Embed Size (px)

Citation preview

THE SIGNIFICANCE OF ADOPTING

THE ISLAMIC CALENDAR IN ISLAMIC

HOUSING FINANCE. CASE STUDY: BANK

MUAMALAT MALAYSIA BERHAD

PARIT RAJA BRANCH

KUNTHI HERMA DWIDAYATI

UNIVERSITI TUN HUSSEIN ONN MALAYSIA

This thesis has been examined on date 5 January 2016, and is sufficient in fulfilling the scope and quality for the purpose of awarding the Degree of Master of Real

Estate and Facilities Management

Chairperson:

Prof. Sr Dr. David Martin @ Daud Juanil

Faculty of Technology Management and Business Universiti Tun Hussein Onn Malaysia

External Examiners: Dr. Hawa bte Ahmad @ Abdul Mutalib

Department of Accunting International Islamic University Malaysia

Internal Examiner

Prof. Madya Sr Dr. Wan Zahari bin Wan Yusoff Faculty of Technology Management and Business Universiti Tun Hussein Onn Malaysia

THE SIGNIFICANCE OF ADOPTING THE ISLAMIC CALENDAR IN ISLAMIC HOUSING FINANCE.

CASE STUDY: BANK MUAMALAT MALAYSIA BERHAD

PARIT RAJA BRANCH

KUNTHI HERMA DWIDAYATI

A thesis submitted in fulfillment of the requirements for the award of the Degree of Master of Real Estate and Facilities Management

Faculty of Technology Management and Business

Universiti Tun Hussein Onn Malaysia

SEPTEMBER 2016

iii

DEDICATION

For my beloved late father and late mother

Susilo Hermanto & Suyati

My lovely sister, supervisor, and friends

Thank you for the encouragement, guidance and support for me

iv

ACKNOWLEDGEMENT

First of all, praise is due to the AlMighty Allah SWT for His compassion and

mercifulness for granting me in completing this thesis. I also would like to extend my

appreciation to my supervisor, Dr. Noralfishah Sulaiman for her support, patience,

time and guidance during my study. My sincerely thanks also due to Prof. Madya

Tono Saksono, who lets me experience researching the area of Real Estate Finance. I

would also like to thank Dr. Bana Handaga and Dr. Madi Hermadi, who always

around supporting me during my research process.

The cooperation given by Bank Muamalat Malaysia Berhad (UTHM) also

highly appreciated. Their contribution and participation in providing data and

interview are very important in my research. Appreciation also goes to all my friends

(Hamimatul Akmam, Shafiqah, Wong Lai Yoong, Wendy Wenxin, Woon Hei Ling,

Jouvan, Firda, Saiful, and Miftahuddin) and others who involved directly or

indirectly towards the completion of my thesis.

Special thanks is also dedicated to my beloved late mother, sister, brother in

law, and also my late father for their warm support, encouragement, and

understanding throughout my study. Last but not least my appreciation goes to my

late father who inspired me a lot to make my dreams come true.

v

ABSTRACT

Malaysia is considered to be one of the most advance developed Muslim

countries among Muslim countries that employ Islamic Banking system. In this

context, Islamic Housing Finance has grown rapidly and becomes popular as a

common solution for Muslims who desire to own home base on shariah principles.

In Malaysia, banks which have Islamic Banking products employ Gregorian

Calendar as the basis for their accounting system even though Surah At-Tawbah: 36-

37 in Al-Quran has clearly depicted that there is a straight guidance for Muslims to

use the Islamic Calendar for their mundane and spiritual lives. Factually, Gregorian

Calendar is 11.5 days longer than the Islamic Calendar, thus using it will affect the

calculation of loan repayment for every Muslim borrower. In previous research,

discovered that Gregorian Calendar has caused the shortage of zakat payments by the

Muslim customers, due to the shorter period of days calculated. This study was

conducted to determine a reliable Islamic Calendar according hisab criteria (wujudul

hilal) using Accurate Times. To identify the difference calculation between two

calendars system and to calculate Islamic Housing Finance repayment in Islamic

Calendar and Gregorian Calendar. Quantitative and Qualitative approach were

employed in this research. Respondents are all customers at the Bank Muamalat

Malaysia Berhad (Parit Raja) who chose Bai Bithamin Ajil (BBA) concept as their

housing finance scheme. The calculation shows that total repayment in Islamic

Calendar is lower than the Gregorian Calendar. Expert interview were used to

identify the effect of employing Islamic Calendar in Islamic Banking system

especially for Islamic Housing Finance. Finding indicates that the differences of total

repayment between two calendar system reach average 1.04 per cent and most of the

banks agree that Islamic Calendar can be employed as the basis of accounting system

although many challenges appeared.

vi

ABSTRAK

Malaysia dianggap sebagai salah satu negara muslim yang berkembang pesat

dikalangan negara-negara muslim yang lain dalam mengaplikasikan perbankan

Islam. Sehubungan itu, skim pembiayaan perumahan Islam turut berkembang pesat

dan menjadi penyelesaian popular untuk orang-orang muslim yang menginginkan

pemilikan rumah berdasarkan prinsip syariah. Di Malaysia, bank memiliki produk

perbankan Islam dan menggunakan kalendar Gregorian sebagai dasar sistem

perakaunan. Telah dijelaskan dalam Quran Surat At-Tawbah ayat 36-37 bahawa

Muslim diharuskan menggunakan kalendar Islam untuk kehidupan duniawi dan

spiritual. Kalendar Gregorian mempunyai 11.5 hari lebih panjang daripada kalendar

Islam, ini mempengaruhi perkiraan bayaran balik untuk setiap peminjam. Dalam

kajian sebelumnya, mendapati bahawa kalendar Gregorian telah menyebabkan

kekurangan pembayaran zakat oleh pelanggan muslim, kerana tempoh yang lebih

singkat. Kajian ini dijalankan untuk menentukan kebolehgunaan kalendar Islam

berdasarkan kriteria hisab (wujudul hilal) menggunakan perisian Accurate Times.

Untuk menentukan perbezaan perkiraan antara dua sistem kalendar dan pengiraan

skim pembiayaan perumahan dalam kalendar Islam dan kalendar Gregorian. Kajian

ini menggunakan pendekatan kuantitatif dan kualitatif. Responden adalah dari

pelanggan di Bank Muamalat Malaysia Berhad (Parit Raja) dan memilih Bai

Bithamin Ajil (BBA) sebagai skim pembiayaan perumahan mereka. Perkiraan

menunjukkan jumlah pembayaran dalam kalendar Islam lebih rendah berbanding

perkiraan dalam kalendar Gregorian. Temubual dengan pakar telah digunakan bagi

mengenal pasti kesan penggunaan kalendar Islam dalam perbankan Islam

terutamanya pembiayaan perumahan. Penemuan daripada hasil kajian menunjukan

perbezaan keseluruhan bayaran balik antara kalendar Islam dan Gregorian mencapai

1.04 peratus dan sebahagian besar penggunaan kalendar Islam sebagai asas pada

sistem perbankan Islam walaupun banyak cabaran dalam pelaksanaannya.

vii

CONTENTS

THESIS TITLE i

DECLARATION ii

DEDICATION iii

ACKNOWLEDGEMENTS iv

ABSTRACT v

ABSTRAK vi

CONTENTS vii

LIST OF TABLES xi

LIST OF FIGURES xiii

LIST OF ABBREVIATIONS xv

LIST OF APPENDICES xvii

CHAPTER 1 INTRODUCTION 1

1.0 Introduction 1

1.1 Problem Statement 3

1.2 Research Question 6

1.3 Research Aim 6

1.4 Research Objectives 6

1.5 Scope and Limitation of the Study 7

1.6 Significance of the Research 7

1.7 Organisation of the Thesis 8

CHAPTER 2 LITERATURE REVIEW 11

2.0 Introduction 11

2.1 Introduction to Islamic Finance (IF) 11

2.1.1 Definition of Islamic Finance 11

2.1.2 Prohibited Elements in Islamic Finance 14

2.1.3 Practice of Islamic Finance in Malaysia 15

viii

2.1.4 Governing Bodies for Islamic Finance in

Malaysia 18

2.1.5 The Framework of Islamic Finance in

Malaysia 21

2.1.6 Islamic Banking System in Malaysia 23

2.2 Islamic Housing Finance (IHF) in Malaysia 24

2.2.1 Definition of Islamic Housing Finance 25

2.2.2 Contracts in Islamic Housing Finance in

Malaysia 27

2.2.2.1 Bai Bithamin Ajil 29

2.2.2.2 Murabahah 30

2.2.2.3 Musharakah 31

2.2.2.4 Musharakah Mutanaqisah 31

2.2.2.5 Ijarah 33

2.2.2.6 Istishna 34

2.2.2.7 Tawarruq 34

2.2.3 Conventional Housing Finance (HF)

in Malaysia 35

2.2.3.1 Definition of Housing

Mortgage 35

2.2.3.2 Characteristic of Housing

Mortgage 36

2.2.3.3 Mortgage Products 37

2.2.4 Utility Theory in Housing Finance 40

2.3 Calendar Systems and Its Calculation 40

2.3.1 Definition of Calendar and It’s System 40

2.3.2 Function of Calendar 41

2.3.3 Types of Calendar 41

2.3.4 Gregorian Calendar (GC) 41

2.3.4.1 History 42

2.3.4.2 Criteria 41

2.3.4.3 Calculation 43

2.3.5 Islamic Calendar (IC) 43

2.3.5.1 History 45

ix

2.3.5.2 Criteria 45

2.3.5.3 Calculation using Time Series

Calendar System (TSCS) 48

2.3.5.4 The Benefit of Islamic Calendar 53

2.3.6 Islamic Calendar (IC) vs. Gregorian

Calendar (GC) 54

2.4 Conceptual Framework for the Research 55

2.5 Summary of the Chapter 57

CHAPTER 3 RESEARCH METHODOLOGY 59

3.0 Introduction 59

3.1 Research Philosophy 60

3.2 Research Methodology 61

3.3 Research Framework 64

3.4 Data Collection 65

3.4.1 Primary Data 65

3.3.2 Secondary Data 70

3.5 Population and Sample 71

3.6 Research Instrument 73

3.7 Protocol of Data Analysis 75

3.8 Phases of Data Analysis 77

3.9 Summary of the Chapter 78

CHAPTER 4 DATA ANALYSIS AND RESULTS 79

4.0 Introduction 79

4.1 Profile of Bank Muamalat Malaysia Berhad

at Universiti Tun Hussein Onn Malaysia (UTHM) 80

4.1.1 Vision and Mission of Islamic Bank

In Malaysia 80

4.1.2 Structure of the Organisation 80

4.1.3 The Practice of Islamic Housing Finance at

Bank Muamalat Malaysia Berhad 81

x

4.2 Data Presentation 84

4.2.1 Bai Bithamin Ajil practice at Bank

Muamalat Malaysia Berhad UTHM 84

4.2.2 Respondent’s or customers of Bai’

Bithamin Ajil in Bank Muamalat

Malaysia Berhad UTHM 84

4.3 Calculation of Islamic Calendar (IC) using

Time Series Calendar System (TSCS):

