Embed Size (px)

Citation preview

CONFIDENTIAL AND PROPRIETARYAny use of this material without specific permission of McKinsey & Company is strictly prohibited

Innovations in SME finance

Cairo, March 28, 2010

Marriott Hotel

Antonino GittoPartner at McKinsey & Company Inc. ItalyItalian mobile: +39 348 8952839Egyptian mobile: +20 106 5540501 E-mail: [email protected]

McKinsey & Company 1|

“World’s most powerful and

capable consulting firm – It commands unrivalled respect”

– Fortune

“Distinguished by its excep-

tional people, top manage-ment approach and one-firm principle”

– Business

Week

Long history of working with leading corporations

• Serving 96% of Global 100 and 76% of Global 500

• Across all industries

Broad geographic reach

• Now with 94 offices in 52 countries, including 5 offices in the Middle East (i.e., Bahrain, Doha, Dubai, Riyadh and Abu Dhabi)

• Common philosophy, base of experience, skills and standards

Unrivalled talent pool

• 8,900 consultants from 52 countries

• 4 in 5 possess advanced management degrees

• 3 in 5 have significant managerial experience

Strategy to deliver impact to leading organizations on a global basis through our extensive expertise

• Global reach and best practice learning

• Substantial reinvestment in industry knowledge building

• Depth of specialist support

• Combine industry insight and functional knowledge

“World’s largest strategic management consultant”

