Embed Size (px)

Citation preview

Investment StrategyEconomy and Financial MarketsAugust 2017

Contents

1 Editorial Better than many had feared

2 Economy Economic upturn amid uncertainty

4 Interest rates and yields Heading for monetary policy tightening

5 Equity markets 2017 emerges as a strong year for equities

6 Currencies Euro strongest currency of 2017

7 Commodities Energy sector looms large

8 Investment Strategy Freshening breeze, squalls easing off

9 Market overview Economic data and cycles Interest rates and currencies Equity and commodity markets Financial markets and forecasts

Impressum

IssuerSt.Galler Kantonalbank AG St.Leonhardstrasse 25 9001 St.GallenTel. +41 71 227 97 00 [email protected]

Analysts

Caroline Hilb Paraskevopoulos, Pascal Stucki (Economy)Patrick Häfeli, CFA, Pascal Stucki (Interest rates and yields)Tobias Kistler, CFA (Equity markets)Daniel Wachter (Currencies, commodities)Beat Schiffhauer, CFA (Investment Strategy)

Editorial deadline

July 21, 2017

Release

Monthly

Title Picture

Costa Itxaspe, Basque region, SpainPhoto: Roland Gerth

August 2017 Investment Strategy 1

Dear investors,

Many of the predictions for 2017 portrayed doomsday scenarios. Following the election of Donald Trump, we were led to believe that right-wing populists would win sweeping political victories across Europe. The financial mar-

kets suddenly started to worry about the Dutch politician Geert Wilders, despite the fact that the Netherlands’ economy is only marginally lar-ger than Switzerland’s, accounting for a mere 1% of global output. Marine Le Pen dominated the headlines, raising the spectre of the end of the euro. Investors gripped by fear scurried for cover in the safe haven of the Swiss franc. This in turn forced the Swiss National Bank to inter-vene in the foreign exchange markets to coun-ter the strength of the franc, increasing its cur-rency reserves by CHF 80 billion in the process. Donald Trump divided the world even before he took office. While some dreamt of tax billions and concrete mixers on the move, others belie-ved the days of free trade were numbered.

Six months on, quite a few things have chang-ed. Geert Wilders is no longer of interest to the headline-makers. Marine Le Pen is licking her wounds and fears for her position at the helm of the Front National. She has been forced to accept that elections cannot be won by pledging to leave the euro. A new king has made his ent-rance into Paris and Versailles to the strains of the European anthem. This has taken some of the pressure off the franc, allowing the SNB to breathe a little more easily. Developments in Washington are more reminiscent of the 1980s TV series «Dallas» than of responsible global and economic policymaking. Relieved, the fi-nancial markets are helping to push the stock-market indices to historic highs.

But the sense of relief among investors is also a danger. The risks have not disappeared from the world of the financial markets, although jud-ging by the record-low risk indicators, such as volatility indices, anyone might think that they had. The conflict with North Korea could get out of control at any time, sending shock waves through the markets, at least in the short term. In Washington, the polarization between a Re-publican party riven by internal divisions and the Democrats, coupled with an administration un-able to act, is threatening to lead to a complete standstill. On top of this, the debt ceiling was reached in March. Unless the ceiling is raised by Congress this autumn, the threat of govern-ment agencies having to shut down will once again loom, along with the risk of a US default. In France, Emmanuel Macron will soon start to lose some of his shine. His reforms will run into opposition, not in parliament, but on the street, with a great deal of media impact.

The financial markets would do well to have a little more sense of reality. The world is not black and white, but many shades of grey. The-se are currently lighter than they have been. The global economy is doing better than at any time since the 2008 financial crisis. This is particular-ly true of Europe and holds out the prospect of a positive second half of the year for investors.

Dr. Thomas Stucki

Chief Investment Officer

EditorialBetter than many had feared

85

90

95

100

105

110

115

44

46

48

50

52

54

56

July 14 Jan. 15 July 15 Jan. 16 July 16 Jan. 17

PMI KOF barometer

PMI Purchasing Managers Index (global) KOF business barometer (Switzerland)

Investment Strategy August 20172

EconomyEconomic upturn amid uncertainty

In the first half of 2017, Switzerland continued to follow a positive economic trend, supported by the international environment. However, de-velopments came with political uncertainties. Far-reaching decisions were due to be taken, with major implications for the future. This peri-od saw the first few months of Donald Trump’s term as US President, for example, along with the triggering of Brexit and the presidential election in France.

At 0.3%, Swiss economic growth in the first quarter remained at the lower end of expecta-tions. A positive change can be inferred from the KOF business barometer which takes the pulse of the Swiss economy. The strong figures at the beginning of the year reflected business confidence that the economic upturn was set to continue. Although the KOF has since dipped again slightly, it remains above the long-term average. In addition to moderate growth in the economy as a whole, the slight fall in unemploy-ment, in progress since mid-2016, continued in-to 2017. However, after rising sharply last year, the number of persons in employment showed barely any further increase during this period. So far this year inflation has remained in the low positive range and therefore meets SNB’s criteri-on for price stability, which sets a limit of 2%. In February, inflation edged up by 0.6% – the highest rate of increase since June 2011. Then in March core inflation – which excludes fresh and seasonal products, as well as energy and fuel – returned to positive territory for the first time since the abandonment of the minimum ex-change rate in January 2015. The growth of the Swiss economy is in line with the global trend. In the first half of 2017, the global economy conti-nued to grow, albeit not at the same pace as in the second half of 2016. Growth led to an im-provement in the international economic en-vironment, which is reflected in rising growth rates and improved conditions on the labour market. The global economy nevertheless re-mains exposed to significant risks owing to the political uncertainties.

Uncertainty as a constantOn 20 January 2017 Donald Trump was sworn in as the 45th president of the United States. His

lack of political experience and penchant for «bold» rhetoric and plans meant that his term of office was awaited with some trepidation. Des-pite this, many investors had high expectations of the President’s actions and expected substan-tial changes in US economic policy. However, such changes have so far largely failed to mate-rialize, and the resulting disappointment has led to a decline in long-term interest rates and yields in the US. Another event was the triggering of the Brexit process in March which set in train the UK’s departure from the EU. There is still con-siderable uncertainty over the precise timetable for Brexit and the nature of its implementation. The exit negotiations will have a major impact

Swiss economy in the slipstream of global growth

Source: Bloomberg

PMI: 50-points line = dividing line between contraction and expansionKOF: 100-points line = long-term average

Foreign currency reserves in CHF bn EUR/CHF exchange rate

1.00

1.05

1.10

1.15

1.20

1.25

1.30

200

300

400

500

600

700

800

2012 2013 2014 2015 2016 2017

SNB foreign currency reserves EUR/CHF

August 2017 Investment Strategy 3

Source: Bloomberg

on the future relationship between the EU and the UK. By contrast, Europe responded with reli-ef to the outcome of the French presidential election on 7 May. Marine Le Pen, the candida-te of the far-right National Front, did not emer-ge victorious. Instead, the pro-European Emma-nuel Macron was elected as the new president, ensuring stability in Europe and the EU. In addi-tion, an absolute majority in France’s parliamen-tary elections has provided Macron with the ne-cessary basis for economic reforms.

