Embed Size (px)

Citation preview

Institutional Structured Products – Fact or Fiction?

Bristol – 29th January 2015

1

• Background

• Facts – Complexity

• Facts – Liquidity

• Facts – Costs

• How We Work With Brewin Dolphin

• Appendix

Agenda

2

Institutional Structured Products - Background

3

The most difficult subjects can be explained to the most slow-witted man if he has

not formed any idea of them already; but the simplest thing cannot be made clear to

the most intelligent man if he is firmly persuaded that he knows already, without a

shadow of a doubt, what is laid before him.

Leo Tolstoy, 1897

“Spread bets on steroids”Martin Wheatley, Chief Executive and FCA Board Member

Fiction

4

Bad Press

5

Evolution of Market

6

Not originally related to the Retail Structured Product market Building Societies

Bank Branch

IFA distribution (latterly)

The Private Placement SP market started as an extension of the Investment

Trust market

Closely linked to the Asset Liability Matching market for institutional pension

schemes

Original participants were Merrill Lynch, Citi and Barclays around 2003

Discretionary Asset Managers have been involved from the start

Facts - Complexity

7

Simple Outcomes

Structures are essentially simple!

8

Payoff Summary

Level of Lower Index

1st anniversary 2nd anniversary 3rd anniversary 4th anniversary 5th anniversary

100%

60%

0%

6th anniversary

Autocall observ ation coupon of 38.36%

Autocall observ ation coupon of 47.95%

Autocall observ ation coupon of 57.54%

Autocall observ ation coupon of 28.77%

Autocall continues to 2nd anniv ersary

Autocall continues to 3rd anniv ersary

Autocall continues to 4th anniv ersary

Autocall continues to 5th anniv ersary

Autocall continues to 6th anniv ersary

Capital protection barrier triggered @ 60% lev el

Cap

ital P

rote

cted

Cap

ital L

oss

Autocall observ ation coupon of 19.18%

100% 100%

65%

Autocall observ ation coupon of 9.59%

100%

100p Capital redeemed 60%

100%100%

Unlike Shares

Companies’ Balance Sheets are complex – most of these were on most Wealth

Managers’ Stock buy lists / in most large cap funds when they suffer large losses or

