Embed Size (px)

Citation preview

GIRIRAJ AMARNATH

International Water Management Institute (IWMI)

INVESTING IN DISASTER RESILIENCE: RISK TRANSFERTHROUGH FLOOD INSURANCE IN SOUTH ASIA

Photo: World Bank

Workshop on Addressing Disaster Risks Specific to South and South-West Asia

30 - 31 October 2017, Kathmandu, Nepal

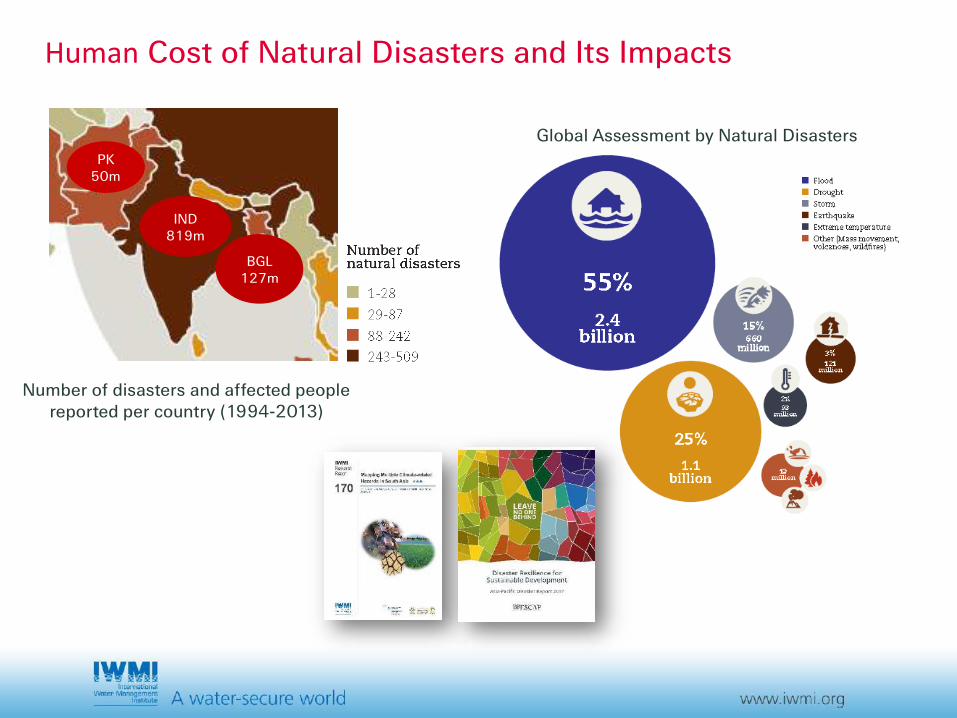

Human Cost of Natural Disasters and Its Impacts

IND819m

PK50m

BGL127m

Global Assessment by Natural Disasters

Number of disasters and affected people reported per country (1994-2013)

