Embed Size (px)

Citation preview

Lecture 31Amortization

of Debts

Ana Nora Evans 403 [email protected]://people.virginia.edu/~ans5k

Math 1140 Financial Mathematics

2Math 1140 - Financial Mathematics

The exam 2 was

A) EasyB) Just rightC) HardD) Too hard

3Math 1140 - Financial Mathematics

Terms

The cash price of an object is the price actually paid for that object.Sometimes, the lender requires the borrower to pay some part of the object and only borrow the rest of the money. This payment is called down payment.The borrower borrows only the difference between the cash price and the down payment.

4Math 1140 - Financial Mathematics

To amortize a debt means to pay a sequence of equal-size payments at equal time intervals.What is this sequence of payments?An ordinary annuity whose price is the amount borrowed.

Math 1140 - Financial Mathematics5

Suppose that you take out a mortgage to buy a house. You borrow $210,000, and agree to repay the loan with monthly payments for 30 years, the first coming a month from now. If the interest rate is 6.25% convertible monthly, what is the monthly payment?

P = $210,000

n = 30 × 12 = 360

i = 0.0625/12

ni

iPR

)1(1

1,293.01$R

6Math 1140 - Financial Mathematics

Each payment has two components 1. the interest due on the balance right after the previous payment 2. part of the principal

7Math 1140 - Financial Mathematics

How much is the interest part of the payment?

The interest part of the payment is the interest on the previous month balance for one month. More precisely, the interest part of the payment is the previous balance times the interest rate per month.The interest part of the payment is iB, where B is the previous month balance and i is the interest rate per month.

8Math 1140 - Financial Mathematics

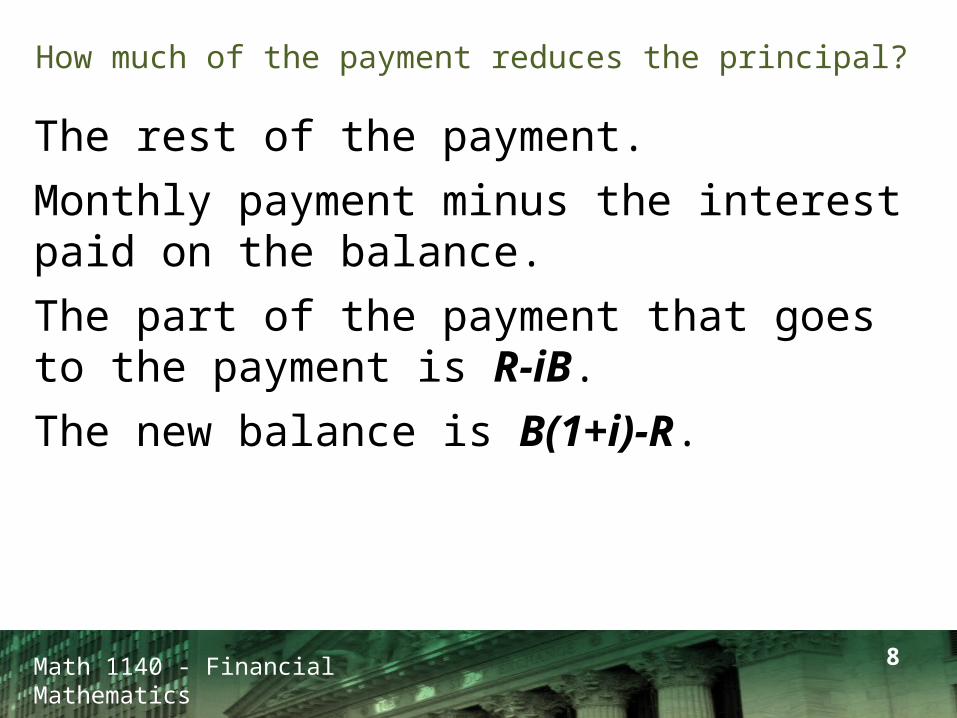

How much of the payment reduces the principal?

The rest of the payment.Monthly payment minus the interest paid on the balance.The part of the payment that goes to the payment is R-iB.The new balance is B(1+i)-R.

