Embed Size (px)

Citation preview

The geographical breadth of coverage in this latest issue of the Legal and Regulatory Bulletin illustrates the ripple effects – sometimes substantial – which regulation can have on our asset class regardless of its origins. In particular, this issue examines the consideration set for investors new to emerging market private equity and provides guidance as to how changing regulations can open up new sources of capital for fund managers. We start the issue with a Guide for New Investors in Emerging Markets, provided by Mara Topping of White & Case. The Guide highlights key considerations for investors committing capital to emerging market private equity funds for the first time. While there is no fundamental legal distinction between private equity funds established to invest in emerging as opposed to developed markets, such vehicles are often evaluated rather differently in practice by investors. Ying White of Clifford Chance then examines an exciting opportunity for fund managers to ac-cess Chinese insurance capital thanks to recent China Insurance Regulatory Commission (CIRC) regulations that lower the entry barriers and expand the eligible investment options for the country’s increasingly wealthy insurance companies. This ground-breaking shift in regulation could create a win-win situation for Chinese insurance companies seeking diversified returns and global fund managers seeking capital, as well as a blueprint for other nascent private equity markets where domestic institutions’ investment portfolios remain largely undiversified. In our coverage of global regulatory developments, the teams at SJ Berwin and AZB & Partners provide examples of how regulation from the US, Europe and India is having broader ripple ef-fects on our industry. Designed to tackle tax avoidance by US taxpayers, the FATCA regulation is having sweeping effects on the international investment community and presents challenges for fund managers managing comingled pools of capital from diverse sources. The European AIFM Directive is as far reaching, and SJ Berwin provides practical steps for implementation and a rationale for continuing use of Luxembourg as a gateway to accessing capital and op-portunities in Europe. AZB updates us on the ramifications of India’s SEBI (Investment Advisers) Regulations, which mark an important milestone in bringing the Indian securities markets up to global standards. To respond to and shape these currents in the regulatory landscape, EMPEA is working to in-troduce the EMPEA Legal & Regulatory Guidelines as a framework for continued discussions with regulators. Last month, the Guidelines served as a starting point for discussions led by the Moroccan private equity and venture capital association, AMIC, with Moroccan government officials, regulators and local industry stakeholders in relation to potential reforms that could enhance the environment for private equity and help to create a central hub of financial activ-ity for the North and West African region. We continue to explore opportunities to grow the asset class drawing on the Guidelines, which have now been translated into French with other versions soon to come. The French version of the Guidelines will be available on our website at www.empea.org/resources/empea-guidelines/. We invite EMPEA Members to alert us to opportunities to partner with local organizations to dis-cuss and overcome regulatory challenges and look forward to continuing the dialogue face-to-face in Washington this May at the Global Private Equity Conference. In the interim we await your com-ments and suggestions, which can as always be shared with Jennifer Choi at [email protected]. Sincerely, Mark Kenderdine-DaviesGeneral Counsel and Company Secretary, CDC Group plcChair, EMPEA Legal & Regulatory Council

A Publication of the Emerging Markets Private Equity Association

Issue No. 8 – Spring 2013

Legal & Regulatory Bulletin

Contents

Risk Mitigation in Fund Documents: A Guide for New Investors in Emerging Markets ...............3

Accessing Chinese Insurance Capital .................6

Investment Adviser Regulations: A New Regime in India .................10

FATCA Fun for Funds .........13

Alternative Investment Fund Managers – Luxembourg’s Attractive Features on Substance and Delegation ..................16

EMPEA Legal and Regulatory Timeline ...........19

EMPEA Legal and Regulatory Guidelines Update ..............................23

1077 30th Street NW, Suite 100 Washington DC 20007 USAPhone: +1.202.333.8171 Fax: +1.202.333.3162 Web: empea.org

About EMPEA

The Emerging Markets Private Equity Association (EMPEA) is an independent, global membership association whose mission is to catalyze the development of private equity and venture capital industries in emerging markets. EMPEA’s 320+ member firms share the belief that private equity can provide superior returns to investors, while creating significant value for companies, economies and communities in emerging economies. Our members include the leading institutional investors and private equity and venture capital fund managers across developing and developed markets. EMPEA leverages its unparalleled global industry network to deliver authoritative intelligence, promote best practices, and provide unique networking opportunities, giving our members a competitive edge for raising funds, making good investments and managing exits to achieve superior returns. EMPEA’s members represent nearly 60 countries and more than US$1 trillion in assets under management.

