Embed Size (px)

Citation preview

1

www.anchorcapital.co.za

www.investorcampus.com I N V E S T O R C A M P U S

Key Global Indices

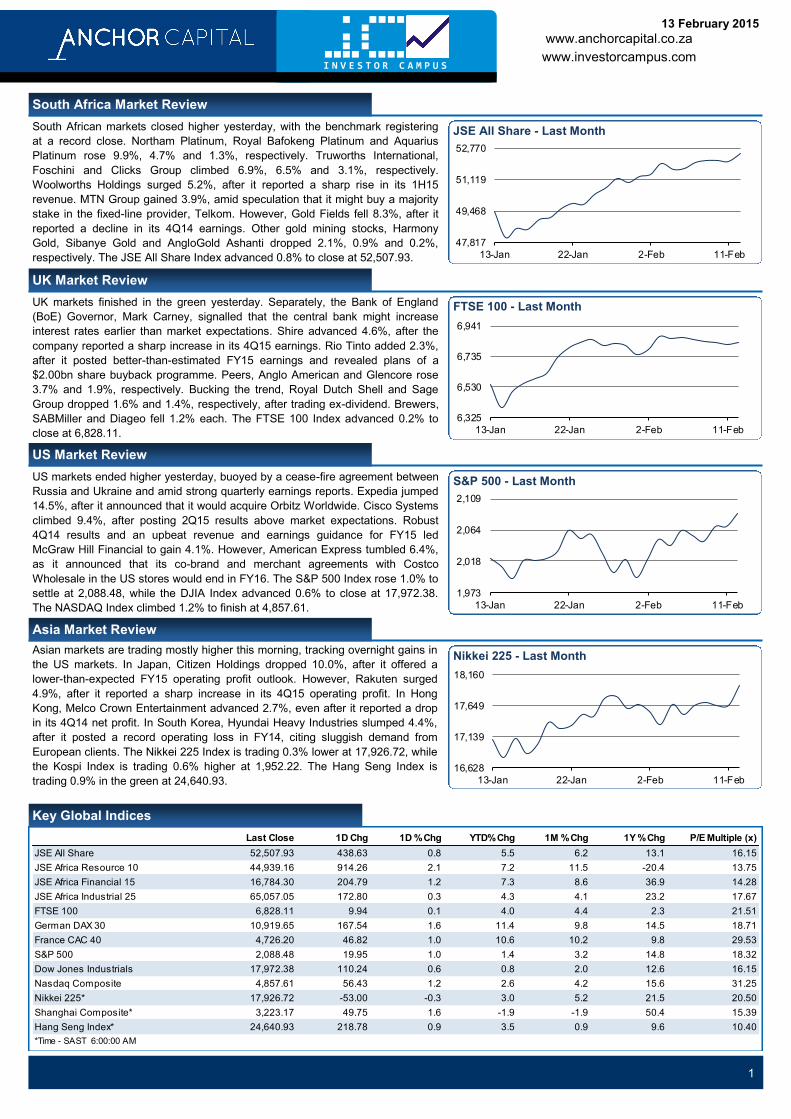

JSE All Share - Last Month

South Africa Market Review

FTSE 100 - Last Month

UK Market Review

S&P 500 - Last Month

US Market Review

Asian markets are trading mostly higher this morning, tracking overnight gains in

the US markets. In Japan, Citizen Holdings dropped 10.0%, after it offered a

lower-than-expected FY15 operating profit outlook. However, Rakuten surged

4.9%, after it reported a sharp increase in its 4Q15 operating profit. In Hong

Kong, Melco Crown Entertainment advanced 2.7%, even after it reported a drop

in its 4Q14 net profit. In South Korea, Hyundai Heavy Industries slumped 4.4%,

after it posted a record operating loss in FY14, citing sluggish demand from

European clients. The Nikkei 225 Index is trading 0.3% lower at 17,926.72, while

the Kospi Index is trading 0.6% higher at 1,952.22. The Hang Seng Index is

trading 0.9% in the green at 24,640.93.

Nikkei 225 - Last Month

Asia Market Review

US markets ended higher yesterday, buoyed by a cease-fire agreement between

Russia and Ukraine and amid strong quarterly earnings reports. Expedia jumped

14.5%, after it announced that it would acquire Orbitz Worldwide. Cisco Systems

climbed 9.4%, after posting 2Q15 results above market expectations. Robust

4Q14 results and an upbeat revenue and earnings guidance for FY15 led

McGraw Hill Financial to gain 4.1%. However, American Express tumbled 6.4%,

as it announced that its co-brand and merchant agreements with Costco

Wholesale in the US stores would end in FY16. The S&P 500 Index rose 1.0% to

settle at 2,088.48, while the DJIA Index advanced 0.6% to close at 17,972.38.

The NASDAQ Index climbed 1.2% to finish at 4,857.61.

UK markets finished in the green yesterday. Separately, the Bank of England

(BoE) Governor, Mark Carney, signalled that the central bank might increase

interest rates earlier than market expectations. Shire advanced 4.6%, after the

company reported a sharp increase in its 4Q15 earnings. Rio Tinto added 2.3%,

after it posted better-than-estimated FY15 earnings and revealed plans of a

$2.00bn share buyback programme. Peers, Anglo American and Glencore rose

3.7% and 1.9%, respectively. Bucking the trend, Royal Dutch Shell and Sage

Group dropped 1.6% and 1.4%, respectively, after trading ex-dividend. Brewers,

SABMiller and Diageo fell 1.2% each. The FTSE 100 Index advanced 0.2% to

close at 6,828.11.

South African markets closed higher yesterday, with the benchmark registering

at a record close. Northam Platinum, Royal Bafokeng Platinum and Aquarius

Platinum rose 9.9%, 4.7% and 1.3%, respectively. Truworths International,

Foschini and Clicks Group climbed 6.9%, 6.5% and 3.1%, respectively.

