Embed Size (px)

Citation preview

INVESTOR PRESENTATION JANUARY 2020

Cautionary Statements

2

Forward-Looking StatementsThis presentation contains statements relating to the Company’s future business and financial performance and future events or developments that may constitute “forward-looking statements” within the meaning of the “safe harbor” provisions of the United States Private Securities Litigation Reform Act of 1995. These statements are based on current expectations and assumptions that are subject to risks and uncertainties. These statements include forward-looking statements with respect to the Company’s business and industry in general. Statements that include the words “expect,” “intend,” “plan,” “believe,” “project,” “forecast,” “estimate,” “may,” “should,” “anticipate,” "target," and similar words identify forward-looking statements. A variety of factors, many of which are beyond the Company’s control, affect the Company’s operations, performance, business strategies and results, and the Company’s actual results may differ materially from those indicated in these statements. These factors include, but are not limited to, continued compliance with governmental regulation, the ability to manage growth, requirements or changes affecting the Company's business, general economic and business conditions and the Company’s ability to open new restaurants and food and beverage locations in existing and new markets. More detailed information about these risk factors may be found in the Company’s filings with the Securities and Exchange Commission, including its Annual Report on Form 10-K for the year ended December 31, 2018. The statements made herein speak only as of the date of this presentation. The Company undertakes no obligation to update its forward-looking statements to reflect events or circumstances after the date of this presentation.

Non-GAAP Financial MeasuresThis presentation contains non-GAAP financial measures. A “non-GAAP financial measure” is a numerical measure of a company’s financial performance that excludes or includes amounts from a measure calculated and presented in accordance with GAAP in the consolidated statements of operations, balance sheets or statements of cash flows of the Company. These measures are presented because management uses this information to monitor and evaluate financial results and trends and believes this information to also be useful for investors. The Company has both wholly owned and partially owned subsidiaries. Total food and beverage sales at owned and managed units represents total revenue from owned operations as well as the sales reported to the Company by the owners of locations the Company manages, where it earns management and incentive fees. EBITDA is defined as net income before interest expense, provision for income taxes and depreciation and amortization. Adjusted EBITDA represents net income before interest expense, provision for income taxes, depreciation and amortization, non-cash impairment loss, non-cash rent, pre-opening expenses, non-recurring gains and losses and losses from discontinued operations. The disclosure of EBITDA and Adjusted EBITDA and other non-GAAP financial measures may not be comparable to similarly titled measures reported by other companies. EBITDA and Adjusted EBITDA should be considered in addition to, and not as a substitute for, or superior to, net income, operating income, cash flows, revenue, or other measures of financial performance prepared in accordance with GAAP. For a reconciliation of total food and beverage sales at owned and managed units, EBITDA, and Adjusted EBITDA to the most directly comparable financial measures presented in accordance with GAAP and a discussion of why we consider them useful, see the Company’s filings with the Securities and Exchange Commission, including its Annual Report on Form 10-K for the year ended December 31, 2018, and its Quarterly Report on Form 10-Q for the quarters ended September 30, 2018 and September 30, 2019.

.

3

We are a global hospitality company that develops and operates upscale

and polished casual, high-energy VIBE dining restaurants and turn-key

food & beverage services for hospitality venues including hotels,

casinos and other high-end locations.

Our clients and partners areleading entertainment and hospitality companies, including Disney, Marriott, Hyatt, Cosmopolitan and Melia Hotels.

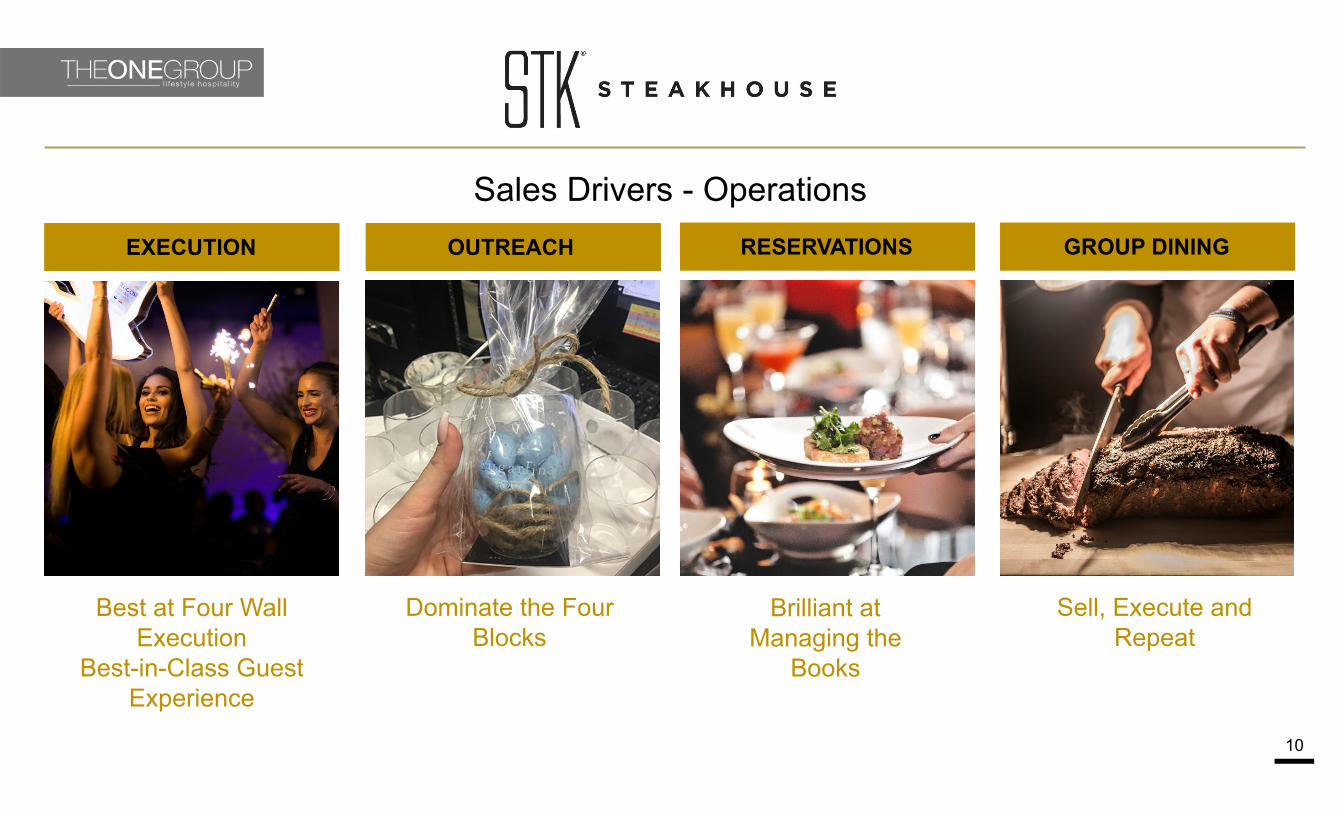

Execution: Best at Four Wall Execution -Best in Class at Guest Experience

Reservations: Brilliant at Managing the Books

Group Dining / Events: Sell, Execute and Repeat

Outreach: Dominate the Four Blocks

Holidays: Celebrate and Convert

Gift Cards: Top of Mind awareness -Advocate

Happy Hour: Build a Value and Entry-Level Layer / Convert to Dinner

Digital: Expand, Innovate and Win

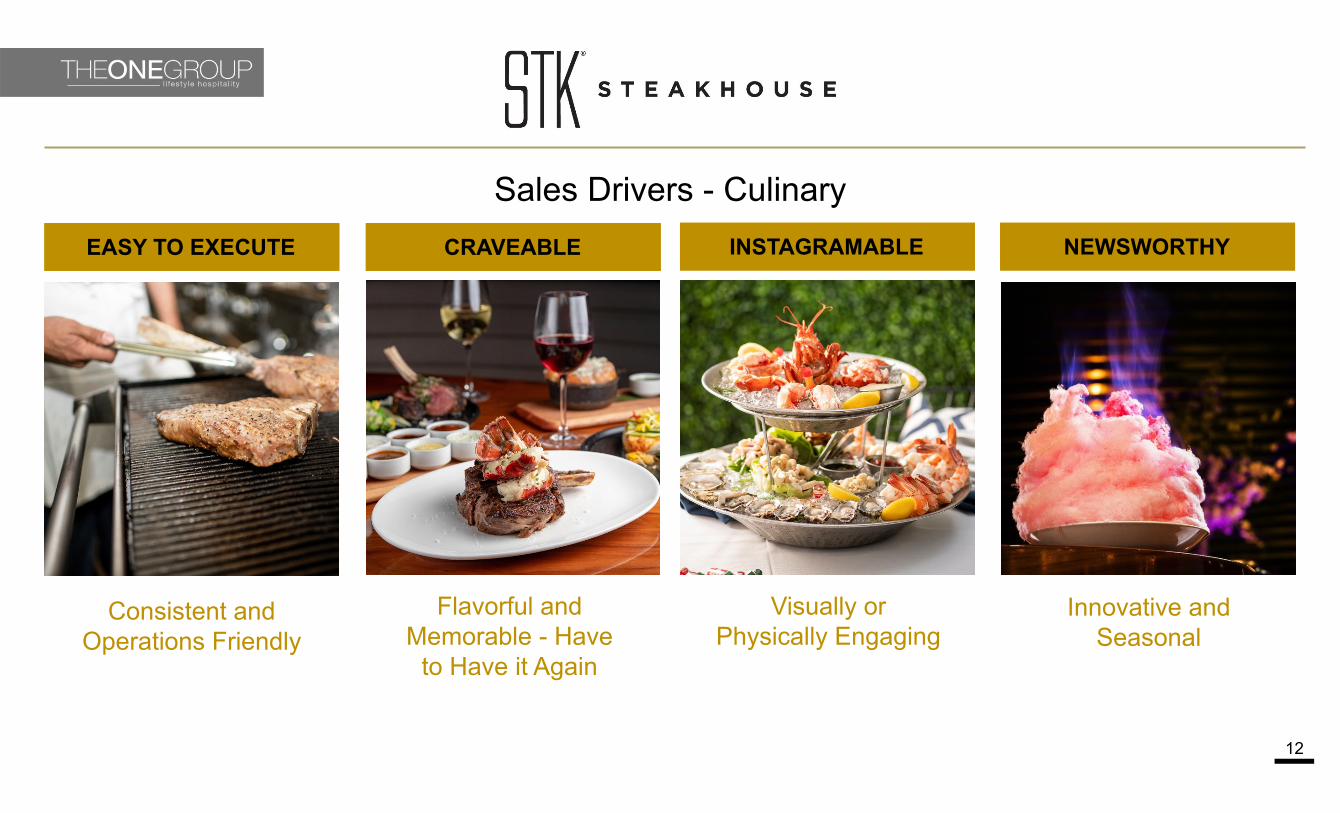

Craveable: Flavorful and Memorable-Have to Have it Again

Easy to Execute: Consistent and Operations Friendly

Newsworthy: Innovative / Seasonal

Instagramable: Visually or Physically Engaging

STRATEGY PILLARS

Vision: The Undisputed Global Leader In VIBE Dining.

Mission: To be the BEST Restaurant In Every Market That We Operate by Delivering Exceptional and Unforgettable Guest Experiences to Every Guest, Every Time.