Accurate Times 86

4.3.1 The Application of Time Series

Calendar Software: Accurate Times 87

4.4 Result Obtained for Research Question (1) 91

4.5 Discussion for Research Question (2) 100

4.6 Discussion for Research Question (3) 102

4.6 Conclusion 106

CHAPTER 5 CONCLUSION AND RECOMMENDATIONS 108

5.0 Introduction 108

5.1 The Arrival of Fact: Research Findings 108

5.2 Summary of Chapter 113

5.3 Limitation and Problem of the Research 118

5.4 The Novelty of the Research 119

5.5 Recommendation for the Future Research 120

5.6 Conclusion of Study 120

REFERENCES 123

APPENDICES 133

xi

LIST OF TABLES

1.1 Previous Studies, Islamic Calendar in Shariah Economy 4

2.1 Three Stages in the Contemporary History of Financial

Institutions

16

2.2 Malaysia’s Islamic Finance (IF) Sector 17

2.3 Financial Institutions in Malaysia 17

2.4 The Development of Islamic Banking Globally 23

2.5 History of Islamic Banking in Malaysia 24

2.6 Islamic Banks and its Financial Products in Malaysia 29

2.7 The Advantage and Disadvantage of Fixed Rate Mortgage 37

2.8 The Advantage and Disadvantage of Adjustable Rate Mortgage 38

2.9 Differences between Islamic Housing Finance and Conventional

Housing Finance

39

2.10 Gregorian Month and Day Each Month 42

2.11 Islamic Month in Islamic Calendar 43

2.12 Criteria Islamic Calendar and Gregorian Calendar 55

3.1 Comparison between Qualitative and Quantitative Approaches

Variable Indicator in Research Instrument

63

3.2 Type of Interview 65

3.3 Sources of Respondents for Expert Interview 69

3.4 Structure of the Interview Schedule for the Expert Interview 70

3.5 Variable Indicator Framed to Establish both Quantitative and

Qualitative Research Instrument

74

3.6 Islamic Bank Profile 75

3.7 Table Instrument for Customer and Islamic Housing Finance

Repayment

75

4.1 Financing Product Offered by Bank Muamalat Malaysia Berhad 82

4.2 Table Customer Data BBA in BMMB UTHM 85

xii

4.3 Development of Accurate Times 86

4.4 Period of Samples in Gregorian Calendar 93

4.5 The Length of Financing using Gregorian Calendar 93

4.6 Period of Samples in Islamic Calendar 94

4.7 The Length of Financing using Islamic Calendar 95

4.8 Calculation of Repayment Using Gregorian Calendar 95

4.9 Calculation of Repayment Using Islamic Calendar 96

4.10 Comparison Repayment between Gregorian Calendar and

Islamic Calendar

97

4.11 Profit Calculation of Bai Bithamin Ajil 101

4.12 Challenges for Implementing Islamic Calendar in Malaysia

Banking System

105

5.1 Summary of Findings 118

xiii

LIST OF FIGURES

1.1 Research Design 10

2.1 Branches of Islam 12

2.3 Shariah Governance Framework Model for Islamic

Financial Institutions 22

2.4 Shariah Contracts in Islamic Banking 28

2.5 The Concept of Bai Bithamin Ajil 30

2.6 The Structure of Musharakah 31

2.7 The Concept of Musharakah Mutanaqisah (MM) 33

2.8 The Concept of Ijarah 33

2.9 The Concept of Istishna’ 34

2.10 The Concept of Tawarruq’ 35

2.11 Adjustable Rate Mortgage 38

2.12 Fixed Rate Mortgage and Adjustable Rate Mortgage 39

2.13 The Phases of Moon 46

2.14 Accurate times 50

2.15 Mooncalc 6.0 51

2.16 Islamic Finder Athan (Azan) 52

2.17 Timeanddate.com 53

2.18 Differences between Two Calendar Systems 55

2.19 Conceptual Framework 57

3.1 Philosophical Research Background of the Research 61

3.2 Research Design 64

3.3 Sampling 73

3.4 Comparative Analysis for Time Series Calendar System (TSCS)

and Analysis Phases 76

3.5 The Relationship between Islamic Calendar; Gregorian Calendar

and Islamic Housing Finance Product Repayment 77

xiv

4.1 Organisation Structure of Bank Muamalat Malaysia Berhad

(BMMB) UTHM Branch 81

4.2 Location in Accurate Times 87

4.3 Crescent Visibility on Main Menu 88

4.4 Crescent Visibility 88

4.5 Crescent Visibility after Preview 89

4.6 Crescent Visibility after Calculation 1 90

4.7 Crescent Visibility after Calculation 2 90

4.8 Differences between Two Calendars 91

4.9 Financing Calculator for Bank Muamalat Malaysia Berhad 92

4.10 The Comparison of Total Repayment between Gregorian

Calendar and Islamic Calendar 100

5.1 Summary of Research Findings 122

xv

LIST OF ABBREVIATIONS

ARM - Adjustable Rate Mortgage

BBA - Bai’ Bithamin Ajil

BIMB - Bank Islam Malaysia Berhad

BMMB - Bank Muamalat Malaysia Berhad

BNM - Bank Negara Malaysia

CEO - Chief Executive Officer

DOS - Disk Operating System

FA - Facility Amount

FRM - Fixed Rate Mortgage

GC - Gregorian Calendar

HSC - Hilal Sighting Committee

IFI - Islamic Financial Industry

IFIs - Islamic Financial Institutions

IF - Islamic Finance

IHF - Islamic Housing Finance

IC - Islamic Calendar

IOFC - International Offshore Financial Centre

ISNA - Islamic Society of North America

KLSE CI - Kuala Lumpur Stock Exchange Composite Index

KLIBOR - Kuala Lumpur Interbank Offered Rate

Labuan FSA - Labuan Financial Services Authority

LOFSA - Labuan Offshore

MM - Musharakah Mutanaqisah

NSAC - National Shariah Advisory Council

SC - Shariah Advisory

SAC - Shariah Advisory Council

SSC - Shariah Supervisory Council

xvi

SAB - Shariah Advisory Board

TSCS - Times Series Calendar System

UTHM - Universiti Tun Hussein Onn Malaysia

xvii

LIST OF APPENDICES

APPENDIX TITLE PAGE

A Islamic Calendar Period 2012-2052 133

B Interview Schedule 144

CHAPTER 1

INTRODUCTION TO RESEARCH

1.0 Introduction

Islamic Financial Industry (IFI) has become a global phenomenon. In the last 20

years, Islamic Finance (IF) has been growing and gaining popularity, not only among

Muslims but also among non-Muslims. Many financial players from the Middle East

(Muslim countries including Iran, Saudi Arabia, Kuwait and Qatar) and also

investors in some countries around the world (United Kingdom, Spain, Turkey,

Canada, North Africa) have introduced the shariah compliant products in banking

system (Hesse & Sole, 2008). In view of that development, many non-Muslims

countries such as Singapore, Hong Kong, and England, also began to offer Islamic

Financial System (IFS) (Aziz, 2008). In fact, Islamic Financial Industry was seen

growing globally at a pace of 15-20 per cent per annum (BNM, 2010). According to

the Asian Banker Research Group, Islamic Banks (IBs) have set an annual asset

growth rate of 26.7 per cent. Based on this statement, it indicated that the

development of Islamic Finance is growing consistently. Thus, this phenomenon

allowed the growth of various other banking products, such as housing financial aid

scheme which is based on the Islamic principles or usually perceives as shariah

compliant products (Biswas, 2013).

Islamic Housing Finance is becoming more popular and as common solutions

for Muslims who desired to easily purchase or possessed own a home base on

shariah principles (Amrillah, 2011). The system is appreciated particularly when

people have difficulties in buying properties in cash due to high property value. As

customers of this system they will find a way to buy property through deferred

payments which is free from riba. Aris et al. (2012) stated that Islamic Housing

Finance is a popular alternative financial product to substitute conventional interest-

based housing finance.

2

Islamic Banking (IBg) provides a range of Islamic Housing Finance based on

Islamic principles. Some of its products follow Bai’ Bithamin Ajil (BBA),

Musharakah Mutanasiqah (MM), ijarah, tawaruq, istishna, etc. However, all of

these products are still causing some problems, the problem arises from the necessity

in dealing with interest free on financing, as in line with Quran Surah Al-Baqarah:

275,“and Allah permits the trade but prohibits usury”(Ahmad, 2003).

Most of the Muslims scholars, practitioners, and academicians are debating

about the implementation of Islamic shariah in the banking system. Their focus is

merely in classical issues namely riba, maisyir, and gharar, which are commonly

being practiced in the trades and conventional banking (Saksono, 2014). However,

there is an overlook in the aspect of the calendar system that is used as basis for the

accounting system as an important issue that governs the calculation of the Islamic

Housing Finance all over the world. In Quran, Surah At-Tawbah: 36-37 has depicted

a clear guidance for Muslims to employ the Islamic calendar for their mundane and

spiritual lives. Due to the inexistence of credible Islamic Calendar that can be well

determined in advance, Islamic Banks are now using the Gregorian Calendar as the

basis of their accounting system (Saksono, 2009). Interestingly, as the Gregorian

Calendar is having 11.5 days longer than Islamic Calendar, the practice of Islamic

Finance is seemingly flaws including its application in the operation of Islamic

Housing Finance. In previous research (Saksono, 2012), a comprehensive study on

the application of Gregorian Calendar and how it would simulate ownership of assets

and the provision of corporate financial statements. He discovered that Gregorian

Calendar has caused the shortage of zakat payments by the Muslim customers, due to

the shorter period of days calculated. His study is in the development a robust

estimation model of the potential loss of the payable zakat from the collective

possession of five different assets from stock market (Saksono, 2011).

Therefore, it is necessary for the researcher to scrutinise the employment of

Gregorian Calendar in Islamic Housing Finance. Simultaneously, it will be also of

paramount important to the researcher to prove that the application of Islamic

Calendar is a better approach to be employed with many Islamic Housing Products

(IHP) that have been widely used in Malaysia.

3

1.1 Problem Statement

Islamic Calendar is a lunar calendar that has 12 months in a year. Currently, only

Saudi Arabia uses the Islamic Calendar as their official calendar. Most of the

Muslims countries use Islamic Calendar merely for the calculation of religious

festivities particularly for the Eid Fitri and Eid al-Adha (Saksono, 2009). However,

it can be seen that many Muslims scholars still have an ambiguous stance while

defining the beginning of the month in Islamic Calendar. In addition, different

criteria to command an Islamic month are the major problems to unite Islamic

Calendar across the globe. This is due to different criteria to confirm the presence of

the crescent (hilal), to mark the beginning of Islamic month. Essentially, there are

some schools of thought (mahzab), namely: the first group will only confirm the

presence of the crescent when it is visible to the eyes because this was practiced by

the Rasul and His companions, known as rukyatul hilal. Thousand years ago it is

impossible to construct Islamic Calendar through this method because the beginning

of Islamic month can only be determined minutes or even hours after it started

through the visibility of the eyes. In line with the occurrence of imaging

technologies, the second group appeared by confirming the presence of Islamic

month through astronomical calculation (wujud hilal). Meanwhile the third group

claims to have combined the above (mahzab), which is called Imkan Rukyat

(Saksono, 2009).

Saksono (2009) indicated that Muslims believe that they have been wasting

their energy in defining the presence of the crescent as the sign of the beginning of

Islamic month (hilal). Most of the scholars have been focusing on determining the

beginning of Islamic month and this has arises problem that is not realised by most

Muslims. The problem is they have not utilised the benefit of Islamic Calendar to the

Muslim society. The impacts emerged both social and economic development, which

at certain degree it can actually become a very important part in human life,

particularly Muslims.

Due to the inconsistent calculation Islamic Calendar; and deficiencies in

practising accounting systems in Muslims countries prefer to apply Gregorian

Calendar as a basis of calculation. As the majority are applying this approach, it can

be seen that Islamic Bank and Islamic Finance System (IFS) also used the same

approach in its operation. In terms of the days of the calendars, it was said earlier that

4

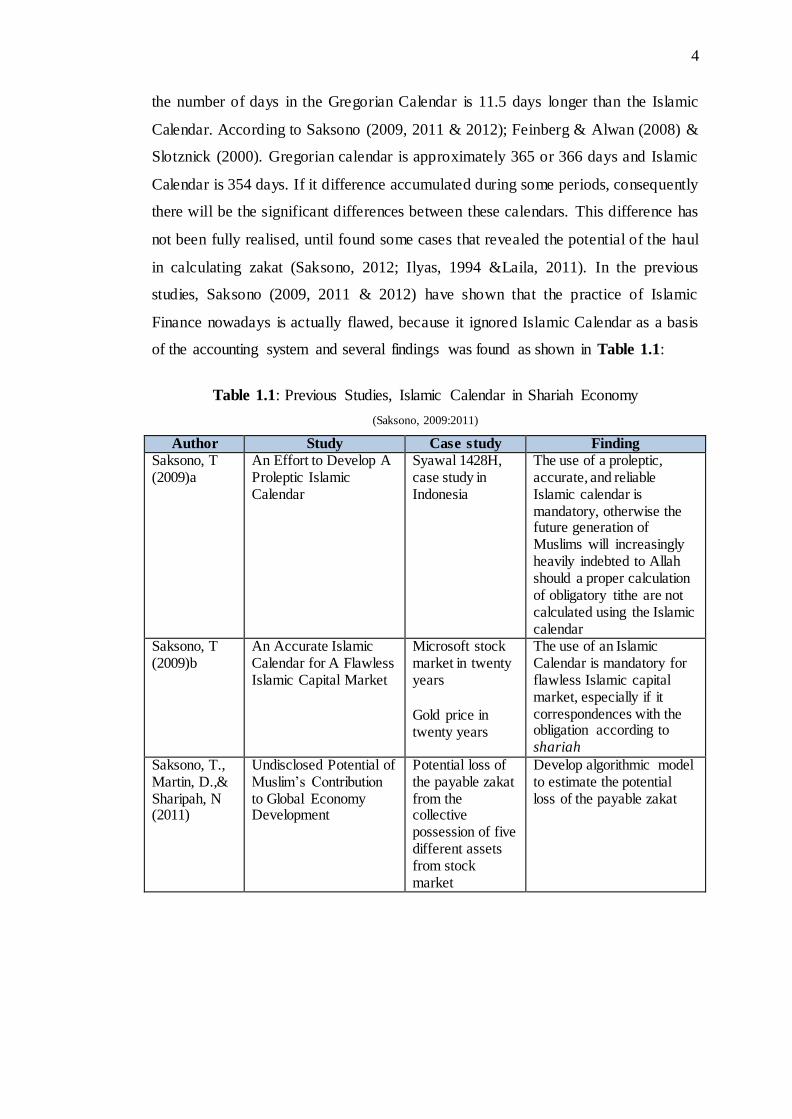

the number of days in the Gregorian Calendar is 11.5 days longer than the Islamic

Calendar. According to Saksono (2009, 2011 & 2012); Feinberg & Alwan (2008) &

Slotznick (2000). Gregorian calendar is approximately 365 or 366 days and Islamic

Calendar is 354 days. If it difference accumulated during some periods, consequently

there will be the significant differences between these calendars. This difference has

not been fully realised, until found some cases that revealed the potential of the haul

in calculating zakat (Saksono, 2012; Ilyas, 1994 &Laila, 2011). In the previous

studies, Saksono (2009, 2011 & 2012) have shown that the practice of Islamic

Finance nowadays is actually flawed, because it ignored Islamic Calendar as a basis

of the accounting system and several findings was found as shown in Table 1.1:

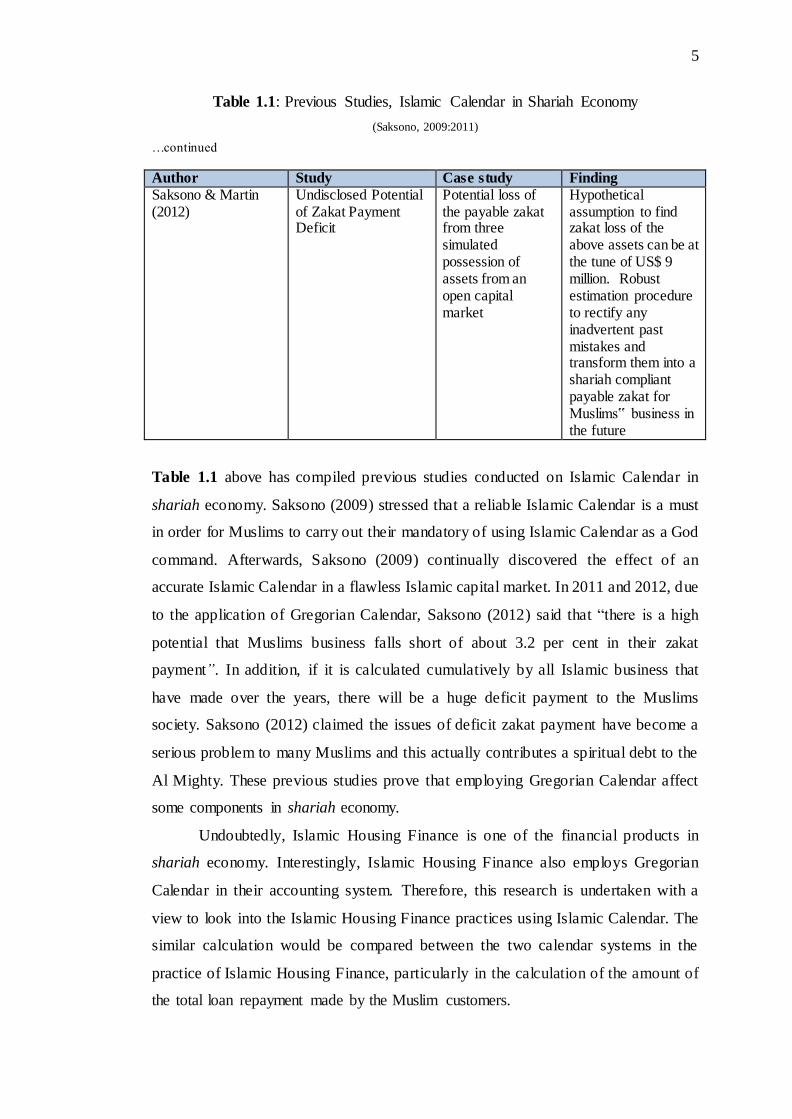

Table 1.1: Previous Studies, Islamic Calendar in Shariah Economy

(Saksono, 2009:2011)

Author Study Case study Finding

Saksono, T (2009)a

An Effort to Develop A Proleptic Islamic Calendar

Syawal 1428H, case study in Indonesia

The use of a proleptic, accurate, and reliable Islamic calendar is mandatory, otherwise the future generation of Muslims will increasingly heavily indebted to Allah should a proper calculation of obligatory tithe are not calculated using the Islamic calendar

Saksono, T (2009)b

An Accurate Islamic Calendar for A Flawless Islamic Capital Market

Microsoft stock market in twenty years

Gold price in twenty years

The use of an Islamic Calendar is mandatory for flawless Islamic capital market, especially if it correspondences with the obligation according to shariah

Saksono, T., Martin, D.,& Sharipah, N (2011)

Undisclosed Potential of Muslim’s Contribution to Global Economy Development

Potential loss of the payable zakat from the collective possession of five different assets from stock market

Develop algorithmic model to estimate the potential loss of the payable zakat

5

Table 1.1: Previous Studies, Islamic Calendar in Shariah Economy

(Saksono, 2009:2011)

…continued

Table 1.1 above has compiled previous studies conducted on Islamic Calendar in

shariah economy. Saksono (2009) stressed that a reliable Islamic Calendar is a must

in order for Muslims to carry out their mandatory of using Islamic Calendar as a God

command. Afterwards, Saksono (2009) continually discovered the effect of an

accurate Islamic Calendar in a flawless Islamic capital market. In 2011 and 2012, due

to the application of Gregorian Calendar, Saksono (2012) said that “there is a high

potential that Muslims business falls short of about 3.2 per cent in their zakat

payment”. In addition, if it is calculated cumulatively by all Islamic business that

have made over the years, there will be a huge deficit payment to the Muslims

society. Saksono (2012) claimed the issues of deficit zakat payment have become a

serious problem to many Muslims and this actually contributes a spiritual debt to the

Al Mighty. These previous studies prove that employing Gregorian Calendar affect

some components in shariah economy.

Undoubtedly, Islamic Housing Finance is one of the financial products in

shariah economy. Interestingly, Islamic Housing Finance also employs Gregorian

Calendar in their accounting system. Therefore, this research is undertaken with a

view to look into the Islamic Housing Finance practices using Islamic Calendar. The

similar calculation would be compared between the two calendar systems in the

practice of Islamic Housing Finance, particularly in the calculation of the amount of

the total loan repayment made by the Muslim customers.

Author Study Case study Finding

Saksono & Martin (2012)

Undisclosed Potential of Zakat Payment Deficit

Potential loss of the payable zakat from three simulated possession of assets from an open capital market

Hypothetical assumption to find zakat loss of the above assets can be at the tune of US$ 9 million. Robust estimation procedure to rectify any inadvertent past mistakes and transform them into a shariah compliant payable zakat for Muslims‟ business in the future

6

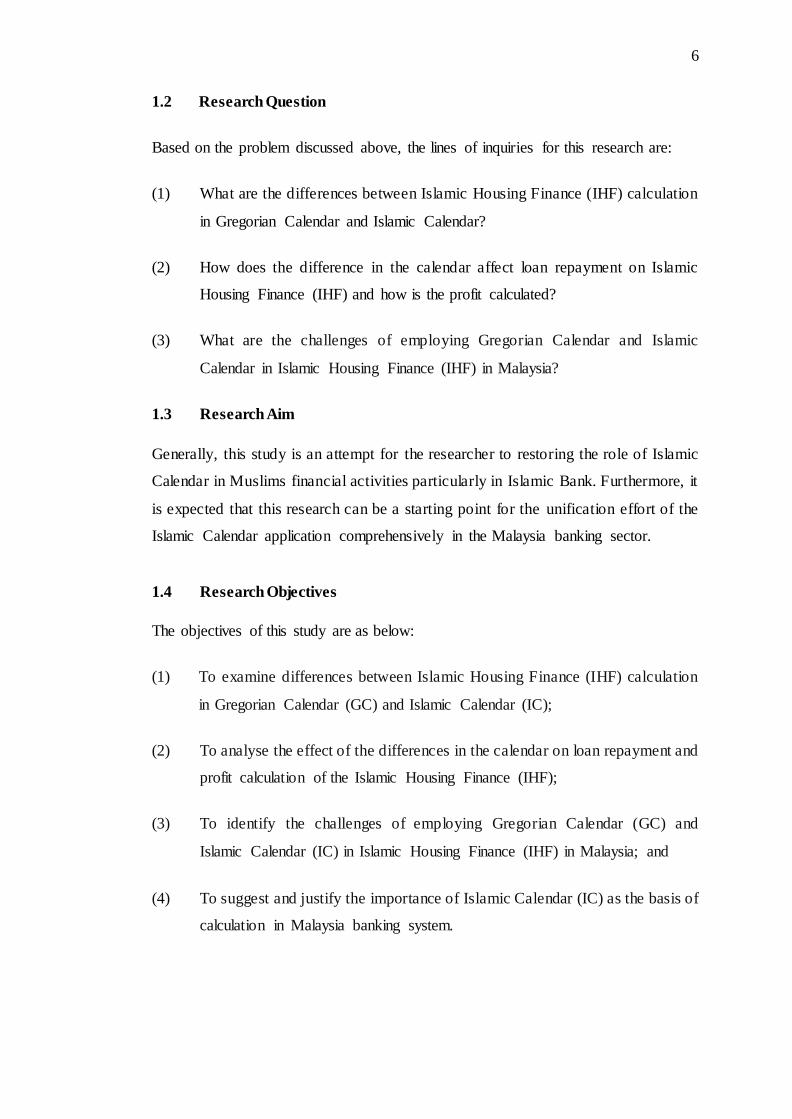

1.2 Research Question

Based on the problem discussed above, the lines of inquiries for this research are:

(1) What are the differences between Islamic Housing Finance (IHF) calculation

in Gregorian Calendar and Islamic Calendar?

(2) How does the difference in the calendar affect loan repayment on Islamic

Housing Finance (IHF) and how is the profit calculated?

(3) What are the challenges of employing Gregorian Calendar and Islamic

Calendar in Islamic Housing Finance (IHF) in Malaysia?

1.3 Research Aim

Generally, this study is an attempt for the researcher to restoring the role of Islamic

Calendar in Muslims financial activities particularly in Islamic Bank. Furthermore, it

is expected that this research can be a starting point for the unification effort of the

Islamic Calendar application comprehensively in the Malaysia banking sector.

1.4 Research Objectives

The objectives of this study are as below:

(1) To examine differences between Islamic Housing Finance (IHF) calculation

in Gregorian Calendar (GC) and Islamic Calendar (IC);

(2) To analyse the effect of the differences in the calendar on loan repayment and

profit calculation of the Islamic Housing Finance (IHF);

(3) To identify the challenges of employing Gregorian Calendar (GC) and

Islamic Calendar (IC) in Islamic Housing Finance (IHF) in Malaysia; and

(4) To suggest and justify the importance of Islamic Calendar (IC) as the basis of

calculation in Malaysia banking system.

7

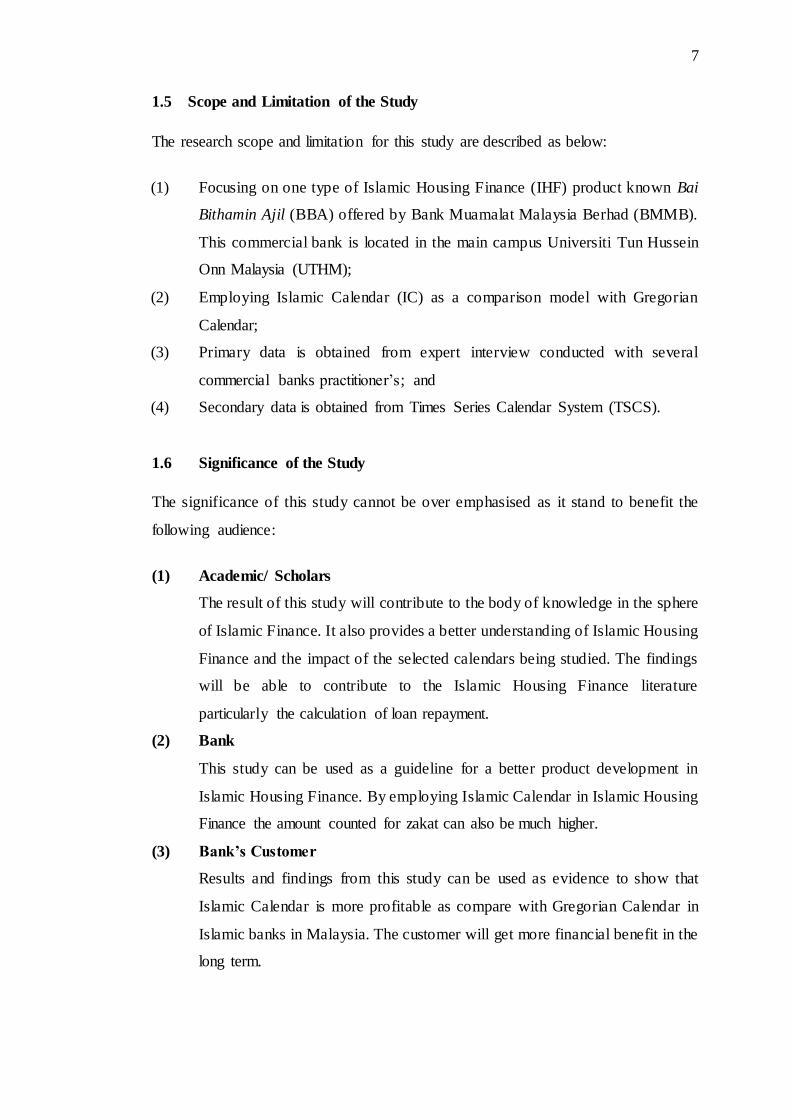

1.5 Scope and Limitation of the Study

The research scope and limitation for this study are described as below:

(1) Focusing on one type of Islamic Housing Finance (IHF) product known Bai

Bithamin Ajil (BBA) offered by Bank Muamalat Malaysia Berhad (BMMB).

