm/US$m) 14,361,697 / 1,027 Major Shareholders Adaro Strategic Investment (%) 43.9 Thohir Garibaldi (%) 6.5 Soeryadjaya Edwin (%) 4.3 Free Float (%) 45.3 3m Avg. Daily Val (US$m) 1.4 ICB Industry : Basic Materials / Mining

DBS Group Research . Equity 18 Jan 2016

Indonesia Company Guide

Adaro Energy Edition 1 Version 2 | Bloomberg: ADRO IJ | Reuters: ADRO.JK Refer to important disclosures at the end of this report

19

69

119

169

219

404.1

604.1

804.1

1,004.1

1,204.1

1,404.1

1,604.1

1,804.1

2,004.1

Jan-12 Jan-13 Jan-14 Jan-15 Jan-16

Relative IndexRp

Adaro Energy (LHS) Relative JCI INDEX (RHS)

ASIAN INSIGHTS VICKERS SECURITIES Page 17

Company Guide

Adaro Energy

CRITICAL DATA POINTS TO WATCH

Earnings Drivers:

Production volume downtrend in the next two years. We assumed coal output would drop by 10% y-o-y to 47m tons in FY16 before further dropping by 5% y-o-y to 44m tons in FY17 premised on cuts at all of ADRO’s mining concessions. Tutupan and Paringin concessions will remain the largest contributor (46m tons) at 98% of ADRO's coal production. Coal pricing outlook is challenging. ADRO is not immune to the challenging coal price environment. We forecast ASP to drop to US$48/ton and US$45.2/ton in FY16 and FY17 respectively. ADRO might try to offset some of the impact by (again) switching its pricing benchmark from Newcastle to another index, but that has not helped to raise ASP so far. Lower cash cost on better operational efficiency. We assumed a slightly lower cash cost of US$37.4/ton and US$35.8/ton in FY16 and FY17 respectively, as we conservatively input lower mining contracting rates. We have factored in lower fuel cost in our cash cost estimate. ADRO’s cost saving measures would help to boost its earnings amid the challenging coal price and flat sales volume outlook. Lower fuel cost will also help ADRO to lower cash cost per ton. We assume ADRO’s fuel cost US$0.5 per litre in our forecast, half of its 5-year average. Low financing cost to help ADRO sustain positive net profit going forward. ADRO will also continue to reduce borrowing costs via refinancing. ADRO significantly reduced its financing cost in FY15 (almost dropped by 80% y-o-y). ADRO's access to competitive financing terms bodes well for the company; it recently refinanced its existing debt with Adaro Indonesia’s US$1bn loan facility at a lower borrowing cost.

Sales volume (m tons)

ASP (US$/ton)

Cash cost/ ton (US$/ton)

EBITDA margin (%)

Interest expenses (US$mn)

Source: Company, DBS Vickers

52.356.2

52.5

4744.5

0.0

7.1

14.2

21.3

28.4

35.5

42.6

49.7

56.8

2013A 2014A 2015F 2016F 2017F

61.558.3

50.848.0

45.2

0.0

12.5

25.1

37.6

50.2

62.7

2013A 2014A 2015F 2016F 2017F

47.8

41.1 39.837.4

35.8

0.0

9.8

19.5

29.3

39.0

48.8

2013A 2014A 2015F 2016F 2017F

2220

21 22 22

0.0

2.8

5.5

8.3

11.0

13.8

16.5

19.3

22.0

2013A 2014A 2015F 2016F 2017F

117

190

44 4234

0

38

77

115

153

2013A 2014A 2015F 2016F 2017F

ASIAN INSIGHTS VICKERS SECURITIES Page 18

Company Guide

Adaro Energy

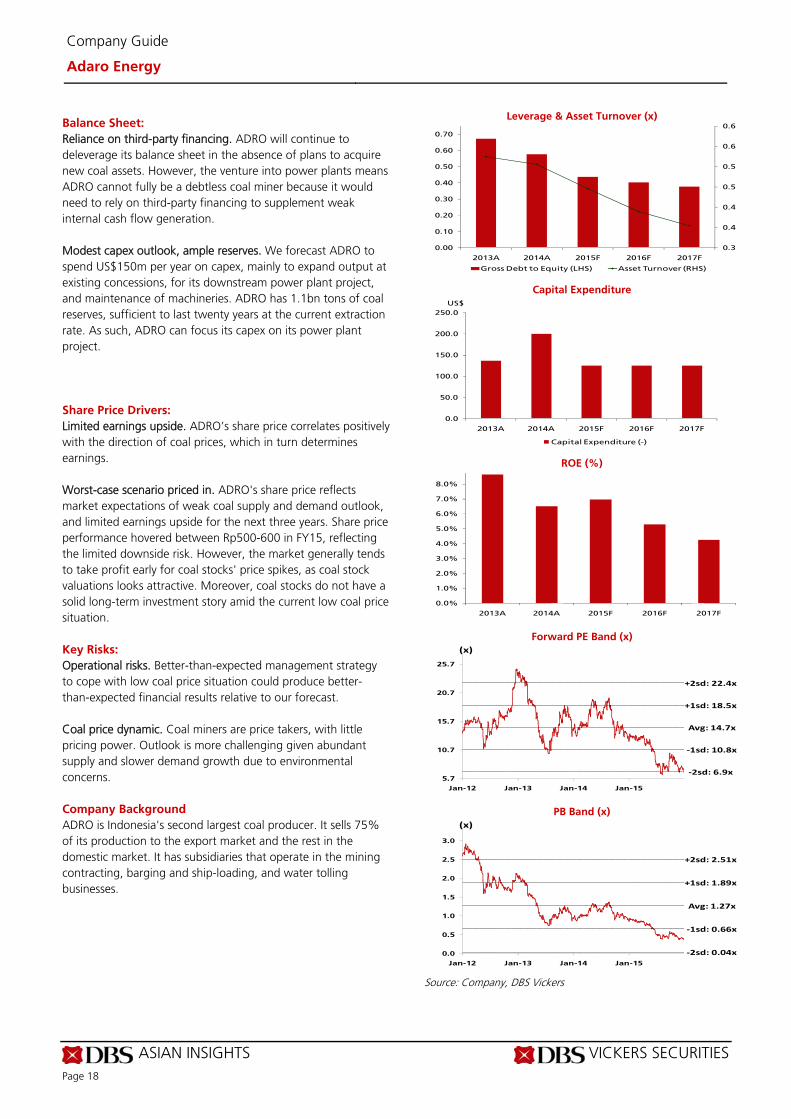

Balance Sheet:

Reliance on third-party financing. ADRO will continue to deleverage its balance sheet in the absence of plans to acquire new coal assets. However, the venture into power plants means ADRO cannot fully be a debtless coal miner because it would need to rely on third-party financing to supplement weak internal cash flow generation. Modest capex outlook, ample reserves. We forecast ADRO to spend US$150m per year on capex, mainly to expand output at existing concessions, for its downstream power plant project, and maintenance of machineries. ADRO has 1.1bn tons of coal reserves, sufficient to last twenty years at the current extraction rate. As such, ADRO can focus its capex on its power plant project.

Share Price Drivers:

Limited earnings upside. ADRO’s share price correlates positively with the direction of coal prices, which in turn determines earnings. Worst-case scenario priced in. ADRO's share price reflects market expectations of weak coal supply and demand outlook, and limited earnings upside for the next three years. Share price performance hovered between Rp500-600 in FY15, reflecting the limited downside risk. However, the market generally tends to take profit early for coal stocks' price spikes, as coal stock valuations looks attractive. Moreover, coal stocks do not have a solid long-term investment story amid the current low coal price situation.

Key Risks:

Operational risks. Better-than-expected management strategy to cope with low coal price situation could produce better-than-expected financial results relative to our forecast. Coal price dynamic. Coal miners are price takers, with little pricing power. Outlook is more challenging given abundant supply and slower demand growth due to environmental concerns.

Company Background

ADRO is Indonesia's second largest coal producer. It sells 75% of its production to the export market and the rest in the domestic market. It has subsidiaries that operate in the mining contracting, barging and ship-loading, and water tolling businesses.

