Embed Size (px)

Citation preview

Toll Roads│Indonesia│July 18, 2017

Company Note │ Alpha series

IMPORTANT DISCLOSURES, INCLUDING ANY REQUIRED RESEARCH CERTIFICATIONS, ARE PROVIDED AT THE END OF THIS REPORT. IF THIS REPORT IS DISTRIBUTED IN THE UNITED STATES IT IS DISTRIBUTED BY CIMB SECURITIES (USA), INC. AND IS CONSIDERED THIRD-PARTY AFFILIATED RESEARCH.

Powered by the EFA Platform

Jasa Marga King of the toll roads ■ JSMR is the oldest and best toll road proxy in the country, in our view. It is on track to

double the length of toll roads managed to 1,226km by FY20F (3-year CAGR of 20%). ■ We project revenue/core net profit CAGR of 16%/21% over FY16-26F. ■ We estimate its funding strategies would allow it to take on 31 toll road concessions

by FY20F, with manageable execution risk and strong government support. ■ At Rp61bn EV/km vs. weighted average replacement cost of Rp140bn/km and

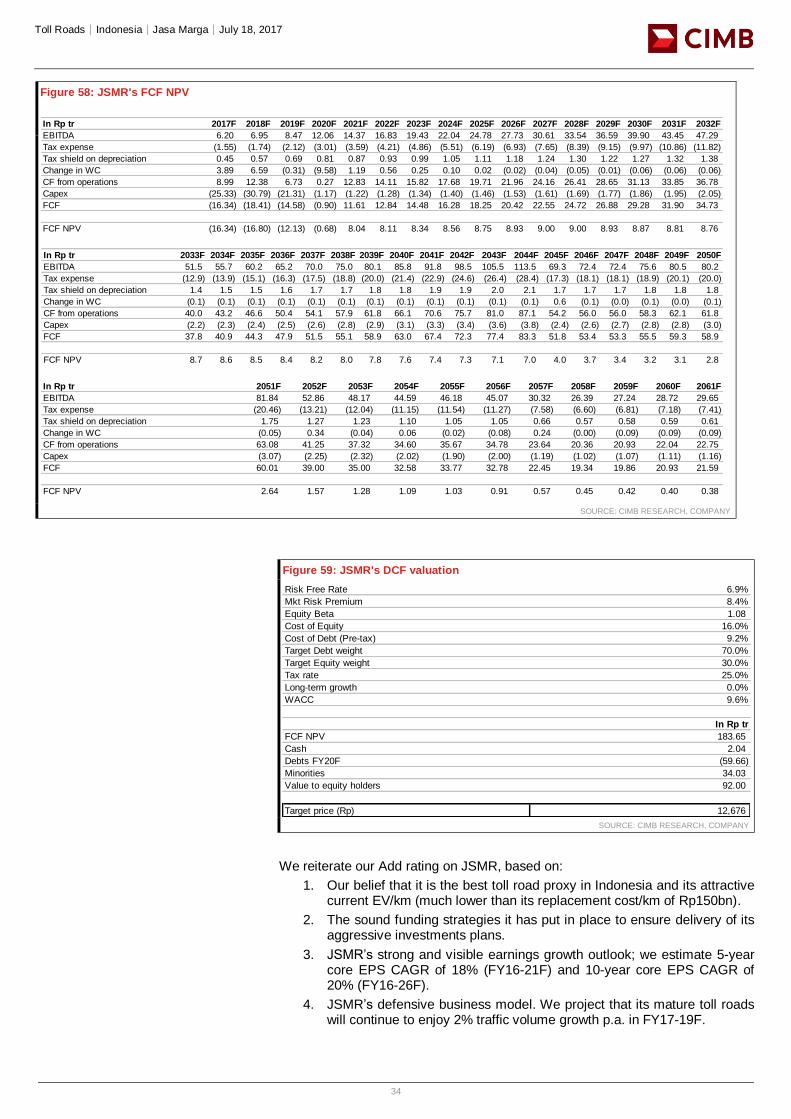

weighted average portfolio IRR of 14%, we think JSMR is under appreciated. ■ We deem our new TP of Rp6,500 (based on 11.5x FY17F EV/EBITDA, historical 5-

year mean) attractive as it is below our DCF value estimate of Rp12,676/share. Add.

The oldest toll road operator is also the best JSMR became a pure toll road operator in 2005 with deregulation. Its toll road concessions total 1,260km (longest of all players), comprising 31 concessions (13 old, 18 new, Figure 18). At end-Apr 2017, it operated 600km of toll roads (660km under development), a c.60% market share, but by traffic volume, its market share was 80%. JSMR’s concessions comprise some of the most congested and mature toll roads, mostly around Greater Jakarta. It aims to own 2,000km of concessions by 2019F at the earliest.

To double toll roads by FY20F; 10-year core net profit CAGR of 21% We estimate JSMR will operate 210km of new toll roads in FY17F, 268km in FY18F and 112km in FY19F, implying 1,189km of total operational toll roads by FY19F (Figure 20). We project EBITDA/core net profit CAGRs of 26%/12% for FY16-19F, 20%/19% for FY16-21F and 13%/21% for FY16-26F. We expect earnings growth to accelerate in long term as toll roads mature and tariffs rise every two years. As most of the concessions would link with the most populous island of Java (c.60% of GDP), we believe growth visibility is strong.

High IRR concessions, with potential upside from linkages JSMR targets 14% average project IRR, which we believe is achievable as only three of its 31 toll road investments are located ex-Java. Java’s high population density, numerous manufacturing centres (more class 2-5 vehicles that pay higher tariffs) and high logistics costs suggest higher IRRs for toll roads in Java than outer islands. By 2019F, once Trans Java, Trans Sumatra and key seaports in Java, Sumatra, Kalimantan and Sulawesi are developed, we expect spike in traffic as linkages are formed.

Has a lot on its plate but sound funding strategies help JSMR expects to invest total Rp70tr-80tr (US$5bn-6bn, CIMBe: ~Rp76tr) in the 16 projects under development. If its plan to add 200km of new toll roads in FY17F materialises, we estimate additional capex of Rp41.8tr in FY17F. We expect capex/debt to peak in FY18F/FY20F. Although it has huge capex planned, we think JSMR’s sound funding strategies and government support would alleviate cash flow concerns. We also expect its cost of debt to fall in future, with its planned asset securitisation programme.

Underappreciated growth and value Our core EPS rises by 2-26% in FY17-19F, as we introduce new forecasts from transfer of analyst coverage. JSMR’s current share price of Rp5,275 (at 9.8x FY17F EV/EBITDA) is 25% below its FY15 peak, due to concerns about earnings pressure from its aggressive growth plan. Our higher TP of Rp6,500 is based on 11.5x FY17F EV/EBITDA (historical 5-year mean), which we deem attractive given our DCF value estimate (WACC: 9.6%, LTG: 0%) of Rp12,676/share. Risks: insufficient funding, delay in new project operations.

SOURCE: COMPANY DATA, CIMB FORECASTS

Financial Summary Dec-15A Dec-16A Dec-17F Dec-18F Dec-19F

Revenue (Rpb) 9,848 16,661 11,345 14,376 17,556

Operating EBITDA (Rpb) 4,334 5,275 6,202 6,946 8,469

Net Profit (Rpb) 1,466 1,889 2,563 2,468 2,603

Core EPS (Rp) 206.8 270.2 299.4 340.1 358.7

Core EPS Growth (0.6%) 30.7% 10.8% 13.6% 5.5%

FD Core P/E (x) 25.51 20.07 17.62 15.51 14.71

DPS (Rp) 43.13 43.38 55.58 68.41 72.15

Dividend Yield 0.82% 0.82% 1.05% 1.30% 1.37%

EV/EBITDA (x) 11.04 9.86 9.75 9.78 9.04

P/FCFE (x) NA 543.9 NA NA NA

Net Gearing 102% 128% 104% 99% 108%

P/BV (x) 3.44 2.80 2.42 2.15 1.92

ROE 14.1% 15.3% 14.7% 14.7% 13.8%

% Change In Core EPS Estimates 2.2% 14.8% 25.6%

CIMB/consensus EPS (x) 1.34 1.20 1.23

Indonesia

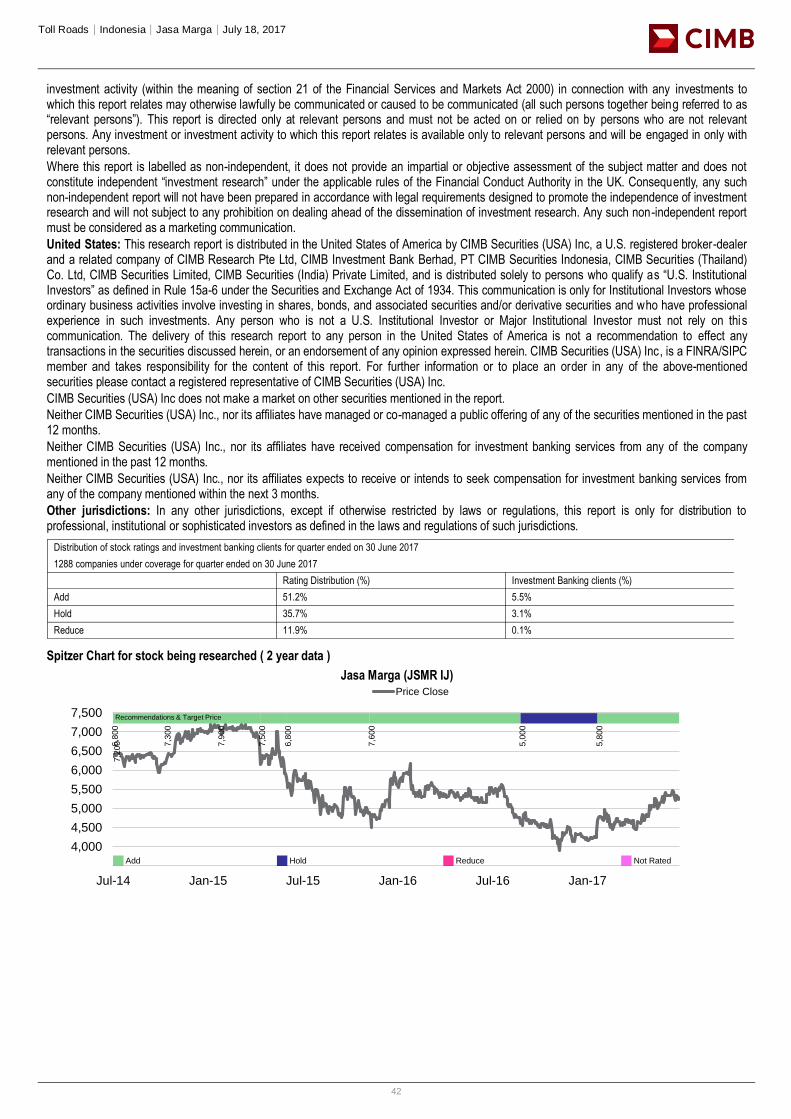

ADD (no change) Consensus ratings*: Buy 17 Hold 5 Sell 1

Current price: Rp5,275

Target price: Rp6,500

Previous target: Rp5,800

Up/downside: 23.2%

CIMB / Consensus: 11.3%

Reuters: JSMR.JK

Bloomberg: JSMR IJ

Market cap: US$2,873m

Rp38,285,272m

Average daily turnover: US$2.78m

Rp37,028m

Current shares o/s: 7,258m

Free float: 30.0% *Source: Bloomberg

Key changes in this note

FY17F core EPS increased by 2%.

FY18F core EPS increased by 15%.

FY19F core EPS increased by 26%.

Source: Bloomberg

Price performance 1M 3M 12M

Absolute (%) 2.4 14.4 -5

Relative (%) 0.3 9.7 -19.3

Major shareholders % held Government of Indonesia 70.0

Analyst(s)

Aurelia BARUS

T (62) 21 3006 1721 E [email protected]

66.0

74.0

82.0

90.0

98.0

106.0

3,700

4,200

4,700

5,200

5,700

6,200

Price Close Relative to JCI (RHS)

20

40

60

80

Jul-16 Oct-16 Jan-17 Apr-17

Vol m

Toll Roads│Indonesia│Jasa Marga│July 18, 2017

2

King of the toll roads

BACKGROUND

The oldest toll road operator in Indonesia

Based on Government Regulation No.4/1978 on Capital Investment of the Republic of Indonesia, the government of Indonesia established PT Jasa Marga (JSMR) on 1 Mar 1978. In 1978, JSMR operated the first toll road in Indonesia, Jakarta-Bogor-Ciawi (Jagorawi), the construction of which was funded by the state budget and foreign loan taken by the government. Subsequently, the Jagorawi toll road asset was handed over to JSMR through equity injection.

In 1980, with the issuance of Road Law No.3/1980, it was assigned the role of Indonesia’s toll road operator, and its key functions were to plan, build, operate, and maintain toll road facilities. This was to avoid over burdening the state budget with sizeable toll road investments. Until 1987, it was the only toll road operator in Indonesia. The development of toll roads was financed by the government of Indonesia via foreign loans and bond issuances by JSMR. The toll roads included Semarang toll road, Jakarta-Tangerang toll road, Prof. Dr. Ir. Sedyatmo toll road, Surabaya-Gempol toll road, and Belawan-Medan-Tanjung Morawa (Belmera) toll road.

By the end of 1980s, the government of Indonesia started to invite private entities to participate in toll road investment and development through a build, operate and transfer (BOT) scheme. As such, in 1990s, JSMR had a dual role as a toll road operator and the toll road authority, and gave out concession rights to private investors. During the financial crisis in 1998, most of the private toll road investors failed to realise their projects. Based on the prevailing rules and regulations at the time, JSMR, as the toll road authority, took over some of the concession rights, including those for Jakarta Outer Ring Road (JORR) and Cikampek-Purwakarta-Padalarang (Cipularang).

Deregulation turned JSMR into pure toll road operator in 2004

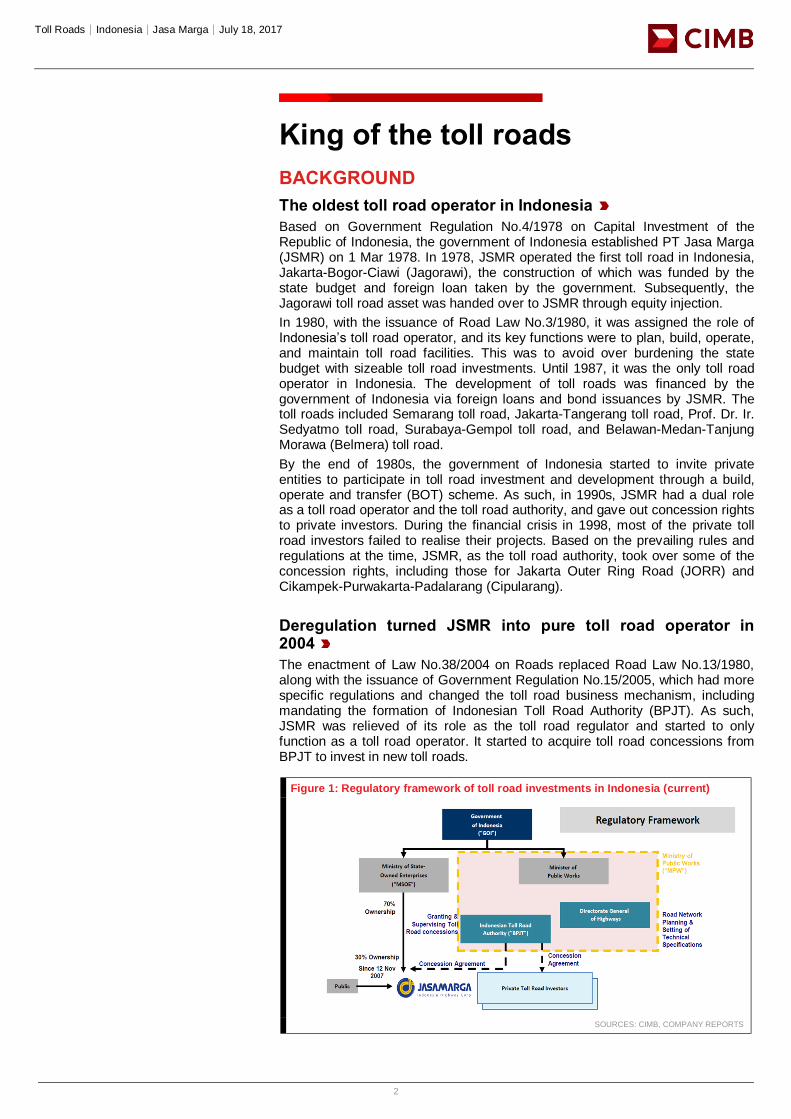

The enactment of Law No.38/2004 on Roads replaced Road Law No.13/1980, along with the issuance of Government Regulation No.15/2005, which had more specific regulations and changed the toll road business mechanism, including mandating the formation of Indonesian Toll Road Authority (BPJT). As such, JSMR was relieved of its role as the toll road regulator and started to only function as a toll road operator. It started to acquire toll road concessions from BPJT to invest in new toll roads.

Figure 1: Regulatory framework of toll road investments in Indonesia (current)

SOURCES: CIMB, COMPANY REPORTS

Toll Roads│Indonesia│Jasa Marga│July 18, 2017

3

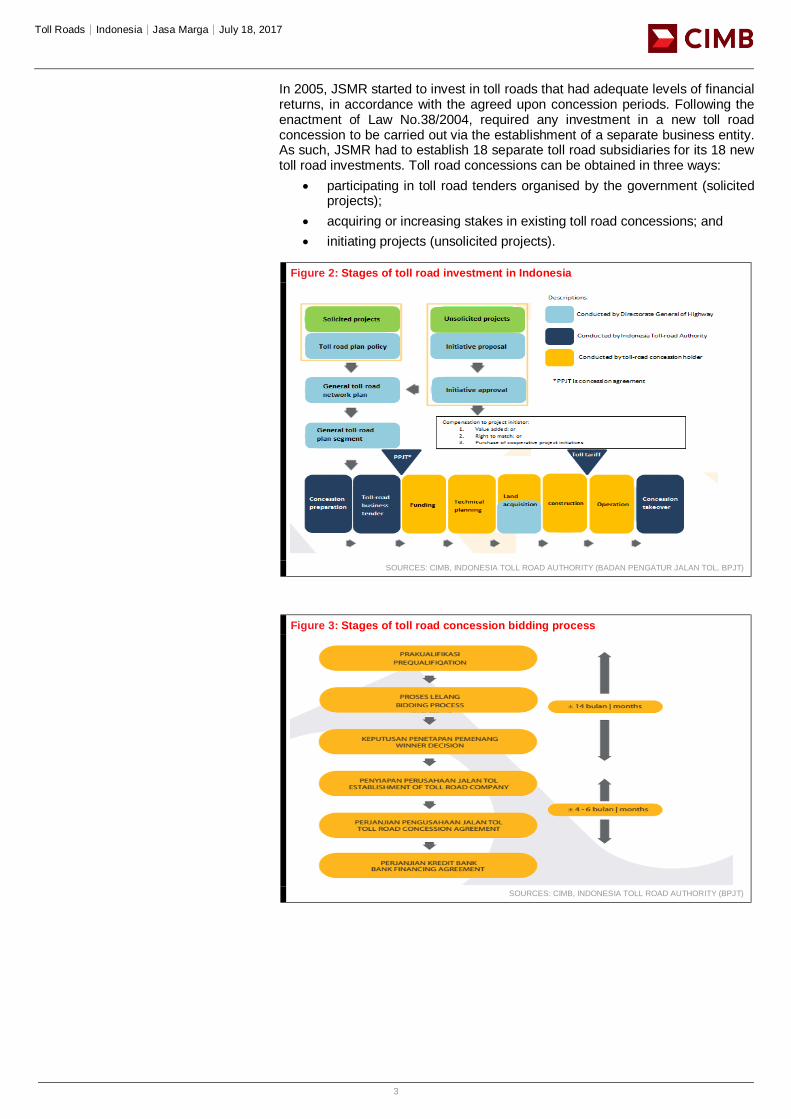

In 2005, JSMR started to invest in toll roads that had adequate levels of financial returns, in accordance with the agreed upon concession periods. Following the enactment of Law No.38/2004, required any investment in a new toll road concession to be carried out via the establishment of a separate business entity. As such, JSMR had to establish 18 separate toll road subsidiaries for its 18 new toll road investments. Toll road concessions can be obtained in three ways:

participating in toll road tenders organised by the government (solicited projects);

acquiring or increasing stakes in existing toll road concessions; and

initiating projects (unsolicited projects).