Woolworths Holdings surged 5.2%, after it reported a sharp rise in its 1H15

revenue. MTN Group gained 3.9%, amid speculation that it might buy a majority

stake in the fixed-line provider, Telkom. However, Gold Fields fell 8.3%, after it

reported a decline in its 4Q14 earnings. Other gold mining stocks, Harmony

Gold, Sibanye Gold and AngloGold Ashanti dropped 2.1%, 0.9% and 0.2%,

respectively. The JSE All Share Index advanced 0.8% to close at 52,507.93.

13 February 2015

47,817

49,468

51,119

52,770

13-Jan 22-Jan 2-Feb 11-Feb

6,325

6,530

6,735

6,941

13-Jan 22-Jan 2-Feb 11-Feb

1,973

2,018

2,064

2,109

13-Jan 22-Jan 2-Feb 11-Feb

16,628

17,139

17,649

18,160

13-Jan 22-Jan 2-Feb 11-Feb

Last Close 1D Chg 1D % Chg YTD% Chg 1M % Chg 1Y % Chg P/E Multiple (x)

JSE All Share 52,507.93 438.63 0.8 5.5 6.2 13.1 16.15

JSE Africa Resource 10 44,939.16 914.26 2.1 7.2 11.5 -20.4 13.75

JSE Africa Financial 15 16,784.30 204.79 1.2 7.3 8.6 36.9 14.28

JSE Africa Industrial 25 65,057.05 172.80 0.3 4.3 4.1 23.2 17.67

FTSE 100 6,828.11 9.94 0.1 4.0 4.4 2.3 21.51

German DAX 30 10,919.65 167.54 1.6 11.4 9.8 14.5 18.71

France CAC 40 4,726.20 46.82 1.0 10.6 10.2 9.8 29.53

S&P 500 2,088.48 19.95 1.0 1.4 3.2 14.8 18.32

Dow Jones Industrials 17,972.38 110.24 0.6 0.8 2.0 12.6 16.15

Nasdaq Composite 4,857.61 56.43 1.2 2.6 4.2 15.6 31.25

Nikkei 225* 17,926.72 -53.00 -0.3 3.0 5.2 21.5 20.50

Shanghai Composite* 3,223.17 49.75 1.6 -1.9 -1.9 50.4 15.39

Hang Seng Index* 24,640.93 218.78 0.9 3.5 0.9 9.6 10.40

*Time - SAST 6:00:00 AM

2

www.anchorcapital.co.za

www.investorcampus.com I N V E S T O R C A M P U S

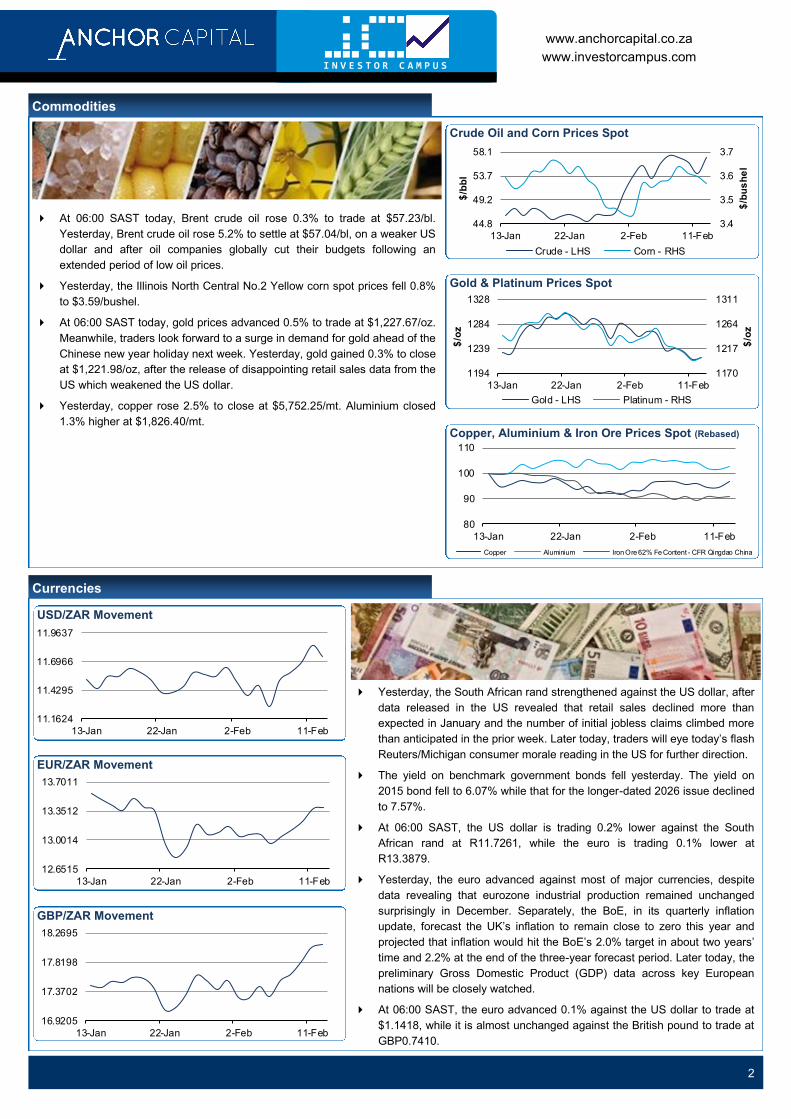

Commodities

At 06:00 SAST today, Brent crude oil rose 0.3% to trade at $57.23/bl.

Yesterday, Brent crude oil rose 5.2% to settle at $57.04/bl, on a weaker US

dollar and after oil companies globally cut their budgets following an

extended period of low oil prices.

Yesterday, the Illinois North Central No.2 Yellow corn spot prices fell 0.8%

to $3.59/bushel.

At 06:00 SAST today, gold prices advanced 0.5% to trade at $1,227.67/oz.

Meanwhile, traders look forward to a surge in demand for gold ahead of the

Chinese new year holiday next week. Yesterday, gold gained 0.3% to close

at $1,221.98/oz, after the release of disappointing retail sales data from the

US which weakened the US dollar.

Yesterday, copper rose 2.5% to close at $5,752.25/mt. Aluminium closed

1.3% higher at $1,826.40/mt.

