Embed Size (px)

Citation preview

SA 510 (REVISED)*INITIAL AUDIT ENGAGEMENTS—OPENING

BALANCES(Effective for audits of financial statements

for periods beginning on or after April 1, 2010)

Contents

Paragraph(s)IntroductionScope of this SA ....................................................................................... 1Effective Date............................................................................................ 2Objective ................................................................................................. 3Definitions ............................................................................................... 4RequirementsAudit Procedures ...................................................................................5-9Audit Conclusions and Reporting ......................................................10-13Application and Other Explanatory MaterialAudit Procedures.............................................................................. .A1-A4Audit Conclusions and Reporting ..................................................... A5-A6Material Modifications vis a vis ISA 510, “Initial Audit Engagements–Opening Balances”Appendix: Illustrations of Auditors’ Reports with Modified Opinions

Standard on Auditing (SA) 510 (Revised), “Initial Audit Engagements—OpeningBalances” should be read in the context of the “Preface to the Standards onQuality Control, Auditing, Review, Other Assurance and Related Services1,”which sets out the authority of SAs and proposed SA 200 (Revised), “OverallObjectives of the Independent Auditor and the Conduct of an Audit inAccordance with Standards on Auditing”2.

* Published in March, 2009 issue of the Journal.1 Published in the July, 2007 issue of the Journal.2 Presently, SA 200, “Basic Principles Governing an Audit” and SA 200A, “Objective and Scope ofan Audit of Financial Statements” correspond to International Standard on Auditing (ISA) 200(Revised and Redrafted). Both the SAs are currently being revised in the light of the ISA 200(Revised and Redrafted). Post revision, the principles covered by SA 200 (AAS 1) and SA 200A(AAS 2) will be merged into one Standard, i.e., SA 200.

Handbook of Auditing Pronouncements-I

SA 510 (Revised) 578

IntroductionScope of this SA1. This Standard on Auditing (SA) deals with the auditor’s responsibilitiesrelating to opening balances when conducting an initial audit engagement. Inaddition to financial statement amounts, opening balances include mattersrequiring disclosure that existed at the beginning of the period, such ascontingencies and commitments. When the financial statements includecomparative financial information, the requirements and guidance in [proposed]SA 710 (Revised)3 also apply. SA 300 (Revised)4 includes additionalrequirements and guidance regarding activities prior to starting an initial audit.

Effective Date2. This SA is effective for audits of financial statements for periods beginningon or after April 1, 2010.

Objective3. In conducting an initial audit engagement, the objective of the auditor withrespect to opening balances is to obtain sufficient appropriate audit evidenceabout whether:(a) Opening balances contain misstatements that materially affect the current

period’s financial statements; and(b) Appropriate accounting policies reflected in the opening balances have

been consistently applied in the current period’s financial statements, orchanges thereto are properly accounted for and adequately presented anddisclosed in accordance with the applicable financial reporting framework.

Definitions4. For the purposes of the SAs, the following terms have the meaningsattributed below:(a) Initial audit engagement – An engagement in which either:

(i) The financial statements for the prior period were not audited; or(ii) The financial statements for the prior period were audited by a

predecessor auditor.

3 Currently, SA 710 (AAS 25), “Comparatives” is in force. The Standard is being revised in the lightof the corresponding International Standard.4 SA 300 (Revised), “Planning an Audit of Financial Statements”.

Initial Audit Engagements – Opening Balances

SA 510 (Revised)579

(b) Opening balances – Those account balances that exist at the beginning ofthe period. Opening balances are based upon the closing balances of theprior period and reflect the effects of transactions and events of priorperiods and accounting policies applied in the prior period. Openingbalances also include matters requiring disclosure that existed at thebeginning of the period, such as contingencies and commitments.

(c) Predecessor auditor – The auditor from a different audit firm, who auditedthe financial statements of an entity in the prior period and who has beenreplaced by the current auditor.

RequirementsAudit ProceduresOpening Balances5. The auditor shall read the most recent financial statements, if any, and thepredecessor auditor’s report thereon, if any, for information relevant to openingbalances, including disclosures.6. The auditor shall obtain sufficient appropriate audit evidence aboutwhether the opening balances contain misstatements that materially affect thecurrent period’s financial statements by:(a) Determining whether the prior period’s closing balances have been

correctly brought forward to the current period or, when appropriate, anyadjustments have been disclosed as prior period items in the current year’sStatement of Profit and Loss5;

(b) Determining whether the opening balances reflect the application ofappropriate accounting policies; and

(c) Performing one or more of the following: (Ref: Para. A1–A4)(i) Where the prior year financial statements were audited, perusing the

copies of the audited financial statements including the other relevantdocuments relating to the prior period financial statements;

(ii) Evaluating whether audit procedures performed in the current periodprovide evidence relevant to the opening balances; or

(iii) Performing specific audit procedures to obtain evidence regarding theopening balances.

5 Accounting Standard (AS) 5, “Net Profit or Loss for the Period, Prior Period Items and Changesin Accounting Policies” requires that prior period items should be separately disclosed in theStatement of Profit and Loss in a manner that their impact on the current profit or loss can beperceived.

Handbook of Auditing Pronouncements-I

SA 510 (Revised) 580

7. If the auditor obtains audit evidence that the opening balances containmisstatements that could materially affect the current period’s financialstatements, the auditor shall perform such additional audit procedures as areappropriate in the circumstances to determine the effect on the current period’sfinancial statements. If the auditor concludes that such misstatements exist in thecurrent period’s financial statements, the auditor shall communicate themisstatements with the appropriate level of management and those charged withgovernance in accordance with SA 4506.Consistency of Accounting Policies8. The auditor shall obtain sufficient appropriate audit evidence aboutwhether the accounting policies reflected in the opening balances have beenconsistently applied in the current period’s financial statements, and whetherchanges in the accounting policies have been properly accounted for andadequately presented and disclosed in accordance with the applicable financialreporting framework.Relevant Information in the Predecessor Auditor’s Report9. If the prior period’s financial statements were audited by a predecessorauditor and there was a modification to the opinion, the auditor shall evaluate theeffect of the matter giving rise to the modification in assessing the risks ofmaterial misstatement in the current period’s financial statements in accordancewith SA 315.7

Audit Conclusions and ReportingOpening Balances10. If the auditor is unable to obtain sufficient appropriate audit evidence regardingthe opening balances, the auditor shall express a qualified opinion or a disclaimer ofopinion, as appropriate, in accordance with Proposed SA 705.8 (Ref: Para. A5)

6 Standard on Auditing (SA) 450, “Evaluation of Misstatements Identified During the Audit”,paragraphs 8 and 12.7 SA 315, “Identifying and Assessing the Risks of Material Misstatement Through Understandingthe Entity and Its Environment”.8 At present, there is no separate Standard on Auditing (SA) corresponding to InternationalStandard on Auditing (ISA) 705, “Modifications to the Opinion in the Independent Auditor’s Report”and the concept of modified audit report has been discussed in SA 700, “The Auditor’s Report onFinancial Statements” (Hitherto known as AAS 28). The Auditing and Assurance Standards Board(AASB) has issued the Exposure Drafts of Revised SA 700, “Forming An Opinion and Reporting onFinancial Statements”; SA 705, “Modifications to the Opinion in the Independent Auditor’s Report”;and SA 706, “Emphasis of Matter Paragraphs and Other Matter Paragraphs in the IndependentAuditor’s Report”, corresponding to the ISA 700, ISA 705 and ISA 706. These Exposure Drafts arepublished in the June, 2009 issue of the Journal.