Figure 2: Stages of toll road investment in Indonesia

SOURCES: CIMB, INDONESIA TOLL ROAD AUTHORITY (BADAN PENGATUR JALAN TOL, BPJT)

Figure 3: Stages of toll road concession bidding process

SOURCES: CIMB, INDONESIA TOLL ROAD AUTHORITY (BPJT)

Toll Roads│Indonesia│Jasa Marga│July 18, 2017

4

Shareholding structure

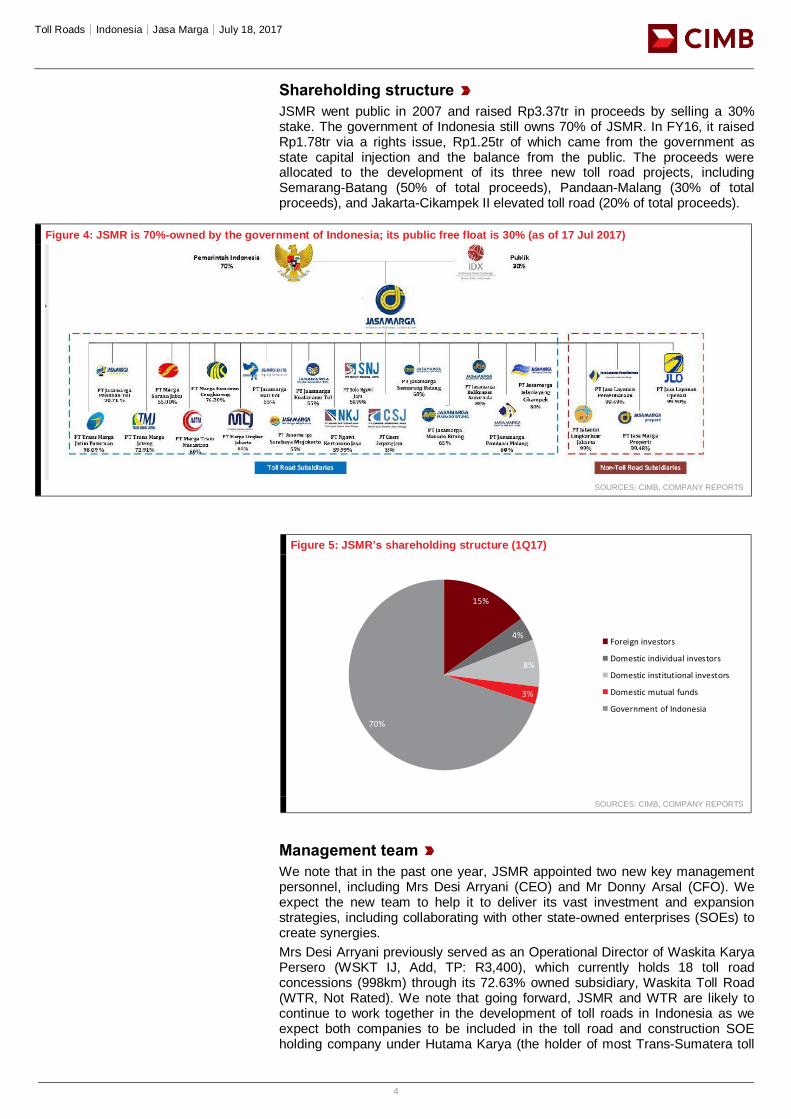

JSMR went public in 2007 and raised Rp3.37tr in proceeds by selling a 30% stake. The government of Indonesia still owns 70% of JSMR. In FY16, it raised Rp1.78tr via a rights issue, Rp1.25tr of which came from the government as state capital injection and the balance from the public. The proceeds were allocated to the development of its three new toll road projects, including Semarang-Batang (50% of total proceeds), Pandaan-Malang (30% of total proceeds), and Jakarta-Cikampek II elevated toll road (20% of total proceeds).

Figure 4: JSMR is 70%-owned by the government of Indonesia; its public free float is 30% (as of 17 Jul 2017)

SOURCES: CIMB, COMPANY REPORTS

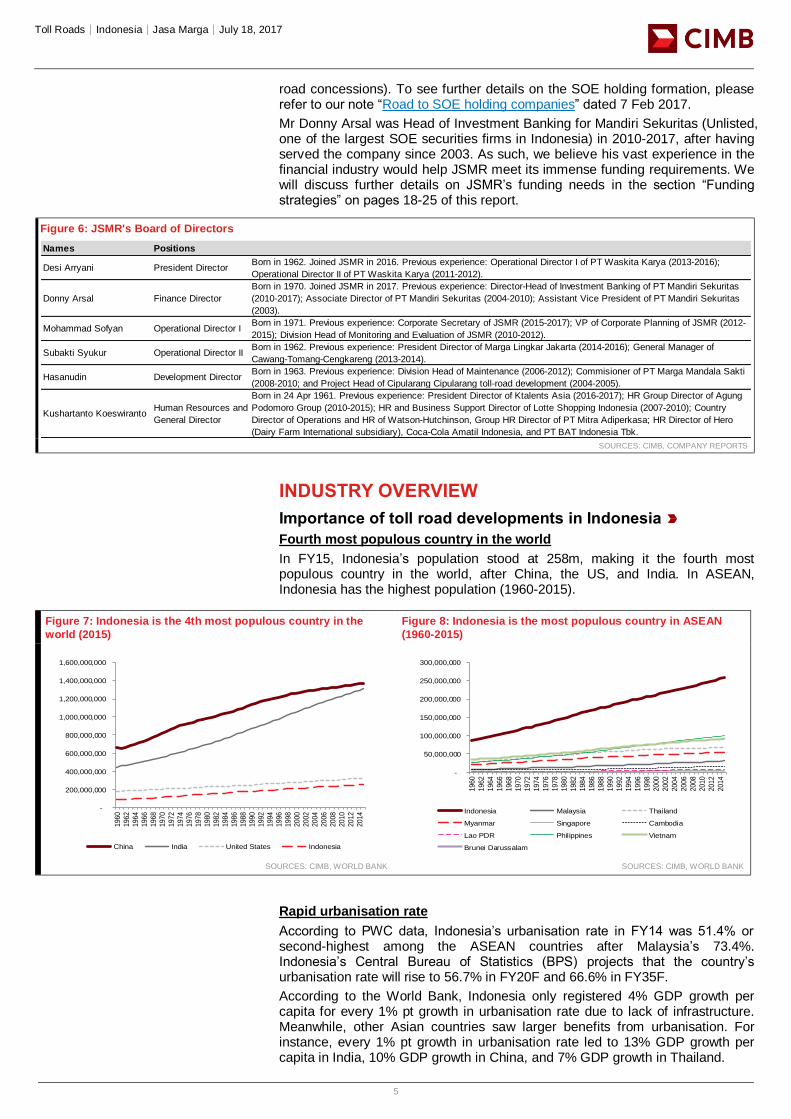

Figure 5: JSMR’s shareholding structure (1Q17)

SOURCES: CIMB, COMPANY REPORTS

Management team

We note that in the past one year, JSMR appointed two new key management personnel, including Mrs Desi Arryani (CEO) and Mr Donny Arsal (CFO). We expect the new team to help it to deliver its vast investment and expansion strategies, including collaborating with other state-owned enterprises (SOEs) to create synergies.

Mrs Desi Arryani previously served as an Operational Director of Waskita Karya Persero (WSKT IJ, Add, TP: R3,400), which currently holds 18 toll road concessions (998km) through its 72.63% owned subsidiary, Waskita Toll Road (WTR, Not Rated). We note that going forward, JSMR and WTR are likely to continue to work together in the development of toll roads in Indonesia as we expect both companies to be included in the toll road and construction SOE holding company under Hutama Karya (the holder of most Trans-Sumatera toll

Title:

Source:

Please fill in the values above to have them entered in your report15%

4%

8%

3%

70%

Foreign investors

Domestic individual investors

Domestic institutional investors

Domestic mutual funds

Government of Indonesia

Toll Roads│Indonesia│Jasa Marga│July 18, 2017

5

road concessions). To see further details on the SOE holding formation, please refer to our note “Road to SOE holding companies” dated 7 Feb 2017.

Mr Donny Arsal was Head of Investment Banking for Mandiri Sekuritas (Unlisted, one of the largest SOE securities firms in Indonesia) in 2010-2017, after having served the company since 2003. As such, we believe his vast experience in the financial industry would help JSMR meet its immense funding requirements. We will discuss further details on JSMR’s funding needs in the section “Funding strategies” on pages 18-25 of this report.

Figure 6: JSMR's Board of Directors

SOURCES: CIMB, COMPANY REPORTS

INDUSTRY OVERVIEW

Importance of toll road developments in Indonesia

Fourth most populous country in the world

In FY15, Indonesia’s population stood at 258m, making it the fourth most populous country in the world, after China, the US, and India. In ASEAN, Indonesia has the highest population (1960-2015).

Figure 7: Indonesia is the 4th most populous country in the

world (2015)

Figure 8: Indonesia is the most populous country in ASEAN

(1960-2015)

SOURCES: CIMB, WORLD BANK SOURCES: CIMB, WORLD BANK

Rapid urbanisation rate

According to PWC data, Indonesia’s urbanisation rate in FY14 was 51.4% or second-highest among the ASEAN countries after Malaysia’s 73.4%. Indonesia’s Central Bureau of Statistics (BPS) projects that the country’s urbanisation rate will rise to 56.7% in FY20F and 66.6% in FY35F.

According to the World Bank, Indonesia only registered 4% GDP growth per capita for every 1% pt growth in urbanisation rate due to lack of infrastructure. Meanwhile, other Asian countries saw larger benefits from urbanisation. For instance, every 1% pt growth in urbanisation rate led to 13% GDP growth per capita in India, 10% GDP growth in China, and 7% GDP growth in Thailand.

Names Positions

Desi Arryani President DirectorBorn in 1962. Joined JSMR in 2016. Previous experience: Operational Director I of PT Waskita Karya (2013-2016);

Operational Director II of PT Waskita Karya (2011-2012).

Donny Arsal Finance Director

Born in 1970. Joined JSMR in 2017. Previous experience: Director-Head of Investment Banking of PT Mandiri Sekuritas

(2010-2017); Associate Director of PT Mandiri Sekuritas (2004-2010); Assistant Vice President of PT Mandiri Sekuritas

(2003).

Mohammad Sofyan Operational Director IBorn in 1971. Previous experience: Corporate Secretary of JSMR (2015-2017); VP of Corporate Planning of JSMR (2012-

2015); Division Head of Monitoring and Evaluation of JSMR (2010-2012).

Subakti Syukur Operational Director IIBorn in 1962. Previous experience: President Director of Marga Lingkar Jakarta (2014-2016); General Manager of

Cawang-Tomang-Cengkareng (2013-2014).

Hasanudin Development DirectorBorn in 1963. Previous experience: Division Head of Maintenance (2006-2012); Commisioner of PT Marga Mandala Sakti

(2008-2010; and Project Head of Cipularang Cipularang toll-road development (2004-2005).

Kushartanto KoeswirantoHuman Resources and

General Director

Born in 24 Apr 1961. Previous experience: President Director of Ktalents Asia (2016-2017); HR Group Director of Agung

Podomoro Group (2010-2015); HR and Business Support Director of Lotte Shopping Indonesia (2007-2010); Country

Director of Operations and HR of Watson-Hutchinson, Group HR Director of PT Mitra Adiperkasa; HR Director of Hero

(Dairy Farm International subsidiary), Coca-Cola Amatil Indonesia, and PT BAT Indonesia Tbk.

Title:

Source:

Please fill in the values above to have them entered in your report

-

200,000,000

400,000,000

600,000,000

800,000,000

1,000,000,000

1,200,000,000

1,400,000,000

1,600,000,000

1960

1962

1964

1966

1968

1970

1972

1974

1976

1978

1980

1982

1984

1986

1988

1990

1992

1994

1996

1998

2000

2002

2004

2006

2008

2010

2012

2014

China India United States Indonesia

Title:

Source:

Please fill in the values above to have them entered in your report

-

50,000,000

100,000,000

150,000,000

200,000,000

250,000,000

300,000,000

1960

1962

1964

1966

1968

1970

1972

1974

1976

1978

1980

1982

1984

1986

1988

1990

1992

1994

1996

1998

2000

2002

2004

2006

2008

2010

2012

2014

Indonesia Malaysia Thailand

Myanmar Singapore Cambodia

Lao PDR Philippines Vietnam

Brunei Darussalam

Toll Roads│Indonesia│Jasa Marga│July 18, 2017

6

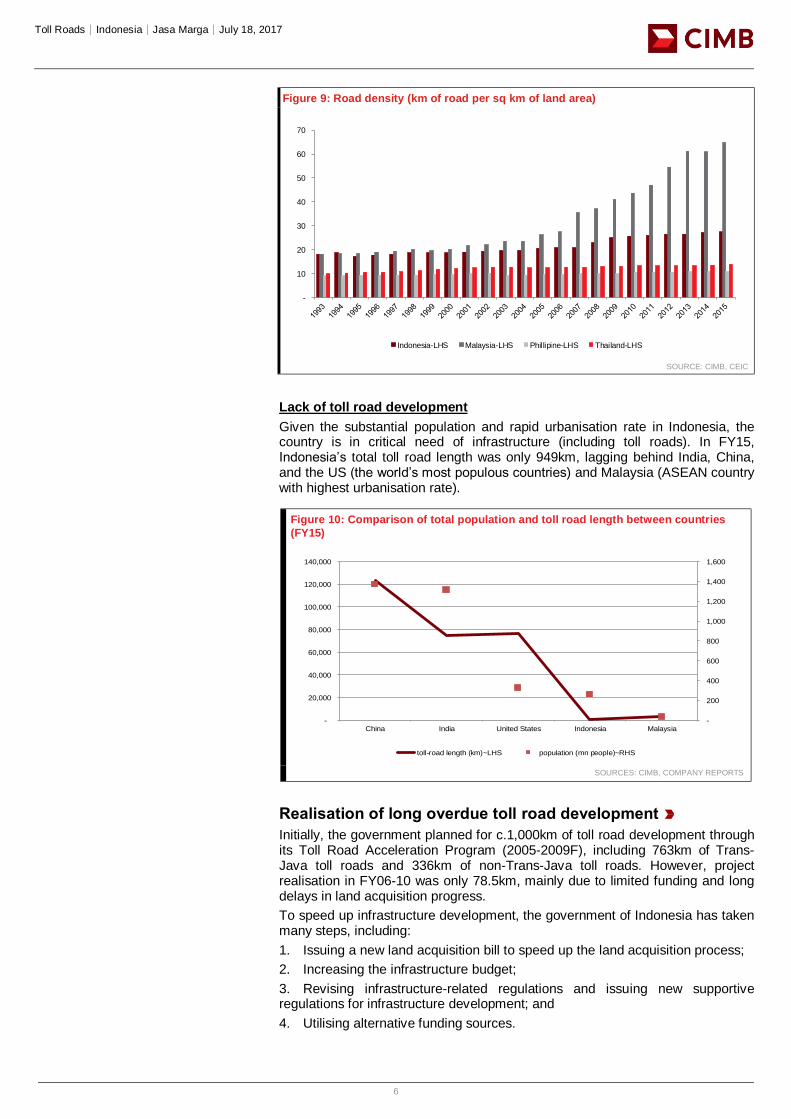

Figure 9: Road density (km of road per sq km of land area)

SOURCE: CIMB, CEIC

Lack of toll road development

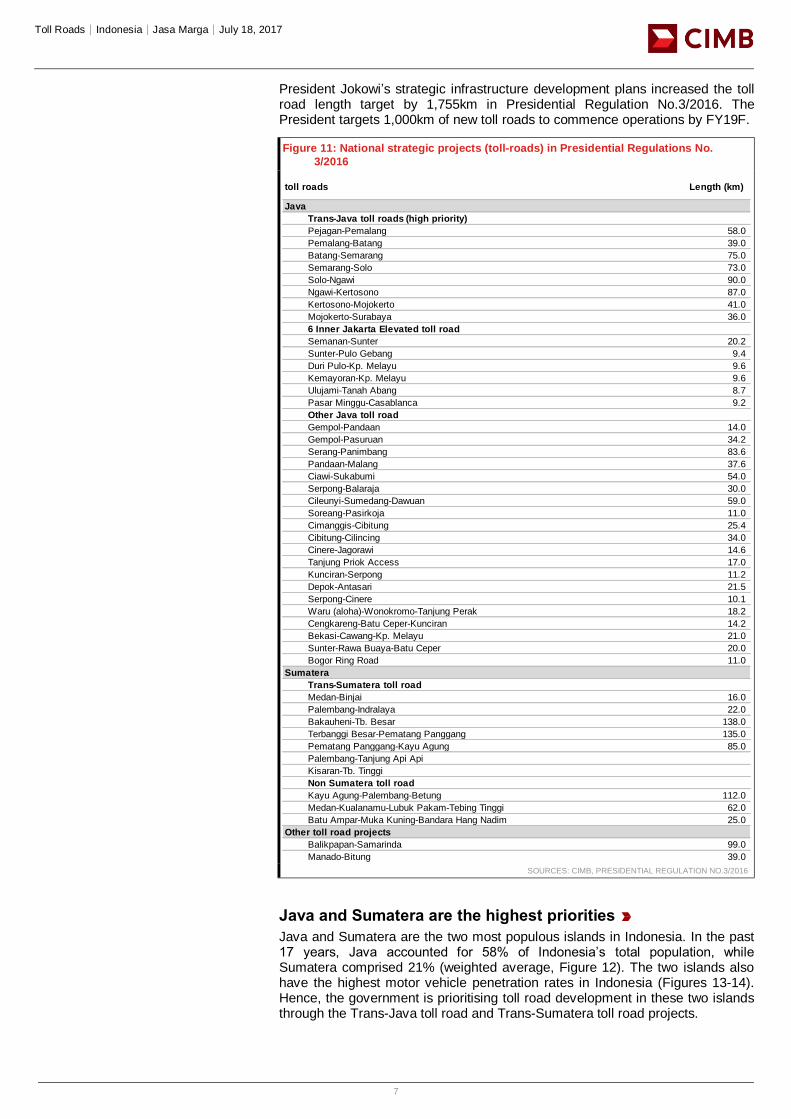

Given the substantial population and rapid urbanisation rate in Indonesia, the country is in critical need of infrastructure (including toll roads). In FY15, Indonesia’s total toll road length was only 949km, lagging behind India, China, and the US (the world’s most populous countries) and Malaysia (ASEAN country with highest urbanisation rate).

Figure 10: Comparison of total population and toll road length between countries

(FY15)

SOURCES: CIMB, COMPANY REPORTS

Realisation of long overdue toll road development

Initially, the government planned for c.1,000km of toll road development through its Toll Road Acceleration Program (2005-2009F), including 763km of Trans-Java toll roads and 336km of non-Trans-Java toll roads. However, project realisation in FY06-10 was only 78.5km, mainly due to limited funding and long delays in land acquisition progress.

