Embed Size (px)

Citation preview

Jamaica, a leading per capita exportcountry known for its commitment to

creativity, innovation and exceptional quality.

The National Export Strategy of Jamaica was developed on the basis of the process, methodology and technical assistance of the International Trade Centre (ITC).

w w w . j a m a i c a t r a d e a n d i n v e s t . o r g / n e s | 1 - 8 8 8 - 4 2 9 - 5 N E S ( 1 - 8 8 8 - 4 2 9 - 5 6 3 7 )

i n d u s t r y s e c t o r s t r a t e g y

4

Fashion

IntroductionRationale

The fashion design sector is a fairly new area of focus, as the country’s once booming industry fell into decline along with the garment construction and other manufacturing sectors in the last decade. Although the actual levels of production for this industry are lower than other industries prioritised in the export strategy, the potential is significant to capture the design value represented by the export of garments, which are currently outsourced. The export strategy for this sector is therefore focussed on capturing greater value from the current value chain, as well as a larger share of the global market.

As with other creative industries it provides the potential for regional development and the economic engagement of less advantaged groups – based on economic (poor) or education level – who may not easily find (have access to) traditional employment opportunities. The current levels of production and export (although not all design value is domestic) is also a significant factor in its prioritisation. The industry is a significant employer – formal and informal (at-home jobs) – as well as a linked industry to entertainment and tourism.

In the same way that it is argued for entertainment that nurturing our creative outlets is critical it is the same for fashion, which is a creative outlet and economic empowerment tool for many Jamaicans. Fashion is therefore deemed to be critical to Jamaica’s development.

Product Groups and Related Programmes

What has traditionally been described as Jamaica’s fashion industry is the garment construction industry. For the purposes of the Export Strategy, the full scope of the value chain is essential: focus is on fashion design, which is regaining recognition and support, assembly, and other support services. In addition to fashion (apparel) design, the sector strategy also covers jewellery and accessories. In particular the work being done by the Jamaica Fashion and Apparel Cluster is integral with the resulting strategies being one and the same.

This strategy will be aligned to the Creative and Cultural industries initiatives under Vision 2030, and to operational elements of the relevant support organisations, such as the Jamaica Business Development Corporation (JBDC).

f a s h i o n a n d a c c e s s o r i e s 5

1 Exports, 2003-2007 (Statistical Institute of Jamaica, 2008).2 International Trade Statistics, 2006 (CountryMap/Jamaica) (International Trade Centre, 2008).

Where Do We Want to Be?The Vision

Jamaica is the fashion centre of the Caribbean.

Objectives

• A strong national fashion clusterthat will be sustained following the termination of the PSDP and its support.

• A competitive fashion sectorproducing quality garments to international-level standards to meet market demands.

• Anationallyandregionallyprominentindustry based on the increased awareness of the Jamaican cluster

• Increased production of locallydesigned and manufactured fashion products

Where Are We Now? - An AssessmentExport Performance and Assessment of Overall Competitiveness

Between 2003 and 2007, apparel

exports fell by 87%, declining from US$11.4m to US$1.5m1. In 2006, apparel exports totalled US$4.3m with apparel/accessories knitted or crocheted totalling US$1.4m and exports of apparel/accessories not knitted or crocheted totalling US$2.9m. While the industry is on the decline, two products have been noted as emerging products, in the latter category – women’s blouse and shirts, which grew in value by 14% and had an increase in its share of exports of 8%; and babies’ garments and clothing accessories, which had an increase in value of just over 50% and an increase in its share of exports of over 40%.2

Figures for jewellery indicate that Jamaica exported US$2.1m in 2006. However, other articles of jewellery were also included among the list of Jamaica’s exports, including clocks and wristwatches (not manufactured in Jamaica), which suggests, along with the destination of imports (USA, Canada and Switzerland), that most jewellery exports, are re-exports, and most likely those traded through the duty free shopping industry. The portion of exports representing Jamaican products is insignificant, however there are opportunities to increase the share of domestic product exported.

The USA is Jamaica’s first and fifth most important trading partner for apparel/

i n d u s t r y s e c t o r s t r a t e g y

6

3 International Trade Statistics (WTO, 2007).

accessories not knitted or crocheted and apparel/accessories knitted or crocheted, respectively. Competitors export significantly larger quantities than Jamaica - the main supplier, China, exports more than ten thousand times the value of Jamaica’s exports to the USA, at US$24,403 million to dominate US clothing imports with 29.4% market share. Regional competitors include Mexico and the Dominican Republic, which rank second and sixteenth, respectively among US top suppliers. 3