Initial Audit Engagements – Opening Balances

SA 510 (Revised)581

11. If the auditor concludes that the opening balances contain a misstatementthat materially affects the current period’s financial statements, and the effect ofthe misstatement is not properly accounted for or not adequately presented ordisclosed, the auditor shall express a qualified opinion or an adverse opinion, asappropriate, in accordance with Proposed SA 705.Consistency of Accounting Policies12. If the auditor concludes that:(a) the current period’s accounting policies are not consistently applied in

relation to opening balances in accordance with the applicable financialreporting framework; or

(b) a change in accounting policies is not properly accounted for or notadequately presented or disclosed in accordance with the applicablefinancial reporting framework,

the auditor shall express a qualified opinion or an adverse opinion as appropriatein accordance with Proposed SA 705.Modification to the Opinion in the Predecessor Auditor’s Report13. If the predecessor auditor’s opinion regarding the prior period’s financialstatements included a modification to the auditor’s opinion that remains relevantand material to the current period’s financial statements, the auditor shall modifythe auditor’s opinion on the current period’s financial statements in accordancewith Proposed SA 705 and Proposed SA 710 (Revised). (Ref: Para. A6)

***Application and Other Explanatory MaterialAudit Procedures (Ref: Para. 6)Opening Balances (Ref: Para. 6(c))A1. The nature and extent of audit procedures necessary to obtain sufficientappropriate audit evidence regarding opening balances depend on such matters as:

The accounting policies followed by the entity.

The nature of the account balances, classes of transactions anddisclosures and the risks of material misstatement in the current period’sfinancial statements.

The significance of the opening balances relative to the current period’sfinancial statements.

Handbook of Auditing Pronouncements-I

SA 510 (Revised) 582

Whether the prior period’s financial statements were audited and, if so,whether the predecessor auditor’s opinion was modified.

A2. If the prior period’s financial statements were audited by a predecessorauditor, the auditor may be able to obtain sufficient appropriate audit evidenceregarding the opening balances by perusing the copies of the audited financialstatements including the other relevant documents relating to the prior periodfinancial statements such as supporting schedules to the audited financialstatements. Ordinarily, the current auditor can place reliance on the closingbalances contained in the financial statements for the preceding period, exceptwhen during the performance of audit procedures for the current period thepossibility of misstatements in opening balances is indicated.A3. For current assets and liabilities, some audit evidence about openingbalances may be obtained as part of the current period’s audit procedures. Forexample, the collection (payment) of opening accounts receivable (accountspayable) during the current period will provide some audit evidence of theirexistence, rights and obligations, completeness and valuation at the beginning ofthe period. In the case of inventories, however, the current period’s auditprocedures on the closing inventory balance provide little audit evidenceregarding inventory on hand at the beginning of the period. Therefore, additionalaudit procedures may be necessary, and one or more of the following mayprovide sufficient appropriate audit evidence:

Observing a current physical inventory count and reconciling it to theopening inventory quantities.

Performing audit procedures on the valuation of the opening inventoryitems.

Performing audit procedures on gross profit and cut-off.A4. For non-current assets and liabilities, such as property plant andequipment, investments and long-term debt, some audit evidence may beobtained by examining the accounting records and other information underlyingthe opening balances. In certain cases, the auditor may be able to obtain someaudit evidence regarding opening balances through confirmation with thirdparties, for example, for long-term debt and investments. In other cases, theauditor may need to carry out additional audit procedures.

Initial Audit Engagements – Opening Balances

SA 510 (Revised)583

Audit Conclusions and ReportingOpening Balances (Ref: Para. 10)A5. Proposed SA 705 establishes requirements and provides guidance oncircumstances that may result in a modification to the auditor’s opinion on thefinancial statements, the type of opinion appropriate in the circumstances, andthe content of the auditor’s report when the auditor’s opinion is modified. Theinability of the auditor to obtain sufficient appropriate audit evidence regardingopening balances may result in one of the following modifications to the opinionin the auditor’s report:(a) A qualified opinion or a disclaimer of opinion, as is appropriate in the

circumstances; or(b) Unless prohibited by law or regulation, an opinion which is qualified or

disclaimed, as appropriate, regarding the results of operations*, and cashflows, where relevant, and unmodified regarding State of Affairs*.

The Appendix includes illustrative auditor’s reports.Modification to the Opinion in the Predecessor Auditor’s Report (Ref: Para.13)A6. In some situations, a modification to the predecessor auditor’s opinion maynot be relevant and material to the opinion on the current period’s financialstatements. This may be the case where, for example, there was a scopelimitation in the prior period, but the matter giving rise to the scope limitation hasbeen resolved in the current period.

Material Modifications vis a vis ISA 510, “Initial AuditEngagements - Opening Balances”Deletions1. Paragraph 6 (a) of ISA 510 dealt with the procedure for obtaining sufficientappropriate audit evidence about the opening balances which containmisstatements that materially affect the current period’s financial statements bydetermining whether the prior period’s closing balances have been correctlybrought forward to the current period or, when appropriate, have been restated.Since in India Accounting Standard (AS) 5, “Net Profit or Loss for the Period,Prior Period Items and Changes in Accounting Policies” requires that prior perioditems should be separately disclosed in the Statement of Profit and Loss in a

* Profit & Loss Account.* Balance Sheet.

Handbook of Auditing Pronouncements-I

SA 510 (Revised) 584

manner that their impact on the current profit or loss can be perceived, therestatement of the prior period financial statements does not exist in the Indianscenario. Hence, to align with the requirements of AS 5, the requirement ofrestatement of prior period items has been replaced with the requirement todisclose the prior period items in the current year’s Statement of Profit & Loss.2. Paragraph 6 (c) (i) of ISA 510 dealt with the procedure for obtainingsufficient appropriate audit evidence about the opening balances which containmisstatements that materially affect the current period’s financial statements byreviewing the predecessor auditor’s working papers, where the prior yearfinancial statements were audited. Since in India Clause 1 of Part I of the SecondSchedule to the Code of Ethics provides that a Chartered Accountant in Practiceshall be deemed to be guilty of professional misconduct if he disclosesinformation acquired in the course of his professional engagement to any personother than his client, an auditor cannot provide access to his working paper to theanother auditor. Therefore, keeping in view the requirements of Code of Ethics,the requirement of reviewing the predecessor auditor’s working papers has beenreplaced with the requirement of perusing the copies of the audited financialstatements including the other relevant documents relating to the prior periodfinancial statements. Corresponding change has also been made in theparagraph A4 of ISA 510 and Paragraphs A1 and A5 have been deleted.3. Paragraph A2 of ISA 510 dealt with the outsourcing of an audit of a publicsector entity by the statutorily appointed auditor to a private sector audit firm.Since in the Indian context such situation does not exist, the paragraph A2 of theapplication part has been deleted completely.

Initial Audit Engagements – Opening Balances

SA 510 (Revised)585

Appendix(Ref: Para. A5)

Illustrations of Auditors’ Reports with Modified Opinions*

Illustration 1:Circumstances described in paragraph A5 (a) include the following: The auditor did not observe the counting of the physical inventory at

the beginning of the current period and was unable to obtainsufficient appropriate audit evidence regarding the opening balancesof inventory.

The possible effects of the inability to obtain sufficient appropriateaudit evidence regarding opening balances of inventory are deemedto be material but not pervasive to the entity’s results of operationsand cash flows.9

The State of Affairs at year end gives a true and fair view. In this particular jurisdiction, law and regulation prohibit the auditor

from giving an opinion which is qualified regarding the results ofoperations and cash flows and unmodified regarding State of Affairs.

INDEPENDENT AUDITOR’S REPORT[Appropriate Addressee]Report on the Financial Statements10

We have audited the accompanying financial statements of ABC Company,which comprise the balance sheet as at March 31, 20X1, and the Statement ofProfit and Loss, and the cash flow statement for the year then ended, and asummary of significant accounting policies and other explanatory notes.

* The Reporting Standards may give rise to conforming amendments to the illustrations of auditors’reports. Further, at present, there is no separate Standard on Auditing (SA) corresponding toInternational Standard on Auditing (ISA) 705, “Modifications to the Opinion in the IndependentAuditors Report” and the concept of modified audit report has been discussed in SA 700, “TheAuditor’s Report on Financial Statements” (Hitherto known as AAS 28). The Auditing andAssurance Standards Board (AASB) has issued the Exposure Drafts of Revised SA 700, “FormingAn Opinion and Reporting on Financial Statements”; SA 705, “Modifications to the Opinion in theIndependent Auditor’s Report”; and SA 706, “Emphasis of Matter Paragraphs and Other MatterParagraphs in the Independent Auditor’s Report”, corresponding to the ISA 700, ISA 705 and ISA706. These Exposure Drafts are published in the June 2009 issue of the Journal.9 If the possible effects, in the auditor’s judgment, are considered to be material and pervasive tothe entity’s results of operations and cash flows, the auditor would disclaim an opinion on theresults of operations and cash flows.10 The sub-title “Report on the Financial Statements” is unnecessary in circumstances when thesecond sub-title “Report on Other Legal and Regulatory Requirements” is not applicable.