Currencies

Yesterday, the South African rand strengthened against the US dollar, after

data released in the US revealed that retail sales declined more than

expected in January and the number of initial jobless claims climbed more

than anticipated in the prior week. Later today, traders will eye today’s flash

Reuters/Michigan consumer morale reading in the US for further direction.

The yield on benchmark government bonds fell yesterday. The yield on

2015 bond fell to 6.07% while that for the longer-dated 2026 issue declined

to 7.57%.

At 06:00 SAST, the US dollar is trading 0.2% lower against the South

African rand at R11.7261, while the euro is trading 0.1% lower at

R13.3879.

Yesterday, the euro advanced against most of major currencies, despite

data revealing that eurozone industrial production remained unchanged

surprisingly in December. Separately, the BoE, in its quarterly inflation

update, forecast the UK’s inflation to remain close to zero this year and

projected that inflation would hit the BoE’s 2.0% target in about two years’

time and 2.2% at the end of the three-year forecast period. Later today, the

preliminary Gross Domestic Product (GDP) data across key European

nations will be closely watched.

At 06:00 SAST, the euro advanced 0.1% against the US dollar to trade at

$1.1418, while it is almost unchanged against the British pound to trade at

GBP0.7410.

Crude Oil and Corn Prices Spot

Gold & Platinum Prices Spot

Copper, Aluminium & Iron Ore Prices Spot (Rebased)

USD/ZAR Movement

EUR/ZAR Movement

GBP/ZAR Movement

3.4

3.5

3.6

3.7

13-Jan 22-Jan 2-Feb 11-Feb

44.8

49.2

53.7

58.1

$/b

us

he

l

$/b

bl

Crude - LHS Corn - RHS

1170

1217

1264

1311

13-Jan 22-Jan 2-Feb 11-Feb

1194

1239

1284

1328

$/o

z

$/o

z

Gold - LHS Platinum - RHS

11.1624

11.4295

11.6966

11.9637

13-Jan 22-Jan 2-Feb 11-Feb

12.6515

13.0014

13.3512

13.7011

13-Jan 22-Jan 2-Feb 11-Feb

16.9205

17.3702

17.8198

18.2695

13-Jan 22-Jan 2-Feb 11-Feb

13-Jan 22-Jan 2-Feb 11-Feb

80

90

100

110

Copper Aluminium Iron Ore 62% Fe Content - CFR Qingdao China

3

www.anchorcapital.co.za

www.investorcampus.com I N V E S T O R C A M P U S

Yield Corner

% Closing

Yield

% Change

on Day

Yield % -

1M Ago

South Africa CPI* 5.30 0.00 5.80

South Africa Repo Rate 5.75 0.00 5.75

JSE SA Listed Property Index 5.26 -1.87 5.69

R157 (2015) (SA Bond) 6.07 -0.12 6.21

R207 (2020) (SA Bond) 6.96 -0.23 6.94

R186 (2026) (SA Bond) 7.57 -0.53 7.56

US 10 Year Treasury 1.98 -1.65 1.90

US 30 Year Treasury 2.58 -0.42 2.50

Italian 10 Year Treasury 1.65 -2.71 1.82

German 10 Year Treasury 0.32 -10.14 0.48

* As on December 2014

South African Government Bond Yields

JSE All Share Index - Major Gainers & Losers

Figures in bracket indicate (Last Close, Absolute Change, % Change)

5.8%

6.4%

7.1%

7.7%

8.4%

9.0%

Feb-14 May-14 Aug-14 Nov-14 Feb-15

R157 (2015) R186 (2026)

-10.9% -8.7% -6.5% -4.4% -2.2% 0.0%

Gold Fields Ltd (6078.00, -548.00, -8.3%)

Aveng Ltd (1532.00, -94.00, -5.8%)

Impala Platinum Holdings Ltd (7450.00, -270.00, -3.5%)

Tsogo Sun Holdings Ltd (2835.00, -95.00, -3.2%)

Zeder Investments Ltd (747.00, -23.00, -3.0%)

Lonmin PLC (2850.00, -85.00, -2.9%)

MiX Telematics Ltd (275.00, -8.00, -2.8%)

Pallinghurst Resources Ltd (390.00, -10.00, -2.5%)

Naspers Ltd (163508.00, -4055.00, -2.4%)

Harmony Gold Mining Co Ltd (3100.00, -66.00, -2.1%)

0.0% 2.2% 4.4% 6.5% 8.7% 10.9%

Northam Platinum Ltd (4789.00, 431.00, 9.9%)

Truworths International Ltd (8604.00, 555.00, 6.9%)

Foschini Group Ltd/The (17391.00, 1054.00, 6.5%)

Fortress Income Fund Ltd (2500.00, 132.00, 5.6%)

Mediclinic International Ltd (12513.00, 655.00, 5.5%)

Woolworths Holdings Ltd/South Africa (8669.00, 432.00, 5.2%)

Resilient Property Income Fund Ltd (9375.00, 420.00, 4.7%)

Royal Bafokeng Platinum Ltd (5595.00, 249.00, 4.7%)

Anglo American PLC (20999.00, 844.00, 4.2%)

Pick n Pay Stores Ltd (5748.00, 222.00, 4.0%)

4

www.anchorcapital.co.za

www.investorcampus.com I N V E S T O R C A M P U S

Dual Listed Companies - Price Differential

Company Name Price (R) - Local

Exchange Primary Exchange

Price (Primary Exchange)

Equivalent Price (R)

Price Difference (R)

Anglo American Plc 209.99 London Stock Exchange 11.66 GBP 210.58 -0.59

BHP Billiton Plc 271.16 London Stock Exchange 14.95 GBP 270.03 1.13

British American Tobacco Plc 656.43 London Stock Exchange 36.27 GBP 655.24 1.19

Capital & Counties Properties Plc 68.53 London Stock Exchange 3.82 GBP 69.09 -0.56

