Embed Size (px)

Citation preview

Industry‐Government Partnership ‐

The Asian Experience in Building Energy Infrastructure

ASEAN Conference on Energy 2010, Innovation and

Sustainable Development

October 4, 2010Presented by: Mr. Abdul Nasir Adnan

2005 2006 2007 2008 2009 2010* 2011*

Central Asia 11.4 13.3 12 6.1 2.7 4.7 5.9

East Asia 8.2 9.4 10.4 7.3 5.9 8.3 7.7

South Asia 9.1 9 8.7 6.4 6.5 7.4 8

South-East Asia 5.8 6.1 6.5 4.3 1.2 5.1 5.30

The Pacific 3.1 1.7 5 5.4 2.3 3.7 5.00

Developing Asia 8 8.9 9.6 6.7 5.2 7.5 7.30

GDP Growth Trend 2005 ‐

2011

Source: Asian Development Outlook 2010

Stimulus Plans by Countries

($ billion)

Georgia 19.92 Thailand 17.22 Kazakhstan 13.83 People's Rep. of China 13.30 Viet Nam 9.68 Rep. of Korea 6.56 Singapore 5.71 Malaysia 5.67 Hong Kong, China 5.22 Philippines 4.40 Taipei,China 4.04 India 3.53 Indonesia 1.40 Bangladesh 1.38 Sri Lanka 1.02 Average 7.53

Source: Asian Development Bank

Composition of Fiscal Packages

Fiscal Packages

Advanced economies

Developing and emerging

economiesEmployment measures 2.90 0.20Infrastructure spending 14.90 46.50Tax cuts 34.10 3.00Transfers to low income households 10.80 6.80Other spending 37.20 43.50

Source: s. Khatiwada. 2009. Stimulus Packages to Counter Global Economic Crisis: A Review. International Institute for Labour Studies Discussion Paper 196/2009.

Energy Production & Consumption

World Energy Production & Consumption

Sourcces: History: Energy Information Administration (EIA), International Energy Annual 2006 (June-December 2008).

Projected Energy Consumption

Source: Annual Energy Review 2008,

June 2009

Projection of World Consumption of Marketed Energy Use by Fuel Type

Source: 2010 International Energy Outlook, U.S. Department of Energy, Energy Information Administration

Project Investment Ranked by Region, 1990–2005

REGION INVESTMENT VALUE (US$M)

Latin America & Carribean 407,202

East Asia & Pacific 224,194

Europe and Central Asia 182,449

South Asia 70,435

Middle East & North Africa 41,163

Sub‐Saharan Africa 36,510

Source: Public‐Private Infrastructure Advisory Facility (PPIAF), World Bank.

Top 10 Countries by Investment, 1990–2005

COUNTRY INVESTMENT VALUE (US$M)

BRAZIL 169,363

ARGENTINA 72,833

P.R. OF CHINA 72,468

MEXICO 70,205

INDIA 51,432

MALAYSIA 47,516

PHILLIPPINES 36,624

INDONESIA 32,624

RUSSIA (FEDERATION) 32,056

TURKEY 30,270

Source: PPIAF, World Bank

Top 6 Countries by Private Investment, 1984–2005

COUNTRY PERCENTAGE INVESTMENT ( %)

P.R OF CHINA 25.3

INDIA 17.0

MALAYSIA 15.5

PHILLIPPINES 10.9

THAILAND 10.5

INDONESIA 8.8

OTHERS 11.2

TOTAL 100

Source: PPIAF, World Bank

Top 10 Countries by Projects, 1990–2005

COUNTRY NUMBER OF PROJECTS

P.R OF CHINA 483

BRAZIL 297

RUSSIA 284

ARGENTINA 182

INDIA 172

MEXICO 151

Chile 103

COLOMBIA 90

MALAYSIA 87

THAILAND 84

Source: PPIAF, World Bank.

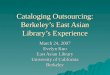

Primary Sectors Ranked by Number of Projects in the World, 1990–2005

SECTOR NUMBER OF PROJECTS

ENERGY 1,307

TRANSPORT 829

TELECOMMUNICATIONS 749

WATER & SEWERAGE 383

Source: PPIAF, World Bank.

