Embed Size (px)

Citation preview

November 22, 2018

IMPORTANT DISCLOSURES, INCLUDING ANY REQUIRED RESEARCH CERTIFICATIONS, ARE PROVIDED AT THE END OF THIS REPORT. IF THIS REPORT IS DISTRIBUTED IN THE UNITED STATES IT IS DISTRIBUTED BY CGS-CIMB SECURITIES (USA), INC. AND IS CONSIDERED THIRD-PARTY AFFILIATED RESEARCH.

Powered by the EFA Platform

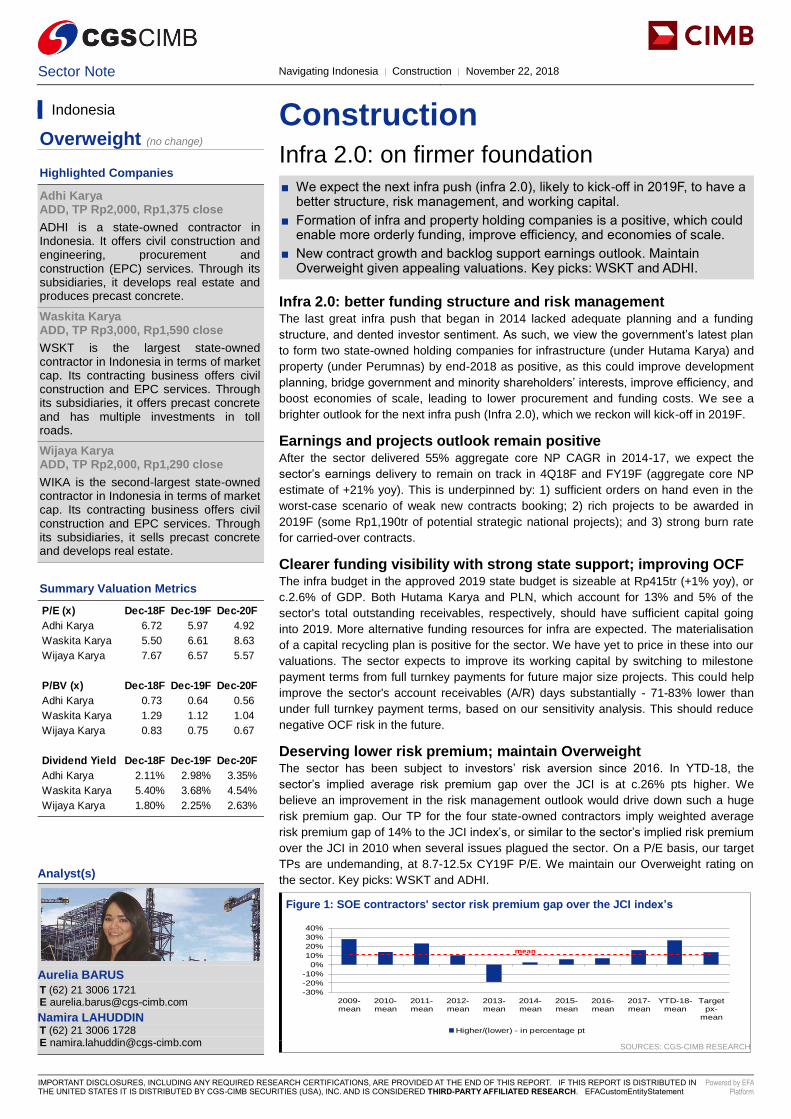

Construction Infra 2.0: on firmer foundation

■ We expect the next infra push (infra 2.0), likely to kick-off in 2019F, to have a better structure, risk management, and working capital.

■ Formation of infra and property holding companies is a positive, which could enable more orderly funding, improve efficiency, and economies of scale.

■ New contract growth and backlog support earnings outlook. Maintain Overweight given appealing valuations. Key picks: WSKT and ADHI.

Analyst(s)

Aurelia BARUS

T (62) 21 3006 1721 E [email protected]

Namira LAHUDDIN T (62) 21 3006 1728 E [email protected]

NA

VIG

AT

IN

G IN

DO

NE

SIA

Navigating Indonesia

Construction and Materials │ Construction │ November 22, 2018

2

TABLE OF CONTENTS

INFRA 2.0: BETTER STRUCTURE AND RISK MANAGEMENT ................................................. 4

EARNINGS OUTLOOK ............................................................................................................... 16

PROJECT PROGRESS AND OUTLOOK ................................................................................... 23

CLEARER FUNDING VISIBILITY AND STATE SUPPORT REMAINS STRONG ..................... 31

PROJECT PAYMENTS ............................................................................................................... 31

VALUATION AND RECOMMENDATION ................................................................................... 38

Sector Note Navigating Indonesia │ Construction │ November 22, 2018

IMPORTANT DISCLOSURES, INCLUDING ANY REQUIRED RESEARCH CERTIFICATIONS, ARE PROVIDED AT THE END OF THIS REPORT. IF THIS REPORT IS DISTRIBUTED IN THE UNITED STATES IT IS DISTRIBUTED BY CGS-CIMB SECURITIES (USA), INC. AND IS CONSIDERED THIRD-PARTY AFFILIATED RESEARCH. EFACustomEntityStatement

Powered by EFA Platform

Construction Infra 2.0: on firmer foundation

■ We expect the next infra push (infra 2.0), likely to kick-off in 2019F, to have a better structure, risk management, and working capital.

■ Formation of infra and property holding companies is a positive, which could enable more orderly funding, improve efficiency, and economies of scale.

■ New contract growth and backlog support earnings outlook. Maintain Overweight given appealing valuations. Key picks: WSKT and ADHI.

Infra 2.0: better funding structure and risk management The last great infra push that began in 2014 lacked adequate planning and a funding

structure, and dented investor sentiment. As such, we view the government’s latest plan

to form two state-owned holding companies for infrastructure (under Hutama Karya) and

property (under Perumnas) by end-2018 as positive, as this could improve development

planning, bridge government and minority shareholders’ interests, improve efficiency, and

boost economies of scale, leading to lower procurement and funding costs. We see a

brighter outlook for the next infra push (Infra 2.0), which we reckon will kick-off in 2019F.

Earnings and projects outlook remain positive After the sector delivered 55% aggregate core NP CAGR in 2014-17, we expect the

sector’s earnings delivery to remain on track in 4Q18F and FY19F (aggregate core NP

estimate of +21% yoy). This is underpinned by: 1) sufficient orders on hand even in the

worst-case scenario of weak new contracts booking; 2) rich projects to be awarded in

2019F (some Rp1,190tr of potential strategic national projects); and 3) strong burn rate

for carried-over contracts.

Clearer funding visibility with strong state support; improving OCF The infra budget in the approved 2019 state budget is sizeable at Rp415tr (+1% yoy), or

c.2.6% of GDP. Both Hutama Karya and PLN, which account for 13% and 5% of the

sector's total outstanding receivables, respectively, should have sufficient capital going

into 2019. More alternative funding resources for infra are expected. The materialisation

of a capital recycling plan is positive for the sector. We have yet to price in these into our

valuations. The sector expects to improve its working capital by switching to milestone

payment terms from full turnkey payments for future major size projects. This could help

improve the sector's account receivables (A/R) days substantially - 71-83% lower than

under full turnkey payment terms, based on our sensitivity analysis. This should reduce

negative OCF risk in the future.

Deserving lower risk premium; maintain Overweight The sector has been subject to investors’ risk aversion since 2016. In YTD-18, the

sector’s implied average risk premium gap over the JCI is at c.26% pts higher. We

believe an improvement in the risk management outlook would drive down such a huge

risk premium gap. Our TP for the four state-owned contractors imply weighted average

risk premium gap of 14% to the JCI index’s, or similar to the sector’s implied risk premium

over the JCI in 2010 when several issues plagued the sector. On a P/E basis, our target

TPs are undemanding, at 8.7-12.5x CY19F P/E. We maintain our Overweight rating on

the sector. Key picks: WSKT and ADHI.

Figure 1: SOE contractors' sector risk premium gap over the JCI index’s

SOURCES: CGS-CIMB RESEARCH

Indonesia

Overweight (no change)

Highlighted Companies

Adhi Karya ADD, TP Rp2,000, Rp1,375 close

ADHI is a state-owned contractor in Indonesia. It offers civil construction and engineering, procurement and construction (EPC) services. Through its subsidiaries, it develops real estate and produces precast concrete.

Waskita Karya ADD, TP Rp3,000, Rp1,590 close

WSKT is the largest state-owned contractor in Indonesia in terms of market cap. Its contracting business offers civil construction and EPC services. Through its subsidiaries, it offers precast concrete and has multiple investments in toll roads.

Wijaya Karya ADD, TP Rp2,000, Rp1,290 close

WIKA is the second-largest state-owned contractor in Indonesia in terms of market cap. Its contracting business offers civil construction and EPC services. Through its subsidiaries, it sells precast concrete and develops real estate.

Summary Valuation Metrics

Insert

Analyst(s)

Aurelia BARUS

T (62) 21 3006 1721 E [email protected]

Namira LAHUDDIN T (62) 21 3006 1728 E [email protected]

P/E (x) Dec-18F Dec-19F Dec-20F

Adhi Karya 6.72 5.97 4.92

Waskita Karya 5.50 6.61 8.63

Wijaya Karya 7.67 6.57 5.57

P/BV (x) Dec-18F Dec-19F Dec-20F

Adhi Karya 0.73 0.64 0.56

Waskita Karya 1.29 1.12 1.04

Wijaya Karya 0.83 0.75 0.67

Dividend Yield Dec-18F Dec-19F Dec-20F

Adhi Karya 2.11% 2.98% 3.35%

Waskita Karya 5.40% 3.68% 4.54%

Wijaya Karya 1.80% 2.25% 2.63%

Title:

Source:

Please fill in the values above to have them entered in your report

-30%

-20%

-10%

0%

10%

20%

30%

40%

2009-mean

2010-mean

2011-mean

2012-mean

2013-mean

2014-mean

2015-mean

2016-mean

2017-mean

YTD-18-mean

Targetpx-

mean

Higher/(lower) - in percentage pt

mean

Navigating Indonesia

Construction │ November 22, 2018

4

Infra 2.0: on firmer foundation

INFRA 2.0: BETTER STRUCTURE AND RISK MANAGEMENT

The first great infra push that began in 2014 lacked coordination and a structure

for planning and funding for infra development. This arguably dented minority

investor sentiment, despite its largesse (14% of cumulative GDP spent over

2014-2019F). The government’s latest plan to form two state-owned holding

companies for infrastructure and property by end-2018 is therefore much more

positive, in our view, as it could help improve development planning, bridge

government and minority shareholders’ interests, improve efficiency, and boost

economies of scale, leading to lower procurement and funding costs. We see a

brighter outlook for the next infra push (infra 2.0), which we reckon could kick-off

in 2019F.

A less organised infra 1.0

During the first great infra push that started in 2014 (which we will call infra 1.0),

the government injected a total of Rp11.2tr capital to the four SOE contractors

through rights issues in 2015-2016. Together with government capital injections,

the four SOE contractors also received rights issue proceeds from public

investors through the same exercises in 2015-2016, totaling Rp7.5tr (see Figure

2).

Figure 2: The four SOE contractors conducted rights issues in 2015-2016 - proceeds

and allocations

SOURCES: CGS-CIMB RESEARCH, COMPANY REPORTS

The rationale behind the capital injections and rights issues in 2015-2016 were

to strengthen the capital structures of the four SOE contractors for them to

participate in various infra investments. This was actually in line with the

government’s funding plan for infra development through the national medium

term development plan (RPJMN or rencana pembangunan jangka menengah) in

2015-2019. In the funding plan, the government’s budget was expected to be

only sufficient to cover 41% of the total infra funding needs in 2015-2019 of

Rp4,979tr (assuming a US$/Rp rate of 13,500). The rest of the funding was to

have been provided by SOE and private entities at 22% and 37% of total needs,

respectively.

ADHI (2015) WSKT (2015) WIKA (2016) PTPP (2016)

Total proceeds (Rp bn) 2,745 5,298 6,149 4,410

from Government of Indonesia 1,400 3,500 4,000 2,250

from public investors 1,345 1,798 2,149 2,160

Allocations

from Government of IndonesiaJabodetabek LRT

investment

toll roads, power

plants, and

industrial estate

investments

toll roads, ports,

low cost high rise

residentials

investments

from public investorsTrainst oriented

development (TOD)

investment,

refinancing, &

working capital

industrial estate,

low cost high rise,

and power plant

investments

toll roads

investments in Java

and Sumatera;

working capital for

electricity

transmission

development in

Sumatera

Navigating Indonesia

Construction │ November 22, 2018

5

Figure 3: National medium-term development infra funding requirement plan in 2015-

2019 (total of Rp4,979tr, assuming Rp13,500/US$)

SOURCES: CGS-CIMB RESEARCH, KPPIP

However, the lack of coordination and structure caused delays and consequently,

investment realisation had been slow. Additionally, there were some changes to

the investment plans and project investors from the initial plans. So far, only the

investment realisations for toll road projects are on track. Hence, WSKT had the

highest capex realisation for toll road projects. The other contractors have yet to

realise their investment plans.