OperationsOperations MarketingMarketing CulinaryCulinary

4

Company Overview

5

Key Financials (2020 Guidance) GAAP Revenue~ $200MM to $210MM

Global F&B Revenue~ $310MM to $320MM

G&A (excluding non-cash stock-based compensation):

~ 6% to 7% of GAAP Revenues

Adj. EBITDA: ~ $23MM to $25MM

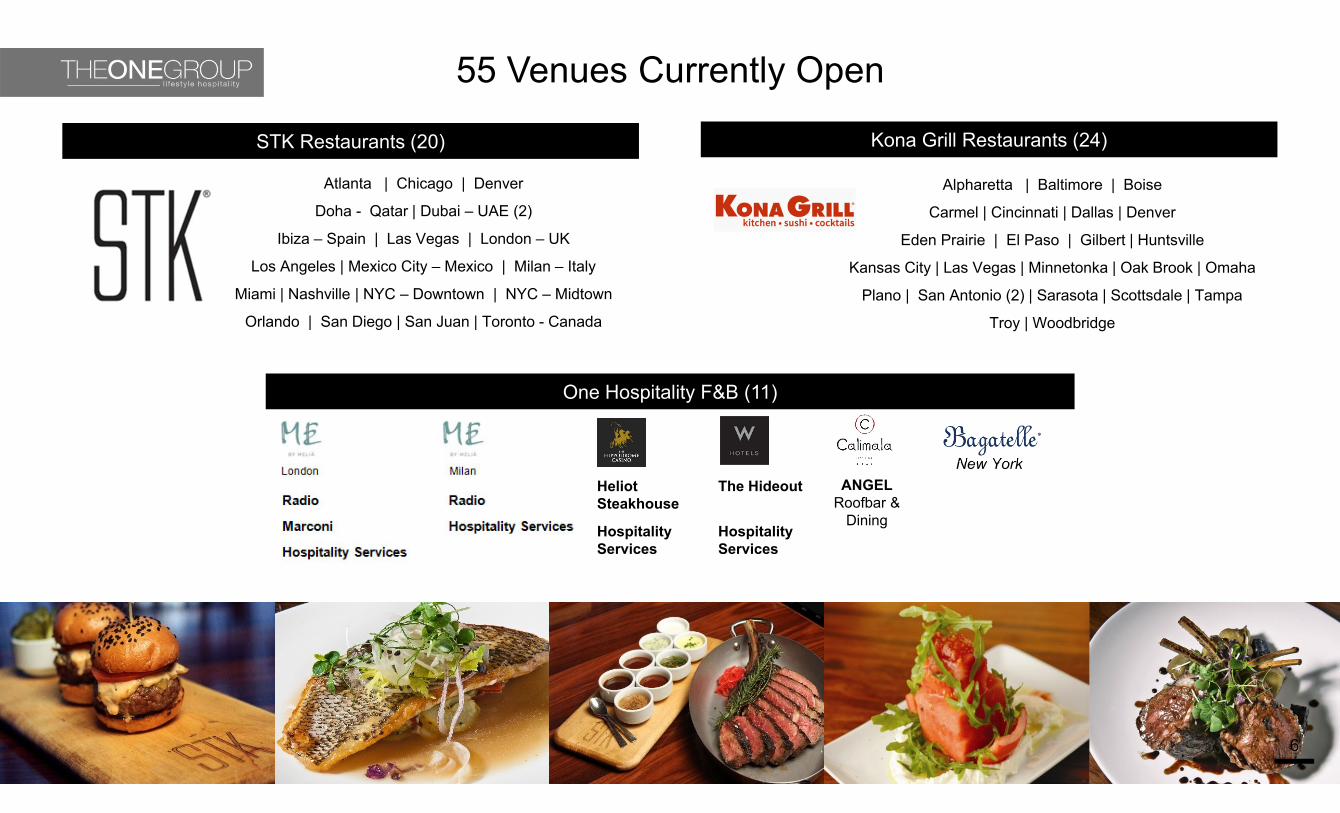

STK RESTAURANTS Upscale, high-energy steakhouse concept

Launched in NYC in 2006

Portfolio of 10 owned, 4 managed and 6 licensed restaurants

An additional 10 venues in operation or under lease / construction in North America, Europe and the Middle East

Includes both large and mid-sized market restaurants, rooftops, and offsite catering and events

STK brand US Sales in 2019 rose to a record $115 million

HOSPITALITY SERVICES

Unique opportunity to leverage restaurant and hospitality expertise, while utilizing Company-branded restaurants or tailored concepts

Generate high margin management and incentive fee income with minimal capital expenditure

Target opportunities generating a minimum of $8mm-10mm in food & beverage (“F&B”) sales

Six hospitality programs in operation

KONA GRILL RESTAURANTS

Polished casual, bar-centric grill concept

Launched in AZ in 1998

Portfolio of 24 owned locations in 17 states

Includes mid-sized markets and large market suburban restaurants, rooftops, catering and events

Kona Grill sales in 2020 projected to be approximately $100 million

Puerto Rico UAE Mexico SpainQatar

United Kingdom

Hippodrome CasinoLondon

ME HotelLondon

Italy

ME HotelMilan

The United States & Canada

The W HotelLos Angeles

(2020)

FlorenceF&B

One Hospitality F&B (11)

55 Venues Currently Open

6

New York

Atlanta | Chicago | Denver

Doha - Qatar | Dubai – UAE (2)

Ibiza – Spain | Las Vegas | London – UK

Los Angeles | Mexico City – Mexico | Milan – Italy

Miami | Nashville | NYC – Downtown | NYC – Midtown

Orlando | San Diego | San Juan | Toronto - Canada

STK Restaurants (20)

Heliot Steakhouse

The Hideout

Hospitality Services

Hospitality Services

ANGELRoofbar &

Dining

Alpharetta | Baltimore | Boise

Carmel | Cincinnati | Dallas | Denver

Eden Prairie | El Paso | Gilbert | Huntsville

Kansas City | Las Vegas | Minnetonka | Oak Brook | Omaha

Plano | San Antonio (2) | Sarasota | Scottsdale | Tampa

Troy | Woodbridge

Kona Grill Restaurants (24)

‐0.5% ‐0.3%‐1.4%

2.1%

0.1% 0.7% 1.1% 0.4%1.3%

0.4%2.0%

2.6%1.7% 1.9%

6.0%7.3% 7.5% 6.9%

15.0%

8.6%

6.4%

9.5% 8.9%

Q1 '17 Q2 '17 Q3 '17 Q4 '17 Q1 '18 Q2 '18 Q3 '18 Q4 '18 Q1 '19 Q2 '19 Q3 '19 Q4 '19

STK Same Store Sales GrowthFine Dining Steak Index* STK

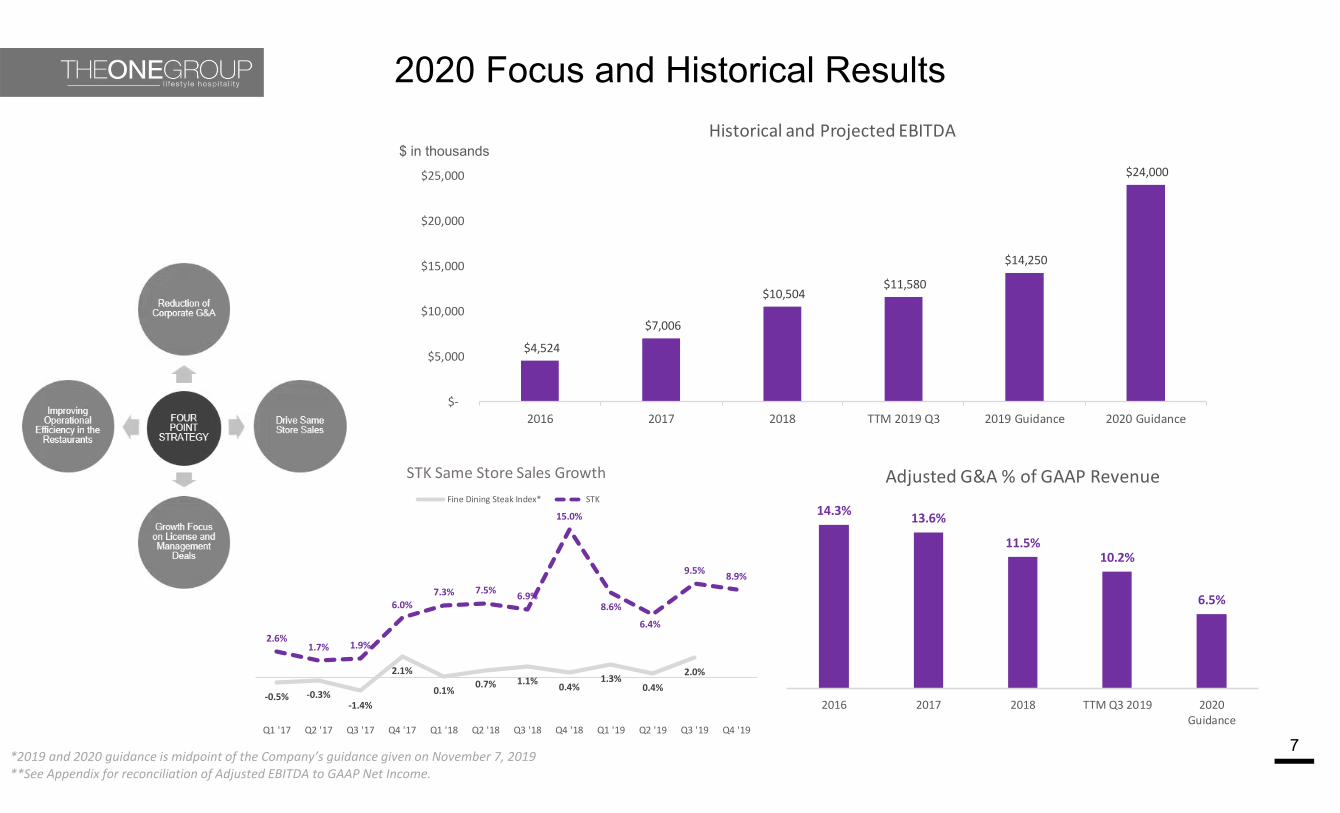

2020 Focus and Historical Results

7*2019 and 2020 guidance is midpoint of the Company’s guidance given on November 7, 2019

$4,524

$7,006

$10,504 $11,580

$14,250

$24,000

$‐

$5,000

$10,000

$15,000

$20,000

$25,000

2016 2017 2018 TTM 2019 Q3 2019 Guidance 2020 Guidance

Historical and Projected EBITDA$ in thousands

**See Appendix for reconciliation of Adjusted EBITDA to GAAP Net Income.

14.3% 13.6%

11.5%10.2%

6.5%

2016 2017 2018 TTM Q3 2019 2020Guidance

Adjusted G&A % of GAAP Revenue

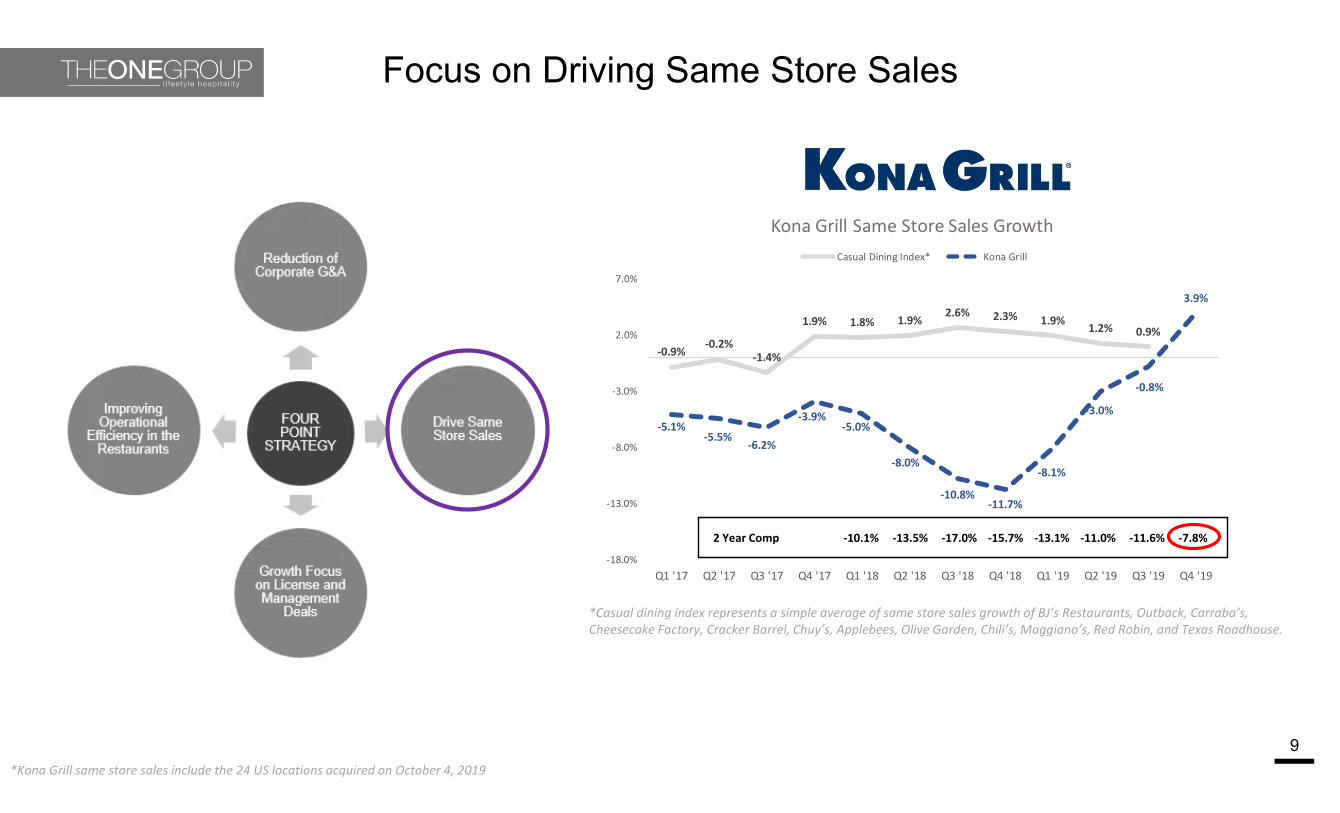

Focus on Driving Same Store Sales

8

*Fine dining steak index represents a simple average of same store sales growth of Del Friscos – Double Eagle (while public), Del Friscos – Grille (while public), Ruth’s Chris, Flemings, and Capital Grill