– Wall Street Journal

McKinsey & company is the world’s leading management consulting firm

McKinsey & Company 2|

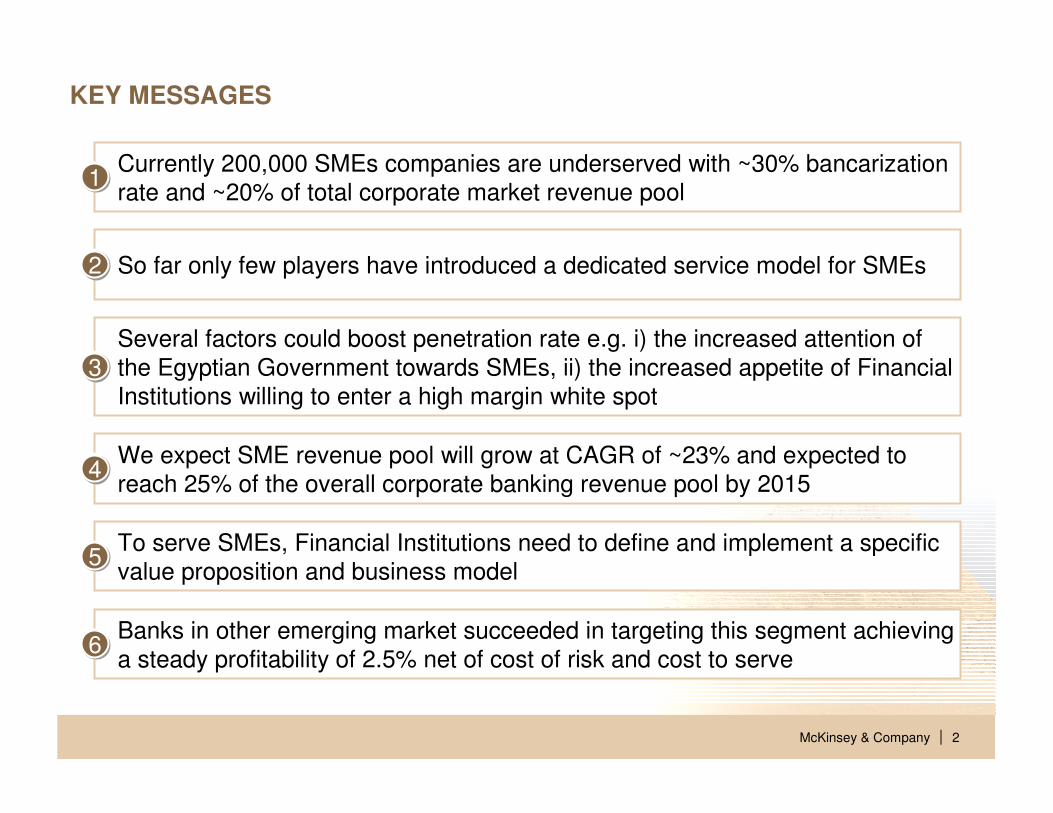

KEY MESSAGES

Currently 200,000 SMEs companies are underserved with ~30% bancarization

rate and ~20% of total corporate market revenue pool1

So far only few players have introduced a dedicated service model for SMEs2

Several factors could boost penetration rate e.g. i) the increased attention of

the Egyptian Government towards SMEs, ii) the increased appetite of Financial

Institutions willing to enter a high margin white spot 3

We expect SME revenue pool will grow at CAGR of ~23% and expected to

reach 25% of the overall corporate banking revenue pool by 2015 4

To serve SMEs, Financial Institutions need to define and implement a specific

value proposition and business model5

Banks in other emerging market succeeded in targeting this segment achieving

a steady profitability of 2.5% net of cost of risk and cost to serve6

McKinsey & Company 3|

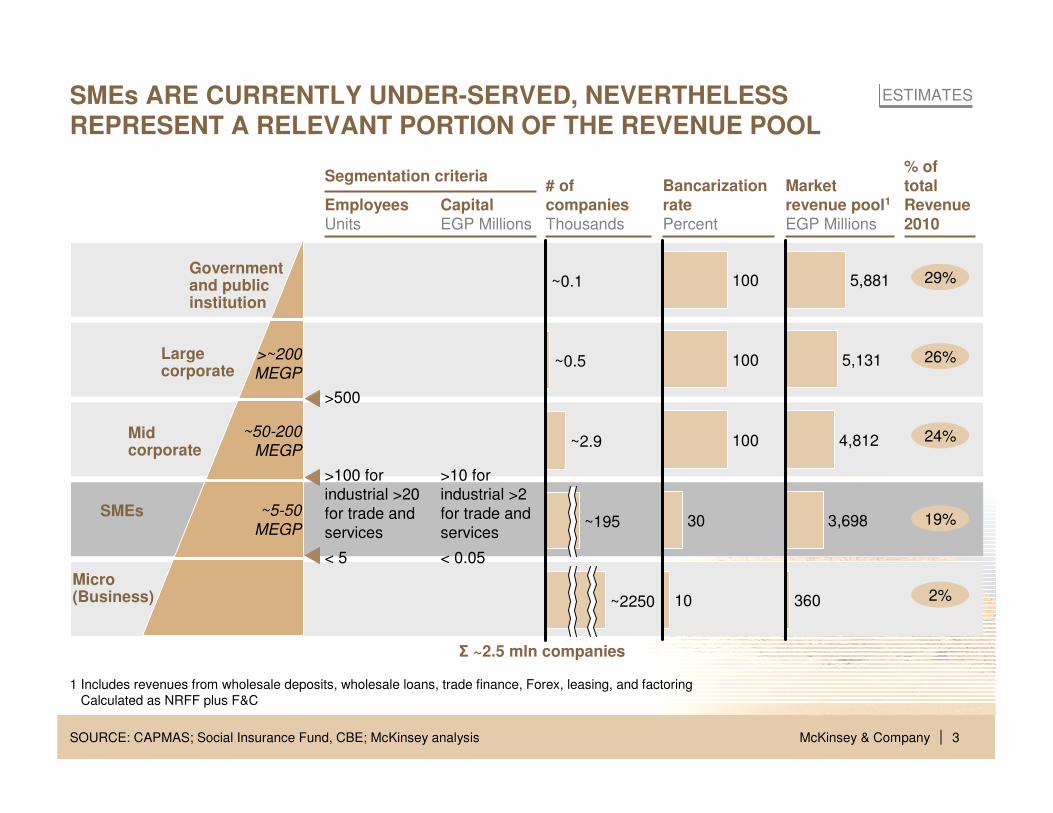

~195

~2250

~2.9

~0.5

~0.1

Σ ~2.5 mln companies

SOURCE: CAPMAS; Social Insurance Fund, CBE; McKinsey analysis

SMEs ARE CURRENTLY UNDER-SERVED, NEVERTHELESS REPRESENT A RELEVANT PORTION OF THE REVENUE POOL

1 Includes revenues from wholesale deposits, wholesale loans, trade finance, Forex, leasing, and factoring

Calculated as NRFF plus F&C

10

30

100

100

100

360

3,698

4,812

5,131

5,881Government and public institution

Large corporate

SMEs

Micro (Business)