The Jakarta-Bandung HSR project was the major delay, by about two and half

years, since it broke ground in early-2016, which aptly illustrates the chaos in

infra 1.0. We further highlight some of the events that deviated from the initial

plans below.

1. Change of Jabodebek LRT investor and uncertainties over funding

sources

In 2015, ADHI received Rp1.4tr in capital injection from the government,

which was initially to be allocated for the Jabodebek LRT investment.

The appointment of ADHI as the project investor for Jabodebek LRT

raised concerns from its minority shareholders. This was on the back of

the project’s total low project IRR of c.7% (unfeasible). Due to this

concern, ADHI proposed a change in the project investor to the

government.

In 2015, ADHI broke ground for the project construction. However, it

was not until early-2017 that it received the official construction contract

for the project. Additionally, over the 2015-2017 period, there were no

certainties on who the project investor for the project would be.

After about two years of long negotiations and two Presidential Decree

revisions as the legal basis for project development, at the end of 2017,

the government finally affirmed Kereta Api Indonesia (KAI) as the project

investor for Jabodebek LRT. The government also finally confirmed the

sources of funding for the project investment. ADHI's share price

performance had been volatile during the process of change in the

Jabodebek LRT investor and determination of sources of funding for the

project (see Figure 4).

Now, ADHI has yet to decide on the Rp1.4tr capital injection utilisation

from government, which was initially to be invested for the whole

Jabodebek LRT development. Based on our latest discussions with

ADHI, it may allocate the capital injection money as working capital for

the Jabodebek LRT depot. It expects the government to repay the

company under the availability payment terms. Under the availability

Title:

Source:

Please fill in the values above to have them entered in your reportState/regional budget

41%

SOEs22%

Private37%

Navigating Indonesia

Construction │ November 22, 2018

6

payment terms, the government will pay ADHI in instalments for the LRT

depot, of which the first payment will only take place after 100% project

delivery. The instalment period will be as long as the concession period.

Figure 4: ADHI's share price performances were volatile in 2015-2017 during the process of Jabodebek LRT investor change

SOURCES: CGS-CIMB RESEARCH, BLOOMBERG

2. Large-size power plant investments yet to be realised

WIKA and PTPP have yet to allocate the bulk of their rights issue

proceeds for power plant investments (see Figures 5-6). However, now,

the government plans to delay the 35GW electricity projects due to

Indonesia’s widening current account deficits (CAD).

The delay in the 35GW electricity projects are expected for power plant

projects that have not yet reached financial close. Based on our

understanding, all the power plant projects to be invested by WIKA and

PTPP have not reached financial close yet. Hence, we think these

projects could be delayed further.

Figure 5: PTPP's progress in utilising funds from state capital injection and its rights issue, as of 9M18

SOURCE: CGS-CIMB RESEARCH, COMPANY

Title:

Source:

Please fill in the values above to have them entered in your report

-

500

1,000

1,500

2,000

2,500

3,000

3,500

2-Jan-15 2-Jul-15 2-Jan-16 2-Jul-16 2-Jan-17 2-Jul-17 2-Jan-18

Rp 3-Sep-2015:

ADHI was appointed as the developer of Jabodebek LRT through issuance of

Presidential Decree No. 98/Year 2015

10-Feb-2017:

ADHI signed Jabodebek LRT contract worth

Rp23.4tr

19-May-2017:

Government issued second revision of Presidential Decree for Jabodebek LRT (Presidential Decree No.49/ Year 2017), which stated about the sources of

funding options for KAI. However, there was still no affirmation about when and

how KAI would make payment for construction progress delivered by ADHI.

28-Nov-2017:

Local news reported Ministry of SOE had asked Indonesia Railways Company (KAI) to be a project operator rather

than project investor for Jabodebek LRT. ADHI's CEO Mr.

Budi Harto was quoted by Detik.com saying that ADHI

would invest in Jabodebek LRT

8-Dec-2017:

Government reconfirmed KAI as the project investor for Jabodebek LRT.

Government as well affirmed about the

sources of funding for the Jabodebek LRT

payment, which would be through

government capital injections and bank

loan consortiums.

3-Aug-2016:

ADHI was officially only appointed as the project contractor, while KAI was appointed as the project investor for

Jabodebek LRT through issuance of first Presidential Decree

revision (Presidential Decree No.65/ Year 2016). However,

uncertainties remained about the funding sources for the

project investment.

Stake

Est.

value

(Rp bn)

Equity

(30%)

Debt

(70%)

Proceeds from state capital injection (PMN)

Port

Multipurpose Terminal Kuala Tanjung 3,177 166 25% 794 238 556 323 Operating

Toll roads

Medan-Kualanamu-Tebing Tinggi 4,072 174 15% 611 183 428 185 Under construction

Depok-Antasari 3,472 62 13% 451 135 316 83 Section I was completed

Balikpapan-Samarinda 9,973 449 15% 1,496 449 1,047 33 Under construction

Pandaan-Malang 5,970 627 35% 2,090 627 1,463 439 Under construction

Manado-Bitung 5,123 231 15% 768 231 538 66 Under construction

Housing

High-rise low-cost residential units 3,277 541 55% 1,802 541 1,262 92 Under construction

Total 35,064 2,250 8,013 2,404 5,609 1,222

Proceeds from rights issues

Industrial Estate

Kuala Tanjung Industrial Estate 8,000 1,260 35% 2,800 840 1,960 -

Housings

High-rise low-cost residentials 2,805 463 55% 1,543 463 1,080 -

Power plant

Coal fired power plant-Meulaboh 400MW 7,330 439 34% 2,483 745 1,738 9

As end-9M18 the total account receivable

balance from the project construction is

Rp271.7bn; the project is yet to finalise the

financial close of the project and currently

under review

Total 18,135 2,162 6,826 2,048 4,778 9

PTPP's equity

(end-9M18)Projects status as of 9M18

PTPP's investmentCapital

injection

(Rp bn)

Total

value

(Rp bn)

Project allocations

Navigating Indonesia

Construction │ November 22, 2018

7

Figure 6: WIKA's utilisation of funds from the state capital injection as of 9M18

SOURCE: CGS-CIMB RESEARCH, COMPANY

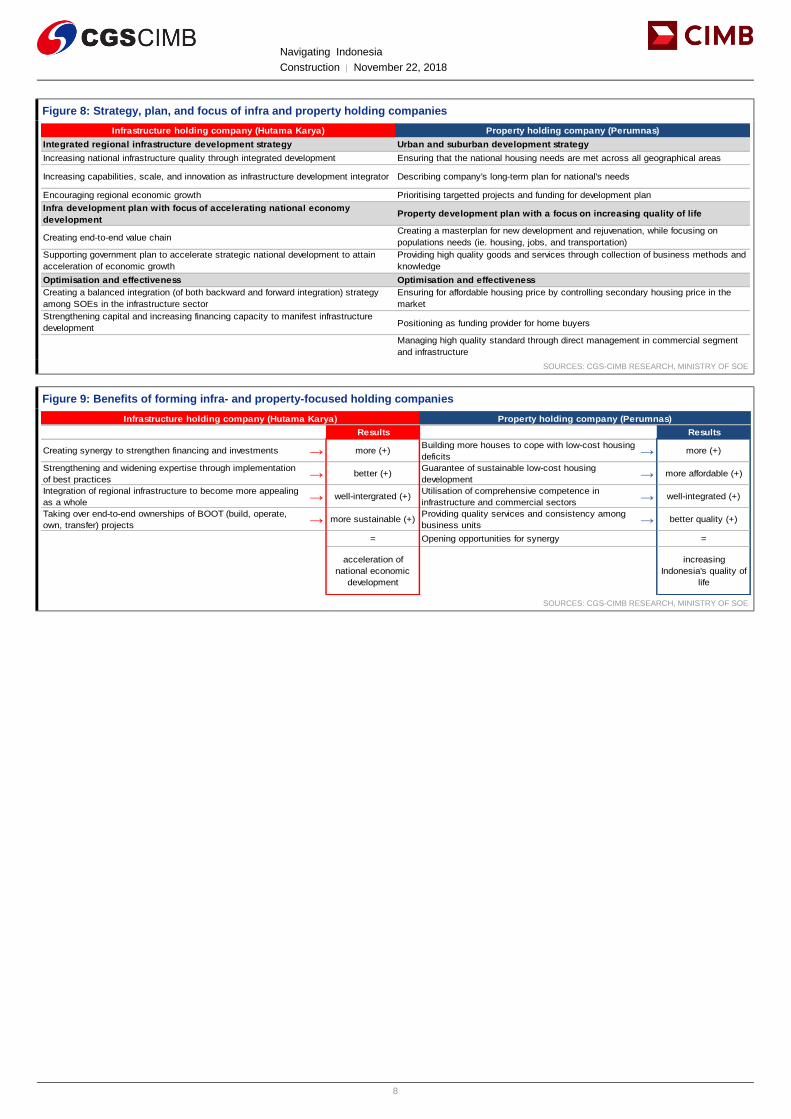

Two newly-formed state-owned holding companies should improve coordination

The government plans to set up two infra and property holding companies by

end-2018. Hutama Karya (HK), a 100% government-owned state-owned

enterprise (SOE) contractor, will be the holding company for its infrastructure-

related ventures. Perumnas, a 100% government-owned SOE developer, will be

the holding company for its property-related ventures (housing and industrial

area). Besides the property sector, we believe Perumnas will likely also focus on

the engineering, procurement, and construction (EPC) sector, e.g. power plants

and oil and gas related businesses. The government aims to convert HK and

Perumnas into holding companies by end-2018F. Following this, the full

immersion is projected by FY2020F.

Some changes have been made to the composition of the holding companies

from the initial plan announced. The new list puts WIKA under Perumnas (vs.

HK previously) and ADHI under HK (vs. Perumnas previously).

We think the changes in WIKA and ADHI's grouping would better align their

competencies with the holding companies’ respective focus. WIKA has a strong

presence in EPC, and recently expanded into housing. ADHI is the appointed

contractor for the whole Jabodebek LRT development.

Based on the respective holding companies’ focus, we think WIKA and PTPP

would be focusing more on property (e.g. real estate and industrial estates) and

EPC projects (e.g. power plant, oil, and gas related projects), respectively. ADHI

and WSKT would focus more on non-EPC infra projects (e.g. toll roads and

water treatment); and JSMR would remain a toll road developer and operator.

Figure 7: Structure of the SOE holding companies for the government's infrastructure and property ventures, respectively (latest)

SOURCES: CGS-CIMB RESEARCH, MINISTRY OF SOE

StakeEst. value

(Rp bn)

Equity

(30%)

Debt

(70%)

Toll roads

Soreang-Pasirkoja 1,500 113 25% 375 113 263 227 Under construction

Manado-Bitung 5,123 307 20% 1,025 307 717 88 Under construction

Balikpapan-Samarinda 9,972 449 15% 1,496 449 1,047 36 Under construction

Power plants

Steamed engine power plant Banten 2

X 1,000 MW37,500 1,688 15% 5,627 1,688 3,939 -

Likely to be replaced with steam

engine power plant Jambi 1 & 2 (2 X 2

X 300 MW); but still no progress up to

now

Steamed engine power plant Aceh 2 X

200 MW10,000 893 30% 3,000 900 2,100 -

Likely to be replaced with Butu Batu

water engine power plant (2 X 100

MW); but still no progress up to now

Clean water treatments

WTP Jatiluhur 50,000L/sec 2,000 84 14% 280 84 196 0 No progress

Industrial estate

Kuala Tanjung Industrial Estate 8,000 467 19% 1,520 456 1,064 - Not started yet, might be changed to

another project located in Java area

Total 74,095 4,000 13,322 3,997 9,325 351

Project status as of 9M18

WIKA's investment

ProjectsTotal value

(Rp bn)

Capital

injection

allocations

WIKA's equity

(end-9M18)

70% 51% 66% 100% 100% 51% 65% 100% 100% 100% 100%

Infrastructure holding company Property (housing and industrial area) holding company

Navigating Indonesia

Construction │ November 22, 2018

8

Figure 8: Strategy, plan, and focus of infra and property holding companies

SOURCES: CGS-CIMB RESEARCH, MINISTRY OF SOE

Figure 9: Benefits of forming infra- and property-focused holding companies

SOURCES: CGS-CIMB RESEARCH, MINISTRY OF SOE

Infrastructure holding company (Hutama Karya) Property holding company (Perumnas)

Integrated regional infrastructure development strategy Urban and suburban development strategy

Increasing national infrastructure quality through integrated development Ensuring that the national housing needs are met across all geographical areas