Handbook of Auditing Pronouncements-I

SA 510 (Revised) 586

Management’s Responsibility for the Financial StatementsManagement is responsible for the preparation and presentation of financialstatements that give a true and fair view in accordance with applicableAccounting Standards.11 This responsibility includes: designing, implementingand maintaining internal control relevant to the preparation and fair presentationof financial statements that are free from material misstatement, whether due tofraud or error; selecting and applying appropriate accounting policies; andmaking accounting estimates that are reasonable in the circumstances.Auditor’s ResponsibilityOur responsibility is to express an opinion on these financial statements basedon our audit. We conducted our audit in accordance with Standards on Auditing.Those standards require that we comply with ethical requirements and plan andperform the audit to obtain reasonable assurance whether the financialstatements are free from material misstatement.An audit involves performing procedures to obtain audit evidence about the amountsand disclosures in the financial statements. The procedures selected depend on theauditor’s judgment, including the assessment of the risks of material misstatement ofthe financial statements, whether due to fraud or error. In making those riskassessments, the auditor considers internal control relevant to the entity’s preparationand presentation12 of financial statements that give a true and fair view in order todesign audit procedures that are appropriate in the circumstances, but not for thepurpose of expressing an opinion on the effectiveness of the entity’s internalcontrol.13 An audit also includes evaluating the appropriateness of accounting policiesused and the reasonableness of accounting estimates made by management, aswell as evaluating the overall presentation of the financial statements.

11 Depending on the circumstances, this sentence may read: “Management is responsible for thepreparation and fair presentation of these financial statements in accordance with applicableaccounting standards”.12 Depending on the circumstances, this sentence may read: “In making those risk assessments, theauditor considers internal control relevant to the entity’s preparation and fair presentation of thefinancial statements in order to design audit procedures that are appropriate in the circumstances, butnot for the purpose of expressing an opinion on the effectiveness of the entity’s internal control”.13 In circumstances when the auditor also has responsibility to express an opinion on theeffectiveness of internal control in conjunction with the audit of the financial statements, thissentence would be worded as follows: “In making those risk assessments, the auditor considersinternal control relevant to the entity’s preparation and fair presentation of the financial statementsin order to design audit procedures that are appropriate in the circumstances”. In the case offootnote 13, this sentence may read: “In making those risk assessments, the auditor considersinternal control relevant to the entity’s preparation and presentation of financial statements thatgive a true and fair view in order to design audit procedures that are appropriate in thecircumstances”.

Initial Audit Engagements – Opening Balances

SA 510 (Revised)587

We believe that the audit evidence we have obtained is sufficient and appropriateto provide a basis for our qualified audit opinion.Basis for Qualified OpinionWe were appointed as auditors of the company on June 30, 20X0 and thus didnot observe the counting of the physical inventories at the beginning of the year.We were unable to satisfy ourselves by alternative means concerning inventoryquantities held at March 31, 20X0. Since opening inventories enter into thedetermination of the results of operations and cash flows, we were unable todetermine whether adjustments might have been necessary in respect of theprofit for the year reported in the Statement of Profit and Loss and the net cashflows from operating activities reported in the cash flow statement.Qualified OpinionIn our opinion, except for the possible effects of the matter described in the Basisfor Qualified Opinion paragraph, the financial statements give a true and fair viewof the State of Affairs of ABC Company as of March 31, 20X1, and of its Resultsof Operations and its cash flows for the year then ended in accordance withapplicable Accounting Standards.Other MattersThe financial statements of the Company for the year ended March 31, 20X0,were audited by another auditor whose report dated July 1, 20X0 expressed anunmodified opinion on those statements.

Report on Other Legal and Regulatory Requirements[Form and content of this section of the auditor’s report will vary depending onthe nature of the auditor’s other reporting responsibilities].

For ABC and Co.Chartered Accountants

Signature (Name of the Member Signing the Audit Report)

(Designation14)Membership Number

Place of SignatureDate

14 Partner or Proprietor, as the case may be.

Handbook of Auditing Pronouncements-I

SA 510 (Revised) 588

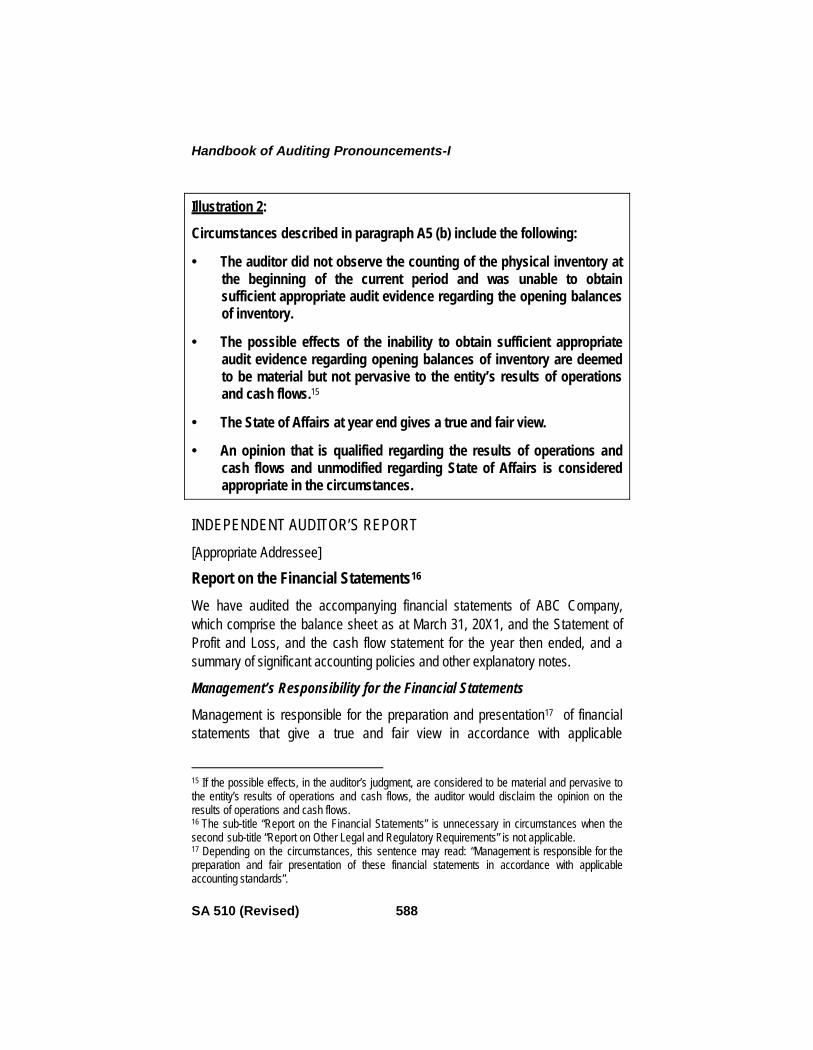

Illustration 2:

Circumstances described in paragraph A5 (b) include the following:

The auditor did not observe the counting of the physical inventory atthe beginning of the current period and was unable to obtainsufficient appropriate audit evidence regarding the opening balancesof inventory.

The possible effects of the inability to obtain sufficient appropriateaudit evidence regarding opening balances of inventory are deemedto be material but not pervasive to the entity’s results of operationsand cash flows.15

The State of Affairs at year end gives a true and fair view.

An opinion that is qualified regarding the results of operations andcash flows and unmodified regarding State of Affairs is consideredappropriate in the circumstances.

INDEPENDENT AUDITOR’S REPORT[Appropriate Addressee]

Report on the Financial Statements16

We have audited the accompanying financial statements of ABC Company,which comprise the balance sheet as at March 31, 20X1, and the Statement ofProfit and Loss, and the cash flow statement for the year then ended, and asummary of significant accounting policies and other explanatory notes.