Leverage & Asset Turnover (x)

Capital Expenditure

ROE (%)

Forward PE Band (x)

PB Band (x)

Source: Company, DBS Vickers

0.3

0.4

0.4

0.5

0.5

0.6

0.6

0.00

0.10

0.20

0.30

0.40

0.50

0.60

0.70

2013A 2014A 2015F 2016F 2017F

Gross Debt to Equity (LHS) Asset Turnover (RHS)

0.0

50.0

100.0

150.0

200.0

250.0

2013A 2014A 2015F 2016F 2017F

Capital Expenditure (-)

US$

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

7.0%

8.0%

2013A 2014A 2015F 2016F 2017F

Avg: 14.7x

+1sd: 18.5x

+2sd: 22.4x

‐1sd: 10.8x

‐2sd: 6.9x5.7

10.7

15.7

20.7

25.7

Jan-12 Jan-13 Jan-14 Jan-15

(x)

Avg: 1.27x

+1sd: 1.89x

+2sd: 2.51x

‐1sd: 0.66x

‐2sd: 0.04x0.0

0.5

1.0

1.5

2.0

2.5

3.0

Jan-12 Jan-13 Jan-14 Jan-15

(x)

ASIAN INSIGHTS VICKERS SECURITIES Page 19

Company Guide

Adaro Energy

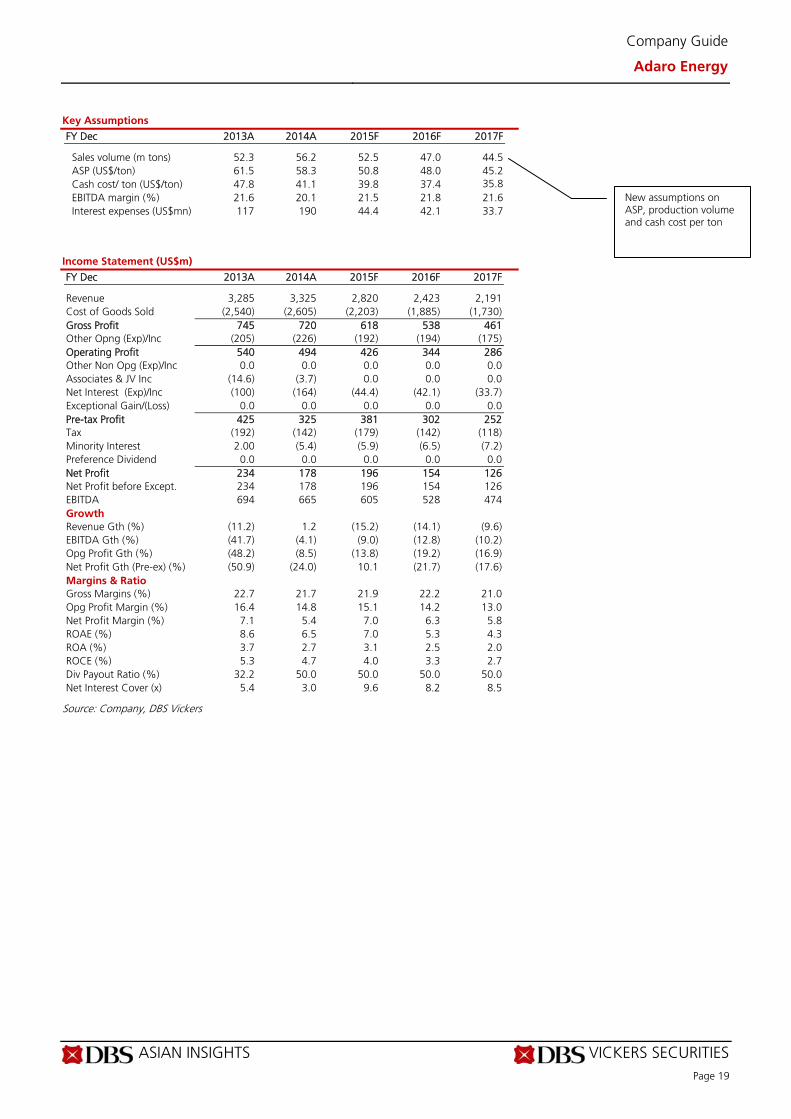

Key Assumptions

FY Dec 2013A 2014A 2015F 2016F 2017F Sales volume (m tons) 52.3 56.2 52.5 47.0 44.5 ASP (US$/ton) 61.5 58.3 50.8 48.0 45.2 Cash cost/ ton (US$/ton) 47.8 41.1 39.8 37.4 35.8 EBITDA margin (%) 21.6 20.1 21.5 21.8 21.6 Interest expenses (US$mn) 117 190 44.4 42.1 33.7

Income Statement (US$m)

FY Dec 2013A 2014A 2015F 2016F 2017F Revenue 3,285 3,325 2,820 2,423 2,191 Cost of Goods Sold (2,540) (2,605) (2,203) (1,885) (1,730) Gross Profit 745 720 618 538 461 Other Opng (Exp)/Inc (205) (226) (192) (194) (175) Operating Profit 540 494 426 344 286 Other Non Opg (Exp)/Inc 0.0 0.0 0.0 0.0 0.0 Associates & JV Inc (14.6) (3.7) 0.0 0.0 0.0 Net Interest (Exp)/Inc (100) (164) (44.4) (42.1) (33.7) Exceptional Gain/(Loss) 0.0 0.0 0.0 0.0 0.0 Pre-tax Profit 425 325 381 302 252 Tax (192) (142) (179) (142) (118) Minority Interest 2.00 (5.4) (5.9) (6.5) (7.2) Preference Dividend 0.0 0.0 0.0 0.0 0.0 Net Profit 234 178 196 154 126 Net Profit before Except. 234 178 196 154 126 EBITDA 694 665 605 528 474 Growth Revenue Gth (%) (11.2) 1.2 (15.2) (14.1) (9.6) EBITDA Gth (%) (41.7) (4.1) (9.0) (12.8) (10.2) Opg Profit Gth (%) (48.2) (8.5) (13.8) (19.2) (16.9) Net Profit Gth (Pre-ex) (%) (50.9) (24.0) 10.1 (21.7) (17.6) Margins & Ratio Gross Margins (%) 22.7 21.7 21.9 22.2 21.0 Opg Profit Margin (%) 16.4 14.8 15.1 14.2 13.0 Net Profit Margin (%) 7.1 5.4 7.0 6.3 5.8 ROAE (%) 8.6 6.5 7.0 5.3 4.3 ROA (%) 3.7 2.7 3.1 2.5 2.0 ROCE (%) 5.3 4.7 4.0 3.3 2.7 Div Payout Ratio (%) 32.2 50.0 50.0 50.0 50.0 Net Interest Cover (x) 5.4 3.0 9.6 8.2 8.5

Source: Company, DBS Vickers

New assumptions on ASP, production volume and cash cost per ton

ASIAN INSIGHTS VICKERS SECURITIES Page 20

Company Guide

Adaro Energy

Quarterly / Interim Income Statement (US$m)