effective bankruptcy

9

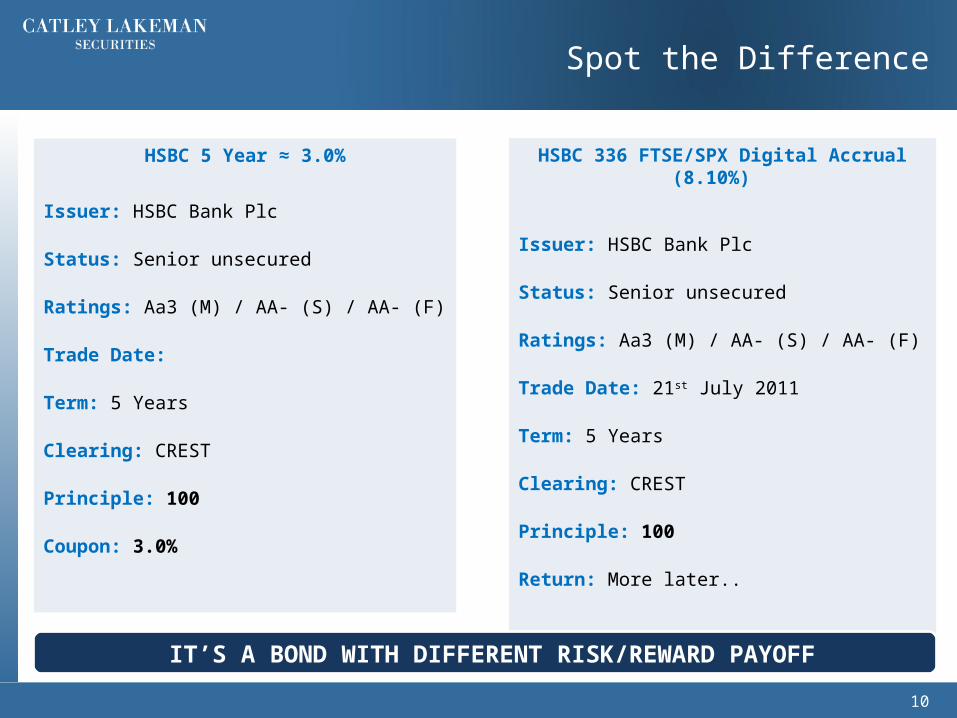

Spot the Difference

HSBC 5 Year ≈ 3.0%

Issuer: HSBC Bank Plc

Status: Senior unsecured

Ratings: Aa3 (M) / AA- (S) / AA- (F)

Trade Date:

Term: 5 Years

Clearing: CREST

Principle: 100

Coupon: 3.0%

HSBC 336 FTSE/SPX Digital Accrual (8.10%)

Issuer: HSBC Bank Plc

Status: Senior unsecured

Ratings: Aa3 (M) / AA- (S) / AA- (F)

Trade Date: 21st July 2011

Term: 5 Years

Clearing: CREST

Principle: 100

Return: More later..

IT’S A BOND WITH DIFFERENT RISK/REWARD PAYOFF

10

Facts - Liquidity

11

Other Defensive Assets?

Real property is by nature illiquid

Property Equity (REITs/IPD) is liquid but correlated to equity ultimately

Funds of Hedge Funds

Absolute Return Funds

Bond Funds..?

12

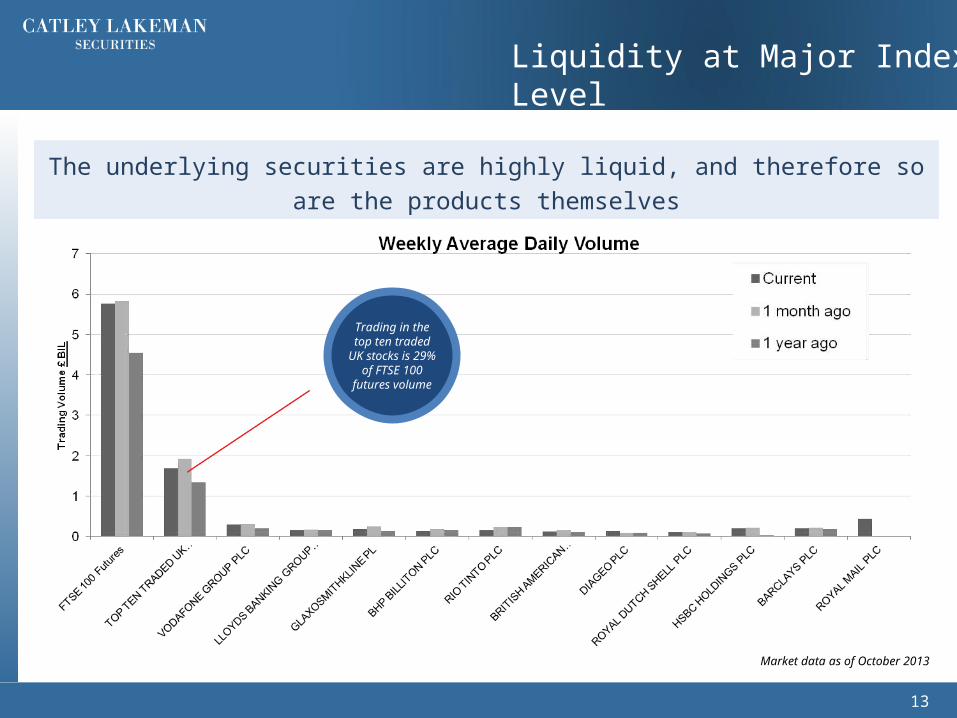

Liquidity at Major Index Level

Trading in the top ten traded UK stocks is 29% of FTSE 100 futures

volume

The underlying securities are highly liquid, and therefore so are the products

themselves

13

Market data as of October 2013

Liquidity at Major Index Level

Current S&P 500 futures volumes are $175.3 BIL

Daily!

