Embed Size (px)

Citation preview

LATIN AMERICAN YOUTH CENTER

Consolidated Financial Statements Together with

Reports of Independent Public Accountants

For the Years Ended September 30, 2010 and 2009

SEPTEMBER 30, 2010 AND 2009 CONTENTS REPORT OF INDEPENDENT PUBLIC ACCOUNTANTS 1 FINANCIAL STATEMENTS Consolidated Statements of Financial Position 2

Consolidated Statements of Activities and Changes in Net Assets 3 Consolidated Statements of Cash Flows 4 Consolidated Statements of Functional Expenses 5 Notes to the Consolidated Financial Statements 7

1776 I Street • 9th Floor • Washington, DC 20006 • P 202-756-4811 • F 202-756-1301

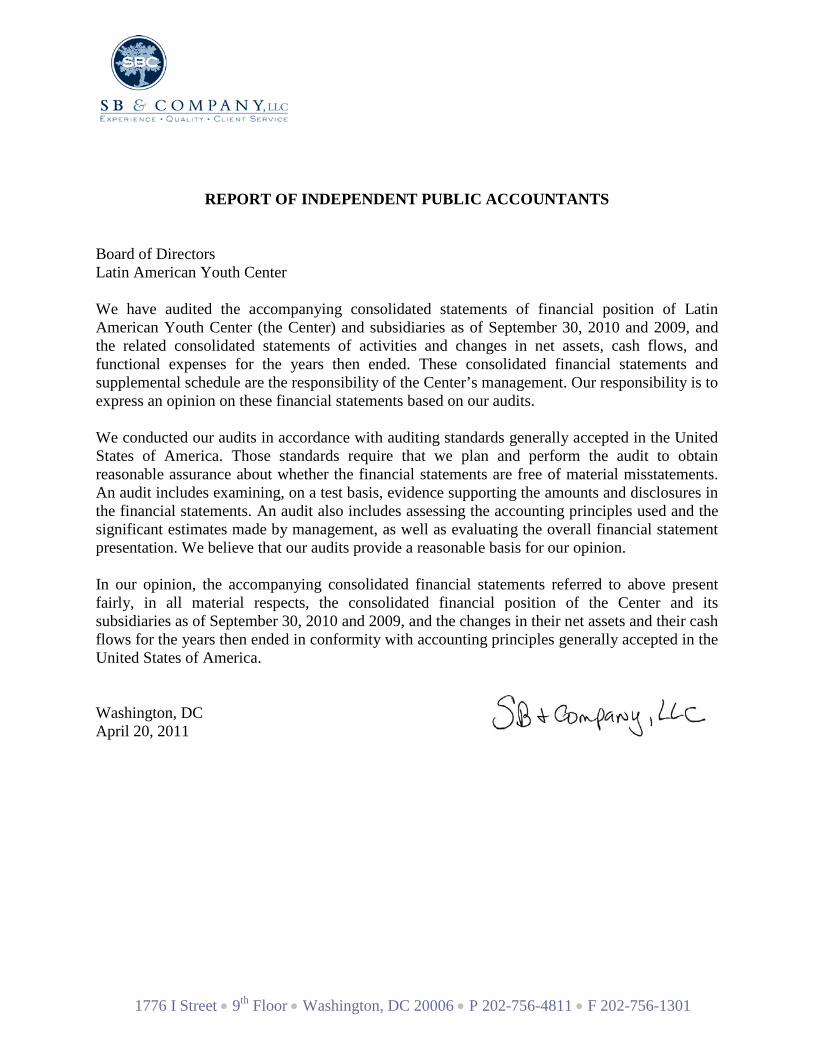

REPORT OF INDEPENDENT PUBLIC ACCOUNTANTS

Board of Directors Latin American Youth Center We have audited the accompanying consolidated statements of financial position of Latin American Youth Center (the Center) and subsidiaries as of September 30, 2010 and 2009, and the related consolidated statements of activities and changes in net assets, cash flows, and functional expenses for the years then ended. These consolidated financial statements and supplemental schedule are the responsibility of the Center’s management. Our responsibility is to express an opinion on these financial statements based on our audits. We conducted our audits in accordance with auditing standards generally accepted in the United States of America. Those standards require that we plan and perform the audit to obtain reasonable assurance about whether the financial statements are free of material misstatements. An audit includes examining, on a test basis, evidence supporting the amounts and disclosures in the financial statements. An audit also includes assessing the accounting principles used and the significant estimates made by management, as well as evaluating the overall financial statement presentation. We believe that our audits provide a reasonable basis for our opinion. In our opinion, the accompanying consolidated financial statements referred to above present fairly, in all material respects, the consolidated financial position of the Center and its subsidiaries as of September 30, 2010 and 2009, and the changes in their net assets and their cash flows for the years then ended in conformity with accounting principles generally accepted in the United States of America. Washington, DC April 20, 2011

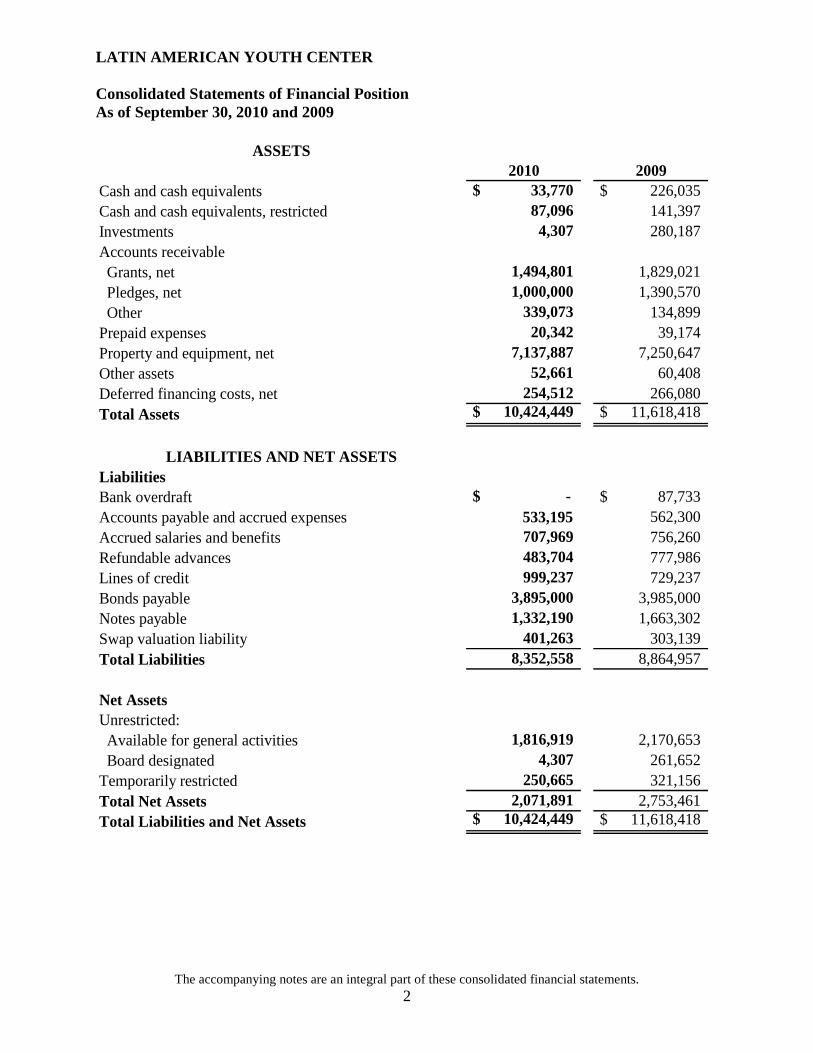

LATIN AMERICAN YOUTH CENTER Consolidated Statements of Financial Position As of September 30, 2010 and 2009

The accompanying notes are an integral part of these consolidated financial statements. 2

ASSETS

2010 2009Cash and cash equivalents $ 33,770 $ 226,035 Cash and cash equivalents, restricted 87,096 141,397 Investments 4,307 280,187 Accounts receivable Grants, net 1,494,801 1,829,021 Pledges, net 1,000,000 1,390,570 Other 339,073 134,899 Prepaid expenses 20,342 39,174 Property and equipment, net 7,137,887 7,250,647 Other assets 52,661 60,408 Deferred financing costs, net 254,512 266,080 Total Assets $ 10,424,449 $ 11,618,418

LIABILITIES AND NET ASSETSLiabilitiesBank overdraft $ - $ 87,733 Accounts payable and accrued expenses 533,195 562,300 Accrued salaries and benefits 707,969 756,260 Refundable advances 483,704 777,986 Lines of credit 999,237 729,237 Bonds payable 3,895,000 3,985,000 Notes payable 1,332,190 1,663,302 Swap valuation liability 401,263 303,139 Total Liabilities 8,352,558 8,864,957

Net AssetsUnrestricted: Available for general activities 1,816,919 2,170,653 Board designated 4,307 261,652 Temporarily restricted 250,665 321,156 Total Net Assets 2,071,891 2,753,461 Total Liabilities and Net Assets $ 10,424,449 $ 11,618,418