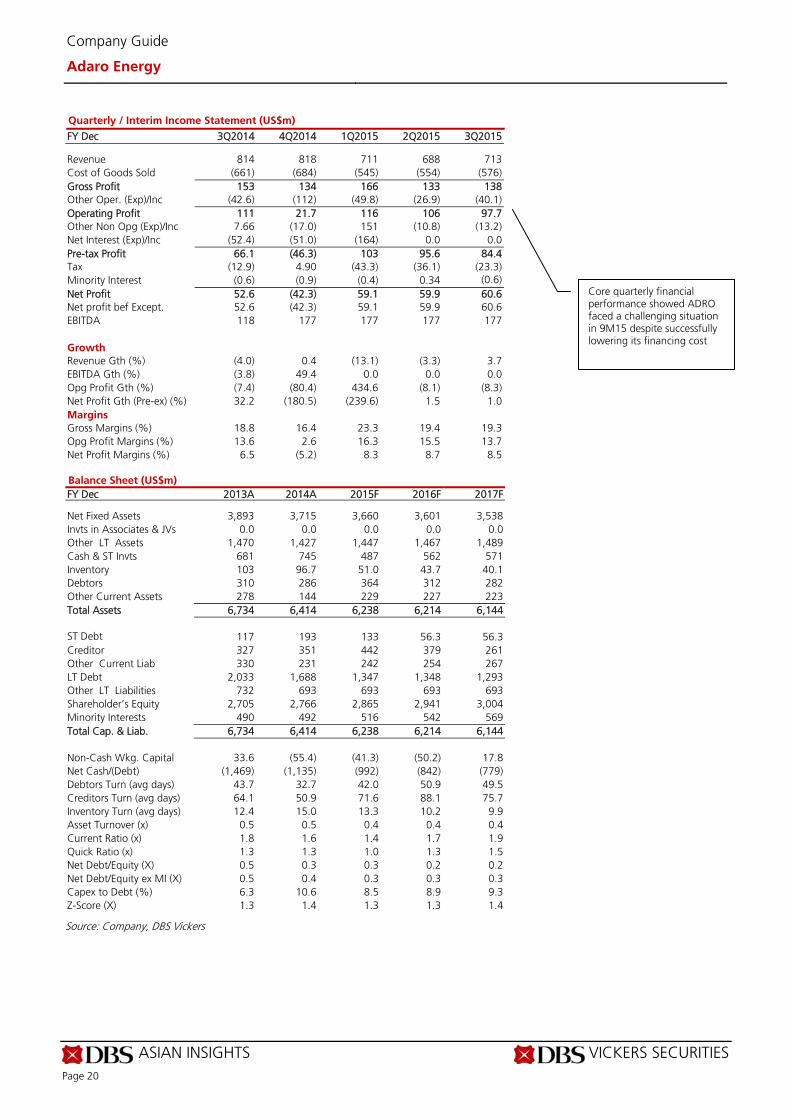

FY Dec 3Q2014 4Q2014 1Q2015 2Q2015 3Q2015 Revenue 814 818 711 688 713 Cost of Goods Sold (661) (684) (545) (554) (576) Gross Profit 153 134 166 133 138 Other Oper. (Exp)/Inc (42.6) (112) (49.8) (26.9) (40.1) Operating Profit 111 21.7 116 106 97.7 Other Non Opg (Exp)/Inc 7.66 (17.0) 151 (10.8) (13.2) Net Interest (Exp)/Inc (52.4) (51.0) (164) 0.0 0.0 Pre-tax Profit 66.1 (46.3) 103 95.6 84.4 Tax (12.9) 4.90 (43.3) (36.1) (23.3) Minority Interest (0.6) (0.9) (0.4) 0.34 (0.6) Net Profit 52.6 (42.3) 59.1 59.9 60.6 Net profit bef Except. 52.6 (42.3) 59.1 59.9 60.6 EBITDA 118 177 177 177 177 Growth Revenue Gth (%) (4.0) 0.4 (13.1) (3.3) 3.7 EBITDA Gth (%) (3.8) 49.4 0.0 0.0 0.0 Opg Profit Gth (%) (7.4) (80.4) 434.6 (8.1) (8.3) Net Profit Gth (Pre-ex) (%) 32.2 (180.5) (239.6) 1.5 1.0 Margins Gross Margins (%) 18.8 16.4 23.3 19.4 19.3 Opg Profit Margins (%) 13.6 2.6 16.3 15.5 13.7 Net Profit Margins (%) 6.5 (5.2) 8.3 8.7 8.5

Balance Sheet (US$m)

FY Dec 2013A 2014A 2015F 2016F 2017F Net Fixed Assets 3,893 3,715 3,660 3,601 3,538 Invts in Associates & JVs 0.0 0.0 0.0 0.0 0.0 Other LT Assets 1,470 1,427 1,447 1,467 1,489 Cash & ST Invts 681 745 487 562 571 Inventory 103 96.7 51.0 43.7 40.1 Debtors 310 286 364 312 282 Other Current Assets 278 144 229 227 223 Total Assets 6,734 6,414 6,238 6,214 6,144 ST Debt 117 193 133 56.3 56.3 Creditor 327 351 442 379 261 Other Current Liab 330 231 242 254 267 LT Debt 2,033 1,688 1,347 1,348 1,293 Other LT Liabilities 732 693 693 693 693 Shareholder’s Equity 2,705 2,766 2,865 2,941 3,004 Minority Interests 490 492 516 542 569 Total Cap. & Liab. 6,734 6,414 6,238 6,214 6,144 Non-Cash Wkg. Capital 33.6 (55.4) (41.3) (50.2) 17.8 Net Cash/(Debt) (1,469) (1,135) (992) (842) (779) Debtors Turn (avg days) 43.7 32.7 42.0 50.9 49.5 Creditors Turn (avg days) 64.1 50.9 71.6 88.1 75.7 Inventory Turn (avg days) 12.4 15.0 13.3 10.2 9.9 Asset Turnover (x) 0.5 0.5 0.4 0.4 0.4 Current Ratio (x) 1.8 1.6 1.4 1.7 1.9 Quick Ratio (x) 1.3 1.3 1.0 1.3 1.5 Net Debt/Equity (X) 0.5 0.3 0.3 0.2 0.2 Net Debt/Equity ex MI (X) 0.5 0.4 0.3 0.3 0.3 Capex to Debt (%) 6.3 10.6 8.5 8.9 9.3 Z-Score (X) 1.3 1.4 1.3 1.3 1.4

Source: Company, DBS Vickers

Core quarterly financial performance showed ADRO faced a challenging situation in 9M15 despite successfully lowering its financing cost

ASIAN INSIGHTS VICKERS SECURITIES Page 21

Company Guide

Adaro Energy

Cash Flow Statement (US$m)

FY Dec 2013A 2014A 2015F 2016F 2017F Pre-Tax Profit 425 325 381 302 252 Dep. & Amort. 169 176 180 184 188 Tax Paid (192) (142) (179) (142) (118) Assoc. & JV Inc/(loss) 0.0 0.0 0.0 0.0 0.0 Chg in Wkg.Cap. 321 54.2 59.1 (5.2) (84.5) Other Operating CF 2.00 1,033 18.7 19.3 19.9 Net Operating CF 724 1,447 460 358 257 Capital Exp.(net) (136) (200) (125) (125) (125) Other Invts.(net) (91.5) 6.40 (19.8) (20.8) (21.8) Invts in Assoc. & JV 0.0 0.0 0.0 0.0 0.0 Div from Assoc & JV 0.0 0.0 0.0 0.0 0.0 Other Investing CF 231 (692) (84.8) 2.00 3.87 Net Investing CF 3.63 (886) (230) (144) (143) Div Paid (75.5) (89.1) (98.1) (76.8) (63.2) Chg in Gross Debt (594) (269) (401) (75.1) (54.6) Capital Issues 0.0 0.0 0.0 0.0 0.0 Other Financing CF 317 (138) 11.5 12.1 12.7 Net Financing CF (353) (496) (488) (140) (105) Currency Adjustments 0.0 0.0 0.0 0.0 0.0 Chg in Cash 375 64.5 (258) 74.5 9.14 Opg CFPS (US cts.) 176 609 175 159 149 Free CFPS (US cts.) 257 545 146 102 57.8

Source: Company, DBS Vickers

Target Price & Ratings History

Source: DBS Vickers

S.No. Date Closing PriceTarget Price

Rating

1: 13 Apr 15 955 1030 HOLD

2: 04 May 15 845 1020 HOLD

3: 23 Jul 15 595 630 HOLD

4: 02 Sep 15 610 500 FULLY VALUED

5: 04 Sep 15 580 550 HOLD

6: 02 Nov 15 610 625 HOLD

Note: Share price and Target price are adjusted for corporate actions.

1 2

3

4

5

6

426

526

626

726

826

926

1026

Jan-15 May-15 Sep-15

Rp

Regular capex for existing concession maintenance and other minor expansion

ASIAN INSIGHTS VICKERS SECURITIES ed: TH / sa: MA

HOLD

Last Traded Price: Rp5,425 (JCI : 4,523.98) Price Target : Rp6,100 (12% upside) (Prev Rp6,900) Potential Catalyst: Double digit dividend yield Where we differ: Our view is that coal prices will stay at current low level

Analyst William Simadiputra +62 2130034939 [email protected]

Price Relative

Forecasts and Valuation FY Dec (US$m) 2014A 2015F 2016F 2017F Revenue 1,943 1,672 1,393 1,117 EBITDA 310 230 163 146 Pre-tax Profit 262 197 129 110 Net Profit 200 144 93.8 80.5 Net Pft (Pre Ex.) 200 144 93.8 80.5 Net Pft Gth (Pre-ex) (%) (13.1) (28.1) (34.8) (14.3) EPS (Rp) 2,478 1,782 1,161 996 EPS Pre Ex. (Rp) 2,478 1,782 1,161 996 EPS Gth Pre Ex (%) (13) (28) (35) (14) Diluted EPS (Rp) 2,478 1,782 1,161 996 Net DPS (Rp) 1,115 1,247 813 697 BV Per Share (Rp) 11,122 11,657 12,005 12,304 PE (X) 2.2 3.0 4.7 5.4 PE Pre Ex. (X) 2.2 3.0 4.7 5.4 P/Cash Flow (X) 1.9 1.5 3.0 3.3 EV/EBITDA (X) 0.7 0.2 0.1 0.0 Net Div Yield (%) 20.6 23.0 15.0 12.8 P/Book Value (X) 0.5 0.5 0.5 0.4 Net Debt/Equity (X) CASH CASH CASH CASH ROAE (%) 22.3 15.6 9.8 8.2 Earnings Rev (%): 0 (10) 1 Consensus EPS (Rp): 1,552 1,329 1,189 Other Broker Recs: B: 10 S: 5 H: 12