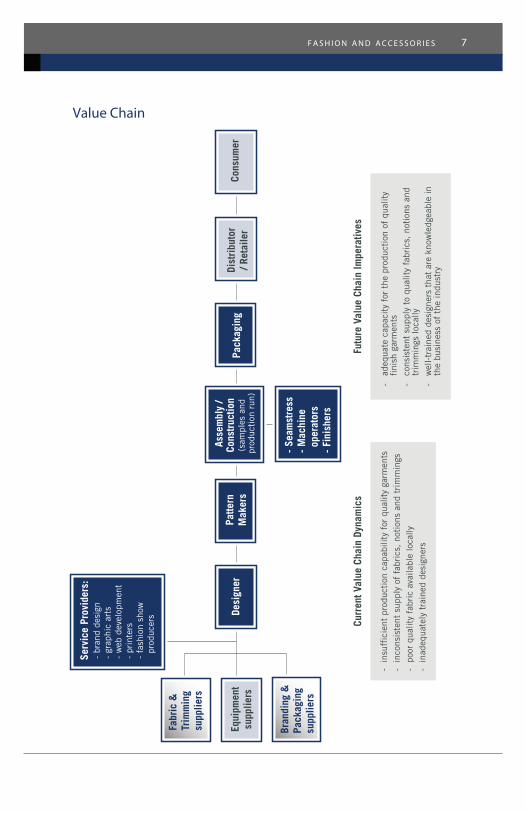

The industry’s Value Chains – Illustration and Analysis

The value chain for the domestic fashion design industry is attached. The traditional garment construction industry in Jamaica represents only that (assembly/construction) component in a global value chain, with design and other value portions captured in other markets. We again re-iterate the expanded focus of the strategy on local designers. The issues related to the assessment of the value chain are noted below, with additional opportunities and constraints identified throughout the document, and summarised in the SWOT.

Improving Efficiencies

• There is no resource listing

available to designers who wish to identify and contract pattern-makers, seamstresses, finishers, contract manufacturers or other value chain participants and service providers. Such a listing would be critical in assisting firms overcome manufacturing capacity and capability constraints and help manufacturers grow their businesses by contracting jobs to increase utilisation/output and therefore their own earnings.

• In addition to the absence of thedatabase, there have been few networking opportunities, but this is improving through the cluster initiative.

• The import practices of fabric andtrimming suppliers impacts on the consistency and the quality of fabrics and trimmings available to the local industry. Fabric suppliers are focussed primarily on the retail market and so there is little to no consideration of the needs of the fashion enterprises – for example commercial quantities or re-orders.

Reducing Leakages

• At the moment, almost all of theinputs and equipment are imported. There is no scope for producing equipment,or most of the fabric

f a s h i o n a n d a c c e s s o r i e s 7

Value Chain

i n d u s t r y s e c t o r s t r a t e g y

8

locally. The main opportunity for local fabric is the use of West Indies Sea Island Cotton, currently grown in the country but not spun from fibre to fabric locally. Other opportunities exist for locally crafted trimmings as well, but overall the scope for reducing leakages is very small.

Value Addition

• Value addition opportunities areprimarily in the area of design, to convert the garment industry from primarily outsourced garment construction to locally designed products that are manufactured in Jamaica. The locally designed products are finished locally.

Value Creation

• The opportunities exist for linkagesin the entertainment industry for costumes (dance, drama and film) and merchandising (primarily music and events).

The value chain remains the same structurally with the desired future state noted on the illustration of the current value chain.

Performance against Critical Success Factors

The critical success factors for the industry are considered to be:

• Highqualityfinishofthegarment,inwhich Jamaican products vary but are generally medium in terms of competitiveness;

• Price, for which Jamaica isperforming fairly;

• Uniquenessindesigns,inwhichweare considered to perform medium to high;

• Order delivery capacity andcapability, in which the sector currently performs poorly;

• Logisticsmanagement,inwhichthesector is also considered to have poor performance;

• Customer service which variesamong enterprises.

Government Policy and Strategy in Support of the Sector

Several years ago the Jamaica Apparel and Fashion Industry (JAFI) policy was developed to guide the sector’s development. There was no full implementation of the JAFI plan and its

f a s h i o n a n d a c c e s s o r i e s 9

status is uncertain.

The current Fashion cluster initiative is supported by the JBDC (the national entity for facilitating the development of the fashion industry).

In the past (80’ to early 90’s) there was significant support to the sector, based on the recognition as an employment industry particularly for women. Support ranged from factory space to training including very specialised technical training to ensure that the requisite skills were in place. The level of support has declined significantly as jobs were lost to more cost competitive outsourcing destinations. The decline in support is such that skills were lost as trained persons exited the industry leaving gaps in competencies now required to rebuild it. With the enhancement of the JBDC

there is an injection of support that is very well complemented by the cluster initiative.

Specific activities and initiatives in the sector, such as trade promotion, usually are able to attract support as well. For example both JTI and JBDC usually provide support for trade show participation and Caribbean Fashion Week has been able to obtain support, which is now declining based on support graduation principles.

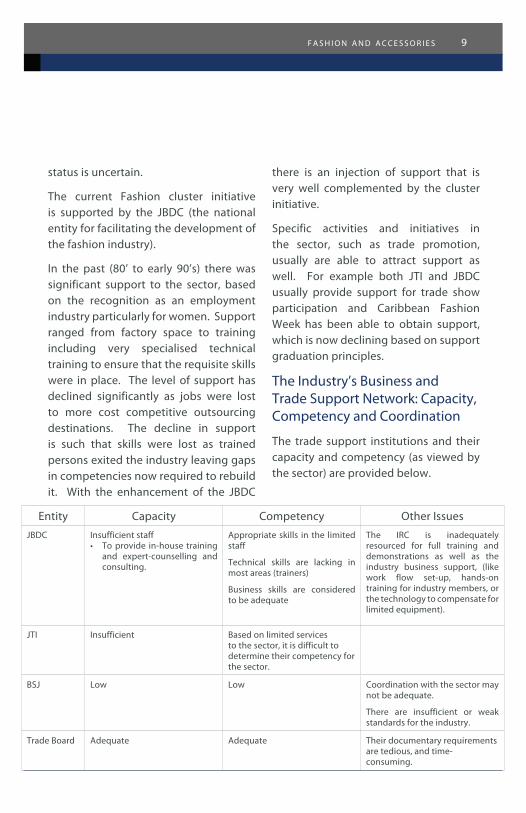

The Industry’s Business and Trade Support Network: Capacity, Competency and Coordination

The trade support institutions and their capacity and competency (as viewed by the sector) are provided below.