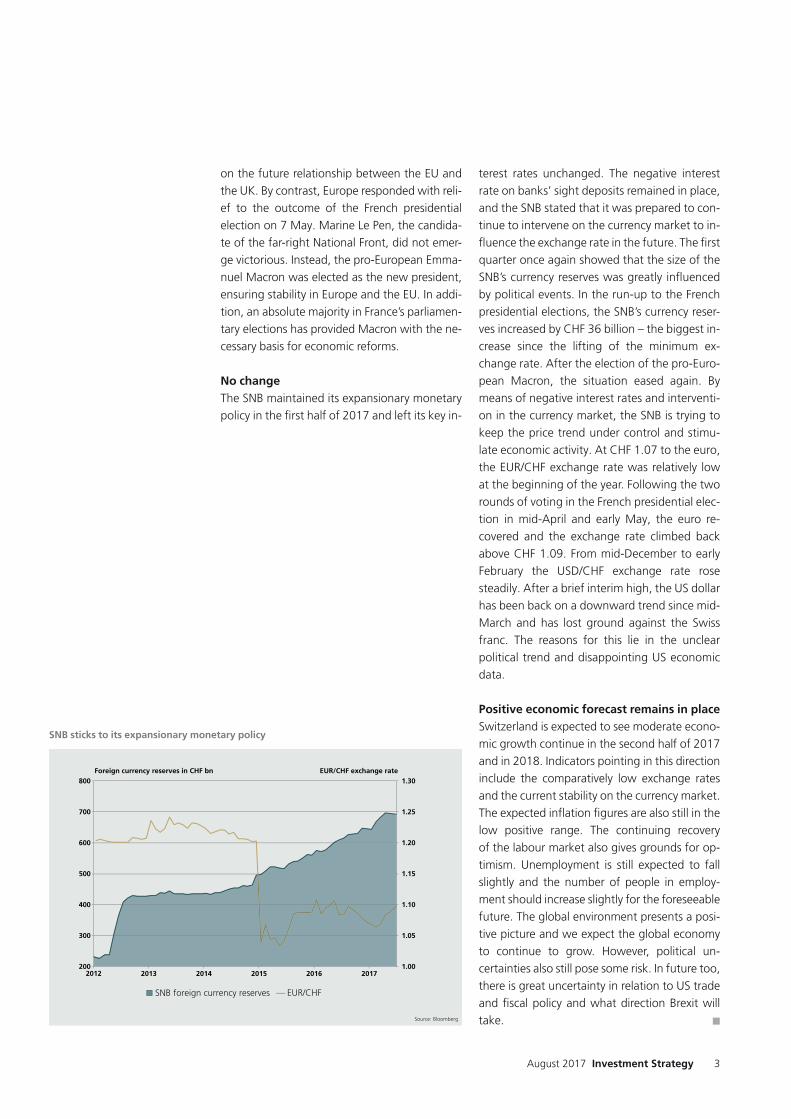

No changeThe SNB maintained its expansionary monetary policy in the first half of 2017 and left its key in-

terest rates unchanged. The negative interest rate on banks’ sight deposits remained in place, and the SNB stated that it was prepared to con-tinue to intervene on the currency market to in-fluence the exchange rate in the future. The first quarter once again showed that the size of the SNB’s currency reserves was greatly influenced by political events. In the run-up to the French presidential elections, the SNB’s currency reser-ves increased by CHF 36 billion – the biggest in-crease since the lifting of the minimum ex-change rate. After the election of the pro-Euro-pean Macron, the situation eased again. By means of negative interest rates and interventi-on in the currency market, the SNB is trying to keep the price trend under control and stimu-late economic activity. At CHF 1.07 to the euro, the EUR/CHF exchange rate was relatively low at the beginning of the year. Following the two rounds of voting in the French presidential elec-tion in mid-April and early May, the euro re-covered and the exchange rate climbed back above CHF 1.09. From mid-December to early February the USD/CHF exchange rate rose steadily. After a brief interim high, the US dollar has been back on a downward trend since mid-March and has lost ground against the Swiss franc. The reasons for this lie in the unclear political trend and disappointing US economic data.

Positive economic forecast remains in placeSwitzerland is expected to see moderate econo-mic growth continue in the second half of 2017 and in 2018. Indicators pointing in this direction include the comparatively low exchange rates and the current stability on the currency market. The expected inflation figures are also still in the low positive range. The continuing recovery of the labour market also gives grounds for op-timism. Unemployment is still expected to fall slightly and the number of people in employ-ment should increase slightly for the foresee able future. The global environment presents a posi-tive picture and we expect the global economy to continue to grow. However, political un-certainties also still pose some risk. In future too, there is great uncertainty in relation to US trade and fiscal policy and what direction Brexit will take. n