Source of all data: Company, DBS Vickers, Bloomberg Finance L.P

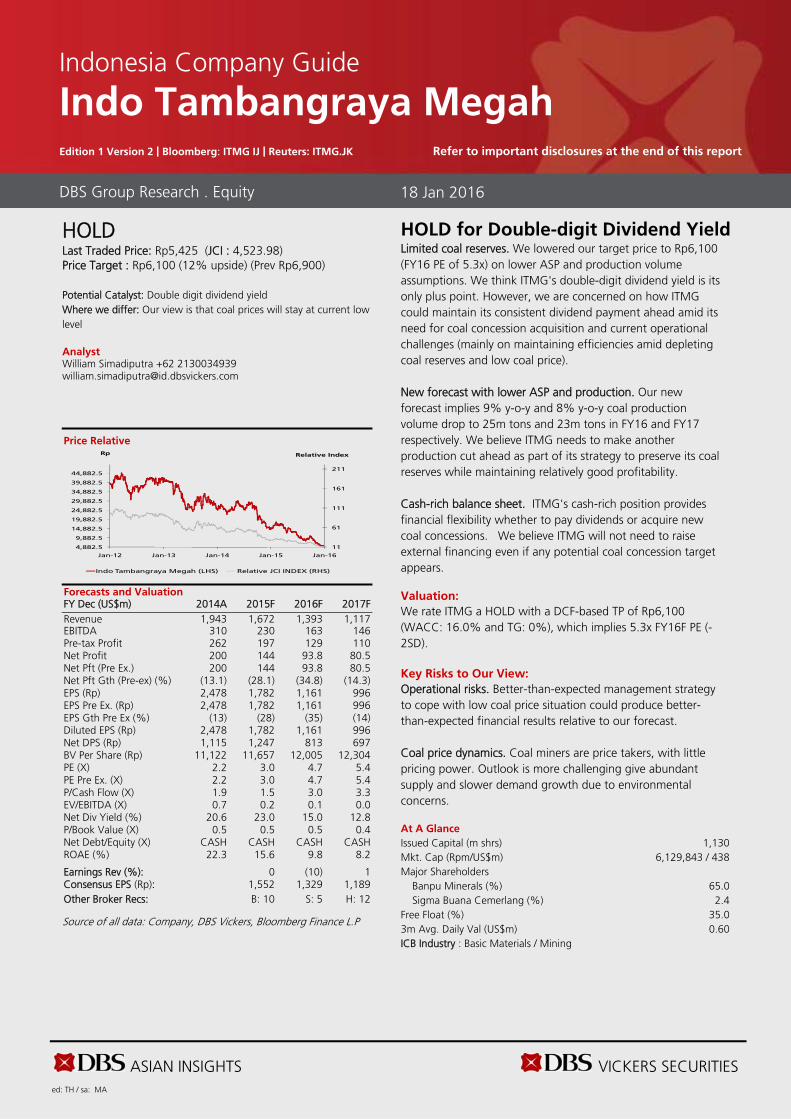

HOLD for Double-digit Dividend Yield Limited coal reserves. We lowered our target price to Rp6,100 (FY16 PE of 5.3x) on lower ASP and production volume assumptions. We think ITMG's double-digit dividend yield is its only plus point. However, we are concerned on how ITMG could maintain its consistent dividend payment ahead amid its need for coal concession acquisition and current operational challenges (mainly on maintaining efficiencies amid depleting coal reserves and low coal price). New forecast with lower ASP and production. Our new forecast implies 9% y-o-y and 8% y-o-y coal production volume drop to 25m tons and 23m tons in FY16 and FY17 respectively. We believe ITMG needs to make another production cut ahead as part of its strategy to preserve its coal reserves while maintaining relatively good profitability. Cash-rich balance sheet. ITMG's cash-rich position provides financial flexibility whether to pay dividends or acquire new coal concessions. We believe ITMG will not need to raise external financing even if any potential coal concession target appears. Valuation:

We rate ITMG a HOLD with a DCF-based TP of Rp6,100 (WACC: 16.0% and TG: 0%), which implies 5.3x FY16F PE (-2SD). Key Risks to Our View:

Operational risks. Better-than-expected management strategy to cope with low coal price situation could produce better-than-expected financial results relative to our forecast. Coal price dynamics. Coal miners are price takers, with little pricing power. Outlook is more challenging give abundant supply and slower demand growth due to environmental concerns. At A Glance Issued Capital (m shrs) 1,130 Mkt. Cap (Rpm/US$m) 6,129,843 / 438 Major Shareholders Banpu Minerals (%) 65.0 Sigma Buana Cemerlang (%) 2.4 Free Float (%) 35.0 3m Avg. Daily Val (US$m) 0.60 ICB Industry : Basic Materials / Mining

DBS Group Research . Equity 18 Jan 2016

Indonesia Company Guide

Indo Tambangraya Megah Edition 1 Version 2 | Bloomberg: ITMG IJ | Reuters: ITMG.JK Refer to important disclosures at the end of this report

11

61

111

161

211

4,882.5

9,882.5

14,882.5

19,882.5

24,882.5

29,882.5

34,882.5

39,882.5

44,882.5

Jan-12 Jan-13 Jan-14 Jan-15 Jan-16

Relative IndexRp

Indo Tambangraya Megah (LHS) Relative JCI INDEX (RHS)

ASIAN INSIGHTS VICKERS SECURITIES Page 23

Company Guide

Indo Tambangraya Megah

CRITICAL DATA POINTS TO WATCH

Earnings Drivers:

Earnings to drop further in FY16. We forecast earnings to drop by 35% y-o-y to US$94m in FY16 before dropping further by 14% to US$80m in FY16. FY16 and FY17 earnings will be dragged by a lower top line due to weaker ASP and lower sales volume. Production volume to be flat. In line with guidance and the group’s focus on profitability rather than production, we assumed production volume will drop to 25m tons and 23m tons in FY16 and FY17 respectively. ITMG’s mines have seven years left. We also assumed that blended strip ratio will drop to 9.3x from 9.9x last year. The lower strip ratio is possible this year if ITMG is able to secure purchase contracts for lower quality coal. Weaker ASP. There will be persistent oversupply ahead, and we forecast the benchmark coal price to remain low at US$55 per ton. This will affect ITMG’s coal pricing ahead. We assumed a lower ASP of US$55.7/ton for FY16. Our ASP assumption implies a 12% discount to our forecast benchmark price. Modest drop in cash cost. We expect cash cost to drop to US$37/ton (-10% y-o-y) in FY16 before falling further to US$32 in FY17 as management focuses on profitability rather than volume expansion. We also assumed that fuel cost would drop further to US$0.5/litre in FY16, on lower crude price. However, we see limited room for mining contracting fee to be renegotiated lower given ITMG’s flat volume. Miners with higher strip ratios will benefit from lower fuel cost. These include ITMG, which we believe will be the largest beneficiary of lower fuel cost because of high usage of machineries. The lower crude oil price has had a positive impact on ITMG’s profitability, as seen in 4Q14; fuel cost fell by 25% q-o-q to US$0.65/litre, and its cash cost fell to US$54.9/ton (-10% q-o-q).

Sales volume (m tons)

Avg selling price (US$/ton)

Cash cost (US$/ton)

Fuel cost (US$/liter)

Capex

Source: Company, DBS Vickers

29.5 29.127.5

2523

0.0

3.7

7.4

11.2

14.9

18.6

22.3

26.1

29.8

2013A 2014A 2015F 2016F 2017F

74.9

65.660.8

55.7

48.5

0.0

15.3

30.6

45.8

61.1

76.4

2013A 2014A 2015F 2016F 2017F

45.243.6

39.136.9

31.8

0.0

9.2

18.4

27.7

36.9

46.1

2013A 2014A 2015F 2016F 2017F

1 1

1

0 0

0.00

0.12

0.24

0.36

0.48

0.60

0.72

0.84

0.96

2013A 2014A 2015F 2016F 2017F

50 50

40 40 40

0.0

10.1

20.2

30.3

40.4

50.5

2013A 2014A 2015F 2016F 2017F

ASIAN INSIGHTS VICKERS SECURITIES Page 24

Company Guide

Indo Tambangraya Megah

Balance Sheet:

Cash-rich balance sheet. ITMG's cash-rich position provides financial flexibility whether to pay dividends or acquire new coal concessions. We believe ITMG will not need to raise external financing even if any potential coal concession target appears.

Share Price Drivers:

Stock de-rating on bleak industry outlook. ITMG’s stock price has de-rated because of concerns over its depleting reserves, but this could be a sign of a sizeable acquisition ahead to remain in operation. The limited reserves could also hurt earnings if it needs to cut output further, and reduce the ability to lower strip ratio.

Key Risks:

Drop in coal prices. Coal miners are price-takers, with little pricing power. And, the pricing outlook is more challenging now, given abundant supply and slower coal demand growth because of environmental concerns. Regulatory changes such as an export ban and increase in royalty fees. The coal industry is strictly regulated. Potential changes in policies such as an export ban, higher royalty fees, and production limits, could have an adverse impact on coal miners’ earnings. Operational risk. If ITMG fails to secure meaningful coal reserves in the future, it may have to halt operations. Moreover, the efficiency-focused strategy may not lead to meaningful reductions in cash cost. Profitability risk. We assume ITMG could maintain its cash margin by lowering its production based on our estimates. It is possible that ITMG may need to further cut its coal production volume if the remaining profitable concessions are lower than our expectations. Company Background

One of the largest coal mining companies owned by Banpu.