Increasing capabilities, scale, and innovation as infrastructure development integrator Describing company's long-term plan for national's needs

Encouraging regional economic growth Prioritising targetted projects and funding for development plan

Infra development plan with focus of accelerating national economy

developmentProperty development plan with a focus on increasing quality of life

Creating end-to-end value chainCreating a masterplan for new development and rejuvenation, while focusing on

populations needs (ie. housing, jobs, and transportation)

Supporting government plan to accelerate strategic national development to attain

acceleration of economic growth

Providing high quality goods and services through collection of business methods and

knowledge

Optimisation and effectiveness Optimisation and effectiveness

Creating a balanced integration (of both backward and forward integration) strategy

among SOEs in the infrastructure sector

Ensuring for affordable housing price by controlling secondary housing price in the

market

Strengthening capital and increasing financing capacity to manifest infrastructure

developmentPositioning as funding provider for home buyers

Managing high quality standard through direct management in commercial segment

and infrastructure

Results Results

Creating synergy to strengthen financing and investments → more (+) Building more houses to cope with low-cost housing

deficits → more (+)

Strengthening and widening expertise through implementation

of best practices → better (+)Guarantee of sustainable low-cost housing

development → more affordable (+)

Integration of regional infrastructure to become more appealing

as a whole → well-intergrated (+)Utilisation of comprehensive competence in

infrastructure and commercial sectors → well-integrated (+)

Taking over end-to-end ownerships of BOOT (build, operate,

own, transfer) projects → more sustainable (+)Providing quality services and consistency among

business units → better quality (+)

= Opening opportunities for synergy =

acceleration of

national economic

development

increasing

Indonesia's quality of

life

Infrastructure holding company (Hutama Karya) Property holding company (Perumnas)

Navigating Indonesia

Construction │ November 22, 2018

9

Expect government and minority shareholders’ interests to be better aligned

In the next cycle of Indonesia's infrastructure development, the development of

ex-Java areas would likely be the focus as Java is already well developed, in our

view. However, projects outside of Java could offer unappealing project

feasibility (lower IRR) given that the majority of Indonesia’s population (57%) is

concentrated in Java, followed by Sumatera (22%), with the remaining spread

across the rest of Indonesia.

We think that if the next cycle of infra development (infra 2.0) focus would be in

ex-Java areas, this could raise concerns among minority shareholders (equity

stock investors) on whether the listed SOE contractors and JSMR could possibly

be asked or be assigned to invest in projects in ex-Java area with less appealing

feasibility (low project IRR). This is on the back of state budget limitations for

infra funding.

From our discussion with Hutama Karya, we understand that following the

formation of the holding companies, the government could assign projects with

less appealing feasibility to the holding companies. As an example, the

government has assigned the Trans-Sumatera toll road development to Hutama

Karya; though the project is guaranteed by the government. Hence, Hutama

Karya could receive lower financing cost from a higher AAA bond rating for the

project from PEFINDO (Indonesia’s Credit Rating Agency). This is higher than

the company’s rating of A- from PEFINDO.

Figure 10: Hutama Karya's financing cost for projects guaranteed by the government

guarantee is much lower compared to what it would get on its own

SOURCES: CGS-CIMB RESEARCH, COMPANY REPORTS

We think that if the government were to possibly only assign less appealing

projects to the holding companies following the holding companies’ formation,

this would be a win-win solution for the government and minority shareholders

and a positive for the sector in infra 2.0.

By assigning the less appealing project investments to the holding companies,

the government should be able to meet its development target (no need to wait

for willing investors to invest in these projects), keeping the infra budget

unchanged. The holding companies could possibly leverage lower financing cost

on the back of the government’s guarantee. The SOE contractors in our

coverage and JSMR would hardly be receiving any government guarantees as

they are not 100% government-owned, which would result in higher financing

costs, in our view.

Yet, the SOE contractors in our coverage would still be able to receive project

construction contracts invested by the holding companies as we believe the

holding companies would not be able to take on the construction of the entire

projects on their own.

Title:

Source:

Please fill in the values above to have them entered in your report

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

7.0%

8.0%

9.0%

10.0%

-

500

1,000

1,500

2,000

2,500

Bond I-Series B2013

Bond I-Series C2013

Bond PUB IPhase I-2016

Bond PUB IPhase II-2017

Bond PUB IPhase III-Series

A-2017

Bond PUB IPhase III-Series

B-2017

Value (Rp bn) Coupon rate- RHS

with government guarantee

PEFINDO rating: A-; tenure: 7 years

PEFINDO rating: A-; tenure: 5 years

PEFINDO rating: AAA; tenure: 10 years

PEFINDO rating: AAA; tenure: 10 years

PEFINDO rating: AAA; tenure: 10 years

PEFINDO rating: AAA;tenure: 10 years

Navigating Indonesia

Construction │ November 22, 2018

10

Hope for efficiency improvements, lower funding costs and increasing scale

According to the roadmap revealed by the government, the first step in the

formation of state-owned infrastructure and property holding companies is the

transfer of the government’s current direct ownership in the respective SOEs to

the two assigned holding companies, Hutama Karya (HK) and Perumnas.

The next step, dubbed "initiation of cooperation", involves the creation of sub-

holding companies under HK and Perumnas (Figure 11).

We think the aim of forming sub-holding companies is to improve efficiency and

boost economies of scale, leading to lower procurement and funding costs.

Currently, all the four SOE contractors have a wide range of investments and

subsidiaries in their portfolios, and they do not necessarily have the expertise to

manage their highly-diversified investment portfolios (Figures 12-13).

Based on the roadmap, Hutama Karya is to have four sub-holding companies -

precast and construction materials, construction, concessions, and property

(leaning towards commercial property, e.g. transit oriented developments (TOD)

property). Perumnas would have six sub-holding companies - sub-holding

management, developer, design and technic, industry and material, construction

and EPC, and operational and maintenance (O&M).

Although we are positive on the idea of sub-holding companies, we think the

most important things to watch out for are fair values and investment structures

in the event of possible asset transfers or restructuring from the SOE contractors

and JSMR to the sub-holding companies.

Figure 11: Roadmap on the formation of Hutama Karya (HK, infrastructure) and Perumnas (property) holding companies

1. Sub-holding management 2. Developer 3. Design & technic 4. Industrial & material 5. Construction & EPC 6. O&M

SOURCES: CGS-CIMB RESEARCH, MINISTRY OF SOE

11

Construction and Materials│Indonesia

Construction│ October 22, 2018

Figure 12: SOE contractors' investments portfolio

SOURCES: CGS-CIMB RESEARCH, COMPANY REPORTS

Stake (%)Equity-

Rp bnStake (%)

Equity-

Rp bnStake (%)

Equity-

Rp bnStake (%)

Equity-

Rp bn

Toll road (length in KM) 1,352 177,780 7 861 1,199 15,043

Balikpapan-Samarinda toll road 99 9,970 15% 33 15% 36 Under construction

Bekasi-Cawang-Kp. Melayu toll road 22 9,500 76% 1,513 Partially operating

Cengkareng-Kunciran toll road 14 4,980 2% 8 Under construction

Ciawi-Sukabumi toll road 54 9,200 77% 1,277 Under construction

Cibitung-Cilincing toll road 34 4,220 42% 423 Under construction

Cileunyi-Sumedang-Dawuan toll road 62 8,400 14% 1 12% 15 Under construction

Cimanggis-Cibitung toll road 25 8,200 69% 952 Under construction

Cinere-Serpong toll road 10 2,800 27% 89 Under construction

Depok-Antasari toll road 22 3,400 13% 83 10% 255 Section I development was completed

Kanci-Pejagan toll road 35 2,900 18% 193 Operating

Kayu Agung-Palembang-Betung toll road 112 14,400 46% 1,063 Under construction

Krian-Legundi-Bunder-Manyar toll road 38 12,200 42% 966 Under construction

Kuala Tanjung-Tb. Tinggi-Parapat toll road 143 13,450 23% 11 Under construction

Manado-Bitung toll road 40 5,120 15% 66 20% 88 Under construction

Medan-Kualanamu-Tebing Tinggi toll road 62 4,710 15% 185 12% 358 Partially operating

Ngawi-Kertosono toll road 87 7,800 31% 354 Partially operating

Nusa Dua-Ngurah Rai-Benoa toll road 10 2,010 1% 7 0% 3 Operating

Pandaan - Malang toll road 38 5,970 35% 439 Under construction

Pasuruan-Probolinggo toll road 31 3,800 23% 227 Under construction

Pejagan-Pemalang toll road 58 6,840 23% 5,878 Operating

Pemalang-Batang toll road 39 5,200 46% 857 Under construction

Semarang-Batang toll road 75 11,050 31% 79 Under construction

Serang-Panimbang toll road 84 5,330 15% 53 80% 642 Under construction

Solo-Ngawi toll road 90 10,800 31% 535 Operating

Soreang-Pasirkoja 32 1,500 25% 227 Under construction

Surabaya-Mojokerto toll road 36 4,030 20% 194 Operating

Investments Length or capacities Total est. inv. cost (Rp bn)

Investment participations (end-9M18)

Status (9M18)ADHI IJ PTPP IJ WIKA IJ WSKT IJ

12

Construction and Materials│Indonesia

Construction│ October 22, 2018

Figure 13: SOE contractors' investments portfolio

SOURCES: CGS-CIMB RESEARCH, COMPANY REPORTS

Stake (%)Equity-

Rp bnStake (%)

Equity-

Rp bnStake (%)

Equity-

Rp bnStake (%)

Equity-

Rp bn

Power plant (capacities in MW) 660 9,553 - 270 92 115

Coal fired power plant -Meulaboh, Aceh 400 7,330 34% 9 Construction started in 2018

Mini hydro power plant-Lau Gunung, No. Sum. 15 288 38% 33 Construction progress: 60.3%

Gas engine power plant- Talang Duku, Palembang 56 - 99% 137 Operating since 2011

Waste to energy power plant-Surakarta, Central Java 10 400 40% 25

Coal fired power plant-Central Lampung 14 - 75% 67 Operating since 2014

Micro gas power plant-Rengat 20 160 100% 46 Operating

Gas engined power plant-Borang 60 806 100% 26 Operating

Micro gas power plant-Rawa Minyak 25 204 70% 20 Operating

Mini hydro power plant-Sangir, W. Sumatera 10 266 95% 113 Operating

Hydroelectric power plant-Wado, W. Java 50 100 100% 2 Under construction

Oil, gas, and asphalt - 4,900 - - - -

Bantaeng storage - 4,900 30% 18

Asphalt mining - - 99% 41 Operating

Upstream and downstream oil and gas - - 70% 15 Operating

Water infrastructure 2,000 - 20 0 -

Water treamemt plant-Jatiluhur 50,000L/sec 2,000 14% 0

Perusahaan Air Indonesia Amerika 25% 20

Port 3,177 - 323 96 273

Multipurpose Terminal Kuala Tanjung 25% 323 20% 273 Operating

Belawan International Container Port 15% 96 Operating

Railway or city train 79,330 - - (187) -

Jakarta-Bandung HSR 78,000 38% (187) Under construction

Metro Kapsul 1,330 51% -

Total 276,740 7 1,474 1,199 15,430

Investments Length or capacities Total est. inv. cost (Rp bn)

Investment participations (end-9M18)

Status (9M18)ADHI IJ PTPP IJ WIKA IJ WSKT IJ

Navigating Indonesia

Construction │ November 22, 2018

13

How operational cost efficiency could be created

Currently, the Trans-Java Toll Road is owned by three majority shareholders -

JSMR, Waskita Toll Road (WTR, a subsidiary of WSKT), and Astra Infra (a

subsidiary of Astra International, ASII, ADD, TP Rp8,500).

Figure 14: Trans-Java Toll Road concessions

SOURCES: CGS-CIMB RESEARCH, COMPANY REPORTS

WTR started investing in the toll road business in 2015, while JSMR has been in

this business since 1978 (it was initially a toll road regulator, from 1978, and

turned into a toll road developer and operator in 2004). Given JSMR's very long

track record in the toll road business, we believe it has the most expertise in

operating toll roads vs. other SOE contractors in our coverage.

Hence, we think that if the whole stretch of Trans-Java Toll Road is managed

under a sub-holding company and operated by JSMR, its operational cost

should be much more efficient due to economies of scale. A single operator

would significantly reduce the number of employees needed to operate the

whole stretch.

