Embed Size (px)

Citation preview

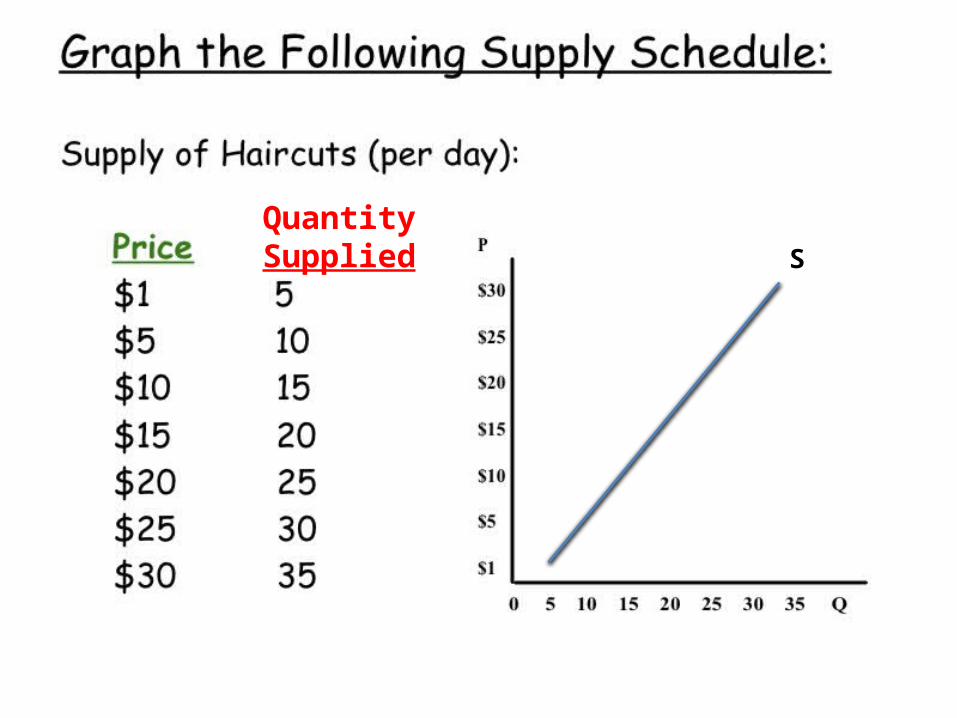

Law of Supply

How Much Do We Make?

