Embed Size (px)

Citation preview

I P C I

F S

CONTENTS Independent Auditors’ Report ........................................................................ 1-2 Statement of Financial Position ......................................................................... 3 Statement of Activities ................................................................................... 4 Statement of Functional Expenses ...................................................................... 5 Statement of Cash Flows ................................................................................. 6 Notes to the Financial Statements .................................................................. 7-15

1

INDEPENDENT AUDITORS’ REPORT To the Session of Irvine Presbyterian Church Incorporated Irvine, California Auditors’ Report on the Statement of Financial Position We have audited the accompanying statement of financial position of Irvine Presbyterian Church Incorporated (the Organization) as of December 31, 2018, and the related notes to this financial statement. Management’s Responsibility for the Financial Statement Management is responsible for the preparation and fair presentation of this financial statement in accordance with accounting principles generally accepted in the United States of America; this includes the design, implementation, and maintenance of internal control relevant to the preparation and fair presentation of the financial statement that is free from material misstatement, whether due to fraud or error. Auditors’ Responsibility Our responsibility is to express an opinion on this financial statement based on our audit. We conducted our audit in accordance with auditing standards generally accepted in the United States of America. Those standards require that we plan and perform the audit to obtain reasonable assurance about whether the financial statement is free from material misstatement. An audit involves performing procedures to obtain audit evidence about the amounts and disclosures in the financial statement. The procedures selected depend on the auditors’ judgment, including the assessment of the risks of material misstatement of the financial statement, whether due to fraud or error. In making those risk assessments, the auditors consider internal control relevant to the Organization’s preparation and fair presentation of the financial statement in order to design audit procedures that are appropriate in the circumstances, but not for the purpose of expressing an opinion on the effectiveness of the Organization’s internal control. Accordingly, we express no such opinion. An audit also includes evaluating the appropriateness of accounting policies used and the reasonableness of significant accounting estimates made by management, as well as evaluating the overall presentation of the financial statement. We believe that the audit evidence we have obtained is sufficient and appropriate to provide a basis for our audit opinion of the statement of activities. Opinion on the Statement of Financial Position In our opinion, the statement of financial position referred to in the first paragraph presents fairly, in all material respects, the financial position of the Organization as of December 31, 2018, in accordance with accounting principles generally accepted in the United States of America.

Long Beach | Irvine | Los Angeles

www.windes.com 844.4WINDES

2

Review Report on Statements of Activities, Functional Expenses, and Cash Flows We have reviewed the accompanying statements of activities, functional expenses, and cash flows, and the related notes to the financial statements, of Irvine Presbyterian Church Incorporated (the Organization) for the year ended December 31, 2018. A review includes primarily applying analytical procedures to management’s financial data and making inquiries of company management. A review is substantially less in scope than an audit, the objective of which is the expression of an opinion regarding the financial statements as a whole. Accordingly, we do not express such an opinion. Management’s Responsibility for the Financial Statements Management is responsible for the preparation and fair presentation of these financial statements in accordance with accounting principles generally accepted in the United States of America; this includes the design, implementation, and maintenance of internal control relevant to the preparation and fair presentation of financial statements that are free from material misstatement, whether due to fraud or error. Accountants’ Responsibility Additionally, our responsibility is to conduct the review engagement in accordance with Statements on Standards for Accounting and Review Services promulgated by the Accounting and Review Services Committee of the AICPA. Those standards require us to perform procedures to obtain limited assurance as a basis for reporting whether we are aware of any material modifications that should be made to the financial statements for them to be in accordance with accounting principles generally accepted in the United States of America. We believe that the results of our procedures provide a reasonable basis for our conclusion. Accountants’ Conclusion Based on our review, we are not aware of any material modifications that should be made to the accompanying statements of activities, functional expenses, and cash flows in order to be in accordance with accounting principles generally accepted in the United States of America. Emphasis of Matter As discussed in Note 2, during the year ended December 31, 2018, the Organization adopted Accounting Standards Update (ASU) No. 2016-14, Not-for-Profit Entities (Topic 958): Presentation of Financial Statements of Not-for-Profit Entities. Our opinion and conclusion are not modified with respect to this matter. Long Beach, California September 10, 2019

