Embed Size (px)

Citation preview

SME Finance – the way forward

Matthew Gamser Head, SME Finance Forum

Dubai, May 2013

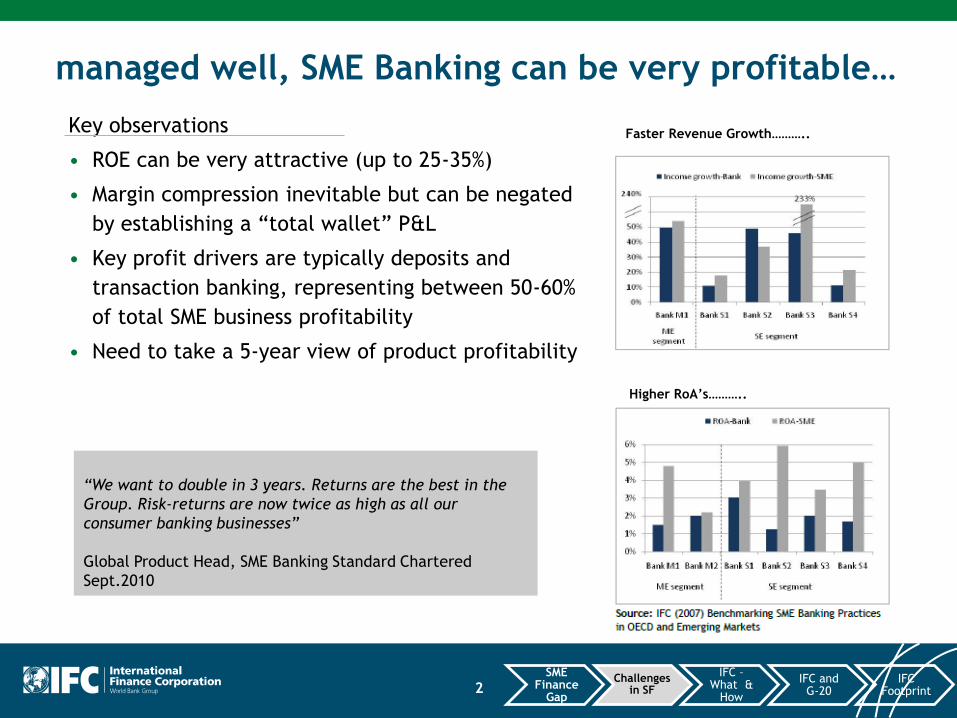

managed well, SME Banking can be very profitable…

Key observations

• ROE can be very attractive (up to 25-35%)

• Margin compression inevitable but can be negated

by establishing a “total wallet” P&L

• Key profit drivers are typically deposits and

transaction banking, representing between 50-60%

of total SME business profitability

• Need to take a 5-year view of product profitability

“We want to double in 3 years. Returns are the best in the

Group. Risk-returns are now twice as high as all our

consumer banking businesses”

Global Product Head, SME Banking Standard Chartered

Sept.2010

Faster Revenue Growth………..

Higher RoA’s………..