Investment Commitments to Infrastructure Project with Private Participation in Developing Countries by Sector, 1990–2005

Sources: World Bank and PPIAF, PPI Project database

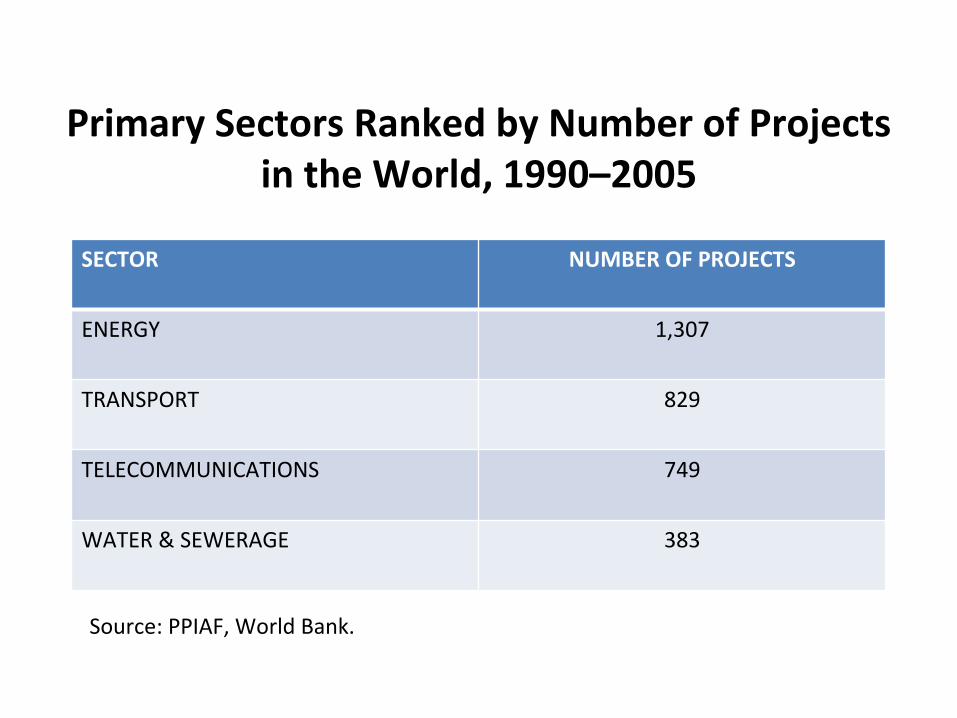

ENERGY SOURCES IN ASEAN

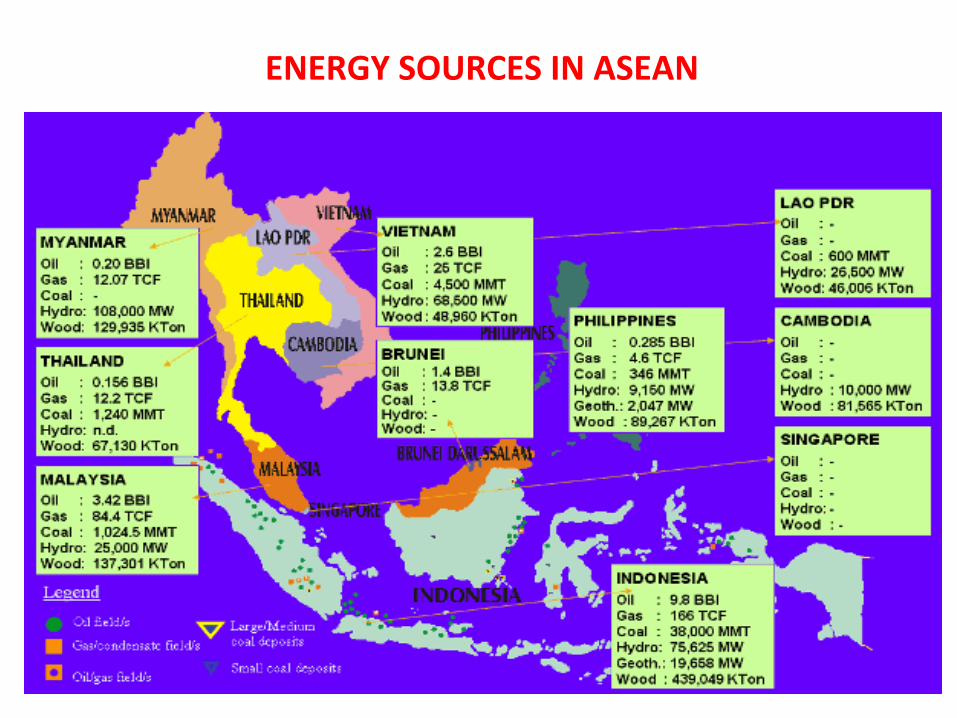

Map of TAGP

TRANS‐ASEAN GAS PIPELINE

Map of ASEAN Power Grid

ASEAN POWER GRID

“ PRIVATE FUNDED RENEWABLE ENERGY PROJECT FOR

SUSTAINABILITY & VALUE CREATION ‐

: THE MALAYSIAN

EXPERIENCE ”

SOURCES OF WASTE

DELIMMA OF SOLID WASTE MANAGEMENT IN MALAYSIA

