Embed Size (px)

Citation preview

Version controlDate:8-May-23Time: 9:21 PM

Chapter 6 – The Australian corporate law policy arguments

Temporary tables of contents

ContentsI. Introduction..................................................................................................................2II. x...................................................................................................................................2III. x...............................................................................................................................2IV. Conclusion...............................................................................................................2V. Text copied from other Chapters.................................................................................2VI. What is the legal reasoning for the doctrine of ratification?...................................2

A. Law of Agency........................................................................................................3B. Law of fiduciaries....................................................................................................4C. Equitable defences to breaches of trust...................................................................5

I. INTRODUCTION

II. X

III. X

IV. CONCLUSION

V. TEXT COPIED FROM OTHER CHAPTERS

A. Significance of doctrine reduced – copied from Ch 2 (version prior to July 2017)

As a result of the establishment of statutory director’s duties under the Corporations Act, the doctrine of ratification has accordingly reduced greatly in significance, however, the doctrine of ratification continues to be relevant to the statutory derivative action in respect of applications for leave to commence derivative proceedings, the liability of the directors and the quantum of damages arising from the breach. These matters are discussed in detail below.

VI. WHAT IS THE LEGAL REASONING FOR THE DOCTRINE OF RATIFICATION?

It is important to note initially that the legal basis for the doctrine of ratification does not

rest on estoppel.1 Rather, an agency by estoppel will arise if a principal holds out that a

person is authorised to act on the principal’s behalf.2

With respect to English law in the context of contracts (external ratification), it has been

considered that the doctrine of ratification can be justified on the basis that it gives effect

to what the parties originally intended.3 It is fundamental to the formation of a contract

that the parties have an intention to contract and if all other aspects of the formation of

1 Harrison & Crossfield Ltd v London & North-Western Railway Co [1917] 2 KB 755; R Munday, Agency law and principles (2010, Oxford University Press), 108.2 Azur v Chase Bank, USA, N.A., 601 F.3d 212 (3d Cir. 2010).3 R Munday, Agency law and principles (2010, Oxford University Press), 106.

Page 2 of 54

the contract are present, it would appear to be an inconsistent legal principle to deny the

existence of a contract once it is shown that the parties intended to contract.4

The doctrine of ratification is a rule of very wide application. It has been applied to

fiduciary relationships including; principal and agent, trustee and beneficiary and director

and company and applied generally in contract law, tort law and corporate law. The

authorities considered below suggest a number of possible different legal bases for the

adoption of the doctrine of ratification into English law although it remains unclear

because of the wide general application of the doctrine.

B. Law of Agency

A principal is responsible for the acts of his agent in accordance with the maxim qui facit

per alium, facit per se. This maxim applies to everything done by the agent within the

scope of the agent’s authority, however the maxim does not apply to the acts of the agent

of an agent.5

The fundamental maxim of ratification is omnis ratihabitio retrotrahitur et mandato

priori aequiparatur.6 The maxim means that every ratification has a retrospective effect

and is equivalent to a previous authority or contract. Thus, where a person acts as agent

for a principal and the agent professes to contract for the principal without the approval

of the principal, a subsequent assent by the principal is equivalent to a previous

authority.7 There is a further related maxim - in maleficio ratihabitio mandato

comparatur which means that he who ratifies a bad action is considered as having

ordered it.8

4 See generally Smith v Hughes (1871) LR 6 QB 597.5 Hilton Jackson, E, (1897, Washinton DC John Byrne and Company), Law-Latin A treatise in latin, with legal maxims and phrases as a basis of instruction6 Every ratification is dragged back and treated as equivalent to a prior authority (see generally Bolton Partners v Lambert (1889) 41 Ch D 295)7 Cotterell, J, A collection of latin maxims & phrases (3rd ed, 1913), London:Stevens and Haynes, Bell yard, Temple Bar, http://archive.org/stream/cu31924021688670/cu31924021688670_djvu.txt8 See generally Firth v Staines [1897] 2 QB 70.

Page 3 of 54

In the context of ratification, Isaac J in Davison v Vickery's Motors Ltd (In Liq)9 adopted

the following principles of law:

(i) the general rule is that no person can become a party to a bilateral contract unless

he enters into it personally or by an authorised agent;

(ii) an exception is recognised where a person ratifies an agreement made by another

as for him but without his antecedent authority;

(iii) on ratification, and not before, the agreement is as a general rule deemed by a

fiction to have been made by his antecedent authority to the person actually

making it;

(iv) fictions, however, are not arbitrary. They are not allowed to work an injury; their

operation is to prevent a mischief or to remedy an inconvenience that might result

from the general rule of law; and

(v) where, therefore, an injury would be caused by the operation of the fiction, it

cannot be invoked to alter the general course of the law.10

If the principal ratifies the conduct of the agent within a reasonable time, the principal

discharges the agent from any liability to the principal for damages.11 This is significant

in the context of the prejudice to stakeholders when the doctrine is applied to companies.

C. Law of fiduciaries

Each of the beneficiaries of a trust may give informed consent and thereby authorise the

fiduciary to engage in conduct which would otherwise be a breach of fiduciary duty, and

thereby may condone or ratify a breach of duty which has already occurred.12 The duties

owed by a trustee to a beneficiary are proscriptive and have been described as inflexible13

9 [1925] HCA 47.10 Davison v Vickery's Motors Ltd (In Liq) [1925] HCA 47 per Isaac J.11 See Ricketson v Dean and Laughton (1870) 4 SALR 78 per Wearing J.12 See generally Clack v Carlon (1861) 30 LJ Ch 639; Boardman v Phipps [1967] 2 AC 46; Hospital Products Ltd v United States Surgical Corp (1984) 156 CLR 41.13 See generally Birtchnell v Equity Trustees, Executors and Agency Co Ltd [1929] HCA 24.

Page 4 of 54

and fundamental.14 In Costa Rica Railway Co v Forwood,15 Williams LJ considered the

fiduciary principles and concluded as follows:

As I understand, the rule is a rule to protect directors, trustees, and others against the

fallibility of human nature by providing that, if they do choose to enter into contracts in

cases in which they have or may have a conflicting interest, the law will denude them of

all profits they may make thereby, and will do so notwithstanding the fact that there may

not seem to be any reason of fairness why the profits should go into the pockets of their

cestuis que trust, and although the profits may be such that their cestuis que trust could

not have earned them.16

The decision in Keech v Sandford17 that a trustee was not permitted to have the benefit of

the beneficiary’s lease is an example of the rule which is based on public policy to ensure

that trustees do not gain a personal advantage from the assets of a trust.18

The principle is closely associated with the principle in partnership law that the partners

may ratify a breach of fiduciary duties of another partner.19 Ratification would be

established if it was shown that the partners knowingly allowed a loss to be charged to the

account of the firm.20 Accordingly, there is a significant overlap of the principles

between agency law, partnership law and trust law with respect to ratification.

The doctrine of ratification performs an important role because it gives the right to the

beneficiary to accept the benefit of a transaction entered into by the trustee, whereas the

beneficiary may avoid the risks associated with a transaction where there was no benefit

to be obtained or an exposure to a risk was evident. The principle however requires that

14 Boardman v Phipps [1967] 2 AC 46.15 Costa Rica Railway Co v Forwood (1901) 1 Ch 746.16 Costa Rica Railway Co v Forwood (1901) 1 Ch 746, 761 (Williams LJ).17 (1726) Sel Cas Ch 61.18 See generally P Young, C Croft, M Smith, On Equity (Lawbook Co, 2009), [7.380].19 Lacey v Hill (1876) 4 Ch D 537. See also Dean v MacDowell (1878) 8 ChD 345, CA. See also Halsbury’s Laws of England, [107] Duty not to compete with the firm (12 November 2014).20 Cragg v Ford (1842) 1 Y. & C. Ch. 280. See generally R. C. I’Anson Banks, Lindley & Banks on Partnership (Sweet & Maxwell, London, 18th ed, 2002), [20-15].

