Embed Size (px)

Citation preview

Lecture 24Annuities

Ana Nora Evans 403 [email protected]://people.virginia.edu/~ans5k/

Math 1140 Financial Mathematics

Math 1140 - Financial Mathematics2

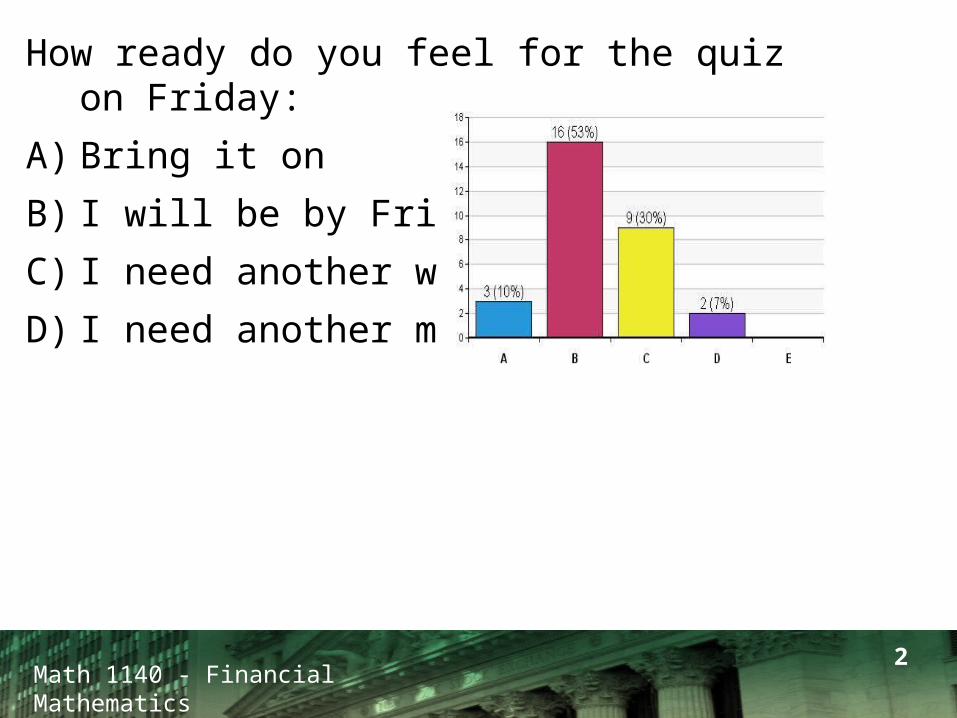

How ready do you feel for the quiz on Friday:

A) Bring it on

B) I will be by Friday

C) I need another week

D) I need another month

3Math 1140 - Financial Mathematics

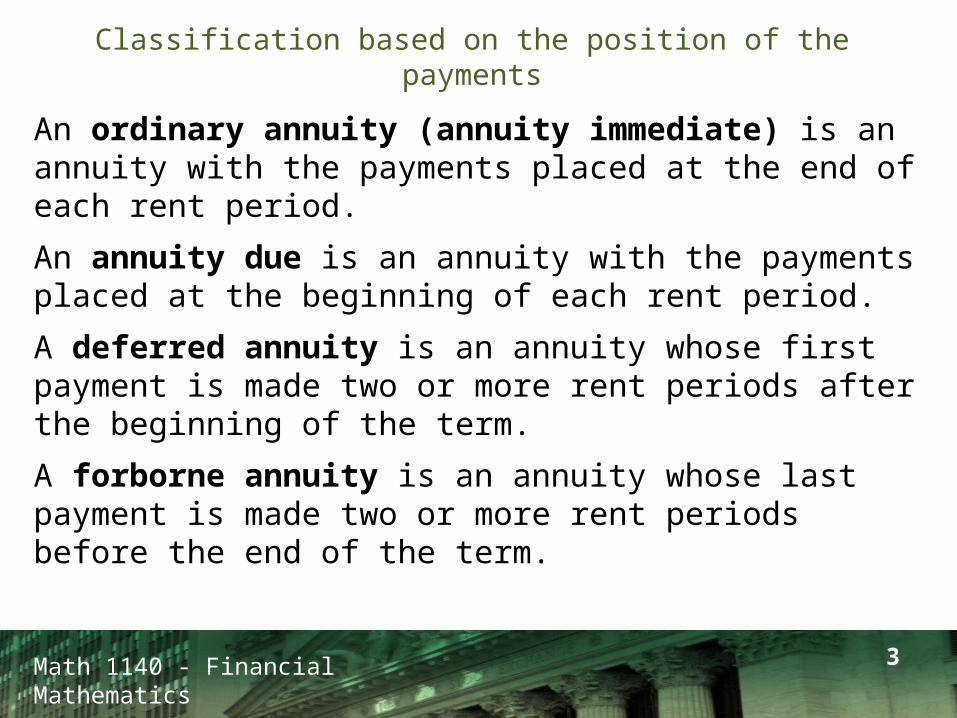

Classification based on the position of the payments

An ordinary annuity (annuity immediate) is an annuity with the payments placed at the end of each rent period.

An annuity due is an annuity with the payments placed at the beginning of each rent period.

A deferred annuity is an annuity whose first payment is made two or more rent periods after the beginning of the term.

A forborne annuity is an annuity whose last payment is made two or more rent periods before the end of the term.