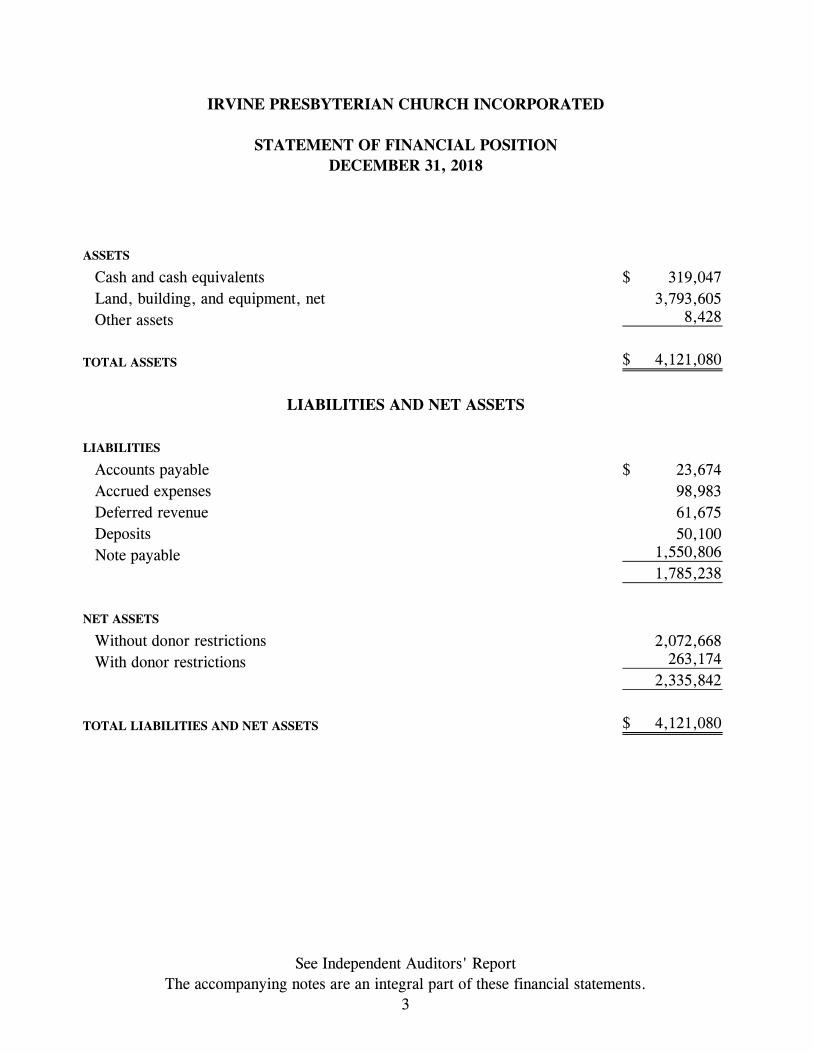

IRVINE PRESBYTERIAN CHURCH INCORPORATED

STATEMENT OF FINANCIAL POSITIONDECEMBER 31, 2018

See Independent Auditors' ReportThe accompanying notes are an integral part of these financial statements.

3

ASSETS

Cash and cash equivalents 319,047$ Land, building, and equipment, net 3,793,605 Other assets 8,428

TOTAL ASSETS 4,121,080$

LIABILITIES

Accounts payable 23,674$ Accrued expenses 98,983 Deferred revenue 61,675 Deposits 50,100 Note payable 1,550,806

1,785,238

NET ASSETS

Without donor restrictions 2,072,668 With donor restrictions 263,174

2,335,842

TOTAL LIABILITIES AND NET ASSETS 4,121,080$

LIABILITIES AND NET ASSETS

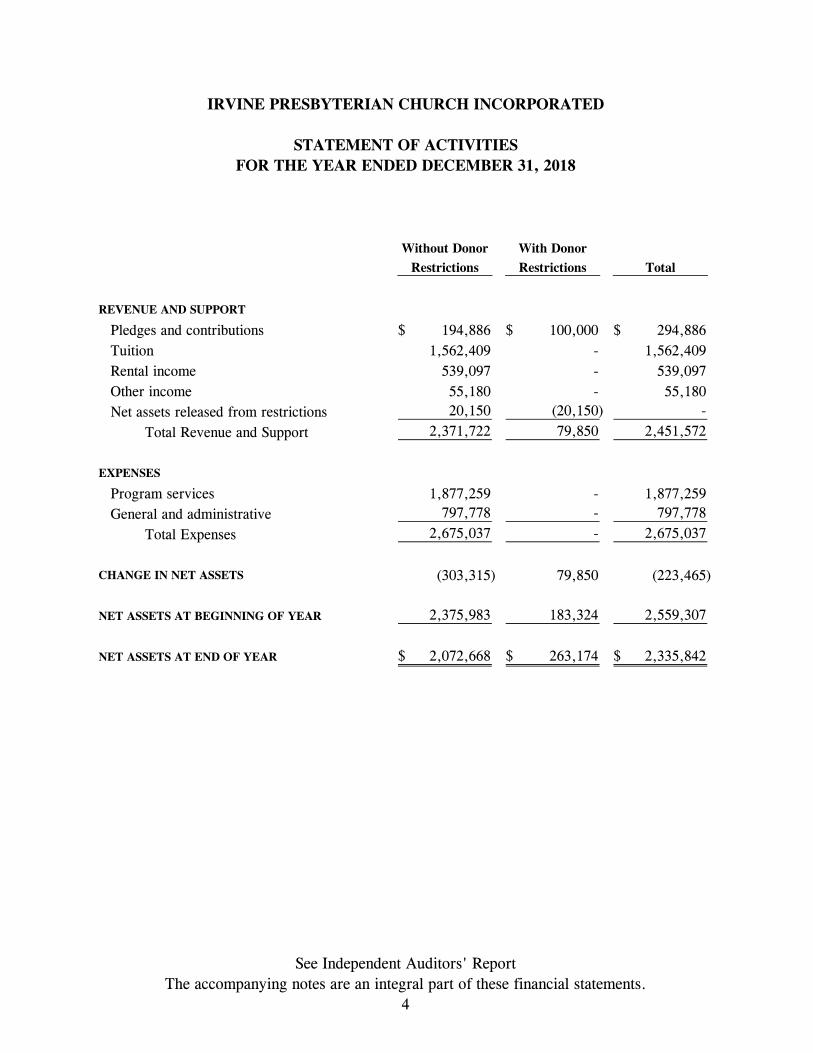

IRVINE PRESBYTERIAN CHURCH INCORPORATED

STATEMENT OF ACTIVITIESFOR THE YEAR ENDED DECEMBER 31, 2018

See Independent Auditors' ReportThe accompanying notes are an integral part of these financial statements.