Page 5 of 54

where there are multiple beneficiaries, each beneficiary must give their informed

consent.21

D. Equitable defences to breaches of trust

The principles which have developed in equity in relation to the defences of consent and

release to a breach of trust are similar to the principles of (i) disclosure of information

and (ii) knowledge of the conduct which give rise to ratification at common law. The

following discussion highlights the relevant equitable principles in relation to prior

consent and subsequent release of a breach of trust which developed in the context of

proscriptive duties owed by a trustee to a beneficiary.

In the context of prior consent, a beneficiary who has consented, or acquiesced to the

trustee’s breach of trust may not proceed against the trustee.22 The beneficiary must have

had full knowledge of the facts and possibility also their legal consequences if their

concurrence is to bar their claim23 and this rule applies whether or not the beneficiary

derived any benefit from the trustee’s breach.24 The reason for the rule is that ‘a

beneficiary cannot be heard to complain of acts which they themselves has knowingly

authorised’.25 A trustee remains liable to any beneficiary who has not consented or

acquiesced to the breach of trust.26

In the context of subsequent release, on the same principles as prior consent discussed

above, a beneficiary may, by subsequent confirmation or release, prevent themselves

from taking proceedings against their trustee for breach of trust.27 The beneficiary must

know all of the relevant facts.28 It is therefore a defence to a claim that the beneficiary

has released the trustee from their obligation.

21 Brice v Stokes (1805) 11 Ves 319. See generally J McGhee, Snell’s Equity (32nd ed, 2010), [30-028] – [30-030].22 Life Assoc of Scotland v Siddal (1861) 3 De G. F. & J. 58; Fletcher v Collins [1905] 2 Ch 2423 Cockerell v Cholmeley (1830) 1 Russ. & M. 418.24 Fletcher v Collins [1905] 2 Ch 24.25 Brice v Stokes (1805) 11 Ves 319.26 Brice v Stokes (1805) 11 Ves 319. See generally J McGhee, Snell’s Equity (32nd ed, 2010), [30-028] – [30-030].27 See generally J McGhee, Snell’s Equity (32nd ed, 2010), [30-028] – [30-030].28 Burrows v Walls (1855) 5 De G. M. & G. 233.

Page 6 of 54

The initial jurisprudence considered that a legal right could be released (or varied) by

agreement for valuable consideration or by deed. The weight of authority now favours

the view that a legal right cannot be released in equity unless it is under an agreement,

including by parol,29 supported by valuable consideration.30 An equitable release of a

legal obligation can be established by conduct. Such cases however may be classified as

estoppel, election or waiver.31

The release of equitable rights, at general law and apart from statute, may be effected in

writing,32 orally or by conduct provided that it is proof of a ‘fixed, deliberate and

unbiased determination that the transaction should not be impeached’.33 There must be a

present fixed intention immediately to release and not a mere promise or mere expression

of a future intention to release.34 The defendant fiduciary must show that the plaintiff was

aware of the nature and circumstances of the transaction giving rise to the right in equity

and of their rights to relief in equity.35

In circumstances where a release is obtained from a party in ignorance of material facts,

which is the duty of the fiduciary to disclose, the release will be held invalid.36 Further,

unless the trustee has fully informed the beneficiary of their rights, or they acted under

the full knowledge of the liability of the trustees, a release will be ineffective.37

29 Creamoata Ltd v Rice Equalization Association Ltd [1953] HCA 40 at [14] per Williams ACJ; Hill v. Gomme [1839] EngR 989; Lady Lanesborough v. Ockshott [1719] EngR 59; Berry v. Berry (1929) 2 KB 316 ; Fry on Specific Performance, 6th ed. (1921), p. 47830 Commissioner of Stamp Duties for the State of NSW v Bone; Byrn v Godfrey; Edwards v Walters. See Up to P W Young, C Croft, M L smith, On equity, Lawbook Co 2009, 17.240.31 Up to P W Young, C Croft, M L smith, On equity, Lawbook Co 2009, [17.240].32 The usual requirements for the disposition of an equitable interest continue to apply under the Property Law Acts enacted by the States and Territories.33 Wright v Vanderplank (1856) 8 De GM & G 133 at 147 per Turner LJ. See Halsburys Laws of Australia [185-1905] Waiver as at 1 December 2013.34 Avtex Airservices Pty Ltd v Bartsch (1992) 107 ALR 539; 23 IPR 469; AIPC ¶90-898. See Halsburys Laws of Australia [185-1905] Waiver as at 1 December 201335 Allcard v Skinner (1887) 36 Ch D 145; [1886-90] All ER Rep 90. See Halsburys Laws of Australia [185-1905] Waiver as at 1 December 201336 Bowles v Stewart, 1 Sch & Lefr. 209, 204; Broderick v Broderick, 1 P. Will. 240. See Story, J, Commentaries on equity jurisprudence, Volume 1, 10th ed, 1870, Boston: Little, Brown and company, at 22137 Burrows v Walls, 5 De Gex, M & G. 233. See See Story, J, Commentaries on equity jurisprudence, Volume 1, 10th ed, 1870, Boston: Little, Brown and company, at 323.

Page 7 of 54

PropositionIt is a proposition advanced by this thesis that at the time of adoption of the Roman

doctrine of ratification into English law, the doctrine had no clear doctrinal basis for its

application to the fiduciary relationship of director and company, however, the common

law principles of agency, equitable principles concerning informed consent by a

beneficiary and the equitable doctrine of release are consistent with the principles of the

doctrine of ratification and consistent with each other.

VII. SIGNIFICANCE OF THE REGULATION OF CORPORATE GOVERNANCE

E. Corporate governance models and the overarching principles of corporate governance

There is no universally accepted definition of ‘corporate governance’. In recent times,

there have been attempts to define corporate governance, the most notable of which in

chronological order, are as follows:

(i) the United Kingdom ‘Cadbury Report’ in which it was stated that:

[c]orporate governance is the system by which companies are directed and

controlled. The boards of directors are responsible for the governance of their

companies. The shareholder’s role in governance is to appoint the directors and

the auditors to satisfy themselves that an appropriate governance structure is in

place. The responsibilities of the board include setting the company’s strategic

aims, providing the leadership to put them into effect, supervising the

management of the business and reporting to shareholders on their stewardship.

The board’s actions are subject to laws, regulations and the shareholders in

general meeting.38

(ii) the Australian Report of the Royal Commission into HIH Insurance in which it

was stated that:

[a]t its broadest, the governance of corporate entities comprehends the

framework of rules, relationships, systems and processes within and by which

38 The Committee on the Financial Aspects of Corporate Governance and Gee and Co Ltd, The Report of the Committee on the financial aspects of corporate governance (1992), Paragraph 2.5 (‘Cadbury Report’).

Page 8 of 54

authority is exercised and controlled in corporations. It includes the practices by

which that exercise and control of authority is in fact effected.39

(iii) the Organisation for Economic Co-operation and Development defined corporate

governance as:

[p]rocedures and processes according to which an organisation is directed and

controlled. The corporate governance structure specifies the distribution of rights

and responsibilities among the different participants in the organisation – such as

the board, managers, shareholders and other stakeholders – and lays down the

rules and procedures for decision-making;40 and

(iv) the Australian Securities Exchange Corporate Governance Council defined

corporate governance as ‘the framework of rules, relationships, systems and

processes within and by which authority is exercised and controlled in

corporations.’41

The above definitions of corporate governance include accountability for conduct by the

directors,42 whether to shareholders alone (the narrow view) or to additional stakeholders

(the broader view).43 It has also been stated that the definitions of corporate governance

rely upon the overarching principles of leadership, effectiveness, ethics, openness,

integrity and accountability.44 Internationally, the various definitions of corporate

governance may diverge in their scope and focus because of social, cultural, economic

and political influences in countries which have followed either a common law or civil

law tradition.45 The complexity which gives rise to the different approaches taken to the

39 Commonwealth, Report of the Royal Commission into HIH Insurance (2001), Part 3 Chapter 6.40 Organisation for Economic Co-operation and Development (21 July 2013) OECD StatExtracts <http://stats.oecd.org/glossary/detail.asp?ID=6778>.41 Australian Securities Exchange Corporate Governance Council, ‘Corporate Governance Principles and Recommendations with 2010 Amendments (2nd ed.)’ (2010) Australian Securities Exchange.42 Accountability is defined ‘as the quality or state of being accountable; especially: an obligation or willingness to accept responsibility or to account for one's actions.’ (Merriam Webster, Dictionary (21 July 2013) Merriam Webster <http://www.merriam-webster.com/>.43 Jill Solomon and Aris Solomon, Corporate Governance and Accountability (John Wiley & Sons, Ltd, 2004), 14.44 The Bell Group Ltd (in liq) v Westpac Banking Corporation (No 9) [2008] WASC 239, [4367] (Owen J). See generally Cadbury Report above n; Financial Reporting Council, The UK Corporate Governance Code (2014), < https://www.frc.org.uk/Our-Work/Publications/Corporate-Governance/UK-Corporate-Governance-Code-2014.pdf> as at 27 October 2014.45 Jeswald W Salacuse, ‘The Cultural roots of Corporate Governance’ (2004-2005) 7 Studies in International, Financial, Economic and Technology Law 433 (2004-2005).