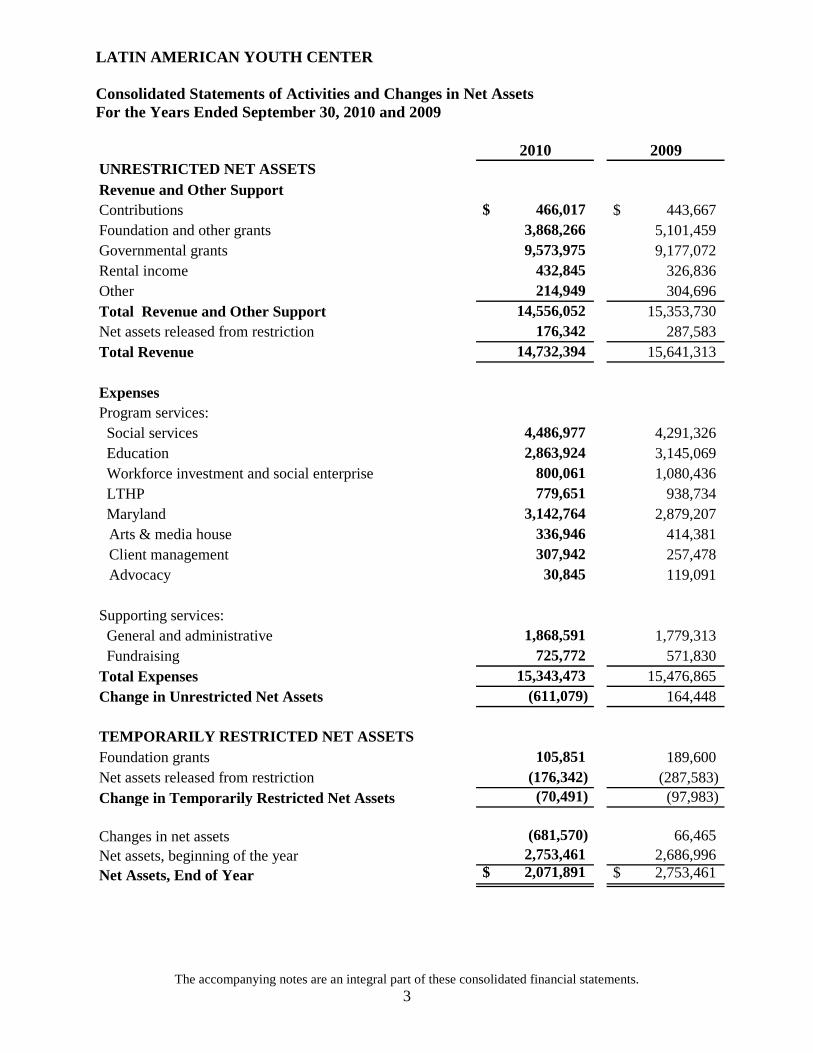

LATIN AMERICAN YOUTH CENTER Consolidated Statements of Activities and Changes in Net Assets For the Years Ended September 30, 2010 and 2009

The accompanying notes are an integral part of these consolidated financial statements. 3

2010 2009

UNRESTRICTED NET ASSETSRevenue and Other SupportContributions $ 466,017 $ 443,667 Foundation and other grants 3,868,266 5,101,459 Governmental grants 9,573,975 9,177,072 Rental income 432,845 326,836 Other 214,949 304,696 Total Revenue and Other Support 14,556,052 15,353,730 Net assets released from restriction 176,342 287,583 Total Revenue 14,732,394 15,641,313

ExpensesProgram services: Social services 4,486,977 4,291,326 Education 2,863,924 3,145,069 Workforce investment and social enterprise 800,061 1,080,436 LTHP 779,651 938,734 Maryland 3,142,764 2,879,207

Arts & media house 336,946 414,381 Client management 307,942 257,478 Advocacy 30,845 119,091

Supporting services: General and administrative 1,868,591 1,779,313 Fundraising 725,772 571,830 Total Expenses 15,343,473 15,476,865 Change in Unrestricted Net Assets (611,079) 164,448

TEMPORARILY RESTRICTED NET ASSETSFoundation grants 105,851 189,600 Net assets released from restriction (176,342) (287,583)Change in Temporarily Restricted Net Assets (70,491) (97,983)

Changes in net assets (681,570) 66,465 Net assets, beginning of the year 2,753,461 2,686,996 Net Assets, End of Year $ 2,071,891 $ 2,753,461

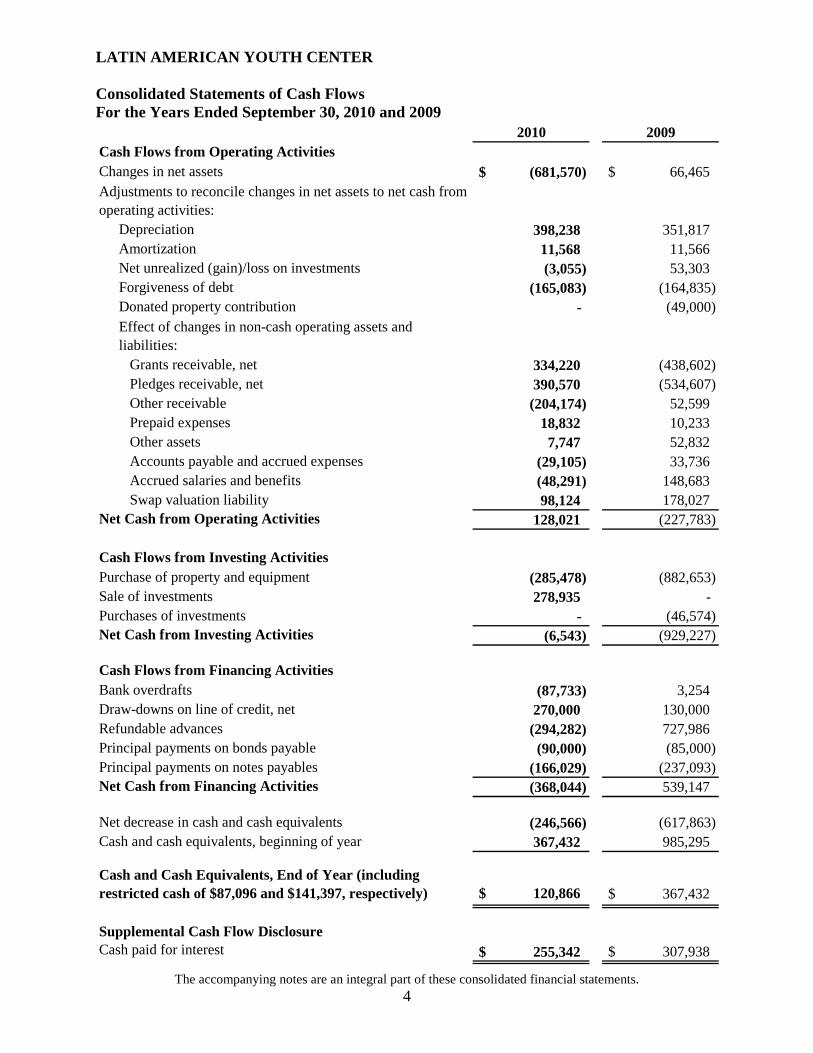

LATIN AMERICAN YOUTH CENTER Consolidated Statements of Cash Flows For the Years Ended September 30, 2010 and 2009

The accompanying notes are an integral part of these consolidated financial statements. 4

2010 2009Cash Flows from Operating ActivitiesChanges in net assets $ (681,570) $ 66,465 Adjustments to reconcile changes in net assets to net cash from operating activities:

Depreciation 398,238 351,817 Amortization 11,568 11,566 Net unrealized (gain)/loss on investments (3,055) 53,303 Forgiveness of debt (165,083) (164,835)Donated property contribution - (49,000)Effect of changes in non-cash operating assets and liabilities: Grants receivable, net 334,220 (438,602) Pledges receivable, net 390,570 (534,607) Other receivable (204,174) 52,599 Prepaid expenses 18,832 10,233 Other assets 7,747 52,832 Accounts payable and accrued expenses (29,105) 33,736 Accrued salaries and benefits (48,291) 148,683 Swap valuation liability 98,124 178,027

Net Cash from Operating Activities 128,021 (227,783)

Cash Flows from Investing ActivitiesPurchase of property and equipment (285,478) (882,653)Sale of investments 278,935 - Purchases of investments - (46,574)Net Cash from Investing Activities (6,543) (929,227)

Cash Flows from Financing ActivitiesBank overdrafts (87,733) 3,254 Draw-downs on line of credit, net 270,000 130,000 Refundable advances (294,282) 727,986 Principal payments on bonds payable (90,000) (85,000)Principal payments on notes payables (166,029) (237,093)Net Cash from Financing Activities (368,044) 539,147

Net decrease in cash and cash equivalents (246,566) (617,863)Cash and cash equivalents, beginning of year 367,432 985,295

Cash and Cash Equivalents, End of Year (including restricted cash of $87,096 and $141,397, respectively) $ 120,866 $ 367,432