9Math 1140 - Financial Mathematics

Balance before the first payment: $210,000.The interest part of the first payment is:

$210,000 × 0.0625/12 = $1,093.75 The principal reduction is

$1,293.01 - $1,093.75 = $199.26The balance after the first payment is

$210,000 - $199.26 = $209,800.74$210,000(1+ 0.0625/12) - $1,293.01 = $209,800.74

10Math 1140 - Financial Mathematics

Balance right after the first payment: $209,800.74.The interest part of the second payment is:

$209,800.74 × 0.0625/12 = $1,092.71 The principal reduction is

$1,293.01 - $1,092.71 = $200.03The balance after the second payment is

$209,800.74 - $200.03 = $209,600.44

11Math 1140 - Financial Mathematics

Amortization SchedulePayment No. Payment Interest Paid Principal Paid Balance

0 210,000.00$ 1 1,293.01$ 1,093.75$ 199.26$ 209,800.74$ 2 1,293.01$ 1,092.71$ 200.30$ 209,600.44$ 3 1,293.01$ 1,091.67$ 201.34$ 209,399.10$ 4 1,293.01$ 1,090.62$ 202.39$ 209,196.71$ 5 1,293.01$ 1,089.57$ 203.44$ 208,993.27$ 6 1,293.01$ 1,088.51$ 204.50$ 208,788.76$ 7 1,293.01$ 1,087.44$ 205.57$ 208,583.20$ 8 1,293.01$ 1,086.37$ 206.64$ 208,376.56$ 9 1,293.01$ 1,085.29$ 207.72$ 208,168.84$

10 1,293.01$ 1,084.21$ 208.80$ 207,960.04$ 11 1,293.01$ 1,083.13$ 209.88$ 207,750.16$ 12 1,293.01$ 1,082.03$ 210.98$ 207,539.18$ 13 1,293.01$ 1,080.93$ 212.08$ 207,327.10$ 14 1,293.01$ 1,079.83$ 213.18$ 207,113.92$ 15 1,293.01$ 1,078.72$ 214.29$ 206,899.63$ 16 1,293.01$ 1,077.60$ 215.41$ 206,684.22$ 17 1,293.01$ 1,076.48$ 216.53$ 206,467.69$ 18 1,293.01$ 1,075.35$ 217.66$ 206,250.04$ 19 1,293.01$ 1,074.22$ 218.79$ 206,031.25$ 20 1,293.01$ 1,073.08$ 219.93$ 205,811.31$

Math 1140 - Financial Mathematics12

13Math 1140 - Financial Mathematics

Recall

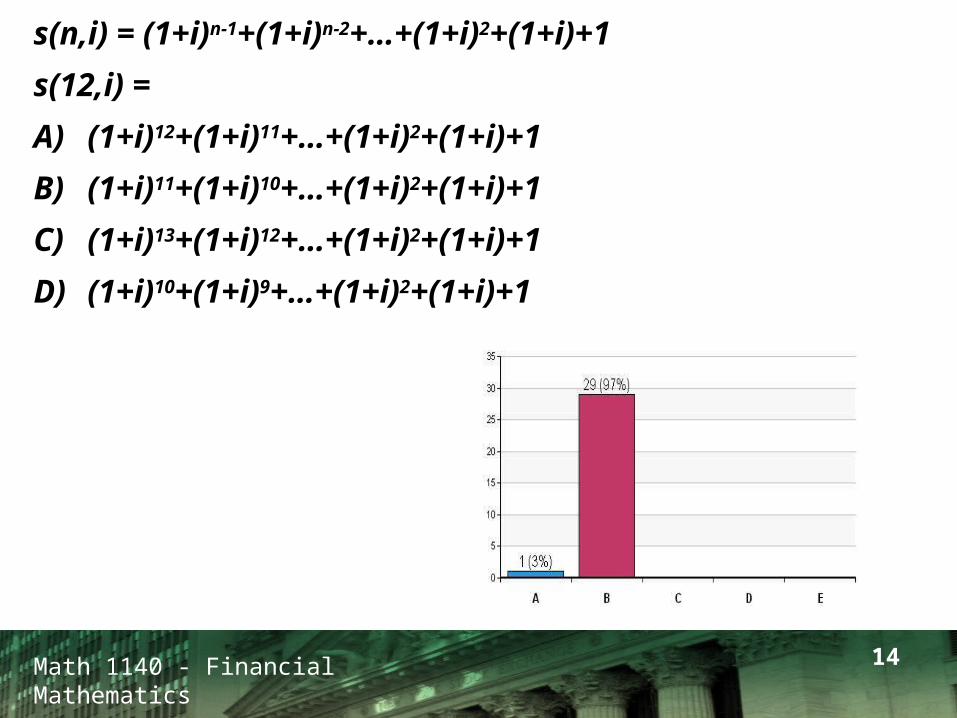

s(n,i) = (1+i)n-1+(1+i)n-2+…+(1+i)2+(1+i)+1

s(1,i)=1

s(n+1,i) = (1+i)n+(1+i)n-1+…+(1+i)2+(1+i)+1

= [(1+i)n-1+(1+i)n-2+…+(1+i)2+(1+i)+1](1+i)+1

= s(n,i)(1+i)+1

14Math 1140 - Financial Mathematics

s(n,i) = (1+i)n-1+(1+i)n-2+…+(1+i)2+(1+i)+1

s(12,i) =

A) (1+i)12+(1+i)11+…+(1+i)2+(1+i)+1

B) (1+i)11+(1+i)10+…+(1+i)2+(1+i)+1

C) (1+i)13+(1+i)12+…+(1+i)2+(1+i)+1

D) (1+i)10+(1+i)9+…+(1+i)2+(1+i)+1

15Math 1140 - Financial Mathematics

Goal: Calculate the balance after kth payment.