JSMR WTR Astra Infra

Jakarta-Cikampek 83.0 Jasa Marga 100% - -

Cikampek-Palimanan 114.0 Lintas Marga Sedaya - - 45%

Palimanan-Kanci 26.3 Jasa Marga 100% - -

Kanci-Pejagan 35.0 Semesta Marga Raya - 78% -

Pejagan-Pemalang 57.5 Pejagan Pemalang Toll Road - 100% -

Pemalang-Batang 39.00 Pemalang Batang Toll Road - 60% -

Batang-Semarang 75.0 Jasamarga Semarang Batang 60% 40% -

Semarang 24.8 Jasa Marga 100% -

Semarang-Solo 72.6 Trans Marga Jateng 59% - -

Solo-Ngawi 90.1 Solo Ngawi Jaya 60% 40% -

Ngawi-Kertosono-Kediri 114.9 Ngawi Kertosono Jaya 60% 40% -

Kertosono-Mojokerto 41.0 Marga Harjaya Infrastruktur - - 100%

Mojokerto-Surabaya 36.3 Jasamarga Surabaya Mojokerto 55% - -

Surabaya-Gempol 49.0 Jasa Marga 100% - -

Gempol-Pandaan 13.6 Jasamarga Pandaan Tol 92% -

Gempol-Pasuruan 34.2 Transmarga Jatim Pasuruan 99% - -

Pasuruan-Probolinggo 31.3 Trans Jawa Paspro Jalan-Tol - 80% -

Probolinggo-Banyuwangi 172.0 Jasamarga Probolinggo Banyuwangi 55% - -

Total 1,110

Length (km) Concession holderStake ownerships

Toll roads

Navigating Indonesia

Construction │ November 22, 2018

14

How enlarged scale could translate into lower cost

Hutama Karya’s GPM improved to 10.2% in 9M18 vs. 8.6% in 9M17. From our

discussion with its management, we understand that this was due to the

implementation of an integrated procuring system at the beginning of 2018.

Figure 15: Improvement of Hutama Karya's GPM

SOURCES: CGS-CIMB RESEARCH, COMPANY REPORTS

We think if Hutama Karya’s case could be a benchmark, in the future, the

formation of a precast and construction material sub-holding company under the

infrastructure holding could have a positive impact on the procurement cost of all

the members of the sub-holding company. This should not only result in higher

operational cost efficiency (e.g. fewer number of employees needed), but also in

larger orders (economies of scale). Economies of scale could perhaps give

additional bargaining power to the group of companies under the sub-holding

company when dealing with suppliers.

Potentially lower funding cost

We believe lower cost of funding can be attained through sub-holding

companies formation.

As an example, the Trans-Java Toll Road includes the Jakarta-Cikampek toll

road, which is already a mature toll road with stable cash flow. If the Jakarta-

Cikampek toll road is combined with new toll road assets of the highway to raise

funds for the whole highway stretch, we believe the cost of funding should be

lower vs. separately raising funds for each new toll road asset.

Enlarging room for leverage

We think the total room of leverage for the holding companies and holding

members should remain the same after the formation of the holding companies.

Our channel checks indicate that this can be achieved through using an equity

method of accounting at the holding company level. This is despite the fact that

holding companies need to have a majority stake in its subsidiaries. Normally,

the parent company needs to apply a full-consolidation accounting method if it

has a majority stake in its subsidiaries.

This is possible, in our view. Based on ED PSAK 4 (Indonesia’s Financial

Accounting Standards), a subsidiary cannot be consolidated if it is subject to the

control of the government, court, administrator, or regulator.

We estimate that a full-consolidation accounting method for both holding

companies could increase total debt of Hutama Karya to Rp111tr (11x from the

level as at end-FY17 and Perumnas to Rp27.5tr (10x from the level as at end-

FY17, post-holding companies’ formation. We estimate Hutama Karya’s and

Title:

Source:

Please fill in the values above to have them entered in your report

8.61%

10.15%

9M17-construction GPM 9M18-construction GPM

Hutama Karya

Navigating Indonesia

Construction │ November 22, 2018

15

Perumnas’ gearing (DER) could shoot up to 7.0x (or fall to 4.2x if we factor in

additional equity injection from the FY19F state budget) and 4.5x, respectively.

Figure 16: HK’s total DER under full-consolidation accounting

method, post-holding company formation (CGS-CIMBe)

Figure 17: Perumnas’ DER under a full-consolidation accounting

method, post-holding company formation (CGS-CIMBe)

*Total debt post-holding = total debts of ADHI, JSMR, and WSKT in FY18F + HK’s total debt at end-FY17; Total equity post-holding = HK’s total equity at end-FY17+NP of ADHI, JSMR, and WSKT in FY18F

**Total debt post-holding + injections = total debts of ADHI, JSMR, and WSKT in FY18F + total debt Hutama Karya in FY17; *Total equity post-holding + injections= HK’s total equity at end-FY17+NP of ADHI, JSMR, and WSKT in FY18F+government equity injections in FY19F

SOURCES: CGS-CIMB RESEARCH, COMPANY REPORTS

*Total debt post-holding = total debts of WIKA and PTPP in FY18F + total debt Perumnas in FY17; Total equity post-holding = Perumnas’ total equity in end-FY17+ NP of WIKA and PTPP in FY18F

SOURCES: CGS-CIMB RESEARCH, COMPANY REPORTS

On the other hand, under an equity accounting method, post-holding companies’

formation, we estimate Hutama Karya’s gearing to decrease slightly to 0.8x (vs.

1.2x prior to the holding company), and further to 0.4x after accounting for the

government’s equity injection in FY19F. We estimate Perumnas’ gearing could

decrease to 0.54x (vs. 0.84x prior to the holding company).

Decreasing gearing of both holding companies, post-holding companies’

formation, could be contributed by a higher total equity balance of both Hutama

Karya and Perumnas by 0.6x. Our estimates assume that both holding

companies will receive additional proportionated net profit from the subsidiaries.

Meanwhile, both holding companies could maintain unchanged total debt

balances as they do not need to consolidate their subsidiaries’ debts.

Figure 18: HK’s DER under equity accounting method, post-

holding company formation (CGS-CIMBe)

Figure 19: Perumnas’ DER under equity accounting method,

post-holding company formation (CGS-CIMBe)

* Total equity post-holding = HK’s total equity at end-FY17 + proportionated NP of ADHI, JSMR, and WSKT in FY18F

** Total equity for DER calculation = HK’s total equity at end-FY17 + proportionated NP of ADHI, JSMR, and WSKT in FY18F

SOURCES: CGS-CIMB RESEARCH, COMPANY REPORTS

* Total equity for DER calculation = Perumnas’ total equity at end-FY17 + proportionated NP of WIKA and PTPP in FY18F

SOURCES: CGS-CIMB RESEARCH, COMPANY REPORTS

Title:

Source:

Please fill in the values above to have them entered in your report

-

20,000

40,000

60,000

80,000

100,000

120,000

Hutama Karya's total debt-pre-holding (based on 2017

equity balance)

Hutama Karya's total debt-post-holding*

Hutama Karya's total debt-post-holding+injections**

Hutama Karya (holding company) Trans Sumatera Operating Co.

Adhi Karya (ADHI) Jasa Marga (JSMR)

Waskita Karya (WSKT) Indra Karya

Yodya Karya

DER: 7.0x

DER: 1.2x

Rp bnDER: 4.2x

Title:

Source:

Please fill in the values above to have them entered in your report

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

Perumnas' total debt- pre-holding (basedon 2017 equity balance)

Perumnas' total debt- post-holding*

Perum Perumnas (holding company) Pembangunan Perumahan (PTPP)

Wijaya Karya (WIKA) Amarta Karya

Indah Karya Virama Karya

Bina Karya

DER: 4.5x

DER: 0.8x

Rp bn

Title:

Source:

Please fill in the values above to have them entered in your report

-

0.20

0.40

0.60

0.80

1.00

1.20

1.40

-

2,000

4,000

6,000

8,000

10,000

12,000

Hutama Karya's totaldebt- pre-holding (based

on 2017 equity balance)

Hutama Karya's totaldebt- post-holding*

Hutama Karya's totaldebt- post-

holding+injections**

Hutama Karya (holding company) DER (x) -RHS

Rp bn

DER: 1.2x DER: 0.8x DER: 0.4x

Title:

Source:

Please fill in the values above to have them entered in your report

-

0.10

0.20

0.30

0.40

0.50

0.60

0.70

0.80

0.90

0

500

1,000

1,500

2,000

2,500

3,000

Perumnas' total debt- pre-holding(based on 2017 equity balance)

Perumnas' total debt- post-holding*

Perum Perumnas (holding company) DER (x) -RHS

Rp bn

DER: 0.84x DER: 0.54x

Navigating Indonesia

Construction │ November 22, 2018

16

EARNINGS OUTLOOK

Robust outlook in 4Q18F

SOE contractors in our coverage reported decent 9M18 results despite lower-

than-expected new contracts booking. This was on the back of 9M18 order book

delivery coming in line, boosted by strong delivery of contracts carried over. We

have a positive outlook on 4Q18F earnings as many projects are in the

completion stage. During the completion stage, project delivery should be faster

than in the early stages of development as there should be fewer non-technical

hurdles (e.g. land acquisition).

Brief review of 9M18 financials

In 9M18, SOE contractors in our coverage reported operational and bottomline

results in line with and above our expectations. This was despite some lower-

than-expected non-joint operations (JO) revenue for PTPP and WIKA, which

was compensated by an improvement in margins and/or higher-than-expected

JO income.

Figure 20: 3Q18 results recap

SOURCES:CGS-CIMB RESEARCH, COMPANY REPORTS

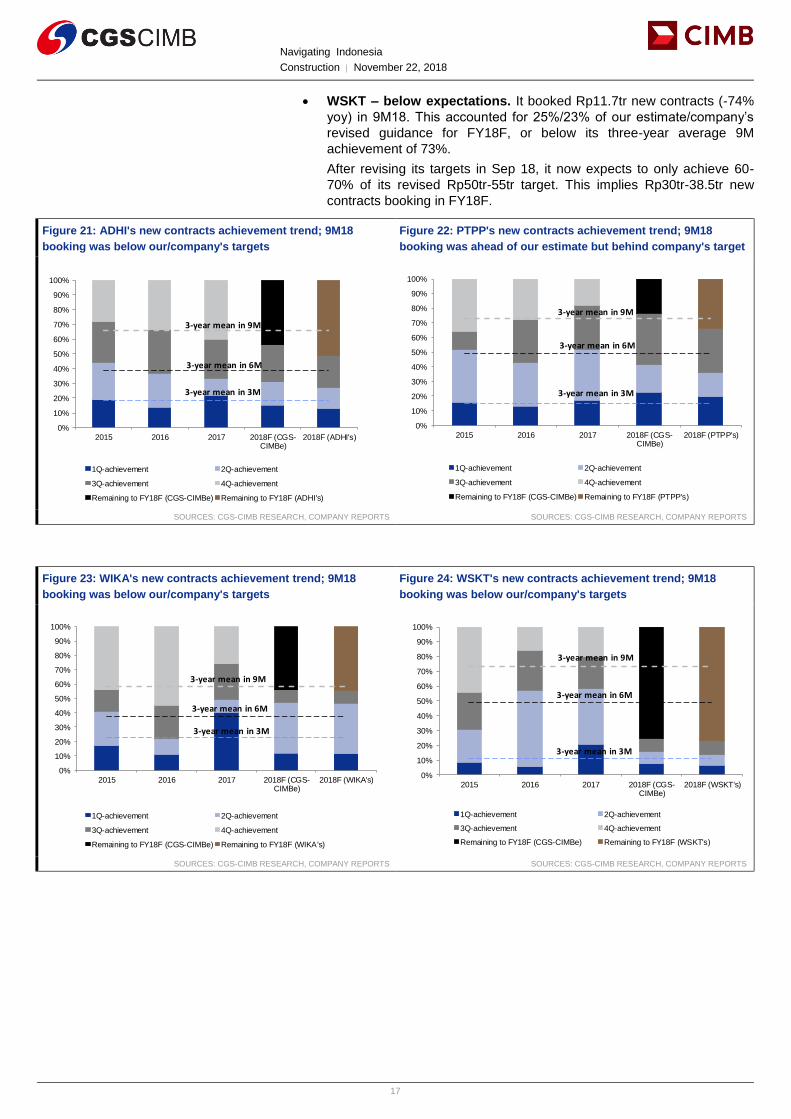

9M18 new contracts booking

The sector’s new contracts booking in 9M18 was below our/companies’

expectations. However, only WSKT has lowered its new contracts target for

FY18F, while the other three SOE contractors in our coverage (ADHI, PTPP,

and WIKA) remain confident they can achieve their targets.

The companies suggested that the weak new contracts booking in 9M18 was

mostly due to delays in the bidding process. Hence, if some contracts are not

received by end-FY18F, this is expected to be delayed until FY19F.

Additionally, we think changes in the management of SOE contractors in Apr 18

were another reason for the weak new contracts booking. We think the new

management needed some time to transition and review the projects to be

tendered.

For example, WSKT’s new management decided to pull out from its investment

in the Pasuruan-Probolinggo toll road. Hence, it no longer expects to receive

construction contracts for the project, and estimates lower new contracts

achievement.