SNB sticks to its expansionary monetary policy

-1%

0%

1%

2%

3%

4%

5%

6%

02 03 04 05 06 07 08 09 10 11 12 13 14 15 16 17

Key interest rates in the US, Europe and Switzerland

SNBFed ECB

Investment Strategy August 20174

Interest rates and yieldsHeading for monetary policy tightening

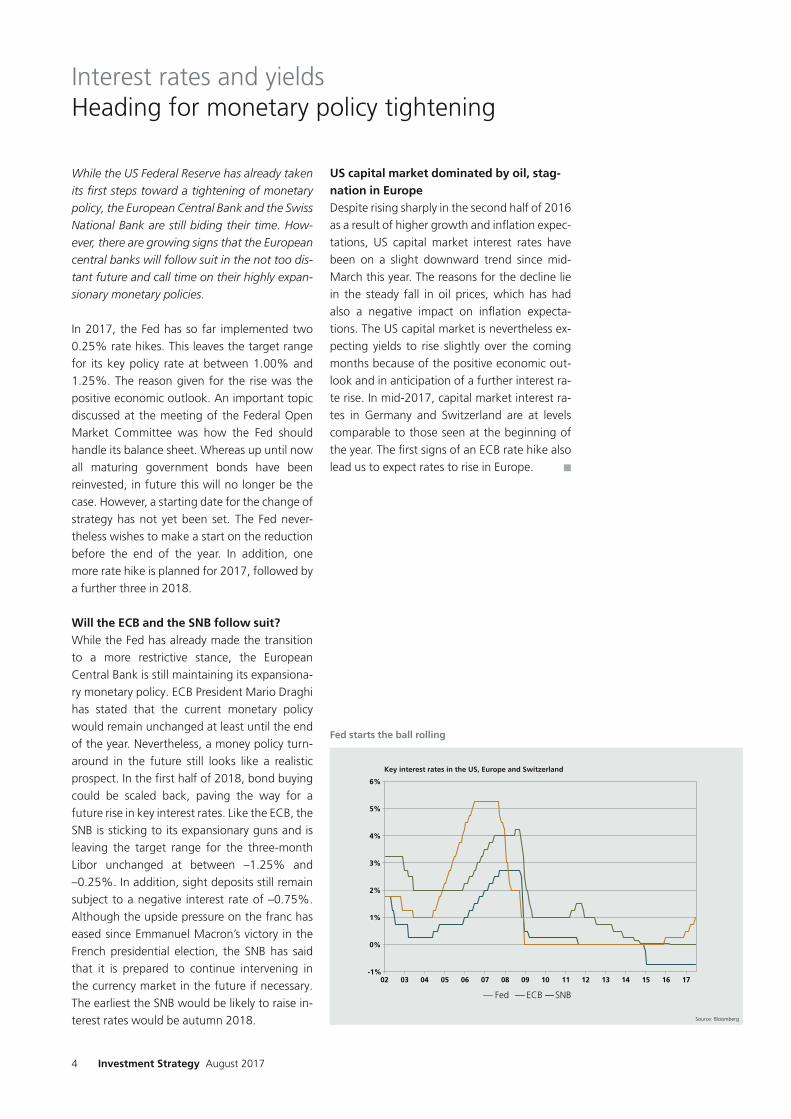

While the US Federal Reserve has already taken its first steps toward a tightening of monetary policy, the European Central Bank and the Swiss National Bank are still biding their time. How-ever, there are growing signs that the European central banks will follow suit in the not too dis-tant future and call time on their highly expan-sionary monetary policies.

In 2017, the Fed has so far implemented two 0.25% rate hikes. This leaves the target range for its key policy rate at between 1.00% and 1.25%. The reason given for the rise was the positive economic outlook. An important topic discussed at the meeting of the Federal Open Market Committee was how the Fed should handle its balance sheet. Whereas up until now all maturing government bonds have been reinvested, in future this will no longer be the case. However, a starting date for the change of strategy has not yet been set. The Fed never-theless wishes to make a start on the reduction before the end of the year. In addition, one more rate hike is planned for 2017, followed by a further three in 2018.

Will the ECB and the SNB follow suit?While the Fed has already made the transition to a more restrictive stance, the European Central Bank is still maintaining its expansiona-ry monetary policy. ECB President Mario Draghi has stated that the current monetary policy would remain unchanged at least until the end of the year. Nevertheless, a money policy turn-around in the future still looks like a realistic prospect. In the first half of 2018, bond buying could be scaled back, paving the way for a future rise in key interest rates. Like the ECB, the SNB is sticking to its expansionary guns and is leaving the target range for the three-month Libor unchanged at between –1.25% and –0.25%. In addition, sight deposits still remain subject to a negative interest rate of –0.75%. Although the upside pressure on the franc has eased since Emmanuel Macron’s victory in the French presidential election, the SNB has said that it is prepared to continue intervening in the currency market in the future if necessary. The earliest the SNB would be likely to raise in-terest rates would be autumn 2018.

US capital market dominated by oil, stag-nation in EuropeDespite rising sharply in the second half of 2016 as a result of higher growth and inflation expec-tations, US capital market interest rates have been on a slight downward trend since mid-March this year. The reasons for the decline lie in the steady fall in oil prices, which has had also a negative impact on inflation expecta-tions. The US capital market is nevertheless ex-pecting yields to rise slightly over the coming months because of the positive economic out-look and in anticipation of a further interest ra-te rise. In mid-2017, capital market interest ra-tes in Germany and Switzerland are at levels comparable to those seen at the beginning of the year. The first signs of an ECB rate hike also lead us to expect rates to rise in Europe. n

Source: Bloomberg

Fed starts the ball rolling

0%

5%

10%

15%

Jan. Feb. Mar. Apr. May June

Index performance in the first half of 2017

SPI SPI Extra STOXX Europe 600 S&P 500

25%

20%

August 2017 Investment Strategy 5

Equity markets2017 emerges as a strong year for equities

pliers Sika and EMS-Chemie and the luxury goods groups Richemont and Swatch. Poor per-forming sectors included insurers and automo-tive suppliers, with stocks such as Swiss Re and Autoneum even recording negative performan-ces for the first half of the year.

What moved the markets?Apart from the strong quarterly figures, the main drivers moving the stock markets were po-litical factors and the positive leading economic indicators. While the initial euphoria over Presi-dent Donald Trump has increasingly evaporated, investor sentiment was boosted by the political developments in Europe. Specifically, the elec- tion of Emmanuel Macron as President of France gave the European stock markets impetus from April onwards. This was also reflected in the per-formance of the currency market, with the euro strengthening by around 9% against the green-back during the first six months of the year. At the same time, the global economic indicators continued to improve across a broad base, parti-cularly in Europe.

Focus returns to central banksTowards the end of the first half of 2017, atten-tion refocused on the central banks. In June, the Fed raised rates by 0.25% for the second time this year and promised a continuing moderate approach to the rate hike cycle. The simultane-ous economic growth and robust company re-sults meant that the stock market took a positi-ve view of this development. The European Cen-tral Bank also hinted that it would be modera-ting its expansionary monetary policy in the fu-ture.

What next?The company reporting season for the second quarter is picking up momentum and will shape events on the stock markets over the coming weeks. So far, companies have fulfilled expecta-tions and the outlook for the current reporting season is good. On the other hand, expectations of significantly higher corporate earnings are al-ready discounted in current high share prices. Over the medium term, the economic data, and contingent on these, the interest rate trend, will exert the strongest influence on share prices. n