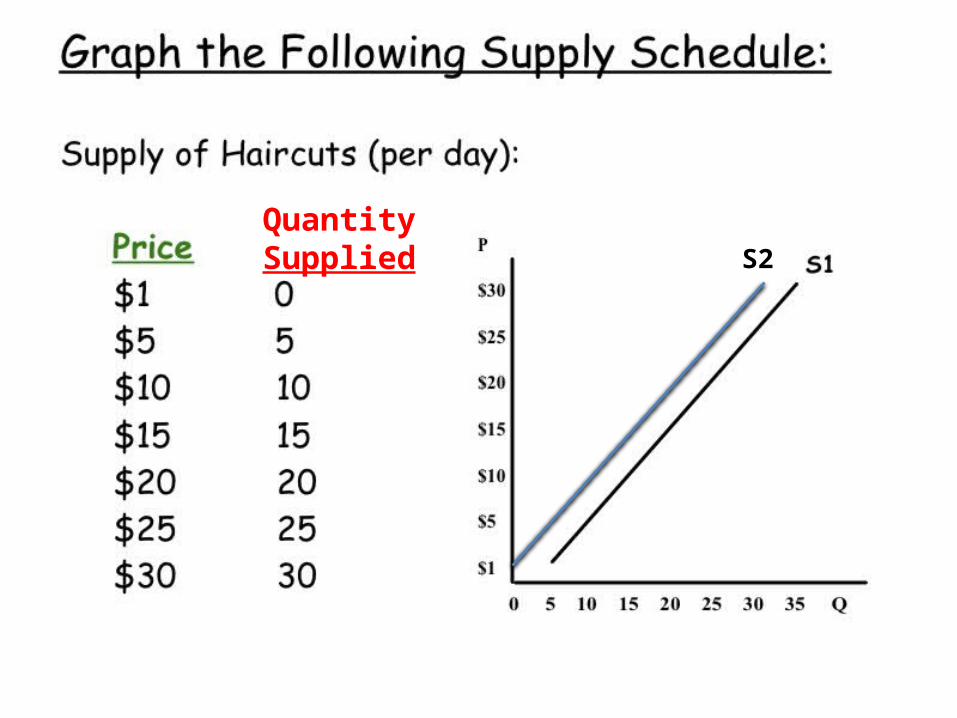

Quantity Supplied S

Quantity Supplied S2

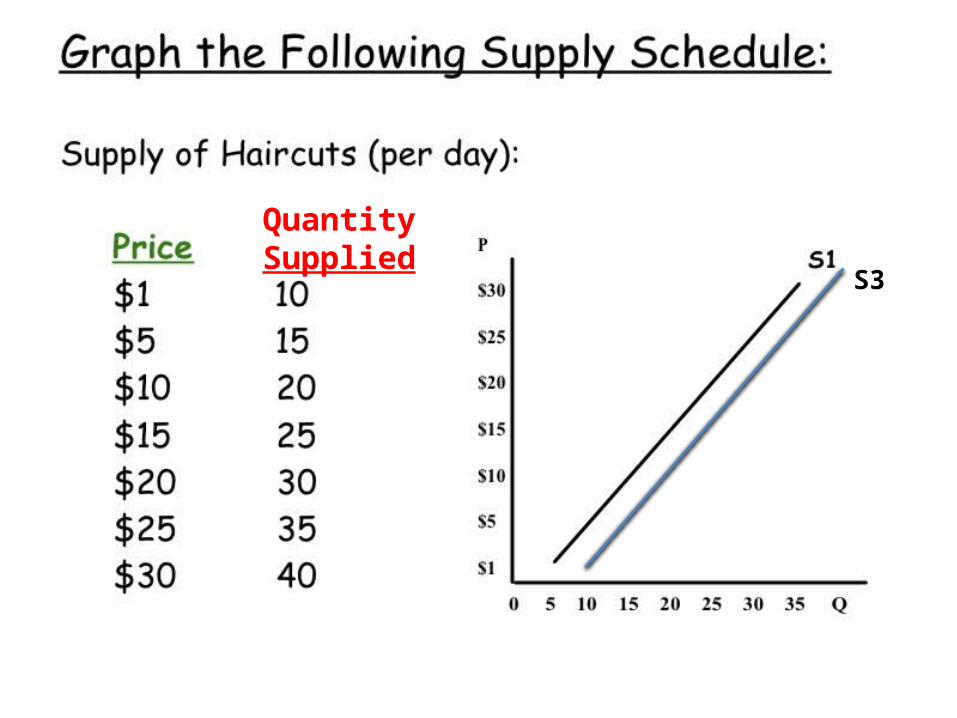

Quantity Supplied

S3

If the price of an input INCREASES, Supply of that good will DECREASE (shift to the left)

If the price of an input DECREASES, Supply of that good will INCREASE (shift to the right)

If the price of Labor INCREASES, Supply of that good will DECREASE (shift to the left)

If the price of Labor DECREASES, Supply of that good will INCREASE (shift to the right)

If the price of a good is expected to INCREASE, the Supply of that good in the short term will DECREASE (shift to the left)

If the price of a good is expected to DECREASE, the Supply of that good in the short term will INCREASE (shift to the right)

If government regulation on a good INCREASES, the Supply of that good will DECREASE (shift to the left)

If government regulation on a good DECREASES, the Supply of that good will INCREASE (shift to the right)

As new technology is applied to production, Supply of that good will INCREASE (shift to the right)

As the number of sellers INCREASES, Supply of that good will INCREASE (shift to the right)

As the number of sellers DECREASES, Supply of that good will DECREASE (shift to the left)

Changes in Supply

• Supply ShockA sudden decrease in production as a result of conflict, a natural disaster or accident.

Supply DECREASES

INCREASES

Shifts right due to change in cost of inputs

INCREASES

Shifts right due to change in technology

DECREASES

Shifts left due to change in cost of inputs

INCREASES

Shifts right due to change in number of suppliers (regulation)

