Embed Size (px)

Citation preview

The history of litigation.

Construction, appropriation, and the use of legal norms in economic life,

late XVIIth-XXth centuries

The warrant agricole (1880-1914) : interstitial form or makeshift legal innovation ?1 Patrice Baubeau, Université Paris X Nanterre, IDHE (UMR 8533)

Introduction : the warehouse warrant, a « minor » historical point

In economic history, the warehouse warrant belongs to that category of obscure forms

cryptically alluded to in passing, as if it were so familiar to both author and reader that any further

explanation was pointless.2 Indeed, it is quite difficult to find out what exactly should be known

about it : here the word masks the meaning, as if quoting it exhausted the topic through mere

reference to a dictionary definition.3 Admittedly, the warehouse warrant is a particular credit

instrument, the study of which can hardly claim to encompass the whole of French economic

history, since it played at most a minor role in trade and commerce. With such a marginal

phenomenon, it seems justified not to enter into the complex details of its evolution and operations,

even though it would certainly provide a fresh insight into the mechanisms of credit. However, by

accepting the added burden of integrating its story into a more general narrative, one can hope to

capture a specific set of issues, of conflicts and compromises, of which the warehouse warrant was

both the crux and the outcome.

Even this may be too general a claim, though, since this legal object was not only obscure

and complicated, it was also diverse. In and of itself, the long list of its various French incarnations

– warehouse warrants could be commercial, agricole, hôtelier, pétrolier, industriel, financier… –

illustrates how many different goals it was supposed to fulfill, and consequently how many different

1 Pierre Gervais translated this text from a rather shabby French version, and, doing so, made extremely

useful remarks and comments : translating parochial legal concepts is a powerful way to refine them and reach a more

general meaning. Thank you, Pierre. 2 A notable exception is André Gueslin, Les origines du crédit agricole, Nancy : Annales de l’Est, Université

Nancy II, 1978, 454 p. 3 See e. g. the article « Warrant », by Victor Saverot, in Yves Guyot and A. Raffalovich (dir.), Dictionnaire

du Commerce, de l’industrie et de la banque, Paris : Guillaumin, [1901], vol. 2, pp. 1685 sq. One should also note that

the next entry, « warrant agricole, » has no author name and is merely a word for word copy of the 1898 Act.

Patrice Baubeau 15/03/2007

2

technical, economic and legal forms this credit instrument had to adopt in order to do so. One of

these forms in particular, the warrant agricole, struck us as exceptionally interesting. The birth,

after a long, drawn-out political and social debate, of this modified version of the original

warehouse warrant as it had appeared in France also marked the beginning of a very slow shift in

credit Law, thanks to a makeshift legal construction quite exceptional in itself. The warrant

agricole thus combined two characteristics; it was one of the credit instruments most slowly

introduced and taken up by its end users in recent French history — both introduction and adoption

each took almost forty years —, and at the same time it eventually brought about several notable

reforms and changes. Moreover, because of its « hybrid »4 character, it provides us with a fresh

perspective on the peculiarities and reciprocal relationships of the various branches of French Law,

while also serving as a reminder of the strength of precedent in legal change. Lastly, and most

importantly, both the creation and the use of the warrant agricole was governed by social and

political balances of power which bring to light the ways in which Law is constructed and operates.

The term warrant commercial (« commercial warrant ») was an imitation of the English

term « warehouse warrant, » and was introduced when this particular instrument became allowed

under French Law, thanks to the Acts of 1848 and 1858. The term warrant agricole (« agricultural

warrant »), however, is not the result of English influence, but was chosen to express the notion that

the sphere of application of the warrant commercial was to be enlarged to include goods owned by

farmers. We will see in the present article that this extension raised a number of questions, but

probably the most notable point is that both the English warehouse warrant and the French warrant

commercial were legally based on a pledge, called nantissement in French Law. However, such a

pledge or nantissement was valid only once the pledged property had been put into the actual

possession of the creditor, either by being given over to the creditor directly, or by being entrusted

to a mandated third party. The warrant agricole on the other hand was very peculiar insofar as it

entailed continued possession of the pledged property by the debtor ; it was therefore a non-

possessory pledge of property under the farmer’s custody, securing a farm commodity warrant, or

more concisely a non-possessory agricultural warrant. Thus, the main difference between a

warehouse warrant and the warrant agricole was that in the case of the latter, the pledge was not

displaced. However, it is very important to note here that while French Law had never recognized a

pledge without displacement until the warrant agricole was introduced, such a pledge had long

been an accepted practice in economic life.

4 As the notion is proposed by Robert Boyer, « Evolution des modèles productifs et hybridation : Géographie,

histoire et théorie », Working Paper n° 9804, CEPREMAP, December 1997, 71 p., and as such relating to the very

process of its evolution.

Patrice Baubeau 15/03/2007

3

The construction of the legal form warrant agricole was embedded within a set of legal

norms governing credit, collateral securities, bankruptcy and the commercial nature of an activity,

and makes for an exceptionally complex story. A possible point of entry into this story is provided

by the question of the commercial nature of agricultural notes and of the agricultural occupation in

general. Indeed, rural access to credit was also at stake, and with it the entire process of

monetarization in the countryside, since this process took place through the diffusion of banknotes,

which themselves resulted from discounting operations.5 Lastly, the discourses legitimizing and

defending the usefulness of this warrant provide a window onto the more general issues raised by

the transition from a landed capitalism, based on real estate and fixed capital, to a new capitalism,

maybe not financial, but certainly personal (i.e. based upon transferable goods and securities). The

agricultural world took a long time to adapt to this new capitalism, based on personal property and

circulating capital ; indeed, prompted by the hesitations of some, and the fears of others, the

Republicans eventually put a sacralized French agriculture out of bounds in the 1880s and 90s.

Because the warrant agricole had such a hard time finding its place in legal

categorizations, agricultural practices and the historical experience of economists, it can truly be

said to be an interstitial form, in complete contrast with the objects of histoire totale. But this very

marginality is enlightening, since it helps us question the boundaries of norms and practices. While

apparently a story of complete failure, the warrant agricole actually provided the basis for the

development of new legal notions, which would later achieve considerable influence. Between

failure and success, agriculture and commerce, legal forms and practical uses, the warrant agricole

sheds light on the processes of interpretation, of appropriation and of transformation of Law

considered as an economic, social and political language.

