Embed Size (px)

Citation preview

BANKING It’s Time to Bank on Banks

JANUARY 16, 2013

Hatim Broachwala, CFA +91-22-6184 4329 hatim.broachwala @karvy.com Paresh Jain +91-22-6184 4324 paresh.jain @karvy.com

January 16, 2013

Banking Institutional Equities

India Research

THEME REPORT

Analysts Contact

Hatim Broachwala, CFA

022‐6184 4329

Paresh Jain

022 6184 4324

It’s Time to Bank on Banks The Banking sector has given a return of 42%, outperforming the broader

markets by whopping 20%, over last 12 months. While the large private banks

i.e. ICICI Bank, HDFC Bank & Axis Bank gave a return of >45% in last one

year, the PSU banks have notably outperformed over last month.

Key Sectoral Dynamics

Rate Cut – Likely from Q4FY13 Onwards: We expect interest rate to ease

by 125‐150bps in CY13, supported by significant correction in core

inflation, OIS rates and recent RBI’s policy statement. RBI is likely to shift

its focus towards protecting growth as against resisting inflation.

Asset Quality – Expected to Improve from FY14 Onwards: We believe

that the asset quality to start improving from FY14E onwards on the back

of improvement in PMI, series of reforms undertaken recently, likely

decline in slippages and moderation in NPA formations for the PSU banks.

Credit Growth – Likely to Remain Buoyant: Credit growth continues to

remain above RBI’s target despite sluggishness in the economy. We expect

improvement in demand, driven by lower interest rate and improvement

in lending climate.

Outlook & Valuation

Even after the recent rally, most of the PSU Banks are trading at discount to

their mean valuation, while few select banks are even trading closer to their 1‐

SD valuation. We believe that in a scenario of economic revival, the PSU banks

offer an attractive risk reward. We have upgraded our recommendations on

four PSU banks (Canara, PNB, SBI & UBI), and downgraded our stance on two

private sector banks (ING & Karur), while revising the target price of the banks

under our coverage except for CUB.

Valuation Summary

Rating Target Price P/E P/ABV

Company CMP New Old New Old FY14E FY15E FY14E FY15E

Axis Bank 1,424 BUY BUY 1,725 1,330 10.3 8.9 1.9 1.6

Bank of Baroda 878 HOLD HOLD 985 740 5.6 4.6 1.1 0.9

Bank of India 385 BUY BUY 465 395 4.8 4.2 1.0 0.8

Canara Bank 523 HOLD SELL 570 410 5.5 4.7 1.0 0.8

City Union Bank 61 HOLD HOLD 65 65 7.4 5.9 1.6 1.3

HDFC Bank 668 HOLD HOLD 690 630 21.0 18.2 3.8 3.3

ICICI Bank # 1,204 BUY BUY 1,520 1,155 13.6 11.2 1.7 1.5

Indian Overseas Bank 92 SELL SELL 96 70 5.4 4.4 0.7 0.7

ING Vysya Bank 581 HOLD BUY 625 495 12.3 10.2 1.8 1.5

J&K Bank 1,358 BUY BUY 1,560 1,500 6.2 5.3 1.2 1.0

Karur Vysya Bank 556 HOLD BUY 610 535 7.7 6.3 1.6 1.4

Oriental Bank of Commerce 347 HOLD HOLD 365 320 5.8 5.0 0.9 0.8

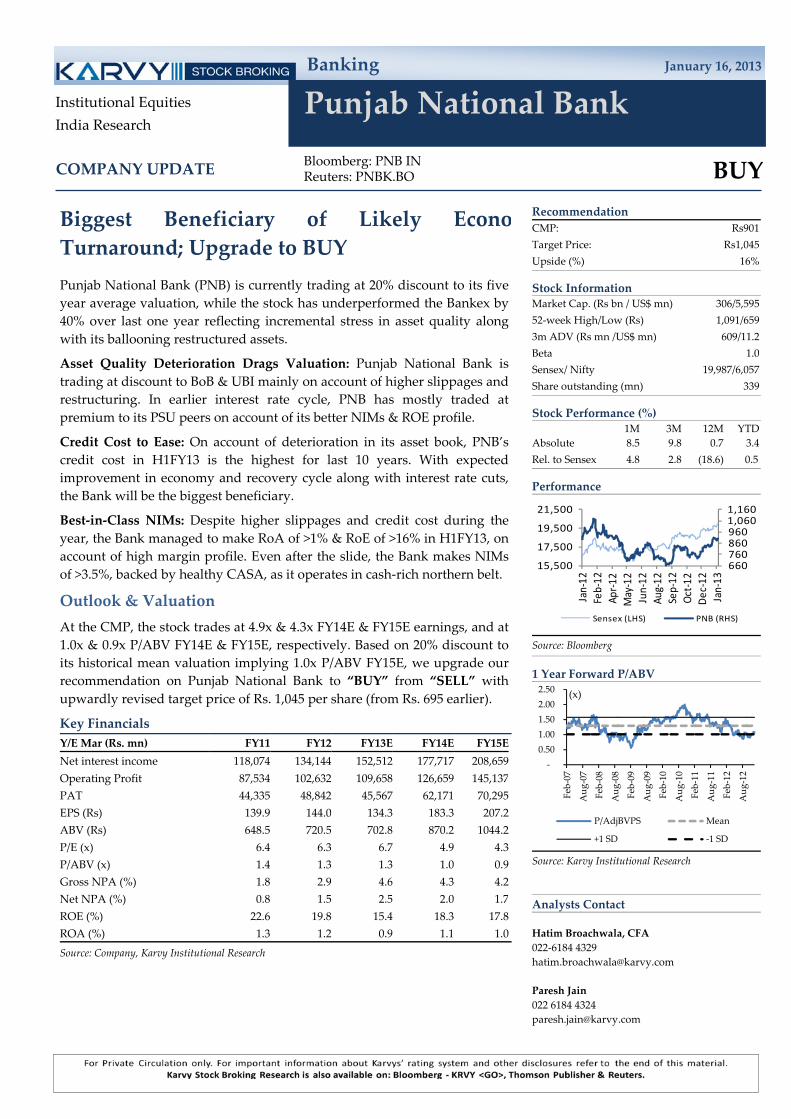

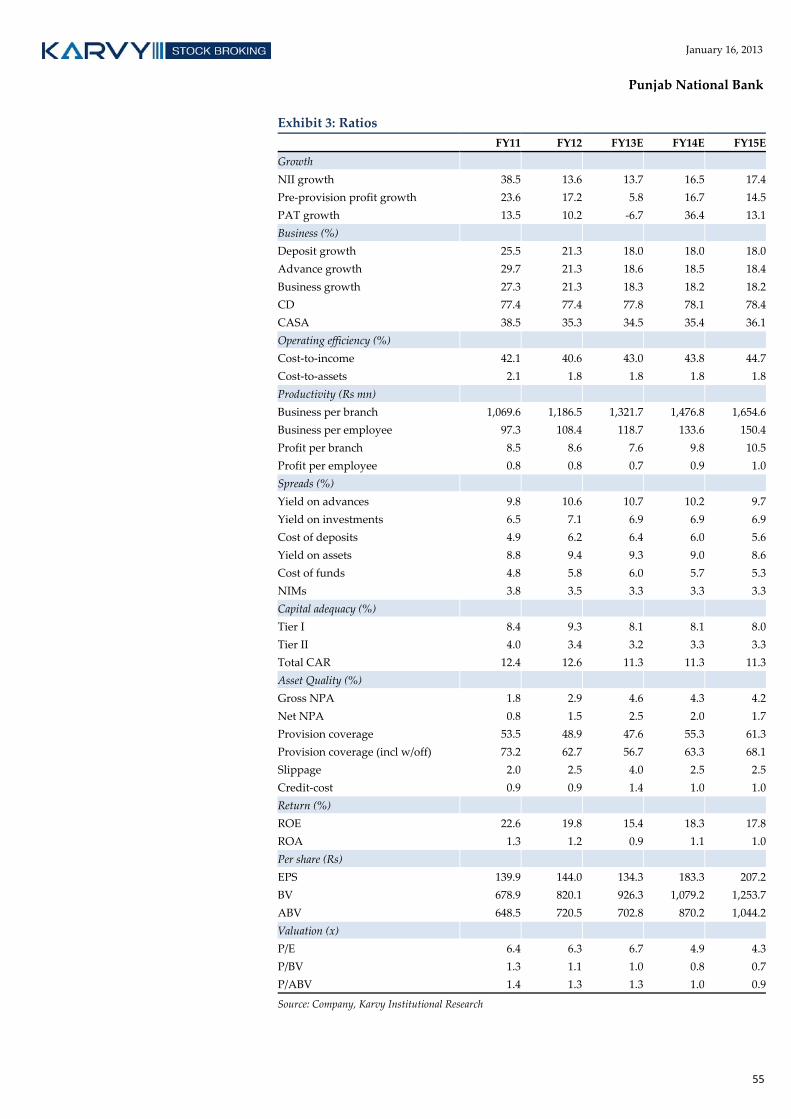

Punjab National Bank 901 BUY SELL 1045 695 4.9 4.3 1.0 0.9

State Bank of India # 2,490 BUY SELL 2,885 1,980 6.9 5.9 1.5 1.2

Syndicate Bank 144 BUY BUY 175 150 4.4 4.1 0.9 0.7

Union Bank of India 269 BUY HOLD 315 260 4.7 4.0 1.0 0.9

Source: Karvy Institutional Research; # Valuation after adjusting for subsidiaries; CMP is as of 15Jan2013

2

January 16, 2013

Banking

Table of contents. Executive Summary ∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙ 3 Rate Cut – A Key Trigger to Watch Out For ∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙ 4

A. Bankex Rallies on Expectations of Rate Cut ....................................................................................................................... 4 B. Core Inflation below 5% for 1st Time in 32 Months ............................................................................................................ 4 C. Correction in OIS also Suggests Correction in Rates ......................................................................................................... 5 D. RBI Turns Dovish – Expect Policy Rates to Start Easing in Q4FY13 ............................................................................... 6

Asset Quality to Improve from FY14 Onwards ∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙ 7 A. Slippage to Ease Significantly especially for PSU Banks .................................................................................................... 7 B. PMI indicates Improvement in Business Sentiment ........................................................................................................... 7 C. Govt on Reform Mode – Added Optimism .......................................................................................................................... 8 D. NPA Formation Moderating for PSU Banks ...................................................................................................................... 8 E. Credit Cost to Moderate ...................................................................................................................................................... 9 F. Provision Coverage to Improve ............................................................................................................................................ 9

Credit Growth Momentum Continues ∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙ 10 A. Credit Growth remains above RBI’s Target despite Slowdown ........................................................................................ 10 B. Credit Growth – Corporate Segment Rules the Roost ....................................................................................................... 10 C. Visible Slowdown in Credit to Vulnerable Sectors ............................................................................................................ 11 D. Engines for Retail Credit keep Altering ............................................................................................................................ 12 E. Lower Loan Origination – Minimal Default Risk ............................................................................................................. 12 F. Lower Deposit Growth – Pressure on Balance‐sheet ......................................................................................................... 13 G. Liquidation of Excess SLR can Provide Relief ................................................................................................................... 13

NIMs – Marginal Compression is Likely ∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙ 14 A. Positive Correlation between Interest Rate & NIMs ........................................................................................................ 14 B. Improvement in CASA to Annul Sharp Fall in Margins ................................................................................................. 14

