Embed Size (px)

Citation preview

THE GLOBAL ANALYST | JANUARY 2014

1

What’s in Store?

January 2014 A Business & Finance Monthly Rs.100

www.theglobalanalyst.co

2014

January - 2014 - TGA.indd 1 30-12-2013 AM 10:51:25

THE GLOBAL ANALYST | JANUARY 20142

January - 2014 - TGA.indd 2 30-12-2013 AM 10:51:25

THE GLOBAL ANALYST | JANUARY 2014

3

It won’t require one much effort to single out the most significant development of the year 2013, which not only hogged limelight in India, but

was noticed by the rest of the world as well. No points for guessing: it’s been the amazing ascent of the AAP or the Aam Admi Party, which came into existence after its anti-corruption campaigns over the last one year received overwhelming response from the public. According to Stanford Graduate School of Business, corruption, which may take many forms such as embezzlement, graft, bribery or extortion, leads to a diminished business environment when the public trust is put at risk. Look no further than the stock market where retail investors’ participation remains in the low single digit, despite the fact that the country boasts of a long history of equity investment, and that the BSE has the distinction of being the oldest stock exchange in Asia. Despite a series of path-breaking reforms carried out by the government since 1991-92 and commendable job done by the market regulator SEBI, issues like insider trading, weak/poor governance, accounting shenanigan, etc., have continued to weigh on prospective investors’, particularly retail investors’, minds. “Recent spate of scams like Satyam, 2G and coal allocation scam to name a few has robbed retail investors of the confidence to invest continually,” said a report in the Business Standard.

EDITORIAL

editorD Nagavender Rao

managing editorN Janardhan Rao

editorial directorAmit Singh Sisodiyaadvisory board

Dr. Paritosh Basu, Former Group Controller, Essar Group

N Harinath Reddy, Advocate & Senior Partner, H&B Law Offices, Hyderabad

Sanjay Banka, Chief Financial OfficerLandmark Group, Saudi Arabia

Prashant Gupta, IIT-K, IIM-LCEO - Edunirvana

Dr David Wyss, Former Chief Economist,S&P & Visiting Fellow, Watson Institute at

Brown University. NY, US

Dean Baker, Economist and Co-founder Center for Economic and Policy, Washington, US

William Gamble, President, Emerging Market Strategies, US

Andrew K P Leung, International and Independent China, Specialist at Andrew

Leung International Consultants, Hong Kong

M G Warrier, Former GM, RBI

research teamM S V Subba Rao, Manager - Strategy & ResearchAnjaneya Naga Sai Prashanth Vijaya Lakshmi, Amita Singh, Naga Lakshmi, GV Tarun, Masthan Rao, Veera Swamy & Nagaswara Rao n ©All rights reserved. No part of this

publication may be reproduced or copied in any form by any means without prior written permission.

n The views expressed in this publication are purely personal judgements of the authors and do not reflect the views of Media Five Publications (P) Ltd.

n The views expressed by outside contributors represent their personal views and do not necessarily the views of the organizations they represent.

n All efforts are made to ensure that the published information is correct. Media Five Publications is not responsible for any errors caused due to oversight or otherwise.

Published & Edited by D Nagavender Rao

January 2014 Vol. 3 | No.1

Pehle ‘AAP’ A New Dawn!

Can the Delhi Drama that unfolded post-December 8, which finally culminated in the installation of the anti-corruption crusader Arvind Kejariwal-led Aam Admi Party’s (AAP) government in Delhi, act as a trigger for the corporate sector to launch similar efforts to fight corruption, improve governance, and, importantly, rebuild trust?

January - 2014 - TGA.indd 3 30-12-2013 AM 10:51:26

THE GLOBAL ANALYST | JANUARY 20144

Chief ExcutiveSyed H Maqsood

Director - MarketingDavid Wilson

Sales Head – MumbaiFreeda Bhati

098330 14501 | [email protected]

Sales Head – ChennaiEmmanuel Rozario

098844 91851 | [email protected]

Sales Head – jnew DelhiSonika Raina

098111 00227 | [email protected]

SUBSCRIPTIONPayment to be made by crossed Cheque/DD drawn in favor of

“MEDIA FIVE PUBLICATIONS (P) LTD.” Payable at Hyderabad.

KNOWLEDGE PARTNERTarget Research & Consulting

ADVERTISEMENT ENQUIRIES

Media Five Publications (P) Ltd.#302, Kautilya Complex, 6-3-652, Beside Medinova, Somajiguda, Hyderabad - 82Andhra Pradesh, IndiaCell: +91- 9247 769 383 | 988 545 1717

SEND YOUR FEEDBACK/ARTICLES TOThe Editor, The Global ANALYST

Submit through our website - www.theglobalanalyst.co

COVER PRICE : Rs. 100/-

subscriptions detailsBy Post By Courier

1 Year (12 Issues) Rs. 1200/- Rs. 1700/-

2 Years (24 Issues) Rs. 2400/- Rs. 3400/-

overseas subscriptions1 Year (12 Issues) $ 180

2 Years (24 Issues) $ 330

design & layout - Creative Graphics Designers WEB DESIGNERS - Y L Narayana Theerdha, Team Leader, K Krishna Reddy, Krishna ChaitanyaPrinted at Sai Kiran Graphics, RTC ‘X’ Roads, Hyderabad-20. Published on behalf of Media Five Publications (P) Ltd, #302, Kautalya Complex, 6-3-652, Beside Medinova, Somajiguda, Hyderabad - 500082, Andhra Pradesh (India).

www.theglobalanalyst.co

This is also reflected in the fact that IPO market in India registered a turnover of just Rs.16bn in 2013 (until November), the lowest in the last five years since 2009. Industry experts and analysts blame it on unscrupulous promoters and their shady investment advisors. Besides, lack of transparency in reporting, instances of companies ignoring interest of minority shareholders, lack of adequate representation of women executives on the board of directors, lack of suitable policies to promote workforce diversity and inclusion, lack of a framework to support a culture of ethical behavior, indifference to environmental related issues, lack of policies to promote CSR activities and philanthropy, etc., have emerged as some of the key concerns among investors. The rise of activist shareholders has further increased the pressure on corporate sector. In essence, it’s no longer enough to earn profits and boost the bottom line – rather, it’s now more about how does a corporate earn its profits (ethically), and also about creating wealth not just for the shareholders, but also for other stakeholders such as employees, customers, and society at large. Can AAP model be replicated in the corporate sector too? The AAP phenomena offers many a valuable lessons in market penetration, consumer-connect strategy, how to devise a solid USP, and, importantly empowerment of all the stakeholders. Shareholder activism, a phenomenon that has been gaining ground in the west underlines the need to emphasize on wealth creation for not just the promoters, but also for the non-promoting shareholders. Can we take it a little further and ask for stakeholder wealth creation also? Maybe it’s time to embrace the culture of Pehle Aap (after you), where stakeholders’ interest takes precedence over those of promoters?Let’s usher in the New Year, hoping for the change - for a better tomorrow!

Amit Singh Sisodiya

January 2014 Vol. 3 | No.1

Media Five Publications (P) Ltd

January - 2014 - TGA.indd 4 30-12-2013 AM 10:51:26

THE GLOBAL ANALYST | JANUARY 2014

5

l ATM card with No Annual Maintenance Fee

l Add on Card

l Mobile Banking

l SMS Alerts

l Auto sweep facility

l NEFT facility upto `1 lacl Demand Drafts upto a max. `50,000* per month

FREE

*Conditions Apply

SBH SMART SALARYACCOUNT

E-mail: [email protected] | visit: www.sbhyd.com Call 1800 425 4055 or sms ‘CALLME’ to 9000 222 444

**Offer valid from 15.11.2013 to 31.01.2014 only

l Personal Accident Insurance upto `2 lacs**l 0.25% OFF on Processing Fee of Personal Loans**

Overdraft Facility Available

January - 2014 - TGA.indd 5 30-12-2013 AM 10:51:28

THE GLOBAL ANALYST | JANUARY 20146

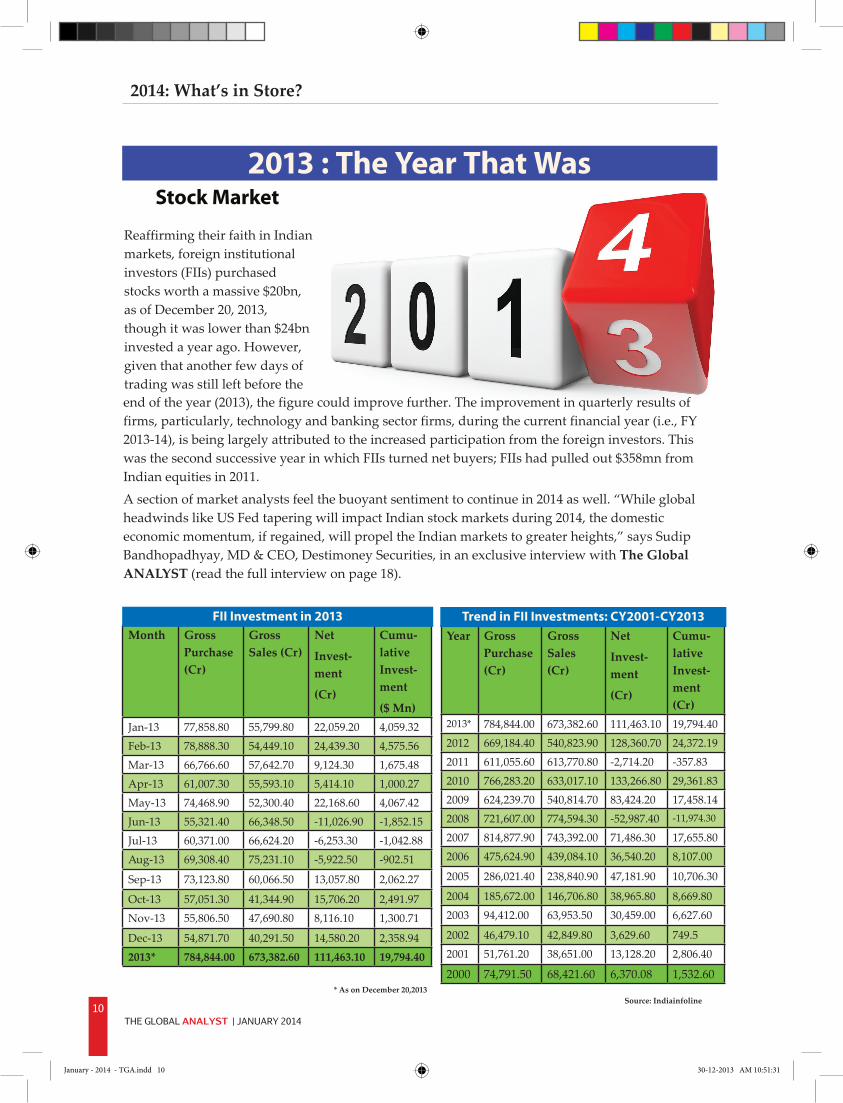

Reaffirming their faith in Indian markets, foreign institutional investors (FIIs) purchased stocks worth a massive $20bn, as of December 20, 2013, though it was lower than $24bn invested a year ago. However, given that another few days of trading was still left before the end of the year (2013), the figure could improve further.

The improvement in quarterly results of firms, particularly, technology and banking sector firms, during the current financial year (i.e., FY 2013-14), is being largely attributed to the increased participation from the foreign investors. This was the second successive year in which FIIs turned net buyers; FIIs had pulled out $358mn from Indian equities in 2011. The billion dollar question is - whether foreign investors would continue to be bullish on India. And, can Indian economy regain its growth momentum? What’s in Store in 2014 for the economy, and also, India Inc?

What’s in Store...........11

09 Kick-starting the Economy - Chalenges before India Derek M. Scissors, Resident Scholar, American Enterprise Institute

(AEI), & an Adjunct Professor, George Washington University.

Exclusive INERVIEWS

Contents

THE GLOBAL ANALYST | JANUARY 2014

1

What’s in Store?

January 2014 A Business & Finance Monthly Rs.100

www.theglobalanalyst.co

2014

18 Stock Market What’s in store in 2014?

Sudip Bandyopadhyay, MD & CEO Destimoney, Securities, Mumbai.

32 CEO Speak Sunil Raisoni, Chairman

The Raisoni Group of Institutions, Nagpur.

40 CFO Speak Bhairav Kothari, Founder & Managing Director

SuperCFO Services, Mumbai.

43 Start-up XpressRaghav Khosla, Managing Director

SKYRA Professional Equipment, New Delhi.

January - 2014 - TGA.indd 6 30-12-2013 AM 10:51:30

THE GLOBAL ANALYST | JANUARY 2014

7

BUSINESS ENVIRONMENT

09 Kick-starting the Economy - Challenges before India

India needs a fundamental shift in either land, labor or taxation. Someone must have the vision and cour-age to make a fundamental change, not to make mi-nor changes and pretend they are sufficient.

14 Infrastructure Sector in 2014 - What’s in Store?A separate ministry for infrastructure would help to pro-vide special attention and be catalyst to the entire process of recovery, says Moses Harding, Group CEO & Chief Economist, Srei Infrastructure Finance Ltd, Kolkata.

16 Indian Real Estate - Tough Times, but a Resil-ient Market India’s real estate market is definitely experiencing its own share of turmoil, but the pain is not wasted - ev-ery market must undergo pain in the process of matur-ing. Cyclical highs and lows apart, I am convinced that Indian real estate’s best times are yet to come. - - Colin Dyer, President & CEO, Jones Lang LaSalle Inc. 27 Retail Sector Dead space management is going to play a crucial role in achieving mall developers’ economic goals, as well as in rejuvenating mall space for the introduc-tion of newer categories and brands,

52 Reviving Agriculture - How Innovation can play a roleThough the government has been doing some modi-cum green activity, it is now time to spearhead mas-sive innovation and roll out initiatives that would revive agriculture its fading glory and help the In-dian and the global community lead a healthy and nutritious life..SPOTLIGHT

20 Microfinance - Failed, so what do we do now?

One can only hope that India’s policy-makers, in-cluding Raghuram Rajan at the RBI, will reflect more deeply on the related failures of microfinance and the neoliberal/Chicago School ‘efficientmarket’ de-velopment model, and firmly commit to a carefully designed and adequately financed institution-led re-sponse to India’s pressing development and growth problems, reckons Dr. Milford Bateman, an interna-tional expert on Microfinance.

MANAGEMENT EDUCATION

24 Nurturing Tomorrow’s Business Leaders, To-day - What it Takes?

Business schools need to ensure that their students are engaging both with leading thinking from the academic realm and with leading practice, avers Brian Moriarty, Adjunct Professor of Management Communications, Darden Graduate School of Busi-ness & Director, Business Roundtable Institute for Corporate Ethics, Virginia, US.

SOCIAL INFRASTRUCTURE

28 Building Sustainable Social Infrastructure - In-novative Delivery Solutions Hold Key

After two decades of liberalization, modern India has emerged as a land of several contradictions. Is-lands of excellence and prosperity are afloat amid the vast seas of mediocrity and also-rans. These ‘is-lands’ are particularly visible in the areas of Health-care, Education and Housing the social sector, pri-mary responsibility of providing which lies with the Government/ public sector.

FINANCIAL MARKETS

18 Stock Markets - What’s in Store?

38 Mutual Funds

40 ENTREPRENEURSHIP DEVELOPMENTStartp-up Xpress: SKYRA Professional Equipment

BANKING SECTOR

46 Mounting Non-Performing Assets - Who’s Footing the Bill?

It is comforting to find that there has been aware-ness at the highest level about the need for quick remedial action to contain NPAs, says M G Warrier, former General Manager, Reserve Bank of India.

REGULARS 03 Editorial12 Digiatal ANALYST 36 Merger mania fades in 2013 51 Webinar Calender - January 201458 Career Planning - 4 Step Planning Process60 Bookshelf 62 Business IQ

January - 2014 - TGA.indd 7 30-12-2013 AM 10:51:30

THE GLOBAL ANALYST | JANUARY 20148

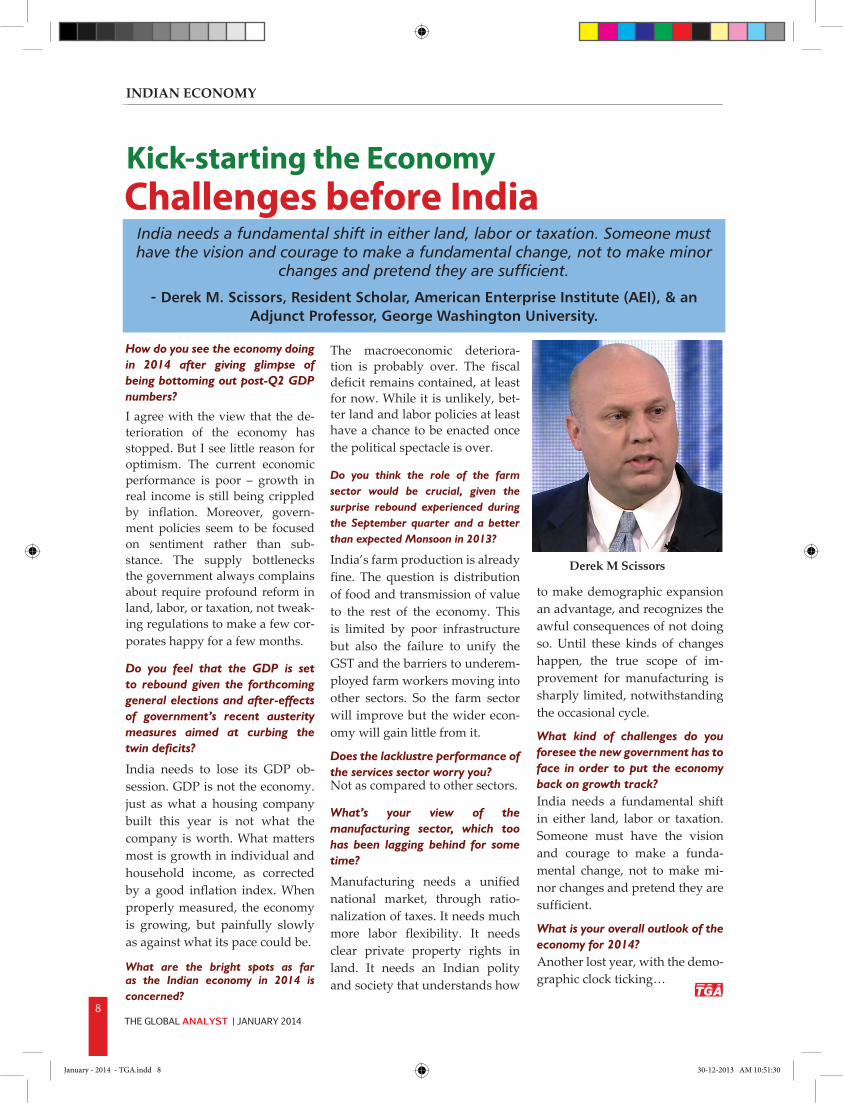

Challenges before India Kick-starting the Economy

India needs a fundamental shift in either land, labor or taxation. Someone must have the vision and courage to make a fundamental change, not to make minor

changes and pretend they are sufficient.

- Derek M. Scissors, Resident Scholar, American Enterprise Institute (AEI), & an Adjunct Professor, George Washington University.

How do you see the economy doing in 2014 after giving glimpse of being bottoming out post-Q2 GDP numbers?

I agree with the view that the de-terioration of the economy has stopped. But I see little reason for optimism. The current economic performance is poor – growth in real income is still being crippled by inflation. Moreover, govern-ment policies seem to be focused on sentiment rather than sub-stance. The supply bottlenecks the government always complains about require profound reform in land, labor, or taxation, not tweak-ing regulations to make a few cor-porates happy for a few months.

Do you feel that the GDP is set to rebound given the forthcoming general elections and after-effects of government’s recent austerity measures aimed at curbing the twin deficits?

India needs to lose its GDP ob-session. GDP is not the economy. just as what a housing company built this year is not what the company is worth. What matters most is growth in individual and household income, as corrected by a good inflation index. When properly measured, the economy is growing, but painfully slowly as against what its pace could be.

What are the bright spots as far as the Indian economy in 2014 is concerned?

The macroeconomic deteriora-tion is probably over. The fiscal deficit remains contained, at least for now. While it is unlikely, bet-ter land and labor policies at least have a chance to be enacted once the political spectacle is over.

Do you think the role of the farm sector would be crucial, given the surprise rebound experienced during the September quarter and a better than expected Monsoon in 2013?

India’s farm production is already fine. The question is distribution of food and transmission of value to the rest of the economy. This is limited by poor infrastructure but also the failure to unify the GST and the barriers to underem-ployed farm workers moving into other sectors. So the farm sector will improve but the wider econ-omy will gain little from it.

Does the lacklustre performance of the services sector worry you?Not as compared to other sectors.

What’s your view of the manufacturing sector, which too has been lagging behind for some time?

Manufacturing needs a unified national market, through ratio-nalization of taxes. It needs much more labor flexibility. It needs clear private property rights in land. It needs an Indian polity and society that understands how

to make demographic expansion an advantage, and recognizes the awful consequences of not doing so. Until these kinds of changes happen, the true scope of im-provement for manufacturing is sharply limited, notwithstanding the occasional cycle.

What kind of challenges do you foresee the new government has to face in order to put the economy back on growth track?India needs a fundamental shift in either land, labor or taxation. Someone must have the vision and courage to make a funda-mental change, not to make mi-nor changes and pretend they are sufficient.

What is your overall outlook of the economy for 2014?Another lost year, with the demo-graphic clock ticking…

Derek M Scissors

INDIAN ECONOMY

January - 2014 - TGA.indd 8 30-12-2013 AM 10:51:30

THE GLOBAL ANALYST | JANUARY 2014

9

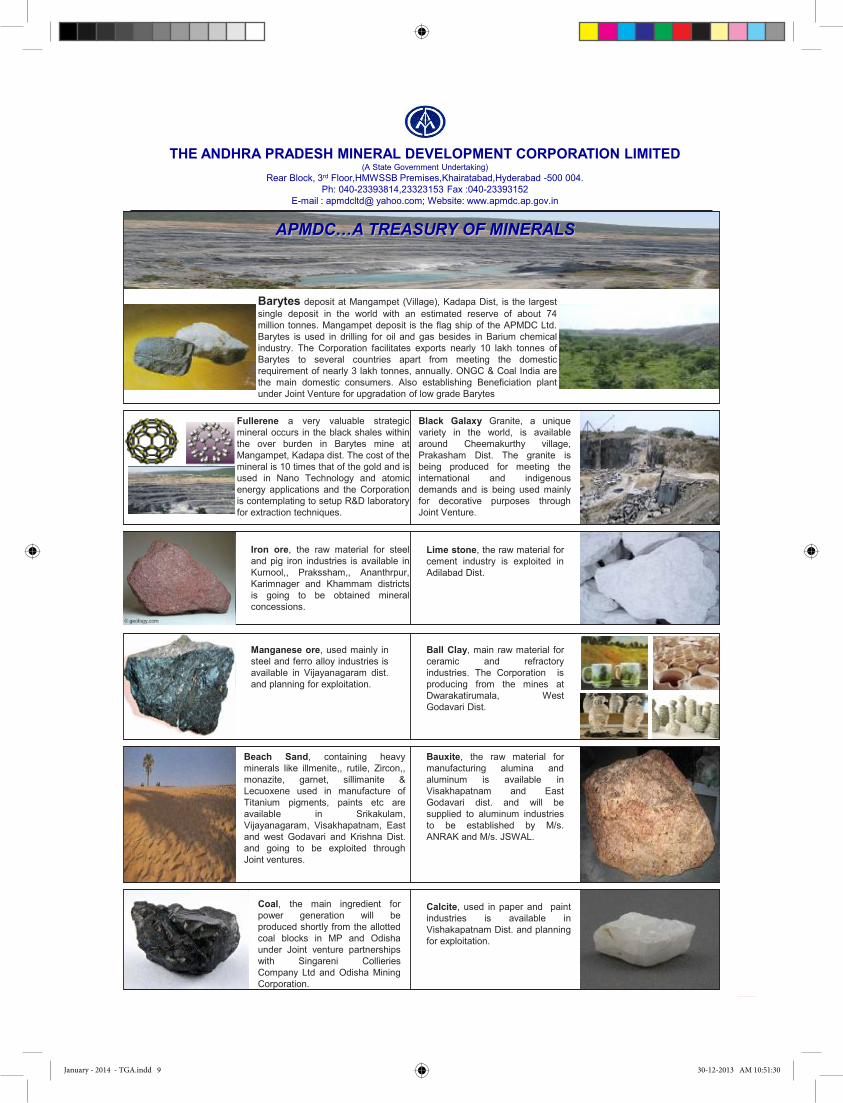

THE ANDHRA PRADESH MINERAL DEVELOPMENT CORPORATION LIMITED(A State Government Undertaking)

Rear Block, 3rd Floor,HMWSSB Premises,Khairatabad,Hyderabad -500 004.Ph: 040-23393814,23323153 Fax :040-23393152

E-mail : apmdcltd@ yahoo.com; Website: www.apmdc.ap.gov.in

Black Galaxy Granite, a uniquevariety in the world, is availablearound Cheemakurthy village,Prakasham Dist. The granite isbeing produced for meeting theinternational and indigenousdemands and is being used mainlyfor decorative purposes throughJoint Venture.

Fullerene a very valuable strategicmineral occurs in the black shales withinthe over burden in Barytes mine atMangampet, Kadapa dist. The cost of themineral is 10 times that of the gold and isused in Nano Technology and atomicenergy applications and the Corporationis contemplating to setup R&D laboratoryfor extraction techniques.

Barytes deposit at Mangampet (Village), Kadapa Dist, is the largestsingle deposit in the world with an estimated reserve of about 74million tonnes. Mangampet deposit is the flag ship of the APMDC Ltd.Barytes is used in drilling for oil and gas besides in Barium chemicalindustry. The Corporation facilitates exports nearly 10 lakh tonnes ofBarytes to several countries apart from meeting the domesticrequirement of nearly 3 lakh tonnes, annually. ONGC & Coal India arethe main domestic consumers. Also establishing Beneficiation plantunder Joint Venture for upgradation of low grade Barytes

APMDC…A TREASURY OF MINERALS

Manganese ore, used mainly insteel and ferro alloy industries isavailable in Vijayanagaram dist.and planning for exploitation.

Ball Clay, main raw material forceramic and refractoryindustries. The Corporation isproducing from the mines atDwarakatirumala, WestGodavari Dist.

Beach Sand, containing heavyminerals like illmenite,, rutile, Zircon,,monazite, garnet, sillimanite &Lecuoxene used in manufacture ofTitanium pigments, paints etc areavailable in Srikakulam,Vijayanagaram, Visakhapatnam, Eastand west Godavari and Krishna Dist.and going to be exploited throughJoint ventures.

Bauxite, the raw material formanufacturing alumina andaluminum is available inVisakhapatnam and EastGodavari dist. and will besupplied to aluminum industriesto be established by M/s.ANRAK and M/s. JSWAL.

Iron ore, the raw material for steeland pig iron industries is available inKurnool,, Prakssham,, Ananthrpur,Karimnager and Khammam districtsis going to be obtained mineralconcessions.

Lime stone, the raw material forcement industry is exploited inAdilabad Dist.

Coal, the main ingredient forpower generation will beproduced shortly from the allottedcoal blocks in MP and Odishaunder Joint venture partnershipswith Singareni CollieriesCompany Ltd and Odisha MiningCorporation.

Calcite, used in paper and paintindustries is available inVishakapatnam Dist. and planningfor exploitation.

January - 2014 - TGA.indd 9 30-12-2013 AM 10:51:30

THE GLOBAL ANALYST | JANUARY 201410

Stock Market

Reaffirming their faith in Indian markets, foreign institutional investors (FIIs) purchased stocks worth a massive $20bn, as of December 20, 2013, though it was lower than $24bn invested a year ago. However, given that another few days of trading was still left before the

2013 : The Year That Was

end of the year (2013), the figure could improve further. The improvement in quarterly results of firms, particularly, technology and banking sector firms, during the current financial year (i.e., FY 2013-14), is being largely attributed to the increased participation from the foreign investors. This was the second successive year in which FIIs turned net buyers; FIIs had pulled out $358mn from Indian equities in 2011.

A section of market analysts feel the buoyant sentiment to continue in 2014 as well. “While global headwinds like US Fed tapering will impact Indian stock markets during 2014, the domestic economic momentum, if regained, will propel the Indian markets to greater heights,” says Sudip Bandhopadhyay, MD & CEO, Destimoney Securities, in an exclusive interview with The Global ANALYST (read the full interview on page 18).

Year Gross Purchase (Cr)

Gross Sales (Cr)

Net

Invest-ment

(Cr)

Cumu-lative Invest-ment (Cr)

2013* 784,844.00 673,382.60 111,463.10 19,794.402012 669,184.40 540,823.90 128,360.70 24,372.192011 611,055.60 613,770.80 -2,714.20 -357.832010 766,283.20 633,017.10 133,266.80 29,361.832009 624,239.70 540,814.70 83,424.20 17,458.142008 721,607.00 774,594.30 -52,987.40 -11,974.30

2007 814,877.90 743,392.00 71,486.30 17,655.802006 475,624.90 439,084.10 36,540.20 8,107.00

2005 286,021.40 238,840.90 47,181.90 10,706.30

2004 185,672.00 146,706.80 38,965.80 8,669.802003 94,412.00 63,953.50 30,459.00 6,627.60

2002 46,479.10 42,849.80 3,629.60 749.52001 51,761.20 38,651.00 13,128.20 2,806.40

2000 74,791.50 68,421.60 6,370.08 1,532.60

Month Gross Purchase (Cr)

Gross Sales (Cr)

Net

Invest-ment

(Cr)

Cumu-lative Invest-ment

($ Mn)Jan-13 77,858.80 55,799.80 22,059.20 4,059.32Feb-13 78,888.30 54,449.10 24,439.30 4,575.56Mar-13 66,766.60 57,642.70 9,124.30 1,675.48Apr-13 61,007.30 55,593.10 5,414.10 1,000.27May-13 74,468.90 52,300.40 22,168.60 4,067.42Jun-13 55,321.40 66,348.50 -11,026.90 -1,852.15Jul-13 60,371.00 66,624.20 -6,253.30 -1,042.88Aug-13 69,308.40 75,231.10 -5,922.50 -902.51

Sep-13 73,123.80 60,066.50 13,057.80 2,062.27

Oct-13 57,051.30 41,344.90 15,706.20 2,491.97Nov-13 55,806.50 47,690.80 8,116.10 1,300.71

Dec-13 54,871.70 40,291.50 14,580.20 2,358.942013* 784,844.00 673,382.60 111,463.10 19,794.40

FII Investment in 2013

2014: What’s in Store?

* As on December 20,2013

Trend in FII Investments: CY2001-CY2013

Source: Indiainfoline

January - 2014 - TGA.indd 10 30-12-2013 AM 10:51:31

THE GLOBAL ANALYST | JANUARY 2014

11

Stock Market

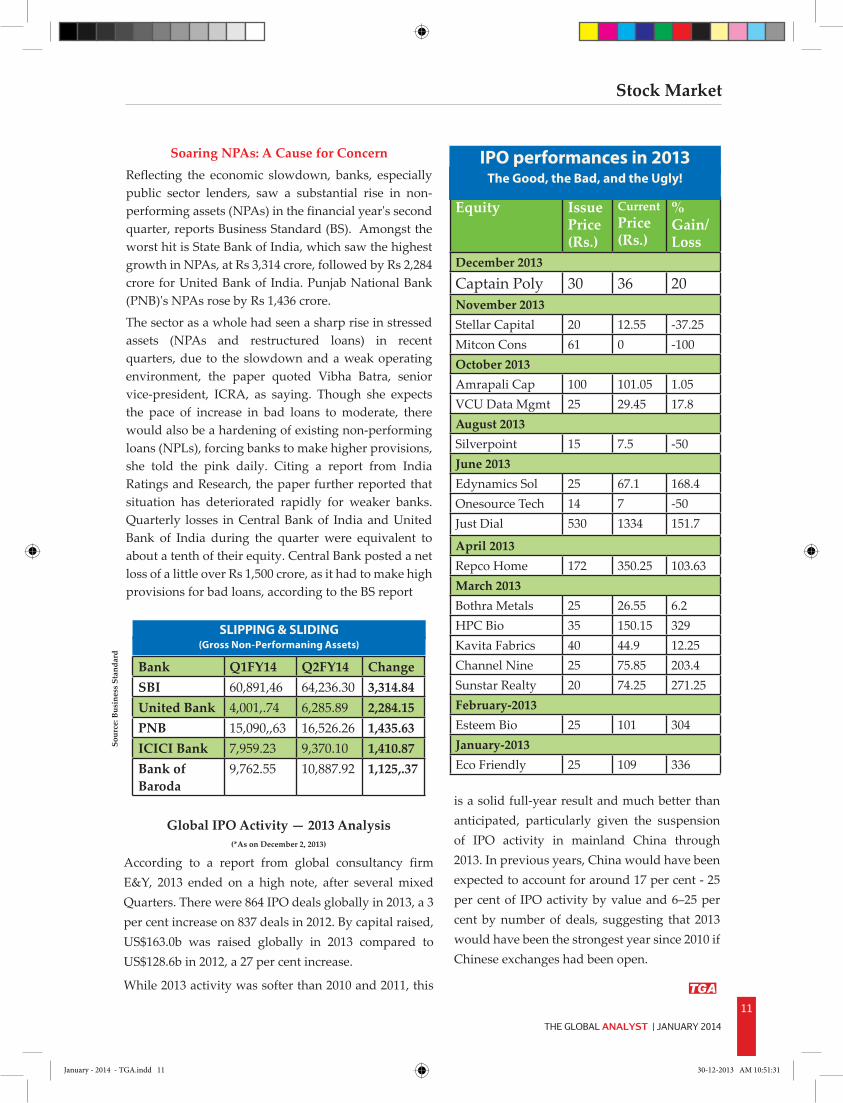

Equity Issue Price (Rs.)

Current Price (Rs.)

% Gain/Loss

December 2013

Captain Poly 30 36 20November 2013Stellar Capital 20 12.55 -37.25Mitcon Cons 61 0 -100October 2013Amrapali Cap 100 101.05 1.05VCU Data Mgmt 25 29.45 17.8August 2013Silverpoint 15 7.5 -50June 2013Edynamics Sol 25 67.1 168.4Onesource Tech 14 7 -50Just Dial 530 1334 151.7

April 2013Repco Home 172 350.25 103.63March 2013Bothra Metals 25 26.55 6.2HPC Bio 35 150.15 329Kavita Fabrics 40 44.9 12.25Channel Nine 25 75.85 203.4Sunstar Realty 20 74.25 271.25February-2013Esteem Bio 25 101 304January-2013Eco Friendly 25 109 336

IPO performances in 2013Soaring NPAs: A Cause for Concern Reflecting the economic slowdown, banks, especially public sector lenders, saw a substantial rise in non-performing assets (NPAs) in the financial year's second quarter, reports Business Standard (BS). Amongst the worst hit is State Bank of India, which saw the highest growth in NPAs, at Rs 3,314 crore, followed by Rs 2,284 crore for United Bank of India. Punjab National Bank (PNB)'s NPAs rose by Rs 1,436 crore.

The sector as a whole had seen a sharp rise in stressed assets (NPAs and restructured loans) in recent quarters, due to the slowdown and a weak operating environment, the paper quoted Vibha Batra, senior vice-president, ICRA, as saying. Though she expects the pace of increase in bad loans to moderate, there would also be a hardening of existing non-performing loans (NPLs), forcing banks to make higher provisions, she told the pink daily. Citing a report from India Ratings and Research, the paper further reported that situation has deteriorated rapidly for weaker banks. Quarterly losses in Central Bank of India and United Bank of India during the quarter were equivalent to about a tenth of their equity. Central Bank posted a net loss of a little over Rs 1,500 crore, as it had to make high provisions for bad loans, according to the BS report

Bank Q1FY14 Q2FY14 ChangeSBI 60,891,46 64,236.30 3,314.84United Bank 4,001,.74 6,285.89 2,284.15PNB 15,090,,63 16,526.26 1,435.63ICICI Bank 7,959.23 9,370.10 1,410.87Bank of Baroda

9,762.55 10,887.92 1,125,.37

SLIPPING & SLIDING

Sour

ce: B

usin

ess

Stan

dard

(Gross Non-Performaning Assets)

Global IPO Activity — 2013 Analysis(*As on December 2, 2013)

According to a report from global consultancy firm E&Y, 2013 ended on a high note, after several mixed Quarters. There were 864 IPO deals globally in 2013, a 3 per cent increase on 837 deals in 2012. By capital raised, US$163.0b was raised globally in 2013 compared to US$128.6b in 2012, a 27 per cent increase.

While 2013 activity was softer than 2010 and 2011, this

is a solid full-year result and much better than anticipated, particularly given the suspension of IPO activity in mainland China through 2013. In previous years, China would have been expected to account for around 17 per cent - 25 per cent of IPO activity by value and 6–25 per cent by number of deals, suggesting that 2013 would have been the strongest year since 2010 if Chinese exchanges had been open.

The Good, the Bad, and the Ugly!

January - 2014 - TGA.indd 11 30-12-2013 AM 10:51:31

THE GLOBAL ANALYST | JANUARY 201412

Digital ANALYST

Discover the Flipkart way to pay!Flipkart, India’s largest e-commerce site, launches customer version of its payment gateway, PayZippy.

Flipkart, the e-commerce giant, recently introduced the cus-

tomer version of its payment gate-way, PayZippy. According to Flip-kart, India’s largest e-commerce player, PayZippy’s customer-fac-ing product for online consumers is a fresh new payment solution for merchants and buyers. This service lets you enjoy a faster, smoother and safer online payment experi-ence across multiple merchants, by saving your card details - just once. Zip through online & mo-bile payments without typing your card number, expiry date, name or billing address, claims the e-tailer, which last year transformed itself into an online marketplace to com-ply with new sets of regulations, which prevent an e-commerce company - that received foreign direct investment - from selling multiple brands directly to cus-tomers. According to Wikipedia, in an online marketplace, consumer transactions are processed by the marketplace operator and then de-

livered and fulfilled by the partici-pating retailers or wholesalers (of-ten called Drop shipping). Flipkart launched its payment gateway for merchants and mobile sites in July last year. The solution is seen as an attempt to wean online customers away from cash-on-delivery, a payment meth-od used for 65 per cent of all online transactions, commented a report in the Times of India. “With PayZippy we have actually reduced the time taken for making online payments by 50 per cent. We are expecting at least 1,50,000 customers to sign up for this service within the first month and our target is to get 1 mil-lion customers by next June,” said Mekin Maheswari, Head of Pay-ments and Digital Media, Flipkart.com.

Profitless Growth!The online commerce market is currently one of the hottest in the world, attracting a number of for-eign investors, including VCs and

private equity industry players, besides witnessing a slew of merg-ers & acquisitions. The Internet and Mobile Association of India (IAMAI) estimates the e-retailing market segment’s revenues in the country to grow by 55 per cent to Rs 10,000 crore by the end of 2013, from Rs 6,454 crore in 2012, even as most of the e-tailers find it hard to earn profits. Flipkart’s losses more than doubled to Rs.281.7 crore in FY 2012-13, from Rs.109.9 crore in-curred in the previous year, though its revenues surged fivefold to more than Rs.1,180 crore, but ex-penses too grew at a similar pace to Rs.1,366 crore (from Rs.265.6 crore in FY 2011-12). “The deeper losses as well as soaring sales are in keep-ing with Flipkart’s winner-takes-all strategy, which involves pur-suing revenue growth and market share at any cost, the same model followed by Amazon.com Inc. in the US,” comments a report in the business daily Mint.

It seems Samsung never sleeps! the world’s top maker of Smart-

phones, which knocked Apple off its perch at the top of the global Smart-phone market, during the third quarter of 2013-14, continues to hit the market with its new product of-ferings at regular intervals. The South Korean giant which also is the world’s leading manufacturer of other consumer electronic devices such as Smart TV, LED TV, Camer-as, Washing Machines, etc., recently unveiled ‘Galaxy Grand 2’, the suc-cessor to the Galaxy Grand which was launched in early last year. Grand 2, essentially a Phablet that

combines the functions of a smart-phone and a tablet PC), is priced below Rs.25,000. This dual-SIM Smartphone promises to perform better compared to its predecessor Grand in every aspect. The Galaxy Grand 2 runs on Android 4.3 (Jelly Bean) and features a 5.25-inch (13.3 cm) HD TFT display with a resolu-tion of 720x1280 pixels. The Grand 2 also boasts of a Multi Window feature which allows for multitask-ing and is powered by a Qualcomm chipset. The device offers the user an enhanced viewing experience, thanks to its High Definition screen. “This new Samsung Galaxy Grand 2 delivers an improved HD viewing experience, more powerful multi-

tasking features, a premium experi-ence through design and entertain-ment on the go,” said Vineet Taneja, India Country Head, Mobile and IT, Samsung, raising expectations level further. The device is sure to putfurther pressure for rivals.

Smartphones

January - 2014 - TGA.indd 12 30-12-2013 AM 10:51:31

THE GLOBAL ANALYST | JANUARY 2014

13

January - 2014 - TGA.indd 13 30-12-2013 AM 10:51:32

THE GLOBAL ANALYST | JANUARY 201414

BUSINESS ENVIRONMENT

What’s in Store?Infrastructure Sector in 2014

A separate ministry for infrastructure would help to provide special attention and be catalyst to the entire process of recovery, says Moses Harding, Group CEO & Chief Economist, Srei Infrastructure Finance Ltd, Kolkata.

India Inc. is not in an enviable position. The domestic mac-ro fundamentals are weak, stuck between growth-infla-

tion conflict, deterioration in twin deficits and the resultant pressure on Rupee exchange rate. RBI is unable to support growth through benign monetary policy given the elevated inflation from supply-side constraints.

The political risk factors have emerged now with fear of hung parliament in 2014 general elec-tions. All taken, economic, mon-etary and political conditions (and cues) do not provide comfort that the worst is behind. The external cues are also no better with the US Fed expected to start the QE taper process soon, thus limiting the availability of external liquid-ity into emerging markets. While

QE taper is sign of optimism on the growth of the US economy, India’s high dependence on hot money in the form of FII flows to fund the Current Account deficit will add to the pressure on Rupee exchange rate and equity capital markets.

There has been relief post Ra-ghuram Rajan taking charge as Governor of RBI. There has been lot of administrative actions (and strictures) to control the Current Account Deficit and cut its ad-verse impact on Rupee exchange rate, but all these are not perma-nent in nature, while providing temporary relief, like a high-dose steroid! The weak macroeconomic fundamentals with no signs of light at the end of the tunnel, investor’s confidence and appetite have been hit.

The expectation of economic data print of FY14 for GDP growth below 5 per cent, WPI print at 7.5 per cent, retail CPI print at around 12 per cent, fiscal deficit to overshoot over 5 per cent, pressure on trade/current account deficit along with headwinds from high interest rates and tight liquidity provide little optimism on the future. The root-cause analysis will point fingers at policy inaction and poor gov-ernance. The outcome of 2014 general elections holds the trigger for scripting the turnaround story. Till then, it will be wishful to assume that the worst for India Inc. is over!

Greater Thrust NeededIt is obvious that UPA2 did not have the band-width to go

January - 2014 - TGA.indd 14 30-12-2013 AM 10:51:33

THE GLOBAL ANALYST | JANUARY 2014

15

Infrastructure Sector in 2014

aggressive on infrastructure sector and failed to remove policy-related bottle-necks (and irritants) across land, labour and legal domains. Most projects got stuck, investments blocked and faced cost over-run. There is unanimity across political parties that infrastructure sector (along with manufacturing and agriculture) has to lead so as to push the economic growth back to over 8 per cent levels. It would need huge off-shore investments (estimated at over $ 1 trillion in the next five years) but long-term foreign investors see it tough to do business (or invest) in India. There should be a clear political mandate either for UPA or NDA to steer the recovery story for India while an indecisive mandate or a hung parliament may cause irreparable damage to the Indian economy (and its financial markets), making the recoveryprocess an extended one!

Major growth drivers to revive infrastructure The first step is to revive the ex-isting projects which are stuck due to policy irritants, liquidity squeeze and high cost of debt. It would need further investments through equity and debt to get these projects on track. So, it is a combination of infra-friendly pol-icies and liquidity support. The need is to pump in fresh investments on priority basis through Public-Private Partner-ships, restructure of existing debt to release cash flows and fresh debt at concessional rates of in-terest. The momentum thereafter should be from uptrend in GDP growth momentum, from below 5 per cent to above 7 per cent, and

ensuring foreign investor’s appe-tite for infrastructure sector.

Needed Some More Actions Infrastructure sector needs sup-port from the system in terms of policy and administrative actions - around Power, Roads, Ports, Rail-ways and Oil & Gas - such as; (a) support to SEBs to sustain op-erations and facilitate investment in power distribution, (b) chan-nelization of private investment into distribution system to reduce AT&C losses and to meet demand growth, (c) tariff rationalization leading to economical power tar-iff for all categories of customers, (d) ensuring speed in awarding and execution of projects, (e) al-lowing commercial coal mining to enhance fuel supply, (f) clarity on policies regarding fuel subsidy, pricing , gas pooling etc., (g) ratio-nalization of land acquisition bills to reduce time and cost of land acquisition, (h) expedite environ-mental clearance and most impor-tantly (i) relax regulatory norms relating to infrastructure financ-ing, assist for raising long-term funds and timely release of funds from the Government towards various programs. Overall, resolu-tions revolve around main themes of policy reforms, administrative actions and ensuring smooth flow of liquidity at affordable cost.

Key Challenges The challenges are from trending in macroeconomic factors, extent of facilitation by the Government and investors/lenders appetite for infrastructure assets, both do-mestic and foreign. The Govern-ment should focus on removing supply side bottle-necks to arrest demand-push inflation and enable RBI to shift the monetary policy to

spur growth. A separate minis-try for infrastructure would help to provide special attention and be catalyst to the entire process of recovery. The Government should play the lead role in extending li-quidity support through equity and debt which will provide comfort (and confidence) for other private and foreign players to follow.

OutlookIndian growth (and prosperity) story is fortunately very much in-tact despite slippage in political, economic and monetary environ-ment. The immediate resolutions shall be from setting up a single window clearance for infrastruc-ture sector (Ministry of Infra-structure) with full empowerment which is currently spread across government departments, minis-tries and regulatory bodies. Gov-ernment should speed up explora-tion of huge reserves in KG basin, else will lose its cost advantage. India needs an image makeover to attract large foreign capital. The country is a permanent exporter of capital for financing the trade defi-cit which needs to be met through long-term and permanent direct investments.

Moses Harding

January - 2014 - TGA.indd 15 30-12-2013 AM 10:51:33

![[2014 ITB 8] Finance Act, 2014 - S.A. Salam updates/Finance Act, 2014... · Income Tax Ready Reference Finance Act, 2014 133 [2014 ITB 8] Finance Act, ... 2000) Finance Act, 2014](https://img.pdfslide.net/doc/110x75/5b4c8db67f8b9ab2668b4759/2014-itb-8-finance-act-2014-sa-updatesfinance-act-2014-income-tax.jpg)