Embed Size (px)

Citation preview

Industry Monitor The EUROCONTROL bulletin on air transport trends

Issue N°159. 31/01/2014

Average daily European flights decreased by 0.8% in 2013. Preliminary data for January show a 2.3% increase in traffic on January 2013.

AEA figures for 2013: traffic (RPK) increased by 1.6%, an additional 5.6 million passengers on 2012. The average load factor was up 0.8 percentage point to an all-time high 79.9% and capacity growth (ASK) was up 1.7%.

IATA expects oil prices to reduce from an average of €80 per barrel in 2013 to €77 per barrel in 2014.

Oil prices were slightly down to €78.5 per barrel in January.

EUROCONTROL statistics and forecasts 1 Other statistics and forecasts 2 Passenger airlines 3 Airports 6 Aircraft manufacturing 7 Regulation 8 Fares 8 Oil 8

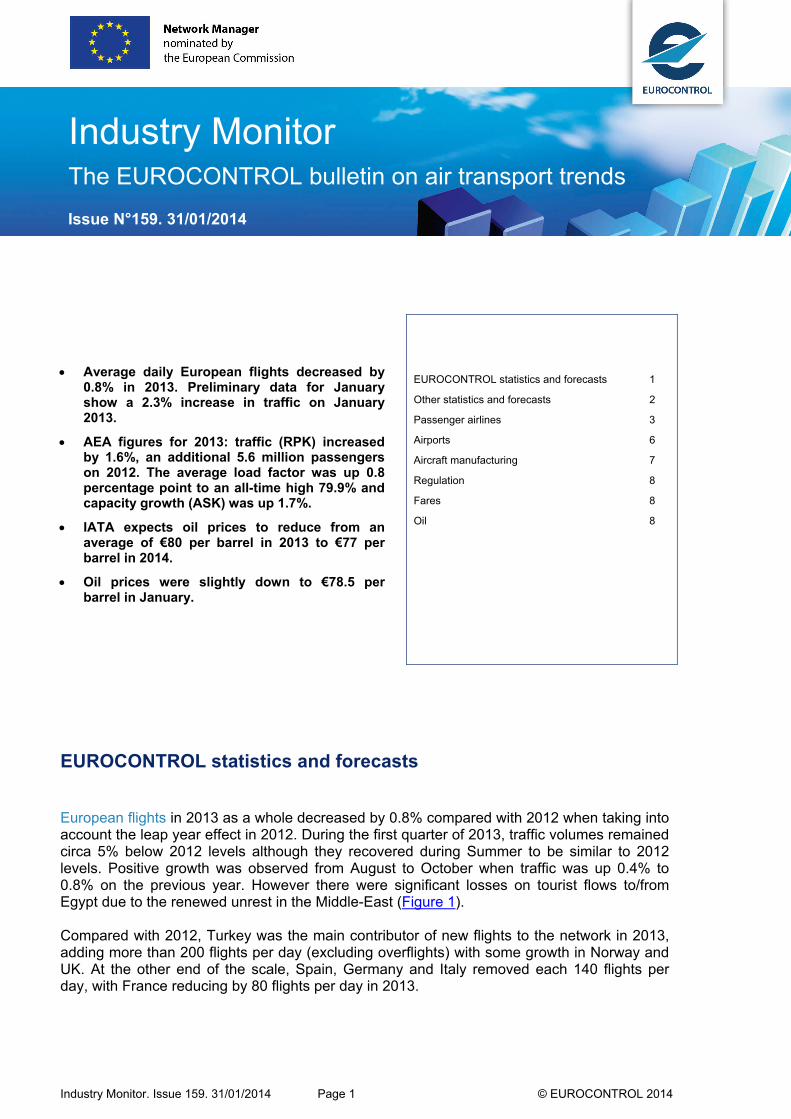

EUROCONTROL statistics and forecasts European flights in 2013 as a whole decreased by 0.8% compared with 2012 when taking into account the leap year effect in 2012. During the first quarter of 2013, traffic volumes remained circa 5% below 2012 levels although they recovered during Summer to be similar to 2012 levels. Positive growth was observed from August to October when traffic was up 0.4% to 0.8% on the previous year. However there were significant losses on tourist flows to/from Egypt due to the renewed unrest in the Middle-East (Figure 1). Compared with 2012, Turkey was the main contributor of new flights to the network in 2013, adding more than 200 flights per day (excluding overflights) with some growth in Norway and UK. At the other end of the scale, Spain, Germany and Italy removed each 140 flights per day, with France reducing by 80 flights per day in 2013.