Page 9 of 54

regulation of corporate governance may in part be explained by the fact that there are at

least seventeen theories of corporate governance.46

The following are the principles of good corporate governance which have been

recognised by the Organisation for Economic Co-operation and Development47 and the

Australian Securities Exchange Corporate Governance Council:48

(i) The corporate governance framework should promote transparent and efficient

markets, be consistent with the rule of law and clearly articulate the division of

responsibilities among different supervisory, regulatory and enforcement

authorities;

(ii) The corporate governance framework should protect and facilitate the exercise of

shareholders’ rights;

(iii) The corporate governance framework should ensure the equitable treatment of all

shareholders, including minority and foreign shareholders. All shareholders

should have the opportunity to obtain effective redress for violation of their rights;

(iv) The corporate governance framework should recognise the rights of stakeholders

established by law or through mutual agreements and encourage active co-

operation between corporations and stakeholders in creating wealth, jobs, and the

sustainability of financially sound enterprises;

(v) The corporate governance framework should ensure that timely and accurate

disclosure is made on all material matters regarding the corporation, including the

financial situation, performance, ownership, and governance of the company;

(vi) The corporate governance framework should ensure the strategic guidance of the

company, the effective monitoring of management by the board, and the board’s

accountability to the company and the shareholders;

(vii) Companies should establish and disclose the respective roles and responsibilities

of the board of directors and management;

46 Richard Ziolkowski, A re-examination of corporate governance: Concepts, models, theories and future directions (PhD, University of Canberra, 2005) 362.47 Organisation for Economic Co-operation and Development, OECD Principles of Corporate Governance (2004) < http://www.oecd.org/daf/ca/corporategovernanceprinciples/31557724.pdf>.48 ASX Corporate Governance Council, Corporate Governance Principles and Recommendations with 2010 Amendments, 2nd ed, (27 August 2010).

Page 10 of 54

(viii) Companies should have a board of effective composition, size and commitment to

adequately discharge its responsibilities and duties;

(ix) Companies should actively promote ethical and responsible decision-making;

(x) Companies should have a structure to independently verify and safeguard the

integrity of their financial reporting;

(xi) Companies should promote timely and balanced disclosure of all material matters

concerning the company;

(xii) Companies should respect the rights of shareholders and facilitate the effective

exercise of those rights;

(xiii) Companies should establish a sound system of risk oversight, management and

internal control; and

(xiv) Companies should ensure that the level and composition of remuneration is

sufficient and reasonable and that its relationship to performance is clear.

The underlying need for corporate governance arises from the separation of the

ownership of the corporation by the shareholders and the control of the corporation by the

board of directors. The separation of ownership and control is the classic agency

problem which was considered in the seminal paper of Berle and Means published in

1932.49

Whilst there are different approaches taken internationally to the regulation of corporate

governance (ipso facto what is self-regulated by companies), there is no academic

agreement about the best model for the regulation of corporate governance.50 There are

two broad models of corporate governance, which may be summarised as follows:

(i) The insider (stakeholder) model. The model arises principally from the existence

of a high concentration of ownership of shares in companies and is prevalent in

Japan, South Korea and in many European countries including Germany. A key

feature of this model is that the ownership and control are predominantly not

49 Adolf Berle Jr and Gardner Means, The modern corporation and private property (Macmillan, 1932).50 See generally Andrei Shleifer and Robert Vishny, ‘A survey of corporate governance’ (1997) Journal of Finance 52(2) 737.

Page 11 of 54

separated thus the major shareholders are actively involved in the management

and/or decision-making of the company;51 and

(ii) The outsider (shareholder) model. The model arises principally from the

dispersed ownership of shares by shareholders and is prevalent in the United

Kingdom, United States of America, Canada, Singapore, New Zealand and

Australia.52 A feature of this model is that there is a distinct separation of

ownership and control and the use of either independent boards of directors, or

non-executive directors.

The insider (stakeholder) model is generally speaking a model which operates in civil law

jurisdictions, whereas the outsider (shareholder) model generally operates in common

law jurisdictions. The key features of the two models is summarised below:

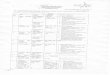

Table [xx]. Features of the insider and outsider corporate governance models.53

Feature Insider (stakeholder)

model

Outsider (shareholder)

model

Share ownership Concentrated Dispersed

Shareholder influence on

management

Strong Weak

Cross-shareholdings Significant Negligible

Company’s relationships

with banks

Long-term relationship of

significant nature

Arm’s-length or

insignificant

51 Mahmoud Ezzamel and Robert Watson ‘Organizational from, ownership structure and corporate performance: A contextual empirical analysis of UK companies’, (1993) 4(3) British Journal of Management 161.52 Yochai Benkler ‘Freedom in the Commons: Towards a Political Economy of Information’ (2003) Duke Law Journal 52(6) 1245.53 See Richard Ziolkowski, A re-examination of corporate governance: Concepts, models, theories and future directions (PhD, University of Canberra, 2005); Kevin Campbell and Magdalena Jerzemowska, ‘Corporate Governance in Developed Economies. Accounting and Audit. Problems of Development’ (1999) University of Latvia 151.

Page 12 of 54

Management Usually two tiered Board of

directors and a supervisory

board

One tier, single Board of

directors

Minority shareholder

protection

Negligible Important

Insolvency/bankruptcy law Strong protection of

investors

Strong protection of

investors

Accounting standards54 Lower requirements for

reporting financial

information

Higher requirements for

reporting financial

information

Transparency Low High

Market control of the

company

Negligible Active

Managerial incentives Negligible Wide

There have been different approaches to regulation which vary along a continuum

between:

(i) rule-based regulatory models where prescriptive rules are established; and

(ii) principles-based regulatory models which allows companies to comply with the

principles of corporate governance in a flexible way.55

Under either of the two broad models of corporate governance, there remains the possibility that a director may seek authorisation of a breach of fiduciary duties from the shareholders.

1 Corporate governance framework

At least one objective of the regulation of corporate governance is to establish a corporate

governance framework for the internal controls of the company through a prism of the 54 The issue of the differences between accounting standards from jurisdiction to jurisdiction will be obviated by the acceptance of International Accounting Stantards Board financial reporting standards (see generally Mehrani, S, Moradi, M and Eskandar, Corporate Governance: Convergence v.s Divergence, British Journal of Economics, Finance and Management Sciences (May 2014 Vol 9(1)).55 See generally Joshua Blackmore, ‘Evaluating New Zealand's evolving corporate governance regulatory regime in a comparative context’ (2006) 12 Canterbury Law Review 34.

Page 13 of 54

overarching principles of good corporate governance, those being leadership,

effectiveness, ethics, openness, integrity and accountability.56 In Australia, the regulation

of corporate governance principally through the Corporations Act allows the shareholders

to monitor the performance of the company’s directors and it enables remedial steps to be

taken if the directors breach their fiduciary or statutory duties to the company.