Futures - Weekly Average Daily Volumes

Current 1 month ago 1 year ago

Americas USD 230.7bn USD 232.6bn USD 151.4bn

S&P 500 USD 175.3bn USD 176.1bn USD 115.7bn

Europe EUR 89.4bn EUR 95.8bn EUR 77.0bn

EuroStoxx 50 EUR 26.1bn EUR 30.7bn EUR 22.3bn

FTSE 100 EUR 6.8bn EUR 6.8bn EUR 5.1bn

14

How You Buy And Sell a Structured Product

Any deal placed by Investment

manager is being dealt economically

directly with the Bank as the sole

Issuer

Desk at the bank wires money to the

Issuer/Treasury

Desk at the bank arranges with the Risk Book to provide the exposure required by the

Note payoff (Structured Investment)

Dealer at stockbroker buying Note (structured investment) directly from

the bank (via Catley Lakeman trading *)

Investment manager places dealing instruction to dealer at stockbroker

15

Past Exceptions

Close Brothers & ELDerS - collateralised with British, Irish and some Icelandic

banks and building societies. Different to modern structures.

Retail Structured Product market

16

Facts – Costs

17

Cost Comparison

Comparing Structured Products to Other Investments

Actively Managed Fund

ETFStructured

Product

Total expense ratio 1.0% 0.5% 0.0%

Other costs including upfront fees 0.0% 0.0% 1-1.5%

18

How We Work With Brewin Dolphin

19

Where CLS Sits…

Client Discretionary Portfolios

Institutional Investor

20

*All pricing as at circa Jul-11

Live Trade Decision Tree

21

Example Product – HSBC 336 FTSE/S&P Worst-Of Digital Accrual (8.1%)

22

HSBC 336 FTSE/S&P Worst-Of Digital Accrual (8.1%)

Strike: 21-Jul-11

Counterparty: HSBC Aa3 (M) / AA- (S) / AA- (F)

Currency: GBP denominated

Underlying: FTSE 100 / S&P 500

Term: 5 years, 5 days (do not have to hold until maturity)

Upside:

8.1% annual coupon accrued daily if both indices close above 60% of their initial level (3521 FTSE points / 788 S&P points)

I.e.: (days indices over barrier)/260*8.1%)

Rolled up and paid at maturity.

Downside:

If at maturity either index has fallen by more than 40% the structure will redeem paying the original 100p capital minus 1% for every 1% the Index has fallen below strike level observed at maturity

I.e.: capital protected at maturity up to 3521 FTSE points / 788 S&P points

Example Product – HSBC 336 FTSE/S&P Worst-Of Digital Accrual (8.1%)

23

The information in this document is derived from sources believed to be reliable but which have not been independently verified. Catley Lakeman Securities makes no

guarantee of its accuracy and completeness and is not responsible for errors of transmission of factual or analytical data, nor is it liable for damages arising out of any

person’s reliance upon this information. All charts and graphs are from publicly available sources or proprietary data. The opinions in this document constitute the

present judgment of Catley Lakeman Securities, which is subject to change without notice. This document is neither an offer to sell, purchase or subscribe for any

investment nor a solicitation of such an offer. This document is intended for the use of institutional and professional customers and is not intended for the use of

private customers. This document is not intended for distribution in the United States of America or to US persons. This document is intended to be distributed in its

entirety. No consideration has been given to the particular investment objectives, financial situation or particular needs of any recipient.

Catley Lakeman Securities is a LLP registered in England and Wales, Registered Office : One Eleven Edmund Street, Birmingham, B3 2HJ. Registration

Number: OC336585, FSA Reference: 484826

DISCLAIMER

24