Industry Monitor. Issue 159. 31/01/2014 Page 1 © EUROCONTROL 2014

Figure 1: Monthly European Traffic and Forecast.

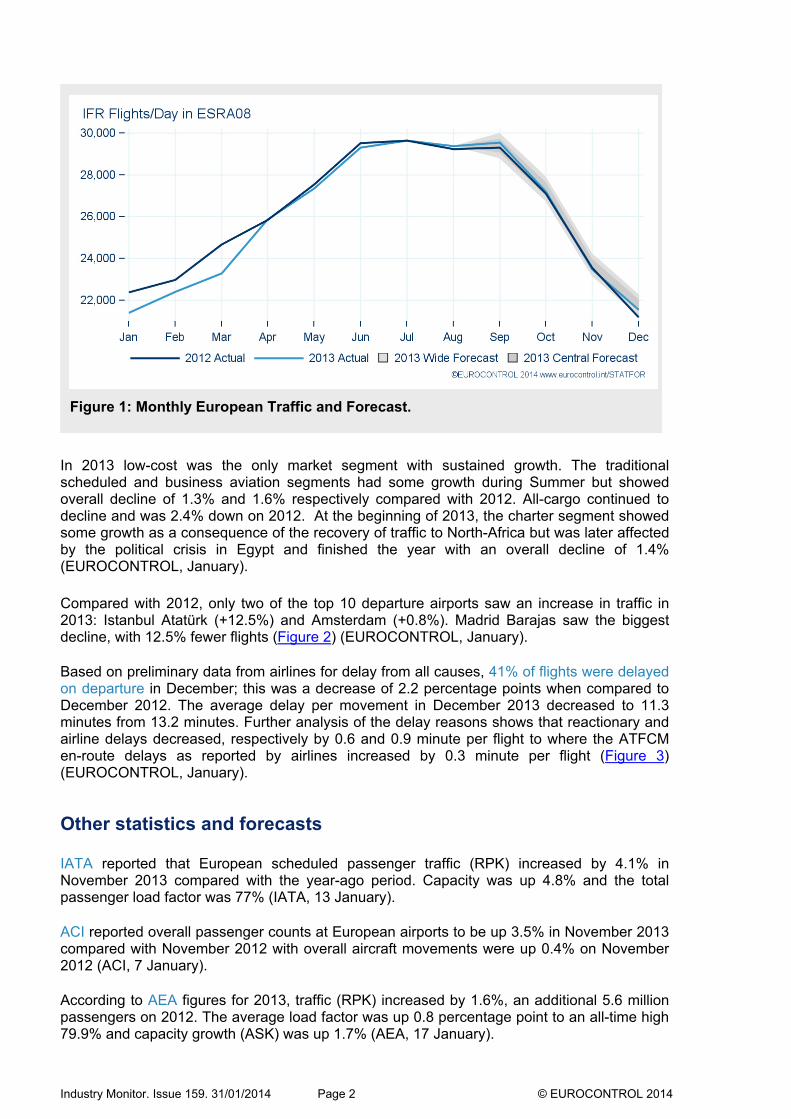

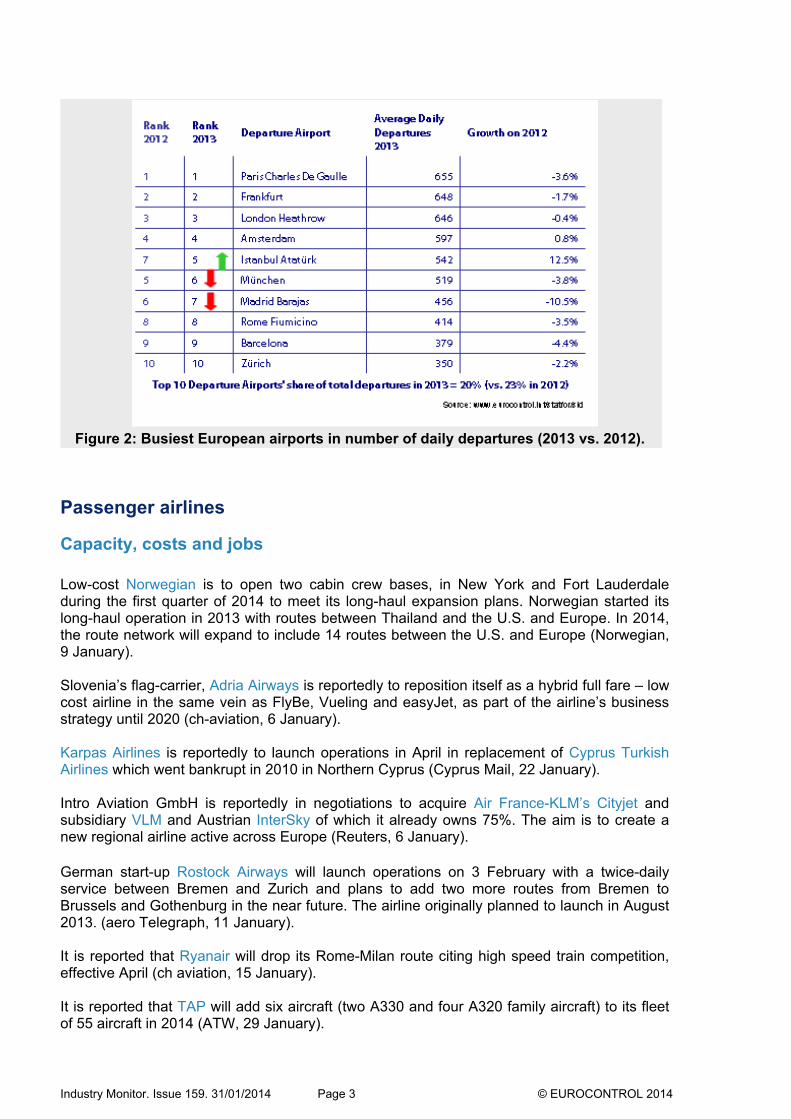

In 2013 low-cost was the only market segment with sustained growth. The traditional scheduled and business aviation segments had some growth during Summer but showed overall decline of 1.3% and 1.6% respectively compared with 2012. All-cargo continued to decline and was 2.4% down on 2012. At the beginning of 2013, the charter segment showed some growth as a consequence of the recovery of traffic to North-Africa but was later affected by the political crisis in Egypt and finished the year with an overall decline of 1.4% (EUROCONTROL, January). Compared with 2012, only two of the top 10 departure airports saw an increase in traffic in 2013: Istanbul Atatürk (+12.5%) and Amsterdam (+0.8%). Madrid Barajas saw the biggest decline, with 12.5% fewer flights (Figure 2) (EUROCONTROL, January). Based on preliminary data from airlines for delay from all causes, 41% of flights were delayed on departure in December; this was a decrease of 2.2 percentage points when compared to December 2012. The average delay per movement in December 2013 decreased to 11.3 minutes from 13.2 minutes. Further analysis of the delay reasons shows that reactionary and airline delays decreased, respectively by 0.6 and 0.9 minute per flight to where the ATFCM en-route delays as reported by airlines increased by 0.3 minute per flight (Figure 3) (EUROCONTROL, January).

Other statistics and forecasts IATA reported that European scheduled passenger traffic (RPK) increased by 4.1% in November 2013 compared with the year-ago period. Capacity was up 4.8% and the total passenger load factor was 77% (IATA, 13 January). ACI reported overall passenger counts at European airports to be up 3.5% in November 2013 compared with November 2012 with overall aircraft movements were up 0.4% on November 2012 (ACI, 7 January). According to AEA figures for 2013, traffic (RPK) increased by 1.6%, an additional 5.6 million passengers on 2012. The average load factor was up 0.8 percentage point to an all-time high 79.9% and capacity growth (ASK) was up 1.7% (AEA, 17 January).