The company’s responsibility for establishing, implementing and maintaining corporate

governance extends to all matters which are regulated by; the Corporations Act, the

listing rules of a securities exchange (if the company is publicly listed) and any licence

held by the company in addition to any matter of self-regulation of corporate governance

which the company determines which are in addition to any statutory obligations. Many

aspects of corporate governance must be established, implemented and maintained by the

board of directors by reason of the mandatory requirements of the Corporations Act. The

shareholders may determine to regulate non-mandatory aspects of corporate governance

either through the company’s constitution by approving a special resolution57 at a general

meeting of shareholders or through an ordinary resolution of the shareholders in general

meeting, provided that the resolution does not effectively control or interfere with the

powers given to the board of directors by the company’s constitution.58 The scope of the

issues related to corporate governance is not restricted to legal matters because of the

management control which the board of directors exercises over the company’s affairs.59

It may be noted that ‘corporate culture’ and ‘corporate social responsibility’ are issues

relevant to corporate governance, albeit not regulated in Australia by the Corporations

Act.

56 The Bell Group Ltd (in liq) v Westpac Banking Corporation (No 9) [2008] WASC 239, [4367] (Owen J); Cadbury Report, above n.57 A special resolution requires at least 75% of shareholders to approve a resolution.58 see, eg, Bamford v Bamford [1970] Ch 212, 220 (Plowman J); National Roads & Motorists’ Association v Parker (1986) 6 NSWLR 517, 521; Howard Smith Ltd v Ampol Ltd [1974] 1 NSWLR 68, 79; Federal Commissioner of Taxation v Commonwealth Aluminium Corporation (1980) 143 CLR 646 at 660-661; John Shaw & Sons (Salford) Ltd v Shaw [1935] 2 KB 113, 134; Salmon v Quin and Axtens [1909] 1 Ch 311; Automatic Self-Cleansing Filter Syndicate Co Ltd v Cunninghame [1906] 2 Ch 34; Imperial Hydropathetic Hotel Co Blackpool v Hampson (1882) 23 Ch D 1; Gramophone and Typewriter Ltd v Stanley [1908] 2 KB 89, 105-106 (Buckley LJ); Towcester Racecourse Co Ltd v The Racecourse Association Ltd [2002] EWHC 2141 (Ch).59 See generally LexisNexis, Ford’s Principles of Corporations Law [6.005].

Page 14 of 54

PropositionIt is a proposition advanced by this thesis that the requirement for a 75% majority of

shareholders to establish or amend corporate governance requirements under a

company’s constitution establishes a procedural barrier to protecting the interests and

rights of minority shareholders and is therefore contrary to the maintenance of good

corporate governance standards.

The corollary of the above proposition is that the ability of a minority of shareholders of

at least 25% to prevent the company’s constitution from being amended by the majority

of shareholders is contraryf to the maintenance of good corporate governance.

Corporate governance has continued to become a matter of greater significance to

shareholders since the release of the Cadbury Report in the United Kingdom in 1992,

however the statutory requirements for a special resolution have remained static. The

constitution establishes all of the shareholders’ rights and obligations, not merely the

substantive and procedural rules which concern corporate governance. It is impractical,

in light of the difficultly of defining corporate governance, to allow shareholders to

establish or amend a constitutional clause which relates to corporate governance, or to

establish a separate procedure by which a smaller majority than 75% could establish or

amend a clause in the constitution relating to corporate governance.

PropositionIt is a proposition advanced by this thesis that the increasing significance of corporate

governance to shareholders indicates that there should be law reform to the Corporations

Act to implement mechanisms by which good corporate governance can be maintained

by all companies.

The primary responsibility for corporate governance lies with the board of directors.60

This arises from the broad power granted to the board of directors to manage the business

60 The Bell Group Ltd (in liq) v Westpac Banking Corporation (No 9) [2008] WASC 239, [4365] (Owen J).

Page 15 of 54

of the company.61 As Middleton J stated in Australian Securities and Investments

Commission v Healey:62

A director is an essential component of corporate governance. Each director is placed at

the apex of the structure of direction and management of a company. The higher the office

that is held by a person, the greater the responsibility that falls upon him or her. The role

of a director is significant as their actions may have a profound effect on the community,

and not just shareholders, employees and creditors.63

In the context of the objective64 reasonable standard of care, it may be noted from the

above statement, the law draws no relevant distinction between an executive and non-

executive director.65 Consequently, all directors are expected to meet minimum standards

of conduct in the performance of their duties.

In Australian Securities and Investments Commission v Rich66 and Australian Securities

and Investments Commission v Healey,67 the Australian Securities and Investments

Commission tendered evidence of the ‘usual practices’ of directors of publicly listed

companies. This evidence was accepted in both cases as being relevant to determining

the obligations upon directors. In this context, without specific legislation, corporate

governance standards could be set at a relatively low level because the usual practices

may not objectively be good practices. Thus what may be considered to be ‘good’

corporate governance may in fact at the relevant time be a usual practice which is

objectively ‘average’, ‘sub-optimal’ or indeed ‘poor’ corporate governance.

PropositionIt is a proposition advanced by this thesis that a reference point of the usual practices of

directors may be an inadequate mechanism to determining good corporate governance

61 Corporations Act 2001 (Cth) s 198A(1).62 (2011) 196 FCR 291.63 Australian Securities and Investments Commission v Healey (2011) 196 FCR 291, [14] (Middleton J).64 See, eg, Gamble v Hoffman (1997) 24 ACSR 369 where the court refused to subjectify the standard of care to the standard of a person who “left school at the age of 14 years, has no tertiary qualifications and has spent his life…essentially as a fruit and vegetable market gardener”.65 Australian Securities and Investments Commission v Healey [2011] FCA 717, [172] (Middleton J).66 (2003) 44 ACSR 341.67 [2011] FCA 717.

Page 16 of 54

practices.

F. How is corporate governance regulated?

It is useful at this point to highlight that the aim of legislation regulating corporations is

to create a self-governing system with a minimal role of the courts.68 Thus it is necessary

for the Commonwealth parliament to give consideration to the principles underlying the

division of powers between the two internal ‘corporate organs’ (the board of directors

and the shareholders69 in general meeting) so as to ensure as far as possible that

shareholders’ rights are protected.70 In practice, a balance must however be reached

because if shareholders are granted too many rights, the additional costs of compliance to

companies may outweigh the benefits of the shareholders having those rights.

The statutory scheme reflects the shareholder primacy theory, however in this Chapter it

is argued that a pluralist approach should be taken in relation to the doctrine of

ratification to eliminate or reduce the prejudice to all stakeholders.

Corporate governance is principally regulated by the Corporations Act through the

regulation of:

(i) director’s and other officer’s duties;71

68 Michael Whincop, ‘The role of the shareholder in corporate governance: A theoretical approach’ (2001) Melbourne University Law Review 25 418, 419.69 Pursuant to section 231(b) of the Corporations Act 2001, a person is a member of a company if they agree to become a member of the company after its registration and their name is entered on the register of members. A company must set up and maintain a register of members pursuant to section 168 of the Corporations Act 2001 in the form prescribed by section 169 of the Corporations Act 2001. A person is not a member until their name is entered on the register of members (Maddocks v DJE Constructions Pty Ltd (1982) 148 CLR 104).70 In the 19th century, the shareholders in general meeting were regarded as the supreme corporate organ (see, eg, Conservators of the River Tone v Ash (1829) 10 B&C 349). See generally Michael Whincop, ‘The role of the shareholder in corporate governance: A theoretical approach’ (2001) Melbourne University Law Review 25 418, 442.71 At least in part, section 107 of the Companies Act 1958 (Vic) (now sections 182 to 184 of the Corporations Act 2001) was designed to encourage good corporate governance (see Angas Law Services Pty Ltd (In liquidation) v Carabelas [2005] HCA 23, [62] (Gummow and Hayne JJ). Section 183 (use of information) and section 184(3) (criminal offence for the use of information) of the Corporations Act 2001 supplement the fiduciary duties upon directors.

Page 17 of 54

(ii) disclosure of director’s conflicts of interest;72

(iii) members’ remedies;73

(iv) the integrity of financial information;74

(v) a member’s right to inspect the company’s books;75 and

(vi) through the separation of powers between the internal corporate organs.76

Separate to the regulation of corporate governance by the Corporations Act, the

constitution is determinative of rights between shareholders inter se and only a majority

of 75% of shareholders may amend the constitution. It follows that a minority of more

than 25% can constrain the actions of a majority of shareholders by preventing any

amendment to the constitution and insisting up procedural and substantive compliance

with the requirements of the constitution.