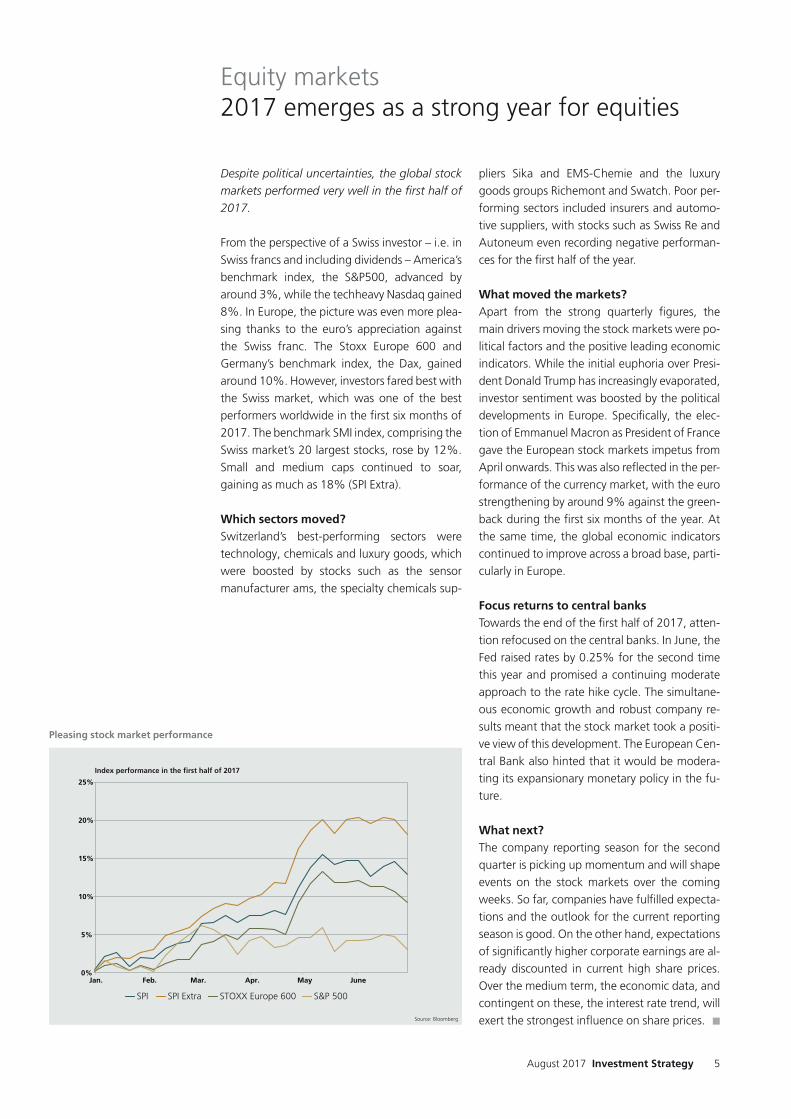

Despite political uncertainties, the global stock markets performed very well in the first half of 2017.

From the perspective of a Swiss investor – i.e. in Swiss francs and including dividends – America’s benchmark index, the S&P500, advanced by around 3%, while the techheavy Nasdaq gained 8%. In Europe, the picture was even more plea-sing thanks to the euro’s appreciation against the Swiss franc. The Stoxx Europe 600 and Germany’s benchmark index, the Dax, gained around 10%. However, investors fared best with the Swiss market, which was one of the best performers worldwide in the first six months of 2017. The benchmark SMI index, comprising the Swiss market’s 20 largest stocks, rose by 12%. Small and medium caps continued to soar, gaining as much as 18% (SPI Extra).

Which sectors moved?Switzerland’s best-performing sectors were technology, chemicals and luxury goods, which were boosted by stocks such as the sensor manufacturer ams, the specialty chemicals sup-

Source: Bloomberg

Pleasing stock market performance

0.6%

1.2%

3.0%

3.2%

3.5%

3.9%

5.1%

5.2%

10.4%

Swedish krona

Australian dollar

Swiss franc

Norwegian krone

New Zealand dollar

Canadian dollar

British pound

Japanese yen

US dollar

Appreciation of the euro between the beginning of the year and 21 July

Investment Strategy August 20176

CurrenciesEuro strongest currency of 2017

The foreign exchange market experienced a shift of focus during the first half of 2017. While the dollar’s weakness has become accentuated in re-cent months, the euro has made broad-based gains. Since mid-April, the dollar has fallen back 10% against the euro and is also well below parity against the Swiss franc. Confidence in the US administration’s ability to push through its poli-tical agenda has been dented. A breakthrough on the issue of healthcare reform – a key com-ponent of the Republicans’ election platform – has so far failed to materialize, for example. We also have yet to see any specific measures on in-frastructure investment or tax cuts. In the conti-nuing absence of any positive element of surpri-se in the US, the focus has shifted.

Euro rides a wave of positive sentiment As the foreign exchange market has grown ac-customed to the Fed’s tighter monetary policy, the financial markets have been turning their attention to the timing of a change in the ECB’s monetary policy as a new cue. A further factor is that since the election of Emmanuel Macron, France and Germany have been showing a uni-ted front – externally at least – on the issue of euro reforms. They are being supported by an improvement in economic conditions in the eurozone, which has prompted ECB President Mario Draghi to make positive statements on the performance of the economy. For the time being, Draghi is referring to the autumn, when more information will be available on the eco-nomy and inflation. The euro has benefited in advance from speculation over a tightening of ECB policy. However, the unilateral positioning in favour of the euro has also significantly raised expectations.

Pound sterling – progress on negotiations as test of sentiment A year after the Brexit referendum, the British economy is so far proving resilient. Brexit has mainly taken place in the media and in the poli-tical arena. The UK remains a member of the EU with all rights and obligations. With the trigge-ring of its exit application at the end of March, the UK entered a two-year transition phase. The

pound and the Conservative party took a hit in June when the government lost its absolute majority in the early general election. Prime Minister Theresa May has since succeeded in forming a minority government. This, coupled with the absence of any background noise on the Brexit negotiations, has benefited the pound recently. Those within the Bank of Eng-land who advocate a rise in interest rates are also growing in number. A rate rise would sup-port the pound.

Commodity currencies – mixed first halfThe commodity currencies had mixed fortunes in the first half of 2017. They are benefiting from the economic upturn in the global econo-my, but are suffering from weaker commodity prices. If the situation in the commodity sector remains stable over next few months, particu-larly in relation to oil, the picture will continue to improve for the commodity currencies, i.e. the Australian dollar, the Canadian dollar and the Norwegian krone. n

Source: Bloomberg

Euro strongest G10-currency

Price trend between the beginning of the year and 21 July

-12.8%

1.4%

3.8%

8.3%

8.8%

19.5%

WTI crude

Silver

Platinum

Gold

Copper

Palladium

August 2017 Investment Strategy 7

In 2016, the international commodity markets trended firmer across the board for the first time in six years. However, the broad-based Bloomberg commodity index is currently down 5% on the beginning of the year. The oil price is a major factor here.

The trend of oil prices is at odds with Opec’s ef-forts to achieve some sort of market equilibrium. In recent months, Opec has failed to keep oil prices above USD 50 per barrel despite produc-tion quotas. The expansion of US production, coupled with high levels of stocks worldwide, still stands in the way of a substantially higher oil pri-ce. Over the coming months, we shall therefore be focusing on the inventory trend in particular.

Gold trending sidewaysAfter getting off to a strong start at the begin-ning of the year, precious metal prices – with the

exception of palladium – also shifted down a gear. Since the end of January, gold has been tra-ding at between USD 1,200 and USD 1,300 per ounce. However, within this range larger move-ments were observed in line with varying interest rate expectations. After the USD 1,200 mark was tested – and held – at the beginning of July, the pendulum went on to swing back the other way later in the month. Doubts about the Fed’s rate hike path lent gold some impetus. US inflation receded from the Fed’s 2% target, reducing the likelihood of a further Fed rate hike this year – a likelihood already priced into Fed funds futures – to less than 50%. This, coupled with the weaker dollar, supports the gold price. Given the benign stock market environment, safe havens such as gold have not been at the forefront of investors’ concerns lately. In this situation, little is likely to change over the next few weeks. While the im-mediate political risks in Europe have receded, the global economic outlook remains positive. This means that the Fed can be expected to stick to its chosen interest rate path, limiting the up-side potential for gold.