DECREASES

Shifts left due to change in number of suppliers

NO CHANGE

Shifts along curve due to Law of Supply

DECREASES

Shifts left due to change in cost of inputs

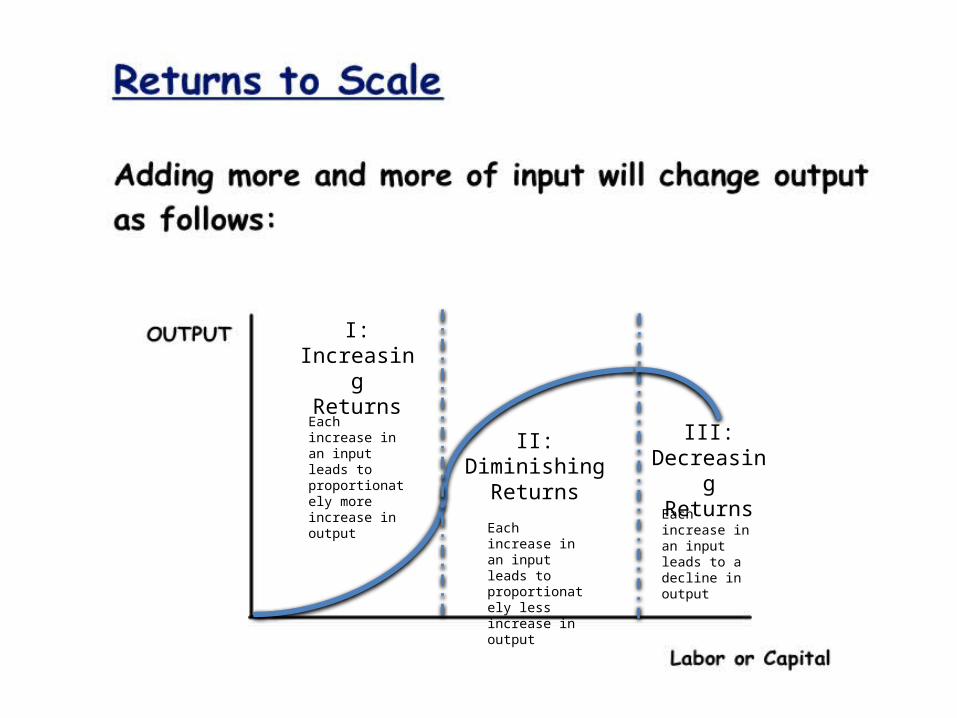

K = Capital L = Labor

I:Increasing

Returns

II:Diminishing

Returns

III:Decreasing

Returns

Each increase in an input leads to proportionately more increase in output

Each increase in an input leads to proportionately less increase in output

Each increase in an input leads to a decline in output

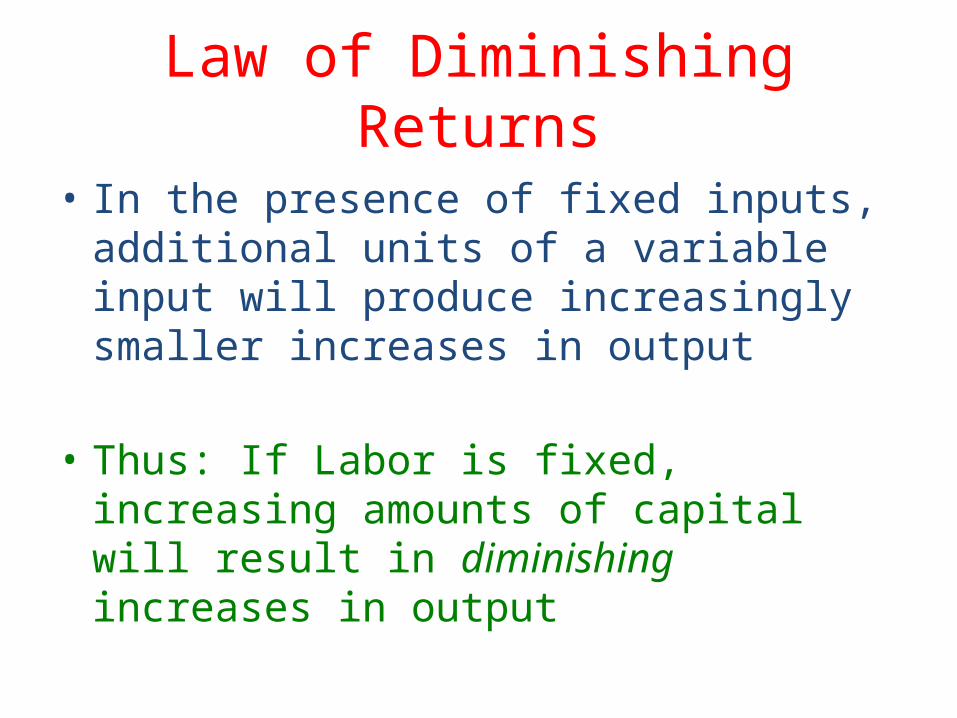

Law of Diminishing Returns

• In the presence of fixed inputs, additional units of a variable input will produce increasingly smaller increases in output

• Thus: If Labor is fixed, increasing amounts of capital will result in diminishing increases in output

