Embed Size (px)

Citation preview

Oil market and NCS outlookJune 9, 2017

Teodor Sveen-NilsenPhone : (+47) 24 13 36 06Mobile : (+47) 95 74 36 26E-mail : [email protected]

Agenda

2

Introduction

Do we need more oil?

Oil market balance

Oil demand

Oil supply

Future of NCS

Summary

Financials

Oil ServicesUtilities & Renewables

3

A full-service investment bank

SB1 Markets’ – Strategic position

Nordic-focus with international reach Core sectors

SB1M has a strong position in the Nordic markets, with a global reach and client base

1

2

3

OsloHQ

Core markets

Client base

A leading full-service investment bank based in Oslo

130 employees1) in total, highly research driven approached

Backed by Norway’s #2 banking group with more than USD 100bn in assets

Natural Resources TMT

Seafood

Real estate

Industrials and Services

1) Including core incoming team from 1 June / 1 September 2017

Jørgen Haug

Teodor Sveen-Nilsen

4

Top-ranked research team and broad sector coverage 1)

Research team – selected members

1) Including core incoming team from 1 June / 1 September 2017

#1 in macro

#1 in credit

Pål Ringholm

• Ranked #1 in credit, top ranked for a decade

• 18 years of experience from investment banking and finance

#1 in strategy

Coverage of 10-15 E&P companies, 75+ companies in total

Harald Magnus Andreassen

• Ranked #1 in macro for 15 consecutive years with clear margin

• 22 years of experience from investment banking research

Peter Hermanrud

• Ranked #1 in strategy for 15 consecutive years with clear margin

• 24 years of experience from asset management and research

Top rated in E&P

Top rated in High Yield

• Ranked top 3 in E&P sector, covers Nordic companies

• Experience from sell-side research and consulting

• M.Sc. in Business and Administration from BI, MBA in Corporate Finance from NHH

OTHER

• Ranked top 4 in credit in Norway

• 7 years of high yield credit research experience

• M. Phil., Finance, University of Cambridge

Agenda

5

Introduction

Do we need more oil?

Oil market balance

Oil demand

Oil supply

Future of NCS

Summary

09/06/20176

Do we need more oil and gas?

Most forecasters agree on:

• World population will grow

• World energy demand will increase

• Oil and gas will probably lose market share vs. other energy carriers

• Renewable will grow at high rates (but from a very low base)

In the public debate, it looks like may forget:

• In its nature, oil and gas are declining and substantial investments are needed to keep production flat

• Losing market share ≠ lower absolute demand

1.0 %

2.0 %

0.5 %

2.1 %

2.4 %

1.4 %

0.0 %

0.5 %

1.0 %

1.5 %

2.0 %

2.5 %

3.0 %

CAGR

CA

GR

Liquids (crude + NGL) Natural gas

Coal Nuclear

Other (hydro, renewable, other) Sum energy demand

EIA: Energy demand will increase by 1.4% per year, all sources expected grow. Oil will lose market share, but still grow ~1% per year