Cie Financiere Richemont SA* 101.63 SIX Swiss Exchange 80.40 CHF 101.61 0.02

Intu Properties Plc 66.18 London Stock Exchange 3.69 GBP 66.58 -0.40

Investec Plc 102.69 London Stock Exchange 5.66 GBP 102.27 0.42

Lonmin Plc 28.50 London Stock Exchange 1.57 GBP 28.37 0.13

Mondi Plc 227.50 London Stock Exchange 12.58 GBP 227.30 0.20

New Europe Property Investments Plc/Fund 131.00 London Stock Exchange 10.00 EUR 133.88 -2.88

Old Mutual Plc 38.74 London Stock Exchange 2.16 GBP 38.94 -0.20

Pan African Resources Plc 2.08 London Stock Exchange 0.12 GBP 2.17 -0.09

Reinet Investments SCA* 26.80 Luxembourg Stock Exchange 19.80 EUR 26.51 0.29

SABMiller Plc 633.03 London Stock Exchange 35.01 GBP 632.56 0.47

AngloGold Ashanti Ltd 141.15 New York Stock Exchange 11.97 USD 140.36 0.79

DRDGOLD Ltd* 2.80 New York Stock Exchange 2.17 USD 2.54 0.26

Gold Fields Ltd 60.78 New York Stock Exchange 5.04 USD 59.10 1.68

Harmony Gold Mining Co Ltd 31.00 New York Stock Exchange 2.67 USD 31.31 -0.31

Redefine International Plc/Isle of Man 10.15 London Stock Exchange 0.57 GBP 10.30 -0.15

Glencore Xstrata Plc 50.37 London Stock Exchange 2.77 GBP 50.03 0.34

* Depositary Reciepts (DR) trade in the ratio of ten DRs to each Company share; Exchange Rate - USDZAR:11.7261, EURZAR:13.3879, GBPZAR:18.0681, CHFZAR:12.6376, Conversion rate as of 6:00 SAST

5

www.anchorcapital.co.za

www.investorcampus.com I N V E S T O R C A M P U S

JSE All Share Stocks Hitting 52 Week High / Low

Company Name Closing Price (R) 1D% Chg 52 Week High / Low

Fortress Income Fund Ltd 25.00 5.6% Hits 52 Week High

Holdsport Ltd 53.00 0.0% Hits 52 Week High

Intu Properties PLC 66.18 0.4% Hits 52 Week High

JSE Ltd 122.00 0.8% Hits 52 Week High

Mediclinic International Ltd 125.13 5.5% Hits 52 Week High

MMI Holdings Ltd/South Africa 33.20 0.8% Hits 52 Week High

Mondi Ltd 226.09 2.3% Hits 52 Week High

Mondi PLC 227.50 2.6% Hits 52 Week High

New Europe Property Investments PLC/Fund 131.00 3.6% Hits 52 Week High

Northam Platinum Ltd 47.89 9.9% Hits 52 Week High

Old Mutual PLC 38.74 -0.7% Hits 52 Week High

Peregrine Holdings Ltd 26.49 2.1% Hits 52 Week High

Redefine Properties Ltd 11.85 3.5% Hits 52 Week High

RMB Holdings Ltd 67.35 2.7% Hits 52 Week High

Rebosis Property Fund Ltd 13.29 3.0% Hits 52 Week High

Resilient Property Income Fund Ltd 93.75 4.7% Hits 52 Week High

Rand Merchant Insurance Holdings Ltd 45.20 2.5% Hits 52 Week High

Steinhoff International Holdings Ltd 65.25 1.4% Hits 52 Week High

Sanlam Ltd 77.75 2.3% Hits 52 Week High

Grindrod Ltd 17.60 -0.3% Hits 52 Week Low

Murray & Roberts Holdings Ltd 18.00 -1.0% Hits 52 Week Low

PPC Ltd 19.91 -1.9% Hits 52 Week Low

Raubex Group Ltd 18.53 -0.9% Hits 52 Week Low

Wilson Bayly Holmes-Ovcon Ltd 114.44 -0.5% Hits 52 Week Low

6

www.anchorcapital.co.za

www.investorcampus.com I N V E S T O R C A M P U S

Economic Updates

Key Economic Releases Today

Country SAST Economic Indicator Relevance Consensus Previous Frequency

France 8:30 Gross Domestic Product, Prelim (QoQ) (4Q) 0.1% 0.3% Quarterly

France 8:30 Gross Domestic Product, Prelim (YoY) (4Q) 0.3% 0.4% Quarterly

Germany 9:00 Wholesale Price Index (MoM) (Jan) - -1.0% Monthly

Germany 9:00 Gross Domestic Product n.s.a., Prelim (QoQ) (4Q) 1.2% 1.2% Quarterly

Germany 9:00 Gross Domestic Product s.a., Prelim (QoQ) (4Q) 0.3% 0.1% Quarterly

Germany 9:00 Gross Domestic Product w.d.a., Prelim (YoY) (4Q) 1.0% 1.2% Quarterly

France 9:45 Nonfarm Payrolls, Prelim (QoQ) (4Q) -0.2% -0.3% Quarterly

Spain 10:00 Consumer Price Index (MoM) (Jan) -1.7% -0.6% Monthly

Spain 10:00 Harmonised Index of Consumer Prices (HICP) (MoM) (Jan) -2.2% -0.7% Monthly

Italy 11:00 Gross Domestic Product, Prelim (YoY) (4Q) -0.5% -0.5% Quarterly

Portugal 11:30 Gross Domestic Product, Prelim (YoY) (4Q) 0.5% 1.1% Quarterly

UK 11:30 Construction Output (YoY) (Dec) 5.5% 3.6% Monthly

Eurozone 12:00 Gross Domestic Product s.a., Prelim (QoQ) (4Q) 0.2% 0.0% Quarterly

Eurozone 12:00 Gross Domestic Product s.a., Prelim (YoY) (4Q) 0.8% 0.8% Quarterly

Eurozone 12:00 Trade Balance s.a. (Dec) EUR20.00bn EUR20.00bn Monthly

US 15:30 Import Price Index (Jan) - 130.20 Monthly

US 15:30 Export Price Index (Jan) - 128.10 Monthly

US 15:30 Import Price Index (MoM) (Jan) -3.2% -2.5% Monthly

US 15:30 Export Price Index (MoM) (Jan) -0.9% -1.2% Monthly

US 17:00 Reuters/Michigan Consumer Sentiment Index, Prelim (Feb) 98.10 98.10 Monthly

Germany - Nominal GDP (4Q) - EUR739.96bn Quarterly

China - M2 Money Supply (YoY) (Jan) 12.1% 12.2% Monthly

China - New Yuan Loans (Jan) CNY1,350.00bn CNY697.30bn Monthly

Note: High Medium Low

In December, on an annual basis, gold production rose 2.3% in South Africa. Gold production had dropped 10.1% in the previous month.