2 SME

Finance Gap

Challenges in SF

IFC – What &

How

IFC and G-20

IFC Footprint

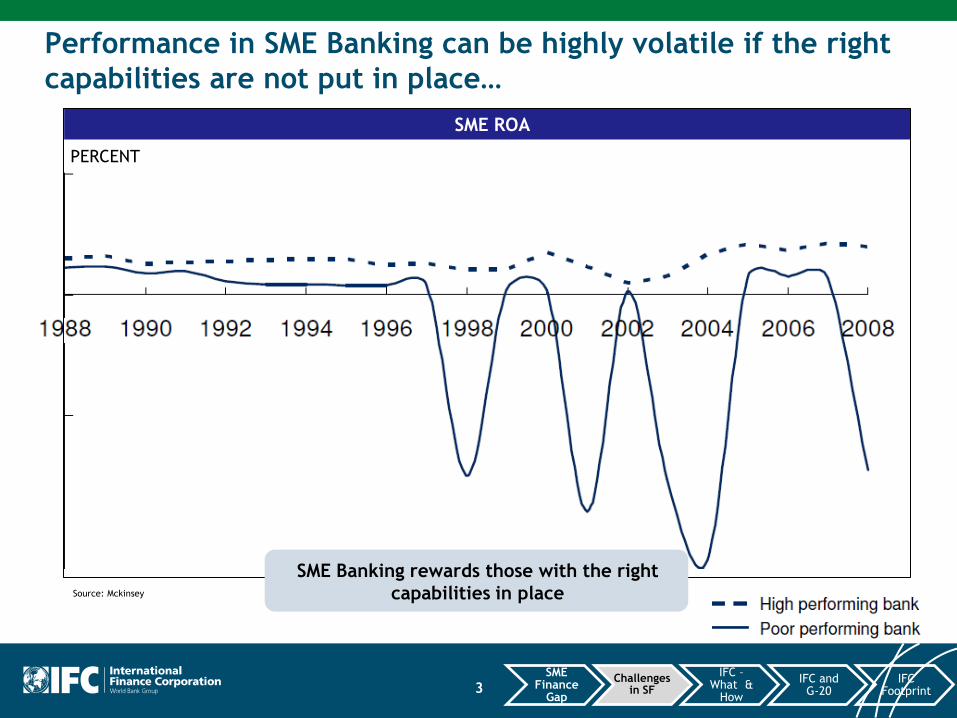

Performance in SME Banking can be highly volatile if the right

capabilities are not put in place…

SME ROA

PERCENT

SME Banking rewards those with the right

capabilities in place Source: Mckinsey

3 SME

Finance Gap

Challenges in SF

IFC – What &

How

IFC and G-20

IFC Footprint

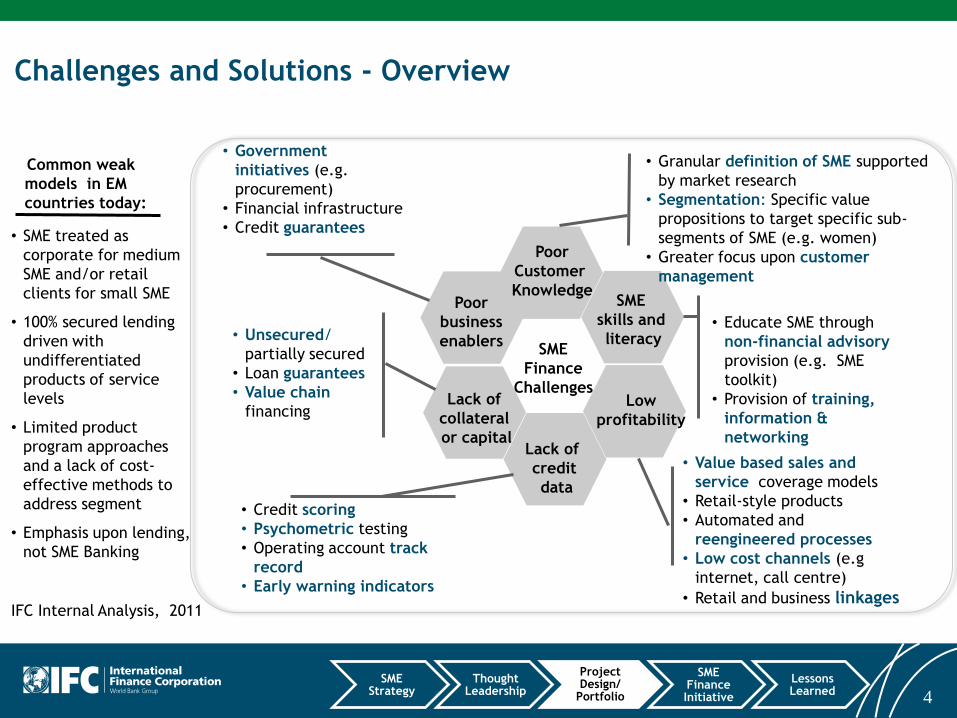

Challenges and Solutions - Overview

Poor

Customer

Knowledge Poor

business

enablers

Lack of

collateral

or capital Lack of

credit

data

Low

profitability

SME

skills and

literacy

• Government

initiatives (e.g.

procurement)

• Financial infrastructure

• Credit guarantees

• Unsecured/

partially secured

• Loan guarantees

• Value chain

financing

• Credit scoring

• Psychometric testing

• Operating account track

record

• Early warning indicators

• Value based sales and

service coverage models

• Retail-style products

• Automated and

reengineered processes

• Low cost channels (e.g

internet, call centre)

• Retail and business linkages

• Educate SME through

non-financial advisory

provision (e.g. SME

toolkit)

• Provision of training,

information &

networking

• Granular definition of SME supported

by market research

• Segmentation: Specific value

propositions to target specific sub-

segments of SME (e.g. women)

• Greater focus upon customer

management

IFC Internal Analysis, 2011

SME

Finance

Challenges

• SME treated as

corporate for medium

SME and/or retail

clients for small SME

• 100% secured lending

driven with

undifferentiated

products of service

levels

• Limited product

program approaches

and a lack of cost-

effective methods to

address segment

• Emphasis upon lending,

not SME Banking

Common weak

models in EM

countries today:

4 SME

Strategy Thought

Leadership

Project Design/

Portfolio

SME Finance Initiative

Lessons Learned

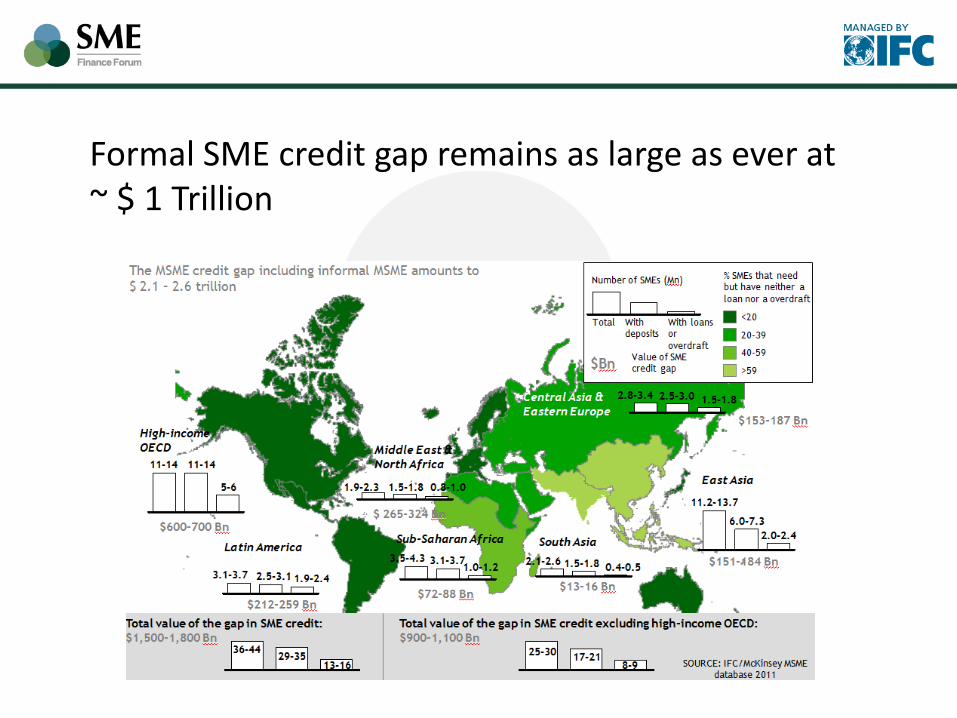

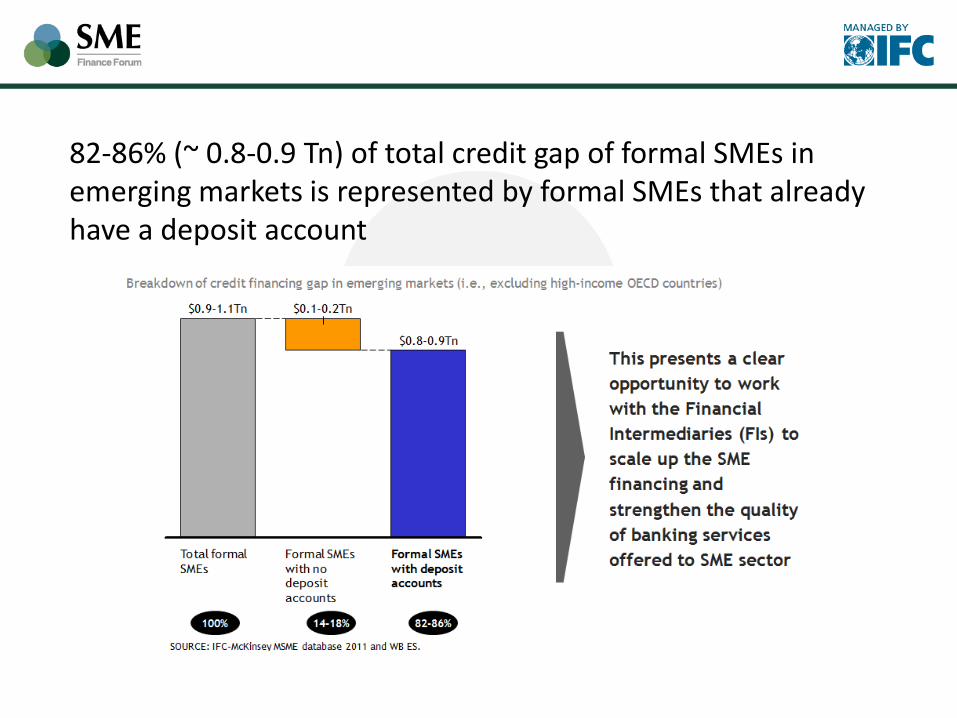

Formal SME credit gap remains as large as ever at ~ $ 1 Trillion

82-86% (~ 0.8-0.9 Tn) of total credit gap of formal SMEs in emerging markets is represented by formal SMEs that already have a deposit account