4Math 1140 - Financial Mathematics

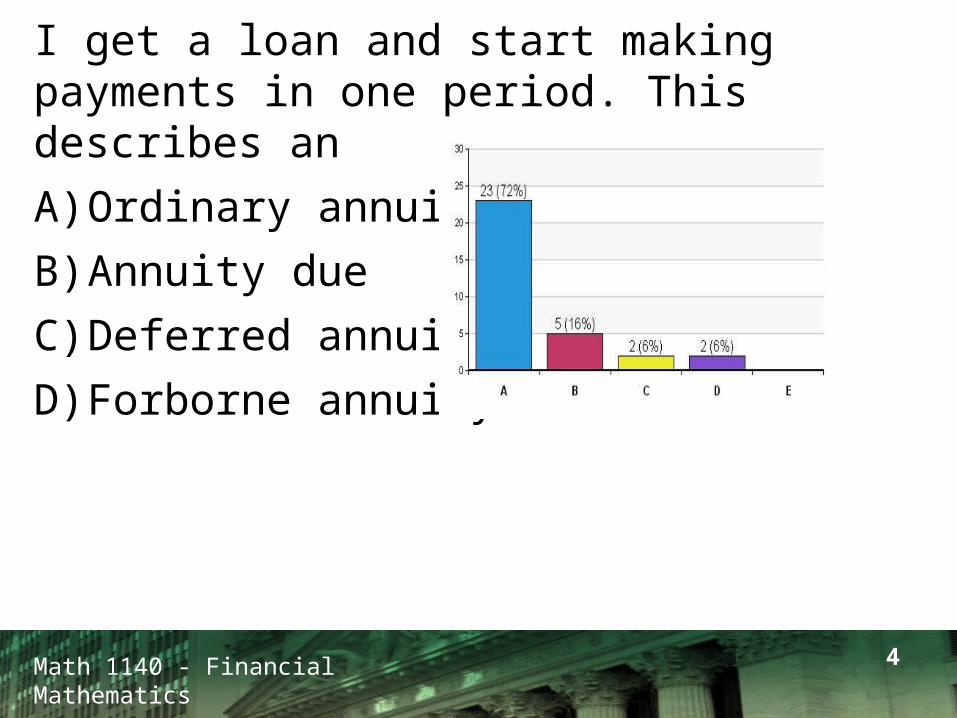

I get a loan and start making payments in one period. This describes an A) Ordinary annuityB) Annuity dueC) Deferred annuityD) Forborne annuity

5Math 1140 - Financial Mathematics

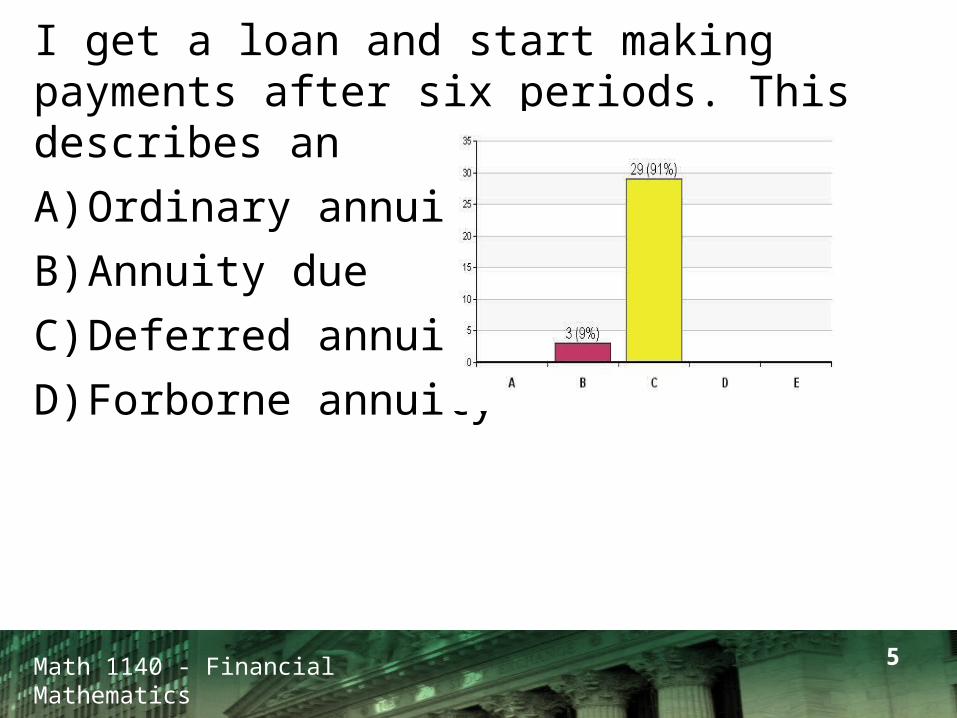

I get a loan and start making payments after six periods. This describes an A) Ordinary annuityB) Annuity dueC) Deferred annuityD) Forborne annuity

6Math 1140 - Financial Mathematics

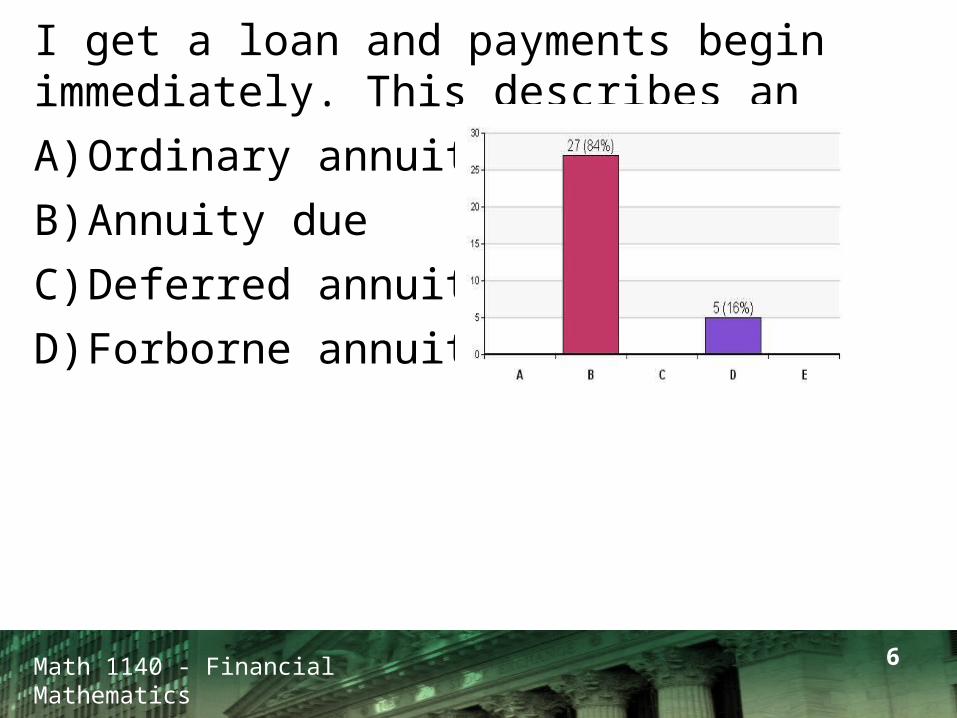

I get a loan and payments begin immediately. This describes an A) Ordinary annuityB) Annuity dueC) Deferred annuityD) Forborne annuity