‐0.5% ‐0.3%‐1.4%

2.1%

0.1% 0.7% 1.1% 0.4%1.3%

0.4%2.0%

2.6%1.7% 1.9%

6.0%7.3% 7.5% 6.9%

15.0%

8.6%

6.4%

9.5% 8.9%

Q1 '17 Q2 '17 Q3 '17 Q4 '17 Q1 '18 Q2 '18 Q3 '18 Q4 '18 Q1 '19 Q2 '19 Q3 '19 Q4 '19

STK Same Store Sales GrowthFine Dining Steak Index* STK

Focus on Driving Same Store Sales

9

*Casual dining index represents a simple average of same store sales growth of BJ’s Restaurants, Outback, Carraba’s, Cheesecake Factory, Cracker Barrel, Chuy’s, Applebees, Olive Garden, Chili’s, Maggiano’s, Red Robin, and Texas Roadhouse.

‐0.9%‐0.2%

‐1.4%

1.9% 1.8% 1.9%2.6% 2.3% 1.9% 1.2% 0.9%

‐5.1%‐5.5%

‐6.2%

‐3.9%‐5.0%

‐8.0%

‐10.8%‐11.7%

‐8.1%

‐3.0%

‐0.8%

3.9%

‐18.0%

‐13.0%

‐8.0%

‐3.0%

2.0%

7.0%

Q1 '17 Q2 '17 Q3 '17 Q4 '17 Q1 '18 Q2 '18 Q3 '18 Q4 '18 Q1 '19 Q2 '19 Q3 '19 Q4 '19

Kona Grill Same Store Sales GrowthCasual Dining Index* Kona Grill

2 Year Comp ‐10.1% ‐13.5% ‐17.0% ‐15.7% ‐13.1% ‐11.0% ‐11.6% ‐7.8%

*Kona Grill same store sales include the 24 US locations acquired on October 4, 2019

10

Best at Four Wall Execution

Best-in-Class Guest Experience

Dominate the Four Blocks

Brilliant at Managing the

Books

Sell, Execute and Repeat

Sales Drivers - OperationsEXECUTION OUTREACH RESERVATIONS GROUP DINING

11

Celebrate andConvert

Top of Mind Awareness and

Advocacy

Build a Value and Entry-level Layer / Convert to Dinner

Expand, Innovate and Win

Sales Drivers - MarketingHOLIDAYS GIFT CARD PROMOTION HAPPY HOUR DIGITAL

12

Consistent and Operations Friendly

Flavorful and Memorable - Have

to Have it Again

Visually or Physically Engaging

Innovative and Seasonal

Sales Drivers - CulinaryEASY TO EXECUTE CRAVEABLE INSTAGRAMABLE NEWSWORTHY

13

Sales Drivers - Operations

Energize, Engage,and Elevate the Bar Business

Develop World-Class Restaurant

Leadership

Ignite & Dominate Delivery, Catering,

and Events

THE BAR LEADERSHIP EVENTS & CATERING

14

Sales Drivers - Bar

New Music Program New Uniforms New Happy Hour Menu: $3, $6, $9

Elevation of Drink Program:

Margarita Heaven

MUSIC UNIFORMS HAPPY HOUR ELEVATE

15

16

Sales Drivers - Leadership

Fully Staffed Restaurants

Hired Private Dining Sales Leadership

Developing Sales Driving Culture

STAFFING EVENT SALES SALES DRIVING

17

Sales Drivers - Events

Rollout New Software Program that Connects all Delivery Platforms

Launched New Events & Private

Dining Menu

Identified Spaces for Private Dining in Every

Location

Begin Relaunching of Offsite Catering

SOFTWARE MENU EVENT SPACES OFFSITE CATERING

18

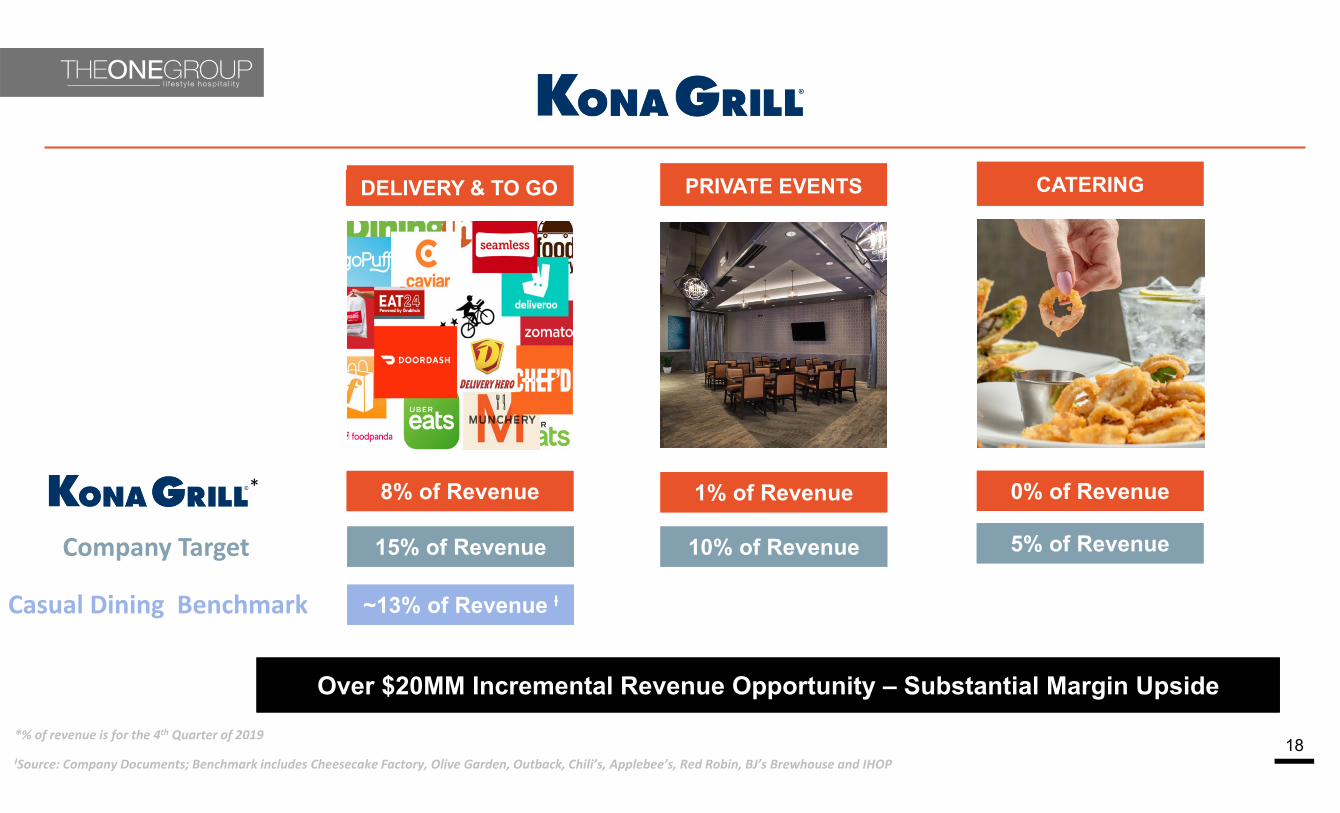

DELIVERY & TO GO PRIVATE EVENTS CATERING

Casual Dining Benchmark

8% of Revenue 1% of Revenue 0% of Revenue

~13% of Revenue Ɨ

Over $20MM Incremental Revenue Opportunity – Substantial Margin UpsideOver $20MM Incremental Revenue Opportunity – Substantial Margin Upside

*

*% of revenue is for the 4th Quarter of 2019

ƗSource: Company Documents; Benchmark includes Cheesecake Factory, Olive Garden, Outback, Chili’s, Applebee’s, Red Robin, BJ’s Brewhouse and IHOP

Company Target 15% of Revenue 10% of Revenue 5% of Revenue

19

Sales Drivers - Marketing

World Class Leader in Driving Reservations, Brand Awareness &

Engagement through Digital Platforms

Expand Customer Base through Gift Card Sales

throughout Holidays, and Everyday

Occasions

Become the Celebration Destination for All Major

Holidays, Converting Celebration Diners to

Regulars

Utilize as Value Driven Entry Point to Kona

Brand, Build Shoulder Periods, and Convert to

Dinner Guest

DIGITAL GIFT CARDS HOLIDAYS HAPPY HOUR

DEVELOPMENT

Levers for Expected Future Organic Growth

21

Hospitality Growth

Opportunity for at least 50 hospitality management agreements globally, 2-3 per city

Long-term target of 1-2 new hospitality management agreement per year

Would include an STK or uniquely tailored concept

Operational Initiatives

Drive same store sales through traffic and average check growth

Enhance margins by focusing on high-quality, high-margin food and beverage menu items

Leverage systemwide operating efficiencies and best practices to further drive EBITDA growth

STK Expansion

Opportunity for ~200 STKs globally, across large and mid-sized markets

Long-term target of 3-5 new STK restaurants per year

Blend of managed and licensed units, which require lower capital investment and produce high-margin royalty, management and incentive fee streams

