Embed Size (px)

Citation preview

KIPF

The contemporary needs of general and earmarked grants in Korea:

Assessment

Hyun-A Kim

Korea Institute of Public Finance

2009 Copenhagen Seminar, Sept. 17-18

KIPF

Political decentralization

• Fiscal decentralization began again in 1991 with the appointment of council members, and established in1995 by the election of local representatives in Korea

• Hypothetically, in an electoral process, people articulate their demands by their voting preference

• Local representatives has to obtain voters’ preference

• Some empirical results : the relationship between election and fiscal expansion

Introduction

2009 Copenhagen Seminar, Sept. 17-18

KIPF

Fiscal decentralization…

• Given the political, global and fiscal trends as well as other hosts of reason, local government’s role has to be expanded alongside the increase of its fiscal size.

• Intergovernmental fiscal transfers has steadily grown

• However, fiscal power of local governments has not symmetrically grown.

Introduction

2009 Copenhagen Seminar, Sept. 17-18

The budget size and expenditure share of general

government

KIPFIncreasing local expenditure by using grants

2009 Copenhagen Seminar, Sept. 17-18

13.60% 13.90% 14.20% 13.40% 14.10% 14.60%

35.90% 37.70% 38.60% 40.50% 43.60% 45.10%

50.50% 48.40% 47.20% 46.10% 42.30% 40.30%

0%

20%

40%

60%

80%

100%

120%

2003 2004 2005 2006 2007 2008

0

50

100

150

200

250

300

Education Local Central Total expenditure

Transfer to total government expenditure in 2005

KIPFIncreasing local expenditure by using grants

2009 Copenhagen Seminar, Sept. 17-18

Source: OECD (2009)Source: OECD (2009)

Limited local tax share and low taxing power

• While the majority of expenditure are done at the local level, only very limited autonomy is available in local spending decisions.

• Local politicians tend to avoid increasing tax rate

• Flexible tax rate is not activated…

• This tendency exacerbate soft budget problem and lower taxing power.

KIPFLimited local tax share and taxing power

2009 Copenhagen Seminar, Sept.17-18

The steady share of local tax

KIPFLimited local tax share and taxing power

2009 Copenhagen Seminar, Sept.17-18

29 32 34 35 38 44

114 122 131 135147

166

20.7%20.8% 20.8 %

20.5%20.5%20.2%

2003 2004 2005 2006 2007 2008

National

Local

Rotio to the National

Revenue assignment

• Local revenue is composed of own source revenue such as local tax(33%), non tax revenue (29.7%), local bonds (2.7%)

• Intergovernmental fiscal transfer such as revenue sharing (LST, 20.9%) and National subsidy (13.8%) in 2007

• Without non-tax revenue, the share of local taxes is around 50%. General and earmarked grants are 29.5% and 19.6% respectively

KIPFLimited local tax share and taxing power

2009 Copenhagen Seminar, Sept.17-18

Revenue composition of local governments

KIPFAn overview of intergovernmental fiscal transfer

2009 Copenhagen Seminar, Sept.17-18

0

10

20

30

40

50

60

70

80

90

100

110

120

130

1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007

Own source revenue

Earmarked Grant

General Grant

Expenditure

Types of grants in Korea

KIPFAn overview of intergovernmental fiscal transfer

2009 Copenhagen Seminar, Sept.17-18

Grants

Non-Earmarked

Mandatory General grants (LST, DRS 2010)

Earmarked

Mandatory(SABND, LTF)

Discretionary(NTS)

Matching

Non-matching

Matching

Non-matching

Local taxes and grants share

KIPFSteady increase in local tax

2009 Copenhagen Seminar, Sept.17-18

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007

Earmarked General TAX

Local Shared Tax

• Major fiscal equalization system by revenue sharing a fixed percentage (19.24%) of Domestic National Tax

• The objective of ordinary LST is to equalize the fiscal capacities of local governments

• Notably, dependence of LST to local revenue has increased significantly from 15.0% in 2002 to 20.9% in 2007.

• 2.5% share of LST to GDP ( Japan 4%, Northern European countries 2-4% share…)

KIPFIntergovernmental fiscal transfers

2009 Copenhagen Seminar, Sept.17-18

Decentralization Revenue Sharing

• From the perspective of grant design, DRS is an example of changing funding system

• Mainly, funding source of social welfare programs has been changed from specific to general grants (0.94% of National Domestic Tax)

• Central local management and operation

• It is scheduled to return to LST in 2010

• It is easily expected that under-provision of welfare spending since money is fungible under the general grants

KIPFIntergovernmental fiscal transfers

2009 Copenhagen Seminar, Sept.17-18

Decentralization Revenue Sharing

• DRS programs are from NTS projects such as mainly social welfare related expenditure.