Companies, which are not otherwise regulated by conditions imposed upon a licence or

the listing rules of a securities exchange, may self-regulate corporate governance in the

following key ways:

(i) determining the criteria for a person to be appointed as a director who is over

18 and not otherwise prohibited from acting as a director;

(ii) whether there should be standing sub-committees of the board of directors

(eg. audit, risk and remuneration committees);

(iii) establishing training standards for directors;

(iv) determining the employment and conditions of key managers including all

employment benefits;

(v) determining the procedural and substantive requirements for corporate

governance in the constitution;

(vi) determining the rights of shareholders inter se in the constitution;

72 Corporations Act 2001 (Cth) s 191(1).73 Ibid Chapter 2F.74 Ibid Chapter 2M. The history of the requirements of providing financial information in relation to Australian companies can be traced back to section 23 of the Companies Act 1896 (Vic) which required that a company produce an audited financial statement.75 Ibid s 247A.76 Ibid s 198A(2). The current regulation of corporate governance has been considered to be a response to ‘demonstrated abuses and errors in the management of Australian corporations in the 1980s’ (see Rich v Australian Securities and Investments Commission [2004] HCA 42, [117] (Kirby J)).

Page 18 of 54

(vii) complaint handling procedures;77

(viii) policies and procedures which relate to risk management;78

(ix) the extent to which corporate social responsibility is implemented into the

company’s business model and operations;79 and

(x) establishing and maintaining an appropriate corporate culture.80

Subject to the constitution of the company, the content and scope of the self-regulation of

corporate governance may be determined by the board of directors, or the shareholders in

general meeting.

It should not be assumed that self-regulation of the above aspects of corporate

governance demonstrates a lack of response by the Commonwealth parliament to

determining how corporate governance should be regulated or that self-regulation is not

the preferred mechanism. Self-regulation of corporate governance is adaptable, flexible

and can be implemented far quicker than any law can be implemented. Further, the

insolvency of a corporation of itself may not result from poor standards of corporate

governance. Rather, economic factors and/or legislative change may be the sole reasons

for a particular business model to cause a company to become insolvent.

PropositionIt is a proposition advanced by this thesis that:

(i) self-regulation of corporate governance is an effective mechanism for

shareholders, however, a majority of shareholders may be unable to amend the

77 See generally SAI Global, ‘Customer satisfaction – guidelines for complaints handling in organizations’ (AS/ISO 10002:2006), SAI Gobal, 2006.78 See generally International Standards Organisation, ‘Risk management – Principles and guidelines’ (ISO 31000:2009), International Standards Organisation, 2009.79 See generally International Standards Organisation ‘Social Responsibility’ (ISO 26000:2010), International Standards Organisation, 2010 which provides guidance to companies on how they can operate in a socially responsible way. One such issue is the extent to which a company voluntarily offsets its carbon emissions.80 Pursuant to section 12.3(6) of the Criminal Code 1995 (Cth), ‘corporate culture’ means an attitude, policy, rule, course of conduct or practice existing within the body corporate generally or in the part of the body corporate in which the relevant activities takes place. The Inquiry into certain Australian companies in relation to the UN Oil-for-Food Programme concluded that AWB Ltd ‘s conduct was ‘indicative of a closed corporate culture...such an approach did not constitute a breach of any Commonwealth, State or Territory Law.’ (see Commonwealth, Report of the Inquiry into certain Australian companies in relation to the UN Oil-for-Food Programme (2006), paragraph 8.135).

Page 19 of 54

company’s constitution to insist on procedural and substantive compliance with

good corporate governance standards; and

(ii) reliance upon an ordinary resolution passed by a majority of shareholders in

general meeting for the purpose of strengthening corporate governance is likely to

be ineffective as at any time a majority of shareholders can pass a new resolution,

eroding the benefits of any good corporate governance policies and practices

which were implemented.

G. Company constitution as a source of shareholder rights

The constitution of a company is the principle source of shareholders’ rights through

which the shareholders may establish a corporate governance framework in addition to

the requirements of the Corporations Act. The constitution may establish both

substantive and procedural corporate governance requirements which may self-regulate

such matters from the engagement of key personnel to significant acquisitions or

disposals of business assets.

For all companies registered after 1 July 1998, the replaceable rules operate.81 The

shareholders of an unlisted public company may elect to put in place a written

constitution which displaces or modifies any or all of the replaceable rules.82 The

company’s constitution, whether it modifies or replaces any replaceable rules, has effect

as a contract between the company and each member, the company and each director and

company secretary and between a member and each other member.83 A breach of any

provision of the company’s constitution is thus a breach of contract for which a remedy

may be sought by a shareholder84 from the Federal Court of Australia or a State or

Territory Supreme Court.85

81 Corporations Act 2001 (Cth) s 135(1)(a)(i).82 Ibid s 135(2).83 Ibid s 140(1).84 Former section 180 was held in Jones v Money Mining NL (1995) 17 ACSR 531 to give an officer standing to obtain a declaration (see R P Austin, I M Ramsay, Ford’s principles of Corporations Law (LexisNexis Butterworths, 13th ed, 2007), [6.030]).85 Section 233 and Part 9.5 of the Corporations Act 2001 grants broad powers to the Court to grant relief.

Page 20 of 54

Companies may elect to regulate corporate governance through the use of; a

shareholders’ agreement, written corporate governance policies and procedures86

compliance and risk management systems and due diligence procedures. Companies may

also create sub-committees of the board of directors for the purpose of the

implementation of a company’s corporate governance practices such as audit, risk and

remuneration committees.87

PropositionIt is a proposition advanced by this thesis that the ability of a majority of 75% of

shareholders to elect to displace the non-mandatory replaceable rules in the company’s

constitution means that there is no uniform mechanism by which good corporate

governance standards may be imposed upon all companies incorporated under the

Corporations Act.

H. Separation of powers between the internal corporate organs

A company incorporated under the Corporations Act has the legal capacity and all the

powers of an individual,88 however, as a creature of statute, the company must act

through its human actors89 in accordance with the division of powers in the constitution.

The two internal corporate organs of a company have original authority to bind the

company or delegate to others, make decisions and act as the company within those areas

allocated to it by law or the company’s constitution.90,91 There is a clear division of 86 See, eg, Belgiorno-Zegna v Exben Pty Ltd [2000] NSWSC 884; Porter v GIO Australia Ltd [2003] NSWSC 668; Australian Securities and Investments Commission, in the matter of Chemeq Limited (ACN 009 135 264) v Chemeq Limited (ACN 009 135 264) [2006] FCA 936.87 See generally Australian Securities and Investments Commission v Healey [2011] FCA 717, [302] (Middleton J).88 Corporations Act 2001 (Cth) s 124(1). A consequence of these rights means that a company can grant a power of attorney to an individual whi can then act on behalf of the company (as distinct from acting as a managing director of a company).89 Lennard’s Carrying Co Ltd v Asiatic Petroleum Co Ltd [1915] AC 705, 713 (Viscount Holden).90 Federal Commissioner of Taxation v Lutovi Investments Pty Ltd (1978) 20 ALR 157, 176 (Deane J). See also LexisNexis, Australian Encyclopedia of Forms & Precedents (at 15 September 2013) ‘Importance of meetings and respective roles of members and directors’ [175.A[1]].91 In the 18th and early 19th century, it was common to include a clause in the deed of settlement of the unincorporated joint stock company conferring managerial power on a board of directors or analogous body (see H Ford, R Austin and I Ramsay, Ford’s Principles of Corporations Law (LexisNexis, 10th ed,

Page 21 of 54

powers between the shareholders in general meeting and the board of directors.92 Unless

there is something specific in the company’s constitution, or the constitution is amended,

the directors cannot usurp the powers which by the constitution are vested in the

shareholders in general meeting.93

The business of a company is managed by or under the direction of the board of

directors94 and the directors may exercise all the powers of the company except any

powers that the Corporations Act or the company's constitution requires the company to

exercise in general meeting.95 A power vested by the constitution of a company

exclusively in the directors cannot be effectively exercised, nor can its exercise by the

directors be effectively controlled or interfered with, by a resolution of shareholders in

general meeting.96 The only way in which the shareholders can control the exercise of

the powers vested by the constitution in the directors is by (i) altering the constitution or

(ii) if the power exists under the constitution, by refusing to re-elect the directors of

whose actions they disapprove.97 These issues highlight the nature of the problem created

by the division between the separation of ownership and control of a company.