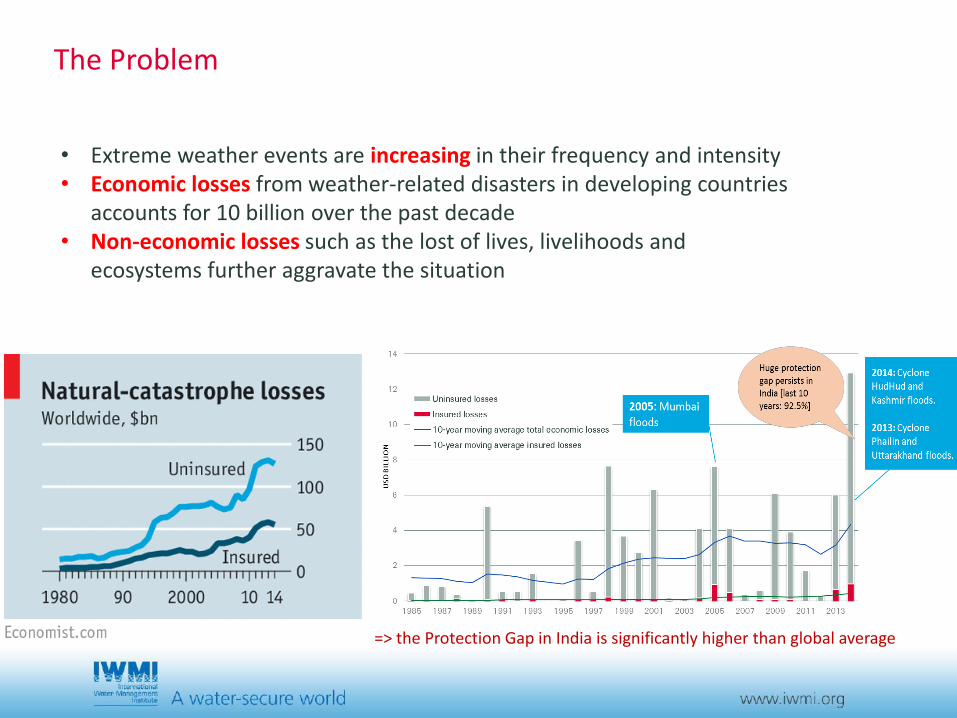

The Problem

• Extreme weather events are increasing in their frequency and intensity• Economic losses from weather-related disasters in developing countries

accounts for 10 billion over the past decade• Non-economic losses such as the lost of lives, livelihoods and

ecosystems further aggravate the situation

=> the Protection Gap in India is significantly higher than global average

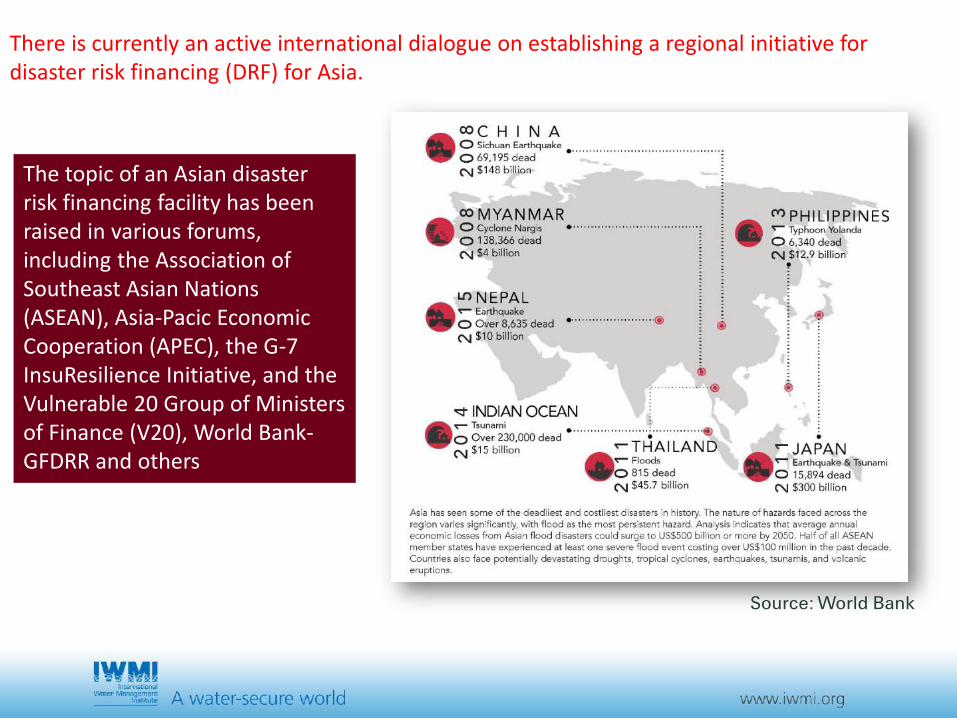

There is currently an active international dialogue on establishing a regional initiative for disaster risk financing (DRF) for Asia.

The topic of an Asian disaster risk financing facility has been raised in various forums, including the Association of Southeast Asian Nations (ASEAN), Asia-Pacic Economic Cooperation (APEC), the G-7 InsuResilience Initiative, and the Vulnerable 20 Group of Ministers of Finance (V20), World Bank-GFDRR and others