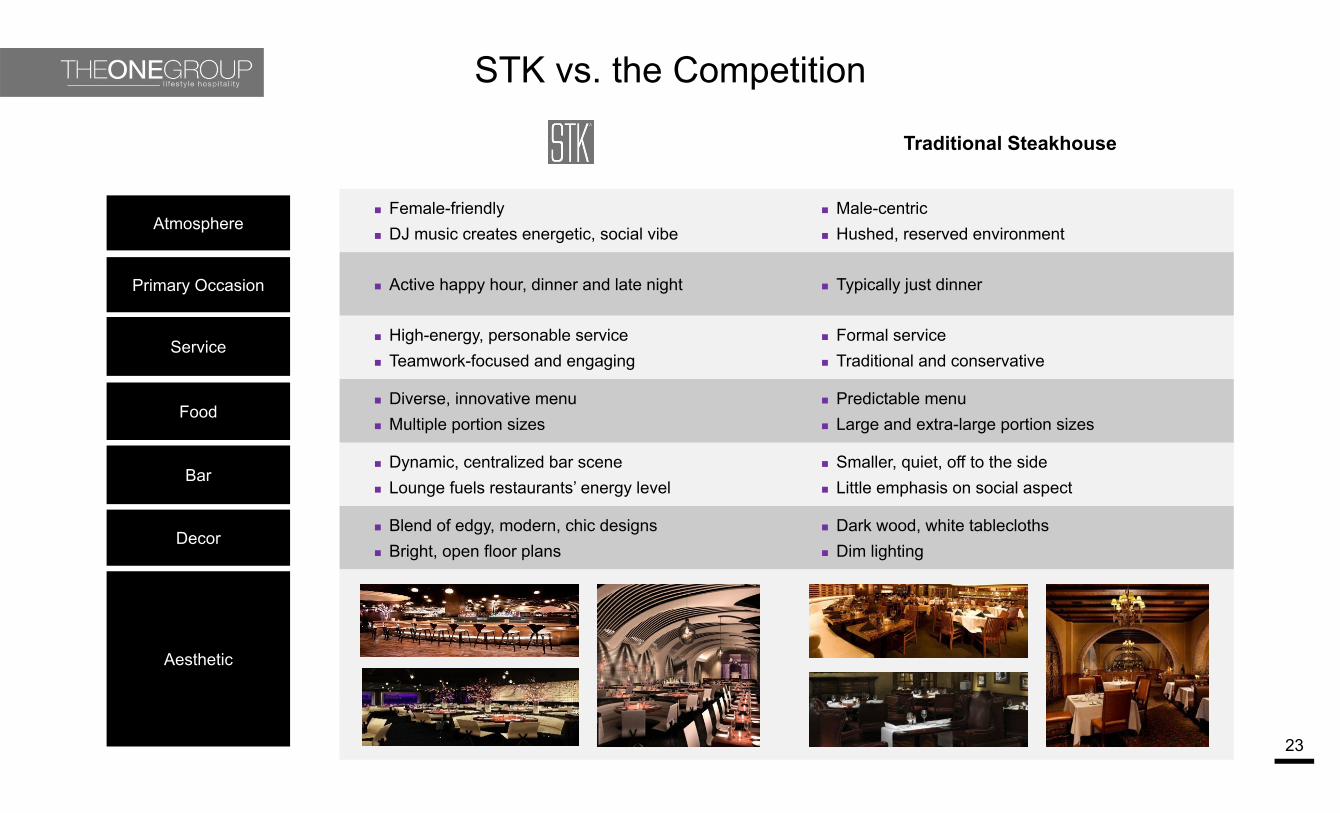

STK: Differentiated Steakhouse with High-Energy & Great Atmosphere

22

Reinvention of the traditional steakhouse

High-energy dining experience

Restaurants built around the bar, featuring DJ played music

High female to male customer mix

Destination locations

Superior quality with innovative menu

STK vs. the Competition

23

Traditional Steakhouse

Female-friendly DJ music creates energetic, social vibe

Male-centric Hushed, reserved environment

Active happy hour, dinner and late night Typically just dinner

High-energy, personable service Teamwork-focused and engaging

Formal service Traditional and conservative

Diverse, innovative menu Multiple portion sizes

Predictable menu Large and extra-large portion sizes

Dynamic, centralized bar scene Lounge fuels restaurants’ energy level

Smaller, quiet, off to the side Little emphasis on social aspect

Blend of edgy, modern, chic designs Bright, open floor plans

Dark wood, white tablecloths Dim lighting

Atmosphere

Food

Aesthetic

Decor

Bar

Service

Primary Occasion

One Night At STK

24

Premier Venues

25

STK – New York Downtown STK – Miami BeachSTK – Chicago

STK – Los Angeles STK – OrlandoSTK – NY Rooftop STK – Denver

STK – Milan STK – AtlantaSTK – Ibiza STK – Toronto

STK – Las Vegas

STK – London STK – New York Midtown STK – San Diego RooftopSTK – Orlando Rooftop

STK – Mexico City

STK – Dubai Downtown

STK – Dubai Marina

STK – San Diego

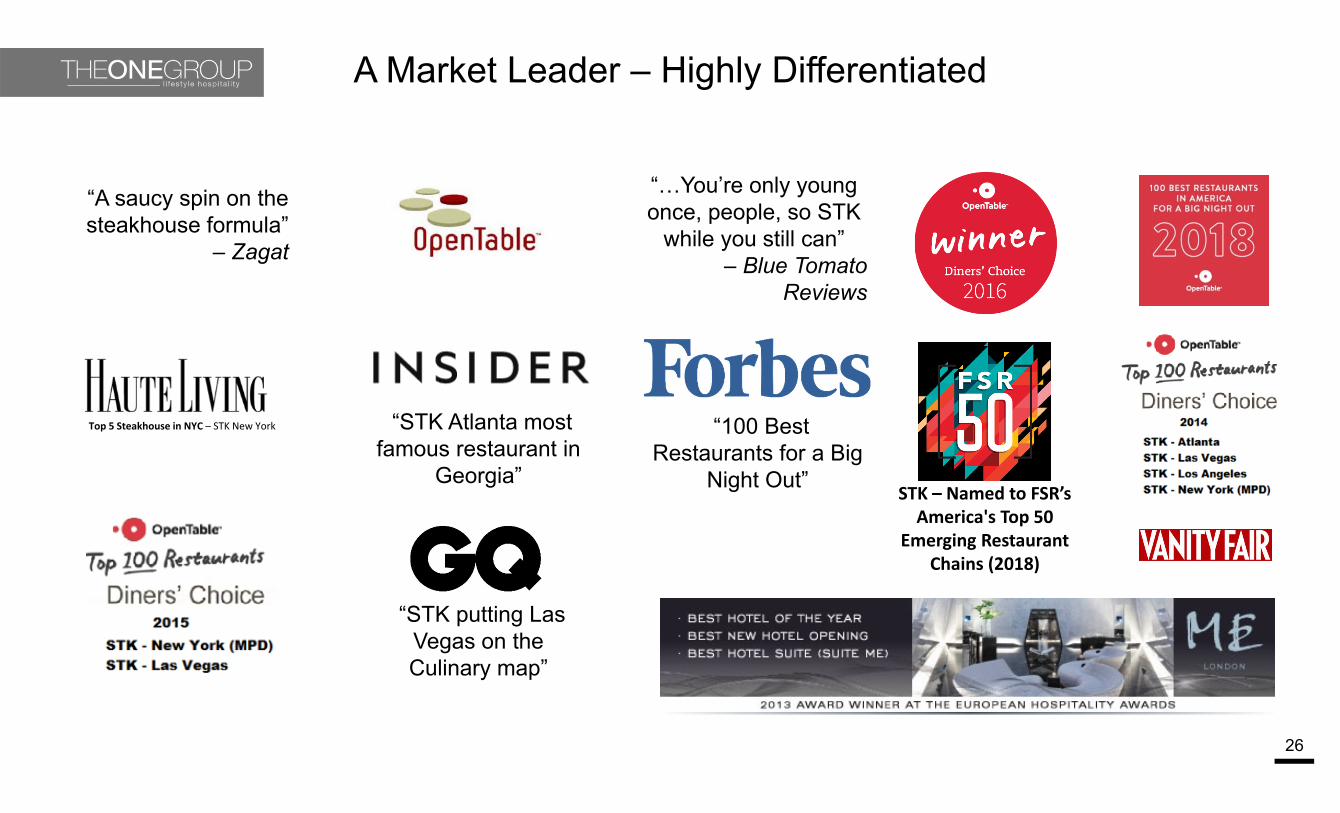

A Market Leader – Highly Differentiated

26

“A saucy spin on the steakhouse formula”

– Zagat

Top 5 Steakhouse in NYC – STK New York

“…You’re only young once, people, so STK

while you still can” – Blue Tomato

Reviews

STK – Named to FSR’s America's Top 50

Emerging Restaurant Chains (2018)

““STK Atlanta most famous restaurant in

Georgia”

““STK putting Las Vegas on the Culinary map”

““100 Best Restaurants for a Big

Night Out”

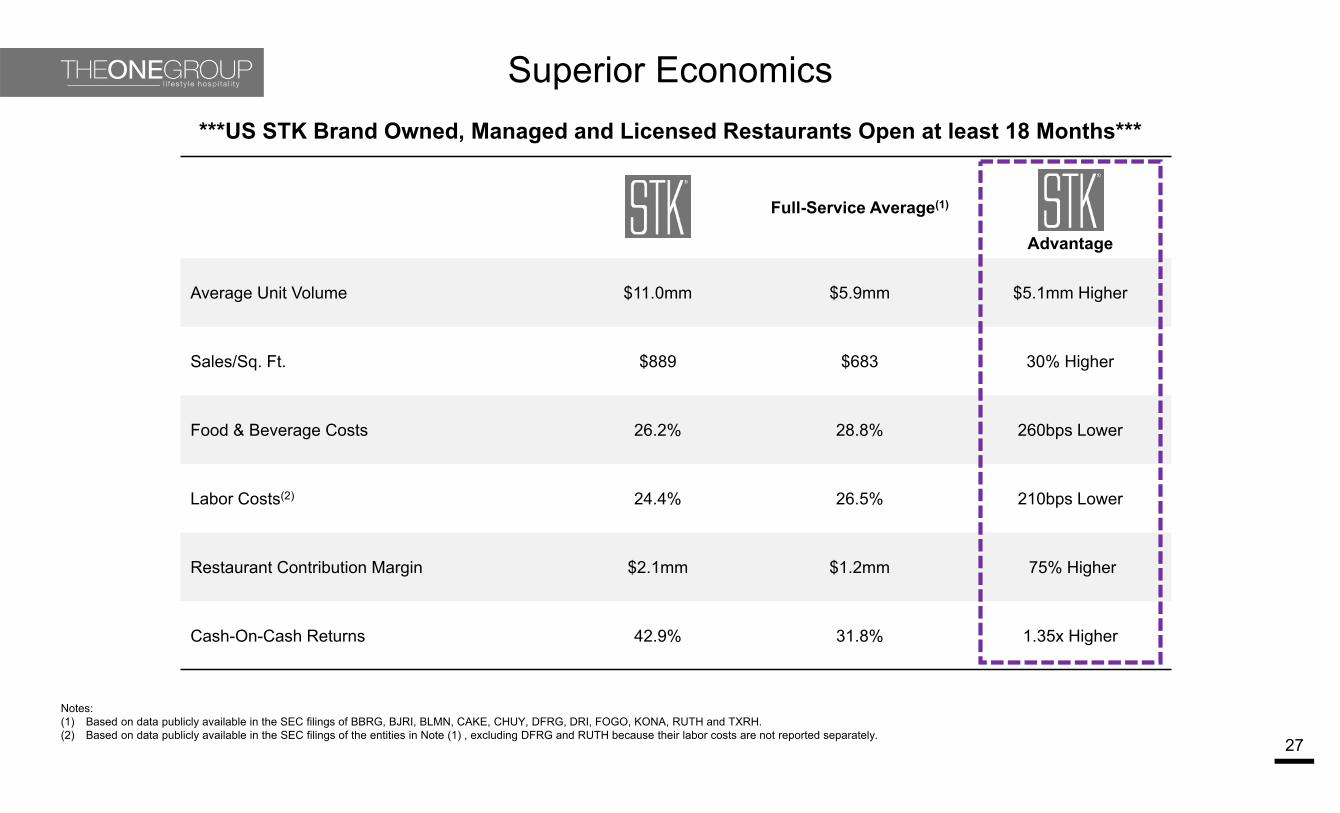

Superior Economics

27

***US STK Brand Owned, Managed and Licensed Restaurants Open at least 18 Months***

Full-Service Average(1)

Advantage

Average Unit Volume $11.0mm $5.9mm $5.1mm Higher

Sales/Sq. Ft. $889 $683 30% Higher

Food & Beverage Costs 26.2% 28.8% 260bps Lower

Labor Costs(2) 24.4% 26.5% 210bps Lower

Restaurant Contribution Margin $2.1mm $1.2mm 75% Higher

Cash-On-Cash Returns 42.9% 31.8% 1.35x Higher

Notes:(1) Based on data publicly available in the SEC filings of BBRG, BJRI, BLMN, CAKE, CHUY, DFRG, DRI, FOGO, KONA, RUTH and TXRH.(2) Based on data publicly available in the SEC filings of the entities in Note (1) , excluding DFRG and RUTH because their labor costs are not reported separately.