Management’s Responsibility for the Financial Statements

Management is responsible for the preparation and presentation17 of financialstatements that give a true and fair view in accordance with applicable

15 If the possible effects, in the auditor’s judgment, are considered to be material and pervasive tothe entity’s results of operations and cash flows, the auditor would disclaim the opinion on theresults of operations and cash flows.16 The sub-title “Report on the Financial Statements” is unnecessary in circumstances when thesecond sub-title “Report on Other Legal and Regulatory Requirements” is not applicable.17 Depending on the circumstances, this sentence may read: “Management is responsible for thepreparation and fair presentation of these financial statements in accordance with applicableaccounting standards”.

Initial Audit Engagements – Opening Balances

SA 510 (Revised)589

Accounting Standards. This responsibility includes: designing, implementing andmaintaining internal control relevant to the preparation and fair presentation offinancial statements that are free from material misstatement, whether due tofraud or error; selecting and applying appropriate accounting policies; andmaking accounting estimates that are reasonable in the circumstances.

Auditor’s Responsibility

Our responsibility is to express an opinion on these financial statements basedon our audit. We conducted our audit in accordance with Standards on Auditing.Those standards require that we comply with ethical requirements and plan andperform the audit to obtain reasonable assurance whether the financialstatements are free from material misstatement.

An audit involves performing procedures to obtain audit evidence about theamounts and disclosures in the financial statements. The procedures selecteddepend on the auditor’s judgment, including the assessment of the risks ofmaterial misstatement of the financial statements, whether due to fraud or error.In making those risk assessments, the auditor considers internal control relevantto the entity’s preparation and presentation18 of financial statements that give atrue and fair view in order to design audit procedures that are appropriate in thecircumstances, but not for the purpose of expressing an opinion on theeffectiveness of the entity’s internal control.19 An audit also includes evaluatingthe appropriateness of accounting policies used and the reasonableness ofaccounting estimates made by management, as well as evaluating the overallpresentation of the financial statements.

18 Depending on the circumstances, this sentence may read: “In making those risk assessments,the auditor considers internal control relevant to the entity’s preparation and fair presentation of thefinancial statements in order to design audit procedures that are appropriate in the circumstances,but not for the purpose of expressing an opinion on the effectiveness of the entity’s internalcontrol”.19 In circumstances when the auditor also has responsibility to express an opinion on theeffectiveness of internal control in conjunction with the audit of the financial statements, thissentence would be worded as follows: “In making those risk assessments, the auditor considersinternal control relevant to the entity’s preparation and fair presentation of the financial statementsin order to design audit procedures that are appropriate in the circumstances”. In the case offootnote 19, this sentence may read: “In making those risk assessments, the auditor considersinternal control relevant to the entity’s preparation and presentation of financial statements thatgive a true and fair view in order to design audit procedures that are appropriate in thecircumstances”.

Handbook of Auditing Pronouncements-I

SA 510 (Revised) 590

We believe that the audit evidence we have obtained is sufficient and appropriateto provide a basis for our unmodified opinion on the State of Affairs and ourqualified audit opinion on the results of operations and cash flows.

Basis for Qualified Opinion on the results of operations and Cash Flows

We were appointed as auditors of the company on June 30, 20X0 and thus didnot observe the counting of the physical inventories at the beginning of the year.We were unable to satisfy ourselves by alternative means concerning inventoryquantities held at March 31, 20X0. Since opening inventories enter into thedetermination of the results of operations and cash flows, we were unable todetermine whether adjustments might have been necessary in respect of theprofit for the year reported in the Statement of Profit and Loss and the net cashflows from operating activities reported in the cash flow statement.

Qualified Opinion on the results of operations and Cash Flows

In our opinion, except for the possible effects of the matter described in the Basisfor Qualified Opinion paragraph, the Statement of Profit and Loss and Cash FlowStatement give a true and fair view of the results of operations and cash flows ofABC Company for the year ended March 31, 20X1 in accordance with applicableAccounting Standards.

Opinion on the State of Affairs

In our opinion, the balance sheet gives a true and fair view of the State of Affairsof ABC Company as of March 31, 20X1 in accordance with applicableAccounting Standards.

Other Matters

The financial statements of the Company for the year ended March 31, 20X0,were audited by another auditor whose report dated July 1, 20X0 expressed anunmodified opinion on those statements.

Report on Other Legal and Regulatory Requirements[Form and content of this section of the auditor’s report will vary depending onthe nature of the auditor’s other reporting responsibilities.]

For ABC and Co.Chartered Accountants

Initial Audit Engagements – Opening Balances

SA 510 (Revised)591

Signature (Name of the Member Signing the Audit Report)

(Designation20)Membership Number

Place of Signature

Date

20 Partner or Proprietor, as the case may be.

SA 510INITIAL ENGAGEMENTS - OPENING BALANCES

(Effective for all audits commencing on or after July 1, 2001)

ContentsParagraph(s)

Introduction ................................................................................. 1-4

Audit Procedures........................................................................5-10

Audit Conclusions and Reporting ...........................................11-12

Effective Date.................................................................................13

Standard on Auditing (SA) 510, “Initial Engagements - Opening Balances”should be read in the context of the “Preface to the Standards on Quality Control,Auditing, Review, Other Assurance and Related Services”, which sets out theauthority of SAs.

Issued in July, 2001. Published in the July, 2007 issue of the Journal.

Initial Engagements - Opening Balances

SA 510593

Introduction1. The purpose of this Standard on Auditing (SA) is to establish standardsregarding audit of opening balances in case of initial engagements, i.e., when thefinancial statements are audited for the first time or when the financial statementsfor the preceding period were audited by another auditor. This Standard wouldalso be considered by the auditor so that he may become aware of contingenciesand commitments existing at the beginning of the current period.2. “Opening balances” means those account balances which exist at thebeginning of the period. Opening balances are the closing balances of thepreceding period brought forward to the current period and reflect the effect of:(a) transactions and other events of the preceding periods; and(b) accounting policies applied in the preceding period.3. For initial audit engagements, the auditor should obtain sufficientappropriate audit evidence that:(a) the closing balances of the preceding period have been correctly

brought forward to the current period;(b) the opening balances do not contain misstatements that materially

affect the financial statements for the current period; and(c) appropriate accounting policies are consistently applied.4. In an initial audit engagement, the auditor will not have previously obtainedaudit evidence supporting the opening balances.

Audit Procedures5. For the purpose of this Statement, the sufficiency and appropriateness ofthe audit evidence, the auditor will need to obtain regarding opening balances,would depend on the following matters:

The accounting policies followed by the entity.

Whether the auditor’s report contained an unqualified opinion, a qualifiedopinion, adverse opinion or disclaimer of opinion where the financialstatements for the preceding period were audited.

The nature of the opening balances, including the risk of their misstatementin the financial statements for the current period.

The materiality of the opening balances relative to the financial statementsfor the current period.

Handbook of Auditing Pronouncements-I

SA 510 594

6. The auditor will need to consider whether the accounting policies followedin the preceding period, as per which the opening balances have been arrived at,were appropriate and that those policies are consistently applied in the financialstatements for the current period and where such accounting policies areinappropriate, the same have been changed in the current period and adequatelydisclosed.7. When the financial statements for the preceding period were audited byanother auditor, the current auditor may be able to obtain sufficient appropriateaudit evidence regarding opening balances by perusing the copies of the auditedfinancial statements. Ordinarily, the current auditor can place reliance on theclosing balances contained in the financial statements for the preceding period,except when during the performance of audit procedures for the current periodthe possibility of misstatements in opening balances is indicated.8. When the financial statements of the preceding period were not audited orthe auditor is not satisfied by using the procedures described in paragraph 7, theauditor will need to perform other procedures such as those discussed inparagraphs 9 and 10.9. For current assets and liabilities, some audit evidence can ordinarily beobtained as part of the audit procedures performed during the current period.For example, the collection/payment of opening accounts receivable/ accountspayable during the current period will provide some audit evidence as to theirexistence, rights and obligations, completeness and valuation at the beginning ofthe period.10. For other assets and liabilities, such as fixed assets, investments and long-term debt, the auditor will ordinarily examine the records underlying the openingbalances. In certain cases, the auditor may be able to obtain confirmation ofopening balances from third parties, for example, for long-term debt andinvestments.