Source: World Bank

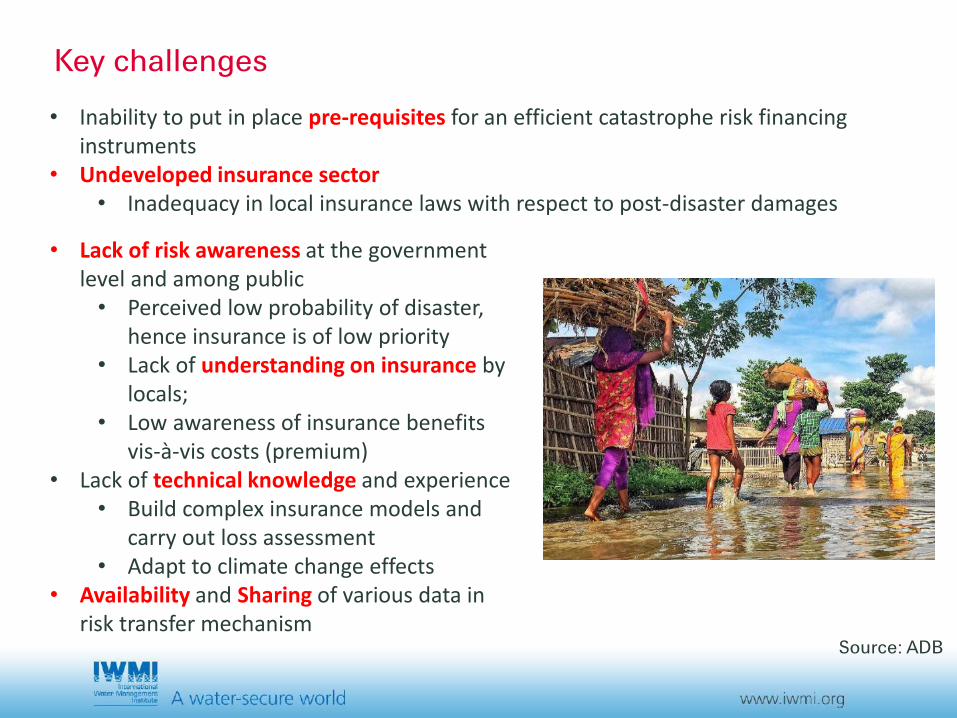

Key challenges

• Inability to put in place pre-requisites for an efficient catastrophe risk financing instruments

• Undeveloped insurance sector• Inadequacy in local insurance laws with respect to post-disaster damages

Source: ADB

• Lack of risk awareness at the government level and among public • Perceived low probability of disaster,

hence insurance is of low priority• Lack of understanding on insurance by

locals;• Low awareness of insurance benefits

vis-à-vis costs (premium)• Lack of technical knowledge and experience

• Build complex insurance models and carry out loss assessment

• Adapt to climate change effects• Availability and Sharing of various data in

risk transfer mechanism

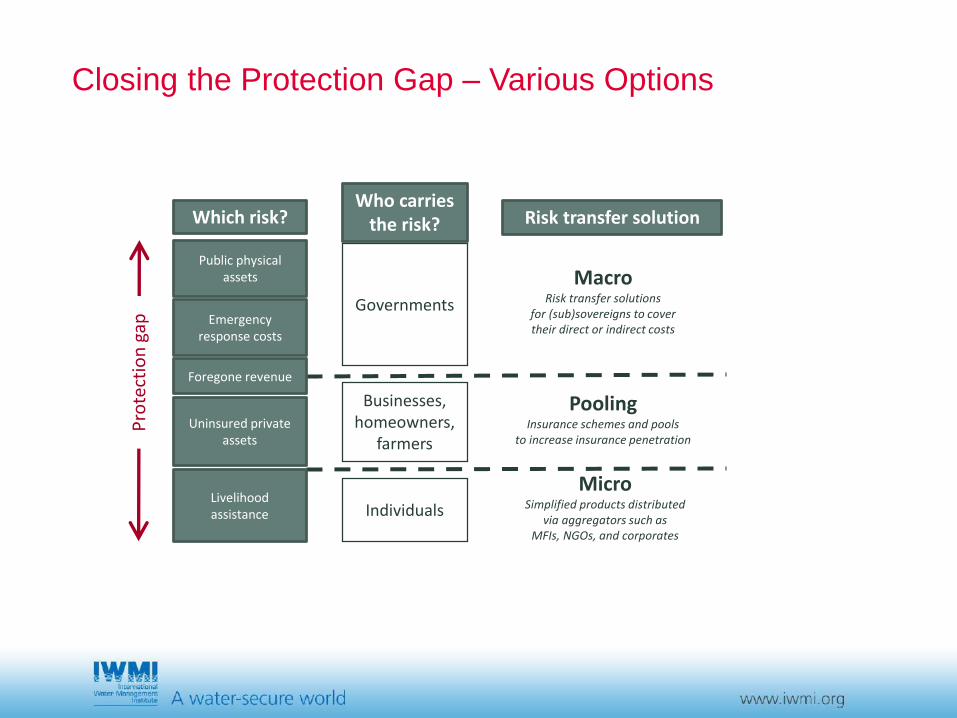

Closing the Protection Gap – Various Options

6

gap

Which risk?