7Math 1140 - Financial Mathematics

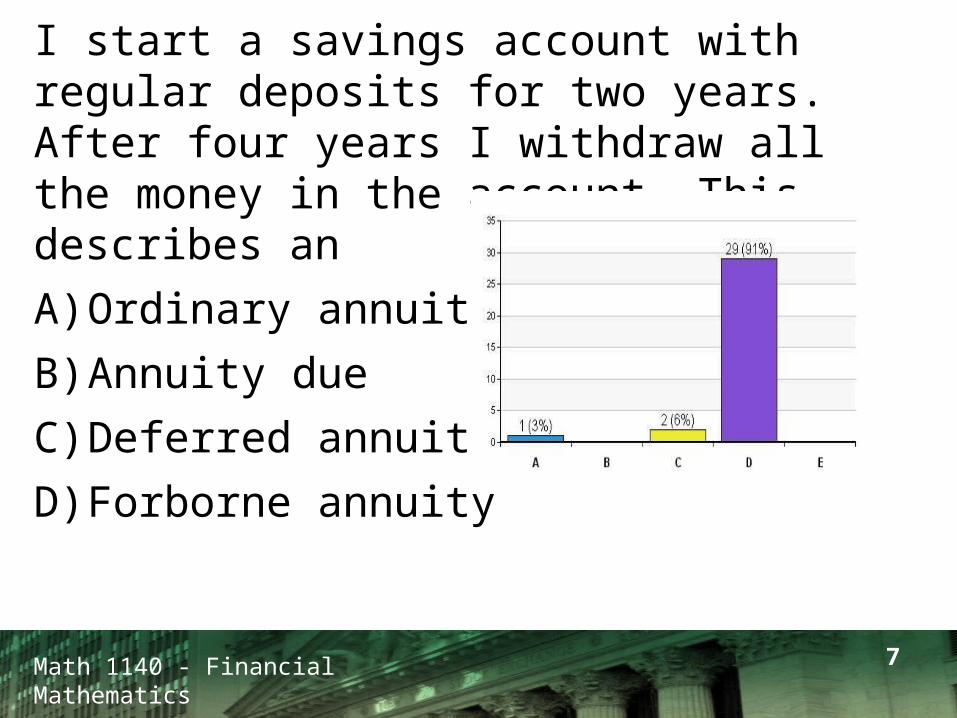

I start a savings account with regular deposits for two years. After four years I withdraw all the money in the account. This describes an A) Ordinary annuityB) Annuity dueC) Deferred annuityD) Forborne annuity

Math 1140 - Financial Mathematics8

Math 1140 - Financial Mathematics9

Alice borrows P dollars at an interest rate i per month. Assume Alice makes a monthly payment, R. Is there a problem if the monthly payment R is less than the interest per month, iP?

Hint: What happens to the balance if the payments do not cover the interest?

HW8#2

Math 1140 - Financial Mathematics10

HW8#10 What is the APR for an 8% add-on loan for $3,000 for three years?

HW8#11 A $9,000 car is purchased using a 4% add-on loan and monthly payments over three years. What is the actual APR?

Hint 1: Recall how the monthly payment of an add-on loan is calculated (lecture 3).

Hint 2: Read lecture 22, section 4 and example 4.6.1 at page 140 of the textbook.

HW8#10, HW9#11

Math 1140 - Financial Mathematics11

A $10,000 loan for 36 months at 6%(12) is arranged for the costumer to make payments R for the first year, 2R for the second year, and 3R for the third year. Find the payments for each of the three years.

Hint 1: Set-up an equation and solve for R.

Hint 2: You don’t know the formula for the case unequal rent payments, but you can split this problem into three problems for which you know the formula.

HW9 Bonus 1

Math 1140 - Financial Mathematics12

13Math 1140 - Financial Mathematics

Annuity Due

An annuity due is an annuity with payments placed at the beginning of each rent period.

The term starts at the first payment and ends one rent period after the last payment.

Math 1140 - Financial Mathematics14

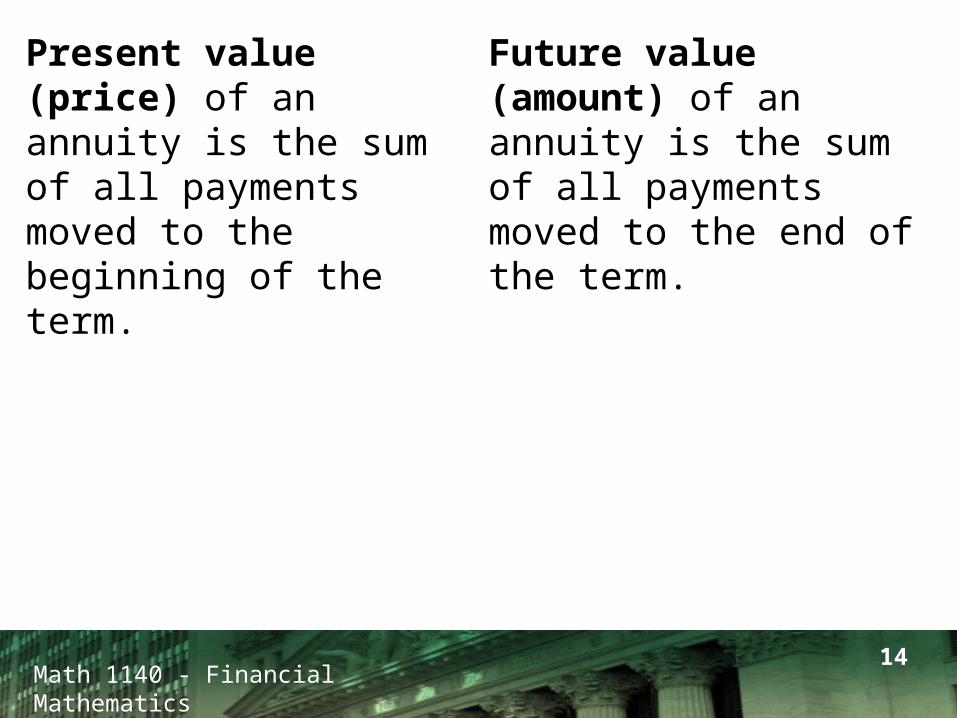

Present value (price) of an annuity is the sum of all payments moved to the beginning of the term.

Future value (amount) of an annuity is the sum of all payments moved to the end of the term.