5 On this issue, cf. P. Baubeau, Les « cathédrales de papier » ou la foi dans le crédit. Naissance et subversion

du système de l’escompte en France. Fin XVIIIe – Premier XXe siècle, unpubl. Ph. D., dir. by Michel Lescure,

University Paris X Nanterre, 2004, 680 p.

Patrice Baubeau 15/03/2007

4

I. The warrant agricole, an interstitial legal form

1.1. The warrant, secured or unsecured credit?

Commercial paper

The 1807 Code de commerce (commercial Law) recognized only bills of exchange,

promissory notes and generally speaking credit obligations, without ever mentioning what they had

in common, i. e. their nature as commercial paper (effets de commerce). However, this latter

denomination, or the equivalent effets commerçables, was already in common use under the Old

Regime. Indeed, all these paper notes were parol obligations (titres chirographaires) ; they had

value and were binding solely because they were signed by the drawer or the debtor, and they could

circulate simply through endorsement. Credit instruments of this kind generally followed the

principles governing the bill of exchange, which constituted in many ways their archetype6.

Commercial paper was a credit obligation mostly used to finance a sale. Moreover, it

made possible the actualization of the sale while deferring actual payment to some other time or

place. Lastly, commercial paper was « endowed with the faculty of passing from hand to hand by

the means of an endorsement, »7 a practice specific to the commercial world. Broadly speaking,

there were two classes of commercial paper. Some paper was commercial « by nature » (par

nature), the best illustration of this category being the bill of exchange, even though it was also

dealt with in the Code civil.8 This meant that a bill of exchange, regardless of who had signed it,

6 Cf. Jean Hilaire, Introduction historique au droit commercial, Paris : PUF, 1986, especially the chapter on

« Les effets de commerce », pp. 251-303. Cf. also Raymond de Roover, L’évolution de la lettre de change du XIIe au

XVIIIe siècle, Foreword by Fernand Braudel, Paris : Armand Colin, 1953. 240 p. ; and Henri Lévy-Bruhl, Histoire de la

lettre de change en France aux XVIIe et XVIIIe siècles, Paris, Sirey, 1933, 428 p. For later periods, one can use

commercial dictionaries and Law treatises, both numerous and frequently updated. 7 « …doué de la faculté de passer de main en main par la voie de l’endossement, » Charles Coquelin,

« Effets de commerce », in C. Coquelin et Guillaumin (dir.), Dictionnaire de l’économie politique […], Paris :

Guillaumin, 1852, vol. 1, p. 673. 8 A protested bill of exchange was often considered a check, which for some XIXth century authors would put

into question its commercial nature. This is due to the fact that under French commercial Law, a bill of exchange is a

commercial transaction « by nature, » i. e. considered as such regardless of the actual professional status of its drawer,

as long as the latter is of adult age and mentally competent. Checks and other such drafts, however, can be either

commercial or non-commercial, depending on the professional status of the drawer. Since, ever since the codification

of the beginning of the XIXth century, a bill of exchange was deemed complete with a 3rd signer, the lack of acceptance

could be taken as meaning that the bill of exchange was incomplete, and therefore was possibly not a bill of exchange

Patrice Baubeau 15/03/2007

5

pertained first and foremost to commercial Law. Other paper however became commercial paper

only because of the commercial activity (qualité) of their users, in other words because they were

issued by traders9 ; the most common example of this was the promissory note.10

This differenciation had important consequences for the legal status applicable to each kind

of paper. In the context of the renovated French Law of the post-Revolutionary era, commercial

paper ended up being the object of a whole separate branch of private Law, called commercial Law

(droit commercial). In this kind of litigation, the admissible evidence was not the same as under

civil Law, there were specific courts of first instance, the tribunaux de commerce, staffed at least in

part by merchants, and setting specific penalties. However, because of its role as archetype of the

commercial paper, the bill of exchange eventually came to bestow some of its characteristics on

most other commercial paper, regardless of whether it was originally commercial by nature as in the

case of commercial warrants or by intention as in the case of the promissory note. Moreover, the

distinction between ordinary private Law (droit civil) and commercial Law (droit commercial) was

far from clear-cut for at least three reasons. First, this differenciation was an outcome of a wider

movement of hierarchization of legal forms, which culminated in the Codes edicted in the opening

years of the XIXth century. This process led to a complete upheaval, in which custom and common

practice became subordinate sources of Law, over which written rules gained priority. Second, the

specific growth of commercial Law, and its increasing influence over other branches of Law,

eventually eroded its boundaries.11 Lastly, the setting apart of commercial Law cut it off from some

of its sources, both in the Law of nations — jus gentium, what is called today private international

Law — and in public Law, for instance in market, antitrust or police regulations, but also in issues

such as the sovereign's rights over legal tender, or the flag flown by merchant ships.

any more, formally at least. If the drawer was a trader, the transaction would still be a commercial one, but by

destination. But if the drawer was not a trader, or if the commercial nature of his activity could be questioned (most

notably, this was the case with femes covertes), then the transaction could end up being seen not as a commercial one,

but as an acte civil. 9 Under French Law, a « trader » is any person engaged in selling, buying, or manufacturing for the market as

a professional occupation ; however, « officiers ministériels » (notaries, sollicitors…) and peasants cannot be traders –

which means that, in some respect, they retained a part of their Old Regime status. 10 Actually whether a promissory note is of a commercial nature is a much more complex question than

indicated here : G. Ripert and R. Roblot, Traité de droit commercial, Tome 2, 15th edition, by P. Delebecque and M.

Germain, Paris, LGDJ, 1996, p. 266. 11 Cf. in particular the writings of Georges Ripert – cf. infra.

Patrice Baubeau 15/03/2007

6

An unsecured credit ?

All commercial paper, and most particularly the bill of exchange, is almost by definition

constitutive of an unsecured credit, a crédit personnel. This may seem paradoxical, since it is often

stated in the literature that in fine the letter of exchange was secured by its « valeur en

marchandise » (i. e. by the « value received »). Indeed, Courcelle-Seneuil explained that a discount

on « valeurs faites » (negotiable instruments of credit) corresponded to an existing « collateral

security, »12 but immediately added that « each transaction provided the collateral for the paper it

gave occasion to create. »13 Thus the collateral was not provided by the goods in their material

capacity, but by the transaction during which they were traded. Here we can clearly see how the

meaning of the notion of « secured credit » (« crédit réel ») was being altered, since stricto sensu a

credit could be secured only by pledging personal or real property, in accordance with the legal rule

that « credit goes to tangible property »14

We will not explore in detail this historical, economic as well as legal debate, but it seems

necessary to clear up several widespread misconceptions when it comes to the differenciation

between unsecured and secured credit. The insertion in the bill of exchange of the expression

« valeur en marchandise » was supposed to show that the said bill had not been fraudulently drawn

up between its two first signers with the sole aim of creating commercial paper which would be

deemed negotiable. Thus the fact that there were actual goods involved, hence an actual

consideration for the transaction, was taken as a presumption that there was an actual outstanding

debt ; but it did not mean that the credit itself was secured by some actual property.