4

Without Donor With DonorRestrictions Restrictions Total

REVENUE AND SUPPORT

Pledges and contributions 194,886$ 100,000$ 294,886$ Tuition 1,562,409 - 1,562,409 Rental income 539,097 - 539,097 Other income 55,180 - 55,180 Net assets released from restrictions 20,150 (20,150) -

Total Revenue and Support 2,371,722 79,850 2,451,572

EXPENSES

Program services 1,877,259 - 1,877,259 General and administrative 797,778 - 797,778

Total Expenses 2,675,037 - 2,675,037

CHANGE IN NET ASSETS (303,315) 79,850 (223,465)

NET ASSETS AT BEGINNING OF YEAR 2,375,983 183,324 2,559,307

NET ASSETS AT END OF YEAR 2,072,668$ 263,174$ 2,335,842$

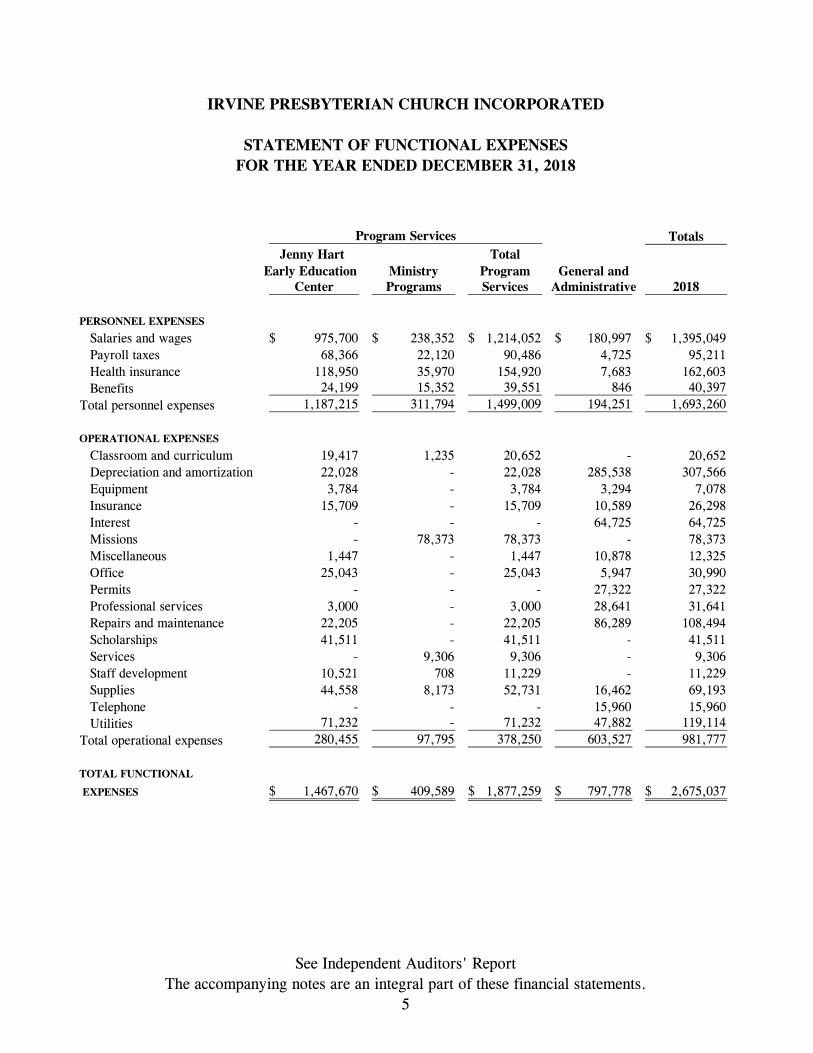

IRVINE PRESBYTERIAN CHURCH INCORPORATED

STATEMENT OF FUNCTIONAL EXPENSESFOR THE YEAR ENDED DECEMBER 31, 2018

See Independent Auditors' ReportThe accompanying notes are an integral part of these financial statements.

5

TotalsJenny Hart Total

Early Education Ministry Program General andCenter Programs Services Administrative 2018

PERSONNEL EXPENSES

Salaries and wages 975,700$ 238,352$ 1,214,052$ 180,997$ 1,395,049$ Payroll taxes 68,366 22,120 90,486 4,725 95,211 Health insurance 118,950 35,970 154,920 7,683 162,603 Benefits 24,199 15,352 39,551 846 40,397

Total personnel expenses 1,187,215 311,794 1,499,009 194,251 1,693,260

OPERATIONAL EXPENSES

Classroom and curriculum 19,417 1,235 20,652 - 20,652 Depreciation and amortization 22,028 - 22,028 285,538 307,566 Equipment 3,784 - 3,784 3,294 7,078 Insurance 15,709 - 15,709 10,589 26,298 Interest - - - 64,725 64,725 Missions - 78,373 78,373 - 78,373 Miscellaneous 1,447 - 1,447 10,878 12,325 Office 25,043 - 25,043 5,947 30,990 Permits - - - 27,322 27,322 Professional services 3,000 - 3,000 28,641 31,641 Repairs and maintenance 22,205 - 22,205 86,289 108,494 Scholarships 41,511 - 41,511 - 41,511 Services - 9,306 9,306 - 9,306 Staff development 10,521 708 11,229 - 11,229 Supplies 44,558 8,173 52,731 16,462 69,193 Telephone - - - 15,960 15,960 Utilities 71,232 - 71,232 47,882 119,114

