Embed Size (px)

Citation preview

Chair of Information Systems IV (ERIS)

Institute for Enterprise Systems (InES)

IS 604: Contemporary Issues in ES

Banking Enterprise Systems

Prof. Dr. Alexander Mädche

Chair of Information Systems IV

Institute for Enterprise Systems

Lecture

supported by:

Goals of this lecture 2

Provide some basic contextual

background on Enterprise Systems

Describe the motivational

background for studying and

teaching Banking Enterprise

Systems

Introduce fundamental concepts

needed to understand retail banking

business

IS 604 Banking Enterprise Systems

2

Agenda – Session I

Agenda

1 Enterprise System Fundamentals

2 Motivation: Enterprise Systems in the Financial Services Industry

3 The Financial Services Industry – Banks in the Market Environment

4 Products and Services of Retail Banks

5 Reference Processes in Banking

6 The Bank as Enterprise System

7 Business Scenario: the Global Retail Bank - GRB

IS 604 Banking Enterprise Systems

3

3

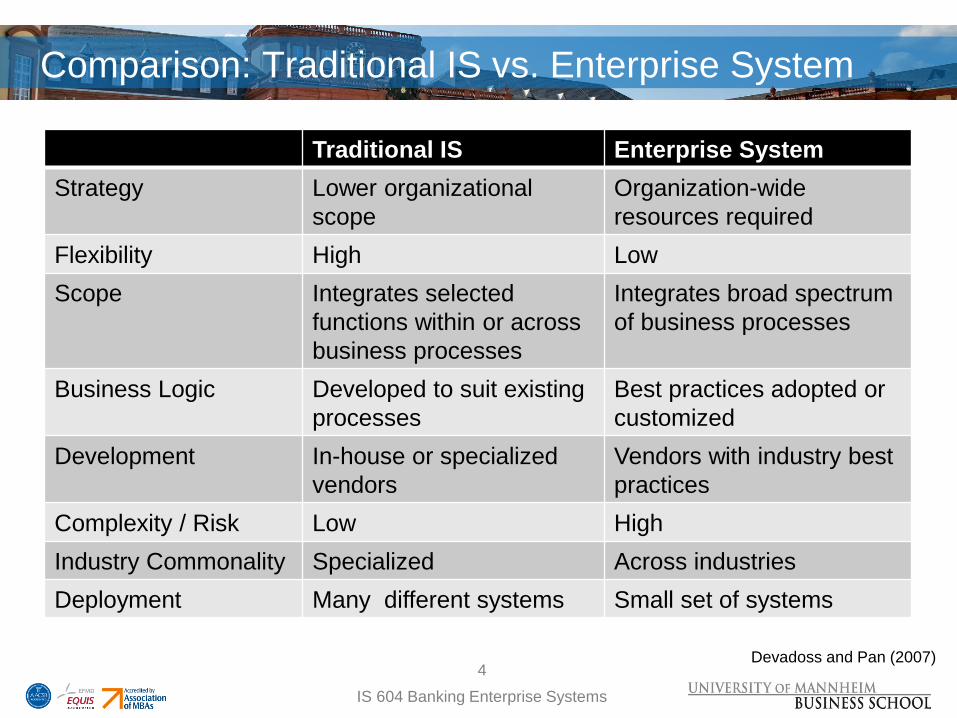

Comparison: Traditional IS vs. Enterprise System

Traditional IS Enterprise System

Strategy Lower organizational

scope

Organization-wide

resources required

Flexibility High Low

Scope Integrates selected

functions within or across

business processes

Integrates broad spectrum

of business processes

Business Logic Developed to suit existing

processes

Best practices adopted or

customized

Development In-house or specialized

vendors

Vendors with industry best

practices

Complexity / Risk Low High

Industry Commonality Specialized Across industries

Deployment Many different systems Small set of systems

Devadoss and Pan (2007)

IS 604 Banking Enterprise Systems

4

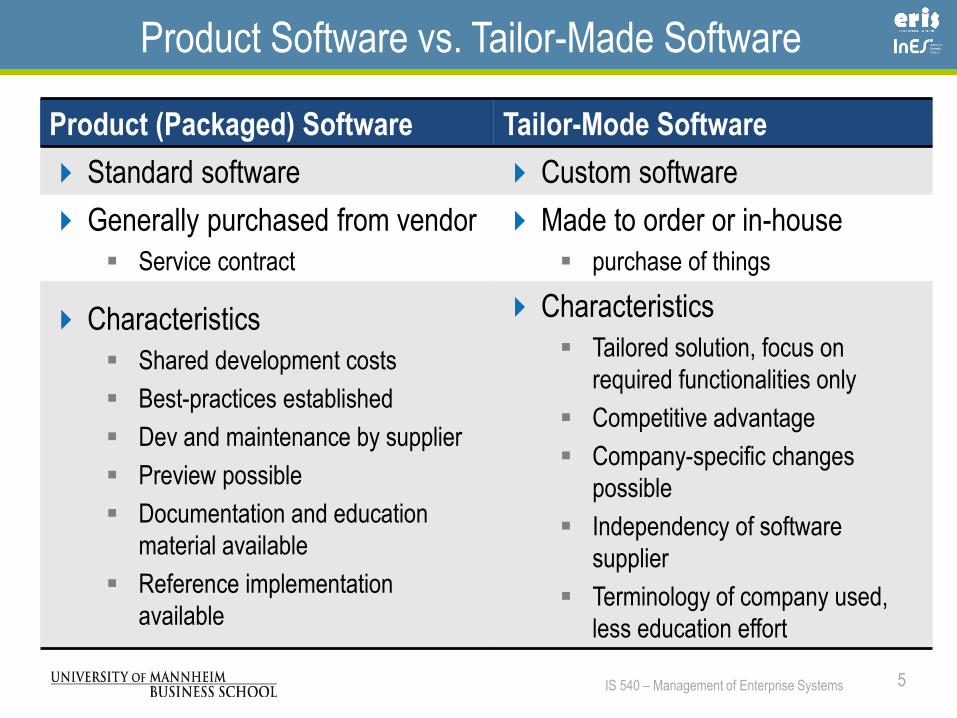

Product Software vs. Tailor-Made Software

Product (Packaged) Software Tailor-Mode Software

Standard software Custom software

Generally purchased from vendor

Service contract

Made to order or in-house

purchase of things

Characteristics

Shared development costs

Best-practices established

Dev and maintenance by supplier

Preview possible

Documentation and education

material available

Reference implementation

available

Characteristics

Tailored solution, focus on

required functionalities only

Competitive advantage

Company-specific changes

possible

Independency of software

supplier

Terminology of company used,

less education effort

5 5 IS 540 – Management of Enterprise Systems

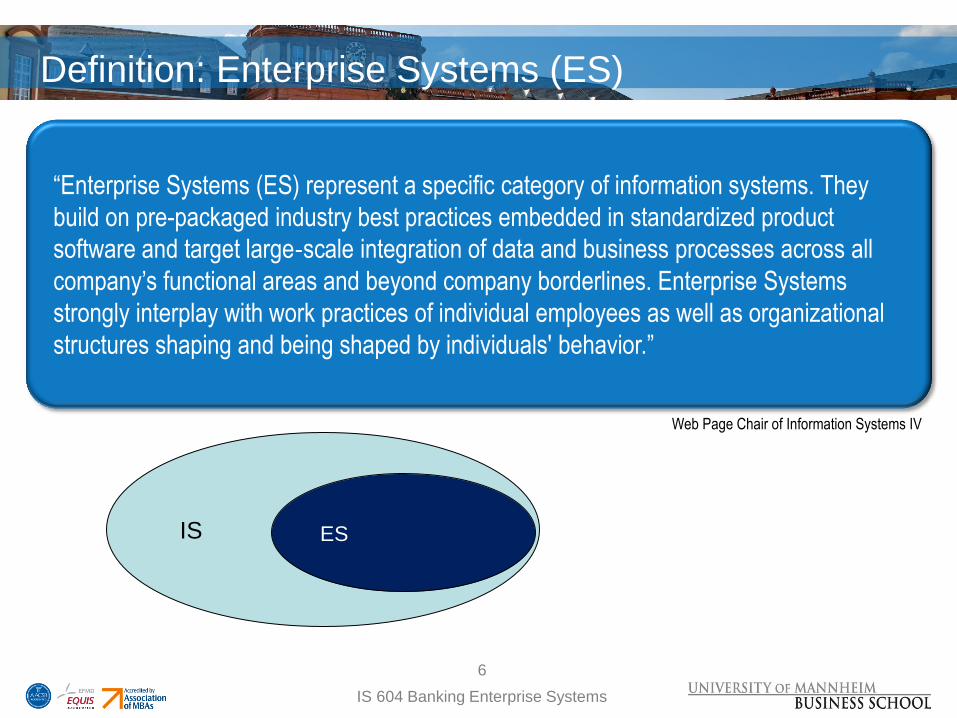

Definition: Enterprise Systems (ES)

“Enterprise Systems (ES) represent a specific category of information systems. They

build on pre-packaged industry best practices embedded in standardized product

software and target large‐scale integration of data and business processes across all

company’s functional areas and beyond company borderlines. Enterprise Systems

strongly interplay with work practices of individual employees as well as organizational

structures shaping and being shaped by individuals' behavior.”