Industrial metals rally stalls After the price rally enjoyed by many industrial metals in 2016, this year has seen a more sober mood set in. The price rise was previously accom-panied by extensive speculative buying. Emer-ging doubts over the announced US infrastruc-ture projects and mixed signals coming out of China led to a reduction in speculative positions, some of which had been large. Copper was not left unscathed either, and by May saw its price fall by 10% from its high at the beginning of the year. By contrast, industrial metals have benefi-ted from the robust economic data of recent months and copper prices have also since been back on a rising trend. Given its substantial influ-ence over the copper market, China remains a key driver. As a major producer and consumer of commodities, China’s government is continuing to modernize its own economic structures. It is increasingly trying to get the country’s credit risks under control. At the same time, China is trying to reduce its overcapacity in the commodity and industrial sectors. The speed and thrust of these efforts will have correspondingly large knock-on effects on industrial metals. n

CommoditiesEnergy sector looms large

Source: Bloomberg

Energy prices lag behind

Investment Strategy August 20178

The eurozone is currently enjoying ideal sailing conditions. The outlook for the economy and earnings is providing a steady, solid tailwind. Brief squalls have provided added momentum.

After the elections in France and the Nether-lands, it looks as though the stormy political gusts are easing off again, giving way to a steady economic breeze. The economy is making better headway than in the US and there appears to be little standing in the way of a further institutional consolidation of the eurozone. It seems the ne-gative headlines surrounding the eurozone are history. Caution is still called for, however. The euro crisis has already been declared over on many occasions only to flare up again shortly afterwards.

The good ship Europe has gained stabilityHowever, some five years after the outbreak of the euro crisis, the eurozone slowly seems to ha-ve found a viable way of tackling its persisting problems calmly and without commotion. On the one hand, it is now clear that the eurozone’s key players, such as Germany and France, have the necessary will to keep the ship on course and continue to stabilize it. The ECB’s new rules on the liquidation of failing banks have an impor-tant part to play by paving the way for swift, tar-geted action to deal with floundering financial institutions. The new standards include clear guidelines on state aid and investor sharehol-dings and enable the supervisory authorities to intervene without fuelling broad-based uncer-tainty. Spain’s Banco Popular, for example, was sold to Banco Santander for a symbolic one euro under pressure from the ECB. The share capital and subordinated bonds (EUR 3.3 billion in total) were completely written off. However, nothing changed for the bank’s customers and priority bondholders.

Could choppy waters rock the boat?However, if the ECB makes waves, the resulting choppy waters could make for a rather uncom-fortable ride on the stock markets. The ECB’s liquidity floodgates are currently wide open which is keeping yields low and equity valuations high. As the economy makes increasing progress and as the US Fed Funds Rate continues to rise,

Investment StrategyFreshening breeze, squalls easing off

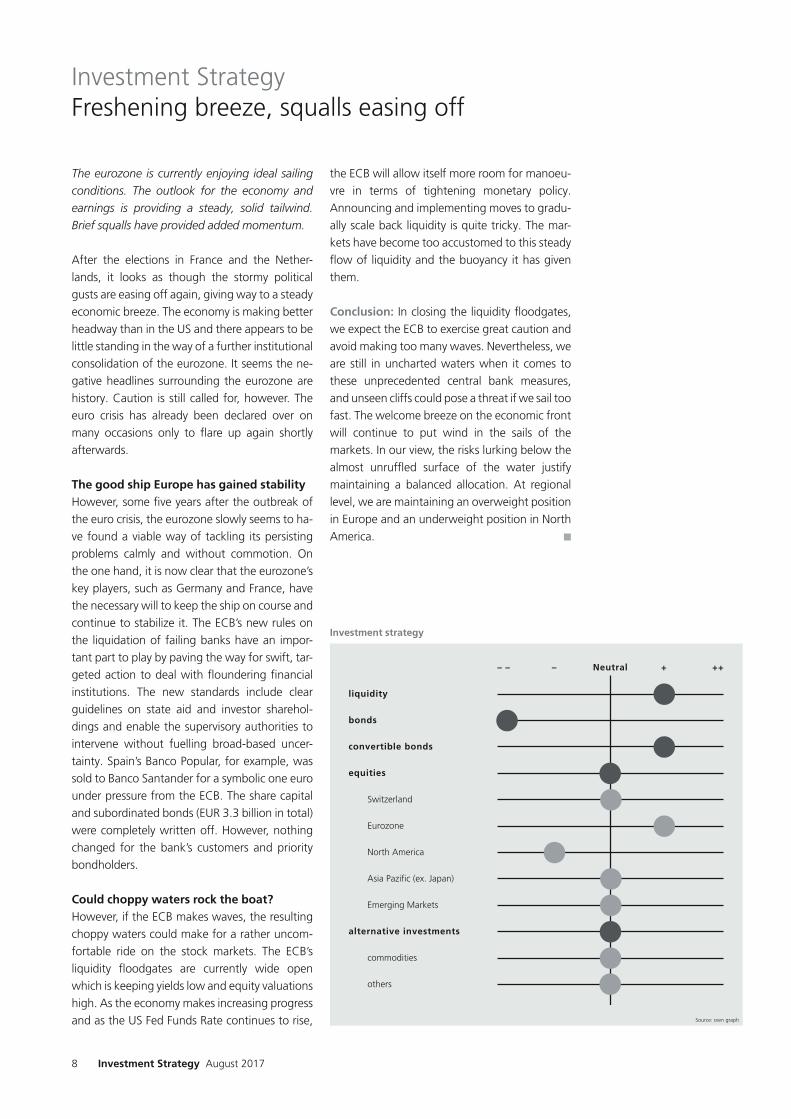

Investment strategy

the ECB will allow itself more room for manoeu-vre in terms of tightening monetary policy. Announcing and implementing moves to gradu-ally scale back liquidity is quite tricky. The mar-kets have become too accustomed to this steady flow of liquidity and the buoyancy it has given them.

Conclusion: In closing the liquidity floodgates, we expect the ECB to exercise great caution and avoid making too many waves. Nevertheless, we are still in uncharted waters when it comes to these unprecedented central bank measures, and unseen cliffs could pose a threat if we sail too fast. The welcome breeze on the economic front will continue to put wind in the sails of the markets. In our view, the risks lurking below the almost unruffled surface of the water justify maintaining a balanced allocation. At regional level, we are maintaining an overweight position in Europe and an underweight position in North America. n

liquidity

bonds

convertible bonds

equities

Switzerland

Eurozone

North America

Asia Pazific (ex. Japan)