“SOLID WASTE COLLECTION IS SATISFACTORY BUT THE DISPOSAL

SYSTEM IS LARGELY BY CONTROLLED TIPPING AND BURNING.

THE DISPOSAL OF SOLID WASTE IS A PROBLEM LIKE THOSE IN

ANY COUNTRIES AND

AN ORGANIZED PROGRAMME IN THIS

DIRECTION IS NEEDED. THE LOCAL AUTHORITIES IN MANY

CASES ARE HAMPERED BY LACK OF TRAINED EXPERIENCED

PERSONNEL, FINANCIAL RESOURCES, AND KNOWLEDGE OF

THE EFFECTS OF HEALTH.”

(Ref: Malaysia, Government of (1971). Report of the Government of Malaysia for the

UN Conference on Human Environment. April 1.p.10)

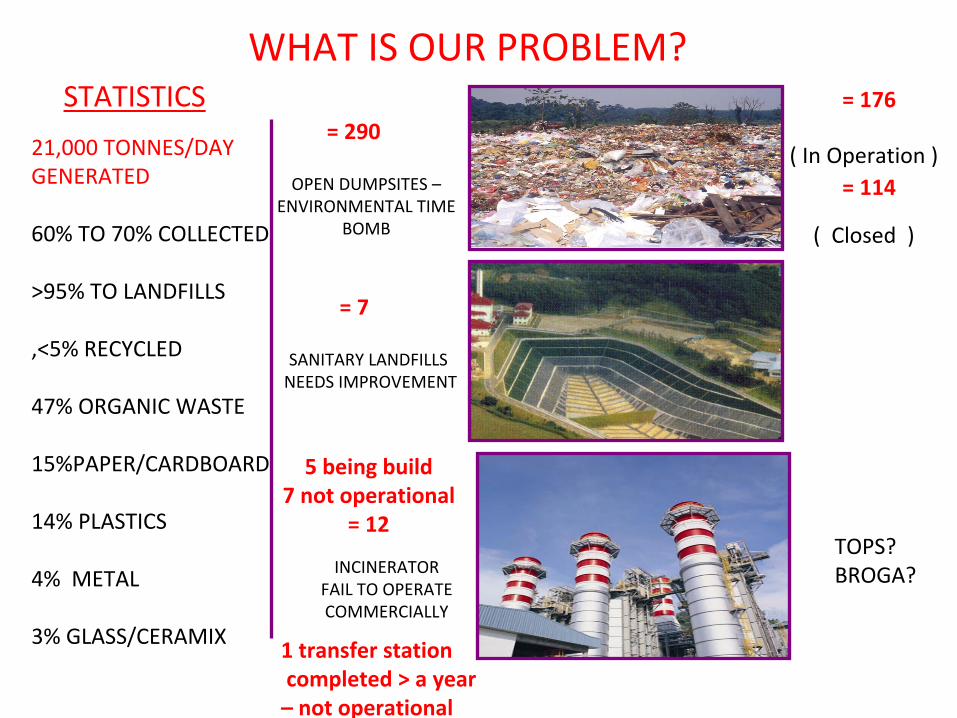

WHAT IS OUR PROBLEM?