Valuations – Seem to be Reasonable ∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙ 15 A. PSU Banks Trading at Discount to Mean Valuation ....................................................................................................... 15 B. ROA & P/ABV Matrix ...................................................................................................................................................... 15

Risk to Our Recommendations ∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙ 16

Companies Section Axis Bank‐Superior Asset Quality & Business Growth; Maintain BUY ∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙ 17

Bank of Baroda‐ Management change can be tricky; Maintain HOLD ∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙ 20 Bank of India‐ Pressure on Asset Quality to Ease, NIMs Set to Improve; Maintain BUY ∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙ 23

Canara Bank‐ Business Growth to Gain Momentum, Pressure on Asset Quality to Ease; Upgrade to HOLD ∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙ 26

City Union Bank‐ Positives Priced‐in; Maintain HOLD ∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙ 29

HDFC Bank‐ Superior Asset Quality, Earning Consistency; Maintain HOLD ∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙ 32

ICICI Bank‐ Improved Asset Quality, NIMs to Sustain at Current Levels; Maintain BUY ∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙ 35

Indian Overseas Bank‐ Worst not yet over; Stock to Continue to Trade at Discount to Peers; Maintain SELL ∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙ 38

ING Vysya Bank‐ Steady Performer, but Positives Priced‐in; Downgrade to HOLD ∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙ 41 J&K Bank‐ Improving Fundamentals – Case for Rerating; Maintain BUY ∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙ 44

Karur Vysya Bank‐ Best in Class, but Positives Priced‐in; Downgrade to HOLD ∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙ 47

Oriental Bank of Commerce‐ Moderate Business Growth amid Contraction in NIMs; Maintain HOLD ∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙ 50

Punjab National Bank‐ Biggest Beneficiary of Likely Economic Turnaround; Upgrade to BUY ∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙ 53

State Bank of India‐ Incremental Slippages & Credit Cost to Move Southwards; Upgrade to BUY ∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙ 56

Syndicate Bank‐ Stable Earning, Better Asset Quality; Maintain BUY ∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙ 59

Union Bank of India‐ Asset Quality Pressure to ease, Rally to Continue; Upgrade to BUY ∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙∙ 62

3

January 16, 2013

Banking

Executive Summary

Bankex Rallies on Expectations of Rate Cut

Outperforming broader markets by whopping 20%, the Banking sector has given a

return of 42% over last 12 months. While the large private banks i.e. ICICI Bank,

HDFC Bank & Axis Bank gave a return of >45% in last 1 year, the PSU banks have

notably outperformed over last month on expectations of rate cut. Meanwhile, the

core inflation dropping below 5% and the WPI‐based inflation easing to 7.18% in

Dec’12 provide significant elbowroom for the RBI to maneuver policy rates to

protect growth. At the same time, the OIS has corrected by ~100 bps from its recent

high, while Repo rate has been cut by only 50 bps over last 9 months. Again, the

OIS spread on the 3 month tenor has eased notably over last year, which indicates

correction in policy rates as well. Although RBI has Kept key rates unchanged in

mid‐quarter policy review in Dec’12, but it has clearly signaled easing in rates

from Q4FY13 onwards with a view to protecting growth.

Asset Quality to Improve from FY14 Onwards

The incremental slippages of PSU banks in H2FY13 are likely to be significantly

lower than H1FY13, while the asset quality of banks, especially PSU banks is

expected to turnaround from Q1FY14 onwards. At the same time, amidst the

allegation of complete policy paralysis, the series of reforms cleared by the UPA

Government would help the economy to rise from the headwinds, which it has

been facing over the last downturn. Meanwhile, the NPA formation has receded

for the PSU Banks in Q2FY13, while the private banks have done exceedingly well

in terms of asset quality. We believe that the pressures on asset quality would start

easing, going forward. In line with likely improvement in asset quality, we believe

that the overall credit cost – especially of the PSU banks – will decline notably

enabling them to report higher profits, while the credit cost of private banks would

normalize from the current low levels.

Credit Growth Momentum Continues

With likely correction in interest rates and revival in economy, the credit growth is

expected to remain buoyant, going ahead. Though the credit to vulnerable risky

sectors has declined significantly from its high in FY11, the PSU Banks have still

relatively higher exposure to difficult sectors, compared to their private

counterparts. We believe that, the banks are in a position to comfortably absorb

some amount of compression in NIMs, as they are on a cyclical high presently.

Again, even though the CASA has deteriorated for most of the banks over last two

years, we believe that the CASA would take a reversal, thereby providing cushion

against sharper decline in NIMs.

Outlook & Valuation

Even after the recent rally, most of the PSU Banks are trading at significant

discount to their mean valuation, while few select banks are even trading closer to

their 1‐SD valuation. We believe that in a scenario of economic revival, the PSU

banks offer an attractive risk reward. We have upgraded Union Bank of India

(UBI), Punjab National Bank (PNB) & State Bank of India (SBI) to “BUY”, and

Canara Bank to “HOLD”, while downgrading ING Vysya Bank & Karur Vysya

Bank to “HOLD” on account of sharp price run‐up.

4

January 16, 2013

Banking

Rate Cut – A Key Trigger to Watch Out For

A. Bankex Rallies on Expectations of Rate Cut Banking sector has given a return of 42%, outperforming broader markets by a

whopping 20% over last 12 months. The private banks i.e. ICICI Bank, HDFC Bank

& Axis Bank – which continued to be in flavor throughout the year – have given >45%

return in last 12 months. Though the PSU Bank traded weak in the early part of the

year, they have considerably outperformed over last month on expectations of rate

cut.

Exhibit 1: Repo & Bankex 1 year Return

Source: Bloomberg, Karvy Institutional Research

Our View: Bankex has rallied over 20% in just last 6 months, and we believe the

rally can be purely attributed to expectations of rate cut. As the Bankex has a very

strong negative correlation with movement in interest rates, we expect another

125‐150 bps of cut in repo in CY13 would enable Bankex to continue to outperform.

We have upgraded recommendation / target price for stocks under our coverage

universe, factoring in reduction in interest rates.

B. Core Inflation below 5% for 1st Time in 32 Months Core inflation has dropped below 5% for the first time in past 32 months, driven

by decline in prices of cement, iron & semis and steel. Correction in core inflation

has also contributed to easing of headline WPI‐based inflation which stood at

7.18% in Dec’12. Inflation in last nine months has expanded by 4.7% YTD, mainly

due to sharp rise in cereal prices.

Exhibit 2: Inflation

Source: Bloomberg, Karvy Institutional Research

‐100.0

‐50.0

0.0

50.0

100.0

150.0

200.0

0.0

2.0

4.0

6.0

8.0

10.0Dec/02

Jun/03

Dec/03

Jun/04

Dec/04

Jun/05

Dec/05

Jun/06

Dec/06

Jun/07

Dec/07

Jun/08

Dec/08

Jun/09

Dec/09

Jun/10

Dec/10

Jun/11

Dec/11

Jun/12

Dec/12

Repo Bankex Return

(%) (%)

‐

2.00

4.00

6.00

8.00

10.00

12.00

Feb‐10

Apr‐10

Jun‐10

Aug‐10

Oct‐10

Dec‐10

Feb‐11

Apr‐11

Jun‐11

Aug‐11

Oct‐11

Dec‐11

Feb‐12

Apr‐12

Jun‐12

Aug‐12

Oct‐12

Dec‐12

Core Inflation WPI

(%)

5

January 16, 2013

Banking

Our View: Expectation on inflation mainly depends on rainfall, going ahead.

Significant control in core inflation amid consistent ease in WPI‐based inflation –

which is now close to RBI’s comfort level – has given significant elbowroom for

the RBI to maneuver policy rates to protect growth.

C. Correction in OIS also Suggests Correction in Rates Overnight Indexed Swap (OIS) is a very good indicator of interbank credit market.

The fixed leg of the interest rate swap is determined by OIS, which can also be

interpreted as short‐term funding cost for the Indian banks. OIS and Repo rate has

a very high co‐relation of 0.92 over last 8 years. OIS has corrected by ~100 bps from

its recent high, whereas Repo is cut by only 50 bps over last 9 months.

Exhibit 3: Repo & OIS 3M

Source: Bloomberg, Karvy Institutional Research

OIS & G‐Sec: OIS also has a very high correlation with G‐Sec on the 3 month as

well as 1 year tenor.

Exhibit 4: OIS & G‐Sec (3M) are trending downwards

Source: Bloomberg, Karvy Institutional Research

Exhibit 5: OIS & G‐Sec (1Year) are relatively flattish

Source: Bloomberg, Karvy Institutional Research

OIS Spread: OIS spread – the difference between interbank rate (floating leg of OIS

swap) and OIS – is a gauge of perception of risk in credit market and also indicates

market expectations of movement in policy rates. OIS spread on the 3 month tenor

has eased significantly over last year which indicates increase in risk taking ability

as well as correction in policy rates.

3

5

7

9

11

13

0

2

4

6

8

10

May/05

Sep

/05

Jan/06

May/06

Sep

/06

Jan/07

May/07

Sep

/07

Jan/08

May/08

Sep

/08

Jan/09

May/09

Sep

/09

Jan/10

May/10

Sep

/10

Jan/11

May/11

Sep

/11

Jan/12

May/12

Sep

/12

Jan/13

Repo OIS 3m

(%) (%)

0

2

4

6

8

10

12

Jan/05

Jul/05

Jan/06

Jul/06

Jan/07

Jul/07

Jan/08

Jul/08

Jan/09

Jul/09

Jan/10

Jul/10

Jan/11

Jul/11

Jan/12

Jul/12

Jan/13

Gsec 3m OIS 3m

(%)

0

2

4

6

8

10

12

Jan/05

Jul/05

Jan/06

Jul/06

Jan/07

Jul/07

Jan/08

Jul/08

Jan/09

Jul/09

Jan/10

Jul/10

Jan/11

Jul/11

Jan/12

Jul/12

Jan/13

Gsec 1 Yr OIS 1 Yr

(%)

6

January 16, 2013

Banking

Exhibit 6: OIS Spread (3M) Indicates Optimism

Source: Bloomberg, Karvy Institutional Research

Our View: Correction in policy rates is imminent, as the OIS has corrected by ~90

bps from its recent high, while Repo is cut by only 50 bps over last 9 months.

Meanwhile, OIS spread on the 3 month tenor has eased notably over last year,

which indicates rise in risk taking ability and correction in policy rates as well.

D. RBI Turns Dovish – Expect Policy Rates to Start

Easing in Q4FY13 Although the RBI in its mid‐quarter policy review in Dec’12 has kept all its key

rates intact, the guidance has become much more dovish. The RBI seems to be very

comfortable with current inflation situation and will now start focusing on

protecting growth.

RBI’s Statement Mid‐Quarter Policy Review in Dec’12: “Headline inflation has

been below the Reserve Bank’s projected levels over the past two months. The

decline in core inflation has also been comforting. These emerging patterns

reinforce the likelihood of steady moderation in inflation going into 2013‐14,

though inflation may edge higher over the next two months. In view of inflation

pressures ebbing, monetary policy has to increasingly shift focus and respond to

the threats to growth from this point onwards … overall, recent inflation patterns

and projections provide a basis for reinforcing our October guidance about policy

easing in the fourth quarter,” the RBI said in its mid‐quarter policy review in

Dec’12, signaling that the policy rates would start easing in Q4FY13.

Our View: While the outlook for policy rate will be highly dependent on monsoon,

125‐150 bps of cut in repo over CY13 is expected with 50 bps cut in Q3FY policy

review on January 29, 2013.