On an annual basis, mining production registered a drop of 2.0% in South Africa, in December. Mining production had fallen 0.4% in the

previous month.

The BoE, in its quarterly inflation report, forecast inflation to dip to zero in 2Q15 and remain "close to zero" for the rest of the year.

Additionally, the central bank projected that inflation would hit the BoE’s 2.0% target in about two years’ time and 2.2% at the end of the

three-year forecast period.

The BoE Governor, Mark Carney, at a press conference in London, hinted that the BoE might raise its interest rates faster than financial

market expectations. However, he cautioned that increases in interest rates would probably be limited and gradual and that the BoE would

not hesitate to cut rates if inflation proves weaker than expected.

The final consumer price index in Germany dropped 1.1% on a monthly basis in January, compared with a flat reading in the prior month.

Market expectations were for the consumer price index to drop 1.0%. The preliminary figures had indicated a drop of 1.0%.

On a seasonally adjusted monthly basis, industrial production remained steady in December, in the eurozone, less compared with market

expectations of a rise of 0.2%. In the previous month, industrial production had recorded a revised rise of 0.1%.

The US Department of Labour has reported that the seasonally adjusted initial jobless claims in the US recorded a rise to 304.00k in the

week ended 7 February 2015, compared with a revised level of 279.00k in the previous week. Market expectations were for initial jobless

claims to climb to 287.00k.

On a monthly basis, advance retail sales fell 0.8% in the US, in January, more than market expectations for a fall of 0.4%. Advance retail

sales had dropped 0.9% in the prior month.

In January, retail sales ex-autos eased 0.9% on a monthly basis in the US, higher than market expectations for a fall of 0.5%. In the

previous month, retail sales ex-autos had registered a revised similar fall.

The leading economic index climbed 0.9% on a monthly basis, in January, in China. In the previous month, the leading economic index had

registered a rise of 1.1%.

7

www.anchorcapital.co.za

www.investorcampus.com I N V E S T O R C A M P U S

South Africa

Woolworths Holdings: The company, in its results for 1H15, indicated that revenue increased 46.3% to R28.46bn, compared with the

same period previous year. Its diluted EPS was R1.83, compared with R1.80 reported in the same period a year ago. Meanwhile, its

adjusted diluted headline EPS rose to R2.42 from R1.86 posted the corresponding period a year ago.

Gold Fields: The gold mining company, in its FY14 results, stated that revenue decreased 1.3% to $2.87bn from the previous year. The

company reported a diluted EPS from continuing operations of $0.02, compared with a diluted loss per share of $0.79 posted in FY13. The

company expects attributable equivalent gold production for FY15 at around 2.20mn oz.

JSE Limited: The company, in its trading statement for FY14, indicated that its basic EPS is expected to be between 20.0% and 30.0%

higher than previous year. Additionally, its headline EPS is expected to be between 10.0% to 20.0% higher than the preceding year.

Mix Telematics: The company, in its 3Q15 results, announced that total revenue was up 13.5% to R351.50mn, compared with the same

period previous year, while its total subscription revenue grew 15.4% on an annual basis to R253.70mn. Its diluted EPS stood at R0.04,

compared with R0.06 posted in the corresponding period a year ago. The company expects revenue to grow 5.8% to 6.6% in FY15,

compared with the previous year.

Anglogold Ashanti: The gold mining company stated that it is seeking to sell or find a partner for one of its “key” gold mines in a bid to

reduce its $3.00bn of net debt, partly accumulated during the decade-long bull run in gold to FY11.

Telkom SA Soc: The company announced that it continues to remain in talks with MTN South Africa regarding the potential extension of

their existing roaming agreement.

Group Five: Media reports revealed that the company is planning to retrench about 250 of its employees and incur retrenchment costs of

about R25.00mn in the year to June, after its profit margin deteriorated to a negative 2.7% in the six months ended December from a target

range of 3.0% to 5.0%.

Nepi sets sights on Serbian malls: JSE-listed New Europe Property Investments, which is Romania’s largest shopping centre owner, has

diversified into Serbian shopping centres as it looks to maintain double digit distribution growth every year.

Investec eyes wider savings accounts: Specialist bank Investec said it would now accept deposits from customers who were not

classified as high-net-worth individuals as part of its plans to offer tax-free savings accounts.

Bad news for MTN Zakhele shareholders: Holders of MTN Zakhele shares will be disappointed to learn that the expiry date of the

temporary exemption granted by the Financial Services Board will remain 31 March.

MTN Said to explore acquisition of Telkom: MTN Group Ltd. is exploring whether to pursue an acquisition of a majority stake in landline

provider Telkom SA SOC Ltd. to challenge Vodacom Group’s dominance in South Africa’s telecommunications market, according to people

familiar with the matter.

UK and US

American International Group: The company, in its FY14 results, indicated that its pre-tax operating income rose 2.0% to $9.57bn from

the previous year. However, its net diluted EPS decreased 15.2% to $5.20, compared with the preceding year.

Liberty Global: The telecommunications and television company, in its FY14 results, stated that its revenue increased to $18.25bn,

compared with $14.47bn posted in the preceding year. The company reported a basic and diluted loss of $0.87, compared with a loss of

$1.43 recorded in the previous year. For FY15, the company expects to deliver mid-single digit rebased OCF growth, along with $2.50bn of

adjusted free cash flow, which would represent combined mid-teens growth on an FX-adjusted basis.