OPEN DUMPSITES –

ENVIRONMENTAL TIME

BOMB

SANITARY LANDFILLSNEEDS IMPROVEMENT

INCINERATOR FAIL TO OPERATE

COMMERCIALLY

= 290

= 7

5 being build7 not operational

= 12

STATISTICS

21,000 TONNES/DAYGENERATED

60% TO 70% COLLECTED

>95% TO LANDFILLS

,<5% RECYCLED

47% ORGANIC WASTE

15%PAPER/CARDBOARD

14% PLASTICS

4% METAL

3% GLASS/CERAMIX

= 176

= 114( In Operation )

( Closed )

1 transfer station completed > a year–

not operational

TOPS?BROGA?

UNSUSTAINABLE MANAGEMENT OF MSW

FOUL

SMELL/UNSIGHTLY

VIEWS

LEACHATE

POTENTIAL ENERGY

LANDFILLGAS FIRES

UNHYGIENIC

ENVIRONMENT

ILLEGALBURNING

NATIONAL STRATEGIC PLAN

FOR PERIOD 2004‐ 2020

FACILITY TYPE AND NUMBERS

ESTIMATED COST

o CAPEX – RM 15.6 BILLION

o OPEX – RM 14.4 BILLION

TYPE NUMBERSSANITARY LANDFILL 22 SITESTRANSFER STATION 45 STATIONSMRF 7 FACILITIESTHERMAL TREATMENT PLANT

6 +2

22

45

7

8

COMMERCIAL RRC/WTE FACILITY (700 TONS/DAY)

“INTEGRATED SOLID WASTE MANAGEMENT FACILITY”

THE RRC‐WTE FACILITY

EFFLUENT TREATMENT

PLANT

ENERGY RECOVERY

MATERIAL RECOVERY

SUSTAINABLE and FULL PRIVATE FUNDING

Sanitary Landfill Incineration Transfer station

+ +

Mechanical Biological Thermal

( INTEGRATED )

PRIVA

TE FUNDIN

G

( STAND ALONE )

PUBLIC FUNDING

IMPACT ON LAND USE & ENVIRONMENT

OPEN DUMPSITE IN

SUNGAI KEMBONG

SUNGAI LALANG SITE

BEFORE

CONSTRUCTION OF

THE FACILITY

COMMERCIAL FACILITY OFWASTE TO ENERGY PLANT

BEFORE

AFTER

ENVIRONMENTAL DEGRADATION CONTROLLED

FOUL

SMELL/UNSIGHTLY

VIEWS

LEACHATE

POTENTIAL ENERGY

LANDFILLGAS FIRES

UNHYGIENIC

ENVIRONMENT

ILLEGALBURNING

S O L V

E D

GENERATE RENEWABLE ENERGY

POWER PLANT BOILER

TURBINE GENERATOR

POLLUTION CONTROL SYSTEM

CHIMNEY WITH CEMs SYSTEM

REDUCE CARBON FOOTPRINT

0.58 kg

CO2/kWh

0.138 kg

CO2/kWh

CONVENTIONAL POWER PLANT RDF POWER PLANT

LEACHATELEACHATE -- TREATED TO STANDARD A TREATED TO STANDARD A QUALITY QUALITY

Treated Leachate Water Treated Leachate Water USEDUSED and and REUSEDREUSED for lorry and plant for lorry and plant washing.washing.