To speed up infrastructure development, the government of Indonesia has taken many steps, including:

1. Issuing a new land acquisition bill to speed up the land acquisition process;

2. Increasing the infrastructure budget;

3. Revising infrastructure-related regulations and issuing new supportive regulations for infrastructure development; and

4. Utilising alternative funding sources.

Title:

Source:

Please fill in the values above to have them entered in your report

-

10

20

30

40

50

60

70

Indonesia-LHS Malaysia-LHS Phillipine-LHS Thailand-LHS

Title:

Source:

Please fill in the values above to have them entered in your report

-

200

400

600

800

1,000

1,200

1,400

1,600

-

20,000

40,000

60,000

80,000

100,000

120,000

140,000

China India United States Indonesia Malaysia

toll-road length (km)~LHS population (mn people)~RHS

Toll Roads│Indonesia│Jasa Marga│July 18, 2017

7

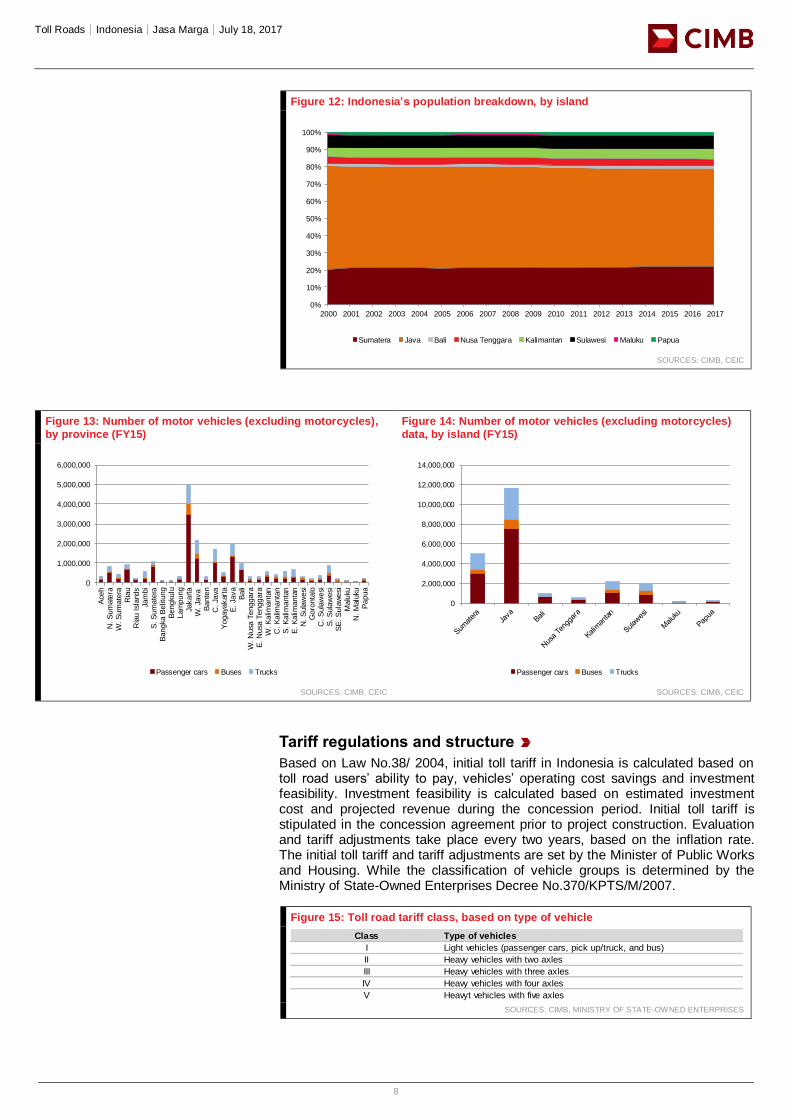

President Jokowi’s strategic infrastructure development plans increased the toll road length target by 1,755km in Presidential Regulation No.3/2016. The President targets 1,000km of new toll roads to commence operations by FY19F.

Figure 11: National strategic projects (toll-roads) in Presidential Regulations No.

3/2016

SOURCES: CIMB, PRESIDENTIAL REGULATION NO.3/2016

Java and Sumatera are the highest priorities

Java and Sumatera are the two most populous islands in Indonesia. In the past 17 years, Java accounted for 58% of Indonesia’s total population, while Sumatera comprised 21% (weighted average, Figure 12). The two islands also have the highest motor vehicle penetration rates in Indonesia (Figures 13-14). Hence, the government is prioritising toll road development in these two islands through the Trans-Java toll road and Trans-Sumatera toll road projects.

Length (km)

Java

Trans-Java toll roads (high priority)

Pejagan-Pemalang 58.0

Pemalang-Batang 39.0

Batang-Semarang 75.0

Semarang-Solo 73.0

Solo-Ngawi 90.0

Ngawi-Kertosono 87.0

Kertosono-Mojokerto 41.0

Mojokerto-Surabaya 36.0

6 Inner Jakarta Elevated toll road

Semanan-Sunter 20.2

Sunter-Pulo Gebang 9.4

Duri Pulo-Kp. Melayu 9.6

Kemayoran-Kp. Melayu 9.6

Ulujami-Tanah Abang 8.7

Pasar Minggu-Casablanca 9.2

Other Java toll road

Gempol-Pandaan 14.0

Gempol-Pasuruan 34.2

Serang-Panimbang 83.6

Pandaan-Malang 37.6

Ciawi-Sukabumi 54.0

Serpong-Balaraja 30.0

Cileunyi-Sumedang-Dawuan 59.0

Soreang-Pasirkoja 11.0

Cimanggis-Cibitung 25.4

Cibitung-Cilincing 34.0

Cinere-Jagorawi 14.6

Tanjung Priok Access 17.0

Kunciran-Serpong 11.2

Depok-Antasari 21.5

Serpong-Cinere 10.1

Waru (aloha)-Wonokromo-Tanjung Perak 18.2

Cengkareng-Batu Ceper-Kunciran 14.2

Bekasi-Cawang-Kp. Melayu 21.0

Sunter-Rawa Buaya-Batu Ceper 20.0

Bogor Ring Road 11.0

Sumatera

Trans-Sumatera toll road

Medan-Binjai 16.0

Palembang-Indralaya 22.0

Bakauheni-Tb. Besar 138.0

Terbanggi Besar-Pematang Panggang 135.0

Pematang Panggang-Kayu Agung 85.0

Palembang-Tanjung Api Api

Kisaran-Tb. Tinggi

Non Sumatera toll road

Kayu Agung-Palembang-Betung 112.0

Medan-Kualanamu-Lubuk Pakam-Tebing Tinggi 62.0

Batu Ampar-Muka Kuning-Bandara Hang Nadim 25.0

Other toll road projects

Balikpapan-Samarinda 99.0

Manado-Bitung 39.0

toll roads

Toll Roads│Indonesia│Jasa Marga│July 18, 2017

8

Figure 12: Indonesia’s population breakdown, by island

SOURCES: CIMB, CEIC

Figure 13: Number of motor vehicles (excluding motorcycles), by province (FY15)

Figure 14: Number of motor vehicles (excluding motorcycles) data, by island (FY15)

SOURCES: CIMB, CEIC SOURCES: CIMB, CEIC

Tariff regulations and structure

Based on Law No.38/ 2004, initial toll tariff in Indonesia is calculated based on toll road users’ ability to pay, vehicles’ operating cost savings and investment feasibility. Investment feasibility is calculated based on estimated investment cost and projected revenue during the concession period. Initial toll tariff is stipulated in the concession agreement prior to project construction. Evaluation and tariff adjustments take place every two years, based on the inflation rate. The initial toll tariff and tariff adjustments are set by the Minister of Public Works and Housing. While the classification of vehicle groups is determined by the Ministry of State-Owned Enterprises Decree No.370/KPTS/M/2007.

Figure 15: Toll road tariff class, based on type of vehicle

SOURCES: CIMB, MINISTRY OF STATE-OWNED ENTERPRISES

Title:

Source:

Please fill in the values above to have them entered in your report

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

Sumatera Java Bali Nusa Tenggara Kalimantan Sulawesi Maluku Papua

Title:

Source:

Please fill in the values above to have them entered in your report

0

1,000,000

2,000,000

3,000,000

4,000,000

5,000,000

6,000,000

Ace

hN

. S

um

ate

raW

. S

um

ate

raR

iau

Ria

u Isl

and

sJa

mbi

S. S

um

ate

raB

angka

Belit

ung

Bengku

luLam

pung

Jakarta

W. Ja

va

Bante

nC

. Ja

vaY

ogaya

kar

taE

. Ja

va

Bali

W. N

usa

Tenggara

E. N

usa

Tenggara

W. K

alim

anta

nC

. K

alim

anta

nS

. K

alim

anta

nE

. K

alim

anta

nN

. S

ula

wesi

Goro

nta

loC

. S

ula

wesi

S. S

ula

wesi

SE

. S

ula

wesi

Malu

kuN

. M

aluku

Papua

Passenger cars Buses Trucks

Title:

Source:

Please fill in the values above to have them entered in your report

0

2,000,000

4,000,000

6,000,000

8,000,000

10,000,000

12,000,000

14,000,000

Passenger cars Buses Trucks

Class Type of vehicles

I Light vehicles (passenger cars, pick up/truck, and bus)

II Heavy vehicles with two axles

III Heavy vehicles with three axles

IV Heavy vehicles with four axles

V Heavyt vehicles with five axles

Toll Roads│Indonesia│Jasa Marga│July 18, 2017

9

Improved land acquisition process

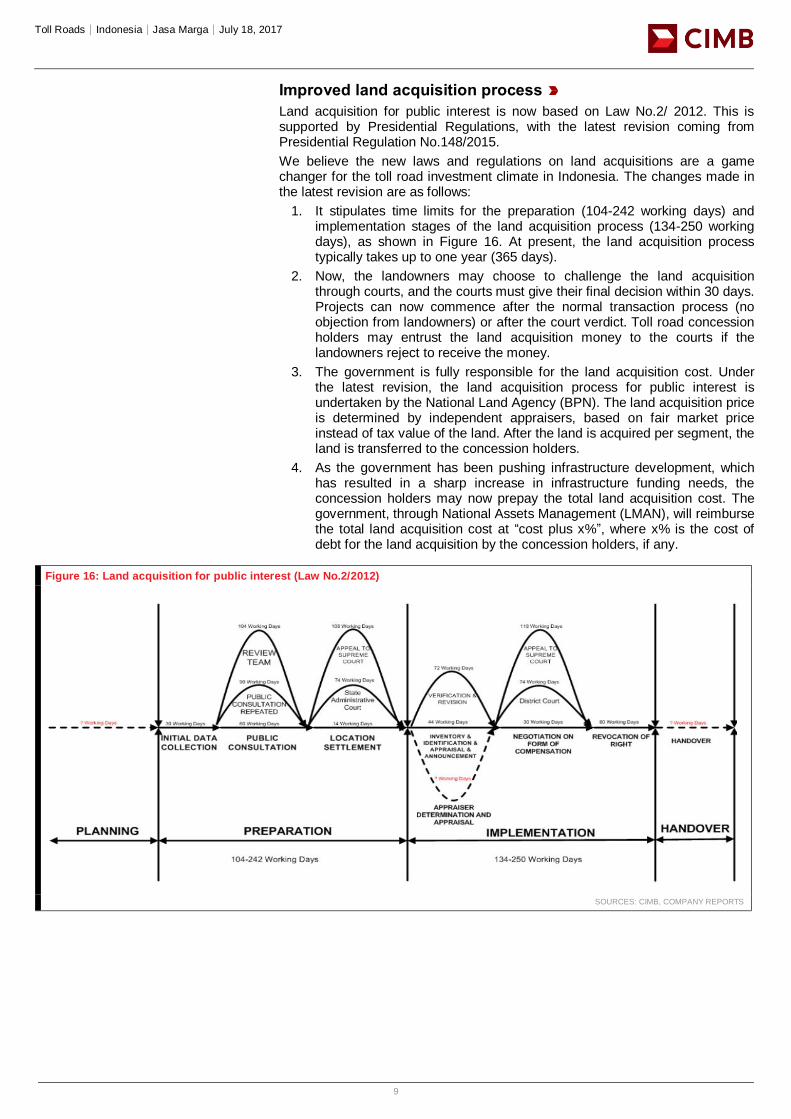

Land acquisition for public interest is now based on Law No.2/ 2012. This is supported by Presidential Regulations, with the latest revision coming from Presidential Regulation No.148/2015.

We believe the new laws and regulations on land acquisitions are a game changer for the toll road investment climate in Indonesia. The changes made in the latest revision are as follows:

1. It stipulates time limits for the preparation (104-242 working days) and implementation stages of the land acquisition process (134-250 working days), as shown in Figure 16. At present, the land acquisition process typically takes up to one year (365 days).

2. Now, the landowners may choose to challenge the land acquisition through courts, and the courts must give their final decision within 30 days. Projects can now commence after the normal transaction process (no objection from landowners) or after the court verdict. Toll road concession holders may entrust the land acquisition money to the courts if the landowners reject to receive the money.

3. The government is fully responsible for the land acquisition cost. Under the latest revision, the land acquisition process for public interest is undertaken by the National Land Agency (BPN). The land acquisition price is determined by independent appraisers, based on fair market price instead of tax value of the land. After the land is acquired per segment, the land is transferred to the concession holders.

4. As the government has been pushing infrastructure development, which has resulted in a sharp increase in infrastructure funding needs, the concession holders may now prepay the total land acquisition cost. The government, through National Assets Management (LMAN), will reimburse the total land acquisition cost at “cost plus x%”, where x% is the cost of debt for the land acquisition by the concession holders, if any.

Figure 16: Land acquisition for public interest (Law No.2/2012)

SOURCES: CIMB, COMPANY REPORTS

Toll Roads│Indonesia│Jasa Marga│July 18, 2017

10

LEADING TOLL ROAD OPERATOR IN INDONESIA

Longest toll road concession holder

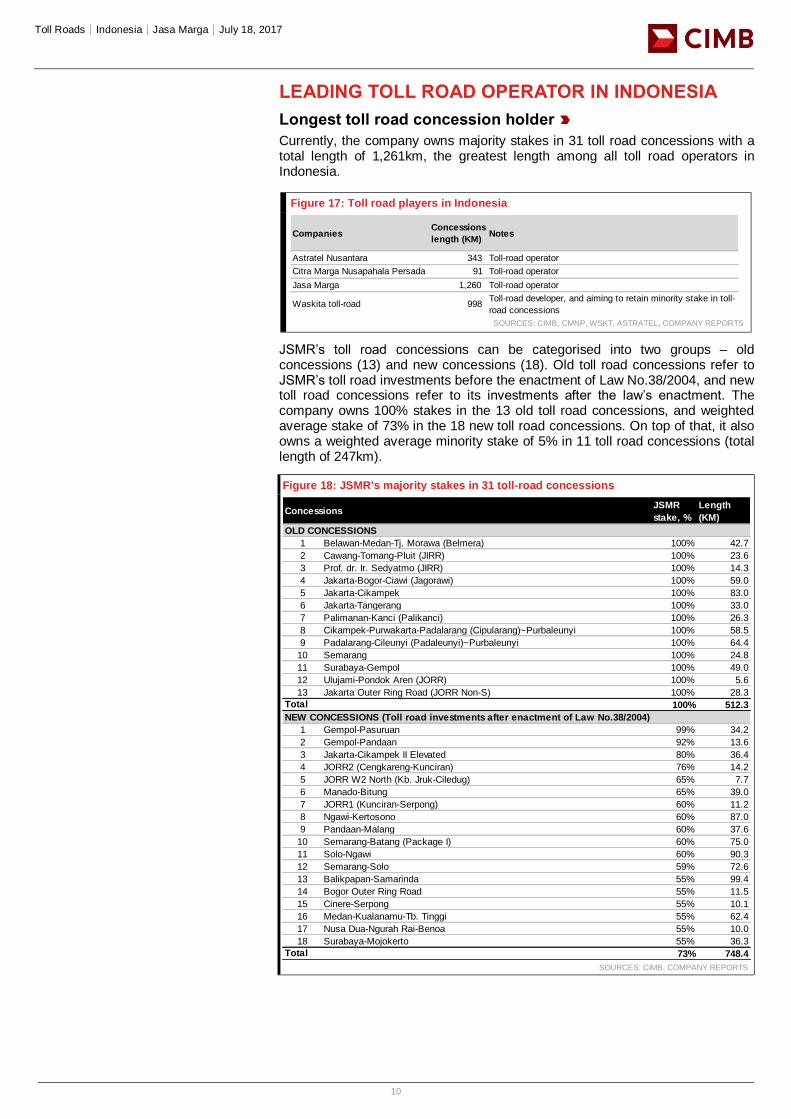

Currently, the company owns majority stakes in 31 toll road concessions with a total length of 1,261km, the greatest length among all toll road operators in Indonesia.

Figure 17: Toll road players in Indonesia

SOURCES: CIMB, CMNP, WSKT, ASTRATEL, COMPANY REPORTS

JSMR’s toll road concessions can be categorised into two groups – old concessions (13) and new concessions (18). Old toll road concessions refer to JSMR’s toll road investments before the enactment of Law No.38/2004, and new toll road concessions refer to its investments after the law’s enactment. The company owns 100% stakes in the 13 old toll road concessions, and weighted average stake of 73% in the 18 new toll road concessions. On top of that, it also owns a weighted average minority stake of 5% in 11 toll road concessions (total length of 247km).

Figure 18: JSMR's majority stakes in 31 toll-road concessions

SOURCES: CIMB, COMPANY REPORTS

CompaniesConcessions

length (KM)Notes

Astratel Nusantara 343 Toll-road operator

Citra Marga Nusapahala Persada 91 Toll-road operator

Jasa Marga 1,260 Toll-road operator

Waskita toll-road 998 Toll-road developer, and aiming to retain minority stake in toll-

road concessions

JSMR

stake, %

Length

(KM)

OLD CONCESSIONS

1 Belawan-Medan-Tj. Morawa (Belmera) 100% 42.7

2 Cawang-Tomang-Pluit (JIRR) 100% 23.6

3 Prof. dr. Ir. Sedyatmo (JIRR) 100% 14.3

4 Jakarta-Bogor-Ciawi (Jagorawi) 100% 59.0

5 Jakarta-Cikampek 100% 83.0

6 Jakarta-Tangerang 100% 33.0

7 Palimanan-Kanci (Palikanci) 100% 26.3

8 Cikampek-Purwakarta-Padalarang (Cipularang)~Purbaleunyi 100% 58.5

9 Padalarang-Cileunyi (Padaleunyi)~Purbaleunyi 100% 64.4

10 Semarang 100% 24.8

11 Surabaya-Gempol 100% 49.0

12 Ulujami-Pondok Aren (JORR) 100% 5.6

13 Jakarta Outer Ring Road (JORR Non-S) 100% 28.3

100% 512.3

NEW CONCESSIONS (Toll road investments after enactment of Law No.38/2004)

1 Gempol-Pasuruan 99% 34.2

2 Gempol-Pandaan 92% 13.6

3 Jakarta-Cikampek II Elevated 80% 36.4

4 JORR2 (Cengkareng-Kunciran) 76% 14.2

5 JORR W2 North (Kb. Jruk-Ciledug) 65% 7.7

6 Manado-Bitung 65% 39.0

7 JORR1 (Kunciran-Serpong) 60% 11.2

8 Ngawi-Kertosono 60% 87.0

9 Pandaan-Malang 60% 37.6

10 Semarang-Batang (Package I) 60% 75.0

11 Solo-Ngawi 60% 90.3

12 Semarang-Solo 59% 72.6

13 Balikpapan-Samarinda 55% 99.4

14 Bogor Outer Ring Road 55% 11.5

15 Cinere-Serpong 55% 10.1

16 Medan-Kualanamu-Tb. Tinggi 55% 62.4

17 Nusa Dua-Ngurah Rai-Benoa 55% 10.0

18 Surabaya-Mojokerto 55% 36.3

73% 748.4

Total

Total

Concessions

Toll Roads│Indonesia│Jasa Marga│July 18, 2017

11

Figure 19: JSMR's minority stakes in 11 toll-road concessions

SOURCES: CIMB, COMPANY REPORTS

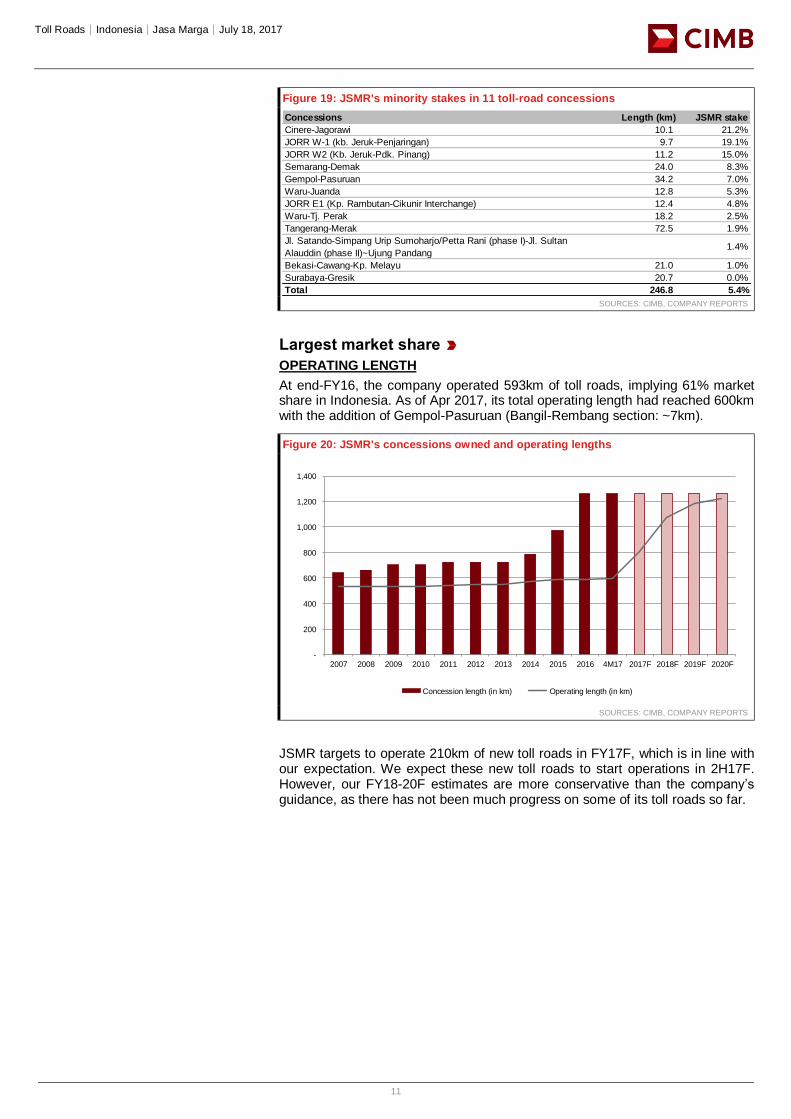

Largest market share

OPERATING LENGTH

At end-FY16, the company operated 593km of toll roads, implying 61% market share in Indonesia. As of Apr 2017, its total operating length had reached 600km with the addition of Gempol-Pasuruan (Bangil-Rembang section: ~7km).