The powers of the company are subject to the company’s constitution.98 If the company’s

constitution merely empowers the directors to perform an action, it may be construed that

the concurrent power of shareholders remains to perform the same action.99 Thus, some

2001) 216-218). See generally Michael Whincop, ‘The role of the shareholder in corporate governance: A theoretical approach’ (2001) Melbourne University Law Review 25 418, 442.92 Duke Group Ltd (in liq) v Pilmer [1998] SASC 6529 citing with approval John Shaw & Sons (Salford) Ltd v Shaw [1935] 2 KB 113, 134 (Greer LJ).93 John Shaw & Sons (Salford) Ltd v Shaw [1935] 2 KB 113, 134 (Greer LJ).94 Corporations Act 2001 (Cth) s 198A(1).95 Ibid s 198A(2).96 see, eg, Bamford v Bamford [1970] Ch 212, 220 (Plowman J); National Roads & Motorists’ Association v Parker (1986) 6 NSWLR 517, 521; Howard Smith Ltd v Ampol Ltd [1974] 1 NSWLR 68, 79; Federal Commissioner of Taxation v Commonwealth Aluminium Corporation (1980) 143 CLR 646 at 660-661; John Shaw & Sons (Salford) Ltd v Shaw [1935] 2 KB 113, 134; Salmon v Quin and Axtens [1909] 1 Ch 311; Automatic Self-Cleansing Filter Syndicate Co Ltd v Cunninghame [1906] 2 Ch 34; Imperial Hydropathetic Hotel Co Blackpool v Hampson (1882) 23 Ch D 1; Gramophone and Typewriter Ltd v Stanley [1908] 2 KB 89, 105-106 (Buckley LJ); Towcester Racecourse Co Ltd v The Racecourse Association Ltd [2002] EWHC 2141 (Ch).97 John Shaw & Sons (Salford) Ltd v Shaw [1935] 2 KB 113, 134 (Greer LJ).98 The doctrine of ultra vires was abolished in Australia for companies incorporated under the Corporations Law following the enactment of the Company Law Review Act 1998 (Cth).99 See, eg, Doncon v Doncon (1990) 2 ACSR 385 where the directors were empowered to issue shares.

Page 22 of 54

powers may be shared between the board of directors and the shareholders in general

meeting. It will therefore be a question of the proper construction of a constitutional

clause as to whether the grant of power is exclusive to any one of the internal corporate

organs.100

Pursuant to the Corporations Act, the following matters are required to be decided by the

shareholders in general meeting:

(i) change of name to the company;101

(ii) an amendment to the constitution;102

(iii) consolidating or subdividing the company’s shares;103

(iv) reducing the company’s issued share capital;104

(v) altering the company’s status;105

(vi) a selective buy-back;106

(vii) the giving of financial assistance by a company for the acquisition of its

shares;107

(viii) voluntary winding up of the company;108 and

(ix) giving retirement benefits.109

It is notable that for proprietary companies, the removal and appointment of directors

pursuant to section 203C of the Corporations Act is a replaceable rule which is subject to

modification or replacement in the company’s constitution. Accordingly, the

shareholders of a proprietary company may not have the right to appoint or remove a

director if section 203C of the Corporations Act is displaced or modified by the

company’s constitution. In the context of the role which the board of director’s plays in

corporate governance, given the significance of a shareholder’s right to remove or

appoint the directors, it is questionable whether all proprietary companies should be 100 See, eg, John Shaw & Sons (Salford) Ltd v Shaw [1935] 2 KB 113.101 Corporations Act 2001 (Cth) s 157.102 Ibid s 136.103 Ibid s 254H.104 Ibid ss 256B; 256C.105 Ibid Part 2B.7.106 Ibid ss 257C; 257D.107 Ibid s 260B.108 Ibid s 491.109 Ibid s 200B.

Page 23 of 54

permitted to modify or exclude from the constitution the right of shareholders to appoint

or remove a director. The Corporations Act however requires that directors of public

companies may be removed from office by the shareholders.110

PropositionIt is a proposition advanced by this thesis that section 203C of the Corporations Act

should not be a replaceable rule which may be displaced or modified by a company’s

constitution so as to strengthen shareholders’ rights for the removal and appointment of

directors.

In extraordinary circumstances, the shareholders in general meeting may exercise the

reserve powers. Those circumstances have been determined to include; when the board is

unable to act due to a deadlock,111 or there are insufficient directors to form a quorum at a

board meeting.112

Where shareholders are granted the power to bind the company, the Commonwealth

parliament has adopted the general rule that a simple majority (50% plus 1) of

shareholders permitted to vote is required to pass a resolution unless it is considered

necessary to require a ‘special majority’ of 75% of shareholders.

In Australia, an important aspect of the shareholders acting in general meeting is that the

shareholders do not owe fiduciary duties inter se or to the company.113 Thus a

shareholder which has an interest in relation to a resolution is not prohibited from voting

on the resolution by reason of a legally recognised conflict of interest. The majority of

shareholders however are restricted in two main ways:

110 Ibid s 203D.111 Barron v Potter [1914] 1 Ch 895. It may be inappropriate for a board of directors to be considered to be deadlocked if the shareholders have the power to appoint or remove a director (see Massey v Wales; Massey v Cooney (2003) 47 ACSR 1).112 See, eg, Isle of Wight Railway Co v Tahourdin (1883) 25 Ch D 320; Barron v Potter [1914] 1 Ch 895. It may be noted that generally under a company’s constitution the directors have the power to appoint additional directors even in circumstances where there are insufficient directors to form a quorum pursuant to section 201H of the Corporations Act 2001.113 Pender v Lushington (1877) 6 Ch D 70; Northern Counties Sec. Ltd v Jackson & Steeple Ltd [1974] 1 WLR 1133.

Page 24 of 54

(i) a majority may only modify the company’s constitution in good faith for the

benefit of the company;114 and

(ii) a majority may not pass a resolution which is a fraud on the minority 115 or is

contrary to the interests of the members as a whole or is oppressive to, unfairly

prejudicial, or unfairly discriminatory against, a member or members whether in

that capacity or in any other capacity.116

In Chapter [2], it was discussed that a breach of a director’s fiduciary duties to the

company may be ratified or prospectively authorised. Further, as discussed above, there

are also cases which indicate that fiduciary duties may be attenuated.117 These cases did

not address the question of whether a statutory duty could be attenuated where the

attenuation of the duty amounts to oppressive conduct pursuant to section 232 of the

Corporations Act. There is no authority on this specific question, however there are

relevant legal principles and authority which indicates that a court would not recognise

the attenuation of a statutory duty in respect of proceedings pursuant to section 232 of the

Corporations Act.

As was discussed above, the considerations applicable under section 239(2) are different

to those under section 232. This accordingly permits a court to focus attention on

whether the relevant conduct is contrary to the interests of the members as a whole or

oppressive to, unfairly prejudicial to, or unfairly discriminatory against shareholders.

It will be relevant to consider whether the directors and/or their associates voted, for

example, to modify a provision of the constitution or to authorise the conduct of a

director.118 Where a director has derived an advantage from their own wrong, a court

may be reluctant to recognise the attenuation of a statutory duty, notwithstanding that a

shareholder has a right to exercise their vote in their own interests because the mere act of 114 Allen v Gold Reefs of W Africa Ltd [1900] 1 Ch 656; Rights & Issues Inv. Ltd v Stylo Shoes Ltd [1965] Ch 250.115 Cooks v Deeks [1916] 1 AC 554; Brown v British Abrasive Wheel Co Ltd [1919] 1 Ch 290.116 Corporations Act 2001 (Cth) ss 232(d)-(e). See especially HNA Irish Nominee Ltd v Kinghorn (No 2) [2012] FCA 228.117 See eg. Levin v Clark [1962] NSWR 686.118 See especially HNA Irish Nominee v Kinghorn (No 2) [2012] FCA 228 where the directors used their voting power to approve a ratification resolution.