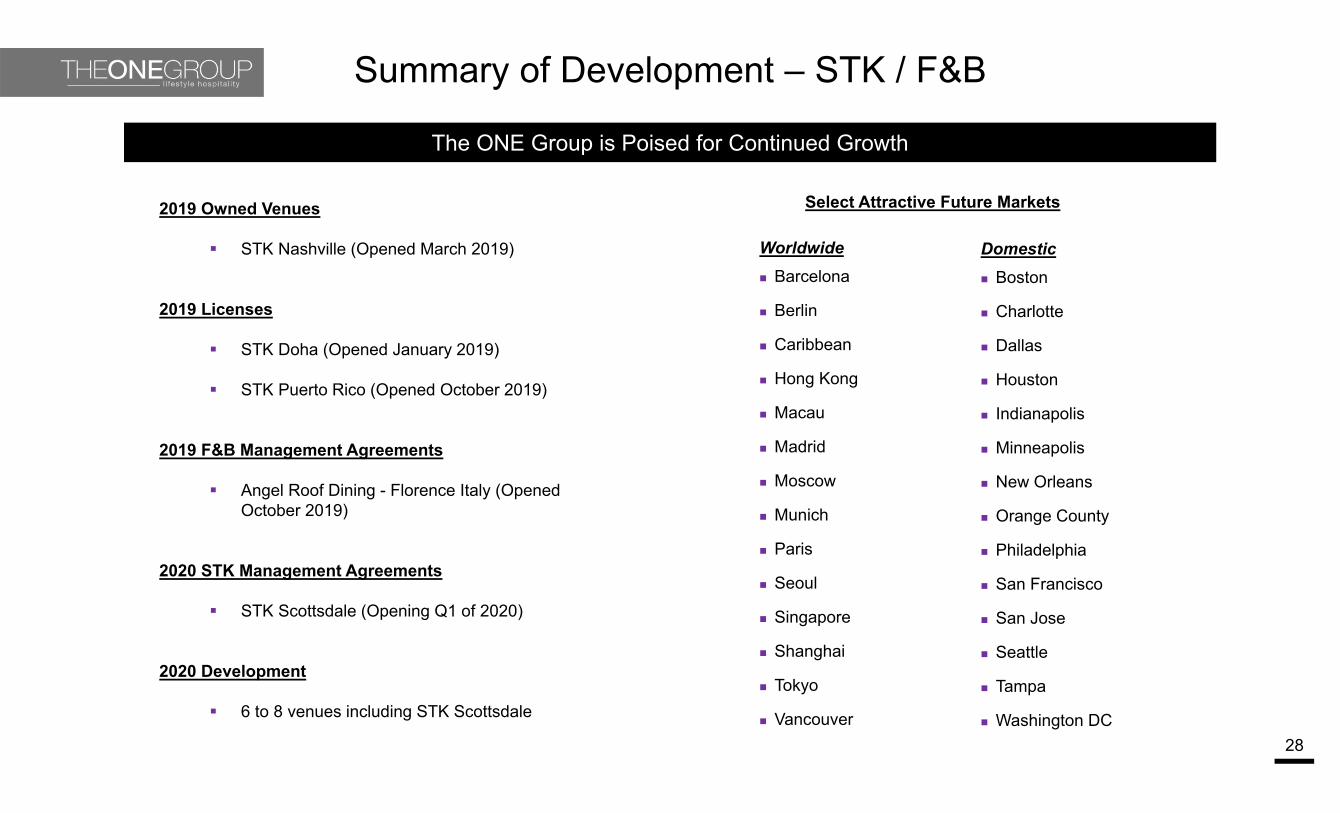

Summary of Development – STK / F&B

28

Select Attractive Future Markets

Worldwide Barcelona

Berlin

Caribbean

Hong Kong

Macau

Madrid

Moscow

Munich

Paris

Seoul

Singapore

Shanghai

Tokyo

Vancouver

Domestic Boston

Charlotte

Dallas

Houston

Indianapolis

Minneapolis

New Orleans

Orange County

Philadelphia

San Francisco

San Jose

Seattle

Tampa

Washington DC

2019 Owned Venues

STK Nashville (Opened March 2019)

2019 Licenses

STK Doha (Opened January 2019)

STK Puerto Rico (Opened October 2019)

2019 F&B Management Agreements

Angel Roof Dining - Florence Italy (Opened October 2019)

2020 STK Management Agreements

STK Scottsdale (Opening Q1 of 2020)

2020 Development

6 to 8 venues including STK Scottsdale

The ONE Group is Poised for Continued Growth

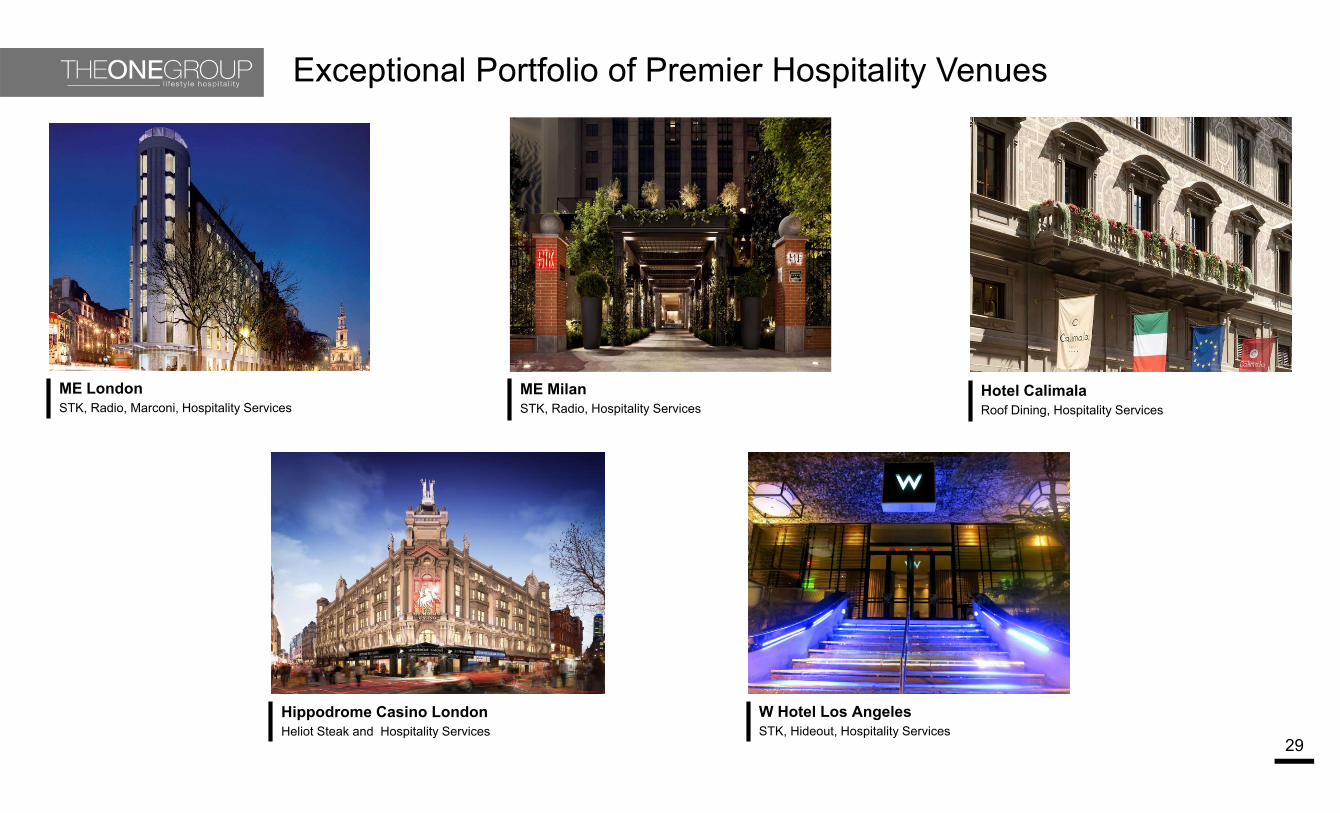

Exceptional Portfolio of Premier Hospitality Venues

29

ME MilanSTK, Radio, Hospitality Services

ME LondonSTK, Radio, Marconi, Hospitality Services

Hippodrome Casino LondonHeliot Steak and Hospitality Services

W Hotel Los AngelesSTK, Hideout, Hospitality Services

Hotel CalimalaRoof Dining, Hospitality Services

A Leading Hospitality Company – ONE Hospitality™

30

Comprehensive Portfolio of Internationally Recognized Brands

Comprehensive Portfolio of Internationally Recognized Brands

Growing List of RecognizedHotel Partners

Growing List of RecognizedHotel Partners

Note: Bagatelle, Marconi, Radio M, Asellina, Cucina Asellina, and Heliot are jointly owned and / or licensed brands.

Focus On Profitability ThroughImproving Restaurant Efficiency

31*Restaurant operating profit includes owned restaurant net revenues and expenses and exclude owned food, beverage and other net revenues and expenses**See Appendix for reconciliation of Adjusted EBITDA to GAAP Net Income.

$6.0

$9.1 $9.9

$‐

$2.0

$4.0

$6.0

$8.0

$10.0

$12.0

2017 2018 TTM Q3 2019

Restaurant Operating Profit ($ millions)

10.2%

13.8% 13.5%

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

14.0%

16.0%

2017 2018 TTM Q3 2019

Restaurant Operating Profit %

FINANCIAL REVIEW

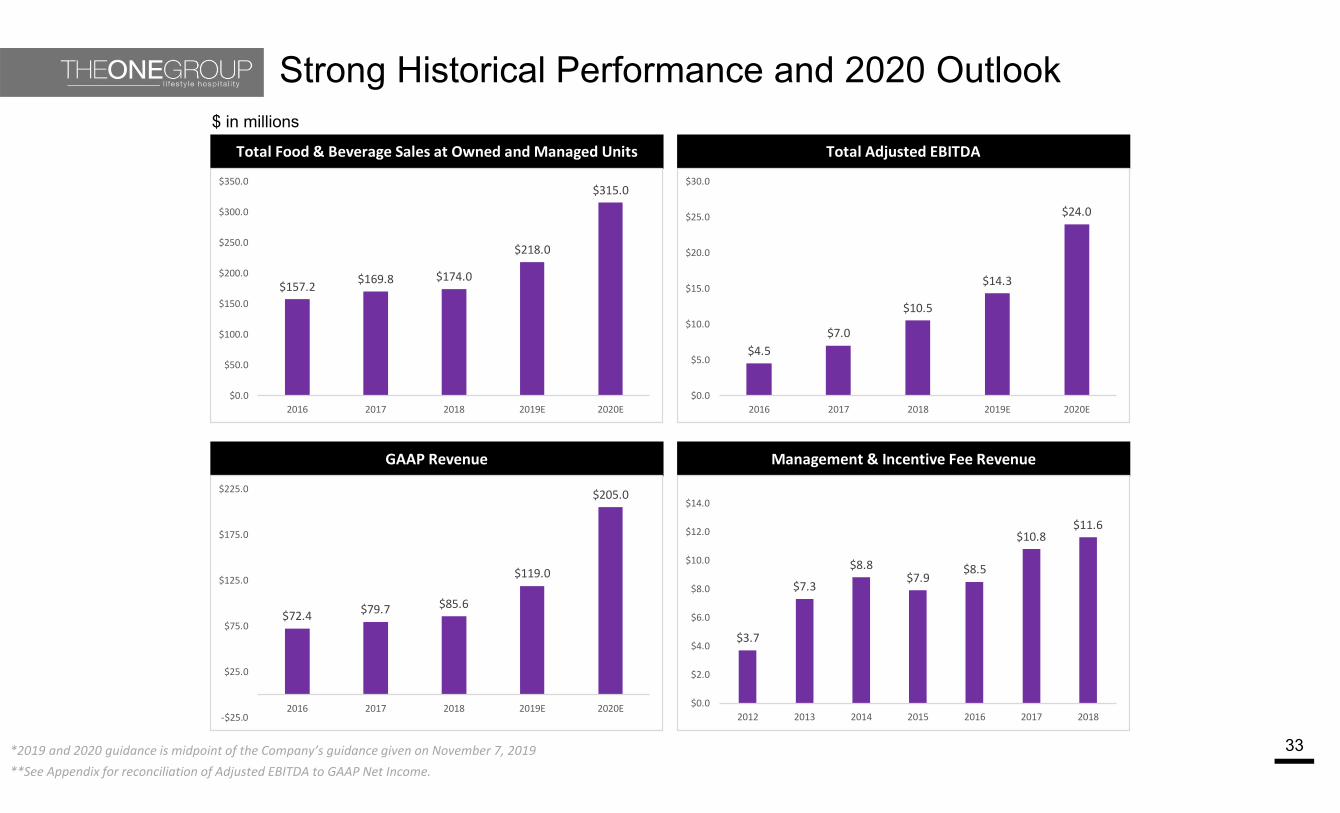

Strong Historical Performance and 2020 Outlook

33

$ in millions

*2019 and 2020 guidance is midpoint of the Company’s guidance given on November 7, 2019