Mid corporate

>~200

MEGP

~50-200

MEGP

~5-50

MEGP

ESTIMATES

29%

26%

24%

19%

2%

% of total Revenue 2010

< 5

>100 for industrial >20

for trade and

services

>10 for industrial >2

for trade and

services

< 0.05

>500

# of companiesThousands

Market revenue pool1

EGP Millions

BancarizationratePercent

Segmentation criteria

CapitalEGP Millions

EmployeesUnits

McKinsey & Company 4|

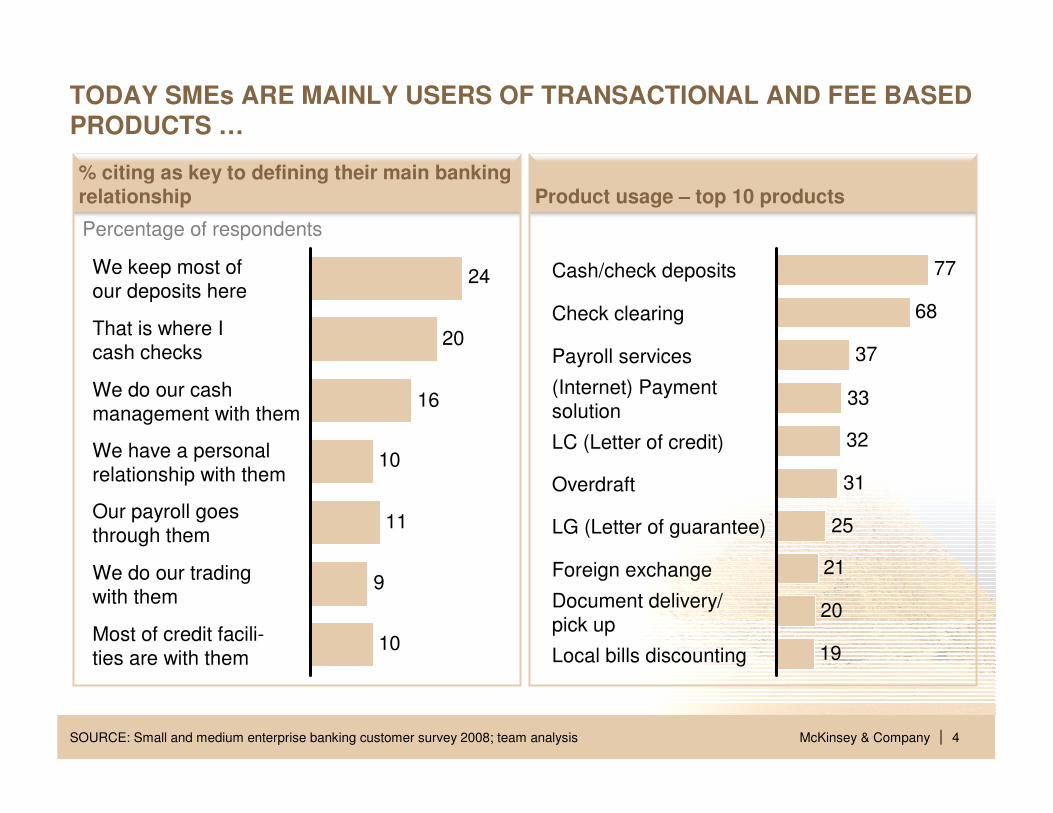

% citing as key to defining their main banking relationship Product usage – top 10 products

TODAY SMEs ARE MAINLY USERS OF TRANSACTIONAL AND FEE BASED PRODUCTS …

Percentage of respondents

10

9

11

10

16

20

24

Most of credit facili-

ties are with them

We do our trading

with them

Our payroll goes

through them

We have a personal

relationship with them

We do our cash

management with them

That is where I

cash checks

We keep most of

our deposits here

19

20

21

25

31

32

33

37

68

77

Local bills discounting

Document delivery/

pick up

Foreign exchange

LG (Letter of guarantee)

Overdraft

LC (Letter of credit)

(Internet) Payment

solution

Payroll services

Check clearing

Cash/check deposits

SOURCE: Small and medium enterprise banking customer survey 2008; team analysis

McKinsey & Company 5|

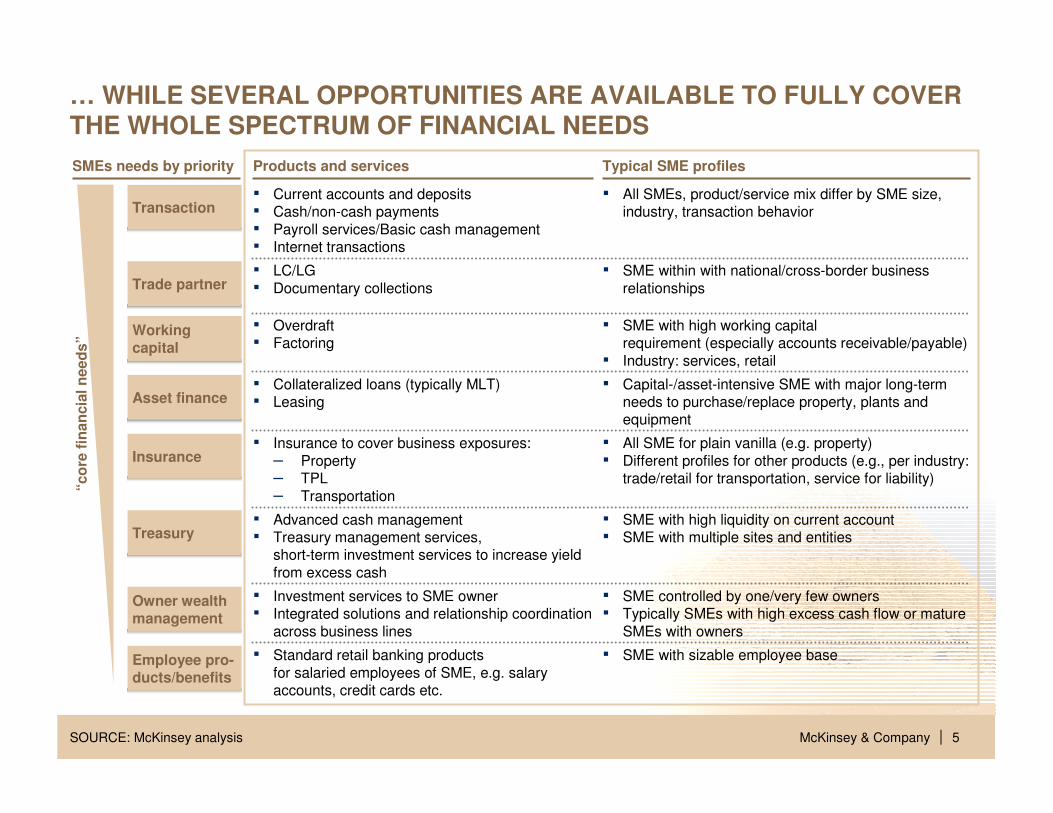

… WHILE SEVERAL OPPORTUNITIES ARE AVAILABLE TO FULLY COVER THE WHOLE SPECTRUM OF FINANCIAL NEEDS

SOURCE: McKinsey analysis

Products and services Typical SME profiles

“co

re f

inan

cia

l n

eed

s”

SMEs needs by priority

Transaction▪ Current accounts and deposits▪ Cash/non-cash payments

▪ Payroll services/Basic cash management▪ Internet transactions

▪ All SMEs, product/service mix differ by SME size, industry, transaction behavior

Treasury▪ Advanced cash management▪ Treasury management services,

short-term investment services to increase yield

from excess cash

▪ SME with high liquidity on current account ▪ SME with multiple sites and entities

Working capital

▪ Overdraft ▪ Factoring

▪ SME with high working capitalrequirement (especially accounts receivable/payable)