Figure 20: JSMR's concessions owned and operating lengths

SOURCES: CIMB, COMPANY REPORTS

JSMR targets to operate 210km of new toll roads in FY17F, which is in line with our expectation. We expect these new toll roads to start operations in 2H17F. However, our FY18-20F estimates are more conservative than the company’s guidance, as there has not been much progress on some of its toll roads so far.

Concessions Length (km) JSMR stake

Cinere-Jagorawi 10.1 21.2%

JORR W-1 (kb. Jeruk-Penjaringan) 9.7 19.1%

JORR W2 (Kb. Jeruk-Pdk. Pinang) 11.2 15.0%

Semarang-Demak 24.0 8.3%

Gempol-Pasuruan 34.2 7.0%

Waru-Juanda 12.8 5.3%

JORR E1 (Kp. Rambutan-Cikunir Interchange) 12.4 4.8%

Waru-Tj. Perak 18.2 2.5%

Tangerang-Merak 72.5 1.9%

Jl. Satando-Simpang Urip Sumoharjo/Petta Rani (phase I)-Jl. Sultan

Alauddin (phase II)~Ujung Pandang1.4%

Bekasi-Cawang-Kp. Melayu 21.0 1.0%

Surabaya-Gresik 20.7 0.0%

Total 246.8 5.4%

Title:

Source:

Please fill in the values above to have them entered in your report

-

200

400

600

800

1,000

1,200

1,400

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 4M17 2017F 2018F 2019F 2020F

Concession length (in km) Operating length (in km)

Toll Roads│Indonesia│Jasa Marga│July 18, 2017

12

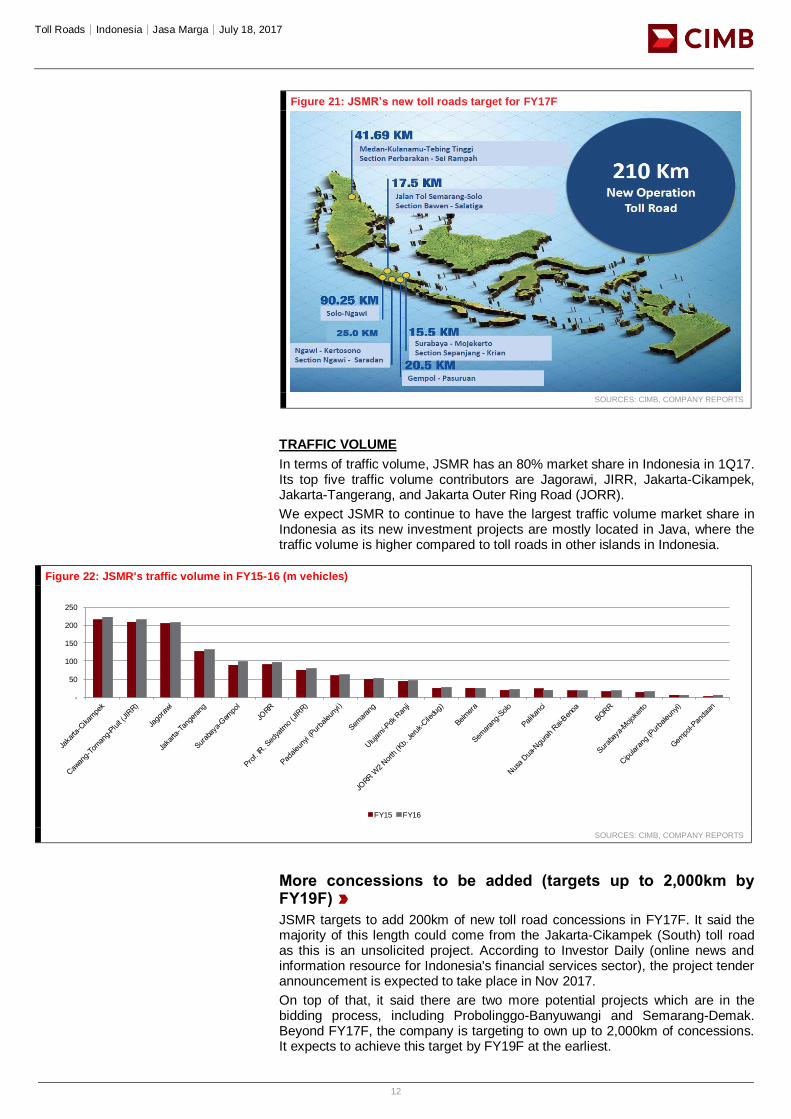

Figure 21: JSMR’s new toll roads target for FY17F

SOURCES: CIMB, COMPANY REPORTS

TRAFFIC VOLUME

In terms of traffic volume, JSMR has an 80% market share in Indonesia in 1Q17. Its top five traffic volume contributors are Jagorawi, JIRR, Jakarta-Cikampek, Jakarta-Tangerang, and Jakarta Outer Ring Road (JORR).

We expect JSMR to continue to have the largest traffic volume market share in Indonesia as its new investment projects are mostly located in Java, where the traffic volume is higher compared to toll roads in other islands in Indonesia.

Figure 22: JSMR's traffic volume in FY15-16 (m vehicles)

SOURCES: CIMB, COMPANY REPORTS

More concessions to be added (targets up to 2,000km by FY19F)

JSMR targets to add 200km of new toll road concessions in FY17F. It said the majority of this length could come from the Jakarta-Cikampek (South) toll road as this is an unsolicited project. According to Investor Daily (online news and information resource for Indonesia's financial services sector), the project tender announcement is expected to take place in Nov 2017.

On top of that, it said there are two more potential projects which are in the bidding process, including Probolinggo-Banyuwangi and Semarang-Demak. Beyond FY17F, the company is targeting to own up to 2,000km of concessions. It expects to achieve this target by FY19F at the earliest.

Title:

Source:

Please fill in the values above to have them entered in your report

-

50

100

150

200

250

FY15 FY16

Toll Roads│Indonesia│Jasa Marga│July 18, 2017

13

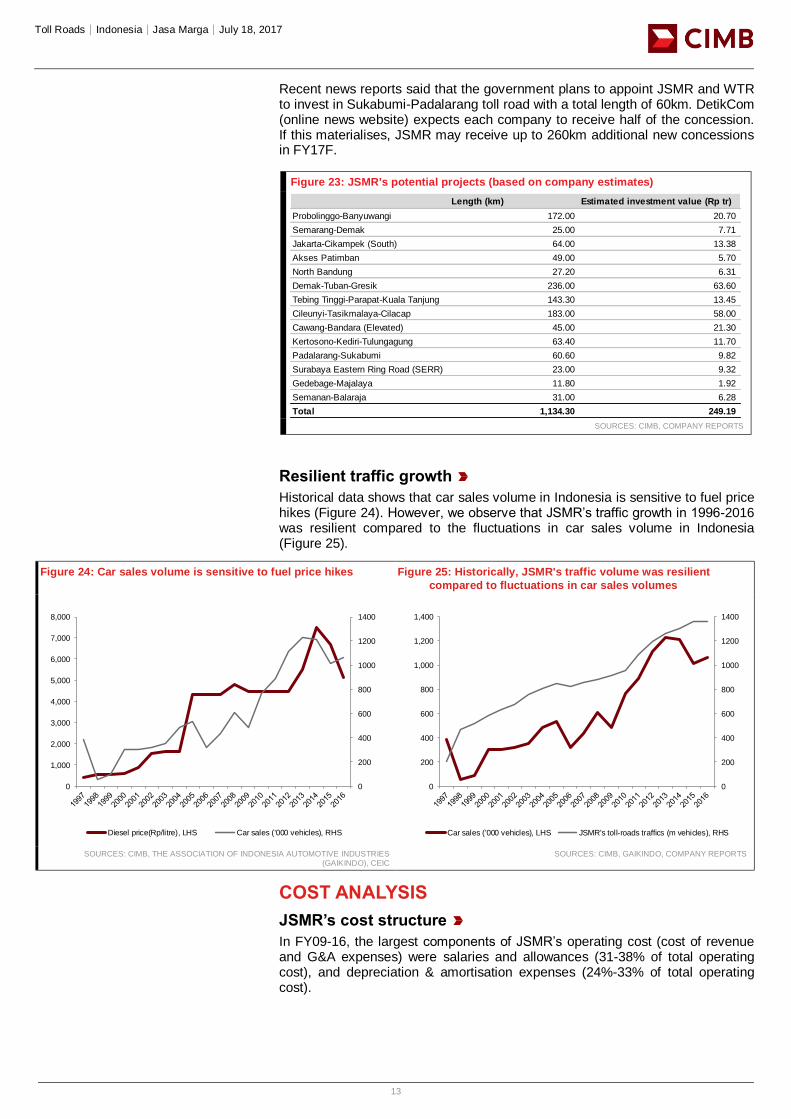

Recent news reports said that the government plans to appoint JSMR and WTR to invest in Sukabumi-Padalarang toll road with a total length of 60km. DetikCom (online news website) expects each company to receive half of the concession. If this materialises, JSMR may receive up to 260km additional new concessions in FY17F.

Figure 23: JSMR's potential projects (based on company estimates)

SOURCES: CIMB, COMPANY REPORTS

Resilient traffic growth

Historical data shows that car sales volume in Indonesia is sensitive to fuel price hikes (Figure 24). However, we observe that JSMR’s traffic growth in 1996-2016 was resilient compared to the fluctuations in car sales volume in Indonesia (Figure 25).

Figure 24: Car sales volume is sensitive to fuel price hikes Figure 25: Historically, JSMR's traffic volume was resilient

compared to fluctuations in car sales volumes

SOURCES: CIMB, THE ASSOCIATION OF INDONESIA AUTOMOTIVE INDUSTRIES

(GAIKINDO), CEIC SOURCES: CIMB, GAIKINDO, COMPANY REPORTS

COST ANALYSIS

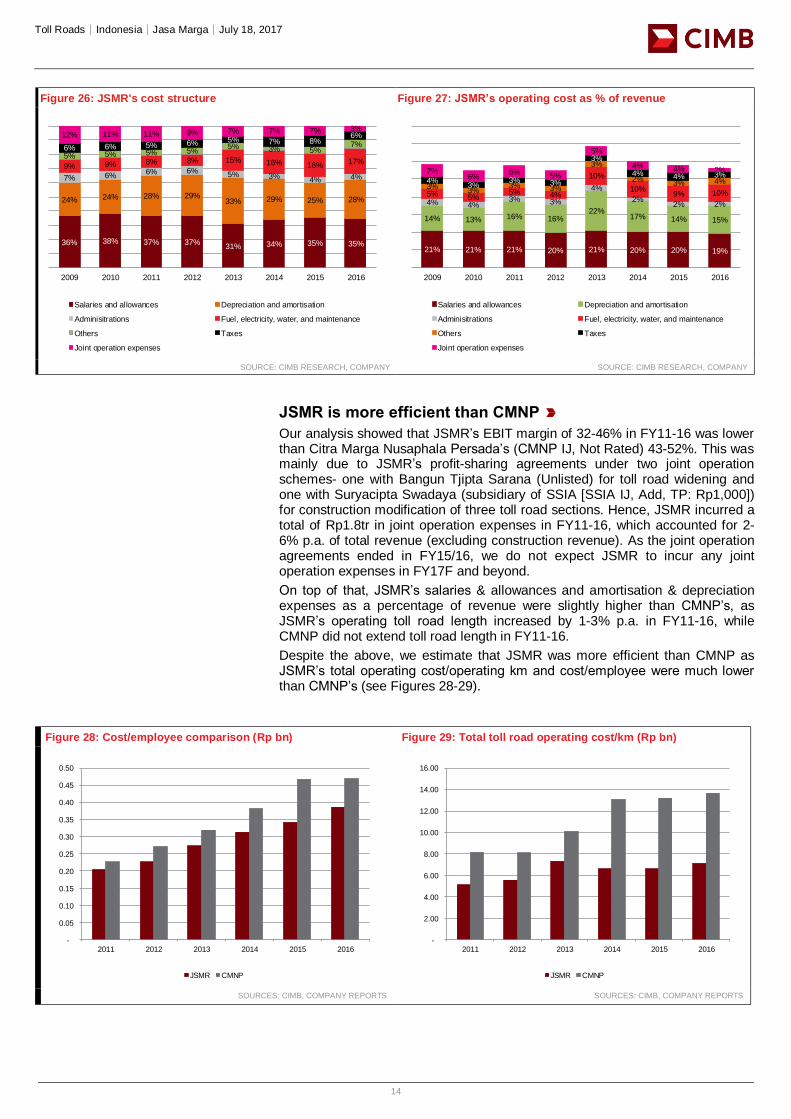

JSMR’s cost structure

In FY09-16, the largest components of JSMR’s operating cost (cost of revenue and G&A expenses) were salaries and allowances (31-38% of total operating cost), and depreciation & amortisation expenses (24%-33% of total operating cost).

Length (km) Estimated investment value (Rp tr)

Probolinggo-Banyuwangi 172.00 20.70

Semarang-Demak 25.00 7.71

Jakarta-Cikampek (South) 64.00 13.38

Akses Patimban 49.00 5.70

North Bandung 27.20 6.31

Demak-Tuban-Gresik 236.00 63.60

Tebing Tinggi-Parapat-Kuala Tanjung 143.30 13.45

Cileunyi-Tasikmalaya-Cilacap 183.00 58.00

Cawang-Bandara (Elevated) 45.00 21.30

Kertosono-Kediri-Tulungagung 63.40 11.70

Padalarang-Sukabumi 60.60 9.82

Surabaya Eastern Ring Road (SERR) 23.00 9.32

Gedebage-Majalaya 11.80 1.92

Semanan-Balaraja 31.00 6.28

Total 1,134.30 249.19

Title:

Source:

Please fill in the values above to have them entered in your report

0

200

400

600

800

1000

1200

1400

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

Diesel price(Rp/litre), LHS Car sales ('000 vehicles), RHS

Title:

Source:

Please fill in the values above to have them entered in your report

0

200

400

600

800

1000

1200

1400

0

200

400

600

800

1,000

1,200

1,400

Car sales ('000 vehicles), LHS JSMR's toll-roads traffics (m vehicles), RHS

Toll Roads│Indonesia│Jasa Marga│July 18, 2017

14

Figure 26: JSMR's cost structure Figure 27: JSMR’s operating cost as % of revenue

SOURCE: CIMB RESEARCH, COMPANY SOURCE: CIMB RESEARCH, COMPANY

JSMR is more efficient than CMNP

Our analysis showed that JSMR’s EBIT margin of 32-46% in FY11-16 was lower than Citra Marga Nusaphala Persada’s (CMNP IJ, Not Rated) 43-52%. This was mainly due to JSMR’s profit-sharing agreements under two joint operation schemes- one with Bangun Tjipta Sarana (Unlisted) for toll road widening and one with Suryacipta Swadaya (subsidiary of SSIA [SSIA IJ, Add, TP: Rp1,000]) for construction modification of three toll road sections. Hence, JSMR incurred a total of Rp1.8tr in joint operation expenses in FY11-16, which accounted for 2-6% p.a. of total revenue (excluding construction revenue). As the joint operation agreements ended in FY15/16, we do not expect JSMR to incur any joint operation expenses in FY17F and beyond.

On top of that, JSMR’s salaries & allowances and amortisation & depreciation expenses as a percentage of revenue were slightly higher than CMNP’s, as JSMR’s operating toll road length increased by 1-3% p.a. in FY11-16, while CMNP did not extend toll road length in FY11-16.

Despite the above, we estimate that JSMR was more efficient than CMNP as JSMR’s total operating cost/operating km and cost/employee were much lower than CMNP’s (see Figures 28-29).

Figure 28: Cost/employee comparison (Rp bn) Figure 29: Total toll road operating cost/km (Rp bn)

SOURCES: CIMB, COMPANY REPORTS SOURCES: CIMB, COMPANY REPORTS

Title:

Source:

Please fill in the values above to have them entered in your report

36% 38% 37% 37%31% 34% 35% 35%

24% 24% 28% 29%33% 29% 25% 28%

7% 6%6% 6% 5% 3% 4% 4%

9% 9% 8% 8% 15% 16% 16%17%

5% 5% 5% 5%5% 3% 5%

7%6% 6% 5% 6% 5% 7% 8%6%12% 11% 11% 9% 7% 7% 7% 3%

2009 2010 2011 2012 2013 2014 2015 2016

Salaries and allowances Depreciation and amortisation

Adminisitrations Fuel, electricity, water, and maintenance

Others Taxes

Joint operation expenses

Title:

Source:

Please fill in the values above to have them entered in your report

21% 21% 21% 20% 21% 20% 20% 19%

14% 13% 16% 16%22%

17% 14% 15%

4% 4%3% 3%

4%

2%2% 2%

5% 5%5% 4%

10%

10%9% 10%

3%3%

3% 3%

3%

2%3% 4%4%

3%3% 3%

3%

4% 4% 3%7%6%

6% 5%

5%

4% 4% 2%

2009 2010 2011 2012 2013 2014 2015 2016

Salaries and allowances Depreciation and amortisation

Adminisitrations Fuel, electricity, water, and maintenance

Others Taxes

Joint operation expenses

Title:

Source:

Please fill in the values above to have them entered in your report

-

0.05

0.10

0.15

0.20

0.25

0.30

0.35

0.40

0.45

0.50

2011 2012 2013 2014 2015 2016

JSMR CMNP

Title:

Source:

Please fill in the values above to have them entered in your report

-

2.00

4.00

6.00

8.00

10.00

12.00

14.00

16.00

2011 2012 2013 2014 2015 2016

JSMR CMNP

Toll Roads│Indonesia│Jasa Marga│July 18, 2017

15

MOVING TO MULTI-LANE FREE FLOW SYSTEM

To be realised by FY18F

The government aims to change Indonesia’s toll road system to a multi-lane free flow (MLFF) system. The rationale behind the change is to improve users’ experience by reducing congestion at toll gates and automating the payment process.

For toll road operators, we believe the change in system offers upside from higher tariffs as a result of integrated systems (if the MLFF tariff remains below the integrated tariff), greater cost efficiency from lower salaries and allowances, increased traffic volumes, as well as reduction in fraud and error risks that plague the conventional toll road payment system.

The government plans for the change to happen in four phases:

1. Full implementation of electronic toll (e-toll) payment system:

The government target is for all toll road gates in Indonesia to accept non-cash payments or e-payments by Oct 2017F. As of Mar 2017, of the 35 operating toll roads in Indonesia, only 23-25% of them offered the e-toll payment system function. By FY18F, the government plans to fully implement the e-toll system at all operating toll roads in Indonesia. Once the e-toll system is fully operational, no cash payments will be accepted.

2. Integration of all toll road concessions:

Under the integrated toll road system, the government expects all toll road users to tap the e-toll card on card readers at toll booths when entering and exiting toll roads.

3. Formation of the electronic toll collection (ETC) consortium:

The ETC consortium will include toll road operators, banks and switching companies under the supervision of Bank Indonesia. ETC will integrate transaction data and tariffs for all toll road concessions. We expect the ETC consortium to start operating by Dec 2017.

4. Implementation of multi-lane free flow (MLFF)

Government targets to fully implement the MLFF system by FY18F.