Total operational expenses 280,455 97,795 378,250 603,527 981,777

TOTAL FUNCTIONAL

EXPENSES 1,467,670$ 409,589$ 1,877,259$ 797,778$ 2,675,037$

Program Services

IRVINE PRESBYTERIAN CHURCH INCORPORATED

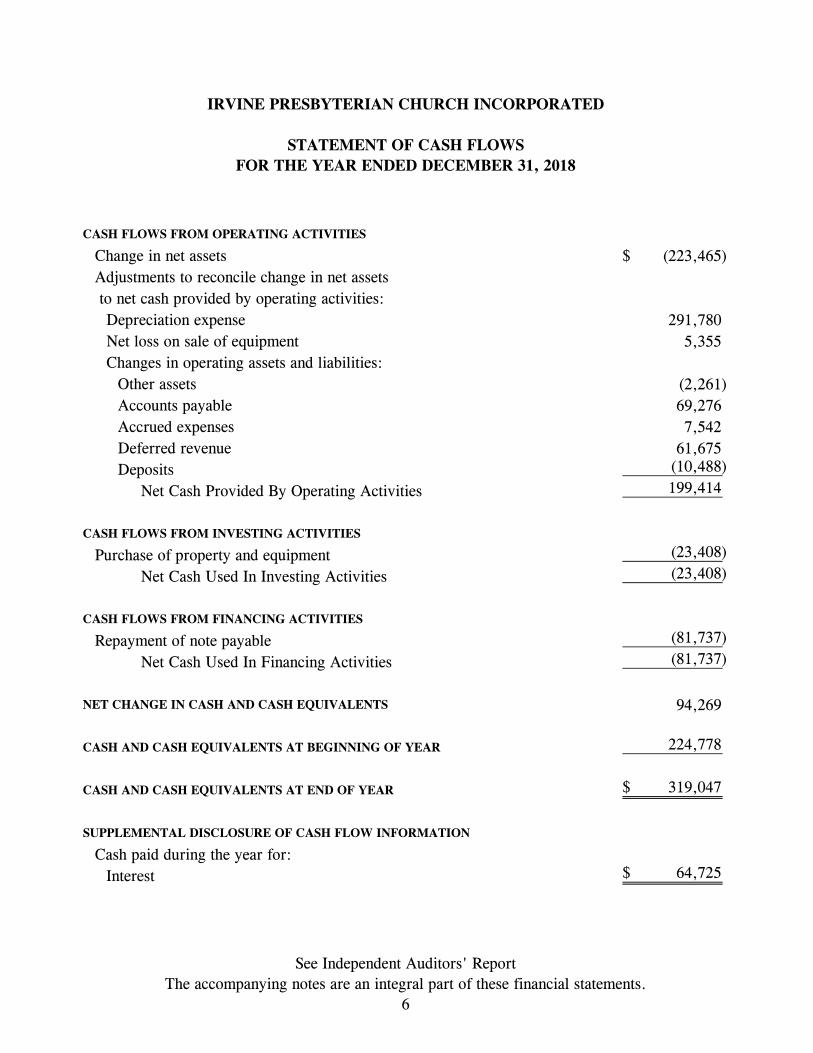

STATEMENT OF CASH FLOWSFOR THE YEAR ENDED DECEMBER 31, 2018

See Independent Auditors' ReportThe accompanying notes are an integral part of these financial statements.

6

CASH FLOWS FROM OPERATING ACTIVITIES

Change in net assets (223,465)$ Adjustments to reconcile change in net assets to net cash provided by operating activities:

Depreciation expense 291,780 Net loss on sale of equipment 5,355 Changes in operating assets and liabilities:

Other assets (2,261) Accounts payable 69,276 Accrued expenses 7,542 Deferred revenue 61,675 Deposits (10,488)

Net Cash Provided By Operating Activities 199,414

CASH FLOWS FROM INVESTING ACTIVITIES

Purchase of property and equipment (23,408)

Net Cash Used In Investing Activities (23,408)

CASH FLOWS FROM FINANCING ACTIVITIES

Repayment of note payable (81,737)

Net Cash Used In Financing Activities (81,737)

NET CHANGE IN CASH AND CASH EQUIVALENTS 94,269

CASH AND CASH EQUIVALENTS AT BEGINNING OF YEAR 224,778

CASH AND CASH EQUIVALENTS AT END OF YEAR 319,047$

SUPPLEMENTAL DISCLOSURE OF CASH FLOW INFORMATION

Cash paid during the year for:Interest 64,725$

IRVINE PRESBYTERIAN CHURCH INCORPORATED

NOTES TO THE FINANCIAL STATEMENTS DECEMBER 31, 2018

7

NOTE 1 – Nature of Organization Irvine Presbyterian Church Incorporated (the Church), an affiliate of the Presbyterian Church (USA) located in Irvine, California, is a non-profit corporation organized in California. The Church also operates a preschool and kindergarten under the name Jenny Hart Early Education Center (the JHEEC). NOTE 2 – Summary of Significant Accounting Policies Management Estimates Basis of Accounting The financial statements of the Church have been prepared on the accrual basis in accordance with accounting principles generally accepted in the United States of America. The following significant accounting policies are described below to enhance the usefulness of the financial statements to the reader. Use of Estimates and Assumptions Management uses estimates and assumptions in preparing financial statements in accordance with accounting principles generally accepted in the United States of America. Those estimates and assumptions affect the reported amounts of assets and liabilities, the disclosure of contingent assets and liabilities, and the reported revenues and expenses. Actual results could vary from the estimates that were assumed in preparing the financial statements. Recently Adopted Accounting Standards In 2018, the Church adopted Accounting Standards Update (ASU) No. 2016-14, Not-for-Profit Entities (Topic 958): Presentation of Financial Statements of Not-for-Profit Entities. The main provisions include: presentation of two classes of net assets versus the previously required three; recognition of capital gifts for construction as a net asset without donor restrictions when the associated long-lived asset is placed in service; and recognition of underwater endowment funds as a reduction to net assets with donor restrictions. The guidance also enhances disclosures for board-designated amounts, components of net assets without donor restrictions, liquidity, and expenses by both their natural and functional classification. With the adoption of the standard, the Church updated net asset presentation in the financial statements and included additional disclosures as required.

IRVINE PRESBYTERIAN CHURCH INCORPORATED

NOTES TO THE FINANCIAL STATEMENTS DECEMBER 31, 2018

8

NOTE 2 – Summary of Significant Accounting Policies (Continued) Financial Statement Presentation The Church reports information regarding its financial position and activities according to two classes of net assets: with donor restrictions and without donor restrictions.