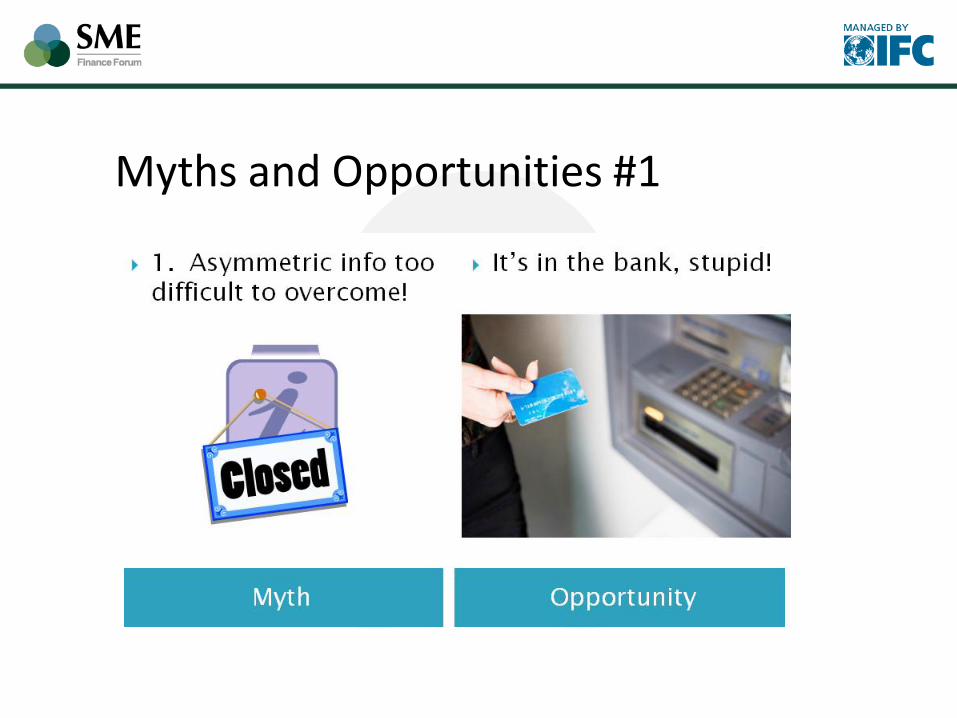

Myths and Opportunities #1

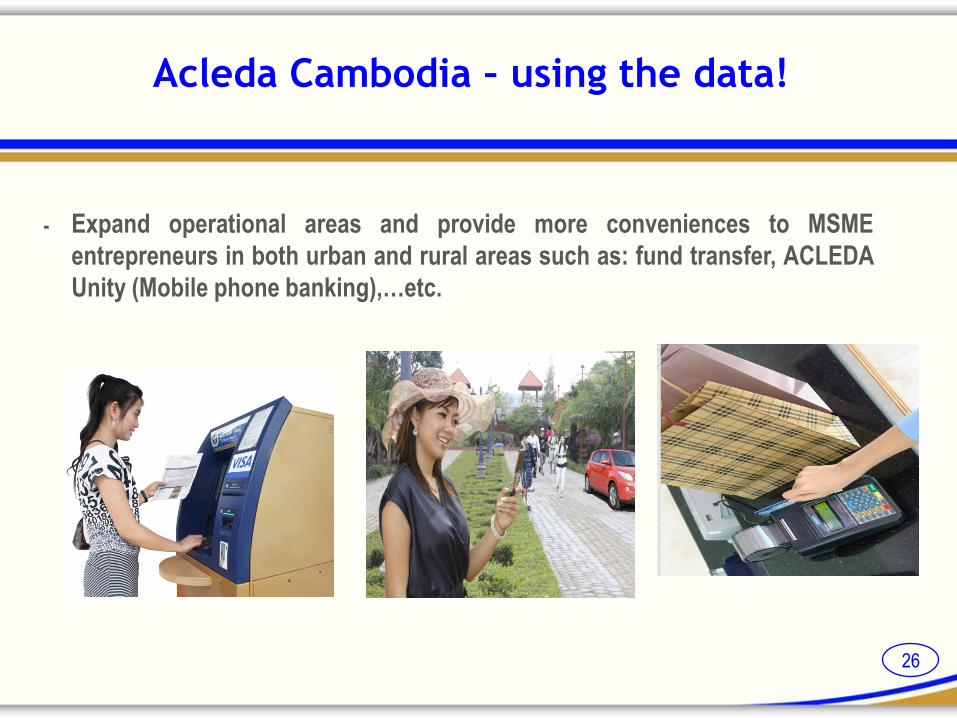

Acleda Cambodia – using the data!

- Expand operational areas and provide more conveniences to MSME

entrepreneurs in both urban and rural areas such as: fund transfer, ACLEDA

Unity (Mobile phone banking),…etc.