Total Food & Beverage Sales at Owned and Managed Units Total Adjusted EBITDA

GAAP Revenue Management & Incentive Fee Revenue

$157.2 $169.8 $174.0

$218.0

$315.0

$0.0

$50.0

$100.0

$150.0

$200.0

$250.0

$300.0

$350.0

2016 2017 2018 2019E 2020E

$4.5$7.0

$10.5

$14.3

$24.0

$0.0

$5.0

$10.0

$15.0

$20.0

$25.0

$30.0

2016 2017 2018 2019E 2020E

$72.4 $79.7 $85.6

$119.0

$205.0

‐$25.0

$25.0

$75.0

$125.0

$175.0

$225.0

2016 2017 2018 2019E 2020E

$3.7

$7.3

$8.8$7.9

$8.5

$10.8$11.6

$0.0

$2.0

$4.0

$6.0

$8.0

$10.0

$12.0

$14.0

2012 2013 2014 2015 2016 2017 2018

**See Appendix for reconciliation of Adjusted EBITDA to GAAP Net Income.

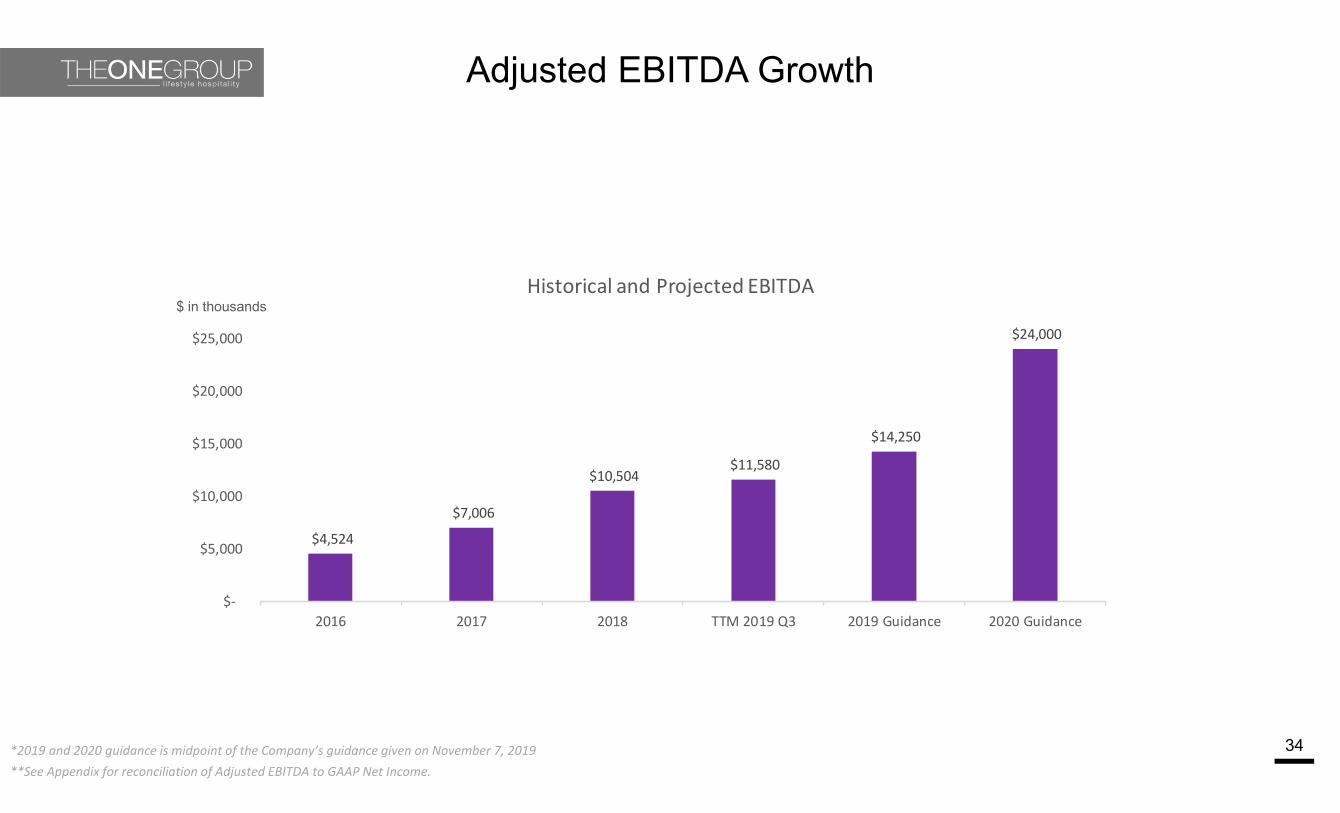

$4,524

$7,006

$10,504 $11,580

$14,250

$24,000

$‐

$5,000

$10,000

$15,000

$20,000

$25,000

2016 2017 2018 TTM 2019 Q3 2019 Guidance 2020 Guidance

Historical and Projected EBITDA

Adjusted EBITDA Growth

34

$ in thousands

*2019 and 2020 guidance is midpoint of the Company’s guidance given on November 7, 2019**See Appendix for reconciliation of Adjusted EBITDA to GAAP Net Income.

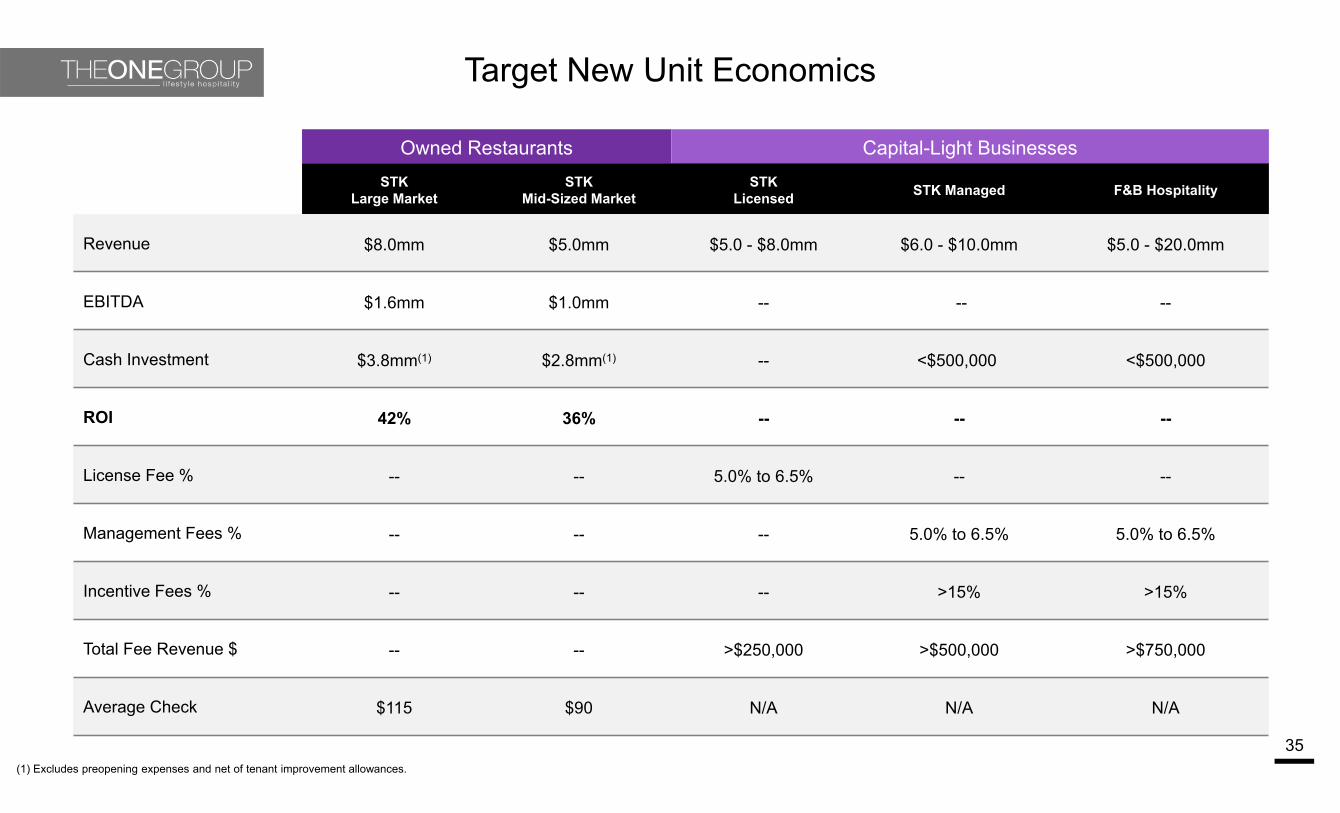

Target New Unit Economics

35

Owned Restaurants Capital-Light BusinessesSTK

Large MarketSTK

Mid-Sized MarketSTK

Licensed STK Managed F&B Hospitality

Revenue $8.0mm $5.0mm $5.0 - $8.0mm $6.0 - $10.0mm $5.0 - $20.0mm

EBITDA $1.6mm $1.0mm -- -- --

Cash Investment $3.8mm(1) $2.8mm(1) -- <$500,000 <$500,000

ROI 42% 36% -- -- --

License Fee % -- -- 5.0% to 6.5% -- --

Management Fees % -- -- -- 5.0% to 6.5% 5.0% to 6.5%

Incentive Fees % -- -- -- >15% >15%

Total Fee Revenue $ -- -- >$250,000 >$500,000 >$750,000

Average Check $115 $90 N/A N/A N/A

(1) Excludes preopening expenses and net of tenant improvement allowances.

STK GAAP Revenue and EBITDA Contribution by Ownership Type(Example - Illustrative Purposes Only)

36(1) Excludes preopening expenses and net of tenant improvement allowances.

*Assume 5.0% license fee and 50/50 split of restaurant EBITDA less license fees

Company-ownedManagement Agreement

License Agreement

System-wide Revenue $5.0MM $5.0MM $5.0MM

COGS 25% 25% 25%

Other Operating 55% 55% 55%

Restaurant EBITDA (Before License & Management Fees) $1.0MM $1.0MM $1.0MM

Management & License Revenue* -$ $250K $250K

Profit Share* -$ $375K $250K

GAAP Revenue $5.0MM $625K $250K

EBITDA Contribution $1.0MM $625K $250K

Cash Investment(1)$2.8MM -$ -$

Focus On Reduction of Corporate G&A to Increase Profitability & Improve Leverage

37*Adjusted G&A does not include stock‐based compensation or integration expenses**See Appendix for reconciliation of Adjusted G&A to GAAP G&A.