1077 30th Street NW • Suite 100 • Washington, DC 20007 USAPhone: +1.202.333.8171 • Fax: +1.202.333.3162 • Web: empea.org

EMPEA Team

Jennifer ChoiActing CEO Shannon StroudVice President, Programs and Business Development Phillip ReidFinancial Controller Nadiya SatyamurthySenior Director, Research Department Mike CaseyDirector, Consulting Services Holly FreedmanDirector of Marketing and Communications Kyoko TeradaSenior Manager, Member Services

To learn more about EMPEA or to request a membership application, please send an email to [email protected].

Emily SandhausManager, Programs & Events

Carolyn KolbManager, Marketingand Communications Ted HickeyManager, Data Program Neeraj BorleAnalyst, Research Jeff SchlapinskiAnalyst, Research Sam VerranAnalyst, Research Aisha RichardsonExecutive Assistant tothe CEO, Office Manager

EMPEA Legal & Regulatory CouncilMark Kenderdine-Davies (Chair) CDC Group plc

David Baylis Norton Rose

Carolyn Campbell Emerging Capital Partners

Folake Elias-Adebowale Udo Udoma & Belo-Osagie

Laura Friedrich Shearman & Sterling LLP

Kem Ihenacho Clifford Chance

Geoffrey Kittredge Debevoise & Plimpton LLP

Prakash Mehta Akin Gump Strauss Hauer & Feld LLP

Zia Mody AZB & Partners

John Morgan Pantheon

Peter O’Driscoll Orrick, Herrington & Sutcliffe LLP

Paul Owers Actis

Mara Topping White & Case LLP

Jordan Urstadt Capital Dynamics

Solomon Wifa O’Melveny & Myers

Simon Witney SJ Berwin

Disclaimer: This material should not be construed as professional legal advice and is intended solely as commentary on legal and regulatory developments affecting the private equity com-munity in emerging markets. The views expressed in this bulletin are those of the authors and not necessarily those of their firms. If you would like to republish this bulletin or link to it from your website, please contact Holly Freedman at [email protected].

EMPEA Legal & Regulatory Bulletin Spring 2013 3

Risk Mitigation in Fund Documents: A GUIDE FOR NEW INVESTORS IN EMERGING MARKETSBy Mara Topping, White & Case LLP

I. IntroductionThere is no fundamental legal distinction between a pri-vate equity fund established to invest into emerging as opposed to developed markets. However, in practice, the legal terms customarily incorporated into the constitutive legal documents of emerging markets funds differ consider-ably from those included in developed market fund papers. This distinction is evident despite the general application of the ILPA guidelines and irrespective of the total size of any particular fund’s capital commitments. For commercial and institutional investors turning their attentions increasingly to the emerging markets investment space, such emerging markets legal terms may be unfamiliar and even discon-certing as to the level of active investor involvement. This paper will not only identify for those commercial investors some of the important distinctions between emerging and developed markets legal terms but also suggest that, given the (real or perceived) increased risk of emerging markets investment, the incorporation of distinctive legal terms in emerging markets fund documentation may provide con-siderable risk mitigation.

Risk mitigation involves not only the insertion into the emerging markets fund documents of activist investor provisions but also protecting the most basic thesis behind the private equity investment fund blind pool structure— management by an active sponsor team of an investment pool contributed to by passive investors. The sponsor/manager is selected by investors (presumably because of expertise in the relevant fund investment strategy and the ability to manage such investment pools) and granted man-agement authority. By accepting investment management

authority, the sponsor/manager often assumes fiduciary duties to the fund and in many instances (depending on the fund structure), unlimited liability. On the other hand, in exchange for relinquishing management authority, the investors obtain critical limited liability protection. Investor oversight and activism and the risk mitigation this affords must not cross the line and cause the loss of investor limited liability or tie the hands of the manager to efficiently operate the fund on the investors’ behalf.