This commercial bank is located in the main campus Universiti Tun Hussein

Onn Malaysia (UTHM);

(2) Employing Islamic Calendar (IC) as a comparison model with Gregorian

Calendar;

(3) Primary data is obtained from expert interview conducted with several

commercial banks practitioner’s; and

(4) Secondary data is obtained from Times Series Calendar System (TSCS).

1.6 Significance of the Study

The significance of this study cannot be over emphasised as it stand to benefit the

following audience:

(1) Academic/ Scholars

The result of this study will contribute to the body of knowledge in the sphere

of Islamic Finance. It also provides a better understanding of Islamic Housing

Finance and the impact of the selected calendars being studied. The findings

will be able to contribute to the Islamic Housing Finance literature

particularly the calculation of loan repayment.

(2) Bank

This study can be used as a guideline for a better product development in

Islamic Housing Finance. By employing Islamic Calendar in Islamic Housing

Finance the amount counted for zakat can also be much higher.

(3) Bank’s Customer

Results and findings from this study can be used as evidence to show that

Islamic Calendar is more profitable as compare with Gregorian Calendar in

Islamic banks in Malaysia. The customer will get more financial benefit in the

long term.

8

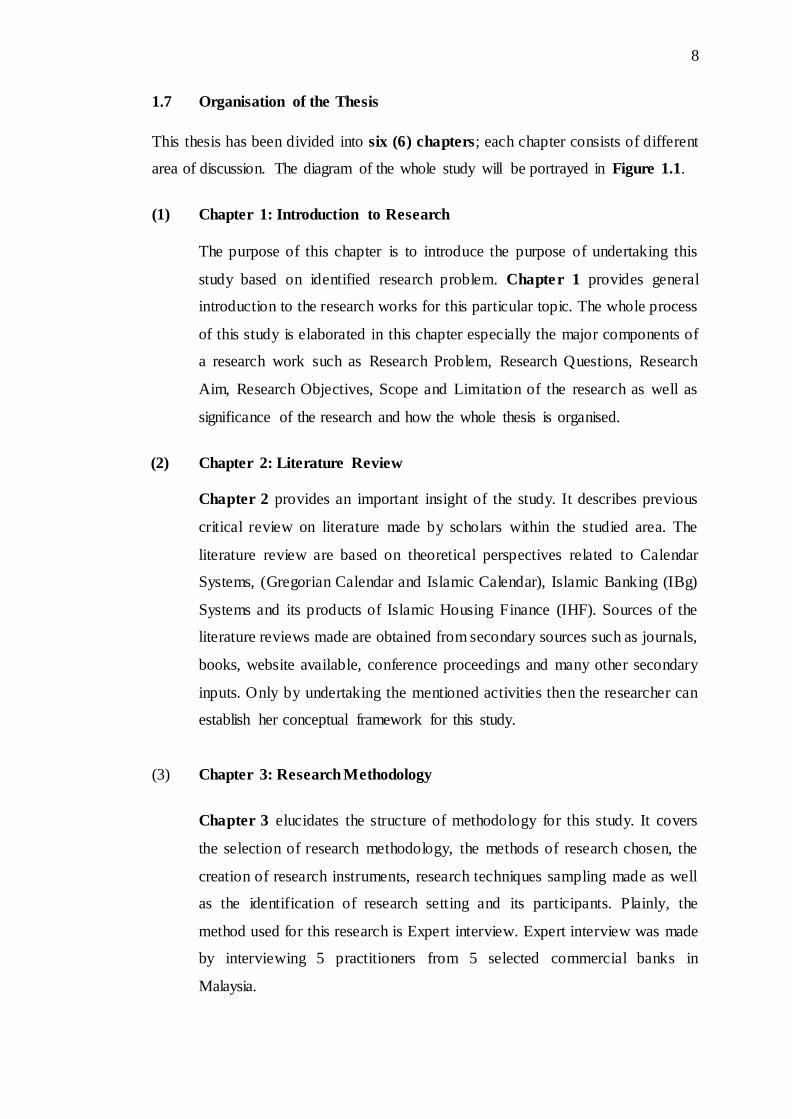

1.7 Organisation of the Thesis

This thesis has been divided into six (6) chapters; each chapter consists of different

area of discussion. The diagram of the whole study will be portrayed in Figure 1.1.

(1) Chapter 1: Introduction to Research

The purpose of this chapter is to introduce the purpose of undertaking this

study based on identified research problem. Chapter 1 provides general

introduction to the research works for this particular topic. The whole process

of this study is elaborated in this chapter especially the major components of

a research work such as Research Problem, Research Questions, Research

Aim, Research Objectives, Scope and Limitation of the research as well as

significance of the research and how the whole thesis is organised.

(2) Chapter 2: Literature Review

Chapter 2 provides an important insight of the study. It describes previous

critical review on literature made by scholars within the studied area. The

literature review are based on theoretical perspectives related to Calendar

Systems, (Gregorian Calendar and Islamic Calendar), Islamic Banking (IBg)

Systems and its products of Islamic Housing Finance (IHF). Sources of the

literature reviews made are obtained from secondary sources such as journals,

books, website available, conference proceedings and many other secondary

inputs. Only by undertaking the mentioned activities then the researcher can

establish her conceptual framework for this study.

(3) Chapter 3: Research Methodology

Chapter 3 elucidates the structure of methodology for this study. It covers

the selection of research methodology, the methods of research chosen, the

creation of research instruments, research techniques sampling made as well

as the identification of research setting and its participants. Plainly, the

method used for this research is Expert interview. Expert interview was made

by interviewing 5 practitioners from 5 selected commercial banks in

Malaysia.

9

(4) Chapter 4: Data Analysis and Results

Chapter 4 explains the process of the analysis made for this study. The

process of analysis for this study is divided into three phases. First is the

analysis of Islamic Calendar prototype, whereby four website-based softwares

were used in order to analyse Islamic Calendar supported with mathematical

(quantitative) computer calculation. Phase 2 involves the calculation of loan

repayment made using selected Islamic Calendar prototype. Then the final

phase involves analysis of EI schedule conducted with 5 commercial banks

personnel.

(5) Chapter 5: Discussion, Conclusion and Recommendation

Chapter 5 discusses results and findings derived from this study. The

purpose of this chapter mainly to show and discuss evidences found in order

to answer the established Research Questions as stated in Section 1-2 earlier

on. Apart from that this chapter also explains how the Research Aim and

Research Objectives of this study being addressed. This chapter summarised

the conclusion made from this study. The implication of this study towards

the existing Body of Knowledge (BOK) and current Islamic Housing

Finance’s practices will be explained. The suggestions of the further research

inquiries will also be proposed to enhance the identified research findings

10

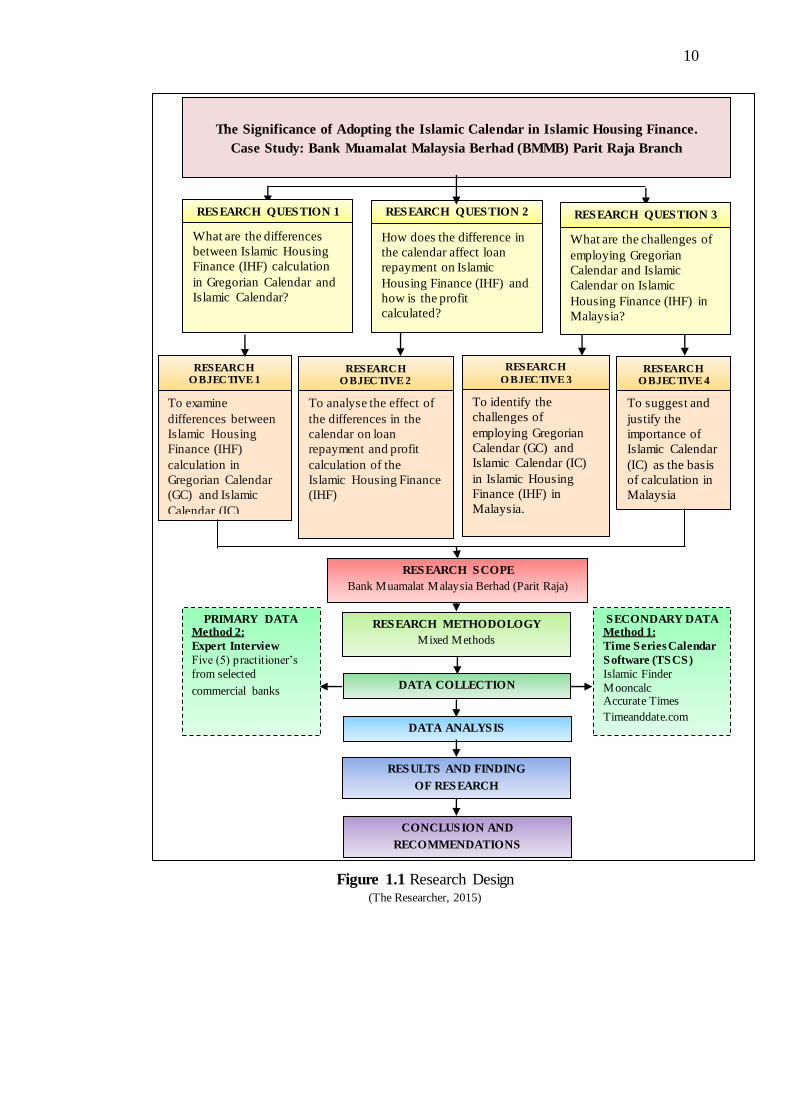

Figure 1.1 Research Design (The Researcher, 2015)

The Significance of Adopting the Islamic Calendar in Islamic Housing Finance.

Case Study: Bank Muamalat Malaysia Berhad (BMMB) Parit Raja Branch

PRIMARY DATA Method 2:

Expert Interview

Five (5) practitioner’s

from selected

commercial banks

What are the differences

between Islamic Housing

Finance (IHF) calculation

in Gregorian Calendar and

Islamic Calendar?

RESEARCH QUESTION 2

2 How does the difference in

the calendar affect loan

repayment on Islamic

Housing Finance (IHF) and

how is the profit

calculated?

RESEARCH O BJECTIVE 1

To examine

differences between

Islamic Housing

Finance (IHF)

calculation in

Gregorian Calendar

(GC) and Islamic

Calendar (IC)

RESEARCH O BJECTIVE 2

To analyse the effect of

the differences in the

calendar on loan

repayment and profit

calculation of the

Islamic Housing Finance

(IHF)

RESEARCH O BJECTIVE 4

To suggest and

justify the

importance of

Islamic Calendar

(IC) as the basis

of calculation in

Malaysia

banking system.

What are the challenges of

employing Gregorian

Calendar and Islamic

Calendar on Islamic

Housing Finance (IHF) in

Malaysia?

RESEARCH QUESTION 3

RESEARCH SCOPE

Bank Muamalat Malaysia Berhad (Parit Raja)

RESEARCH METHODOLOGY

Mixed Methods

SECONDARY DATA Method 1:

Time Series Calendar

Software (TSCS)

Islamic Finder

Mooncalc Accurate Times

Timeanddate.com

DATA COLLECTION

DATA ANALYSIS

RESULTS AND FINDING

OF RESEARCH

CONCLUSION AND

RECOMMENDATIONS

RESEARCH QUESTION 1

RESEARCH

O BJECTIVE 3

To identify the

challenges of

employing Gregorian

Calendar (GC) and

Islamic Calendar (IC)

in Islamic Housing

Finance (IHF) in

Malaysia.

11

CHAPTER 2

LITERATURE REVIEW

2.0 Introduction

Chapter 2 reviews the literature theories relating to the topic of this research.

Islamic Housing Finance (IHF) and calendar system are the focus of attention being

reviewed theoretically in this study. Yam (2006) said that literature review is the

important elements that have to be involved in any research work through a thorough

understanding on research issues and theoretical perspectives in order to achieve the

objectives established for the research. Conducting literature review will help the

researcher to understand and study of their research interest further with a good

supporting evidence through previous validated studies. By doing this, therefore this

chapter consists of two parts; first is the introduction of Islamic Finance and Islamic

Housing Finance, and the second part is the review of Islamic Calendar based on its

historical background, criteria and how it is calculated and how possible it can be

used in banking institutions.