IS ES

Web Page Chair of Information Systems IV

IS 604 Banking Enterprise Systems

6

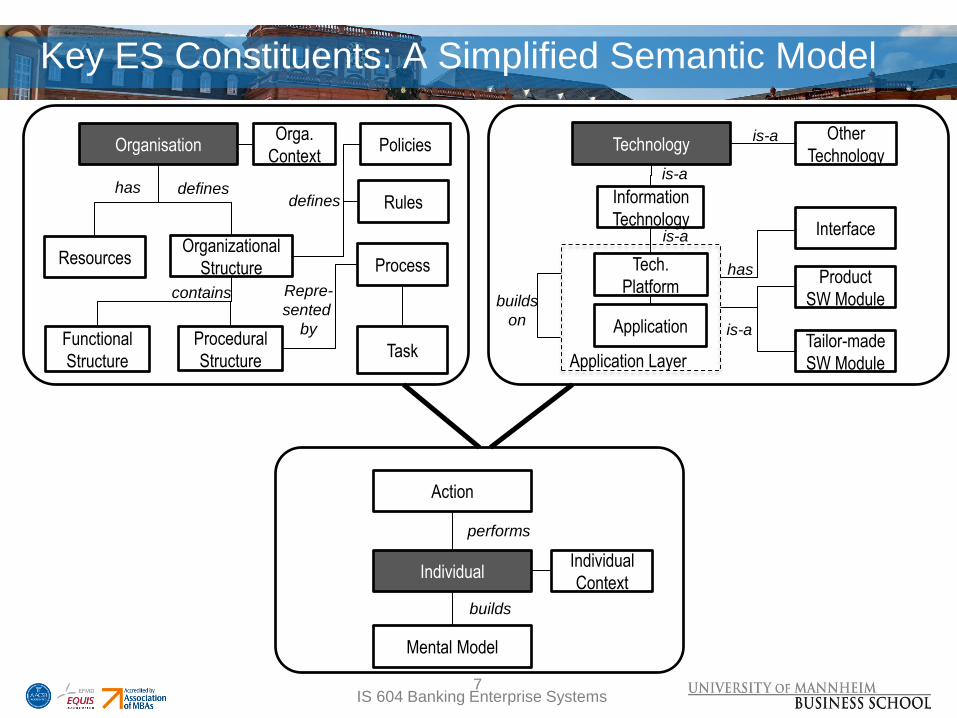

Key ES Constituents: A Simplified Semantic Model

Individual Individual

Context

Mental Model

Organisation

Organizational

Structure

Functional

Structure

Procedural

Structure

Orga.

Context

Process Resources

Technology

Information

Technology

Tech.

Platform Product

SW Module

Tailor-made

SW Module

Other

Technology

is-a

has

builds

performs

is-a

builds

on

is-a

is-a defines

contains

Task

Repre-

sented

by

Action

Application

Application Layer

Interface

has

Policies

Rules defines

IS 604 Banking Enterprise Systems 7

Platform

Platform

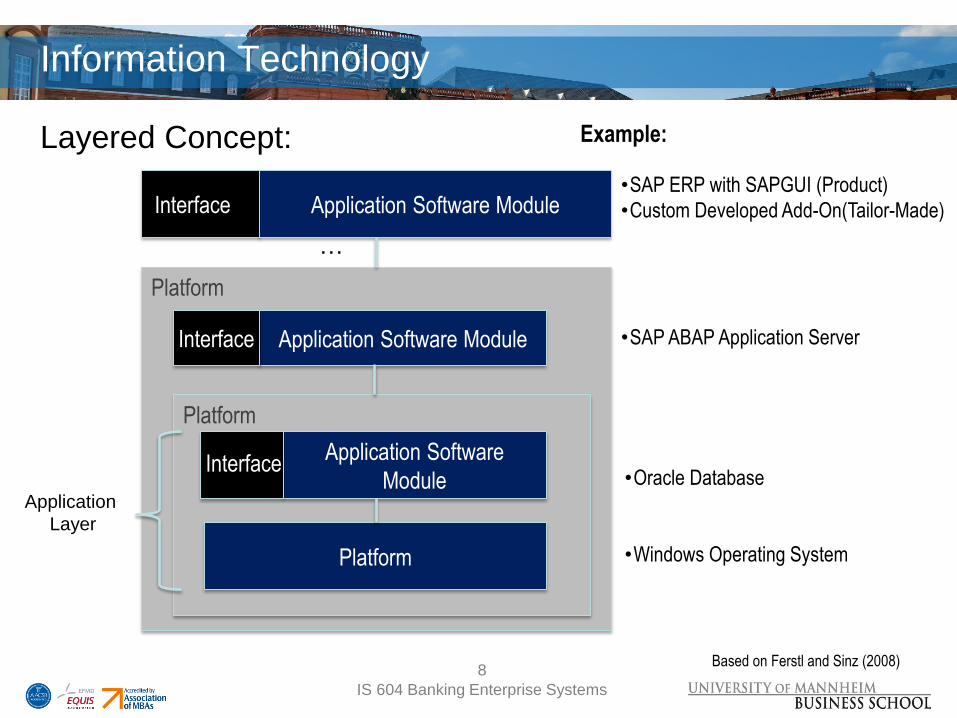

Information Technology

Layered Concept:

Platform

Application Software

Module

Application Software Module

Application Software Module

Example:

•Oracle Database

•Windows Operating System

•SAP ABAP Application Server

•SAP ERP with SAPGUI (Product)

•Custom Developed Add-On(Tailor-Made)

…

Based on Ferstl and Sinz (2008)

Interface

Interface

Interface

Application

Layer

IS 604 Banking Enterprise Systems

8

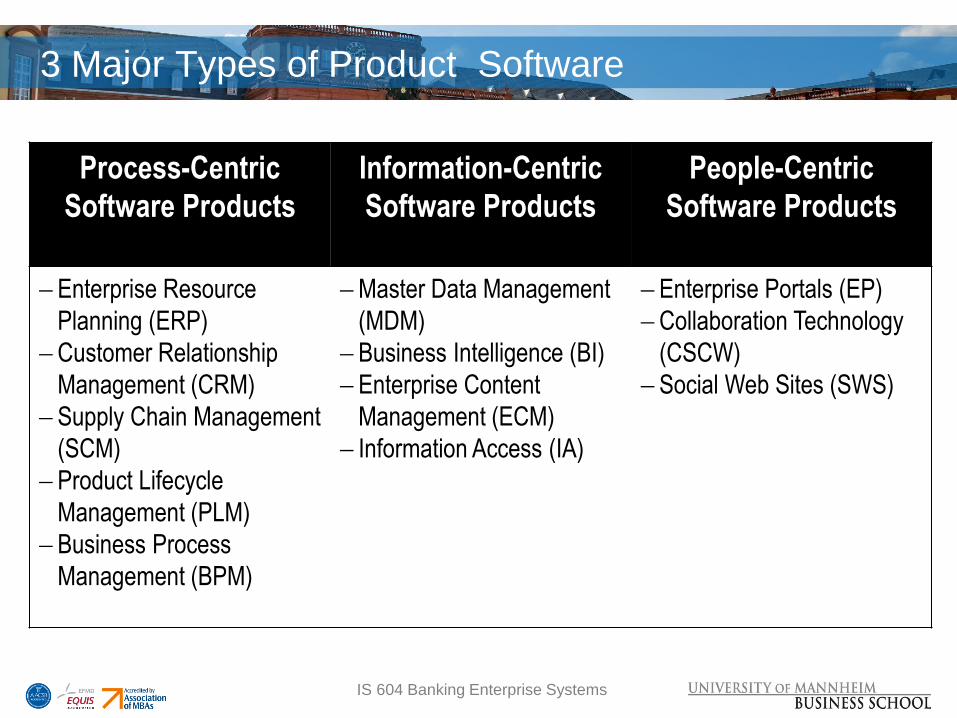

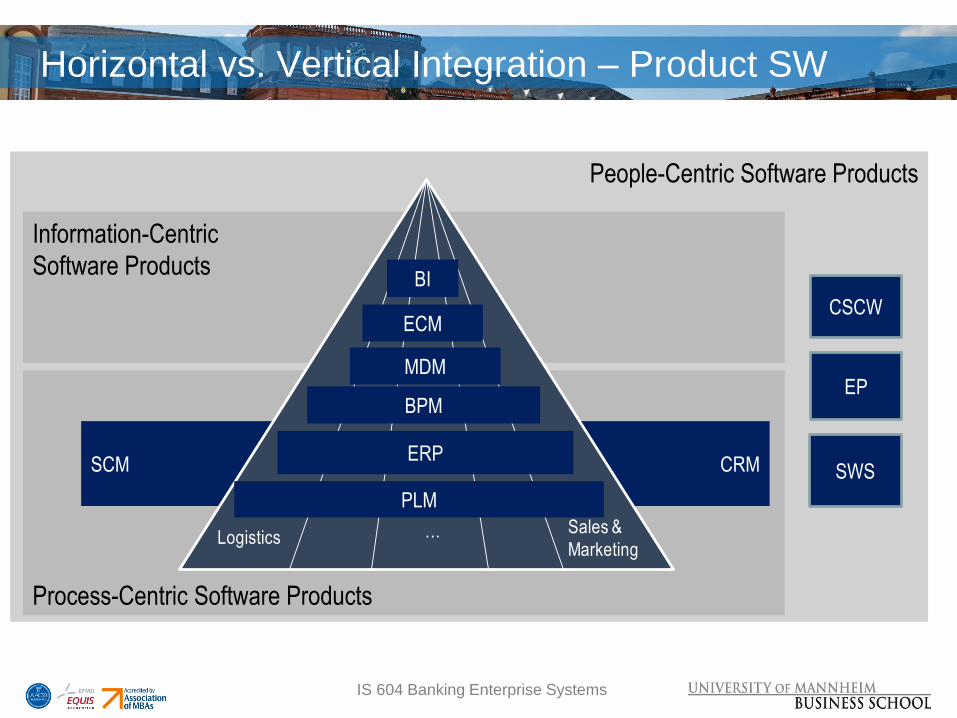

3 Major Types of Product Software

Process-Centric

Software Products

Information-Centric

Software Products

People-Centric

Software Products

Enterprise Resource

Planning (ERP)

Customer Relationship

Management (CRM)

Supply Chain Management

(SCM)

Product Lifecycle

Management (PLM)

Business Process

Management (BPM)

Master Data Management

(MDM)

Business Intelligence (BI)

Enterprise Content

Management (ECM)

Information Access (IA)

Enterprise Portals (EP)

Collaboration Technology

(CSCW)

Social Web Sites (SWS)