Industry Monitor. Issue 159. 31/01/2014 Page 2 © EUROCONTROL 2014

Figure 2: Busiest European airports in number of daily departures (2013 vs. 2012).

Passenger airlines

Capacity, costs and jobs Low-cost Norwegian is to open two cabin crew bases, in New York and Fort Lauderdale during the first quarter of 2014 to meet its long-haul expansion plans. Norwegian started its long-haul operation in 2013 with routes between Thailand and the U.S. and Europe. In 2014, the route network will expand to include 14 routes between the U.S. and Europe (Norwegian, 9 January). Slovenia’s flag-carrier, Adria Airways is reportedly to reposition itself as a hybrid full fare – low cost airline in the same vein as FlyBe, Vueling and easyJet, as part of the airline’s business strategy until 2020 (ch-aviation, 6 January). Karpas Airlines is reportedly to launch operations in April in replacement of Cyprus Turkish Airlines which went bankrupt in 2010 in Northern Cyprus (Cyprus Mail, 22 January). Intro Aviation GmbH is reportedly in negotiations to acquire Air France-KLM’s Cityjet and subsidiary VLM and Austrian InterSky of which it already owns 75%. The aim is to create a new regional airline active across Europe (Reuters, 6 January). German start-up Rostock Airways will launch operations on 3 February with a twice-daily service between Bremen and Zurich and plans to add two more routes from Bremen to Brussels and Gothenburg in the near future. The airline originally planned to launch in August 2013. (aero Telegraph, 11 January). It is reported that Ryanair will drop its Rome-Milan route citing high speed train competition, effective April (ch aviation, 15 January). It is reported that TAP will add six aircraft (two A330 and four A320 family aircraft) to its fleet of 55 aircraft in 2014 (ATW, 29 January).