2.1 Introduction to Islamic Finance (IF)

Islam is a divine religion which holds a man as a vicegerent on earth and given a

mandate to exploit the earth and everything in it for the common good (Antonio,

2001). Islam is a universal religion widely accepted and Islam can be applied in a

flexible way and in a broad time and any places. This is apparent in the field of

muamalah, which Islamic principles do not discriminate between Muslims and non-

Muslims. One of it is in the economic sector as the application of Islamic principles

will continue to be accepted, developed and adapted over time even by the non-

Muslims believers indeed. That is why Islam is accepted as the way of life of human

12

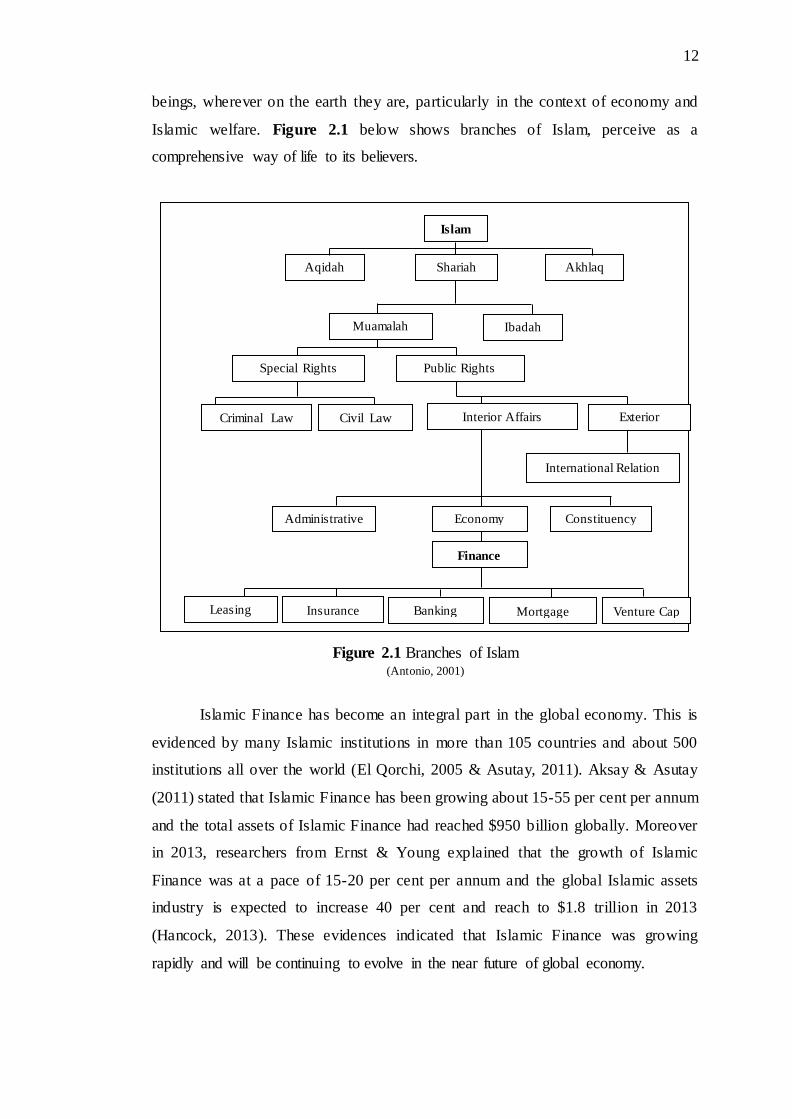

beings, wherever on the earth they are, particularly in the context of economy and

Islamic welfare. Figure 2.1 below shows branches of Islam, perceive as a

comprehensive way of life to its believers.

Figure 2.1 Branches of Islam (Antonio, 2001)

Islamic Finance has become an integral part in the global economy. This is

evidenced by many Islamic institutions in more than 105 countries and about 500

institutions all over the world (El Qorchi, 2005 & Asutay, 2011). Aksay & Asutay

(2011) stated that Islamic Finance has been growing about 15-55 per cent per annum

and the total assets of Islamic Finance had reached $950 billion globally. Moreover

in 2013, researchers from Ernst & Young explained that the growth of Islamic

Finance was at a pace of 15-20 per cent per annum and the global Islamic assets

industry is expected to increase 40 per cent and reach to $1.8 trillion in 2013

(Hancock, 2013). These evidences indicated that Islamic Finance was growing

rapidly and will be continuing to evolve in the near future of global economy.

Islam

Aqidah Shariah Akhlaq

Muamalah Ibadah

Special Rights Public Rights

Criminal Law Civil Law Interior Affairs Exterior

Affairs

International Relation

Economy Administrative Constituency

Finance

Leasing Insurance Banking Mortgage Venture Cap

13

2.1.1 Definition of Islamic Finance (IF)

Usmani (2002); El-Gamal (2006) and Gait & Worthington (2007) define Islamic

Finance as a financial service principally implemented to comply with the main

tenets of Shariah (interest- free basis). Shariah or law of Islam originates from two

principles, there are based on Al-Quran (the Holly of the Muslims) and Sunnah

which is the way of life based on the practices and teachings of Prophet Muhammad

SAW. Jobst (2007) defines Islamic Finance as follows:

“Islamic Finance is limited to financial relationships involving entrepreneurial investment subject to the moral prohibition of interest earnings or usury (riba) and money lending, and haram (sinful activity). speculation, betting, and gambling, including the speculative trade or exchange of money for debt without an underlying asset transfer, the trading of the same object between buyer and seller (bay’ al inah), as well as preventable uncertainty (gharar) such as all financial derivative instruments, forwarding contracts, and future agreements.”

Basically, there are two relevant principles of Islam as stated by Ranjbar &

Pahlevan (2008), known as shariah and muamalah. Shariah according to Joshi

(2012) “literally means a waterway which leads to a mainstream, a drinking place,

and also a road or the right path“. Meanwhile Jobst (2007) defines shariah as

“Islamic religious law, which is binding upon Muslims as a matter of religio us

mandate and also may be incorporated into the secular law of a given jurisdiction.”

Muamalah according to Ahmed (1990) is civil contract and can be used in Islamic

banking and finance.

In Malaysia, shariah principles according Bank Negara Malaysia (2010) are

the foundation for the practice of Islamic Finance through the observance of the

tenets, conditions and principles espoused by shariah. Muamalah is referred to in

term of Islamic Bank, includes buying and selling activities (bai’), receivables

(qara'ah), pledge (rahn), transferring debt (hawalah), for profit in the trade (ijarah),

assurance (dhaman), fellowship (syirkah), and others (Ensiklopedi Hukum Islam,

2013).

Interestingly, Islamic Finance is the application of different contractual and

financial techniques to mobilise funds in the economy according to the principles of

Islamic law (Hegazy, 1999). Additionally, Samad et al. (2005) stated the principles

of sharia law in Islamic Finance are as below:

14

(1) Transaction must be free of interest (riba);

(2) Goods and services that are illegal (haram) from the Islamic point of a view

cannot be produced or consumed;

(3) Activities or transactions involving speculation (gharar) must be avoided;

and

(4) Zakat (the compulsory Islamic tax) must be paid.

Combining all the definitions, Islamic finance can be defined as the application of

financial services and techniques which comply with shariah principals or free from

the prohibition such as riba, gharar, maysir and gambling. Most of definitions stated

that the application must free from the prohibition elements, however there are no

mentioned regarding the period of time, specifically the use of calendar.

2.1.2 Prohibited Elements in Islamic Finance

Based on the context of Islamic Finance as discussed earlier, there are rules that

bring some prohibitions in transaction of Islamic Finance such as riba, gharar and

maysir (gambling) (Samad et.al., 2005). The prohibition matters in Islamic Finance

and it is very important to be taken into account while involving shariah muamalah

as below:

(1) Riba

Riba literally (Arabic) means the excess or increase. Khan (2008) adopted riba

definition “an excess which, in an exchange or sale, accrues to the lender without the

return of any equivalent counter value, substitute or recompense to the other party.”

In Quran, Al Baqarah 275 riba has been described as below:

“Those who consume interest cannot stand (on the Day of Resurrection)

except as one stands that is being beaten by Satan into insanity. That is because they say, “Trade is (just) like interest. “But Allah has permitted trade and has forbidden interest. So whoever has received an admonition from his

Lord and desists may have what is past, and his affair rests with Allah. But whoever returns to (dealing in interest or usury) those are the companions of

the fire; they will abide eternally therein.”

15

In fact, on top of the above verse Quran Al-Baqarah: 276 explained that:

“Allah will destroy Riba (usury) and will give increase for Sadaqat (deeds of charity, alms, etc.) And Allâh likes not the disbelievers, sinners.”

(2) Gharar

Gharar means uncertainty, cheat, or have excessive risk and harm to others

(Ensiklopedi Hukum Islam, 2013). Gharar is prohibited in Islam, as it is clearly

depicted in Quran Surah Al-Baqarah:188 as:

“And do not eat up your property among yourselves for vanities, nor use it as

bait for the judges, with intent that ye may eat up wrongfully and knowingly a little of (other) people’s property.”

(3) Maysir

Maysir or gambling means a game of chance which was played by the Arab before

Islam. Maysir is also often used as the grounds for criticism of conventional financial

practices such as conventional insurance, derivatives and speculation (Islamic

Banker Online, 2013). The prohibition of maysir is stated in Quran Surah Al-

Ma’idah: 90-91 as below,

“O believers, wine and gambling, idols and divining arrows are abhorrence,

the work of Satan. So keep away from it, that you may prevail. Satan only deserves to arouse discord and hatred among you with wine and gambling,

and to deter you from the mention of God and from prayer. Will you desist?

2.1.3 Practice of Islamic Finance in Malaysia

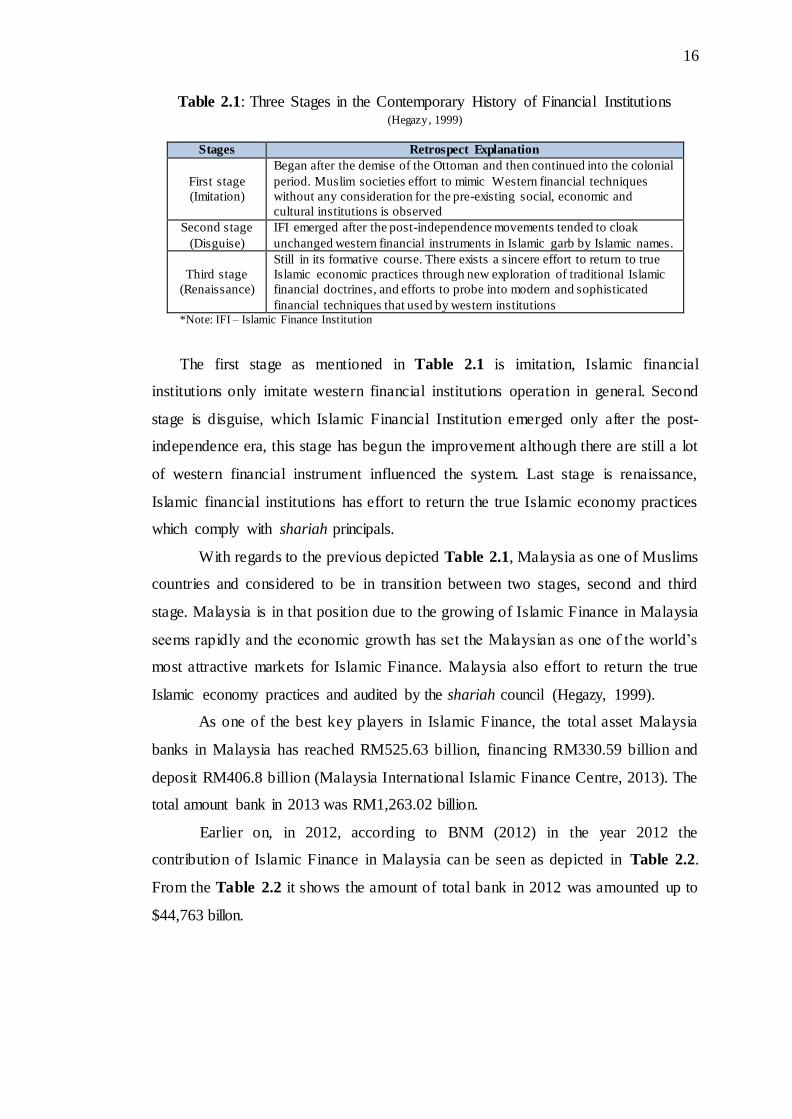

Retrospectively, Hegazy (1999) in his study distinguishes that there are three stages

of the contemporary history of financial institutions in most Muslims countries. The

stages were known as (1) Imitation, (2) Disguise and (3) Renaissance. Table 2.1

below shows the explanation of those stages according to Hegazy (1999):

16

Table 2.1: Three Stages in the Contemporary History of Financial Institutions (Hegazy, 1999)

Stages Retrospect Explanation

First stage

(Imitation)

Began after the demise of the Ottoman and then continued into the colonial

period. Muslim societies effort to mimic Western financial techniques

without any consideration for the pre-existing social, economic and

cultural institutions is observed

Second stage

(Disguise)

IFI emerged after the post-independence movements tended to cloak

unchanged western financial instruments in Islamic garb by Islamic names.

Third stage

(Renaissance)

Still in its formative course. There exists a sincere effort to return to true

Islamic economic practices through new exploration of traditional Islamic

financial doctrines, and efforts to probe into modern and sophisticated

financial techniques that used by western institutions *Note: IFI – Islamic Finance Institution

The first stage as mentioned in Table 2.1 is imitation, Islamic financial

institutions only imitate western financial institutions operation in general. Second

stage is disguise, which Islamic Financial Institution emerged only after the post-

independence era, this stage has begun the improvement although there are still a lot

of western financial instrument influenced the system. Last stage is renaissance,

Islamic financial institutions has effort to return the true Islamic economy practices

which comply with shariah principals.

With regards to the previous depicted Table 2.1, Malaysia as one of Muslims

countries and considered to be in transition between two stages, second and third

stage. Malaysia is in that position due to the growing of Islamic Finance in Malaysia

seems rapidly and the economic growth has set the Malaysian as one of the world’s

most attractive markets for Islamic Finance. Malaysia also effort to return the true

Islamic economy practices and audited by the shariah council (Hegazy, 1999).

