Embed Size (px)

Citation preview

Confidential. © 2018 IHS Markit®. All Rights Reserved.Confidential. © 2018 IHS MarkitTM. All Rights Reserved.

International Petrochemical

Industry Forum13 September 2018 | Chengdu, China

Paul Pang

Vice President \ IHS Markit\ APAC Oil, Mid-down Streams, and Chemical

+86 21 24229016

Confidential. © 2018 IHS Markit®. All Rights Reserved.

Asia Chemical Industry Overview

Confidential. © 2018 IHS Markit®. All Rights Reserved.© 2017 IHS Markit

Asia is by far the largest market

Rest of World45%

China36%

Japan3%

Korea4%

Taiwan2%

Singapore1%

Thailand2%

Malaysia1%

Indonesia1%

Philippines0%

Vietnam0% India

5%

Benzene8%

PX7%

Ethylene25%

Propylene17%

MEOH13%

PVC9%

Caustic12%

Soda Ash9%

World total demand in 2018 = 639 million tons

Confidential. © 2018 IHS Markit®. All Rights Reserved.© 2017 IHS Markit

Asia market is a very diversified

Demand in 2018 (million Tons)

Gro

wth

Rate

(%, 2

01

3-1

8)

China

India

Indonesia

Thailand

Philippines

Taiwan

Malaysia

Korea

Singapore

Japan

(5.0)