REUSE AND RECYCLEREUSE AND RECYCLE

Film Plastic Resin Products

. Organics to composting. Organics to composting

. Recover . Recover METALS, PLASTICS, RECYCLABLESMETALS, PLASTICS, RECYCLABLES

RECYCLABLESRECYCLABLES

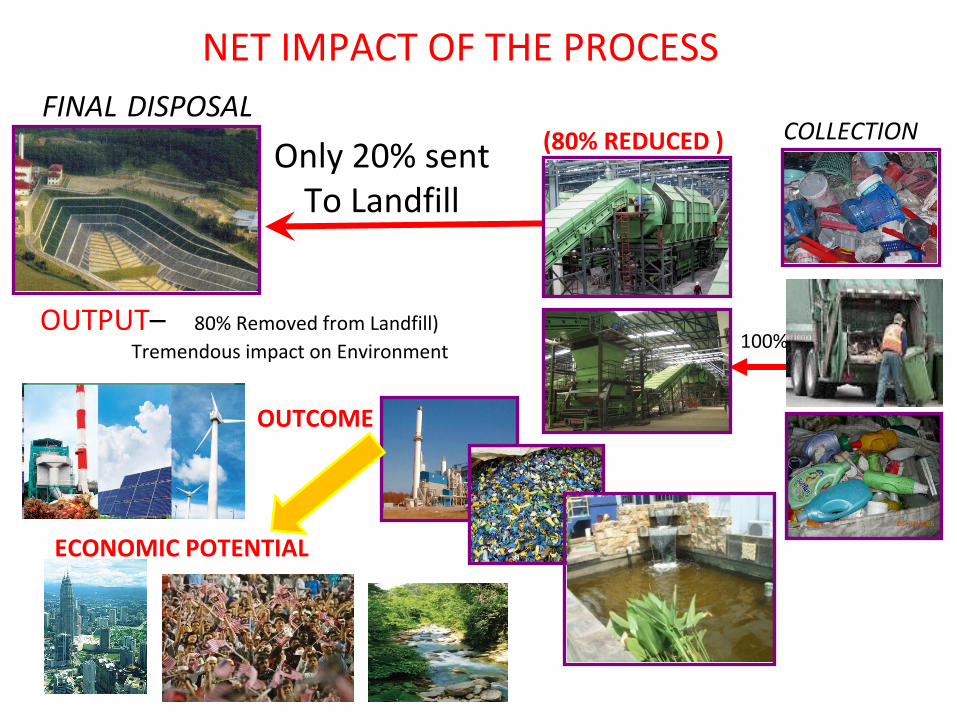

NET IMPACT OF THE PROCESS

COLLECTIONFINAL

DISPOSAL

100%

Only 20% sentTo Landfill

(80% REDUCED )

ECONOMIC POTENTIAL

OUTPUT–

80% Removed from Landfill)

Tremendous impact on Environment

OUTCOME

OUTPUT AND OUTCOME

INTANGIBLESTANGIBLES

Recover and Recycle Resources

Renewable Energy

Better Use of Land than Landfill

Jobs/Businesse

s

Beautiful Environment

Avoid Future Environment Cleanup

Healthy SocietySOCIETY

ENERGY

ECONOMY ENVIRONMENT

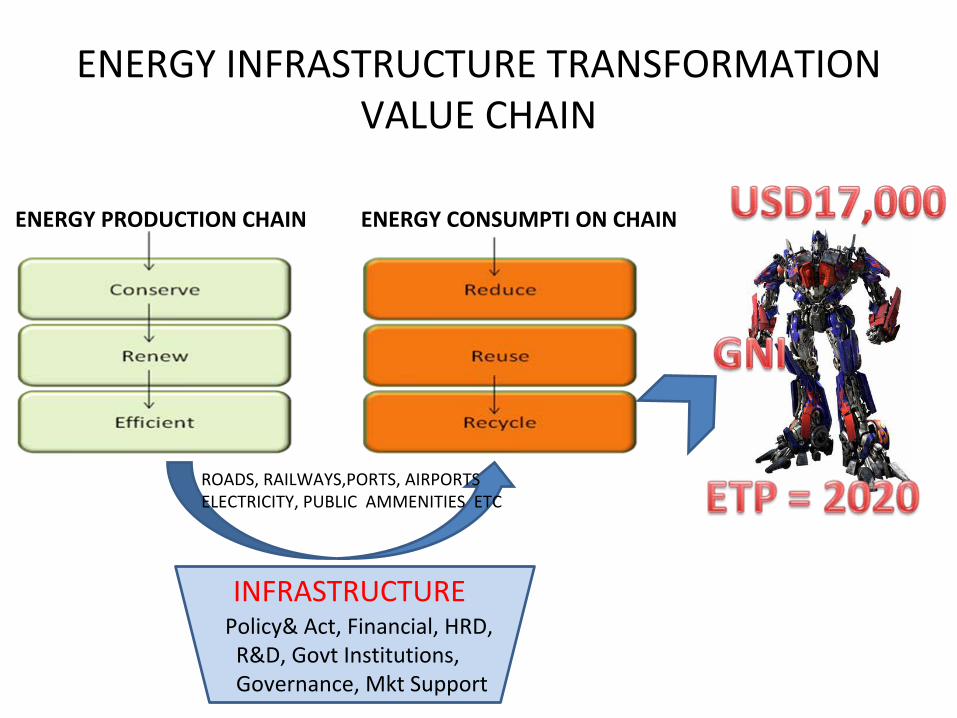

THE WAY FORWARD – THE BIG PICTURE

RM 30 Billion + RM4 Billion( Redeployment)