Supplemental Cash Flow DisclosureCash paid for interest $ 255,342 $ 307,938

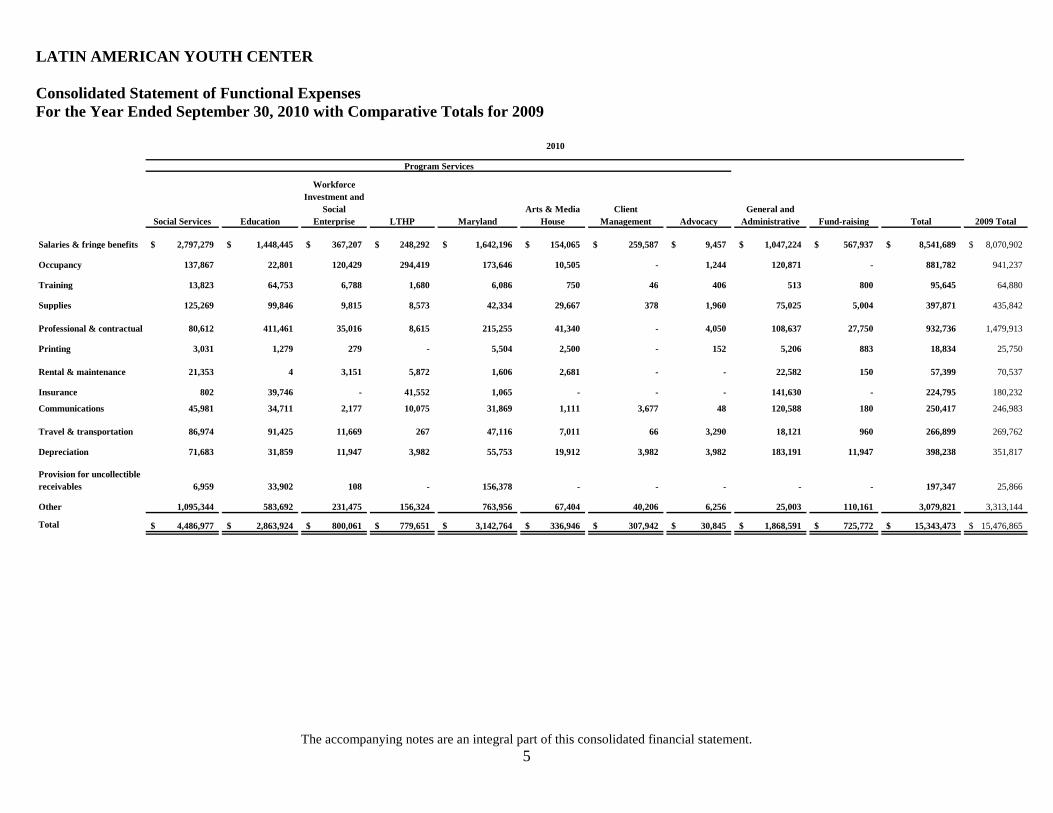

LATIN AMERICAN YOUTH CENTER Consolidated Statement of Functional Expenses For the Year Ended September 30, 2010 with Comparative Totals for 2009

The accompanying notes are an integral part of this consolidated financial statement. 5

Social Services Education

Workforce Investment and

Social Enterprise LTHP Maryland

Arts & Media House

Client Management Advocacy

General and Administrative Fund-raising Total 2009 Total

Salaries & fringe benefits 2,797,279$ 1,448,445$ 367,207$ 248,292$ 1,642,196$ 154,065$ 259,587$ 9,457$ 1,047,224$ 567,937$ 8,541,689$ 8,070,902$

Occupancy 137,867 22,801 120,429 294,419 173,646 10,505 - 1,244 120,871 - 881,782 941,237

Training 13,823 64,753 6,788 1,680 6,086 750 46 406 513 800 95,645 64,880

Supplies 125,269 99,846 9,815 8,573 42,334 29,667 378 1,960 75,025 5,004 397,871 435,842

Professional & contractual 80,612 411,461 35,016 8,615 215,255 41,340 - 4,050 108,637 27,750 932,736 1,479,913

Printing 3,031 1,279 279 - 5,504 2,500 - 152 5,206 883 18,834 25,750

Rental & maintenance 21,353 4 3,151 5,872 1,606 2,681 - - 22,582 150 57,399 70,537

Insurance 802 39,746 - 41,552 1,065 - - - 141,630 - 224,795 180,232

Communications 45,981 34,711 2,177 10,075 31,869 1,111 3,677 48 120,588 180 250,417 246,983

Travel & transportation 86,974 91,425 11,669 267 47,116 7,011 66 3,290 18,121 960 266,899 269,762

Depreciation 71,683 31,859 11,947 3,982 55,753 19,912 3,982 3,982 183,191 11,947 398,238 351,817

Provision for uncollectible receivables 6,959 33,902 108 - 156,378 - - - - - 197,347 25,866

Other 1,095,344 583,692 231,475 156,324 763,956 67,404 40,206 6,256 25,003 110,161 3,079,821 3,313,144

Total 4,486,977$ 2,863,924$ 800,061$ 779,651$ 3,142,764$ 336,946$ 307,942$ 30,845$ 1,868,591$ 725,772$ 15,343,473$ 15,476,865$

2010

Program Services

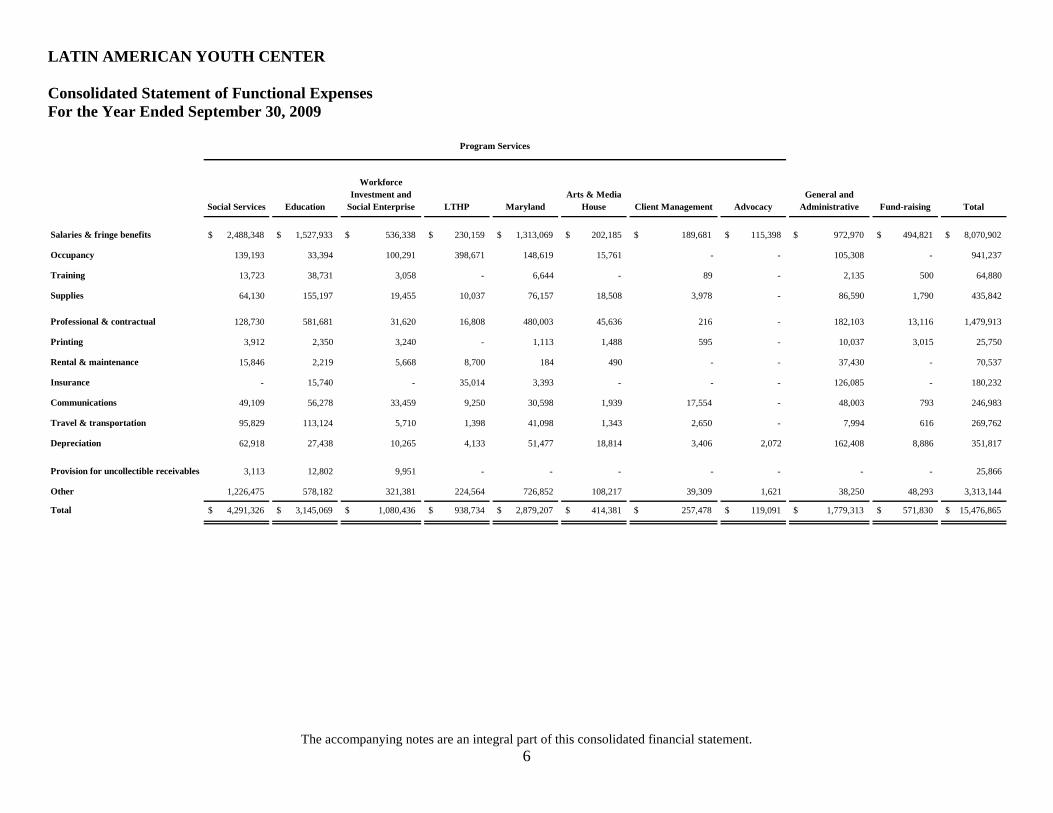

LATIN AMERICAN YOUTH CENTER Consolidated Statement of Functional Expenses For the Year Ended September 30, 2009

The accompanying notes are an integral part of this consolidated financial statement. 6

Social Services Education

Workforce Investment and

Social Enterprise LTHP MarylandArts & Media

House Client Management AdvocacyGeneral and

Administrative Fund-raising Total

Salaries & fringe benefits $ 2,488,348 $ 1,527,933 $ 536,338 $ 230,159 $ 1,313,069 $ 202,185 $ 189,681 $ 115,398 $ 972,970 $ 494,821 $ 8,070,902

Occupancy 139,193 33,394 100,291 398,671 148,619 15,761 - - 105,308 - 941,237

Training 13,723 38,731 3,058 - 6,644 - 89 - 2,135 500 64,880

Supplies 64,130 155,197 19,455 10,037 76,157 18,508 3,978 - 86,590 1,790 435,842

Professional & contractual 128,730 581,681 31,620 16,808 480,003 45,636 216 - 182,103 13,116 1,479,913

Printing 3,912 2,350 3,240 - 1,113 1,488 595 - 10,037 3,015 25,750

Rental & maintenance 15,846 2,219 5,668 8,700 184 490 - - 37,430 - 70,537

Insurance - 15,740 - 35,014 3,393 - - - 126,085 - 180,232

Communications 49,109 56,278 33,459 9,250 30,598 1,939 17,554 - 48,003 793 246,983

Travel & transportation 95,829 113,124 5,710 1,398 41,098 1,343 2,650 - 7,994 616 269,762