Consequently, the goods referred to in a bill of exchange were merely evidence used to

prove that this particular commercial paper was indeed based on an outstanding debt. From this

point of view, the bill of exchange drew much of its strength from the intrisic pledge of payment at

maturity it was supposed to entail. For as long as the bill of exchange was for « valeur en

marchandise, » or value received — and leaving aside some of the complexities of this issue —, it

stood for an outstanding debt which was bound to be cancelled upon resale of the goods which had

been bought thanks to the credit thus extended. Let us take the example of a trader buying goods

from a manufacturer. Once again simplifying the issue somewhat, we can see the manufacturer as a

creditor, and the trader as a debtor. Because the trader sold his goods to consumers who were

obliged to pay cash, he could count on receiving the currency with which he would be able to pay

12 J.-G. Courcelle-Seneuil, Traité théorique et pratique des opérations de banque, Paris : Guillaumin, 4th ed.,

1853, p. 93. 13 « chaque affaire sert de gage au papier à la création duquel elle donne lieu, » Ibid. 14 « le crédit est fait à la chose, » quoted by André Gueslin, op. cit., p. 25.

Patrice Baubeau 15/03/2007

7

his debt. The maturity of this debt corresponded to the length of time the debtor would need to

realize the sales which would enable him to repay his creditor. This is why the bill of exchange has

been called a « self-liquidating credit. »

More generally, unsecured credit is characterized by the fact that it expresses a degree of

confidence in the ability of the debtor to repay his debt at maturity. Strictly speaking, an unsecured

credit is a measure of a borrower's personal standing. Therefore, the ability of a trader to sell the

goods thus bought on credit would have been far more significant than the value of these same

goods.

In contrast, all secured credit relies on a collateral security. The creditor is secure because

in the case of a debtor defaulting on a matured note, he can ask for a writ of execution against the

assets pledged as collateral to the loan, and recover his property thanks to these assets. Credits on

mortgages or on pledges, and even in a way indentures, hostage-taking or ransoming, belong in this

category of secure credits.

Here again, therefore, we should put aside the misleading notion that secured credit would

have been naturally a safer, somehow, and/or more archaic form than unsecured credit ; any

comparative assessment had to take into account both context and the specific modes of credit

chosen by the parties.

Last, we should also qualify both categories, since they shared a significant common

ground. First of all, all secured credit was also unsecured to a certain extent ; as Adam Smith put it,

no lender would loan to a profligate borrower, even on the safest collateral.15

Conversely, many unsecured credits were actually secured up to a point. We have seen

above how in the case of the bill of exchange, it would be absurd to deny that the « valeur en

marchandise » clause actually corresponded to a certain amount of security, albeit limited, even

though the bill of exchange was undoubtedly an unsecured credit in principle. In summary, one

might say that secured and unsecured credits were less mutually exclusive categorization than polar

opposites, with every possible form of credit falling somewhere along the spectrum in between.

Certainly, the warehouse warrant was a kind of commercial paper which fell similarly

someplace in between these two poles :

15 « The man who borrows in order to spend will soon be ruined, and he who lends to him will generally have

occasion to repent of his folly. » Adam Smith, An Inquiry into the Nature and Causes of the Wealth of Nations, 1776,

II.4.2. (http://www.econlib.org/library/Smith/smWN.html)

Patrice Baubeau 15/03/2007

8

- It was an unsecured credit, circulating through endorsement only. Just as with the bill

of exchange, it could be discounted, and its value was enhanced when the number of

endorsers increased, since each signature added an individual surety which

strengthened the overall promise made.

- It was also a secured credit, since its value was backed by collateral security, a personal

asset warranté16, i. e. precisely identified and with which the debtor could not part

without compensation to his creditor.

In its standard commercial version, which was introduced in France most notably by the

acts and décrets of 184817 and 1858,18 the warehouse warrant was the result of the deposit of goods

of an authorized type in a general warehouse (magasin général). In return, the owner of the goods

received a receipt for his deposit (récépissé), which represented a title of ownership to the goods

deposited and could be sold as such, as well as a warrant, or certificate of collateral (certificat de

gage), which the owner could use as collateral security when asking for a loan. In France, the usual

rules of ordinary private Law were applied to this certificate, i. e. that a pledge is complete only

once the pledged assets are deposited in the hands of the creditor or of an agreed upon third party

(art. 2076 C.civ.)

1.2. The issue of the warrant agricole : a social, political and legal debate

The warrant agricole appeared much later than the commercial warehouse warrant, itself a

late innovation in French Law since it was created in 1848. We can already observe here that there

was a significant gap between rules and practice : extending credit on a bill of lading or on a pledge,

whether the pledged assets were displaced or not, was already common practice in France well

before the 1848 act, but this type of operation suffered from an insecure legal environment, and

16 The French « warranté » could be translated by « warranted », which seems to have been only locally used

in London during the XIXth Century. A perhaps more appropriate translation would be « secured » or « granted as a bill

of lading ». But this last translation confuses « bill of lading » (connaissement) and « warrant », while secured sounds to

general. « warranted » will then be used afterwards. 17 Décret of March 21, 1848 ; décret of March 24, 1848 ; décret of March 26, 1848 ; arrêté of the Ministry of

Finances, March 26, 1848 ; décret of August 23-26, 1848 : cf. Archives de la Banque de France (hereafter ABDF), Box

Warrants 3 – File Magasins généraux – 1069199303/3. 18 Acts of May 28, 1858, promulgated June 11, 1858 and décret of March 12, 1859 promulgated March 31,

1859 ; circulaire of the Ministry of Agriculture, Commerce and Public Works of April 12, 1859 : see Dépôt des Lois,

Paris, Muzard Librairie, n° 5653, in ABDF, Box Warrants 3 – File Magasins généraux – 1069199303/3. A major

change in the laws on warrants and magasins généraux took place with the act of August 31, 1870.