Audit Conclusions and Reporting11. If, after performing procedures including those set out above, theauditor is unable to obtain sufficient appropriate audit evidence concerningopening balances, the auditor should, as appropriate, express:(a) a qualified opinion, or(b) a disclaimer of opinion.The auditor may also express an opinion which is qualified or disclaimedregarding the profit or loss and unqualified regarding state of affairs, asappropriate.

Initial Engagements - Opening Balances

SA 510595

12. If the opening balances contain misstatements which materially affectthe financial statements for the current period and the effect of the same isnot properly accounted for and adequately disclosed, the auditor shouldexpress a qualified opinion or an adverse opinion, as appropriate.

Effective Date13. This Standard on Auditing becomes operative for all audits commencing onor after 1st July, 2001.

SA 520ANALYTICAL PROCEDURES

(Effective for all audits relating toaccounting periods beginning on or after April 1, 1997)

ContentsParagraph(s)

Introduction ................................................................................. 1-3

Nature and Purpose of Analytical Procedures ........................... 4-7

Analytical Procedures in Planning the Audit ............................. 8-9

Analytical Procedures as Substantive Procedures.................10-12

Analytical Procedures in the Overall Reviewat the End of the Audit ..................................................................13

Extent of Reliance on Analytical Procedures ..........................14-16

Investigating Unusual Items ....................................................17-18

Effective Date.................................................................................19

Standard on Auditing (SA) 520*, “Analytical Procedures” should be read in thecontext of the “Preface to the Standards on Quality Control, Auditing, Review,Other Assurance and Related Services”1, which sets out the authority of SAs.

* Issued in December, 1997.1 Published in the July, 2007 issue of the Journal.

Analytical Procedures

SA 520597

Introduction1. The purpose of this Standard on Auditing (SA) is to establish standards onthe application of analytical procedures during an audit.2. The auditor should apply analytical procedures at the planning andoverall review stages of the audit. Analytical procedures may also be appliedat other stages.3. “Analytical procedures” means the analysis of significant ratios and trends,including the resulting investigation of fluctuations and relationships that areinconsistent with other relevant information or which deviate from predictedamounts.

Nature and Purpose of Analytical Procedures4. Analytical procedures include the consideration of comparisons of theentity's financial information with, for example:

Comparable information for prior periods.

Anticipated results of the entity, such as budgets or forecasts.

Predictive estimates prepared by the auditor, such as an estimation ofdepreciation charge for the year.

Similar industry information, such as a comparison of the entity's ratio ofsales to trade debtors with industry averages, or with other entities ofcomparable size in the same industry.

5. Analytical procedures also include consideration of relationships:

Among elements of financial information that would be expected to conformto a predictable pattern based on the entity's experience, such as grossmargin percentages.

Between financial information and relevant non-financial information, suchas payroll costs to number of employees.

6. Various methods may be used in performing the above procedures. Theserange from simple comparisons to complex analyses using advanced statisticaltechniques. Analytical procedures may be applied to consolidated financialstatements, financial statements of components (such as subsidiaries, divisionsor segments) and individual elements of financial information. The auditor'schoice of procedures, methods and level of application is a matter of professionaljudgement.

Handbook of Auditing Pronouncements-I

SA 520 598

7. Analytical procedures are used for the following purposes:(a) to assist the auditor in planning the nature, timing and extent of other audit

procedures;(b) as substantive procedures when their use can be more effective or efficient

than tests of details in reducing detection risk for specific financialstatement assertions; and

(c) as an overall review of the financial statements in the final review stage ofthe audit.

Analytical Procedures in Planning the Audit8. The auditor should apply analytical procedures at the planning stageto assist in understanding the business and in identifying areas ofpotential risk. Application of analytical procedures may indicate aspects of thebusiness of which the auditor was unaware and will assist in determining thenature, timing and extent of other audit procedures.9. Analytical procedures in planning the audit use both financial and non-financial information, for example, the relationship between sales and squarefootage of selling space or volume of goods sold.

Analytical Procedures as Substantive Procedures10. The auditor's reliance on substantive procedures to reduce detection riskrelating to specific financial statement assertions may be derived from tests ofdetails, from analytical procedures, or from a combination of both. The decisionabout which procedures to use to achieve a particular audit objective is based onthe auditor's judgement about the expected effectiveness and efficiency of theavailable procedures in reducing detection risk for specific financial statementassertions.11. The auditor will ordinarily inquire of management as to the availability andreliability of information needed to apply analytical procedures and the results ofany such procedures performed by the entity. It may be efficient to use analyticaldata prepared by the entity, provided the auditor is satisfied that such data isproperly prepared.12. When intending to perform analytical procedures as substantiveprocedures, the auditor will need to consider a number of factors such as the:

Objectives of the analytical procedures and the extent to which their resultscan be relied upon (paragraphs 14-16).

Analytical Procedures

SA 520599

Nature of the entity and the degree to which information can bedisaggregated, for example, analytical procedures may be more effectivewhen applied to financial information on individual sections of an operationor to financial statements of components of a diversified entity, than whenapplied to the financial statements of the entity as a whole.

Availability of information, both financial, such as budgets or forecasts, andnon-financial, such as the number of units produced or sold.

Reliability of the information available, for example, whether budgets areprepared with sufficient care.

Relevance of the information available, for example, whether budgets havebeen established as results to be expected rather than as goals to beachieved.

Source of the information available, for example, sources independent of theentity are ordinarily more reliable than internal sources.

Comparability of the information available, for example, broad industry datamay need to be supplemented to be comparable to that of an entity thatproduces and sells specialised products.

Knowledge gained during previous audits, together with the auditor'sunderstanding of the effectiveness of the accounting and internal controlsystems and the types of problems that in prior periods have given rise toaccounting adjustments.

Analytical Procedures in the Overall Review at the End ofthe Audit13. The auditor should apply analytical procedures at or near the end ofthe audit when forming an overall conclusion as to whether the financialstatements as a whole are consistent with the auditor's knowledge of thebusiness. The conclusions drawn from the results of such procedures areintended to corroborate conclusions formed during the audit of individualcomponents or elements of the financial statements and assist in arriving at theoverall conclusion as to the reasonableness of the financial statements.However, in some cases, as a result of application of analytical procedures, theauditor may identify areas where further procedures need to be applied beforethe auditor can form an overall conclusion about the financial statements.

Extent of Reliance on Analytical Procedures14. The application of analytical procedures is based on the expectation thatrelationships among data exist and continue in the absence of known conditions

Handbook of Auditing Pronouncements-I

SA 520 600

to the contrary. The presence of these relationships provides audit evidence asto the completeness, accuracy and validity of the data produced by theaccounting system. However, reliance on the results of analytical procedures willdepend on the auditor's assessment of the risk that the analytical proceduresmay identify relationships as expected when, in fact, a material misstatementexists.15. The extent of reliance that the auditor places on the results of analyticalprocedures depends on the following factors:(a) materiality of the items involved, for example, when inventory balances are

material, the auditor does not rely only on analytical procedures in formingconclusions. However, the auditor may rely solely on analytical proceduresfor certain income and expense items when they are not individuallymaterial;

(b) other audit procedures directed toward the same audit objectives, forexample, other procedures performed by the auditor in reviewing thecollectibility of accounts receivable, such as the review of subsequent cashreceipts, might confirm or dispel questions raised from the application ofanalytical procedures to an ageing schedule of customers' accounts;

(c) accuracy with which the expected results of analytical procedures can bepredicted. For example, the auditor will ordinarily expect greaterconsistency in comparing gross profit margins from one period to anotherthan in comparing discretionary expenses, such as research or advertising;and

(d) assessments of inherent and control risks, for example, if internal controlover sales order processing is weak and, therefore, control risk is high,more reliance on tests of details of transactions and balances than onanalytical procedures in drawing conclusions on receivables may berequired.