IS 604 Banking Enterprise Systems

Horizontal vs. Vertical Integration – Product SW

People-Centric Software Products

Process-Centric Software Products

CRM SCM

Information-Centric

Software Products

LogisticsSales &

Marketing…

ERP

BI

EP BPM

MDM

SWS

PLM

CSCW ECM

IS 604 Banking Enterprise Systems

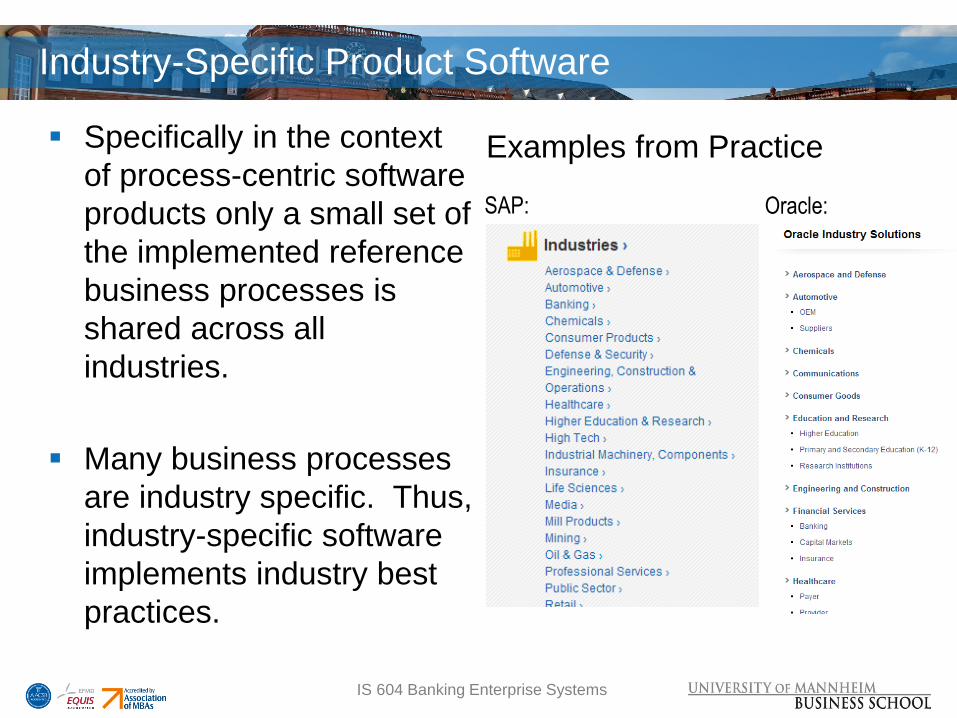

Industry-Specific Product Software

Specifically in the context

of process-centric software

products only a small set of

the implemented reference

business processes is

shared across all

industries.

Many business processes

are industry specific. Thus,

industry-specific software

implements industry best

practices.

IS 604 Banking Enterprise Systems

SAP:

Examples from Practice

Oracle:

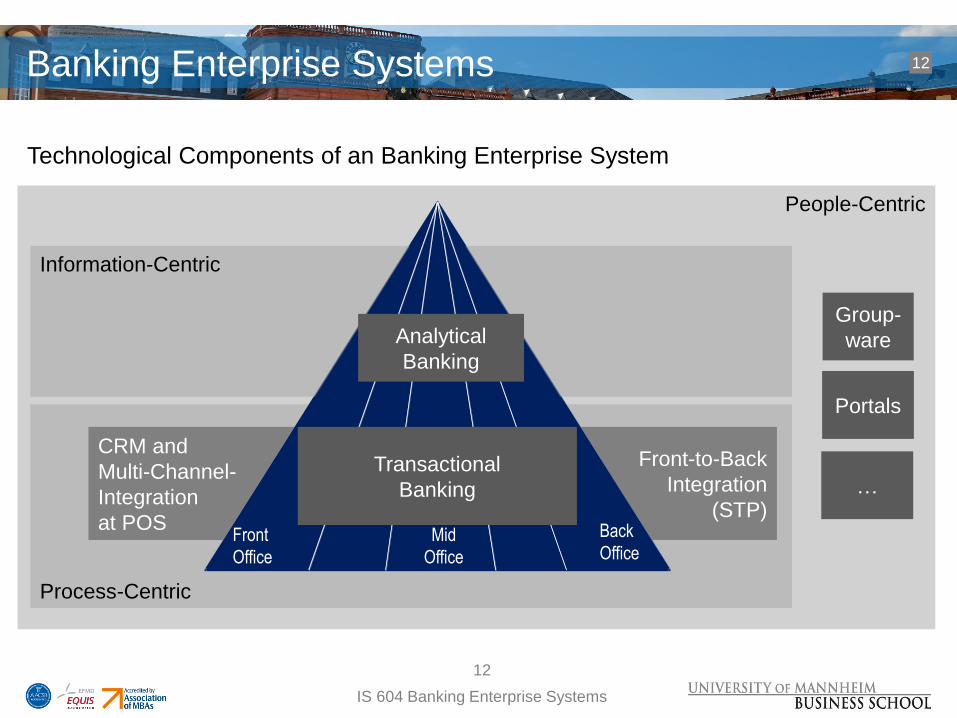

Banking Enterprise Systems

People-Centric

Process-Centric

Front-to-Back

Integration

(STP)

CRM and

Multi-Channel-

Integration

at POS

Information-Centric

Group-

ware

Portals

…

Front

Office

Back

Office

Transactional

Banking

Analytical

Banking

Mid

Office

IS 604 Banking Enterprise Systems

12

Technological Components of an Banking Enterprise System

12

Agenda – Session I

Agenda

1 Enterprise System Fundamentals

2 Motivation: Enterprise Systems in the Financial Services Industry

3 The Financial Services Industry – Banks in the Market Environment

4 Products and Services of Retail Banks

5 Reference Processes in Banking

6 The Bank as Enterprise System

7 Business Scenario: the Global Retail Bank - GRB

IS 604 Banking Enterprise Systems

13

13

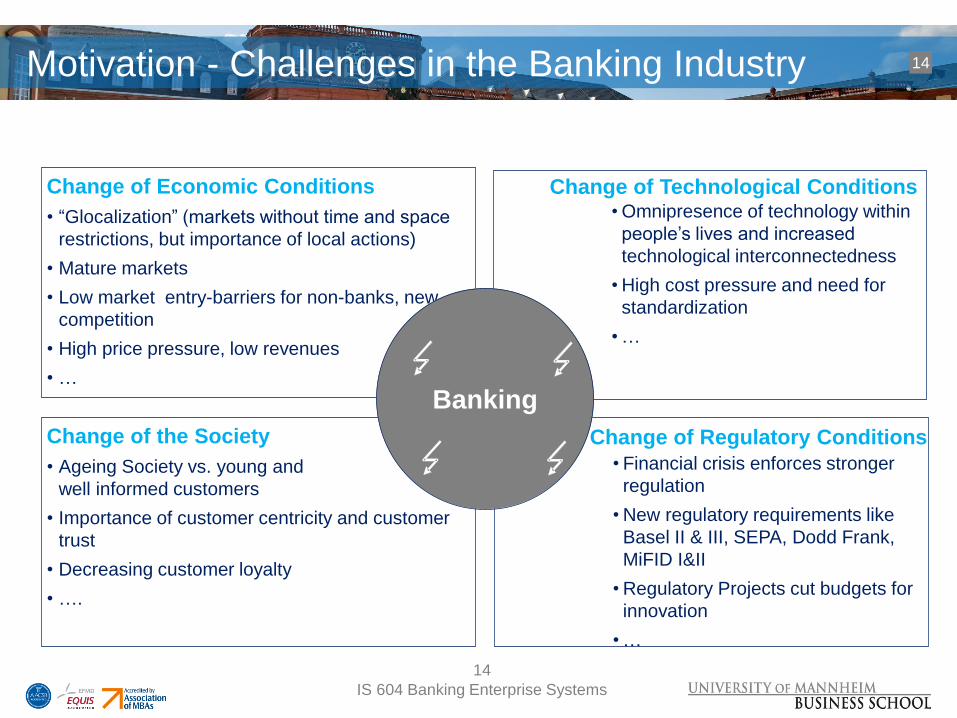

Motivation - Challenges in the Banking Industry

IS 604 Banking Enterprise Systems

14

Change of Economic Conditions

• “Glocalization” (markets without time and space

restrictions, but importance of local actions)

• Mature markets

• Low market entry-barriers for non-banks, new

competition

• High price pressure, low revenues

• …

Change of the Society

• Ageing Society vs. young and

well informed customers

• Importance of customer centricity and customer

trust

• Decreasing customer loyalty

• ….

• Financial crisis enforces stronger

regulation

• New regulatory requirements like

Basel II & III, SEPA, Dodd Frank,

MiFID I&II

• Regulatory Projects cut budgets for

innovation

• …

• Omnipresence of technology within

people’s lives and increased

technological interconnectedness

• High cost pressure and need for

standardization

• …

Banking

Change of Technological Conditions

Change of Regulatory Conditions

14

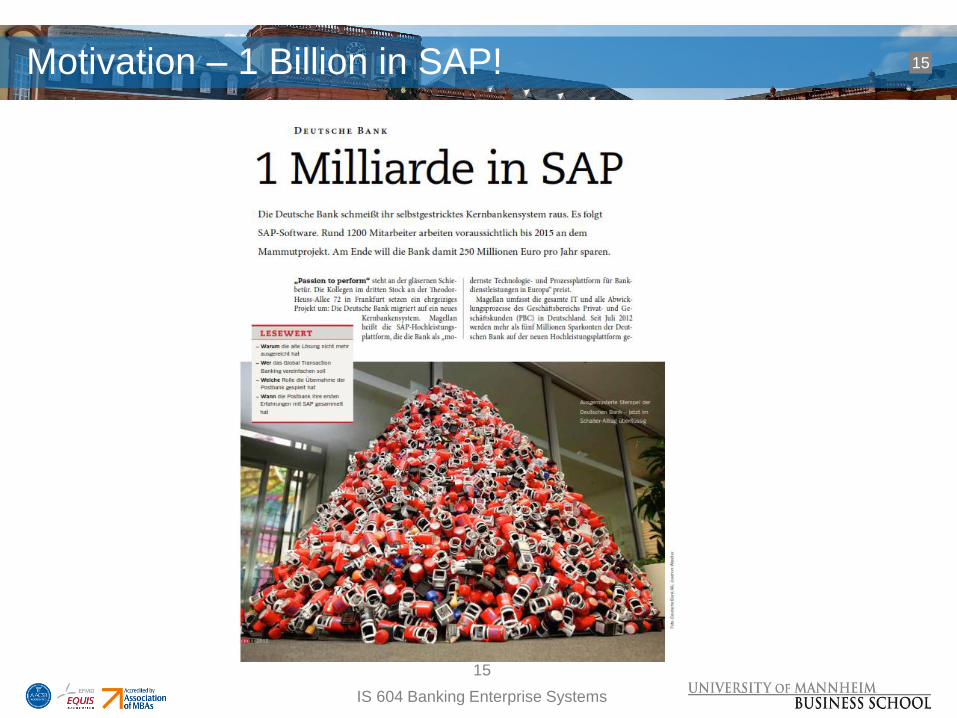

Motivation – 1 Billion in SAP!