▪ Industry: services, retail

Asset finance▪ Collateralized loans (typically MLT) ▪ Leasing

▪ Capital-/asset-intensive SME with major long-term needs to purchase/replace property, plants and equipment

Trade partner▪ LC/LG

▪ Documentary collections

▪ SME within with national/cross-border business

relationships

Insurance▪ Insurance to cover business exposures:

– Property– TPL

– Transportation

▪ All SME for plain vanilla (e.g. property)

▪ Different profiles for other products (e.g., per industry: trade/retail for transportation, service for liability)

Owner wealth management

▪ Investment services to SME owner▪ Integrated solutions and relationship coordination

across business lines

▪ SME controlled by one/very few owners▪ Typically SMEs with high excess cash flow or mature

SMEs with owners

Employee pro-ducts/benefits

▪ Standard retail banking products

for salaried employees of SME, e.g. salary accounts, credit cards etc.

▪ SME with sizable employee base

McKinsey & Company 6|

1

16

18

25

36

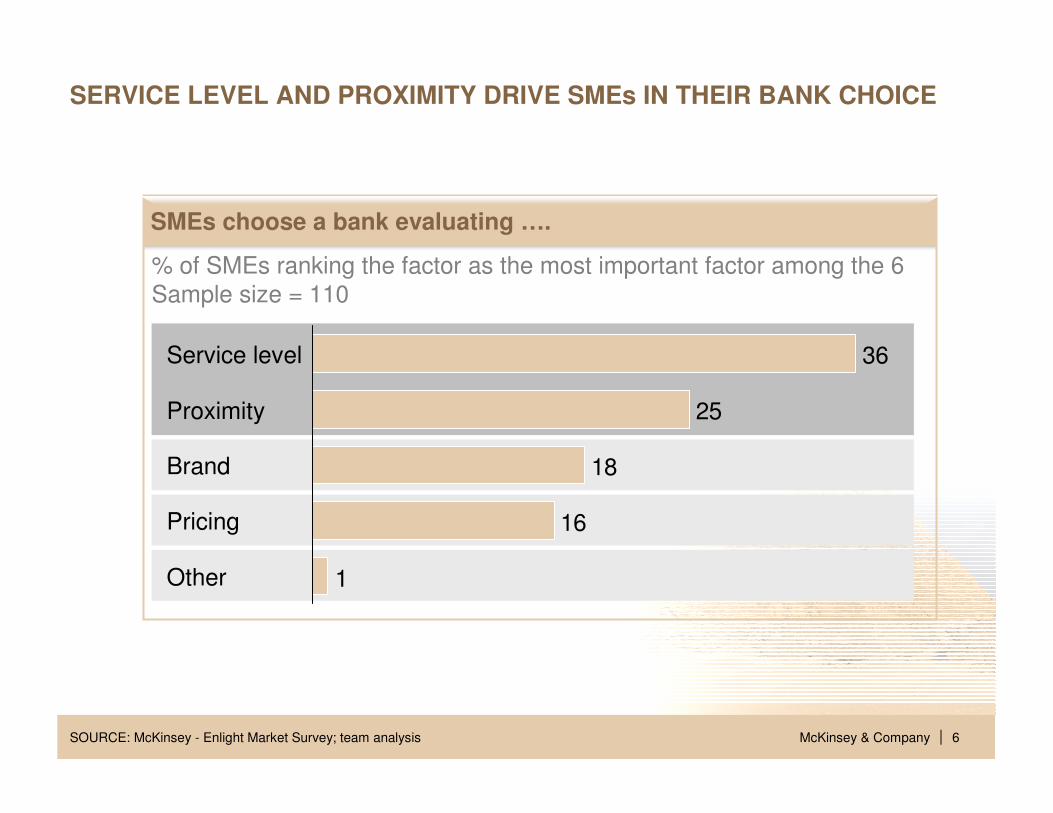

Other

Pricing

Brand

Proximity

Service level

SMEs choose a bank evaluating ….