Without Donor Restrictions – Net assets that are not subject to donor-imposed restrictions. With Donor Restrictions – Net assets subject to donor-imposed stipulations that may be temporary in nature to be met by the actions of the Organization or the passage of time; or perpetual in nature, where the donor stipulates that the corpus be maintained in tact in perpetuity. As the restrictions are satisfied, net assets with donor restrictions are reclassified to net assets without donor restrictions and reported in the accompanying statement of activities as net assets released from restrictions.

Contributions All contributions are considered to be available for use without restriction unless specifically restricted by the donor. Contributions received that are designated for future periods or restricted by the donor for specific purposes are reported as net assets with donor restrictions. When a donor’s stipulated time restriction ends or purpose restriction is accomplished, restricted net assets are reclassified to net assets without restrictions and reported in the statement of activities as net assets released from restrictions. Contributions, including endowment gifts and pledges, are recognized as support in the period received or pledged. Unconditional promises to give that are expected to be collected within one year are recorded at their net realizable value. Unconditional promises to give that are expected to be collected in future years are recorded at the present value of their estimated future cash flows. Amortization of the discounts is included in contribution revenue. Conditional promises to give are not included as support until the conditions are substantially met. Contributions are included in donations and collections in the accompanying statement of activities.

IRVINE PRESBYTERIAN CHURCH INCORPORATED

NOTES TO THE FINANCIAL STATEMENTS DECEMBER 31, 2018

9

NOTE 2 – Summary of Significant Accounting Policies (Continued) Contributed Services A substantial number of volunteers make significant contributions of their time in the furtherance of the Church’s purpose. The value of this contributed time is not reflected in the accompanying financial statements, as it does not meet the recognition criteria under generally accepted accounting principles for contributed services. Cash and Cash Equivalents Cash consists of cash on hand, in banks, and in money market accounts. The Church considers all highly liquid investments with maturities of 90 days or less to be cash equivalents. The Church maintains its cash accounts at various financial institutions. Deposits of up to $250,000 at FDIC-insured institutions are covered by FDIC insurance. At times, deposits may be in excess of the FDIC insurance limit; however, management does not believe the Church is exposed to any significant related credit risk. Property and Equipment Property and equipment are stated at cost, with the exception of donated equipment, which is recorded at fair market value on the date received. Depreciation has been provided using the straight-line method over the estimated useful lives of the assets, which range from three to ten years. Building improvements are amortized over the remaining term of the building lease where the improvements are made. Expenditures for repairs and maintenance are expensed as incurred. Amortization of equipment under the capital lease is computed based on the shorter of the lease terms or the life of the asset and is included in depreciation expense. Allocation of Expenses Expenses that can be identified with a specific program or supporting service are charged directly to the program or supporting service. Expenses which apply to more than one functional category have been allocated based on estimates made by management based on time and effort.

IRVINE PRESBYTERIAN CHURCH INCORPORATED

NOTES TO THE FINANCIAL STATEMENTS DECEMBER 31, 2018

10

NOTE 2 – Summary of Significant Accounting Policies (Continued) Impairment of Long-Lived Assets The Church's long-lived assets include land, building, and equipment. Long-lived assets are reviewed for impairment whenever events or changes in circumstances indicate that the carrying amount may not be recoverable. If the expected future cash flow from the use of the asset and its eventual disposition is less than the carrying amount of the asset, an impairment loss is recognized and measured using the fair value of the related asset. As of December 31, 2018, management did not identify any material impairment of the Church's long-lived assets. Recently Issued Accounting Standards In May 2014, the FASB issued ASU 2014-09, Revenue from Contracts with Customers (Topic 606) (ASU 2014-09), requiring an entity to recognize the amount of revenue to which it expects to be entitled for the transfer of promised goods or services to customers. The updated standard will replace most existing revenue recognition guidance in U.S. GAAP when it becomes effective and permits the use of either a full retrospective or retrospective with cumulative-effect-transition method. In August 2015, the FASB issued ASU 2015-14, which defers the effective date of ASU 2014-09 one year, making it effective for annual reporting periods beginning after December 15, 2018. The Church is currently evaluating the impact of the adoption of the new standard. In February 2016, the FASB issued ASU 2016-02, Leases (Topic 842) (ASU 2016-02). The guidance in this ASU supersedes the leasing guidance in Leases (Topic 840). Under the new guidance, lessees are required to recognize lease assets and lease liabilities on the balance sheet for all leases with terms longer than 12 months. Leases will be classified as either finance or operating, with classification affecting the pattern of expense recognition in the income statement. The new standard is effective for fiscal years beginning after December 15, 2019, including interim periods within those fiscal years. The Church is currently evaluating the impact of the adoption of the new standard. In June 2018, the FASB issues ASU 2018-08, Not-for-Profit Entities (Topic 958): Clarifying the Scope and the Accounting Guidance for Contributions Received and Contributions Made (ASU 2018-08), which provides additional guidance on characterizing grants and similar contracts with resource providers as either exchange transactions or contributions, as well as distinguishing between conditional and unconditional contributions. The updated standard will be effective for annual reporting periods beginning after December 15, 2018. The Church is currently evaluating the impact of the adoption of the new standard.