Industry Monitor. Issue 159. 31/01/2014 Page 3 © EUROCONTROL 2014

Breakdown of average delay per flight

Percentage of flights delayed on departure

Figure 3: Delay Statistics (all causes, airline-reported delay – preliminary data for December 2013).

Polish charter Bingo Airways is reportedly planning to launch scheduled flights in 2014 (ch-aviation, 6 January). State-owned Montenegro Airlines is reportedly to be privatised in the course of 2014. The first attempt to sell the company failed in 2010 (Ex-YU Aviation News, January) Croatian government is reportedly to sell 49% of Croatia Airlines (Ex-YU Aviation News, January).

Routes, Alliances, Codeshares Air Méditerranée is reportedly planning to launch 11 new routes in its Summer 2014 season. Five routes from Charles de Gaulle to Palma, Ibiza, Menorca, Split, Agadir. Two routes from Marseille to Malaga and Palma. Two routes from Lyon to Malaga and Ibiza and two routes from Nantes to Menorca and Agadir (routesonline, 20 January). Air Europa and Etihad signed a codeshare agreement for direct flights from Madrid to Abu Dhabi. Air Europa will place its code on Ethiad’s service from Abu Dhabi to Amsterdam, Brussels and Malpensa whereas Etihad will place its code on Air Europa services from Madrid to Amsterdam, Barcelona, Brussels, Malpensa and Palma de Mallorca. Codeshare destinations will be expanded in summer 2014 to include Air Europa services to South America from Madrid and Etihad services to Asia, Africa, Australia and the Gulf region (Etihad, 20 January). Air Serbia is to expand its network with six new routes from Belgrade to Beirut, Budapest, Sofia, Varna and Warsaw during the first half of 2014 (Air Serbia, 13 January). Ryanair will open three new bases in April as follows: (1) Athens with two based aircraft and six new routes to Chania, London, Milan, Paphos, Rhodes and Thessaloniki. (2) Thessaloniki with one based aircraft and three new routes to Athens, Pisa and Warsaw. (3) Lisbon with one based aircraft and four new routes to Dole, Manchester, Marseille and Pisa (Ryanair, 14 and 24 January).