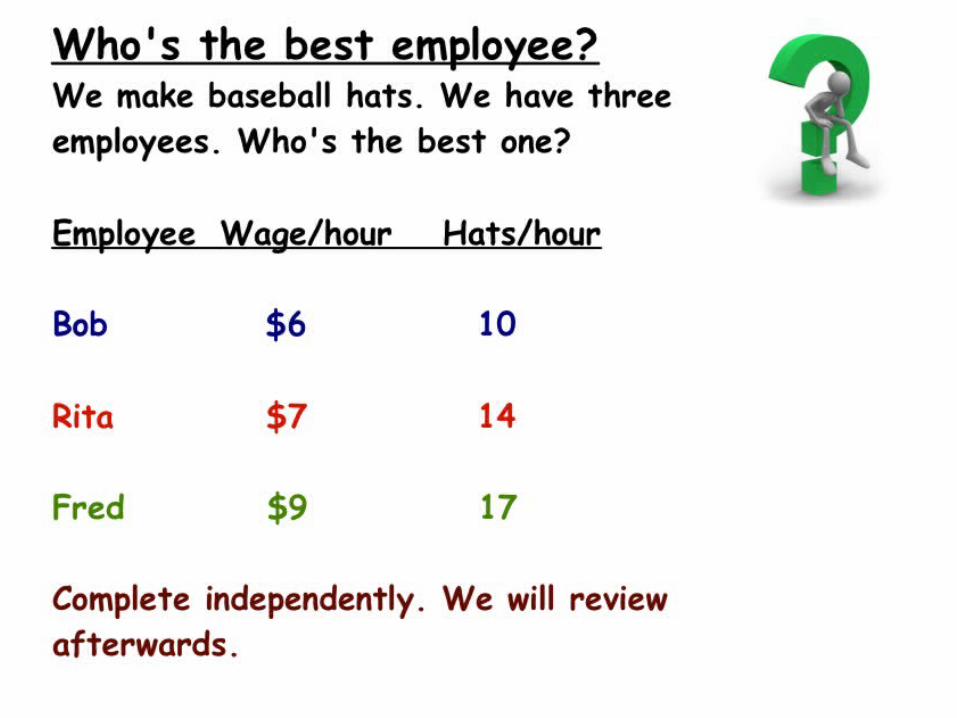

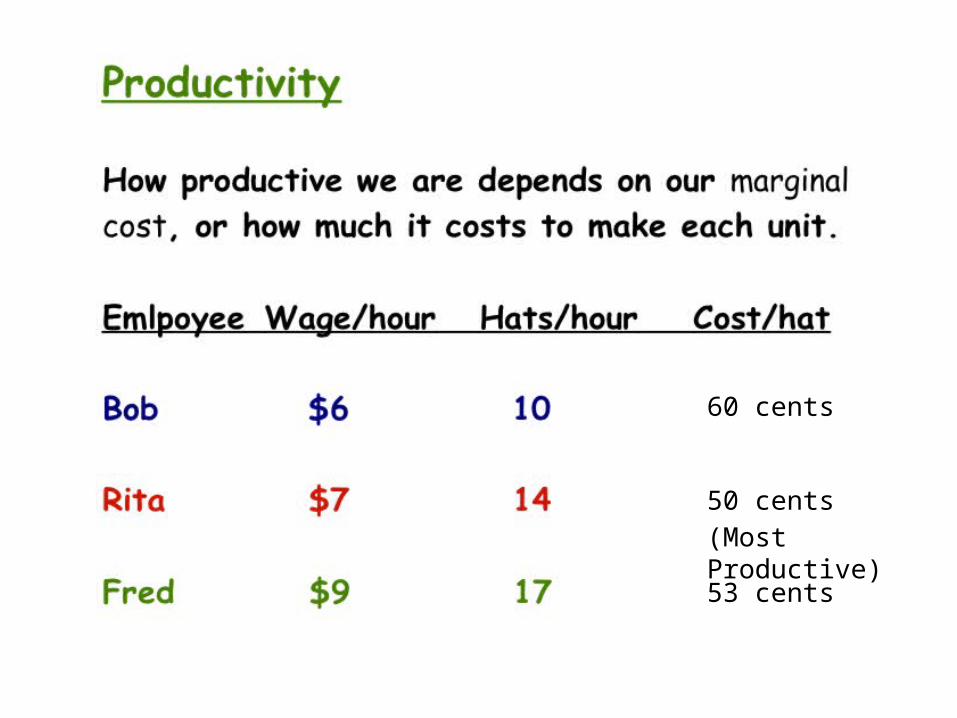

60 cents

50 cents

53 cents

(Most Productive)