26

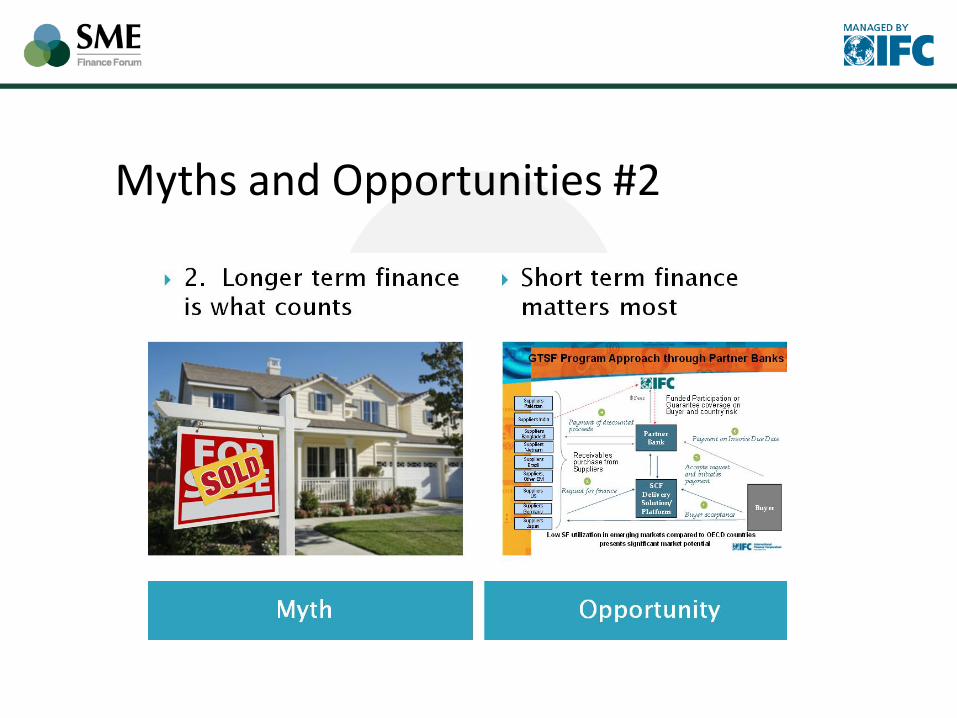

Myths and Opportunities #2

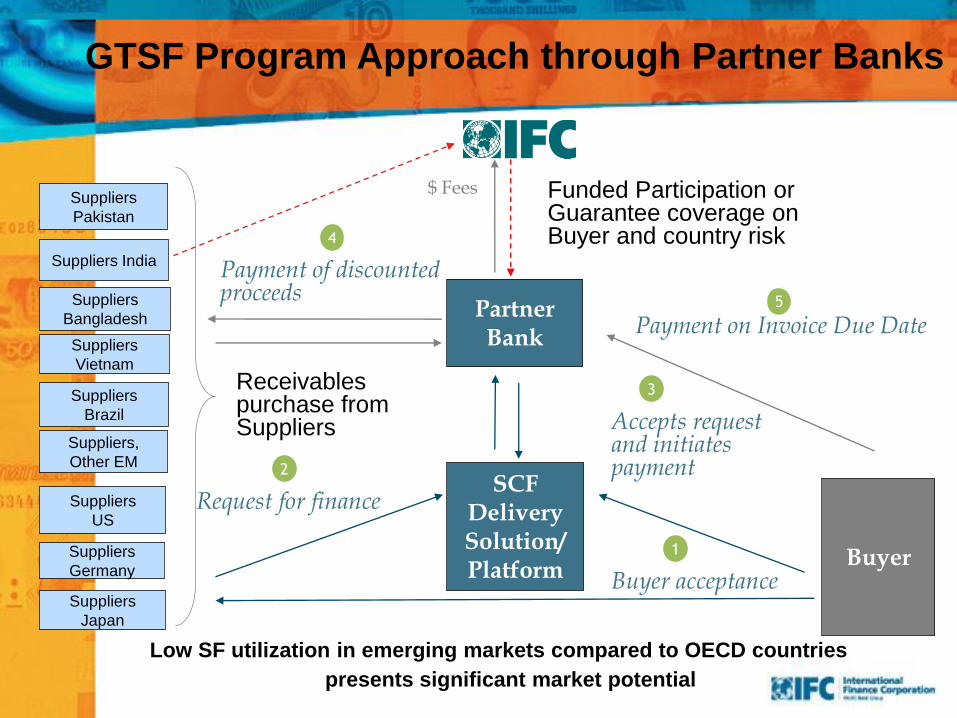

Suppliers

Pakistan

Suppliers India

Suppliers

Bangladesh

Suppliers

Vietnam

Suppliers

Brazil

Buyer

SCF Delivery Solution/ Platform

Receivables purchase from Suppliers

Suppliers,

Other EM

Suppliers

US

Suppliers

Germany

Suppliers

Japan

Buyer acceptance

Payment of discounted proceeds

Request for finance

Payment on Invoice Due Date

Accepts request and initiates payment

Funded Participation or Guarantee coverage on Buyer and country risk

$ Fees

GTSF Program Approach through Partner Banks

Partner Bank

1

2

3

4

5

Low SF utilization in emerging markets compared to OECD countries

presents significant market potential

Myth Opportunity

3. It’s all about banks Banks matter, but so do partnerships - with real sector large firms, and others.

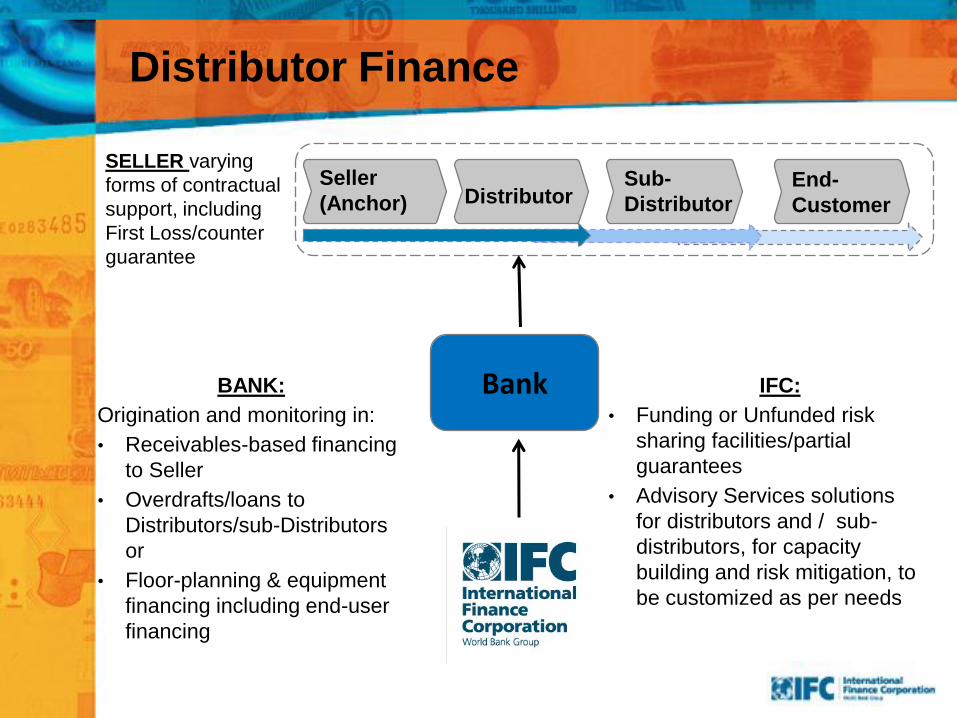

Distributor Finance

IFC:

• Funding or Unfunded risk

sharing facilities/partial

guarantees

• Advisory Services solutions

for distributors and / sub-

distributors, for capacity

building and risk mitigation, to

be customized as per needs

BANK:

Origination and monitoring in:

• Receivables-based financing

to Seller

• Overdrafts/loans to

Distributors/sub-Distributors

or

• Floor-planning & equipment

financing including end-user

financing

End-

Customer

SELLER varying

forms of contractual

support, including

First Loss/counter

guarantee

Distributor Seller

(Anchor)

Sub-

Distributor

Bank

and

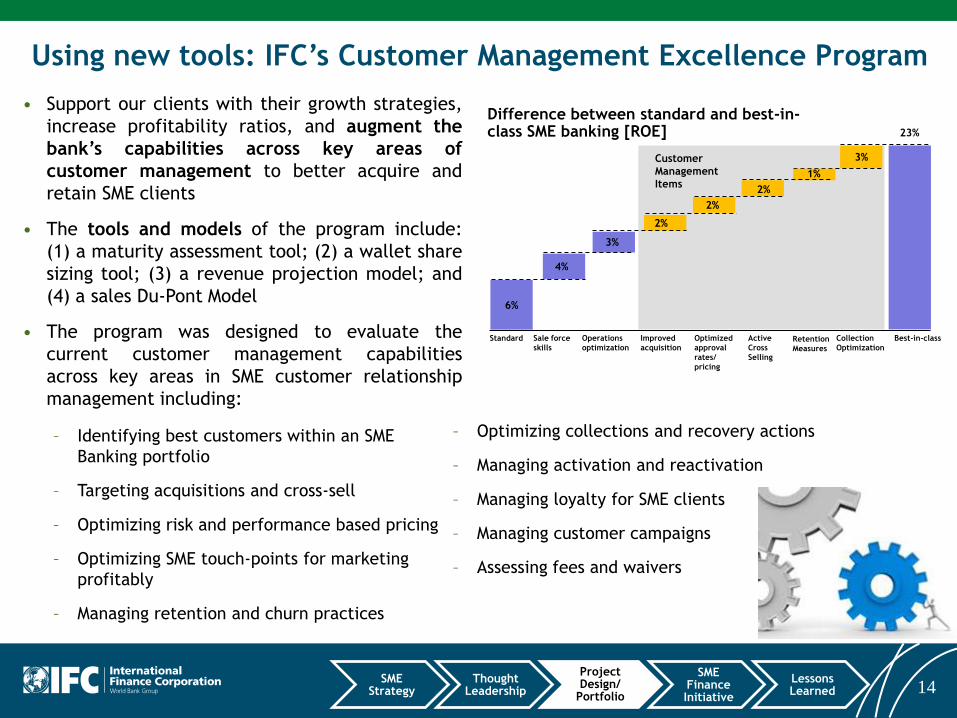

Using new tools: IFC’s Customer Management Excellence Program

• Support our clients with their growth strategies,

increase profitability ratios, and augment the

bank’s capabilities across key areas of

customer management to better acquire and

retain SME clients

• The tools and models of the program include:

(1) a maturity assessment tool; (2) a wallet share

sizing tool; (3) a revenue projection model; and

(4) a sales Du-Pont Model

• The program was designed to evaluate the

current customer management capabilities

across key areas in SME customer relationship

management including:

– Identifying best customers within an SME

Banking portfolio

– Targeting acquisitions and cross-sell

– Optimizing risk and performance based pricing

– Optimizing SME touch-points for marketing

profitably

– Managing retention and churn practices

– Optimizing collections and recovery actions

– Managing activation and reactivation

– Managing loyalty for SME clients

– Managing customer campaigns

– Assessing fees and waivers

3%

23%

1%

2%

2%

2%

3%

4%

6%

Customer

Management

Items

Standard Sale force

skills

Operations

optimization

Improved

acquisition

Optimized

approval

rates/

pricing

Active

Cross

Selling

Retention

Measures

Collection

Optimization

Best-in-class

Difference between standard and best-in-class SME banking [ROE]

14 SME

Strategy Thought

Leadership

Project Design/

Portfolio

SME Finance Initiative

Lessons Learned

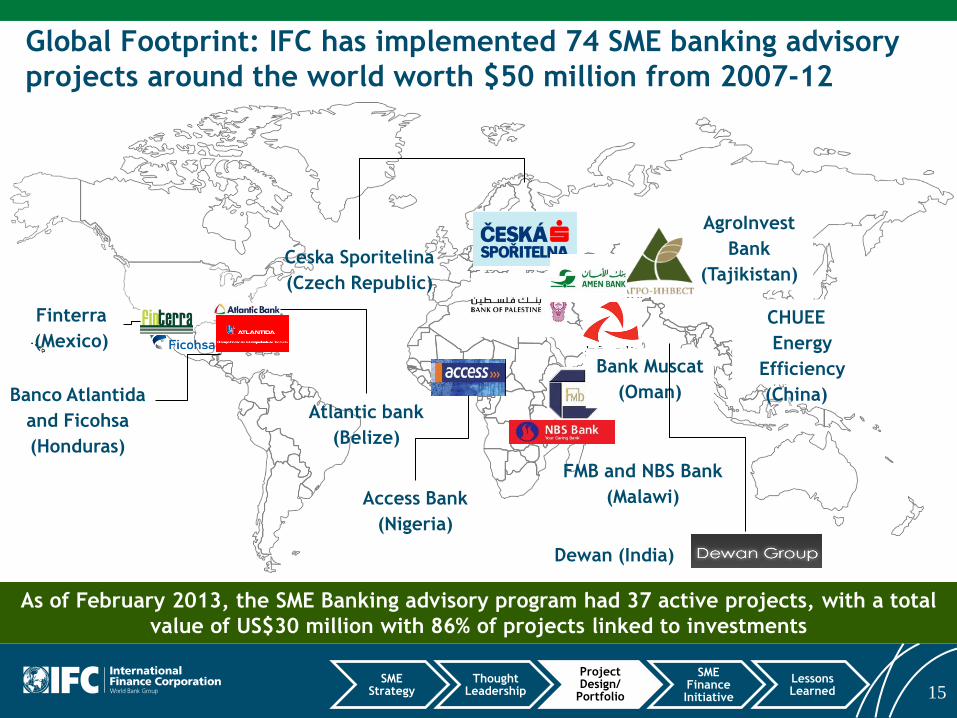

As of February 2013, the SME Banking advisory program had 37 active projects, with a total

value of US$30 million with 86% of projects linked to investments

Global Footprint: IFC has implemented 74 SME banking advisory

projects around the world worth $50 million from 2007-12

Ceska Sporitelina

(Czech Republic)

FMB and NBS Bank

(Malawi)

Bank Muscat

(Oman)

Access Bank

(Nigeria)

AgroInvest

Bank

(Tajikistan)

CHUEE

Energy

Efficiency

(China)

Dewan (India)

Finterra

(Mexico)