Patrice Baubeau 15/03/2007

9

above all could not benefit from an eventual rediscount by the Banque de France, a crucial element

in any system of credit.

Still, a possible adaptation to agriculture of the warehouse warrant was already discussed at

the beginning of the 1850s. For if land banks were already being organized, with the founding of

the Crédit Foncier de France in 1852, followed in 1863 by the creation of the first Crédit agricole,

also originally a land bank, there were as yet no institutions able to provide credit on personal

property, and thus to help finance the new cycles of cultivation and the mechanized tools which

were spreading in the French countryside at the time. Actually, banks were extremely reluctant to

grant loans with only personal property as collateral, because accurate information on rural

borrowers was hard to come by. The inspection reports of the Banque de France are full of

references to the uncertainty surrounding the actual wealth of rural dwellers.19 Anyway, tenant

farmers or sharecroppers could hardly mortgage a land they did not own. Moreover, most of the

personal assets one could find on a farm, and which could be used as collateral, were held as part of

the real estate according to the French definition of biens immeubles (immovables), either par

nature (by the nature of the goods, as with standing crops) or par destination (by destination), and

therefore could not be subjected to seizure by execution, in accordance with article 592 of the Code

of civil procedure.

The primary issue raised by the warrant agricole was thus social: would landowners

accept to give up at least part of their privileged position in favor of second-tier creditors grounding

their claims on mere parol obligations? Would not such an instrument overthrow social hierarchies,

by granting more independence to tenant farmers and sharecroppers, and marginalizing the

landowners, who were supposed to play naturally the role of banker to their tenants?20

This debate also had instant political meaning, since both the Second Empire and the Third

Republic did their best to attract the peasantry and win its loyalty. Republicans who had pondered

Napoleon III's success in this area « can well judge that the peasantry is evolving naturally within

the frame they created, and that agriculture will remain their biggest success. »21 Thus success

depended primarily on the support offered smallholders, whether landowners or tenants, especially

after international markets for agricultural produce downturned from 1880 on. Indeed, « this layer

19 Particularly because of the uncertain legal standing of the biens immeubles (immovables) of a household.

Thus, in Cantal, Banque de France inspectors made reference to the continued use of a regime of dowry, which

deprived the husband from the right to sell the assets his wife brought into the marriage. Cf. for instance the report by

Reiset, Inspector of the Banque de France, on the Aurillac branch, August 16, 1880, ABDF. 20 André Gueslin, op. cit., p. 43. 21 Francis Démier, La France du XIXe siècle, 1814-1914, Paris : Seuil, 2000, p. 434.

Patrice Baubeau 15/03/2007

10

of owner-cultivators working to improve their smallholding with the help of their household »

offered a preview of the kind of society Republicans hoped to bring about.22

Hence the systematic policy favoring this form of agricultural enterprise from the end of

the XIXth century on,23 through protectionist measures such as the so-called Méline Acts of 1885

and especially 1892,24 and also through numerous acts bearing on financial and credit issues. The

latter were designed to help farmers in two main ways :

- institutionally, with the Act of November 5, 1894 creating Crédit mutuel agricole, or

the Act of March 31, 1899, setting up regional mutual agricultural credit unions in the

form of branches of the Crédit mutuel agricole, called caisses régionales, offering

agricultural credit ;

- financially, by mobilizing and directing resources through the Act of November 17,

1897, which set up a Banque de France fee for the benefit of Crédit mutuel agricole, or

the Act of July 18, 1898 on the warrant agricole, and its later modification by the Act

of April 30, 1906.

All in all, from the first debates on pledges in agriculture to the final adoption of what

would be the definitive version of the warrant agricole under French Law, almost forty-five years

had passed by, a rather impressive length of time for a debate on a form of credit which was

supposed not to have played any significant role in the first place.

This is where a third order of discussion comes into play, covering the legal aspects of the

issue.

1.3. The warrant agricole, a legal chimera ?

The warrant agricole was indeed a warrant, but one which introduced a significant

innovation, since the warranted merchandize was kept in the possession of the pledgor, thus

creating a pledge without displacement foreign to the French legal tradition. It is true that an Act of

1863 relaxed the rules governing the transmission of a complete title on a pledge, but the law on

warrant agricoles implied a more fundamental break with tradition, since it did not respect the

principle according to which the collateral used for a pledge had to be transferred to the pledgee-

creditor or to an agreed-upon third party.

22 Serge Berstein, « La politique sociale des républicains », In S. Berstein and O. Rudelle (dir.), Le modèle

républicain, Paris : PUF, 1992, p. 199. 23 Ibid. 24 Pierre Barral, « Un secteur dominé : la terre », In F. Braudel and E. Labrousse, Histoire économique et

sociale de la France, Vol. IV, Part 1, Paris : PUF, 1979, pp. 371-372.

Patrice Baubeau 15/03/2007

11

Moreover, this « agricultural » warrant was not identical to the commercial warehouse

warrants created by the Acts of 1848 and 1858, even though it flowed from them from the point of

view of commercial Law. For a farmer did not always have the commercial status which was

needed to create a true commercial warehouse warrant. This was a second important innovation in

the warrant agricole, since it introduced into a non-commercial sphere a commercial technique.

Thus, it provided one of the first, and one of the best, illustrations of the « commercialization » of

legal processes which George Ripert criticized so virulently, explaining that « Rural life itself has

not escaped this commercialization, and has discovered agricultural credit, warranting harvests, the

shipments of goods on railroads, or payment credits on outstanding invoices. »25 Note that the two

first examples quoted by this most famous expert in commercial Law were precisely these two

innovations so closely linked chronologically, since they appeared in 1894 and 1898 respectively.

There were other consequences here. In spite of the suppression of imprisonment for

debt26 in 1867, commercial Law, and especially that part of securities Law, called droit cambiaire,

which dealt more specifically with credit issues,27 still prescribed nonstandard rules of procedures,

such as speedy judgment, business records as proof, compulsory seizure and sale, declaration of

bankruptcy, etc., all indispensable tools to answer to the need for speed, security and simplicity in

commercial life. Nothing equivalent existed in ordinary private Law, and there was no autonomous

sphere of rural Law. Consequently, there was a distinct tendency to bring these particular

commercial obligations under penal Law through the use of articles 406 and 408 of the Code pénal

on breaches of trust,28 a criminalizing trend which meant the reintroduction of imprisonment for

debt29.