% of SMEs ranking the factor as the most important factor among the 6

Sample size = 110

SERVICE LEVEL AND PROXIMITY DRIVE SMEs IN THEIR BANK CHOICE

SOURCE: McKinsey - Enlight Market Survey; team analysis

McKinsey & Company 7|

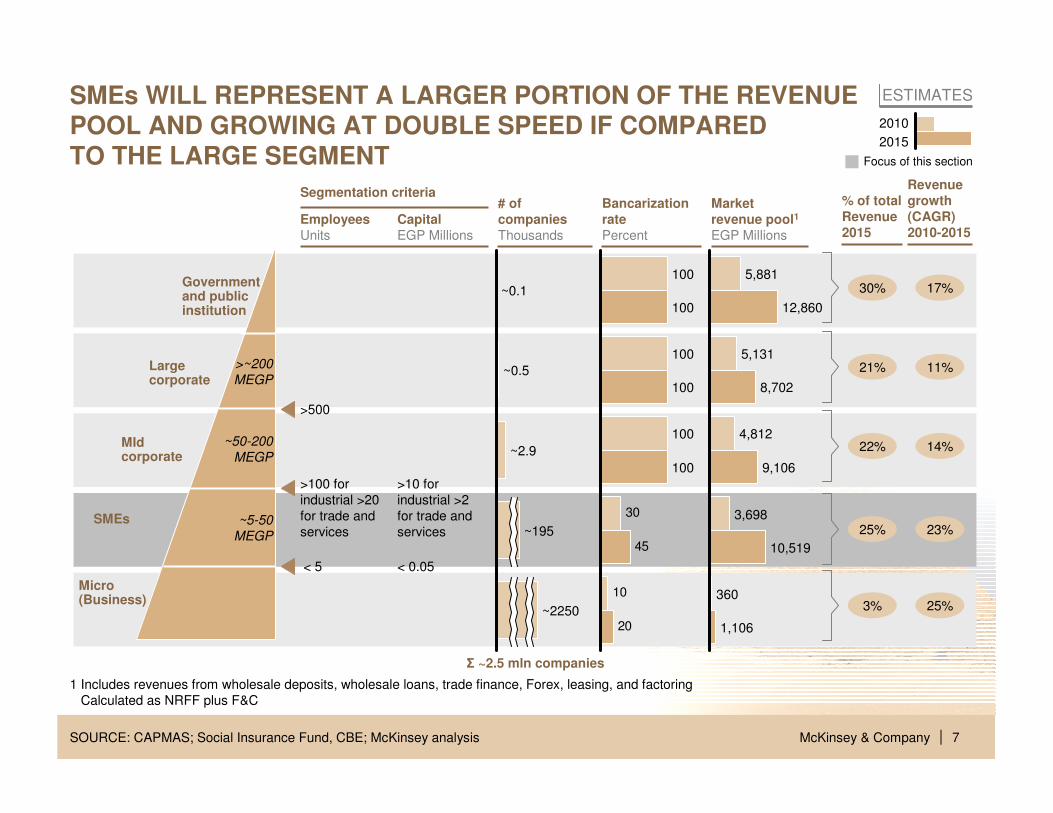

~2250

~195

~2.9

~0.5

~0.1

Σ ~2.5 mln companies

< 5

>100 for

industrial >20

for trade and

services

SOURCE: CAPMAS; Social Insurance Fund, CBE; McKinsey analysis

>10 for

industrial >2

for trade and

services

< 0.05

SMEs WILL REPRESENT A LARGER PORTION OF THE REVENUE POOL AND GROWING AT DOUBLE SPEED IF COMPARED TO THE LARGE SEGMENT

1 Includes revenues from wholesale deposits, wholesale loans, trade finance, Forex, leasing, and factoring

Calculated as NRFF plus F&C

10

30

20

45

100

100

100

100

100

100

1,106

360

10,519

3,698

9,106

4,812

8,702

5,131

12,860

5,881

2010

2015

>500

Government and public institution

Large corporate

SMEs

Micro (Business)

MIdcorporate

>~200

MEGP

~50-200

MEGP

~5-50

MEGP

Focus of this section

17%

11%

14%

23%

25%

30%

21%

22%

25%

3%

ESTIMATES

Revenue growth (CAGR) 2010-2015

% of total Revenue 2015

# of companiesThousands

Market revenue pool1

EGP Millions

BancarizationratePercent

Segmentation criteria

CapitalEGP Millions

EmployeesUnits

McKinsey & Company 8|SOURCE: McKinsey

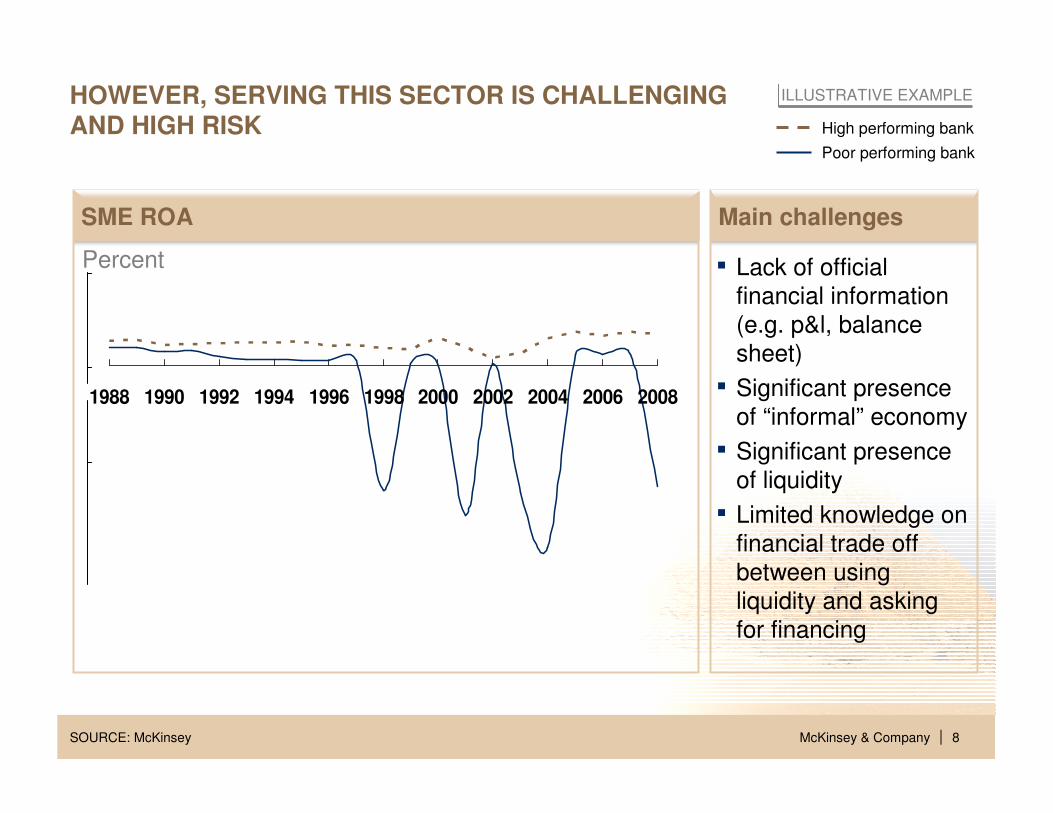

HOWEVER, SERVING THIS SECTOR IS CHALLENGING AND HIGH RISK High performing bank

Poor performing bank

ILLUSTRATIVE EXAMPLE

SME ROA

Percent

1988 1990 1992 1994 1996 1998 2000 2002 2004 2006 2008

Main challenges

▪ Lack of official

financial information

(e.g. p&l, balance

sheet)