II. Distinctive Aspects Of Emerging Markets Legal DocumentationThere are five broad aspects frequently handled distinctive-ly in emerging markets fund constitutive legal documents: (i) the balance of authority between the fund sponsor and the fund investors, (ii) investor oversight over day-to-day fund operations, (iii) investor oversight over the internal workings of the sponsor team, (iv) transparency, monitoring and reporting and (v) the ability to “pull the plug” whether on the manager or the fund as a whole.

I. Balance of Authority between Sponsors and InvestorsIn emerging markets fund legal documents, the balance of authority is frequently tipped much more heavily towards investors than in developed markets fund documentation. Investor advisory committees for emerging markets funds often play a role in far more issues than conflicts of interest and valuations as would be typical in developed markets legal papers. Differing from fund to fund, emerging mar-kets investment advisory committees may weigh in on e.g. settlements involving fund indemnity obligations, caps on expenses of fund committees, or waivers on diversification and other investment restrictions. In addition, sharehold-ers may directly engage on matters that are more typically deferred to managers in the developed markets. Such in-creased shareholder roles may include e.g. consent to the granting of time for a defaulting investor to cure, the right to require an interim audit or the ability of the fund to incur debt. In emerging markets, investor representatives may even sit on the investment committee of the fund although this is increasingly rare and generally limited to representa-tives of anchor investors only and the investment committees of first time fund managers.

“Risk mitigation involves not only the insertion into the emerging markets fund documents of activist investor provisions but also protecting the most basic thesis behind the private equity investment fund blind pool structure— management by an active sponsor team of an investment pool contributed to by passive investors.”

© 2013 Emerging Markets Private Equity Association4

II. Investor Oversight over Day-to-Day Fund OperationsWhether with regard to the incurrence of on-going oper-ating expenditures or payment of extraordinary expenses, emerging markets funds documents typically grant far more consent rights over the incurrence of fund expenses. This frequently includes strict caps on broken deal expenses, caps on regulatory compliance expenditures (often subject to investor advisory committee waiver) and even, in the very rare instance, caps on overall fund expenses, whether annual or over the term of the fund (again often subject to advisory committee waiver). In addition certain expenses frequently relegated to the fund in the developed markets legal documents are firmly shifted one hundred percent to the manager, notably travel expenses. Cash management is also typically more precisely set forth in emerging markets fund legal documentation. Rather than rely on the align-ment of interest and impact on overall IRR as is typical in the developed markets papers, the emerging markets legal documents frequently specifically cap operating reserves at a sum certain or percentage of capital commitments. Further, unused capital contributions and investment proceeds must be returned or distributed out to investors within a specified short number of days and even the types of accounts wherein temporary investments may be held are carefully defined.

III. Investor Oversight over the Internal Workings of the Sponsor TeamAlthough key person provisions are important in both emerging markets and developed markets funds and change of control provisions are also increasingly prevalent in both types of legal documents, emerging markets legal documents may reach much further into the internal work-ings of the sponsor team. To ensure alignment of interest

and adequate incentivizing of manager team personnel, this detail may include an obligation to report on the carried interest allocation plan of the manager, investor consent rights over changes to carried interest allocations amongst the manager team and restrictions on the assignment of carried interest to outside third parties.

An additional level of oversight of the manager’s operations may be introduced into emerging markets legal documenta-tion with respect to third-party service providers. Emerging markets legal documents may require such independent service providers (such as e.g. auditors or tax advisors) to undertake a review and issue a certification regarding the manager’s operations including with respect to such items as whether VAT calculations accurately reflect local tax regimes or if the manager’s allocations of funds flows conform to the requirements of the fund’s constitutive legal documents. This may include verifying e.g. waterfall calculations, the escrow and even carried interest distributions.

IV. Transparency, Monitoring and ReportingLargely due to the important historical and ongoing role of the development financial institutions in the emerging markets investment sphere, emerging markets fund legal documents typically require an extensive set of reports to investors that go well beyond the customary annual and quarterly financials generally required in the developed markets. Not only is required monitoring and reporting on environmental and social impacts general practice in the emerging markets fund documents, but there are typically also detailed narrative description requirements regard-ing fund portfolio investments. Legal documents also frequently provide emerging markets investors with broad access not only to the books and records of the fund but also to the books and records, site and even management of the underlying portfolio companies themselves.