Leverage & Asset Turnover (x)

Capital Expenditure

ROE (%)

Forward PE Band (x)

PB Band (x)

Source: Company, DBS Vickers

0.8

0.9

1.0

1.1

1.2

1.3

1.4

1.5

1.6

0.00

0.01

0.01

0.02

0.02

0.03

0.03

0.04

0.04

0.05

0.05

2013A 2014A 2015F 2016F 2017F

Gross Debt to Equity (LHS) Asset Turnover (RHS)

0.0

20.0

40.0

60.0

80.0

100.0

120.0

2013A 2014A 2015F 2016F 2017F

Capital Expenditure (-)

US$

0.0%

5.0%

10.0%

15.0%

20.0%

2013A 2014A 2015F 2016F 2017F

Avg: 13.3x

+1sd: 17.3x

+2sd: 21.3x

‐1sd: 9.3x

‐2sd: 5.4x4.2

6.2

8.2

10.2

12.2

14.2

16.2

18.2

20.2

22.2

Jan-12 Jan-13 Jan-14 Jan-15

(x)

Avg: 3.15x

+1sd: 4.76x

+2sd: 6.38x

‐1sd: 1.53x

0.0

1.0

2.0

3.0

4.0

5.0

6.0

7.0

Jan-12 Jan-13 Jan-14 Jan-15

(x)

ASIAN INSIGHTS VICKERS SECURITIES Page 25

Company Guide

Indo Tambangraya Megah

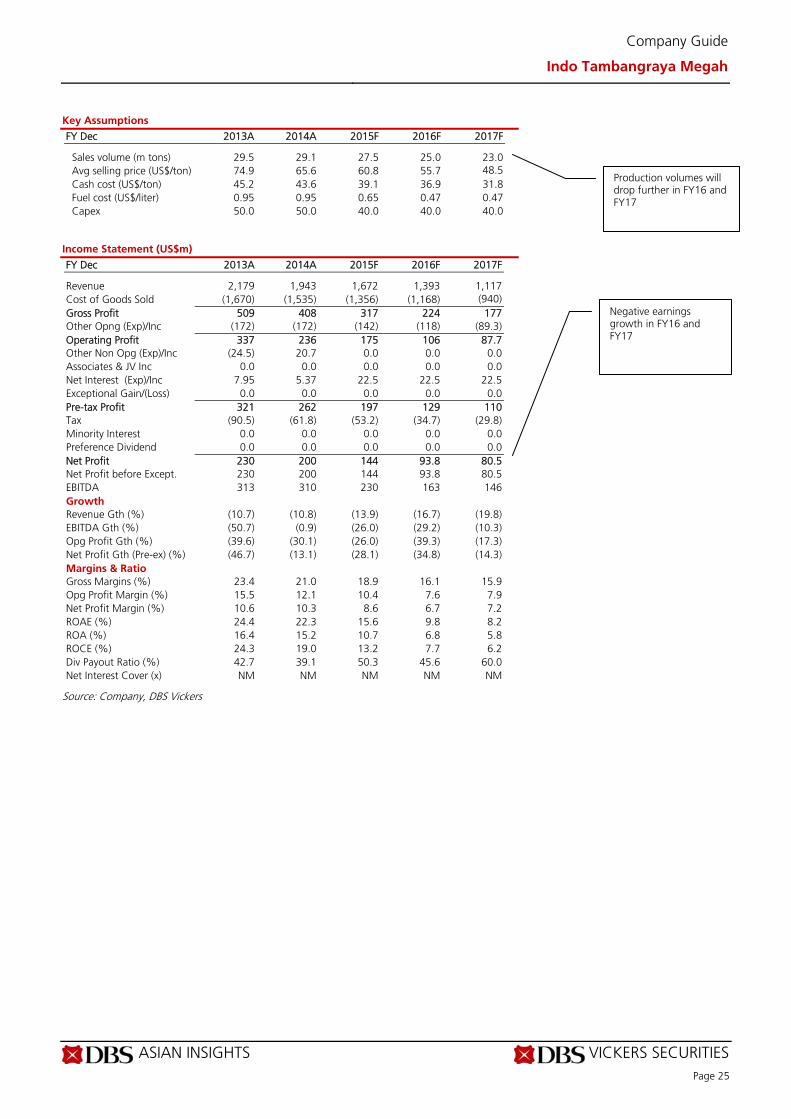

Key Assumptions

FY Dec 2013A 2014A 2015F 2016F 2017F Sales volume (m tons) 29.5 29.1 27.5 25.0 23.0 Avg selling price (US$/ton) 74.9 65.6 60.8 55.7 48.5 Cash cost (US$/ton) 45.2 43.6 39.1 36.9 31.8 Fuel cost (US$/liter) 0.95 0.95 0.65 0.47 0.47 Capex 50.0 50.0 40.0 40.0 40.0

Income Statement (US$m)

FY Dec 2013A 2014A 2015F 2016F 2017F Revenue 2,179 1,943 1,672 1,393 1,117 Cost of Goods Sold (1,670) (1,535) (1,356) (1,168) (940) Gross Profit 509 408 317 224 177 Other Opng (Exp)/Inc (172) (172) (142) (118) (89.3) Operating Profit 337 236 175 106 87.7 Other Non Opg (Exp)/Inc (24.5) 20.7 0.0 0.0 0.0 Associates & JV Inc 0.0 0.0 0.0 0.0 0.0 Net Interest (Exp)/Inc 7.95 5.37 22.5 22.5 22.5 Exceptional Gain/(Loss) 0.0 0.0 0.0 0.0 0.0 Pre-tax Profit 321 262 197 129 110 Tax (90.5) (61.8) (53.2) (34.7) (29.8) Minority Interest 0.0 0.0 0.0 0.0 0.0 Preference Dividend 0.0 0.0 0.0 0.0 0.0 Net Profit 230 200 144 93.8 80.5 Net Profit before Except. 230 200 144 93.8 80.5 EBITDA 313 310 230 163 146 Growth Revenue Gth (%) (10.7) (10.8) (13.9) (16.7) (19.8) EBITDA Gth (%) (50.7) (0.9) (26.0) (29.2) (10.3) Opg Profit Gth (%) (39.6) (30.1) (26.0) (39.3) (17.3) Net Profit Gth (Pre-ex) (%) (46.7) (13.1) (28.1) (34.8) (14.3) Margins & Ratio Gross Margins (%) 23.4 21.0 18.9 16.1 15.9 Opg Profit Margin (%) 15.5 12.1 10.4 7.6 7.9 Net Profit Margin (%) 10.6 10.3 8.6 6.7 7.2 ROAE (%) 24.4 22.3 15.6 9.8 8.2 ROA (%) 16.4 15.2 10.7 6.8 5.8 ROCE (%) 24.3 19.0 13.2 7.7 6.2 Div Payout Ratio (%) 42.7 39.1 50.3 45.6 60.0 Net Interest Cover (x) NM NM NM NM NM

Source: Company, DBS Vickers

Production volumes will drop further in FY16 and FY17

Negative earnings growth in FY16 and FY17

ASIAN INSIGHTS VICKERS SECURITIES Page 26

Company Guide

Indo Tambangraya Megah

Quarterly / Interim Income Statement (US$m)

FY Dec 3Q2014 4Q2014 1Q2015 2Q2015 3Q2015 Revenue 522 455 428 397 382 Cost of Goods Sold (431) (362) (329) (322) (296) Gross Profit 91.9 92.9 99.0 75.2 85.6 Other Oper. (Exp)/Inc (44.0) (49.7) (39.7) (37.5) (36.2) Operating Profit 47.9 43.2 59.3 37.7 49.4 Other Non Opg (Exp)/Inc (14.3) (11.8) 1.50 (8.1) (11.5) Net Interest (Exp)/Inc 0.0 0.28 0.99 0.95 0.91 Pre-tax Profit 33.6 30.4 61.8 30.6 38.7 Tax (12.7) 0.94 (24.0) (10.4) (13.8) Net Profit 20.9 31.4 37.8 20.2 24.9 Net profit bef Except. 20.9 31.4 37.8 20.2 24.9 EBITDA 33.6 30.2 74.0 55.0 55.0 Growth Revenue Gth (%) 13.2 (12.9) (6.0) (7.2) (3.7) EBITDA Gth (%) (43.7) (10.2) 145.4 (25.7) 0.0 Opg Profit Gth (%) (7.4) (9.9) 37.3 (36.3) 30.8 Net Profit Gth (Pre-ex) (%) (60.1) 50.1 20.5 (46.4) 23.1 Margins Gross Margins (%) 17.6 20.4 23.1 19.0 22.4 Opg Profit Margins (%) 9.2 9.5 13.9 9.5 12.9 Net Profit Margins (%) 4.0 6.9 8.8 5.1 6.5