IS 604 Banking Enterprise Systems

15

15

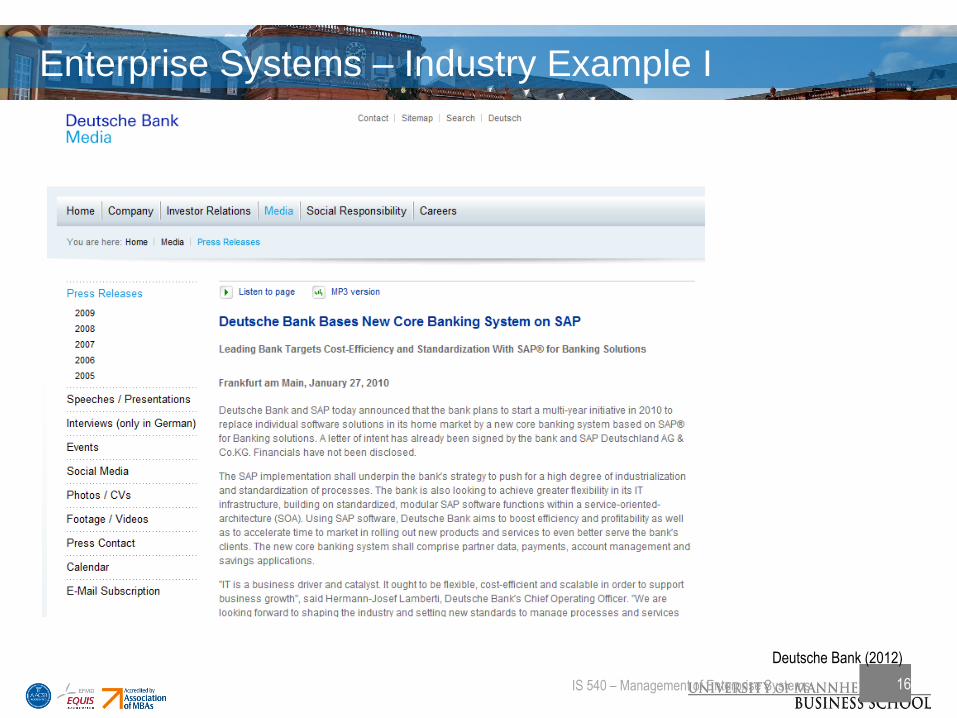

Enterprise Systems – Industry Example I

16

Deutsche Bank (2012)

IS 540 – Management of Enterprise Systems

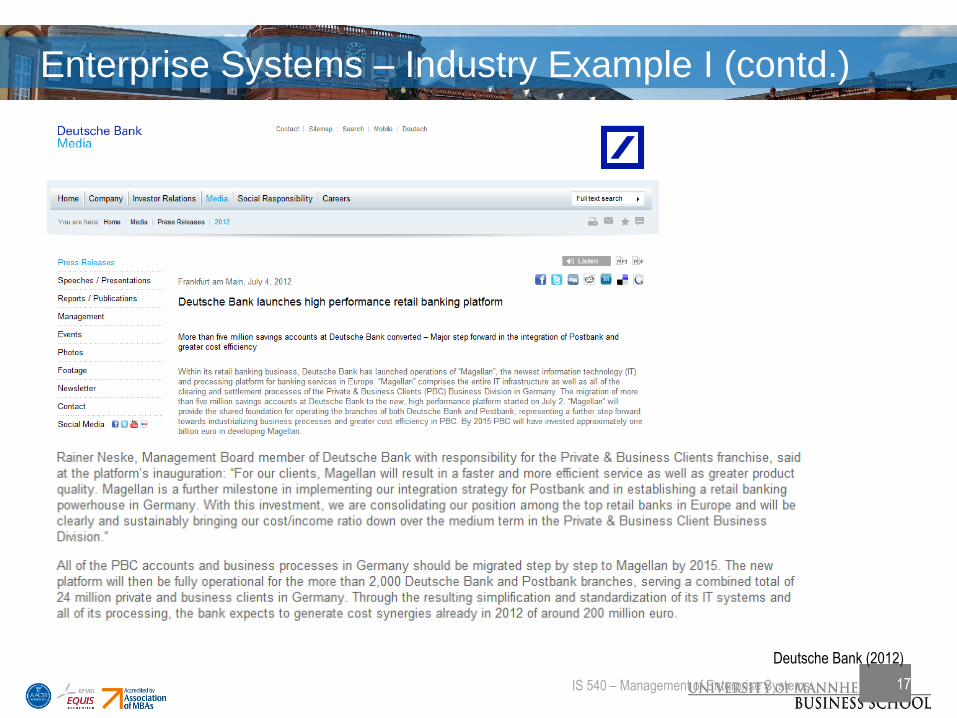

Enterprise Systems – Industry Example I (contd.)

17

Deutsche Bank (2012)

IS 540 – Management of Enterprise Systems

Agenda – Session I

Agenda

1 Enterprise System Fundamentals

2 Motivation: Enterprise Systems in the Financial Services Industry

3 The Financial Services Industry – Banks in the Market Environment

4 Products and Services of Retail Banks

5 Reference Processes in Banking

6 The Bank as Enterprise System

7 Business Scenario: the Global Retail Bank - GRB

IS 604 Banking Enterprise Systems

18

18

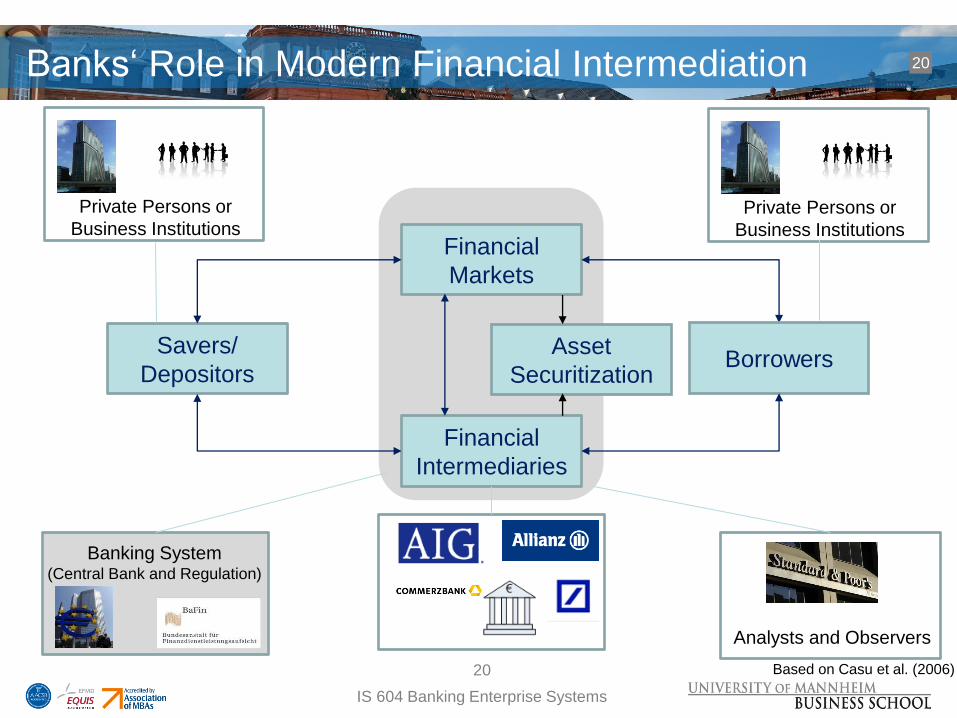

Financial Intermediation

IS 604 Banking Enterprise Systems

19

Financial

Markets

Savers/

Depositors Borrowers

Financial

Intermediaries

Savers/

Depositors Borrowers

DIRECT FINANCE

INTERMEDIATION

Casu et al. (2006)

“A bank is a financial intermediary whose core activity is to provice loans

to borrowers and collect deposits from savers. In other words they act as

intermediaries between borrowers and savers.” (Casu et al. (2006), p.4)

Banks‘ Role in Modern Financial Intermediation

Banking System (Central Bank and Regulation)

IS 604 Banking Enterprise Systems

20

20

Financial

Markets

Savers/

Depositors

Financial

Intermediaries

Borrowers

Private Persons or

Business Institutions Private Persons or

Business Institutions

Asset

Securitization

Analysts and Observers

Based on Casu et al. (2006)