Although provisions regarding anti-money laundering, anti-terrorism, anti-bribery and other anti-corrupt practices are increasingly prevalent in both developed and emerging markets legal documents, emerging markets legal docu-ments typically contain even more specific requirements regarding prohibited payments and investor involvement in monitoring certain AML and anti-corruption matters. For example, it is fairly common for the manager of an emerg-ing markets fund to provide advance notification to existing investors of potential new investors so that existing investors can conduct their own independent “know-your-customer” due diligence.

“ Largely due to the important historical and ongoing role of the development financial institutions in the emerging markets investment sphere, emerging markets fund legal documents typically require an extensive set of reports to investors that go well beyond the customary annual and quarterly financials generally required in the developed markets.”

EMPEA Legal & Regulatory Bulletin Spring 2013 5

V. The Ability to “Pull the Plug”Whether due to concerns regarding the viability of an emerging markets manager team or risks arising from the potential volatility of one or another emerging market, it is customary for emerging markets legal documents to enable the removal of the manager or the termination of the fund upon a vote of the investors. This means that emerging markets fund documents not only include a provision for removal for cause as is typical also in the developed markets but also provisions for “no cause” removal, a legal provision more rarely accepted by developed markets managers.

Provisions not uncommon in emerging markets legal docu-mentation also enable investors to respond and take action in response to changes in the viability of the fund strategy. This may include not only a provision to shut down the fund if a minimum commitment size is not achieved by a date certain, but also provisions granting a unilateral right to investors to vote to terminate the investment period of a fund or the unilateral right to terminate the fund, entirely.

VI. ConclusionThere is, of course, diversity of legal documentation within the emerging markets themselves and a frequent increase in the oversight of first-time fund managers or frontier mar-ket targeted funds. Nonetheless, provisions ranging from increased investor authority, ongoing investor oversight in day-to-day fund operations, investor reach into the internal workings of the sponsor team, transparency, monitoring and reporting obligations and the ability of investors to “pull the plug” on the manager or the fund, provide for far greater investor activism in emerging markets fund docu-ments than in developed markets legal documents. Such increased investor engagement enables investors to gauge the “pulse” of the emerging markets fund in which they are invested and respond to risks and vicissitudes that may be faced by an emerging markets fund over its term.

About the Author

Mara Topping is a Partner with White & Case’s Capital Markets practice group.

Disclaimer: This material should not be construed as pro-fessional legal advice and is intended solely as commentary on legal and regulatory developments affecting the private equity community in emerging markets. The views expressed in this bulletin are those of the authors and not necessarily those of their firms. If you would like to republish this bulletin or link to it from your website, please contact Holly Freedman at [email protected].

“ Such increased investor engagement enables investors to gauge the “pulse” of the emerging markets fund in which they are invested and respond to risks and vicissitudes that may be faced by an emerging markets fund over its term.”

© 2013 Emerging Markets Private Equity Association6

Accessing Chinese Insurance CapitalBy Ying White, Clifford Chance LLP

Chinese institutional investors have been playing an increas-ingly important role in the global investment management industry. However, to date, only a handful of Chinese institu-tions, namely, CDB Capital, China Investment Corporation, the State Administration of Foreign Exchange and the National Social Security Fund are able to make allocations to overseas investment funds. Additionally, there is a sizeable amount of insurance funds in China, which has reached RMB 6,900 billion (approximately US$1,105 billion) by September 2012 according to statistics published by the China Insurance Regulatory Commission (“CIRC”). Recent CIRC regulations governing global investments of the Chinese insurance capi-tal lowered the entry barriers for many of the participants and expanded the eligible asset classes that insurance capi-tal may invest in. This presents an exciting opportunity for international managers looking to raise funds in China.

Evolution of the Global Investment Regime of Chinese Insurance Capital The first set of rules governing the overseas investment of insurance capital was the Interim Measures for the Overseas Deployment of Insurance Foreign Exchange Funds promul-gated by CIRC and the People’s Bank of China (“PBoC”) on August 9, 2004 (2004 Interim Measures) and its accompany-ing implementing rules issued by CIRC on September 1, 2005. In 2007, a separate “qualified domestic institutional investor” (“QDII”) regime was established under the Interim Measures for Overseas Investment of Insurance Capital promulgated by CIRC, PBoC and the State Administration of Foreign Exchange (“SAFE”) on June 28, 2007 (2007 Interim QDII Measures), which replaced the 2004 Interim Measures.