15Math 1140 - Financial Mathematics

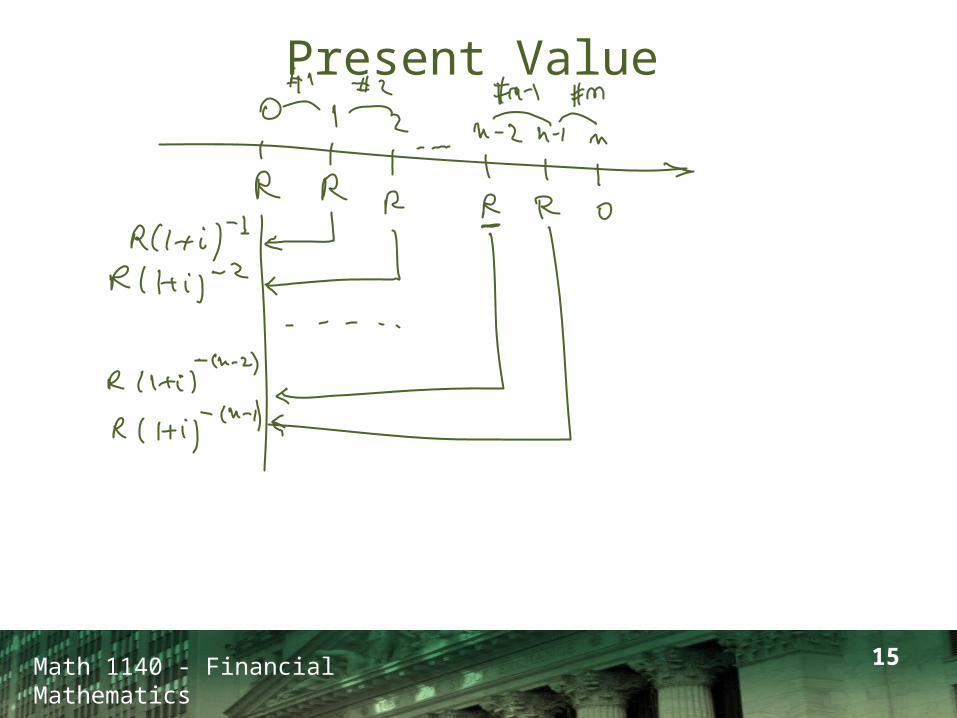

Present Value

16Math 1140 - Financial Mathematics

Present Value

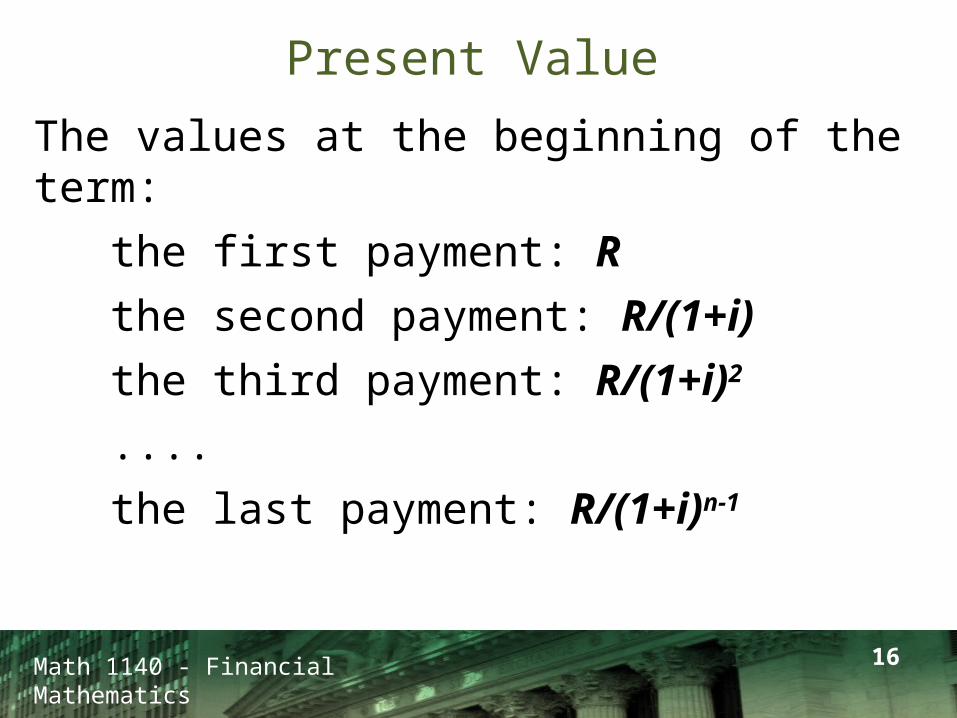

The values at the beginning of the term: the first payment: R the second payment: R/(1+i)