Details are as follows:

ADHI - below expectations. It booked Rp11.4tr new contracts (+10.7%

yoy vs. 9M17’s ex-LRT contracts) in 9M18. This accounted for 56%/49%

of our/company’s new contracts estimates for FY18F, or below its three-

year average 9M achievement of 66%.

PTPPs - in line. It booked Rp32.4tr (+1.6% yoy) new contracts in 9M18.

This accounted for 77%/66% of our/company’s new contracts estimates

for FY18F. This was ahead of our expectation, but remained behind

PTPP’s target for FY18F (three-year average achievement in 9M: 73%).

WIKA – below expectations. It booked Rp25.3tr new contracts (-19.5%

yoy) in 9M18. This accounted for 44%/44% of our/company’s new

contracts estimates for FY18F, or below its three-year average 9M

achievement of 58%.

ADHI PTPP WIKA WSKT

Revenue In line Behind Behind Ahead

GPM (vs. previous year's) Improved Improved Improved Lower

JO income Ahead Ahead Behind Ahead

EBIT Ahead In line In line Ahead

Core NP Ahead In line In line Ahead

Navigating Indonesia

Construction │ November 22, 2018

17

WSKT – below expectations. It booked Rp11.7tr new contracts (-74%

yoy) in 9M18. This accounted for 25%/23% of our estimate/company’s

revised guidance for FY18F, or below its three-year average 9M

achievement of 73%.

After revising its targets in Sep 18, it now expects to only achieve 60-

70% of its revised Rp50tr-55tr target. This implies Rp30tr-38.5tr new

contracts booking in FY18F.

Figure 21: ADHI's new contracts achievement trend; 9M18

booking was below our/company's targets

Figure 22: PTPP's new contracts achievement trend; 9M18

booking was ahead of our estimate but behind company's target

SOURCES: CGS-CIMB RESEARCH, COMPANY REPORTS SOURCES: CGS-CIMB RESEARCH, COMPANY REPORTS

Figure 23: WIKA's new contracts achievement trend; 9M18

booking was below our/company's targets

Figure 24: WSKT's new contracts achievement trend; 9M18

booking was below our/company's targets

SOURCES: CGS-CIMB RESEARCH, COMPANY REPORTS SOURCES: CGS-CIMB RESEARCH, COMPANY REPORTS

Title:

Source:

Please fill in the values above to have them entered in your report

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2015 2016 2017 2018F (CGS-CIMBe)

2018F (ADHI's)

1Q-achievement 2Q-achievement

3Q-achievement 4Q-achievement

Remaining to FY18F (CGS-CIMBe) Remaining to FY18F (ADHI's)

3-year mean in 6M

3-year mean in 9M

3-year mean in 3M

Title:

Source:

Please fill in the values above to have them entered in your report

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2015 2016 2017 2018F (CGS-CIMBe)

2018F (PTPP's)

1Q-achievement 2Q-achievement

3Q-achievement 4Q-achievement

Remaining to FY18F (CGS-CIMBe) Remaining to FY18F (PTPP's)

3-year mean in 6M

3-year mean in 9M

3-year mean in 3M

Title:

Source:

Please fill in the values above to have them entered in your report

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2015 2016 2017 2018F (CGS-CIMBe)

2018F (WIKA's)

1Q-achievement 2Q-achievement

3Q-achievement 4Q-achievement

Remaining to FY18F (CGS-CIMBe) Remaining to FY18F (WIKA's)

3-year mean in 6M

3-year mean in 9M

3-year mean in 3M

Title:

Source:

Please fill in the values above to have them entered in your report

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2015 2016 2017 2018F (CGS-CIMBe)

2018F (WSKT's)

1Q-achievement 2Q-achievement

3Q-achievement 4Q-achievement

Remaining to FY18F (CGS-CIMBe) Remaining to FY18F (WSKT's)

3-year mean in 6M

3-year mean in 9M

3-year mean in 3M

Navigating Indonesia

Construction │ November 22, 2018

18

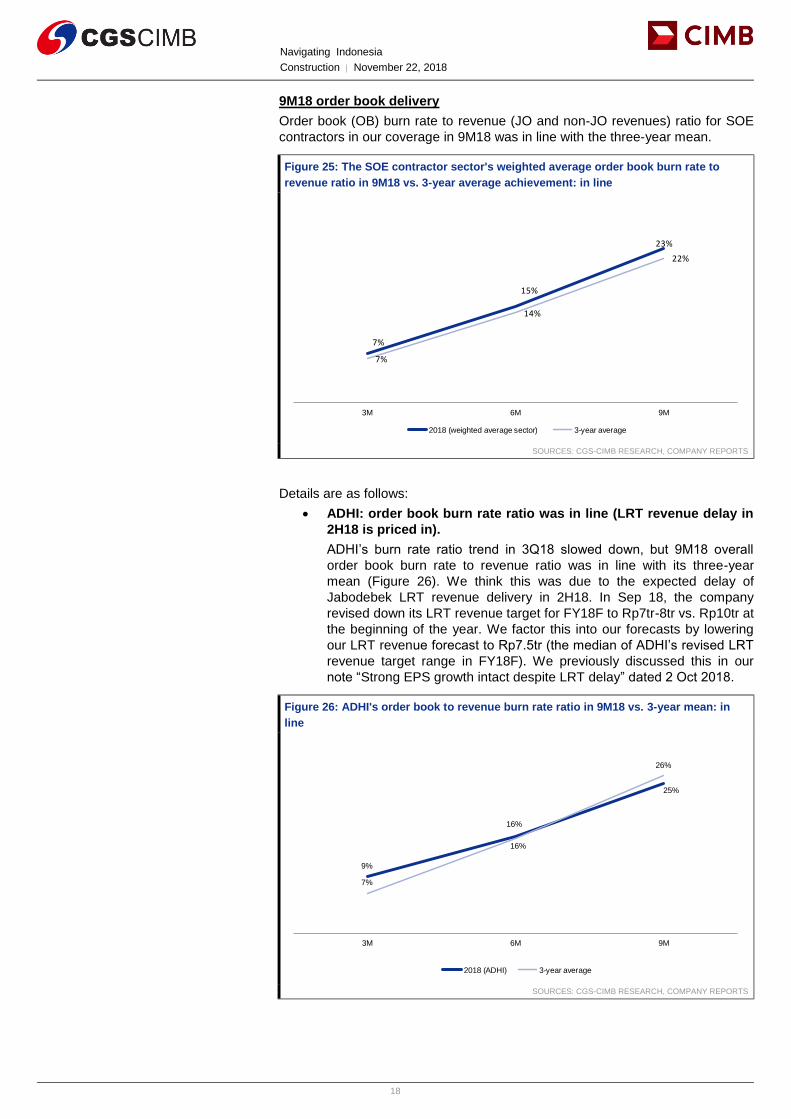

9M18 order book delivery

Order book (OB) burn rate to revenue (JO and non-JO revenues) ratio for SOE

contractors in our coverage in 9M18 was in line with the three-year mean.

Figure 25: The SOE contractor sector's weighted average order book burn rate to

revenue ratio in 9M18 vs. 3-year average achievement: in line

SOURCES: CGS-CIMB RESEARCH, COMPANY REPORTS

Details are as follows:

ADHI: order book burn rate ratio was in line (LRT revenue delay in

2H18 is priced in).

ADHI’s burn rate ratio trend in 3Q18 slowed down, but 9M18 overall

order book burn rate to revenue ratio was in line with its three-year

mean (Figure 26). We think this was due to the expected delay of

Jabodebek LRT revenue delivery in 2H18. In Sep 18, the company

revised down its LRT revenue target for FY18F to Rp7tr-8tr vs. Rp10tr at

the beginning of the year. We factor this into our forecasts by lowering

our LRT revenue forecast to Rp7.5tr (the median of ADHI’s revised LRT

revenue target range in FY18F). We previously discussed this in our

note “Strong EPS growth intact despite LRT delay” dated 2 Oct 2018.

Figure 26: ADHI's order book to revenue burn rate ratio in 9M18 vs. 3-year mean: in

line

SOURCES: CGS-CIMB RESEARCH, COMPANY REPORTS

Title:

Source:

Please fill in the values above to have them entered in your report

7%

15%

23%

7%

14%

22%

3M 6M 9M

2018 (weighted average sector) 3-year average

Title:

Source:

Please fill in the values above to have them entered in your report

9%

16%

25%

7%

16%

26%

3M 6M 9M

2018 (ADHI) 3-year average

Navigating Indonesia

Construction │ November 22, 2018

19

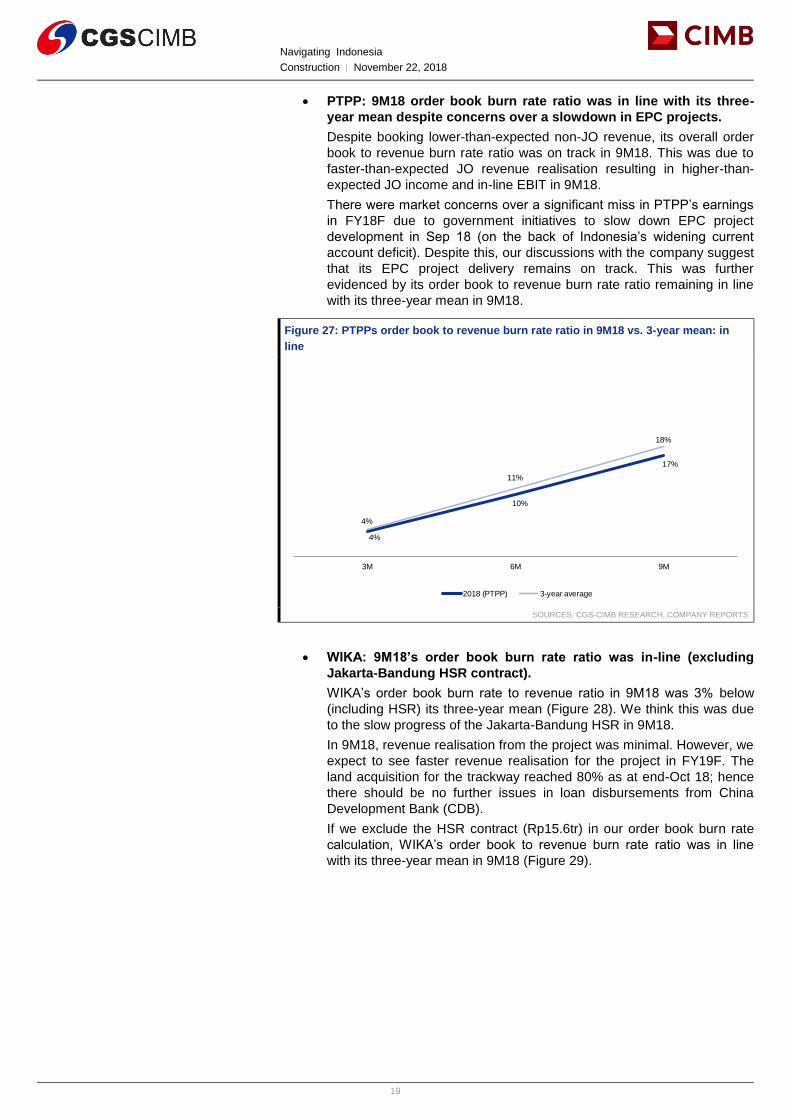

PTPP: 9M18 order book burn rate ratio was in line with its three-

year mean despite concerns over a slowdown in EPC projects.

Despite booking lower-than-expected non-JO revenue, its overall order

book to revenue burn rate ratio was on track in 9M18. This was due to

faster-than-expected JO revenue realisation resulting in higher-than-

expected JO income and in-line EBIT in 9M18.

There were market concerns over a significant miss in PTPP’s earnings

in FY18F due to government initiatives to slow down EPC project

development in Sep 18 (on the back of Indonesia’s widening current

account deficit). Despite this, our discussions with the company suggest

that its EPC project delivery remains on track. This was further

evidenced by its order book to revenue burn rate ratio remaining in line

with its three-year mean in 9M18.

