Embed Size (px)

Citation preview

Investor Presentation

May 2010

Safe HarborForward-Looking Statements

This presentation contains certain forward-looking information within the meaning of the PrivateSecurities Litigation Reform Act of 1995. The words “believe,” “expect,” “anticipate,” “estimate,” “target,”and similar expressions, among others, identify forward-looking statements. All forward-lookingstatements are based on information currently available to management. Such forward-lookingstatements are subject to certain risks and uncertainties that could cause events and the Company’sactual results to differ materially from those expressed or implied. Please see the disclosure regardingforward-looking statements immediately preceding Part I of the Company’s Annual Report on Form 10-Kfor the fiscal year ended October 31, 2009. The Company assumes no obligation to update anyforward-looking statements.

Regulation G

This presentation includes certain non-GAAP financial measures that exclude restructuring and otherunusual charges and gains that are volatile from period to period. Management believes the non-GAAPmeas res pro ide a better indication of operational performance and a more stable platform on hich tomeasures provide a better indication of operational performance and a more stable platform on which tocompare the historical performance of the Company than the most nearly equivalent GAAP data. Allnon-GAAP data in the presentation are indicated by footnotes. Tables showing the reconciliationbetween GAAP and non-GAAP measures are available at the end of this presentation and on the GreifW b it t if

2

Web site at www.greif.com.

Greif Profile

• Founded in 1877 as a packaging companycompany

• Initial public offering in 1926

• Diversified business platform

• Leading industrial packaging companywith over 30% global market share

• Approximately 200 operations in morethan 45 countries

3

Twelve months ended January 31 2010

Diversified Business Platform(Dollars in millions)Twelve months ended January 31, 2010

Sales $2,836

Operating Profit (1)

$304

Industrial Packaging

Paper Packaging

Land Management

Sales $2,302

Operating Profit (1)

$250

Sales $514

Operating Profit (1)

$32

Sales $20

Operating Profit (1)

$22

4

(1) Before restructuring charges, restructuring-related inventory charges, acquisition-related costs and timberland disposals, net. See GAAP to Non-GAAP reconciliation included in the Appendix of this presentation.

Our AspirationsTop-quartile performance• Organic growth: 5.0%

• Operating profit margin: 12.5%

Top-quartile performance metrics• Organic growth: 5.0%

• Operating profit margin: 12.5%SG&A t t l 7 5%

Preferred productivity partner• Compelling value proposition

based on what customers are willing to pay for

Growth • SG&A to net sales: 7.5%• OWC to net sales: 7.5%• RONA: 25.0%

• SG&A to net sales: 7.5%• OWC to net sales: 7.5%• RONA: 25.0%

willing to pay for• Low-cost provider of high-quality

products with consistent and reliable delivery

Value

People ProductivityPeople Productivity

Strong performance ethicT t

Strong performance ethic• Transparent governance

Productivity imperative• Real-cost productivity: ≥ 4% per year• Transparent governance

structure• Performance management • Talent and succession

management

a spa e t go e a cestructure

• Performance management • Talent and succession

management

ea cost p oduct ty % pe yea• Capital productivity

› Asset turns: ≥ 2x› World-class strategic sourcing

capabilities

5

management capabilities

Note: Performance metrics over a complete business cycle.

Our Catalyst – Greif Business System

The Greif WayGreif Production S tSystem

Greif Operational

WorkingCapital

Global Operating System

Operational Excellence

Commercial Excellence

Supply Chain

Core Processes

Strategy People Performance Management

6

Greif Business System Illustrated

Operational Commercial Global Sourcing Working Capital

Holistic Approach

Excellence Excellence and Supply Chaing p

Key Overall Equipment Pocket Margin Identify key suppliers & Fully integrated yElements

q pEffectiveness (OEE)

5S (Sort/Set in Order/Shine/Standardize/

Sustain)

l

g

Account Management

Value Selling

Channel

y y ppsource raw material requirements effectively

Reduce raw material price volatility

O d l d li i

y gglobal cash management system

Strong credit approval process

Line Balancing

Visual Management

Value Stream Mapping

Channel Management

Performance Management

Orderly deliveries

Aggressively pursue direct and indirect cost savings

Automated tools to manage and monitor cash requirements

GBS diagnostics have identified approximately $100 million of additional cost savings.