$10.3 $10.8 $9.8 $9.6

$13.3

$‐

$2.0

$4.0

$6.0

$8.0

$10.0

$12.0

$14.0

2016 2017 2018 TTM Q3 2019 2020Guidance

Adjusted G&A ($ millions)

14.3% 13.6%

11.5%10.2%

6.5%

2016 2017 2018 TTM Q3 2019 2020Guidance

Adjusted G&A % of GAAP Revenue

***2020 guidance is midpoint of the Company’s guidance given on November 7, 2019

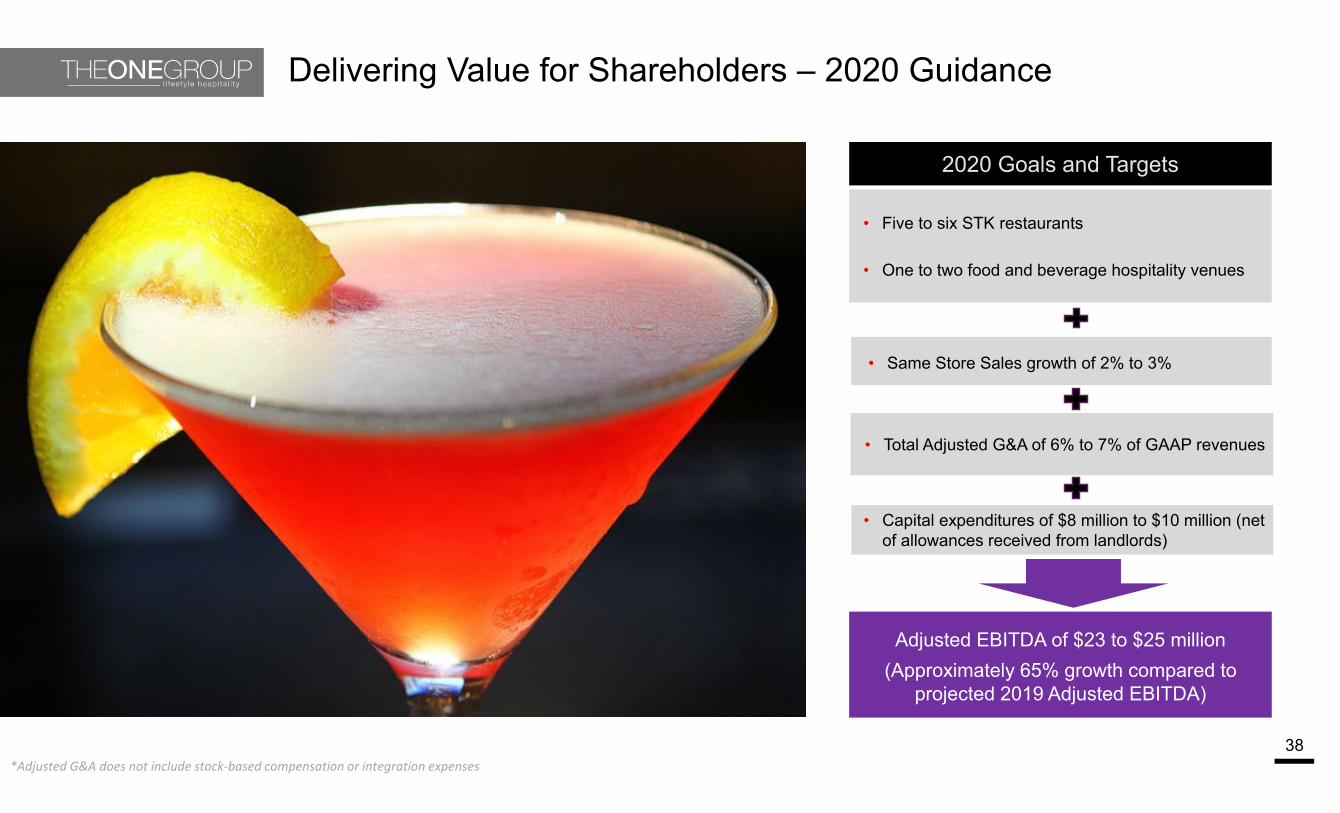

Delivering Value for Shareholders – 2020 Guidance

38

• Five to six STK restaurants

• One to two food and beverage hospitality venues

Adjusted EBITDA of $23 to $25 million(Approximately 65% growth compared to

projected 2019 Adjusted EBITDA)

2020 Goals and Targets

• Same Store Sales growth of 2% to 3%

• Capital expenditures of $8 million to $10 million (net of allowances received from landlords)

• Total Adjusted G&A of 6% to 7% of GAAP revenues

*Adjusted G&A does not include stock‐based compensation or integration expenses

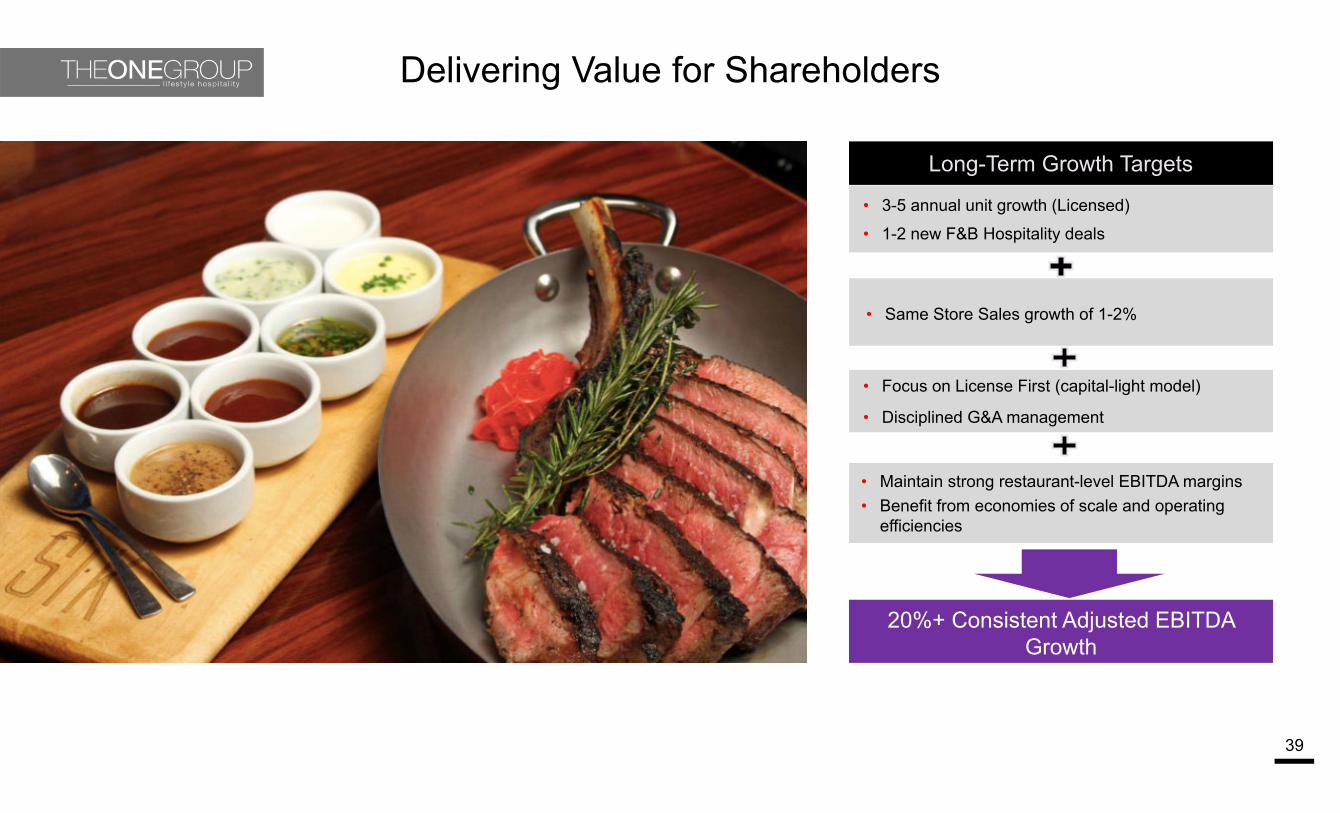

Delivering Value for Shareholders

39

• 3-5 annual unit growth (Licensed)• 1-2 new F&B Hospitality deals

20%+ Consistent Adjusted EBITDA Growth

Long-Term Growth Targets

• Same Store Sales growth of 1-2%

• Maintain strong restaurant-level EBITDA margins• Benefit from economies of scale and operating

efficiencies

• Focus on License First (capital-light model)

• Disciplined G&A management

The ONE Group Highlights

40

Fast Growing Hospitality Company

Strong Management Team and Infrastructure to Support

Growth

Multiple Levers to Drive Revenues and Profitability

Significant Pipeline for Unit Growth in 2020 and

Beyond

Strong Portfolio of High Volume, High Margin Brands with Industry Leading ROIC

Acquisitions can Further Enhances our Brand Portfolio

and Unit Pipeline

Well Positioned for Significant Growth in a

Transforming Hospitality Sector

APPENDIX

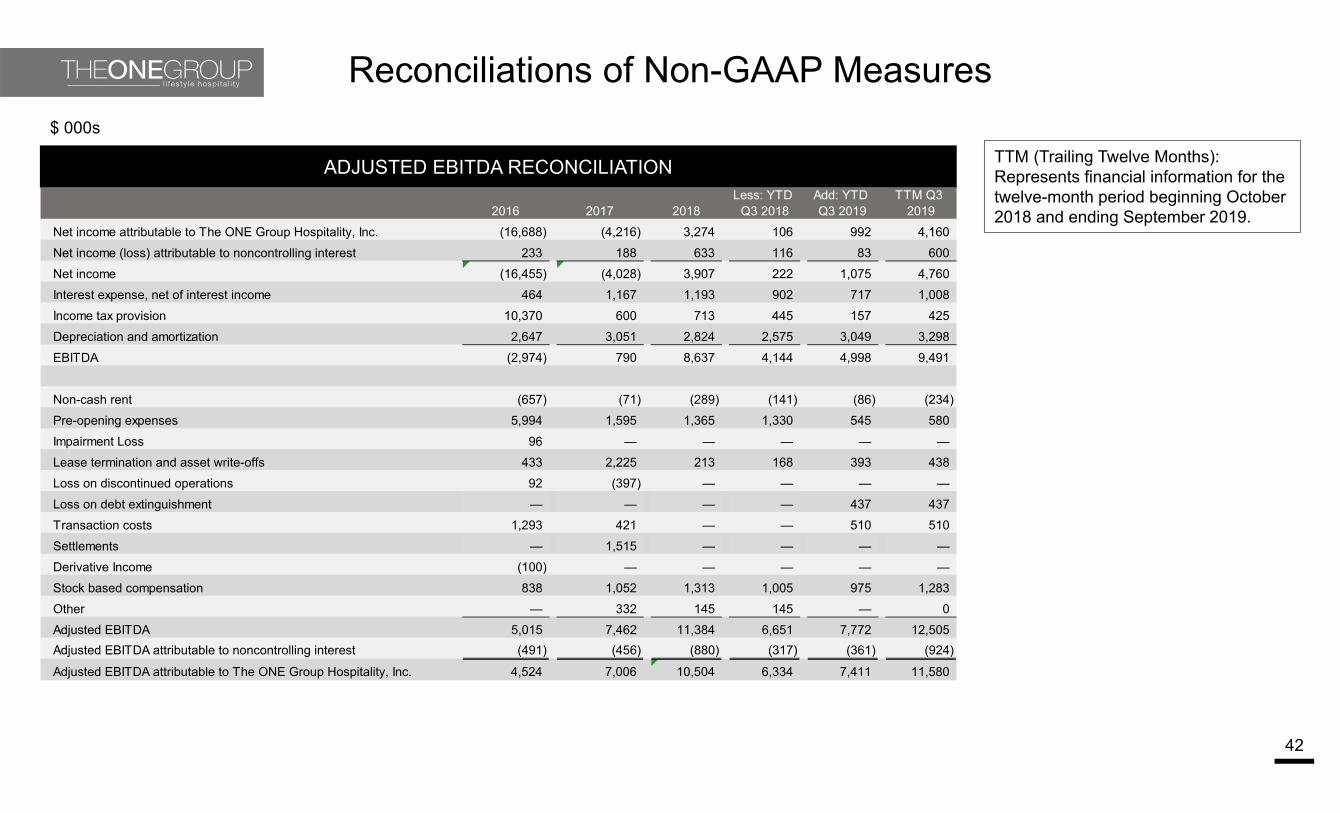

Reconciliations of Non-GAAP Measures

42

ADJUSTED EBITDA RECONCILIATION

$ 000s

TTM (Trailing Twelve Months): Represents financial information for the twelve-month period beginning October 2018 and ending September 2019. 2016 2017 2018