‐1

0

1

2

3

4

5

6

7

Jan/03

Jun/03

Nov/03

Apr/04

Sep

/04

Feb/05

Jul/05

Dec/05

May/06

Oct/06

Mar/07

Aug/07

Jan/08

Jun/08

Nov/08

Apr/09

Sep

/09

Feb/10

Jul/10

Dec/10

May/11

Oct/11

Mar/12

Aug/12

Jan/13

OIS Spread 3m

(%)

7

January 16, 2013

Banking

Asset Quality to Improve from FY14 Onwards

A. Slippage to Ease Significantly especially for PSU

Banks We expect asset quality of banks, especially PSU banks to turnaround starting

from Q1FY14. As per the information we receive from our recent interaction with

the managements of several PSU banks, the incremental slippages in H2FY13 are

likely to be significantly lower than H1FY13. Incremental recovery / upgradation is

expected to excel and match incremental slippages thereby maintaining absolute

GNPA at current levels.

Exhibit 7: PSU Banks – Slippages to Ease

Source: Company, Karvy Institutional Research

On the other hand, private banks have done exceedingly well in terms of asset

quality. We have conservatively factored slippages to normalize over FY14‐15E.

Exhibit 8: Private Banks – Slippages Already at a Comfortable Levels

Source: Company, Karvy Institutional Research

Our View: PSU Banks have seen huge increase in slippages in H1FY13. Even after

accounting for relatively better H2FY13, slippages for FY13E will increase

substantially over FY12. We expect asset quality pressure to ease significantly

over FY14‐15E.

B. PMI indicates Improvement in Business Sentiment Improvement in business sentiment as indicated by HSBC PMI surged to a six

month high amid a spike in new orders.

0.0

1.0

2.0

3.0

4.0

5.0

BOB Canara UBI BOI IOB PNB Syndicate SBI OBC

FY12 FY13E FY14E FY15E

(%)

0.0

0.5

1.0

1.5

2.0

ING KVB HDFC J&K Axis ICICI CUB

FY12 FY13E FY14E FY15E

(%)

8

January 16, 2013

Banking

Exhibit 9: Strengthening PMI

Source: Bloomberg, Karvy Institutional Research

Our View: Improvement in business sentiment would contribute towards banks’

efforts on recovery as well as assist them in containing incremental slippages.

C. Govt on Reform Mode – Added Optimism The UPA Government has been able to clear few landmark bills which were

pending for a considerable period of time. Amidst the allegation of complete

policy paralysis with regard to reforms, the Government surprised everyone

including their most staunch supporters by clearing FDI in Multi‐band Retail,

Aviation, Insurance, & Pension, which along with other reforms spread a wave of

optimism amongst the investors’ community. Meanwhile, amendment to “Banking

Regulation Act & Banking Companies Acquisition & Transfer Act” will enable the RBI

to issue additional bank licenses along with additional powers to regulate banks.

Positive initiatives from government to address fuel issues are expected to bring

faster developments on policy. We also expect regular power tariff hikes by all

states would resolve power sector issues.

Our View: Such series of reforms would help the economy to rise from the

headwinds it has been facing over the last downturn, while the plan for gradual

hike in diesel prices to cut fuel subsidy and thereby moving towards fiscal

consolidation could be seen as the preparatory work for next phase of growth.

D. NPA Formation Moderating for PSU Banks

After series of turbulent quarters, the NPA formation has receded for PSU Banks

in Q2FY13, while the private banks have done exceedingly well in terms of asset

quality. The pressures on asset quality would start easing, as we progress into

policy rate cuts followed by economic recovery.

Exhibit 10: PSU Bank – GNPA has bottomed out

Source: Company, Karvy Institutional Research

44

49

54

59

64

Dec‐08

Mar‐09

Jun‐09

Sep‐09

Dec‐09

Mar‐10

Jun‐10

Sep‐10

Dec‐10

Mar‐11

Jun‐11

Sep‐11

Dec‐11

Mar‐12

Jun‐12

Sep‐12

Dec‐12

PMI Index

1.0

2.0

3.0

4.0

5.0

6.0

BOB Canara BOI Syndicate IOB PNB UBI OBC SBI

FY12 FY13E FY14E FY15E

(%)

9

January 16, 2013

Banking

Exhibit 11: Private Banks – Gross NPA to Normalize

Source: Company, Karvy Institutional Research

Our View: While the NPAs of PSU banks and ICICI Bank are likely improve; it

would remain flattish for other private banks.

E. Credit Cost to Moderate In line with likely improvement in asset quality, we believe that the overall credit

cost – especially of PSU banks – will decline notably enabling them to report higher

profits, while the credit cost of private banks would normalize from the current

low levels.

Exhibit 12: Credit Cost to Ease

Source: Company, Karvy Institutional Research

Our View: While the overall credit cost of PSU banks will decline significantly,

the credit cost of private banks would normalize from the current low levels.

F. Provision Coverage to Improve With expected slippage level to ease significantly, we expect provision coverage to

improve even after accounting for lower credit cost. Banks would also like to

buffer up for next down‐cycle.

Exhibit 13: Provision Coverage to Improve

Source: Company, Karvy Institutional Research

0.0

1.0

2.0

3.0

4.0

Axis CUB HDFC ICICI ING J&K KVB

FY12 FY13E FY14E FY15E

(%)

0.0

0.5

1.0

1.5

KVB

ING

J&K

HDFC

ICICI

CUB

Can

ara

Axis

BOB

BOI

PNB

UBI

OBC

IOB

Syndicate

SBI

FY12 FY13E FY14E FY15E

(%)

40.050.060.070.080.090.0100.0

OBC

UBI

PNB

BOI

SBI

IOB

Can

ara

KVB

CUB

BOB

Syndicate

ICICI

Axis

HDFC

ING

J&K

FY12 FY13E FY14E FY15E

(%)

10

January 16, 2013

Banking

Credit Growth Momentum Continues

A. Credit Growth remains above RBI’s Target despite

Slowdown Even though the credit growth has taken a hit on account of slowdown in the

economy and halt in capex cycle, it remains above the RBI’s FY13 target of 16%.

Exhibit 14: Credit Growing at Decent Pace

Source: Bloomberg, Karvy Institutional Research

Our View: With likely correction in interest rates and revival in economy, credit

growth is expected to remain buoyant, going ahead.

B. Credit Growth – Corporate Segment Rules the Roost Growth in corporate / industry segment is showing a declining trend, yet it

continues to be the fastest growing segment over last five years. After the burst in

unsecured personal loan segment in 2008, the retail segment has grown at a very

modest rate over last five years, though off late it is showing some signs of revival.

Agriculture has been the fastest growing segment this year, whereas services

continue to be sluggish.

Exhibit 15: Growth in Industry Segment – Better than Other Segments

Source: RBI, Karvy Institutional Research

Our View: Within the industry segment, the large corporates have contributed to

bulk of the growth. On account of cautious approach adopted by banks, growth in

small and medium segment has seen a significant downturn.

051015202530

Mar/09

Jun/09

Sep

/09

Dec/09

Mar/10

Jun/10

Sep

/10

Dec/10

Mar/11

Jun/11

Sep

/11

Dec/11

Mar/12

Jun/12

Sep

/12

Dec/12

Credit Growth

(%)

0.0

10.0

20.0

30.0

FY09 FY10 FY11 FY12 Nov‐12

Agriculture Industry Services Retail

(%

11

January 16, 2013

Banking

Exhibit 16: Large Industries Contributed to Growth

Source: RBI, Karvy Institutional Research

C. Visible Slowdown in Credit to Vulnerable Sectors Credit growth to risky sectors like Infrastructure, Metal/Mining & Textiles has

significantly slowed down from its high in FY10‐11.

Exhibit 17: Growth to Troubled Sectors has slowed down

Source: RBI, Karvy Institutional Research

The PSU Banks have relatively higher exposure to vulnerable sectors in

comparison to their private counterparts.

Exhibit 18: Vulnerable Sectors (% of Loan Book) – Pvt Banks are Well‐placed

Source: Company, Karvy Institutional Research

Our View: Though the credit to vulnerable risky sectors has declined significantly

from its high in FY11, the PSU Banks have still relatively higher exposure to

difficult sectors, compared to their private counterparts.

0.0

5.0

10.0

15.0

20.0

25.0

30.0

35.0

40.0

FY09 FY10 FY11 FY12 Nov‐12

Micro/Small Medium Large

(%)

0.0

10.0

20.0

30.0

40.0

50.0

FY09 FY10 FY11 FY12 Nov‐12

Infrastructure Metal/Mining Textiles

(%)

0.0

5.0

10.0

15.0

20.0

25.0

30.0

35.0

HDFC

ING

Axis

BOI

BOB

Syndicate

CUB

J&K

ICICI

PNB

OBC

UBI

KVB

IOB

Can

ara

SBI

Infrastructure Metal/Mining Textiles

(%)

12

January 16, 2013

Banking

D. Engines for Retail Credit keep Altering The mortgage segment has seen a decent growth, despite the recent slowdown on

account of higher real estate prices. After a brief lull in FY09‐10, the auto segment

is growing at brisk rate on the back of strong auto sales, while the education loans

have nosedived after rise in NPA post recession. Following a muted growth in

FY09‐12, the credit cards / personal loans have evidently grown at a higher rate.

Exhibit 19: Growth within Retail Segment

Source: RBI, Karvy Institutional Research

E. Lower Loan Origination – Minimal Default Risk In the following chart, we provide the loans origination by the banks under our

coverage during FY09‐12 period.

Exhibit 20: Loan Origination over FY09‐12

Source: Company, Karvy Institutional Research

Our View: The banks originating lower loans over last three years are at more

comfortable position than their peers, as the likelihood of default remains high for

loans originated during economic slowdown.

‐10.0

0.0

10.0

20.0

30.0

40.0

50.0

FY09 FY10 FY11 FY12 Nov‐12

Mortgage Auto Education Credit Cards/Personal

(%)

0.0

10.0

20.0

30.0

40.0

50.0

60.0

ICICI

Syndicate

J&K

SBI

OBC

Can

ara

ING

BOI

UBI

IOB

PNB

HDFC

BOB

Axis

CUB

KVB

Loan Origination over FY09‐12

(%)

13

January 16, 2013

Banking

F. Lower Deposit Growth – Pressure on Balance‐sheet Deposit growth, which has significantly declined over last year, has been putting

pressure on balance sheet of banks.

Exhibit 21: Languishing Deposit Growth

Source: Bloomberg, Karvy Institutional Research

Our View: Credit‐Deposit (CD) ratio has been hovering closer to its all time high

levels. Despite successive OMOs and CRR cuts, deficit in Liquidity Adjustment

Facility (LAF) has remained above the RBI’s comfort zone.

G. Liquidation of Excess SLR can Provide Relief Statutory Liquidity Ratio (SLR) is currently maintained by banks at ~28% is much

in excess of regulatory stipulated 23%. Dspite reduction in SLR by the RBI, banks

have not brought down their SLR ratios.

Exhibit 22: Excess SLR to Compensate for Lower Deposit Growth

Source: Bloomberg, Karvy Institutional Research

Our View: The banks prefer to park funds with government over lending in times

of tough conditions, but with initial signs of economic recovery, the banks can

now utilize excess SLR to fund credit compensating for lower deposit growth.