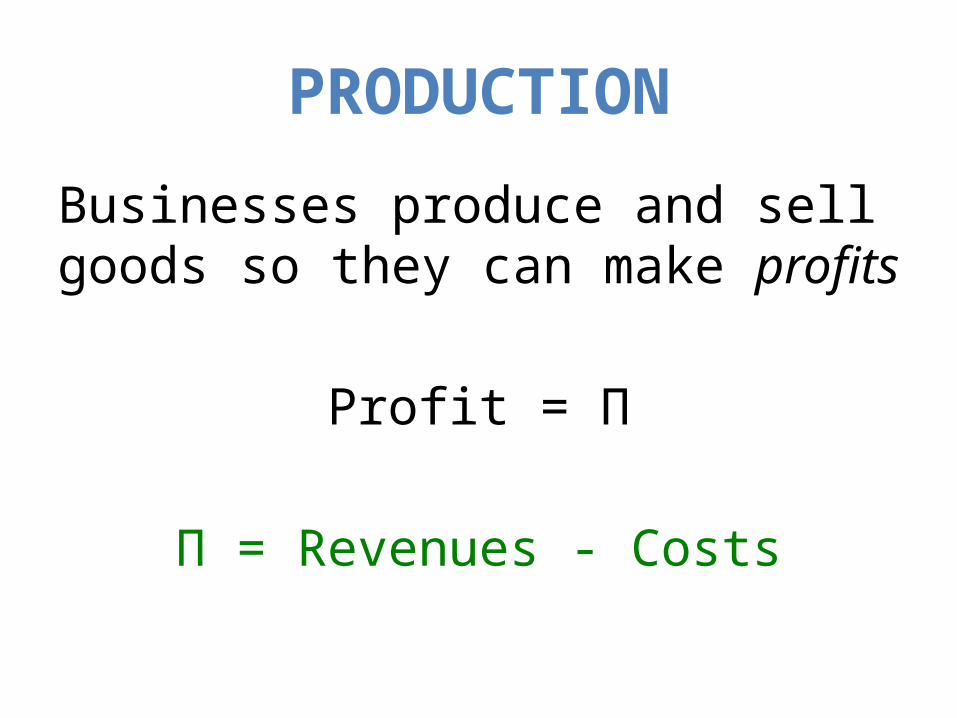

PRODUCTION

Businesses produce and sell goods so they can make profits

Profit = Π

Π = Revenues - Costs

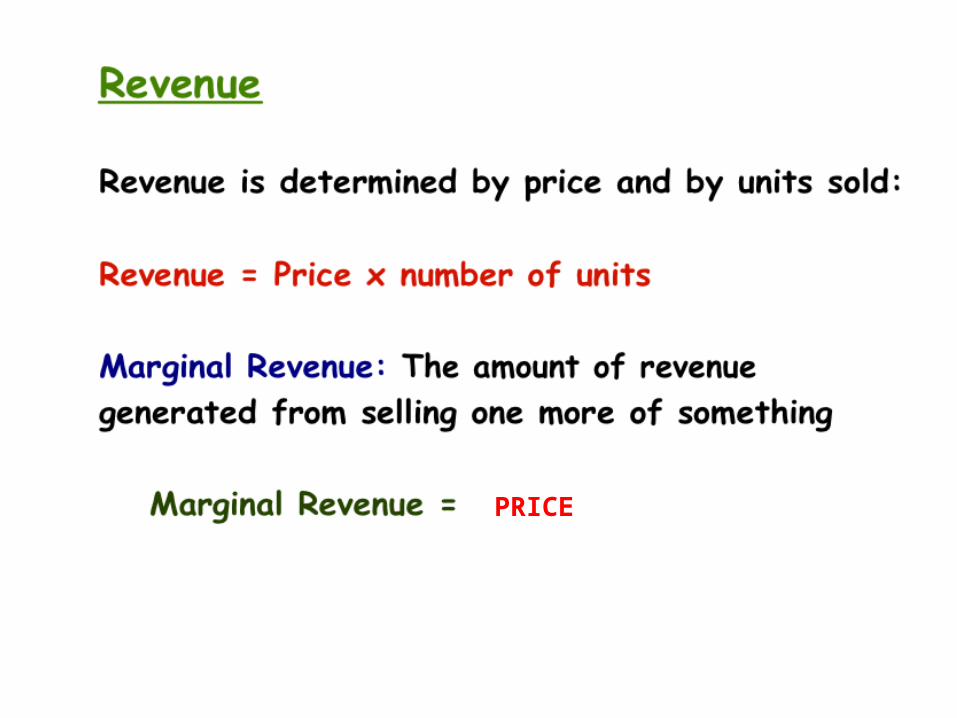

PRICE