09/06/20177

Demand per energy source CAGR per energy source

Source: EIA, Sb1 Markets. 1 quadrillion btu = 170 mill boe

0

50

100

150

200

250

300

350

400

450

0

100

200

300

400

500

600

700

800

900

2016 2020 2025 2030 2035 2040

mill

bo

e/d

qu

adri

llio

n B

tu

Liquids (crude + NGL) Natural gas

Coal Nuclear

Other (hydro, renewable, other) mill boe/d

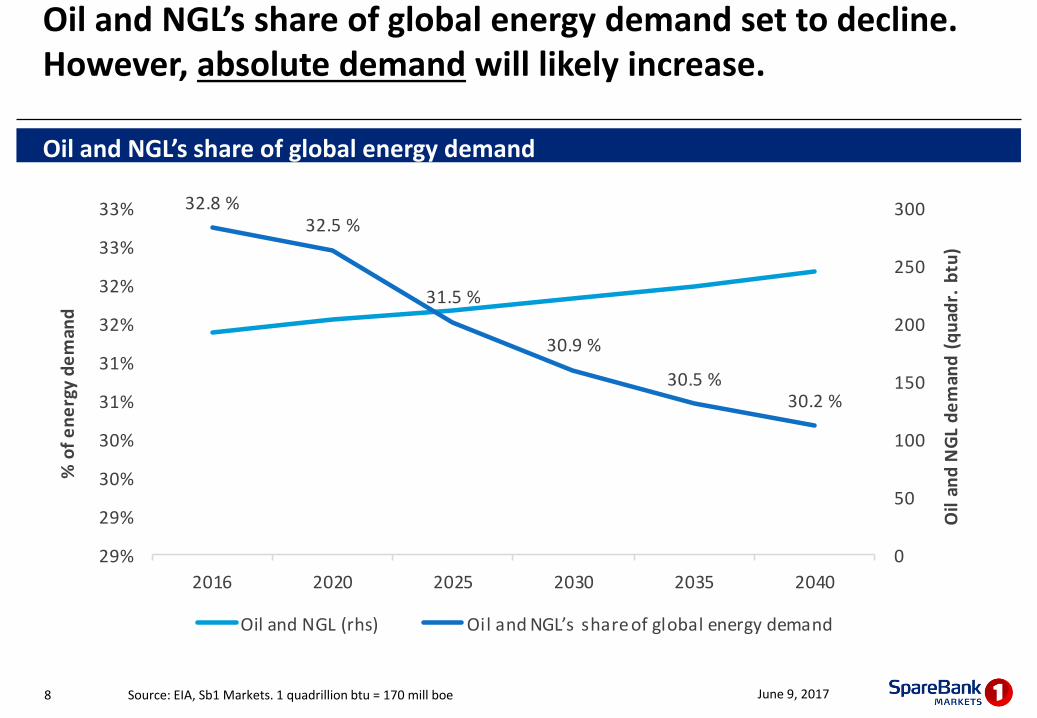

Oil and NGL’s share of global energy demand set to decline. However, absolute demand will likely increase.

June 9, 2017Source: EIA, Sb1 Markets. 1 quadrillion btu = 170 mill boe8

Oil and NGL’s share of global energy demand

32.8 %32.5 %

31.5 %

30.9 %

30.5 %30.2 %

29%

29%

30%

30%

31%

31%

32%

32%

33%

33%

2016 2020 2025 2030 2035 2040

0

50

100

150

200

250

300

% o

f e

ne

rgy

de

man

d

Oil

and

NG

L d

em

and

(q

uad

r. b

tu)

Oil and NGL (rhs) Oil and NGL’s share of global energy demand

Energy intensity will probably increase

• According to UN, the world population will grow to 9.2 bn by 2040, or 0.9% per year

• If EIA’s energy demand forecasts are correct, the global energy intensity will increase

• Total emery demand per billion is set to increase from 79 quadrillion btu in 2016 to 89 per quadrillion btu in 2040, or 0.5% per year

June 9, 2017Source: EIA, UN, IMF, Sb1 Markets9

World population and energy intensity UN and EIA projections to 2040

7.4

7.8

8.1

8.5

8.8

9.2

5

6

6

7

7

8

8

9

9

10

10

75

77

79

81

83

85

87

89

91

93

95

2016 2020 2025 2030 2035 2040

Glo

bal

po

pu

lati

on

, b

n

Ene

rgy

inte

nsi

ty p

er

pe

rso

n

Energy consumption per bn Global population bn, (rhs)

Agenda

10

Introduction

Do we need more oil?