Governments

Who carries the risk?

PoolingInsurance schemes and pools

to increase insurance penetration

MacroRisk transfer solutions

for (sub)sovereigns to cover their direct or indirect costs

MicroSimplified products distributed

via aggregators such as MFIs, NGOs, and corporates

Risk transfer solution

Businesses, homeowners,

farmers

Public physical assets

Emergency response costs

Foregone revenue

Uninsured private assets

Livelihood assistance

Pro

tect

ion

gap

Individuals

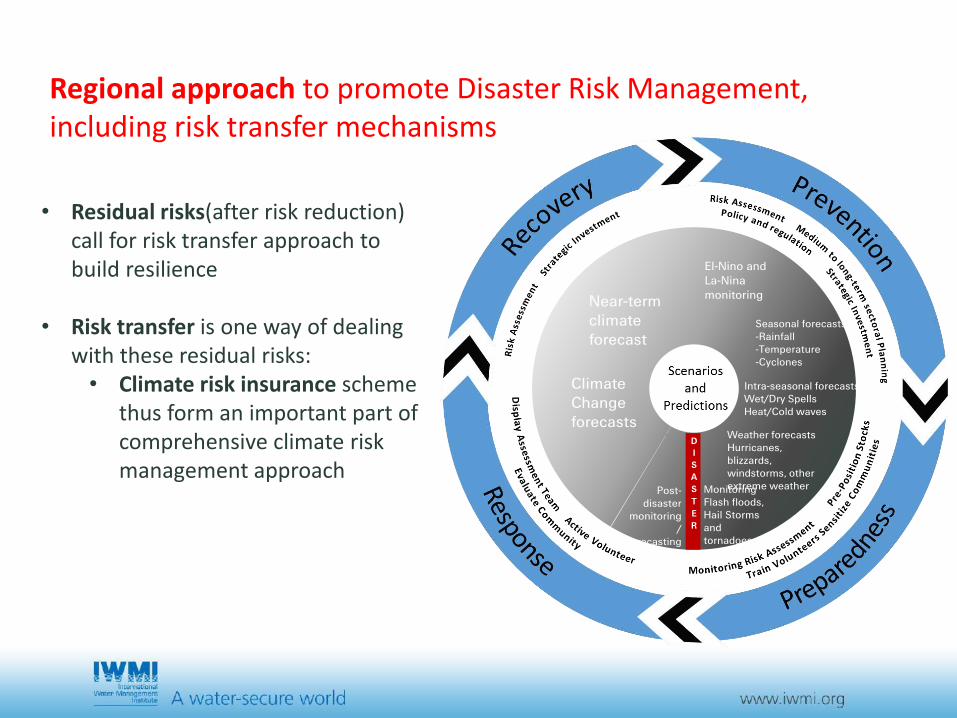

Regional approach to promote Disaster Risk Management, including risk transfer mechanisms

• Residual risks(after risk reduction) call for risk transfer approach to build resilience

• Risk transfer is one way of dealing with these residual risks:• Climate risk insurance scheme

thus form an important part of comprehensive climate risk management approach

El-Nino andLa-Nina monitoring

Seasonal forecasts-Rainfall-Temperature-Cyclones

Intra-seasonal forecastsWet/Dry SpellsHeat/Cold waves

Weather forecastsHurricanes, blizzards, windstorms, other extreme weatherMonitoring