Kraft Foods Group: The grocery manufacturing and processing conglomerate, in its FY14 results, revealed that its net revenue was

$18.21bn, compared with $18.22bn posted in the prior year. Meanwhile, its diluted EPS dropped sharply to $1.74 from $4.51 posted in

FY13. Furthermore, it announced that George Zoghbi, currently Vice Chairman, operations, R&D, sales and strategy, has been named

Chief Operating Officer and Chris Kempczinski, who currently leads its Canada business unit, would assume an expanded role as

Executive Vice President of growth initiatives and President of International.

CBS Corporation: The mass media company, in its FY14 results, indicated that total revenue dropped 1.4% to $13.81bn from the

preceding year. Its diluted net EPS stood at $5.27, compared with $3.01 posted in the previous year.

McGraw Hill Financial: The financial company, in its FY14 results, stated that revenue was up 7.4% to $5.05bn, compared with the

previous year. Additionally, the company reported a net diluted loss per share of $0.42, compared with a net diluted EPS of $4.91 posted in

FY13. The company gave FY15 revenue guidance of mid single-digit growth and adjusted diluted EPS guidance of $4.35 to $4.45.

Apache Corporation: The oil and gas company, in its FY14 results, revealed that total revenue and other income dropped to $13.85bn,

compared with $15.56bn posted in the previous year. It reported a net diluted loss per share of $14.06, compared with a net diluted EPS of

$5.50 posted in the preceding year. It anticipates capital spending of $2.10bn to $2.30bn in onshore North America and plans to run an

average of 17 rigs in FY15. Furthermore, the company is planning a capital budget of $1.50bn to $1.70bn for international and offshore

activities in the coming year.

Corporate Updates

8

www.anchorcapital.co.za

www.investorcampus.com I N V E S T O R C A M P U S

Kellogg Co.: The company, in its FY14 results, indicated that its net sales decreased to $14.58bn from $14.79bn posted in the previous

year. Its diluted EPS dropped to $1.75 from 4.94 recorded in the prior year. The company expects net sales in FY15 to remain

approximately unchanged annually.

Microsoft: Media reports revealed that it plans to buy mobile-productivity apps that work on Apple, iOS and Google Android mobile

operating systems for which it would spend a few hundred million dollars on deals over the next few months. Meanwhile, the company has

released Windows 10 technical preview for phones by supporting just midrange to lower-end devices.

American Express: The company announced that its US co-brand and merchant acceptance agreements with Costco Wholesale

Corporation is set to end on 31 March 2016, as it was unable to reach terms that would have made economic sense for the company and its

shareholders.

Expedia Inc.: The travel based company announced that it would acquire Orbitz Worldwide, Inc., including all of Orbitz Worldwide's brands,

for $12.00/ share in cash, representing an enterprise value of approximately $1.60bn, and a premium of approximately 29.0% over the

volume weighted average share price for the five trading days up to and including 11 February 2015.

Rio Tinto: The metals and mining company, in its preliminary FY14 results, indicated that sales revenue dropped 6.9% to $47.66bn from

the preceding year. Its diluted EPS from continuing operations stood at $3.51, compared with $1.97 recorded a year ago. The company

expects capital expenditure to decline less than $7.00bn in FY15 and remain at around $7.00bn in FY16 and FY17. Meanwhile, the

company stated that it would buy back $2.00bn of its shares this year as it grapples with a sharp drop in the price of its main commodity,

iron ore.

Imperial Tobacco Group: The tobacco company, in its 1Q15 interim management statement, stated that its tobacco net revenue fell 2.0%

to GBP1.49bn, compared with the previous year. At constant currency, revenue grew 4.0%, while underlying revenue dropped 1.0%.Its total

tobacco volume increased 1.0% from last year to 71.80bn SE on a reported basis, but dropped 4.0% on underlying basis.

Informa Plc: The publishing and events company, in its FY14 results, revealed that revenue from continuing operations increased

marginally to GBP1.14bn from GBP1.13bn posted in FY13. The company reported a diluted loss per share from continuing operations of

8.60p, compared with a diluted EPS of 17.10p posted in the previous year. The company remains committed to increase the annual

dividend per share by a minimum of 2.0% annually through the period of FY14 to FY17.

DCC Plc: The investment company, in its interim management statement, revealed that its operating profit in 3Q15 was ahead of the same

period a year ago. The company has reiterated its expectation that FY15 would show growth in operating profit and adjusted EPS in the

range of 5.0% to 10.0% from the previous year. It further stated that the agreement to acquire the assets that comprise the Esso Express

unmanned retail petrol station network and the Esso Motorway concessions in France has been signed, following the conclusion of the

French Works Council consultation process.

Lancashire Holdings: The insurance company, in its FY14 results, stated that total net revenue increased to $764.80mn from $642.60mn

posted in the previous year. However, its diluted EPS dropped marginally to $1.16 from $1.17 recorded in the preceding year.

Morgan Advanced Materials: The company, in its FY14 results, indicated that total revenue was GBP921.70mn, lower compared with

GBP957.80mn reported in the preceding year. Its diluted EPS dropped sharply to 2.70p from 14.70p posted in FY13. In FY15, the company

would continue to focus and invest in its key technology areas to drive differentiation, positive mix shift and sustainable growth potential.

Zoopla Property Group: The online property company, in its trading statement for the period between 1 October 2014 and 31 January

2015, indicated that its average monthly visits increased 14.0% to 42.30mn, compared with the same period last year and with a record total

of 50.50mn visits during January. It further stated that the number of total advertising members at the end of the period dropped 11.0% over

the past year to 16,967.

Kennedy Wilson Europe Real Estate: The real estate company announced that it has completed the acquisition of Gardner House, Wilton

Place, Dublin 2, previously held as two loans secured by a first ranking mortgage. The purchase price for the property (including costs) is

EUR45.00mn, reflecting a net initial yield of 6.7%.

Galliford Try: The housebuilding and construction company announced that its building business has reached financial close on the new

landmark headquarters for Northamptonshire county council in a contract worth GBP40.00mn.

SuperGroup Plc: The company announced that Susanne Given, the Chief Operating Officer, has stepped down from the board as a

director with immediate effect and would leave the business in order to explore other opportunities.