68.0

70.0

72.0

74.0

76.0

78.0

80.0

10.0

12.0

14.0

16.0

18.0

20.0

22.0

24.0

Mar/09

May/09

Jul/09

Sep

/09

Nov/09

Jan/10

Mar/10

May/10

Jul/10

Sep

/10

Nov/10

Jan/11

Mar/11

May/11

Jul/11

Sep

/11

Nov/11

Jan/12

Mar/12

May/12

Jul/12

Sep

/12

Nov/12

Deposit Growth CD Ratio (RHS)

(%)

22.0

24.0

26.0

28.0

30.0

32.0

Apr/06

Aug/06

Dec/06

Apr/07

Aug/07

Dec/07

Apr/08

Aug/08

Dec/08

Apr/09

Aug/09

Dec/09

Apr/10

Aug/10

Dec/10

Apr/11

Aug/11

Dec/11

Apr/12

Aug/12

Dec/12

SLR maintained by banks SLR Required by RBI

(%)

14

January 16, 2013

Banking

NIMs – Marginal Compression is Likely

A. Positive Correlation between Interest Rate & NIMs During last interest rate cycle, the Net Interest Margins (NIMs) of the banks have

shown a positive correlation with movement in the interest rates on account of

assets getting reprised faster than deposits.

Exhibit 23: NIMs off‐late has a Positive Co‐Relation with Interest Rates

Source: Bloomberg, Karvy Institutional Research

Our View: As the NIMs are on a cyclical high presently, the banks are in a

position to comfortably absorb some amount of compression.

B. Improvement in CASA to Annul Sharp Fall in

Margins CASA has deteriorated for most of the banks over last 2 years, as in times of high

interest rates canabilzation of saving to term deposits happens.

Exhibit 24: CASA to Improve with Fall in Rates

Source: Company, Karvy Institutional Research

Our View: With expectation of decline in interest rate, we believe that the CASA

should take a reversal, thereby providing cushion against sharper fall in NIMs.

Also the proposed direct cash transfer scheme would aid banks garner higher float

adding to accumulation of CASA.

2.5

2.6

2.7

2.8

2.9

3

3.1

3.2

0

2

4

6

8

10

Mar/03

Aug/03

Jan/04

Jun/04

Nov/04

Apr/05

Sep

/05

Feb/06

Jul/06

Dec/06

May/07

Oct/07

Mar/08

Aug/08

Jan/09

Jun/09

Nov/09

Apr/10

Sep

/10

Feb/11

Jul/11

Dec/11

May/12

Oct/12

Repo NIMs

(%)

10.0

20.0

30.0

40.0

50.0

60.0

HDFC

ICICI

SBI

Axis

J&K

PNB

ING

Syndicate

UBI

BOB

BOI

Can

ara

IOB

OBC

KVB

CUB

FY12 FY13E FY14E FY15E

(%)

15

January 16, 2013

Banking

Valuations – Seem to be Reasonable

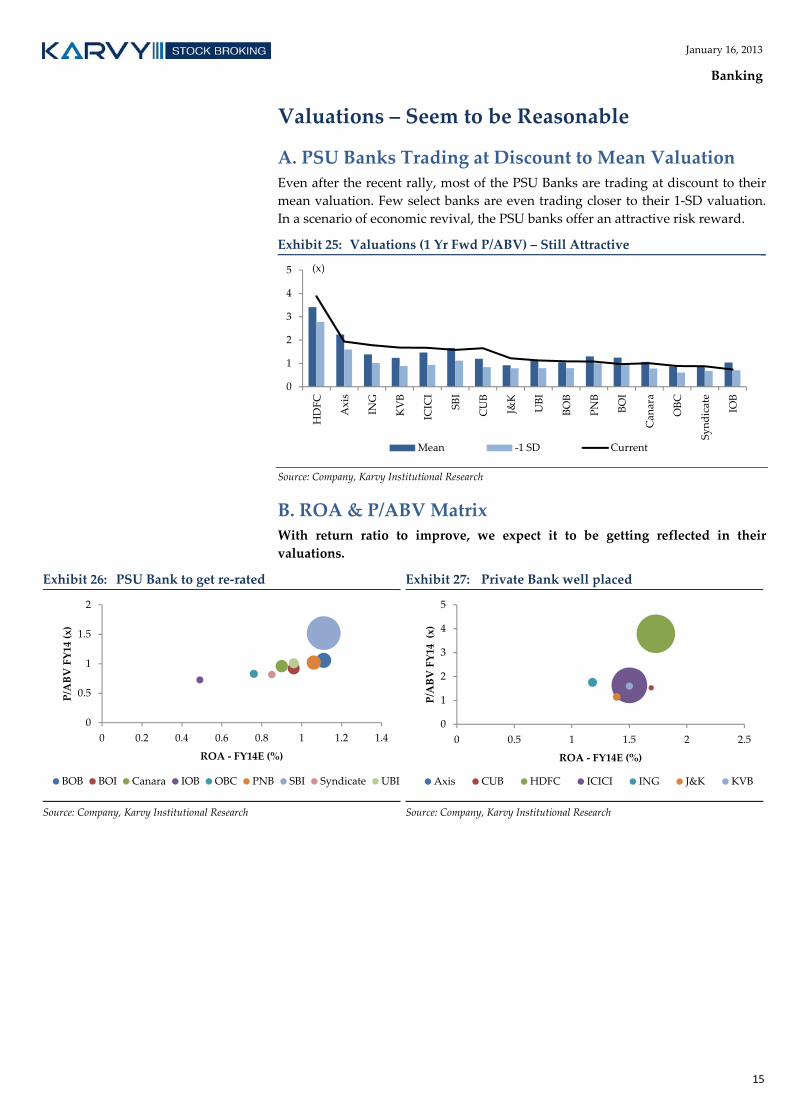

A. PSU Banks Trading at Discount to Mean Valuation Even after the recent rally, most of the PSU Banks are trading at discount to their

mean valuation. Few select banks are even trading closer to their 1‐SD valuation.

In a scenario of economic revival, the PSU banks offer an attractive risk reward.

Exhibit 25: Valuations (1 Yr Fwd P/ABV) – Still Attractive

Source: Company, Karvy Institutional Research

B. ROA & P/ABV Matrix With return ratio to improve, we expect it to be getting reflected in their

valuations.

Exhibit 26: PSU Bank to get re‐rated

Source: Company, Karvy Institutional Research

Exhibit 27: Private Bank well placed

Source: Company, Karvy Institutional Research

0

1

2

3

4

5

HDFC

Axis

ING

KVB

ICICI

SBI

CUB

J&K

UBI

BOB

PNB

BOI

Can

ara

OBC

Syndicate

IOB

Mean ‐1 SD Current

(x)

0

0.5

1

1.5

2

0 0.2 0.4 0.6 0.8 1 1.2 1.4

P/ABV FY14 (x)

ROA ‐ FY14E (%)

BOB BOI Canara IOB OBC PNB SBI Syndicate UBI

0

1

2

3

4

5

0 0.5 1 1.5 2 2.5

P/ABV FY14 (x)

ROA ‐ FY14E (%)

Axis CUB HDFC ICICI ING J&K KVB

16

January 16, 2013

Banking

Risk to Our Recommendations

Basel‐III Implementation: Migration to Basel‐III from Apr’13 will enhance the

need for core equity capital and restrict leverage flexibility especially for the

PSU banks.

Provisions for Wage Hike: As the wage hike agreement expired in Nov 12, the

new wage hike agreement would impact profitability of the PSU Banks.

Higher Provision on Restructured Assets: The RBI has increased provision on

restructured assets by 0.75% to 2.75% in the last quarter. In case the proposal

to increase the provision on restructured assets to 5% is implemented, it would

impact profitability of banks. However, excluding the accounts with

satisfactory performance of two years will bring down the quantum of

restructured book.

Banking January 16, 2013

Axis Bank

Bloomberg: AXSB INReuters: AXBK.BO BUY

Institutional Equities

India Research

COMPANY UPDATE

Recommendation

CMP: Rs1,424

Target Price: Rs1,725

Upside (%) 21%

Stock Information Market Cap. (Rs bn / US$ mn) 608/11,141

52‐week High/Low (Rs) 1,431/917

3m ADV (Rs mn /US$ mn) 2,280/41.8

Beta 1.2

Sensex/ Nifty 19,987/6,057

Share outstanding (mn) 427

Stock Performance (%) 1M 3M 12M YTD

Absolute 5.3 27.3 51.6 5.0

Rel. to Sensex 1.8 19.2 22.5 2.1

Performance

Source: Bloomberg

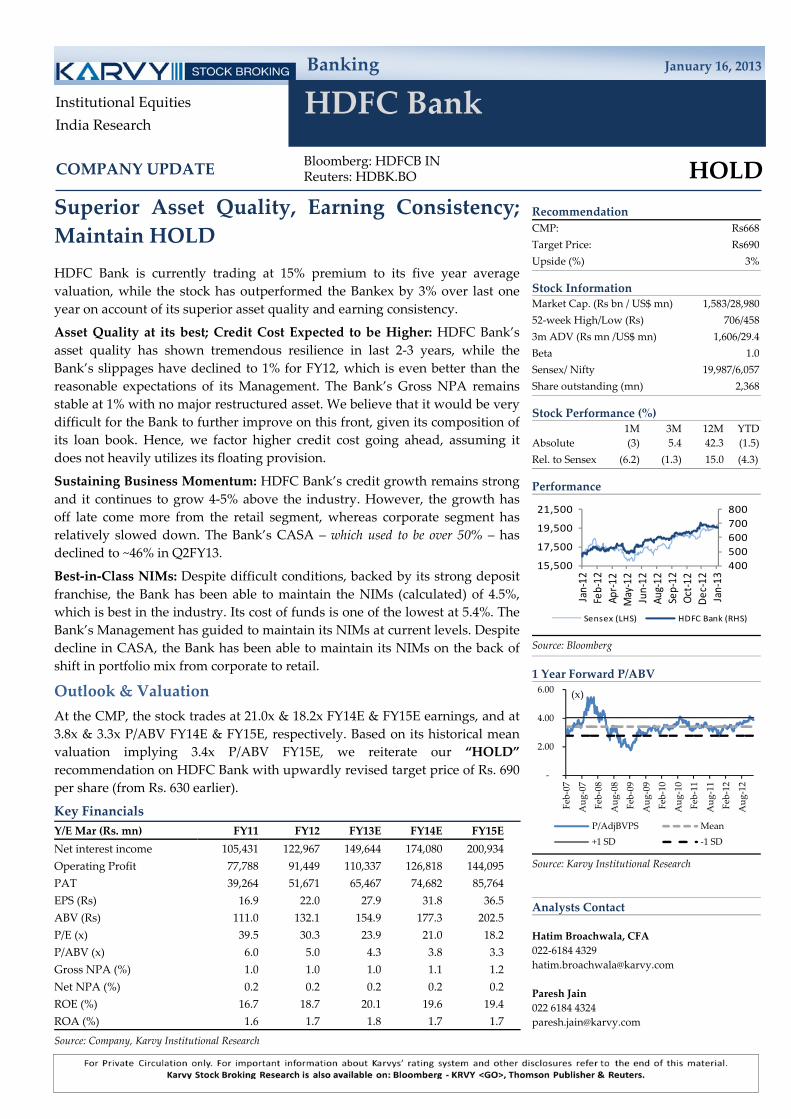

1 Year Forward P/ABV

Source: Karvy Institutional Research

Analysts Contact

Hatim Broachwala, CFA

022‐6184 4329

Paresh Jain

022 6184 4324

800

1,000

1,200

1,400

1,600

15,500

17,500

19,500

21,500

Jan‐12

Feb‐12

Apr‐12

May‐12

Jun‐12

Aug‐12

Sep‐12

Oct‐12

Dec‐12

Jan‐13

Sensex (LHS) Axis Bank (RHS)

‐

2.00

4.00

6.00

Feb‐07

Aug‐07

Feb‐08

Aug‐08

Feb‐09

Aug‐09

Feb‐10

Aug‐10

Feb‐11

Aug‐11

Feb‐12

Aug‐12

P/AdjBVPS Mean

+1 SD ‐1 SD

(x)

Superior Asset Quality & Business Growth;

Maintain BUY

Axis Bank is currently trading at 15% discount to its five year average

valuation. However, the stock has outperformed the Bankex by 6% over last

one year on account of superior asset quality, management efficiency and

earning momentum.