The 2007 Interim QDII Measures provided a general frame-work whereby insurance capital could be invested overseas. However, it did not contain any operational details and there was not an active global investment program for the Chinese insurance capital. Since 2007, CIRC circulated sev-eral consultation drafts of implementing rules for internal industry discussion, with the final rules, Implementing Rules of the Interim Administrative Measures on the Overseas Investment of Insurance Capital, issued on October 12, 2012 (CIRC QDII Implementing Rules).

The new CIRC QDII Implementing Rules reflected some ground-breaking changes in the overseas investment regime concerning the insurance capital, including increased asset classes in which insurance capital may invest, and more flexible quantitative ceilings on investments. This signaled

that the Chinese insurance regulator has begun to place more emphasis on improving investment returns and asset-liability management of Chinese insurers. As a result, there will be many opportunities for international private equity firms that are interested in exploring the newly revamped insurance QDII regime.

Key Features of the Expanded Insurance QDII Program Overall Limit on Global Investments The new CIRC QDII Implementing Rules set an overall limit of 15% of an insurer’s total assets as of the preceding year that can be invested globally. It means in theory, approxi-mately US$166 billion of insurers’ assets would be available for global investments. In practice, however, only a portion of this amount can be deployed abroad, as only “qualified” Chinese insurers can take advantage of this program and the qualification criteria tend to favor large insurance companies.

Eligible MarketsThe new rules expanded the eligible markets in which the insurance capital can invest from Hong Kong to 25 devel-oped countries and economies and 20 emerging market countries and economies. These emerging markets are Brazil, Chile, Colombia, the Czech Republic, Egypt, Hungary, India, Indonesia, Korea, Malaysia, Mexico, Morocco, Peru, the Philippines, Poland, Russia, South Africa, Taiwan, Thailand and Turkey. China is excluded from the list of eligible markets on the theory that for any investments in China, insurers can invest as a domestic investor and be entitled to much more flexibility and less regulatory restrictions.

Eligible Asset ClassesEligible investment assets are greatly expanded to include:

• money market products

• commercial papers with a term not longer than 1 year

• bank negotiable instruments

• negotiable certificates of deposit in large denominations

• reverse repurchase agreements

• short term government bonds

• overnight lending

• fixed income products

• bank deposits

• government bonds

• government-backed bonds

• international financial organization bonds

EMPEA Legal & Regulatory Bulletin Spring 2013 7

• corporate bonds

• convertible bonds

• equity products

• common stocks

• preferred stocks

• global depositary receipts

• American depositary receipts

• private equity

• real estate

Among the new asset classes, global private equity and real estate investments have captured a lot of attention from the private funds industry, as other parallel overseas investment programs administered by the Chinese banking regulator and the securities regulator have not elevated private equity or real estate investments to permissible asset classes.

The CIRC QDII Implementing Rules allow the AUM of the parent company or asset management institutions within the same group of an international manager to be calcu-lated on a consolidated basis. However, assets managed by or related to investment advisors or investment banks are excluded from such calculation.

In addition, an international manager seeking specialized mandates can consider qualifying for “specialist asset management”, which has a lower AUM criteria. Thus, if (i) a specialist manager has an AUM of not less than US$5 billion; (ii) its specialist assets under management account for not less than 70% of the total AUM; and (iii) it has a good reputation and outstanding performance in special-ized asset management, such manager can seek to manage a specialist mandate (e.g., real estate, infrastructure).

Investments in Private Equity Funds and FoFs and Direct InvestmentsThe rules in this area largely mirror the rules applicable for investment of insurance capital in domestic Chinese private equity funds and FoFs. An insurer’s maximum exposure to direct private equity investments as well as private equity funds is 10% of the insurers’ total assets at the end of the preceding quarter. What remains to be clarified is whether this 10% ceiling applies only to an insurer’s overseas invest-ments or whether it is an aggregate cap of an insurer’s overseas and domestic investments in the private equity asset class.