Financial Times

BT raises GBP1.00bn to help fund EE acquisition: BT has raised GBP1.00bn through a share sale to investors to help fund its

GBP12.50bn acquisition of EE, the UK’s largest mobile group.

Zoopla hit by launch of rival property website: Property portal Zoopla has reported an 11.0% fall in the number of estate agents

advertising on its website over the past year, partly due to competition from recently launched rival website On the Market.

Bankers face extension of pay clawbacks to 10 years: Bankers found guilty of wrongdoing could see their bonuses and fixed pay clawed

back even if the offence took place 10 years ago, under a package of reforms to be announced by Labour on Friday.

Corporate Updates

9

www.anchorcapital.co.za

www.investorcampus.com I N V E S T O R C A M P U S

Former HSBC banker Dorner joins Rolls-Royce board: Rolls-Royce has tapped a former HSBC banker to join its board as a non-

Executive Director to help the aero-engine maker restore relations with investors and regulators after a dire FY14 marked by profit

warnings.

Informa writes down value of Datamonitor by almost 40.0%: Informa has written down the value of Datamonitor by almost 40.0%, eight

years after the business media group acquired the market intelligence company for GBP500.00mn.

Shire says $1.60bn windfall from AbbVie is tax-free: Shire has been advised that the $1.60bn “break fee” received from AbbVie after the

collapse of their abortive merger is not taxable — exposing the Dublin-based, UK-listed drugmaker to fresh scrutiny over its tax affairs.

Rio Tinto dismisses talk of deal with Glencore: Rio Tinto does not need to do a deal with Glencore, its Chief Executive Sam Walsh said

after the Anglo-Australian miner defied the gloom in the commodities sector by increasing its dividend and announcing a $2.00bn share

buyback.

St James’s Place targets Gulf expats: St James’s Place, the fast-growing FTSE 100 wealth manager, is planning to open its first offices

in the Middle East by the end of this year in an attempt to win business from wealthy European expatriates, and gain an entry into the Gulf

market.

Morrison chief Dalton Philips checks out early: Dalton Philips, the embattled Chief Executive of Wm Morrison, is to leave the

supermarket group with immediate effect rather than working out his notice period, the company announced on Thursday.

Executives at UK grocer Ocado see bonuses fall by up to 40.0%: Ocado executives had their bonuses cut by as much as 40.0% last

year – despite steering the online grocery delivery company to its first pre-tax profit in 15 years of trading.

Christie’s improves digital service for wealthy buyers:. Christie’s has bolstered its online operations with the purchase of a platform that

allows art buyers to manage collections on digital devices as it attempts to strengthen ties to wealthy investors.

John Laing IPO prices at bottom of range: John Laing, the British infrastructure group, has priced its shares at the very bottom of its

range ahead of its listing, reflecting a weakening investor enthusiasm for London’s initial public offerings market.

Commerzbank warns of future challenges: Commerzbank warned that it could take further provisions for legal risks in the US, where it is

under investigation for allegedly breaching both American sanctions on Iran and Sudan, and anti-money-laundering rules.

GM fires Chevrolet Bolt into production: General Motors signalled its determination to “completely shake up” the electric vehicle market

by announcing it would manufacture the Chevrolet Bolt, intended to run 200 miles on a battery charge and cost just $30,000.

WPP to buy stake in ComScore: WPP has agreed to buy a stake worth about $300.00mn in ComScore, as the world’s largest advertising

group forges an alliance with the US-based internet audience measurement company.

Publicis’s growth lags behind US rival Omnicom: Publicis promised that growth would accelerate to “cruising speed” in the second half

of this year, as the French advertising group reported fourth-quarter revenue figures that lagged behind its US rival Omnicom.

Hong Kong’s Chow Tai Fook to invest $2.60bn in South Korean casino: Chow Tai Fook Enterprises of Hong Kong plans to invest

$2.60bn in a casino project in Incheon in South Korea, which is working to attract Chinese gamblers.

Xiaomi set to launch gadgets in US: Xiaomi, the fast-growing Chinese gadget maker, will make its first tentative steps into the US market

this year.

L’Oréal confident after sales pick-up: L’Oréal, the world’s biggest cosmetics group by sales, said on Thursday that it looked to the future

“with confidence” after a pick-up in sales in the final quarter of the year.

AngelList equity crowdfunding platform to launch in UK: AngelList, the US-based equity crowdfunding platform, will launching in the UK

on Friday, in the latest sign of interest in the UK’s burgeoning technology sector.

Rocket Internet seeks about EUR600.00mn in fresh equity: Rocket Internet is planning to raise about EUR600.00mn in a fresh equity

offer, underlining the rate of cash burn at the Berlin-based ecommerce group that floated in October.

IAG refuses to make further concessions on Aer Lingus bid: A commitment by International Airlines Group to allow Aer Lingus to use

its take-off and landing slots at Heathrow airport for flights to Ireland cannot be extended beyond five years, IAG’s Chief Executive said on

Thursday.

Shire: Rallied 4.6% to GBP49.97, even after its FY15 guidance came in at the low end of analysts’ expectations.

Afren: Dived 20.6% to 7.10p ahead of Seplat’s deadline of Friday to make a formal offer for the African explorer or walk away.

Corporate Updates

10

www.anchorcapital.co.za

www.investorcampus.com I N V E S T O R C A M P U S

Lex:

Renault: up and down and round the bend: So it is a shame, that French carmaker Renault gives investors plenty of exposure to all

these markets. One can only hope that a good performance in one will cancel out a poor one in the others. Which is what happened in

FY14. Full-year results on Thursday beat expectations, with operating profits up almost a third. That was enough to send the shares up

11.0%. Europe was the star of the show. Renault’s European volumes grew twice as fast as the market. Customers warmed to its Dacia

brand (originally developed for emerging markets using old technology). Dacia margins are higher than on cars higher up the range, too.

Renault expects continued growth next year. Once again, Europe should compensate for weakness in both Russia and Brazil (although it

may be able to take market share in Russia thanks to its low local production costs). Sales across the company should benefit from a

refresh of the mid-range models, while margins should be helped by moves to manufacture more cars on a common platform. Renault

shares are up 17.0% in the past year, although most of that came on Thursday. Its enterprise value is 9.00 times earnings before interest,

tax, depreciation and amortisation, in line with local rival Peugeot.