IRVINE PRESBYTERIAN CHURCH INCORPORATED

NOTES TO THE FINANCIAL STATEMENTS DECEMBER 31, 2018

11

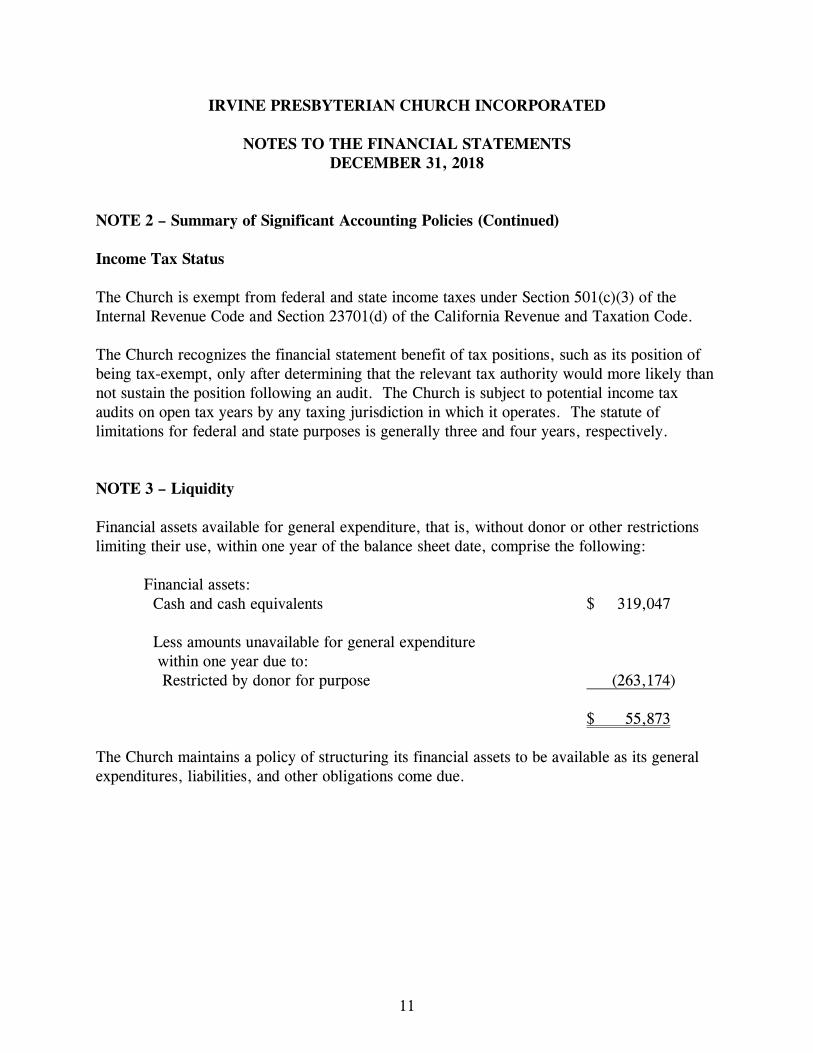

NOTE 2 – Summary of Significant Accounting Policies (Continued) Income Tax Status The Church is exempt from federal and state income taxes under Section 501(c)(3) of the Internal Revenue Code and Section 23701(d) of the California Revenue and Taxation Code. The Church recognizes the financial statement benefit of tax positions, such as its position of being tax-exempt, only after determining that the relevant tax authority would more likely than not sustain the position following an audit. The Church is subject to potential income tax audits on open tax years by any taxing jurisdiction in which it operates. The statute of limitations for federal and state purposes is generally three and four years, respectively. NOTE 3 – Liquidity Financial assets available for general expenditure, that is, without donor or other restrictions limiting their use, within one year of the balance sheet date, comprise the following: Financial assets: Cash and cash equivalents $ 319,047 Less amounts unavailable for general expenditure within one year due to: Restricted by donor for purpose (263,174) $ 55,873 The Church maintains a policy of structuring its financial assets to be available as its general expenditures, liabilities, and other obligations come due.