Flash floods, Hail Storms and tornadoes

Post-disaster

monitoring/

forecasting

Climate Change forecasts

Near-term climate forecast

D

I

S

A

S

T

E

R

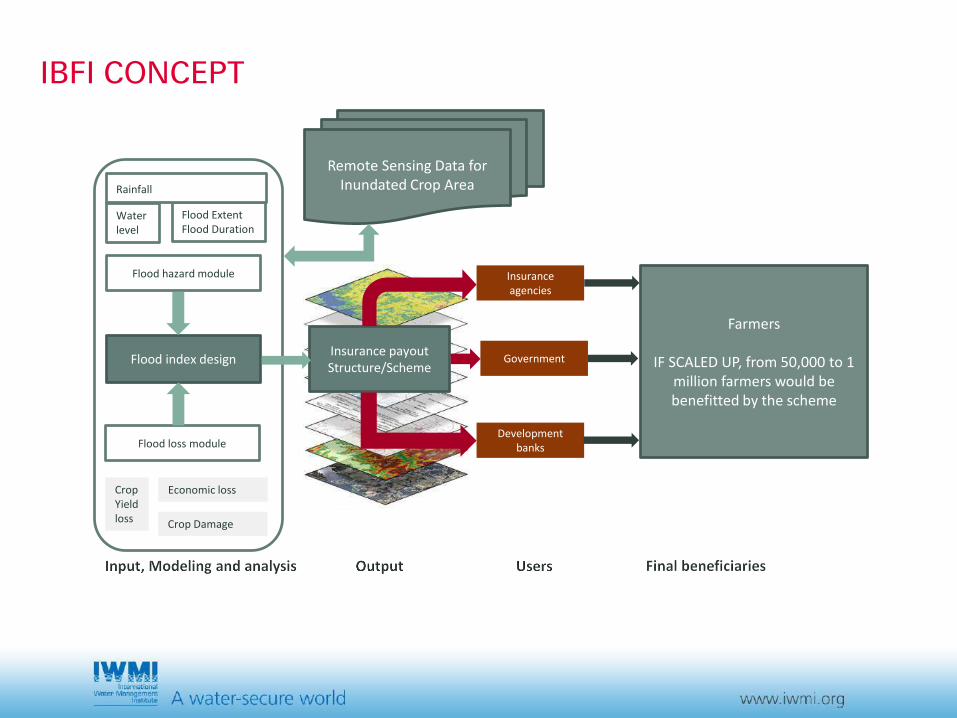

Index Based Flood Insurance (IBFI)