Emerging Markets

alternative investments

commodities

others

– – – Neutral + ++

Source: own graph

August 2017 Investment Strategy 9

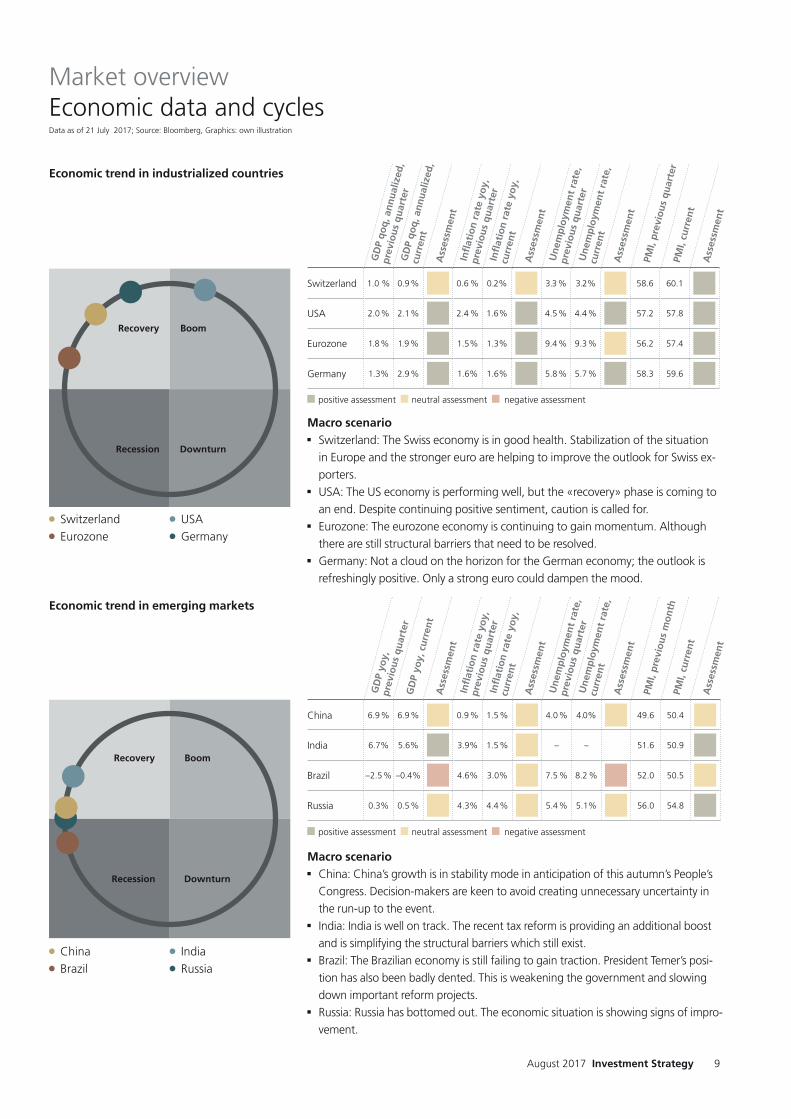

Market overviewEconomic data and cycles Data as of 21 July 2017; Source: Bloomberg, Graphics: own illustration

Economic trend in industrialized countries

Switzerland USA Eurozone Germany

Switzerland 1.0 % 0.9 % 0.6 % 0.2% 3.3 % 3.2% 58.6 60.1

USA 2.0 % 2.1 % 2.4 % 1.6 % 4.5 % 4.4 % 57.2 57.8

Eurozone 1.8 % 1.9 % 1.5 % 1.3% 9.4 % 9.3 % 56.2 57.4

Germany 1.3% 2.9 % 1.6% 1.6% 5.8 % 5.7 % 58.3 59.6

GD

P qo

q, a

nnua

lized

,

prev

ious

qua

rter

GD

P qo

q, a

nnua

lized

,

curr

ent

Ass

essm

ent

Infl

atio

n ra

te y

oy,

prev

ious

qua

rter

Infl

atio

n ra

te y

oy,

curr

ent

Ass

essm

ent

Une

mpl

oym

ent

rate

,

prev

ious

qua

rter

Une

mpl

oym

ent

rate

,

curr

ent

Ass

essm

ent

PMI,

prev

ious

qua

rter

PMI,

curr

ent

Ass

essm

ent

Macro scenarion Switzerland: The Swiss economy is in good health. Stabilization of the situation

in Europe and the stronger euro are helping to improve the outlook for Swiss ex-porters.

n USA: The US economy is performing well, but the «recovery» phase is coming to an end. Despite continuing positive sentiment, caution is called for.

n Eurozone: The eurozone economy is continuing to gain momentum. Although there are still structural barriers that need to be resolved.

n Germany: Not a cloud on the horizon for the German economy; the outlook is refreshingly positive. Only a strong euro could dampen the mood.

Economic trend in emerging markets

China India Brazil Russia

GD

P yo

y,

prev

ious

qua

rter

GD

P yo

y, c

urre

ntA

sses

smen

tIn

flat

ion

rate

yoy

, pr

evio

us q

uart

erIn

flat

ion

rate

yoy

, cu

rren

t

Ass

essm

ent

Une

mpl

oym

ent

rate

,

prev

ious

qua

rter

Une

mpl

oym

ent

rate

,

curr

ent

Ass

essm

ent

PMI,

prev

ious

mon

thPM

I, cu

rren

t

Ass

essm

ent

China 6.9 % 6.9 % 0.9 % 1.5 % 4.0 % 4.0% 49.6 50.4

India 6.7% 5.6% 3.9% 1.5 % – – 51.6 50.9

Brazil –2.5 % –0.4% 4.6% 3.0% 7.5 % 8.2 % 52.0 50.5

Russia 0.3% 0.5 % 4.3% 4.4 % 5.4 % 5.1% 56.0 54.8

Macro scenarion China: China’s growth is in stability mode in anticipation of this autumn’s People’s

Congress. Decision-makers are keen to avoid creating unnecessary uncertainty in the run-up to the event.

n India: India is well on track. The recent tax reform is providing an additional boost and is simplifying the structural barriers which still exist.

n Brazil: The Brazilian economy is still failing to gain traction. President Temer’s posi-tion has also been badly dented. This is weakening the government and slowing down important reform projects.

n Russia: Russia has bottomed out. The economic situation is showing signs of impro-vement.