• The rationale of the implementation of DRS was the devolution of welfare provision from central and local governments

• Under the lower fiscal capacity and political incentive, the reduction of social service budget will happen

• Now, it is evaluated that DRS failed to be operated in its real sense

KIPFIntergovernmental fiscal transfers

2009 Copenhagen Seminar, Sept.17-18

Local transfer fund

KIPFIntergovernmental fiscal transfers

2009 Copenhagen Seminar, Sept.17-18

• Local transfer fund was introduced in 1991 as a conditional block grant

• Contribution : around 70% of the LTF is to be used for local road maintenance.

• Tax-sharing: the fund was transferred directly to local govts without first being accounted for in the central budget.

• Qualitatively, it was almost same with the NTS

• This was abolished in 2005 LST

• Earmarked General way

National treasury subsidy

• National treasury subsidies are categorical grants provided by the central government to local governments for specific projects

• Social welfare and the increase of fiscal needs after local autonomy are the reasons of expanding NTS from 1995 to 2002 The reform of NTS in 2005

• Finally, reliance on earmarked grants has been reduced from 22% in 2002 to 13.8% in 2007.

KIPFIntergovernmental fiscal transfers

2009 Copenhagen Seminar, Sept.17-18

Special Account of Balanced National Grants

• Implementation of new formula to distribute for provincial bases : NTS earmarked block grant

• The discretionary power of the line ministries had been reduced because nearly half of the SABND grants are formula based

• Fiscal flexibility in local government

• However, the three-year implementation evaluation did not manifest local efforts to promote high quality of public delivery

KIPFIntergovernmental fiscal transfers

2009 Copenhagen Seminar, Sept.17-18

Political needs : Tax-sharing or general grants?

• With a long debate, new ‘tax-sharing’ way of revenue increasing in local govt. are determined by the Introduction of Local Consumption Tax and Local Income Tax

• For example, 20% of VATLCT

• Arguments : urban concentration of tax bases, qualitatively same with LST…..

• Despite of many problems, political meaning of LOCAL TAXES dominate rather than GRANTS….

KIPFIntergovernmental fiscal transfers

2009 Copenhagen Seminar, Sept.17-18

Reform of the specific grants:

Comparison of transfers

KIPFSystem change of intergovernmental fiscal transfers

from 2005Determination Method of

Financial ResourceDistribution Method

among Regions

LST, DRSConstant Portion of Domestic Tax Revenue

Formula Based

SABND• 100% of Liquor tax• Specific Transfer• Other Fees

Formula Based

NTS Determined Every Year at discretion

2009 Copenhagen Seminar, Sept.17-18

Contrasting figure after 2000

(among 16 regions)

KIPFIntergovernmental fiscal grants

2009 Copenhagen Seminar, Sept.17-18

General Grants

0%

1%

2%

3%

4%

5%

6%

7%

8%

1997 2000 2005

Capital area Non capital area

Earmarked Grants

0%

1%

2%

3%

4%

5%

6%

7%

8%

1997 2000 2005

Capital area Non capital area

Recent change turns to the way of general grants….

• NTS DRSLST , NTS SABND, LTFLST

• Tax sharing or general grants : The introduction of Local Consumption Tax and Local Income Tax

• ‘Federalist approach’ : simple lump-sum transfers with no conditionality would be desirable

• Korea is one the leading countries to expand general grants for fiscal federalism

• Easy money dependency is getting bigger

KIPFIntergovernmental fiscal transfers

2009 Copenhagen Seminar, Sept.17-18

Would this trend be desirable in Korea?