Case studies on integrated toll road system

Jakarta-Merak toll road integrated system and tariff

The integration of Jakarta-Tangerang toll road (26km) and Tangerang-Merak toll road (72.5km) was completed in Apr 2017. Pre-integration, the Jakarta-Tangerang toll road tariffs were Rp2,500-Rp13,000 (class I-V) and Tangerang-Merak toll road tariffs were Rp3,000-Rp108,000 (class I-V). Post-integration, the Jakarta-Merak toll road tariffs decrease to Rp7,000-Rp20,000 (class I-V).

Early years of Cikampek-Palimanan toll road operations

We observed that the Cikampek-Palimanan (Cipali) toll road struggled to attract traffic during its first two years of operations. The major impediment was the expensive tariff, which discouraged truck traffic (more price sensitive) in particular. Cipali’s toll road tariffs (for longest distance of 116km) range from Rp126,000 for class II vehicles to Rp251,500 for class V vehicles.

Surya Semesta Internusa (SSIA IJ, Add, TP: Rp1,000), the previous owner of the Cipali toll road concession estimated to achieve cash flow breakeven, the traffic level would have to be 28,000 cars/day, comprising 55% class II-V vehicles and 45% class I vehicles. However, as of Jul 2016 (after one year of operations), Cipali’s daily traffic volume was only 24,150 vehicles/day on average, with 17% class II- V vehicles and 83% class I vehicles.

Truck drivers seem to prefer to use the non-toll road route from Jakarta to Cirebon, despite the longer travel time of 5-6 hours (vs. 2.5-3.0 hours using Cipali toll road). We calculated that by avoiding the Cipali toll road, a truck driver’s income would increase by 60% per trip. This is because most truck drivers in Indonesia are given lump-sum payments that include the gas cost, truck rental cost and driver fees.

Toll Roads│Indonesia│Jasa Marga│July 18, 2017

16

Conclusions

Based on the two cases above, we think the integrated Jakarta-Merak toll road (longest distance tariff lower than Cipali’s) would attract higher volumes of class II-V vehicle traffic (higher tariffs than class I vehicles) in the future. The Jakarta-Merak toll road connects Jakarta to Merak port, which is a key transportation link between Java and Sumatera. It is the major provider of heavy vehicles and commercial ferry traffic from Merak to Bakauheni.

We believe the greater proportion of heavy vehicles as a percentage of total traffic volumes would offset Jakarta-Merak toll road’s lower post-integration tariff for longest possible distance of 98km. Additionally, the Jakarta-Merak toll road would enjoy higher post-integration tariff for the closest distance of 3km, which would help to offset the lower tariff for the longest possible distance.

Impact of multi-lane free flow (MLFF) on JSMR

We believe JSMR will benefit from the implementation of the MLFF system as:

1. The full implementation of the e-toll card payment system would reduce JSMR’s biggest operating cost component – salaries & allowances that formed 19-21% of annual revenue (excluding construction revenue) and 31-38% of total operating cost in FY09-16. We observed that Malaysian toll road companies incur much lower salaries & allowances-to-revenue ratio of 6% in 2013-2016, as the country implemented the electronic toll collection system in 2004. Using Malaysia’s experience as a benchmark, we estimate that JSMR’s operating costs would decline significantly with the implementation of the MLFF system.

2. JSMR has 13 old toll road concessions, which have lower tariff/km rate than the new operating toll road average. Hence, we believe there could be tariff upside for its old toll road concessions if they are integrated with the new toll roads. Furthermore, we think the integrated toll road system would attract more class II-V vehicle traffic that offer higher tariff/km rates. In FY16, JSMR’s traffic volume mainly consisted of class I vehicles (88.8%).

3. As the leading toll road operator in Indonesia, JSMR’s third-party toll road operating services revenue could increase if it successfully becomes the main operator of the MLFF toll roads, in our view.

Toll Roads│Indonesia│Jasa Marga│July 18, 2017

17

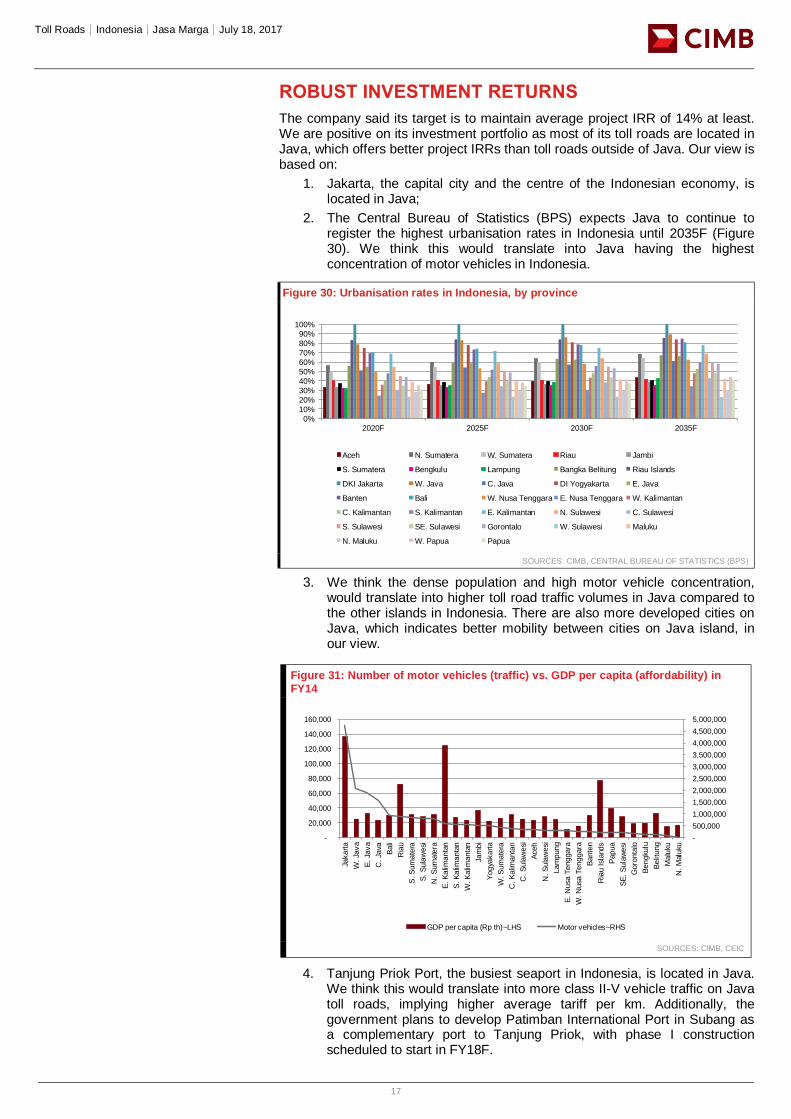

ROBUST INVESTMENT RETURNS

The company said its target is to maintain average project IRR of 14% at least. We are positive on its investment portfolio as most of its toll roads are located in Java, which offers better project IRRs than toll roads outside of Java. Our view is based on:

1. Jakarta, the capital city and the centre of the Indonesian economy, is located in Java;

2. The Central Bureau of Statistics (BPS) expects Java to continue to register the highest urbanisation rates in Indonesia until 2035F (Figure 30). We think this would translate into Java having the highest concentration of motor vehicles in Indonesia.

Figure 30: Urbanisation rates in Indonesia, by province

SOURCES: CIMB, CENTRAL BUREAU OF STATISTICS (BPS)

3. We think the dense population and high motor vehicle concentration, would translate into higher toll road traffic volumes in Java compared to the other islands in Indonesia. There are also more developed cities on Java, which indicates better mobility between cities on Java island, in our view.

Figure 31: Number of motor vehicles (traffic) vs. GDP per capita (affordability) in

FY14

SOURCES: CIMB, CEIC

4. Tanjung Priok Port, the busiest seaport in Indonesia, is located in Java. We think this would translate into more class II-V vehicle traffic on Java toll roads, implying higher average tariff per km. Additionally, the government plans to develop Patimban International Port in Subang as a complementary port to Tanjung Priok, with phase I construction scheduled to start in FY18F.

Title:

Source:

Please fill in the values above to have them entered in your report

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2020F 2025F 2030F 2035F

Aceh N. Sumatera W. Sumatera Riau Jambi

S. Sumatera Bengkulu Lampung Bangka Belitung Riau Islands

DKI Jakarta W. Java C. Java DI Yogyakarta E. Java

Banten Bali W. Nusa Tenggara E. Nusa Tenggara W. Kalimantan

C. Kalimantan S. Kalimantan E. Kalimantan N. Sulawesi C. Sulawesi

S. Sulawesi SE. Sulawesi Gorontalo W. Sulawesi Maluku

N. Maluku W. Papua Papua

Title:

Source:

Please fill in the values above to have them entered in your report

-

500,000

1,000,000

1,500,000

2,000,000

2,500,000

3,000,000

3,500,000

4,000,000

4,500,000

5,000,000

-

20,000

40,000

60,000

80,000

100,000

120,000

140,000

160,000

Jakarta

W. Ja

va

E. Ja

va

C. Ja

va

Bali

Ria

u

S. S

um

ate

ra

S. S

ula

wesi

N. S

um

ate

ra

E. K

alim

anta

n

S. K

alim

anta

n

W. K

alim

anta

n

Jam

bi

Yogya

karta

W. S

um

ate

ra

C. K

alim

anta

n

C. S

ula

wesi

Ace

h

N. S

ula

wesi

Lam

pung

E. N

usa

Tenggara

W. N

usa

Tenggara

Bante

n

Ria

u Isl

and

s

Papua

SE

. S

ula

wesi

Goro

nta

lo

Bengku

lu

Belit

ung

Malu

ku

N. M

aluku

GDP per capita (Rp th)~LHS Motor vehicles~RHS

Toll Roads│Indonesia│Jasa Marga│July 18, 2017

18

Figure 32: Number of trucks, by island (FY15)

SOURCES: CIMB, CEIC

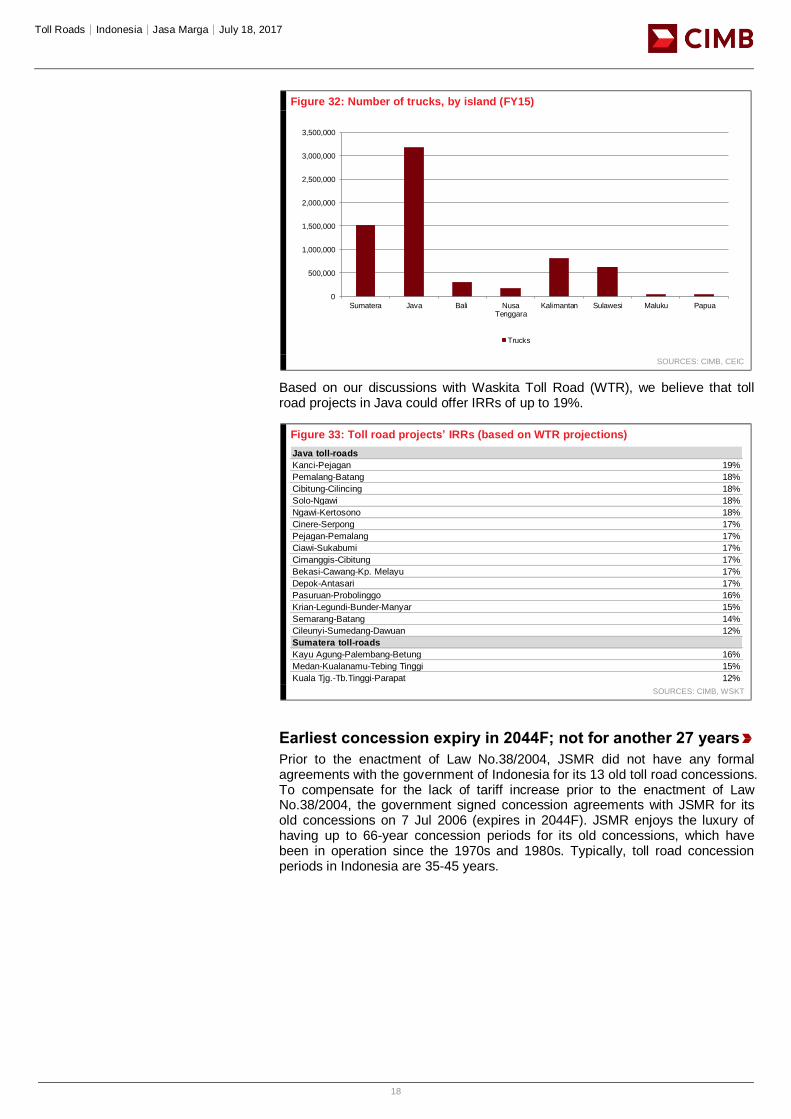

Based on our discussions with Waskita Toll Road (WTR), we believe that toll road projects in Java could offer IRRs of up to 19%.

Figure 33: Toll road projects’ IRRs (based on WTR projections)

SOURCES: CIMB, WSKT

Earliest concession expiry in 2044F; not for another 27 years

Prior to the enactment of Law No.38/2004, JSMR did not have any formal agreements with the government of Indonesia for its 13 old toll road concessions. To compensate for the lack of tariff increase prior to the enactment of Law No.38/2004, the government signed concession agreements with JSMR for its old concessions on 7 Jul 2006 (expires in 2044F). JSMR enjoys the luxury of having up to 66-year concession periods for its old concessions, which have been in operation since the 1970s and 1980s. Typically, toll road concession periods in Indonesia are 35-45 years.

Title:

Source:

Please fill in the values above to have them entered in your report

0

500,000

1,000,000

1,500,000

2,000,000

2,500,000

3,000,000

3,500,000

Sumatera Java Bali NusaTenggara

Kalimantan Sulawesi Maluku Papua

Trucks

Java toll-roads

Kanci-Pejagan 19%

Pemalang-Batang 18%

Cibitung-Cilincing 18%

Solo-Ngawi 18%

Ngawi-Kertosono 18%

Cinere-Serpong 17%

Pejagan-Pemalang 17%

Ciawi-Sukabumi 17%

Cimanggis-Cibitung 17%

Bekasi-Cawang-Kp. Melayu 17%

Depok-Antasari 17%

Pasuruan-Probolinggo 16%

Krian-Legundi-Bunder-Manyar 15%

Semarang-Batang 14%

Cileunyi-Sumedang-Dawuan 12%

Sumatera toll-roads

Kayu Agung-Palembang-Betung 16%

Medan-Kualanamu-Tebing Tinggi 15%

Kuala Tjg.-Tb.Tinggi-Parapat 12%

Toll Roads│Indonesia│Jasa Marga│July 18, 2017

19

Figure 34: JSMR’s toll road concession periods

SOURCES: CIMB, COMPANY REPORTS

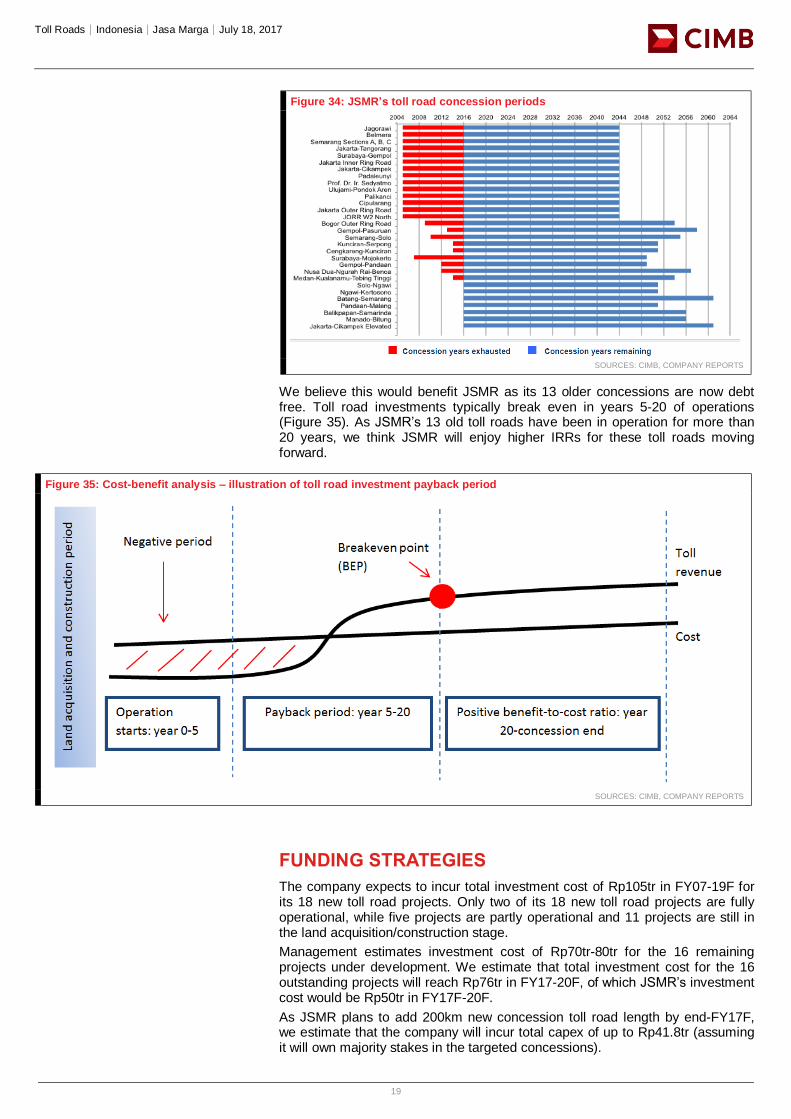

We believe this would benefit JSMR as its 13 older concessions are now debt free. Toll road investments typically break even in years 5-20 of operations (Figure 35). As JSMR’s 13 old toll roads have been in operation for more than 20 years, we think JSMR will enjoy higher IRRs for these toll roads moving forward.

Figure 35: Cost-benefit analysis – illustration of toll road investment payback period

SOURCES: CIMB, COMPANY REPORTS

FUNDING STRATEGIES

The company expects to incur total investment cost of Rp105tr in FY07-19F for its 18 new toll road projects. Only two of its 18 new toll road projects are fully operational, while five projects are partly operational and 11 projects are still in the land acquisition/construction stage.

Management estimates investment cost of Rp70tr-80tr for the 16 remaining projects under development. We estimate that total investment cost for the 16 outstanding projects will reach Rp76tr in FY17-20F, of which JSMR’s investment cost would be Rp50tr in FY17F-20F.

As JSMR plans to add 200km new concession toll road length by end-FY17F, we estimate that the company will incur total capex of up to Rp41.8tr (assuming it will own majority stakes in the targeted concessions).

Toll Roads│Indonesia│Jasa Marga│July 18, 2017

20

Although it has sizeable capex needs, we believe JSMR’s funding strategies would alleviate cash flow pressure and lower its cost of debt. It plans to fund capex via contractor pre-financing (CPF) payment terms, asset recycling, debt recycling and fund raising.

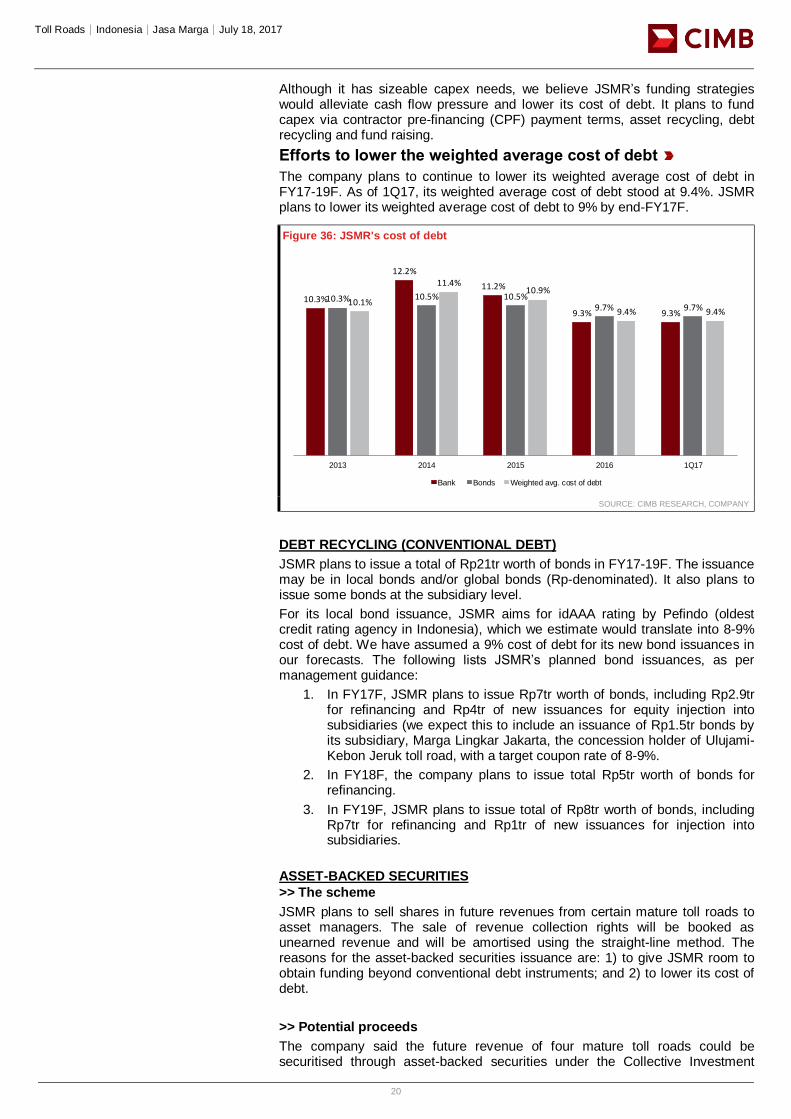

Efforts to lower the weighted average cost of debt

The company plans to continue to lower its weighted average cost of debt in FY17-19F. As of 1Q17, its weighted average cost of debt stood at 9.4%. JSMR plans to lower its weighted average cost of debt to 9% by end-FY17F.