0.0

5.0

10.0

0.00 100.00 200.00 300.00

Confidential. © 2018 IHS Markit®. All Rights Reserved.© 2017 IHS Markit

0

100

200

300

400

2012 2013 2014 2015 2016 2017 2018 2019 2020 2021 2022 2023 2024 2025

Japan Korea Taiwan China

Mill

ion ton

China is the only growing country in Northeast Asia

Demand

Confidential. © 2018 IHS Markit®. All Rights Reserved.© 2017 IHS Markit

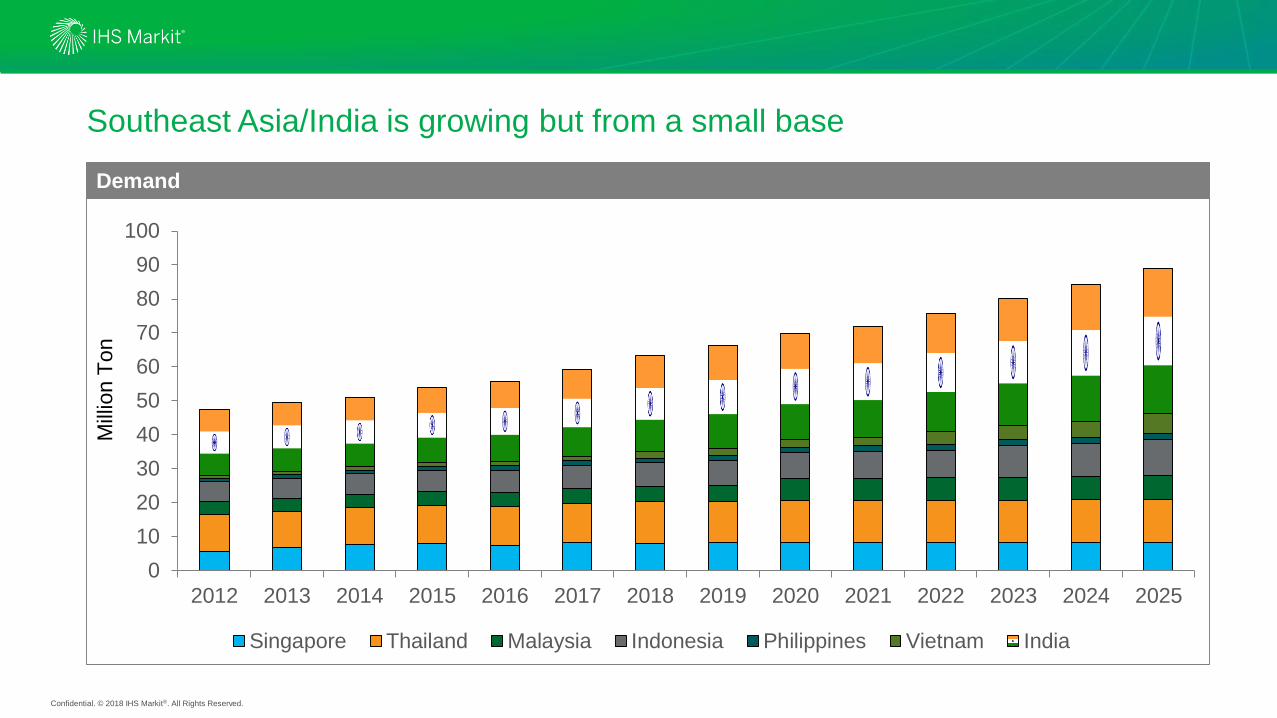

Southeast Asia/India is growing but from a small base

0

10

20

30

40

50

60

70

80

90

100

2012 2013 2014 2015 2016 2017 2018 2019 2020 2021 2022 2023 2024 2025

Singapore Thailand Malaysia Indonesia Philippines Vietnam India

Mill

ion T

on

Demand

Confidential. © 2018 IHS Markit®. All Rights Reserved.© 2017 IHS Markit

SEA: Multiple projects are constructed or planned

-

1

1

2

2

3

3

4

4

2019 2020 2021 2022 2023 2024 2025

Singapore Thailand Malaysia

Indonesia Philippines Vietnam

Million Ton

Capacity addition

PRPC (2019)

Ethylene: 1,260 KTA

Propylene: 1,200 KTA

Long Son (2023)

Ethylene: 1,000 KTA

Propylene: 500 KTA

PTTGC(2021)

Ethylene: 500 KTA

Propylene: 250 KTAHengyi PC (2020)

PX: 1,500 KTA

Bz: 550 KTA

Nghi Son PC (2018)

PX: 700 KTA

Bz: 250 KTA

Confidential. © 2018 IHS Markit®. All Rights Reserved.© 2017 IHS Markit

India: quiet but there likely be more projects coming after 2020

HPCL Mittal Energy(2022)

Ethylene: 1,200 KTA

Propylene: 500 KTA

Confidential. © 2018 IHS Markit®. All Rights Reserved.

China Highlight

Confidential. © 2018 IHS Markit®. All Rights Reserved.

Evolution of policy: opening up but gradual

Launch discharge

permitting system

NOV

2019 20202017 20182015 20162013 201420122007

Deregulate most

investment in chemical;

Restrict less than 1000

KTA refining to JV with

local majority share

JAN

Started opening FDI

in oil / gas, and

Petrochemicals

OCT

Deregulate

refining/

chemical FDI;

deregulate

crude import

FEB

Deregulate

approval

system

JAN

Completely deregulate

refining/chemical;

restrict FDI in oil / gas

upstream to JV only

JULY

Launch nationwide

CO2 trading

DEC Environment

protection tax

JAN ???

Carbon

tax

Confidential. © 2018 IHS Markit®. All Rights Reserved.

• Policy change paves way for private investment

• Private companies are more nimble and efficient

• Strong entrepreneurship

• Grow big to survive: eat or be eaten

Private investment is leading the growth

Product: olefins, PX, Bz, PTA, MEOH, MEG, Caustic, soda ash

Percent of capacityCapacity (million ton)

0%

20%

40%

60%

80%

0

100

200

300

400

2000 2002 2004 2006 2008 2010 2012 2014 2016 2018 2020 2022

Sinopec PetroChina CNOOC Foreign

Local Private

Capacity Comparison between SOEs and Private

Private & Local

Confidential. © 2018 IHS Markit®. All Rights Reserved.

Capital investment in billion US$

© 2018 IHS MarkitSource: IHS Markit

Conventional petrochemical leads growth again

• Coal chemicals

– High CAPEX

– High emission

– Less policy incentives

– Competitive cash cost

• Conventional

– High profitability

– Lowered entry barriers

0

5

10

15

20

25

30

2012 2013 2014 2015 2016 2017 2018 2019 2020 2021 2022

CTO/CTP MTO PDH CTMEG PX Cracker

Petrochemical

Unconventional

Confidential. © 2018 IHS Markit®. All Rights Reserved.

17%

North America

Commodity and specialty chemicals by value

• Strong in commodity but weak in

specialty

• Short-term focus investment strategy

• Short history in the business

• Insufficient investment into R&D, due

to poor IP protection

Commodity versus specialty

Source: IHS Markit

8%

China

Specialty Commodity© 2018 IHS Markit

Confidential. © 2018 IHS Markit®. All Rights Reserved.

North & Northeast

Middle & West

South

East

A wave of integrated refining / petrochemical complexes

8.Wanhua

Chemical

2.SP

Chemicals

Standalone light feed cracker

4.Sinopec

Wuhan

14.Panjin-

Aarmco

7.Shandong

Yuhuang

9.Hengli PC

13.Shenghong

PC

12.Zhejiang PC-

Rongsheng II

3.Zhejiang PC-

Rongsheng I

6.Sinochem QZ

10.Sinopec Gulei

1.CNOOC-

SHELL

11.Sinopec

Hainan

5.Sinopec/

KPC

Integrated complex

Capacity addition (2018-2021), million ton

0

30

60

90

120

Refinery CDU

0

5

10

15

20

C2 C3 PX

Confidential. © 2018 IHS Markit®. All Rights Reserved.