▪ Significant presence

of “informal” economy

▪ Significant presence

of liquidity

▪ Limited knowledge on

financial trade off

between using

liquidity and asking

for financing

McKinsey & Company 9|

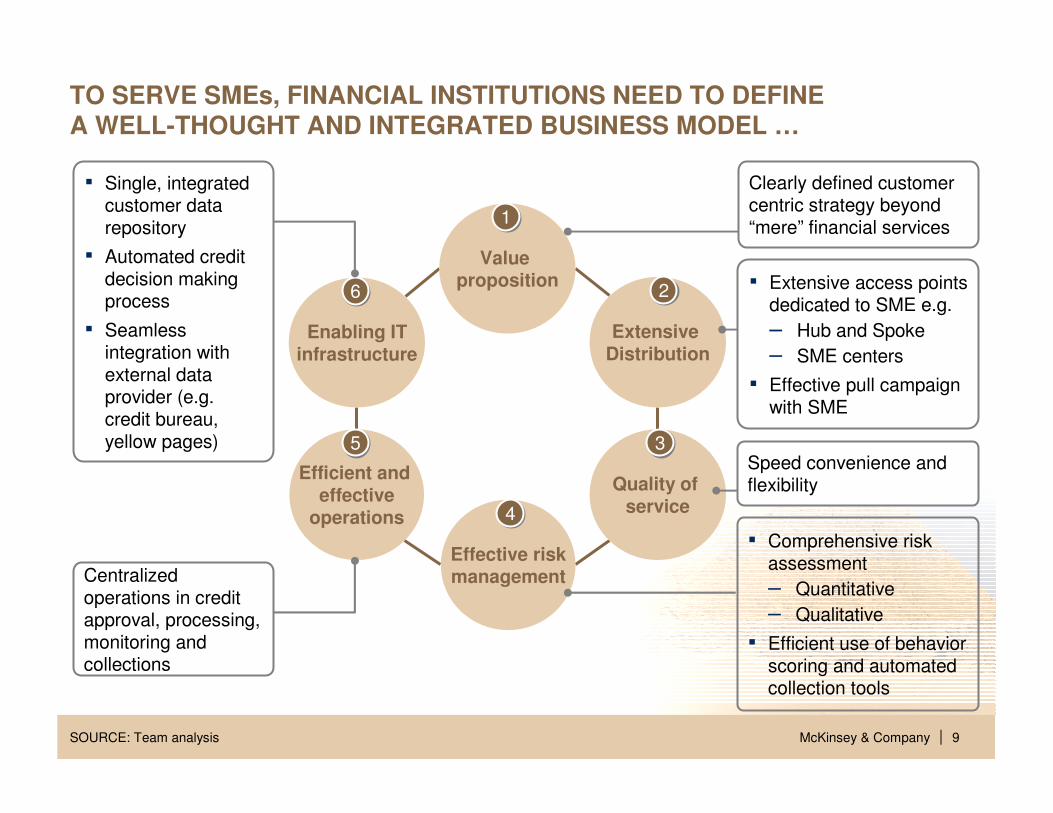

▪ Extensive access points dedicated to SME e.g.

– Hub and Spoke

– SME centers

▪ Effective pull campaign with SME

TO SERVE SMEs, FINANCIAL INSTITUTIONS NEED TO DEFINEA WELL-THOUGHT AND INTEGRATED BUSINESS MODEL …

SOURCE: Team analysis

Value proposition

Effective riskmanagement

Enabling ITinfrastructure

Extensive Distribution

Efficient and effective

operations

Quality of service

11

22

33

44

55

66

Clearly defined customer centric strategy beyond “mere” financial services

Speed convenience and flexibility

Centralized operations in credit approval, processing, monitoring and collections

▪ Single, integrated customer data repository

▪ Automated credit decision making process

▪ Seamless integration with external data provider (e.g. credit bureau, yellow pages)