American Express: leaving the club: Membership has its privileges goes the famous American Express slogan. But not enough for

Costco. Amex said on Thursday that its long-time partnership with Costco (Costco exclusively accepts an Amex credit card in its discount

retail warehouses) would not be renewed when the agreement expires in early FY16. It was apparently a mutual decision. Amex is “closed-

loop” card business. Unlike MasterCard and Visa, which are just payment networks, Amex is the underlying bank extending credi t to

customers. The interchange fee it charges to merchants is higher than the other two and its reputation comes from its customer service.

During the financial crisis, it converted to bank holding company status and now faces the capital requirements imposed by the Federal

Reserve. By discarding Costco, considered its crown jewel partner, Amex is saying that it wants to focus on profitability not volume. And

while the company’s top-line growth target of 8.0% seems unrealistic now, the focus on return may comfort investors. In its recent heyday,

Amex traded at a juicy 20.00 times earnings. Once there is more visibility on revised earnings, a lower multiple may lead to investors putting

in an application.

Boliden: zinc and swim: One Swedish miner, Boliden, has found the light. On Thursday it beat analysts’ fourth-quarter earnings

expectations. Its shares rallied 8.0%. A strong dollar hurts most commodity producers as the value of commodities tends to go down by

more than their costs. But Boliden, whose costs are largely in the rapidly weakening Swedish krona, is benefiting from recent FX moves.

Boliden primarily produces zinc and copper. Its shares have had a great run this year, up 17.0% in dollar terms. The MSCI European Metals

and Mining index has fallen. It helps that 60.0% of the company’s revenues this year should come from zinc. Two years ago it made up just

a quarter of its sales. Zinc has fallen less than other metals, such as copper, in the past year. One support for the zinc pr ice is tightening

supply. Global inventories have halved over the past two years. And large mines in Australia and Ireland, representing over 4.0% of global

supply, should close this year. Earnings before interest, tax, depreciation and amortisation from its expanded zinc mine, Garpenberg,

should double by FY17 to SKr2.60bn, representing a quarter of the total. Meanwhile, overall investment has peaked. So net debt to equity

should fall from 35.0% towards zero by FY17. There is little financing risk.

Corporate Updates

11

www.anchorcapital.co.za

www.investorcampus.com I N V E S T O R C A M P U S

Key Corporate Releases Today

South Africa

Full Year Consensus

Company Name Results Currency Estimated EPS Estimated Revenue (Millions)

ArcelorMittal South Africa Limited Final ZAr 252.80 43,419.10

UK

Full Year Consensus

Company Name Results Currency Estimated EPS Estimated Revenue (Millions)

Anglo American Plc FY14 $ 1.63 27,358.10

Rolls-Royce Holdings Plc FY14 GBP 0.61 14,213.10

Riverstone Energy Limited FY14 GBP - -

Europe

Full Year Consensus

Company Name Results Currency Estimated EPS Estimated Revenue (Millions)

Beiersdorf AG FY14 EUR 2.74 6,629.38

ArcelorMittal SA 4Q EUR 0.89 80,040.20

ThyssenKrupp AG 1Q EUR 1.13 42,659.40

US

Full Year Consensus

Company Name Results Currency Estimated EPS Estimated Revenue (Millions)

VF Corp. 4Q $ 3.4 13089.4

Exelon Corp. 4Q $ 2.48 24144.9

Ventas Inc. 4Q $ 1.9 3440.19

DTE Energy Co. 4Q $ 4.6 10936.9

J M Smucker Co. 3Q $ 5.55 5537.06

Interpublic Group of Companies Inc. 4Q $ 1.15 7712.16

Red Robin Gourmet Burgers Inc. 4Q $ 3.07 1287.59

Ruth's Hospitality Group Inc. 4Q $ 0.84 379.78

EMC Insurance Group Inc. 4Q $ 2.33 632.05

Note: All Estimates are for Full Year

South Africa Ex-Dividend Calendar

Date Company Name Dividend Type Last Day to Trade Amount

- Capital Property Fund Final 13-Feb-15 R0.44

- Putprop Limited Rights Issue 13-Feb-15 0.5515:1

- Sekunjalo Investments Limited Final 13-Feb-15 R0.02

12 Anchor Capital (Pty) Ltd (Reg no: 2009/002925/07). An authorised Financial Services Provider; FSP no: 39834

www.anchorcapital.co.za

www.investorcampus.com I N V E S T O R C A M P U S

Disclaimer

This report and its contents are confidential, privileged and only for the information of the intended recipient. Anchor Capital (Pty) Ltd and Ripple Effect 4

(Pty) Ltd make no representations or warranties in respect of this report or its content and will not be liable for any loss or damage of any nature arising

from this report, the content thereof, your reliance thereon its unauthorised use or any electronic viruses associated therewith. This report is proprietary

to Anchor Capital (Pty) Ltd and Ripple Effect 4 (Pty) and you may not copy or distribute the report without the prior written consent of the authors.

The business of money: Global asset management and

stockbroking

The business of knowledge: Financial education, information

and valuation services

![New Wines · 2021. 1. 26. · Marques de Murrieta “Castillo Ygay” Gran Reserva Especial 2010 [750ml/6cs] $209.99 “Sourced from a 98-acre plot planted in 1950, it is made only](https://img.pdfslide.net/doc/110x75/60c2ccbac9dc0d746f4fa67e/new-wines-2021-1-26-marques-de-murrieta-aoecastillo-ygaya-gran-reserva-especial.jpg)

![[PPT]Name of presentation · Web viewABG on 35%- pH-7.47 p02-11.66 pCO2- 3.65 HCO3- 22.5 Lactate-2.01 ECG- Sinus tachycardia Investigations Blood Results-2000hr Na 129 K 4.1 Urea](https://img.pdfslide.net/doc/110x75/5adf17f57f8b9a8f298c745a/pptname-of-presentation-viewabg-on-35-ph-747-p02-1166-pco2-365-hco3-225.jpg)