Depreciation 62,918 27,438 10,265 4,133 51,477 18,814 3,406 2,072 162,408 8,886 351,817

Provision for uncollectible receivables 3,113 12,802 9,951 - - - - - - - 25,866

Other 1,226,475 578,182 321,381 224,564 726,852 108,217 39,309 1,621 38,250 48,293 3,313,144

Total $ 4,291,326 $ 3,145,069 $ 1,080,436 $ 938,734 $ 2,879,207 $ 414,381 $ 257,478 $ 119,091 $ 1,779,313 $ 571,830 $ 15,476,865

Program Services

LATIN AMERICAN YOUTH CENTER Notes to the Consolidated Financial Statements September 30, 2010 and 2009

7

1. BACKGROUND OF THE ORGANIZATION

The Latin American Youth Center (the Center) was organized under the laws of the District of Columbia as a not-for-profit corporation. The Center’s purpose is to provide Latino, African-American and other multicultural youth and families with the education, skills, training and support they need to live, work and study with dignity, in good health and in neighborhoods that are safe and secure. The Center is related to “LAYC Creative Enterprises, Inc.,” (CEI) doing business as Ben and Jerry’s Ice Cream. CEI was incorporated on November 7, 2001 in the District of Columbia as a not-for-profit organization. CEI had received an exemption from Federal income taxation from the Internal Revenue Service. The Center appointed the Board of Directors of CEI. The CEI Board of Directors elected its own Chairman and officers. The Center had passed through the proceeds from certain notes payable to CEI. CEI ceased operation in 2009. The Center has also established the LAYC Social Ventures, Inc. (Social Ventures) to operate a second Ben and Jerry’s Ice Cream in Washington, DC. The Center appointed the Board of Directors of Social Ventures. The Social Ventures Board of Directors elected its own Chairman and officers. Social Ventures ceased operation in 2010. The financial statements of the operations of the CEI and Social Ventures as of and for the years ended September 30, 2010 and 2009, have been consolidated into the Center’s financial statements in accordance with Financial Accounting Standards Board (FASB) Accounting Standards Codification (ASC) Topic 958 Not-for-Profit Entities. Intercompany balances and transactions have been eliminated in the accompanying consolidated financial statements.

2. SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES

Basis of Accounting

The accompanying consolidated financial statements of the Center are presented on the accrual basis of accounting in accordance with accounting principles generally accepted in the United States of America. Use of Estimates

The preparation of financial statements in conformity with accounting principles generally accepted in the United States of America requires the Center’s management to make estimates and assumptions that affect the reported amounts of assets and liabilities and disclosure of contingent assets and liabilities as of the date of the consolidated financial statements and the reported amounts of support and revenue and expenses during the reporting period. Actual results could differ from those estimates.

LATIN AMERICAN YOUTH CENTER Notes to the Consolidated Financial Statements September 30, 2010 and 2009

8

2. SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES (continued) Cash and Cash Equivalents

Cash and cash equivalents include amounts invested in short-term investments with original maturities of three months or less. Cash equivalents as of September 30, 2010 and 2009, consisted of overnight investment accounts and money market funds. Restricted cash of $87,096 and $83,256 was held in a sinking fund account for debt service related to bonds payables as of September 30, 2010 and 2009, respectively. As of September 30, 2009, restricted cash of $58,141 was remaining funds from bond proceeds, restricted for the purpose of renovating property purchased by the Center in 2007. Fair Value Measurement

FASB ASC Topic 820, Fair Value Measurements and Disclosures, establishes a framework for measuring fair value. That framework provides a fair value hierarchy that prioritizes the inputs to valuation techniques used to measure fair value. The hierarchy gives the highest priority to unadjusted quoted prices in active markets for identical assets or liabilities (Level 1 measurements) and the lowest priority to unobservable inputs (Level 3 measurements). The three levels of the fair value hierarchy under FASB ASC Topic 820 are described below: Level 1 Inputs to the valuation methodology are unadjusted quoted prices for identical

assets or liabilities in active markets that the Center has the ability to access.

Level 2 Inputs to the valuation methodology include: • quoted prices for similar assets or liabilities in active markets; • quoted prices for identical or similar assets or liabilities in inactive

markets; • inputs other than quoted prices that are observable for the asset or liability;

and • inputs that are derived principally from or corroborated by observable

market data by correlation or other means. If the asset or liability has a specified (contractual) term, the Level 2 input must be observable for substantially the full term of the asset or liability.

Level 3 Inputs to the valuation methodology are unobservable and significant to the fair value measurement.

The asset’s or liability’s fair value measurement level within the fair value hierarchy is based on the lowest level of any input that is significant to the fair value measurement. Valuation techniques used need to maximize the use of observable inputs and minimize the use of unobservable inputs.

LATIN AMERICAN YOUTH CENTER Notes to the Consolidated Financial Statements September 30, 2010 and 2009

9

2. SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES (continued)

Accounts Receivable

Receivables are valued at management’s estimate of the amount that will ultimately be collected. The allowance for doubtful accounts is based on specific identification of uncollectible accounts and the Center’s historical collection experience. As of September 30, 2010 and 2009, the allowance was $60,574 and $60,574, respectively.

Pledges Receivable For pledges expected to be collected in over one year, the Center discounts those pledges using a 2.77% discount rate for the year ended September 30, 2009, respectively. The rate is based on the Center’s borrowing rate as of the balance sheet date. Management expects to fully collect all of its pledges and thus no reserve has been recorded as of September 30, 2010 and 2009.

Deferred Financing Costs Deferred financing costs consist of costs related to the bonds issued to purchase and renovate property. The deferred financing costs of $286,826 will be amortized using the effective interest method over the life of the debt. The Center recorded $11,568 and $11,566 in amortization expense during the years ended September 30, 2010 and 2009, respectively, and recorded these amounts as other expenses in the accompanying consolidated statements of functional expenses. Property and Equipment

Property and equipment purchases are recorded at cost. Donated property and equipment are capitalized at the estimated fair market value on the date received. Depreciation of property and equipment is recorded using the straight-line method over the estimated useful life of the assets. Net Assets

Unrestricted net assets are assets and contributions that are not restricted by donors or for which restrictions have expired. The Board has designated $4,307 and $261,652 as a future working capital reserve as of September 30, 2010 and 2009, respectively.

LATIN AMERICAN YOUTH CENTER Notes to the Consolidated Financial Statements September 30, 2010 and 2009

10

2. SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES (continued) Net Assets (continued) Temporarily restricted net assets are those whose use by the Center has been limited by donors, primarily for a specific time period or purpose. When a donor restriction is met, temporarily restricted net assets are reclassified to unrestricted net assets. If a donor restriction is met in the same reporting period in which the contribution is received, the contribution (to the extent that the restrictions have been met) is reported as unrestricted net assets. Permanently restricted net assets are those that are restricted by donors to be maintained by the Center in perpetuity. There are no permanently restricted net assets as of September 30, 2010 and 2009. Restricted and Unrestricted Support and Revenue

Contributions received are recorded as unrestricted or temporarily restricted support, depending on the existence and/or nature of any donor imposed restrictions. Donor-restricted support is reported as an increase in temporarily restricted net assets, depending on the nature of the restriction. Gifts of cash and other assets are reported as restricted support if they are received with donor stipulations that limit the use of the donated assets. When a donor restriction expires, that is, when the stipulated time restriction ends or purpose of the restriction is accomplished, temporarily restricted net assets are reclassified to unrestricted net assets and reported in the accompanying consolidated statements of activities and changes in net assets as net assets released from restrictions. Functional Allocation of Expenses

The costs of providing the various programs and other activities have been summarized on a functional basis in the accompanying consolidated statements of activities and changes in net assets and in the consolidated statements of functional expenses. Accordingly, certain costs have been allocated among the programs and supporting services that benefit from those costs. General and management expenses include those expenses that are not directly identified with any other specific function but provide for the overall support and direction of the Center.

LATIN AMERICAN YOUTH CENTER Notes to the Consolidated Financial Statements September 30, 2010 and 2009

11

2. SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES (continued) Income Taxes The Center is a not-for-profit organization exempt from Federal income other than net unrelated business income tax under Section 501(c)(3) of the Internal Revenue Code and is recognized as such by the Internal Revenue Service. Effective October 1, 2009, the Center adopted the authoritative guidance relating to accounting for uncertainty in income taxes included in FASB ASC Topic 740, Income Taxes. These provisions provide consistent guidance for the accounting for uncertainty in income taxes recognized in an entity’s financial statements and prescribe a threshold of “more likely than not” for recognition of tax positions taken or expected to be taken in a tax return. The Center performed an evaluation of uncertain tax positions for the year ended September 30, 2010, and determined that there were no matters that would require recognition in the financial statements or which may have any effect on its tax-exempt status. For the year ended September 30, 2010, the statute of limitations for tax years 2007 through 2009 remains open with the U.S. federal jurisdiction or the various states and local jurisdictions in which the Center files tax returns. It is the Center’s policy to recognize interest and/or penalties related to uncertain tax positions, if any, in income tax expense. Subsequent Events The Center evaluated the accompanying consolidated financial statements subsequent events and transactions through April 20, 2011, the date the consolidated financial statements were available for issue and have determined that no material subsequent events have occurred that would affect the information presented in the accompanying consolidated financial statements or require additional disclosure. Reclassification

Certain 2009 amounts have been reclassified to conform to the 2010 financial statement presentation.