Figure 27: PTPPs order book to revenue burn rate ratio in 9M18 vs. 3-year mean: in

line

SOURCES: CGS-CIMB RESEARCH, COMPANY REPORTS

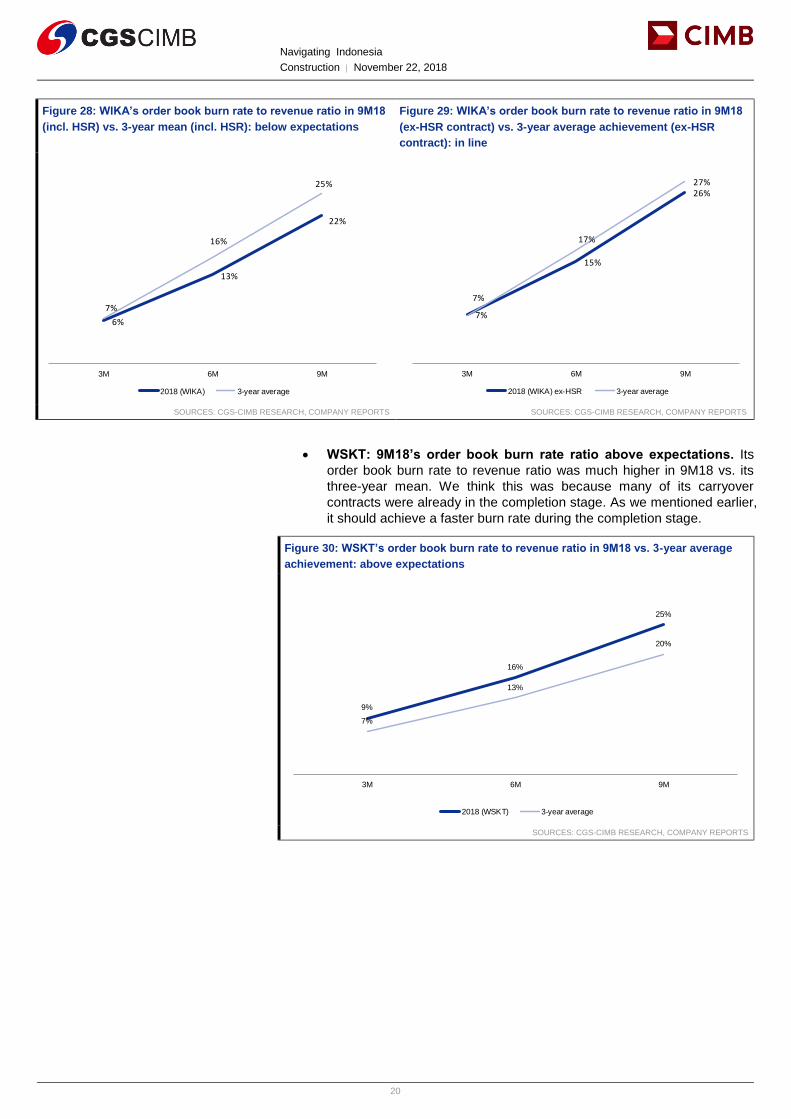

WIKA: 9M18’s order book burn rate ratio was in-line (excluding

Jakarta-Bandung HSR contract).

WIKA’s order book burn rate to revenue ratio in 9M18 was 3% below

(including HSR) its three-year mean (Figure 28). We think this was due

to the slow progress of the Jakarta-Bandung HSR in 9M18.

In 9M18, revenue realisation from the project was minimal. However, we

expect to see faster revenue realisation for the project in FY19F. The

land acquisition for the trackway reached 80% as at end-Oct 18; hence

there should be no further issues in loan disbursements from China

Development Bank (CDB).

If we exclude the HSR contract (Rp15.6tr) in our order book burn rate

calculation, WIKA’s order book to revenue burn rate ratio was in line

with its three-year mean in 9M18 (Figure 29).

Title:

Source:

Please fill in the values above to have them entered in your report

4%

10%

17%

4%

11%

18%

3M 6M 9M

2018 (PTPP) 3-year average

Navigating Indonesia

Construction │ November 22, 2018

20

Figure 28: WIKA’s order book burn rate to revenue ratio in 9M18

(incl. HSR) vs. 3-year mean (incl. HSR): below expectations

Figure 29: WIKA’s order book burn rate to revenue ratio in 9M18

(ex-HSR contract) vs. 3-year average achievement (ex-HSR

contract): in line

SOURCES: CGS-CIMB RESEARCH, COMPANY REPORTS SOURCES: CGS-CIMB RESEARCH, COMPANY REPORTS

WSKT: 9M18’s order book burn rate ratio above expectations. Its

order book burn rate to revenue ratio was much higher in 9M18 vs. its

three-year mean. We think this was because many of its carryover

contracts were already in the completion stage. As we mentioned earlier,

it should achieve a faster burn rate during the completion stage.

Figure 30: WSKT’s order book burn rate to revenue ratio in 9M18 vs. 3-year average

achievement: above expectations

SOURCES: CGS-CIMB RESEARCH, COMPANY REPORTS

Title:

Source:

Please fill in the values above to have them entered in your report

6%

13%

22%

7%

16%

25%

3M 6M 9M

2018 (WIKA) 3-year average

Title:

Source:

Please fill in the values above to have them entered in your report

7%

15%

26%

7%

17%

27%

3M 6M 9M

2018 (WIKA) ex-HSR 3-year average

Title:

Source:

Please fill in the values above to have them entered in your report

9%

16%

25%

7%

13%

20%

3M 6M 9M

2018 (WSKT) 3-year average

Navigating Indonesia

Construction │ November 22, 2018

21

Stabilising earnings outlook in FY19F

In FY19F, we estimate the sector will deliver +21% yoy aggregate core NP

growth due to a low base in FY18F; we estimate -9% yoy core NP in FY18F.

Negative core NP growth for the sector in FY18F is likely to be dragged by

negative core NP growth estimates for WSKT (-32% yoy). We expect WSKT’s

core NP growth to be negative in FY18F as we exclude gains from its first RDPT

issuance, while WSKT’s headline NP in FY18F is expected to show positive

growth of +1% yoy.

We think our core NP growth estimates for the sector can be achieved as: 1) the

sector should have enough orders on hand at the beginning of FY19F, even in

the worst-case scenario; 2) enough projects should be awarded in FY19F and 3)

order book burn rate should remain strong as more projects are expected to be

completed in FY19F.

Figure 31: SOE contractors' core NP growth (yoy) - historical and estimates

SOURCES: CGS-CIMB RESEARCH, COMPANY REPORTS

Enough orders on hand even in the worst-case scenario

Based on our sensitivity analysis, in the worst-case scenario, we estimate the

sector’s aggregate outstanding order book at the end of FY18F (through the

beginning of FY19F) to be Rp362tr. The implied order book (at end-FY18F

through the beginning of FY19F) to revenue (average in FY19-20F) ratio for

SOE contractors is still at 1.1x-1.4x (Figure 32).

In the worst-case scenario, we estimate the sector’s aggregate outstanding

order book at the end of FY18F (through the beginning of FY19F) includes no

additional new contracts booking in 4Q18F and our estimate of Rp63.8tr

revenue in 4Q18F.

Based on our sensitivity analysis, in the best-case scenario, we estimate the

sector’s aggregate outstanding order book at the end of FY18F (through the

beginning of FY19F) to be Rp449tr. The implied order book (at end-FY18F

through the beginning of FY19F) to revenue (average in FY19-20F) ratio for

SOE contractors is 1.2x-2.5x (Figure 33).

In the best-case scenario, our assumption for the sector’s outstanding order

book at the end of FY18F through the beginning of FY19F includes achieving

100% of our FY18F new contracts estimate and our estimate of Rp63.8tr

revenue in 4Q18F.

Title:

Source:

Please fill in the values above to have them entered in your report

-40%

-20%

0%

20%

40%

60%

80%

100%

120%

140%

2015 2016 2017 2018F 2019F

ADHI PTPP WIKA WSKT Sector

Navigating Indonesia

Construction │ November 22, 2018

22

Figure 32: OB at the end of FY18F (our estimate: worst-case

scenario) vs. average annual revenue estimates in FY19-20F

Figure 33: OB at the end of FY18F (our estimate: best-case

scenario) vs. average annual revenue estimates in FY19-20F

SOURCES: CGS-CIMB RESEARCH, COMPANY REPORTS SOURCES: CGS-CIMB RESEARCH, COMPANY REPORTS

New contracts outlook in FY19F

We estimate FY19F new contracts growth of between -20% yoy and +20% yoy

for the four SOE contractors in our coverage. We expect negative new contracts

growth for WSKT on a high base, while the remaining three contractors are

expected to achieve 14-20% yoy new contracts booking in FY19F. Project

outlook is discussed in the following section.

Figure 34: SOE contractors’ new contracts booking - historical

and estimates

Figure 35: SOE contractors new contracts growth (yoy) -

historical and estimates

SOURCES: CGS-CIMB RESEARCH, COMPANY REPORTS SOURCES: CGS-CIMB RESEARCH, COMPANY REPORTS

Title:

Source:

Please fill in the values above to have them entered in your report

-

20,000

40,000

60,000

80,000

100,000

120,000

140,000

160,000

180,000

ADHI PTPP WIKA WSKT

OB at the end of FY18F (CGS-CIMBe)- worst case: no contracts booking in 4Q18F

Avg. annual revenue FY19-20F

Rp bnTitle:

Source:

Please fill in the values above to have them entered in your report

-

20,000

40,000

60,000

80,000

100,000

120,000

140,000

160,000

180,000

ADHI PTPP WIKA WSKT

OB at the end of FY18F (CGS-CIMBe)-best case: 100% estimate

Avg. annual revenue FY19-20F

Rp bn

Title:

Source:

Please fill in the values above to have them entered in your report

13,965 16,500 17,100 20,459 24,083

27,07332,600 38,800

42,25050,700

25,222

37,08042,402

57,515

65,456

32,160

69,97455,834

47,459

37,967

2015 2016 2017 2018F 2019F

ADHI PTPP WIKA WSKT

Rp bnTitle:

Source:

Please fill in the values above to have them entered in your report

-40%

-20%

0%

20%

40%

60%

80%

100%

120%

140%

2015 2016 2017 2018F 2019F

ADHI PTPP WIKA WSKT Sector

Navigating Indonesia

Construction │ November 22, 2018

23

PROJECT PROGRESS AND OUTLOOK

Project progress

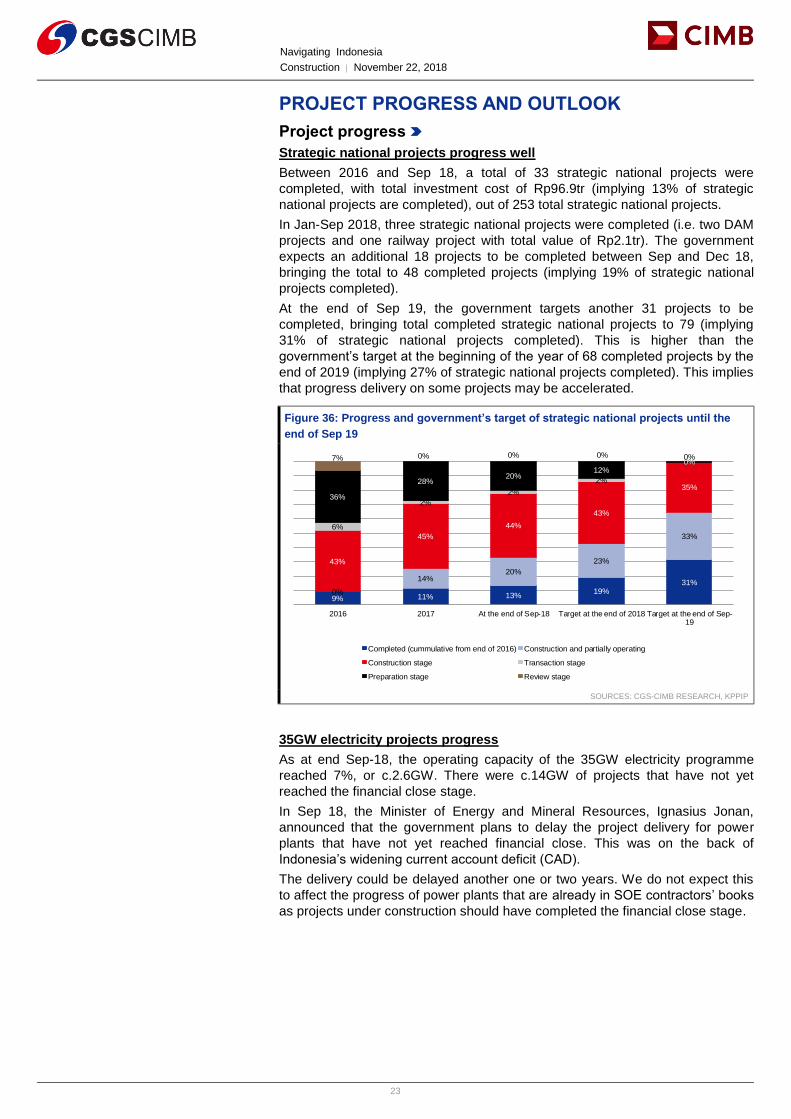

Strategic national projects progress well

Between 2016 and Sep 18, a total of 33 strategic national projects were

completed, with total investment cost of Rp96.9tr (implying 13% of strategic

national projects are completed), out of 253 total strategic national projects.

In Jan-Sep 2018, three strategic national projects were completed (i.e. two DAM

projects and one railway project with total value of Rp2.1tr). The government

expects an additional 18 projects to be completed between Sep and Dec 18,

bringing the total to 48 completed projects (implying 19% of strategic national

projects completed).