(Injection)

POLITICAL WILL

MINDSET CHANGE

+

Malaysian Experience

Soft Infrastructure• Policy and Act • Financial• HRD• R&D• Gov Institutions and governance• Market support

Hard Infrastructure

ENERGY INFRASTRUCTURE TRANSFORMATION VALUE CHAIN

ENERGY PRODUCTION CHAIN ENERGY CONSUMPTI ON CHAIN

Policy& Act, Financial, HRD,R&D, Govt Institutions,Governance, Mkt Support

INFRASTRUCTURE

ROADS, RAILWAYS,PORTS, AIRPORTSELECTRICITY, PUBLIC AMMENITIES ETC

Malaysian Experience

Soft Infrastructure• Policy and Act

‐

Integrated

policy

not

contravening

other

policies

set

by

governments.

Policy

executed

in

silos

by

different

government

agencies

serving

their

own

agencies

needs

rather

than

the

broad

and

integrated

country

needs.

Eg

Science

&Technology

Policy

encouraged

local

technology

development

thru

R&D,

RE

and

Solid

Waste

Policy

and

Act

should

give

a

relevant

recognition

and

priorities to address, facilitate and make it happen.

‐

Need

a

clear

policy

nationwide

and

well

integrated

for

local

technology to be developed at R&D, Pilot, Trail and Demonstration

Scale,

to

nurture

the

local

technology

with

final

objectives

of

implementing and exporting them.

Malaysian Experience

• Financial

‐

Must have a good and able financial support institutions.‐

Able

to

take

risks.

E,g

Venture

capital

failure

in

understanding the project merits.‐

Combination of Equity, Venture Capital, Commercial Loans,

Development

Bank

Loan

and

Risk

Guarantee

Mechanisms/Credit

Guarantee

Schemes

,

Vendors

Financing

Scheme should be made available.‐

Continuous development of the capital markets, products in

place.‐

Clear

understanding

between

funders,

lenders

operators,

and government officers the new PPP procurement methods.