positive assessment neutral assessment negative assessment

positive assessment neutral assessment negative assessment

Recovery

Recession

Boom

Downturn

Recovery

Recession

Boom

Downturn

Investment Strategy August 201710

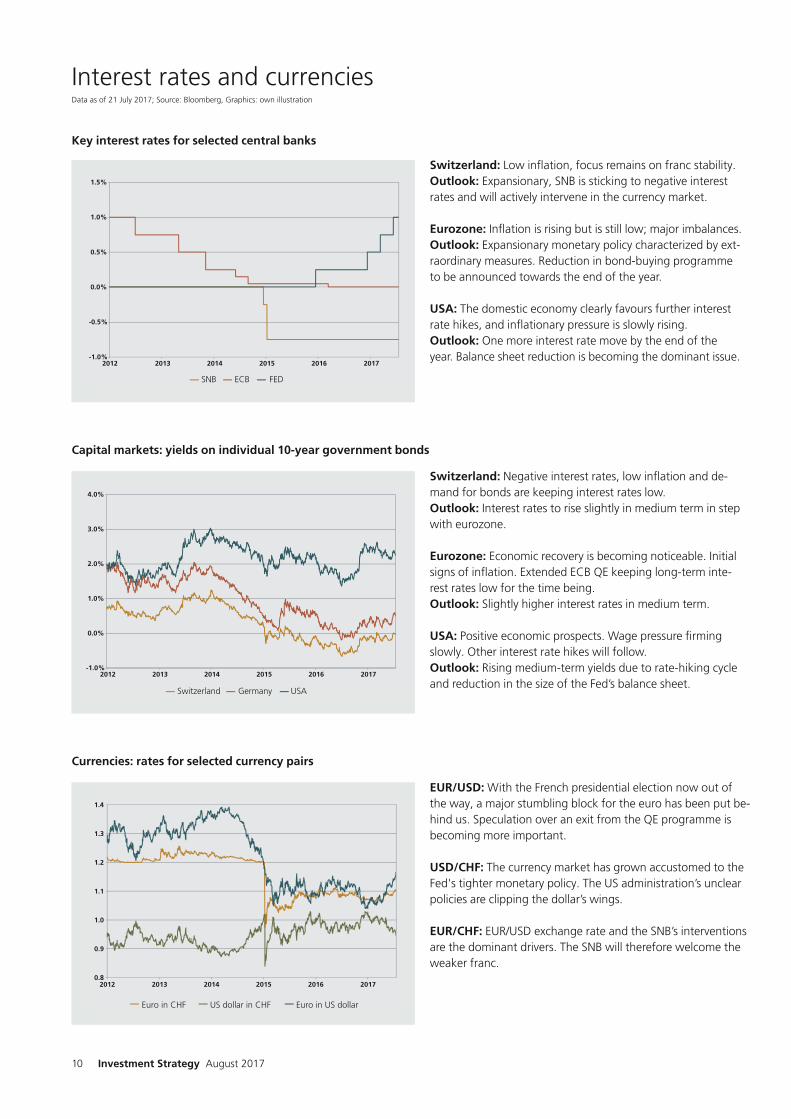

Interest rates and currenciesData as of 21 July 2017; Source: Bloomberg, Graphics: own illustration

Switzerland: Low inflation, focus remains on franc stability.Outlook: Expansionary, SNB is sticking to negative interest rates and will actively intervene in the currency market.

Eurozone: Inflation is rising but is still low; major imbalances.Outlook: Expansionary monetary policy characterized by ext-raordinary measures. Reduction in bond-buying programme to be announced towards the end of the year.

USA: The domestic economy clearly favours further interest rate hikes, and inflationary pressure is slowly rising.Outlook: One more interest rate move by the end of the year. Balance sheet reduction is becoming the dominant issue.

Switzerland: Negative interest rates, low inflation and de-mand for bonds are keeping interest rates low.Outlook: Interest rates to rise slightly in medium term in step with eurozone.

Eurozone: Economic recovery is becoming noticeable. Initial signs of inflation. Extended ECB QE keeping long-term inte-rest rates low for the time being.Outlook: Slightly higher interest rates in medium term.

USA: Positive economic prospects. Wage pressure firming slowly. Other interest rate hikes will follow.Outlook: Rising medium-term yields due to rate-hiking cycle and reduction in the size of the Fed’s balance sheet.

EUR/USD: With the French presidential election now out of the way, a major stumbling block for the euro has been put be-hind us. Speculation over an exit from the QE programme is becoming more important.

USD/CHF: The currency market has grown accustomed to the Fed's tighter monetary policy. The US administration’s unclear policies are clipping the dollar’s wings.

EUR/CHF: EUR/USD exchange rate and the SNB’s interventions are the dominant drivers. The SNB will therefore welcome the weaker franc.

Key interest rates for selected central banks

Capital markets: yields on individual 10-year government bonds

Currencies: rates for selected currency pairs

-0.5%

0.0%

0.5%

1.0%

1.5%

2012 2013 2014 2015 2016 2017

SNB ECB FED

-1.0%

0.0%

1.0%

2.0%

3.0%

4.0%

2012 2013 2014 2015 2016 2017

Switzerland Germany USA

-1.0%

0.8

0.9

1.0

1.1

1.2

1.3

1.4

2012 2013 2014 2015 2016 2017

Euro in CHF US dollar in CHF Euro in US dollar

August 2017 Investment Strategy 11

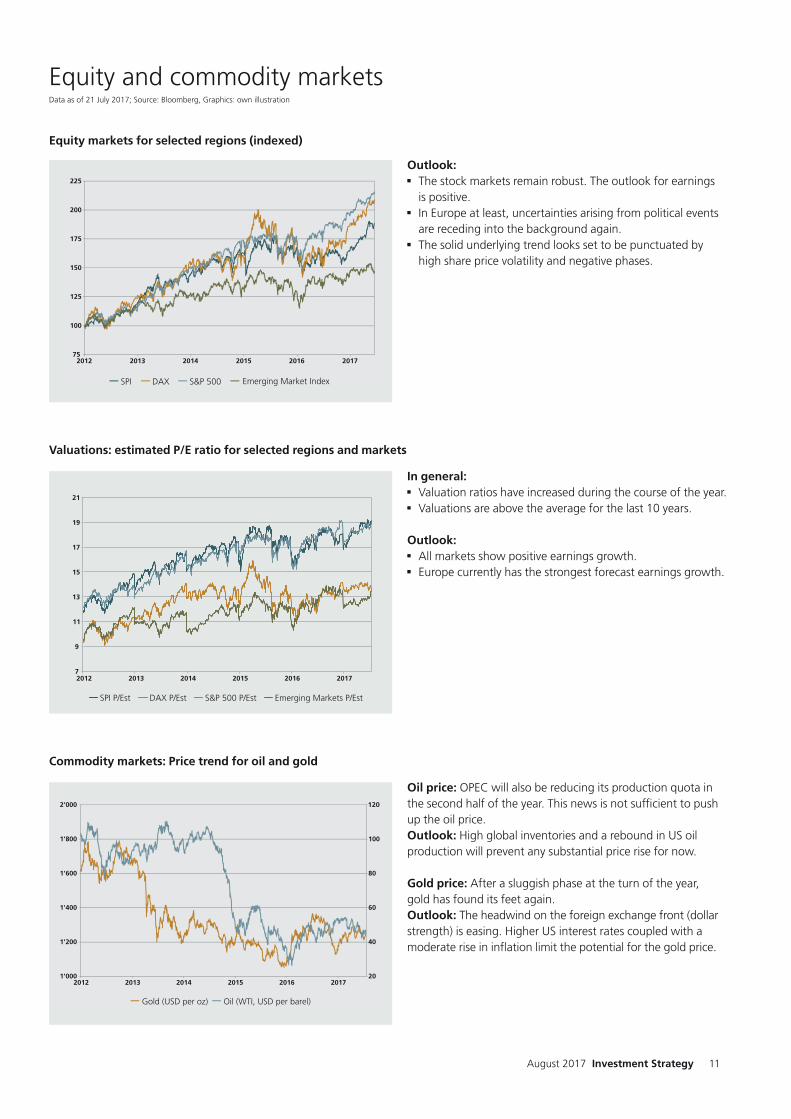

Equity and commodity marketsData as of 21 July 2017; Source: Bloomberg, Graphics: own illustration

Outlook: n The stock markets remain robust. The outlook for earnings

is positive.n In Europe at least, uncertainties arising from political events

are receding into the background again.n The solid underlying trend looks set to be punctuated by

high share price volatility and negative phases.