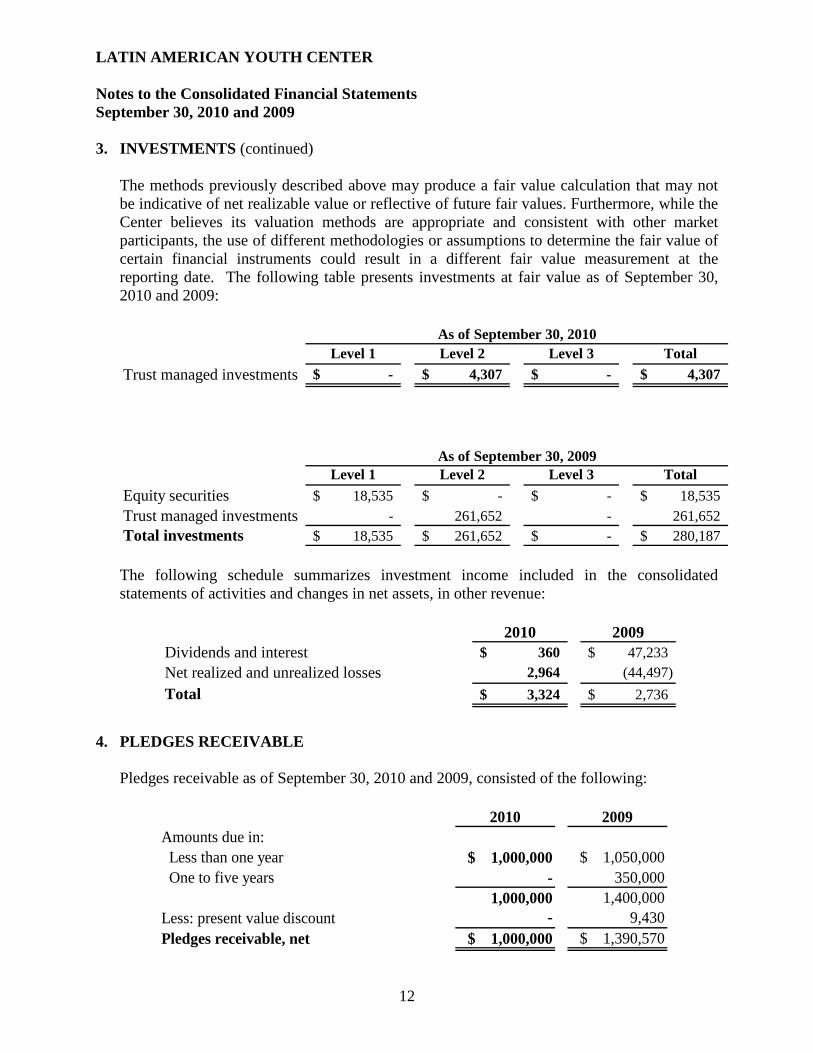

3. INVESTMENTS The following is a description of the valuation methodologies used for investments measured at fair value. Equity securities: Valued at the closing price reported on the active market on which the individual securities are traded. Trust managed investments: Valued on underlying investments of the fund as valued by the fund’s management.

LATIN AMERICAN YOUTH CENTER Notes to the Consolidated Financial Statements September 30, 2010 and 2009

12

3. INVESTMENTS (continued) The methods previously described above may produce a fair value calculation that may not be indicative of net realizable value or reflective of future fair values. Furthermore, while the Center believes its valuation methods are appropriate and consistent with other market participants, the use of different methodologies or assumptions to determine the fair value of certain financial instruments could result in a different fair value measurement at the reporting date. The following table presents investments at fair value as of September 30, 2010 and 2009:

Level 1 Level 2 Level 3 TotalTrust managed investments -$ 4,307$ -$ 4,307$

As of September 30, 2010

Level 1 Level 2 Level 3 TotalEquity securities 18,535$ -$ -$ 18,535$ Trust managed investments - 261,652 - 261,652 Total investments 18,535$ 261,652$ -$ 280,187$

As of September 30, 2009

The following schedule summarizes investment income included in the consolidated statements of activities and changes in net assets, in other revenue:

2010 2009Dividends and interest 360$ 47,233$ Net realized and unrealized losses 2,964 (44,497) Total 3,324$ 2,736$

4. PLEDGES RECEIVABLE Pledges receivable as of September 30, 2010 and 2009, consisted of the following:

2010 2009

Amounts due in: Less than one year $ 1,000,000 $ 1,050,000 One to five years - 350,000

1,000,000 1,400,000 Less: present value discount - 9,430 Pledges receivable, net $ 1,000,000 $ 1,390,570

LATIN AMERICAN YOUTH CENTER Notes to the Consolidated Financial Statements September 30, 2010 and 2009

13

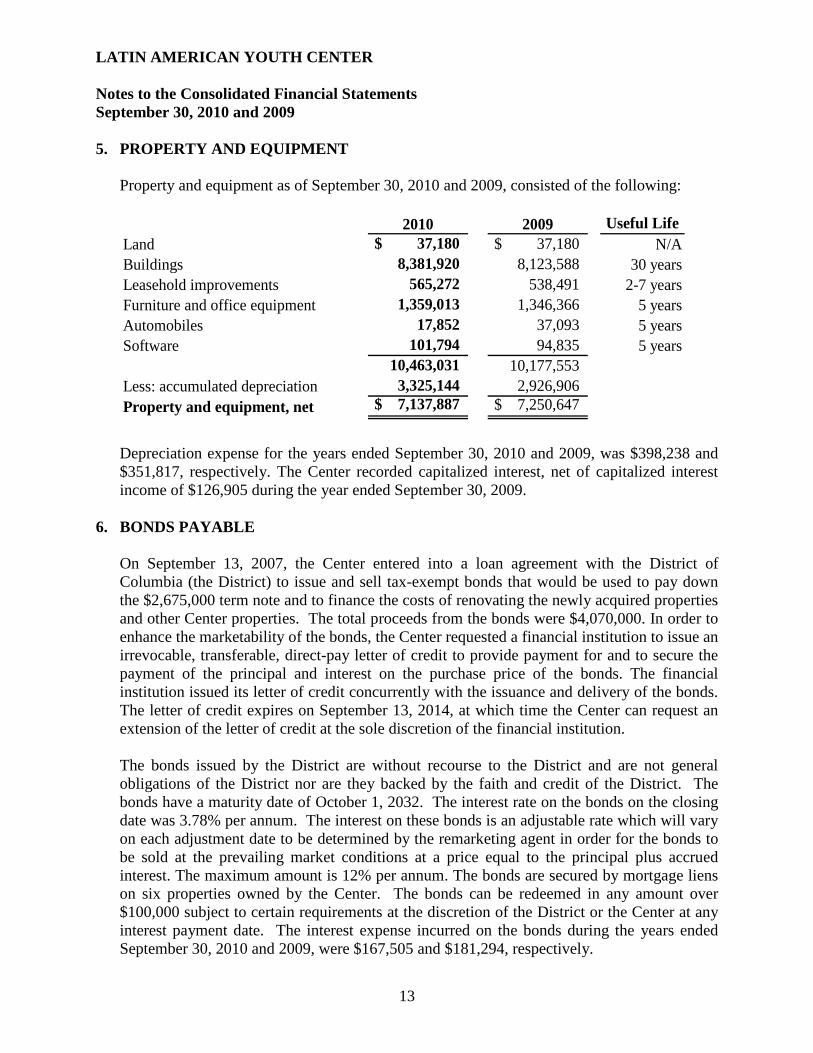

5. PROPERTY AND EQUIPMENT

Property and equipment as of September 30, 2010 and 2009, consisted of the following:

2010 2009 Useful LifeLand $ 37,180 $ 37,180 N/ABuildings 8,381,920 8,123,588 30 yearsLeasehold improvements 565,272 538,491 2-7 yearsFurniture and office equipment 1,359,013 1,346,366 5 yearsAutomobiles 17,852 37,093 5 yearsSoftware 101,794 94,835 5 years

10,463,031 10,177,553 Less: accumulated depreciation 3,325,144 2,926,906 Property and equipment, net $ 7,137,887 $ 7,250,647

Depreciation expense for the years ended September 30, 2010 and 2009, was $398,238 and $351,817, respectively. The Center recorded capitalized interest, net of capitalized interest income of $126,905 during the year ended September 30, 2009.

6. BONDS PAYABLE On September 13, 2007, the Center entered into a loan agreement with the District of Columbia (the District) to issue and sell tax-exempt bonds that would be used to pay down the $2,675,000 term note and to finance the costs of renovating the newly acquired properties and other Center properties. The total proceeds from the bonds were $4,070,000. In order to enhance the marketability of the bonds, the Center requested a financial institution to issue an irrevocable, transferable, direct-pay letter of credit to provide payment for and to secure the payment of the principal and interest on the purchase price of the bonds. The financial institution issued its letter of credit concurrently with the issuance and delivery of the bonds. The letter of credit expires on September 13, 2014, at which time the Center can request an extension of the letter of credit at the sole discretion of the financial institution. The bonds issued by the District are without recourse to the District and are not general obligations of the District nor are they backed by the faith and credit of the District. The bonds have a maturity date of October 1, 2032. The interest rate on the bonds on the closing date was 3.78% per annum. The interest on these bonds is an adjustable rate which will vary on each adjustment date to be determined by the remarketing agent in order for the bonds to be sold at the prevailing market conditions at a price equal to the principal plus accrued interest. The maximum amount is 12% per annum. The bonds are secured by mortgage liens on six properties owned by the Center. The bonds can be redeemed in any amount over $100,000 subject to certain requirements at the discretion of the District or the Center at any interest payment date. The interest expense incurred on the bonds during the years ended September 30, 2010 and 2009, were $167,505 and $181,294, respectively.