Oil market balance

Oil demand

Oil supply

Future of NCS

Summary

The oil market is rebalanced

09/06/201711

Global oil market balance

90

91

92

93

94

95

96

97

98

99

100

Jan

14

Mar

14

May

14

Jul

14

Sep

14

Nov

14

Jan

15

Mar

15

May

15

Jul

15

Sep

15

Nov

15

Jan

16

Mar

16

May

16

Jul

16

Sep

16

Nov

16

Jan

17

Mar

17

May

17

Jul

17

Sep

17

Nov

17

mb

/d

Oil demand Oil production

Source: IEA, Sb1 Markets.

Agenda

12

Introduction

Do we need more oil?

Oil market balance

Oil demand

Oil supply

Future of NCS

Summary

Oil demand is not a problem: Demand estimates revised up…but growth estimates revised significantly less up due to baseline revisions

June 9, 201713

REGIONAL: Oil demand 2017e (mb/d) GLOBAL: Oil demand 2017e (mb/d)

Average of IEA, EIA and OPEC estimates: +0.8 mb/d since September 2016

44.0

45.0

46.0

47.0

48.0

49.0

50.0

51.0

sep. 16 okt. 16 nov. 16 des. 16 jan. 17 feb. 17 mar. 17 apr. 17 mai. 17

mb

/d

OEDC demand Non-OEDC demand

95.8

96.0

96.2

96.4

96.6

96.8

97.0

97.2

97.4

97.6

sep. 16 okt. 16 nov. 16 des. 16 jan. 17 feb. 17 mar. 17 apr. 17 mai. 17

mb

/d

Global demand

Source: IEA, Sb1 Markets.

We estimate 2017e demand growth of 1.4-1.5 mb/d, vs. average of ~1.2 mb/d last 30 years

June 9, 201714

Oil demand growth y/y

1.10

1.15

1.20

1.25

1.30

1.35

1.40

1.45

1.50

2017 demand growth Average demand growth last 30 yrs

mb

/d

Sb1 forecast: 1.4-1.5 mb/d based on three different models

Source: IEA, EIA, OPEC, Sb1 Markets.

y/ y changes 2017,

mb/ d

OED C

demand

N o n-OED C

demand

Glo bal

demand

N o n-OP EC

supply +

OP EC N GL

C all o n

OP EC

IEA -0.2 1.4 1.3 0.7 0.6

EIA 0.3 1.3 1.6 1.4 0.2

OPEC 0.2 1.1 1.3 0.1 1.2

Average 0.1 1.3 1.4 0.7 0.7

Consensus: 2017e demand growth at 1.4 mb/d vs average of ~1.2 mb/d last 30 years

June 9, 201715

y/y estimates

y/y oil demand growth

Average growth = 1.2 mb/d

Source: MacrobondOECD, Sb1 Markets.

Agenda

16

Introduction

Do we need more oil?

Oil market balance

Oil demand

Oil supply

Future of NCS

Summary

June 9, 201717

Key issues oil supply

1. Non-OPEC production and US shale companies’ return to the market

2. Long term:

» Reserve replacement ratio

» Impact of low capex on future production

OPEC cut positive, surging non-OPEC production forecast adds risk

• The OPEC cut in late 2016 and increased global oil demand are the key reason for a balance oil market.

• However, with higher oil prices, we have seen that a number of forecasters have increased 2017e non-OPEC supply forecast (particularly US), which is negative for oil prices

• In the short to medium term, increased non-OPEC production is the key risk for the oil market

June 9, 201718

2017 non-OPEC supply estimates

60.0

61.0

62.0

63.0

64.0

65.0

66.0

67.0

mb

/d

IEA EIA OPEC Average all sources

Shale companies: Positive EBIT, still negative free cash flow

June 9, 201719

Shale oil companies’ EBIT Shale oil companies’ free cash flow*

Gulfport Energy CorporationLaredo Petroleum, Inc.Memorial Resource Development CorpNewfield Exploration CompanyOasis Petroleum Inc.QEP Resources, Inc.Range Resources CorporationRSP Permian, Inc.SM Energy CompanySouthwestern Energy CompanyWPX Energy, Inc. Class A

Continental Resources, Inc.EOG Resources, Inc.Pioneer Natural Resources CompanyWhiting Petroleum CorporationApache CorporationCabot Oil & Gas CorporationChesapeake Energy CorporationConcho Resources Inc.Denbury Resources Inc.Devon Energy CorporationDiamondback Energy, Inc.