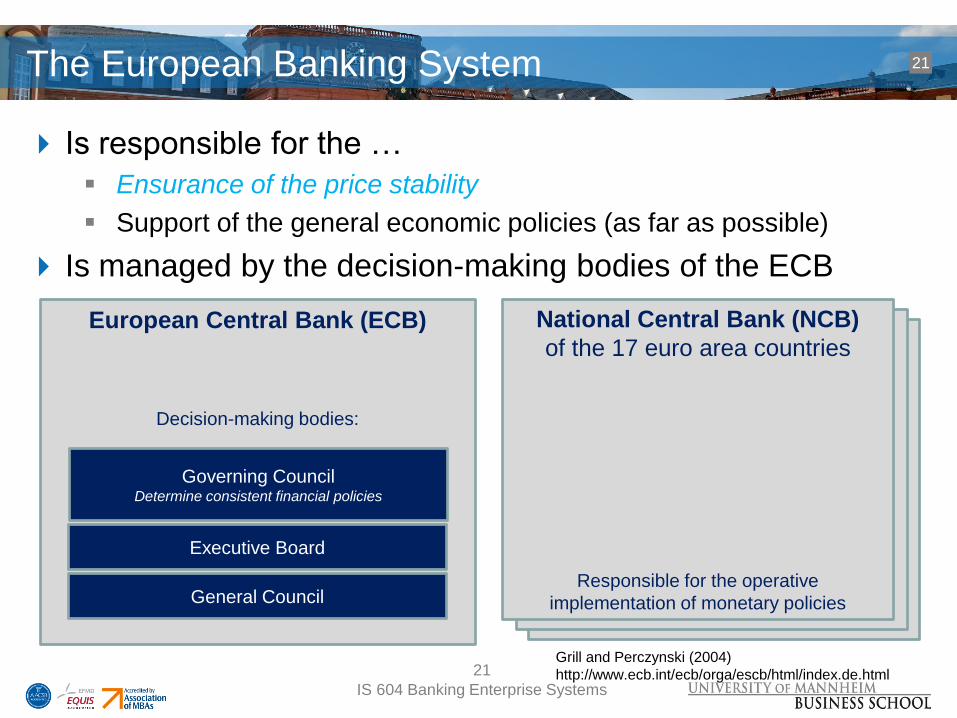

Is responsible for the …

Ensurance of the price stability

Support of the general economic policies (as far as possible)

Is managed by the decision-making bodies of the ECB

The European Banking System

IS 604 Banking Enterprise Systems

21

Grill and Perczynski (2004)

http://www.ecb.int/ecb/orga/escb/html/index.de.html

European Central Bank (ECB)

Decision-making bodies:

Governing Council Determine consistent financial policies

National Central Bank (NCB)

of the 17 euro area countries

Responsible for the operative

implementation of monetary policies

Executive Board

General Council

21

The European Banking System (cont‘d)

IS 604 Banking Enterprise Systems

22

Monetary Policy Instruments of the Eurosystem are used to

achieve the goals of the Eurosystem

Instruments:

Influence the money supply (open market operations)

Change interest rates (prime rate)

Reserve requirements

Approved business partners

Need to fulfill operational and regulatory requirements

Requirements: minimum reserve system involvement, supervision by

national authorities of a standard comparable to harmonized

EU/EEA, and financial solidity

Grill and Perczynski (2004) 22

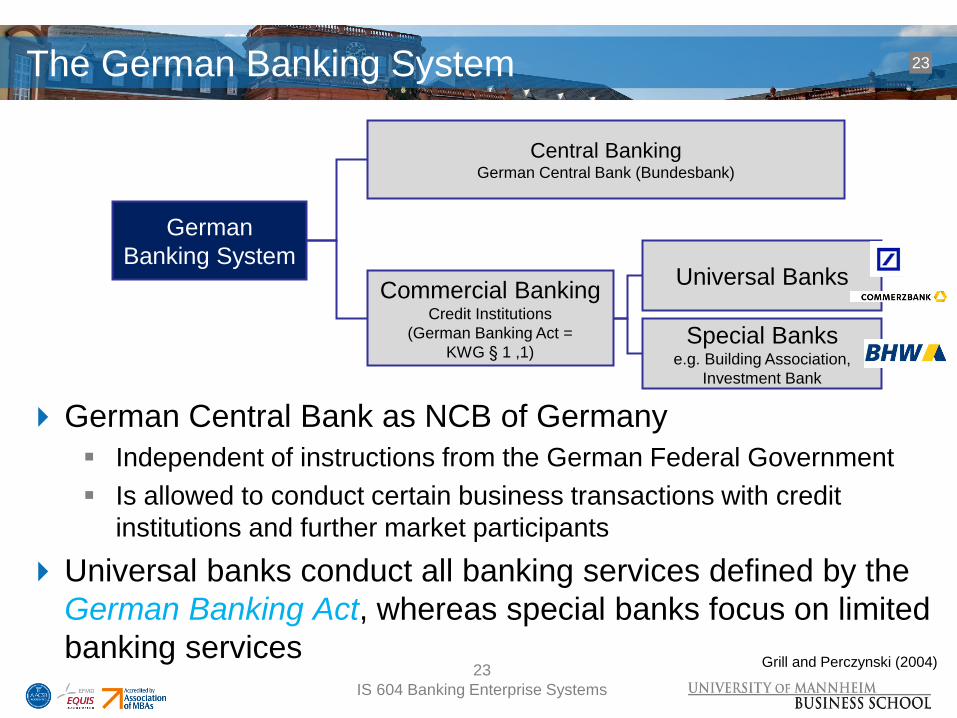

The German Banking System

IS 604 Banking Enterprise Systems

23

German Central Bank as NCB of Germany

Independent of instructions from the German Federal Government

Is allowed to conduct certain business transactions with credit

institutions and further market participants

Universal banks conduct all banking services defined by the

German Banking Act, whereas special banks focus on limited

banking services

German

Banking System

Central Banking German Central Bank (Bundesbank)

Commercial Banking Credit Institutions

(German Banking Act =

KWG § 1 ,1)

Universal Banks

Special Banks e.g. Building Association,

Investment Bank

Grill and Perczynski (2004) 23

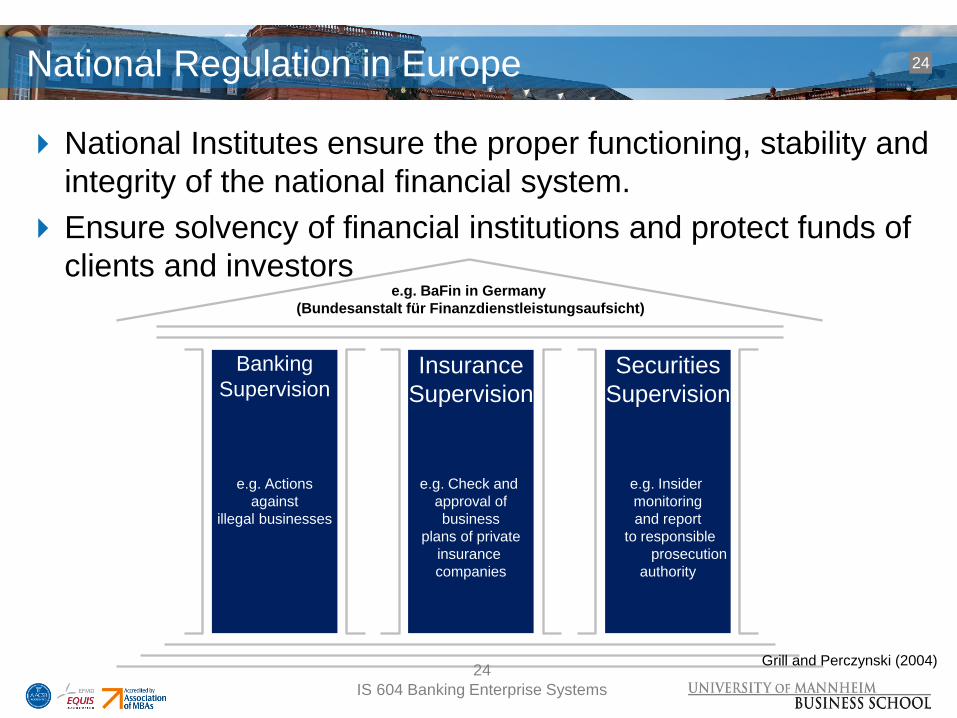

National Regulation in Europe

IS 604 Banking Enterprise Systems

24

National Institutes ensure the proper functioning, stability and

integrity of the national financial system.

Ensure solvency of financial institutions and protect funds of

clients and investors

Banking

Supervision

e.g. Actions

against

illegal businesses

Insurance

Supervision

e.g. Check and

approval of

business

plans of private

insurance

companies

Securities

Supervision

e.g. Insider

monitoring

and report

to responsible

prosecution

authority

e.g. BaFin in Germany

(Bundesanstalt für Finanzdienstleistungsaufsicht)

Grill and Perczynski (2004) 24

Agenda – Session I

Agenda

1 Enterprise System Fundamentals

2 Motivation: Enterprise Systems in the Financial Services Industry

3 The Financial Services Industry – Banks in the Market Environment

4 Products and Services of Retail Banks

5 Reference Processes in Banking

6 The Bank as Enterprise System

7 Business Scenario: the Global Retail Bank - GRB

IS 604 Banking Enterprise Systems

25

25

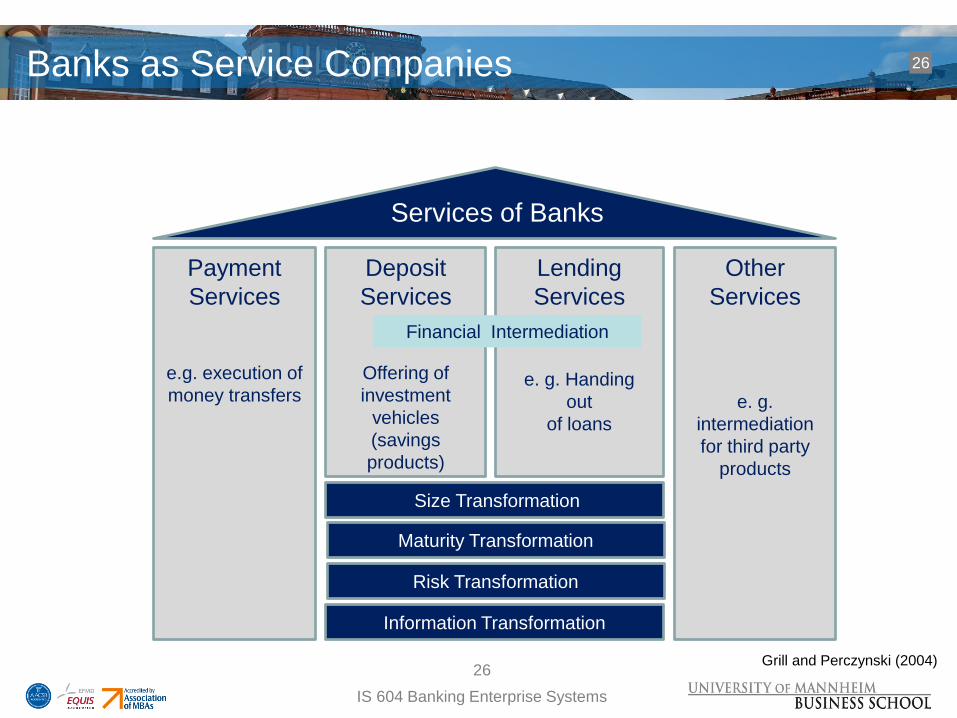

Banks as Service Companies 26

IS 604 Banking Enterprise Systems

Grill and Perczynski (2004) 26

Payment

Services

e.g. execution of

money transfers

Size Transformation

Deposit

Services

Offering of

investment

vehicles

(savings

products)

Lending

Services

e. g. Handing

out

of loans

Other

Services

e. g.

intermediation

for third party

products

Maturity Transformation

Risk Transformation

Information Transformation

Services of Banks

Financial Intermediation

IS 604 Banking Enterprise Systems

27

Credit institutions (Kreditinstitute) are companies that

conduct professional banking business

Financial service providers are non-banks, conducting

professional financial business

The Business of Banks

Types of banking businesses

Loan

Lending

Bill-Broking

Financial Commission

Deposit Investment Guarantee

Giro Issuing E-Money

Types of financial businesses

Investment Intermediation Acquisition Brokerage

Foreign Currency

Proprietary Trading Finance Portfolio Management

Credit Card Money Transmission

Grill and Perczynski (2004) 27

What do Banks do?