Industry Monitor. Issue 159. 31/01/2014 Page 4 © EUROCONTROL 2014

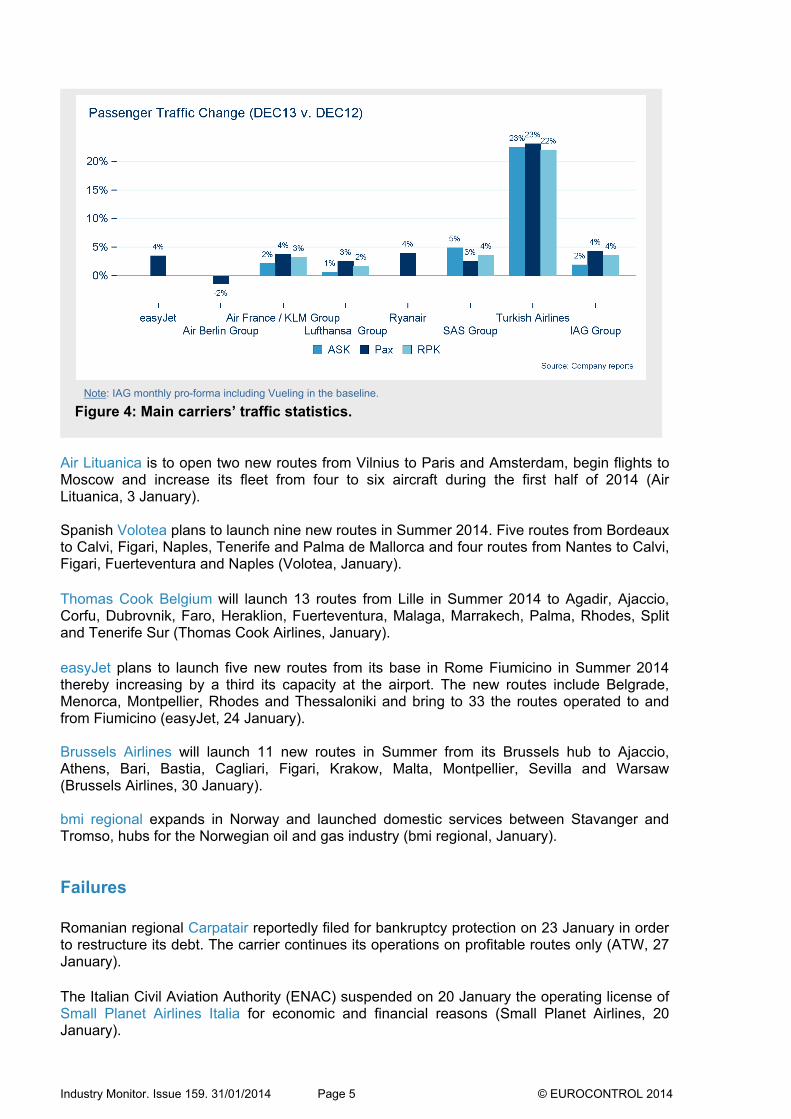

Note: IAG monthly pro-forma including Vueling in the baseline.

Figure 4: Main carriers’ traffic statistics.

Air Lituanica is to open two new routes from Vilnius to Paris and Amsterdam, begin flights to Moscow and increase its fleet from four to six aircraft during the first half of 2014 (Air Lituanica, 3 January). Spanish Volotea plans to launch nine new routes in Summer 2014. Five routes from Bordeaux to Calvi, Figari, Naples, Tenerife and Palma de Mallorca and four routes from Nantes to Calvi, Figari, Fuerteventura and Naples (Volotea, January). Thomas Cook Belgium will launch 13 routes from Lille in Summer 2014 to Agadir, Ajaccio, Corfu, Dubrovnik, Faro, Heraklion, Fuerteventura, Malaga, Marrakech, Palma, Rhodes, Split and Tenerife Sur (Thomas Cook Airlines, January). easyJet plans to launch five new routes from its base in Rome Fiumicino in Summer 2014 thereby increasing by a third its capacity at the airport. The new routes include Belgrade, Menorca, Montpellier, Rhodes and Thessaloniki and bring to 33 the routes operated to and from Fiumicino (easyJet, 24 January). Brussels Airlines will launch 11 new routes in Summer from its Brussels hub to Ajaccio, Athens, Bari, Bastia, Cagliari, Figari, Krakow, Malta, Montpellier, Sevilla and Warsaw (Brussels Airlines, 30 January). bmi regional expands in Norway and launched domestic services between Stavanger and Tromso, hubs for the Norwegian oil and gas industry (bmi regional, January).

Failures Romanian regional Carpatair reportedly filed for bankruptcy protection on 23 January in order to restructure its debt. The carrier continues its operations on profitable routes only (ATW, 27 January). The Italian Civil Aviation Authority (ENAC) suspended on 20 January the operating license of Small Planet Airlines Italia for economic and financial reasons (Small Planet Airlines, 20 January).