7

Strategy Statement• Continue to strengthen the core

> Industry consolidationE i k t> Emerging markets

> Product line extensions

O G f S• Optimize and embed the Greif Business System throughout theenterprise to achieve top quartile profitability and lowest costproducer status while enhancing safety and quality.

• Pursue adjacencies.

• Emphasize sustainability in all of the company’s activities to meet• Emphasize sustainability in all of the company s activities to meetor exceed our stewardship responsibilities as a global citizen, andcreate long-term competitive and shareholder advantages.

8

• Fix, sell or close underperforming assets.

2010 Goals

• Deliver operating profit comparable to record levels of 2008 and top-quartile returns

• Permanent cost reduction / margin improvement of at least $120 million

• Optimize and leverage GBS – catalyst for performance improvement and acquisition integration

• Disciplined execution of growth strategy and portfolio optimization

• Protect financial and operational flexibility

Focus Discipline Passion

9

p

Rigid Industrial Packaging(Dollars in billions)

Served marketsNet sales

Lubricants, Oilsand Additives

2005 2010(2) CAGR

$1.8 $2.3 6%

(Dollars in billions)

Agriculture

Pharmaceutical

Competitive advantagesOperating profit margin (1)

Pharmaceutical

Chemicals

(2)

Leading market position

Growing global footprint

C lli l iti

Competitive advantagesOperating profit margin

Compelling value proposition

Comprehensive product portfolio

Strong customer relationships (2)

10

(1) Calculated as operating profit before restructuring charges, restructuring-related inventory charges and acquisition-related costs divided by net sales. See GAAP to Non-GAAP reconciliation included in the Appendix of this presentation.

(2) Represents the twelve months ended January 31, 2010.

Most Comprehensive Rigid Industrial Products and Services Portfolioand Services Portfolio

Plastic FibreSteelIntermediate Bulk

Containers ClosuresGlobal

PresenceFilling &Blending

#1 #1#2 #4 #1#1 #1#2 #4 #1

Mauser

Schutz

Greif’s global market share exceeds 30%11

Flexible Industrial Products

• Fle ible ind strial prod cts incl de the pol o en• Flexible industrial products include the polywovenindustry, which is a $2 billion global market whoseproducts are distributed regionally.

1 loop bag

• Storsack, acquired in February 2010, is the leaderin the polywoven industry with approximately a10% share.10% share.

• Principal end markets for polywoven productsinclude chemical, construction, food, feed, seed and

2 loop bag

pharmaceutical. 4 loop bags

12

Greif’s Advantaged Position in Flexible Industrial Products

• World-class global sourcing platform.g g p

• Industry leader with identified acquisitionopportunities and a record of successful businessopportunities and a record of successful businessintegration.

P b fit f G if B i S t t l k l• Proven benefits of Greif Business System to unlock value.

• Substantial percentage of customers who use bothflexible and rigid industrial products.

13

Paper Packaging(Dollars in millions)

Served marketsNet sales

2005 2010(2) CAGR

$608 $514 (4)%

(Dollars in millions)

• Automotive• Automotive• Building Products• Food• Packaging

Competitive advantagesOperating profit margin (1)

(2)

Customer focus

Integrated containerboard network

p gp g p g

Integrated containerboard network

Highly efficient sheet feeder footprint(2)

14

(1) Calculated as operating profit before restructuring charges divided by net sales. See GAAP to Non-GAAP reconciliation included in the Appendix of thispresentation.

(2) Represents the twelve months ended January 31, 2010.

Land Management

Core Timberlands 229,350 0 229,350

United States Canada Total

Special Use Land 34,900 25,050 59,950

Total Acres 264,250 25,050 289,300

L d M t i l ti h ti l d ti f U S ti b ti• Land Management involves active harvesting, sale and regeneration of U.S. timber properties,Special Use (Higher and Better Use, surplus and development land) sales, timberland management, wildlife stewardship, recreation and development.