IS 604 Banking Enterprise Systems

28

LIABILITIES ASSETS

Customer Deposits Cash

Equity Liquid Assets

Loans

Other Investments

Fixed Assets

TOTAL TOTAL

• A banks main funding comes from customer deposits (reported on the

liabilities side of the balance sheet)

• This funding is then invested in loans, other investments and fixed assets

Based on Casu et al. (2006)

Including

retained profits

+Interest income

-Interest expense

+Net interest income (spread)

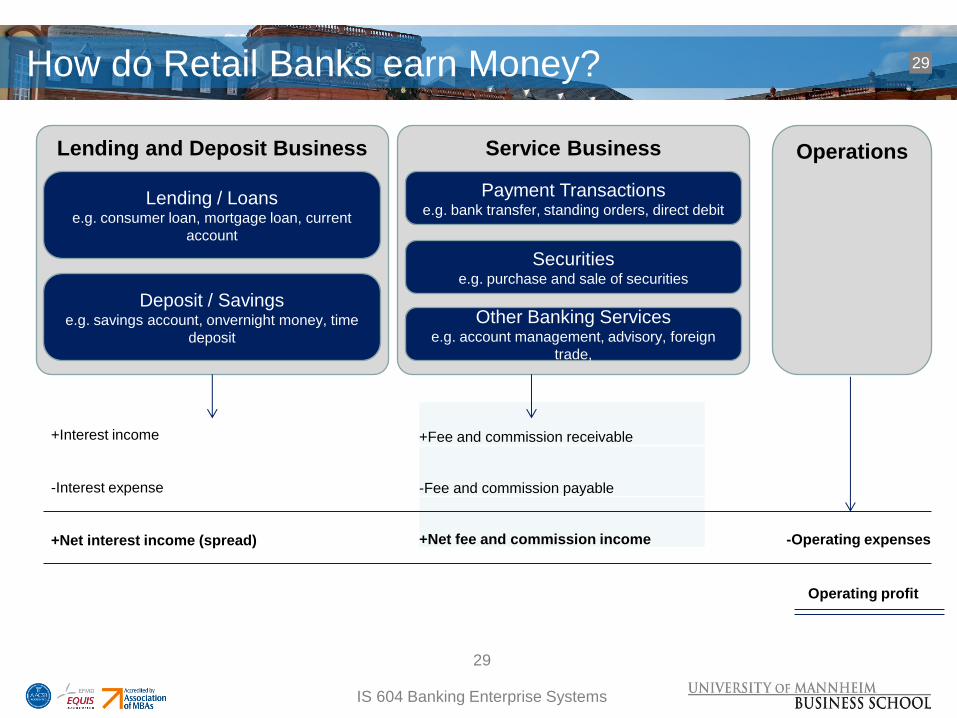

How do Retail Banks earn Money? 29

IS 604 Banking Enterprise Systems

Lending and Deposit Business Service Business

Lending / Loans e.g. consumer loan, mortgage loan, current

account

Deposit / Savings e.g. savings account, onvernight money, time

deposit

Other Banking Services e.g. account management, advisory, foreign

trade,

Payment Transactions e.g. bank transfer, standing orders, direct debit

Securities e.g. purchase and sale of securities

29

+Fee and commission receivable

-Fee and commission payable

+Net fee and commission income

Operations

Operating profit

-Operating expenses

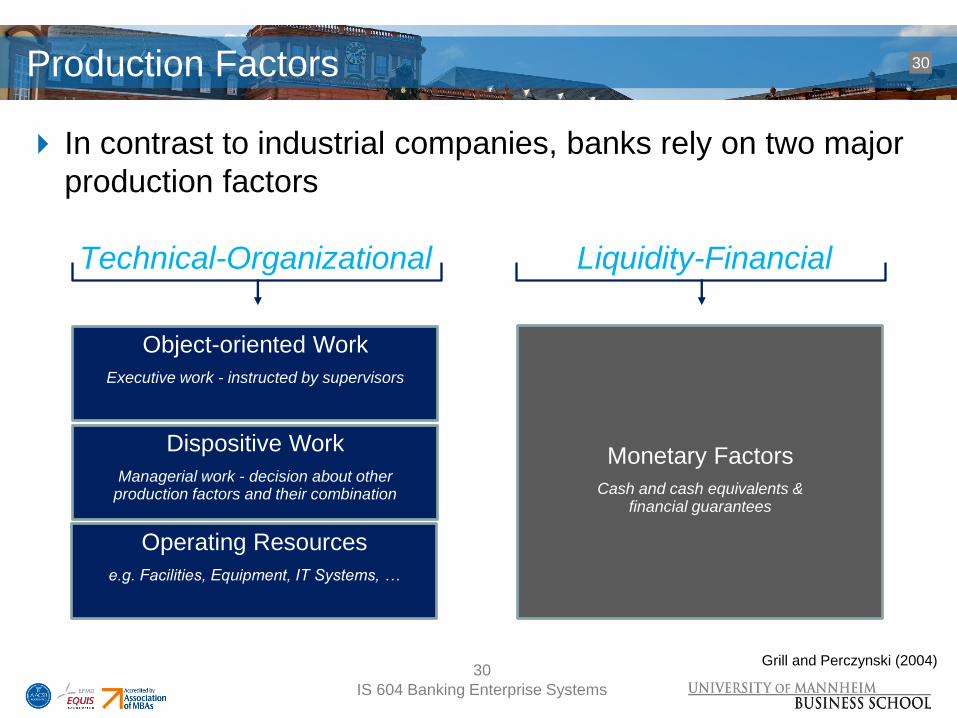

Production Factors

IS 604 Banking Enterprise Systems

30

In contrast to industrial companies, banks rely on two major

production factors

Technical-Organizational Liquidity-Financial

Object-oriented Work

Executive work - instructed by supervisors

Monetary Factors

Cash and cash equivalents & financial guarantees

Dispositive Work

Managerial work - decision about other production factors and their combination

Operating Resources

e.g. Facilities, Equipment, IT Systems, …

Grill and Perczynski (2004) 30

Distribution of Banking Services

IS 604 Banking Enterprise Systems

31

A bank needs a consequent market-oriented business

strategy in order to protect or enhance its market share

Marketing Management

Protect or enhance the segment- and product-related market shares by

focusing on customers needs

Marketing Instruments

Usage of aligned, sales-political instruments (“Marketing Mix”) to protect

and enhance the demand

Grill and Perczynski (2004) 31

IS 604 Banking Enterprise Systems

32

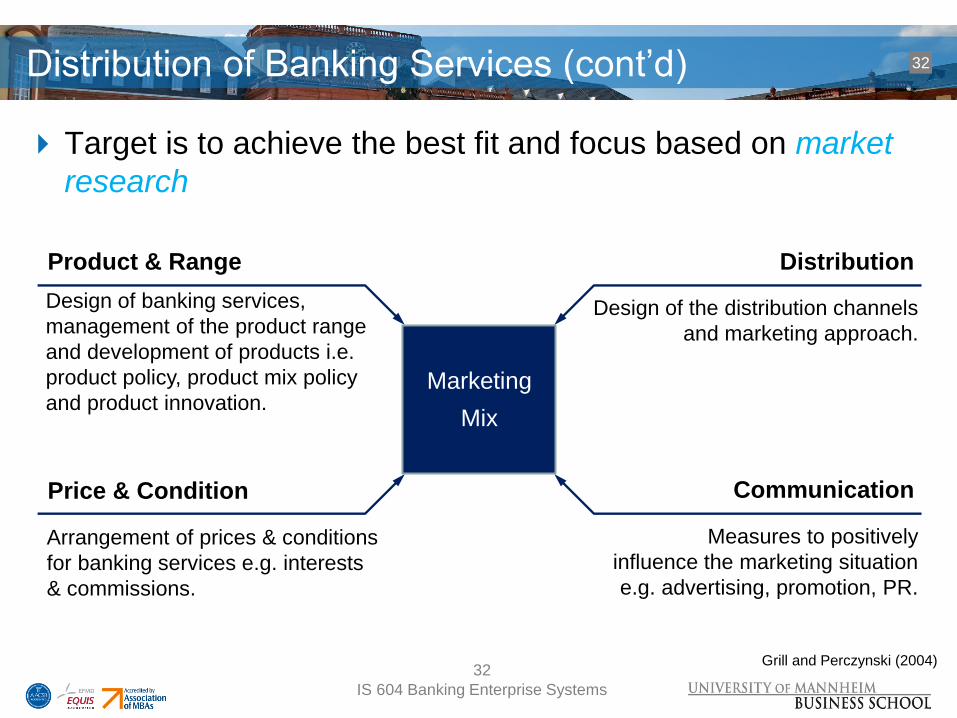

Target is to achieve the best fit and focus based on market

research

Communication

Distribution

Price & Condition

Product & Range

Design of the distribution channels

and marketing approach.