Soft Infrastructure

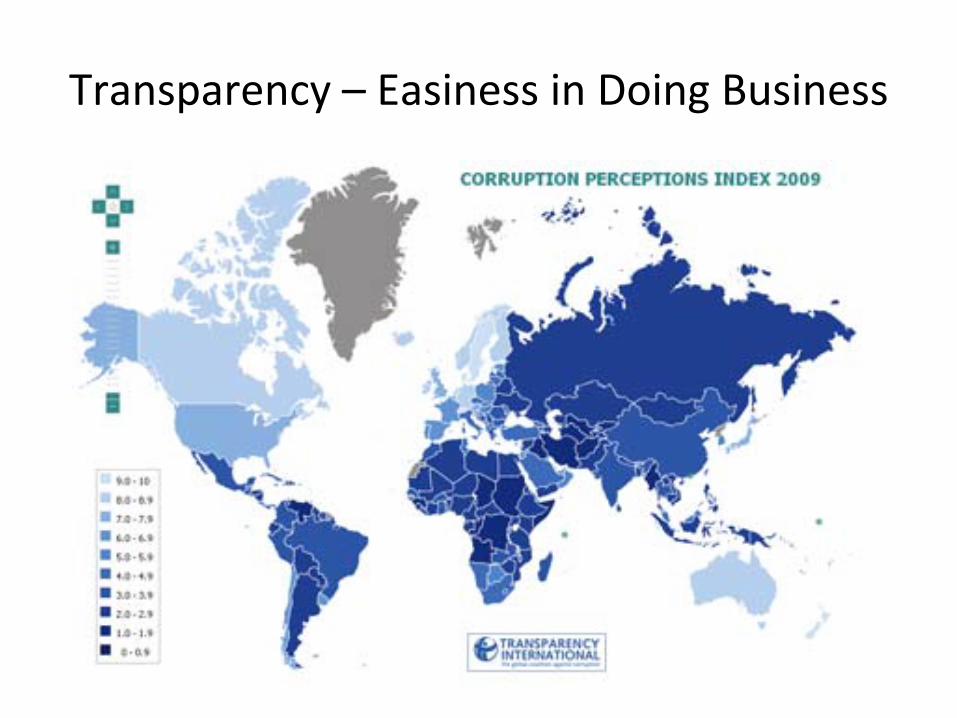

Transparency – Easiness in Doing Business

Corruption Perceptions Index

Country Rank 2001 2005 2009

PR China 57 78 79

India 71 88 84

Bangladesh 91 158 139

Pakistan 79 144 139

Thailand 61 59 84

Singapore 4 5 3

Phillippines 65 117 139

Vietnam 75 107 120

Malaysia 36 39 56

Indonesia 88 137 111

Japan 21 21 17

Source: Transparency International

Malaysian Experience

Soft Infrastructure• Human Resource Development

‐

Human

capital

capabilities

in

practical

and

detail S&T

not

yet

available,

especially

at

technical

scale

(most of our champions resides in the lab)

‐

Government

must

pay

to

this

effort

by

leveraging government

R&D

and

Universities

to

interact

with

private

by

virtue

of

attachments,

OJT,

etc

over

the project development/management period

Malaysian Experience

Soft Infrastructure• Human Resource Development‐

No

local

engineering

capabilities/

consultants/

universities/

research

assistants

in

process

engineering e.g boilers have to be designed overseas.

‐

Ability

to

rate

technology

and

financial

viability

of

energy

projects

e.g

technical due

diligence

by

outsiders.

Government insist

on

Local

teams

but

evaluation

has

been

delayed

for

an

unreasonable

time

due

to

inexperience

and

lack of knowledge in the said technology.

Malaysian Experience

Soft Infrastructure• Research & Development

‐

Local

R&D

are

very

lab

oriented,

due

to

weak

HR above,

relatively

rigid

government

procedures

not

giving

opportunities

for

free

flow

of

staff

and knowledge between private and public sector

‐

Funding and Research Scientist Engineers need to be enhanced by many fold.

Malaysian Experience

Soft Infrastructure• Government Institutions and governance

‐

Vested interest serving certain quarters and working in silos

‐

To have a clear role of government and private, concept of

PFI (success of ETP depends on the PPP…92% private).

‐

Lack

of

understanding

in

the

global

view

e.g

fighting

between the advantage of landfill vs MRF vs RDF/RE

‐

Establishment

of

a

capable

technical

and

financial

rating

agency

badly

needed

for

technology

and

investment

assessment

Malaysian Experience

Soft Infrastructure• Market support

‐

Allow fair competition, less politicking/political intervention

Malaysian ExperienceHard Infrastructure

• Industrial Capabilities and Support‐

Local

capabilities

in

engineering

are

good

but

lack

the

process

engineering and scaling up experience

• Physical Infrastructure‐

Physical infra like roads, waste disposal sites, utilities ‐

normal

• TechnologiesLocal

technological

development

should

be

given

priorities

to

be

developed, supported and nurtured till success

‐

STAKEHOLDERS ROUNDTABLE

Regular & ContinuousConsultation & Feedback

ENERGY DEMAND TREND 2006 ‐

2030

• The trend between 2006 and 2030, on current trends under a

“baseline”

scenario,

world

energy

demand*

will

increase

by

47

per

cent

to

17.7

billion

toe,

with

the

Asia‐Pacific**

region

accounting

for

almost

50

per

cent

of

the

total

global

energy

demand in 2030.

• If

countries

in

the

region

were

to

change

their

policies

and

embark on more sustainable energy paths, this demand could

be contained to 7.7 billion toe and requires $375 billionannually—over $9 trillion in total

• Note:* growth rate provided by IEA** growth rate provided by Institute of Energy Economics

WAY FORWARD

• There could be a wide supply‐demand gap due to tight supplies

and

high

prices

and

the

region’s

economic

powers

are

concerned

about

energy

security

which will pose constrain on economic growth

• The

cost

of

expanding

and

modernizing

the

region’s energy

systems

on

the

baseline

scenario

expected

at

$375

billion

annually—over

$9

trillion

in

total. Financing is of major concern.

WAY FORWARD

• The

authorities

should

design

strategies

to

reduce energy

demand

(via

EE),

secure

additional

energy

supplies, move towards more sustainable technologies and

fuel

types,

and

hence

build

the

necessary

infrastructure

• This

call

for

a

greater

partnership

inclusiveness between the Industry and Government to achieve the goal.

THANK YOU