Banco Atlantida

and Ficohsa

(Honduras)

Atlantic bank

(Belize)

15 SME

Strategy Thought

Leadership

Project Design/

Portfolio

SME Finance Initiative

Lessons Learned

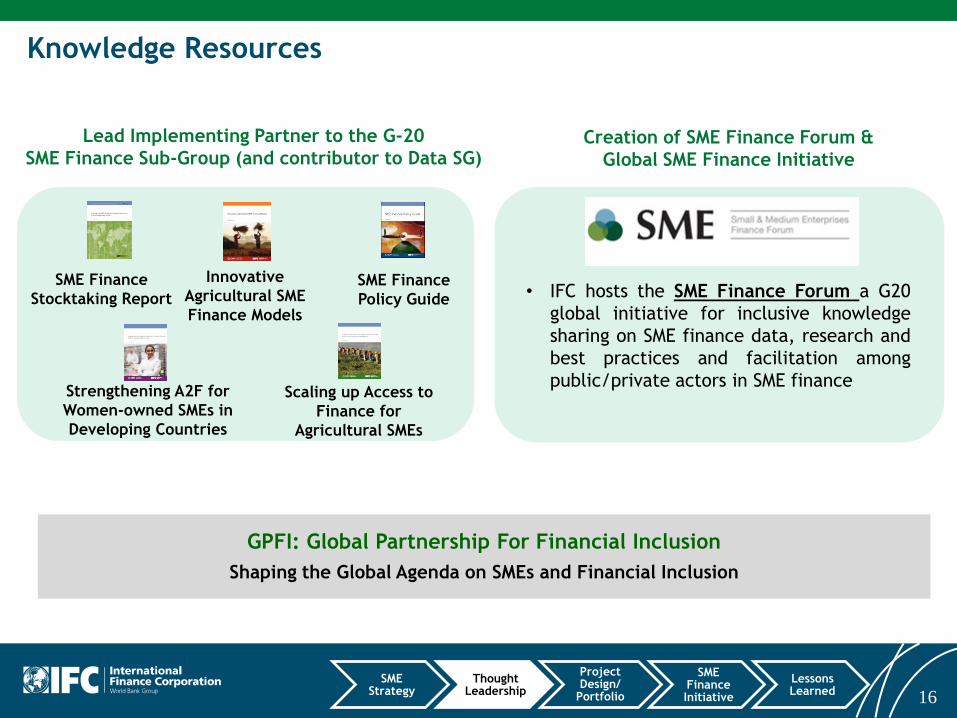

Knowledge Resources

16

Creation of SME Finance Forum &

Global SME Finance Initiative

• IFC hosts the SME Finance Forum a G20

global initiative for inclusive knowledge

sharing on SME finance data, research and

best practices and facilitation among

public/private actors in SME finance

Lead Implementing Partner to the G-20

SME Finance Sub-Group (and contributor to Data SG)

SME Finance

Stocktaking Report

Innovative

Agricultural SME

Finance Models

Strengthening A2F for

Women-owned SMEs in

Developing Countries

SME Finance

Policy Guide

Scaling up Access to

Finance for

Agricultural SMEs

GPFI: Global Partnership For Financial Inclusion

Shaping the Global Agenda on SMEs and Financial Inclusion

SME Strategy

Thought Leadership

Project Design/

Portfolio

SME Finance Initiative

Lessons Learned

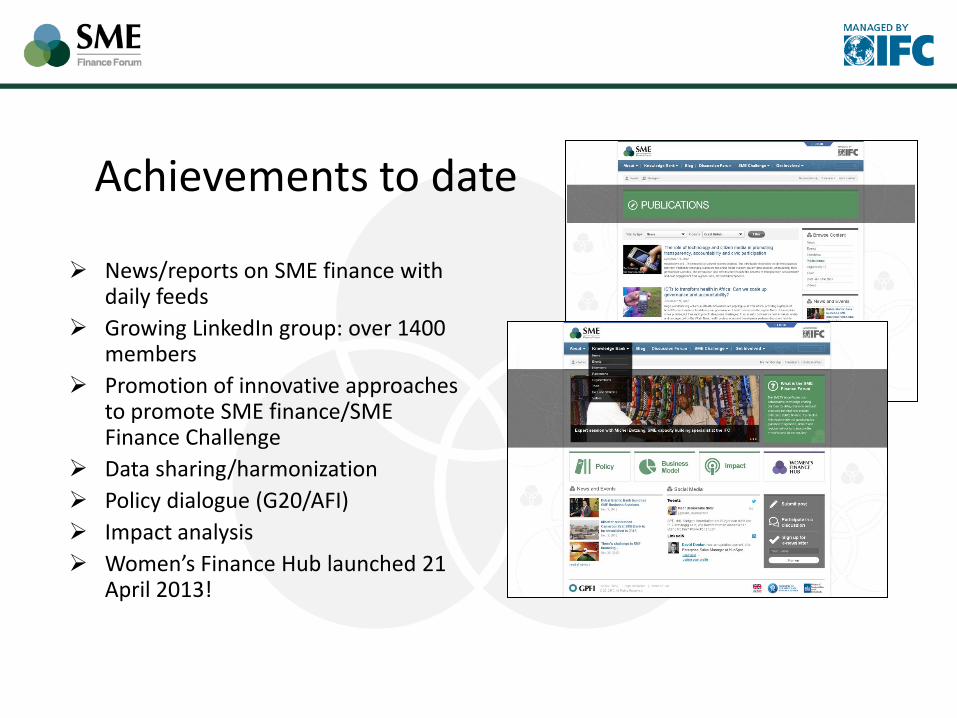

Achievements to date

News/reports on SME finance with daily feeds

Growing LinkedIn group: over 1400 members

Promotion of innovative approaches to promote SME finance/SME Finance Challenge

Data sharing/harmonization

Policy dialogue (G20/AFI)

Impact analysis

Women’s Finance Hub launched 21 April 2013!