• This paper tends to focus more on the effectiveness of earmarked grants in Korea as a developing economy

• The reasons are following :

• 1) Korea is not a developed country, but in an immature stage in local autonomy

• 2) Soft budget relations between donor and recipient

3) Welfare expenditure needs rises

KIPFDiscussion

2009 Copenhagen Seminar, Sept.17-18

Soft-budget problem

• Intergovernmental risk sharing might be fundamental issue

• Soft budget relations between donor and recipient may exacerbate the effectiveness of grant purpose regardless of the choice of grants

• To smooth soft budget problem, tight linkage between marginal increase of revenue and their works should be done

• Now, local governments are not main providers of education, health, social services to be the ultimate fiscal charger, expenditure assignment should be rearranged

KIPFAn assessment

2009 Copenhagen Seminar, Sept. 17-18

Fundamental incentive effect in LST

• “Tax effort problem” : Intrinsically, local gvts have incentive to enlarge local needs while reduce local revenue

• The process of calculating the incentive revenue is not legally binding. The ambiguity leads local gvts. to believe that efforts to boost their tax revenue reduce the amount of the LST that they receive

• Accountability and responsibility of general grants?

KIPFAn assessment

2009 Copenhagen seminar, Sept. 17-18

Welfare expenditure rises…

• Fiscal needs Social welfare

• Intergovernmental welfare arrangement in function and money is the hottest issue

• Asymmetric information problem between central (revenue source) and sub-central (local information) governments is growing especially in welfare service program

• Under-provision of public good such as politically unattractive service (disabled supports, low income people…..) would happen

KIPFAn assessment

2009 Copenhagen Seminar, Sept.17-18

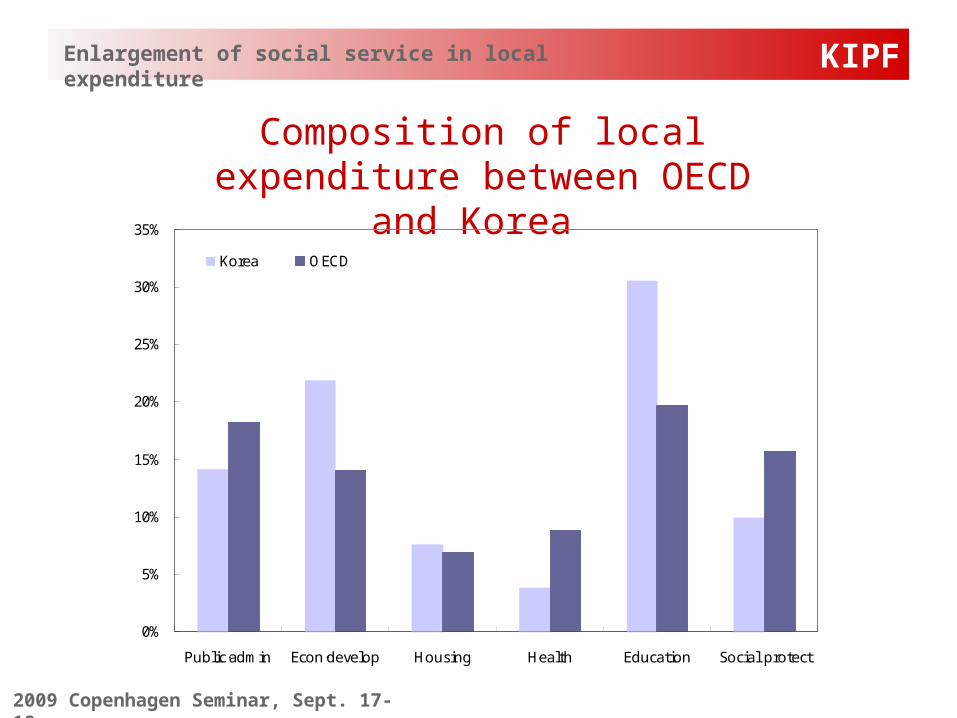

Composition of local expenditure between OECD and

Korea

KIPFEnlargement of social service in local expenditure

2009 Copenhagen Seminar, Sept. 17-18

0%

5%

10%

15%

20%

25%

30%

35%

Public·admin Econ·develop Housing Health Education Social protect

Korea OECD

Per capita social expenditure in Seoul

KIPFEnlargement of social service in local expenditure

2009 Copenhagen Seminar, Sept.17-18

0

15

30

45

60

75

90

1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007

Public Admin

Social Expenditure

Economic Expenditure

Findings and policy suggestion

• Own purpose of grants is established from 2000, especially in earmarked grants.

• Soft budget issue and the introduction of tax-sharing with the same source of money seem to impede the justification of the increase of general grants.

• My conclusion : with these observations, the function of earmarked grants in comparison with general grants might be more suggestive in Korea.

KIPFConclusion

2009 Copenhagen Seminar, Sept.17-18