Companies included in sample:

-7 000

-6 000

-5 000

-4 000

-3 000

-2 000

-1 000

0

Q4 15 Q1 16 Q2 16 Q3 16 Q4 16 Q1 17

USD

m

-5 000

-4 000

-3 000

-2 000

-1 000

0

1 000

2 000

3 000

Q4 15 Q1 16 Q2 16 Q3 16 Q4 16 Q1 17

USD

m

* Free cash flow = operational cash flow less capex. Source: Factset, company reports, Sb1 Markets

June 9, 201720

Long term supply considerations

1. Reserve replacement ratio

2. Long-term impact of low capex

Declining trend for majors’ reserve replacement ratio

June 9, 2017Source: Company reports *Includes, Statoil, ENI, BP, Total, Shell, Repsol, Chevron, Exxon, ConocoPillips21

Average RRR E&P majors*

60

70

80

90

100

110

120

130

140

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

Re

serv

e r

ep

lace

me

nt

rati

o

Average majors

Capex drives production, but a lot of noise in dataIntuitively, capex is the most important variable for production growth

June 9, 201722

Non-OPEC capex vs. production

1971

1972

1973

19741975

197619771978

19791980

1981

1982

1983

19841985

19861987

1988

1989

1990

1991

19921993

1994

1995

1996

1997

1998

1999

20002001

2002

2003 2004

2005

2006

2007

2008

2009

2010

2011

2012

y = 0.0384x + 0.0124R² = 0.1795

-6 %

-4 %

-2 %

0 %

2 %

4 %

6 %

8 %

-40 % -20 % 0 % 20 % 40 % 60 % 80 % 100 %

No

n-O

PEC

pro

du

ctio

n, t

+3

Non-OPEC capex

Source: Rystad, IEA Sb1 Markets

June 9, 201723

• Why look at capex vs. production?

» Intuitively correct. With no investments, declining oil production will accelerate decline.

» History gives support to the thesis that lower capex = lower production, in particular in certain areas

» However, on a aggregated basis, non-OPEC capex vs. non-OPEC production does not give any statistical significance.

• Why exclude OPEC in the analysis?

» OPEC is a cartel

» Production and investments decisions are made on different criteria that in non-OPEC (social security, national security, market share, prestige more important than NPV and IRR?)

Agenda

24

Introduction

Do we need more oil?

Oil market balance

Oil demand

Oil supply

Future of NCS

Summary

June 9, 201725

Two key challenges for NCS:

1. Declining production past 15 years

2. Investments back to 2007 levels

1: Norway has reduced its global market share by 50%

June 9, 2017Soure: Rystad uCube26

Global vs. NCS liquids production (mb/d)

1.5 %

1.7 %

1.9 %

2.4 %2.6 %

3.0 %

3.4 %

3.6 %

4.0 %

4.2 %

4.5 % 4.4 %

4.2 %4.3 %

4.4 %4.5 %

4.4 %

4.1 %

3.8 %

3.5 %

3.3 %

3.0 %2.9 %

2.8 %

2.5 %2.3 %

2.1 %2.0 % 2.0 % 2.0 % 2.1 %

0.0 %

0.5 %

1.0 %

1.5 %

2.0 %

2.5 %

3.0 %

3.5 %

4.0 %

4.5 %

5.0 %

0

20

40

60

80

100

120

1986 1987 1988 1989 1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

NCS liquids production RoW NCS % of global oil production (rhs)

2: E&P investments dropped significantly1) Global and NCS investments back to 2007 levels, 2) NCS correlates with global capex