Flood index design

Flood hazard module

Flood loss module

CropYieldloss

Economic loss

Water level

Flood ExtentFlood Duration

Crop Damage

Rainfall

Insurance payout Structure/Scheme

Government

Insurance agencies

Development banks

Farmers

IF SCALED UP, from 50,000 to 1 million farmers would be benefitted by the scheme

Remote Sensing Data for Inundated Crop Area

IBFI CONCEPT

0

500

1000

1500

2000

2500

3000

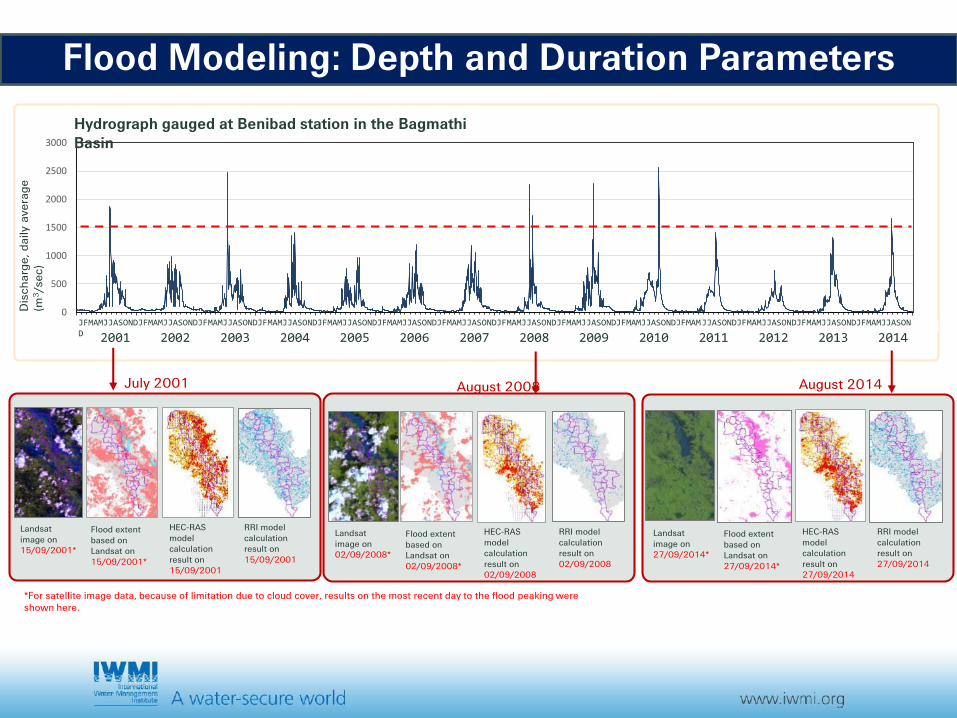

01-Jan-01 01-Jan-02 01-Jan-03 01-Jan-04 01-Jan-05 01-Jan-06 01-Jan-07 01-Jan-08 01-Jan-09 01-Jan-10 01-Jan-11 01-Jan-12 01-Jan-13 01-Jan-14 01-Jan-15

Dis

ch

arg

e,

da

ily

ave

rag

e

(m3/s

ec)

Hydrograph gauged at Benibad station in the BagmathiBasin

August 2014July 2001 August 2008

Landsat image on 15/09/2001*

Flood extent based on Landsat on 15/09/2001*

HEC-RAS model calculation result on 15/09/2001

RRI model calculation result on 15/09/2001

Landsat image on 02/09/2008*

Flood extent based on Landsat on 02/09/2008*

HEC-RAS model calculation result on 02/09/2008

RRI model calculation result on 02/09/2008

Landsat image on 27/09/2014*

Flood extent based on Landsat on 27/09/2014*

HEC-RAS model calculation result on 27/09/2014

RRI model calculation result on 27/09/2014

*For satellite image data, because of limitation due to cloud cover, results on the most recent day to the flood peaking wereshown here.

JFMAMJJASONDJFMAMJJASONDJFMAMJJASONDJFMAMJJASONDJFMAMJJASONDJFMAMJJASONDJFMAMJJASONDJFMAMJJASONDJFMAMJJASONDJFMAMJJASONDJFMAMJJASONDJFMAMJJASONDJFMAMJJASONDJFMAMJJASOND 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