Business Growth above Industry: Credit growth has slightly slowed down as

against its earlier trends; still it continues to grow above industry. We believe

it has rightly slowed down to support any asset quality pressures in tough

times. The Bank’s majority of the growth has come from retail segment and

large corporates, while the composition of SME loans has come down over

500bps in last three years to 14%.

Stable NIMs: Despite volatile interest rate movement, the Bank’s NIMs remain

stable at ~3.3% over past three years. We expect the ability to maintain its

CASA ratio of >40% would enable it to prevent any major erosion in NIMs.

Strong Non‐Interest Income: Axis Bank is a very strong player in debt capital

markets including placement and syndication of bonds. Post‐acquisition of

Enam, the Bank has positioned itself to offer equity products. Higher growth

in retail fee income has offset lackluster performance in corporate segment.

Resilience in Asset Quality: The Bank has displayed decent resilience in its

asset quality as against market expectations of sharp deterioration. Though the

market is concerned over its larger infrastructure book, its Management is

confident of its quality. We have conservatively built in slightly higher credit

cost, going ahead.

Outlook & Valuation

At the CMP, the stock trades at 10.3x & 8.9x FY14E & FY15E earnings, and at

1.9x & 1.6x P/ABV FY13E & FY14E, respectively. Based on 10% discount to its

historical mean valuation implying 2.0x P/ABV FY15E, we reiterate our “BUY”

recommendation on Axis Bank with unrevised target price of Rs. 1725 per

share.

Key Financials

Rs Mn FY11 FY12 FY13E FY14E FY15E

Net interest income 65,630 80,178 96,188 112,905 131,879

Operating Profit 60,564 73,378 83,652 98,905 114,903

PAT 33,885 42,422 48,483 57,245 66,579

EPS 82.5 102.7 117.3 138.5 161.1

ABV 452.8 540.6 631.2 738.2 873.0

P/E 17.3 13.9 12.2 10.3 8.9

P/ABV 3.2 2.6 2.3 1.9 1.6

Gross NPA 1.1 1.1 1.1 1.3 1.3

Net NPA 0.3 0.3 0.3 0.4 0.3

ROE 19.3 20.3 19.6 19.7 19.5

ROA 1.6 1.6 1.6 1.6 1.5

Source: Company, Karvy Institutional Research

18

January 16, 2013

Axis Bank

Exhibit 1: Income Statement

FY11 FY12 FY13E FY14E FY15E

Interest Income 151,548 219,947 268,475 306,463 351,022

Interest expense 85,918 139,769 172,288 193,558 219,143

Net interest income 65,630 80,178 96,188 112,905 131,879

Fees 33,574 43,417 47,759 57,310 68,773

Other Income 9,154 9,854 9,426 12,113 14,642

Net Revenue 108,358 133,449 153,373 182,329 215,294

Operating Expense 47,794 60,071 69,720 83,424 100,391

‐Employee Exp 16,139 20,802 24,561 30,136 36,445

‐Other Exp 31,655 39,269 45,159 53,288 63,946

Operating Profit 60,564 73,378 83,652 98,905 114,903

Investment Profit 3,593 931 4,907 4,410 5,012

Pre‐provision Profit 64,157 74,309 88,560 103,315 119,915

Provisions 12,800 11,431 16,197 17,874 20,543

‐Loan Loss Provisions 11,364 10,996 17,631 18,478 21,377

‐Investment Depreciation 993 581 ‐1,488 ‐658 ‐888

‐Other Provisions 443 ‐146 54 54 54

PBT 51,357 62,878 72,362 85,441 99,372

Taxes 17,472 20,456 23,880 28,195 32,793

PAT 33,885 42,422 48,483 57,245 66,579

Source: Company, Karvy Institutional Research

Exhibit 2: Balance Sheet

FY11 FY12 FY13E FY14E FY15E

Equity Capital 4,105 4,132 4,132 4,132 4,132

Reserves & Surplus 185,883 223,954 263,493 310,587 365,564

Shareholderʹs Funds 189,988 228,086 267,625 314,719 369,696

Deposits 1,892,378 2,201,044 2,597,232 3,168,623 3,802,348

‐Current deposits 369,171 397,541 437,160 522,868 617,927

‐Saving deposits 408,503 516,680 615,727 787,144 977,262

‐Term deposit 1,114,704 1,286,823 1,544,345 1,858,610 2,207,159

Borrowings 262,679 340,717 394,732 449,778 510,828

‐Sub ordinate debt 69,932 105,740 121,944 138,458 156,773

Other liabilities 82,089 86,430 86,628 92,377 97,094

Total liabilities 2,427,134 2,856,277 3,346,217 4,025,496 4,779,965

Cash/Equivalent 214,087 139,339 189,392 261,579 341,642

Advances 1,424,078 1,697,595 2,022,469 2,468,154 2,962,459

Investments 719,916 931,921 1,030,968 1,173,816 1,332,247

Fixed Assets 22,732 22,593 25,593 28,593 31,593

Other assets 46,321 64,829 77,795 93,354 112,025

Total assets 2,427,134 2,856,277 3,346,217 4,025,496 4,779,965

Source: Company, Karvy Institutional Research

19

January 16, 2013

Axis Bank

Exhibit 3: Key Ratios

Ratioʹs FY11 FY12 FY13E FY14E FY15E

Growth (%)

NII growth 31.1 22.2 20.0 17.4 16.8

Pre‐provision profit growth 22.4 15.8 19.2 16.7 16.1

PAT growth 34.8 25.2 14.3 18.1 16.3

Business (%)

Deposit growth 33.9 16.3 18.0 22.0 20.0

Advance growth 36.5 19.2 19.1 22.0 20.0

Business growth 35.0 17.6 18.5 22.0 20.0

CD 75.3 77.1 77.9 77.9 77.9

CASA 41.1 41.5 40.5 41.3 42.0

Operating effeciency (%)

Cost‐to‐income 44.1 45.0 45.5 45.8 46.6

Cost‐to‐assets 2.4 2.4 2.4 2.4 2.4

Productivity (Rs mn)

Business per branch 2385.9 2403.6 2535.5 2787.7 3044.5

Business per employee 125.5 122.8 125.7 135.1 144.7

Profit per branch 24.4 26.2 26.6 28.3 30.0

Profit per employee 1.3 1.3 1.3 1.4 1.4

Spreads (%)

Yield on advances 8.4 9.9 10.2 9.7 9.3

Yield on investments 7.0 7.8 8.0 8.0 7.8

Cost of deposits 4.5 6.0 6.1 5.8 5.5

Yield on assets 7.7 8.9 9.2 8.9 8.5

Cost of funds 4.4 5.7 6.0 5.7 5.4

NIMs 3.3 3.2 3.3 3.3 3.2

Capital adequacy (%)

Tier I 9.4 9.5 9.5 9.3 9.2

Tier II 3.2 4.2 4.2 3.9 3.7

Total CAR 12.7 13.7 13.6 13.2 12.9

Asset Quality (%)

Gross NPA 1.1 1.1 1.1 1.3 1.3

Net NPA 0.3 0.3 0.3 0.4 0.3

Provision coverage 74.3 73.8 70.8 69.6 77.4

Provision coverage (incl w/off) 80.9 80.9 79.0 77.9 83.6

Slippage 1.2 1.2 1.1 1.3 1.2

Credit‐cost 0.8 0.6 0.8 0.7 0.7

Return (%)

ROE 19.3 20.3 19.6 19.7 19.5

ROA 1.6 1.6 1.6 1.6 1.5

Per share (Rs)

EPS 82.5 102.7 117.3 138.5 161.1

BV 462.8 552.0 647.7 761.7 894.7

ABV 452.8 540.6 631.2 738.2 873.0

Valuation (x)

P/E 17.3 13.9 12.2 10.3 8.9

P/BV 3.1 2.6 2.2 1.9 1.6

P/ABV 3.2 2.6 2.3 1.9 1.6

Source: Company, Karvy Institutional Research

Banking January 16, 2013

Bank Of Baroda

Bloomberg: BOB INReuters: BOB.BO HOLD

Institutional Equities

India Research

COMPANY UPDATE

Recommendation

CMP: Rs878

Target Price: Rs985

Upside (%) 12%

Stock Information Market Cap. (Rs bn / US$ mn) 361/6,609

52‐week High/Low (Rs) 900/606

3m ADV (Rs mn /US$ mn) 543/9.9

Beta 0.9

Sensex/ Nifty 19,987/6,057

Share outstanding (mn) 411

Stock Performance (%) 1M 3M 12M YTD

Absolute 4.3 12.6 20.7 1.3

Rel. to Sensex 0.8 5.4 (2.4) (1.5)

Performance

Source: Bloomberg

1 Year Forward P/ABV

Source: Karvy Institutional Research

Analysts Contact

Hatim Broachwala, CFA

022‐6184 4329

Paresh Jain

022 6184 4324

600

700

800

900

1,000

15,500

17,500

19,500

21,500

Jan‐12

Feb‐12

Apr‐12

May‐12

Jun‐12

Aug‐12

Sep‐12

Oct‐12

Dec‐12

Jan‐13

Sensex (LHS) Bank of Baroda (RHS)

‐

0.50

1.00

1.50

2.00

Feb‐07

Aug‐07

Feb‐08

Aug‐08

Feb‐09

Aug‐09

Feb‐10

Aug‐10

Feb‐11

Aug‐11

Feb‐12

Aug‐12

P/AdjBVPS Mean

+1 SD ‐1 SD

(x)

Management change can be tricky; Maintain

HOLD

Bank of Baroda (BoB) is currently trading at its five year average valuation.

However, the stock has underperformed the Bankex by 23% over last one

year reflecting incremental stress in last two quarters along with expectation

of further deterioration in asset portfolio in the aftermath of change in

management and partial correction of valuation premium over its peers.

Asset Quality Matrix – Better Placed: Bank of Baroda is better placed

amongst the large PSU banks in terms of total stress assets with Gross NPA

of 2% and restructured assets of 7.2%, though some amount of incremental

deterioration in asset quality is seen in H1FY13. The Bank enjoys comfortable

provision coverage of 76%.

Business Parameters – Good Show: The Bank has grown its business well

above the industry rate. The average growth for last four years has been 26%

in deposits and 28% in advances. But in the process, the Bank’s CASA has

taken a hit of ~500 bps during the same period. Its overseas business has

grown at an even higher average rate of 39% over last four years and now

forms 30% of its total business.

Change in Management – A Key Risk: With the change in management,

concern over deterioration in asset quality has risen. Higher growth in credit

along with resilience in asset quality has been strength, but it can turn into a

risk if slippages start increasing.

Outlook & Valuation

At the CMP, the stock trades at 5.6x & 4.6x FY14E & FY15E earnings, and at

1.1x & 0.9x P/ABV FY14E & FY15E, respectively. Based on its historical mean

valuation implying 1x P/ABV FY15E, we reiterate our “HOLD”

recommendation on Bank of Baroda with upwardly revised target price of

Rs. 985 per share (from Rs. 740 earlier).