the third payment: R/(1+i)2

.... the last payment: R/(1+i)n-1

17Math 1140 - Financial Mathematics

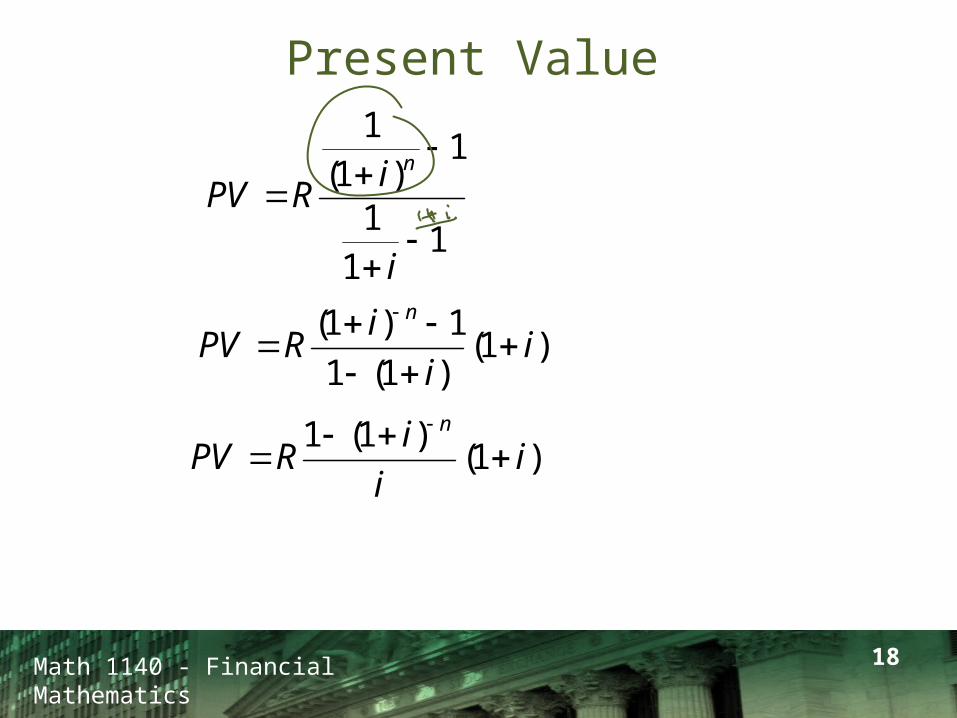

Present Value

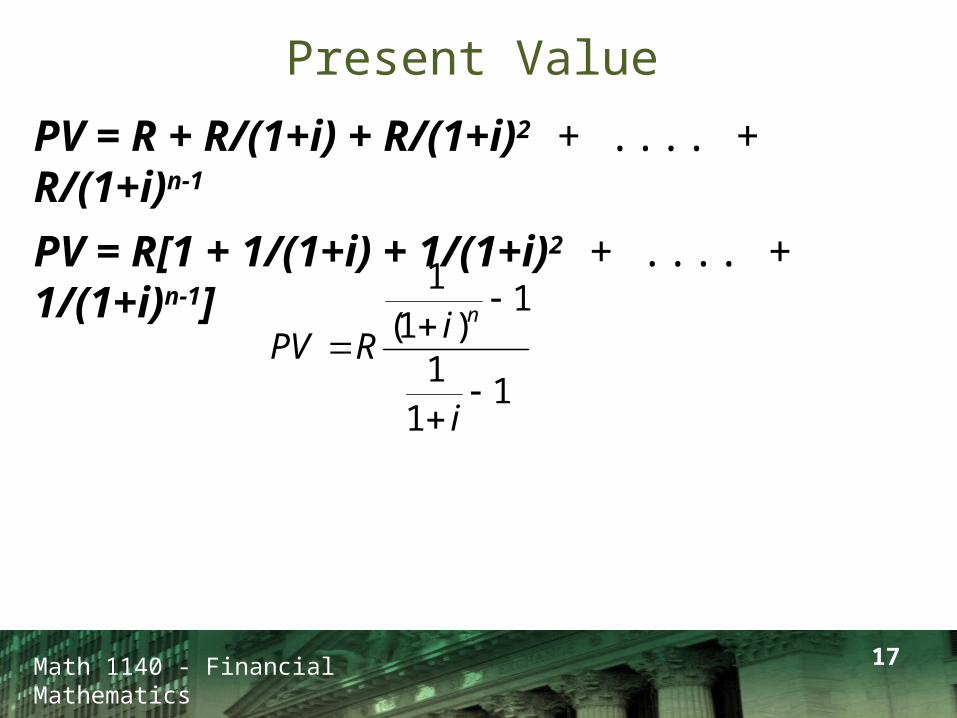

PV = R + R/(1+i) + R/(1+i)2 + .... + R/(1+i)n-1

PV = R[1 + 1/(1+i) + 1/(1+i)2 + .... + 1/(1+i)n-1]

111

1)1(

1

i

iRPV

n

18Math 1140 - Financial Mathematics

Present Value

111

1)1(

1

i

iRPV

n

)1()1(1

1)1(i

i

iRPV

n

)1()1(1

ii

iRPV

n

19Math 1140 - Financial Mathematics

Another Strategy

Use the formula for present value for ordinary annuities and move it one rent period forward.