Entity Capacity Competency Other IssuesJBDC Insufficient staff

• Toprovide in-house trainingand expert-counselling and consulting.

Appropriate skills in the limited staff

Technical skills are lacking in most areas (trainers)

Business skills are considered to be adequate

The IRC is inadequately resourced for full training and demonstrations as well as the industry business support, (like work flow set-up, hands-on training for industry members, or the technology to compensate for limited equipment).

JTI Insufficient Based on limited services to the sector, it is difficult to determine their competency for the sector.

BSJ Low Low Coordination with the sector may not be adequate.

There are insufficient or weak standards for the industry.

Trade Board Adequate Adequate Their documentary requirements are tedious, and time-consuming.

i n d u s t r y s e c t o r s t r a t e g y

10

In the area of training, there are some weaknesses in addition to fragmentation. The HEART/NTA is the national vocational entity that provides regular training in technical areas to support the fashion and apparel sector (such as garment construction and patternmaking). While the institution trains persons consistently each year, there is no database for professionals or firms to identify them or for a mechanism to view skills and contract persons.

The Edna Manley College offers courses and complementary training in fashion design as well as jewellery design and textiles. UTech also offers a fashion design programme, however there seems to be no clear alignment in the programmes that are offered by each of these institutions.

The level of coordination is not currently at the desired level, however through the efforts of the cluster, this may improve.

The Resource Situation in the Public and Private Sectors (Current and Projected)As alluded to, support has increased recently with the increased resource that was provided to the JBDC and with the support to the fashion Cluster. There is however no additional resources beyond these areas to date. It is expected that with improvements from these additional resources, the sector will be able to advocate for and attract additional resources based on the advancement resulting from the recent resources.

SWOT Analysis of the Sector

Strengths• Strong national brand linked to

creativity.

• Creativeandskilleddesigners.

• Trained pool of workers in garmentconstruction.

• Presence of support institutions(though needs some strengthening).

f a s h i o n a n d a c c e s s o r i e s 11

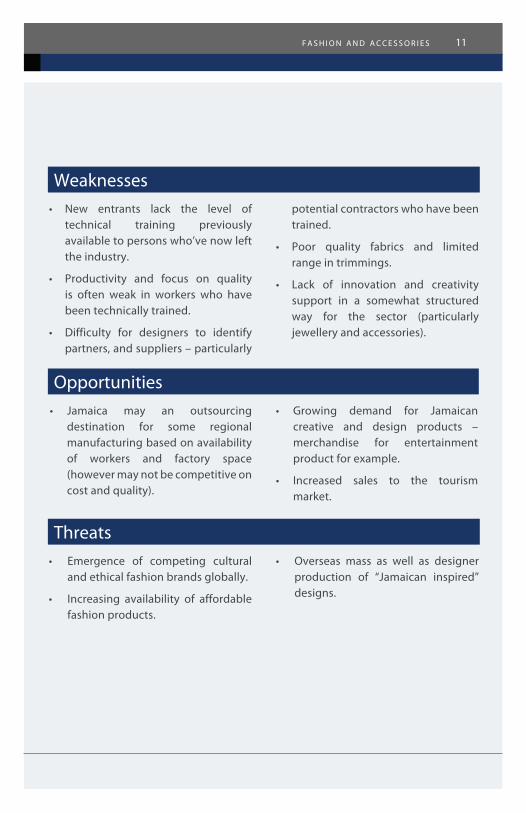

Weaknesses• New entrants lack the level of

technical training previously available to persons who’ve now left the industry.

• Productivity and focus on qualityis often weak in workers who have been technically trained.

• Difficulty for designers to identifypartners, and suppliers – particularly

potential contractors who have been trained.

• Poor quality fabrics and limitedrange in trimmings.

• Lack of innovation and creativitysupport in a somewhat structured way for the sector (particularly jewellery and accessories).

Opportunities• Jamaica may an outsourcing

destination for some regional manufacturing based on availability of workers and factory space (however may not be competitive on cost and quality).

• Growing demand for Jamaicancreative and design products – merchandise for entertainment product for example.

• Increased sales to the tourismmarket.

Threats• Emergence of competing cultural

and ethical fashion brands globally.

• Increasing availability of affordablefashion products.

• Overseas mass as well as designerproduction of “Jamaican inspired” designs.

i n d u s t r y s e c t o r s t r a t e g y

12

The Way Forward(over 3-5 years):The Development Perspective: Developmental Considerations and Priorities

The development priority is to increase employment in the industry by increasing output from the current suite of designers and new entrants. The quality of jobs may also increase based on the formation of new enterprises with the spinoff effects from entrepreneurial ventures that generate more economic activity in business support services and goods. There would be a small contribution to rural and regional development if the option to pursue indigenous products is pursued.

The Competitiveness Perspective

Strategic Consideration #2 – Border-In Issues and Priorities

• Atthefirm-level,thereisinconsistencyin quality and supply of finished products from manufacturers due to:

o Absence in quality control

o Low skills level of staff

o Poor equipment

• Fashion designers not trainedin manufacturing relations and procedures evidenced in absence of specifications sheets given to manufacturers. Also, designers sometimes lack the ability to convert design to product.

• There are challenges in sourcingfabric, particularly the quality and consistency, which is based on limited numbers that suppliers are not typically able to re-order.

• Enterprises in the sector areoften micro-enterprises and have constraints to develop adequate capacity at start-up based on limited funding, and in early stages often are unable to significantly build capacity.

Strategic Consideration #3– Border Issues and Priorities

• Like with other industries issuesinclude:

• Business and trade facilitation(taxation and customs processes)

• Customsbureaucracy

• Complicated export stepswith alot of required paperwork

• Theindustryparticipantsmentioned

f a s h i o n a n d a c c e s s o r i e s 13

high duties on equipment as a constraint; however these firms qualify for incentives under the MOI indicating lack of awareness of support programmes for the sector.

• Highersecurityandelectricitycosts(compared to the region) limit the ability to capitalise on regional outsourcing based on existing worker pool that is available at lower labour costs.

Strategic Consideration #4– Border-Out Issues and Priorities

• Highduties–evenwithinCARICOM– on exports increase export market prices.

The Client Perspective

Strategic Consideration #5– Client Prioritisation: Support Requirements and Response

Industry level considerations need to be addressed to develop the enterprises within the sector, many of which are informal or do not use professional business practices in areas of accounting, contracting, etc. General upgrade to the sector is therefore critical and expands across the exporter categories noted below.

Current Exporters and Other Current Participants in the Value Chain:

Product quality is the first export-ready factor for the sector. Once achieved the firm must have the manufacturing and management capability to be able to pursue and service international sales accounts and meet delivery requirements. Firms able to achieve this are considered export ready.

Potential Exporters and Other Potential Participants in the Value Chain:

Potential exporters are those that have developed a track record, produce international quality goods and have an established business. An example is Uzuri, that has been established in Jamaica and whose potential is now recognised globally (having provided opening costumes for the 2008 Miss World Pageant). In some instances, the brand is demanded. To transition to exporter status the firm must be prepared and resourced to manage international clients and customers and to be able to manage the export logistics.

Aspiring Exporters and Other Aspiring Participants in the Value

i n d u s t r y s e c t o r s t r a t e g y

14

Chain:

An aspiring exporter has the potential to grow a successful domestic business. The enterprise will also have to focus on growing from experiences in the industry.

Implications for Sector Support Services

Strategic Consideration #6– Business Competency

The following are areas for improvements in business competency:

• Costingandpricing

• Developingandcommunicating/presenting manufacturing specifications

• Outsourcingcontractmanagement

• Marketinginthefashionindustry

• Logisticsandsupplychainmanagement

• Businessplanning

• Financialmanagement

The list of competencies appears long based on the nature of the industry: designers as creative persons usually start and manage the businesses and

may not have the necessary business and management training and experience. Based on the scale of operations and challenges in funding/capitalising the enterprise, they are (more often than not) not able to hire such services and so some competency is required until such staff or partners are acquired by the firm. As such, access to group/cluster back-office services providers would be ideal for the industry.

Strategic Consideration #7– Trade Information

The trade information required is similar to the categories and templates identified for other industries: market potential, market entry requirements, distribution channels and potential importer lists.

Strategic Consideration #8 – Finance

A particular finance need for this industry is that of start-up funding and micro-enterprise funding. Typically skilled individuals try to enter the fashion industry. As there are typically no design jobs, they enter the industry as entrepreneurs, many of whom in any event wish to express their own creative point of view. Assistance in developing business plans and proposals to access funds, as well as financial management to ensure success in its use are important gaps to be filled.

f a s h i o n a n d a c c e s s o r i e s 15

Strategic Consideration #9 – Quality Management

Despite being trained, practitioners sometimes bypass the quality steps they are to take, or ignore those given to them by either managers of manufacturing facilities or by designers to whom they are contracted. An attitude that embraces quality is required by the industry to ensure that standards are consistently maintained. Like other areas, a quality culture is essential for firms and the sector.

The industry would also like to see a review of current international standards to see which may be applicable locally on the updating or national standards for the industry and development of new ones.

Please see institutional gaps related to quality that are noted in section 6.4.

Strategic Consideration #10– Other Support Services

Technical competency

• There is an array of technicaltraining programmes, however there is a lack of re-training or upgrading in skills competencies.

• There is an absence of innovationcircles, or mechanism to challenge the participants and foster increased innovation.

The Institutional Perspective

• Thereisnonationalindustryqualitycontrol – such as checks on sizes, fabric types, or accuracy of labels. This may be taken on as a regional initiative to first survey sizes to assist in developing the size standards, and has been proposed.

• No standard job classifications inthe industry: such as seamstresses, pattern-makers, etc. and the institutional support for training and certifying these persons.

• No coordination of the traininginstitutions in the sector (EMC, UTech, UWI, HEART). An audit would be useful to inform coordination, while the University Council is to be consulted for curriculum development and the approval and certification of programmes.

• Thereisanopportunitytostrengthenthe JAF Cluster to be a sustainable entity (to act as the coordinating/ leading industry association).

Strategic Consideration #11– Strengthening the Sector’s Strategy Support Network:

Strategy Coordination and Management:

Structure

i n d u s t r y s e c t o r s t r a t e g y

16

The JAF Cluster is developing an exit strategy to address the sustainability of the cluster initiative at the close of the PSDP. It is proposing the entity support the continued development of the sector, and as such would be the recommended entity for this sector. In terms of the structure of the entity itself, it needs a secretariat staffed fulltime to support the cluster. The cluster will work through the JBDC and JTI to effect policy and would also link into the NES secretariat.

Process (Strategy Monitoring)

The recommended approach is that this be jointly done between the cluster and the JBDC. This PPP structure would work with the Secretariat on monitoring and evaluation.

Strategic Consideration #12– The Sector’s Services Delivery Network

Based on the weaknesses and gaps identified earlier, the most critical service providers need capacity strengthening in order to better serve the industry. In addition to the competency and capacity a service orientation to the client group based on aiding them to achieve their objectives is also important.

s t r a t e g y a t a g l a n c e

f a s h i o n a n d a c c e s s o r i e s 17

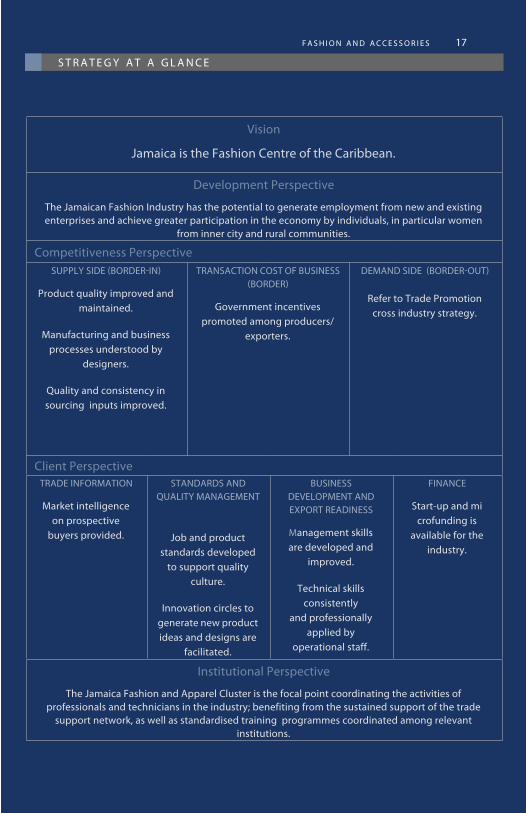

Vision

Jamaica is the Fashion Centre of the Caribbean.

Development Perspective

The Jamaican Fashion Industry has the potential to generate employment from new and existing enterprises and achieve greater participation in the economy by individuals, in particular women

from inner city and rural communities.

Competitiveness PerspectiveSUPPLY SIDE (BORDER-IN)

Product quality improved and maintained.

Manufacturing and business processes understood by

designers.

Quality and consistency in sourcing inputs improved.

TRANSACTION COST OF BUSINESS (BORDER)

Government incentives promoted among producers/

exporters.

DEMAND SIDE (BORDER-OUT)

Refer to Trade Promotion cross industry strategy.

Client PerspectiveTRADE INFORMATION

Market intelligence on prospective

buyers provided.

STANDARDS AND QUALITY MANAGEMENT

Job and product standards developed

to support quality culture.

Innovation circles to generate new product ideas and designs are

facilitated.

BUSINESS DEVELOPMENT AND EXPORT READINESS

Management skills are developed and

improved.

Technical skills consistently

and professionally applied by

operational staff.

FINANCE

Start-up and mi crofunding is

available for the industry.

Institutional Perspective

The Jamaica Fashion and Apparel Cluster is the focal point coordinating the activities of professionals and technicians in the industry; benefiting from the sustained support of the trade

support network, as well as standardised training programmes coordinated among relevant institutions.

18

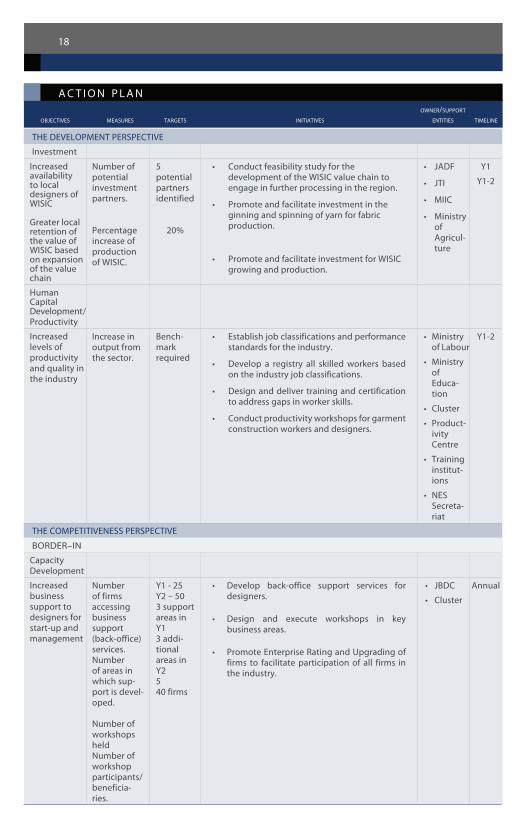

owner/support

objectives measures targets initiatives entities timeline

a c t i o n p l a n

THE DEVELOPMENT PERSPECTIVE

Investment

Increased availability to local designers of WISIC

Greater local retention of the value of WISIC based on expansion of the value chain

Number of potential investment partners.

Percentage increase of production of WISIC.

5 potential partners identified

20%

• Conductfeasibilitystudyforthedevelopment of the WISIC value chain to engage in further processing in the region.

• Promoteandfacilitateinvestmentintheginning and spinning of yarn for fabric production.

• PromoteandfacilitateinvestmentforWISICgrowing and production.

• JADF

• JTI

• MIIC

• Ministryof Agricul-ture

Y1

Y1-2

Human Capital Development / Productivity

Increased levels of productivity and quality in the industry

Increase in output from the sector.

Bench-mark required

• Establishjobclassificationsandperformancestandards for the industry.

• Develop a registry all skilledworkers basedon the industry job classifications.

• Designanddelivertrainingandcertificationto address gaps in worker skills.

• Conductproductivityworkshopsforgarmentconstruction workers and designers.

• Ministryof Labour

• Ministryof Educa-tion

• Cluster

• Product-ivity Centre

• Traininginstitut-ions

• NESSecreta-riat

Y1-2

THE COMPETITIVENESS PERSPECTIVE

BORDER–IN

Capacity Development

Increased business support to designers for start-up and management

Number of firms accessing business support (back-office) services.Number of areas in which sup-port is devel-oped.

Number of workshops heldNumber of workshop participants/ beneficia-ries.

Y1 - 25Y2 – 503 support areas in Y13 addi-tional areas in Y2540 firms

• Develop back-office support services fordesigners.

• Design and execute workshops in keybusiness areas.

• PromoteEnterpriseRatingandUpgradingoffirms to facilitate participation of all firms in the industry.

• JBDC

• Cluster

Annual

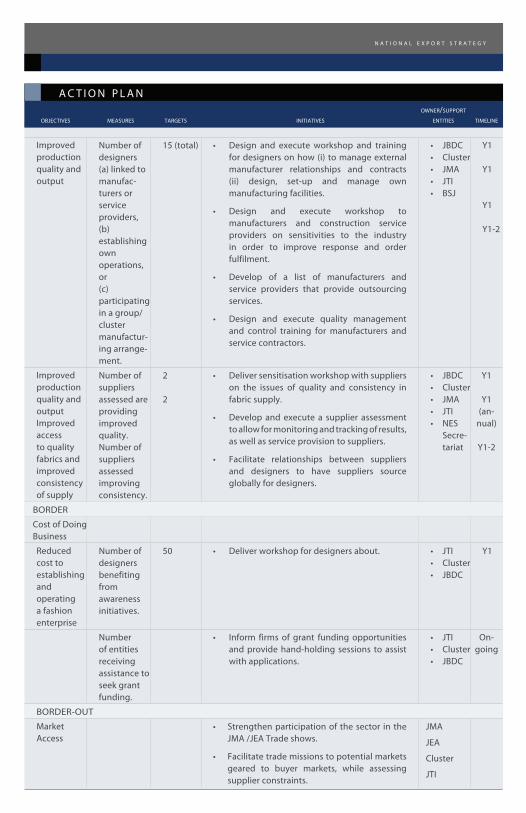

n a t i o n a l e x p o r t s t r a t e g y 19

a c t i o n p l a n owner/support

objectives measures targets initiatives entities timeline

Improved production quality and output

Number of designers (a) linked to manufac-turers or service providers, (b) establishing own operations, or(c) participating in a group/cluster manufactur-ing arrange-ment.

15 (total) • Design and execute workshop and trainingfor designers on how (i) to manage external manufacturer relationships and contracts (ii) design, set-up and manage own manufacturing facilities.

• Design and execute workshop tomanufacturers and construction service providers on sensitivities to the industry in order to improve response and order fulfilment.

• Develop of a list of manufacturers andservice providers that provide outsourcing services.

• Design and execute quality managementand control training for manufacturers and service contractors.

• JBDC• Cluster• JMA• JTI• BSJ

Y1

Y1

Y1

Y1-2

Improved production quality and output Improved access to quality fabrics and improved consistency of supply

Number of suppliers assessed are providing improved quality.Number of suppliers assessed improving consistency.

2

2

• Deliversensitisationworkshopwithsupplierson the issues of quality and consistency in fabric supply.

• Developandexecutea supplier assessmentto allow for monitoring and tracking of results, as well as service provision to suppliers.

• Facilitate relationships between suppliersand designers to have suppliers source globally for designers.

• JBDC• Cluster• JMA• JTI• NES

Secre-tariat

Y1

Y1(an-

nual)

Y1-2

BORDER

Cost of Doing Business

Reduced cost to establishing and operating a fashion enterprise

Number of designers benefiting from awareness initiatives.

50 • Deliverworkshopfordesignersabout. • JTI• Cluster• JBDC

Y1

Number of entities receiving assistance to seek grant funding.

• Inform firmsof grant fundingopportunitiesand provide hand-holding sessions to assist with applications.

• JTI• Cluster• JBDC

On-going

BORDER-OUT

Market Access

• Strengthenparticipationof thesector intheJMA /JEA Trade shows.

• Facilitatetrademissionstopotentialmarketsgeared to buyer markets, while assessing supplier constraints.

JMA

JEA

Cluster

JTI

20

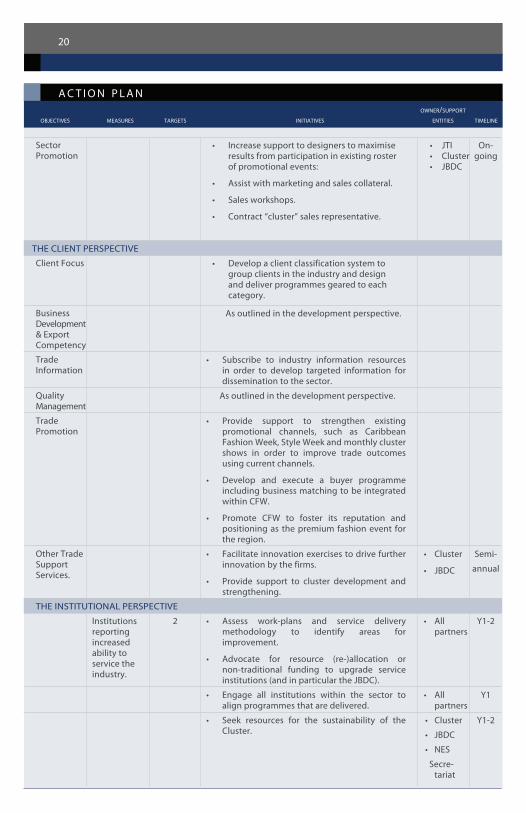

a c t i o n p l a n owner/support

objectives measures targets initiatives entities timeline

Sector Promotion

• Increasesupporttodesignerstomaximiseresults from participation in existing roster of promotional events:

• Assistwithmarketingandsalescollateral.

• Salesworkshops.

• Contract“cluster”salesrepresentative.

• JTI• Cluster• JBDC

On-going

THE CLIENT PERSPECTIVE

Client Focus • Developaclientclassificationsystemtogroup clients in the industry and design and deliver programmes geared to each category.

Business Development & Export Competency

As outlined in the development perspective.

Trade Information

• Subscribe to industry information resourcesin order to develop targeted information for dissemination to the sector.

Quality Management

As outlined in the development perspective.

Trade Promotion

• Provide support to strengthen existingpromotional channels, such as Caribbean Fashion Week, Style Week and monthly cluster shows in order to improve trade outcomes using current channels.

• Develop and execute a buyer programmeincluding business matching to be integrated within CFW.

• Promote CFW to foster its reputation andpositioning as the premium fashion event for the region.

Other Trade Support Services.

• Facilitateinnovationexercisestodrivefurtherinnovation by the firms.

• Provide support to cluster development andstrengthening.

• Cluster

• JBDC

Semi-

annual

THE INSTITUTIONAL PERSPECTIVE

Institutions reporting increased ability to service the industry.

2 • Assess work-plans and service deliverymethodology to identify areas for improvement.

• Advocate for resource (re-)allocation ornon-traditional funding to upgrade service institutions (and in particular the JBDC).

• Allpartners

Y1-2

• Engage all institutions within the sector toalign programmes that are delivered.

• Allpartners

Y1

• Seek resources for the sustainability of theCluster.

• Cluster

• JBDC

• NES

Secre-tariat

Y1-2

f a s h i o n a n d a c c e s s o r i e s 21

owner/support

objectives measures targets initiatives entities timeline

4 p r i o r i t y i n d u s t r y s t r a t e g i e s

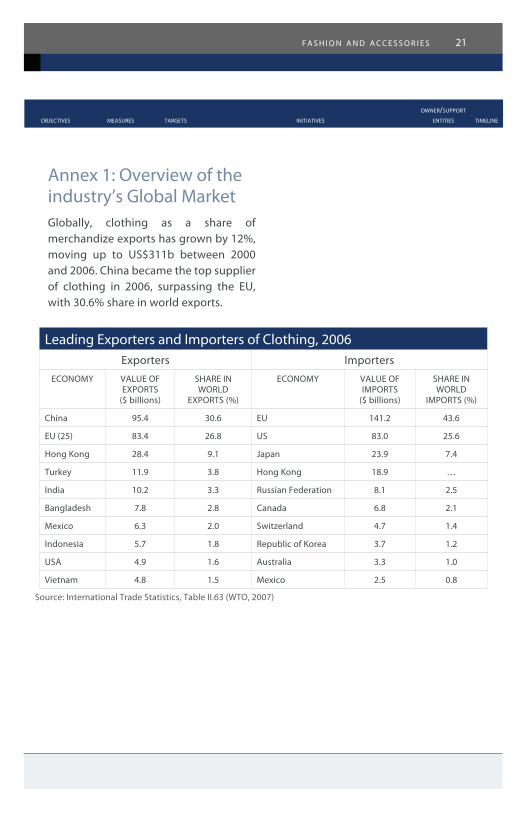

Annex 1: Overview of the industry’s Global MarketGlobally, clothing as a share of merchandize exports has grown by 12%, moving up to US$311b between 2000 and 2006. China became the top supplier of clothing in 2006, surpassing the EU, with 30.6% share in world exports.

Leading Exporters and Importers of Clothing, 2006Exporters Importers

ECONOMY VALUE OF EXPORTS

($ billions)

SHARE IN WORLD

EXPORTS (%)

ECONOMY VALUE OF IMPORTS

($ billions)

SHARE IN WORLD

IMPORTS (%)

China 95.4 30.6 EU 141.2 43.6

EU (25) 83.4 26.8 US 83.0 25.6

Hong Kong 28.4 9.1 Japan 23.9 7.4

Turkey 11.9 3.8 Hong Kong 18.9 …

India 10.2 3.3 Russian Federation 8.1 2.5

Bangladesh 7.8 2.8 Canada 6.8 2.1

Mexico 6.3 2.0 Switzerland 4.7 1.4

Indonesia 5.7 1.8 Republic of Korea 3.7 1.2

USA 4.9 1.6 Australia 3.3 1.0

Vietnam 4.8 1.5 Mexico 2.5 0.8

Source: International Trade Statistics, Table II.63 (WTO, 2007)

4 International Trade Statistics, 2006 (International Trade Centre, 2008).5 The Interior category includes items such as furniture, tableware, wallpaper, glassware, porcelain, and lighting sets. The Fashion category includes handbags, belts, accessories such as ties, shawls, scarves, gloves, hats etc), sunglasses, headgear, lea ther goods and perfume. Jewelry and toys were the other top four exports. 6 The Creative Economy Report (UNCTAD, 2007).

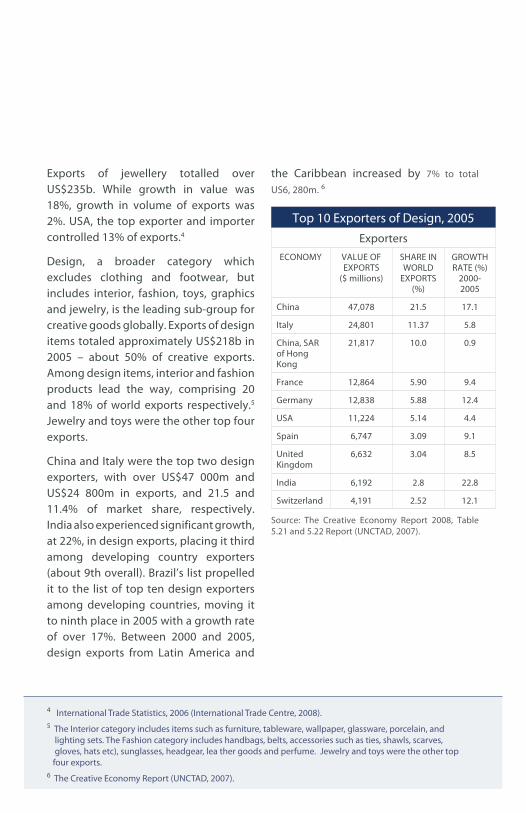

Exports of jewellery totalled over US$235b. While growth in value was 18%, growth in volume of exports was 2%. USA, the top exporter and importer controlled 13% of exports.4

Design, a broader category which excludes clothing and footwear, but includes interior, fashion, toys, graphics and jewelry, is the leading sub-group for creative goods globally. Exports of design items totaled approximately US$218b in 2005 – about 50% of creative exports. Among design items, interior and fashion products lead the way, comprising 20 and 18% of world exports respectively.5 Jewelry and toys were the other top four exports.

China and Italy were the top two design exporters, with over US$47 000m and US$24 800m in exports, and 21.5 and 11.4% of market share, respectively. India also experienced significant growth, at 22%, in design exports, placing it third among developing country exporters (about 9th overall). Brazil’s list propelled it to the list of top ten design exporters among developing countries, moving it to ninth place in 2005 with a growth rate of over 17%. Between 2000 and 2005, design exports from Latin America and

the Caribbean increased by 7% to total

US6, 280m. 6

Top 10 Exporters of Design, 2005Exporters

ECONOMY VALUE OF EXPORTS

($ millions)

SHARE IN WORLD

EXPORTS (%)

GROWTH RATE (%)

2000-2005

China 47,078 21.5 17.1

Italy 24,801 11.37 5.8

China, SAR of Hong Kong

21,817 10.0 0.9

France 12,864 5.90 9.4

Germany 12,838 5.88 12.4

USA 11,224 5.14 4.4

Spain 6,747 3.09 9.1

United Kingdom

6,632 3.04 8.5

India 6,192 2.8 22.8

Switzerland 4,191 2.52 12.1

Source: The Creative Economy Report 2008, Table 5.21 and 5.22 Report (UNCTAD, 2007).

w w w . j a m a i c a t r a d e a n d i n v e s t . o r g / n e s | 1 - 8 8 8 - 4 2 9 - 5 N E S ( 1 - 8 8 8 - 4 2 9 - 5 6 3 7 )