As one of the best key players in Islamic Finance, the total asset Malaysia

banks in Malaysia has reached RM525.63 billion, financing RM330.59 billion and

deposit RM406.8 billion (Malaysia International Islamic Finance Centre, 2013). The

total amount bank in 2013 was RM1,263.02 billion.

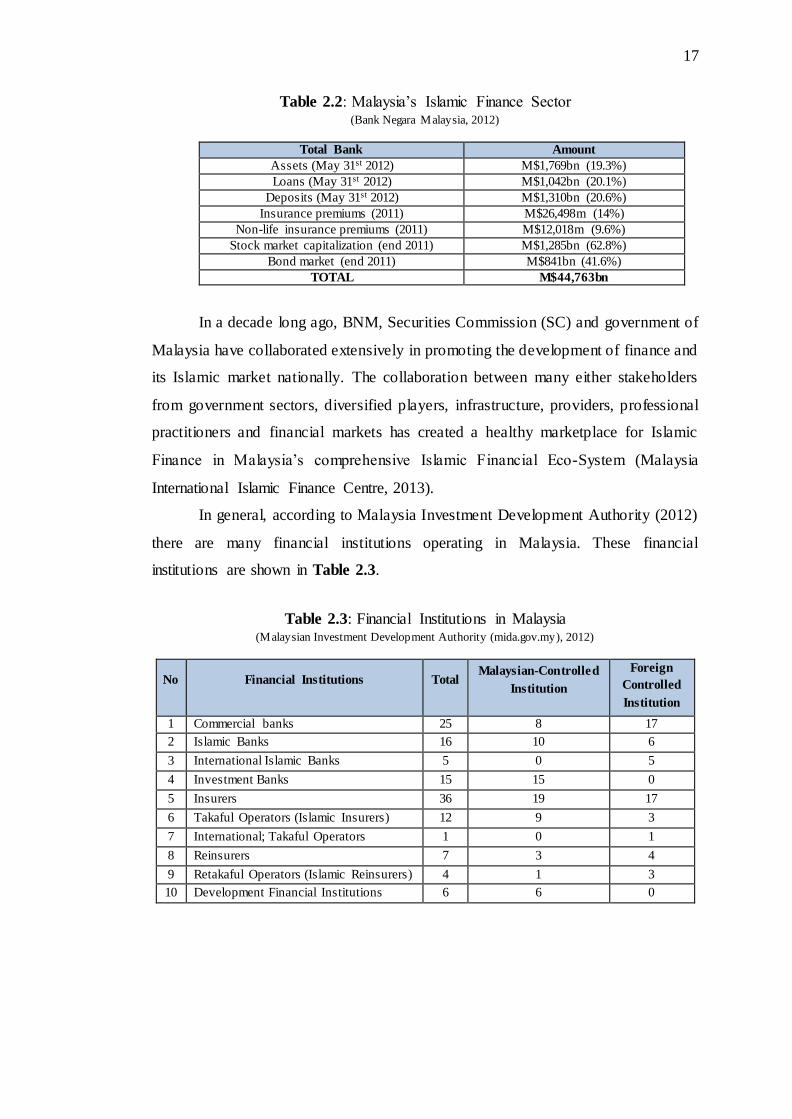

Earlier on, in 2012, according to BNM (2012) in the year 2012 the

contribution of Islamic Finance in Malaysia can be seen as depicted in Table 2.2.

From the Table 2.2 it shows the amount of total bank in 2012 was amounted up to

$44,763 billon.

17

Table 2.2: Malaysia’s Islamic Finance Sector (Bank Negara Malaysia, 2012)

Total Bank Amount

Assets (May 31st 2012) M$1,769bn (19.3%)

Loans (May 31st 2012) M$1,042bn (20.1%)

Deposits (May 31st 2012) M$1,310bn (20.6%)

Insurance premiums (2011) M$26,498m (14%)

Non-life insurance premiums (2011) M$12,018m (9.6%)

Stock market capitalization (end 2011) M$1,285bn (62.8%)

Bond market (end 2011) M$841bn (41.6%)

TOTAL M$44,763bn

In a decade long ago, BNM, Securities Commission (SC) and government of

Malaysia have collaborated extensively in promoting the development of finance and

its Islamic market nationally. The collaboration between many either stakeholders

from government sectors, diversified players, infrastructure, providers, professional

practitioners and financial markets has created a healthy marketplace for Islamic

Finance in Malaysia’s comprehensive Islamic Financial Eco-System (Malaysia

International Islamic Finance Centre, 2013).

In general, according to Malaysia Investment Development Authority (2012)

there are many financial institutions operating in Malaysia. These financial

institutions are shown in Table 2.3.

Table 2.3: Financial Institutions in Malaysia (Malaysian Investment Development Authority (mida.gov.my), 2012)

No Financial Institutions Total Malaysian-Controlled

Institution

Foreign

Controlled

Institution

1 Commercial banks 25 8 17

2 Islamic Banks 16 10 6

3 International Islamic Banks 5 0 5

4 Investment Banks 15 15 0

5 Insurers 36 19 17

6 Takaful Operators (Islamic Insurers) 12 9 3

7 International; Takaful Operators 1 0 1

8 Reinsurers 7 3 4

9 Retakaful Operators (Islamic Reinsurers) 4 1 3

10 Development Financial Institutions 6 6 0

18

Table 2.3 above shows an overview of the number of financial institutions

under the preview of Bank Negara Malaysia as at the end February 2012.

Furthermore, when the practices of Islamic Finance grow in large scale, the

Islamic financial instruments also exist. Islamic financia l instruments today were

developed in the daily practices of Islamic financing and banking. According to

Jamaldeen (2010) , Islamic financial instrument can be divided into two, there are:

(1) Instruments for Mobilising Fund

This instrument is similar to conventional dealings, but different in principal,

it has no interest and also has a predetermined return of savings for current

accounts, savings accounts, investment accounts and sukuk or Islamic bonds.

(2) Instruments for Utilising Fund

This instrument is a new concept and similar to the entrepreneurship factor in

banking system such as mudaraba, musharaka, murabaha and ijara.

Jamaldeen (2010) added that other several of financial instruments are also

available such as short term transaction between Islamic Bank, lines for financing

working capital and redeemable participation.

2.1.4 Governing Bodies for Islamic Finance in Malaysia

It has been said earlier that Islamic Finance Institutions (IFI) must comply with

shariah principles, hence corporate governance in banking sector is established in

order to control the process, policies and law that affects it (Sulaiman et al., 2011).

Sulaiman et al. (2011) also added more specifically about the interrelation between

Corporate Governance and Islamic Finance Institutions (IFs) as it should include the

components as below:

(1) Safeguarding interests of Investment Account Holders;

(2) Compliance with the Shariah;

(3) Governance and risk management of Mudaraba and Musharaka contracts;

and

(4) Establishment of a comprehensive Corporate Governance framework

articulating the fiduciary responsibilities of the board and senior management.

19

In Malaysia’s financial system, there are three main regulators for Islamic

Finance operation. There are Bank Negara Malaysia (BNM), Suruhanjaya

Sekuriti (SC), and the Labuan Offshore (LOFSA). These three regulators will

oversee and monitor the activities and operation being practiced by players in Islamic

Finance banking sector, such as the markets, the institutions, the payments and its

settlement systems. Furthermore, the government of Malaysia will also adjust,

modify and ensure that policies made by the aforesaid regulators are followed by all

the players involved in the financial market (Hussin, 2010).

(1) Bank Negara Malaysia

Bank Negara Malaysia (BNM) has to ensure that all IFs operate in accordance with

shariah law or principles. BNM has to indeed do its primary functions in order to set

out it function as stated in the newly enacted Central Bank of Malaysia Act 2009.

According to Central Bank of Malaysia Act 2009 the function of BNM are as below:

(a) Formulate and conduct monetary policy in Malaysia;

(b) Issue currency in Malaysia;

(c) Regulate and supervise financial institutions which are subject to the laws

enforced by the Bank;

(d) Provide oversight over money and foreign exchange markets;

(e) Exercise oversight over payment systems;

(f) Promote a sound, progressive and inclusive financial system;

(g) Hold and manage the foreign reserves of Malaysia;

(h) Promote an exchange rate regime consistent with the fundamentals of the

economy; and

(i) Act as financial adviser, banker and financial agent of the Government.

In addition, to the above mentioned general function of BNM, there are two-

tier shariah governance infrastructures structured by BNM internally. These

governance infrastructures are the vital components in BNM known as Shariah

Advisory Council (SAC) body at the BNM and an Internal Shariah Committee (SA)

was formed in BNM to monitor the operation of Islamic Banking in each respective

IFI (BNM, 2010).

Plainly, The Shariah Advisory Council of Bank Negara Malaysia (SAC) is a

body established under section 51 of the Central Bank of Malaysia Act 2009, that

20

also has positioned the SAC as the apex authority for the determination of Islamic

law (shariah principles) for the purposes of Islamic Finance such as IBg business,

takaful business, Islamic financial business, Islamic development financial business

and any other business which based on shariah principles. SAC was established in

May 1997 and as the highest shariah authority in monitoring Islamic Finance

Malaysia operation (BNM, 2010). The roles of SAC according Ismail & Tohirin

(2010) are:

(a) Has authority to scrutinise and approve any documents used by IBs and

ensure all transactions (including products and services) not involve any

element which is not approved by Islamic principles; and

(b) To proactively develop and innovate new products and services hand- in-hand

with the bank management.

(2) Suruhanjaya Security

Suruhanjaya Security or Securities Commission (SC) Malaysia established on 1

March 1993 under the Securities Commission Act 1993. SC is a self- funding

statutory body with investigative and enforcement powers in the area within its

jurisdiction. SC has many regulatory functions (Suruhanjaya Sekuriti, 2014), as

stated:

(1) Supervising exchanges, clearing houses and central depositories;

(2) Registering authority to prospectuses of corporations other than unlisted

recreational clubs;

(3) Approving authority for corporate bond issues;

(4) Regulating all matters relating to securities and futures contracts;

(5) Regulating the take over and mergers of companies;

(6) Regulating all matters relating to unit trust schemes;

(7) Licensing and supervising all licensed persons;

(8) Encouraging self-regulation; and

(9) Ensuring proper conduct of market institutions and licensed persons.

21

(3) Labuan Financial Services Authority (Labuan FSA)

Labuan Financial Services Authority (Labuan FSA) was established on 15 February

1996 under section 3 of the Labuan Financial Services Authority Act 1996. Labuan

FSA was established with some objectives as below (Labuan FSA, 2010):

(1) To promote and develop Labuan as an international center for business and

financial services;

(2) To develop national objectives, policies and priorities for the orderly

development and administration of the international business and financial

services in Labuan; and

(3) To act as the central regulatory, supervisory and enforcement authority of the

international business and financial services industry in Labuan.

2.1.5 The Framework of Islamic Finance in Malaysia

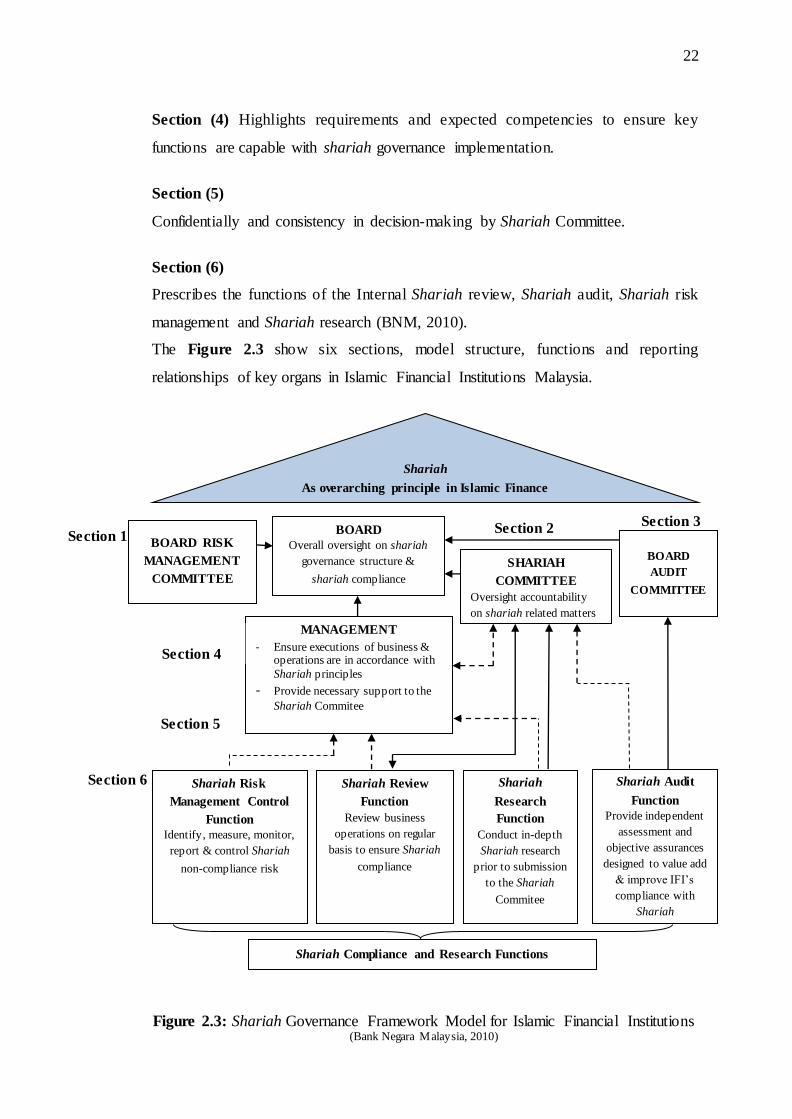

According to Bank Negara Malaysia (2010), the framework of Islamic Finance in

Malaysia based on approach is divided into six sections. Certainly, it is distinguished

into 6 sections to ensure that Islamic finance is comply with shariah principals

relatively. The explanations of the framework are as below:

Section (1)

Outlines the general requirements of the Shariah governance framework which

describes the essential key functions.