Measures to positively

influence the marketing situation

e.g. advertising, promotion, PR.

Arrangement of prices & conditions

for banking services e.g. interests

& commissions.

Marketing

Mix

Design of banking services,

management of the product range

and development of products i.e.

product policy, product mix policy

and product innovation.

Distribution of Banking Services (cont’d)

Grill and Perczynski (2004) 32

How Banks reach their Customers

IS 604 Banking Enterprise Systems

33

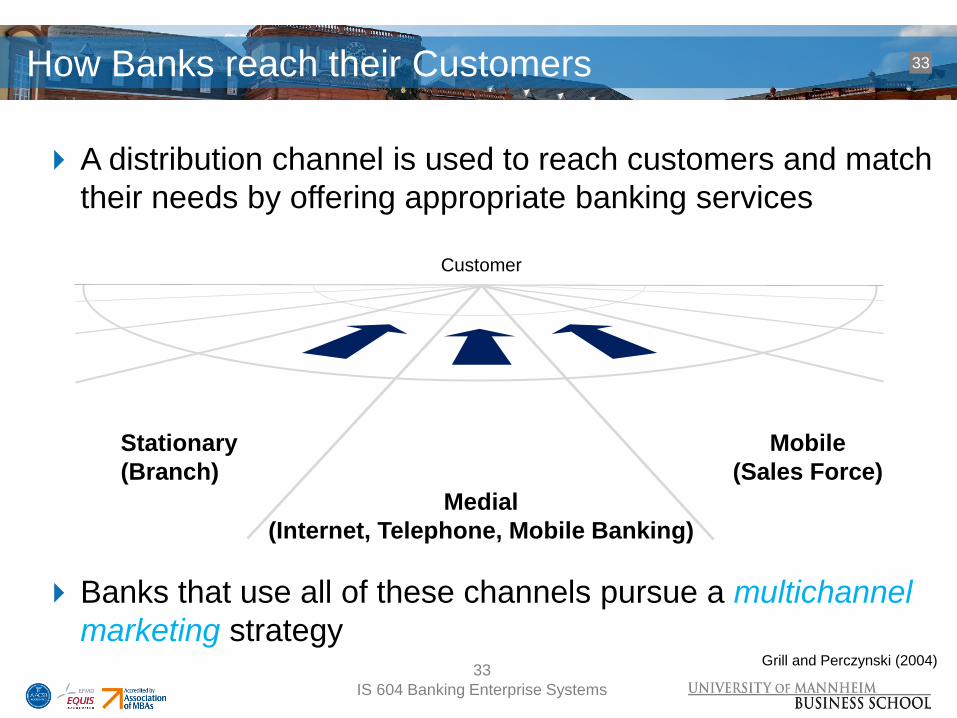

A distribution channel is used to reach customers and match

their needs by offering appropriate banking services

Banks that use all of these channels pursue a multichannel

marketing strategy

Customer

Stationary

(Branch)

Medial

(Internet, Telephone, Mobile Banking)

Mobile

(Sales Force)

Grill and Perczynski (2004) 33

Types of Distribution Channels

IS 604 Banking Enterprise Systems

34

Stationary channels: Traditional sale of banking services at

permanent locations

Direct banks

No personnel-intensive sale via branches

Competence

centers

Offer tailored services to specific customer

segments at selected locations e.g. investment-,

real estate-, and business-center

Standard

branches

offer basic services to standard private customer

segments with middle and low income

Self-service

branches

offering technology to pursue routine businesses

Grill and Perczynski (2004) 34

Types of Distribution Channels (cont‘d)

IS 604 Banking Enterprise Systems

35

Medial channels: Sale of banking services using

electronic media. Also called home banking as

customer can use services at home

Online banking (PIN/TAN or HBCI approach for security

purposes)

Telephone banking (in combination with call centers)

Internet Banking

Mobile Banking

Mobile channels:

Sales representative, independent brokers,

and mobile branches

Grill and Perczynski (2004) 35

Retail Banking Customers

IS 604 Banking Enterprise Systems

36

Banking Customers can be categorized into two main

business areas:

Retail Business Private and Commercial

Business

Standard private customers

e.g. salary earner, pensioner

Wealthy (private)

customers

e.g. entrepreneur,

freelancer,

manager

Business/Corporate

customers

e.g. (small)

companies,

municipalities,

associations

Focus on deposits Focus on

deposit/investment

Focus on

lending/financing

• Practically not manageable

customer base

• Need for an easy to understand

and standardized offerings

• Individually addressable customer base

• Need for tailored offerings

Grill and Perczynski (2004) 36

The Account in a Business Relation

IS 604 Banking Enterprise Systems

37

Deals between banks and customers are usually processed

using bank accounts

Bank accounts are used to record claims and liabilities

Account Book as archive for deals

Consistent and economic processing

Deals are based on contracts (e.g. giro, lending)

Benefits of using Bank Accounts

Customer Bank

Protection against theft by reduced cash

holdings (cashless payments)

Settlement of customer claims

and liabilities

Usage of further banking services possible

(e.g. credit card)

Procurement of deposits and processing of

loans

Interest earnings or expenses depending on

the type of contract

Cross selling strategy

Interest and commission earnings Grill and Perczynski (2004)

37

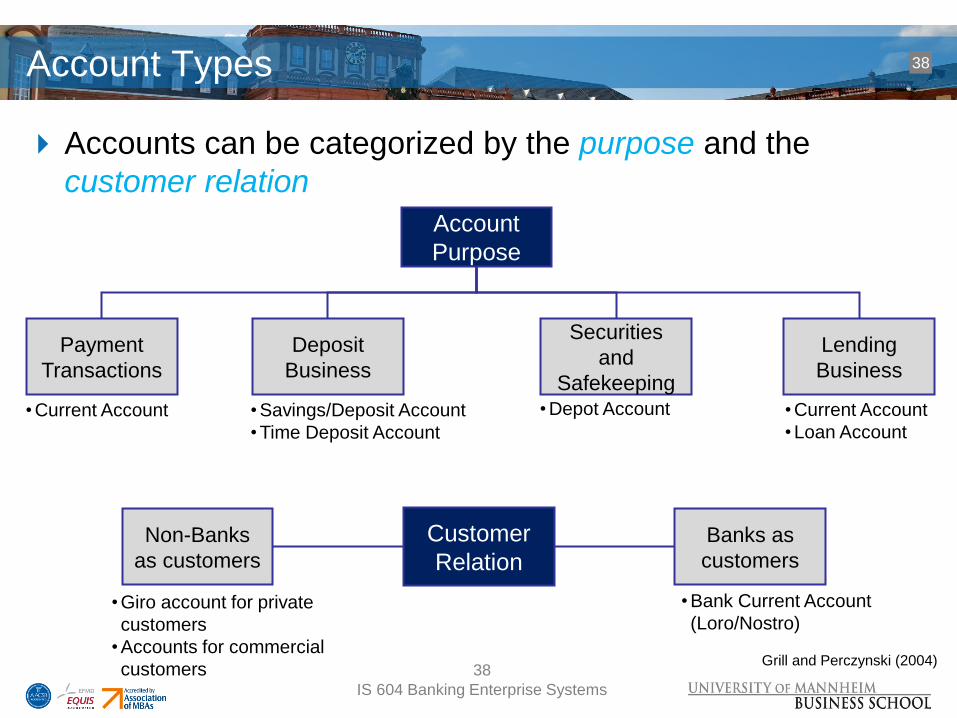

Account Types

IS 604 Banking Enterprise Systems

38

Accounts can be categorized by the purpose and the

customer relation

Account

Purpose

Payment

Transactions

Deposit

Business

Lending

Business

Securities

and

Safekeeping

Customer

Relation

Banks as

customers

Non-Banks

as customers

• Current Account • Savings/Deposit Account

• Time Deposit Account

• Depot Account

• Bank Current Account

(Loro/Nostro)

• Current Account

• Loan Account

• Giro account for private

customers

• Accounts for commercial

customers Grill and Perczynski (2004)