At the end of Sep 19, the government targets another 31 projects to be

completed, bringing total completed strategic national projects to 79 (implying

31% of strategic national projects completed). This is higher than the

government’s target at the beginning of the year of 68 completed projects by the

end of 2019 (implying 27% of strategic national projects completed). This implies

that progress delivery on some projects may be accelerated.

Figure 36: Progress and government’s target of strategic national projects until the

end of Sep 19

SOURCES: CGS-CIMB RESEARCH, KPPIP

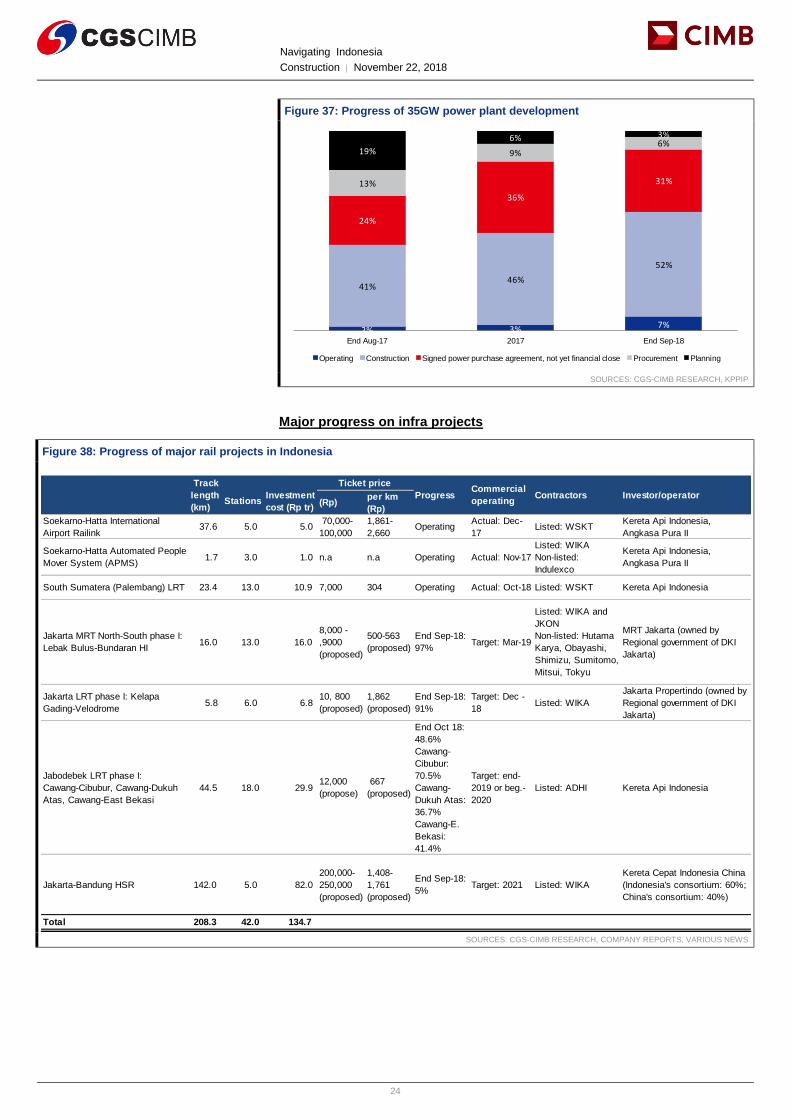

35GW electricity projects progress

As at end Sep-18, the operating capacity of the 35GW electricity programme

reached 7%, or c.2.6GW. There were c.14GW of projects that have not yet

reached the financial close stage.

In Sep 18, the Minister of Energy and Mineral Resources, Ignasius Jonan,

announced that the government plans to delay the project delivery for power

plants that have not yet reached financial close. This was on the back of

Indonesia’s widening current account deficit (CAD).

The delivery could be delayed another one or two years. We do not expect this

to affect the progress of power plants that are already in SOE contractors’ books

as projects under construction should have completed the financial close stage.

Title:

Source:

Please fill in the values above to have them entered in your report

9% 11% 13%19%

31%

0%

14%20%

23%

33%

43%

45%

44%

43%

35%

6%

2%

2%

2%

0%

36%

28%20%

12%0%

7% 0% 0% 0% 0%

2016 2017 At the end of Sep-18 Target at the end of 2018 Target at the end of Sep-19

Completed (cummulative from end of 2016) Construction and partially operating

Construction stage Transaction stage

Preparation stage Review stage

Navigating Indonesia

Construction │ November 22, 2018

24

Figure 37: Progress of 35GW power plant development

SOURCES: CGS-CIMB RESEARCH, KPPIP

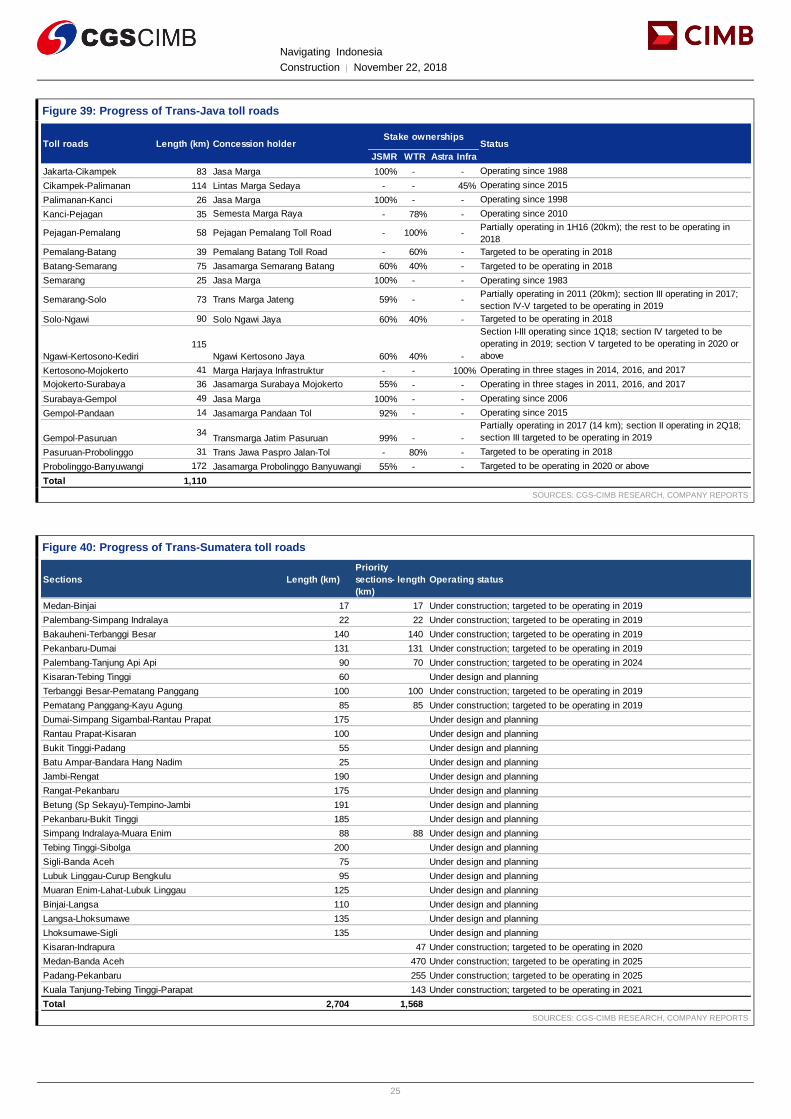

Major progress on infra projects

Figure 38: Progress of major rail projects in Indonesia

SOURCES: CGS-CIMB RESEARCH, COMPANY REPORTS, VARIOUS NEWS

Title:

Source:

Please fill in the values above to have them entered in your report

2% 3% 7%

41%46%

52%

24%

36%

31%13%

9%6%

19%

6% 3%

End Aug-17 2017 End Sep-18

Operating Construction Signed power purchase agreement, not yet financial close Procurement Planning

(Rp)per km

(Rp)

Soekarno-Hatta International

Airport Railink 37.6 5.0 5.0

70,000-

100,000

1,861-

2,660Operating

Actual: Dec-

17Listed: WSKT

Kereta Api Indonesia,

Angkasa Pura II

Soekarno-Hatta Automated People

Mover System (APMS) 1.7 3.0 1.0 n.a n.a Operating Actual: Nov-17

Listed: WIKA

Non-listed:

Indulexco

Kereta Api Indonesia,

Angkasa Pura II

South Sumatera (Palembang) LRT 23.4 13.0 10.9 7,000 304 Operating Actual: Oct-18 Listed: WSKT Kereta Api Indonesia

Jakarta MRT North-South phase I:

Lebak Bulus-Bundaran HI 16.0 13.0 16.0

8,000 -

,9000

(proposed)

500-563

(proposed)

End Sep-18:

97%Target: Mar-19

Listed: WIKA and

JKON

Non-listed: Hutama

Karya, Obayashi,

Shimizu, Sumitomo,

Mitsui, Tokyu

MRT Jakarta (owned by

Regional government of DKI

Jakarta)

Jakarta LRT phase I: Kelapa

Gading-Velodrome 5.8 6.0 6.8

10, 800

(proposed)

1,862

(proposed)

End Sep-18:

91%

Target: Dec -

18Listed: WIKA

Jakarta Propertindo (owned by

Regional government of DKI

Jakarta)

Jabodebek LRT phase I:

Cawang-Cibubur, Cawang-Dukuh

Atas, Cawang-East Bekasi

44.5 18.0 29.9 12,000

(propose)

667

(proposed)

End Oct 18:

48.6%

Cawang-

Cibubur:

70.5%

Cawang-

Dukuh Atas:

36.7%

Cawang-E.

Bekasi:

41.4%

Target: end-

2019 or beg.-

2020

Listed: ADHI Kereta Api Indonesia

Jakarta-Bandung HSR 142.0 5.0 82.0

200,000-

250,000

(proposed)

1,408-

1,761

(proposed)

End Sep-18:

5%Target: 2021 Listed: WIKA

Kereta Cepat Indonesia China

(Indonesia's consortium: 60%;

China's consortium: 40%)

Total 208.3 42.0 134.7

Contractors Investor/operator

Ticket price Track

length

(km)

Stations

Investment

cost (Rp tr)

ProgressCommercial

operating

Navigating Indonesia

Construction │ November 22, 2018

25

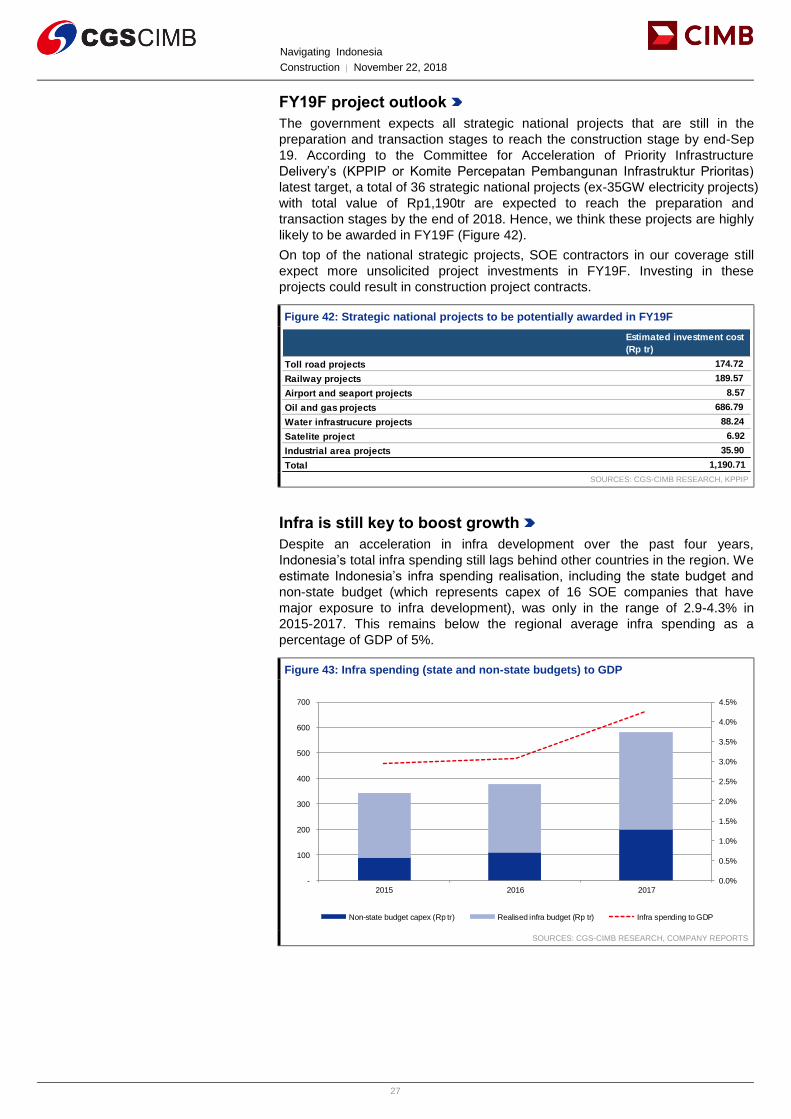

Figure 39: Progress of Trans-Java toll roads

SOURCES: CGS-CIMB RESEARCH, COMPANY REPORTS

Figure 40: Progress of Trans-Sumatera toll roads

SOURCES: CGS-CIMB RESEARCH, COMPANY REPORTS

JSMR WTR Astra Infra

Jakarta-Cikampek 83 Jasa Marga 100% - - Operating since 1988

Cikampek-Palimanan 114 Lintas Marga Sedaya - - 45% Operating since 2015

Palimanan-Kanci 26 Jasa Marga 100% - - Operating since 1998

Kanci-Pejagan 35 Semesta Marga Raya - 78% - Operating since 2010

Pejagan-Pemalang 58 Pejagan Pemalang Toll Road - 100% - Partially operating in 1H16 (20km); the rest to be operating in