Lastly, while the warrant agricole was drafted by somebody not engaged in commercial

activity, it became nonetheless commercial paper as soon as it had been endorsed, and in this

capacity was receivable in all public institutions of credit, the Banque de France first and foremost,

and also turned all co-signers of the warrant into joint sureties, a clear sign that the whole process

came out of commercial Law.

25 G. Ripert, Aspects juridiques du capitalisme moderne, Paris : LGDJ, 1998 [1951], p. 338. 26 The French « contrainte par corps » is a commercial rule through which a debtor is jailed, at the expense of

his creditor, until he repays his debt. Of course the possibility to put someone in jail for debt, after a trial, had never

been questioned. The law of 1867 only suppressed a kind of preemptive imprisonment. 27 Droit cambiaire was mostly concerned with commercial paper, and indeed its name comes from that

canonical form of all commercial paper, the bill of exchange, more precisely its Italian appellation of cambiale. 28 Article 13 of the Act of July 18, 1898 on warrant agricoles. 29 Because the case was to be judged on the basis of forgery or breach of trust, and not on the basis of the

actual existence of a debt. See note 26 above.

Patrice Baubeau 15/03/2007

12

How are we to understand this baroque construction, part ordinary private Law, part

commercial Law, and part criminal Law ? First of all, it clearly illustrated how much the notion of

Law as a hierarchized and coherent whole, built on principles which manifested themselves

variously in different areas but were fundamentally identical throughout, was in the process of

falling apart at the time. For Paul Jamin, « The year 1900 will mark the end of the reign of the

specialists in ordinary private Law [civilistes] and the death of a certain ideal of droit civil. »30

However, he also warned, this new interest for the evolving branches of Law on the part of his

fellow jurists of the Belle époque was actually mostly focussed on case Law, and led to « juridical

constructions, i. e. general theories. » Hence the fact that a jurist like Demogue (1872-1938),

precisely because he had « tried to follow as faithfully as possible social reality with all its

complexity and fluidity, and even with its contradiction, without ever reducing it to principle for

fear of misrepresenting it », suffered the condemnation of other jurists.31 Conversely, one can feel

the nostalgia for this lost juridical order pervading the writings of Georges Ripert32. Thus Law,

confronted with the political need for action, became a kind of toolbox to which legislators would

turn when building the legal instruments needed to achieve a given political goal.

Obviously, such a legal approach, in spite of undeniable early successes, was bound to run

into difficulties in the long run, as it became increasingly difficult to bring into a common

framework different principles born from practices foreign to each other, a case in point here being

commercial Law and rural life. The warrant agricole took center stage in this evolution of

commercial Law because it appeared at a particular juncture, between the end of the early modern

era of the bill of exchange and the beginning of the contemporary proliferation of commercial

paper. But it remained one of a series of legal chimera, the practical import of which was quite

limited at first considering all the hopes it had raised.

This credit instrument with all its peculiarities was perfectly fitted to the Republican goals

for agriculture. Because it allowed for a pledge in which the pledged assets stayed on the farm, it

30 Paul Jamin, « Dix-neuf cent : crise et renouveau dans la culture juridique », In D. Alland and S. Rials,

(dir.), op. cit., p. 380. 31 Idem, p. 384. 32 In his work quoted above note 16, and also in a famous article from 1934, « L’ordre économique et la

liberté contractuelle », Recueil d’études sur les sources du droit en l’honneur de François Gény, Vol. II, Les sources

générales des systèmes juridiques actuels, Paris ; Vaduz/Paris : Topos Verlag/Duchemin, 1977 [1934], pp. 347-353.

Demogue's work, Notions fondamentales du droit privé, was rightly condemned by François Gény, according to whom

Demogue, albeit his would-be disciple, tended to « dislocate social life », Paul Jamin, op. cit., p. 384.

Patrice Baubeau 15/03/2007

13

made unnecessary costly shipments of the harvests to some storage site, to which farmers would

never have agreed anyway; and the huge warehouses which it would have been necessary to build

for such shipments could be dispensed with, at considerable savings. The warrant was recorded at

the Clerk's office of the nearest lower tribunal (tribunal d'instance, justice of the peace) and was not

held a bankable paper, since only some later endorsement could turn it into an obligation which the

Banque de France would discount in lieu of a third signature. It was also well adapted to the

hierarchical structure, from local branches to regional branches, which was being set up between

1894 and 1899. Lastly, and most importantly, it brought to bear in new directions current political

and legal evolutions. While aimed at giving smallholders better access to credit, it also gave tenant

farmers a right to pledge their harvest which squarely clashed with accepted principles of private

property and with the interests of large landholders who leased their lands.33 The Sénat was well

aware of this aspect, and its members called upon the basic principles of Law when they registered

their opposition to this innovation.34 On the other hand, the agricultural warrant made life more

difficult for creditors, since their collateral security could turn out to be charged with hidden liens.

But the problem dated back to the introduction of the commercial warehouse warrant, and would

only worsen in the XXth century with the proliferation of privileged creditors, whether fiscal or

social security administrations or salaried employees, and the increasingly varied forms of pledges

and mortgages.

33 Article 2 of the Act of July 18, 1898 : « The cultivator not owner or usufructuary of his domain must,

before borrowing any sum, give proper warning to the owner of the property leased, including a description of the

nature, the value and the quantities of goods used as collateral for the loan, as well as the total sums which will be

borrowed. » Thereafter, the property owner, usufructuary or their agent are granted a twelve-days waiting period during

which they can register their opposition; at the end of this period, they are held to be in implied agreement. 34 Thus, during the Sénat session of July 8, 1898, Senator Théodore Girard, backed in particular by Guibourd

de Luzinais, attacked the warrant agricole scheme in the name of the « privilege of the property owner, » and was

vocally approved by members on the Right, Journal Officiel, Sénat, « Séance du 8 juillet 1898, Débats », ABDF, Box

Warrants 1 - 1877-1939, 7e F81 - 1069199303/1, Warrants Agricoles, File 1 - « Discussions à la Chambre et au Sénat »,

Journal Officiel, 1897-1939.