IRVINE PRESBYTERIAN CHURCH INCORPORATED

NOTES TO THE FINANCIAL STATEMENTS DECEMBER 31, 2018

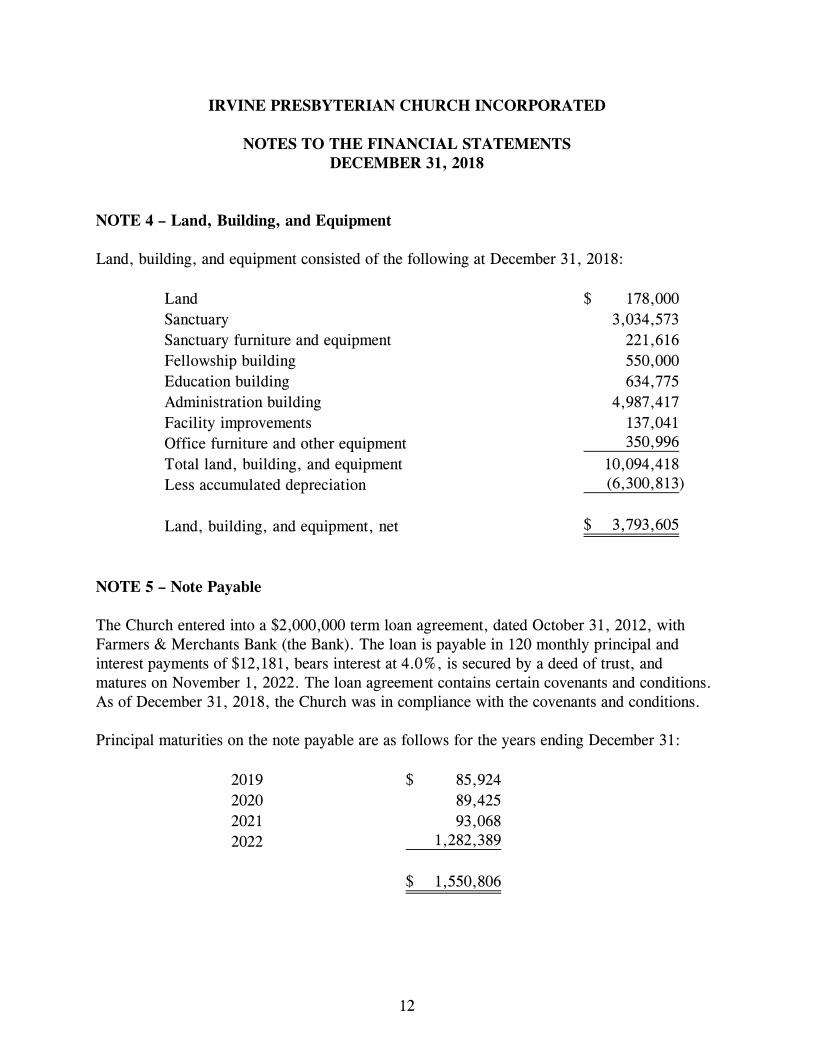

12

NOTE 4 – Land, Building, and Equipment Land, building, and equipment consisted of the following at December 31, 2018:

Land 178,000$ Sanctuary 3,034,573 Sanctuary furniture and equipment 221,616 Fellowship building 550,000 Education building 634,775 Administration building 4,987,417 Facility improvements 137,041 Office furniture and other equipment 350,996 Total land, building, and equipment 10,094,418 Less accumulated depreciation (6,300,813)

Land, building, and equipment, net 3,793,605$

NOTE 5 – Note Payable The Church entered into a $2,000,000 term loan agreement, dated October 31, 2012, with Farmers & Merchants Bank (the Bank). The loan is payable in 120 monthly principal and interest payments of $12,181, bears interest at 4.0%, is secured by a deed of trust, and matures on November 1, 2022. The loan agreement contains certain covenants and conditions. As of December 31, 2018, the Church was in compliance with the covenants and conditions. Principal maturities on the note payable are as follows for the years ending December 31:

2019 85,924$ 2020 89,425 2021 93,068 2022 1,282,389

1,550,806$

IRVINE PRESBYTERIAN CHURCH INCORPORATED

NOTES TO THE FINANCIAL STATEMENTS DECEMBER 31, 2018

13

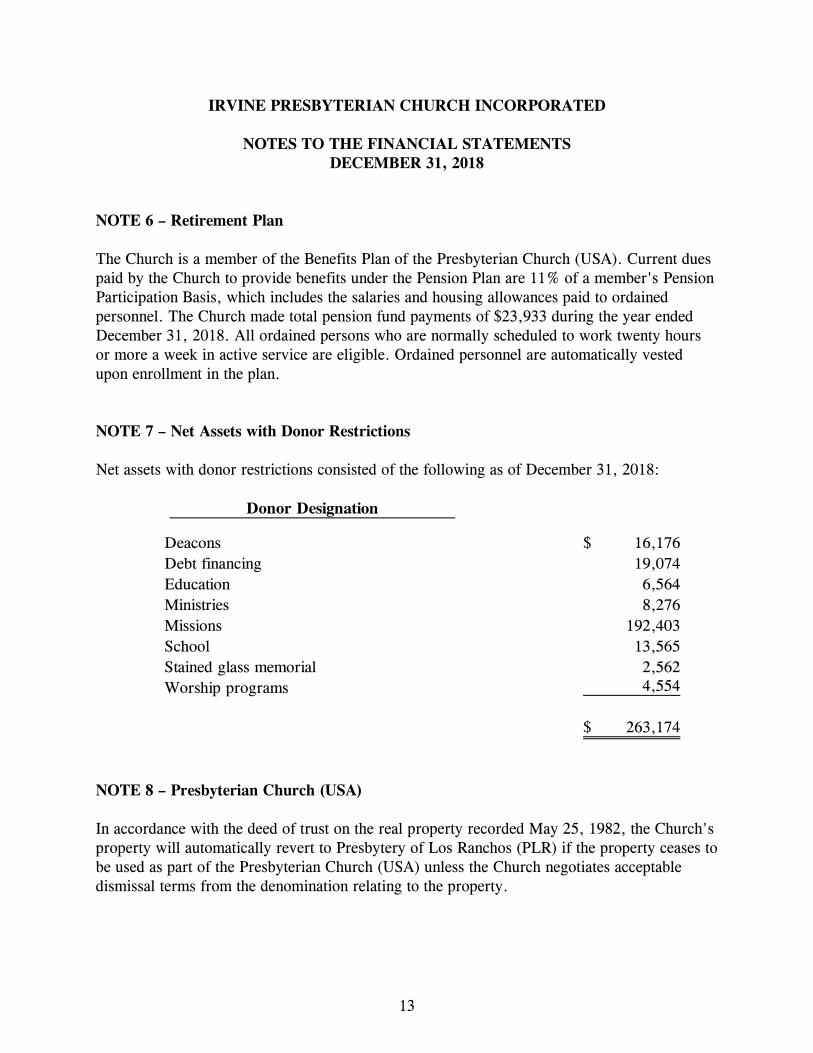

NOTE 6 – Retirement Plan The Church is a member of the Benefits Plan of the Presbyterian Church (USA). Current dues paid by the Church to provide benefits under the Pension Plan are 11% of a member's Pension Participation Basis, which includes the salaries and housing allowances paid to ordained personnel. The Church made total pension fund payments of $23,933 during the year ended December 31, 2018. All ordained persons who are normally scheduled to work twenty hours or more a week in active service are eligible. Ordained personnel are automatically vested upon enrollment in the plan. NOTE 7 – Net Assets with Donor Restrictions Net assets with donor restrictions consisted of the following as of December 31, 2018:

Donor Designation

Deacons 16,176$ Debt financing 19,074 Education 6,564 Ministries 8,276 Missions 192,403 School 13,565 Stained glass memorial 2,562 Worship programs 4,554

263,174$

NOTE 8 – Presbyterian Church (USA) In accordance with the deed of trust on the real property recorded May 25, 1982, the Church's property will automatically revert to Presbytery of Los Ranchos (PLR) if the property ceases to be used as part of the Presbyterian Church (USA) unless the Church negotiates acceptable dismissal terms from the denomination relating to the property.