Global vs NCS E&P capex (including exploration), USDm

Correlation global vs. NCS capex: 0.98

Soure: Rystad uCube

-

5 000

10 000

15 000

20 000

25 000

30 000

35 000

40 000

-

100 000

200 000

300 000

400 000

500 000

600 000

700 000

800 000

900 000

1 000 000

1986 1987 1988 1989 1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

Sum World Sum Norway (rhs)

0

10

20

30

40

50

60

70

80

90

100

Produced Reserves* Resources Resources in discoveries Other** Undiscovered resources Total

bn

bo

e

09/06/201728

Vast resources left, even after almost 40 years of production!

*Includes resource classes 1, 2 and 3, **Production not evaluated. Source: NPD

NPD says: 48% of total resources were produced as of end 2016

Not produced

Produced

NCS exploration: Set to increase

09/06/201729

NCS exploration wells vs oil price

33

51

3742

34

5749

45

27

6

43

4

17

13

1

5

10

13

98

62

80

111 112 109

99

54

45

0

20

40

60

80

100

120

0

10

20

30

40

50

60

2008 2009 2010 2011 2012 2013 2014 2015 2016 2017e 2018e 2019e

Nu

mb

er

of

we

lls

Completed In porgress Firm Planned Likley* DoD Avg. Brent oil price (rhs)

* Drill-or-drop wells risked with 25% in 2016, 2017 and 2018, and 35% thereafter. Likely wells risked with 50%. Soure: Rystad, NPD, company presentations

2017-19e: Estimates likely to increase as new information becomes available

Zero sanctions = flat NCS capex. Sanctions = capex growth…zero sanctions highly unlikely

09/06/201730

NCS capex (USDm)

-

5 000

10 000

15 000

20 000

25 000

30 000

35 000

2012 2013 2014 2015 2016 2017 2018 2019 2020 2021

USD

m

Abandoned Producing Under development Discovery

Soure: Rystad, NPD

2017e-2020e: Sverdrup 10-25% of NCS capex

09/06/201731

Is there a NCS future?

• Large amount of non-produced resources

• Stable framework (fiscal and regulatory)

• Investments set to pick up

• New players increasingly more important

= YES

Agenda

32

Introduction

Do we need more oil?

Oil market balance

Oil demand

Oil supply

Future of NCS

Summary

Summary

• The oil market is rebalanced

• Global oil demand is not a problem, we forecast 1.4-1.5 mb/d growth for 2017 (above historical average of 1.2 mb/d)

• OPEC cut positive, surging non-OPEC production forecast adds risk (but US shale oil companies not able to report positive cash flow)

• NCS activity set to increase

June 9, 2017

Teodor Sveen-NilsenPhone : (+47) 24 13 36 06Mobile : (+47) 95 74 36 26E-mail : [email protected]

09/06/201735

No Solicitation

This report or summary is provided for informational purposes only and under no circumstances is it to be used or considered as an offer to sell, or a solicitation of any offer to buy any securities. This report or summary is prepared for general circulation and general information only. It does not have regard to the specific investment objectives, financial situation or the particular needs of any person who may receive this report or summary. Investors should seek financial advice regarding the appropriateness of investing in any securities or investment strategies discussed or recommended in this report or summary and should understand that statements regarding future prospects may not be realized.

Performance in the past is not a guide to future performance. SpareBank 1 Markets accepts no liability whatsoever for any direct or consequential loss arising from the use of this publication or its contents.

These materials may not be reproduced, distributed or published by any recipient for any purpose. Please cite source when quoting.