▪ Comprehensive risk assessment

– Quantitative

– Qualitative

▪ Efficient use of behavior scoring and automated collection tools

McKinsey & Company 10|

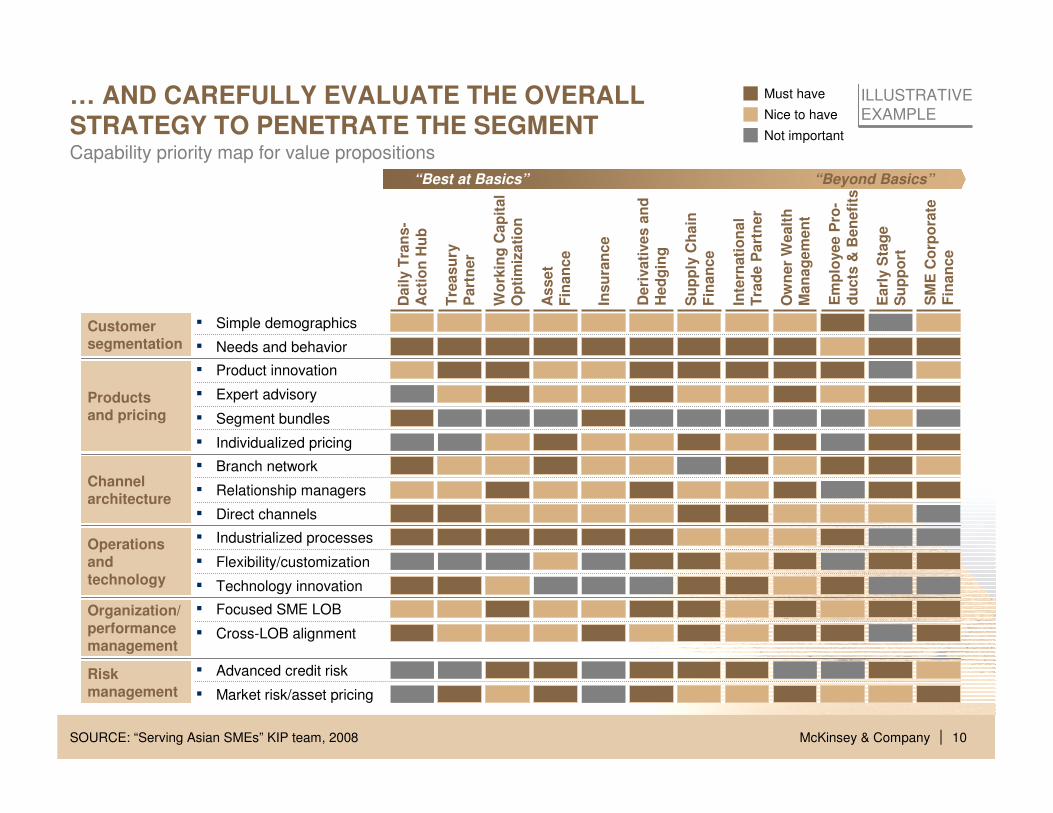

… AND CAREFULLY EVALUATE THE OVERALL STRATEGY TO PENETRATE THE SEGMENT

SOURCE: “Serving Asian SMEs” KIP team, 2008

Capability priority map for value propositions

Must have

Nice to have

Not important

ILLUSTRATIVE

EXAMPLE

Dail

y T

ran

s-

Acti

on

Hu

b

Tre

asu

ry

Part

ner

Wo

rkin

g C

ap

ital

Op

tim

izati

on

As

set

Fin

an

ce

Insu

ran

ce

Inte

rnati

on

al

Tra

de P

art

ner

Ow

ner

Wealt

hM

an

ag

em

en

t

Em

plo

yee P

ro-

du

cts

& B

en

efi

ts

Su

pp

ly C

hain

Fin

an

ce

Earl

y S

tag

eS

up

po

rt

SM

E C

orp

ora

teF

inan

ce

Deri

vati

ves a

nd

H

ed

gin

g

“Best at Basics” “Beyond Basics”