817

≥42

0%

20%

40%

60%

80%

100%

Global Refinery 2016 Petro Rabigh Hengli Refinery-PX

Others Jet/Kerosene Diesel Gasoline Chemicals

Refinery product yields

NaphthaNaphtha

All chemicals

A New China

Refinery/Petrochemical Complex

Confidential. © 2018 IHS Markit®. All Rights Reserved.

In operation

Under construction

China

Mongolia

South Korea

CTO projects

No. Name Cap./KTA Startup Status

1 SXYCPC-Yan'an E&C 700 Mid-2018 Constructing

2 Huating Coal Group 200 Apr-2018 Constructing

3 Baofeng Energy phase 2 600 Nov-2019 Constructing

4 Zhong'an Coal Chem. 600 Oct-2019 Constructing

5 Shanxi Coking Corp. 600 Apr-2020 Constructing

6 Yulin Energy & Chem. 600 Apr-2020 Constructing

7 Qinghai Damei 600 Mid-2021 Constructing

Total 3,900

1 Baotou Shenhua 630 Apr-2022 Planning

2 Qinghai Mining 670 Mid-2022 Planning

3 Sinopec Zhijin 600 2022 Planning

4 Shenhua Ningmei&SABIC 700 Jul-2023 Planning

5 China Coal Yuheng 600 Mid-2023 Planning

6 CPI/Total JV 890 2024 Planning

7 Sinopec Hebi 600 2024 Planning

Total 4,690

Confidential. © 2018 IHS Markit®. All Rights Reserved.

A wave of CTMEG projects is coming

Capacity KTA On stream

1 CNSG Hong Si Fang 300 2018

2 ECO Coal Chemical 240 2018

3 Jiutai 100 2018

4 Yongjin Xinxiang 200 2018

5 Xinjiang Tianye 100 2018

6 Xinhang Energy 100 2018

7 Xinjiang Tianying 150 2018

8 Qianxi 300 2018

9 Hualu Hengsheng 500 2019

10 Huiteng Energy 400 2019

11 Xiangkuang Hongtong 200 2019

12 Binzhou Chem 300 2019

13 Connel 300 2019

14 Xinjiang Tianye 600 2020

Total 3,790

Coal-based

Existing CTMEG capacity 2,075 KTA

Planned capacity > 5,000 KTA

Confidential. © 2018 IHS Markit®. All Rights Reserved.

• Nation-wide carbon trading

• “Gas for coal” in “2+26” regions

• Enforcement of new regulations

• Ban on waste imports

Pollution issue: too serious to be ignored further

Confidential. © 2018 IHS Markit®. All Rights Reserved.

Ban on waste import: a big impact in recycling materials

© 2018 IHS MarkitSource: IHS MarkitDomestic Import

0

2

4

6

8

10

12

2000 2003 2006 2009 2012 2015 2018

China recycled PE/PP consumption, million ton

Ban waste

import

Confidential. © 2018 IHS Markit®. All Rights Reserved.

Trade Friction between

China & America

Confidential. © 2018 IHS Markit®. All Rights Reserved.