16. The auditor will need to consider testing the controls, if any, over thepreparation of information used in applying analytical procedures. When suchcontrols are effective, the auditor will have greater confidence in the reliability ofthe information and, therefore, in the results of analytical procedures. Thecontrols over non-financial information can often be tested in conjunction withtests of accounting-related controls. For example, an entity in establishingcontrols over the processing of sales invoices may include controls over therecording of unit sales. In these circumstances, the auditor could test the controlsover the recording of unit sales in conjunction with tests of the controls over theprocessing of sales invoices.

Analytical Procedures

SA 520601

Investigating Unusual Items17. When analytical procedures identify significant fluctuations orrelationships that are inconsistent with other relevant information or thatdeviate from predicted amounts, the auditor should investigate and obtainadequate explanations and appropriate corroborative evidence.18. The investigation of unusual fluctuations and relationships ordinarily beginswith inquiries of management, followed by:(a) corroboration of management's responses, for example, by comparing

them with the auditor's knowledge of the business and other evidenceobtained during the course of the audit; and

(b) consideration of the need to apply other audit procedures based on theresults of such inquiries, if management is unable to provide an explanationor if the explanation is not considered adequate.

Effective Date19. This Standard on Auditing becomes operative for all audits relating toaccounting periods beginning on or after April 1, 1997.

SA 530 (REVISED)AUDIT SAMPLING

(Effective for audits of financial statementsfor periods beginning on or after April 1, 2009)

Contents

Paragraph(s)

IntroductionScope of this SA ................................................................................... 1−2Effective Date ........................................................................................... 3Objective ................................................................................................. 4Definitions ............................................................................................... 5RequirementsSample Design, Size and Selection of Items for Testing ..................... 6−8Performing Audit Procedures .............................................................9−11Nature and Cause of Deviations and Misstatements .......................12−13Projecting Misstatements ....................................................................... 14Evaluating Results of Audit Sampling .................................................... 15Application and Other Explanatory MaterialDefinitions ....................................................................................... A1−A3Sample Design, Size and Selection of Items for Testing .............. A4−A13Performing Audit Procedures ...................................................... A14−A16Nature and Cause of Deviations and Misstatements ...........................A17Projecting Misstatements ............................................................ A18−A20Evaluating Results of Audit Sampling ......................................... A21−A23Material Modifications vis a vis ISA 530, “Audit Sampling”Appendix 1: Stratification and Value-Weighted SelectionAppendix 2: Examples of Factors Influencing Sample Size for Tests ofControls

Published in February, 2009 issue of the Journal.

Audit Sampling

SA 530 (Revised)603

Appendix 3: Examples of Factors Influencing Sample Size for Tests ofDetailsAppendix 4: Sample Selection Methods

Standard on Auditing (SA) 530 (Revised), “Audit Sampling” should be read in thecontext of the “Preface to the Standards on Quality Control, Auditing, Review,Other Assurance and Related Services1”, which sets out the authority of SAs andproposed SA 200 (Revised), “Overall Objectives of the Independent Auditor andthe Conduct of an Audit in Accordance with Standards on Auditing” 2.

1 Published in the July, 2007 issue of the Journal.2 Presently, SA 200, “Basic Principles Governing an Audit” and SA 200A, “Objective and Scope ofan Audit of Financial Statements” correspond to International Standard on Auditing (ISA) 200(Revised and Redrafted). Both the SAs are currently being revised in the light of the ISA 200(Revised and Redrafted). Post revision, the principles covered by SA 200 (AAS 1) and SA 200A(AAS 2) will be merged into one Standard, i.e., SA 200.

Handbook of Auditing Pronouncements-I

SA 530 (Revised) 604

IntroductionScope of this SA1. This Standard on Auditing (SA) applies when the auditor has decided touse audit sampling in performing audit procedures. It deals with the auditor’s useof statistical and non-statistical sampling when designing and selecting the auditsample, performing tests of controls and tests of details, and evaluating theresults from the sample.2. This SA complements SA 500 (Revised)3, which deals with the auditor’sresponsibility to design and perform audit procedures to obtain sufficientappropriate audit evidence to be able to draw reasonable conclusions on whichto base the audit opinion. SA 500 (Revised) provides guidance on the meansavailable to the auditor for selecting items for testing, of which audit sampling isone means.

Effective Date3. This SA is effective for audits of financial statements for periods beginningon or after April 1, 2009.

Objective4. The objective of the auditor when using audit sampling is to provide areasonable basis for the auditor to draw conclusions about the population fromwhich the sample is selected.

Definitions5. For purposes of the SAs, the following terms have the meanings attributedbelow:(a) Audit sampling (sampling) – The application of audit procedures to less

than 100% of items within a population of audit relevance such that allsampling units have a chance of selection in order to provide the auditorwith a reasonable basis on which to draw conclusions about the entirepopulation.

(b) Population – The entire set of data from which a sample is selected andabout which the auditor wishes to draw conclusions.

(c) Sampling risk – The risk that the auditor’s conclusion based on a samplemay be different from the conclusion if the entire population were

3 Revised SA 500, “Audit Evidence”.

Audit Sampling

SA 530 (Revised)605

subjected to the same audit procedure. Sampling risk can lead to twotypes of erroneous conclusions:(i) In the case of a test of controls, that controls are more effective than

they actually are, or in the case of a test of details, that a materialmisstatement does not exist when in fact it does. The auditor isprimarily concerned with this type of erroneous conclusion because itaffects audit effectiveness and is more likely to lead to aninappropriate audit opinion.

(ii) In the case of a test of controls, that controls are less effective thanthey actually are, or in the case of a test of details, that a materialmisstatement exists when in fact it does not. This type of erroneousconclusion affects audit efficiency as it would usually lead toadditional work to establish that initial conclusions were incorrect.

(d) Non-sampling risk – The risk that the auditor reaches an erroneousconclusion for any reason not related to sampling risk. (Ref: Para A1)

(e) Anomaly – A misstatement or deviation that is demonstrably notrepresentative of misstatements or deviations in a population.

(f) Sampling unit – The individual items constituting a population. (Ref: ParaA2)

(g) Statistical sampling – An approach to sampling that has the followingcharacteristics:(i) Random selection of the sample items; and(ii) The use of probability theory to evaluate sample results, including

measurement of sampling risk.A sampling approach that does not have characteristics (i) and (ii) isconsidered non-statistical sampling.

(h) Stratification – The process of dividing a population into sub-populations,each of which is a group of sampling units which have similarcharacteristics (often monetary value).

(i) Tolerable misstatement – A monetary amount set by the auditor in respectof which the auditor seeks to obtain an appropriate level of assurance thatthe monetary amount set by the auditor is not exceeded by the actualmisstatement in the population. (Ref: Para. A3)

(j) Tolerable rate of deviation – A rate of deviation from prescribed internalcontrol procedures set by the auditor in respect of which the auditor seeksto obtain an appropriate level of assurance that the rate of deviation set by

Handbook of Auditing Pronouncements-I

SA 530 (Revised) 606

the auditor is not exceeded by the actual rate of deviation in thepopulation.

RequirementsSample Design, Size and Selection of Items for Testing6. When designing an audit sample, the auditor shall consider the purpose ofthe audit procedure and the characteristics of the population from which thesample will be drawn. (Ref: Para. A4-A9)

7. The auditor shall determine a sample size sufficient to reduce samplingrisk to an acceptably low level. (Ref: Para. A10-A11)

8. The auditor shall select items for the sample in such a way that eachsampling unit in the population has a chance of selection. (Ref: Para. A12-A13)

Performing Audit Procedures9. The auditor shall perform audit procedures, appropriate to the purpose, oneach item selected.10. If the audit procedure is not applicable to the selected item, the auditorshall perform the procedure on a replacement item. (Ref: Para. A14)

11. If the auditor is unable to apply the designed audit procedures, or suitablealternative procedures, to a selected item, the auditor shall treat that item as adeviation from the prescribed control, in the case of tests of controls, or amisstatement, in the case of tests of details. (Ref: Para. A15-A16)

Nature and Cause of Deviations and Misstatements12. The auditor shall investigate the nature and cause of any deviations ormisstatements identified, and evaluate their possible effect on the purpose of theaudit procedure and on other areas of the audit. (Ref: Para. A17)

13. In the extremely rare circumstances when the auditor considers amisstatement or deviation discovered in a sample to be an anomaly, the auditorshall obtain a high degree of certainty that such misstatement or deviation is notrepresentative of the population. The auditor shall obtain this degree of certaintyby performing additional audit procedures to obtain sufficient appropriate auditevidence that the misstatement or deviation does not affect the remainder of thepopulation.