Section (2)

Oversight, accountability and responsibility expected of the board of directors,

Shariah Committee and also management. Board director oversight on shariah

governance structure & shariah compliance, Shariah Committee oversight

accountability on shariah related matters and management is ensuring executions of

business & operations are in accordance with Shariah principles and also provide

necessary support to the Shariah Committee.

Section (3)

This section aims to safeguard the independence of the Shariah Committee in

ensuring sound Shariah decision-making and emphasis on the role of the board of

directors in recognising the independence of the Shariah Committee.

22

Section (4) Highlights requirements and expected competencies to ensure key

functions are capable with shariah governance implementation.

Section (5)

Confidentially and consistency in decision-making by Shariah Committee.

Section (6)

Prescribes the functions of the Internal Shariah review, Shariah audit, Shariah risk

management and Shariah research (BNM, 2010).

The Figure 2.3 show six sections, model structure, functions and reporting

relationships of key organs in Islamic Financial Institutions Malaysia.

Section 2

Section 1

Section 3

Section 5

Section 6

Figure 2.3: Shariah Governance Framework Model for Islamic Financial Institutions (Bank Negara Malaysia, 2010)

BOARD RISK

MANAGEMENT

COMMITTEE

BOARD

Overall oversight on shariah

governance structure &

shariah compliance

SHARIAH

COMMITTEE

Oversight accountability

on shariah related matters

BOARD

AUDIT

COMMITTEE

MANAGEMENT

- Ensure executions of business & operations are in accordance with

Shariah principles

- Provide necessary support to the

Shariah Commitee

Shariah Risk

Management Control

Function

Identify, measure, monitor,

report & control Shariah

non-compliance risk

Shariah Review

Function

Review business

operations on regular

basis to ensure Shariah

compliance

Shariah

Research

Function

Conduct in-depth

Shariah research

prior to submission

to the Shariah Commitee

Shariah Audit

Function

Provide independent

assessment and

objective assurances

designed to value add

& improve IFI’s

compliance with

Shariah

Shariah Compliance and Research Functions

Shariah

As overarching principle in Islamic Finance

Section 4

23

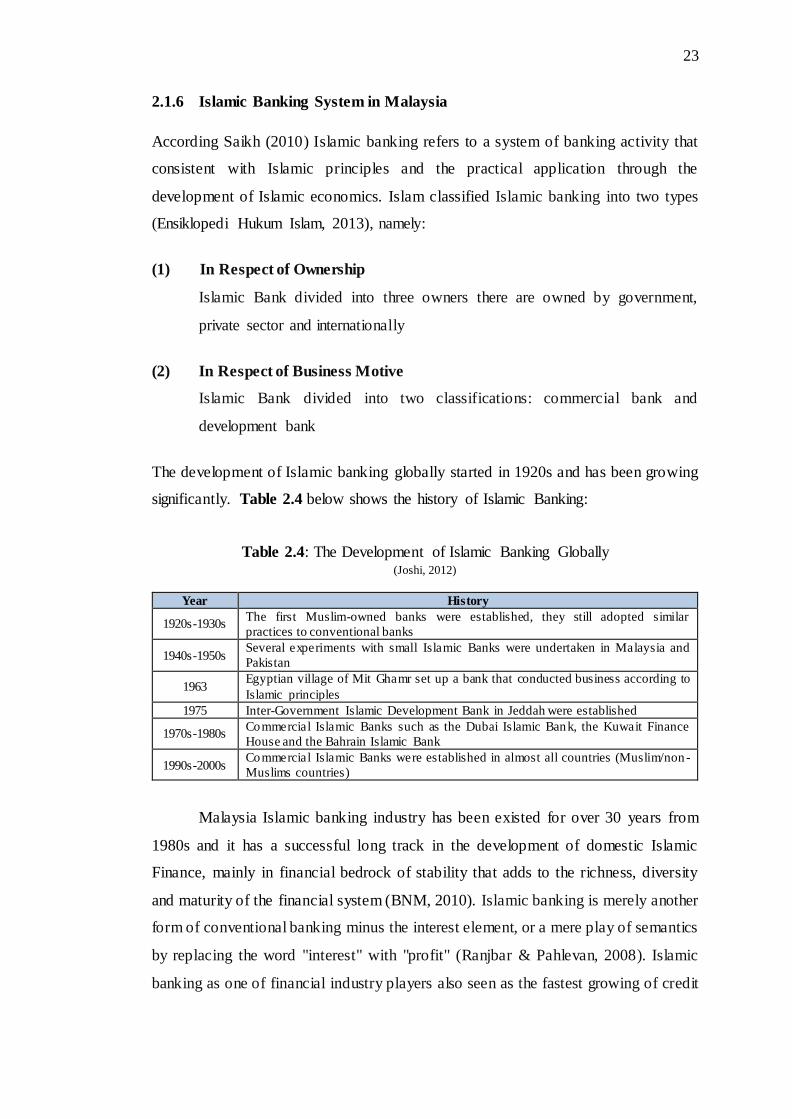

2.1.6 Islamic Banking System in Malaysia

According Saikh (2010) Islamic banking refers to a system of banking activity that

consistent with Islamic principles and the practical application through the

development of Islamic economics. Islam classified Islamic banking into two types

(Ensiklopedi Hukum Islam, 2013), namely:

(1) In Respect of Ownership

Islamic Bank divided into three owners there are owned by government,

private sector and internationally

(2) In Respect of Business Motive

Islamic Bank divided into two classifications: commercial bank and

development bank

The development of Islamic banking globally started in 1920s and has been growing

significantly. Table 2.4 below shows the history of Islamic Banking:

Table 2.4: The Development of Islamic Banking Globally (Joshi, 2012)

Year History

1920s-1930s The first Muslim-owned banks were established, they still adopted similar

practices to conventional banks

1940s-1950s Several experiments with small Islamic Banks were undertaken in Malaysia and

Pakistan

1963 Egyptian village of Mit Ghamr set up a bank that conducted business according to

Islamic principles

1975 Inter-Government Islamic Development Bank in Jeddah were established

1970s-1980s Commercial Islamic Banks such as the Dubai Islamic Bank, the Kuwait Finance

House and the Bahrain Islamic Bank

1990s-2000s Commercial Islamic Banks were established in almost all countries (Muslim/non -

Muslims countries)

Malaysia Islamic banking industry has been existed for over 30 years from

1980s and it has a successful long track in the development of domestic Islamic

Finance, mainly in financial bedrock of stability that adds to the richness, diversity

and maturity of the financial system (BNM, 2010). Islamic banking is merely another

form of conventional banking minus the interest element, or a mere play of semantics

by replacing the word "interest" with "profit" (Ranjbar & Pahlevan, 2008). Islamic

banking as one of financial industry players also seen as the fastest growing of credit

24

market in Muslim countries. Geographically, the effect has grown has grown from

Middle East to Europe and in South East Asian market as well (Shaikh, 2010).

Malaysia has a significant number of full-pledged Islamic Banks, including

some foreign owned entities (BNM, 2010). Islamic banking and the takaful market in

Malaysia are reasonably concentrated. There are some major banks are going global

such as Maybank Islamic, Bank Islam Malaysia, Am Islamic Bank, Public Islamic

Bank, CIMB Islamic (BNM, 2015).

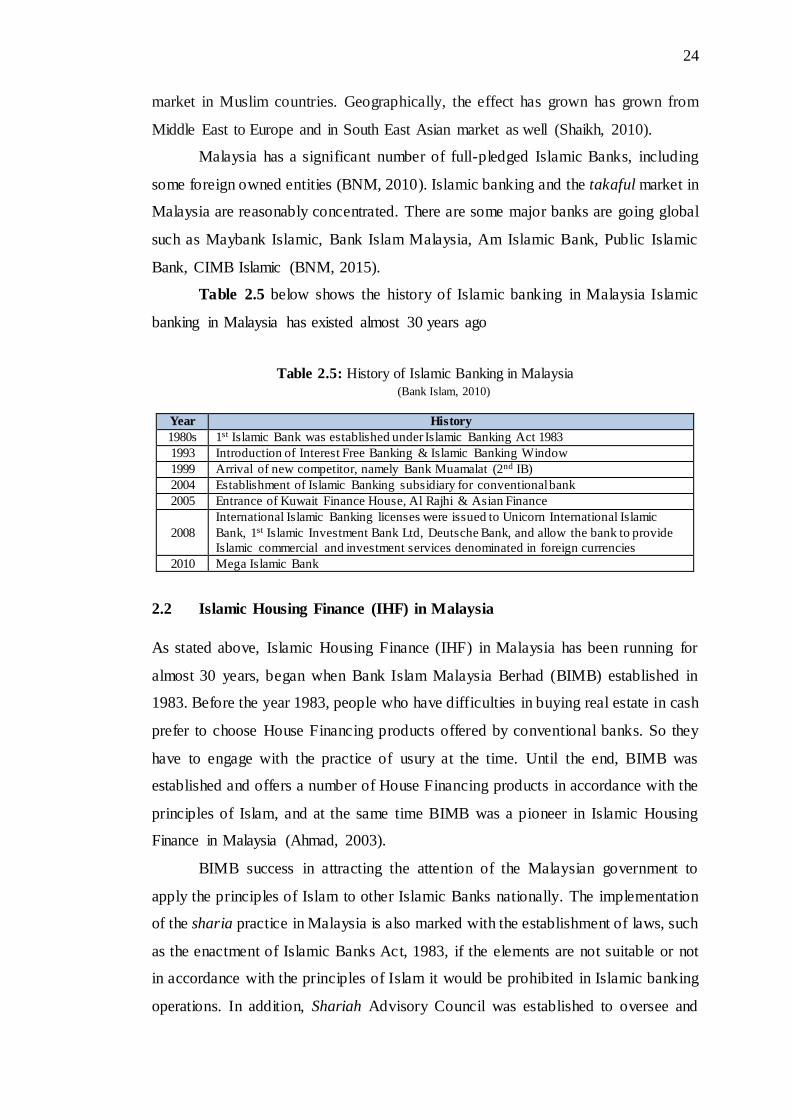

Table 2.5 below shows the history of Islamic banking in Malaysia Islamic

banking in Malaysia has existed almost 30 years ago

Table 2.5: History of Islamic Banking in Malaysia (Bank Islam, 2010)

Year History

1980s 1st Islamic Bank was established under Islamic Banking Act 1983

1993 Introduction of Interest Free Banking & Islamic Banking Window

1999 Arrival of new competitor, namely Bank Muamalat (2nd IB)

2004 Establishment of Islamic Banking subsidiary for conventional bank

2005 Entrance of Kuwait Finance House, Al Rajhi & Asian Finance

2008

International Islamic Banking licenses were issued to Unicorn International Islamic

Bank, 1st Islamic Investment Bank Ltd, Deutsche Bank, and allow the bank to provide

Islamic commercial and investment services denominated in foreign currencies

2010 Mega Islamic Bank

2.2 Islamic Housing Finance (IHF) in Malaysia

As stated above, Islamic Housing Finance (IHF) in Malaysia has been running for

almost 30 years, began when Bank Islam Malaysia Berhad (BIMB) established in

1983. Before the year 1983, people who have difficulties in buying real estate in cash

prefer to choose House Financing products offered by conventional banks. So they

have to engage with the practice of usury at the time. Until the end, BIMB was

established and offers a number of House Financing products in accordance with the

principles of Islam, and at the same time BIMB was a pioneer in Islamic Housing

Finance in Malaysia (Ahmad, 2003).

BIMB success in attracting the attention of the Malaysian government to

apply the principles of Islam to other Islamic Banks nationally. The implementation

of the sharia practice in Malaysia is also marked with the establishment of laws, such

as the enactment of Islamic Banks Act, 1983, if the elements are not suitable or not

in accordance with the principles of Islam it would be prohibited in Islamic banking

operations. In addition, Shariah Advisory Council was established to oversee and

123

REFFERENCE

Abu Bakar, A. (2009). Pelaksanaan Bay Al Inah Dalam Pembiayaan Peribadi

(Personal Loan) di Malaysia. International conference on corporate law

(ICCL) . Retrieved December 9, 2012. from p.5 at

http://repo.uum.edu.my/1166/1/Azizi_Abu_Bakar.pdf

Adams, J., Khan, H, T.A., Raeside, Robert., & White, D. (2007). Research Methods

for Graduate Business and Social Science Students. New Delhi: Response

Books.