Math 1140 - Financial Mathematics20

21Math 1140 - Financial Mathematics

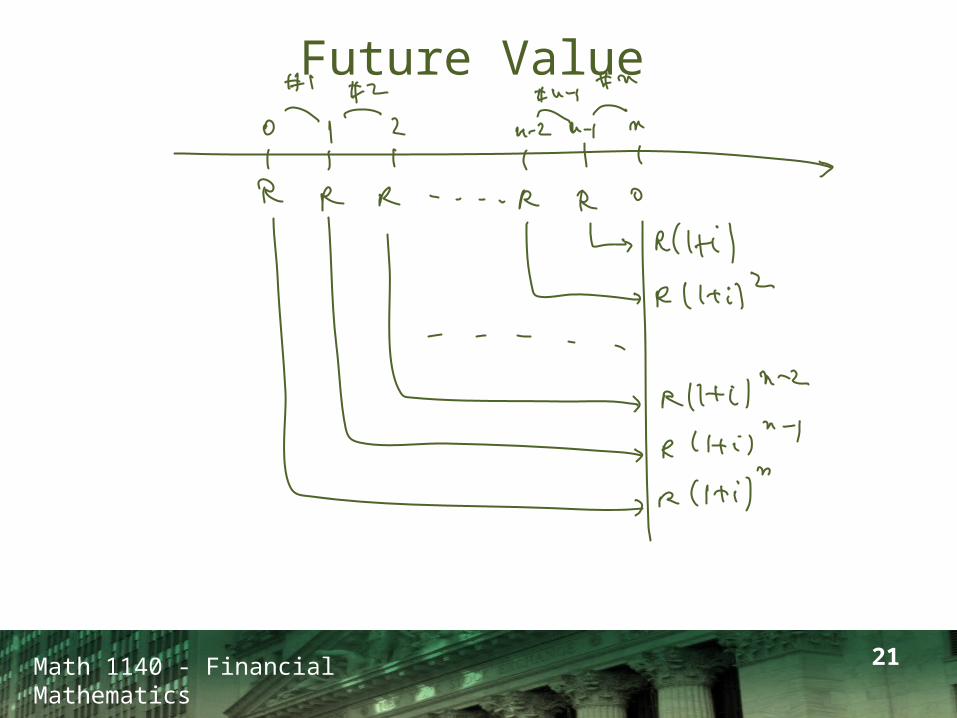

Future Value

22Math 1140 - Financial Mathematics

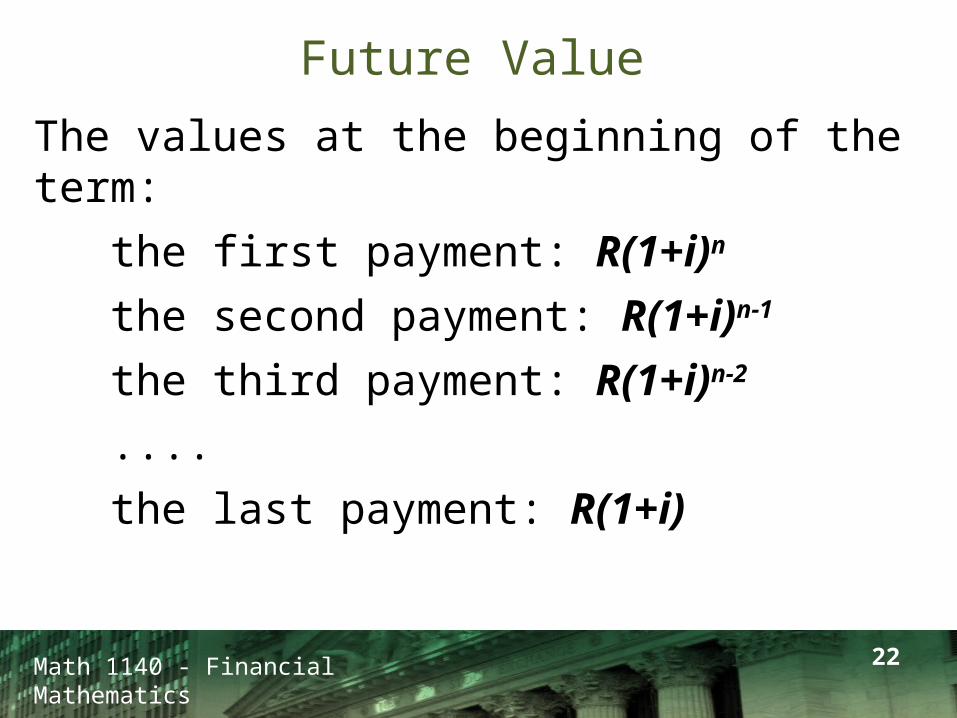

Future Value

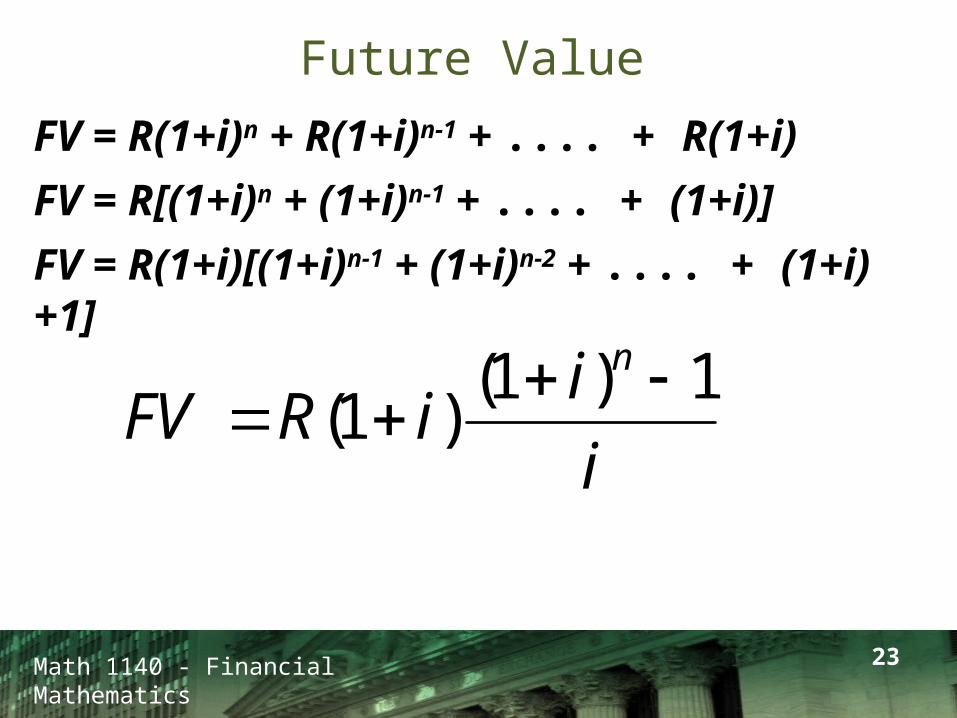

The values at the beginning of the term: the first payment: R(1+i)n

the second payment: R(1+i)n-1

the third payment: R(1+i)n-2

.... the last payment: R(1+i)

23Math 1140 - Financial Mathematics

Future Value

FV = R(1+i)n + R(1+i)n-1 + .... + R(1+i)

FV = R[(1+i)n + (1+i)n-1 + .... + (1+i)]

FV = R(1+i)[(1+i)n-1 + (1+i)n-2 + .... + (1+i)+1]

i

iiRFV

n 1)1()1(

24Math 1140 - Financial Mathematics

Another Strategy

Use the formula for future value for ordinary annuities and move it one rent period forward.

Math 1140 - Financial Mathematics25

Math 1140 - Financial Mathematics26

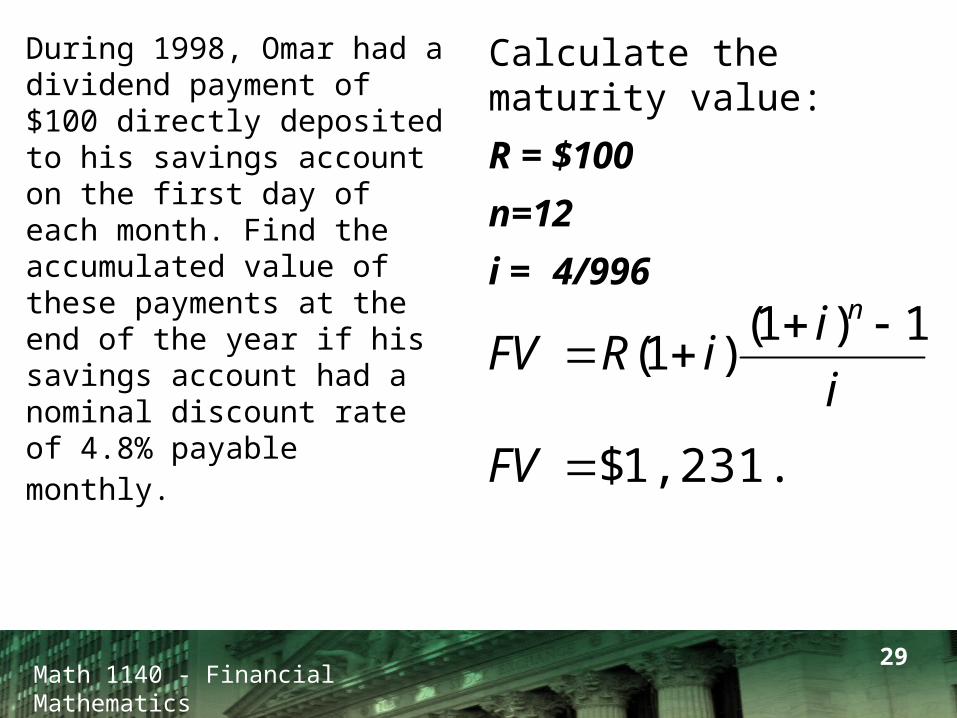

During 1998, Omar had a dividend payment of $100 directly deposited to his savings account on the first day of each month. Find the accumulated value of these payments at the end of the year if his savings account had a nominal discount rate of 4.8% payable monthly.