Separately, international private equity sponsors have to meet a few eligibility criteria, including (i) a paid-in capital or net assets of not less than US$15 million and (ii) an AUM of US$1.0 billion.

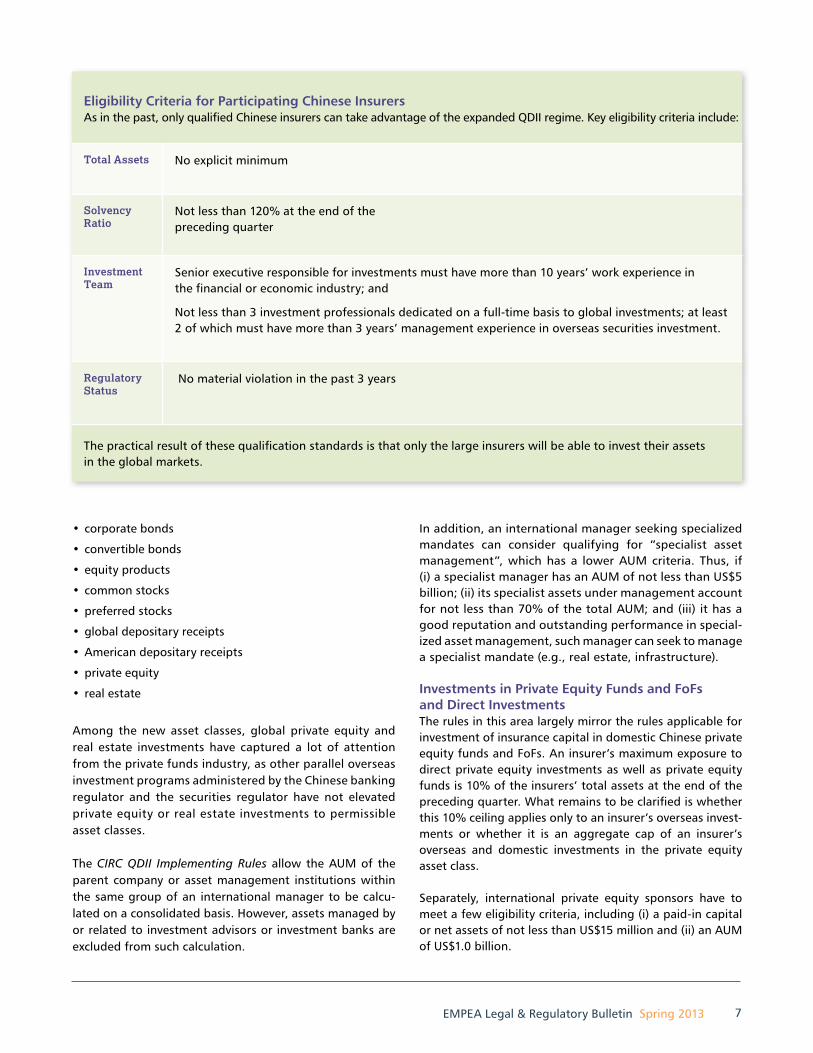

Eligibility Criteria for Participating Chinese Insurers As in the past, only qualified Chinese insurers can take advantage of the expanded QDII regime. Key eligibility criteria include:

Total Assets No explicit minimum

Solvency Ratio

Not less than 120% at the end of the preceding quarter

Investment Team

Senior executive responsible for investments must have more than 10 years’ work experience in the financial or economic industry; and

Not less than 3 investment professionals dedicated on a full-time basis to global investments; at least 2 of which must have more than 3 years’ management experience in overseas securities investment.

Regulatory Status

No material violation in the past 3 years

The practical result of these qualification standards is that only the large insurers will be able to invest their assets in the global markets.

© 2013 Emerging Markets Private Equity Association8

Chinese insurance companies are now also permitted to make direct investments in a handful of industries and sectors, which are seen as closely relevant to the normal “insurance” business of Chinese insurers. These sectors include financial institutions, senior citizen nursing, medi-cal care, energy, resources, automobile service and modern agriculture. It is believed that familiarity with these indus-tries will contribute positively toward an insurer’s investment due diligence, execution and management and facilitate a win-win investment.