IRVINE PRESBYTERIAN CHURCH INCORPORATED

NOTES TO THE FINANCIAL STATEMENTS DECEMBER 31, 2018

14

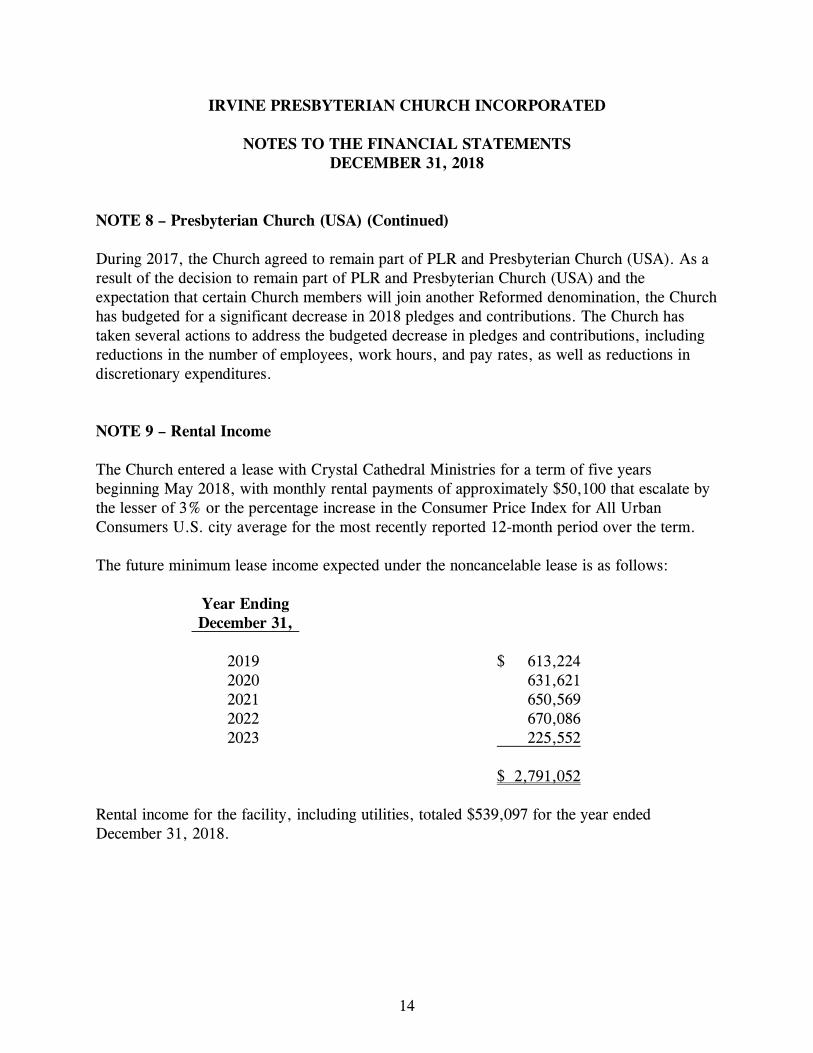

NOTE 8 – Presbyterian Church (USA) (Continued) During 2017, the Church agreed to remain part of PLR and Presbyterian Church (USA). As a result of the decision to remain part of PLR and Presbyterian Church (USA) and the expectation that certain Church members will join another Reformed denomination, the Church has budgeted for a significant decrease in 2018 pledges and contributions. The Church has taken several actions to address the budgeted decrease in pledges and contributions, including reductions in the number of employees, work hours, and pay rates, as well as reductions in discretionary expenditures. NOTE 9 – Rental Income The Church entered a lease with Crystal Cathedral Ministries for a term of five years beginning May 2018, with monthly rental payments of approximately $50,100 that escalate by the lesser of 3% or the percentage increase in the Consumer Price Index for All Urban Consumers U.S. city average for the most recently reported 12-month period over the term. The future minimum lease income expected under the noncancelable lease is as follows: Year Ending December 31, 2019 $ 613,224 2020 631,621 2021 650,569 2022 670,086 2023 225,552 $ 2,791,052 Rental income for the facility, including utilities, totaled $539,097 for the year ended December 31, 2018.

IRVINE PRESBYTERIAN CHURCH INCORPORATED

NOTES TO THE FINANCIAL STATEMENTS DECEMBER 31, 2018

15

NOTE 10 – Subsequent Events Management has evaluated subsequent events through September 10, 2019, the date the financial statements were available to be issued. In February 2019, the Church entered into a merger agreement with The Crystal Cathedral DBA Shepherd’s Grove (TCC). Under the terms of the merger, the assets of TCC were combined with those of IPC, TCC would cease as a corporate entity, and IPC would be the surviving entity. The assets transferred in the merger included cash and equipment of approximately $800,000. The assets of Crystal Cathedral Ministries were not included in the merger. Crystal Cathedral Ministries was affiliated with TCC through control by a common board of directors until the merger with IPC became effective. Subsequent to the merger, Crystal Cathedral Ministries entered into an agreement with Irvine Presbyterian Church Incorporated to provide for reimbursement of certain shared services, rent and to license certain intellectual property. In March 2019, the Church obtained a loan of $585,000 with an interest rate of 5.25%, set to mature on November 1, 2022. The loan is secured by the property in Orange County, California. The loan is intended for refurbishment and improvement of the facility.