• Undervalued timber portfolio with book value of $208 million at January 31, 2010.p $ y ,

• Over $225 million of timber properties have been monetized since 2001.

• Timber properties are located in Alabama, Louisiana and Mississippi in the United States and the Provinces of Quebec and Ontario in Canada

15

the Provinces of Quebec and Ontario in Canada.

Financial ReviewFinancial Review

Financial Profile(Dollars in millions)

2005 2006 2007 2008 2009 2010(3)

CAGR

(Dollars in millions)

Net Sales $2,424 $2,628 $3,322 $3,777 $2,792 $2,836 4%

(1)Operating Profit

(1)$ 165 $ 242 $ 312 $ 425 $ 277 $ 304 15%

RONA(1) (2)

15.4% 21.9% 21.3% 25.5% 15.7% 16.8%

(1) B f t t i h t t i l t d h i iti l t d t d ti b l d di l t

( )Before restructuring charges, restructuring-related charges, acquisition-related costs and timberland disposals net. See GAAP to Non-GAAP reconciliation included in the Appendix of this presentation.

(2) An explanation of the calculation of RONA is included in the Appendix of this presentation.

(3) Represents the twelve-months ended January 31, 2010.

17

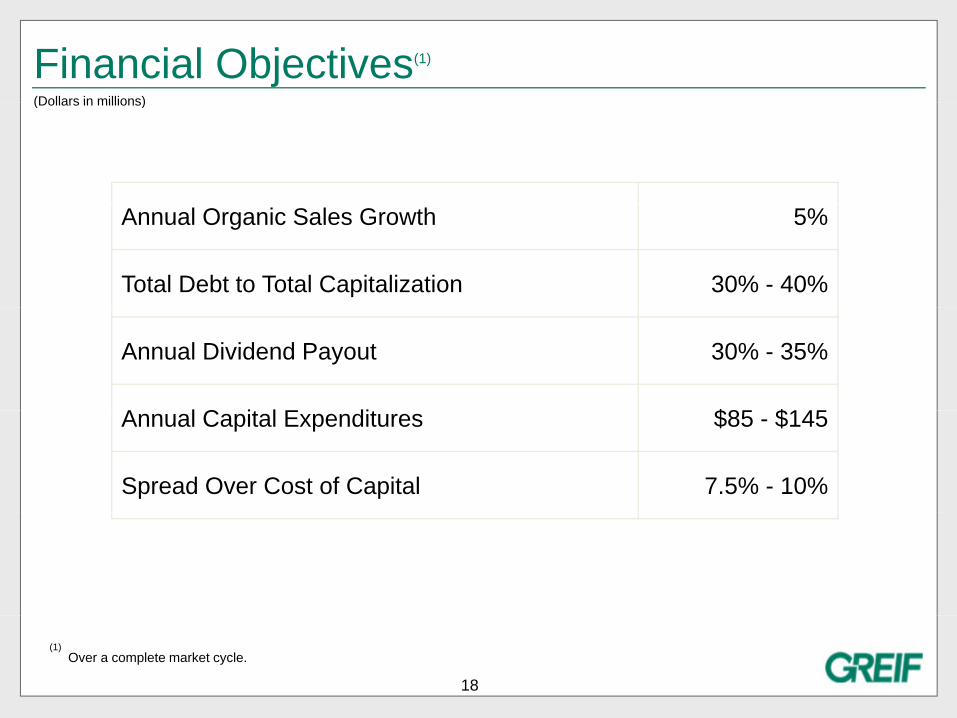

Financial Objectives(1)

(Dollars in millions)(Dollars in millions)

Annual Organic Sales Growth 5%

Total Debt to Total Capitalization 30% - 40%

Annual Dividend Payout 30% - 35%

A l C it l E dit $85 $145Annual Capital Expenditures $85 - $145

Spread Over Cost of Capital 7.5% - 10%

18

(1) Over a complete market cycle.