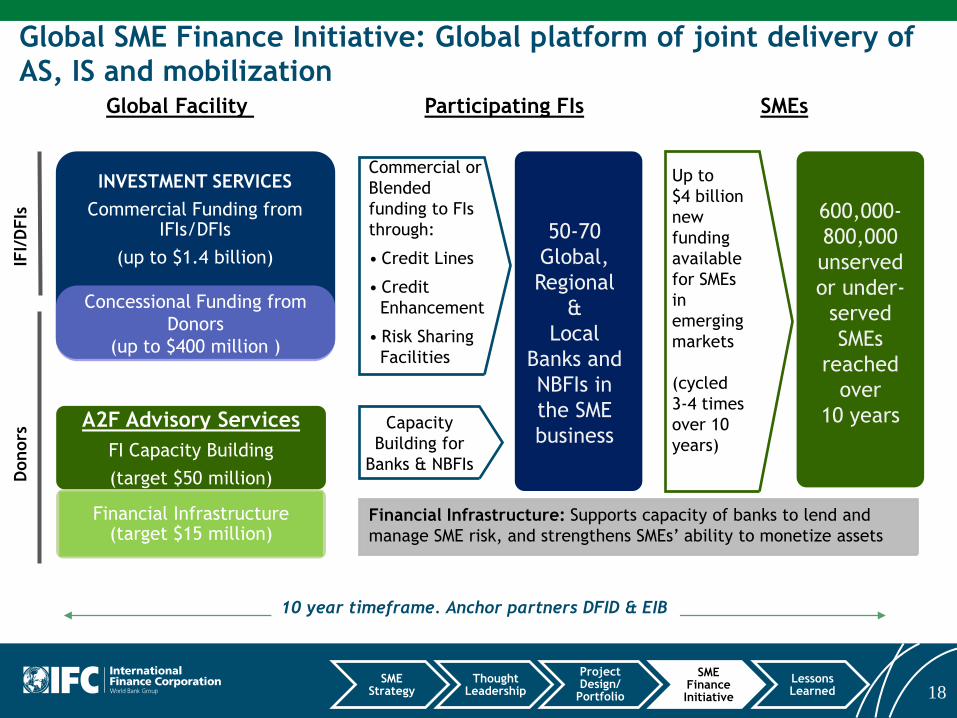

600,000-

800,000

unserved

or under-

served

SMEs

reached

over

10 years

Global SME Finance Initiative: Global platform of joint delivery of AS, IS and mobilization

Capacity

Building for

Banks & NBFIs

Donors

Financial Infrastructure: Supports capacity of banks to lend and

manage SME risk, and strengthens SMEs’ ability to monetize assets

IFI/

DFIs

10 year timeframe. Anchor partners DFID & EIB

INVESTMENT SERVICES

Commercial Funding from IFIs/DFIs

(up to $1.4 billion)

A2F Advisory Services

FI Capacity Building

(target $50 million)

Financial Infrastructure (target $15 million)

Global Facility Participating FIs SMEs

Concessional Funding from

Donors

(up to $400 million )

Commercial or

Blended

funding to FIs

through:

• Credit Lines

• Credit

Enhancement

• Risk Sharing

Facilities

50-70

Global,

Regional

&

Local

Banks and

NBFIs in

the SME

business

Up to

$4 billion

new

funding

available

for SMEs

in

emerging

markets

(cycled

3-4 times

over 10

years)