Figure 36: JSMR's cost of debt

SOURCE: CIMB RESEARCH, COMPANY

DEBT RECYCLING (CONVENTIONAL DEBT)

JSMR plans to issue a total of Rp21tr worth of bonds in FY17-19F. The issuance may be in local bonds and/or global bonds (Rp-denominated). It also plans to issue some bonds at the subsidiary level.

For its local bond issuance, JSMR aims for idAAA rating by Pefindo (oldest credit rating agency in Indonesia), which we estimate would translate into 8-9% cost of debt. We have assumed a 9% cost of debt for its new bond issuances in our forecasts. The following lists JSMR’s planned bond issuances, as per management guidance:

1. In FY17F, JSMR plans to issue Rp7tr worth of bonds, including Rp2.9tr for refinancing and Rp4tr of new issuances for equity injection into subsidiaries (we expect this to include an issuance of Rp1.5tr bonds by its subsidiary, Marga Lingkar Jakarta, the concession holder of Ulujami-Kebon Jeruk toll road, with a target coupon rate of 8-9%.

2. In FY18F, the company plans to issue total Rp5tr worth of bonds for refinancing.

3. In FY19F, JSMR plans to issue total of Rp8tr worth of bonds, including Rp7tr for refinancing and Rp1tr of new issuances for injection into subsidiaries.

ASSET-BACKED SECURITIES

>> The scheme

JSMR plans to sell shares in future revenues from certain mature toll roads to asset managers. The sale of revenue collection rights will be booked as unearned revenue and will be amortised using the straight-line method. The reasons for the asset-backed securities issuance are: 1) to give JSMR room to obtain funding beyond conventional debt instruments; and 2) to lower its cost of debt.

>> Potential proceeds

The company said the future revenue of four mature toll roads could be securitised through asset-backed securities under the Collective Investment

Title:

Source:

Please fill in the values above to have them entered in your report10.3%

12.2%

11.2%

9.3% 9.3%

10.3% 10.5% 10.5%9.7% 9.7%

10.1%

11.4%10.9%

9.4% 9.4%

2013 2014 2015 2016 1Q17

Bank Bonds Weighted avg. cost of debt

Toll Roads│Indonesia│Jasa Marga│July 18, 2017

21

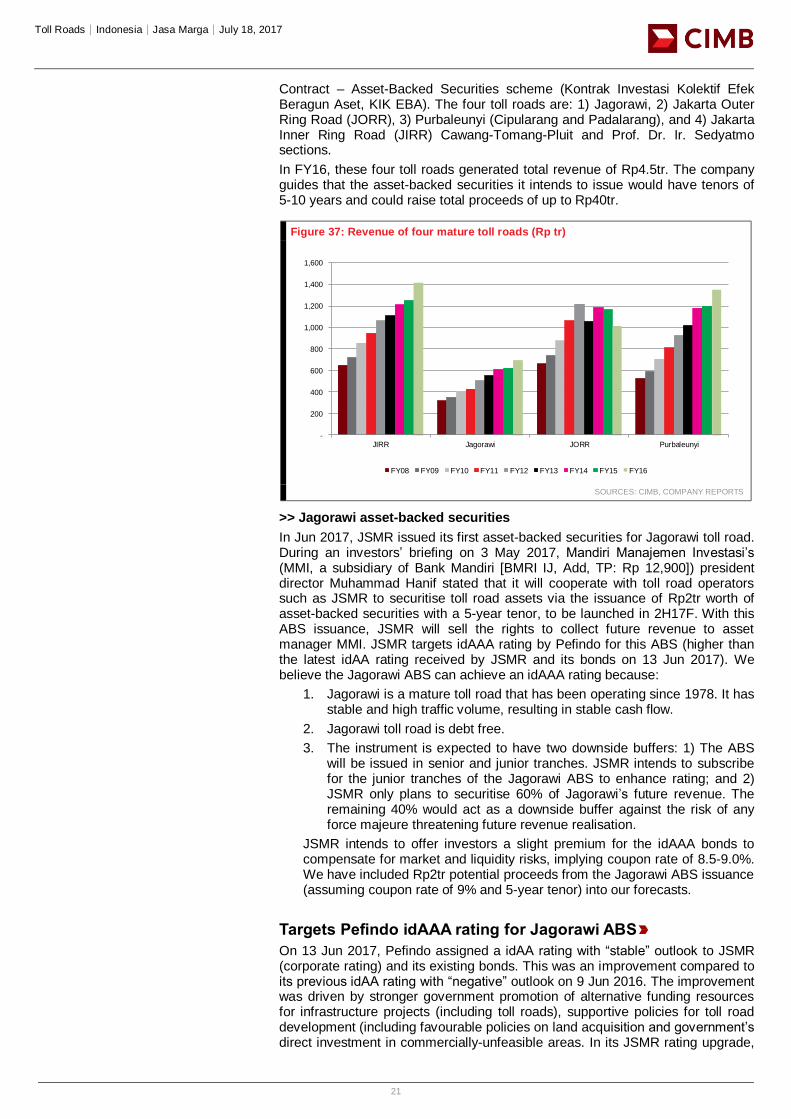

Contract – Asset-Backed Securities scheme (Kontrak Investasi Kolektif Efek Beragun Aset, KIK EBA). The four toll roads are: 1) Jagorawi, 2) Jakarta Outer Ring Road (JORR), 3) Purbaleunyi (Cipularang and Padalarang), and 4) Jakarta Inner Ring Road (JIRR) Cawang-Tomang-Pluit and Prof. Dr. Ir. Sedyatmo sections.

In FY16, these four toll roads generated total revenue of Rp4.5tr. The company guides that the asset-backed securities it intends to issue would have tenors of 5-10 years and could raise total proceeds of up to Rp40tr.

Figure 37: Revenue of four mature toll roads (Rp tr)

SOURCES: CIMB, COMPANY REPORTS

>> Jagorawi asset-backed securities

In Jun 2017, JSMR issued its first asset-backed securities for Jagorawi toll road. During an investors’ briefing on 3 May 2017, Mandiri Manajemen Investasi’s (MMI, a subsidiary of Bank Mandiri [BMRI IJ, Add, TP: Rp 12,900]) president director Muhammad Hanif stated that it will cooperate with toll road operators such as JSMR to securitise toll road assets via the issuance of Rp2tr worth of asset-backed securities with a 5-year tenor, to be launched in 2H17F. With this ABS issuance, JSMR will sell the rights to collect future revenue to asset manager MMI. JSMR targets idAAA rating by Pefindo for this ABS (higher than the latest idAA rating received by JSMR and its bonds on 13 Jun 2017). We believe the Jagorawi ABS can achieve an idAAA rating because:

1. Jagorawi is a mature toll road that has been operating since 1978. It has stable and high traffic volume, resulting in stable cash flow.

2. Jagorawi toll road is debt free.

3. The instrument is expected to have two downside buffers: 1) The ABS will be issued in senior and junior tranches. JSMR intends to subscribe for the junior tranches of the Jagorawi ABS to enhance rating; and 2) JSMR only plans to securitise 60% of Jagorawi’s future revenue. The remaining 40% would act as a downside buffer against the risk of any force majeure threatening future revenue realisation.

JSMR intends to offer investors a slight premium for the idAAA bonds to compensate for market and liquidity risks, implying coupon rate of 8.5-9.0%. We have included Rp2tr potential proceeds from the Jagorawi ABS issuance (assuming coupon rate of 9% and 5-year tenor) into our forecasts.

Targets Pefindo idAAA rating for Jagorawi ABS

On 13 Jun 2017, Pefindo assigned a idAA rating with “stable” outlook to JSMR (corporate rating) and its existing bonds. This was an improvement compared to its previous idAA rating with “negative” outlook on 9 Jun 2016. The improvement was driven by stronger government promotion of alternative funding resources for infrastructure projects (including toll roads), supportive policies for toll road development (including favourable policies on land acquisition and government’s direct investment in commercially-unfeasible areas. In its JSMR rating upgrade,

Title:

Source:

Please fill in the values above to have them entered in your report

-

200

400

600

800

1,000

1,200

1,400

1,600

JIRR Jagorawi JORR Purbaleunyi

FY08 FY09 FY10 FY11 FY12 FY13 FY14 FY15 FY16

Toll Roads│Indonesia│Jasa Marga│July 18, 2017

22

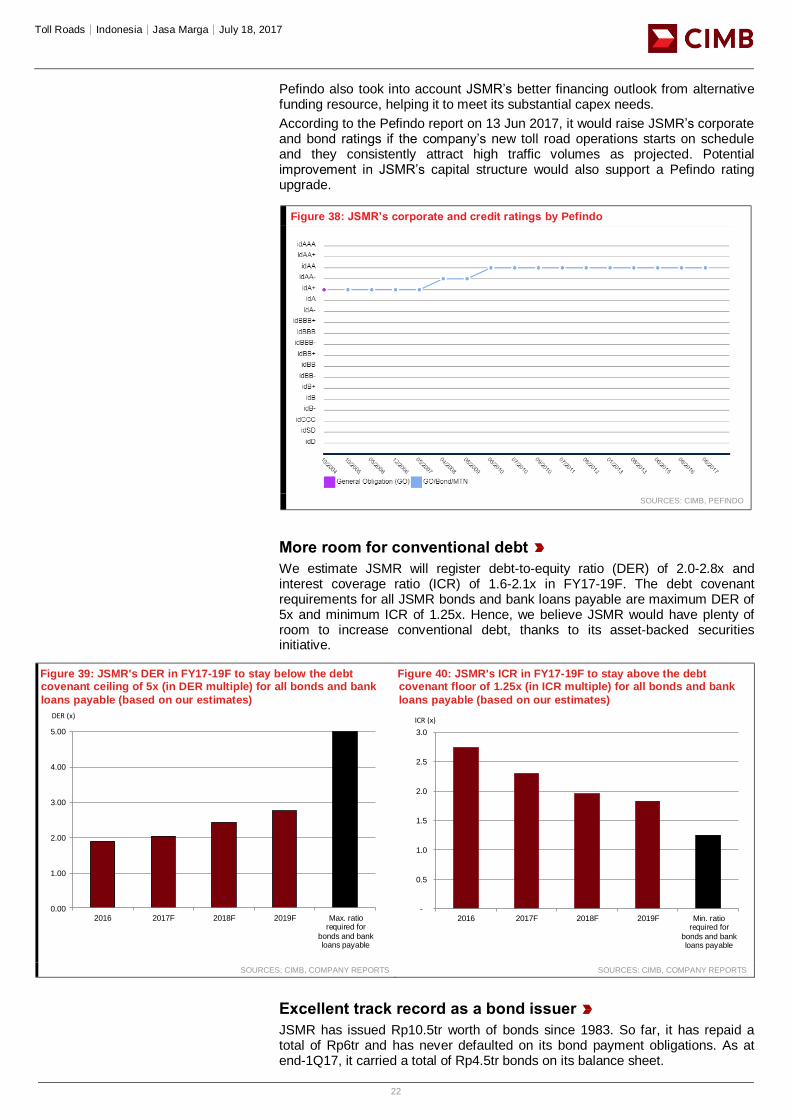

Pefindo also took into account JSMR’s better financing outlook from alternative funding resource, helping it to meet its substantial capex needs.

According to the Pefindo report on 13 Jun 2017, it would raise JSMR’s corporate and bond ratings if the company’s new toll road operations starts on schedule and they consistently attract high traffic volumes as projected. Potential improvement in JSMR’s capital structure would also support a Pefindo rating upgrade.

Figure 38: JSMR’s corporate and credit ratings by Pefindo

SOURCES: CIMB, PEFINDO

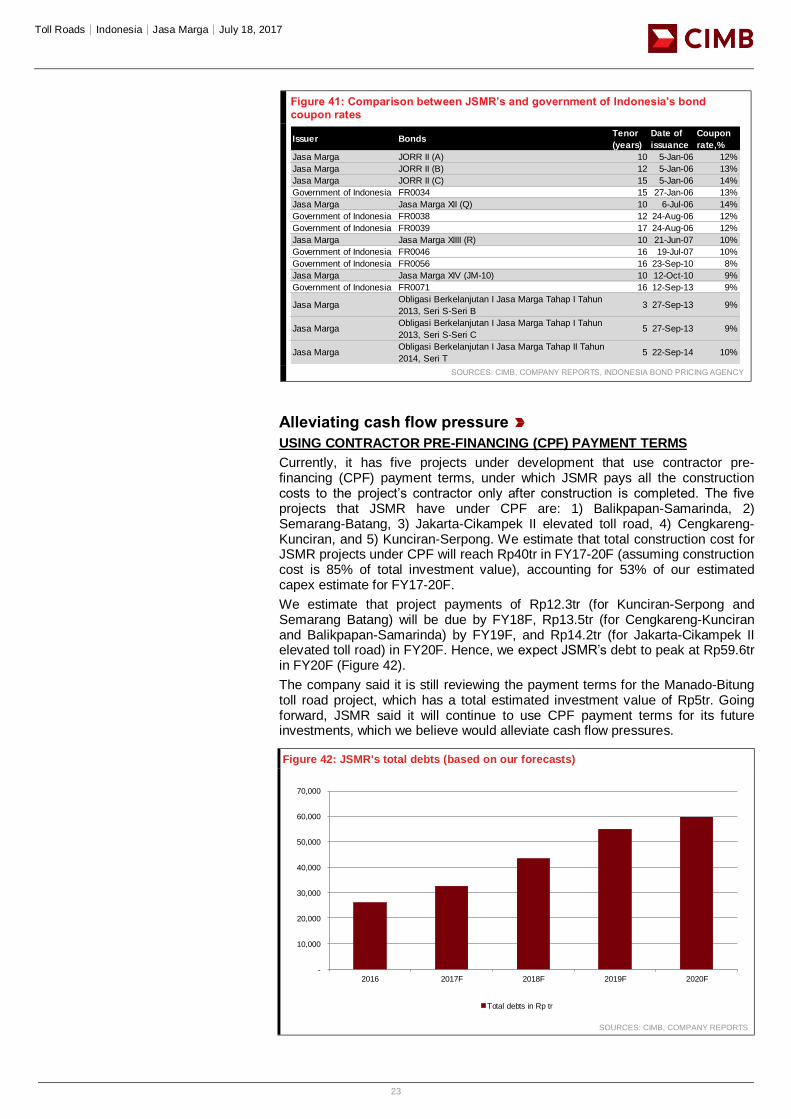

More room for conventional debt

We estimate JSMR will register debt-to-equity ratio (DER) of 2.0-2.8x and interest coverage ratio (ICR) of 1.6-2.1x in FY17-19F. The debt covenant requirements for all JSMR bonds and bank loans payable are maximum DER of 5x and minimum ICR of 1.25x. Hence, we believe JSMR would have plenty of room to increase conventional debt, thanks to its asset-backed securities initiative.

Figure 39: JSMR's DER in FY17-19F to stay below the debt covenant ceiling of 5x (in DER multiple) for all bonds and bank

loans payable (based on our estimates)

Figure 40: JSMR's ICR in FY17-19F to stay above the debt covenant floor of 1.25x (in ICR multiple) for all bonds and bank

loans payable (based on our estimates)

SOURCES: CIMB, COMPANY REPORTS SOURCES: CIMB, COMPANY REPORTS

Excellent track record as a bond issuer

JSMR has issued Rp10.5tr worth of bonds since 1983. So far, it has repaid a total of Rp6tr and has never defaulted on its bond payment obligations. As at end-1Q17, it carried a total of Rp4.5tr bonds on its balance sheet.

Title:

Source:

Please fill in the values above to have them entered in your report

0.00

1.00

2.00

3.00

4.00

5.00

2016 2017F 2018F 2019F Max. ratiorequired for

bonds and bankloans payable

Title:

Source:

Please fill in the values above to have them entered in your report

-

0.5

1.0

1.5

2.0

2.5

3.0

2016 2017F 2018F 2019F Min. ratiorequired for

bonds and bankloans payable

DER (x) ICR (x)

Toll Roads│Indonesia│Jasa Marga│July 18, 2017

23

Figure 41: Comparison between JSMR’s and government of Indonesia's bond coupon rates

SOURCES: CIMB, COMPANY REPORTS, INDONESIA BOND PRICING AGENCY

Alleviating cash flow pressure

USING CONTRACTOR PRE-FINANCING (CPF) PAYMENT TERMS

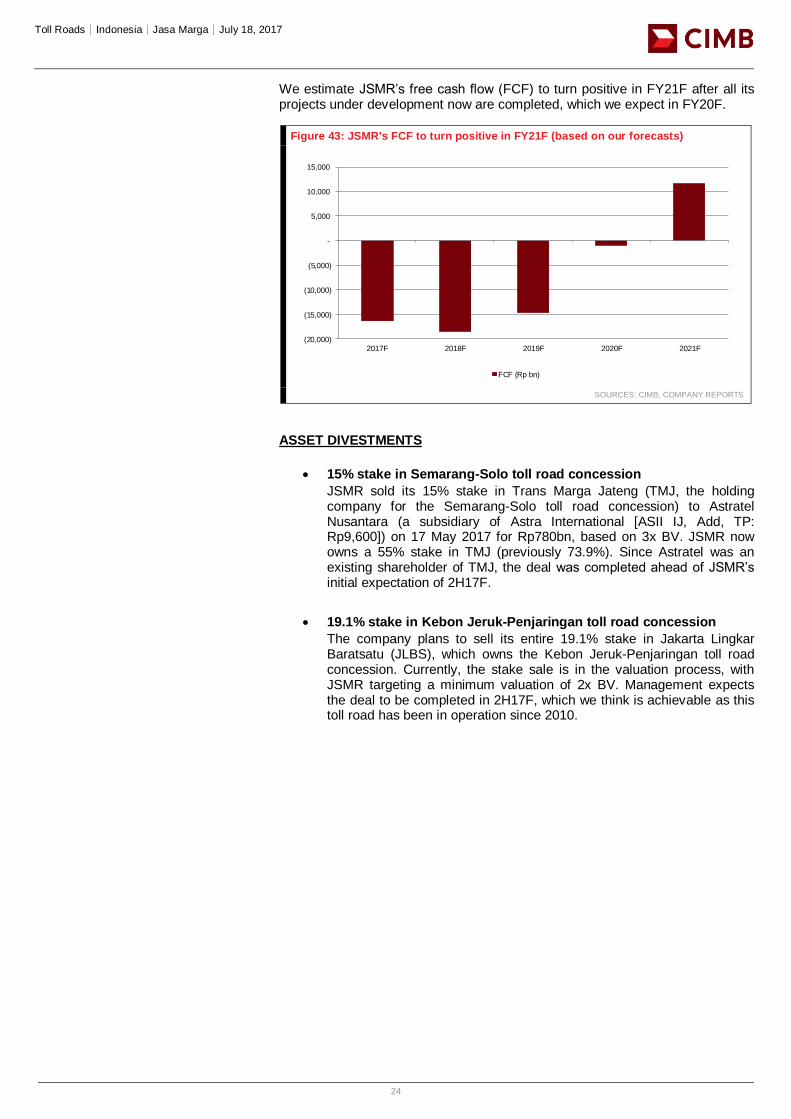

Currently, it has five projects under development that use contractor pre-financing (CPF) payment terms, under which JSMR pays all the construction costs to the project’s contractor only after construction is completed. The five projects that JSMR have under CPF are: 1) Balikpapan-Samarinda, 2) Semarang-Batang, 3) Jakarta-Cikampek II elevated toll road, 4) Cengkareng-Kunciran, and 5) Kunciran-Serpong. We estimate that total construction cost for JSMR projects under CPF will reach Rp40tr in FY17-20F (assuming construction cost is 85% of total investment value), accounting for 53% of our estimated capex estimate for FY17-20F.