38

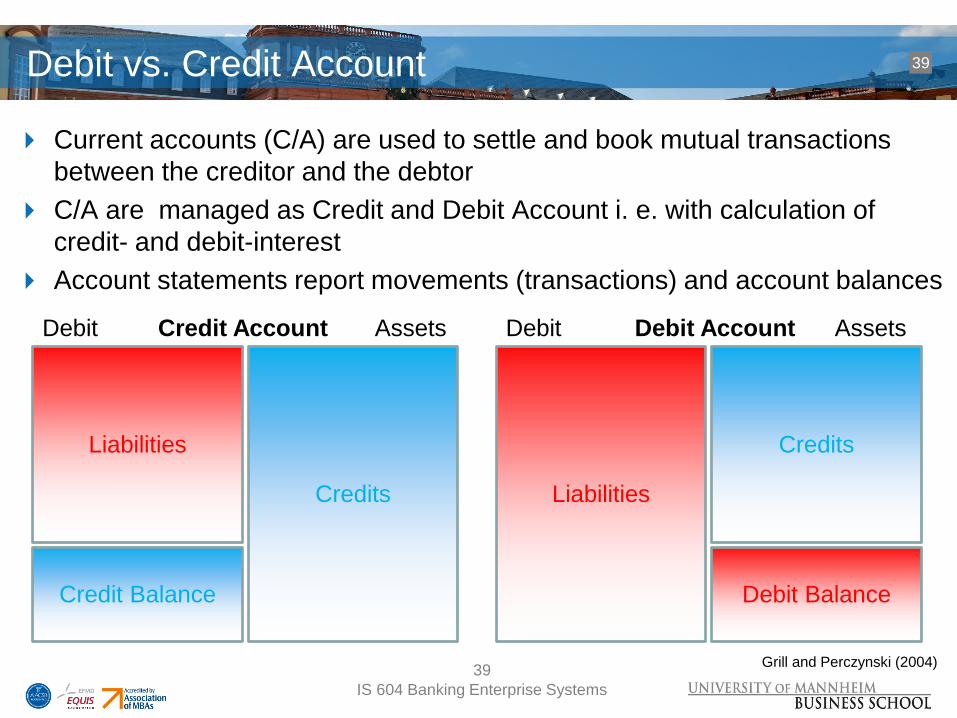

Debit vs. Credit Account

IS 604 Banking Enterprise Systems

39

Current accounts (C/A) are used to settle and book mutual transactions

between the creditor and the debtor

C/A are managed as Credit and Debit Account i. e. with calculation of

credit- and debit-interest

Account statements report movements (transactions) and account balances

Liabilities

Credits

Credit Balance

Liabilities

Credits

Debit Balance

Debit Credit Account Assets Debit Debit Account Assets

Grill and Perczynski (2004) 39

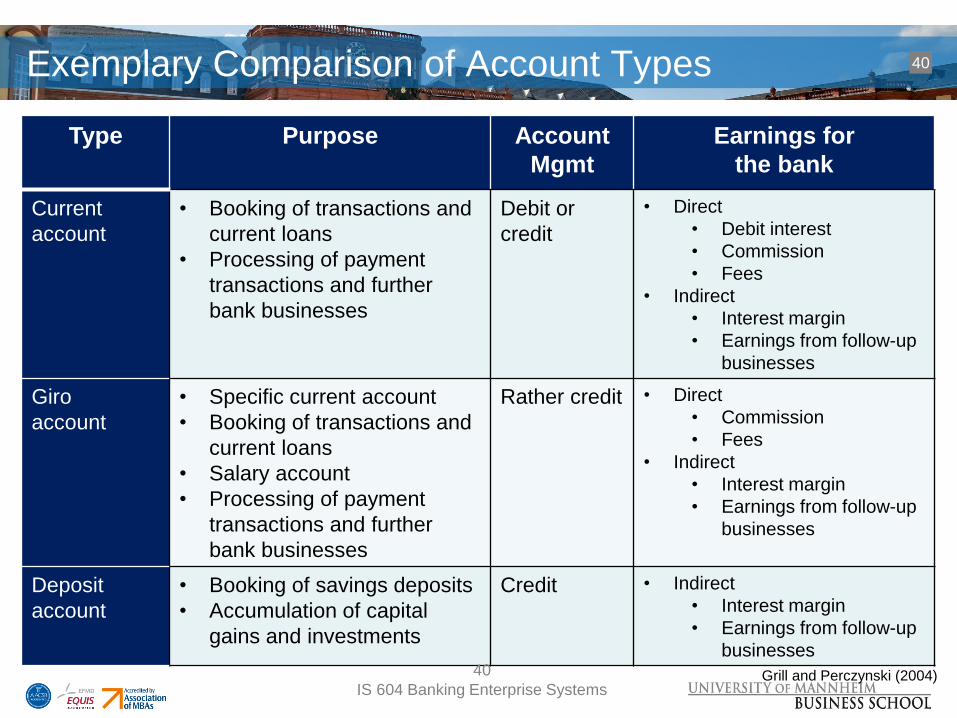

Exemplary Comparison of Account Types

IS 604 Banking Enterprise Systems

40

Type Purpose Account

Mgmt

Earnings for

the bank

Current

account

• Booking of transactions and

current loans

• Processing of payment

transactions and further

bank businesses

Debit or

credit

• Direct

• Debit interest

• Commission

• Fees

• Indirect

• Interest margin

• Earnings from follow-up

businesses

Giro

account

• Specific current account

• Booking of transactions and

current loans

• Salary account

• Processing of payment

transactions and further

bank businesses

Rather credit • Direct

• Commission

• Fees

• Indirect

• Interest margin

• Earnings from follow-up

businesses

Deposit

account

• Booking of savings deposits

• Accumulation of capital

gains and investments

Credit • Indirect

• Interest margin

• Earnings from follow-up

businesses

Grill and Perczynski (2004) 40

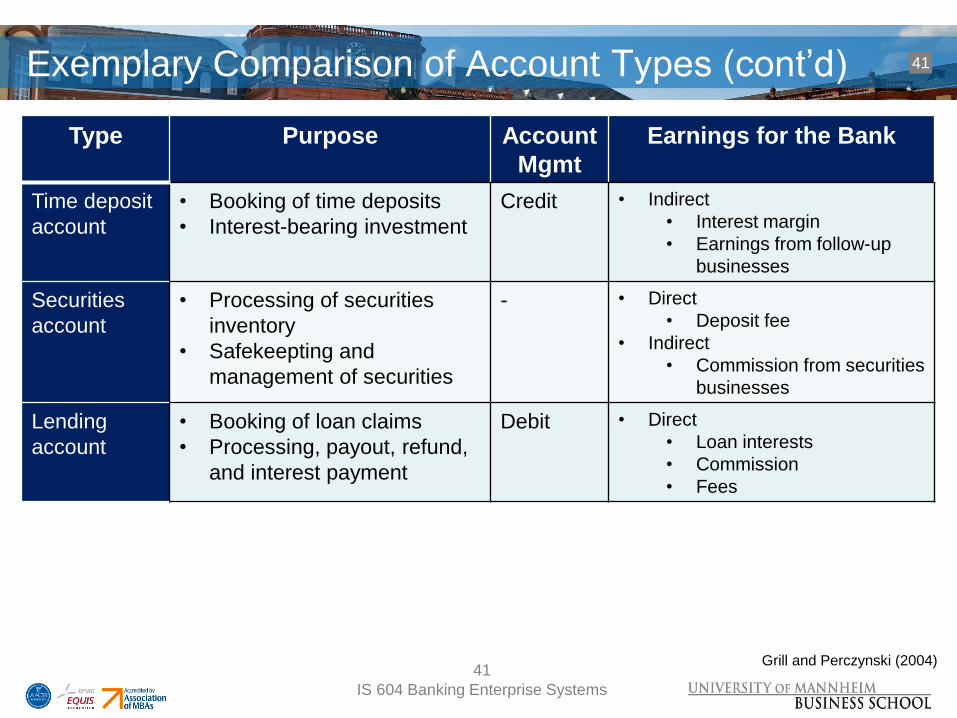

Exemplary Comparison of Account Types (cont’d)

IS 604 Banking Enterprise Systems

41

Type Purpose Account

Mgmt

Earnings for the Bank

Time deposit

account

• Booking of time deposits

• Interest-bearing investment

Credit • Indirect

• Interest margin

• Earnings from follow-up

businesses

Securities

account

• Processing of securities

inventory

• Safekeepting and

management of securities

- • Direct

• Deposit fee

• Indirect

• Commission from securities

businesses

Lending

account

• Booking of loan claims

• Processing, payout, refund,

and interest payment

Debit • Direct

• Loan interests

• Commission

• Fees

Grill and Perczynski (2004) 41

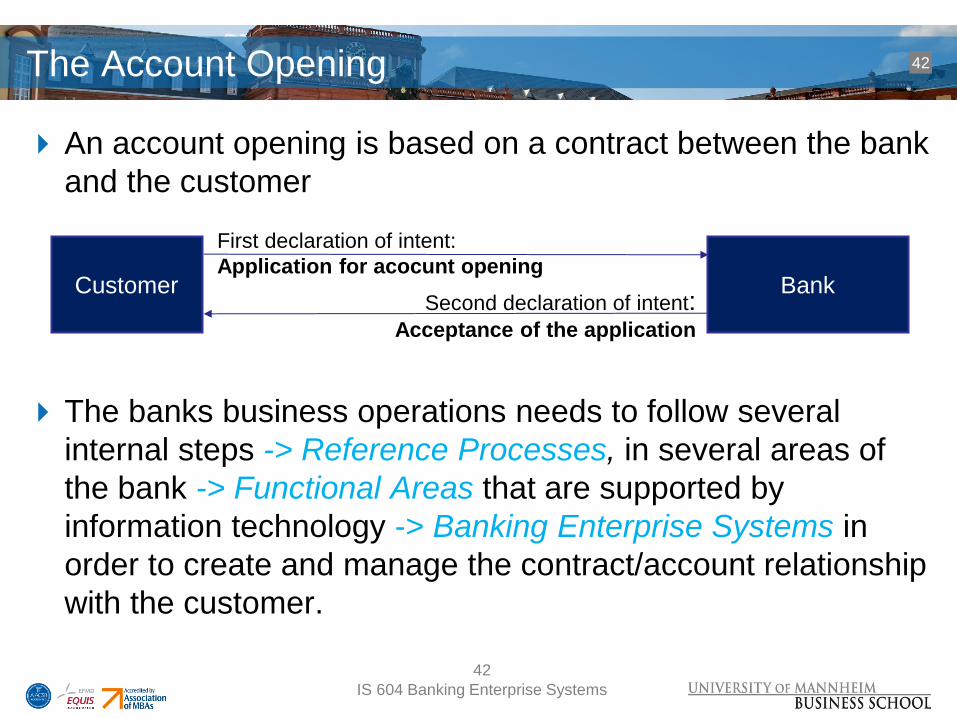

The Account Opening

IS 604 Banking Enterprise Systems

42

An account opening is based on a contract between the bank

and the customer

The banks business operations needs to follow several

internal steps -> Reference Processes, in several areas of

the bank -> Functional Areas that are supported by

information technology -> Banking Enterprise Systems in

order to create and manage the contract/account relationship

with the customer.

Customer

First declaration of intent:

Application for acocunt opening

Second declaration of intent: Acceptance of the application

Bank

42

Questions, Comments, Observations

43 IS 604 Banking Enterprise Systems

Suggested Literature

44 IS 604 Banking Enterprise Systems

44

Essvale (2011); Business Knowledge for IT in Global

Retail Banking; Available in the Uni Mannheim e-library:

http://site.ebrary.com/lib/unimannheim/docDetail.action?d

ocID=10466331

Casu B., Giardone C., Molyneux P. (2006); Introduction to

Banking, Prentice Hall

Grill and Perczynski (2004), “Wirtschaftslehre des

Kreditwesens”, 38. Edition (only German)

IS 604 Banking Enterprise Systems

45

Grill and Perczynski (2004), “Wirtschaftslehre des Kreditwesens”, 38.

Edition

http://www.ecb.int/ecb/orga/escb/html/index.de.html

References

45

![A Contemporary Design Tool [TOC] Embedded Systems](https://img.pdfslide.net/doc/110x75/577cc12a1a28aba7119270b7/a-contemporary-design-tool-toc-embedded-systems.jpg)