Page 25 of 54

a minority shareholder voting to attenuate the statutory duty is not likely to be regarded

as oppressive conduct within the meaning of section 232 of the Corporations Act.

A factor which would also be relevant is whether any constitutional amendment or

authorisation resolution was approved by the shareholders in general meeting

notwithstanding the votes of the director(s) and/or their associates.

In HNA Irish Nominee Ltd v Kinghorn (No 2)119 it was held that two shareholders could

not rely on their control of the general meeting to ratify conduct in breach of their

director’s duties,120 however, the ordinary shareholders can ratify a decision taken by the

directors, provided the decision taken by the ordinary shareholders is not itself oppressive

within the meaning of section 232 of the Corporations Act.121

In relation to oppressive conduct, HNA Irish Nominee Ltd v Kinghorn (No 2)122 is a

significant development in relation to the lawfulness of a ratification resolution and the

limitations on the operation of the doctrine of ratification in Australia. The Court held

that the approval by the major shareholders of a ratification resolution was oppressive

pursuant to section 232 of the Corporations Act, ergo oppressive conduct is independent

of the doctrine of ratification. The obiter statements in Angas Law Services did not

consider the possibility that conduct which seeks to give rise to the attenuation of a

statutory duty may be oppressive conduct under section 232 in the sense of HNA Irish

Nominee Ltd.123

The ratio decidendi of HNA Irish Nominee Ltd124 at least includes the following

propositions:

119 [2012] FCA 228.120 HNA Irish Nominee Ltd v Kinghorn (No 2) [2012] FCA 228, [601] (Emmett J).121 HNA Irish Nominee Ltd v Kinghorn (No 2) [2012] FCA 228, [659] (Emmett J).122 [2012] FCA 228.123 HNA Irish Nominee Ltd v Kinghorn (No 2) [2012] FCA 228.124 HNA Irish Nominee Ltd v Kinghorn (No 2) [2012] FCA 228.

Page 26 of 54

(i) that an action of directors is in breach of fiduciary duty will be relevant to

whether there has been unfairness in the context of oppression;125 and

(ii) directors which prefer their own interests over those of another group of

shareholders is capable of constituting oppression and unfair discrimination

within the meaning of section 232 of the Corporations Act.126

The reasoning in HNA Irish Nominee Ltd127 leaves open the legal possibility that where

there is a decision taken by the shareholders in general meeting, provided that the

resolution which authorises the future conduct of directors or amends the provision of a

constitution is not contrary to section 232 of the Corporations Act, the decision of the

shareholders could be effective to attenuate a statutory duty.

At the current time, no authorities have followed HNA Irish Nominee in relation to

statutory oppressive conduct within the meaning of section 232 of the Corporations Act.

I. Public companies listed on a securities exchange

If a company is listed on the Australian Securities Exchange, there are the additional

requirements of the Corporations Act and the ASX Listing Rules which relate to

corporate governance. The key additional requirements are that:

(i) the Corporations Act128 requires that the listed company ensure the continuous129

disclosure of information which is not generally available130 and is information

which a reasonable person would expect to have a material effect on the price or

125 see Sumiseki Materials Co Ltd v Wambo Coal Pty Ltd [2013] NSWSC 235 citing with authority Tomanovic v Global Mortgage Equity Corporation Pty Ltd [2011] NSWCA 104; HNA Irish Nominee Ltd v Kinghorn (No 2) [2012] FCA 228; Re Cumberland Holdings Ltd (1976) 1 ACLR 361; Jenkins v Enterprise Gold Mines NL (1992) 6 ACSR 539.126 See HNA Irish Nominee Ltd v Kinghorn (No 2) [2012] FCA 228, [665] citing with authority Reid v Bagot Well Pastoral Co Pty Ltd (1993) 12 ACSR 197, 205-7.127 HNA Irish Nominee Ltd v Kinghorn (No 2) [2012] FCA 228.128 Corporations Act 2001 (Cth) s 674.129 For companies listed on the Australian Securities Exchange, ASX Listing Rule 3.1 requires that the listed entity must immediately tell ASX that information. The Australian Securities Exchange consider that the word ‘immediately’ means ‘promptly and without delay’, not ‘instantaneously’ (see Australian Securities Exchange, ASX Listing Rules Guidance Note 8 (21 July 2013) Australian Securities Exchange <http://www.asxgroup.com.au/media/PDFs/gn08_continuous_disclosure.pdf>.130 Corporations Act 2001 (Cth) s 676.

Page 27 of 54

value131 of the company’s securities. The law seeks to reduce as far as possible the

ability of a person with ‘inside information’132 the opportunity to use the

information by purchasing or disposing of shares before the information is made

publicly available;133

(ii) the company must have in place a written constitution;134 and

(iii) annual reports are required to outline the entity's compliance with ASX operating

rules, including corporate governance requirements.135

Compliance with ASX Listing Rules is a requirement under the contract the entity enters

into with ASX on being admitted to the official list of companies. Further, the ASX

Listing Rules are enforceable against listed entities and their associates under the

Corporations Act.136

J. Significance of the regulation of corporate governance

In this part of the Chapter, it is necessary at this point to reflect on the significance of the

regulation of corporate governance before embarking upon a consideration of the

importance of the role of shareholders in the context of authorisation.

It is important to note from the preceding discussion that the current rule-based model of

corporate governance regulation established by the Corporations Act requires companies

to implement a minimum standard of corporate governance which is considered by the

Commonwealth parliament to be an appropriate standard of corporate governance. A

company can therefore comply with the minimum standards of corporate governance by

meeting the technical threshold for compliance with the statutory requirements,

irrespective of the size, scale and complexity of the business which the company

operates. The rule-based (threshold) approach to regulation has been criticised by reason

131 Ibid s 677.132 Ibid s 1043A.133 A person involved in a contravention of 674(2) of the Corporations Act 2001 also contravenes the section. The term ‘involved’ is defined by section 79 of the Corporations Act 2001.134 See, eg, Australian Securities Exchange, Listing Rules (at 29 October 2014) r 15.11.135 Australian Securities Exchange, Listing Rules (at 29 October 2014) r 4.10.136 Corporations Act 2001 (Cth) ss 793C; 1101B.

Page 28 of 54

that rules are just a ‘best guess’ as to the future, rules are never perfectly congruent with

their purpose, whether a rule is clear or certain depends on shared understandings and

how a rule affects behaviour does not depend solely on the rule.137 This approach to

regulation is to be contrasted with statutory requirements which adopt a principles-based

or risk-based approach.

A principles-based regulatory model establishes a broad and operative principle. The

advantages of adopting this model of regulation include; the principles are easy to

understand, the avoidance of ‘bright-line’ tests, the avoidance of loopholes and the

flexibility with which the principles can be complied with by companies.138 The major

criticism of this model of regulation is the uncertainty which it can introduce into the

operation of a law and consequently, too much power is given to the executive and to the

courts in applying the legislation.139

A risk-based regulatory model requires the directors to consider the risks which the

company faces in the context of the size, scale and complexity of the business operated

by the company.140 An example of a risk-based regulatory approach is the capital

adequacy requirement for all banks, building societies and credit unions.141 Very few

companies in Australia are required to comply with capital adequacy requirements and/or

the Australian Standard for Risk Management142 which mandates that companies identify,

monitor and put in place measures to control risks faced by the company.143 This model

137 Black, J, Principles Based Regulation: Risks, Challenges and Opportunities (2007) London School of Economics and Political Science, 8.138 See generally Sauder School of Business, Broshko, E. B, Li, K, Corporate Governance Requirements in Canada and the United States: A Legal and Emirical Comparison of the Principles-based and Rules-based Approaches (2006), < http://finance.sauder.ubc.ca/~kaili/BroshkoLi.pdf>139 See generally Office of Parliamentary Counsel, Lovric, D, Principles-based drafting: experiences from tax drafting (30 October 2014) < http://www.opc.gov.au/calc/docs/Loophole_papers/Lovric_Dec2010.pdf>140 See generally Andenas, M, Chiu, I, The Foundations and future of Financial Regulation: Governance for responsibility (Routledge, 2014), 381-382.141 See Australian Prudential Regulatory Authority, APS 110 Capital Adequacy (19 August 2013) Australian Prudential Regulatory Authority <http://www.apra.gov.au/adi/PrudentialFramework/Documents/Basel-III-Prudential-Standard-APS-110-%28January-2013%29.pdf>.142 International Standards Organisation, ‘Risk management – Principles and guidelines’ (ISO 31000:2009), International Standards Organisation, 2009.143 Companies which are required to comply with the Australian Standard on Risk Management include; companies regulated by the Australian Prudential Regulation Authority (such as financial institutions) and Australian Financial Services Licensees including stockbrokers, financial planners and accountants.