We estimate that project payments of Rp12.3tr (for Kunciran-Serpong and Semarang Batang) will be due by FY18F, Rp13.5tr (for Cengkareng-Kunciran and Balikpapan-Samarinda) by FY19F, and Rp14.2tr (for Jakarta-Cikampek II elevated toll road) in FY20F. Hence, we expect JSMR’s debt to peak at Rp59.6tr in FY20F (Figure 42).

The company said it is still reviewing the payment terms for the Manado-Bitung toll road project, which has a total estimated investment value of Rp5tr. Going forward, JSMR said it will continue to use CPF payment terms for its future investments, which we believe would alleviate cash flow pressures.

Figure 42: JSMR's total debts (based on our forecasts)

SOURCES: CIMB, COMPANY REPORTS

Issuer BondsTenor

(years)

Date of

issuance

Coupon

rate,%

Jasa Marga JORR II (A) 10 5-Jan-06 12%

Jasa Marga JORR II (B) 12 5-Jan-06 13%

Jasa Marga JORR II (C) 15 5-Jan-06 14%

Government of Indonesia FR0034 15 27-Jan-06 13%

Jasa Marga Jasa Marga XII (Q) 10 6-Jul-06 14%

Government of Indonesia FR0038 12 24-Aug-06 12%

Government of Indonesia FR0039 17 24-Aug-06 12%

Jasa Marga Jasa Marga XIIII (R) 10 21-Jun-07 10%

Government of Indonesia FR0046 16 19-Jul-07 10%

Government of Indonesia FR0056 16 23-Sep-10 8%

Jasa Marga Jasa Marga XIV (JM-10) 10 12-Oct-10 9%

Government of Indonesia FR0071 16 12-Sep-13 9%

Jasa MargaObligasi Berkelanjutan I Jasa Marga Tahap I Tahun

2013, Seri S-Seri B3 27-Sep-13 9%

Jasa MargaObligasi Berkelanjutan I Jasa Marga Tahap I Tahun

2013, Seri S-Seri C5 27-Sep-13 9%

Jasa MargaObligasi Berkelanjutan I Jasa Marga Tahap II Tahun

2014, Seri T5 22-Sep-14 10%

Title:

Source:

Please fill in the values above to have them entered in your report

-

10,000

20,000

30,000

40,000

50,000

60,000

70,000

2016 2017F 2018F 2019F 2020F

Total debts in Rp tr

Toll Roads│Indonesia│Jasa Marga│July 18, 2017

24

We estimate JSMR’s free cash flow (FCF) to turn positive in FY21F after all its projects under development now are completed, which we expect in FY20F.

Figure 43: JSMR's FCF to turn positive in FY21F (based on our forecasts)

SOURCES: CIMB, COMPANY REPORTS

ASSET DIVESTMENTS

15% stake in Semarang-Solo toll road concession

JSMR sold its 15% stake in Trans Marga Jateng (TMJ, the holding company for the Semarang-Solo toll road concession) to Astratel Nusantara (a subsidiary of Astra International [ASII IJ, Add, TP: Rp9,600]) on 17 May 2017 for Rp780bn, based on 3x BV. JSMR now owns a 55% stake in TMJ (previously 73.9%). Since Astratel was an existing shareholder of TMJ, the deal was completed ahead of JSMR’s initial expectation of 2H17F.

19.1% stake in Kebon Jeruk-Penjaringan toll road concession

The company plans to sell its entire 19.1% stake in Jakarta Lingkar Baratsatu (JLBS), which owns the Kebon Jeruk-Penjaringan toll road concession. Currently, the stake sale is in the valuation process, with JSMR targeting a minimum valuation of 2x BV. Management expects the deal to be completed in 2H17F, which we think is achievable as this toll road has been in operation since 2010.

Title:

Source:

Please fill in the values above to have them entered in your report

(20,000)

(15,000)

(10,000)

(5,000)

-

5,000

10,000

15,000

2017F 2018F 2019F 2020F 2021F

FCF (Rp bn)

Toll Roads│Indonesia│Jasa Marga│July 18, 2017

25

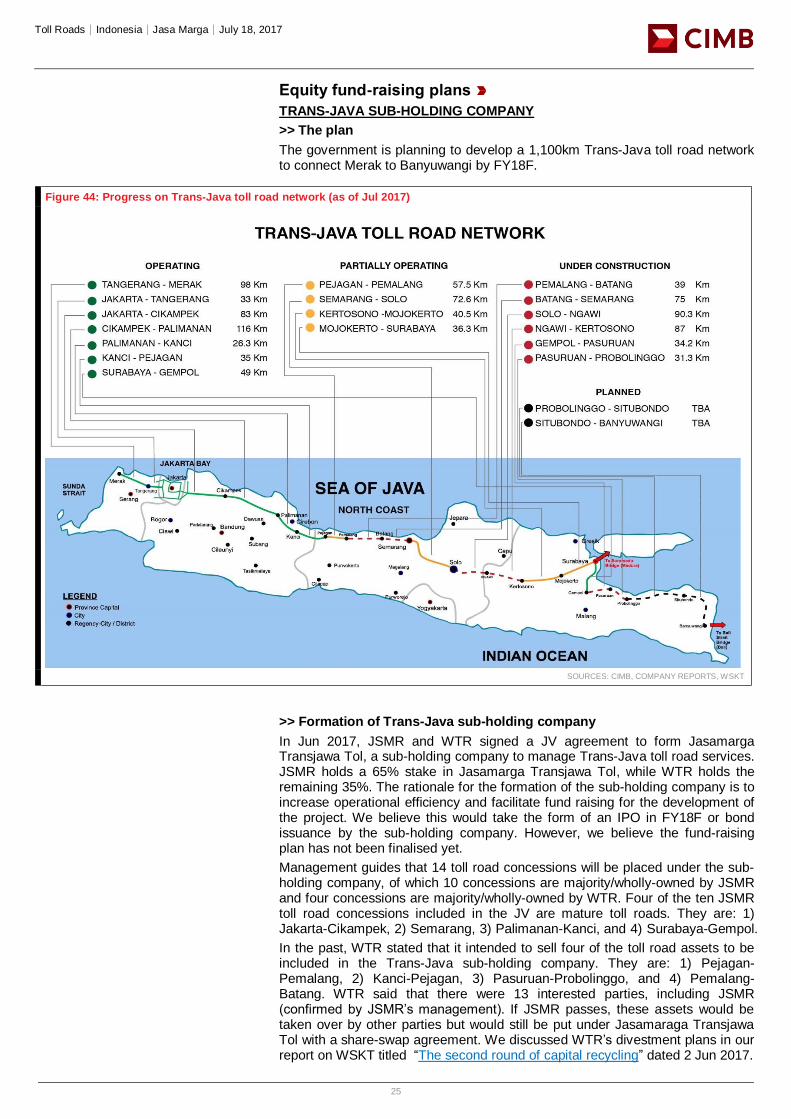

Equity fund-raising plans

TRANS-JAVA SUB-HOLDING COMPANY

>> The plan

The government is planning to develop a 1,100km Trans-Java toll road network to connect Merak to Banyuwangi by FY18F.

Figure 44: Progress on Trans-Java toll road network (as of Jul 2017)

SOURCES: CIMB, COMPANY REPORTS, WSKT

>> Formation of Trans-Java sub-holding company

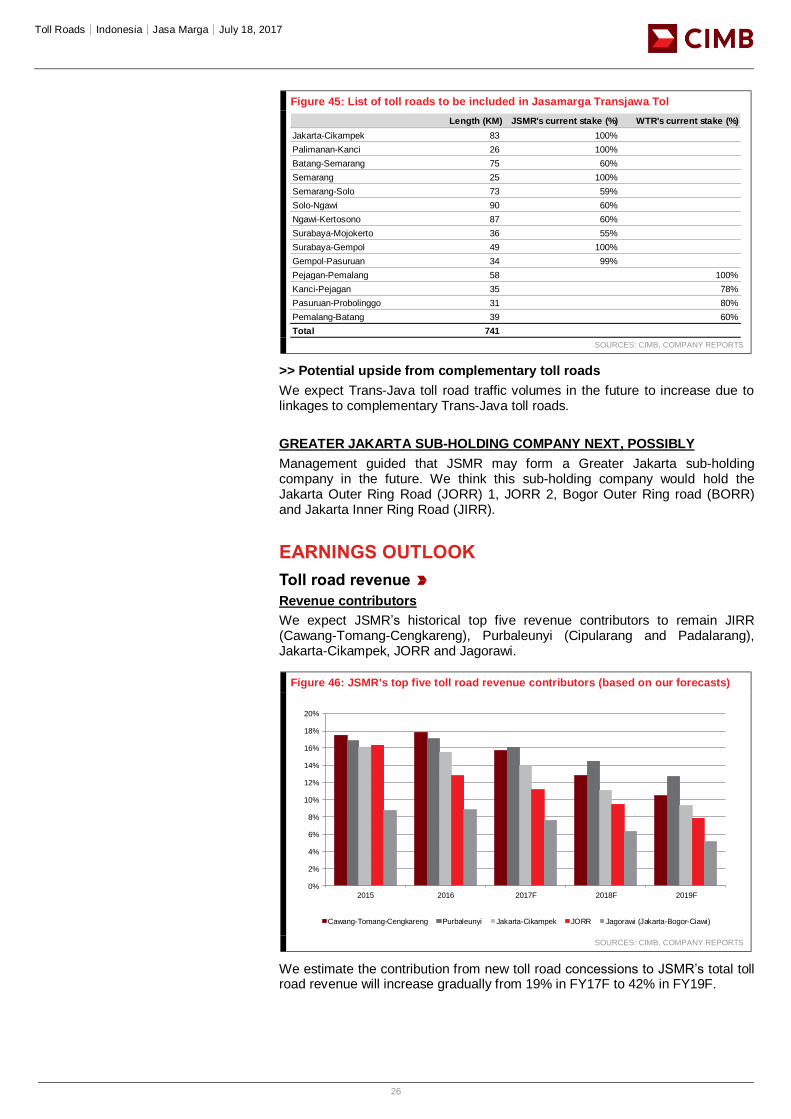

In Jun 2017, JSMR and WTR signed a JV agreement to form Jasamarga Transjawa Tol, a sub-holding company to manage Trans-Java toll road services. JSMR holds a 65% stake in Jasamarga Transjawa Tol, while WTR holds the remaining 35%. The rationale for the formation of the sub-holding company is to increase operational efficiency and facilitate fund raising for the development of the project. We believe this would take the form of an IPO in FY18F or bond issuance by the sub-holding company. However, we believe the fund-raising plan has not been finalised yet.

Management guides that 14 toll road concessions will be placed under the sub-holding company, of which 10 concessions are majority/wholly-owned by JSMR and four concessions are majority/wholly-owned by WTR. Four of the ten JSMR toll road concessions included in the JV are mature toll roads. They are: 1) Jakarta-Cikampek, 2) Semarang, 3) Palimanan-Kanci, and 4) Surabaya-Gempol.

In the past, WTR stated that it intended to sell four of the toll road assets to be included in the Trans-Java sub-holding company. They are: 1) Pejagan-Pemalang, 2) Kanci-Pejagan, 3) Pasuruan-Probolinggo, and 4) Pemalang-Batang. WTR said that there were 13 interested parties, including JSMR (confirmed by JSMR’s management). If JSMR passes, these assets would be taken over by other parties but would still be put under Jasamaraga Transjawa Tol with a share-swap agreement. We discussed WTR’s divestment plans in our report on WSKT titled “The second round of capital recycling” dated 2 Jun 2017.

Toll Roads│Indonesia│Jasa Marga│July 18, 2017

26

Figure 45: List of toll roads to be included in Jasamarga Transjawa Tol

SOURCES: CIMB, COMPANY REPORTS

>> Potential upside from complementary toll roads

We expect Trans-Java toll road traffic volumes in the future to increase due to linkages to complementary Trans-Java toll roads.

GREATER JAKARTA SUB-HOLDING COMPANY NEXT, POSSIBLY

Management guided that JSMR may form a Greater Jakarta sub-holding company in the future. We think this sub-holding company would hold the Jakarta Outer Ring Road (JORR) 1, JORR 2, Bogor Outer Ring road (BORR) and Jakarta Inner Ring Road (JIRR).

EARNINGS OUTLOOK

Toll road revenue

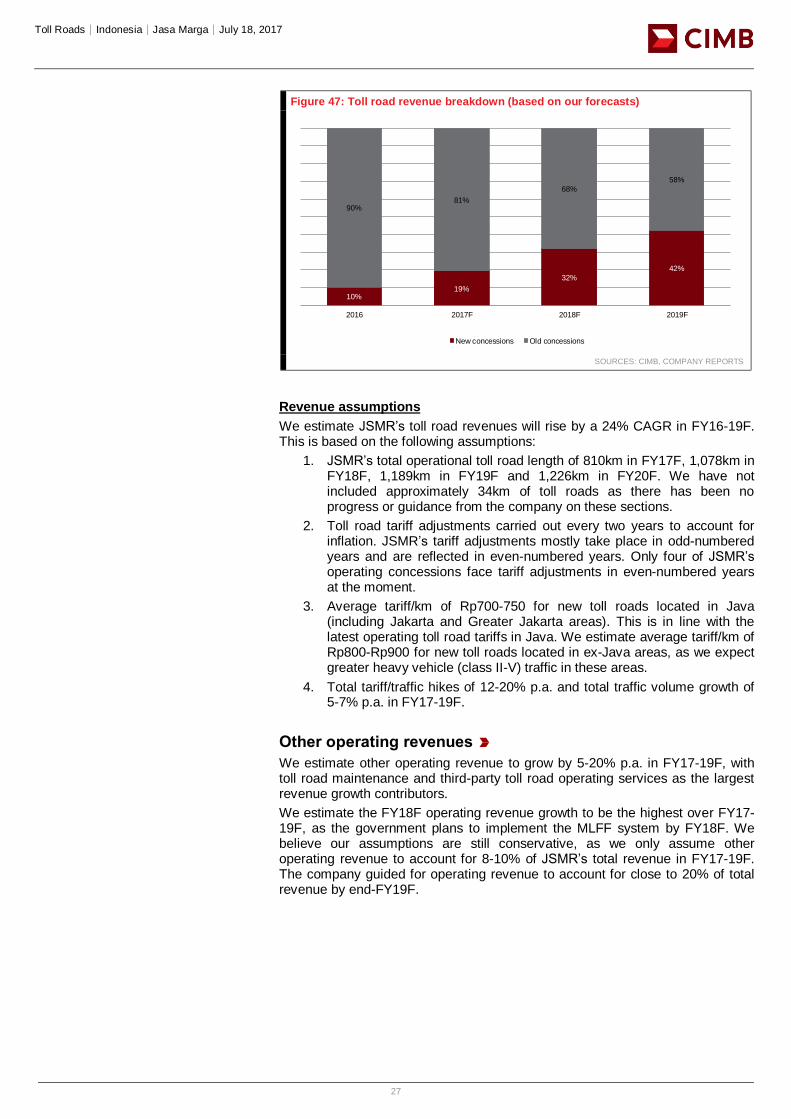

Revenue contributors

We expect JSMR’s historical top five revenue contributors to remain JIRR (Cawang-Tomang-Cengkareng), Purbaleunyi (Cipularang and Padalarang), Jakarta-Cikampek, JORR and Jagorawi.

Figure 46: JSMR's top five toll road revenue contributors (based on our forecasts)

SOURCES: CIMB, COMPANY REPORTS

We estimate the contribution from new toll road concessions to JSMR’s total toll road revenue will increase gradually from 19% in FY17F to 42% in FY19F.

Length (KM) JSMR's current stake (%) WTR's current stake (%)

Jakarta-Cikampek 83 100%

Palimanan-Kanci 26 100%

Batang-Semarang 75 60%

Semarang 25 100%

Semarang-Solo 73 59%

Solo-Ngawi 90 60%

Ngawi-Kertosono 87 60%

Surabaya-Mojokerto 36 55%

Surabaya-Gempol 49 100%

Gempol-Pasuruan 34 99%

Pejagan-Pemalang 58 100%

Kanci-Pejagan 35 78%

Pasuruan-Probolinggo 31 80%

Pemalang-Batang 39 60%

Total 741

Title:

Source:

Please fill in the values above to have them entered in your report

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

20%

2015 2016 2017F 2018F 2019F

Cawang-Tomang-Cengkareng Purbaleunyi Jakarta-Cikampek JORR Jagorawi (Jakarta-Bogor-Ciawi)

Toll Roads│Indonesia│Jasa Marga│July 18, 2017

27

Figure 47: Toll road revenue breakdown (based on our forecasts)

SOURCES: CIMB, COMPANY REPORTS

Revenue assumptions

We estimate JSMR’s toll road revenues will rise by a 24% CAGR in FY16-19F. This is based on the following assumptions:

1. JSMR’s total operational toll road length of 810km in FY17F, 1,078km in FY18F, 1,189km in FY19F and 1,226km in FY20F. We have not included approximately 34km of toll roads as there has been no progress or guidance from the company on these sections.

2. Toll road tariff adjustments carried out every two years to account for inflation. JSMR’s tariff adjustments mostly take place in odd-numbered years and are reflected in even-numbered years. Only four of JSMR’s operating concessions face tariff adjustments in even-numbered years at the moment.

3. Average tariff/km of Rp700-750 for new toll roads located in Java (including Jakarta and Greater Jakarta areas). This is in line with the latest operating toll road tariffs in Java. We estimate average tariff/km of Rp800-Rp900 for new toll roads located in ex-Java areas, as we expect greater heavy vehicle (class II-V) traffic in these areas.

4. Total tariff/traffic hikes of 12-20% p.a. and total traffic volume growth of 5-7% p.a. in FY17-19F.

Other operating revenues

We estimate other operating revenue to grow by 5-20% p.a. in FY17-19F, with toll road maintenance and third-party toll road operating services as the largest revenue growth contributors.

We estimate the FY18F operating revenue growth to be the highest over FY17-19F, as the government plans to implement the MLFF system by FY18F. We believe our assumptions are still conservative, as we only assume other operating revenue to account for 8-10% of JSMR’s total revenue in FY17-19F. The company guided for operating revenue to account for close to 20% of total revenue by end-FY19F.

Title:

Source:

Please fill in the values above to have them entered in your report

10%19%

32%

42%

90%81%

68%

58%

2016 2017F 2018F 2019F

New concessions Old concessions

Toll Roads│Indonesia│Jasa Marga│July 18, 2017

28

Figure 48: JSMR's other operating revenue (excluding construction) in FY17-19F (Rp bn), based on our forecasts

SOURCES: CIMB, COMPANY REPORTS

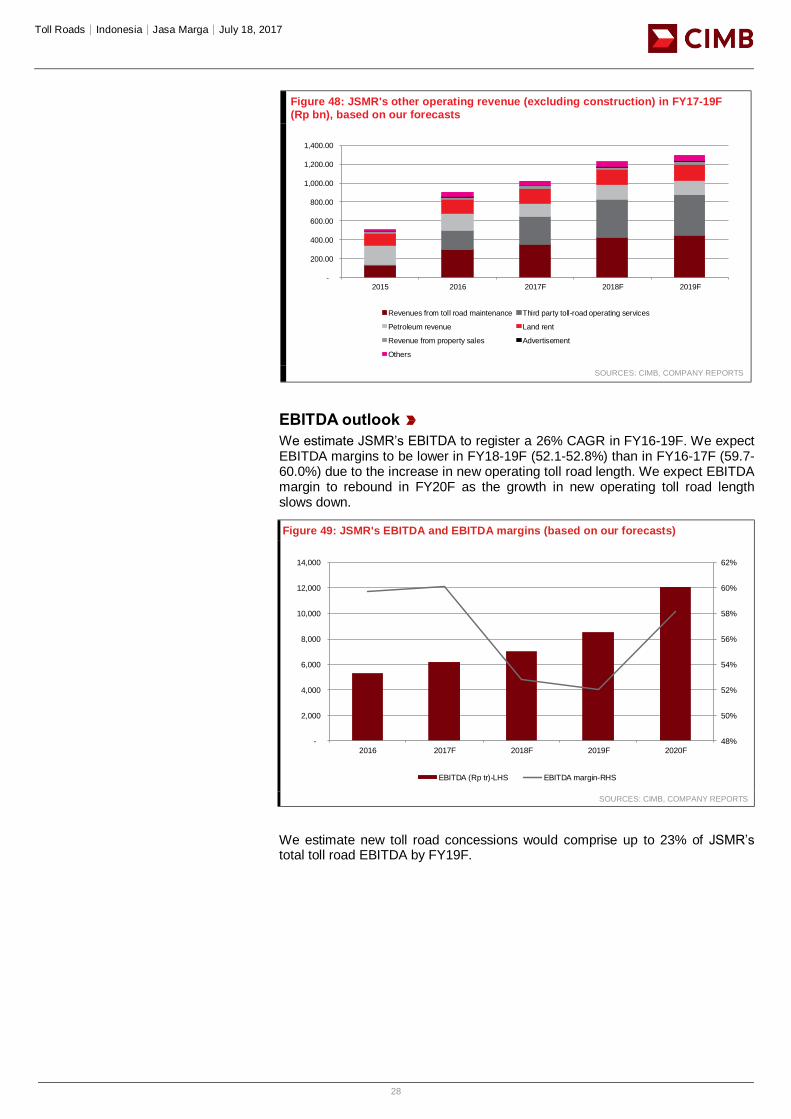

EBITDA outlook

We estimate JSMR’s EBITDA to register a 26% CAGR in FY16-19F. We expect EBITDA margins to be lower in FY18-19F (52.1-52.8%) than in FY16-17F (59.7-60.0%) due to the increase in new operating toll road length. We expect EBITDA margin to rebound in FY20F as the growth in new operating toll road length slows down.