Industry Monitor. Issue 159. 31/01/2014 Page 5 © EUROCONTROL 2014

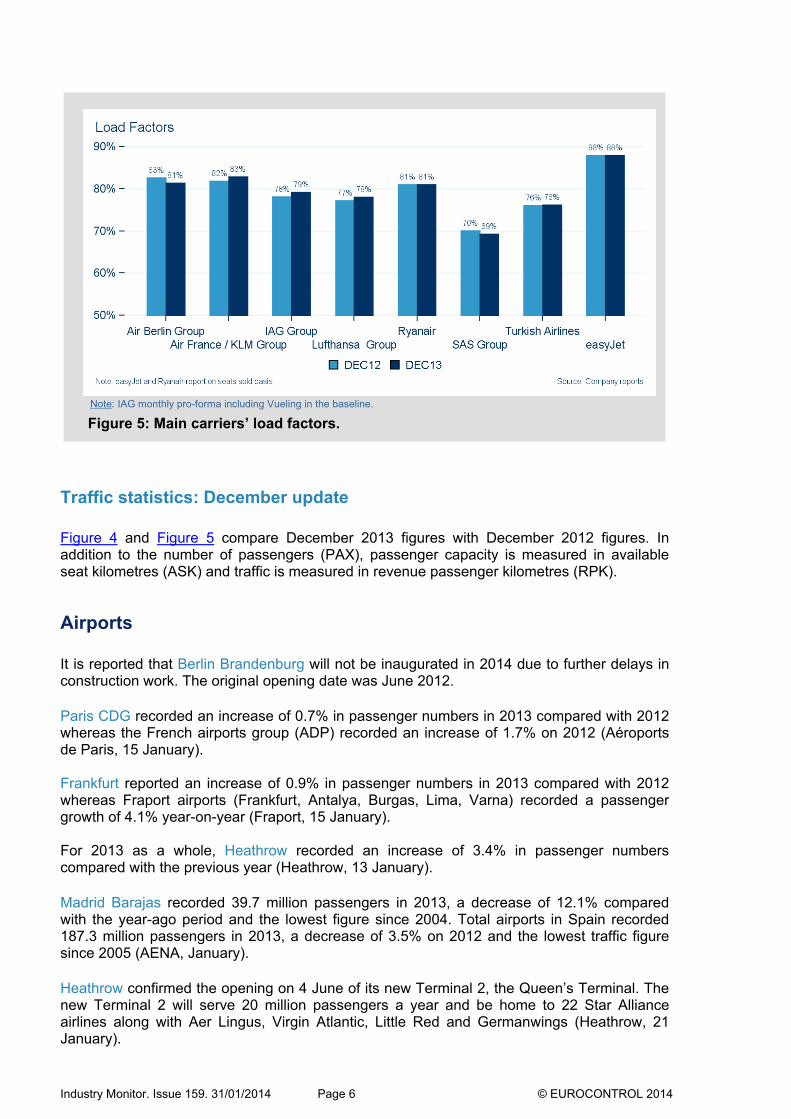

Note: IAG monthly pro-forma including Vueling in the baseline.

Figure 5: Main carriers’ load factors.

Traffic statistics: December update Figure 4 and Figure 5 compare December 2013 figures with December 2012 figures. In addition to the number of passengers (PAX), passenger capacity is measured in available seat kilometres (ASK) and traffic is measured in revenue passenger kilometres (RPK).

Airports It is reported that Berlin Brandenburg will not be inaugurated in 2014 due to further delays in construction work. The original opening date was June 2012. Paris CDG recorded an increase of 0.7% in passenger numbers in 2013 compared with 2012 whereas the French airports group (ADP) recorded an increase of 1.7% on 2012 (Aéroports de Paris, 15 January). Frankfurt reported an increase of 0.9% in passenger numbers in 2013 compared with 2012 whereas Fraport airports (Frankfurt, Antalya, Burgas, Lima, Varna) recorded a passenger growth of 4.1% year-on-year (Fraport, 15 January). For 2013 as a whole, Heathrow recorded an increase of 3.4% in passenger numbers compared with the previous year (Heathrow, 13 January). Madrid Barajas recorded 39.7 million passengers in 2013, a decrease of 12.1% compared with the year-ago period and the lowest figure since 2004. Total airports in Spain recorded 187.3 million passengers in 2013, a decrease of 3.5% on 2012 and the lowest traffic figure since 2005 (AENA, January). Heathrow confirmed the opening on 4 June of its new Terminal 2, the Queen’s Terminal. The new Terminal 2 will serve 20 million passengers a year and be home to 22 Star Alliance airlines along with Aer Lingus, Virgin Atlantic, Little Red and Germanwings (Heathrow, 21 January).