Patrice Baubeau 15/03/2007

14

II. A few indications on all too inconspicuous practices

2.1. The overall failure of the warrant agricole

As we stated above, the warrant agricole was an overall failure. Even in litigation, I was

unable to discover anything significant before 1914: in matters of agricultural litigation on

commercial paper, what was argued was whether it was commercial or not in nature. Indeed, the

failure was immediately perceived,35 and led to an inquiry which in turn resulted in an overhaul of

the law in 1906, with no effect whatsoever in practice.36 Thus, from 1898 to 1905, « the yearly

amount of warrants distributed was 7 million francs. This is a very small sum. »37

More concretely, from 1900 to 1912, i. e. both before and after the adoption of the Act of

April 30, 1906, the amount of warrant agricoles found in the portfolio of the Banque de France

was never superior to 0.1 % of the total amount of discounted securities, obviously an extremely

low figure. Moreover, warrant agricoles did not follow a linear path of development, a fact clearly

observable on Graph 1 (see next page): there was a peak around the years 1906-1909, exclusively

caused by the wine-growing crisis in the South of France.

In point of fact, the warrant agricole had not yet met its audience before the First World

War. There are several possible reasons, invoked either by contemporary students and later

historians of the issue, or by bankers from the Crédit agricole and the Banque de France.

35 Henri Joubert, Le warrantage des produits agricoles, Paris, Arthur Rousseau, 1933. 213 p. 36 André Gueslin, op. cit., p. 306 37 Idem, p. 289.

Patrice Baubeau 15/03/2007

15

Graph 1 - "Warrants agricoles" discounted in the départements by the Banque de France

(current french francs)

Source : ABDF, PV du Conseil général, 1898-1914

First, the credit one could get through this instrument was relatively expensive, because of

the variety of fees it incurred. At the same time the pace of development of local branches of the

Banque de France, at the level of the départements, quickened from the 1890s on, especially after

its charter was renewed in 1897, and resulted in the disappearance of usury from the French

countryside. Also, as far as the first lender was concerned, the debtor was still not liable to

commercial tribunals, in spite of the commercial nature his draft gained once endorsed, and one had

to sue in standard civil jusrisdictions, which led to long, costly, and often uncertain litigation.

Moreover, the Banque de France, at least in the early period, had capped at a rather low 60% its

loan quotas on warrant agricoles, which increased the interest rate on the capital invested (rather

than on the capital borrowed). Lastly, when registering his warrant at the Clerk's office, among

other formal requirements, a borrower had to list all his other charges and show a proof of insurance

for the warranted goods.

Actually, even in the interwar period, the warrant agricole was suffering from the absence

of a suitable, farmer-friendly substitute to the system of magasins généraux (official warehouses).

This substitute would eventually appear with the stockpiling institutions which were developed

Patrice Baubeau 15/03/2007

16

from the end of the 1920s on, and which started playing a major role with the creation of the Office

national interprofessionnel du blé – ONIB – set up under Front Populaire to stockpile wheat

surpluses.38

2.2. The behavior of banks and warrantors

Still, all this is not enough to account for such a failure. Two sets of causes can be

hypothesized, one factual, the second counterfactual.

As we have seen, the creation of the warrant agricole was simultaneous with the founding

of the system of mutual agricultural credit unions backed by the State, and the Banque de France

was asked to open its purse, or more specifically to operate its printing press, in order to back these

two operations. The least one can say is that the Banque de France made no show of enthusiasm.

Only after considerable arm-twisting did its managers accept to grant a 40 Million Franc one-time

subsidy and a yearly contribution to the caisses régionales of agricultural credit, and moreover they

made clear their dislike for this new form of credit, which according to them was not part of the

missions of their institution according to its charter, hence the small quota allowed. This is also the

only reason why we do have a relatively complete series of data on warrant agricoles discounted

before 1914; a wary General board (Conseil général) of the Banque decided to track this kind of

security as part of the quarterly inspection of its portfolio. Noting the failure of the scheme, the

Banque gave up this tracking after the First World War, an unfortunate decision since its is

precisely during the interwar period that the warrant agricole started to be widely used…

The hostility of the Banque de France was even better expressed, and directly so, in the

inspection reports coming from its branches, in which it took two different forms.

First, these reports strove to show that without using any new credit formula, the Banque

de France was still perfectly able to relax its practices without compromising its security. The

recourse to feeder loans, coupled with complete failure in 1906 of a renovated form of warrant

agricole designed specifically for cattle, was thus taken as proof of the futility of legislative

intervention in the matter. For instance, in a rather obvious reference to this, the Crédit agricole

was described as « an artifical institution. »39 Similarly, the creation of two caisses régionales for

agricultural credit in the Nivernais was commented upon as follows: « On the contrary, the

somewhat artificial nature of the Crédit agricole mutuel is most easy to observe here. Over the

whole of the Nivernais, one or two very small caisses are barely able to live a stunted life; they have

38 Created by the Act of August 15, 1936. 39 Inspection of the Nevers branch bank, 1910, digitized version, ABDF.

Patrice Baubeau 15/03/2007

17

been launched by some powerful landowners, and their influence is felt only in the circles

immediately surrounding these landowners, proof positive that any institution of this kind is in the

end no more than the expression of mere personal considerations. »40

A second line of argument questioned the specificity of agricultural credit. The inspector

already quoted above included in his peroration the following maxim, which he attributed to « a

famous financier : “I know only one kind of credit : credit.” »41 This was a direct echo of André

Marie Dupin, who wrote that : « Credit cannot be subdivided, it is but one ; there is no agricultural

credit, there is credit. »42 Indeed, during the Central agricultural congress of 1845, Dupin had

declared his complete opposition to any limitation of the privileged position as creditor of the lessor

(landowner) of a farm (art. 2102 C. Civ), and to any legal reform which would end up weakening

private property.

However, it is also possible to attempt a counterfactual analysis of the failure of the

warrant agricole. As we have seen above, wine-growers provided the main body of users of this

instrument. However, this group did not have at all the traits which were hoped for. First of all,

wine-growers were often traders themselves, and indeed some of them had long used the

commercial warehouse warrant form for their wines. But above all, the warrant agricole as it was

discussed in the parliamentary debates of 1898 and 1906 was supposed to be directed at the widest

possible strata among cultivators, starting with those growing the primary crop at the time, grains.

But this type of warrant was adopted by wine-growers because they found specific advantages for

themselves in the stipulations of the new law.