In general:n Valuation ratios have increased during the course of the year.n Valuations are above the average for the last 10 years.

Outlook: n All markets show positive earnings growth.n Europe currently has the strongest forecast earnings growth.

Oil price: OPEC will also be reducing its production quota in the second half of the year. This news is not sufficient to pushup the oil price.Outlook: High global inventories and a rebound in US oil production will prevent any substantial price rise for now.

Gold price: After a sluggish phase at the turn of the year, gold has found its feet again.Outlook: The headwind on the foreign exchange front (dollar strength) is easing. Higher US interest rates coupled with a moderate rise in inflation limit the potential for the gold price.

Equity markets for selected regions (indexed)

Valuations: estimated P/E ratio for selected regions and markets

Commodity markets: Price trend for oil and gold

75

100

125

150

175

200

225

2012 2013 2014 2015 2016 2017

SPI DAX S&P 500 Emerging Market Index

7

9

11

13

15

17

19

21

2012 2013 2014 2015 2016 2017

SPI P/Est DAX P/Est S&P 500 P/Est Emerging Markets P/Est

20

40

60

80

100

120

1'000

1'200

1'400

1'600

1'800

2'000

2012 2013 2014 2015 2016 2017

Gold (USD per oz) Oil (WTI, USD per barel)

Investment Strategy August 201712

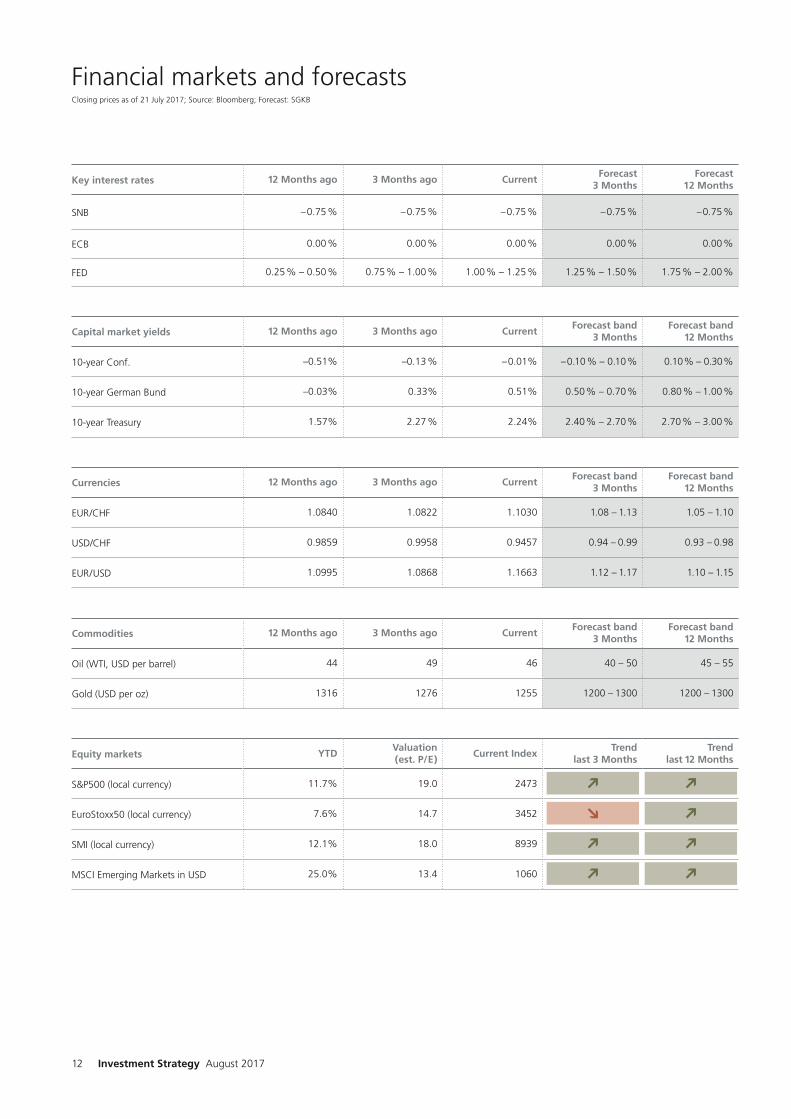

Financial markets and forecastsClosing prices as of 21 July 2017; Source: Bloomberg; Forecast: SGKB

Key interest rates 12 Months ago 3 Months ago Current Forecast 3 Months

Forecast 12 Months

SNB –0.75 % –0.75 % –0.75 % –0.75 % –0.75 %

ECB 0.00 % 0.00 % 0.00 % 0.00 % 0.00 %

FED 0.25 % – 0.50 % 0.75 % – 1.00 % 1.00 % – 1.25 % 1.25 % – 1.50 % 1.75 % – 2.00 %

Capital market yields 12 Months ago 3 Months ago Current Forecast band 3 Months

Forecast band12 Months

10-year Conf. –0.51% –0.13 % –0.01% –0.10 % – 0.10 % 0.10 % – 0.30 %

10-year German Bund –0.03% 0.33% 0.51% 0.50 % – 0.70 % 0.80 % – 1.00 %

10-year Treasury 1.57% 2.27 % 2.24% 2.40 % – 2.70 % 2.70 % – 3.00 %

Currencies 12 Months ago 3 Months ago Current Forecast band 3 Months

Forecast band12 Months

EUR/CHF 1.0840 1.0822 1.1030 1.08 – 1.13 1.05 – 1.10

USD/CHF 0.9859 0.9958 0.9457 0.94 – 0.99 0.93 – 0.98

EUR/USD 1.0995 1.0868 1.1663 1.12 – 1.17 1.10 – 1.15

Commodities 12 Months ago 3 Months ago Current Forecast band 3 Months

Forecast band12 Months

Oil (WTI, USD per barrel) 44 49 46 40 – 50 45 – 55

Gold (USD per oz) 1316 1276 1255 1200 – 1300 1200 – 1300

Equity markets YTD Valuation(est. P/E) Current Index Trend

last 3 MonthsTrend

last 12 Months

S&P500 (local currency) 11.7% 19.0 2473

EuroStoxx50 (local currency) 7.6% 14.7 3452

SMI (local currency) 12.1% 18.0 8939

MSCI Emerging Markets in USD 25.0% 13.4 1060

Disclaimer: The information contained on this Recommendation List and specifically the descriptions of individual securities constitute neither an offer to purchase the securities nor an invitation to engage in any other transactions. All of the information contained in this document has been carefully selected and obtained from sources that the Invest-ment Center of the St.Galler Cantonal Bank AG fundamentally believes to be reliable. Opinions or other representations conveyed in this document are subject to change without notice. No guarantee is assumed as to the accuracy or completeness of the information. St.Galler Cantonal Bank AG is regulated and supervised by Swiss Financial Market Super vision Authority FINMA, Einsteinstrasse 2, 3003 Berne, Switzerland, www.finma.ch.