Key Financials

Y/E Mar (Rs. mn) FY11 FY12 FY13E FY14E FY15E

Net interest income 88,022 103,170 119,262 144,362 170,415

Operating Profit 65,381 79,732 96,812 115,349 134,053

PAT 42,417 50,070 51,185 64,798 78,290

EPS (Rs) 108.0 121.4 124.1 157.1 189.8

ABV (Rs) 536.0 649.5 701.9 829.6 984.9

P/E (x) 8.1 7.2 7.1 5.6 4.6

P/ABV (x) 1.6 1.3 1.2 1.1 0.9

Gross NPA (%) 1.4 1.5 2.1 2.2 2.2

Net NPA (%) 0.3 0.5 0.8 0.7 0.6

ROE (%) 23.5 20.7 17.5 19.3 19.7

ROA (%) 1.3 1.2 1.0 1.1 1.1

Source: Company, Karvy Institutional Research

21

January 16, 2013

Bank Of Baroda

Exhibit 1: Income Statement

Y/E Mar (Rs. mn) FY11 FY12 FY13E FY14E FY15E

Interest Income 218,859 296,737 358,873 412,454 468,789

Interest expense 130,837 193,567 239,612 268,093 298,374

Net interest income 88,022 103,170 119,262 144,362 170,415

Fees 10,206 12,261 13,487 16,185 19,421

Other Income 13,451 15,888 18,830 20,048 22,180

Net Revenue 111,679 131,319 151,579 180,594 212,016

Operating Expense 46,298 51,587 54,767 65,246 77,963

‐Employee Exp 29,168 29,856 30,863 35,365 40,613

‐Other Exp 17,130 21,731 23,904 29,880 37,350

Operating Profit 65,381 79,732 96,812 115,349 134,053

Investment Profit 4,435 6,075 3,249 6,840 8,364

Pre‐provision Profit 69,816 85,807 100,061 122,189 142,417

Provisions 13,313 25,549 31,814 34,624 36,620

‐Loan Loss Provisions 12,640 20,171 28,462 33,418 35,564

‐Investment Depreciation 90 2,363 ‐567 ‐753 ‐904

‐Other Provisions 583 3,015 3,920 1,960 1,960

PBT 56,503 60,258 68,246 87,564 105,797

Taxes 14,086 10,188 17,062 22,767 27,507

PAT 42,417 50,070 51,185 64,798 78,290

Source: Company, Karvy Institutional Research

Exhibit 2: Balance Sheet

Y/E Mar (Rs. mn) FY11 FY12 FY13E FY14E FY15E

Equity Capital 3,928 4,124 4,124 4,124 4,124

Reserves & Surplus 206,003 270,645 305,157 359,354 425,602

Shareholderʹs Funds 209,931 274,769 309,281 363,478 429,726

Deposits 3,054,395 3,848,711 4,618,453 5,542,144 6,650,573

‐Current deposits 231,347 289,444 366,418 458,787 569,630

‐Saving deposits 644,540 745,795 861,256 1,045,994 1,267,680

‐Term deposit 2,178,508 2,813,472 3,390,779 4,037,362 4,813,262

Borrowings 223,079 235,730 289,612 354,270 431,860

‐Sub ordinate debt 107,487 109,280 125,445 144,842 168,119

Other liabilities 96,567 114,005 125,895 117,274 104,193

Total liabilities 3,583,972 4,473,215 5,343,240 6,377,166 7,616,351

Cash/Equivalent 499,341 641,686 729,744 826,732 943,117

Advances 2,286,764 2,873,773 3,451,080 4,143,848 4,975,169

Investments 712,606 832,094 1,024,530 1,255,452 1,532,559

Fixed Assets 22,997 23,415 25,415 27,415 29,415

Other assets 62,264 102,247 112,472 123,719 136,091

Total assets 3,583,972 4,473,215 5,343,240 6,377,166 7,616,351

Source: Company, Karvy Institutional Research

22

January 16, 2013

Bank Of Baroda

Exhibit 3: Ratios

FY11 FY12 FY13E FY14E FY15E

Growth(%)

NII growth 48.2 17.2 15.6 21.0 18.0

Pre‐provision profit growth 41.5 22.9 16.6 22.1 16.6

PAT growth 38.7 18.0 2.2 26.6 20.8

Business (%)

Deposit growth 26.7 26.0 20.0 20.0 20.0

Advance growth 30.6 25.7 20.1 20.1 20.1

Business growth 28.4 25.9 20.0 20.0 20.0

CD 74.9 74.7 74.7 74.8 74.8

CASA 28.7 26.9 26.6 27.2 27.6

Operating efficiency (%)

Cost‐to‐income 41.5 39.3 36.1 36.1 36.8

Cost‐to‐assets 1.6 1.4 1.2 1.2 1.2

Productivity (Rs mn)

Business per branch 1562.7 1698.0 1851.2 2035.3 2253.5

Business per employee 135.6 159.4 177.2 202.5 231.5

Profit per branch 12.4 12.6 11.7 13.6 15.2

Profit per employee 1.1 1.2 1.1 1.4 1.6

Spreads (%)

Yield on advances 8.0 8.7 8.7 8.2 7.7

Yield on investments 7.2 8.0 7.5 7.5 7.2

Cost of deposits 4.3 5.1 5.3 4.9 4.5

Yield on assets 7.4 8.0 7.9 7.6 7.2

Cost of funds 4.4 5.1 5.2 4.9 4.5

NIMs 3.0 2.8 2.6 2.6 2.6

Capital adequacy (%)

Tier I 10.0 10.8 8.3 8.1 8.1

Tier II 4.5 3.8 3.0 2.9 2.8

Total CAR 14.5 14.7 11.3 11.1 10.9

Asset Quality (%)

Gross NPA 1.4 1.5 2.1 2.2 2.2

Net NPA 0.3 0.5 0.8 0.7 0.6

Provision coverage 74.9 65.4 61.0 67.5 71.6

Provision coverage (incl w/off) 85.0 80.1 74.5 78.1 80.4

Slippage 0.9 1.3 1.6 1.3 1.2

Credit‐cost 0.5 0.6 0.9 0.8 0.7

Return (%)

ROE 23.5 20.7 17.5 19.3 19.7

ROA 1.3 1.2 1.0 1.1 1.1

Per share (Rs)

EPS 108.0 121.4 124.1 157.1 189.8

BV 534.4 666.3 750.0 881.4 1042.0

ABV 536.0 649.5 701.9 829.6 984.9

Valuation (x)

P/E 8.1 7.2 7.1 5.6 4.6

P/BV 1.6 1.3 1.2 1.0 0.8

P/ABV 1.6 1.3 1.2 1.1 0.9

Source: Company, Karvy Institutional Research

Banking January 16, 2013

Bank of India

Bloomberg: BOI INReuters: BOI.BO BUY

Institutional Equities

India Research

COMPANY UPDATE

Recommendation

CMP: Rs385

Target Price: Rs465

Upside (%) 21%

Stock Information Market Cap. (Rs bn / US$ mn) 221/4,044

52‐week High/Low (Rs) 408/253

3m ADV (Rs mn /US$ mn) 318/5.8

Beta 1.1

Sensex/ Nifty 19,987/6,057

Share outstanding (mn) 574

Stock Performance (%) 1M 3M 12M YTD

Absolute 24.2 26.9 27.6 12.2

Rel. to Sensex 20.0 18.8 3.1 9.1

Performance

Source: Bloomberg

1 Year Forward P/ABV

Source: Karvy Institutional Research

Analysts Contact

Hatim Broachwala, CFA

022‐6184 4329

Paresh Jain

022 6184 4324

250

300

350

400

450

15,500

17,500

19,500

21,500

Jan‐12

Feb‐12

Apr‐12

May‐12

Jun‐12

Aug‐12

Sep‐12

Oct‐12

Dec‐12

Jan‐13

Sensex (LHS) Bank of India (RHS)

‐

0.50

1.00

1.50

2.00

2.50

Feb‐07

Aug‐07

Feb‐08

Aug‐08

Feb‐09

Aug‐09

Feb‐10

Aug‐10

Feb‐11

Aug‐11

Feb‐12

Aug‐12

P/AdjBVPS Mean

+1 SD ‐1 SD

(x)

Pressure on Asset Quality to Ease, NIMs Set

to Improve; Maintain BUY

Bank of India (BoI) is currently trading at 20% discount to its five year

average valuation. Stock has underperformed the Bankex by 13% over last

one year reflecting pressure on asset quality. However, with the expected

improvement in macro conditions, such huge discount to its peers and to its

own average valuation seems to be unjustified.

Pressure on Asset Quality to Ease: After witnessing improving trend in

H2FY12, Bank of India’s asset quality has shown stress in H1FY13. As per

our recent interaction with BoI’s Management coupled with expected

improvement in economy and likely cut in interest rates, we believe that the

pressure on asset quality would ease from now onwards. Unlike its peers,

Bank of India has relatively lesser exposure to relatively vulnerable sectors

i.e. infrastructure, metals, mining and textiles etc.

NIMs – Set to Improve: Bank of India’s NIMs suffered by over 50 bps over

last three years. We expect the Bank’s NIMs to improve from now onwards

backed by lower proportion of high cost deposits, stable CASA and interest

recognized on recovered NPAs.

RoE Expansion – To Drive Valuation: Bank of India’s average RoE for

FY10‐12 has declined to 14.2% as against 23.3% for FY07‐09 on account of

compression in NIMs and rise in credit cost. We expect the Bank’s RoE

would improve to 18.2%, would lead to improvement in valuations.

Outlook & Valuation

At the CMP, the stock trades at 4.8x & 4.2x FY13E & FY14E earnings, and at

1.0x & 0.8x P/ABV FY14E & FY15E, respectively. Based on 20% discount to

its historical mean valuation implying 1.0x P/ABV FY15E, we reiterate our

“BUY” recommendation on Bank of India with upwardly revised target

price of Rs. 465 per share (from Rs. 395 earlier).