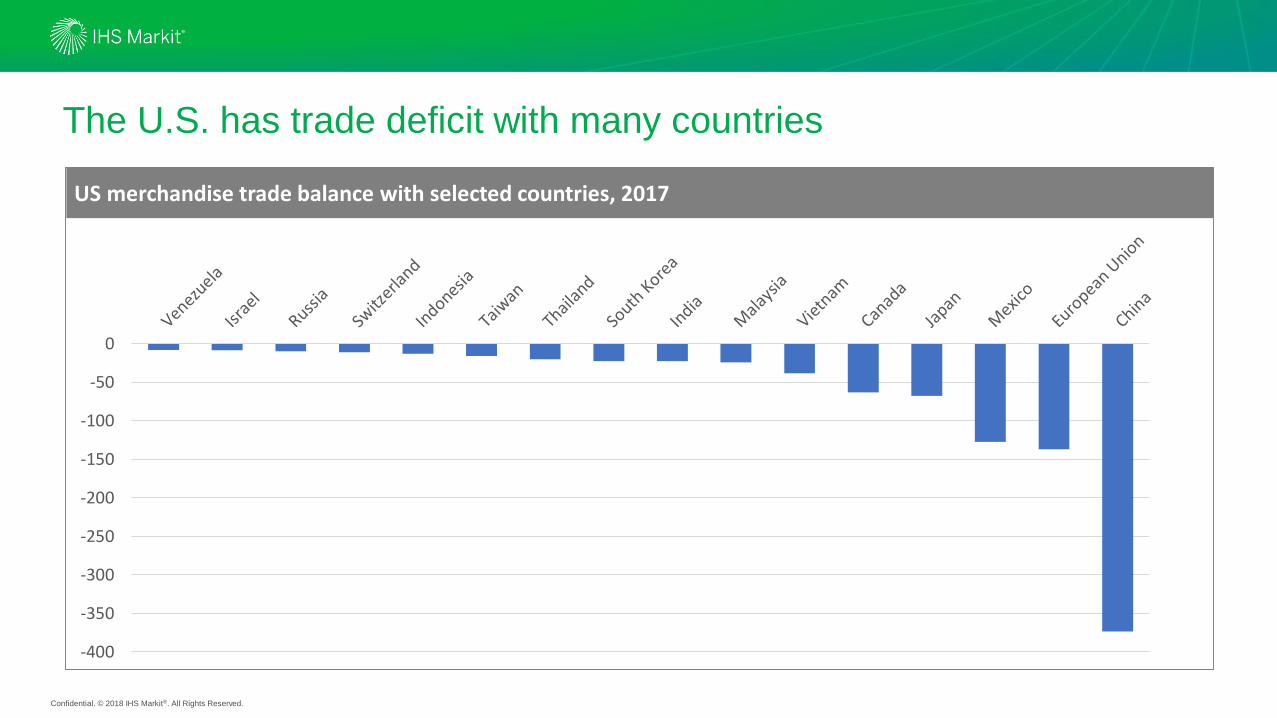

The U.S. has trade deficit with many countries

-400

-350

-300

-250

-200

-150

-100

-50

0

US merchandise trade balance with selected countries, 2017

Confidential. © 2018 IHS Markit®. All Rights Reserved.

China and U.S. trade balance

China America

Bil. USD % GDP Bil. USD % GDP

GDP 12,217 19,391

Commodity export 2,280 18.7 1,546 8.0

Commodity import 1,832 15.0 2,343 12.1

Net export 448 3.7 -797 -4.1

Export to US/China 434 3.6 130 0.7

Date sources: Trade date from IMF,GDP data from IHS Markit

Note: Corresponding export and import data between trading partners are frequently inconsistent in the IMF Direction of Trade database, due to

“difference in 1) classification concepts and detail, 2) time of recording, 3) valuation, and 4) coverage, as well as 5) processing errors”.Source: http://datahelp.imf.org/knowledgebase/articles/484353-why-do-the-exports-of-country-a-to-country-b-not-e

Confidential. © 2018 IHS Markit®. All Rights Reserved.

The impact of trade friction to China

• The direct impact from current tariffs is insignificant.

• However, unpredictability and hostile stand of Trump post a risk of further

escalation.

• Escalated trade war will not only impact China, but also these countries in the

supply chains.

• In the worst case, China may retaliate with other measures beyond tariff.

• There is a high probability that both countries will make compromises to come

to a resolution.

Confidential. © 2018 IHS Markit®. All Rights Reserved.

Key takeaway

•Strong margins supporting acceleration in new capacity

additions.

•Asia chemical industry is very diversified, and continues to be

the fastest growing region.

•China will continue driving global demand and capacity

expansion.

•Threats to the positive outlook include escalating protectionist

trade rhetoric, geo-politics, rising energy costs….

IHS Markit Customer Care

Americas: +1 800 IHS CARE (+1 800 447 2273)

Europe, Middle East, and Africa: +44 (0) 1344 328 300

Asia and the Pacific Rim: +604 291 3600

Disclaimer

The information contained in this presentation is confidential. Any unauthorized use, disclosure, reproduction, or dissemination, in full or in part, in any media or by any means, without the prior written permission of IHS Markit Ltd. or any of its aff iliates ("IHS Markit") is

strictly prohibited. IHS Markit owns all IHS Markit logos and trade names contained in this presentation that are subject to license. Opinions, statements, estimates, and projections in this presentation (including other media) are solely those of the individual author(s) at the

time of writing and do not necessarily reflect the opinions of IHS Markit. Neither IHS Markit nor the author(s) has any obligation to update this presentation in the event that any content, opinion, statement, estimate, or projection (collectively, "information") changes or

subsequently becomes inaccurate. IHS Markit makes no warranty, expressed or implied, as to the accuracy, completeness, or timeliness of any information in this presentation, and shall not in any way be liable to any recipient for any inaccuracies or omissions. Without

limiting the foregoing, IHS Markit shall have no liability whatsoever to any recipient, whether in contract, in tort (including negligence), under warranty, under statute or otherwise, in respect of any loss or damage suffered by any recipient as a result of or in connection with

any information provided, or any course of action determined, by it or any third party, whether or not based on any information provided. The inclusion of a link to an external website by IHS Markit should not be understood to be an endorsement of that website or the site's

owners (or their products/services). IHS Markit is not responsible for either the content or output of external websites. Copyright © 2018, IHS Markit®. All rights reserved and all intellectual property rights are retained by IHS Markit.

25