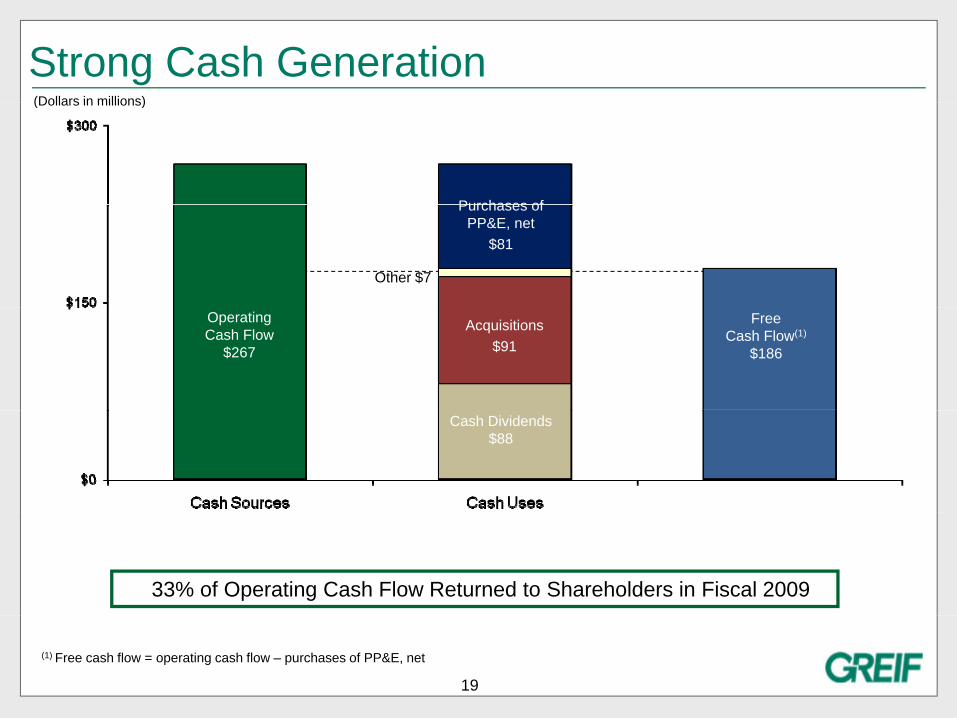

Strong Cash Generation(Dollars in millions)

Purchases of

(Dollars in millions)

Purchases of PP&E, net

$81

Other $7

Operating Cash Flow

$267

Acquisitions$91

Free Cash Flow(1)

$186

Cash Dividends$88

33% of Operating Cash Flow Returned to Shareholders in Fiscal 2009

19

(1) Free cash flow = operating cash flow – purchases of PP&E, net

Cash Dividends(Dollars per Class A Common Share)(Dollars per Class A Common Share)

2000-2009: 22%CAGR

• More than 75 consecutive years of cash dividends paid

• 30%-35% payout target over complete business cycle

• 3.1% current yield (1)

20

(1) Based on cash dividends paid during last 12 months (February 1, 2010).

Re-earning the Right to Premium Valuation• GBS – a catalyst enabling strong relative performance and value

creation during cyclical trough

• Diversity – a compelling competitive advantage

• Strong balance sheet and access to alternate sources of liquidity

• Balanced focus on defense (contingency planning/enterprise risk management) and offense

• Solid, experienced and performance-driven management team with record of accomplishment

Diversity > Strength > Performance

21

AppendixAppendix

GAAP to Non-GAAP ReconciliationR t N t A tReturn on Net Assets

UNAUDITED(Dollars in millions) 2005 2006 2007 2008 2009 2010

GAAP operating profit 185.8$ 250.2$ 289.8$ 382.3$ 199.9$ 239.1$

(2)

p g pRestructuring charges 35.8 33.2 21.2 43.2 66.6 45.4Restructuring-related inventory charges - - - - 10.8 9.0Acquisition-related costs - - - - - 10.1Timberland disposals, net (56.3) (41.3) 0.7 (0.4) - -