LATIN AMERICAN YOUTH CENTER Notes to the Consolidated Financial Statements September 30, 2010 and 2009

14

6. BONDS PAYABLE (continued)

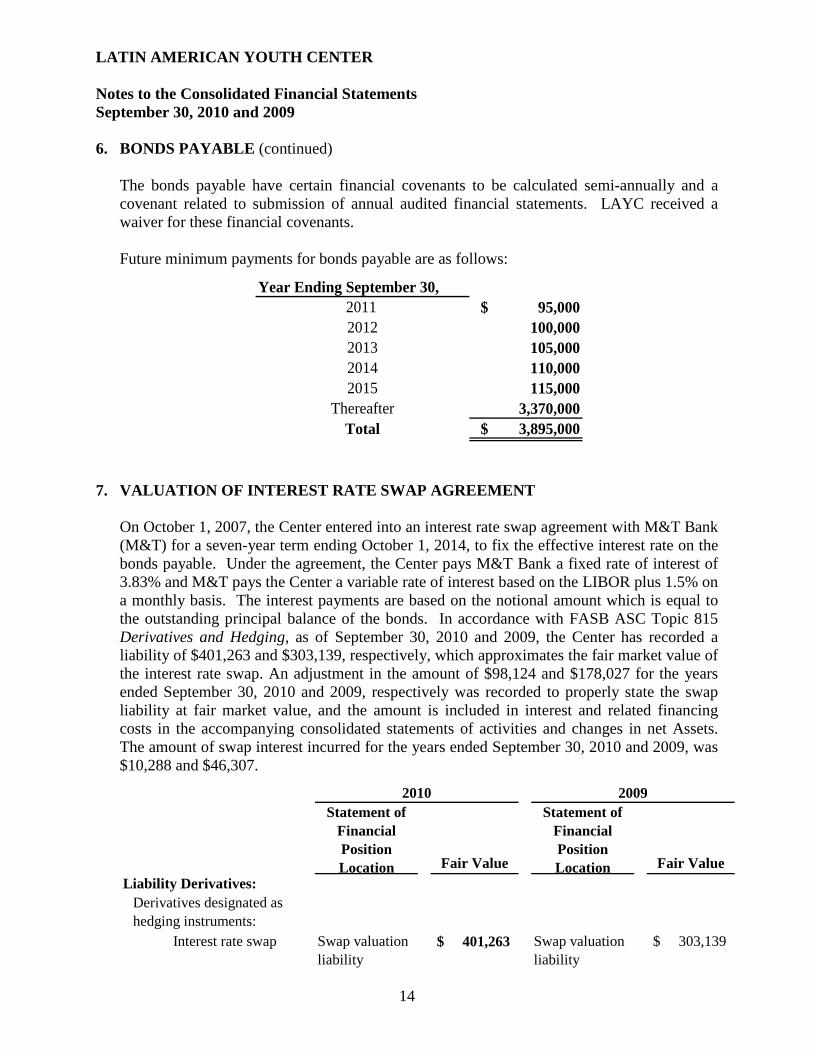

The bonds payable have certain financial covenants to be calculated semi-annually and a covenant related to submission of annual audited financial statements. LAYC received a waiver for these financial covenants.

Future minimum payments for bonds payable are as follows:

Year Ending September 30,2011 $ 95,000 2012 100,000 2013 105,000 2014 110,000 2015 115,000

Thereafter 3,370,000 Total $ 3,895,000

7. VALUATION OF INTEREST RATE SWAP AGREEMENT

On October 1, 2007, the Center entered into an interest rate swap agreement with M&T Bank (M&T) for a seven-year term ending October 1, 2014, to fix the effective interest rate on the bonds payable. Under the agreement, the Center pays M&T Bank a fixed rate of interest of 3.83% and M&T pays the Center a variable rate of interest based on the LIBOR plus 1.5% on a monthly basis. The interest payments are based on the notional amount which is equal to the outstanding principal balance of the bonds. In accordance with FASB ASC Topic 815 Derivatives and Hedging, as of September 30, 2010 and 2009, the Center has recorded a liability of $401,263 and $303,139, respectively, which approximates the fair market value of the interest rate swap. An adjustment in the amount of $98,124 and $178,027 for the years ended September 30, 2010 and 2009, respectively was recorded to properly state the swap liability at fair market value, and the amount is included in interest and related financing costs in the accompanying consolidated statements of activities and changes in net Assets. The amount of swap interest incurred for the years ended September 30, 2010 and 2009, was $10,288 and $46,307.

Statement of Financial Position Location Fair Value

Statement of Financial Position Location Fair Value

Liability Derivatives:Derivatives designated as hedging instruments:

Interest rate swap Swap valuation liability

$ 401,263 Swap valuation liability

$ 303,139

2010 2009

LATIN AMERICAN YOUTH CENTER Notes to the Consolidated Financial Statements September 30, 2010 and 2009

15

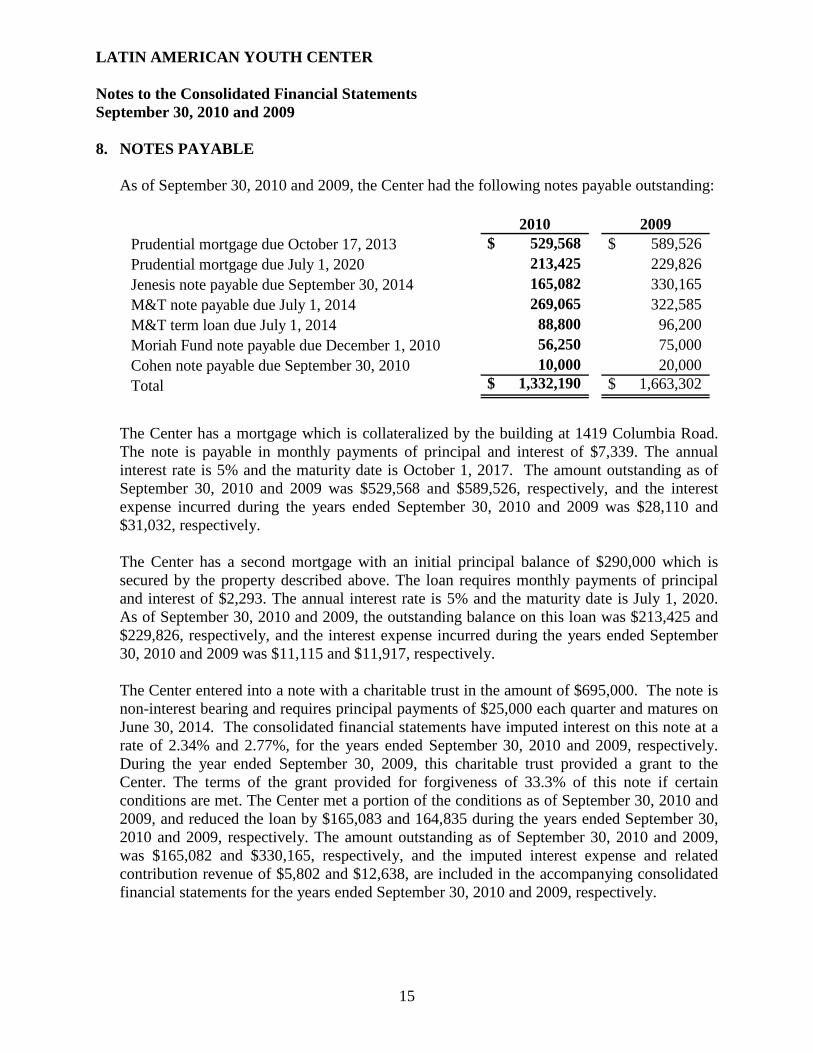

8. NOTES PAYABLE

As of September 30, 2010 and 2009, the Center had the following notes payable outstanding:

2010 2009Prudential mortgage due October 17, 2013 $ 529,568 $ 589,526 Prudential mortgage due July 1, 2020 213,425 229,826 Jenesis note payable due September 30, 2014 165,082 330,165 M&T note payable due July 1, 2014 269,065 322,585 M&T term loan due July 1, 2014 88,800 96,200 Moriah Fund note payable due December 1, 2010 56,250 75,000 Cohen note payable due September 30, 2010 10,000 20,000 Total $ 1,332,190 $ 1,663,302

The Center has a mortgage which is collateralized by the building at 1419 Columbia Road. The note is payable in monthly payments of principal and interest of $7,339. The annual interest rate is 5% and the maturity date is October 1, 2017. The amount outstanding as of September 30, 2010 and 2009 was $529,568 and $589,526, respectively, and the interest expense incurred during the years ended September 30, 2010 and 2009 was $28,110 and $31,032, respectively. The Center has a second mortgage with an initial principal balance of $290,000 which is secured by the property described above. The loan requires monthly payments of principal and interest of $2,293. The annual interest rate is 5% and the maturity date is July 1, 2020. As of September 30, 2010 and 2009, the outstanding balance on this loan was $213,425 and $229,826, respectively, and the interest expense incurred during the years ended September 30, 2010 and 2009 was $11,115 and $11,917, respectively. The Center entered into a note with a charitable trust in the amount of $695,000. The note is non-interest bearing and requires principal payments of $25,000 each quarter and matures on June 30, 2014. The consolidated financial statements have imputed interest on this note at a rate of 2.34% and 2.77%, for the years ended September 30, 2010 and 2009, respectively. During the year ended September 30, 2009, this charitable trust provided a grant to the Center. The terms of the grant provided for forgiveness of 33.3% of this note if certain conditions are met. The Center met a portion of the conditions as of September 30, 2010 and 2009, and reduced the loan by $165,083 and 164,835 during the years ended September 30, 2010 and 2009, respectively. The amount outstanding as of September 30, 2010 and 2009, was $165,082 and $330,165, respectively, and the imputed interest expense and related contribution revenue of $5,802 and $12,638, are included in the accompanying consolidated financial statements for the years ended September 30, 2010 and 2009, respectively.