Page 29 of 54

of regulation has not been adopted on a broad scale unlike the rule-based and principles-

based regulatory models.

There is unlikely to be a direct and immediate financial benefit to a company which

implements a standard of corporate governance which is higher than the minimum

statutory standard. This arises because generally the risk of failure of a company from

any single event is very unlikely because such events are rare. A company may however

be frequently exposed to the risks of a failure arising from a single event making the

company more likely to fail in the future. By way of example, the insolvency of Lehman

Brothers Holdings, Inc in September 2008 arose from the rapid decline in value of

mortgage-backed securities which it underwrote which in total were circa US$85

billion.144 Clearly, the higher the frequency of exposure to such events, the more likely a

company would be to implement policies, procedures, methods and systems to minimise

the chance of a single event causing the failure of the company.

Given that there is unlikely to be a short-term financial benefit from complying

voluntarily with higher standards of corporate governance, a majority of shareholders of a

company would likely consider that the additional compliance costs are a misallocation

of resources and thus not directed to maximising the profitability of the company. It is

important to recognise that any additional corporate governance regulation will tend to

increase the costs of compliance of a company and therefore there is logically a limit to

regulation beyond which the average company’s costs of complying with the corporate

governance regulation would outweigh the benefits to shareholders and to other

stakeholders.

PropositionIt is a proposition advanced by this thesis that a strictly rule-based approach to regulation

is inconsistent with good corporate governance because all companies are permitted to

legally comply with the minimum statutory requirements for corporate governance,

irrespective of the size, scale and complexity of the company’s affairs.

144 See generally Epiq Systems, Lehman Brothers Holding, Inc (26 October 2014) Epiq Systems debtorMatrix < http://dm.epiq11.com/LBH/Project>.

Page 30 of 54

The regulation of corporate governance is in part designed to be beneficial to

shareholders and separately to stakeholders including employees and creditors of a

company. In summary, the significance of corporate governance regulation to

shareholders is to:

(i) encourage diligence by the directors in carrying out their fiduciary and statutory

duties;

(ii) discourage unethical or unlawful behaviour by directors;

(iii) require companies to implement internal controls;

(iv) require the disclosure by directors and other officers of conflicts of interest;

(v) establish standards for the reporting of financial performance by a company;

(vi) require disclosure of financial information for the benefit of shareholders making

informed decisions;

(vii) permit shareholders to inspect the company’s books in specified circumstances;

(viii) protect shareholders’ equity;

(ix) permit shareholders to enforce legal rights arising from the regulation of corporate

governance; and

(x) permit the Australian Securities & Investments Commission to commence action

against directors and other officers who breach their statutory duties.

The above points arise directly from the regulation of corporate governance by the

Corporations Act. It has been the progressive implementation of new corporate

governance regulation which has resulted in the above suite of benefits to shareholders.

In particular, from 13 March 2000 members’ remedies were reformed by the Corporate

Law Economic Reform Program Act 1999 (Cth) which enacted a new statutory derivative

action145 to overcome the shortcomings of the common law rule in Foss v Harbottle.146

The regulation of corporate governance is also significant generally because:

145 Corporations Act 2001 (Cth) s 236.146 [1843] EngR 478.

Page 31 of 54

(i) at least in part it protects the interests of stakeholders such as employees and

creditors because there is less likely to be a failure of the company resulting from

inadequate corporate governance;

(ii) it promotes investor confidence in capital markets; and

(iii) it is relevant to the extent to which foreign capital investment is attracted to

Australia.

Whilst the regulation of corporate governance is beneficial to shareholders, it is not a

panacea for preventing corporate governance failures. In Peoples Department Stores Inc.

v Wise,147 the Supreme Court of Canada opined that ‘the establishment of good corporate

governance rules should be a shield that protects directors from allegations that they

have breached their duty of care.’148 The corporate collapses in Australia and

internationally which have highlighted problems with the regulation of corporate

governance or the failure of corporate governance include; Long Term Capital

Management, WorldCom, Lehman Brothers, Enron Corp, AIG, Bear Stearns, Parmalat,

HIH Insurance, One-Tel, Firepower International and Australian Wheat Board.

The understanding of the significance of the regulation of corporate governance as it

relates to shareholders is fundamental to the analysis of whether the underlying principles

of corporate governance are consistent with the principles of authorisation. Before

attempting to consider any such analysis, the next part of this Chapter considers the

importance of the role of shareholders in the context of authorisation.

VIII. IMPORTANCE OF THE ROLE OF SHAREHOLDERS IN THE CONTEXT OF

AUTHORISATION

In this part of the Chapter, the role of shareholders in corporate governance is examined

and an analysis undertaken of whether the shareholders’ power of ratification is

consistent with the principles of corporate governance considered earlier in this Chapter.

147 [2004] 3 SCR 461.148 [2004] 3 SCR 461, 491 (the Court).

Page 32 of 54

K. The division of power amongst the internal corporate organs

The decisions of the board of directors ultimately determines how funds and other assets

owned or controlled by the company will be employed leaving the shareholders (as

owners of the company) to determine other matters outside of the exclusive powers of the

board of directors.149 A company’s constitution may however vary the powers which are

exclusive to the directors and the shareholders.150

Powers which are exclusively for the exercise of shareholders in general meeting

relevantly include:

(i) the alteration of the constitution of the company;151

(ii) altering rights attaching to shares;152 and

(iii) the authorisation of a prospective breach153 or ratification of a past breach of a

director’s fiduciary or statutory duties.154

The Corporations Act does not mandate that the shareholders in general meeting have a

right to remove a director from office, other than for public companies.155 It is commonly

the case however for proprietary companies that the removal of directors is regulated by

the company’s constitution (including a constitution which adopts the replaceable rules)

and/or a shareholders’ agreement.

L. The shareholder’s right to vote

149 The powers given to the equivalent of the board of directors of a body corporate incorporated under an Act may be different to the powers given to the board of directors of a company incorporated under the Corporations Act 2001. A determination of the powers which are specific to the board of directors may only be determined by considering the specific legislative scheme pursuant to which the body corporate was incorporated.150 See R P Austin, I M Ramsay, Ford’s principles of Corporations Law (LexisNexis Butterworths, 13th ed, 2007), [7.070]. Further, special rules relate to the powers of a director who is a sole director and sole shareholder (see section 198E of the Corporations Act 2001 (Cth)).151 Corporations Act 2001 (Cth) s 136.152 Ibid Part 2F.2.153 Winthrop Investments Ltd v Winns Ltd [1975] 2 NSWLR 666.154 Bamford v Bamford [1970] Ch 212; Angas Law Services Pty Ltd (In liquidation) v Carabelas [2005] HCA 23.155 Corporations Act 2001 (Cth) s 203D.

Page 33 of 54

In Angas Law Services Pty Ltd (In liquidation) v Carabelas,156 the High Court followed

the English decision of Bamford v Bamford157 which concluded that shareholders are

entitled to ratify or excuse directors’ breaches of fiduciary duty by ordinary resolution. It

is important therefore to consider the extent to which a shareholder may be excluded

from voting on a proposed resolution for the ratification or authorisation of a breach of

fiduciary or statutory duties.

Subject to the rights established by a company’s constitution, the company may issue a

class of shares which exclude the right to vote. Accordingly, there may shareholders who

have all of the rights attaching to their shares (such as the right to receive a dividend), but

not the right to vote at a general meeting of the shareholders. In such circumstances, the

shareholders entitled to vote on a resolution at a general meeting is a subset of all of the

company’s shareholders.

PropositionIt is a proposition advanced by this thesis that the ability of a company to issue classes of