Projecting Misstatements14. For tests of details, the auditor shall project misstatements found in thesample to the population. (Ref: Para. A18-A20)

Audit Sampling

SA 530 (Revised)607

Evaluating Results of Audit Sampling15. The auditor shall evaluate:(a) The results of the sample; and (Ref: Para. A21-A22)

(b) Whether the use of audit sampling has provided a reasonable basis forconclusions about the population that has been tested. (Ref: Para. A23)

***Application and Other Explanatory MaterialDefinitionsNon-Sampling Risk (Ref: Para. 5(d))A1. Examples of non-sampling risk include use of inappropriate auditprocedures, or misinterpretation of audit evidence and failure to recognise amisstatement or deviation.Sampling Unit (Ref: Para. 5(f))A2. The sampling units might be physical items (for example, cheques listed ondeposit slips, credit entries on bank statements, sales invoices or debtors’balances) or monetary units.Tolerable Misstatement (Ref: Para. 5(i))A3. When designing a sample, the auditor determines tolerable misstatementin order to address the risk that the aggregate of individually immaterialmisstatements may cause the financial statements to be materially misstated andprovide a margin for possible undetected misstatements. Tolerable misstatementis the application of performance materiality, as defined in SA 320 (Revised)4, toa particular sampling procedure. Tolerable misstatement may be the sameamount or an amount lower than performance materiality.

Sample Design, Size and Selection of Items for TestingSample Design (Ref: Para. 6)A4. Audit sampling enables the auditor to obtain and evaluate audit evidenceabout some characteristic of the items selected in order to form or assist informing a conclusion concerning the population from which the sample is drawn.Audit sampling can be applied using either non-statistical or statistical samplingapproaches.

4 Standard on Auditing (SA) 320 (Revised), “Materiality in Planning and Performing an Audit”,paragraph 9.

Handbook of Auditing Pronouncements-I

SA 530 (Revised) 608

A5. When designing an audit sample, the auditor’s consideration includes thespecific purpose to be achieved and the combination of audit procedures that islikely to best achieve that purpose. Consideration of the nature of the auditevidence sought and possible deviation or misstatement conditions or othercharacteristics relating to that audit evidence will assist the auditor in definingwhat constitutes a deviation or misstatement and what population to use forsampling. In fulfilling the requirement of paragraph 8 of SA 500 (Revised), whenperforming audit sampling, the auditor performs audit procedures to obtainevidence that the population from which the audit sample is drawn is complete.A6. The auditor’s consideration of the purpose of the audit procedure, asrequired by paragraph 6, includes a clear understanding of what constitutes adeviation or misstatement so that all, and only, those conditions that are relevantto the purpose of the audit procedure are included in the evaluation of deviationsor projection of misstatements. For example, in a test of details relating to theexistence of accounts receivable, such as confirmation, payments made by thecustomer before the confirmation date but received shortly after that date by theclient, are not considered a misstatement. Also, a misposting between customeraccounts does not affect the total accounts receivable balance. Therefore, it maynot be appropriate to consider this a misstatement in evaluating the sampleresults of this particular audit procedure, even though it may have an importanteffect on other areas of the audit, such as the assessment of the risk of fraud orthe adequacy of the allowance for doubtful accounts.A7. In considering the characteristics of a population, for tests of controls, theauditor makes an assessment of the expected rate of deviation based on theauditor’s understanding of the relevant controls or on the examination of a smallnumber of items from the population. This assessment is made in order to designan audit sample and to determine sample size. For example, if the expected rateof deviation is unacceptably high, the auditor will normally decide not to performtests of controls. Similarly, for tests of details, the auditor makes an assessmentof the expected misstatement in the population. If the expected misstatement ishigh, 100% examination or use of a large sample size may be appropriate whenperforming tests of details.A8. In considering the characteristics of the population from which the samplewill be drawn, the auditor may determine that stratification or value-weightedselection is appropriate. Appendix 1 provides further discussion on stratificationand value-weighted selection.A9. The decision whether to use a statistical or non-statistical samplingapproach is a matter for the auditor’s judgment; however, sample size is not avalid criterion to distinguish between statistical and non-statistical approaches.

Audit Sampling

SA 530 (Revised)609

Sample Size (Ref: Para. 7)A10. The level of sampling risk that the auditor is willing to accept affects thesample size required. The lower the risk the auditor is willing to accept, thegreater the sample size will need to be.A11. The sample size can be determined by the application of a statistically-based formula or through the exercise of professional judgment. Appendices 2and 3 indicate the influences that various factors typically have on thedetermination of sample size. When circumstances are similar, the effect onsample size of factors such as those identified in Appendices 2 and 3 will besimilar regardless of whether a statistical or non-statistical approach is chosen.Selection of Items for Testing (Ref: Para. 8)A12. With statistical sampling, sample items are selected in a way that eachsampling unit has a known probability of being selected. With non-statisticalsampling, judgment is used to select sample items. Because the purpose ofsampling is to provide a reasonable basis for the auditor to draw conclusionsabout the population from which the sample is selected, it is important that theauditor selects a representative sample, so that bias is avoided, by choosingsample items which have characteristics typical of the population.A13. The principal methods of selecting samples are the use of randomselection, systematic selection and haphazard selection. Each of these methodsis discussed in Appendix 4.

Performing Audit Procedures (Ref: Para. 10-11)

A14. An example of when it is necessary to perform the procedure on areplacement item is when a cancelled cheque is selected while testing forevidence of payment authorisation. If the auditor is satisfied that the cheque hasbeen properly cancelled such that it does not constitute a deviation, anappropriately chosen replacement is examined.A15. An example of when the auditor is unable to apply the designed auditprocedures to a selected item is when documentation relating to that item hasbeen lost.A16. An example of a suitable alternative procedure might be the examination ofsubsequent cash receipts together with evidence of their source and the itemsthey are intended to settle when no reply has been received in response to apositive confirmation request.

Handbook of Auditing Pronouncements-I

SA 530 (Revised) 610

Nature and Cause of Deviations and Misstatements (Ref: Para. 12)

A17. In analysing the deviations and misstatements identified, the auditor mayobserve that many have a common feature, for example, type of transaction,location, product line or period of time. In such circumstances, the auditor maydecide to identify all items in the population that possess the common feature,and extend audit procedures to those items. In addition, such deviations ormisstatements may be intentional, and may indicate the possibility of fraud.

Projecting Misstatements (Ref: Para. 14)

A18. The auditor is required to project misstatements for the population to obtaina broad view of the scale of misstatement but this projection may not besufficient to determine an amount to be recorded.A19. When a misstatement has been established as an anomaly, it may beexcluded when projecting misstatements to the population. However, the effectof any such misstatement, if uncorrected, still needs to be considered in additionto the projection of the non-anomalous misstatements.A20. For tests of controls, no explicit projection of deviations is necessary sincethe sample deviation rate is also the projected deviation rate for the populationas a whole. SA 3305 provides guidance when deviations from controls uponwhich the auditor intends to rely are detected.