18 SME

Strategy Thought

Leadership

Project Design/

Portfolio

SME Finance Initiative

Lessons Learned

On the Web at www.smefinanceforum.org

LinkedIn Group: SME Finance Forum

Twitter: @SMEFinanceForum

Annexes

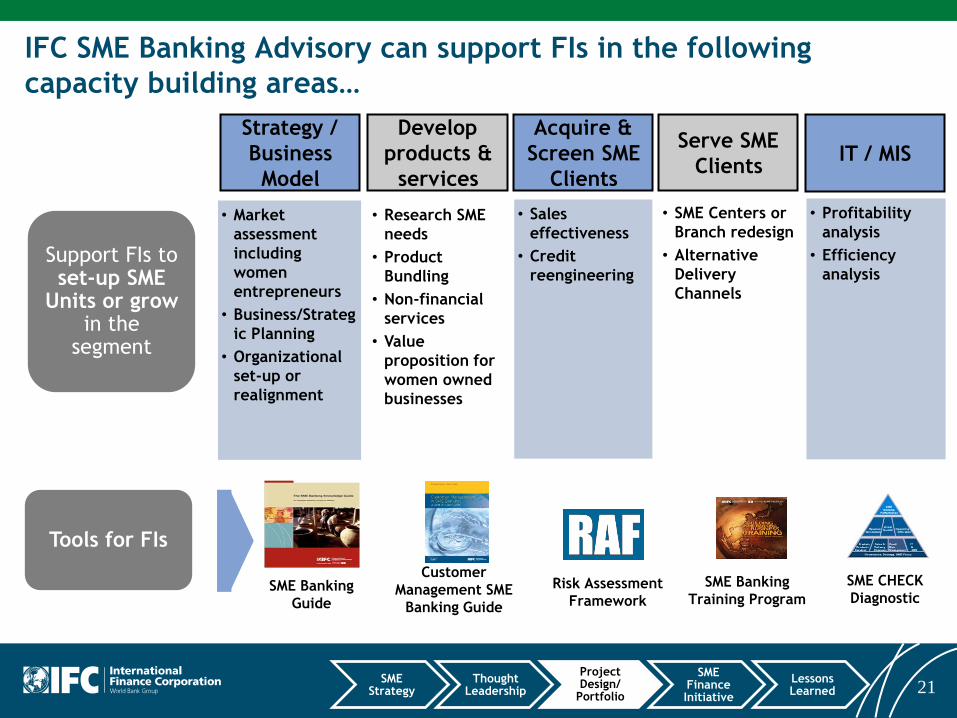

IFC SME Banking Advisory can support FIs in the following

capacity building areas…

Develop

products &

services

Acquire &

Screen SME

Clients

Serve SME

Clients IT / MIS

Strategy /

Business

Model

• Market

assessment

including

women

entrepreneurs

• Business/Strateg

ic Planning

• Organizational

set-up or

realignment

Support FIs to set-up SME

Units or grow in the

segment

• Research SME

needs

• Product

Bundling

• Non-financial

services

• Value

proposition for

women owned

businesses

• SME Centers or

Branch redesign

• Alternative

Delivery

Channels

• Profitability

analysis

• Efficiency

analysis

• Sales

effectiveness

• Credit

reengineering

21

SME Banking

Guide

SME Banking

Training Program Risk Assessment

Framework

Customer

Management SME

Banking Guide

SME CHECK

Diagnostic

Tools for FIs

SME Strategy

Thought Leadership

Project Design/

Portfolio

SME Finance Initiative

Lessons Learned

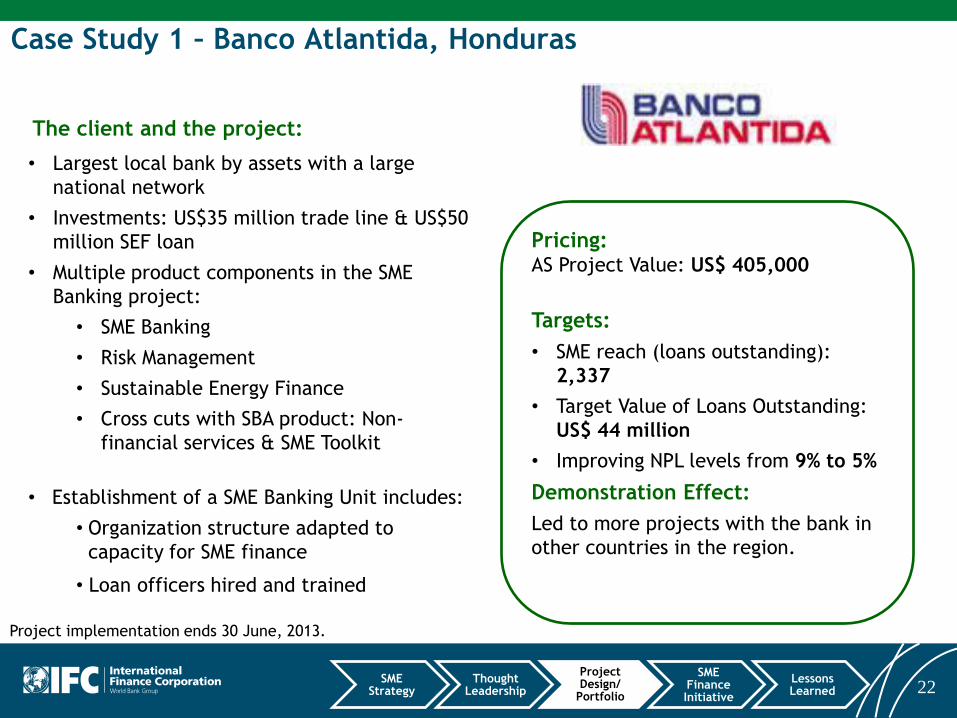

Case Study 1 – Banco Atlantida, Honduras

The client and the project:

22

Pricing: AS Project Value: US$ 405,000

Targets:

• SME reach (loans outstanding):

2,337

• Target Value of Loans Outstanding:

US$ 44 million

• Improving NPL levels from 9% to 5%

Demonstration Effect:

Led to more projects with the bank in

other countries in the region.

Project implementation ends 30 June, 2013.

• Largest local bank by assets with a large

national network

• Investments: US$35 million trade line & US$50

million SEF loan

• Multiple product components in the SME

Banking project:

• SME Banking

• Risk Management

• Sustainable Energy Finance

• Cross cuts with SBA product: Non-

financial services & SME Toolkit

• Establishment of a SME Banking Unit includes:

• Organization structure adapted to

capacity for SME finance

• Loan officers hired and trained

SME Strategy

Thought Leadership

Project Design/

Portfolio

SME Finance Initiative

Lessons Learned

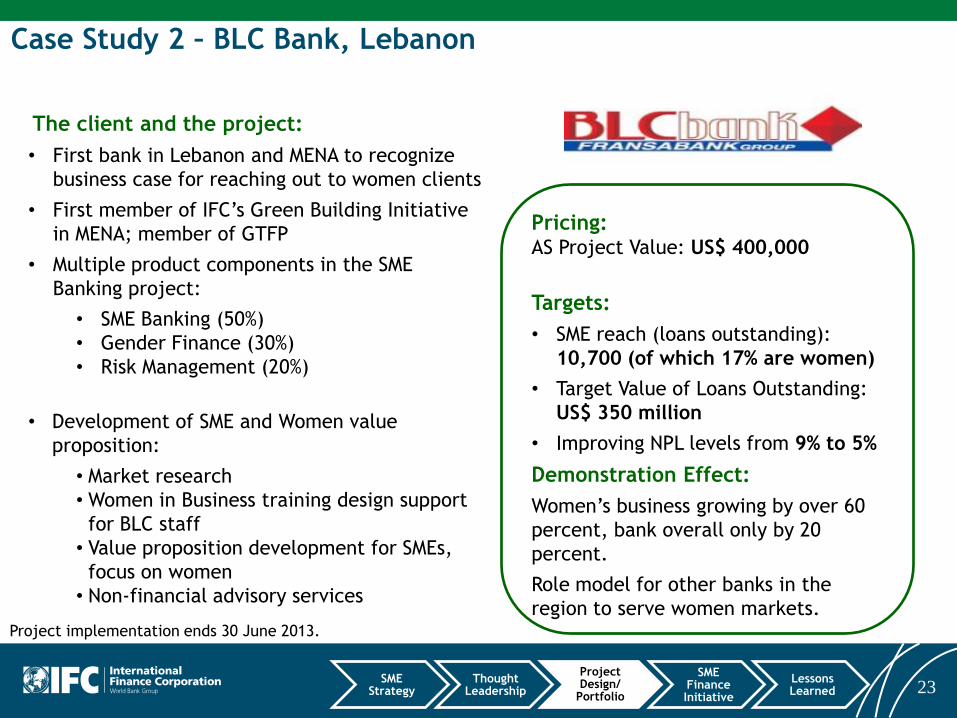

Case Study 2 – BLC Bank, Lebanon

The client and the project:

23

Pricing: AS Project Value: US$ 400,000

Targets:

• SME reach (loans outstanding):

10,700 (of which 17% are women)

• Target Value of Loans Outstanding:

US$ 350 million

• Improving NPL levels from 9% to 5%

Demonstration Effect:

Women’s business growing by over 60

percent, bank overall only by 20

percent.

Role model for other banks in the

region to serve women markets.

Project implementation ends 30 June 2013.

• First bank in Lebanon and MENA to recognize

business case for reaching out to women clients

• First member of IFC’s Green Building Initiative

in MENA; member of GTFP

• Multiple product components in the SME

Banking project:

• SME Banking (50%)

• Gender Finance (30%)

• Risk Management (20%)

• Development of SME and Women value

proposition:

• Market research

• Women in Business training design support

for BLC staff

• Value proposition development for SMEs,

focus on women

• Non-financial advisory services

SME Strategy

Thought Leadership

Project Design/

Portfolio

SME Finance Initiative

Lessons Learned

Case Study 3 - BINHAI RURAL COMMERCIAL BANK (BRCB)

• Formed 2007 through consolidation of two existing rural cooperative banks and

one rural credit union in the Tianjin Binhai New District

• IFC committed US$32 million in equity and a 3-year comprehensive advisory

program

corporate governance, risk management, internal controls, and lending to SMEs

• As of December 2008, the Bank had 8,895 SME loans worth US$765.5 million

Increased its SME loan portfolio by 84 percent in number and by 49 percent in volume

from 2007 to 2008

“Over the past year, IFC provided training and advisory services and played an

active role at the Board level. These are instrumental in helping the bank

implement its strategy, advance its SME and rural financing business, improve

staff quality as well as its corporate governance and risk management

situation.”

Fengchang Qi, Chairman, Binhai Rural Commercial Bank

24