Figure 49: JSMR's EBITDA and EBITDA margins (based on our forecasts)

SOURCES: CIMB, COMPANY REPORTS

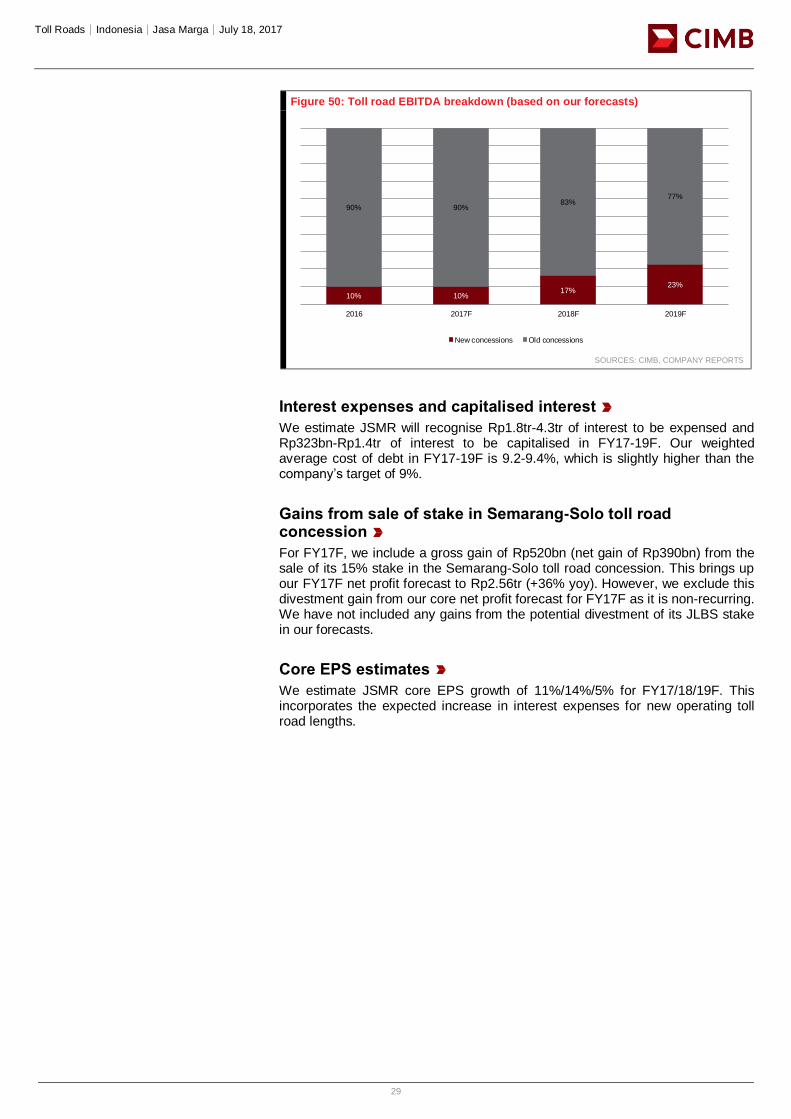

We estimate new toll road concessions would comprise up to 23% of JSMR’s total toll road EBITDA by FY19F.

Title:

Source:

Please fill in the values above to have them entered in your report

-

200.00

400.00

600.00

800.00

1,000.00

1,200.00

1,400.00

2015 2016 2017F 2018F 2019F

Revenues from toll road maintenance Third party toll-road operating services

Petroleum revenue Land rent

Revenue from property sales Advertisement

Others

Title:

Source:

Please fill in the values above to have them entered in your report

48%

50%

52%

54%

56%

58%

60%

62%

-

2,000

4,000

6,000

8,000

10,000

12,000

14,000

2016 2017F 2018F 2019F 2020F

EBITDA (Rp tr)-LHS EBITDA margin-RHS

Toll Roads│Indonesia│Jasa Marga│July 18, 2017

29

Figure 50: Toll road EBITDA breakdown (based on our forecasts)

SOURCES: CIMB, COMPANY REPORTS

Interest expenses and capitalised interest

We estimate JSMR will recognise Rp1.8tr-4.3tr of interest to be expensed and Rp323bn-Rp1.4tr of interest to be capitalised in FY17-19F. Our weighted average cost of debt in FY17-19F is 9.2-9.4%, which is slightly higher than the company’s target of 9%.

Gains from sale of stake in Semarang-Solo toll road concession

For FY17F, we include a gross gain of Rp520bn (net gain of Rp390bn) from the sale of its 15% stake in the Semarang-Solo toll road concession. This brings up our FY17F net profit forecast to Rp2.56tr (+36% yoy). However, we exclude this divestment gain from our core net profit forecast for FY17F as it is non-recurring. We have not included any gains from the potential divestment of its JLBS stake in our forecasts.

Core EPS estimates

We estimate JSMR core EPS growth of 11%/14%/5% for FY17/18/19F. This incorporates the expected increase in interest expenses for new operating toll road lengths.

Title:

Source:

Please fill in the values above to have them entered in your report

10% 10%17%

23%

90% 90%83%

77%

2016 2017F 2018F 2019F

New concessions Old concessions

Toll Roads│Indonesia│Jasa Marga│July 18, 2017

30

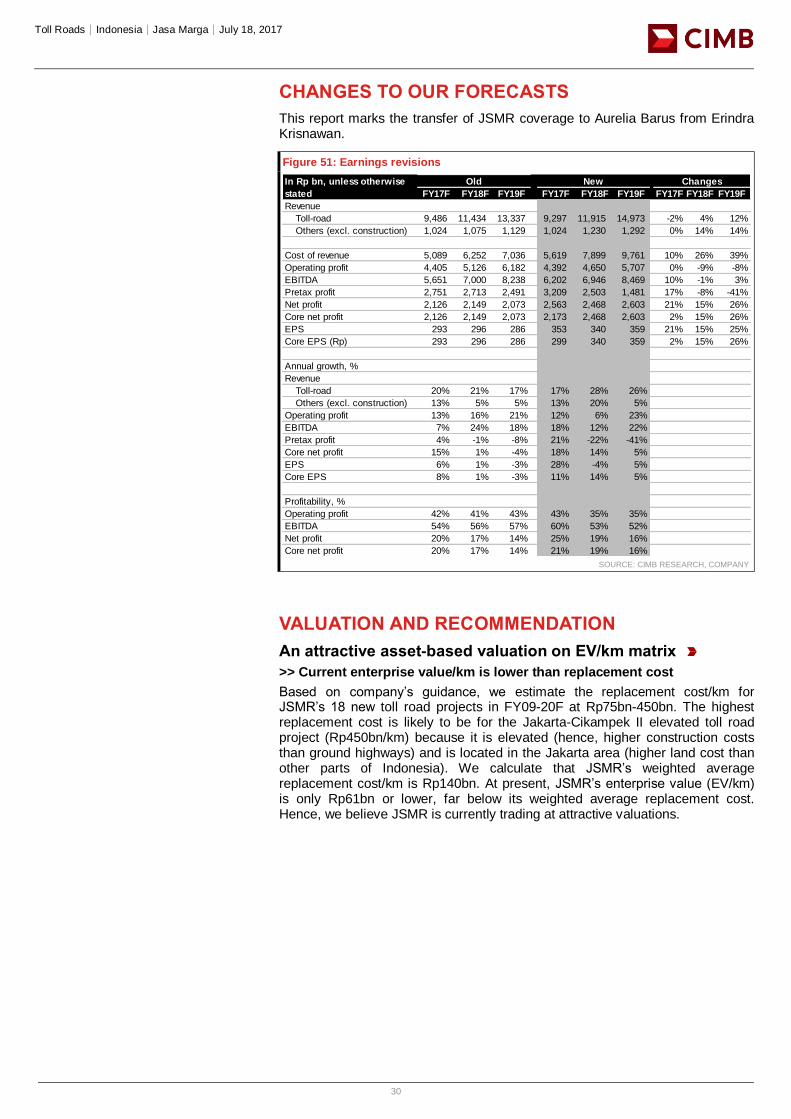

CHANGES TO OUR FORECASTS

This report marks the transfer of JSMR coverage to Aurelia Barus from Erindra Krisnawan.

Figure 51: Earnings revisions

SOURCE: CIMB RESEARCH, COMPANY

VALUATION AND RECOMMENDATION

An attractive asset-based valuation on EV/km matrix

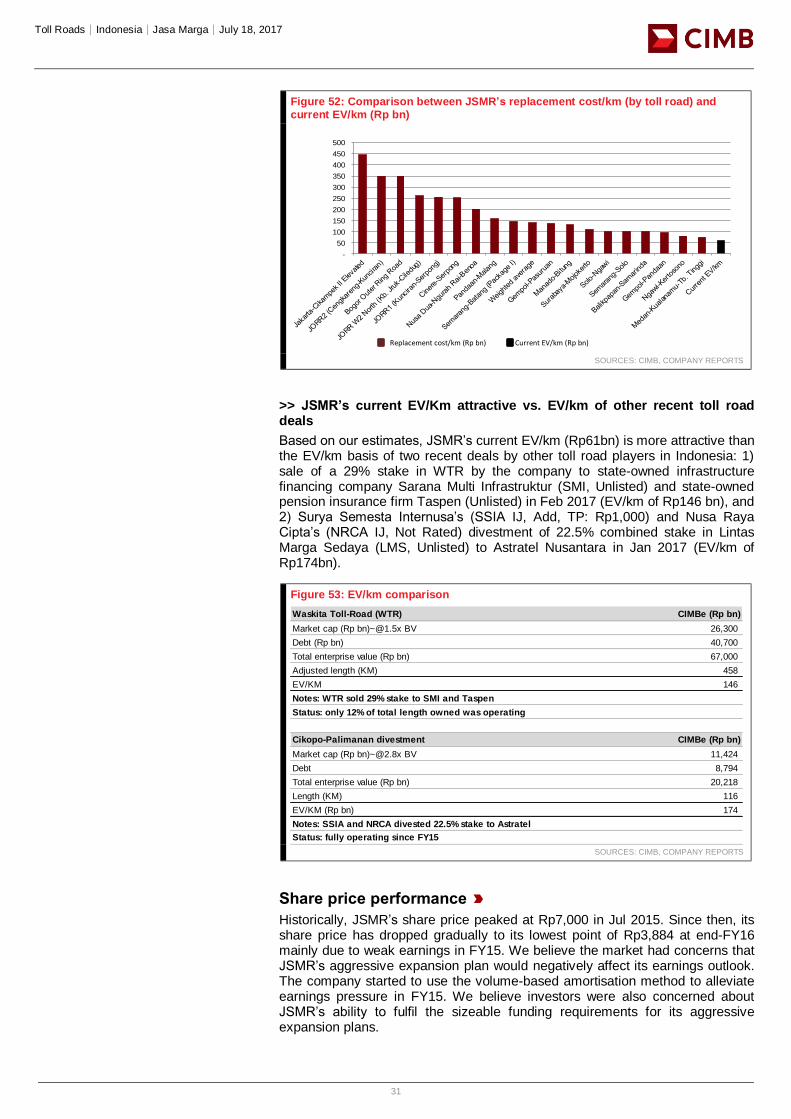

>> Current enterprise value/km is lower than replacement cost

Based on company’s guidance, we estimate the replacement cost/km for JSMR’s 18 new toll road projects in FY09-20F at Rp75bn-450bn. The highest replacement cost is likely to be for the Jakarta-Cikampek II elevated toll road project (Rp450bn/km) because it is elevated (hence, higher construction costs than ground highways) and is located in the Jakarta area (higher land cost than other parts of Indonesia). We calculate that JSMR’s weighted average replacement cost/km is Rp140bn. At present, JSMR’s enterprise value (EV/km) is only Rp61bn or lower, far below its weighted average replacement cost. Hence, we believe JSMR is currently trading at attractive valuations.

FY17F FY18F FY19F FY17F FY18F FY19F FY17F FY18F FY19F

Revenue

Toll-road 9,486 11,434 13,337 9,297 11,915 14,973 -2% 4% 12%

Others (excl. construction) 1,024 1,075 1,129 1,024 1,230 1,292 0% 14% 14%

Cost of revenue 5,089 6,252 7,036 5,619 7,899 9,761 10% 26% 39%

Operating profit 4,405 5,126 6,182 4,392 4,650 5,707 0% -9% -8%

EBITDA 5,651 7,000 8,238 6,202 6,946 8,469 10% -1% 3%

Pretax profit 2,751 2,713 2,491 3,209 2,503 1,481 17% -8% -41%

Net profit 2,126 2,149 2,073 2,563 2,468 2,603 21% 15% 26%

Core net profit 2,126 2,149 2,073 2,173 2,468 2,603 2% 15% 26%

EPS 293 296 286 353 340 359 21% 15% 25%

Core EPS (Rp) 293 296 286 299 340 359 2% 15% 26%

Annual growth, %

Revenue

Toll-road 20% 21% 17% 17% 28% 26%

Others (excl. construction) 13% 5% 5% 13% 20% 5%

Operating profit 13% 16% 21% 12% 6% 23%

EBITDA 7% 24% 18% 18% 12% 22%

Pretax profit 4% -1% -8% 21% -22% -41%

Core net profit 15% 1% -4% 18% 14% 5%

EPS 6% 1% -3% 28% -4% 5%

Core EPS 8% 1% -3% 11% 14% 5%

Profitability, %

Operating profit 42% 41% 43% 43% 35% 35%

EBITDA 54% 56% 57% 60% 53% 52%

Net profit 20% 17% 14% 25% 19% 16%

Core net profit 20% 17% 14% 21% 19% 16%

In Rp bn, unless otherwise

stated

Old New Changes

Toll Roads│Indonesia│Jasa Marga│July 18, 2017

31

Figure 52: Comparison between JSMR’s replacement cost/km (by toll road) and current EV/km (Rp bn)

SOURCES: CIMB, COMPANY REPORTS

>> JSMR’s current EV/Km attractive vs. EV/km of other recent toll road deals

Based on our estimates, JSMR’s current EV/km (Rp61bn) is more attractive than the EV/km basis of two recent deals by other toll road players in Indonesia: 1) sale of a 29% stake in WTR by the company to state-owned infrastructure financing company Sarana Multi Infrastruktur (SMI, Unlisted) and state-owned pension insurance firm Taspen (Unlisted) in Feb 2017 (EV/km of Rp146 bn), and 2) Surya Semesta Internusa’s (SSIA IJ, Add, TP: Rp1,000) and Nusa Raya Cipta’s (NRCA IJ, Not Rated) divestment of 22.5% combined stake in Lintas Marga Sedaya (LMS, Unlisted) to Astratel Nusantara in Jan 2017 (EV/km of Rp174bn).

Figure 53: EV/km comparison

SOURCES: CIMB, COMPANY REPORTS

Share price performance

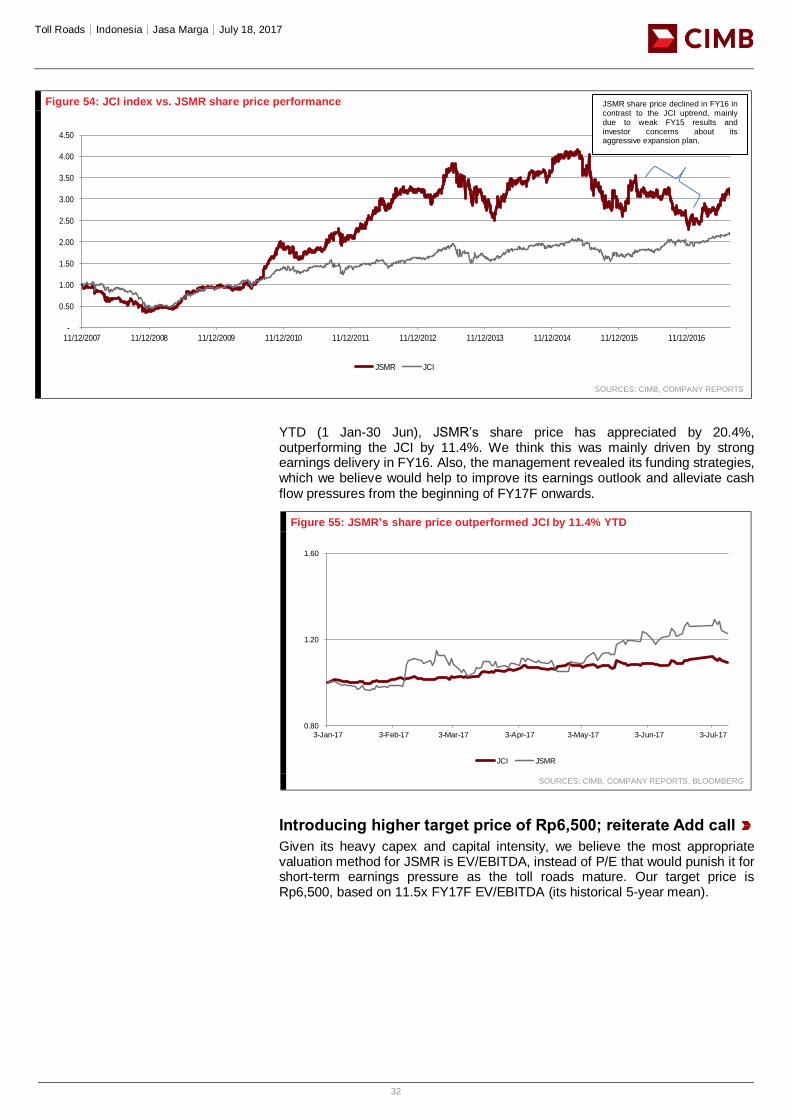

Historically, JSMR’s share price peaked at Rp7,000 in Jul 2015. Since then, its share price has dropped gradually to its lowest point of Rp3,884 at end-FY16 mainly due to weak earnings in FY15. We believe the market had concerns that JSMR’s aggressive expansion plan would negatively affect its earnings outlook. The company started to use the volume-based amortisation method to alleviate earnings pressure in FY15. We believe investors were also concerned about JSMR’s ability to fulfil the sizeable funding requirements for its aggressive expansion plans.

Title:

Source:

Please fill in the values above to have them entered in your report

-

50

100

150

200

250

300

350

400

450

500

Waskita Toll-Road (WTR) CIMBe (Rp bn)

Market cap (Rp bn)[email protected] BV 26,300

Debt (Rp bn) 40,700

Total enterprise value (Rp bn) 67,000

Adjusted length (KM) 458

EV/KM 146

Cikopo-Palimanan divestment CIMBe (Rp bn)

Market cap (Rp bn)[email protected] BV 11,424

Debt 8,794

Total enterprise value (Rp bn) 20,218

Length (KM) 116

EV/KM (Rp bn) 174

Status: fully operating since FY15

Notes: WTR sold 29% stake to SMI and Taspen

Status: only 12% of total length owned was operating

Notes: SSIA and NRCA divested 22.5% stake to Astratel

Replacement cost/km (Rp bn) Current EV/km (Rp bn)

Toll Roads│Indonesia│Jasa Marga│July 18, 2017

32

Figure 54: JCI index vs. JSMR share price performance

SOURCES: CIMB, COMPANY REPORTS