Evaluating Results of Audit Sampling (Ref: Para. 15)

A21. For tests of controls, an unexpectedly high sample deviation rate may leadto an increase in the assessed risk of material misstatement, unless further auditevidence substantiating the initial assessment is obtained. For tests of details, anunexpectedly high misstatement amount in a sample may cause the auditor tobelieve that a class of transactions or account balance is materially misstated, inthe absence of further audit evidence that no material misstatement exists.A22. In the case of tests of details, the projected misstatement plus anomalousmisstatement, if any, is the auditor’s best estimate of misstatement in thepopulation. When the projected misstatement plus anomalous misstatement, ifany, exceeds tolerable misstatement, the sample does not provide a reasonablebasis for conclusions about the population that has been tested. The closer theprojected misstatement plus anomalous misstatement is to tolerablemisstatement, the more likely that actual misstatement in the population mayexceed tolerable misstatement. Also if the projected misstatement is greater thanthe auditor’s expectations of misstatement used to determine the sample size,

5 SA 330, “The Auditor’s Responses to Assessed Risks”, paragraphs 17 and A41.

Audit Sampling

SA 530 (Revised)611

the auditor may conclude that there is an unacceptable sampling risk that theactual misstatement in the population exceeds the tolerable misstatement.Considering the results of other audit procedures helps the auditor to assess therisk that actual misstatement in the population exceeds tolerable misstatement,and the risk may be reduced if additional audit evidence is obtained.A23. If the auditor concludes that audit sampling has not provided a reasonablebasis for conclusions about the population that has been tested, the auditor may:

Request management to investigate misstatements that have beenidentified and the potential for further misstatements and to make anynecessary adjustments; or

Tailor the nature, timing and extent of those further audit procedures tobest achieve the required assurance. For example, in the case of tests ofcontrols, the auditor might extend the sample size, test an alternativecontrol or modify related substantive procedures.

Material Modifications vis a vis ISA 530, “Audit Sampling”SA 530 (Revised), “Audit Sampling” does not contain any material modificationsvis à vis ISA 530.

Handbook of Auditing Pronouncements-I

SA 530 (Revised) 612

Appendix 1(Ref: Para. A8)

Stratification and Value-Weighted SelectionIn considering the characteristics of the population from which the sample will bedrawn, the auditor may determine that stratification or value-weighted selection isappropriate. This Appendix provides guidance to the auditor on the use ofstratification and value-weighted sampling techniques.

Stratification1. Audit efficiency may be improved if the auditor stratifies a population bydividing it into discrete sub-populations which have an identifying characteristic.The objective of stratification is to reduce the variability of items within eachstratum and therefore allow sample size to be reduced without increasingsampling risk.2. When performing tests of details, the population is often stratified bymonetary value. This allows greater audit effort to be directed to the larger valueitems, as these items may contain the greatest potential misstatement in terms ofoverstatement. Similarly, a population may be stratified according to a particularcharacteristic that indicates a higher risk of misstatement, for example, whentesting the allowance for doubtful accounts in the valuation of accountsreceivable, balances may be stratified by age.3. The results of audit procedures applied to a sample of items within astratum can only be projected to the items that make up that stratum. To draw aconclusion on the entire population, the auditor will need to consider the risk ofmaterial misstatement in relation to whatever other strata make up the entirepopulation. For example, 20% of the items in a population may make up 90% ofthe value of an account balance. The auditor may decide to examine a sample ofthese items. The auditor evaluates the results of this sample and reaches aconclusion on the 90% of value separately from the remaining 10% (on which afurther sample or other means of gathering audit evidence will be used, or whichmay be considered immaterial).4. If a class of transactions or account balance has been divided into strata,the misstatement is projected for each stratum separately. Projectedmisstatements for each stratum are then combined when considering thepossible effect of misstatements on the total class of transactions or accountbalance.

Audit Sampling

SA 530 (Revised)613

Value-Weighted Selection5. When performing tests of details it may be efficient to identify the samplingunit as the individual monetary units that make up the population. Havingselected specific monetary units from within the population, for example, theaccounts receivable balance, the auditor may then examine the particular items,for example, individual balances, that contain those monetary units. One benefitof this approach to defining the sampling unit is that audit effort is directed to thelarger value items because they have a greater chance of selection, and canresult in smaller sample sizes. This approach may be used in conjunction withthe systematic method of sample selection (described in Appendix 4) and is mostefficient when selecting items using random selection.

Handbook of Auditing Pronouncements-I

SA 530 (Revised) 614

Appendix 2(Ref: Para. A11)

Examples of Factors Influencing Sample Size for Tests ofControlsThe following are factors that the auditor may consider when determining thesample size for tests of controls. These factors, which need to be consideredtogether, assume the auditor does not modify the nature or timing of tests ofcontrols or otherwise modify the approach to substantive procedures in responseto assessed risks.FACTOR EFFECT ON

SAMPLE SIZE1. An increase in theextent to which theauditor’s riskassessment takes intoaccount relevant controls

Increase The more assurance the auditorintends to obtain from theoperating effectiveness ofcontrols, the lower the auditor’sassessment of the risk of materialmisstatement will be, and thelarger the sample size will need tobe. When the auditor’sassessment of the risk of materialmisstatement at the assertionlevel includes an expectation ofthe operating effectiveness ofcontrols, the auditor is required toperform tests of controls. Otherthings being equal, the greater thereliance the auditor places on theoperating effectiveness of controlsin the risk assessment, thegreater is the extent of theauditor’s tests of controls (andtherefore, the sample size isincreased).

2. An increase in thetolerable rate ofdeviation

Decrease The lower the tolerable rate ofdeviation, the larger the samplesize needs to be.

3. An increase in the Increase The higher the expected rate of

Audit Sampling

SA 530 (Revised)615

expected rate ofdeviation of thepopulation to be tested

deviation, the larger the samplesize needs to be so that theauditor is in a position to make areasonable estimate of the actualrate of deviation. Factors relevantto the auditor’s consideration ofthe expected rate of deviationinclude the auditor’sunderstanding of the business (inparticular, risk assessmentprocedures undertaken to obtainan understanding of internalcontrol), changes in personnel orin internal control, the results ofaudit procedures applied in priorperiods and the results of otheraudit procedures. High expectedcontrol deviation rates ordinarilywarrant little, if any, reduction ofthe assessed risk of materialmisstatement.

4. An increase in theauditor’s desired level ofassurance that thetolerable rate ofdeviation is notexceeded by the actualrate of deviation in thepopulation

Increase The greater the level of assurancethat the auditor desires that theresults of the sample are in factindicative of the actual incidenceof deviation in the population, thelarger the sample size needs tobe.

5. An increase in thenumber of sampling unitsin the population

Negligibleeffect

For large populations, the actualsize of the population has little, ifany, effect on sample size. Forsmall populations however, auditsampling may not be as efficientas alternative means of obtainingsufficient appropriate auditevidence.

Handbook of Auditing Pronouncements-I

SA 530 (Revised) 616

Appendix 3(Ref: Para. A11)

Examples of Factors Influencing Sample Size for Tests ofDetailsThe following are factors that the auditor may consider when determining thesample size for tests of details. These factors, which need to be consideredtogether, assume the auditor does not modify the approach to tests of controls orotherwise modify the nature or timing of substantive procedures in response tothe assessed risks.FACTOR EFFECT ON

SAMPLE SIZE1. An increase in theauditor’s assessment ofthe risk of materialmisstatement

Increase The higher the auditor’sassessment of the risk of materialmisstatement, the larger thesample size needs to be. Theauditor’s assessment of the riskof material misstatement isaffected by inherent risk andcontrol risk. For example, if theauditor does not perform tests ofcontrols, the auditor’s riskassessment cannot be reducedfor the effective operation ofinternal controls with respect tothe particular assertion.Therefore, in order to reduceaudit risk to an acceptably lowlevel, the auditor needs a lowdetection risk and will rely moreon substantive procedures. Themore audit evidence that isobtained from tests of details(that is, the lower the detectionrisk), the larger the sample sizewill need to be.

2. An increase in theuse of other substantiveprocedures directed at

Decrease The more the auditor is relying onother substantive procedures(tests of details or substantive

Audit Sampling

SA 530 (Revised)617

the same assertion analytical procedures) to reduceto an acceptable level thedetection risk regarding aparticular population, the lessassurance the auditor will requirefrom sampling and, therefore, thesmaller the sample size can be.

3. An increase in theauditor’s desired level ofassurance that tolerablemisstatement is notexceeded by actualmisstatement in thepopulation

Increase The greater the level ofassurance that the auditorrequires that the results of thesample are in fact indicative ofthe actual amount ofmisstatement in the population,the larger the sample size needsto be.

4. An increase intolerable misstatement

Decrease The lower the tolerablemisstatement, the larger thesample size needs to be.

5. An increase in theamount of misstatementthe auditor expects tofind in the population