LATIN AMERICAN YOUTH CENTER Notes to the Consolidated Financial Statements September 30, 2010 and 2009

16

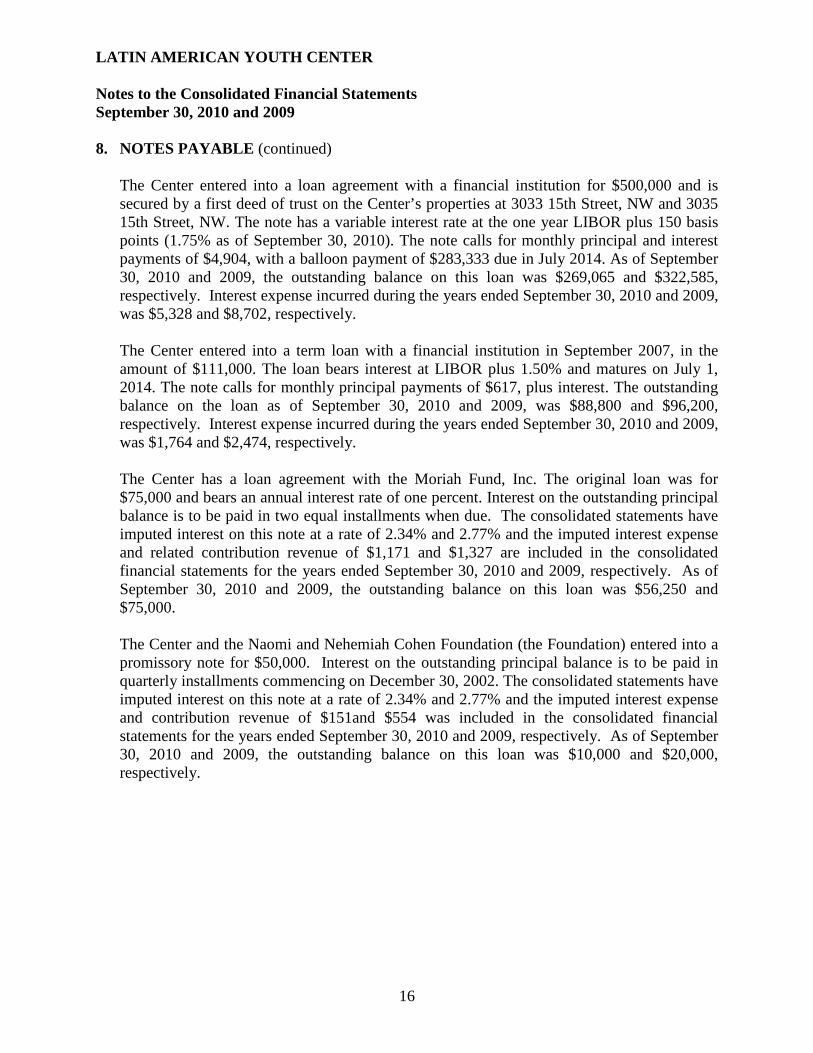

8. NOTES PAYABLE (continued)

The Center entered into a loan agreement with a financial institution for $500,000 and is secured by a first deed of trust on the Center’s properties at 3033 15th Street, NW and 3035 15th Street, NW. The note has a variable interest rate at the one year LIBOR plus 150 basis points (1.75% as of September 30, 2010). The note calls for monthly principal and interest payments of $4,904, with a balloon payment of $283,333 due in July 2014. As of September 30, 2010 and 2009, the outstanding balance on this loan was $269,065 and $322,585, respectively. Interest expense incurred during the years ended September 30, 2010 and 2009, was $5,328 and $8,702, respectively. The Center entered into a term loan with a financial institution in September 2007, in the amount of $111,000. The loan bears interest at LIBOR plus 1.50% and matures on July 1, 2014. The note calls for monthly principal payments of $617, plus interest. The outstanding balance on the loan as of September 30, 2010 and 2009, was $88,800 and $96,200, respectively. Interest expense incurred during the years ended September 30, 2010 and 2009, was $1,764 and $2,474, respectively. The Center has a loan agreement with the Moriah Fund, Inc. The original loan was for $75,000 and bears an annual interest rate of one percent. Interest on the outstanding principal balance is to be paid in two equal installments when due. The consolidated statements have imputed interest on this note at a rate of 2.34% and 2.77% and the imputed interest expense and related contribution revenue of $1,171 and $1,327 are included in the consolidated financial statements for the years ended September 30, 2010 and 2009, respectively. As of September 30, 2010 and 2009, the outstanding balance on this loan was $56,250 and $75,000. The Center and the Naomi and Nehemiah Cohen Foundation (the Foundation) entered into a promissory note for $50,000. Interest on the outstanding principal balance is to be paid in quarterly installments commencing on December 30, 2002. The consolidated statements have imputed interest on this note at a rate of 2.34% and 2.77% and the imputed interest expense and contribution revenue of $151and $554 was included in the consolidated financial statements for the years ended September 30, 2010 and 2009, respectively. As of September 30, 2010 and 2009, the outstanding balance on this loan was $10,000 and $20,000, respectively.

LATIN AMERICAN YOUTH CENTER Notes to the Consolidated Financial Statements September 30, 2010 and 2009

17

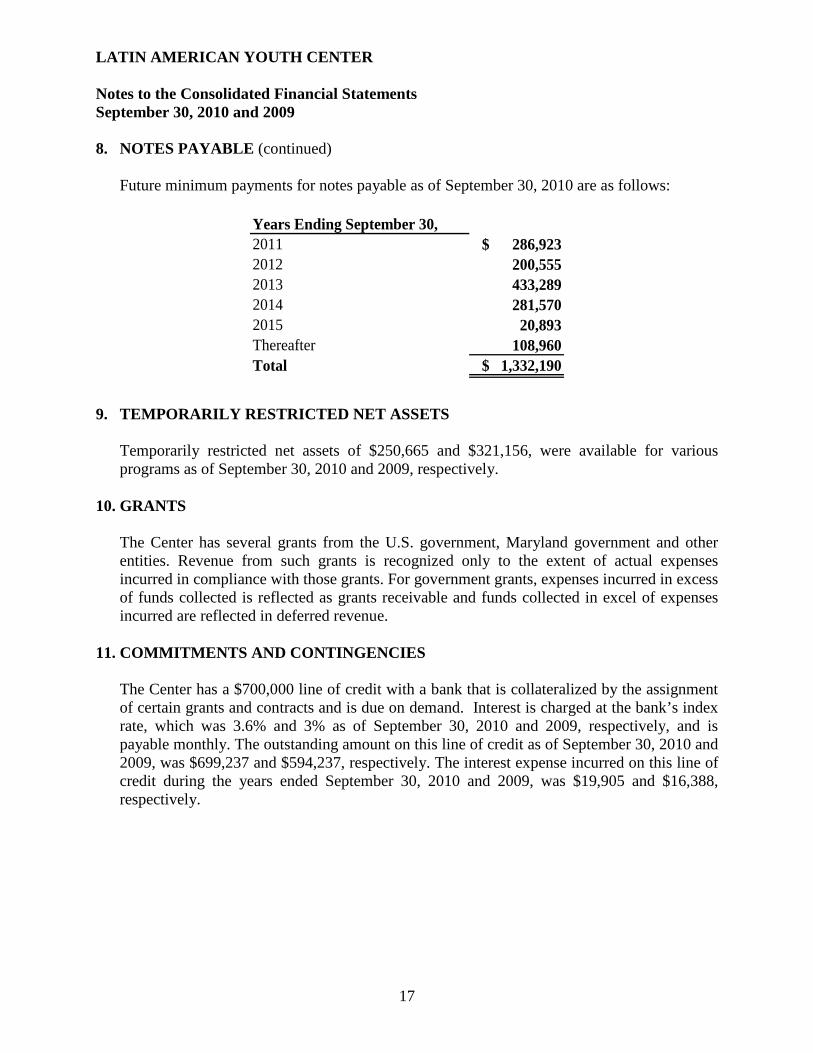

8. NOTES PAYABLE (continued) Future minimum payments for notes payable as of September 30, 2010 are as follows:

Years Ending September 30,2011 $ 286,923 2012 200,555 2013 433,289 2014 281,570 2015 20,893 Thereafter 108,960 Total $ 1,332,190

9. TEMPORARILY RESTRICTED NET ASSETS

Temporarily restricted net assets of $250,665 and $321,156, were available for various programs as of September 30, 2010 and 2009, respectively.