Non-GAAP - operating profit before restructuring charges, restructuring-related inventory charges, acquisition-related costs and timberland disposals, net 165.3$ 242.1$ 311.7$ 425.1$ 277.3$ 303.6$

Average cash (1) (67.9)$ (148.9)$ (120.4)$ (101.0)$ (79.5)$ (81.9)$ Average short-term borrowings (1) 17.9 24.6 34.9 48.4 56.8 56.3 Average current portion of long-term debt (1) - - - - 3.5 7.5 Average long-term debt (1) 446.8 449.7 645.1 687.0 748.5 789.7 Average shareholders' equity (1) 677.9 779.6 904.0 1,030.4 1,034.9 1,036.8Average net assets 1,074.7$ 1,105.0$ 1,463.6$ 1,664.8$ 1,764.2$ 1,808.4$

GAAP return on net assets (GAAP operating profit divided by average net assets) 17.3% 22.6% 19.8% 23.0% 11.3% 13.2%

Non-GAAP return on net assets (non-

(1) Amounts used in the calculation for this graph are based upon the average balances as of the beginning of the

(GAAP operating profit before restructuring charges, restructuring-related inventory charges, acquisition-related costs and timberland disposals, net divided by average net assets) 15.4% 21.9% 21.3% 25.5% 15.7% 16.8%

23

g p p g g gfiscal year and end of each fiscal quarter for the years presented.

(2) Represents the twelve months ended January 31, 2010.

GAAP to Non-GAAP ReconciliationO ti P fit M i b S tOperating Profit Margin by Segment

UNAUDITED(Dollars in millions) 2005 2006 2007 2008 2009 2010

Industrial Packaging

Net Sales 1 804 2$ 1 993 1$ 2 662 9$ 3 074 8$ 2 266 9$ 2 302 2$

(1)

Net Sales 1,804.2$ 1,993.1$ 2,662.9$ 3,074.8$ 2,266.9$ 2,302.2$

GAAP - operating profit 89.0$ 143.4$ 213.0$ 292.0$ 134.4$ 184.1$ Restructuring charges 31.4 24.0 16.0 34.0 65.7 46.5 Restructuring - related inventory charges - - - - 10.8 9.0 Acquisition-related costs - - - - - 10.1

Non-GAAP - operating profit before restructuring charges, restructuring-relatedrestructuring charges, restructuring related inventory charges and acquisition-related costs 120.4$ 167.4$ 229.0$ 326.0$ 210.9$ 249.7$

GAAP- operating profit margin 4.9% 7.2% 8.0% 9.5% 5.9% 8.0%Non-GAAP operating profit margin 6.7% 8.4% 8.6% 10.6% 9.3% 10.8%

Paper Packagingp g gNet Sales 607.8$ 620.3$ 653.7$ 696.9$ 504.7$ 513.8$

GAAP - operating profit 32.6$ 55.0$ 63.1$ 69.6$ 43.4$ 32.8$ Restructuring charges 4.3 9.2 5.2 9.1 0.7 (1.2)

Non-GAAP - operating profit before restructuring charges 36.9$ 64.2$ 68.3$ 78.7$ 44.1$ 31.6$

GAAP- operating profit margin 5.4% 8.9% 9.7% 10.0% 8.6% 6.4%Non-GAAP-operating profit margin 6.1% 10.3% 10.4% 11.3% 8.7% 6.2%

Land Management

GAAP - Operating profit 64.2$ 51.9$ 13.7$ 20.9$ 22.1$ 22.1$ Restructuring charges 0.1 - - 0.1 0.2 - Timberland disposals, net (56.3) (41.3) 0.7 (0.4) - -

24

Non-GAAP - operating profit before restructuring charges and timberland disposals, net 8.0$ 10.6$ 14.4$ 20.6$ 22.3$ 22.1$

(1) Represents the twelve months ended January 31, 2010.