Ahmad, F. A. (2003). Pembiayaan Perumahan Secara Islam. Kuala Lumpur: Utusan

Publications & Distributors Sdn Bhd.

Ahmed, Hassan O. (1990). Shariah Contract in Islamic Banking and Finance.

Retrieved June 2014, from

http://www.islamicbanker.com/publications/shariah-contracts- islamic-

banking-and-finance

Alam, M.N. (2008). Institutionalization and Development of Saving Habits Through

Bai-Muajjal Mode of Financing. Retrieved April 2013, from

http://www.kantakji.com/media/8768/ins.pdf

Ali, e. a. (n.d.). (2011) Islamic Benchmarking: An Alternative to Interest Rate.

Retrieved October 11.from p.2 at

http://www.cba.edu.kw/wtou/download/conf4/Ali.pdf

Alway, P. (2015). Lunar Eclipse. Retrieved January, 2015, from

http://www.umich.edu/~lowbrows/astrophotos/alway/lunareclipse.html

Amrillah, M. A. (2011). Analisis Komparasi Aplikasi PInjaman Kredit Pemilikan

Rumah (KPR) dan Pembiayaan Kredit Pemilikan Rumah Syariah (KPRS)

Pada Perusahaan Perbankan di Malang . Universitas Islam Negeri Maulana

Malik Ibrahim.

Antonio, M. S. (2001). Bank Syariah: Dari Teori ke Praktek . Jakarta: Gema Insani.

124

Aris, N.A., Othman, R., Azli, R.M., Arshad, R., Shahri, M., & Yaakub, A.R. (2012).

Islamic Housing Finance: Comparison between Bai' Bithamin Ajil (BBA) and

Musharakah Mutanaqisah (MM). African Journal of Business Management

Vol. 6(1) pp 263-277. Retrieved September 26,2012. from p: 266-273. at

http://www.academicjournals.org

Asutay, M & Aksak, E. (2011). Does Islamic Finance Make the World Economically

and Financially Safer? Islamic Finance and Its Implications on

Sustainable Economic Growth. 8th International Conference on Islamic

Economics and Finance. Retrieved October 29, 2012. from p: 10, at

http://conference.qfis.edu.qa/app/media/215

Audenhove, L.V. (2010). Expert Interviews and Interview Techniques for Policy

Analysis. Power Point Presentation Notes. Vrije Universiteit Brussel:

Belgium.

Aziz, A. Z. (2008). Islamic Finance: Global trends and Challenges. Retrieved

November 7, 2012 from p. 7 at http://www.nbr.org

Bank Islam. (2010). An Overview of Shariah Contract Practice in Malaysian Islamic

Banks. Retrieved May 2013. from

http://www.bankislam.com.my/en/documents/shariah/anoverviewofshariahco

ntractpractice.pdf

Bank Negara Malaysia. (2010). Syariah Resolutions in Islamic Finance Second

Edition. Retrieved October 14,2012, from http://www.bnm.go.my

Bank Negara Malaysia. (2015). Listed of Lisenced Banking Institutions in Malaysia.

Retrieved 2015 from

http://www.bnm.gov.my/?ch=li&cat=islamic&type=IB&lang=en

Bank Muamalat Malaysia Berhad (2012) Retrieved November 7, 2012 from p. 7

at http://www.muamalat.com.my

Barbera, S., Hammond, P.J., & Seidl, C. (1998). Handbook of Utility Theory. Kluwer

Academic Publisher: Netherland.

Barreiro, P. L., & Albandoz, J. P. (2001). Population and Sample. Sample

Techniques. Retrieved June , 2013 from http://optimierung.mathematik.uni-

kl.de/mamaeusch/veroeffentlichungen/ver_texte/sampling_en.pdf

Bentchikou, A., Rasiwala, M., & Patel, A. (2011). An Islamic calendar for Mekkah.

Selonology Today. Retrieved August 1, 2013 from

http://www.makkahcalendar.orgp

125

Bodie, Z., & Merton, R. (2000). Finance. New Jersey: Prentice Hall.

Bogner, A., Littig, B.,& Menz, W. (2009). Interviewing Experts. New York: Palgrave

Macmillan

Biswas, Rajiv. (2013). FutureAsia: The New Gold Rush in the East. New York:

Palgrave Macmillan.

Bofah, Kofi. (2013). The Definition of a Legal Mortgage. Retrieved July 2013, from

http://homeguides.sfgate.com/definition- legal-mortgage-8946.html

Bruin, M.J., & Crull, S. R. (2001). Housing Finance. Retrieved 2014, from

http://www.housingeducators.org/Journals/H&S_Vol_28_1&2_Housing_Fina

nce.pdf

Castillo, J.J. (2009). Measuring and Scaling. Retrieved February, 2013, from

http://www.memoireonline.com/03/12/5600/m

Chiquier, L., & Lea, M. (2009). Housing Finance Policy in Emerging Markets.

World Bank: Washington DC.

Crotty, M. (1998). The Foundation of Social Research. Sage Publication: London.

Deming, W. Edwards. (1990). Sample Design in business research. John Wiley and

Sons. p. 31. ISBN 0-471-52370-4.

Devlin, J. F. (2013). An Analysis of Choice Criteria in the Home Loan Market.

International Journal of Bank Marketing 20/5, PP 212-226.

Dogget, L.E. (2013). Calendars. Retrieved on August, 2012, from

http://astro.nmsu.edu

Diamond, D. (2000). Islamic Housing Finance. Retrieved July 2013, from

http://www.housingfinance.org/uploads/Publicationsmanager/0009_Isl.pdf

Dwidayati, K.H., Sulaiman, N., & Saksono,T. (2013). A Comparative Analysis

between Two Systems Calendars in Islamic Banking System. 1st FPTP

Postgraduate Seminar 2013: Univesiti Tun Hussein Onn Malaysia.

El Qorchi, Mohammed. (2005). Islamic Finance Gears Up. Finance & Development

Vol4 No 4. Retrieved July, 2013 from

http://ibtra.com/pdf/journal/v2_n2_article2.pdf.

126

El Gamal, M. A. (2006). Islamic Finance: Law, Economic and Practice. Retrieved

August,2012,from

books.google.com.my/books?hl=id&lr=&id=2ElRUvoVRxYC&oi=fnd&pg=

PR10&dq=El+Gamal+2006+Islamic+finance&ots=vdhg2NVnEu&sig=-

PayioxeT7BraXXWPd1b99DYdXA&redir_esc=y#v=onepage&q=El%20Ga

mal%202006%20Islamic%20finance&f=false

Endut, N., & Toh, G.H. (2009). Household Debt in Malaysia. Retrieved July 2013,

from http://www.bis.org/publ/bppdf/bispap46l.pdf

Ensiklopedi Hukum Islam. (2013). Tentang Gharar. Retrieved March 2013, from

http://www.fiqhislam.com/index.php?option=com_content&view=article&id

=66491:tentang-gharar&catid=46:syariahakidahakhlakibadah&Itemid=362

Free Dictionary Online. (2013). Definition of Islam. Retrieved July, 2013, from

http://www.thefreedictionary.com/Islam

Feinberg, Y., & Alwan, A. (2008). Simultaneous display of multiple calendar

systems. Retrieved July, 2015 from

https://www.google.com/patents/US7349920

Fuster, A., & Vickery, J. (2013). Securitization and the Fixed-Rate Mortgage.

Retrieved July 2013, from

http://www.newyorkfed.org/research/staff_reports/sr594.pdf

Gait, A. H., & Worthington, A. C. (2007). A Primer on Islamic Finance: Definitions,

Sources, Principles and Methods. School of Accounting and Finance Working

Paper Series No. 07/05. Retrieved February 1, 2013, from

http://ro.uow.edu.au/cgi/viewcontent.cgi?article=1359&context=commpapers

Gibb, K., Munro, M., & Satsangi, M. (1999). Housing Finance in the UK. New

York: Palgrave

Global Islamic Finance Magazine. UK takes initiatives to issue Islamic Bond (Sukuk)

Retrieved November 7, 2012, from

http://www.globalislamicfinancemagazine.com

Gregorian calendar. (2013). Developers. Retrieved September 11, 2013 from

http://developer.android.com

Guba, E. G., & Lincoln, Y. S. (1989). Fourth Generation Evaluation. Newbury Park:

Sage.

Hart, C. (2005). Doing Your Maasters Dissertation. Sage Publication: London.

127

Hancock, Mellisa. (2013). Islamic finance in 2013: Beyond the growth. Retrieved

September 1, 2013 from http://www.thebanker.com/Markets/Islamic-

Finance/Islamic-finance-in-2013-beyond-the-growth

Hegazy, W. (1999). Islamic Finance in Malaysia, A Tax Perspective. Pro. of the

Second Harvard University Forum on Islamic Finance: Islamic Finance into

the 21st Century Cambridge. Massachussetts. Center for Middle Eastern

Studies. Harvard University. pp. 215-224.

Heiko Hesse, A. A., & Sole, J. (2008). Trends and Challenges in Islamic Finance ,

Vol.9. October 11, 2012. Retrieved from p.175 at

http://relooney.fatcow.com/0_Middle-East_1.pdf

Howe, Kenneth. R. (2012). Mixed Methods, Triangulation, and Causal Explanation.

Journal of Mixed Methods Research vol. 6 no.2. Retrieved June, 2013, from

http://mmr.sagepub.com/content/6/2/89.short

Huda. (2013). Moon Sighting at Ramadhan. Retrieved March, 2013, from

http://islam.about.com/od/ramadan/a/moonsighting.htm

Hussain, A. S. (2013). Fundamental of Shariah. Retrieved July 2013, from

http://www.ibbm.org.my/pdf/FSTEP%20Fundamentals%20of%20Shariah-

3rd%20DAY.pdf

Hussin, T. M. T. T. (2010). Proposed Structure of the Islamic Financial System in

Malaysia. Retrieved March 2013, from

https://www.academia.edu/1340209/Proposed_Structure_of_the_Islamic_Fin

ancial_System_in_Malaysia

Ishak, M. S., & Abdullah, O. C. (2012). Islamic Perspective on Marketing Mix.

European Journal of Scientific Research , Retrieved September 26, 2012.

from pp. 214-220 at

http://www.europeanjournalofscientificresearch.com/ISSUES/EJSR_77_2_07

Ilyas, M. (1994). Lunar Crescent Visibility Criterion and Islamic Calendar. Q. J. R

astr. Soc, 35 . Retrieved November 13, 2012 pp: 425 461 at

http://adsabs.harvard.edu/full/1994QJRAS..35..425L

Investopedia. (2013). Definition of Finance. Retrieved February, 2013, from

http://www.investopedia.com/terms/f/finance.asp

Islamic Banker Online. (2013). Maysir. Retrieved March 2013, from

http://www.islamicbanker.com/dictionary/m/maysir

128

Islamic Finder. (2012). Islamic Finder. Retrieved December, 2012, from

http://www.islamicfinder.org/

Ismail, A. G., & Tohirin, A. (2010). Islamic Law and Finance. Humanomics. Vol. 26

Issue. 3. Retrieved March 2013, from p. 178-199 at

http://www.emeraldinsight.com/journals.htm?articleid=1881982

Jamaldeen, M. (2010). Islamic Financial Instruments. Retrieved March 2013, from

http://www.slideshare.net/jmfsaad/islamic-financial-instruments

Jeudi. (2012). Islamic banking and finance to continue growth in 2013. Retrieved

July, 2013 from http://www.islamicfinancialtimes.net

Jobst, Andreas A (2007). Derivatives in Islamic Finance. Islamic Economic Studies.

Vol. 15, No. 1. Retrieved on October 20, 2013, from

http://ssrn.com/abstract=1015615

Jabareen, Y. R. (2009). Building a Conceptual Framework: Philosophy, Definition

and Procedure. Retrieved May 2013 from

http://ejournals.library.ualberta.ca/index.php/IJQM/article/viewArticle/6118

Joshi, V. (2012). Islamic Finance: Understanding an Impending Financial

Phenomenon. International Journal of Management and Strategy (IJMS), Vol.

3, Issue 4 at

http://www.facultyjournal.com/webmaster/upload/__Islamic%20Finance(IJM

S).pdf

Khan, Salar M. (2008). Islamic Banking & Finance Rationale, Framework and

Prospectus. Islamic Banking & Finance: Shariah Guidance on Principles

and Practices pp: 39-42. (S. M. Khan, Ed.) Bangalore, Bangalore, India: AS

Noordeen.

King, P. (2009). Understanding Housing Finance. Routledge: London

Labuan FSA. (2010). Annual Report 2010. Retrieved March 2013, from

http://labuanfsa.gov.my/documents/10156/e93928c4-cfc3-44f6-8587-

24f139ac5d7b

Laila, N. (2011). Algoritma Astronomi Modern Dalam Penentuan Awal Bulan

Qomariyah. Jurisdictic, Jurnal Hukum dan Syariah. Retrieved December 9,

2012 from p.92-99 at http://ejournal.uin-malang.ac.id

129

Littig, B. (2013). Expert Interviews. Methodology and Practice. IASR Lecture

Series. from

http://www.uta.fi/iasr/lectures/index/17.9.2013_Beate%20Littig_Tampere%2

0Expert-Interviews.pdf

Malaysia International Islamic Financial Centre. (2013). Islamic Finance Leadership