2018

Pemalang-Batang 39 Pemalang Batang Toll Road - 60% - Targeted to be operating in 2018

Batang-Semarang 75 Jasamarga Semarang Batang 60% 40% - Targeted to be operating in 2018

Semarang 25 Jasa Marga 100% - - Operating since 1983

Semarang-Solo 73 Trans Marga Jateng 59% - - Partially operating in 2011 (20km); section III operating in 2017;

section IV-V targeted to be operating in 2019

Solo-Ngawi 90 Solo Ngawi Jaya 60% 40% - Targeted to be operating in 2018

Ngawi-Kertosono-Kediri

115

Ngawi Kertosono Jaya 60% 40% -

Section I-III operating since 1Q18; section IV targeted to be

operating in 2019; section V targeted to be operating in 2020 or

above

Kertosono-Mojokerto 41 Marga Harjaya Infrastruktur - - 100% Operating in three stages in 2014, 2016, and 2017

Mojokerto-Surabaya 36 Jasamarga Surabaya Mojokerto 55% - - Operating in three stages in 2011, 2016, and 2017

Surabaya-Gempol 49 Jasa Marga 100% - - Operating since 2006

Gempol-Pandaan 14 Jasamarga Pandaan Tol 92% - - Operating since 2015

Gempol-Pasuruan34

Transmarga Jatim Pasuruan 99% - -

Partially operating in 2017 (14 km); section II operating in 2Q18;

section III targeted to be operating in 2019

Pasuruan-Probolinggo 31 Trans Jawa Paspro Jalan-Tol - 80% - Targeted to be operating in 2018

Probolinggo-Banyuwangi 172 Jasamarga Probolinggo Banyuwangi 55% - - Targeted to be operating in 2020 or above

Total 1,110

Length (km) Concession holder StatusToll roadsStake ownerships

Sections Length (km)

Priority

sections- length

(km)

Operating status

Medan-Binjai 17 17 Under construction; targeted to be operating in 2019

Palembang-Simpang Indralaya 22 22 Under construction; targeted to be operating in 2019

Bakauheni-Terbanggi Besar 140 140 Under construction; targeted to be operating in 2019

Pekanbaru-Dumai 131 131 Under construction; targeted to be operating in 2019

Palembang-Tanjung Api Api 90 70 Under construction; targeted to be operating in 2024

Kisaran-Tebing Tinggi 60 Under design and planning

Terbanggi Besar-Pematang Panggang 100 100 Under construction; targeted to be operating in 2019

Pematang Panggang-Kayu Agung 85 85 Under construction; targeted to be operating in 2019

Dumai-Simpang Sigambal-Rantau Prapat 175 Under design and planning

Rantau Prapat-Kisaran 100 Under design and planning

Bukit Tinggi-Padang 55 Under design and planning

Batu Ampar-Bandara Hang Nadim 25 Under design and planning

Jambi-Rengat 190 Under design and planning

Rangat-Pekanbaru 175 Under design and planning

Betung (Sp Sekayu)-Tempino-Jambi 191 Under design and planning

Pekanbaru-Bukit Tinggi 185 Under design and planning

Simpang Indralaya-Muara Enim 88 88 Under design and planning

Tebing Tinggi-Sibolga 200 Under design and planning

Sigli-Banda Aceh 75 Under design and planning

Lubuk Linggau-Curup Bengkulu 95 Under design and planning

Muaran Enim-Lahat-Lubuk Linggau 125 Under design and planning

Binjai-Langsa 110 Under design and planning

Langsa-Lhoksumawe 135 Under design and planning

Lhoksumawe-Sigli 135 Under design and planning

Kisaran-Indrapura 47 Under construction; targeted to be operating in 2020

Medan-Banda Aceh 470 Under construction; targeted to be operating in 2025

Padang-Pekanbaru 255 Under construction; targeted to be operating in 2025

Kuala Tanjung-Tebing Tinggi-Parapat 143 Under construction; targeted to be operating in 2021

Total 2,704 1,568

Navigating Indonesia

Construction │ November 22, 2018

26

Progress on One Million Houses programme

The One Million Houses programme is part of the government’s efforts to reduce

the current housing backlog in Indonesia, and in anticipation of additional annual

housing backlog of c.800,000 units. In FY15, total housing backlog in Indonesia

was 11.5m units, of which 7.6m units (66%) were low-cost housing. The

government targets to lower the low-cost housing backlog to 5.4m units in

FY19F.

Since 2015, the government’s progress on the One Million Houses programme

has gradually increased. We expect this to continue to improve, supported by

implementation of the TAPERA savings programme (tabungan perumahan

rakyat, or public housing savings) in 2019.

Figure 41: Achievement of One Million Houses development programme

SOURCES: CGS-CIMB RESEARCH, MINISTRY OF PUBLIC WORKS AND HOUSING

Title:

Source:

Please fill in the values above to have them entered in your report

-

100,000

200,000

300,000

400,000

500,000

600,000

700,000

800,000

900,000

1,000,000

2015 2016 2017 2018F

Target Achievement

Achievement as of Oct-18

unit of house

Navigating Indonesia

Construction │ November 22, 2018

27

FY19F project outlook

The government expects all strategic national projects that are still in the

preparation and transaction stages to reach the construction stage by end-Sep

19. According to the Committee for Acceleration of Priority Infrastructure

Delivery’s (KPPIP or Komite Percepatan Pembangunan Infrastruktur Prioritas)

latest target, a total of 36 strategic national projects (ex-35GW electricity projects)

with total value of Rp1,190tr are expected to reach the preparation and

transaction stages by the end of 2018. Hence, we think these projects are highly

likely to be awarded in FY19F (Figure 42).

On top of the national strategic projects, SOE contractors in our coverage still

expect more unsolicited project investments in FY19F. Investing in these

projects could result in construction project contracts.

Figure 42: Strategic national projects to be potentially awarded in FY19F

SOURCES: CGS-CIMB RESEARCH, KPPIP

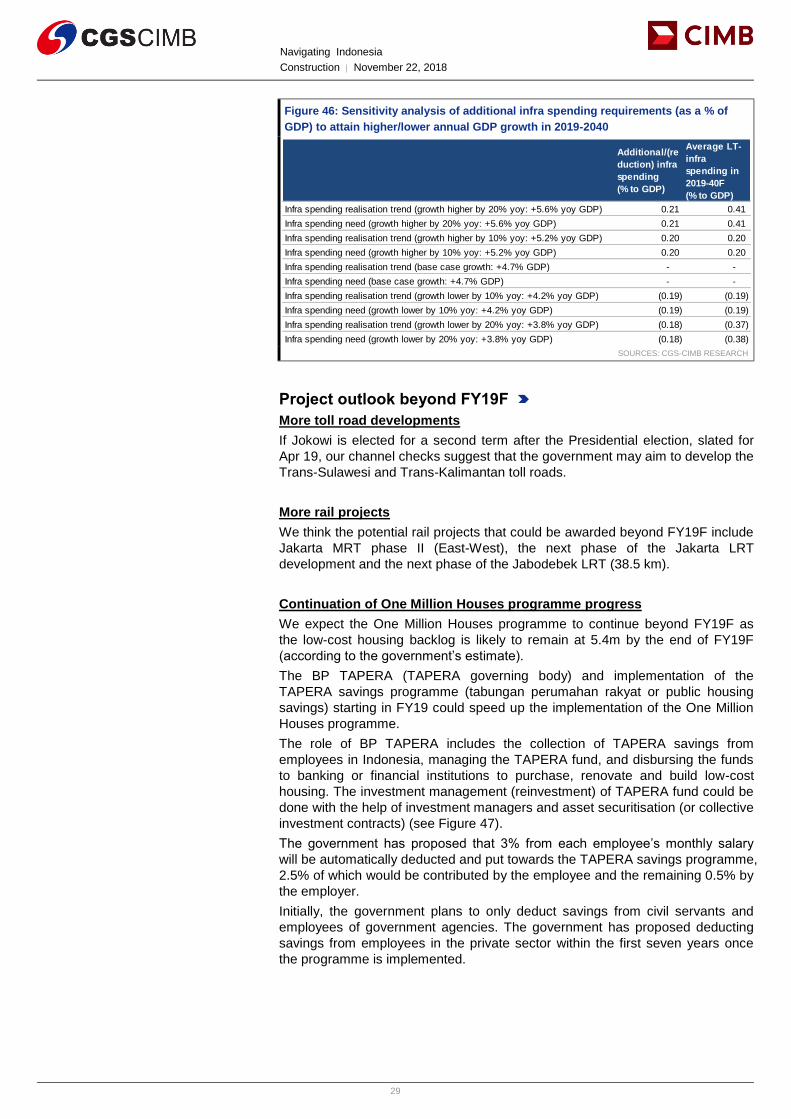

Infra is still key to boost growth

Despite an acceleration in infra development over the past four years,

Indonesia’s total infra spending still lags behind other countries in the region. We

estimate Indonesia’s infra spending realisation, including the state budget and

non-state budget (which represents capex of 16 SOE companies that have

major exposure to infra development), was only in the range of 2.9-4.3% in

2015-2017. This remains below the regional average infra spending as a

percentage of GDP of 5%.

Figure 43: Infra spending (state and non-state budgets) to GDP

SOURCES: CGS-CIMB RESEARCH, COMPANY REPORTS

Estimated investment cost

(Rp tr)

Toll road projects 174.72

Railway projects 189.57

Airport and seaport projects 8.57

Oil and gas projects 686.79

Water infrastrucure projects 88.24

Satelite project 6.92

Industrial area projects 35.90

Total 1,190.71

Title:

Source:

Please fill in the values above to have them entered in your report

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

3.0%

3.5%

4.0%

4.5%

-

100

200

300

400

500

600

700

2015 2016 2017

Non-state budget capex (Rp tr) Realised infra budget (Rp tr) Infra spending to GDP

Navigating Indonesia

Construction │ November 22, 2018

28

Based on data analytics provided by the Global Infrastructure Hub, in order for

Indonesia to achieve sustainable 4.7% annual GDP growth until 2040F,

Indonesia’s infra spending as a percentage of GDP needs to be maintained

above 4% until 2028F (Figure 44).

Figure 44: Sensitivity analysis of infra spending requirements and realisation (based on current trend) in 2019-2040F, as % of GDP

SOURCES: CGS-CIMB RESEARCH, GLOBAL INFRASTRUCTURE HUB

Figure 45: Sensitivity analysis of infra spending requirements and realisation (based on current trend) in 2019-2040F

SOURCES: CGS-CIMB RESEARCH, GLOBAL INFRASTRUCTURE HUB

Our sensitivity analysis from the data set suggests that Indonesia needs to

increase/decrease its infra spending by c.0.2% pt to GDP p.a. on average in

order to attain 10% higher/lower annual GDP growth from the base case GDP

growth assumption of 4.7% (Figure 45).

For example:

1) In FY19F, in our base-case scenario, in order to attain 4.7% GDP growth,

Indonesia needs to achieve 5% infra spending as a percentage of GDP.

2) In FY19F, in order for Indonesia to attain 5.2% annual GDP growth (10%

above our base-case GDP growth assumption of 4.7%), it needs to achieve

5.2% infra spending as a percentage of GDP.

3) In FY19F, if Indonesia only achieves 4.8% infra spending as a percentage of

GDP, its annual GDP growth could decline to 4.2% (10% below our base-case

GDP assumption growth of 4.7%).

Title:

Source:

Please fill in the values above to have them entered in your report

-

1.0

2.0

3.0

4.0

5.0

6.0

7.0

2019F 2020F 2021F 2022F 2023F 2024F 2025F 2026F 2027F 2028F 2029F 2030F 2031F 2032F 2033F 2034F 2035F 2036F 2037F 2038F 2039F 2040F