Less: YTD Q3 2018

Add: YTD Q3 2019

TTM Q3 2019

Net income attributable to The ONE Group Hospitality, Inc. (16,688) (4,216) 3,274 106 992 4,160Net income (loss) attributable to noncontrolling interest 233 188 633 116 83 600Net income (16,455) (4,028) 3,907 222 1,075 4,760Interest expense, net of interest income 464 1,167 1,193 902 717 1,008Income tax provision 10,370 600 713 445 157 425Depreciation and amortization 2,647 3,051 2,824 2,575 3,049 3,298EBITDA (2,974) 790 8,637 4,144 4,998 9,491

Non-cash rent (657) (71) (289) (141) (86) (234)Pre-opening expenses 5,994 1,595 1,365 1,330 545 580Impairment Loss 96 — — — — —Lease termination and asset write-offs 433 2,225 213 168 393 438Loss on discontinued operations 92 (397) — — — —Loss on debt extinguishment — — — — 437 437Transaction costs 1,293 421 — — 510 510Settlements — 1,515 — — — —Derivative Income (100) — — — — —Stock based compensation 838 1,052 1,313 1,005 975 1,283Other — 332 145 145 — 0Adjusted EBITDA 5,015 7,462 11,384 6,651 7,772 12,505Adjusted EBITDA attributable to noncontrolling interest (491) (456) (880) (317) (361) (924)

Adjusted EBITDA attributable to The ONE Group Hospitality, Inc. 4,524 7,006 10,504 6,334 7,411 11,580

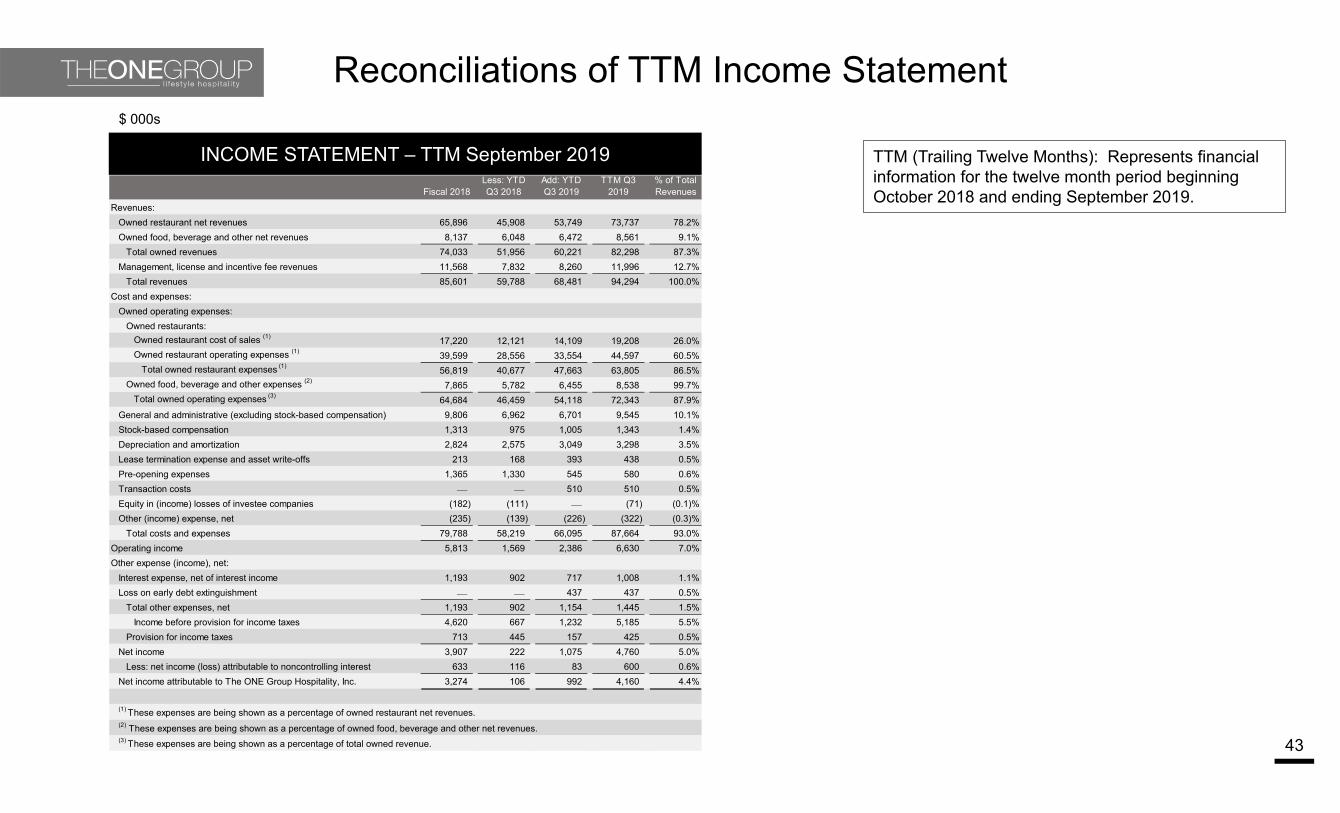

Reconciliations of TTM Income Statement

43

INCOME STATEMENT – TTM September 2019

$ 000s

Fiscal 2018Less: YTD Q3 2018

Add: YTD Q3 2019

TTM Q3 2019

% of Total Revenues

Revenues:Owned restaurant net revenues 65,896 45,908 53,749 73,737 78.2%Owned food, beverage and other net revenues 8,137 6,048 6,472 8,561 9.1%

Total owned revenues 74,033 51,956 60,221 82,298 87.3%Management, license and incentive fee revenues 11,568 7,832 8,260 11,996 12.7%

Total revenues 85,601 59,788 68,481 94,294 100.0%Cost and expenses:

Owned operating expenses:Owned restaurants:

Owned restaurant cost of sales (1) 17,220 12,121 14,109 19,208 26.0%Owned restaurant operating expenses (1) 39,599 28,556 33,554 44,597 60.5%

Total owned restaurant expenses (1) 56,819 40,677 47,663 63,805 86.5%Owned food, beverage and other expenses (2) 7,865 5,782 6,455 8,538 99.7%

Total owned operating expenses (3) 64,684 46,459 54,118 72,343 87.9%General and administrative (excluding stock-based compensation) 9,806 6,962 6,701 9,545 10.1%Stock-based compensation 1,313 975 1,005 1,343 1.4%Depreciation and amortization 2,824 2,575 3,049 3,298 3.5%Lease termination expense and asset write-offs 213 168 393 438 0.5%Pre-opening expenses 1,365 1,330 545 580 0.6%Transaction costs — — 510 510 0.5%Equity in (income) losses of investee companies (182) (111) — (71) (0.1)%Other (income) expense, net (235) (139) (226) (322) (0.3)%

Total costs and expenses 79,788 58,219 66,095 87,664 93.0%Operating income 5,813 1,569 2,386 6,630 7.0%Other expense (income), net:

Interest expense, net of interest income 1,193 902 717 1,008 1.1%Loss on early debt extinguishment — — 437 437 0.5%

Total other expenses, net 1,193 902 1,154 1,445 1.5%Income before provision for income taxes 4,620 667 1,232 5,185 5.5%

Provision for income taxes 713 445 157 425 0.5%Net income 3,907 222 1,075 4,760 5.0%

Less: net income (loss) attributable to noncontrolling interest 633 116 83 600 0.6%Net income attributable to The ONE Group Hospitality, Inc. 3,274 106 992 4,160 4.4%

(1) These expenses are being shown as a percentage of owned restaurant net revenues.(2) These expenses are being shown as a percentage of owned food, beverage and other net revenues.(3) These expenses are being shown as a percentage of total owned revenue.

TTM (Trailing Twelve Months): Represents financial information for the twelve month period beginning October 2018 and ending September 2019.

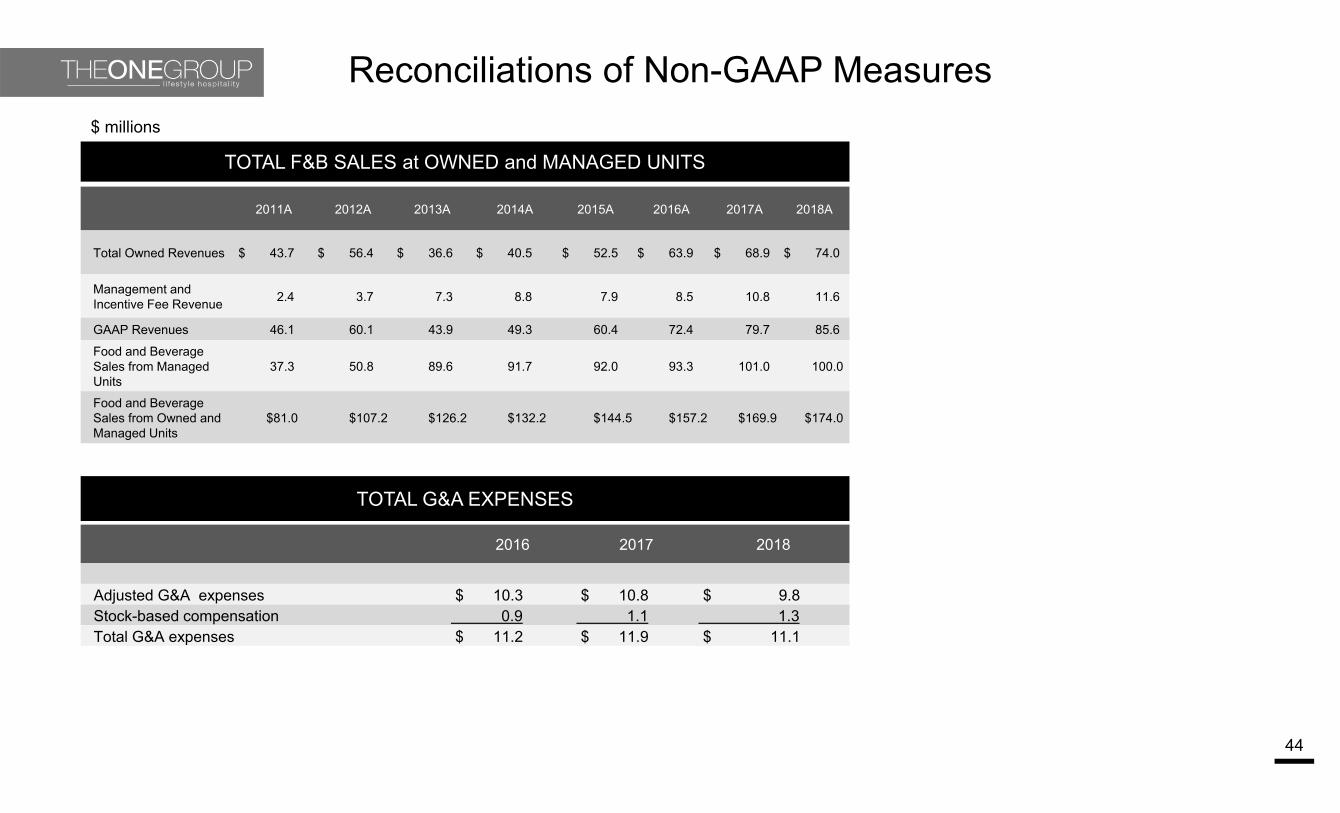

Reconciliations of Non-GAAP Measures

44

2011A 2012A 2013A 2014A 2015A 2016A 2017A 2018A

Total Owned Revenues $ 43.7 $ 56.4 $ 36.6 $ 40.5 $ 52.5 $ 63.9 $ 68.9 $ 74.0

Management and Incentive Fee Revenue 2.4 3.7 7.3 8.8 7.9 8.5 10.8 11.6

GAAP Revenues 46.1 60.1 43.9 49.3 60.4 72.4 79.7 85.6

Food and Beverage Sales from Managed Units

37.3 50.8 89.6 91.7 92.0 93.3 101.0 100.0

Food and Beverage Sales from Owned and Managed Units

$81.0 $107.2 $126.2 $132.2 $144.5 $157.2 $169.9 $174.0

TOTAL F&B SALES at OWNED and MANAGED UNITS

$ millions

2016 2017 2018

Adjusted G&A expenses $ 10.3 $ 10.8 $ 9.8Stock-based compensation 0.9 1.1 1.3 Total G&A expenses $ 11.2 $ 11.9 $ 11.1

TOTAL G&A EXPENSES