Flood Modeling: Depth and Duration Parameters

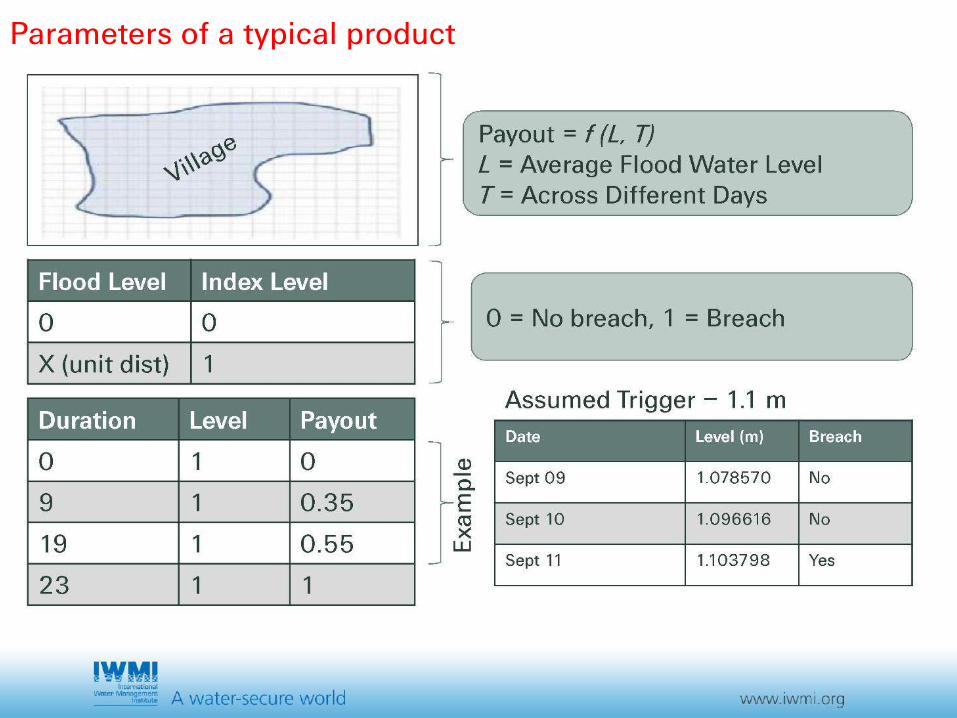

Parameters of a typical product

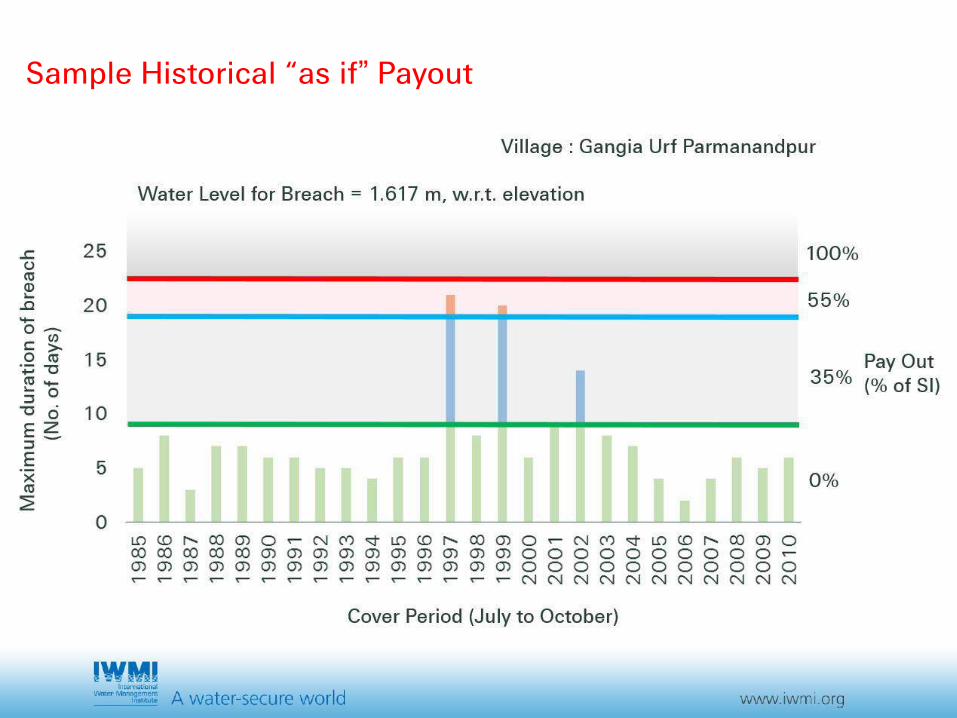

Sample Historical “as if” Payout

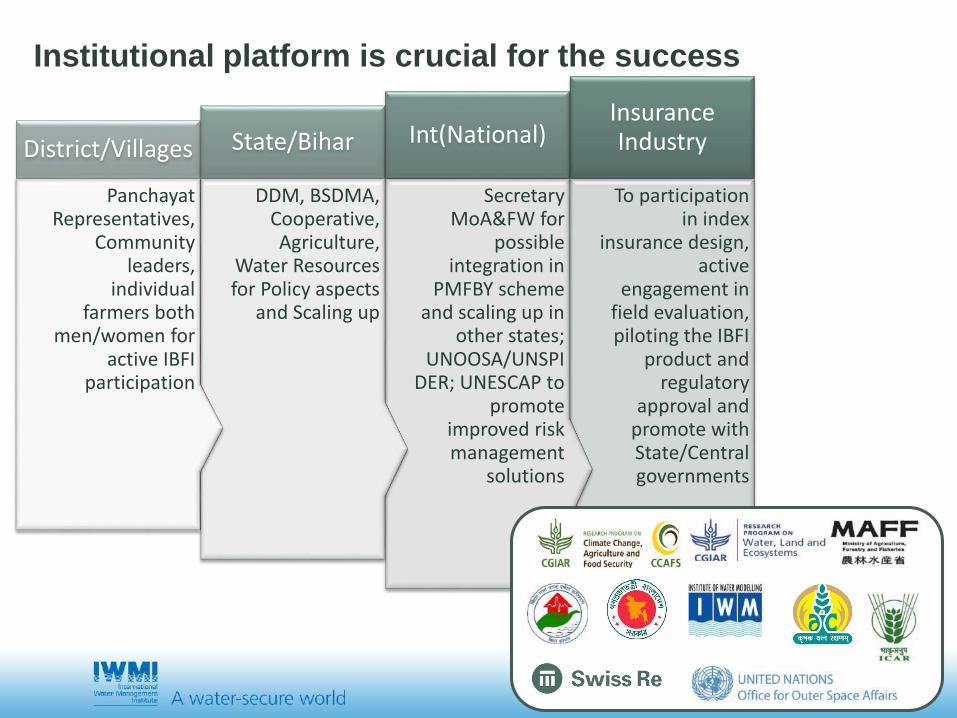

Institutional platform is crucial for the success

To participation in index

insurance design, active

engagement in field evaluation, piloting the IBFI

product and regulatory

approval and promote with State/Central governments

Insurance Industry

Secretary MoA&FW for

possible integration in

PMFBY scheme and scaling up in

other states; UNOOSA/UNSPI

DER; UNESCAP to promote

improved risk management

solutions

Int(National)