Math 1140 - Financial Mathematics27

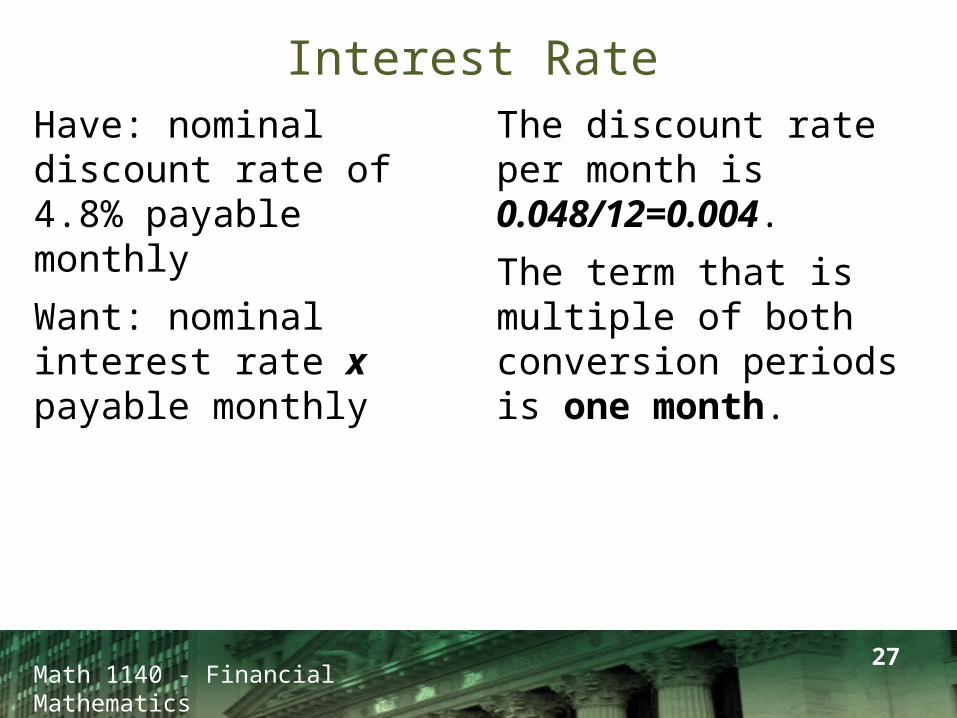

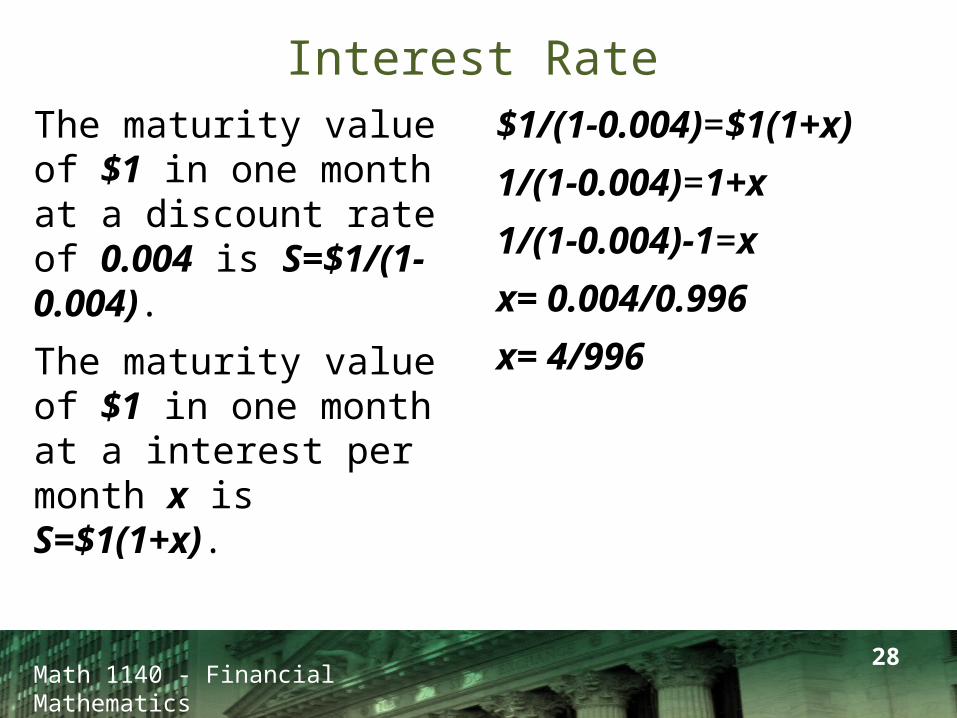

Have: nominal discount rate of 4.8% payable monthly

Want: nominal interest rate x payable monthly

The discount rate per month is 0.048/12=0.004.

The term that is multiple of both conversion periods is one month.

Interest Rate

Math 1140 - Financial Mathematics28

The maturity value of $1 in one month at a discount rate of 0.004 is S=$1/(1-0.004).

The maturity value of $1 in one month at a interest per month x is S=$1(1+x).

$1/(1-0.004)=$1(1+x)

1/(1-0.004)=1+x

1/(1-0.004)-1=x

x= 0.004/0.996

x= 4/996

Interest Rate

Math 1140 - Financial Mathematics29

During 1998, Omar had a dividend payment of $100 directly deposited to his savings account on the first day of each month. Find the accumulated value of these payments at the end of the year if his savings account had a nominal discount rate of 4.8% payable monthly.

