Embed Size (px)

Citation preview

ISSN 0388-0605

MONTHLY FINANCE REVIEW

June 2017

No. 527

Policy Research Institute

MINISTRY OF FINANCE

JAPAN

MONTHLY FINANCE REVIEW

June. 2017 (No.527)

CONTENTS

STATISTICS(Released by Ministry of Finance)

A. Balance of the Fiscal Loan Fund (20 Apr.) ............................................................. 2

B. Trade Statistics (27 Apr.) ....................................................................................... 4

C. Taxes and Stamp Revenues (28 Apr.) .................................................................... 8

D. Receipts and Payments of the Treasury Funds with the Private Sector (2 May.) ....... 12

E. Official Reserve Assets at the End of Periods (10 May.) ........................................ 16

F. Balance of Payments (11 May.) ........................................................................... 18

G. International Transaction in Securities (Monthly; Based on reports from

designated major investors) (11 May.) .................................................................. 22

H. The balance of Offshore Accounts (18 May.) ........................................................ 24

I. Central Government Debt (10 May.) ................................................................. 26

PUBLIC RELATIONS & PRESS RELEASE A. The Joint Statement of The 20th ASEAN+3 Finance Ministers’ Meeting

(5 May 2017 / Yokohama, Japan) (5 May.) ............................................................. 30

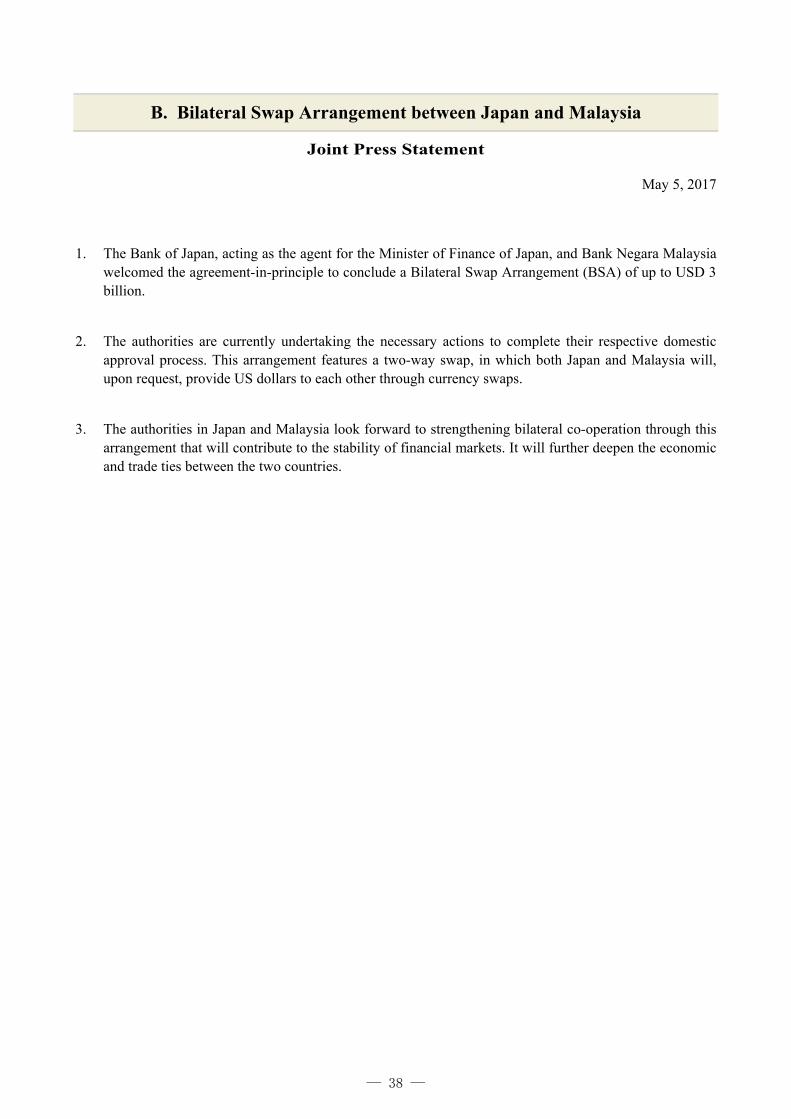

B. Bilateral Swap Arrangement between Japan and Malaysia (5 May.) ....................... 38

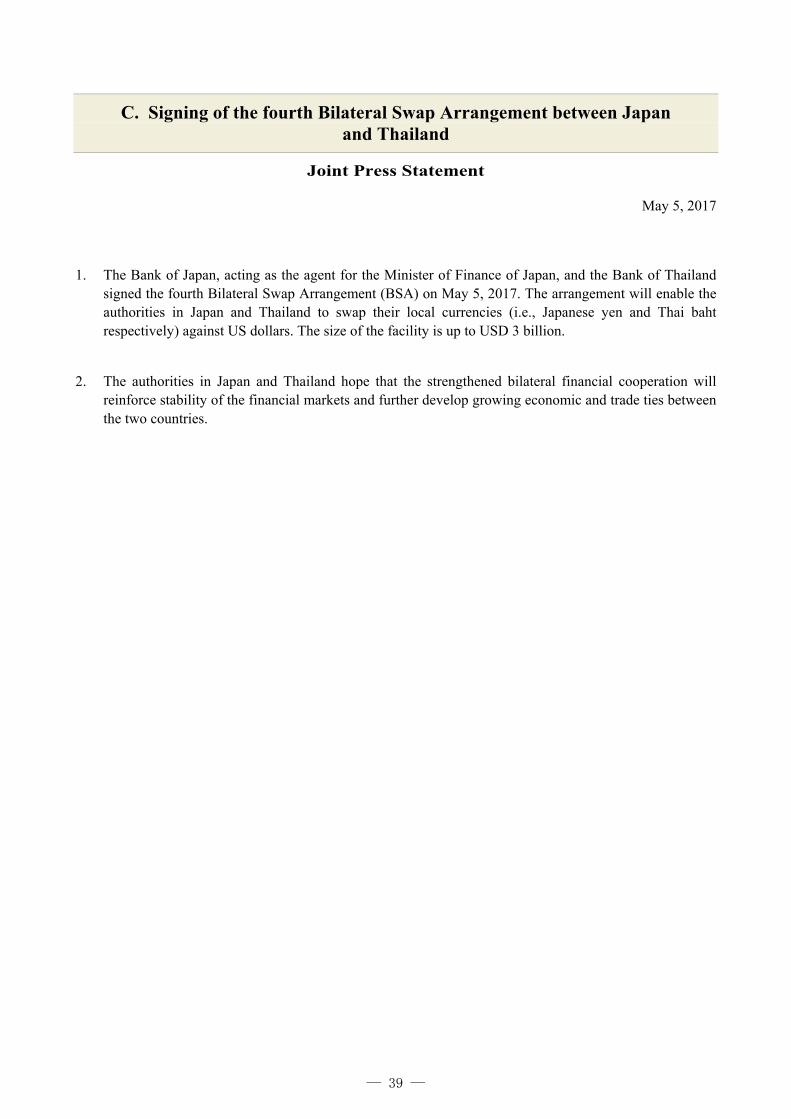

C. Signing of the fourth Bilateral Swap Arrangement between Japan and Thailand

(5 May.) ...................................................................................................................... 39

D. 17th Trilateral Finance Ministers and Central Bank Governors' Meeting Joint

Message(May 5, 2017, Yokohama, Japan) (5 May.) ................................................ 40

E. Joint Press Release of the Sixth China-Japan Finance Dialogue (6 May.) .............. 43

F. Statement at the 50th Annual Meeting of the ADB (Yokohama, Japan / May 6,

2017) (6 May.) .......................................................................................................... 45

G. Statement at the 26th Annual Meeting of the EBRD (Nicosia, Cyprus / May 10,

2017) (10 May.) ........................................................................................................ 51

H. COMMUNIQUÉ ,G7 Finance Ministers and Central Banks’ Governors Meeting

(Bari, Italy, May 12-13, 2017) (13 May.) .................................................................. 55

I. Tax Convention with Estonia Agreed in Principle (15 May.) ..................................... 63

J. New Tax Convention with Denmark Agreed in Principle (15 May.) ......................... 64

K. Statement at the Annual Meetings of 52nd AfDB / 43rd AfDF (Ahmedabad, India

/ May 23, 2017) (23 May.) ....................................................................................... 65

L. Tax Convention with Iceland Agreed in Principle (29 May.) .................................... 72

APPENDIX

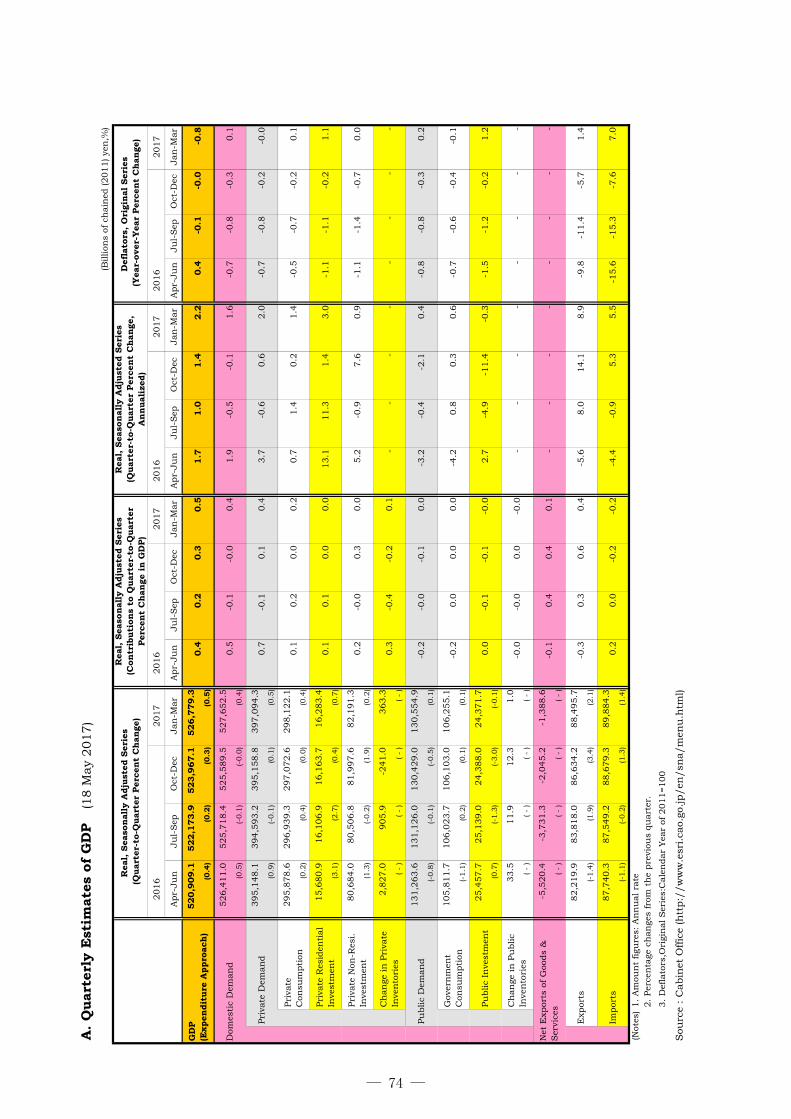

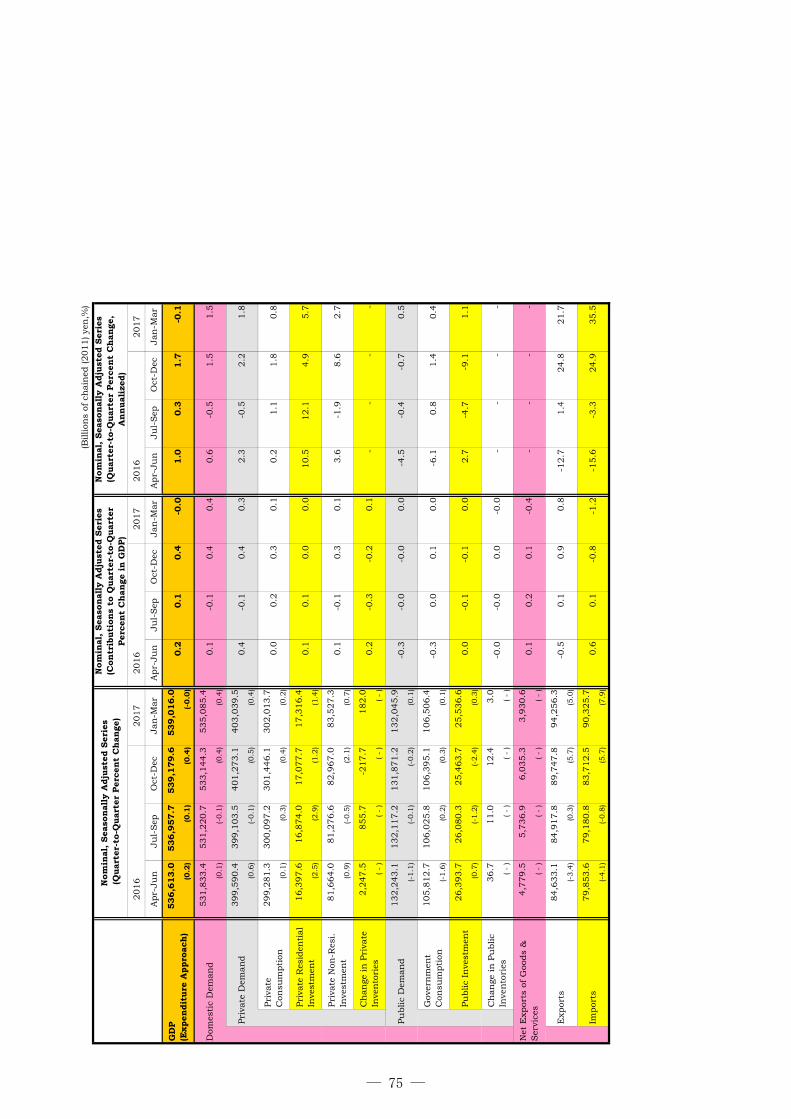

A. Quarterly Estimates of GDP, Jan.-Mar. 2017 (The 1st preliminary) (18 May.) ....... 74

B. Monthly Economic Report (May) (24 May.) .............................................................. 76

MAIN ECONOMIC INDICATORS OF JAPAN .......................................................... 80

STATISTICS

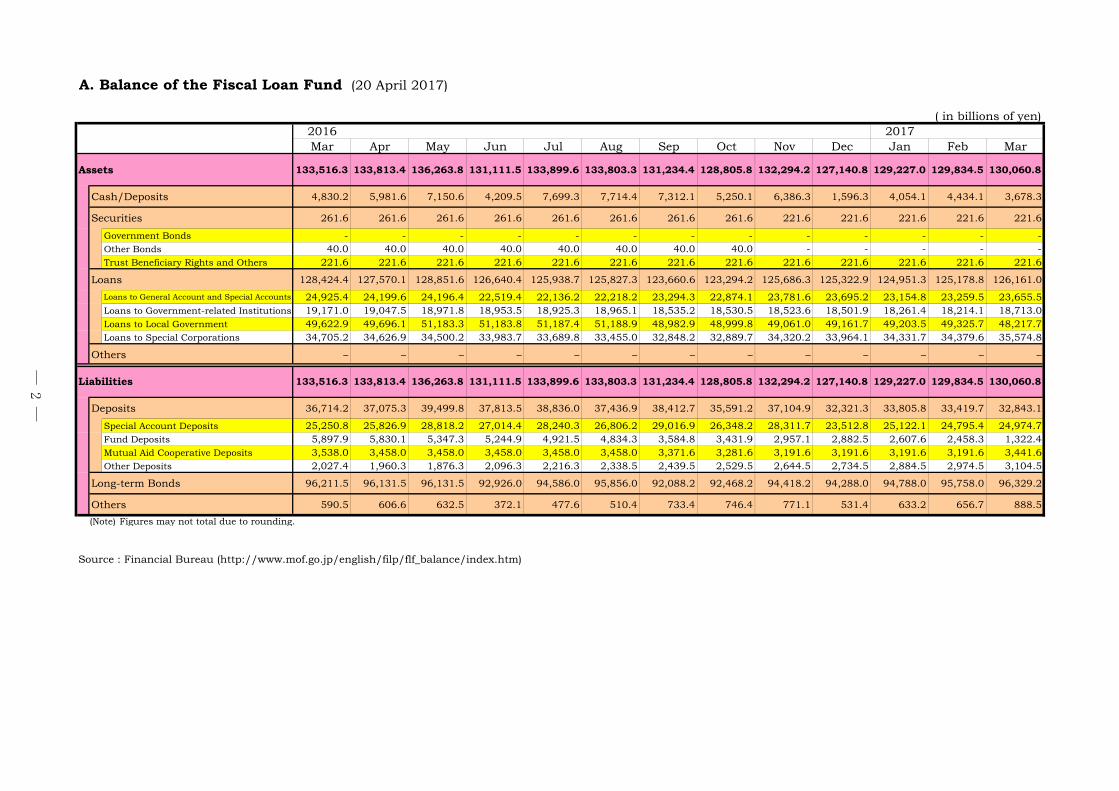

A. Balance of the Fiscal Loan Fund (20 April 2017)

( in billions of yen)2016 2017Mar Apr May Jun Jul Aug Sep Oct Nov Dec Jan Feb Mar

Assets 133,516.3 133,813.4 136,263.8 131,111.5 133,899.6 133,803.3 131,234.4 128,805.8 132,294.2 127,140.8 129,227.0 129,834.5 130,060.8

Cash/Deposits 4,830.2 5,981.6 7,150.6 4,209.5 7,699.3 7,714.4 7,312.1 5,250.1 6,386.3 1,596.3 4,054.1 4,434.1 3,678.3

Securities 261.6 261.6 261.6 261.6 261.6 261.6 261.6 261.6 221.6 221.6 221.6 221.6 221.6

Government Bonds - - - - - - - - - - - - -Other Bonds 40.0 40.0 40.0 40.0 40.0 40.0 40.0 40.0 - - - - -Trust Beneficiary Rights and Others 221.6 221.6 221.6 221.6 221.6 221.6 221.6 221.6 221.6 221.6 221.6 221.6 221.6

Loans 128,424.4 127,570.1 128,851.6 126,640.4 125,938.7 125,827.3 123,660.6 123,294.2 125,686.3 125,322.9 124,951.3 125,178.8 126,161.0

Loans to General Account and Special Accounts 24,925.4 24,199.6 24,196.4 22,519.4 22,136.2 22,218.2 23,294.3 22,874.1 23,781.6 23,695.2 23,154.8 23,259.5 23,655.5Loans to Government-related Institutions 19,171.0 19,047.5 18,971.8 18,953.5 18,925.3 18,965.1 18,535.2 18,530.5 18,523.6 18,501.9 18,261.4 18,214.1 18,713.0Loans to Local Government 49,622.9 49,696.1 51,183.3 51,183.8 51,187.4 51,188.9 48,982.9 48,999.8 49,061.0 49,161.7 49,203.5 49,325.7 48,217.7Loans to Special Corporations 34,705.2 34,626.9 34,500.2 33,983.7 33,689.8 33,455.0 32,848.2 32,889.7 34,320.2 33,964.1 34,331.7 34,379.6 35,574.8

Others – – – – – – – – – – – – –

Liabilities 133,516.3 133,813.4 136,263.8 131,111.5 133,899.6 133,803.3 131,234.4 128,805.8 132,294.2 127,140.8 129,227.0 129,834.5 130,060.8

Deposits 36,714.2 37,075.3 39,499.8 37,813.5 38,836.0 37,436.9 38,412.7 35,591.2 37,104.9 32,321.3 33,805.8 33,419.7 32,843.1

Special Account Deposits 25,250.8 25,826.9 28,818.2 27,014.4 28,240.3 26,806.2 29,016.9 26,348.2 28,311.7 23,512.8 25,122.1 24,795.4 24,974.7Fund Deposits 5,897.9 5,830.1 5,347.3 5,244.9 4,921.5 4,834.3 3,584.8 3,431.9 2,957.1 2,882.5 2,607.6 2,458.3 1,322.4Mutual Aid Cooperative Deposits 3,538.0 3,458.0 3,458.0 3,458.0 3,458.0 3,458.0 3,371.6 3,281.6 3,191.6 3,191.6 3,191.6 3,191.6 3,441.6Other Deposits 2,027.4 1,960.3 1,876.3 2,096.3 2,216.3 2,338.5 2,439.5 2,529.5 2,644.5 2,734.5 2,884.5 2,974.5 3,104.5

Long-term Bonds 96,211.5 96,131.5 96,131.5 92,926.0 94,586.0 95,856.0 92,088.2 92,468.2 94,418.2 94,288.0 94,788.0 95,758.0 96,329.2

Others 590.5 606.6 632.5 372.1 477.6 510.4 733.4 746.4 771.1 531.4 633.2 656.7 888.5

(Note) Figures may not total due to rounding.

Source : Financial Bureau (http://www.mof.go.jp/english/filp/flf_balance/index.htm)

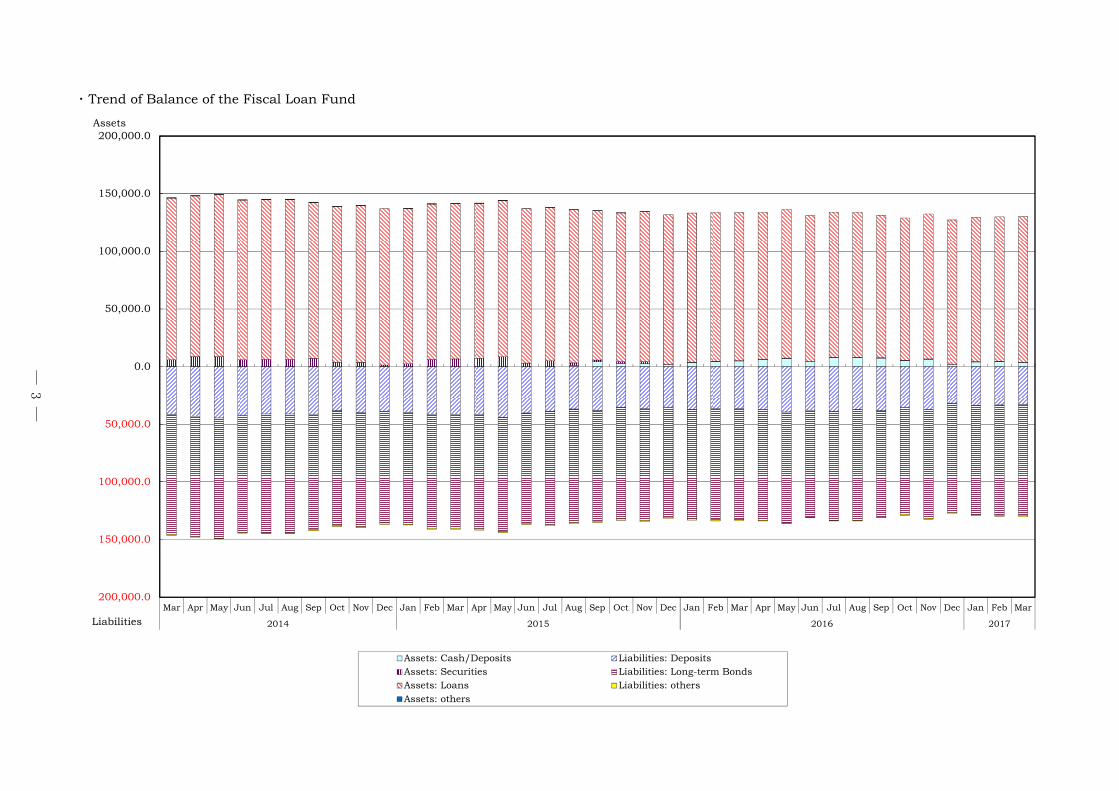

― 2 ―

・ Trend of Balance of the Fiscal Loan Fund

200,000.0

150,000.0

100,000.0

50,000.0

0.0

50,000.0

100,000.0

150,000.0

200,000.0

Mar Apr May Jun Jul Aug Sep Oct Nov Dec Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec Jan Feb Mar

2014 2015 2016 2017

Assets: Cash/Deposits Liabilities: DepositsAssets: Securities Liabilities: Long-term BondsAssets: Loans Liabilities: othersAssets: others

Assets

Liabilities

― 3 ―

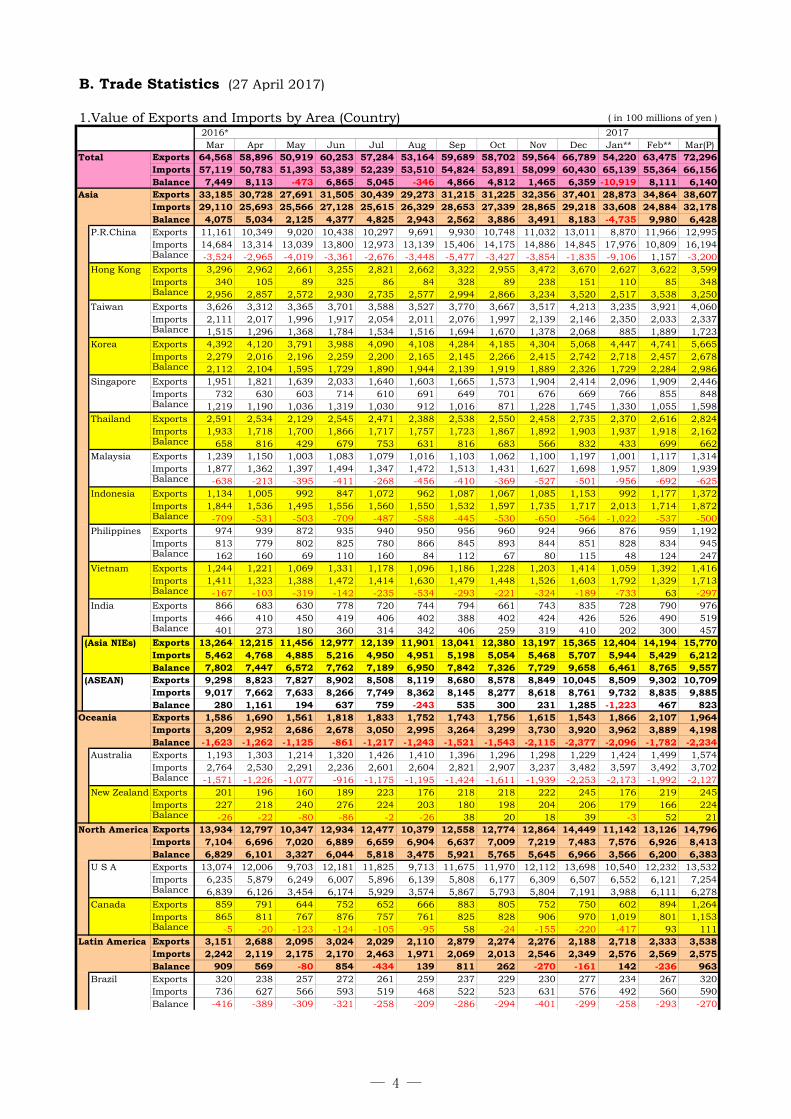

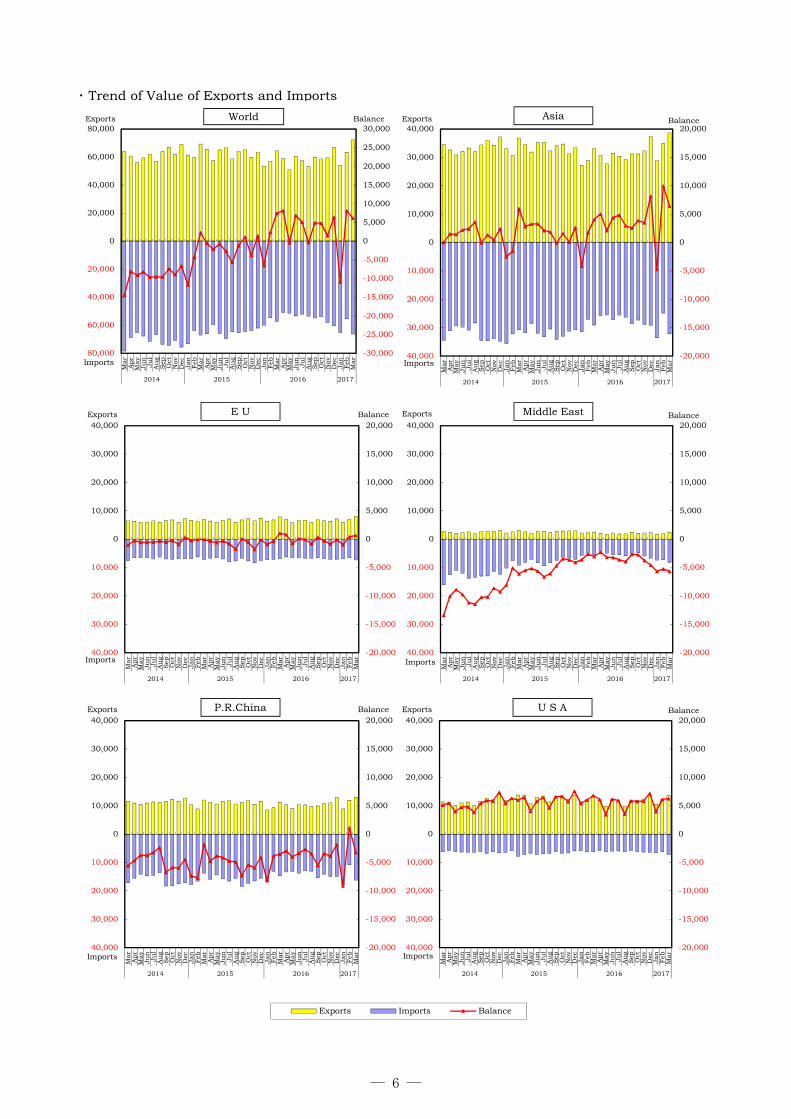

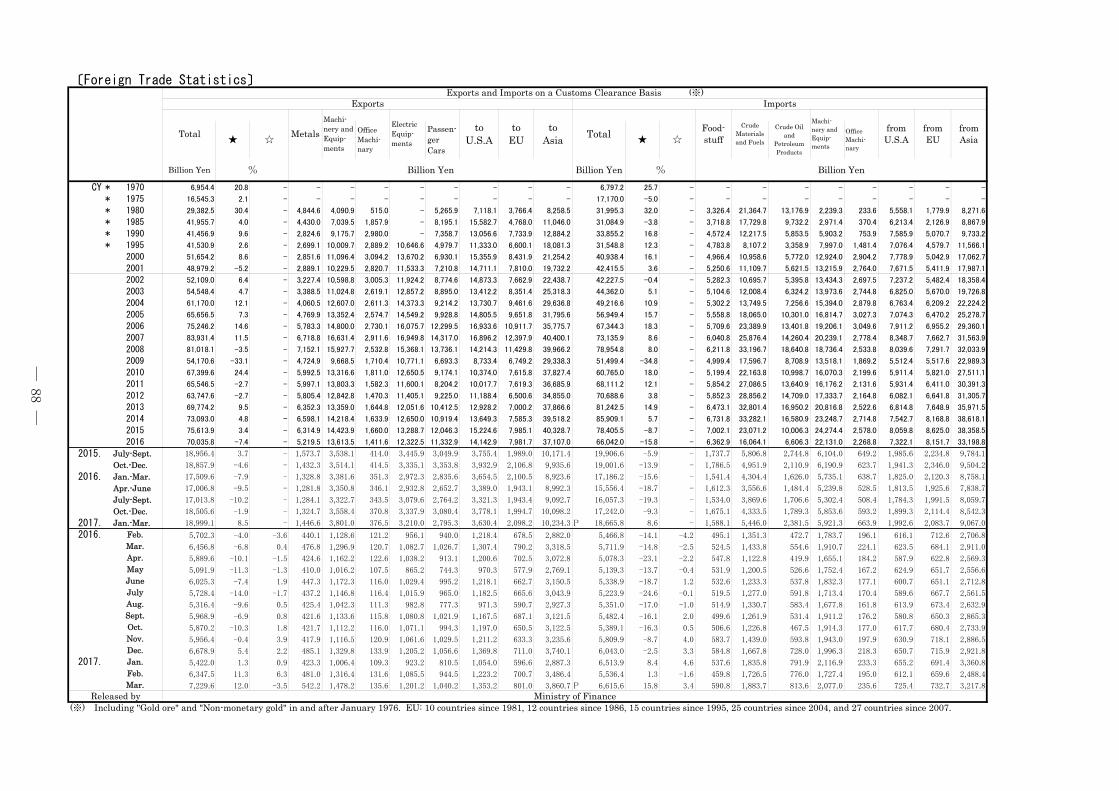

B. Trade Statistics (27 April 2017)

1.Value of Exports and Imports by Area (Country) ( in 100 millions of yen )

2016* 2017Mar Apr May Jun Jul Aug Sep Oct Nov Dec Jan** Feb** Mar(P)

Total Exports 64,568 58,896 50,919 60,253 57,284 53,164 59,689 58,702 59,564 66,789 54,220 63,475 72,296Imports 57,119 50,783 51,393 53,389 52,239 53,510 54,824 53,891 58,099 60,430 65,139 55,364 66,156Balance 7,449 8,113 -473 6,865 5,045 -346 4,866 4,812 1,465 6,359 -10,919 8,111 6,140

Asia Exports 33,185 30,728 27,691 31,505 30,439 29,273 31,215 31,225 32,356 37,401 28,873 34,864 38,607Imports 29,110 25,693 25,566 27,128 25,615 26,329 28,653 27,339 28,865 29,218 33,608 24,884 32,178Balance 4,075 5,034 2,125 4,377 4,825 2,943 2,562 3,886 3,491 8,183 -4,735 9,980 6,428

P.R.China Exports 11,161 10,349 9,020 10,438 10,297 9,691 9,930 10,748 11,032 13,011 8,870 11,966 12,995Imports 14,684 13,314 13,039 13,800 12,973 13,139 15,406 14,175 14,886 14,845 17,976 10,809 16,194Balance -3,524 -2,965 -4,019 -3,361 -2,676 -3,448 -5,477 -3,427 -3,854 -1,835 -9,106 1,157 -3,200

Hong Kong Exports 3,296 2,962 2,661 3,255 2,821 2,662 3,322 2,955 3,472 3,670 2,627 3,622 3,599Imports 340 105 89 325 86 84 328 89 238 151 110 85 348Balance 2,956 2,857 2,572 2,930 2,735 2,577 2,994 2,866 3,234 3,520 2,517 3,538 3,250

Taiwan Exports 3,626 3,312 3,365 3,701 3,588 3,527 3,770 3,667 3,517 4,213 3,235 3,921 4,060Imports 2,111 2,017 1,996 1,917 2,054 2,011 2,076 1,997 2,139 2,146 2,350 2,033 2,337Balance 1,515 1,296 1,368 1,784 1,534 1,516 1,694 1,670 1,378 2,068 885 1,889 1,723

Korea Exports 4,392 4,120 3,791 3,988 4,090 4,108 4,284 4,185 4,304 5,068 4,447 4,741 5,665Imports 2,279 2,016 2,196 2,259 2,200 2,165 2,145 2,266 2,415 2,742 2,718 2,457 2,678Balance 2,112 2,104 1,595 1,729 1,890 1,944 2,139 1,919 1,889 2,326 1,729 2,284 2,986

Singapore Exports 1,951 1,821 1,639 2,033 1,640 1,603 1,665 1,573 1,904 2,414 2,096 1,909 2,446Imports 732 630 603 714 610 691 649 701 676 669 766 855 848Balance 1,219 1,190 1,036 1,319 1,030 912 1,016 871 1,228 1,745 1,330 1,055 1,598

Thailand Exports 2,591 2,534 2,129 2,545 2,471 2,388 2,538 2,550 2,458 2,735 2,370 2,616 2,824Imports 1,933 1,718 1,700 1,866 1,717 1,757 1,723 1,867 1,892 1,903 1,937 1,918 2,162Balance 658 816 429 679 753 631 816 683 566 832 433 699 662

Malaysia Exports 1,239 1,150 1,003 1,083 1,079 1,016 1,103 1,062 1,100 1,197 1,001 1,117 1,314Imports 1,877 1,362 1,397 1,494 1,347 1,472 1,513 1,431 1,627 1,698 1,957 1,809 1,939Balance -638 -213 -395 -411 -268 -456 -410 -369 -527 -501 -956 -692 -625

Indonesia Exports 1,134 1,005 992 847 1,072 962 1,087 1,067 1,085 1,153 992 1,177 1,372Imports 1,844 1,536 1,495 1,556 1,560 1,550 1,532 1,597 1,735 1,717 2,013 1,714 1,872Balance -709 -531 -503 -709 -487 -588 -445 -530 -650 -564 -1,022 -537 -500

Philippines Exports 974 939 872 935 940 950 956 960 924 966 876 959 1,192Imports 813 779 802 825 780 866 845 893 844 851 828 834 945Balance 162 160 69 110 160 84 112 67 80 115 48 124 247

Vietnam Exports 1,244 1,221 1,069 1,331 1,178 1,096 1,186 1,228 1,203 1,414 1,059 1,392 1,416Imports 1,411 1,323 1,388 1,472 1,414 1,630 1,479 1,448 1,526 1,603 1,792 1,329 1,713Balance -167 -103 -319 -142 -235 -534 -293 -221 -324 -189 -733 63 -297

India Exports 866 683 630 778 720 744 794 661 743 835 728 790 976Imports 466 410 450 419 406 402 388 402 424 426 526 490 519Balance 401 273 180 360 314 342 406 259 319 410 202 300 457

(Asia NIEs) Exports 13,264 12,215 11,456 12,977 12,139 11,901 13,041 12,380 13,197 15,365 12,404 14,194 15,770Imports 5,462 4,768 4,885 5,216 4,950 4,951 5,198 5,054 5,468 5,707 5,944 5,429 6,212Balance 7,802 7,447 6,572 7,762 7,189 6,950 7,842 7,326 7,729 9,658 6,461 8,765 9,557

(ASEAN) Exports 9,298 8,823 7,827 8,902 8,508 8,119 8,680 8,578 8,849 10,045 8,509 9,302 10,709Imports 9,017 7,662 7,633 8,266 7,749 8,362 8,145 8,277 8,618 8,761 9,732 8,835 9,885Balance 280 1,161 194 637 759 -243 535 300 231 1,285 -1,223 467 823

Oceania Exports 1,586 1,690 1,561 1,818 1,833 1,752 1,743 1,756 1,615 1,543 1,866 2,107 1,964Imports 3,209 2,952 2,686 2,678 3,050 2,995 3,264 3,299 3,730 3,920 3,962 3,889 4,198Balance -1,623 -1,262 -1,125 -861 -1,217 -1,243 -1,521 -1,543 -2,115 -2,377 -2,096 -1,782 -2,234

Australia Exports 1,193 1,303 1,214 1,320 1,426 1,410 1,396 1,296 1,298 1,229 1,424 1,499 1,574Imports 2,764 2,530 2,291 2,236 2,601 2,604 2,821 2,907 3,237 3,482 3,597 3,492 3,702Balance -1,571 -1,226 -1,077 -916 -1,175 -1,195 -1,424 -1,611 -1,939 -2,253 -2,173 -1,992 -2,127

New Zealand Exports 201 196 160 189 223 176 218 218 222 245 176 219 245Imports 227 218 240 276 224 203 180 198 204 206 179 166 224Balance -26 -22 -80 -86 -2 -26 38 20 18 39 -3 52 21

North America Exports 13,934 12,797 10,347 12,934 12,477 10,379 12,558 12,774 12,864 14,449 11,142 13,126 14,796Imports 7,104 6,696 7,020 6,889 6,659 6,904 6,637 7,009 7,219 7,483 7,576 6,926 8,413Balance 6,829 6,101 3,327 6,044 5,818 3,475 5,921 5,765 5,645 6,966 3,566 6,200 6,383

U S A Exports 13,074 12,006 9,703 12,181 11,825 9,713 11,675 11,970 12,112 13,698 10,540 12,232 13,532Imports 6,235 5,879 6,249 6,007 5,896 6,139 5,808 6,177 6,309 6,507 6,552 6,121 7,254Balance 6,839 6,126 3,454 6,174 5,929 3,574 5,867 5,793 5,804 7,191 3,988 6,111 6,278

Canada Exports 859 791 644 752 652 666 883 805 752 750 602 894 1,264Imports 865 811 767 876 757 761 825 828 906 970 1,019 801 1,153Balance -5 -20 -123 -124 -105 -95 58 -24 -155 -220 -417 93 111

Latin America Exports 3,151 2,688 2,095 3,024 2,029 2,110 2,879 2,274 2,276 2,188 2,718 2,333 3,538Imports 2,242 2,119 2,175 2,170 2,463 1,971 2,069 2,013 2,546 2,349 2,576 2,569 2,575Balance 909 569 -80 854 -434 139 811 262 -270 -161 142 -236 963

Brazil Exports 320 238 257 272 261 259 237 229 230 277 234 267 320Imports 736 627 566 593 519 468 522 523 631 576 492 560 590Balance -416 -389 -309 -321 -258 -209 -286 -294 -401 -299 -258 -293 -270

― 4 ―

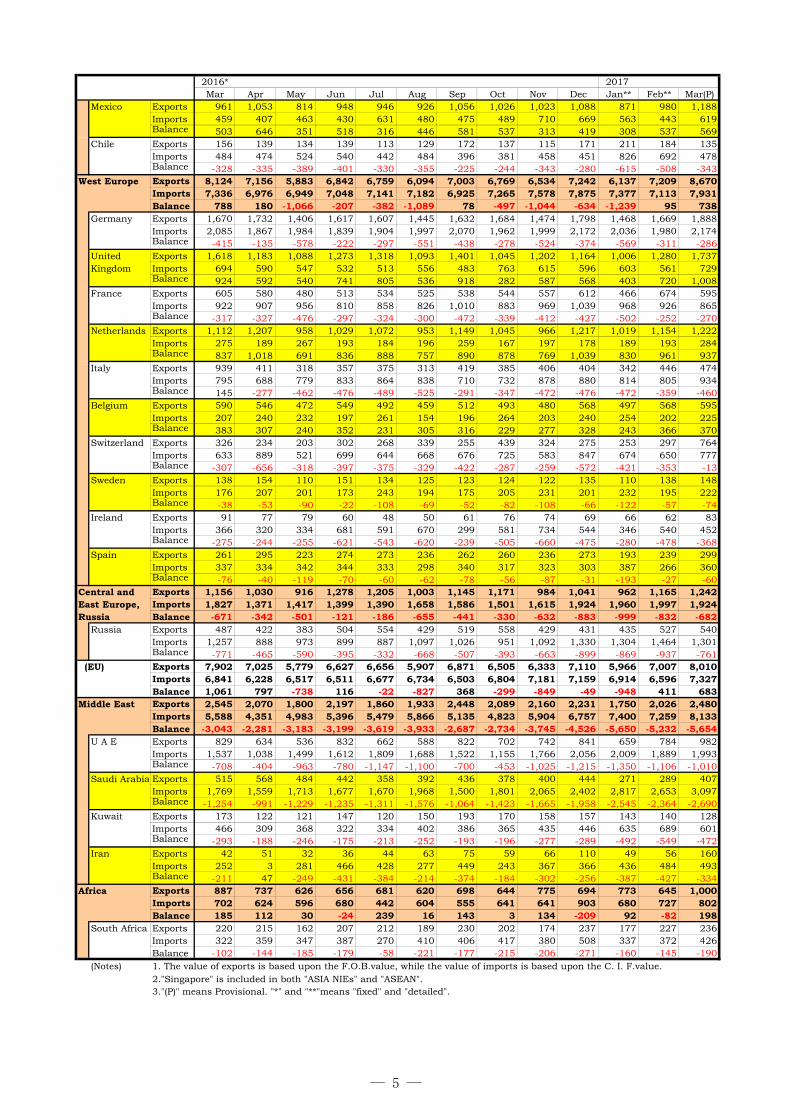

2016* 2017Mar Apr May Jun Jul Aug Sep Oct Nov Dec Jan** Feb** Mar(P)

Mexico Exports 961 1,053 814 948 946 926 1,056 1,026 1,023 1,088 871 980 1,188Imports 459 407 463 430 631 480 475 489 710 669 563 443 619Balance 503 646 351 518 316 446 581 537 313 419 308 537 569

Chile Exports 156 139 134 139 113 129 172 137 115 171 211 184 135Imports 484 474 524 540 442 484 396 381 458 451 826 692 478Balance -328 -335 -389 -401 -330 -355 -225 -244 -343 -280 -615 -508 -343

West Europe Exports 8,124 7,156 5,883 6,842 6,759 6,094 7,003 6,769 6,534 7,242 6,137 7,209 8,670Imports 7,336 6,976 6,949 7,048 7,141 7,182 6,925 7,265 7,578 7,875 7,377 7,113 7,931Balance 788 180 -1,066 -207 -382 -1,089 78 -497 -1,044 -634 -1,239 95 738

Germany Exports 1,670 1,732 1,406 1,617 1,607 1,445 1,632 1,684 1,474 1,798 1,468 1,669 1,888Imports 2,085 1,867 1,984 1,839 1,904 1,997 2,070 1,962 1,999 2,172 2,036 1,980 2,174Balance -415 -135 -578 -222 -297 -551 -438 -278 -524 -374 -569 -311 -286

United Exports 1,618 1,183 1,088 1,273 1,318 1,093 1,401 1,045 1,202 1,164 1,006 1,280 1,737Kingdom Imports 694 590 547 532 513 556 483 763 615 596 603 561 729

Balance 924 592 540 741 805 536 918 282 587 568 403 720 1,008France Exports 605 580 480 513 534 525 538 544 557 612 466 674 595

Imports 922 907 956 810 858 826 1,010 883 969 1,039 968 926 865Balance -317 -327 -476 -297 -324 -300 -472 -339 -412 -427 -502 -252 -270

Netherlands Exports 1,112 1,207 958 1,029 1,072 953 1,149 1,045 966 1,217 1,019 1,154 1,222Imports 275 189 267 193 184 196 259 167 197 178 189 193 284Balance 837 1,018 691 836 888 757 890 878 769 1,039 830 961 937

Italy Exports 939 411 318 357 375 313 419 385 406 404 342 446 474Imports 795 688 779 833 864 838 710 732 878 880 814 805 934Balance 145 -277 -462 -476 -489 -525 -291 -347 -472 -476 -472 -359 -460

Belgium Exports 590 546 472 549 492 459 512 493 480 568 497 568 595Imports 207 240 232 197 261 154 196 264 203 240 254 202 225Balance 383 307 240 352 231 305 316 229 277 328 243 366 370

Switzerland Exports 326 234 203 302 268 339 255 439 324 275 253 297 764Imports 633 889 521 699 644 668 676 725 583 847 674 650 777Balance -307 -656 -318 -397 -375 -329 -422 -287 -259 -572 -421 -353 -13

Sweden Exports 138 154 110 151 134 125 123 124 122 135 110 138 148Imports 176 207 201 173 243 194 175 205 231 201 232 195 222Balance -38 -53 -90 -22 -108 -69 -52 -82 -108 -66 -122 -57 -74

Ireland Exports 91 77 79 60 48 50 61 76 74 69 66 62 83Imports 366 320 334 681 591 670 299 581 734 544 346 540 452Balance -275 -244 -255 -621 -543 -620 -239 -505 -660 -475 -280 -478 -368

Spain Exports 261 295 223 274 273 236 262 260 236 273 193 239 299Imports 337 334 342 344 333 298 340 317 323 303 387 266 360Balance -76 -40 -119 -70 -60 -62 -78 -56 -87 -31 -193 -27 -60

Central and Exports 1,156 1,030 916 1,278 1,205 1,003 1,145 1,171 984 1,041 962 1,165 1,242East Europe, Imports 1,827 1,371 1,417 1,399 1,390 1,658 1,586 1,501 1,615 1,924 1,960 1,997 1,924Russia Balance -671 -342 -501 -121 -186 -655 -441 -330 -632 -883 -999 -832 -682

Russia Exports 487 422 383 504 554 429 519 558 429 431 435 527 540Imports 1,257 888 973 899 887 1,097 1,026 951 1,092 1,330 1,304 1,464 1,301Balance -771 -465 -590 -395 -332 -668 -507 -393 -663 -899 -869 -937 -761

(EU) Exports 7,902 7,025 5,779 6,627 6,656 5,907 6,871 6,505 6,333 7,110 5,966 7,007 8,010Imports 6,841 6,228 6,517 6,511 6,677 6,734 6,503 6,804 7,181 7,159 6,914 6,596 7,327Balance 1,061 797 -738 116 -22 -827 368 -299 -849 -49 -948 411 683

Middle East Exports 2,545 2,070 1,800 2,197 1,860 1,933 2,448 2,089 2,160 2,231 1,750 2,026 2,480Imports 5,588 4,351 4,983 5,396 5,479 5,866 5,135 4,823 5,904 6,757 7,400 7,259 8,133Balance -3,043 -2,281 -3,183 -3,199 -3,619 -3,933 -2,687 -2,734 -3,745 -4,526 -5,650 -5,232 -5,654

U A E Exports 829 634 536 832 662 588 822 702 742 841 659 784 982Imports 1,537 1,038 1,499 1,612 1,809 1,688 1,522 1,155 1,766 2,056 2,009 1,889 1,993Balance -708 -404 -963 -780 -1,147 -1,100 -700 -453 -1,025 -1,215 -1,350 -1,106 -1,010

Saudi Arabia Exports 515 568 484 442 358 392 436 378 400 444 271 289 407Imports 1,769 1,559 1,713 1,677 1,670 1,968 1,500 1,801 2,065 2,402 2,817 2,653 3,097Balance -1,254 -991 -1,229 -1,235 -1,311 -1,576 -1,064 -1,423 -1,665 -1,958 -2,545 -2,364 -2,690

Kuwait Exports 173 122 121 147 120 150 193 170 158 157 143 140 128Imports 466 309 368 322 334 402 386 365 435 446 635 689 601Balance -293 -188 -246 -175 -213 -252 -193 -196 -277 -289 -492 -549 -472

Iran Exports 42 51 32 36 44 63 75 59 66 110 49 56 160Imports 252 3 281 466 428 277 449 243 367 366 436 484 493Balance -211 47 -249 -431 -384 -214 -374 -184 -302 -256 -387 -427 -334

Africa Exports 887 737 626 656 681 620 698 644 775 694 773 645 1,000Imports 702 624 596 680 442 604 555 641 641 903 680 727 802Balance 185 112 30 -24 239 16 143 3 134 -209 92 -82 198

South Africa Exports 220 215 162 207 212 189 230 202 174 237 177 227 236Imports 322 359 347 387 270 410 406 417 380 508 337 372 426Balance -102 -144 -185 -179 -58 -221 -177 -215 -206 -271 -160 -145 -190

(Notes) 1. The value of exports is based upon the F.O.B.value, while the value of imports is based upon the C. I. F.value.2."Singapore" is included in both "ASIA NIEs" and "ASEAN".3."(P)" means Provisional. "*" and "**"means "fixed" and "detailed".

― 5 ―

・ Trend of Value of Exports and Imports

-30,000

-25,000

-20,000

-15,000

-10,000

-5,000

0

5,000

10,000

15,000

20,000

25,000

30,000

80,000

60,000

40,000

20,000

0

20,000

40,000

60,000

80,000M

ar

Apr

May

Ju

nJu

lA

ug

Sep Oct

Nov

Dec

Jan

Feb

Mar

Apr

May

Ju

nJu

lA

ug

Sep Oct

Nov

Dec

Jan

Feb

Mar

Apr

May

Ju

nJu

lA

ug

Sep Oct

Nov

Dec

Jan

Feb

Mar

2014 2015 2016 2017

Exports Imports Balance

Exports

Imports

World Balance

-20,000

-15,000

-10,000

-5,000

0

5,000

10,000

15,000

20,000

40,000

30,000

20,000

10,000

0

10,000

20,000

30,000

40,000

Mar

Apr

May

Ju

nJu

lA

ug

Sep Oct

Nov

Dec

Jan

Feb

Mar

Apr

May

Ju

nJu

lA

ug

Sep Oct

Nov

Dec

Jan

Feb

Mar

Apr

May

Ju

nJu

lA

ug

Sep Oct

Nov

Dec

Jan

Feb

Mar

2014 2015 2016 2017

AsiaExports

Imports

Balance

-20,000

-15,000

-10,000

-5,000

0

5,000

10,000

15,000

20,000

40,000

30,000

20,000

10,000

0

10,000

20,000

30,000

40,000

Mar

Apr

May

Ju

nJu

lA

ug

Sep Oct

Nov

Dec

Jan

Feb

Mar

Apr

May

Ju

nJu

lA

ug

Sep Oct

Nov

Dec

Jan

Feb

Mar

Apr

May

Ju

nJu

lA

ug

Sep Oct

Nov

Dec

Jan

Feb

Mar

2014 2015 2016 2017

E UExports

Imports

Balance

-20,000

-15,000

-10,000

-5,000

0

5,000

10,000

15,000

20,000

40,000

30,000

20,000

10,000

0

10,000

20,000

30,000

40,000

Mar

Apr

May

Ju

nJu

lA

ug

Sep Oct

Nov

Dec

Jan

Feb

Mar

Apr

May

Ju

nJu

lA

ug

Sep Oct

Nov

Dec

Jan

Feb

Mar

Apr

May

Ju

nJu

lA

ug

Sep Oct

Nov

Dec

Jan

Feb

Mar

2014 2015 2016 2017

Middle EastExports

Imports

Balance

-20,000

-15,000

-10,000

-5,000

0

5,000

10,000

15,000

20,000

40,000

30,000

20,000

10,000

0

10,000

20,000

30,000

40,000

Mar

Apr

May

Ju

nJu

lA

ug

Sep Oct

Nov

Dec

Jan

Feb

Mar

Apr

May

Ju

nJu

lA

ug

Sep Oct

Nov

Dec

Jan

Feb

Mar

Apr

May

Ju

nJu

lA

ug

Sep Oct

Nov

Dec

Jan

Feb

Mar

2014 2015 2016 2017

P.R.ChinaExports

Imports

Balance

-20,000

-15,000

-10,000

-5,000

0

5,000

10,000

15,000

20,000

40,000

30,000

20,000

10,000

0

10,000

20,000

30,000

40,000

Mar

Apr

May

Ju

nJu

lA

ug

Sep Oct

Nov

Dec

Jan

Feb

Mar

Apr

May

Ju

nJu

lA

ug

Sep Oct

Nov

Dec

Jan

Feb

Mar

Apr

May

Ju

nJu

lA

ug

Sep Oct

Nov

Dec

Jan

Feb

Mar

2014 2015 2016 2017

U S AExports

Imports

Balance

― 6 ―

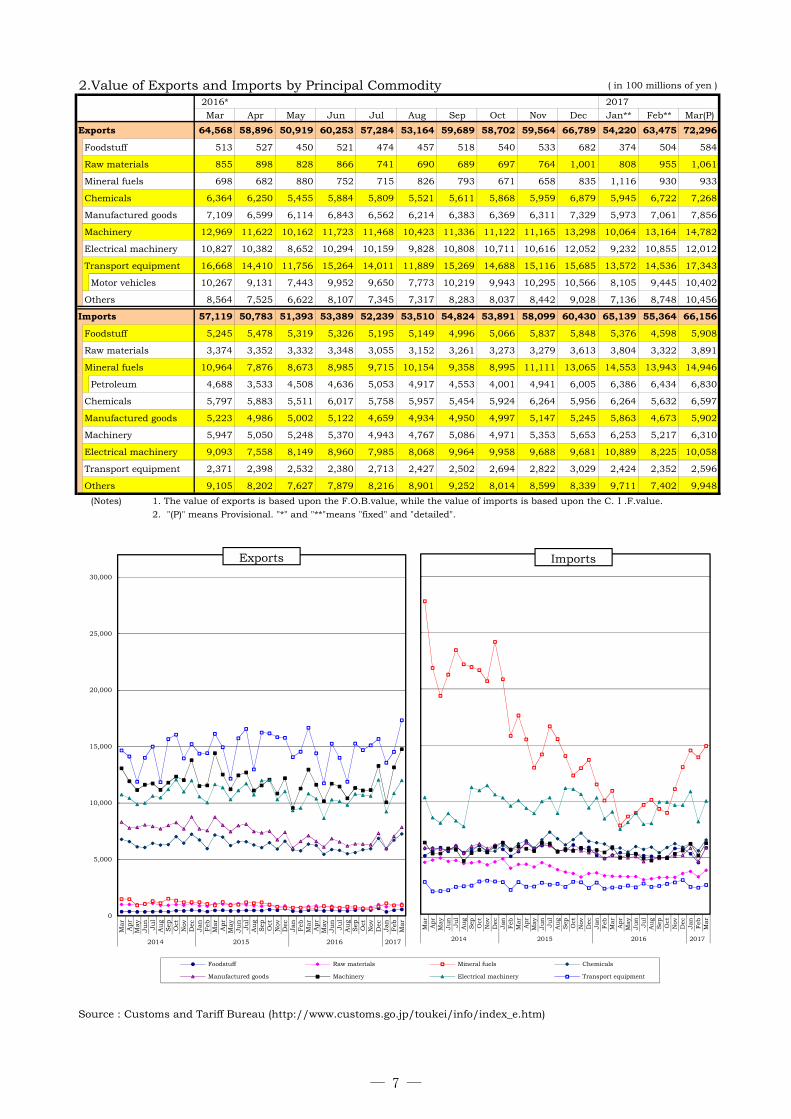

2.Value of Exports and Imports by Principal Commodity ( in 100 millions of yen )

2016* 2017Mar Apr May Jun Jul Aug Sep Oct Nov Dec Jan** Feb** Mar(P)

Exports 64,568 58,896 50,919 60,253 57,284 53,164 59,689 58,702 59,564 66,789 54,220 63,475 72,296

Foodstuff 513 527 450 521 474 457 518 540 533 682 374 504 584

Raw materials 855 898 828 866 741 690 689 697 764 1,001 808 955 1,061

Mineral fuels 698 682 880 752 715 826 793 671 658 835 1,116 930 933

Chemicals 6,364 6,250 5,455 5,884 5,809 5,521 5,611 5,868 5,959 6,879 5,945 6,722 7,268

Manufactured goods 7,109 6,599 6,114 6,843 6,562 6,214 6,383 6,369 6,311 7,329 5,973 7,061 7,856

Machinery 12,969 11,622 10,162 11,723 11,468 10,423 11,336 11,122 11,165 13,298 10,064 13,164 14,782

Electrical machinery 10,827 10,382 8,652 10,294 10,159 9,828 10,808 10,711 10,616 12,052 9,232 10,855 12,012

Transport equipment 16,668 14,410 11,756 15,264 14,011 11,889 15,269 14,688 15,116 15,685 13,572 14,536 17,343

Motor vehicles 10,267 9,131 7,443 9,952 9,650 7,773 10,219 9,943 10,295 10,566 8,105 9,445 10,402

Others 8,564 7,525 6,622 8,107 7,345 7,317 8,283 8,037 8,442 9,028 7,136 8,748 10,456

Imports 57,119 50,783 51,393 53,389 52,239 53,510 54,824 53,891 58,099 60,430 65,139 55,364 66,156

Foodstuff 5,245 5,478 5,319 5,326 5,195 5,149 4,996 5,066 5,837 5,848 5,376 4,598 5,908

Raw materials 3,374 3,352 3,332 3,348 3,055 3,152 3,261 3,273 3,279 3,613 3,804 3,322 3,891

Mineral fuels 10,964 7,876 8,673 8,985 9,715 10,154 9,358 8,995 11,111 13,065 14,553 13,943 14,946

Petroleum 4,688 3,533 4,508 4,636 5,053 4,917 4,553 4,001 4,941 6,005 6,386 6,434 6,830

Chemicals 5,797 5,883 5,511 6,017 5,758 5,957 5,454 5,924 6,264 5,956 6,264 5,632 6,597

Manufactured goods 5,223 4,986 5,002 5,122 4,659 4,934 4,950 4,997 5,147 5,245 5,863 4,673 5,902

Machinery 5,947 5,050 5,248 5,370 4,943 4,767 5,086 4,971 5,353 5,653 6,253 5,217 6,310

Electrical machinery 9,093 7,558 8,149 8,960 7,985 8,068 9,964 9,958 9,688 9,681 10,889 8,225 10,058

Transport equipment 2,371 2,398 2,532 2,380 2,713 2,427 2,502 2,694 2,822 3,029 2,424 2,352 2,596

Others 9,105 8,202 7,627 7,879 8,216 8,901 9,252 8,014 8,599 8,339 9,711 7,402 9,948

(Notes) 1. The value of exports is based upon the F.O.B.value, while the value of imports is based upon the C.Ⅰ.F.value.2. "(P)" means Provisional. "*" and "**"means "fixed" and "detailed".

Source : Customs and Tariff Bureau (http://www.customs.go.jp/toukei/info/index_e.htm)

0

5,000

10,000

15,000

20,000

25,000

30,000

Mar

Apr

May

Ju

nJu

lA

ug

Sep Oct

Nov

Dec

Jan

Feb

Mar

Apr

May

Ju

nJu

lA

ug

Sep Oct

Nov

Dec

Jan

Feb

Mar

Apr

May

Ju

nJu

lA

ug

Sep Oct

Nov

Dec

Jan

Feb

Mar

2014 2015 2016 2017

Foodstuff Raw materials Mineral fuels Chemicals

Manufactured goods Machinery Electrical machinery Transport equipment

Mar

Apr

May

Ju

nJu

lA

ug

Sep Oct

Nov

Dec

Jan Feb

Mar

Apr

May

Ju

nJu

lA

ug

Sep Oct

Nov

Dec

Jan Feb

Mar

Apr

May

Ju

nJu

lA

ug

Sep Oct

Nov

Dec

Jan Feb

Mar

2014 2015 2016 2017

Exports Imports

― 7 ―

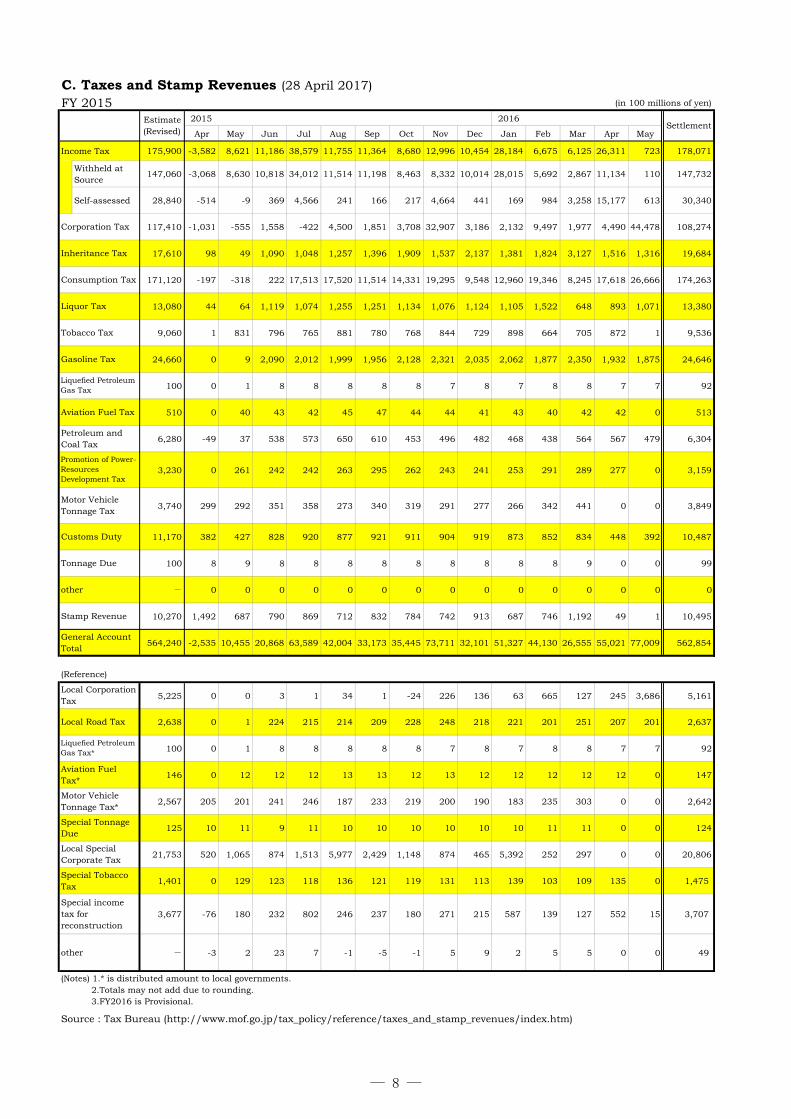

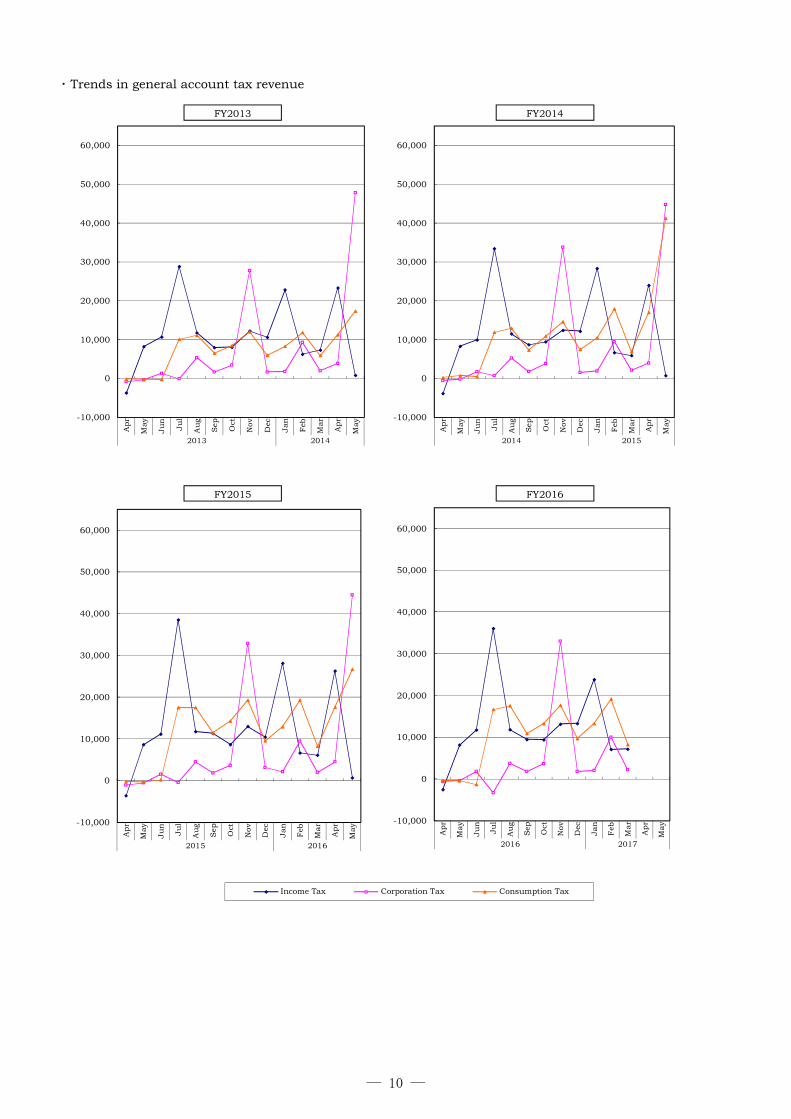

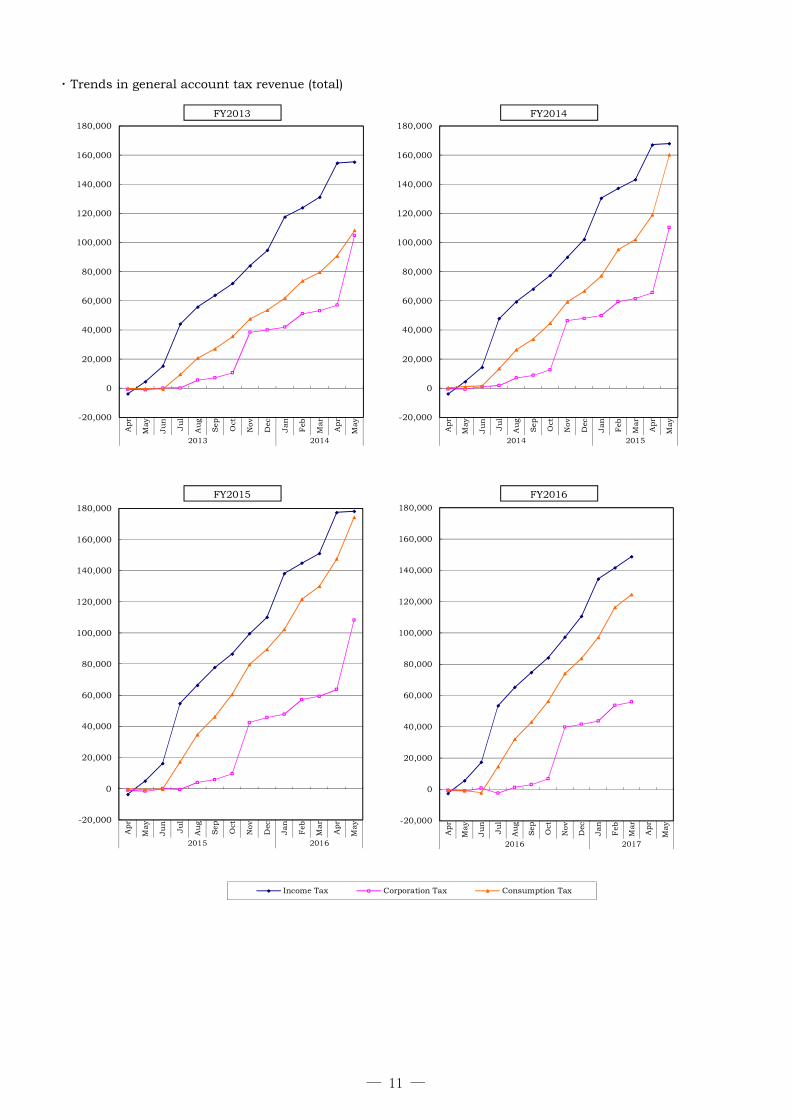

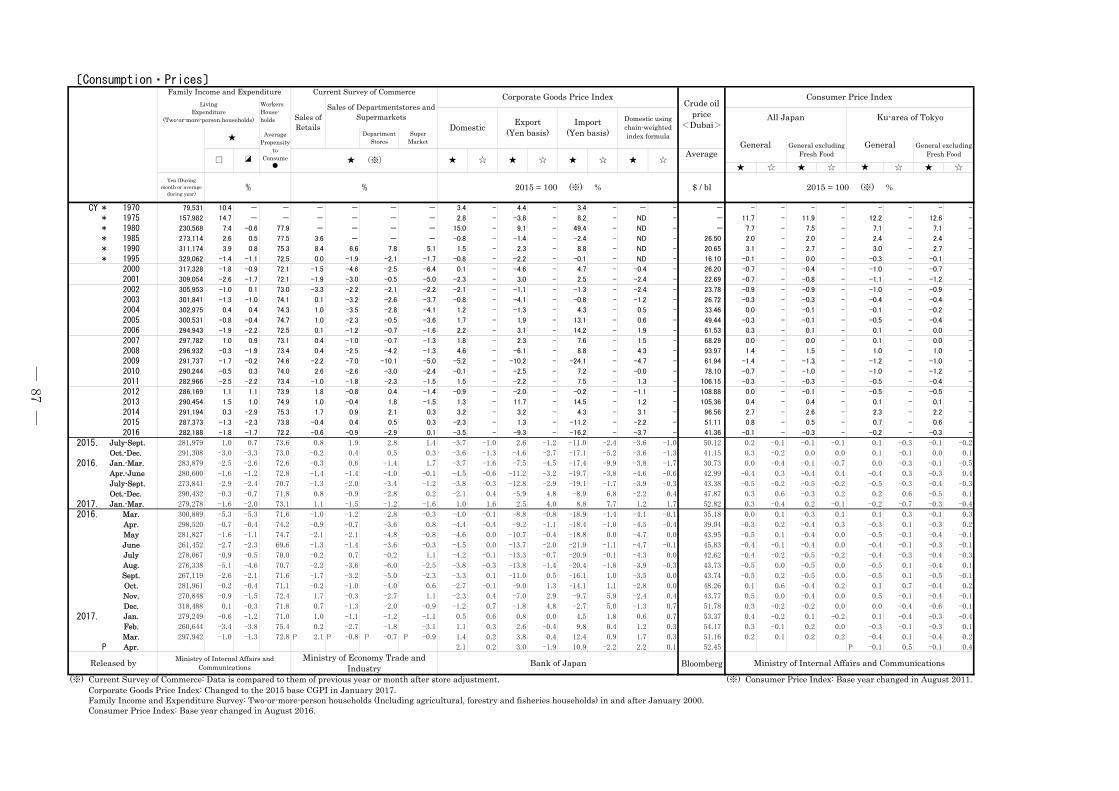

C. Taxes and Stamp Revenues (28 April 2017)FY 2015 (in 100 millions of yen)

2015 2016

Apr May Jun Jul Aug Sep Oct Nov Dec Jan Feb Mar Apr May

Income Tax 175,900 -3,582 8,621 11,186 38,579 11,755 11,364 8,680 12,996 10,454 28,184 6,675 6,125 26,311 723 178,071

Withheld atSource

147,060 -3,068 8,630 10,818 34,012 11,514 11,198 8,463 8,332 10,014 28,015 5,692 2,867 11,134 110 147,732

Self-assessed 28,840 -514 -9 369 4,566 241 166 217 4,664 441 169 984 3,258 15,177 613 30,340

117,410 -1,031 -555 1,558 -422 4,500 1,851 3,708 32,907 3,186 2,132 9,497 1,977 4,490 44,478 108,274

17,610 98 49 1,090 1,048 1,257 1,396 1,909 1,537 2,137 1,381 1,824 3,127 1,516 1,316 19,684

171,120 -197 -318 222 17,513 17,520 11,514 14,331 19,295 9,548 12,960 19,346 8,245 17,618 26,666 174,263

13,080 44 64 1,119 1,074 1,255 1,251 1,134 1,076 1,124 1,105 1,522 648 893 1,071 13,380

9,060 1 831 796 765 881 780 768 844 729 898 664 705 872 1 9,536

24,660 0 9 2,090 2,012 1,999 1,956 2,128 2,321 2,035 2,062 1,877 2,350 1,932 1,875 24,646

100 0 1 8 8 8 8 8 7 8 7 8 8 7 7 92

510 0 40 43 42 45 47 44 44 41 43 40 42 42 0 513

6,280 -49 37 538 573 650 610 453 496 482 468 438 564 567 479 6,304

3,230 0 261 242 242 263 295 262 243 241 253 291 289 277 0 3,159

3,740 299 292 351 358 273 340 319 291 277 266 342 441 0 0 3,849

11,170 382 427 828 920 877 921 911 904 919 873 852 834 448 392 10,487

100 8 9 8 8 8 8 8 8 8 8 8 9 0 0 99

- 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0

10,270 1,492 687 790 869 712 832 784 742 913 687 746 1,192 49 1 10,495

564,240 -2,535 10,455 20,868 63,589 42,004 33,173 35,445 73,711 32,101 51,327 44,130 26,555 55,021 77,009 562,854

(Reference)

5,225 0 0 3 1 34 1 -24 226 136 63 665 127 245 3,686 5,161

2,638 0 1 224 215 214 209 228 248 218 221 201 251 207 201 2,637

100 0 1 8 8 8 8 8 7 8 7 8 8 7 7 92

146 0 12 12 12 13 13 12 13 12 12 12 12 12 0 147

2,567 205 201 241 246 187 233 219 200 190 183 235 303 0 0 2,642

125 10 11 9 11 10 10 10 10 10 10 11 11 0 0 124

21,753 520 1,065 874 1,513 5,977 2,429 1,148 874 465 5,392 252 297 0 0 20,806

1,401 0 129 123 118 136 121 119 131 113 139 103 109 135 0 1,475

3,677 -76 180 232 802 246 237 180 271 215 587 139 127 552 15 3,707

- -3 2 23 7 -1 -5 -1 5 9 2 5 5 0 0 49other

Estimate(Revised)

Corporation Tax

Consumption Tax

Inheritance Tax

Tobacco Tax

Aviation Fuel Tax

Motor VehicleTonnage Tax

Liquor Tax

Local SpecialCorporate Tax

Liquefied PetroleumGas Tax

Settlement

(Notes) 1.* is distributed amount to local governments. 2.Totals may not add due to rounding. 3.FY2016 is Provisional.

Gasoline Tax

other

General AccountTotal

Local CorporationTax

Stamp Revenue

Customs Duty

Tonnage Due

Source : Tax Bureau (http://www.mof.go.jp/tax_policy/reference/taxes_and_stamp_revenues/index.htm)

Special TobaccoTax

Special incometax forreconstruction

Petroleum andCoal Tax

Motor VehicleTonnage Tax*

Aviation FuelTax*

Liquefied PetroleumGas Tax*

Local Road Tax

Promotion of Power-ResourcesDevelopment Tax

Special TonnageDue

― 8 ―

FY 2016* (in 100 millions of yen)

2016 2017

Apr May Jun Jul Aug Sep Oct Nov Dec Jan Feb Mar(P) Apr May

Income Tax 177,100 -2,513 8,168 11,740 36,085 11,812 9,484 9,405 13,182 13,333 23,873 7,067 7,181 148,817

Withheld atSource

146,560 -2,062 8,184 11,431 31,282 11,544 9,286 9,196 8,188 12,885 23,711 6,133 3,548 133,326

Self-assessed 30,540 -451 -16 308 4,804 267 198 209 4,994 449 162 934 3,632 15,491

111,360 -586 -359 1,819 -3,278 3,749 1,790 3,687 33,035 1,811 2,051 10,030 2,187 55,937

21,100 70 45 1,648 1,835 1,489 1,611 1,659 1,669 1,988 1,457 1,994 3,105 18,568

168,010 -360 -357 -1,337 16,657 17,569 10,903 13,309 17,680 9,721 13,336 19,161 8,277 124,559

13,590 37 61 1,165 1,025 1,246 1,180 1,138 1,068 1,074 1,131 1,474 677 11,277

9,230 3 754 718 810 818 788 799 739 742 865 635 652 8,323

23,860 0 38 2,093 2,184 1,757 1,868 2,412 2,005 2,038 2,036 1,904 2,278 20,613

90 0 1 7 7 7 8 8 7 7 7 8 7 74

520 0 40 42 42 45 47 44 44 42 43 43 39 470

6,880 -87 30 619 643 527 757 573 535 583 523 445 675 5,824

3,200 0 250 237 240 265 291 284 252 247 264 297 289 2,916

3,850 280 296 324 313 291 349 320 324 297 293 351 477 3,914

9,190 334 373 752 764 787 777 774 826 789 817 728 851 8,573

100 8 8 8 8 8 9 8 8 9 8 8 8 98

- 0 0 0 0 0 0 0 0 0 0 0 0 0

10,520 1,529 724 856 818 783 889 798 774 897 718 763 1,214 10,762

558,600 -1,286 10,073 20,691 58,154 41,152 30,750 35,220 72,147 33,578 47,421 44,907 27,918 420,725

(Reference)

6,293 -4 -4 173 180 461 134 236 1,786 81 97 515 100 3,756

2,553 0 4 224 234 188 200 258 215 218 218 204 244 2,205

90 0 1 7 7 7 8 8 7 7 7 8 7 74

149 0 12 12 12 13 13 13 13 12 12 12 11 134

2,642 192 203 223 215 199 240 220 222 204 201 241 327 2,686

125 10 10 10 10 11 11 11 10 11 10 10 11 123

17,565 481 764 606 1,828 3,788 1,752 995 899 454 5,661 277 311 17,816

1,428 0 117 111 125 127 122 124 114 115 134 98 101 1,288

3,714 -54 171 245 751 247 198 196 276 277 496 147 150 3,099

- 3 1 11 3 2 1 2 2 7 -2 3 3 35

Tonnage Due

Consumption Tax

Inheritance Tax

Corporation Tax

Estimate(Revised)

Gasoline Tax

Tobacco Tax

Liquor Tax

Special TonnageDue

Special incometax forreconstruction

Total(P)

Local CorporationTax

General AccountTotal

Customs Duty

Motor VehicleTonnage Tax

Promotion of Power-ResourcesDevelopment Tax

Petroleum andCoal Tax

Local SpecialCorporate Tax

Stamp Revenue

Special TobaccoTax

other

Motor VehicleTonnage Tax*

Aviation FuelTax*

Liquefied PetroleumGas Tax*

Local Road Tax

Aviation Fuel Tax

Liquefied PetroleumGas Tax

other

― 9 ―

・ Trends in general account tax revenue

-10,000

0

10,000

20,000

30,000

40,000

50,000

60,000

Apr

May

Ju

n

Ju

l

Au

g

Sep Oct

Nov

Dec

Jan Feb

Mar

Apr

May

2015 2016

Income Tax Corporation Tax Consumption Tax

-10,000

0

10,000

20,000

30,000

40,000

50,000

60,000

Apr

May

Ju

n

Ju

l

Au

g

Sep Oct

Nov

Dec

Jan Feb

Mar

Apr

May

2016 2017

-10,000

0

10,000

20,000

30,000

40,000

50,000

60,000

Apr

May

Ju

n

Ju

l

Au

g

Sep Oct

Nov

Dec

Jan Feb

Mar

Apr

May

2013 2014

FY2013

-10,000

0

10,000

20,000

30,000

40,000

50,000

60,000

Apr

May

Ju

n

Ju

l

Au

g

Sep Oct

Nov

Dec

Jan Feb

Mar

Apr

May

2014 2015

FY2014

FY2015 FY2016

― 10 ―

・ Trends in general account tax revenue (total)

-20,000

0

20,000

40,000

60,000

80,000

100,000

120,000

140,000

160,000

180,000

Apr

May

Ju

n

Ju

l

Au

g

Sep Oct

Nov

Dec

Jan Feb

Mar

Apr

May

2015 2016

Income Tax Corporation Tax Consumption Tax

-20,000

0

20,000

40,000

60,000

80,000

100,000

120,000

140,000

160,000

180,000

Apr

May

Ju

n

Ju

l

Au

g

Sep Oct

Nov

Dec

Jan Feb

Mar

Apr

May

2016 2017

-20,000

0

20,000

40,000

60,000

80,000

100,000

120,000

140,000

160,000

180,000A

pr

May

Ju

n

Ju

l

Au

g

Sep Oct

Nov

Dec

Jan Feb

Mar

Apr

May

2013 2014

FY2013

-20,000

0

20,000

40,000

60,000

80,000

100,000

120,000

140,000

160,000

180,000

Apr

May

Ju

n

Ju

l

Au

g

Sep Oct

Nov

Dec

Jan Feb

Mar

Apr

May

2014 2015

FY2014

FY2015 FY2016

― 11 ―

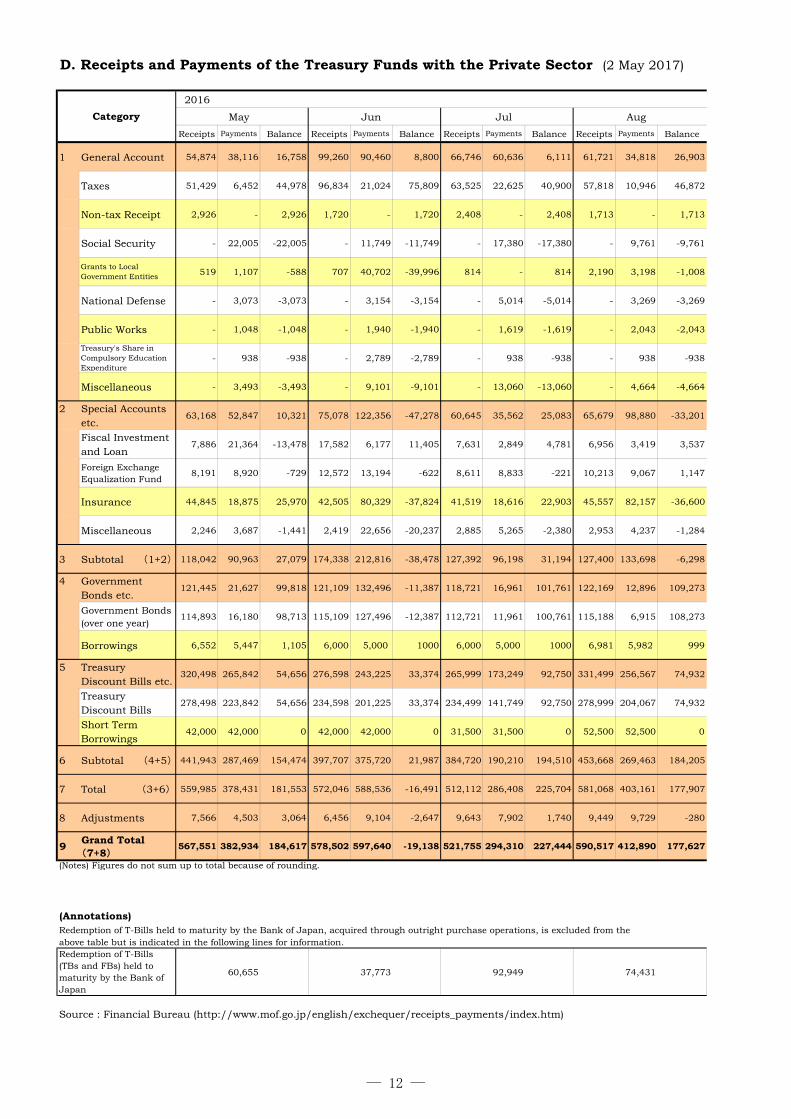

2016

May Jun Jul Aug

Receipts Payments Balance Receipts Payments Balance Receipts Payments Balance Receipts Payments Balance

1 General Account 54,874 38,116 16,758 99,260 90,460 8,800 66,746 60,636 6,111 61,721 34,818 26,903

Taxes 51,429 6,452 44,978 96,834 21,024 75,809 63,525 22,625 40,900 57,818 10,946 46,872

Non-tax Receipt 2,926 - 2,926 1,720 - 1,720 2,408 - 2,408 1,713 - 1,713

Social Security - 22,005 -22,005 - 11,749 -11,749 - 17,380 -17,380 - 9,761 -9,761

Grants to LocalGovernment Entities 519 1,107 -588 707 40,702 -39,996 814 - 814 2,190 3,198 -1,008

National Defense - 3,073 -3,073 - 3,154 -3,154 - 5,014 -5,014 - 3,269 -3,269

Public Works - 1,048 -1,048 - 1,940 -1,940 - 1,619 -1,619 - 2,043 -2,043

Treasury's Share inCompulsory EducationExpenditure

- 938 -938 - 2,789 -2,789 - 938 -938 - 938 -938

Miscellaneous - 3,493 -3,493 - 9,101 -9,101 - 13,060 -13,060 - 4,664 -4,664

2 Special Accountsetc.

63,168 52,847 10,321 75,078 122,356 -47,278 60,645 35,562 25,083 65,679 98,880 -33,201

Fiscal Investmentand Loan

7,886 21,364 -13,478 17,582 6,177 11,405 7,631 2,849 4,781 6,956 3,419 3,537

Foreign ExchangeEqualization Fund

8,191 8,920 -729 12,572 13,194 -622 8,611 8,833 -221 10,213 9,067 1,147

Insurance 44,845 18,875 25,970 42,505 80,329 -37,824 41,519 18,616 22,903 45,557 82,157 -36,600

Miscellaneous 2,246 3,687 -1,441 2,419 22,656 -20,237 2,885 5,265 -2,380 2,953 4,237 -1,284

3 Subtotal (1+2) 118,042 90,963 27,079 174,338 212,816 -38,478 127,392 96,198 31,194 127,400 133,698 -6,298

4 GovernmentBonds etc.

121,445 21,627 99,818 121,109 132,496 -11,387 118,721 16,961 101,761 122,169 12,896 109,273

Government Bonds(over one year)

114,893 16,180 98,713 115,109 127,496 -12,387 112,721 11,961 100,761 115,188 6,915 108,273

Borrowings 6,552 5,447 1,105 6,000 5,000 1000 6,000 5,000 1000 6,981 5,982 999

5 TreasuryDiscount Bills etc.

320,498 265,842 54,656 276,598 243,225 33,374 265,999 173,249 92,750 331,499 256,567 74,932

TreasuryDiscount Bills

278,498 223,842 54,656 234,598 201,225 33,374 234,499 141,749 92,750 278,999 204,067 74,932

Short TermBorrowings

42,000 42,000 0 42,000 42,000 0 31,500 31,500 0 52,500 52,500 0

6 Subtotal (4+5) 441,943 287,469 154,474 397,707 375,720 21,987 384,720 190,210 194,510 453,668 269,463 184,205

7 Total (3+6) 559,985 378,431 181,553 572,046 588,536 -16,491 512,112 286,408 225,704 581,068 403,161 177,907

8 Adjustments 7,566 4,503 3,064 6,456 9,104 -2,647 9,643 7,902 1,740 9,449 9,729 -280

9Grand Total(7+8)

567,551 382,934 184,617 578,502 597,640 -19,138 521,755 294,310 227,444 590,517 412,890 177,627

(Notes) Figures do not sum up to total because of rounding.

(Annotations)Redemption of T-Bills held to maturity by the Bank of Japan, acquired through outright purchase operations, is excluded from theabove table but is indicated in the following lines for information.

60,655 37,773 92,949 74,431

Source : Financial Bureau (http://www.mof.go.jp/english/exchequer/receipts_payments/index.htm)

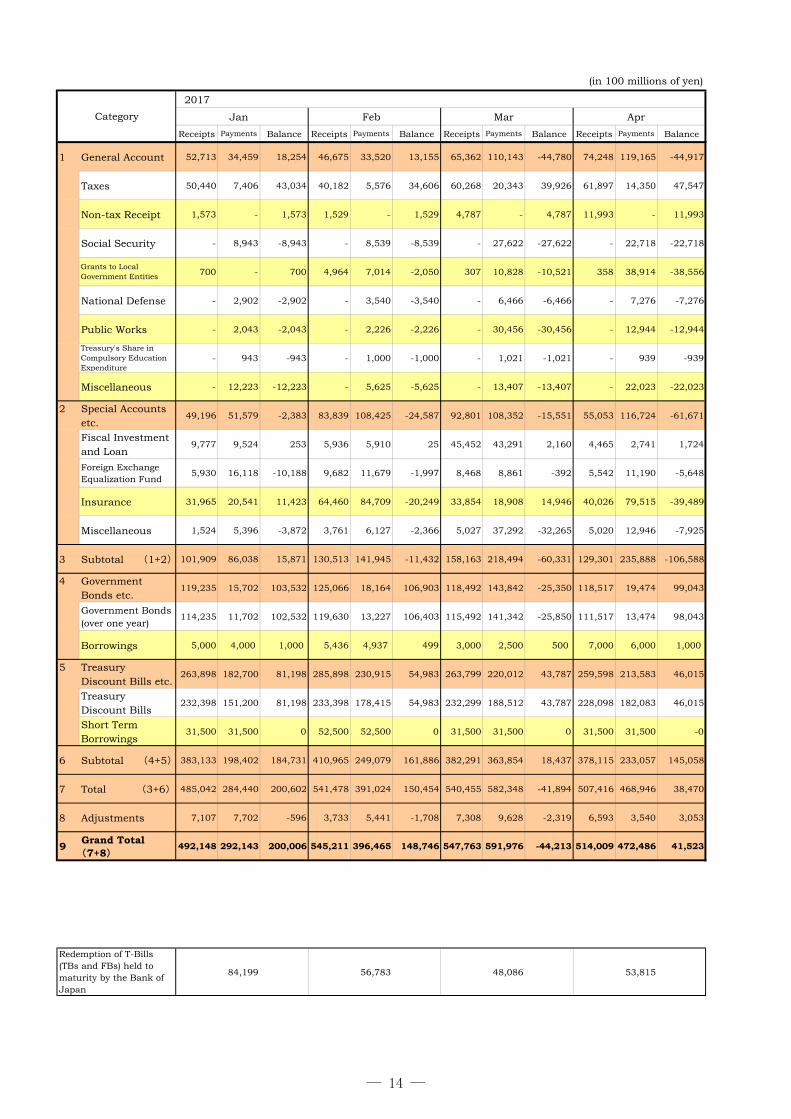

D. Receipts and Payments of the Treasury Funds with the Private Sector (2 May 2017)

Redemption of T-Bills(TBs and FBs) held tomaturity by the Bank ofJapan

Category

― 12 ―

(in 100 millions of yen)

2016

Sep Oct Nov Dec

Receipts Payments Balance Receipts Payments Balance Receipts Payments Balance Receipts Payments Balance

54,173 73,495 -19,322 43,748 49,834 -6,086 50,006 81,821 -31,815 88,378 55,607 32,771 1

49,357 8,352 41,005 40,598 9,560 31,038 47,386 7,183 40,203 84,529 10,639 73,890 Taxes

1,590 - 1,590 1,391 - 1,391 1,605 - 1,605 2,557 - 2,557 Non-tax Receipt

- 11,967 -11,967 - 21,594 -21,594 - 13,825 -13,825 - 15,643 -15,643 Social Security

3,226 43,441 -40,215 1,759 0 1,759 1,015 47,474 -46,459 1,292 3,572 -2,280Grants to LocalGovernment Entities

- 2,545 -2,545 - 3,080 -3,080 - 2,732 -2,732 - 5,558 -5,558 National Defense

- 2,138 -2,138 - 2,098 -2,098 - 2,339 -2,339 - 3,226 -3,226 Public Works

- 938 -938 - 938 -938 - 943 -943 - 2,929 -2,929Treasury's Share inCompulsory EducationExpenditure

- 4,113 -4,113 - 12,563 -12,563 - 7,326 -7,326 - 14,041 -14,041 Miscellaneous

104,063 61,396 42,667 58,939 104,050 -45,111 58,420 52,498 5,922 65,482 142,813 -77,3312

42,662 5,025 37,637 6,190 4,629 1,560 6,548 21,827 -15,280 10,773 6,042 4,731Fiscal Investmentand Loan

10,818 10,352 466 14,876 11,705 3,171 12,598 8,957 3,641 9,584 8,497 1,087Foreign ExchangeEqualization Fund

47,891 22,013 25,879 35,711 81,052 -45,340 37,285 15,586 21,699 38,466 81,204 -42,738 Insurance

2,692 24,006 -21,314 2,162 6,664 -4,502 1,989 6,128 -4,139 6,659 47,070 -40,411 Miscellaneous

158,236 134,890 23,345 102,687 153,884 -51,197 108,426 134,319 -25,893 153,861 198,420 -44,559 3

115,321 133,195 -17,873 125,937 21,300 104,637 119,539 24,423 95,116 114,099 154,424 -40,3254

109,322 127,195 -17,873 120,437 16,300 104,137 113,877 18,980 94,897 108,099 149,424 -41,325Government Bonds(overone year)

6,000 6,000 -0 5,500 5,000 500 5,662 5,443 219 6,000 5,000 1,000 Borrowings

267,498 222,945 44,552 310,698 210,278 100,421 277,598 208,295 69,302 278,699 216,181 62,5185

235,998 191,445 44,553 279,198 178,778 100,421 235,597 166,295 69,302 236,698 174,181 62,518TreasuryDiscount Bills

31,500 31,500 -0 31,500 31,500 0 42,000 42,000 -0 42,000 42,000 0Short TermBorrowings

382,819 356,140 26,679 436,635 231,578 205,058 397,137 232,718 164,418 392,797 370,605 22,193 6

541,055 491,030 50,025 539,323 385,462 153,861 505,563 367,038 138,525 546,658 569,025 -22,367 7

5,976 10,165 -4,189 5,186 4,932 254 6,478 6,487 -8 10,983 14,166 -3,182 8

547,030 501,195 45,835 544,509 390,394 154,115 512,041 373,524 138,517 557,641 583,191 -25,549 9

43,153 99,221 69,204 61,817

Category

Redemption of T-Bills (TBsand FBs) held to maturityby the Bank of Japan

Grand Total(7+8)

Adjustments

General Account

Subtotal (4+5)

Total (3+6)

Special Accountsetc.

Subtotal (1+2)

Government Bondsetc.

Treasury DiscountBills etc.

― 13 ―

(in 100 millions of yen)

2017

Jan Feb Mar Apr

Receipts Payments Balance Receipts Payments Balance Receipts Payments Balance Receipts Payments Balance

1 General Account 52,713 34,459 18,254 46,675 33,520 13,155 65,362 110,143 -44,780 74,248 119,165 -44,917

Taxes 50,440 7,406 43,034 40,182 5,576 34,606 60,268 20,343 39,926 61,897 14,350 47,547

Non-tax Receipt 1,573 - 1,573 1,529 - 1,529 4,787 - 4,787 11,993 - 11,993

Social Security - 8,943 -8,943 - 8,539 -8,539 - 27,622 -27,622 - 22,718 -22,718

Grants to LocalGovernment Entities 700 - 700 4,964 7,014 -2,050 307 10,828 -10,521 358 38,914 -38,556

National Defense - 2,902 -2,902 - 3,540 -3,540 - 6,466 -6,466 - 7,276 -7,276

Public Works - 2,043 -2,043 - 2,226 -2,226 - 30,456 -30,456 - 12,944 -12,944

Treasury's Share inCompulsory EducationExpenditure

- 943 -943 - 1,000 -1,000 - 1,021 -1,021 - 939 -939

Miscellaneous - 12,223 -12,223 - 5,625 -5,625 - 13,407 -13,407 - 22,023 -22,023

2 Special Accountsetc.

49,196 51,579 -2,383 83,839 108,425 -24,587 92,801 108,352 -15,551 55,053 116,724 -61,671

Fiscal Investmentand Loan

9,777 9,524 253 5,936 5,910 25 45,452 43,291 2,160 4,465 2,741 1,724

Foreign ExchangeEqualization Fund

5,930 16,118 -10,188 9,682 11,679 -1,997 8,468 8,861 -392 5,542 11,190 -5,648

Insurance 31,965 20,541 11,423 64,460 84,709 -20,249 33,854 18,908 14,946 40,026 79,515 -39,489

Miscellaneous 1,524 5,396 -3,872 3,761 6,127 -2,366 5,027 37,292 -32,265 5,020 12,946 -7,925

3 Subtotal (1+2) 101,909 86,038 15,871 130,513 141,945 -11,432 158,163 218,494 -60,331 129,301 235,888 -106,588

4 GovernmentBonds etc.

119,235 15,702 103,532 125,066 18,164 106,903 118,492 143,842 -25,350 118,517 19,474 99,043

Government Bonds(over one year)

114,235 11,702 102,532 119,630 13,227 106,403 115,492 141,342 -25,850 111,517 13,474 98,043

Borrowings 5,000 4,000 1,000 5,436 4,937 499 3,000 2,500 500 7,000 6,000 1,000

5 TreasuryDiscount Bills etc.

263,898 182,700 81,198 285,898 230,915 54,983 263,799 220,012 43,787 259,598 213,583 46,015

TreasuryDiscount Bills

232,398 151,200 81,198 233,398 178,415 54,983 232,299 188,512 43,787 228,098 182,083 46,015

Short TermBorrowings

31,500 31,500 0 52,500 52,500 0 31,500 31,500 0 31,500 31,500 -0

6 Subtotal (4+5) 383,133 198,402 184,731 410,965 249,079 161,886 382,291 363,854 18,437 378,115 233,057 145,058

7 Total (3+6) 485,042 284,440 200,602 541,478 391,024 150,454 540,455 582,348 -41,894 507,416 468,946 38,470

8 Adjustments 7,107 7,702 -596 3,733 5,441 -1,708 7,308 9,628 -2,319 6,593 3,540 3,053

9Grand Total(7+8)

492,148 292,143 200,006 545,211 396,465 148,746 547,763 591,976 -44,213 514,009 472,486 41,523

84,199 56,783 48,086 53,815

Category

Redemption of T-Bills(TBs and FBs) held tomaturity by the Bank ofJapan

― 14 ―

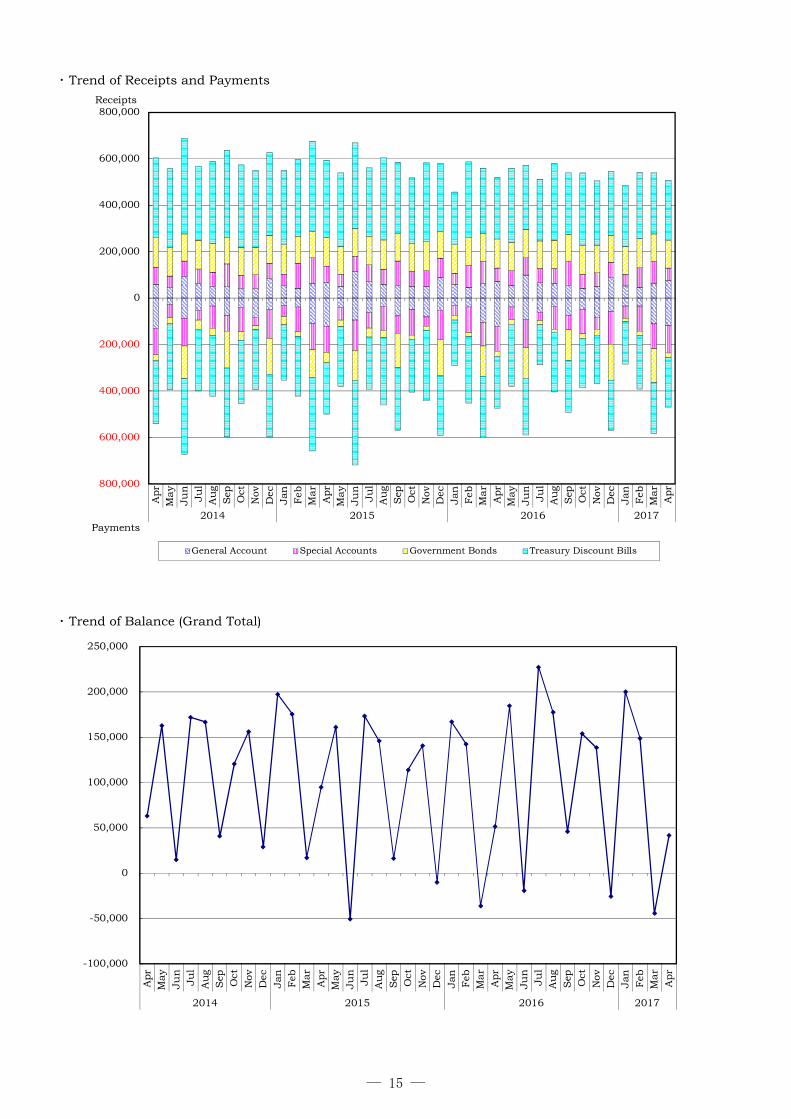

・ Trend of Receipts and Payments

・ Trend of Balance (Grand Total)

800,000

600,000

400,000

200,000

0

200,000

400,000

600,000

800,000

Apr

May

Ju

nJu

lA

ug

Sep Oct

Nov

Dec

Jan Feb

Mar

Apr

May

Ju

nJu

lA

ug

Sep Oct

Nov

Dec

Jan Feb

Mar

Apr

May

Ju

nJu

lA

ug

Sep Oct

Nov

Dec

Jan Feb

Mar

Apr

2014 2015 2016 2017

General Account Special Accounts Government Bonds Treasury Discount Bills

-100,000

-50,000

0

50,000

100,000

150,000

200,000

250,000

Apr

May

Ju

nJu

lA

ug

Sep Oct

Nov

Dec

Jan Feb

Mar

Apr

May

Ju

nJu

lA

ug

Sep Oct

Nov

Dec

Jan Feb

Mar

Apr

May

Ju

nJu

lA

ug

Sep Oct

Nov

Dec

Jan Feb

Mar

Apr

2014 2015 2016 2017

Receipts

Payments

― 15 ―

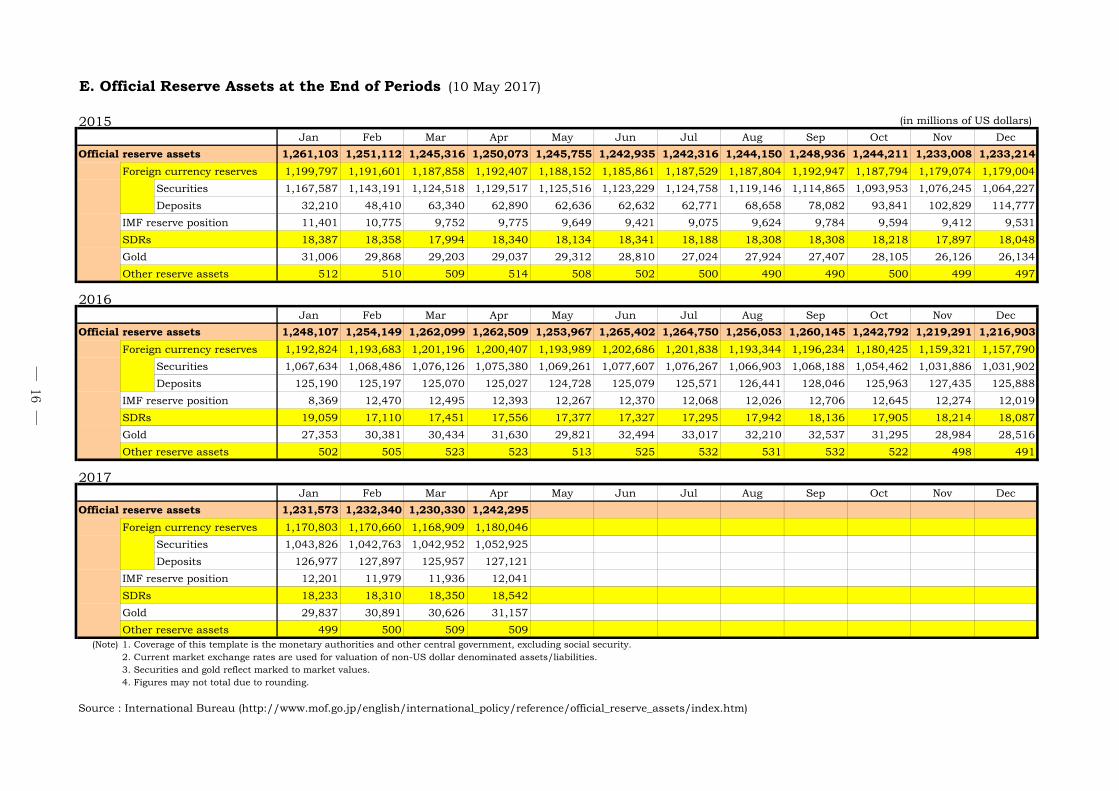

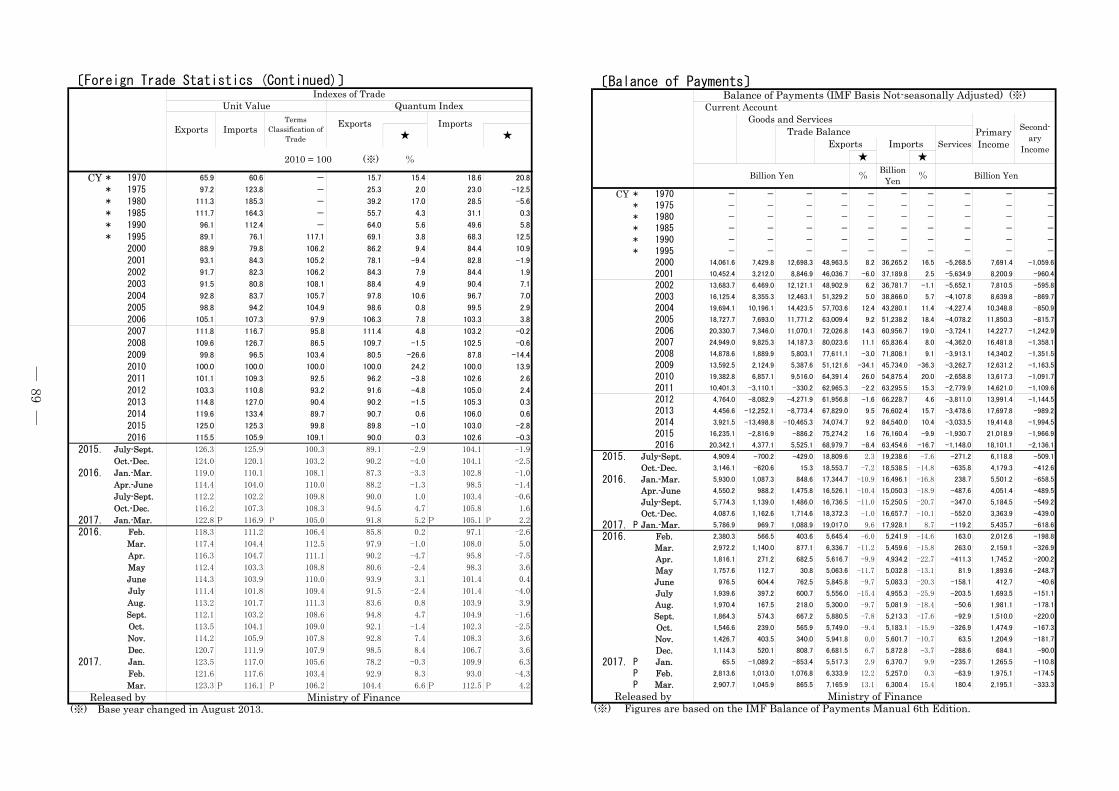

E. Official Reserve Assets at the End of Periods (10 May 2017)

2015 (in millions of US dollars)

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

Official reserve assets 1,261,103 1,251,112 1,245,316 1,250,073 1,245,755 1,242,935 1,242,316 1,244,150 1,248,936 1,244,211 1,233,008 1,233,214

Foreign currency reserves 1,199,797 1,191,601 1,187,858 1,192,407 1,188,152 1,185,861 1,187,529 1,187,804 1,192,947 1,187,794 1,179,074 1,179,004

Securities 1,167,587 1,143,191 1,124,518 1,129,517 1,125,516 1,123,229 1,124,758 1,119,146 1,114,865 1,093,953 1,076,245 1,064,227

Deposits 32,210 48,410 63,340 62,890 62,636 62,632 62,771 68,658 78,082 93,841 102,829 114,777

IMF reserve position 11,401 10,775 9,752 9,775 9,649 9,421 9,075 9,624 9,784 9,594 9,412 9,531

SDRs 18,387 18,358 17,994 18,340 18,134 18,341 18,188 18,308 18,308 18,218 17,897 18,048

Gold 31,006 29,868 29,203 29,037 29,312 28,810 27,024 27,924 27,407 28,105 26,126 26,134

Other reserve assets 512 510 509 514 508 502 500 490 490 500 499 497

2016Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

Official reserve assets 1,248,107 1,254,149 1,262,099 1,262,509 1,253,967 1,265,402 1,264,750 1,256,053 1,260,145 1,242,792 1,219,291 1,216,903

Foreign currency reserves 1,192,824 1,193,683 1,201,196 1,200,407 1,193,989 1,202,686 1,201,838 1,193,344 1,196,234 1,180,425 1,159,321 1,157,790

Securities 1,067,634 1,068,486 1,076,126 1,075,380 1,069,261 1,077,607 1,076,267 1,066,903 1,068,188 1,054,462 1,031,886 1,031,902

Deposits 125,190 125,197 125,070 125,027 124,728 125,079 125,571 126,441 128,046 125,963 127,435 125,888

IMF reserve position 8,369 12,470 12,495 12,393 12,267 12,370 12,068 12,026 12,706 12,645 12,274 12,019

SDRs 19,059 17,110 17,451 17,556 17,377 17,327 17,295 17,942 18,136 17,905 18,214 18,087

Gold 27,353 30,381 30,434 31,630 29,821 32,494 33,017 32,210 32,537 31,295 28,984 28,516

Other reserve assets 502 505 523 523 513 525 532 531 532 522 498 491

2017Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

Official reserve assets 1,231,573 1,232,340 1,230,330 1,242,295

Foreign currency reserves 1,170,803 1,170,660 1,168,909 1,180,046

Securities 1,043,826 1,042,763 1,042,952 1,052,925

Deposits 126,977 127,897 125,957 127,121

IMF reserve position 12,201 11,979 11,936 12,041

SDRs 18,233 18,310 18,350 18,542

Gold 29,837 30,891 30,626 31,157

Other reserve assets 499 500 509 509(Note) 1. Coverage of this template is the monetary authorities and other central government, excluding social security.

2. Current market exchange rates are used for valuation of non-US dollar denominated assets/liabilities.3. Securities and gold reflect marked to market values.4. Figures may not total due to rounding.

Source : International Bureau (http://www.mof.go.jp/english/international_policy/reference/official_reserve_assets/index.htm)

― 16 ―

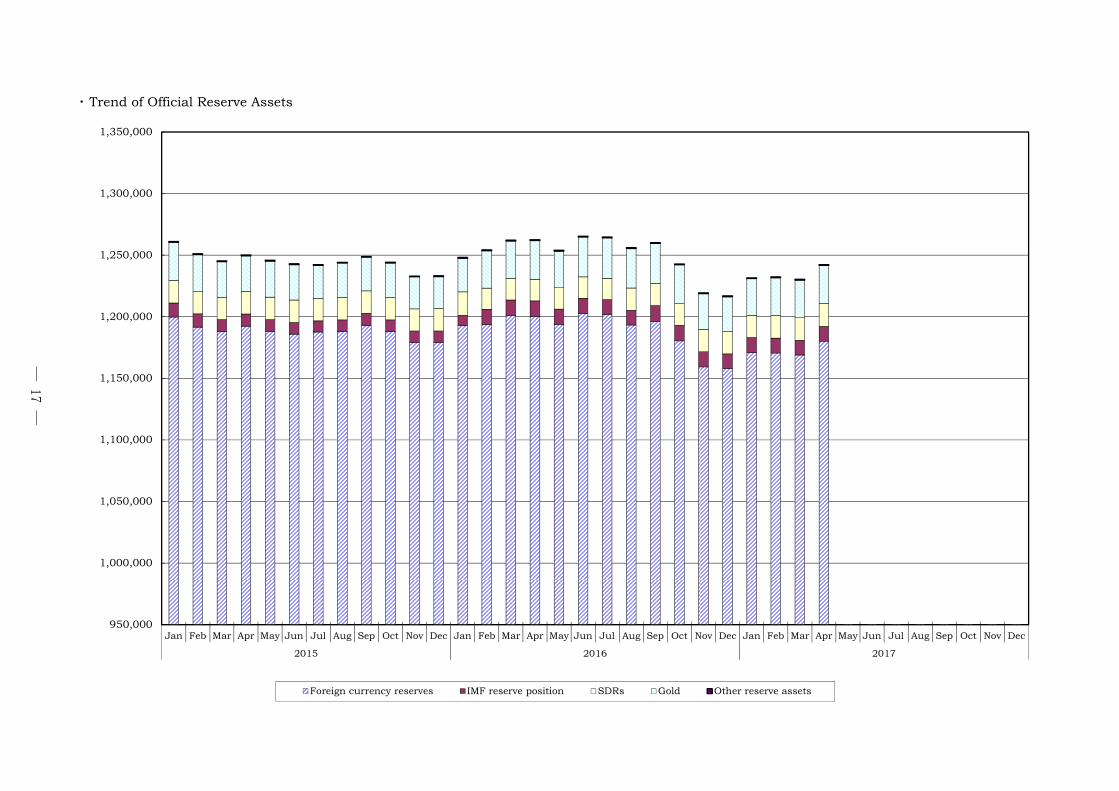

・ Trend of Official Reserve Assets

950,000

1,000,000

1,050,000

1,100,000

1,150,000

1,200,000

1,250,000

1,300,000

1,350,000

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

2015 2016 2017

Foreign currency reserves IMF reserve position SDRs Gold Other reserve assets

― 17 ―

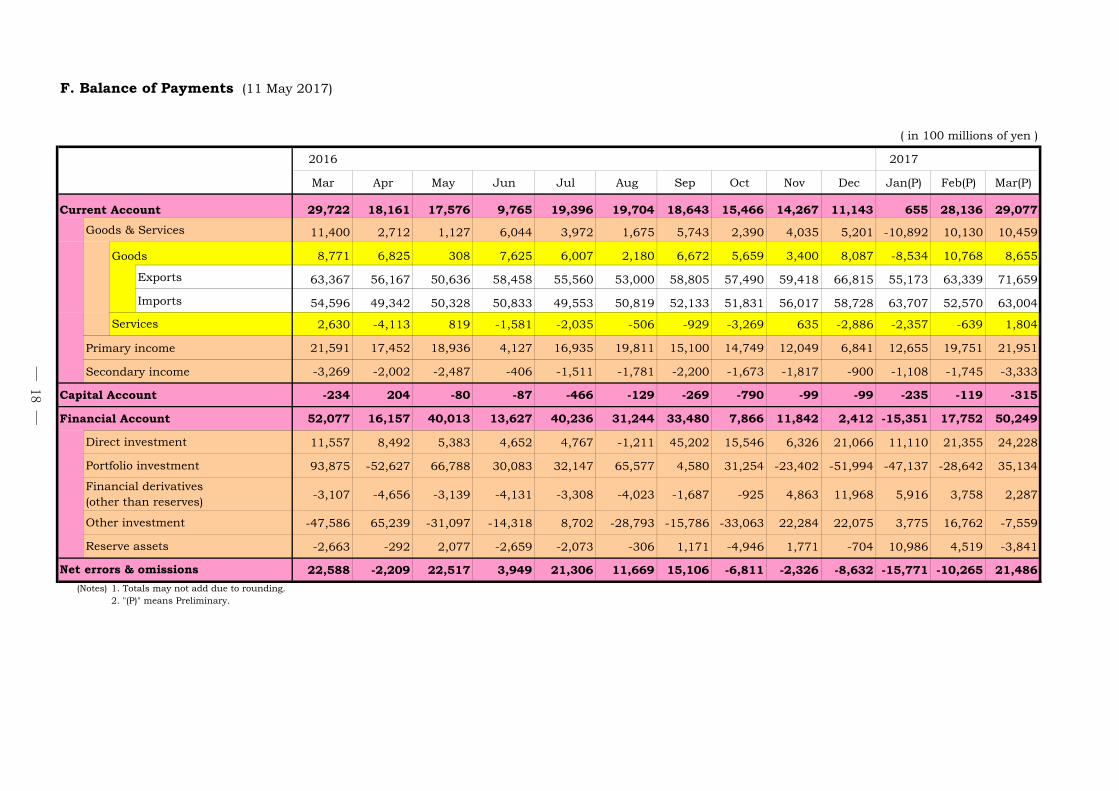

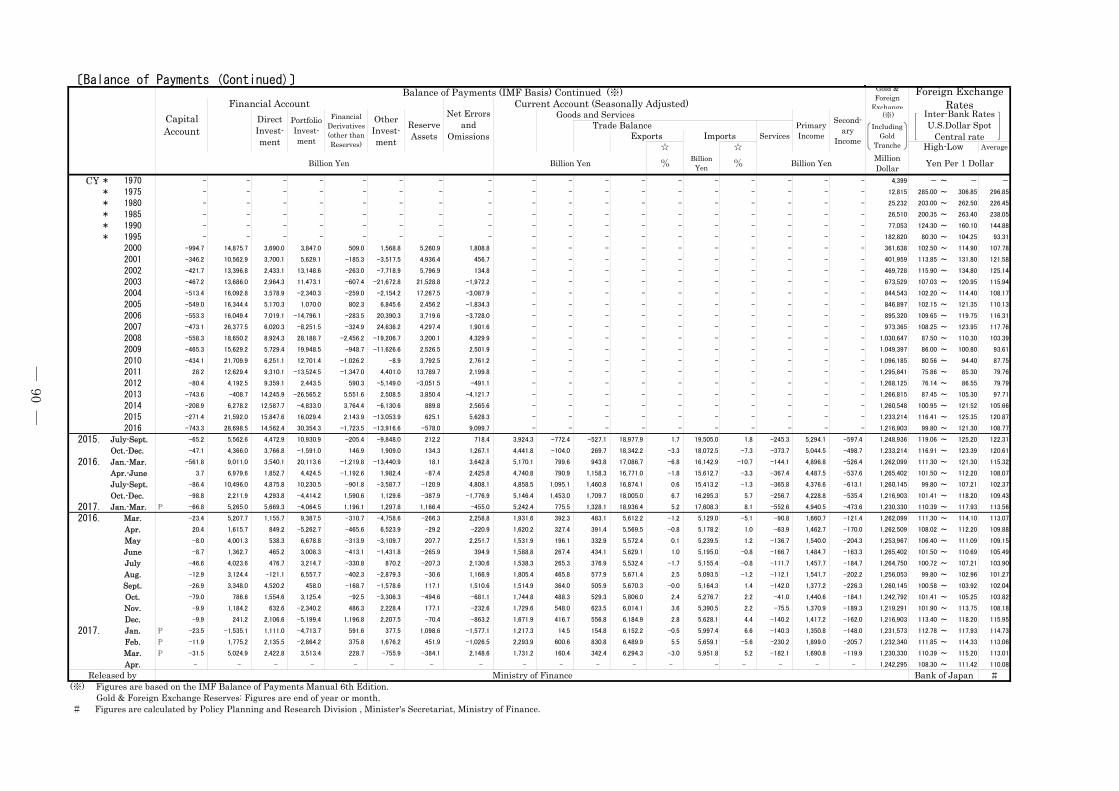

F. Balance of Payments (11 May 2017)

( in 100 millions of yen )

2016 2017

Mar Apr May Jun Jul Aug Sep Oct Nov Dec Jan(P) Feb(P) Mar(P)

Current Account 29,722 18,161 17,576 9,765 19,396 19,704 18,643 15,466 14,267 11,143 655 28,136 29,077

Goods & Services 11,400 2,712 1,127 6,044 3,972 1,675 5,743 2,390 4,035 5,201 -10,892 10,130 10,459

Goods 8,771 6,825 308 7,625 6,007 2,180 6,672 5,659 3,400 8,087 -8,534 10,768 8,655

Exports 63,367 56,167 50,636 58,458 55,560 53,000 58,805 57,490 59,418 66,815 55,173 63,339 71,659

Imports 54,596 49,342 50,328 50,833 49,553 50,819 52,133 51,831 56,017 58,728 63,707 52,570 63,004

2,630 -4,113 819 -1,581 -2,035 -506 -929 -3,269 635 -2,886 -2,357 -639 1,804

Primary income 21,591 17,452 18,936 4,127 16,935 19,811 15,100 14,749 12,049 6,841 12,655 19,751 21,951

Secondary income -3,269 -2,002 -2,487 -406 -1,511 -1,781 -2,200 -1,673 -1,817 -900 -1,108 -1,745 -3,333

Capital Account -234 204 -80 -87 -466 -129 -269 -790 -99 -99 -235 -119 -315

Financial Account 52,077 16,157 40,013 13,627 40,236 31,244 33,480 7,866 11,842 2,412 -15,351 17,752 50,249

11,557 8,492 5,383 4,652 4,767 -1,211 45,202 15,546 6,326 21,066 11,110 21,355 24,228

93,875 -52,627 66,788 30,083 32,147 65,577 4,580 31,254 -23,402 -51,994 -47,137 -28,642 35,134

-3,107 -4,656 -3,139 -4,131 -3,308 -4,023 -1,687 -925 4,863 11,968 5,916 3,758 2,287

-47,586 65,239 -31,097 -14,318 8,702 -28,793 -15,786 -33,063 22,284 22,075 3,775 16,762 -7,559

-2,663 -292 2,077 -2,659 -2,073 -306 1,171 -4,946 1,771 -704 10,986 4,519 -3,841

22,588 -2,209 22,517 3,949 21,306 11,669 15,106 -6,811 -2,326 -8,632 -15,771 -10,265 21,486

(Notes) 1. Totals may not add due to rounding.2. "(P)" means Preliminary.

Services

Direct investment

Portfolio investment

Financial derivatives(other than reserves)

Other investment

Reserve assets

Net errors & omissions

― 18 ―

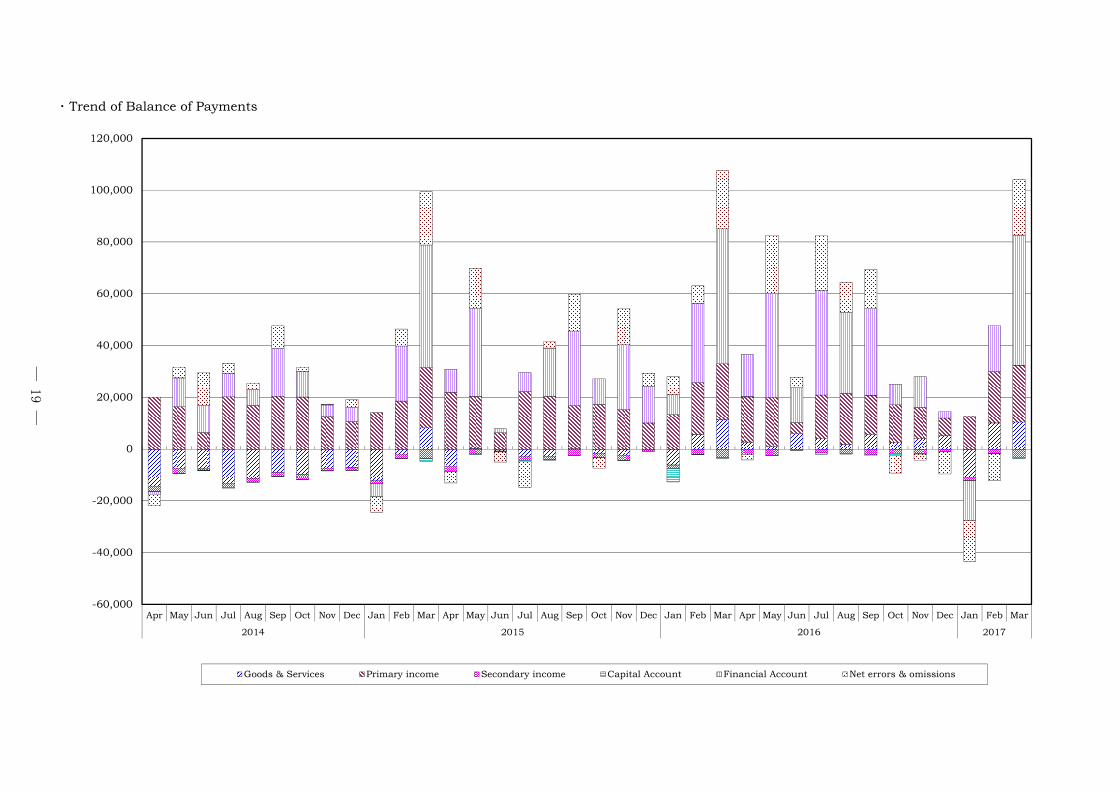

・ Trend of Balance of Payments

-60,000

-40,000

-20,000

0

20,000

40,000

60,000

80,000

100,000

120,000

Apr May Jun Jul Aug Sep Oct Nov Dec Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec Jan Feb Mar

2014 2015 2016 2017

Goods & Services Primary income Secondary income Capital Account Financial Account Net errors & omissions

― 19 ―

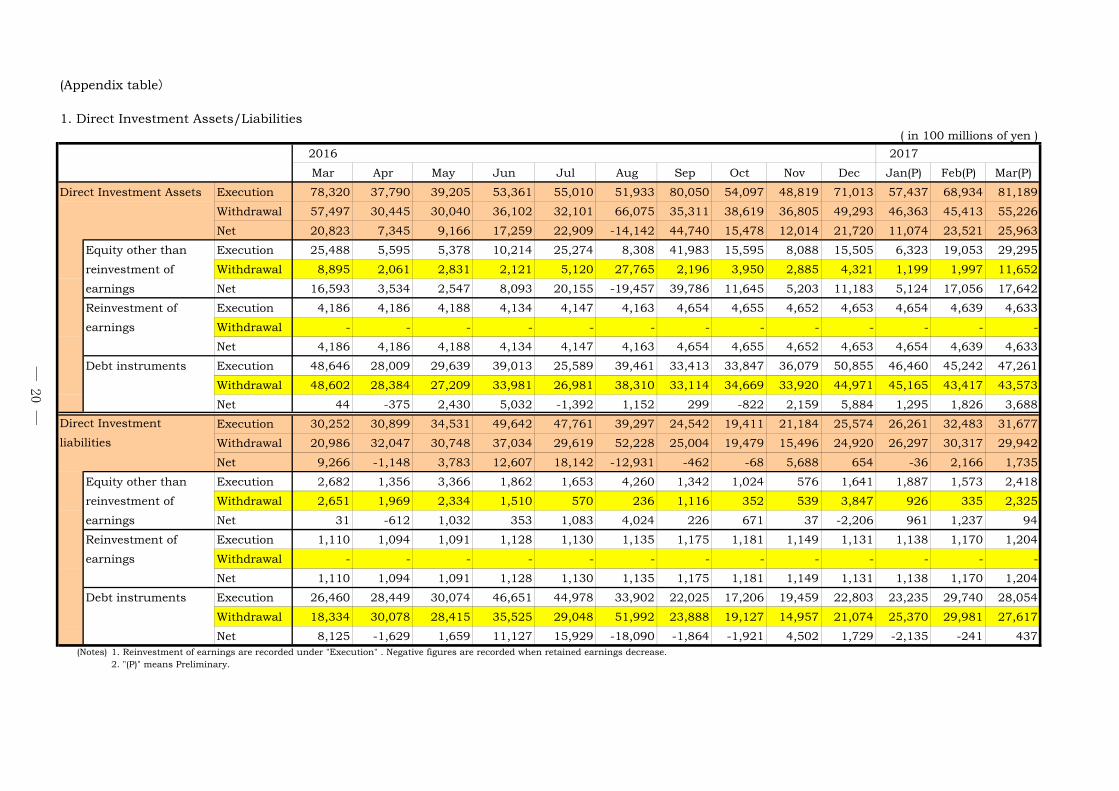

(Appendix table)

1. Direct Investment Assets/Liabilities( in 100 millions of yen )

2016 2017

Mar Apr May Jun Jul Aug Sep Oct Nov Dec Jan(P) Feb(P) Mar(P)

Direct Investment Assets Execution 78,320 37,790 39,205 53,361 55,010 51,933 80,050 54,097 48,819 71,013 57,437 68,934 81,189

Withdrawal 57,497 30,445 30,040 36,102 32,101 66,075 35,311 38,619 36,805 49,293 46,363 45,413 55,226

Net 20,823 7,345 9,166 17,259 22,909 -14,142 44,740 15,478 12,014 21,720 11,074 23,521 25,963

Equity other than Execution 25,488 5,595 5,378 10,214 25,274 8,308 41,983 15,595 8,088 15,505 6,323 19,053 29,295

reinvestment of Withdrawal 8,895 2,061 2,831 2,121 5,120 27,765 2,196 3,950 2,885 4,321 1,199 1,997 11,652

earnings Net 16,593 3,534 2,547 8,093 20,155 -19,457 39,786 11,645 5,203 11,183 5,124 17,056 17,642

Reinvestment of Execution 4,186 4,186 4,188 4,134 4,147 4,163 4,654 4,655 4,652 4,653 4,654 4,639 4,633

earnings Withdrawal - - - - - - - - - - - - -

Net 4,186 4,186 4,188 4,134 4,147 4,163 4,654 4,655 4,652 4,653 4,654 4,639 4,633

Debt instruments Execution 48,646 28,009 29,639 39,013 25,589 39,461 33,413 33,847 36,079 50,855 46,460 45,242 47,261

Withdrawal 48,602 28,384 27,209 33,981 26,981 38,310 33,114 34,669 33,920 44,971 45,165 43,417 43,573

Net 44 -375 2,430 5,032 -1,392 1,152 299 -822 2,159 5,884 1,295 1,826 3,688

Execution 30,252 30,899 34,531 49,642 47,761 39,297 24,542 19,411 21,184 25,574 26,261 32,483 31,677

Withdrawal 20,986 32,047 30,748 37,034 29,619 52,228 25,004 19,479 15,496 24,920 26,297 30,317 29,942

Net 9,266 -1,148 3,783 12,607 18,142 -12,931 -462 -68 5,688 654 -36 2,166 1,735

Equity other than Execution 2,682 1,356 3,366 1,862 1,653 4,260 1,342 1,024 576 1,641 1,887 1,573 2,418

reinvestment of Withdrawal 2,651 1,969 2,334 1,510 570 236 1,116 352 539 3,847 926 335 2,325

earnings Net 31 -612 1,032 353 1,083 4,024 226 671 37 -2,206 961 1,237 94

Reinvestment of Execution 1,110 1,094 1,091 1,128 1,130 1,135 1,175 1,181 1,149 1,131 1,138 1,170 1,204

earnings Withdrawal - - - - - - - - - - - - -

Net 1,110 1,094 1,091 1,128 1,130 1,135 1,175 1,181 1,149 1,131 1,138 1,170 1,204

Debt instruments Execution 26,460 28,449 30,074 46,651 44,978 33,902 22,025 17,206 19,459 22,803 23,235 29,740 28,054

Withdrawal 18,334 30,078 28,415 35,525 29,048 51,992 23,888 19,127 14,957 21,074 25,370 29,981 27,617

Net 8,125 -1,629 1,659 11,127 15,929 -18,090 -1,864 -1,921 4,502 1,729 -2,135 -241 437(Notes) 1. Reinvestment of earnings are recorded under "Execution" . Negative figures are recorded when retained earnings decrease.

2. "(P)" means Preliminary.

liabilities

Direct Investment

― 20 ―

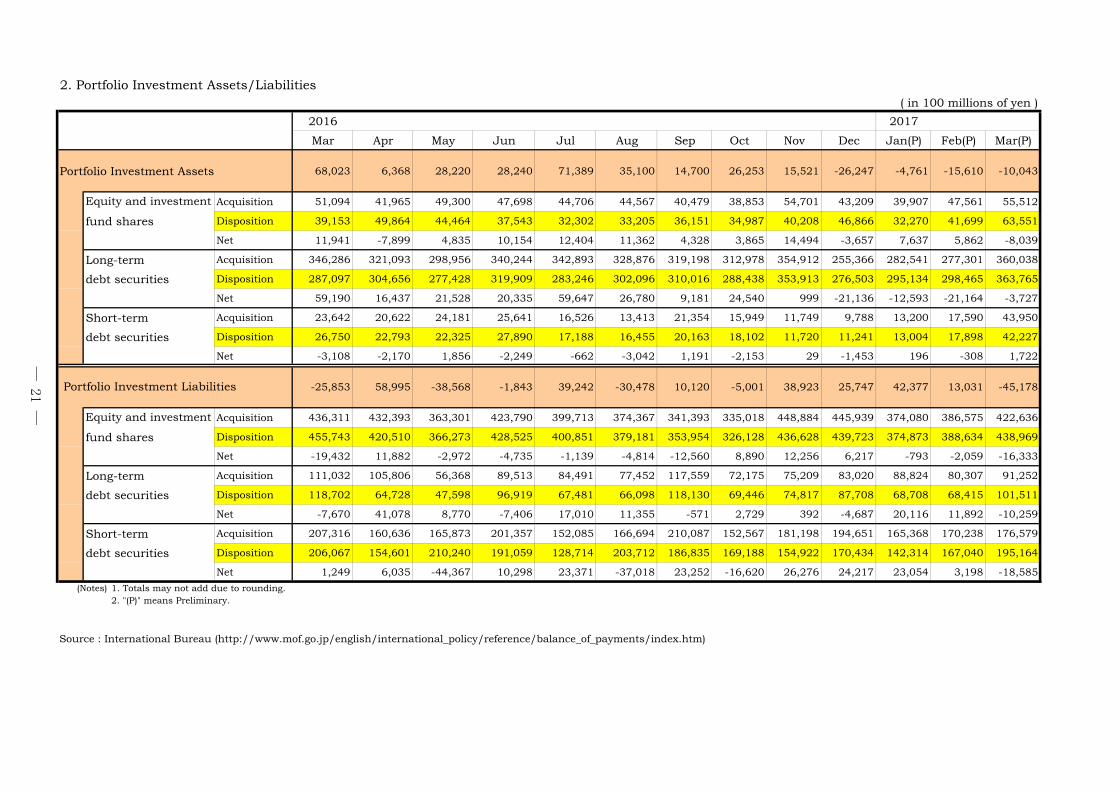

2. Portfolio Investment Assets/Liabilities( in 100 millions of yen )

2016 2017

Mar Apr May Jun Jul Aug Sep Oct Nov Dec Jan(P) Feb(P) Mar(P)

Portfolio Investment Assets 68,023 6,368 28,220 28,240 71,389 35,100 14,700 26,253 15,521 -26,247 -4,761 -15,610 -10,043

Acquisition 51,094 41,965 49,300 47,698 44,706 44,567 40,479 38,853 54,701 43,209 39,907 47,561 55,512

fund shares Disposition 39,153 49,864 44,464 37,543 32,302 33,205 36,151 34,987 40,208 46,866 32,270 41,699 63,551

Net 11,941 -7,899 4,835 10,154 12,404 11,362 4,328 3,865 14,494 -3,657 7,637 5,862 -8,039

Long-term Acquisition 346,286 321,093 298,956 340,244 342,893 328,876 319,198 312,978 354,912 255,366 282,541 277,301 360,038

debt securities Disposition 287,097 304,656 277,428 319,909 283,246 302,096 310,016 288,438 353,913 276,503 295,134 298,465 363,765

Net 59,190 16,437 21,528 20,335 59,647 26,780 9,181 24,540 999 -21,136 -12,593 -21,164 -3,727

Short-term Acquisition 23,642 20,622 24,181 25,641 16,526 13,413 21,354 15,949 11,749 9,788 13,200 17,590 43,950

debt securities Disposition 26,750 22,793 22,325 27,890 17,188 16,455 20,163 18,102 11,720 11,241 13,004 17,898 42,227

Net -3,108 -2,170 1,856 -2,249 -662 -3,042 1,191 -2,153 29 -1,453 196 -308 1,722

-25,853 58,995 -38,568 -1,843 39,242 -30,478 10,120 -5,001 38,923 25,747 42,377 13,031 -45,178

Acquisition 436,311 432,393 363,301 423,790 399,713 374,367 341,393 335,018 448,884 445,939 374,080 386,575 422,636

fund shares Disposition 455,743 420,510 366,273 428,525 400,851 379,181 353,954 326,128 436,628 439,723 374,873 388,634 438,969

Net -19,432 11,882 -2,972 -4,735 -1,139 -4,814 -12,560 8,890 12,256 6,217 -793 -2,059 -16,333

Long-term Acquisition 111,032 105,806 56,368 89,513 84,491 77,452 117,559 72,175 75,209 83,020 88,824 80,307 91,252

debt securities Disposition 118,702 64,728 47,598 96,919 67,481 66,098 118,130 69,446 74,817 87,708 68,708 68,415 101,511

Net -7,670 41,078 8,770 -7,406 17,010 11,355 -571 2,729 392 -4,687 20,116 11,892 -10,259

Short-term Acquisition 207,316 160,636 165,873 201,357 152,085 166,694 210,087 152,567 181,198 194,651 165,368 170,238 176,579

debt securities Disposition 206,067 154,601 210,240 191,059 128,714 203,712 186,835 169,188 154,922 170,434 142,314 167,040 195,164

Net 1,249 6,035 -44,367 10,298 23,371 -37,018 23,252 -16,620 26,276 24,217 23,054 3,198 -18,585

(Notes) 1. Totals may not add due to rounding.2. "(P)" means Preliminary.

Source : International Bureau (http://www.mof.go.jp/english/international_policy/reference/balance_of_payments/index.htm)

Portfolio Investment Liabilities

Equity and investment

Equity and investment

― 21 ―

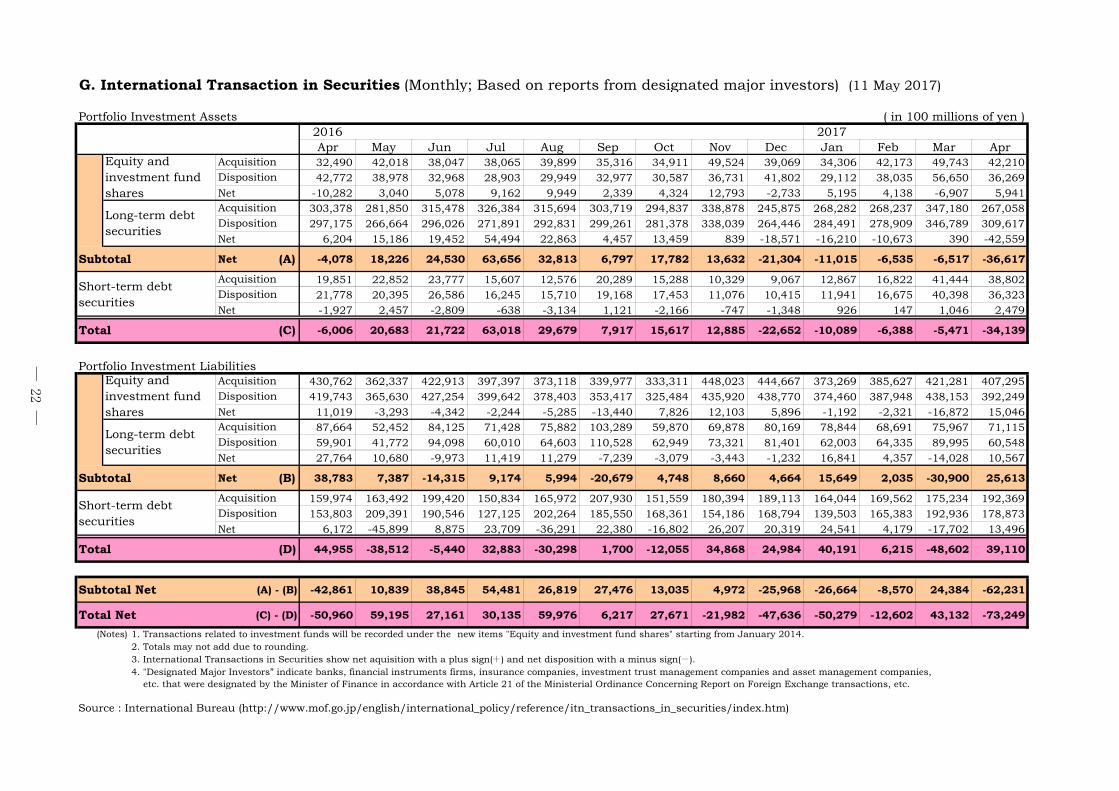

G. International Transaction in Securities (Monthly; Based on reports from designated major investors) (11 May 2017)

Portfolio Investment Assets ( in 100 millions of yen )2016 2017Apr May Jun Jul Aug Sep Oct Nov Dec Jan Feb Mar Apr32,490 42,018 38,047 38,065 39,899 35,316 34,911 49,524 39,069 34,306 42,173 49,743 42,21042,772 38,978 32,968 28,903 29,949 32,977 30,587 36,731 41,802 29,112 38,035 56,650 36,269

Net -10,282 3,040 5,078 9,162 9,949 2,339 4,324 12,793 -2,733 5,195 4,138 -6,907 5,941303,378 281,850 315,478 326,384 315,694 303,719 294,837 338,878 245,875 268,282 268,237 347,180 267,058297,175 266,664 296,026 271,891 292,831 299,261 281,378 338,039 264,446 284,491 278,909 346,789 309,617

Net 6,204 15,186 19,452 54,494 22,863 4,457 13,459 839 -18,571 -16,210 -10,673 390 -42,559

Subtotal Net (A) -4,078 18,226 24,530 63,656 32,813 6,797 17,782 13,632 -21,304 -11,015 -6,535 -6,517 -36,617

19,851 22,852 23,777 15,607 12,576 20,289 15,288 10,329 9,067 12,867 16,822 41,444 38,80221,778 20,395 26,586 16,245 15,710 19,168 17,453 11,076 10,415 11,941 16,675 40,398 36,323

Net -1,927 2,457 -2,809 -638 -3,134 1,121 -2,166 -747 -1,348 926 147 1,046 2,479

Total (C) -6,006 20,683 21,722 63,018 29,679 7,917 15,617 12,885 -22,652 -10,089 -6,388 -5,471 -34,139

Portfolio Investment Liabilities430,762 362,337 422,913 397,397 373,118 339,977 333,311 448,023 444,667 373,269 385,627 421,281 407,295419,743 365,630 427,254 399,642 378,403 353,417 325,484 435,920 438,770 374,460 387,948 438,153 392,249

Net 11,019 -3,293 -4,342 -2,244 -5,285 -13,440 7,826 12,103 5,896 -1,192 -2,321 -16,872 15,04687,664 52,452 84,125 71,428 75,882 103,289 59,870 69,878 80,169 78,844 68,691 75,967 71,11559,901 41,772 94,098 60,010 64,603 110,528 62,949 73,321 81,401 62,003 64,335 89,995 60,548

Net 27,764 10,680 -9,973 11,419 11,279 -7,239 -3,079 -3,443 -1,232 16,841 4,357 -14,028 10,567

Subtotal Net (B) 38,783 7,387 -14,315 9,174 5,994 -20,679 4,748 8,660 4,664 15,649 2,035 -30,900 25,613

159,974 163,492 199,420 150,834 165,972 207,930 151,559 180,394 189,113 164,044 169,562 175,234 192,369153,803 209,391 190,546 127,125 202,264 185,550 168,361 154,186 168,794 139,503 165,383 192,936 178,873

Net 6,172 -45,899 8,875 23,709 -36,291 22,380 -16,802 26,207 20,319 24,541 4,179 -17,702 13,496

Total (D) 44,955 -38,512 -5,440 32,883 -30,298 1,700 -12,055 34,868 24,984 40,191 6,215 -48,602 39,110

Subtotal Net (A) - (B) -42,861 10,839 38,845 54,481 26,819 27,476 13,035 4,972 -25,968 -26,664 -8,570 24,384 -62,231

Total Net (C) - (D) -50,960 59,195 27,161 30,135 59,976 6,217 27,671 -21,982 -47,636 -50,279 -12,602 43,132 -73,249

(Notes) 1. Transactions related to investment funds will be recorded under the new items "Equity and investment fund shares" starting from January 2014.2. Totals may not add due to rounding.3. International Transactions in Securities show net aquisition with a plus sign(+) and net disposition with a minus sign(-).4. "Designated Major Investors” indicate banks, financial instruments firms, insurance companies, investment trust management companies and asset management companies, etc. that were designated by the Minister of Finance in accordance with Article 21 of the Ministerial Ordinance Concerning Report on Foreign Exchange transactions, etc.

Source : International Bureau (http://www.mof.go.jp/english/international_policy/reference/itn_transactions_in_securities/index.htm)

AcquisitionDisposition

Equity andinvestment fundshares

AcquisitionDisposition

Long-term debtsecurities

AcquisitionDisposition

Short-term debtsecurities

Short-term debtsecurities

Equity andinvestment fundshares

Long-term debtsecurities

AcquisitionDisposition

AcquisitionDisposition

AcquisitionDisposition

― 22 ―

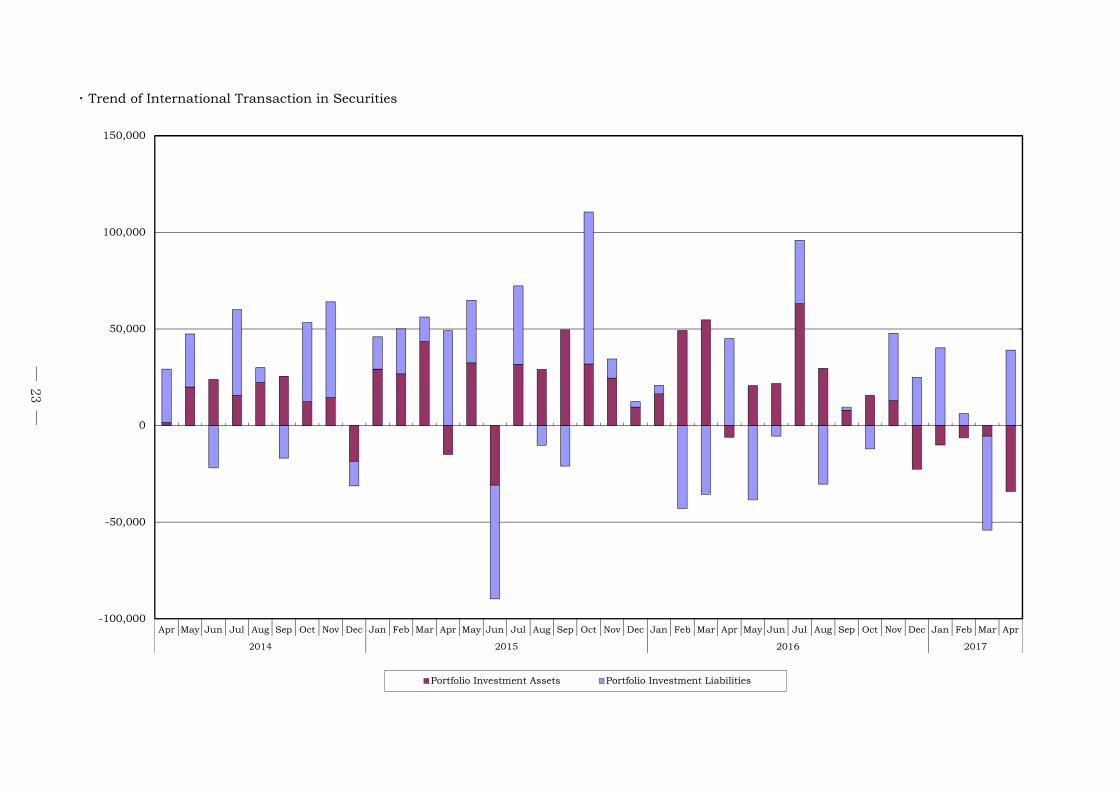

・ Trend of International Transaction in Securities

-100,000

-50,000

0

50,000

100,000

150,000

Apr May Jun Jul Aug Sep Oct Nov Dec Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec Jan Feb Mar Apr

2014 2015 2016 2017

Portfolio Investment Assets Portfolio Investment Liabilities

― 23 ―

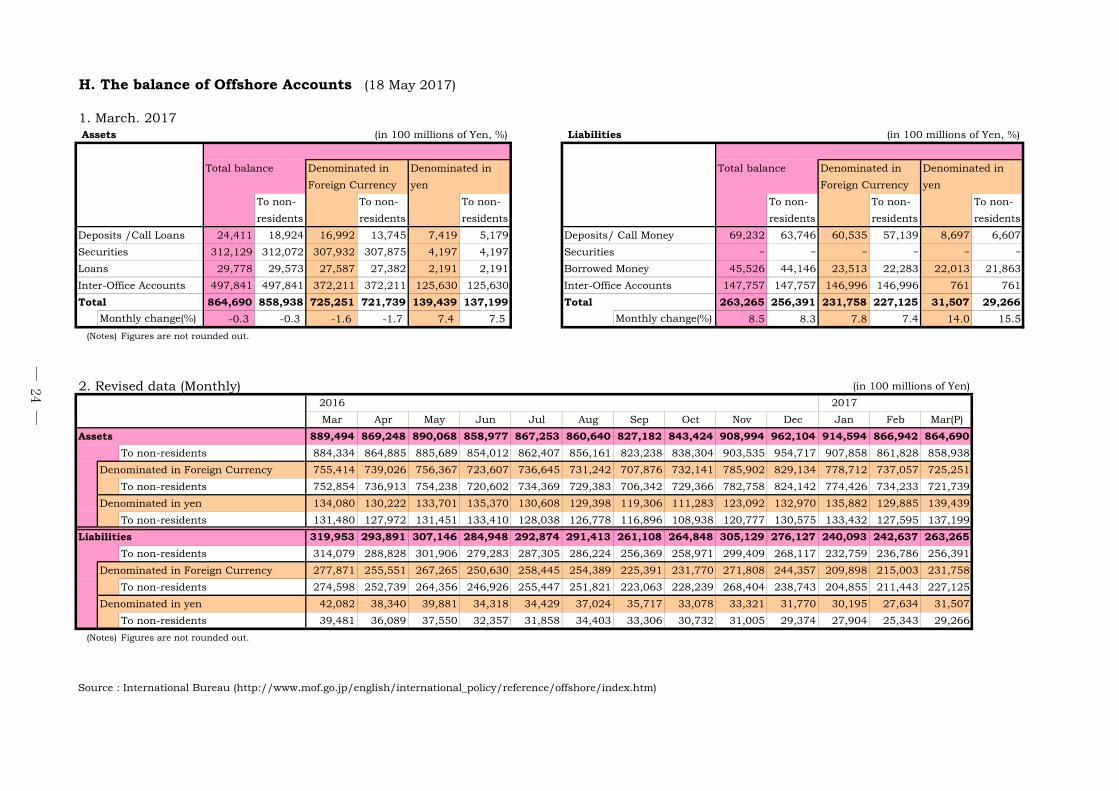

H. The balance of Offshore Accounts (18 May 2017)

1. March. 2017 Assets (in 100 millions of Yen, %) Liabilities (in 100 millions of Yen, %)

Total balance Denominated in Denominated in Total balance Denominated in Denominated in

Foreign Currency yen Foreign Currency yen

To non- To non- To non- To non- To non- To non-

residents residents residents residents residents residents

Deposits /Call Loans 24,411 18,924 16,992 13,745 7,419 5,179 Deposits/ Call Money 69,232 63,746 60,535 57,139 8,697 6,607

Securities 312,129 312,072 307,932 307,875 4,197 4,197 Securities - - - - - -

Loans 29,778 29,573 27,587 27,382 2,191 2,191 Borrowed Money 45,526 44,146 23,513 22,283 22,013 21,863

Inter-Office Accounts 497,841 497,841 372,211 372,211 125,630 125,630 Inter-Office Accounts 147,757 147,757 146,996 146,996 761 761

Total 864,690 858,938 725,251 721,739 139,439 137,199 Total 263,265 256,391 231,758 227,125 31,507 29,266

-0.3 -0.3 -1.6 -1.7 7.4 7.5 8.5 8.3 7.8 7.4 14.0 15.5

(Notes) Figures are not rounded out.

2. Revised data (Monthly) (in 100 millions of Yen)

2016 2017

Mar Apr May Jun Jul Aug Sep Oct Nov Dec Jan Feb Mar(P)

Assets 889,494 869,248 890,068 858,977 867,253 860,640 827,182 843,424 908,994 962,104 914,594 866,942 864,690

To non-residents 884,334 864,885 885,689 854,012 862,407 856,161 823,238 838,304 903,535 954,717 907,858 861,828 858,938

Denominated in Foreign Currency 755,414 739,026 756,367 723,607 736,645 731,242 707,876 732,141 785,902 829,134 778,712 737,057 725,251

To non-residents 752,854 736,913 754,238 720,602 734,369 729,383 706,342 729,366 782,758 824,142 774,426 734,233 721,739

Denominated in yen 134,080 130,222 133,701 135,370 130,608 129,398 119,306 111,283 123,092 132,970 135,882 129,885 139,439

To non-residents 131,480 127,972 131,451 133,410 128,038 126,778 116,896 108,938 120,777 130,575 133,432 127,595 137,199

Liabilities 319,953 293,891 307,146 284,948 292,874 291,413 261,108 264,848 305,129 276,127 240,093 242,637 263,265

To non-residents 314,079 288,828 301,906 279,283 287,305 286,224 256,369 258,971 299,409 268,117 232,759 236,786 256,391

Denominated in Foreign Currency 277,871 255,551 267,265 250,630 258,445 254,389 225,391 231,770 271,808 244,357 209,898 215,003 231,758

To non-residents 274,598 252,739 264,356 246,926 255,447 251,821 223,063 228,239 268,404 238,743 204,855 211,443 227,125

Denominated in yen 42,082 38,340 39,881 34,318 34,429 37,024 35,717 33,078 33,321 31,770 30,195 27,634 31,507

To non-residents 39,481 36,089 37,550 32,357 31,858 34,403 33,306 30,732 31,005 29,374 27,904 25,343 29,266

(Notes) Figures are not rounded out.

Source : International Bureau (http://www.mof.go.jp/english/international_policy/reference/offshore/index.htm)

Monthly change(%)Monthly change(%)

― 24 ―

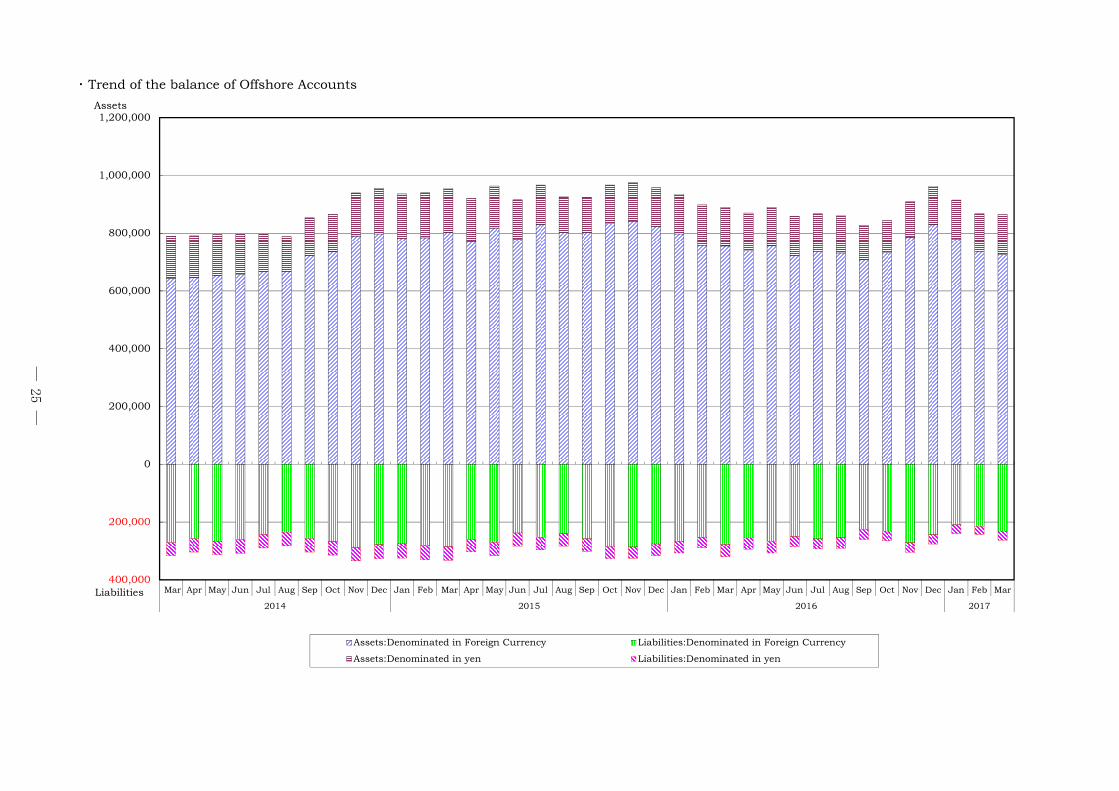

・ Trend of the balance of Offshore Accounts

400,000

200,000

0

200,000

400,000

600,000

800,000

1,000,000

1,200,000

Mar Apr May Jun Jul Aug Sep Oct Nov Dec Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec Jan Feb Mar

2014 2015 2016 2017

Assets:Denominated in Foreign Currency Liabilities:Denominated in Foreign Currency

Assets:Denominated in yen Liabilities:Denominated in yen

Assets

Liabilities

― 25 ―

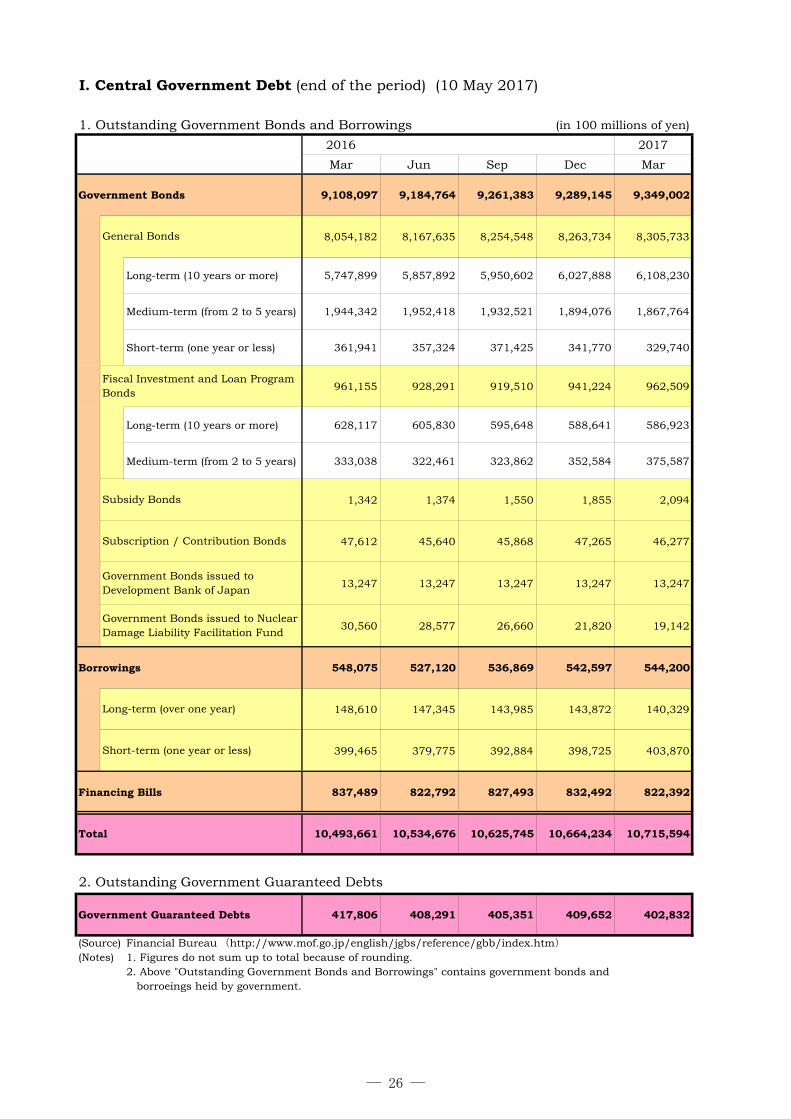

I. Central Government Debt (end of the period) (10 May 2017)

1. Outstanding Government Bonds and Borrowings (in 100 millions of yen)

2016 2017

Mar Jun Sep Dec Mar

Government Bonds 9,108,097 9,184,764 9,261,383 9,289,145 9,349,002

8,054,182 8,167,635 8,254,548 8,263,734 8,305,733

Long-term (10 years or more) 5,747,899 5,857,892 5,950,602 6,027,888 6,108,230

Medium-term (from 2 to 5 years) 1,944,342 1,952,418 1,932,521 1,894,076 1,867,764

Short-term (one year or less) 361,941 357,324 371,425 341,770 329,740

961,155 928,291 919,510 941,224 962,509

Long-term (10 years or more) 628,117 605,830 595,648 588,641 586,923

Medium-term (from 2 to 5 years) 333,038 322,461 323,862 352,584 375,587

1,342 1,374 1,550 1,855 2,094

47,612 45,640 45,868 47,265 46,277

13,247 13,247 13,247 13,247 13,247

30,560 28,577 26,660 21,820 19,142

Borrowings 548,075 527,120 536,869 542,597 544,200

148,610 147,345 143,985 143,872 140,329

399,465 379,775 392,884 398,725 403,870

Financing Bills 837,489 822,792 827,493 832,492 822,392

Total 10,493,661 10,534,676 10,625,745 10,664,234 10,715,594

2. Outstanding Government Guaranteed Debts

Government Guaranteed Debts 417,806 408,291 405,351 409,652 402,832

(Source) Financial Bureau (http://www.mof.go.jp/english/jgbs/reference/gbb/index.htm)

(Notes) 1. Figures do not sum up to total because of rounding.2. Above "Outstanding Government Bonds and Borrowings" contains government bonds and borroeings heid by government.

General Bonds

Fiscal Investment and Loan ProgramBonds

Subsidy Bonds

Long-term (over one year)

Short-term (one year or less)

Government Bonds issued toDevelopment Bank of Japan

Government Bonds issued to NuclearDamage Liability Facilitation Fund

Subscription / Contribution Bonds

― 26 ―

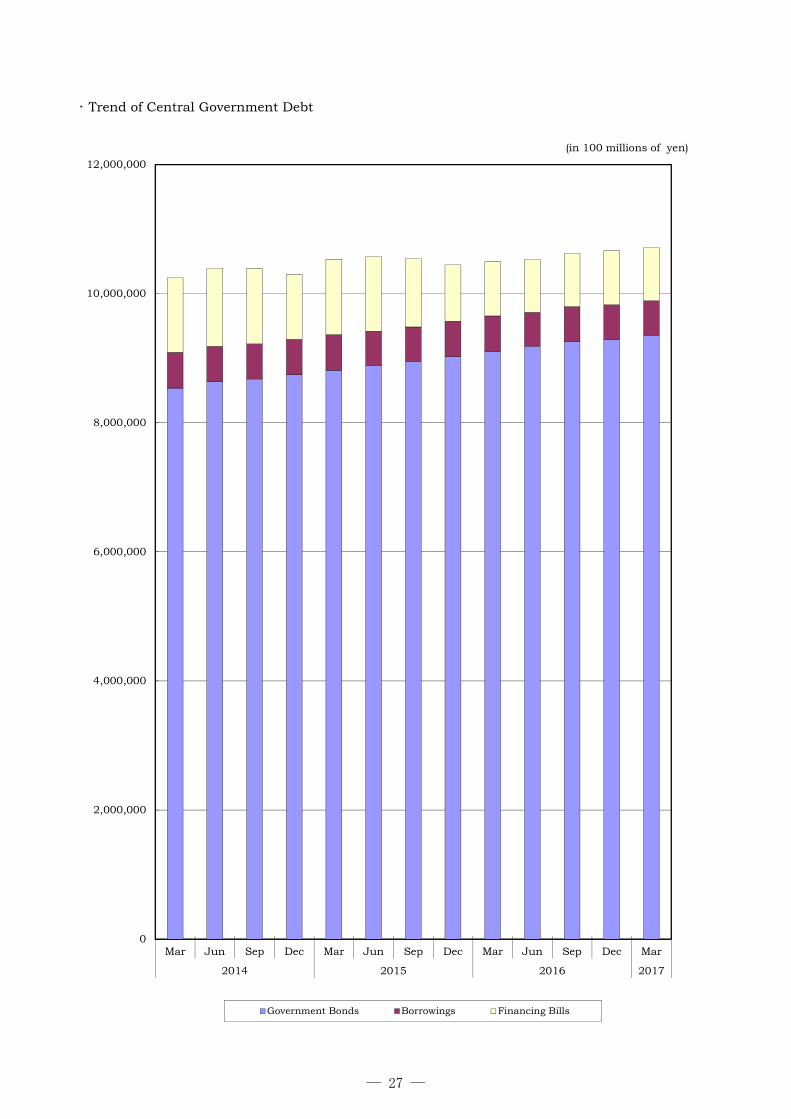

・ Trend of Central Government Debt

0

2,000,000

4,000,000

6,000,000

8,000,000

10,000,000

12,000,000

Mar Jun Sep Dec Mar Jun Sep Dec Mar Jun Sep Dec Mar

2014 2015 2016 2017

Government Bonds Borrowings Financing Bills

(in 100 millions of yen)

― 27 ―

PUBLIC RELATIONS & PRESS RELEASE

A. The Joint Statement of The 20th ASEAN+3 Finance Ministers’ Meeting (5 May 2017 / Yokohama, Japan)

May 5, 2017

― 30 ―

The Joint Statement of the 20th ASEAN+3 Finance Ministers’ and Central Bank Governors’ Meeting

(Yokohama, Japan, May 5th 2017)

I. Introduction 1. We, the Finance Ministers and Central Bank Governors of ASEAN, China, Japan and Korea

(ASEAN+3), convened our 20th meeting in Yokohama, Japan, under the co-chairmanship ofH.E. Carlos G. Dominguez III, Finance Secretary of the Philippines, and H.E. Taro Aso,Deputy Prime Minister and Minister of Finance of Japan. The President of the AsianDevelopment Bank (ADB), the Director of ASEAN+3 Macroeconomic Research Office(AMRO), the Deputy Secretary General of ASEAN, and the Deputy Managing Director of theInternational Monetary Fund (IMF) were also present at our meeting.

2. We exchanged views on recent global and regional economic developments and policyresponses. We reviewed the progress of regional financial cooperation achieved since our lastmeeting in Frankfurt, Germany, including the Chiang Mai Initiative Multilateralisation(CMIM), AMRO and Asian Bond Markets Initiative (ABMI). We also discussed measures tofurther strengthen our regional financial cooperation in the future and agreed on the“Yokohama Vision”, our guiding principles for a more resilient and integrated ASEAN+3(attached as “Annex” to this statement).

II. Recent Economic and Financial Developments in the Region3. We are pleased that the ASEAN+3 region is expected to maintain a relatively robust growth

and will continue to play a leading role in sustaining global growth, supported by regionalmembers’ continuing structural reforms and effective implementation of macroeconomicpolicies. We recognize that global growth is expected to rise with buoyant financial market anda long-awaited cyclical recovery in manufacturing and trade underway. However, risks for theglobal economy remain skewed to the downside, especially over the medium term, withpervasive uncertainties surrounding policies. The sources of uncertainties include an inwardshift in policies, including toward protectionism, and sharper-than-expected financialtightening.

4. Under these circumstances, we reaffirmed our commitment to regional financial cooperation,and support our open and rules-based multilateral trade and investment systems, which willcontinue to strengthen our economies. We also reiterated the importance of utilizing allnecessary policy tools – monetary, fiscal and structural – individually and collectively topromote sustainable, balanced and inclusive growth and to enhance economic and financial

― 31 ―

resilience, taking into account regional members’ specific circumstances. Monetary policy will continue to support economic activity and ensure price stability, consistent with Central Banks’ mandate, but monetary policy alone cannot lead to balanced growth. Fiscal policy should be used flexibly and be growth-friendly, prioritize high-quality investment, and support reforms that would provide opportunities and promote inclusiveness, while ensuring debt as a share of GDP is on a sustainable path. We reaffirmed our commitment to structural reforms that will lift potential growth of the region and enhance member countries’ resilience. These reforms should be appropriately tailored, prioritized and sequenced, depending on country-specific circumstances. We will continue to adopt the appropriate policy mix to achieve balanced growth and financial stability. We will carefully calibrate and clearly communicate our macroeconomic and structural policy actions, including the use of macro-prudential measures, to reduce policy uncertainty, minimize negative spillovers and promote transparency.

5. We recognized the importance and benefits of open capital markets and of improving the system underpinning international capital flows while continuing to enhance the monitoring of capital flows and to strengthen the management of risks stemming from excessive capital flow volatility. An open and resilient financial system is crucial to supporting sustainable growth and development. In this light, we will continue to closely monitor, and if necessary, address emerging risks, particularly those that are systemic, as well as the vulnerabilities in the financial system.

III. Strengthening Regional Financial Cooperation Chiang Mai Initiative Multilateralisation (CMIM)

6. We affirmed our commitment to further strengthen the CMIM as an essential part of the regional financial safety net. In this regard, we welcomed the revision of the CMIM Operational Guidelines to clarify the activation process of the IMF De-linked Portion of the CMIM, as well as the progress in the preparation of the CMIM Conditionality Framework. We also welcomed the Deputies’ endorsement of the assessment methodology on the increase in the IMF De-linked Portion. We appreciated all these efforts and the significant progress that has been made in working towards the potential increase of the IMF De-linked Portion. We look forward to further progress on this issue. It is encouraging to note that the CMIM, with its current size of USD 240 billion, is at the center of our regional financial safety net, complemented by the network of bilateral swap arrangements in the region amounting to more than USD 160 billion.

7. We welcomed the development of the qualification indicators for the CMIM-Precautionary Line, based on the Economic Review and Policy Dialogue (ERPD) Matrix, that consists of key economic and financial indicators of all ASEAN+3 member economies. We look forward to the successful completion of the pilot project for the ERPD Matrix peacetime procedure and progress on ERPD Matrix indicators and benchmarks, in cooperation with AMRO.

― 32 ―

8. We noted that the CMIM also contributes to a stronger global financial safety net with the IMF at its center. In this regard, we welcomed the successful completion of the 7th Test Run which examined the activation of the CMIM arrangement with the IMF program. It has highlighted the importance of improving CMIM’s readiness and effectiveness by (i) addressing issues that are fundamental to the CMIM, (ii) improving CMIM-IMF coordination (including burden sharing, financing conditions and information sharing), and (iii) enhancing AMRO’s capacity. These important works have been included in our plan on the Periodic Review of the CMIM Agreement, and we look forward to strong progress towards this direction by our next meeting, including the reports from the two Working Groups (WGs), one on CMIM fundamental issues and the other on the coordination with IMF. We will deepen our engagement with the IMF with the aim of resolving operational issues that may arise in order to further strengthen the supplementary role of the CMIM in the global financial safety net.

ASEAN+3 Macroeconomic Research Office (AMRO) 9. We are pleased with the finalization of AMRO's Strategic Direction and Medium-term

Implementation Plan (SD&MTIP) as approved by the Deputies. We encouraged AMRO to execute the SD&MTIP and contribute to the region’s macroeconomic and financial stability, by delivering high quality and original surveillance to member economies, and providing strong support for the CMIM. We noted AMRO’s significant efforts in enhancing its surveillance capacity which resulted in the publication of the very first edition of its flagship report, the "ASEAN+3 Regional Economic Outlook”. We look forward to more focused and comprehensive surveillance activities and welcomed AMRO’s "Guidance Note for AMRO Country Surveillance Consultation” to serve as guidelines for its country consultations and regional assessments. We commended the Deputies' endorsement of AMRO's Publication Policy which will promote its accountability and visibility beyond the regional platform and solidify its presence as an international organization. We continue to support AMRO in enhancing its surveillance and organizational capacity to fulfill its mandate as an independent, credible and professional regional organization acting as a trusted policy advisor to members in the ASEAN+3 region.

10. We appreciate AMRO's efforts to support the CMIM activities of ASEAN+3. We expect to enhance AMRO’s role to support members in the implementation of the CMIM. With AMRO's enhanced surveillance capacity, we look forward to its further contribution to ensuring the macroeconomic and financial stability of the region. We expect AMRO’s active participation in the CMIM Periodic Review in coordination with the WGs to enhance the operational readiness of the CMIM.

11. Recognizing that building multi-layered macroeconomic and financial stability mechanism worldwide is key to stability, we encouraged AMRO to explore closer cooperation with global and other regional financial institutions, which would also help enhance AMRO's organizational capacity through information sharing, joint activities and staff exchanges. We

― 33 ―

welcomed the conclusion of a Memorandum of Understanding between AMRO and the ADB to further their cooperation, and look forward to the early conclusion of a Memorandum of Understanding between AMRO and the IMF.

12. We welcomed the establishment of the trust funds in AMRO, with contributions from China, Japan and Korea, boosting the implementation of AMRO's technical assistance program. We reiterated the importance of enhancing surveillance capacity of member economies and encouraged AMRO to continue upgrading and expanding its technical assistance activities according to the needs of members.

13. We commended Director Chang Junhong for her excellent management of AMRO as a full-fledged international organization, and look forward to her continued leadership in guiding AMRO as an independent, credible and reliable surveillance unit.

Asian Bond Markets Initiative (ABMI) 14. We welcomed the significant contribution of the ABMI to developing local currency bond

markets across the region, channeling the region’s large savings to finance its own investment, and mitigating currency and maturity mismatches since its establishment. Beyond the bond markets, we recognized the necessity of expanding ABMI’s role on building up our financial markets as a whole, and further promoting use of local currencies, given increased funding needs in local currencies within the region, as a way of managing heightened volatility in global financial markets.

15. We noted the proposal to increase the capital of the Credit Guarantee and Investment Facility (CGIF), recognized the importance of expanding its guarantee capacity, and look forward to an early decision on this issue. We encouraged continued support and financial contribution from the ADB. In view of massive infrastructure needs in the region, we encouraged CGIF to contribute to fulfilling funding needs through its guarantee to project bonds for infrastructure. We welcomed the effort and steady progress since our last meeting toward implementing the Central Securities Depository (CSD)-Real Time Gross Settlement (RTGS) linkage between BOJ and HKMA in accordance with the roadmap for establishing a regional settlement intermediary in ASEAN+3. We look forward to further cross-border bond issuances under the ASEAN+3 Multi-currency Bond Issuance Framework (AMBIF).

16. We noted the progress of the new study to promote local currency denominated green bond for infrastructure, the expansion of data coverage and analysis of Asian Bonds Online (ABO), in line with the ABMI Medium-Term Road Map. We also welcomed the launch of a new study for ASEAN+3 bonds to be recognized as prime collateral globally. We will strategically implement the technical assistance under the Technical Assistance Coordination Team (TACT), especially to better prepare the recipient countries, which are still dependent on external concessionary loans to cover their fiscal deficit, for the development of their government bond markets.

17. We welcomed the publication of “Good Practices in Developing Bond Market”, which puts

― 34 ―