Balance Sheet (US$m)

FY Dec 2013A 2014A 2015F 2016F 2017F Net Fixed Assets 317 286 271 264 256 Invts in Associates & JVs 0.0 0.0 0.0 0.0 0.0 Other LT Assets 404 452 475 498 523 Cash & ST Invts 289 226 383 416 442 Inventory 118 150 67.5 58.2 46.8 Debtors 169 170 152 126 101 Other Current Assets 30.1 23.2 24.4 25.6 26.9 Total Assets 1,327 1,307 1,372 1,389 1,397 ST Debt 0.0 0.0 0.0 0.0 0.0 Creditor 166 166 175 151 121 Other Current Liab 209 199 208 219 230 LT Debt 0.0 0.0 0.0 0.0 0.0 Other LT Liabilities 53.6 44.6 46.8 49.1 51.6 Shareholder’s Equity 898 899 942 970 994 Minority Interests 0.0 0.0 0.0 0.0 0.0 Total Cap. & Liab. 1,327 1,307 1,372 1,389 1,397 Non-Cash Wkg. Capital (56.8) (20.7) (140) (159) (176) Net Cash/(Debt) 289 226 383 416 442 Debtors Turn (avg days) 33.0 31.9 35.2 36.5 37.3 Creditors Turn (avg days) 38.4 40.8 47.8 53.5 56.3 Inventory Turn (avg days) 29.4 33.1 30.5 20.6 21.7 Asset Turnover (x) 1.6 1.5 1.2 1.0 0.8 Current Ratio (x) 1.6 1.6 1.6 1.7 1.8 Quick Ratio (x) 1.2 1.1 1.4 1.5 1.5 Net Debt/Equity (X) CASH CASH CASH CASH CASH Net Debt/Equity ex MI (X) CASH CASH CASH CASH CASH Capex to Debt (%) N/A N/A N/A N/A N/A Z-Score (X) 4.2 4.1 3.6 3.5 3.3

Source: Company, DBS Vickers

Quarterly growth showed weakening trend on lower ASP and production volume

However, ITMG successfully maintains relatively stable profitability

Net cash position provide ITMG flexibility whether to pay dividends or pursue coal concessions acquisition

ASIAN INSIGHTS VICKERS SECURITIES Page 27

Company Guide

Indo Tambangraya Megah

Cash Flow Statement (US$m)

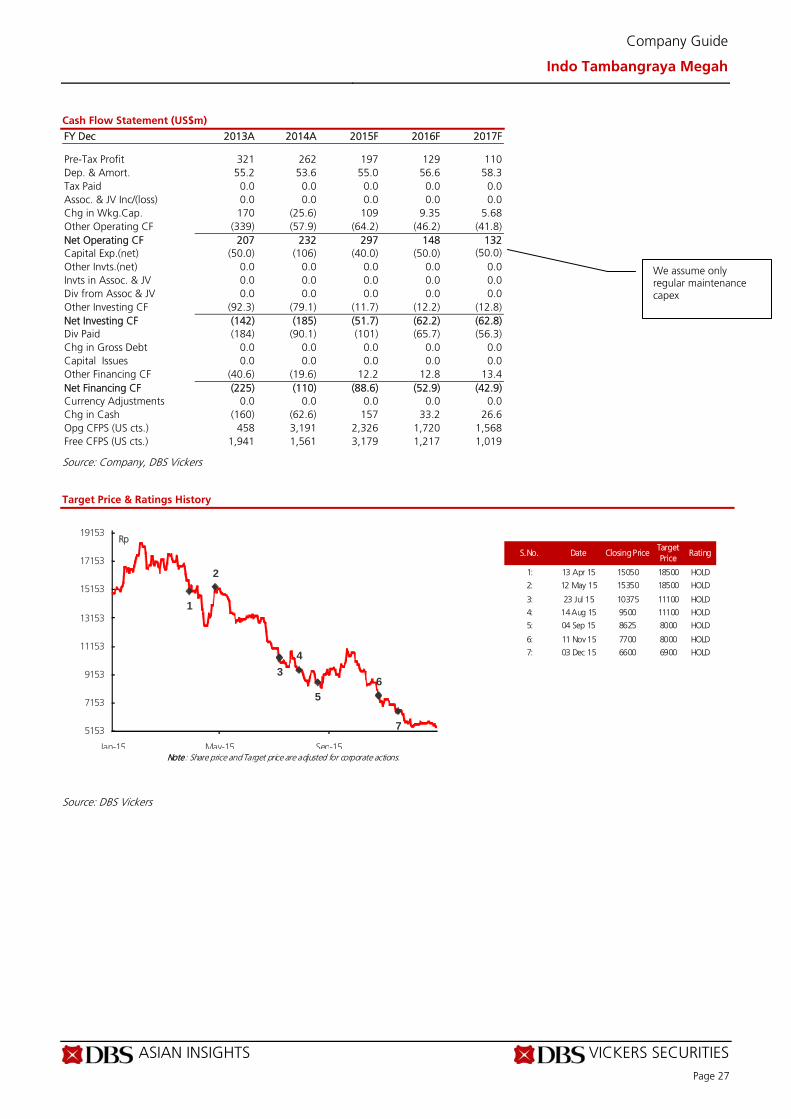

FY Dec 2013A 2014A 2015F 2016F 2017F Pre-Tax Profit 321 262 197 129 110 Dep. & Amort. 55.2 53.6 55.0 56.6 58.3 Tax Paid 0.0 0.0 0.0 0.0 0.0 Assoc. & JV Inc/(loss) 0.0 0.0 0.0 0.0 0.0 Chg in Wkg.Cap. 170 (25.6) 109 9.35 5.68 Other Operating CF (339) (57.9) (64.2) (46.2) (41.8) Net Operating CF 207 232 297 148 132 Capital Exp.(net) (50.0) (106) (40.0) (50.0) (50.0) Other Invts.(net) 0.0 0.0 0.0 0.0 0.0 Invts in Assoc. & JV 0.0 0.0 0.0 0.0 0.0 Div from Assoc & JV 0.0 0.0 0.0 0.0 0.0 Other Investing CF (92.3) (79.1) (11.7) (12.2) (12.8) Net Investing CF (142) (185) (51.7) (62.2) (62.8) Div Paid (184) (90.1) (101) (65.7) (56.3) Chg in Gross Debt 0.0 0.0 0.0 0.0 0.0 Capital Issues 0.0 0.0 0.0 0.0 0.0 Other Financing CF (40.6) (19.6) 12.2 12.8 13.4 Net Financing CF (225) (110) (88.6) (52.9) (42.9) Currency Adjustments 0.0 0.0 0.0 0.0 0.0 Chg in Cash (160) (62.6) 157 33.2 26.6 Opg CFPS (US cts.) 458 3,191 2,326 1,720 1,568 Free CFPS (US cts.) 1,941 1,561 3,179 1,217 1,019

Source: Company, DBS Vickers

Target Price & Ratings History

Source: DBS Vickers

S.No. Date Closing PriceTarget Price

Rating

1: 13 Apr 15 15050 18500 HOLD

2: 12 May 15 15350 18500 HOLD

3: 23 Jul 15 10375 11100 HOLD

4: 14 Aug 15 9500 11100 HOLD

5: 04 Sep 15 8625 8000 HOLD

6: 11 Nov 15 7700 8000 HOLD

7: 03 Dec 15 6600 6900 HOLD

Note: Share price and Target price are adjusted for corporate actions.

1

2

3

4

5

6

75153

7153

9153

11153

13153

15153

17153

19153

Jan-15 May-15 Sep-15

Rp

We assume only regular maintenance capex

ASIAN INSIGHTS VICKERS SECURITIES ed: TH / sa: MA

FULLY VALUED Last Traded Price: Rp670 (JCI : 4,523.98) Price Target : Rp450 (33% downside) (Prev Rp700) Potential Catalyst: Coal concession acquisition Where we differ: We believe HRUM is the most negatively impacted by the low coal price trend Analyst William Simadiputra +62 2130034939 [email protected]

Price Relative

Forecasts and Valuation FY Dec (US$m) 2014A 2015F 2016F 2017F Revenue 478 285 183 183 EBITDA 32.1 29.4 12.6 17.6 Pre-tax Profit 24.1 25.5 11.7 16.2 Net Profit 0.41 15.0 6.78 9.57 Net Pft (Pre Ex.) 0.41 15.0 6.78 9.57 Net Pft Gth (Pre-ex) (%) (99.0) 3,552.0 (54.8) 41.2 EPS (Rp) 2.13 77.7 35.1 49.6 EPS Pre Ex. (Rp) 2.13 77.7 35.1 49.6 EPS Gth Pre Ex (%) (99) 3,552 (55) 41 Diluted EPS (Rp) 2.13 77.7 35.1 49.6 Net DPS (Rp) 155 23.3 10.5 14.9 BV Per Share (Rp) 1,490 1,544 1,569 1,603 PE (X) 314.9 8.6 19.1 13.5 PE Pre Ex. (X) 314.9 8.6 19.1 13.5 P/Cash Flow (X) 2.4 nm 4.8 5.8 EV/EBITDA (X) 0.1 1.1 1.7 1.0 Net Div Yield (%) 23.1 3.5 1.6 2.2 P/Book Value (X) 0.4 0.4 0.4 0.4 Net Debt/Equity (X) CASH CASH CASH CASH ROAE (%) 0.1 5.1 2.3 3.1 Earnings Rev (%): 0 (60) (11) Consensus EPS (Rp): 28.0 42.0 69.9 Other Broker Recs: B: 0 S: 7 H: 5