DDM, BSDMA, Cooperative, Agriculture,

Water Resources for Policy aspects

and Scaling up

State/Bihar

Panchayat Representatives,

Community leaders,

individual farmers both

men/women for active IBFI

participation

District/Villages

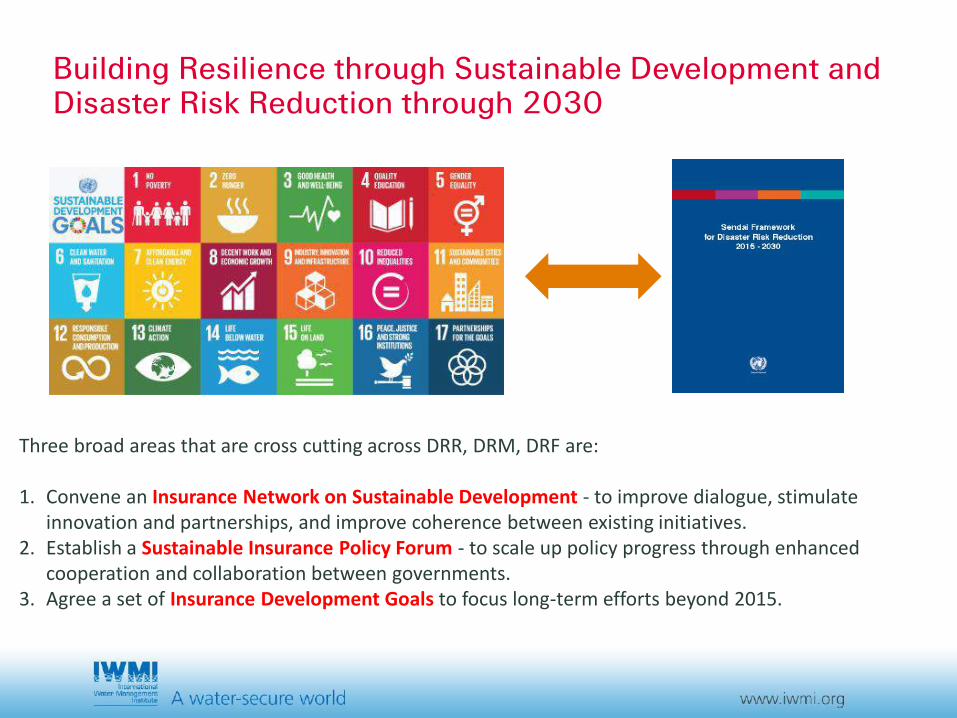

Building Resilience through Sustainable Development and Disaster Risk Reduction through 2030

Three broad areas that are cross cutting across DRR, DRM, DRF are:

1. Convene an Insurance Network on Sustainable Development - to improve dialogue, stimulate innovation and partnerships, and improve coherence between existing initiatives.

2. Establish a Sustainable Insurance Policy Forum - to scale up policy progress through enhanced cooperation and collaboration between governments.

3. Agree a set of Insurance Development Goals to focus long-term efforts beyond 2015.

Conclusions

• Awareness raising and risk education: Insurers and government can partner to make available risk data and information systems.

• Risk pricing: By accurately pricing risk, insurers can incentivise risk reducing decision making.

• Enabling conditions and regulation of insurance programmes: Through legislation, financial oversight and monitoring, government can provide incentives for insurance to promote risk-reducing activities.

• Direct financing of risk reduction measures: Insurers can invest directly in risk reduction measures to avoid large compensation claims.

• Risk reduction as a prerequisite for insurance: As a prerequisite for coverage, insurers can require that policy holders undertake specific disaster risk reduction measures.

Disaster risk management (ex-ante + ex-post) are crucial element of sustainable development to reduce disaster losses and enable achievement of the Sustainable Development Goals.