Key Financials

Y/E Mar (Rs. mn) FY11 FY12 FY13E FY14E FY15E

Net interest income 78,107 83,135 94,553 109,975 128,043

Operating Profit 50,624 62,852 74,516 83,184 95,033

PAT 24,887 26,775 32,790 46,528 52,933

EPS (Rs) 45.5 46.6 57.1 81.0 92.1

ABV (Rs) 290.4 310.7 330.4 394.9 463.0

P/E (x) 8.5 8.3 6.8 4.8 4.2

P/ABV (x) 1.3 1.2 1.1 1.0 0.8

Gross NPA (%) 2.2 2.3 3.2 2.9 2.8

Net NPA (%) 0.9 1.5 1.8 1.6 1.4

ROE (%) 15.8 14.0 14.7 18.2 17.9

ROA (%) 0.8 0.7 0.8 1.0 0.9

Source: Company, Karvy Institutional Research

24

January 16, 2013

Bank of India

Exhibit 1: Income Statement

Y/E Mar (Rs. mn) FY11 FY12 FY13E FY14E FY15E

Interest Income 217,517 284,807 323,871 360,924 401,582

Interest expense 139,410 201,672 229,318 250,949 273,539

Net interest income 78,107 83,135 94,553 109,975 128,043

Fees 11,811 12,715 12,715 15,258 18,310

Other Income 11,389 16,409 20,147 20,644 23,266

Net Revenue 101,307 112,259 127,414 145,877 169,618

Operating Expense 50,683 49,407 52,898 62,692 74,586

‐Employee Exp 34,754 30,534 30,251 34,383 39,199

‐Other Exp 15,929 18,873 22,648 28,310 35,387

Operating Profit 50,624 62,852 74,516 83,184 95,033

Investment Profit 3,218 4,088 3,708 6,337 7,244

Pre‐provision Profit 53,842 66,940 78,224 89,521 102,276

Provisions 18,888 31,165 35,079 26,645 30,745

‐Loan Loss Provisions 12,039 23,036 34,501 24,619 28,880

‐Investment Depreciation 1,369 4,369 ‐1,422 26 ‐135

‐Other Provisions 5,480 3,760 2,000 2,000 2,000

PBT 34,954 35,775 43,145 62,876 71,531

Taxes 10,067 9,000 10,355 16,348 18,598

PAT 24,887 26,775 32,790 46,528 52,933

Source: Company, Karvy Institutional Research

Exhibit 2: Balance Sheet

Y/E Mar (Rs. mn) FY11 FY12 FY13E FY14E FY15E

Equity Capital 5,472 5,745 5,745 5,745 5,745

Reserves & Surplus 167,435 203,873 230,150 268,885 312,090

Shareholderʹs Funds 172,907 209,618 235,895 274,630 317,835

Deposits 2,988,858 3,182,160 3,723,127 4,356,059 5,096,589

‐Current deposits 168,708 179,609 233,706 296,999 371,052

‐Saving deposits 590,968 668,446 749,591 876,177 1,024,283

‐Term deposit 2,229,182 2,334,105 2,739,830 3,182,883 3,701,254

Borrowings 220,214 321,142 388,019 434,618 489,139

‐Sub ordinate debt 91,598 93,655 120,406 139,045 160,854

Other liabilities 129,747 132,434 146,671 154,195 163,890

Total liabilities 3,511,726 3,845,354 4,493,712 5,219,502 6,067,453

Cash/Equivalent 373,101 347,112 430,218 495,805 572,542

Advances 2,130,962 2,488,333 2,921,107 3,427,452 4,019,876

Investments 858,724 867,536 986,549 1,125,794 1,288,710

Fixed Assets 24,807 27,716 29,716 31,716 33,716

Other assets 124,132 114,657 126,123 138,735 152,608

Total assets 3,511,726 3,845,354 4,493,712 5,219,502 6,067,453

Source: Company, Karvy Institutional Research

25

January 16, 2013

Bank of India

Exhibit 3: Ratios

FY11 FY12 FY13E FY14E FY15E

Growth (%)

NII growth 35.7 6.4 13.7 16.3 16.4

Pre‐provision profit growth 14.4 24.3 16.9 14.4 14.2

PAT growth 42.9 7.6 22.5 41.9 13.8

Business (%)

Deposit growth 30.1 6.5 17.0 17.0 17.0

Advance growth 26.5 16.8 17.4 17.3 17.3

Business growth 28.6 10.8 17.2 17.1 17.1

CD 71.3 78.2 78.5 78.7 78.9

CASA 25.4 26.7 26.4 26.9 27.4

Operating efficiency (%)

Cost‐to‐income 50.0 44.0 41.5 43.0 44.0

Cost‐to‐assets 1.8 1.5 1.4 1.4 1.4

Productivity (Rs mn)

Business per branch 1454.9 1400.5 1493.4 1605.2 1736.8

Business per employee 128.7 127.6 146.6 163.6 182.4

Profit per branch 7.1 6.6 7.4 9.6 10.1

Profit per employee 0.6 0.6 0.7 1.0 1.1

Spreads (%)

Yield on advances 8.1 8.8 8.8 8.3 7.9

Yield on investments 6.8 8.3 7.8 7.8 7.5

Cost of deposits 4.6 5.8 5.8 5.4 5.0

Yield on assets 7.7 8.5 8.4 8.0 7.7

Cost of funds 4.7 5.8 5.8 5.5 5.1

NIMs 2.8 2.5 2.5 2.5 2.5

Capital adequacy (%)

Tier I 8.3 8.6 8.4 8.5 8.4

Tier II 3.8 3.4 3.8 3.8 3.7

Total CAR 12.2 12.0 12.2 12.2 12.2

Asset Quality (%)

Gross NPA 2.2 2.3 3.2 2.9 2.8

Net NPA 0.9 1.5 1.8 1.6 1.4

Provision coverage 59.6 38.0 45.4 47.4 49.7

Provision coverage (incl w/off) 72.2 64.2 63.8 66.1 67.7

Slippage 1.5 2.3 2.8 1.8 1.8

Credit‐cost 0.6 0.9 1.2 0.7 0.7

Return (%)

ROE 15.8 14.0 14.7 18.2 17.9

ROA 0.8 0.7 0.8 1.0 0.9

Per share (Rs)

EPS 45.5 46.6 57.1 81.0 92.1

BV 316.0 364.9 410.6 478.0 553.2

ABV 290.4 310.7 330.4 394.9 463.0

Valuation (x)

P/E 8.5 8.3 6.8 4.8 4.2

P/BV 1.2 1.1 0.9 0.8 0.7

P/ABV 1.3 1.2 1.2 1.0 0.8

Source: Company, Karvy Institutional Research

Banking January 16, 2013

Canara Bank

Bloomberg: CBK INReuters: CBK.BO HOLD

Institutional Equities

India Research

COMPANY UPDATE

Recommendation

CMP: Rs523

Target Price: Rs570

Upside (%) 9%

Stock Information Market Cap. (Rs bn / US$ mn) 232/4,243

52‐week High/Low (Rs) 566/306

3m ADV (Rs mn /US$ mn) 417/7.6

Beta 1.1

Sensex/ Nifty 19,987/6,057

Share outstanding (mn) 443

Stock Performance (%) 1M 3M 12M YTD

Absolute 13.0 21.4 28.2 5.3

Rel. to Sensex 9.2 13.7 3.6 2.3

Performance

Source: Bloomberg

1 Year Forward P/ABV

Source: Karvy Institutional Research

Analysts Contact

Paresh Jain

022 6184 4324

Hatim Broachwala, CFA

022‐6184 4329

300350400450500550600

15,500

17,500

19,500

21,500

Jan‐12

Feb‐12

Apr‐12

May‐12

Jun‐12

Aug‐12

Sep‐12

Oct‐12

Dec‐12

Jan‐13

Sensex (LHS) Canara Bank (RHS)

0.0

1.0

2.0

Apr‐07

Aug‐07

Dec‐07

Apr‐08

Aug‐08

Dec‐08

Apr‐09

Aug‐09

Dec‐09

Apr‐10

Aug‐10

Dec‐10

Apr‐11

Aug‐11

Dec‐11

Apr‐12

Aug‐12

Dec‐12

1yr fwd P/Adj BV Mean + Std Dev

Mean ‐ Std Dev Mean

(x)

Business Growth to Gain Momentum,

Pressure on Asset Quality to Ease; Upgrade to

HOLD

Canara Bank is currently trading at 8% discount to mean valuation, while the

stock has underperformed the Bankex by 19% over last one year reflecting

weak balance sheet growth and concerns over asset quality.

Business Growth to Gain Momentum from H2FY13: Canara Bank’s

business growth has been under severe pressure since FY12. The Bank’s

credit has slowed down with 600 bps growth below system. Its C‐D ratio also

has declined by 700 bps since FY12. We expect business growth to gain

momentum from H2FY13 onwards on the back of lower base. However, the

overall growth in Bank’s loan book will remain muted for FY13 at 11%.

NIMs – Set to Improve The Bank’s NIM in H1FY13 declined by 15bps as

against FY12, partially owing to increase in cost of funds and decline in C‐D

ratio. We expect the Bank’s margin would improve in H2FY13 driven by rise

in CD ratio and reduction in cost of deposits.

Pressure on Asset Quality – Expected to Ease: Canara Bank’s NPAs have

shown deterioration in H1FY12. Though the Bank’s slippage ratio has

increased to 3% in H1FY13, its asset quality remains better than some of its

peers. The Bank’s restructured loan book stood at 7.9% of advances, and we

expect its asset quality to improve from now onwards.

Outlook & Valuation

At the CMP, the stock trades at 5.5x & 4.7x FY14E & FY15E earnings, and at

1.0x & 0.8x P/ABV FY14E & FY15E, respectively. Based on 20% discount to its

historical mean valuation implying 0.9x P/ABV FY15E, we have upgraded

our recommendation on Canara Bank to “HOLD” from “SELL” with

upwardly revised target price of Rs. 570 per share (from Rs. 410 earlier).

Key Financials

Y/E Mar (Rs. mn) FY11 FY12 FY13E FY14E FY15E

Net Interest Income 78,233 76,893 78,929 97,872 119,857

Operating profit 58,707 56,195 52,549 67,284 83,122

PAT 40,259 32,827 32,309 41,965 48,959

EPS (Rs) 97.8 74.1 72.9 94.7 110.5

ABV (Rs) 369.7 414.6 458.1 535.3 627.5

P/E (x) 5.3 7.1 7.2 5.5 4.7

P/ABV (x) 1.4 1.3 1.1 1.0 0.8

Gross NPA (%) 1.5 1.7 2.2 2.0 2.0

Net NPA (%) 1.1 1.5 1.7 1.5 1.3

ROE (%) 26.4 17.0 14.7 16.8 16.9

ROA (%) 1.3 0.9 0.8 0.9 0.9

Source: Company, Karvy Institutional Research

27

January 16, 2013

Canara Bank

Exhibit 1: Income Statement

Y/E Mar (Rs. mn) FY11 FY12 FY13E FY14E FY15E

Interest Income 230,640 308,506 337,663 361,605 413,674

Interest expense 152,407 231,613 258,734 263,733 293,818

Net interest income 78,233 76,893 78,929 97,872 119,857

Fees 7,558 7,969 8,350 9,345 11,111

Other Income 19,472 21,307 20,995 25,464 29,069

Net Revenue 105,263 106,169 108,274 132,681 160,037

Operating Expense 44,193 46,737 51,726 60,547 71,125

‐Employee Exp 29,548 29,731 32,231 37,677 44,195

‐Other Exp 14,645 17,007 19,495 22,870 26,930

Operating Profit 58,707 56,195 52,549 67,284 83,122

Investment Profit 2,363 3,237 4,000 4,850 5,790

Pre‐Provision Profits 61,070 59,432 56,549 72,134 88,912

Provisions 10,811 18,605 16,240 19,669 26,453

‐Loan Loss Provisions 10,012 12,941 16,850 16,824 21,484

‐Investment Depreciation 426 1,539 (3,500) (800) 1,124

‐Other Provisions 373 4,125 2,890 3,645 3,845

PBT 50,259 40,827 40,309 52,465 62,459

Taxes 10,000 8,000 8,000 10,500 13,500

PAT 40,259 32,827 32,309 41,965 48,959

Source: Company, Karvy Institutional Research

Exhibit 2: Balance Sheet

Y/E Mar (Rs. mn) FY11 FY12 FY13E FY14E FY15E

Equity Capital 4,430 4,430 4,430 4,430 4,430

Reserves & Surplus 195,968 222,470 248,548 283,763 324,934

Shareholderʹs Funds 200,398 226,900 252,978 288,193 329,364

Deposits 2,934,366 3,270,537 3,675,414 4,317,970 5,171,970

Current deposits 245,000 148,185 170,455 203,011 267,315

Saving deposits 586,171 647,922 752,534 922,534 1,122,534

Term deposit 2,108,555 2,474,430 2,752,426 3,192,426 3,782,122

Borrowings 142,616 155,254 179,445 206,172 247,172

‐Sub ordinate debt 43,540 41,040 45,444 47,554 49,554

Other liabilities 82,068 88,911 131,739 198,570 266,907

Total liabilities 3,359,449 3,741,602 4,239,576 5,010,905 6,015,413

Cash/Equivalent 307,081 281,794 352,290 429,509 515,019

Advances 2,112,683 2,324,898 2,559,188 3,010,189 3,609,188

Investments 836,360 1,020,574 1,204,910 1,434,910 1,734,910

Fixed Assets 28,444 28,575 30,454 34,545 38,545

Other assets 74,880 85,760 92,734 101,752 117,752

Total assets 3,359,449 3,741,602 4,239,576 5,010,905 6,015,413

Source: Company, Karvy Institutional Research

28

January 16, 2013

Canara Bank

Exhibit 3: Ratios

FY11 FY12 FY13E FY14E FY15E

Growth (%)