Calculate the maturity value:

R = $100

n=12

i = 4/996

i

iiRFV

n 1)1()1(

1,231.79$FV

Math 1140 - Financial Mathematics 30

Math 1140 - Financial Mathematics31

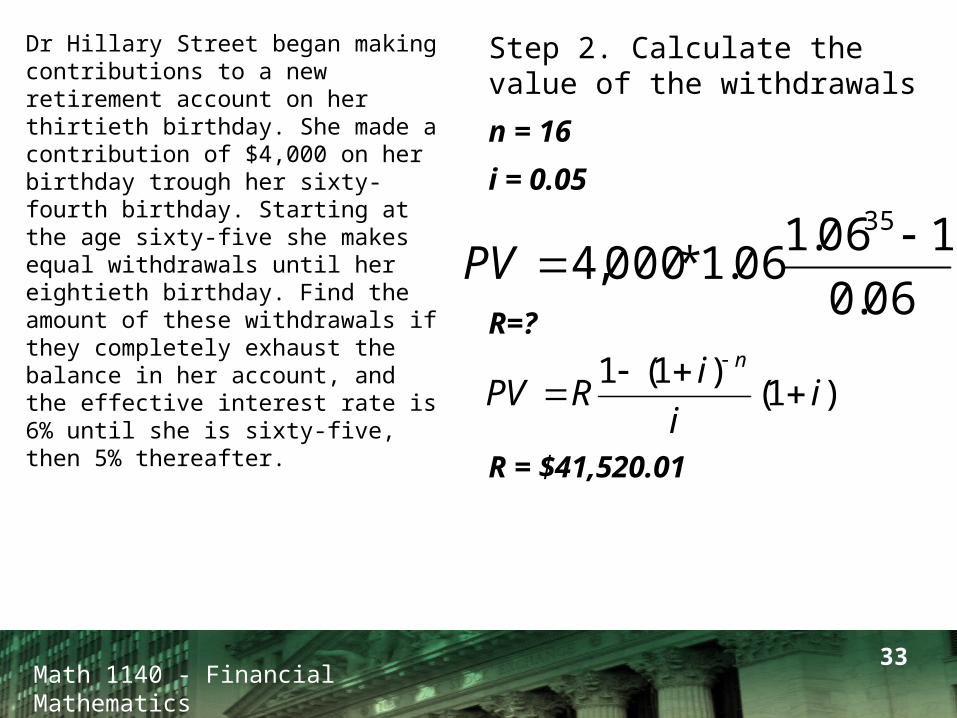

Dr Hillary Street began making contributions to a new retirement account on her thirtieth birthday. She made a contribution of $4,000 on her birthday trough her sixty-fourth birthday. Starting at the age sixty-five she makes equal withdrawals until her eightieth birthday. Find the amount of these withdrawals if they completely exhaust the balance in her account, and the effective interest rate is 6% until she is sixty-five, then 5% thereafter.

Math 1140 - Financial Mathematics32

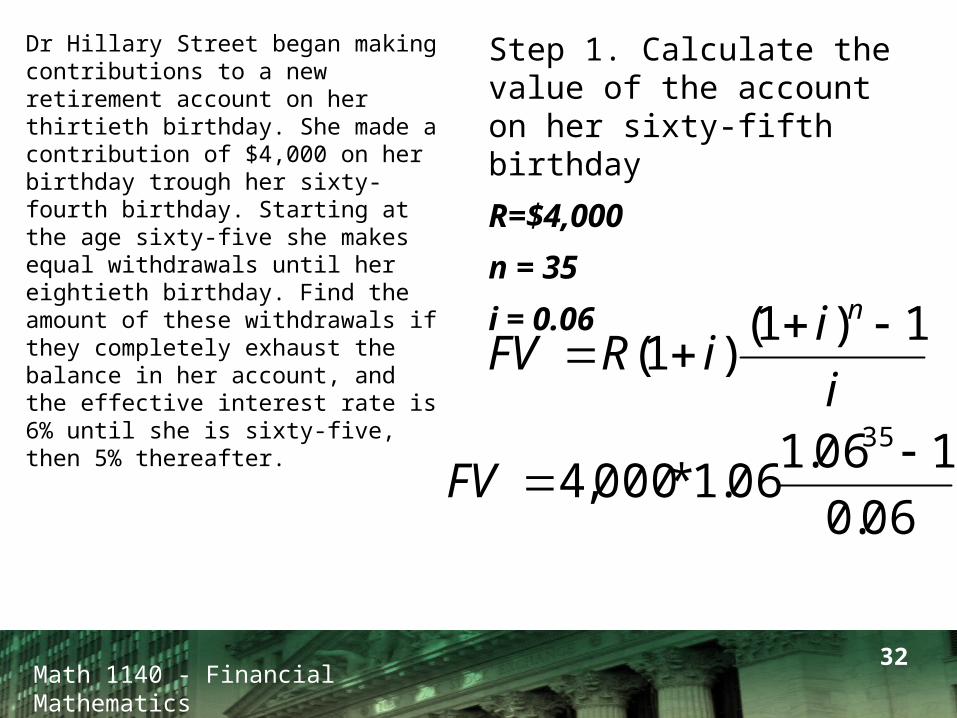

Dr Hillary Street began making contributions to a new retirement account on her thirtieth birthday. She made a contribution of $4,000 on her birthday trough her sixty-fourth birthday. Starting at the age sixty-five she makes equal withdrawals until her eightieth birthday. Find the amount of these withdrawals if they completely exhaust the balance in her account, and the effective interest rate is 6% until she is sixty-five, then 5% thereafter.

Step 1. Calculate the value of the account on her sixty-fifth birthday

R=$4,000

n = 35

i = 0.06

i

iiRFV

n 1)1()1(

06.0

106.106.1*000,4

35 FV

Math 1140 - Financial Mathematics33

Dr Hillary Street began making contributions to a new retirement account on her thirtieth birthday. She made a contribution of $4,000 on her birthday trough her sixty-fourth birthday. Starting at the age sixty-five she makes equal withdrawals until her eightieth birthday. Find the amount of these withdrawals if they completely exhaust the balance in her account, and the effective interest rate is 6% until she is sixty-five, then 5% thereafter.

Step 2. Calculate the value of the withdrawals

n = 16

i = 0.05

R=?

R = $41,520.01

06.0

106.106.1*000,4

35 PV

)1()1(1

ii

iRPV

n

Math 1140 - Financial Mathematics34

Math 1140 - Financial Mathematics35

Friday

Read sections 5.3, 5.4

Quiz from compound interest and annuities.

Charge