Risk

management

▪ Advanced credit risk

▪ Market risk/asset pricing

Organization/

performancemanagement

▪ Focused SME LOB

▪ Cross-LOB alignment

Operationsand

technology▪ Flexibility/customization

▪ Industrialized processes

▪ Technology innovation

Channel architecture

▪ Relationship managers

▪ Branch network

▪ Direct channels

Productsand pricing

▪ Expert advisory

▪ Segment bundles

▪ Product innovation

▪ Individualized pricing

Customersegmentation

▪ Simple demographics

▪ Needs and behavior

McKinsey & Company 11|

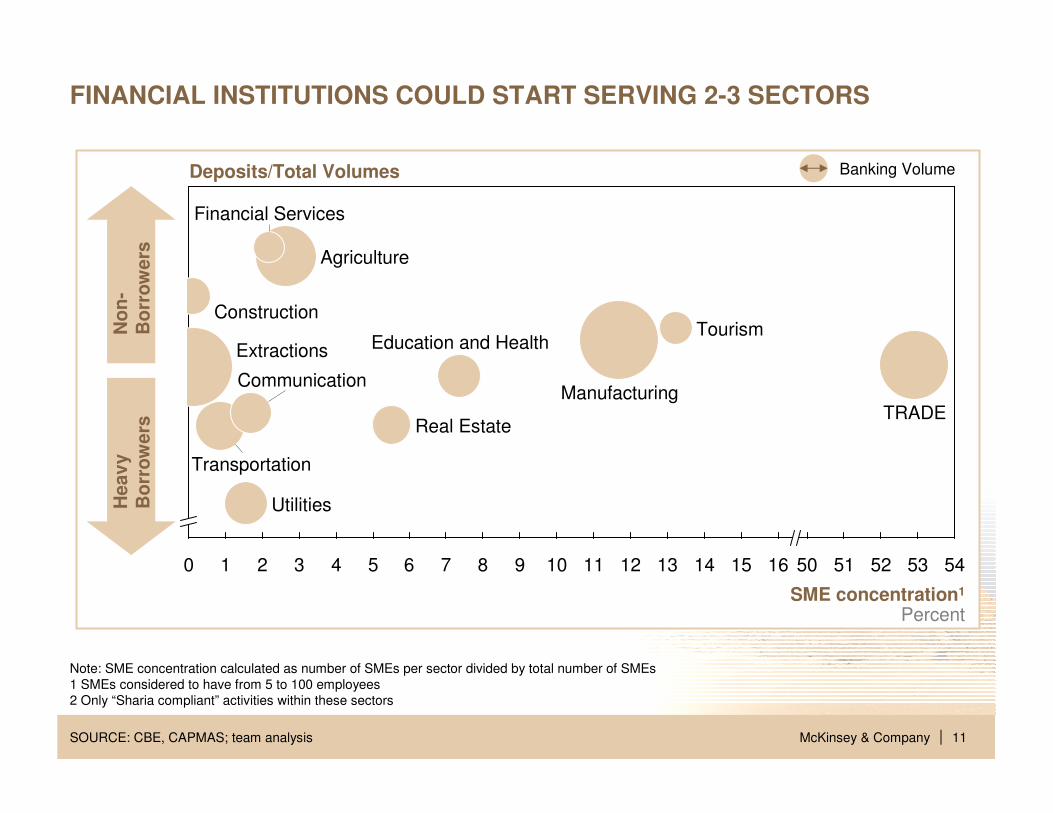

SME concentration1

Percent

5453524 5 6 7 81 10 11 12 13 14 15 16 50 5120

Utilities

Real Estate

Communication

Financial Services

Tourism

9

Education and Health

Construction

TRADE

Extractions

Agriculture

Manufacturing

3

Transportation

SOURCE: CBE, CAPMAS; team analysis

FINANCIAL INSTITUTIONS COULD START SERVING 2-3 SECTORS

Banking Volume

Note: SME concentration calculated as number of SMEs per sector divided by total number of SMEs

1 SMEs considered to have from 5 to 100 employees

2 Only “Sharia compliant” activities within these sectors

No

n-

Bo

rro

wers

Heav

y

Bo

rro

wers

Deposits/Total Volumes

McKinsey & Company 12|

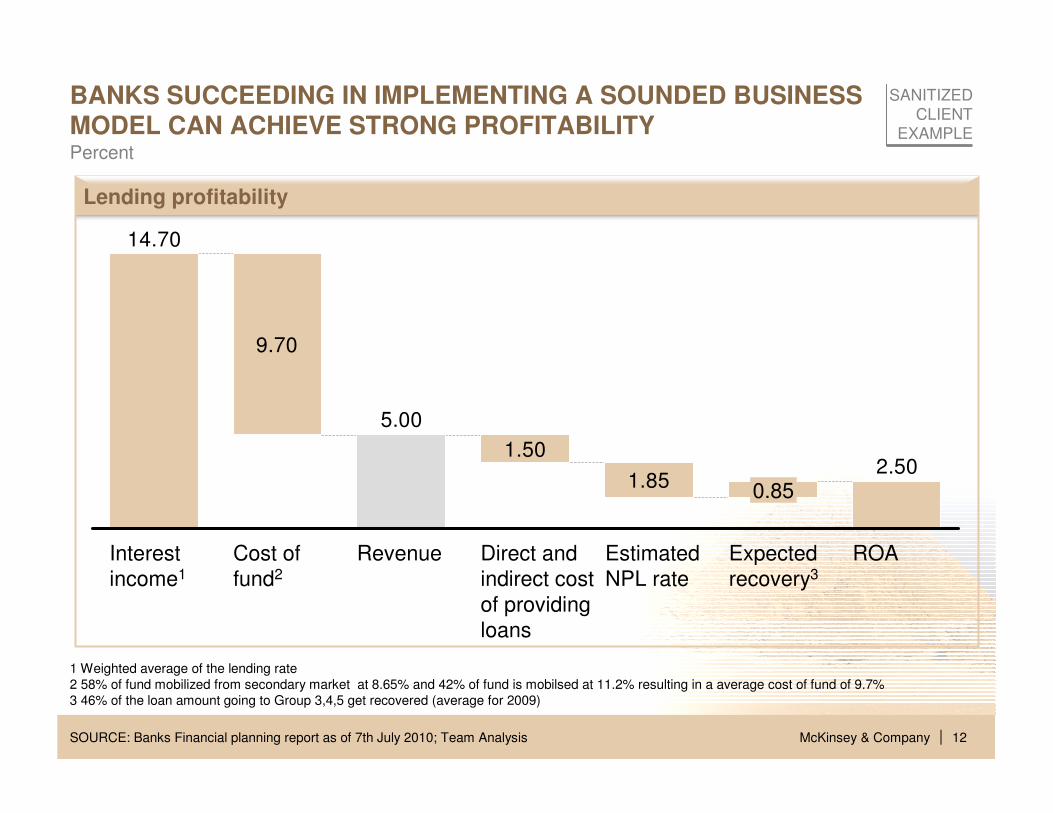

BANKS SUCCEEDING IN IMPLEMENTING A SOUNDED BUSINESS MODEL CAN ACHIEVE STRONG PROFITABILITY

1 Weighted average of the lending rate

2 58% of fund mobilized from secondary market at 8.65% and 42% of fund is mobilsed at 11.2% resulting in a average cost of fund of 9.7%

3 46% of the loan amount going to Group 3,4,5 get recovered (average for 2009)

SOURCE: Banks Financial planning report as of 7th July 2010; Team Analysis

Lending profitability

9.70

1.50

1.852.50

5.00

14.70

ROAExpected

recovery3

0.85

Estimated

NPL rate

Direct and

indirect cost

of providing

loans

RevenueCost of

fund2

Interest

income1

Percent

SANITIZED

CLIENT

EXAMPLE