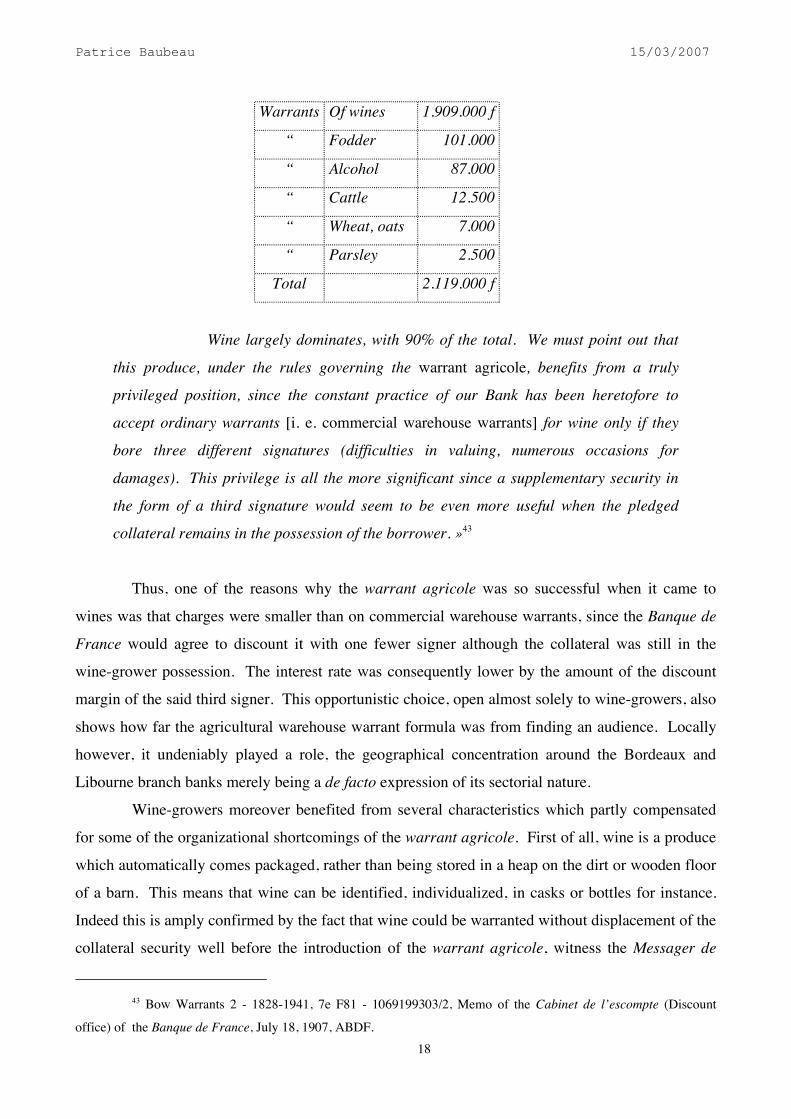

A first tentative explanation can be built using a « Memo on agricultural warrants » dated

1907, emanating from the Banque de France and written in reaction to the wine-grower's

insurrection :

« The first warrant agricoles entrusted to the Banque de France

concerned wines (Bordeaux and Libourne branches). Here are the nature and amount

of the securities presently held in our portfolio according to the latest bimonthly

statements:

40 Idem, 1905. 41 Ibid. 42 André Gueslin, Les origines du crédit agricole, p. 73.

Patrice Baubeau 15/03/2007

18

Warrants Of wines 1.909.000 f

“ Fodder 101.000

“ Alcohol 87.000

“ Cattle 12.500

“ Wheat, oats 7.000

“ Parsley 2.500

Total 2.119.000 f

Wine largely dominates, with 90% of the total. We must point out that

this produce, under the rules governing the warrant agricole, benefits from a truly

privileged position, since the constant practice of our Bank has been heretofore to

accept ordinary warrants [i. e. commercial warehouse warrants] for wine only if they

bore three different signatures (difficulties in valuing, numerous occasions for

damages). This privilege is all the more significant since a supplementary security in

the form of a third signature would seem to be even more useful when the pledged

collateral remains in the possession of the borrower. »43

Thus, one of the reasons why the warrant agricole was so successful when it came to

wines was that charges were smaller than on commercial warehouse warrants, since the Banque de

France would agree to discount it with one fewer signer although the collateral was still in the

wine-grower possession. The interest rate was consequently lower by the amount of the discount

margin of the said third signer. This opportunistic choice, open almost solely to wine-growers, also

shows how far the agricultural warehouse warrant formula was from finding an audience. Locally

however, it undeniably played a role, the geographical concentration around the Bordeaux and

Libourne branch banks merely being a de facto expression of its sectorial nature.

Wine-growers moreover benefited from several characteristics which partly compensated

for some of the organizational shortcomings of the warrant agricole. First of all, wine is a produce

which automatically comes packaged, rather than being stored in a heap on the dirt or wooden floor

of a barn. This means that wine can be identified, individualized, in casks or bottles for instance.

Indeed this is amply confirmed by the fact that wine could be warranted without displacement of the

collateral security well before the introduction of the warrant agricole, witness the Messager de

43 Bow Warrants 2 - 1828-1941, 7e F81 - 1069199303/2, Memo of the Cabinet de l’escompte (Discount

office) of the Banque de France, July 18, 1907, ABDF.

Patrice Baubeau 15/03/2007

19

Paris of September 30, 1877, which reported the warranting of wine in the cellar, without either

displacement or pledge.44

Next, wine was a produce which tended to be stored by the wine-grower or the cooperative

he belonged to, whereas wheat was stockpiled by grain merchants and millers rather than farmers.

This situation is illustrated in the minutes of the general board of the Banque de France, in which

the largest wheat warrants explicitly mentioned are commercial warrants rather than warrant

agricoles.

One reason why wine tended to be stored by wine-growers or cooperatives is that the

formers were also primary processors of their produce, a situation which gave a more commercial

orientation to their activity: « In our region, only wine is warranted, so as not to be sold right away,

but later, either because demand is momentarily flagging, or because the prices offered are so low

that they become unacceptable. »45 Admittedly, this explanation did not fit all French wine-growing

areas, but concerned rather those vineyards from the South of France which, once reconstituted after

the phylloxera crisis, had become highly productive and therefore very sensitive to crises of

overproduction.46

Third, another characteristic of wine important for ordinary warrantage, i. e. not including

high-quality wines, was that if the product was deteriorated, it was never entirely irrecoverable,

since one could use it either to make vinegar or to distill alcohol; this was observed as early as 1867

by the conseil d'escompte (discount board) of the Banque de France.47 Last, wine, as alcohol, was

an easily taxed merchandize, which was consequently watched by French authorities, for which

distillation was also one of the possible means of regulation of markets and inventories.