10. GRANTS

The Center has several grants from the U.S. government, Maryland government and other entities. Revenue from such grants is recognized only to the extent of actual expenses incurred in compliance with those grants. For government grants, expenses incurred in excess of funds collected is reflected as grants receivable and funds collected in excel of expenses incurred are reflected in deferred revenue.

11. COMMITMENTS AND CONTINGENCIES The Center has a $700,000 line of credit with a bank that is collateralized by the assignment of certain grants and contracts and is due on demand. Interest is charged at the bank’s index rate, which was 3.6% and 3% as of September 30, 2010 and 2009, respectively, and is payable monthly. The outstanding amount on this line of credit as of September 30, 2010 and 2009, was $699,237 and $594,237, respectively. The interest expense incurred on this line of credit during the years ended September 30, 2010 and 2009, was $19,905 and $16,388, respectively.

LATIN AMERICAN YOUTH CENTER Notes to the Consolidated Financial Statements September 30, 2010 and 2009

18

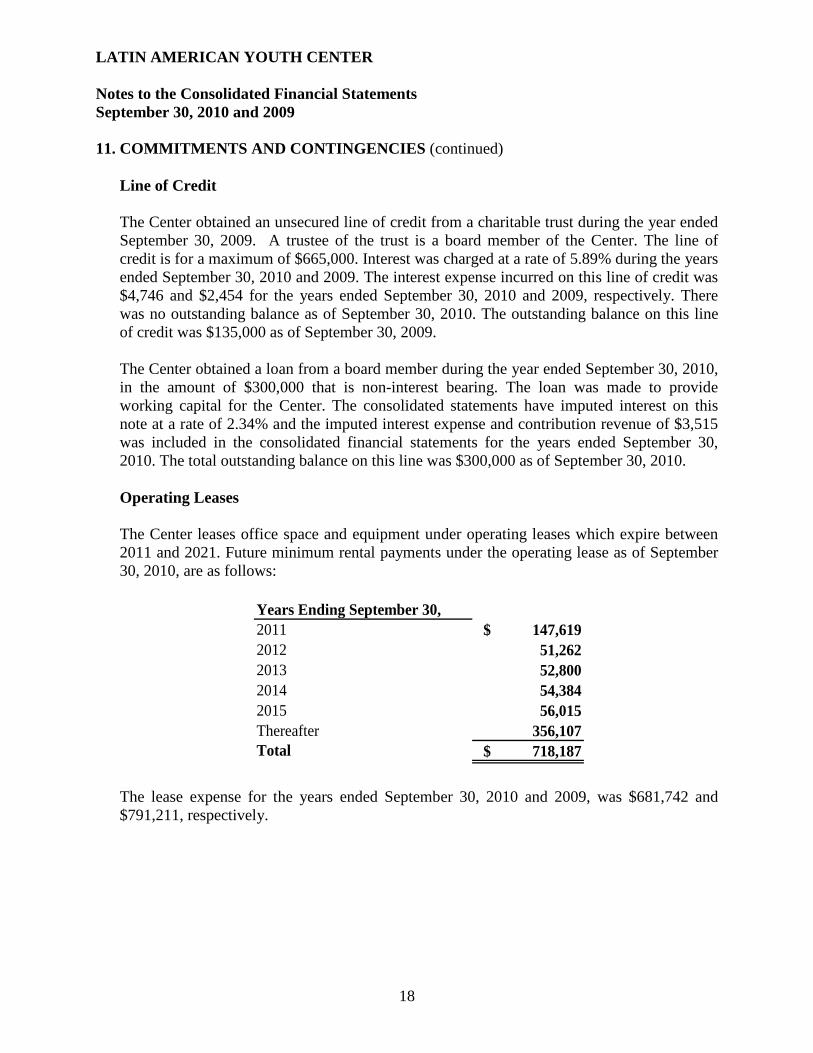

11. COMMITMENTS AND CONTINGENCIES (continued) Line of Credit The Center obtained an unsecured line of credit from a charitable trust during the year ended September 30, 2009. A trustee of the trust is a board member of the Center. The line of credit is for a maximum of $665,000. Interest was charged at a rate of 5.89% during the years ended September 30, 2010 and 2009. The interest expense incurred on this line of credit was $4,746 and $2,454 for the years ended September 30, 2010 and 2009, respectively. There was no outstanding balance as of September 30, 2010. The outstanding balance on this line of credit was $135,000 as of September 30, 2009. The Center obtained a loan from a board member during the year ended September 30, 2010, in the amount of $300,000 that is non-interest bearing. The loan was made to provide working capital for the Center. The consolidated statements have imputed interest on this note at a rate of 2.34% and the imputed interest expense and contribution revenue of $3,515 was included in the consolidated financial statements for the years ended September 30, 2010. The total outstanding balance on this line was $300,000 as of September 30, 2010. Operating Leases The Center leases office space and equipment under operating leases which expire between 2011 and 2021. Future minimum rental payments under the operating lease as of September 30, 2010, are as follows:

Years Ending September 30,2011 $ 147,619 2012 51,262 2013 52,800 2014 54,384 2015 56,015 Thereafter 356,107 Total $ 718,187

The lease expense for the years ended September 30, 2010 and 2009, was $681,742 and $791,211, respectively.

LATIN AMERICAN YOUTH CENTER Notes to the Consolidated Financial Statements September 30, 2010 and 2009

18

11. COMMITMENTS AND CONTINGENCIES (continued) Grants Reimbursed costs under the Center’s government awards are subject to final determination of allowability by the government agency. Until such audits have been completed and final settlement reached, there exists a contingency to refund any amount received in excess of allowable costs. Management is of the opinion that no material liability will result from such audits.

12. DEFINED CONTRIBUTION PLAN

The Center provides benefits to all eligible employees under a defined contribution plan at a rate determined annually by the Board of Directors. Eligible employees are able to contribute up to the annual Federal cap after completing 24 months of service at the Center. The employer contribution for the years ended September 30, 2010 and 2009, was $100,468 and $94,792, respectively.

13. RELATED-PARTY TRANSACTIONS The Center is related to “LAYC Creative Enterprises, Inc. (CEI),” doing business as Ben and Jerry’s Ice Cream. CEI was incorporated on November 7, 2001 in the District of Columbia as a nonprofit organization. CEI had received an exemption from Federal income taxation from the Internal Revenue Service. The Center appointed the Board of Directors of CEI. The CEI Board of Directors elected its own Chairman and officers. The Center contributed financially and had a financial interest in CEI. The Center loaned CEI $175,000 through a non-interest bearing loan. CEI ceased operations during fiscal year 2009 without repaying the loan. The $175,000 note was written off by the Center. The Center had also established the LAYC Social Ventures, Inc. (Social Ventures) to operate a second Ben and Jerry’s Ice Cream in Washington, DC. The Center appointed the Board of Directors of Social Ventures. The Social Ventures Board of Directors elected its own Chairman and officers. The Center contributed financially and had a financial interest in Social Ventures. The Center loaned Social Ventures $305,016 through a non-interest bearing loan. Social Ventures ceased operations during fiscal year 2010. The $305,016 loan was written off by the Center. Both CEI and Social Ventures are consolidated within the accompanying consolidated financial statements.

The Center is related to the Next Step Public Charter School (the Charter School). The Center appoints the Board of Trustees of the Charter School. The Charter School Board of Trustees elects its Chairman and President. The Charter School reimbursed the Center $161,175 and $135,982 for shared costs during the years ended September 30, 2010 and 2009, respectively.

LATIN AMERICAN YOUTH CENTER Notes to the Consolidated Financial Statements September 30, 2010 and 2009

19

13. RELATED-PARTY TRANSACTIONS (continued) On November 5, 2001, the Center was awarded a charter school contract by the District of Columbia Public Schools for the establishment of the Latin American Montessori Bilingual Public Charter School. A nonprofit organization similar to the Next Step Public Charter School has been formed to operate this school. There were no reimbursed costs to the Center for shared costs during the years ended September 30, 2010 and 2009. On October 7, 2004, the Center was awarded a charter school contract by the District of Columbia Public Schools for the establishment of the Youth Build Public Charter School. A nonprofit organization similar to the Next Step Public Charter School has been formed to operate this school. The Charter School reimbursed the Center $396,000 and $355,700 for shared costs during the years ended September 30, 2010 and 2009, respectively.

![Latin America 100 million youth with productivewhite.lim.ilo.org/tdj/informes/pdfs/tdj_informe_regional[ingles].pdf · DECENT WORK AND YOUTH Agenda for the Hemisphere Latin America](https://img.pdfslide.net/doc/110x75/5f90c692a7481e74a444f7e8/latin-america-100-million-youth-with-inglespdf-decent-work-and-youth-agenda.jpg)