Industry Monitor. Issue 159. 31/01/2014 Page 6 © EUROCONTROL 2014

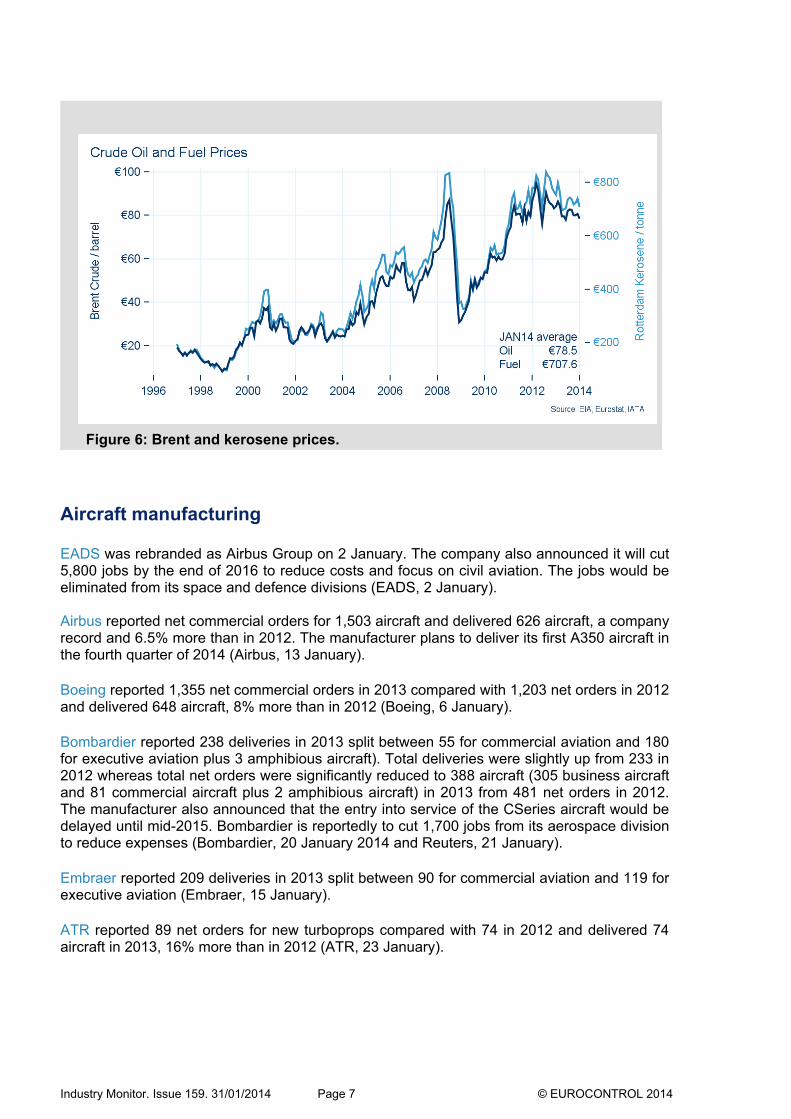

Figure 6: Brent and kerosene prices.

Aircraft manufacturing EADS was rebranded as Airbus Group on 2 January. The company also announced it will cut 5,800 jobs by the end of 2016 to reduce costs and focus on civil aviation. The jobs would be eliminated from its space and defence divisions (EADS, 2 January). Airbus reported net commercial orders for 1,503 aircraft and delivered 626 aircraft, a company record and 6.5% more than in 2012. The manufacturer plans to deliver its first A350 aircraft in the fourth quarter of 2014 (Airbus, 13 January). Boeing reported 1,355 net commercial orders in 2013 compared with 1,203 net orders in 2012 and delivered 648 aircraft, 8% more than in 2012 (Boeing, 6 January). Bombardier reported 238 deliveries in 2013 split between 55 for commercial aviation and 180 for executive aviation plus 3 amphibious aircraft). Total deliveries were slightly up from 233 in 2012 whereas total net orders were significantly reduced to 388 aircraft (305 business aircraft and 81 commercial aircraft plus 2 amphibious aircraft) in 2013 from 481 net orders in 2012. The manufacturer also announced that the entry into service of the CSeries aircraft would be delayed until mid-2015. Bombardier is reportedly to cut 1,700 jobs from its aerospace division to reduce expenses (Bombardier, 20 January 2014 and Reuters, 21 January). Embraer reported 209 deliveries in 2013 split between 90 for commercial aviation and 119 for executive aviation (Embraer, 15 January). ATR reported 89 net orders for new turboprops compared with 74 in 2012 and delivered 74 aircraft in 2013, 16% more than in 2012 (ATR, 23 January).