Source of all data: Company, DBS Vickers, Bloomberg Finance L.P

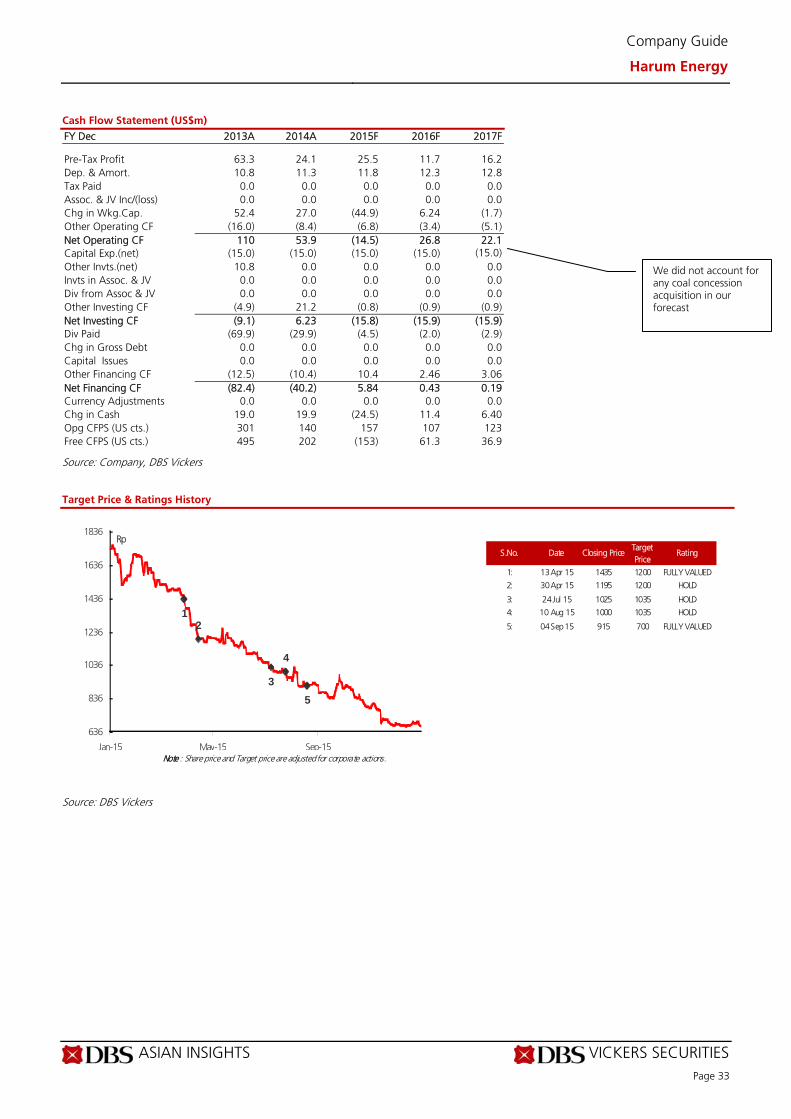

Fragile Lowering our TP to Rp450, reiterate FULLY VALUED. We see HRUM's earnings outlook to be sensitive to its execution capability to maintain profitability amid the lower ASP and coal reserve outlook. Cut our FY16 and FY17 earnings forecast by 29% and 11% on lower production volume and ASP respectively. We believe HRUM needs to lower its production volume on new lower ASP assumption in order to stay at positive earnings. Prioritising profitability. We assume HRUM could lower its cash cost per ton by 8% in FY16 and FY17 relative to our previous forecast. HRUM will focus on shortening its overburden hauling distances and maintaining equipment productivities. Limited reserves, acquisition is key. Since HRUM has not found any strong acquisition candidate yet, the company will continue its exploration programme at its Santan Batu Bara (SBB) Biarawa block in 2016. HRUM believes the block hosts the largest coal resources and resources relative to the rest of the blocks at SBB. Valuation:

We rate HRUM as FULLY VALUED with a target price of Rp450, which implies 13.9x FY16F PE. Our DCF-based TP assumes 15.1% WACC and 0% terminal growth. Key Risks to Our View:

Coal price. Coal price is the key risk for coal miners, as they are price takers with minimal pricing power. Outlook is more challenging due to abundant supply and slower coal demand growth due to environmental concerns. However, on the other hand, if the coal price rebounds, we will need to reverse back our miners' reserve assumption and target price. Concession acquisition. If HRUM announces any new reserve acquisition, we should add the new reserves to our forecast and valuation, resulting in a higher target price. At A Glance Issued Capital (m shrs) 2,704 Mkt. Cap (Rpm/US$m) 1,811,425 / 130 Major Shareholders Karuni Bara Perkasa (%) 69.7 Free Float (%) 30.2 3m Avg. Daily Val (US$m) 0.04 ICB Industry : Basic Materials / Mining

DBS Group Research . Equity 18 Jan 2016

Indonesia Company Guide

Harum Energy Edition 1 Version 2 | Bloomberg: HRUM IJ | Reuters: HRUM.JK Refer to important disclosures at the end of this report

7

57

107

157

207

603.0

1,603.0

2,603.0

3,603.0

4,603.0

5,603.0

6,603.0

7,603.0

8,603.0

9,603.0

Jan-12 Jan-13 Jan-14 Jan-15 Jan-16

Relative IndexRp

Harum Energy (LHS) Relative JCI INDEX (RHS)

ASIAN INSIGHTS VICKERS SECURITIES Page 29

Company Guide

Harum Energy

CRITICAL DATA POINTS TO WATCH

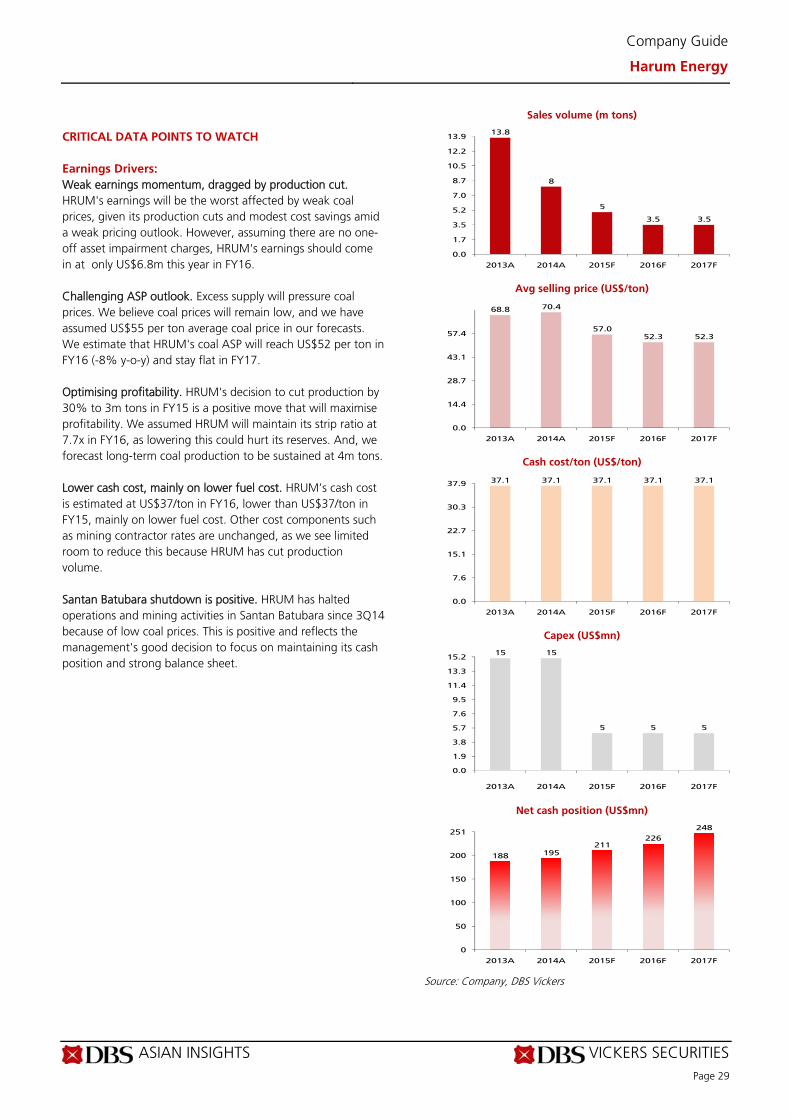

Earnings Drivers:

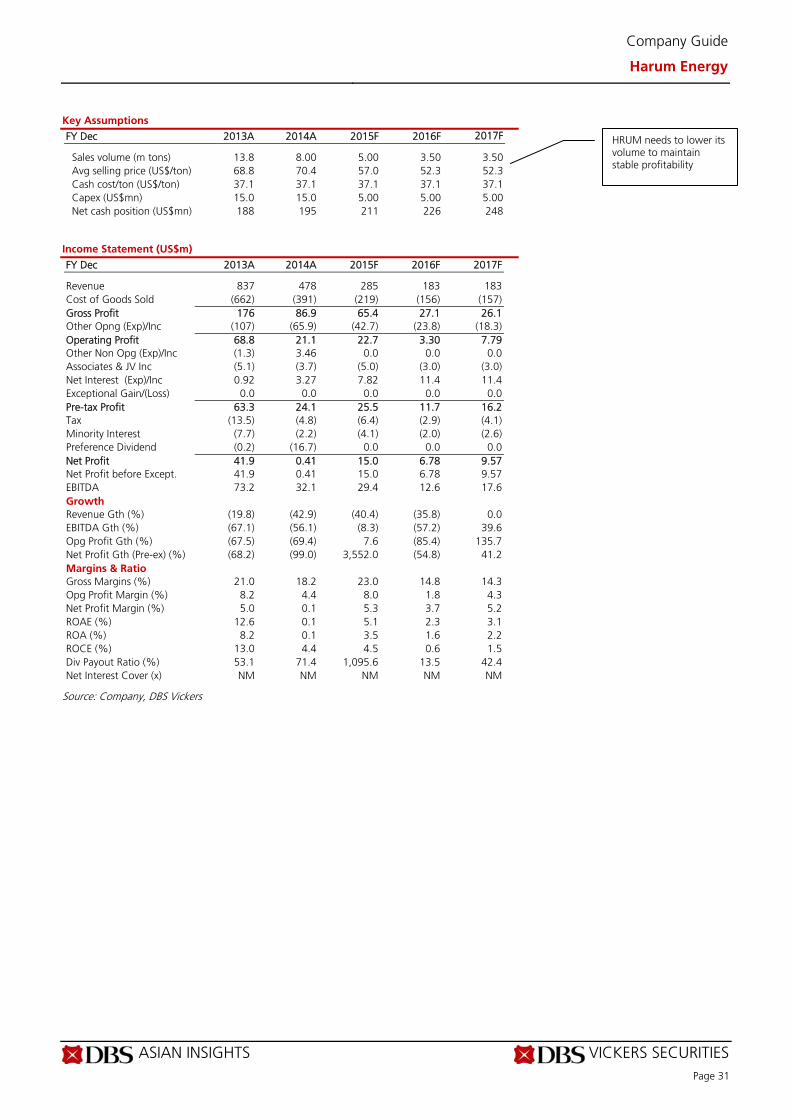

Weak earnings momentum, dragged by production cut. HRUM's earnings will be the worst affected by weak coal prices, given its production cuts and modest cost savings amid a weak pricing outlook. However, assuming there are no one-off asset impairment charges, HRUM's earnings should come in at only US$6.8m this year in FY16. Challenging ASP outlook. Excess supply will pressure coal prices. We believe coal prices will remain low, and we have assumed US$55 per ton average coal price in our forecasts. We estimate that HRUM's coal ASP will reach US$52 per ton in FY16 (-8% y-o-y) and stay flat in FY17.

Optimising profitability. HRUM's decision to cut production by 30% to 3m tons in FY15 is a positive move that will maximise profitability. We assumed HRUM will maintain its strip ratio at 7.7x in FY16, as lowering this could hurt its reserves. And, we forecast long-term coal production to be sustained at 4m tons. Lower cash cost, mainly on lower fuel cost. HRUM’s cash cost is estimated at US$37/ton in FY16, lower than US$37/ton in FY15, mainly on lower fuel cost. Other cost components such as mining contractor rates are unchanged, as we see limited room to reduce this because HRUM has cut production volume. Santan Batubara shutdown is positive. HRUM has halted operations and mining activities in Santan Batubara since 3Q14 because of low coal prices. This is positive and reflects the management's good decision to focus on maintaining its cash position and strong balance sheet.

Sales volume (m tons)

Avg selling price (US$/ton)

Cash cost/ton (US$/ton)

Capex (US$mn)

Net cash position (US$mn)

Source: Company, DBS Vickers

13.8

8

5

3.5 3.5

0.0

1.7

3.5

5.2

7.0

8.7

10.5

12.2

13.9

2013A 2014A 2015F 2016F 2017F

68.8 70.4

57.052.3 52.3

0.0

14.4

28.7

43.1

57.4

2013A 2014A 2015F 2016F 2017F

37.1 37.1 37.1 37.1 37.1

0.0

7.6

15.1

22.7

30.3

37.9

2013A 2014A 2015F 2016F 2017F

15 15

5 5 5

0.0

1.9

3.8

5.7

7.6

9.5

11.4

13.3

15.2

2013A 2014A 2015F 2016F 2017F

188 195211

226

248

0

50

100

150

200

251

2013A 2014A 2015F 2016F 2017F

ASIAN INSIGHTS VICKERS SECURITIES Page 30

Company Guide

Harum Energy

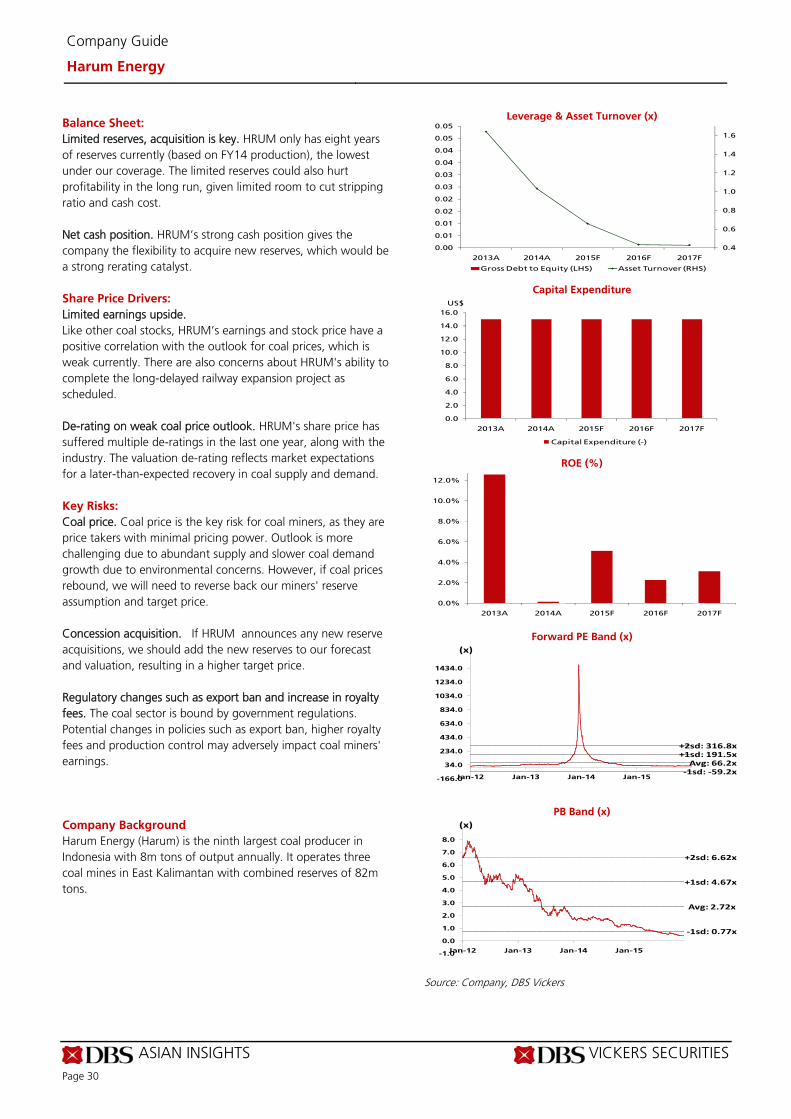

Balance Sheet:

Limited reserves, acquisition is key. HRUM only has eight years of reserves currently (based on FY14 production), the lowest under our coverage. The limited reserves could also hurt profitability in the long run, given limited room to cut stripping ratio and cash cost. Net cash position. HRUM’s strong cash position gives the company the flexibility to acquire new reserves, which would be a strong rerating catalyst.

Share Price Drivers: