Embed Size (px)

Citation preview

Impossible d’afficher l’image.

Impossible d’afficher l’image.

AXA European Work Council

Jean-Paul RignaultCEO AXA Spain

Madrid, April 2014

2 – AXA European Work Council

Agenda

1

2

3

Spain macro-economic context

Insurance Market Context

Overview of The MedLA Region

AXA Spain

Overview

Human Resources

4A

B

3 – AXA European Work Council

MACRO-ECONOMIC ENVIRONMENT (1/2)Continuing signs of economic recovery. Q4 ´13 GDP increased +0.3% q/q IMF raised its 2014 and 2015 GDP forecast

GDP Evolution Unemployment rate evolution(Annual Average)

• Q4’13 GDP reflects a recovery of the activity with avariation of +0.3% q/q (+0,1% Q3’13; -0,1% Q2’13)

• IMF raised GDP forecasts vs Oct’13 estimation. 2014:+0.6% (+0.4 pts) 2015: +0.8% (+0.3 pts).

� In 2013 unemployment decreases by 69,000 people, thebest performance since 2007 , and reaches 5.896.300.Unemployment rate stands at 26,06% (Source: EPASurvey) with an annual average of 26,36%

January Harmonized CPI: 0.3% y/y remains stable vs. December data. This performance is mainly due to a decrease of prices of oil and lubricants.

9,16 8,51 8,2611,34

18,0120,06

21,64

25,0326,36 25,80

`05 `06 `07 `08 `09 `10 '11 '12 '13 14(p)

Source: Real data - INE. Forecast data - Funcas

0,6 0,8

3,64,1 3,5

0,9

-3,8

-0,2

0,1

-1,6 -1,2

'05 '06 '07 '08 '09 '10 '11 `12 `13 `14 `15

GDP market prices for actual data 2005-13 (INE)

GDP constant prices forecast data 2014-15 (IFM Projection – WEO January)

Market PricesMarket Prices Constant pricesConstant prices

4 – AXA European Work Council

MACRO-ECONOMIC ENVIRONMENT (2/2)Anfac expects 800,000 new car registrations in 2014 , +11% vs 2013

•Feb’14 cumulative car sales increased +13% (vs.Feb’13), mainly due to good performance of individualsales: +23% boosted through Plan Pive.

•Anfac (Spanish Automobile Manufacturer's Association)expects 800,000 new car registrations in 2014, around+100,000 (+11%) vs 2013.

-23,3

-32-36,5

-41,1-37,3

-35,1

-32,42

-33,62

-37,89

-24,7-30,3

-35,2

-22,30

-27,92

-40,49

-12,72

-18,47-20,19

-14,95

-21,52

-9,55

-12,00

-8,60

Jan Feb Mar Abr May Jun Jul Ago Sep Oct Nov Dic

2012 2013

Source: INE – “Otros indicadores de Construcción”

723

1.523

0

200

400

600

800

1.000

1.200

1.400

1.600

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec2014 2013 Promedio 03-08

Source: ANFAC

New Cars Registration (# accumulated k) Sales of Cement - apparent consumption (% y/y)

New Mortgages (% y/y of total amount )

-34

-50

-42

-26

-32

-20

-27

-33

-36

-21

-35

-29

-21

-14

-35

-23 -25

-44

-32

-38

-30

-14

-27

-60,00

-50,00

-40,00

-30,00

-20,00

-10,00

0,00Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

2012

2013

Source: INE – “Hipotecas inmobiliarias constituidas”

•Decrease due to lack of consumer confidence, difficulties to access credit and price reductions for homes

5 – AXA European Work Council

Agenda

3

Spain macro-economic context

Insurance Market Context

Overview of The MedLA Region

AXA Spain

Overview

Human Resources

4

1

2

A

B

6 – AXA European Work Council

Evolution of Non-Life Insurance marketShrinking market in P&C: negative trend in Motor and Multirisk, both strongl y impacted by economic crisis. AXA motor behaved in 2 013 better than the market

Source: ICEA

Premium Growth % Premium Growth %

Premium Growth %

Source: ICEA

Source: ICEA Source: ICEA

Premium Growth % Premium Growth %

TOTAL MARKET P&C (€ 30.3 bn in 2013 ) Total Market P&C w/o Health (€ 23.4 bn in 2013)

Motor (€ 10.0 bn in 2013) Health (€ 6.9 bn in 2013)

Source: ICEA

Multirisk (€ 6.5 bn in 2013)

7 – AXA European Work Council

Evolution of Life Insurance marketLife trend strongly impacted by financial crisis an d M&A in financial sector. In 2013 AXA beats market trend (+24% vs -3% in market)

Source: ICEA

Premium Growth %

Premium Growth %Premium Growth %

TOTAL MARKET L&S (€ 25.5 bn in 2013 )

Source: ICEA Source: ICEA

Savings (€ 21.2 bn in 2013) Protection (€ 3.3 bn in 2013)

8 – AXA European Work Council

AXA ´s position in the Spanish marketAXA Total Business behaved better than the market ( +2% AXA vs -2,8% market)

P&C:

•Allianz, Mutua Madrileña and specialists beatmarket trend

•AXA maintains position vs 2013 (MS of 6,7%)

L&S :

•AXA beats market trend in L&S with a growth of+24% vs -3% in market, moving up one place inL&S ranking until 11th with an increase in MSstanding at 2.7%

9 – AXA European Work Council

Agenda

Spain macro-economic context

Insurance Market Context

Overview of The MedLA Region

AXA Spain

Overview

Human Resources

4

1

3

2

A

B

MedLA 2014 Priorities

�Commercial lines profitable growth

�Profitable growth in Health

�Turn-around of GA products and increasing the UL sh are in L&S portfolio

�Accelerate full deployment of Multi-Access & Digital Transformation

�Foster the development of new segmented value propositions through Digital to accelerate growth and consolidate AXA Brand differentiation

�Drive the Distribution Transformation from digital

�Cost Efficiency Framework including the simplification of the operating model through digital (e-claims)

�Accelerate profitable growth in Protection business

�Consolidation of new emerging entities: Colombia and Brazil

�Cultural transformation articulating digital revolution

Acceleration

Selectivity

Efficiency

Trust & Achievement

CustomerCentricity

Which are the strategic actions that we should develop in 2014 towards our AXA Ambition 2015?

MedLA FTEs overview FY 2013

*Total Holdings FTEs at 346

� MedLA FTEs at 11.387 in FY 2013. This means a reduction of -305 FTEs vs. previous year due to the decrease in

P&C business lines in Mature Markets, that remain impacted by the recession

2.800*

FY 2013 growth at constant exchange rate vs. FY 2012. FY 2013 Exchange rates vs. Eur: 2.52 Turkish Lira, 16.95 Mexican Peso, 11.16 Moroccan Dirham, 1.33 US Dollar

MedLA P&C Business overview FY 2013

� Total MedLA P&C revenues reached €7.4m in 2013 which represents 26% of overall Group´́́́s revenues

� Overall revenues increased by +5,5% vs. FY 2012 thanks to the two digits growth in High Growth Markets

(+12%) and despite the deterioration in Mature markets (-3%) mainly driven by motor business

MedLA L&S Business overview FY 2013

FY 2013 growth at constant exchange rate vs. FY 2012. FY 2013 Exchange rates vs. Eur: 2.52 Turkish Lira, 16.95 Mexican Peso, 11.16 Moroccan Dirham, 1.33 US Dollar

� Overall MedLA revenues reached €5.6m in 2013 which represents 6% of overall Group´́́́s revenues and +16%

revenues growth vs. FY 2012 thanks to Mature Markets (+17%)

� Progressive shift in all entities from GA to UL and Protection share within the L&S portfolio

14 – AXA European Work Council

Agenda

Spain macro-economic context

Insurance Market Context

Overview of The MedLA Region

AXA Spain

Overview

HH.RR.

1

2

3

4A

B

15 – AXA European Work Council

2,3

The AXA Group in the Spanish market

2.613

17837

A reference player in Spain,

with a market share of 4,86%(3)

(1)

Million euros

(1) Includes net premiums, net of cancellations, transfers to pension plans and investment funds. Companies: AXA Seguros Generales, AXA Vida y AXA Aurora Vida.(2) Calculated over direct Insurance business, + Reinsurance.(3) Source: ICEA 2013.

Premiums (2) 2.829 millions

16 – AXA European Work Council

AXA Spain

Buenos Aires

Aragon

Cornellà

S. Cugat

Sevilla

S.Cruz Tenerife

Palma Mallorca

Valencia

Fuente de la Mora

Burgos

Mexico 118

Direct business (5,9%)

6 branches that ensure service and

proximity: +1.100 exclusive shops

and 7.000 points of sale

6 branches that ensure service and

proximity: +1.100 exclusive shops

and 7.000 points of sale

+3 million customers

and +5.4 million contracts

+3 million customers

and +5.4 million contracts

Nearly 2.800 employees:

26 nationalities, 58% women

Nearly 2.800 employees:

26 nationalities, 58% women

(weight vs total premiums)

8,9%12,8%

19,4%

12,8%

24,9%

Vigo

14,8%

17 – AXA European Work Council

Almost 2.800 employees providing services to 3 million customers

Million euros paid in compensation for Non-Life claims

Severe weather events handled

Million phone calls from customers

2,3

1.200

23

3,4

2 Million healthcare services provided

Million claims handled

18 – AXA European Work Council

AXA SpainOur organizational structure

19 – AXA European Work Council

Business evolution 2010-2013Key indicators

GWP 2010 -2013 (€ M)

2010 2013

608

2.743

1.797

699

2.496

2.135

2010-12

-5,7%

-3,9%

-6,2%

+24,6%

-4,3%

+2,3%

2012-13CAGR

P&C

L&S

Individual Motor: average premium

2010 20132011 2012

530524

495

469

-1,1%

-5,6%

-5,1%

-4,0%

CAGR 2010-13

Particular Motor 1ª category (€)

2010 20132011 2012

53

2927

39

8109

136148

61

138162

187 -31% CAGR 2010-13

Underlying Earnings ( €M)

Strong decrease in GWP, average premiums and Underlying Earnings, triggered by the country’s economic crisis.

20 – AXA European Work Council

2013 Business resultsIncrease in business volumes

5,3

5,4

1 22012 2013

+ 100.000

• Net Inflow of 100.000 policies.

• Stable client base of over 3 million customers

2 540

2 613

2012 2013

+2,9%

Market -2,81%

Total Premiums (million €) Total Policies (millions)

+1M NB policies (+11,33% in P&C)

+31,4% in Savings &

Investments

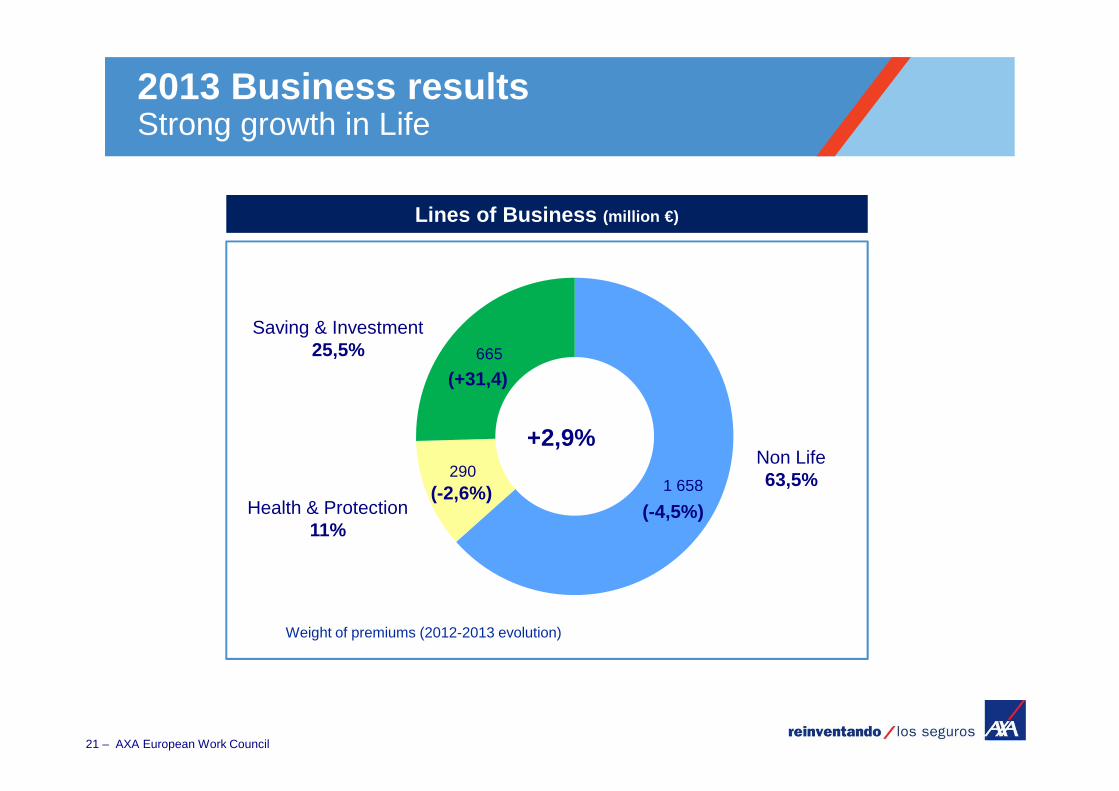

21 – AXA European Work Council

1 658290

665

2013 Business resultsStrong growth in Life

Health & Protection11%

Non Life63,5%

Saving & Investment 25,5%

+2,9%

(+31,4)

(-4,5%)(-2,6%)

Lines of Business (million €)

Weight of premiums (2012-2013 evolution)

22 – AXA European Work Council

2013 Business resultsDistribution by network

AXA Exclusiv4% Large Brokers &

Distributors5%

Small & Medium Brokers

37%

Direct business5%

Agents49%

139

9771.270

128

100

Non Proprietary Network1.115M€ (42,7%)

Proprietary Network 1.498M€ (57,3%) � Multiaccess

� Multichannel

� Distribution challenges� Segmentation� Professionalization� Specialization

� Deep changes� Digital

transformation

23 – Comunicación, Responsabilidad Corporativa y Relaciones Institucionales

• 100.000 policies (~10% NB)• 10 online products (+2 in 2014)• m-commerce

Digital transformation

• Commercial LinesSelf-servicing

34,5% claims declared online

• Retail

AXA Drive APP AXAContigo210.000 e-clients

58,4% claims declared online.

13.000 Club AXA Vip clients

• Multibrowser platform

• Adapted tosmartphones/tablets

• High connectivity

Business Services Distribution

ACJ4

Diapositive 23

ACJ4 si solo podemos poner una imagen yo pondría la de axa contigo, es la app de los servicios que mencionasarreglar el texto del cuadro central, demasiado grande y justificarAlfonso Caro Josep; 17/03/2014

24 – AXA European Work Council

2013 Key MilestonesSocial Responsability and awards

25 – AXA European Work Council

2014 Priorities

++++

• Sales dynamics consolidation. • Segmented pricing. • Acceleration of profitable segments. • Average costs and expense optimization.

Profitability

• Health, Life and Commercial Lines: focus of our business.

• Customer retention and cross-selling.• Segmented, specialized and professional

Distribution network.

Diversification

• Multichannel and Multiaccess capabilities.• SOLOMO (Social, Local, Mobile).• Product & service range evolution (Easy to do

business with) to respond to new customer needs.• People & Culture.

Transformation