Balance after first payment: P(1+i)-R= P(1+i)-Rs(1,i).

Balance after second payment:

[P(1+i)-Rs(1,i)](1+i)-R

= P(1+i)2 - R[s(1,i)(1+i)+1]

= P(1+i)2 - R s(2,i)

16Math 1140 - Financial Mathematics

Balance after third payment:(P(1+i)2 - R s(2,i))(1+i)-R

= P(1+i)3 - R [s(2,i)(1+i)+1]

= P(1+i)3 - R s(3,i)

Balance after fourth payment:(P(1+i)3 - R s(3,i))(1+i)-R

= P(1+i)4 - R [s(3,i)(1+i)+1]

= P(1+i)4 - R s(4,i)

17Math 1140 - Financial Mathematics

Balance after kth payment: P(1+i)k - R s(k,i)

How much of the (k+1)th payment goes to the interest?

[P(1+i)k - R s(k,i)](1+i)

How much of the (k+1)th payment goes to the principal?

R - [P(1+i)k - R s(k,i)](1+i)

Math 1140 - Financial Mathematics18

Suppose that you take out a mortgage to buy a house. You borrow $210,000, and agree to repay the loan with monthly payments for 30 years, the first coming a month from now. If the interest rate is 6.25% convertible monthly, what is the 12th line of the amortization table?

P=$210,000

R =$1,293.01

i = 0.0625/12

Math 1140 - Financial Mathematics19

The part of the (k+1)th payment goes to the interest is

[P(1+i)k - R s(k,i)](1+i).

The part of the 12th payment that goes to the interest is:

A) [P(1+i)10 - R s(10,i)](1+i)

B)[P(1+i)11 - R s(11,i)](1+i)

C) [P(1+i)12 - R s(12,i)](1+i)

D)[P(1+i)11 - R s(12,i)](1+i)

Math 1140 - Financial Mathematics20

How much of the (k+1)th payment goes to the principal? R - [P(1+i)k - R s(k,i)](1+i)

The part of the 12th payment that goes to the principal isA) R - [P(1+i)10 - R

s(10,i)](1+i)

B) R - [P(1+i)11 - R s(11,i)](1+i)

C) R - [P(1+i)12 - R s(12,i)](1+i)

D) R - [P(1+i)11 - R s(12,i)](1+i)

Math 1140 - Financial Mathematics21

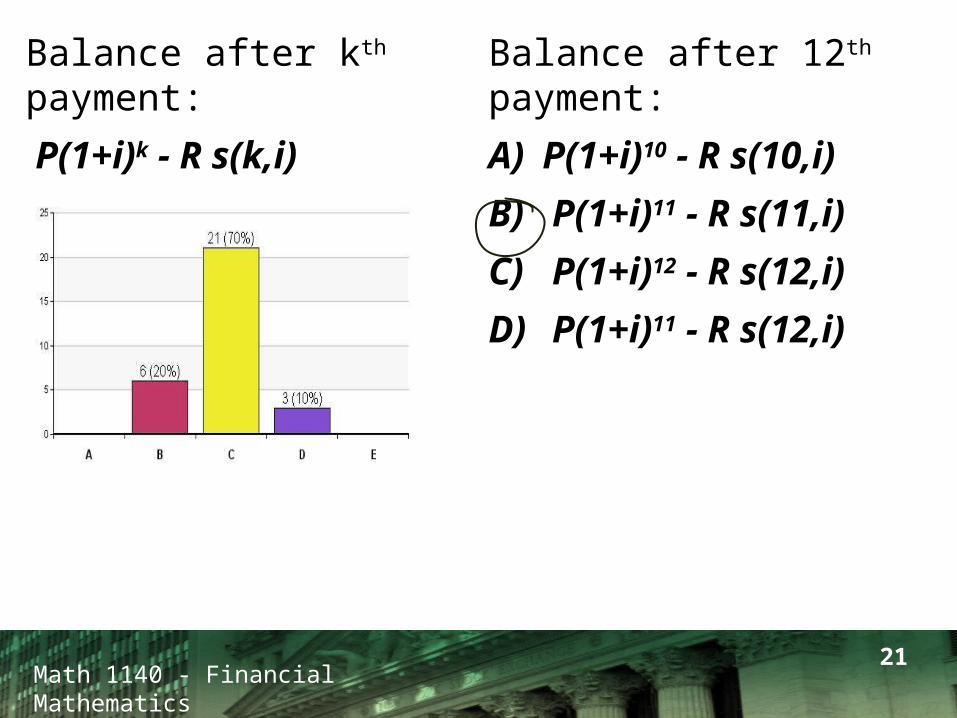

Balance after kth payment:

P(1+i)k - R s(k,i)

Balance after 12th payment:

A) P(1+i)10 - R s(10,i)

B) P(1+i)11 - R s(11,i)

C) P(1+i)12 - R s(12,i)

D) P(1+i)11 - R s(12,i)

Math 1140 - Financial Mathematics22

23Math 1140 - Financial Mathematics

Discount Points

A point is 1% of the amount of money being lent.Discount points is an up-front charge on the amount being lent.The discount points are similar to discount interest.Compound interest is also charged as usual.The borrower receives the amount being borrowed less the discount points.The borrower pays back the amount borrowed, plus the interest.

24Math 1140 - Financial Mathematics

Example

Alice takes out a 15 years, $100,000 loan from a bank charging 2 points and 7.25%(12) interest.How much money Alice gets on the day of the loan?$100,000 - 0.02 × $100,000 = $98,000

How much does Alice has to pay back?$100,000 and the compound interest on $100,000.

Math 1140 - Financial Mathematics25

Alice takes out a 15 years, $100,000 loan from a bank charging 2 points and 7.25%(12) interest. If Alice has to pay equal monthly payments, how much is the payment?

i = 0.0725/12

n = 15 × 12

P = $100,000

R = $912.86

ni

iPR

)1(1

Math 1140 - Financial Mathematics26

Alice takes out a 15 years, $100,000 loan from a bank charging 2 points and 7.25%(12) interest. What is the actual interest paid by Alice?

Alice receives $98,000 from the bank.

Alice pays this loan by making monthly payments of $912.86.

Use Wolfram Alpha to determine the interest rate

0.6316% per month or

7.5792%(12).

Math 1140 - Financial Mathematics27

28Math 1140 - Financial Mathematics

What if Alice does not have the money for the discount points?Alice needs P dollars to buy the item she wants. The bank charges p discount points. How much does Alice need to borrow to pay both the item and the discount points charge?

29Math 1140 - Financial Mathematics

The discount charge is pP. Alice needs to borrow P+pP.Let’s check it!

Math 1140 - Financial Mathematics30

Alice borrows P+pP. The discount points charge is p(P+pP).

The amount Alice gets from the bank is

P+pP - p(P+pP) = P – p2P

Math 1140 - Financial Mathematics31

What if Alice does not have the money for the discount points?

Alice needs P dollars to buy the item she wants.

The bank charges p discount points.

How much does Alice need to borrow to pay both the item and the discount points charge?

We denote the amount borrowed by X.

The discount charge is pX.

The amount Alice gets is

X – pX.

This is the amount she uses to pay for the item.

P = X – pX = X(1-p)

Math 1140 - Financial Mathematics32

Alice takes out a 15 years, $100,000 loan from a bank charging 2 points and 7.25%(12) interest. The points are added to the loan. Alice has to pay equal monthly payments.

What is the actual interest Alice is being charged?

Step 1: Calculate the amount borrowed

X = $100,000 / (1 – 0.02)

X = $102,040.82

p

PX

1

Math 1140 - Financial Mathematics33

Alice takes out a 15 years, $100,000 loan from a bank charging 2 points and 7.25%(12) interest. The points are added to the loan. Alice has to pay equal monthly payments.

What is the actual interest Alice is being charged?

Step 2: Calculate the monthly payment

P = $102,040.82

i = 0.0725/12

n = 15 × 12

R = $931.49

ni

iPR

)1(1

Math 1140 - Financial Mathematics34

Alice takes out a 15 years, $100,000 loan from a bank charging 2 points and 7.25%(12) interest. The points are added to the loan. Alice has to pay equal monthly payments.

What is the actual interest Alice is being charged?

Step 3: Calculate the monthly interest rate

P = $100,000

i = 0.0725/12

n = 15 × 12

R = $931.49

Monthly interest rate is 0.6316%

The nominal interest rate is 7.5792%.

Math 1140 - Financial Mathematics35

Monday

Read sections 6.1 and 6.2

Nov 11 (next Friday)

Project Progress Report

Dec 8 (a little over a month)

FINAL!!!!

Charge