On the whole, while one of the original goals of the warrant agricole was the mitigation of

the seasonal swings on the grains markets, which always headed down after harvest and up in the

44 Box Warrants 1 - 1877-1939, 7e F81 - 1069199303/1, File « Journaux, 1877-1910 », « Le warrantement en

fabrique », Le Messager de Paris, September 30, 1877, ABDF. 45 Box Warrants 1 - 1877-1939, 7e F81 - 1069199303/1, Barber, Les warrants agricoles Montpellier :

Imprimerie Centrale du Midi – Hamelin Frères, 1902, 11 p. Barber was vice-president of the Caisse Régionale de crédit

mutuel agricole du Midi, Administrator of the Crédit agricole des Syndicats de l’Hérault, and headed the Société

Générale branch in Montpellier, ABDF. 46 Serge Berstein and Pierre Milza, Histoire de la France au XXe siècle, Bruxelles : Complexe, 1995, pp. 48

and 64. 47 « But the same objections cannot be made to ordinary wines, and even less to wines from Hérault, Gard,

etc., which are intended for distillation, and are actually but the raw materials for an industry which ranks among the

most important ones in many départements. », Box Warrants 2 - 1828-1941, 7e F81 - 1069199303/2, Décisions par

produits, ABDF.

Patrice Baubeau 15/03/2007

20

pre-harvest period, the soudure,48 wine-growers put it to quite different uses. Mostly, they used it as

a speculative instrument which enabled them to mobilize an inventory, turning it into working

capital while waiting for more favorable market conditions. And they used warrant agricoles rather

than commercial warehouse warrants mainly to avoid having to move their merchandize, so that it

would stay in the wine storehouse where it would be best kept, and also to earn a rebate compared

with the discount costs of the warehouse warrant.

The case of the warrant agricole is interesting precisely because the logic according to

which it was used diverged from its originally assigned goals. Admittedly, its later destiny was

hardly influenced by this divergence: Jean de Cambiaire remarked in 1954 that « In practice,

warrants are little used: while they do free the borrower from the necessity of finding a surety, they

require the Caisses régionales to maintain a continuous watch, which is a very difficult

endeavour. »49 Given all this, we can now understand why wine-growers later gave up on the

warrant agricole. The décrets-lois of September 28 and October 23, 1935,50 modifying the Act of

April 30, 1906, on warrants agricoles, specified that « The collaboration of Administration des

contributions indirectes [Indirect Tax Revenue Service - ACI], for warrants on wines and alcohol,

non-binding heretofore, becomes compulsory for all that concerns the transfer of these goods

(issuance of receipts or releases by ACI). »51

With this reform, the regulatory status of wines came closer to that of the various kinds of

sugar, for which transfers of ownership have long since been traceable through compulsory

registration in the books of the Régie des Sucres [National Sugar Authority].52 Thus, from the year

1935 on, warrants agricoles for wines were replaced by engagements de garantie (« pledge

agreements »), « which the Caisses demanded in exchange for their granting wine-growers

advances on the grape harvest without asking for a surety. The agreements were registered by

Contributions indirectes and gave Caisses de crédit [agricole] an almost perfect certainty that they

would be refunded. »53

48 I am currently researching this debated question. 49 Jean de Cambiaire, Le Crédit agricole mutuel en France, Albi : Imprimerie coopérative du Sud-Ouest,

1954, p. 120. 50 Box Warrants 1 - 1877-1939, 7e F81 - 1069199303/1, File warrants agricoles, J.O. of September 29, 1935,

p. 10 523, ABDF. 51 Box Warrants 1 - 1877-1939, 7e F81 - 1069199303/1, File warrants agricoles, Typed memo from

Directeur Général de l'Escompte, M. Gravière, « Warrants agricoles, Modifications apportées à la loi du 30 avril

1906 », ABDF. 52 Box Warrants 1 - 1877-1939, 7e F81 - 1069199303/1, File « Journaux, 1877-1910 », « Le warrantement en

fabrique », Le Messager de Paris, September 30, 1877, ABDF. 53 J. de Cambiaire, op. cit., p. 120.

Patrice Baubeau 15/03/2007

21

The warrant agricole instrument was thus used before the War for opportunistic reasons,

so as to benefit from the comparative advantages it offered, which could disappear with each

change in the regulatory and fiscal framework. We perceive here a mode of appropriation of the

regulations which illustrates perfectly the extent to which these regulations show their true meaning

only in reference to a complex whole, both global and local, and which only its users really

understood. We are quite far here from the original intent of the lawmakers...

Conclusion: construction, appropriation and uses without litigation?

In the end, what did the warrant agricole leave behind? As a judicial makeshift

contraption, first and foremost, it did enter posterity, since it was used as a blueprint for warrant

hôtelier (« hotel warrant, » adopted in 1913), then for warrant petrolier (« oil warrant, » created in

1932), and finally for warrant industriel (« industrial warrant »), which, much like the warrant

agricole, became an ever-recurring house ghost in credit Law from 1915 to 1951. Today, a large

proportion of pledges occur without the giving up of pledged property, and while the warrant

agricole certainly was not the engine of this evolution, it was still certainly one of its most notable

expressions and its basic legal model.

Also, the reach of the warrant agricole as an instrument for agriculture was transformed

with the creation by the Front populaire of the ONIB, Office national interprofessionnel du blé,

today's ONIC. Considerable sums were generated as commercial paper during each agricultural

season, endorsed by the ONIB and then rediscounted by the Banque de France; at the end of the

1930s, admittedly a time of commercial recession, up to a quarter of the total value in the Banque's

portfolio was made up of such paper in the weeks following the harvests.54

Lastly, as noted by Georges Ripert, the warrant agricole has remained a symbol of a

definite disturbance in the hierarchized and specialized juridical order which the Codes of the First

Empire had built, as well as a prime example of the breaking down of those quasi-absolute

principles of private property which the Code civil had tried to establish once and for all.

54 For instance, 24 % on October 10, 1939, but in a rather exceptional context. Still, on October 3, 1938, the

total amount reached 7.15 % of the overall portfolio of the Banque de France, i. e. almost 800 times the pre-First World

War figure. Source Annhis.

Patrice Baubeau 15/03/2007

22

From the point of view of the appropriation and uses of Law, we have seen that we can

schematically identify two situations. On one hand, the audience lawmakers were trying to reach

with the warrant agricole generally ignored it. On the other hand, and in complete contrast, wine-

growers who perceived the opportunity gain the warrant agricole was providing compared to the

warehouse warrant eagerly seized upon it. As for the banks, and especially the Banque de France,

they had a role to play with respect to this instrument, but never really promoted its use.