Industry Monitor. Issue 159. 31/01/2014 Page 7 © EUROCONTROL 2014

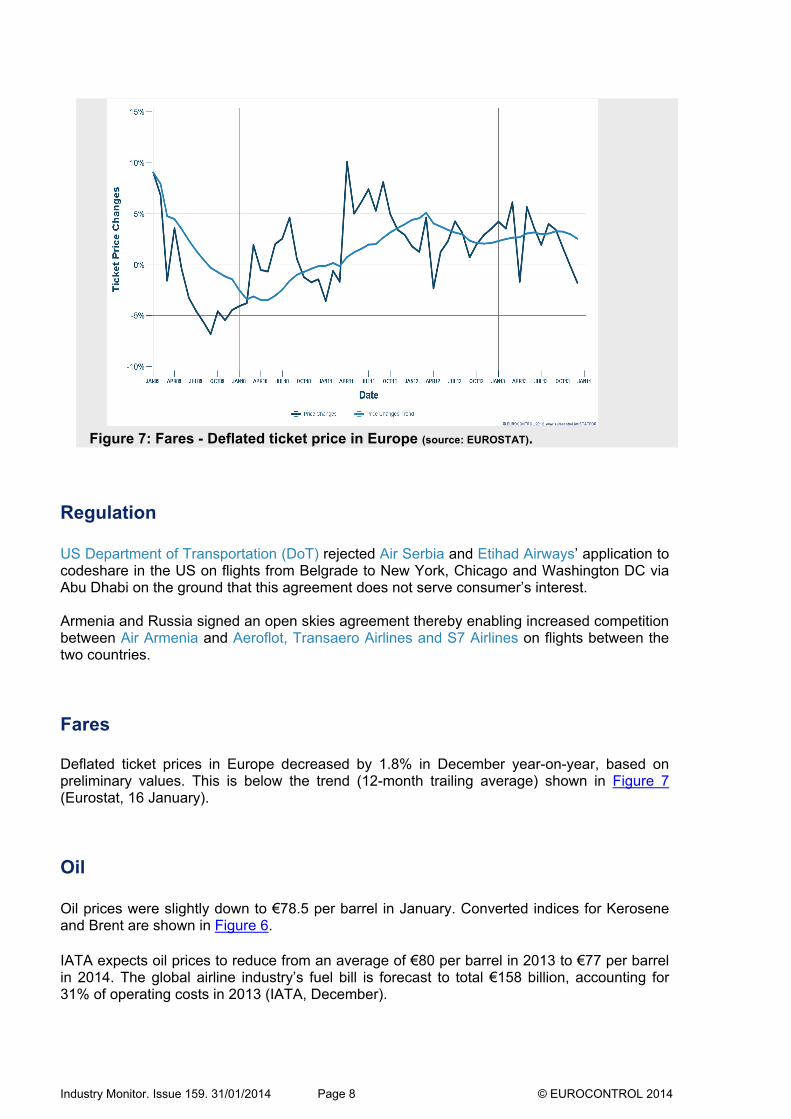

Figure 7: Fares - Deflated ticket price in Europe (source: EUROSTAT).

Regulation US Department of Transportation (DoT) rejected Air Serbia and Etihad Airways’ application to codeshare in the US on flights from Belgrade to New York, Chicago and Washington DC via Abu Dhabi on the ground that this agreement does not serve consumer’s interest. Armenia and Russia signed an open skies agreement thereby enabling increased competition between Air Armenia and Aeroflot, Transaero Airlines and S7 Airlines on flights between the two countries.

Fares Deflated ticket prices in Europe decreased by 1.8% in December year-on-year, based on preliminary values. This is below the trend (12-month trailing average) shown in Figure 7 (Eurostat, 16 January).

Oil Oil prices were slightly down to €78.5 per barrel in January. Converted indices for Kerosene and Brent are shown in Figure 6. IATA expects oil prices to reduce from an average of €80 per barrel in 2013 to €77 per barrel in 2014. The global airline industry’s fuel bill is forecast to total €158 billion, accounting for 31% of operating costs in 2013 (IATA, December).

Industry Monitor. Issue 159. 31/01/2014 Page 8 © EUROCONTROL 2014

Industry Monitor. Issue 159. 31/01/2014 Page 9 © EUROCONTROL 2014

© European Organisation for the Safety of Air Navigation(EUROCONTROL)

This document is published by EUROCONTROL for information purposes.It may be copied in whole or in part, provided that EUROCONTROLis mentioned as the source and it is not used for commercial purposes(i.e. for financial gain). The information in this document may not bemodified without prior written permission from EUROCONTROL.

STATFOR, the EUROCONTROL Statistics and Forecast [email protected]/statfor

2013-

The EUROCONTROL Statistics and Forecast Service (STATFOR)is ISO 9001:2008 certified.

© European Organisation for the Safety of Air Navigation(EUROCONTROL)

This document is published by EUROCONTROL for information purposes.It may be copied in whole or in part, provided that EUROCONTROLis mentioned as the source and it is not used for commercial purposes(i.e. for financial gain). The information in this document may not bemodified without prior written permission from EUROCONTROL.

STATFOR, the EUROCONTROL Statistics and Forecast [email protected]/statfor

2013-2014

The EUROCONTROL Statistics and Forecast Service (STATFOR)is ISO 9001:2008 certified.