Notice to U.S. Investors

If this report is being furnished directly to U.S. recipients by a non-U.S. SpareBank 1 Markets entity in reliance on section (a)(2) of Rule 15a-6 under the U.S. Securities Exchange Act of 1934, as amended (each a “direct U.S. recipient”), each such direct U.S. recipient of this report represents and agrees, by virtue of its acceptance thereof, that it is “major U.S. institutional investor” (as such term is defined in section (b)(4) of Rule 15a-6) and that it understands the risks involved in executing transactions in such securities. Any direct U.S. recipient of this report that wishes to discuss or receive additional information regarding any security or issuer mentioned herein, or engage in any transaction to purchase or sell or solicit or offer the purchase or sale of such securities, should contact a registered representative of SpareBank 1 Capital Markets Inc. (“SpareBank 1 Capital Markets”), a registered U.S. broker-dealer and member of FINRA and SIPC.

In certain cases, unless prohibited by the provisions of Regulation S under the U.S. Securities Act of 1933, as amended, this report may be provided by SpareBank 1 Capital Markets to a U.S. recipient (a “SpareBank 1 Capital Markets U.S. recipient”), in which case each such SpareBank 1 Capital Markets U.S. recipient of this report represents and agrees, by virtue of its acceptance thereof, that it is “major U.S. institutional investor” (as such term is defined in section (b)(4) of Rule 15a-6), or that it is a U.S. institutional investor (as such term is defined in section (b)(7) of Rule 15a-6), and that it understands the risks involved in executing transactions in such securities. In such cases, SpareBank 1 Capital Markets accepts responsibility for the content of this report; however, although it has accepted responsibility for the content of this report in such cases, SpareBank 1 Capital Markets did not contribute to the preparation of this report, and the specific authors of the report are not employed by, and are not associated persons of, SpareBank 1 Capital Markets. The SpareBank 1 Markets entity that prepared the report, and the authors of this report, may not be subject to all of the registration, qualification, disclosure, independence and other U.S. regulatory requirements that apply to SpareBank 1 Capital Markets and its employees and associated persons. Any SpareBank 1 Capital Markets U.S. recipient of this report that wishes to discuss or receive additional information regarding any security or issuer mentioned herein, or to engage in any transaction to purchase or sell or solicit or offer the purchase or sale of such securities, should contact a registered representative of SpareBank 1 Capital Markets.

Any transaction in the securities discussed in this report by U.S. persons (other than a registered U.S. broker-dealer or bank acting in a broker-dealer capacity) must be effected with or through SpareBank 1 Capital Markets.

The securities referred to in this report may not be registered under the U.S. Securities Act of 1933, as amended, and the issuer of such securities may not be subject to U.S. reporting and/or other requirements. Available information regarding the issuers of such securities may be limited, and such issuers may not be subject to the same auditing and reporting standards as U.S. issuers.

Such information is provided for informational purposes only and does not constitute a solicitation to buy or an offer to sell any securities under the Securities Act of 1933, as amended, or under any other U.S. federal or state securities laws, rules or regulations. The investment opportunities discussed in this report may be unsuitable for certain investors depending on their specific investment objectives, risk tolerance and financial position. In jurisdictions where SpareBank 1 Capital Markets is not registered or licensed to trade in securities, commodities or other financial products, transactions may be executed only in accordance with applicable law and legislation, which may vary from jurisdiction to jurisdiction and which may require that a transaction be made in accordance with applicable exemptions from registration or licensing requirements.

The information in this publication is based on carefully selected sources believed to be reliable, but SpareBank 1 Capital Markets does not make any representation with respect to its completeness or accuracy. All opinions expressed herein reflect the author’s judgment at the original time of publication, without regard to the date on which you may receive such information, and are subject to change without notice.

The information contained herein may include forward-looking statements as described above within the meaning of U.S. federal securities laws that are subject to risks and uncertainties. Factors that could cause a company’s actual results and financial condition to differ from expectations include, without limitation: political uncertainty, changes in general economic conditions that adversely affect the level of demand for the company’s products or services, changes in foreign exchange markets, changes in international and domestic financial markets and in the competitive environment, and other factors relating to the foregoing. All forward-looking statements contained in this report are qualified in their entirety by this cautionary statement.

Disclaimer