NII growth 37.7 (1.7) 2.6 24.0 22.5

Pre‐provision profit growth 20.7 (2.7) (4.9) 27.6 23.3

PAT growth 33.2 (18.5) (1.6) 29.9 16.7

Business (%)

Deposit growth 25.1 11.5 12.4 17.5 19.8

Advance growth 24.8 10.0 10.1 17.6 19.9

Business growth 24.9 10.9 11.4 17.5 19.8

CD 72.0 71.1 69.6 69.7 69.8

CASA 28.1 24.3 25.1 26.1 26.9

Operating efficiency (%)

Cost‐to‐income 42.0 44.0 47.8 45.6 44.4

Cost‐to‐assets 1.5 1.3 1.3 1.3 1.3

Productivity (Rs mn)

Business per branch 1,549.6 1,554.3 1,578.4 1,698.3 1,874.3

Business per employee 122.8 132.4 131.5 141.5 156.2

Profit per branch 12.4 9.1 8.2 9.7 10.5

Profit per employee 1.0 0.8 0.7 0.8 0.9

Spreads (%)

Yield on advances 9.0 10.6 10.3 9.4 8.9

Yield on investments 7.6 7.6 7.5 7.3 7.2

Cost of deposits 5.4 7.1 7.1 6.2 5.9

Yield on assets 7.9 9.0 8.7 8.0 7.7

Cost of funds 5.5 7.0 7.0 6.2 5.8

NIMs 2.7 2.2 2.0 2.2 2.2

Capital adequacy (%)

Tier I 10.9 10.4 9.8 9.5 9.1

Tier II 4.5 3.4 3.2 3.1 2.8

Total CAR 15.4 13.8 13.0 12.7 12.0

Asset Quality (%)

Gross NPA 1.5 1.7 2.2 2.0 2.0

Net NPA 1.1 1.5 1.7 1.5 1.3

Provision coverage 25.2 16.0 20.1 21.5 32.6

Provision coverage (incl w/off) 73.0 68.6 70.3 69.5 71.3

Slippage 1.8 2.1 2.3 1.7 1.7

Credit‐cost 0.5 0.6 0.7 0.6 0.6

Return (%)

ROE 26.4 17.0 14.7 16.8 16.9

ROA 1.3 0.9 0.8 0.9 0.9

Per share (Rs)

EPS 97.8 74.1 72.9 94.7 110.5

BV 405.0 465.6 525.1 605.3 700.5

ABV 369.7 414.6 458.1 535.3 627.5

Valuation (x)

P/E 5.3 7.1 7.2 5.5 4.7

P/BV 1.3 1.1 1.0 0.9 0.7

P/ABV 1.4 1.3 1.1 1.0 0.8

Source: Company, Karvy Institutional Research

Banking January 16, 2013

City Union Bank

Bloomberg: CUBK INReuters: CTBK.BO HOLD

Institutional Equities

India Research

COMPANY UPDATE

Recommendation

CMP: Rs61

Target Price: Rs65

Upside (%) 7%

Stock Information Market Cap. (Rs bn / US$ mn) 31/568

52‐week High/Low (Rs) 61/35

3m ADV (Rs mn /US$ mn) 57/1.1

Beta 0.8

Sensex/ Nifty 19,987/6,057

Share outstanding (mn) 512

Stock Performance (%) 1M 3M 12M YTD

Absolute 7.5 20.1 63.3 8.4

Rel. to Sensex 3.9 12.5 32.0 5.4

Performance

Source: Bloomberg

1 Year Forward P/ABV

Source: Karvy Institutional Research

Analysts Contact

Paresh Jain

022 6184 4324

Hatim Broachwala, CFA

022‐6184 4329

30

40

50

60

70

15,500

17,500

19,500

21,500

Jan‐12

Feb‐12

Apr‐12

May‐12

Jun‐12

Aug‐12

Sep‐12

Oct‐12

Dec‐12

Jan‐13

Sensex (LHS) City Union Bank (RHS)

0.0 0.5 1.0 1.5 2.0 2.5 3.0

Apr‐07

Aug‐07

Dec‐07

Apr‐08

Aug‐08

Dec‐08

Apr‐09

Aug‐09

Dec‐09

Apr‐10

Aug‐10

Dec‐10

Apr‐11

Aug‐11

Dec‐11

Apr‐12

Aug‐12

Dec‐12

1yr fwd P/Adj BV Mean + Std Dev

Mean ‐ Std Dev Mean

(x)

Positives Priced‐in; Maintain HOLD

City Union Bank (CUB) is currently trading at 35% premium to its five year

average valuation, while the stock has outperformed the Bankex by 19% over

last one year reflecting better than the industry growth, healthy NIM and

strong asset quality. The Bank has one of the best return ratios amongst its

peers.

Business Growth – Outperformance to Continue: City Union Bank’s

business growth has surpassed the industry by a significant margin, while

we expect such outperformance to continue, going ahead. The Bank does

majority of its lending to MSMEs, wholesale and retail traders, which is its

niche segment. The Bank’s overall lending book mainly constitutes of high‐

yielding working capital loans (60%) and rest of term loans (40%).

NIMs – Continue to Remain Healthy: City Union Bank has been able to

maintain its NIMs in excess of 3.2% in H1FY13. Though the Bank expects

marginal reduction in yield on advance, it would get offset by reduction in

cost of deposits. We expect the Bank to continue to maintain its NIM ~ 3.2%

in H2FY13.

Asset Quality – to Remain under Control: City Union Bank’s asset quality

continued to show resilience in a deteriorating economic environment.

However, we believe that it would be difficult for the Bank to report further

improvement in its asset quality. Thus, considering marginally higher

slippage ratio, we expect the Bank’s NPA ratio would increase marginally in

FY13. Meanwhile, the Bank has maintained its restructured loan book at 3.2%

which is lesser than peers.

Outlook & Valuation

At CMP, the stock trades at 7.4x & 5.9x FY14E & FY15E earnings, and at 1.6x

& 1.3x P/ABV FY14E & FY15E, respectively. Based on 20% premium to its

mean valuation implying 1.45x P/ABV FY15E, we reiterate our “HOLD”

recommendation on City Union Bank with unrevised target price of Rs. 65

per share.

Key Financials

Y/E Mar (Rs. mn) FY11 FY12 FY13E FY14E FY15E

Net Interest Income 4,200 4,998 6,141 7,724 9,899

Operating profit 3,544 4,193 4,959 6,232 7,737

PAT 2,151 2,803 3,509 4,421 5,489

EPS (Rs) 5.4 6.9 6.5 8.2 10.2

ABV (Rs) 24.0 29.5 31.7 37.7 45.5

P/E (x) 11.3 8.8 9.3 7.4 5.9

P/ABV (x) 2.5 2.1 1.9 1.6 1.3

Gross NPA (%) 1.2 1.0 1.3 1.7 1.7

Net NPA (%) 0.5 0.4 0.6 0.7 0.6

ROE (%) 23.5 24.9 23.2 22.6 23.4

ROA (%) 1.6 1.7 1.7 1.7 1.7

Source: Company, Karvy Institutional Research

30

January 16, 2013

City Union Bank

Exhibit 1: Income Statement

Y/E Mar (Rs. mn) FY11 FY12 FY13E FY14E FY15E

Interest Income 12,184 16,968 21,773 25,701 32,131

Interest expense 7,984 11,970 15,632 17,977 22,232

Net interest income 4,200 4,998 6,141 7,724 9,899

Fees 303 345 470 589 722

Other Income 1,271 1,726 2,140 2,657 2,997

Net Revenue 5,774 7,069 8,751 10,970 13,618

Operating Expense 2,164 2,798 3,497 4,336 5,369

‐Employee Exp 1,016 1,223 1,431 1,746 2,130

‐Other Exp 1,148 1,575 2,066 2,590 3,239

Operating Profit 3,544 4,193 4,959 6,232 7,737

Investment Profit 66 78 295 402 512

Pre‐Provision Profits 3,610 4,271 5,254 6,634 8,249

Provisions 790 838 841 1,108 1,388

‐Loan Loss Provisions 673 570 662 960 1,097

‐Investment Depreciation 76 74 (16) (100) 84

‐Other Provisions 41 194 195 248 207

PBT 2,821 3,433 4,413 5,526 6,861

Taxes 670 630 905 1,105 1,372

PAT 2,151 2,803 3,509 4,421 5,489

Source: Company, Karvy Institutional Research

Exhibit 2: Balance Sheet

Y/E Mar (Rs mn) FY11 FY12 FY13E FY14E FY15E

Equity Capital 405 408 539 539 539

Reserves & Surplus 9,661 12,023 17,225 20,764 25,117

Shareholderʹs Funds 10,066 12,431 17,764 21,303 25,656

Deposits 129,143 163,408 203,808 258,130 326,012

‐Current deposits 10,876 12,031 14,678 18,935 24,047

‐Saving deposits 14,407 17,685 22,283 28,967 37,078

‐Term deposit 103,859 133,692 166,847 210,227 264,886

Borrowings 1,862 3,487 5,030 6,400 7,600

‐Sub ordinate debt 400 400 850 1,100 1,100

Other liabilities 4,845 4,181 5,507 6,306 7,619

Total liabilities 145,915 183,507 232,109 292,138 366,887

Cash/Equivalent 12,863 11,361 13,125 15,578 18,378

Advances 92,555 121,375 155,578 200,696 256,890

Investments 36,162 45,862 57,250 69,253 84,224

Fixed Assets 685 977 1,045 1,245 1,545

Other assets 3,650 3,932 5,111 5,367 5,850

Total assets 145,915 183,507 232,109 292,138 366,887

Source: Company, Karvy Institutional Research

31

January 16, 2013

City Union Bank

Exhibit 3: Ratios

FY11 FY12 FY13E FY14E FY15E

Growth (%)

NII growth 51.0 19.0 22.9 25.8 28.2

Pre‐provision profit growth 41.1 18.3 23.0 26.3 24.3

PAT growth 40.7 30.3 25.2 26.0 24.2

Business (%)

Deposit growth 25.6 26.5 24.7 26.7 26.3

Advance growth 35.4 31.1 28.2 29.0 28.0

Business growth 29.5 28.5 26.2 27.7 27.0

CD 71.7 74.3 76.3 77.7 78.8

CASA 19.6 18.2 18.1 18.6 18.7

Operating efficiency (%)

Cost‐to‐income 37.5 39.6 40.0 39.5 39.4

Cost‐to‐assets 1.7 1.7 1.7 1.7 1.6

Productivity (Rs mn)

Business per branch 901.2 949.3 1012.4 1092.4 1214.4