Investments in Real EstateInsurance capital can now be directly invested in foreign real properties, as long as they are in the core districts of major urban areas of eligible “developed market counties or economies”. Investments in mature commercial property and office buildings in those markets are also permitted, pro-vided that the underlying property is capable of generating a steady cash flow. Insurers’ capital can also be invested in REITs traded on stock exchanges of all Eligible Markets.

Investments in Hedge FundsHedge funds was included as an eligible asset class to which insurers can allocate capital in an earlier consultation draft of the rules. However, the final rules removed hedge funds without further explanation. This legislative history has made market participants hopeful that hedge funds may become an eligible asset class for insurance capital in due course. CIRC has indicated that it will issue further guidance on the QDII Implementation Rules. It remains uncertain as to whether hedge funds would make the list of eligible asset classes in the near future.

Comparison Between Insurance QDII Regime and Other QDII RegimesCompared to the overseas investments regimes adminis-tered by the China Banking Regulatory Commission and the China Securities Regulatory Commission, the QDII regime administered by CIRC allows insurance capital to be invested in a broader range of products (such as real estate) and asset classes. Still, all QDII regimes share certain common

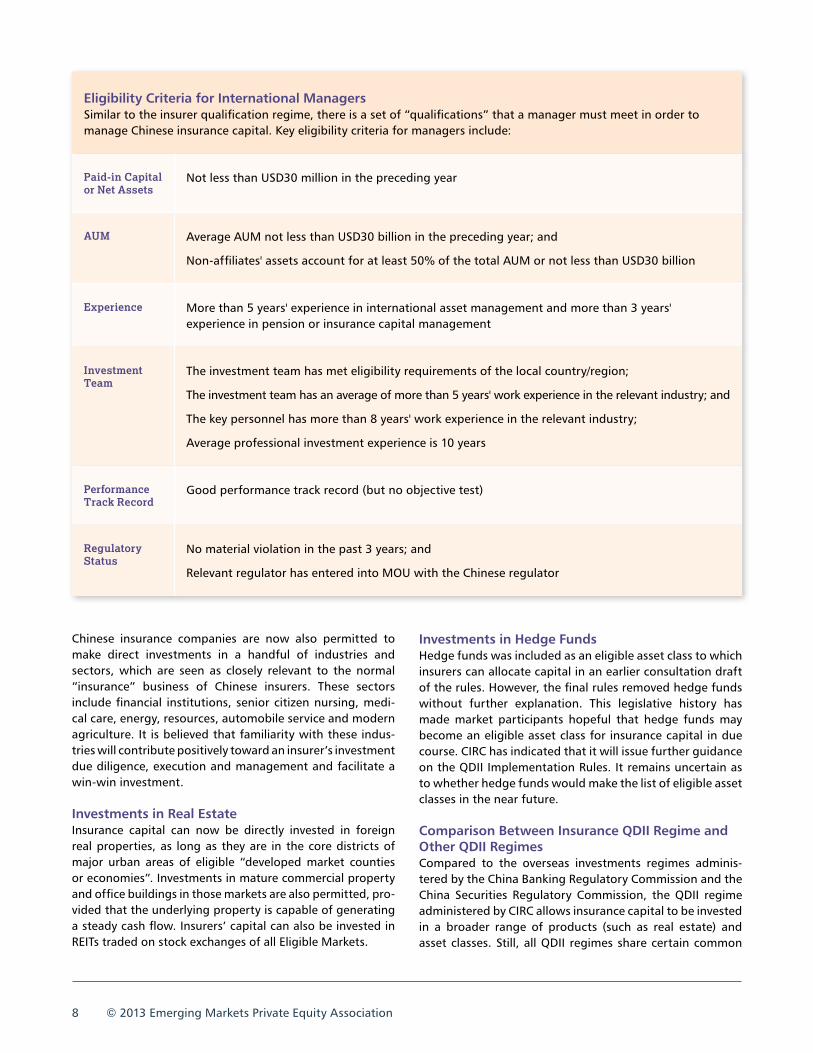

Eligibility Criteria for International Managers Similar to the insurer qualification regime, there is a set of “qualifications” that a manager must meet in order to manage Chinese insurance capital. Key eligibility criteria for managers include:

Paid-in Capital or Net Assets

Not less than USD30 million in the preceding year

AUM Average AUM not less than USD30 billion in the preceding year; and

Non-affiliates' assets account for at least 50% of the total AUM or not less than USD30 billion

Experience More than 5 years' experience in international asset management and more than 3 years' experience in pension or insurance capital management

Investment Team

The investment team has met eligibility requirements of the local country/region;

The investment team has an average of more than 5 years' work experience in the relevant industry; and

The key personnel has more than 8 years' work experience in the relevant industry;

Average professional investment experience is 10 years

Performance Track Record

Good performance track record (but no objective test)

Regulatory Status

No material violation in the past 3 years; and

Relevant regulator has entered into MOU with the Chinese regulator

EMPEA Legal & Regulatory Bulletin Spring 2013 9

characteristics, including prohibiting direct investment in precious metals, commodity derivatives and physical commodities.

ConclusionEver since the Chinese national Insurance Law was first promulgated in 1995, insurance capital has been strin-gently regulated in terms of the entities that are allowed to manage it and the eligible asset classes in which it could be invested. The new QDII regulations initiated a breath of ground-breaking changes in how the insurance capital can be invested. They are a testimony to the Chinese regulator’s resolution to enhance the returns on insurance capital by bringing market competition into this important sector. We are hopeful that this embrace of market mechanism will represent the beginning of a win-win proposition for all parties involved.

About the Author

Ying White is a Partner at Clifford Chance’s Beijing office and leads the firm’s China Investment Funds Practice.

Eligibility Criteria for Private Equity Funds and FoFs:

Fund Strategy Limited to growth, mature and buy-out strategies

Fund Geographic Restriction

None

Committed Capital of Fund

Not less than USD 300 million

Contributed Capital of Fund

Contributed pro rata

Governance Must have effective key person mechanisms

Must have an effective compensation system

Investment Team

Not less than 10 investment professionals;

At least 2 are senior investment professionals with not less than 8 years experience in fund raising, fund management and exit management and have managed at least 5 exits;

At least 3 key investment personnel have not less than 3 years experience in fund management.

Maximum Investment in a Single Fund

20% of total target size of the fund

General Partner Affiliated with Financial Institutions

Proof of investment team independence from the group or affiliates

Disclaimer: This material should not be construed as pro-fessional legal advice and is intended solely as commentary on legal and regulatory developments affecting the private equity community in emerging markets. The views expressed in this bulletin are those of the authors and not necessarily those of their firms. If you would like to republish this bulletin or link to it from your website, please contact Holly Freedman at [email protected].

For a more detailed review of the liberalization of the Chinese insurance sector, please see Clifford Chance client briefing, “China Liberalizes Insurance Capital Investment Regulations”.

© 2013 Emerging Markets Private Equity Association10

Investment Adviser Regulations: A NEW REGIME IN INDIABy Darshika Kothari & Aditya Jhaveri, AZB & Partners, Advocates & Solicitors

In the early days of February 2013, Richard Ketchum CEO and Chairman of the Financial Industry Regulatory Authority (“FINRA”), drew the curtains on a debate that threatened to alter the regulatory landscape for the roughly 11,000 strong United States investment adviser industry. The debate centered on regulatory oversight of invest-ment advisers – while investment advisers are currently governed by the U.S. Securities and Exchange Commission (“SEC”), FINRA had been making concerted efforts to bring them in its fold since about 2008. Having met with severe opposition from various investment adviser bodies and a not-too-forthcoming U.S. House of Representatives, FINRA (for now) abandoned its efforts.

This forms an interesting backdrop for events closer to home in India. On the 21 January 2013, the Securities and Exchange Board of India (“SEBI”) released the final SEBI (Investment Advisers) Regulations, 2013 (“IA Regulations”). Investment advisers were previously unregulated in India. With the enactment of the IA Regulations, SEBI has finally sought to plug this gap. In fact, SEBI has long sought to regulate investment advisers as is demonstrated by two consultative papers on the subject issued by SEBI in 2007 and 2011.

These regulations are an important milestone in SEBI’s attempts to bring the Indian securities markets in line with global standards. Having had the benefit of accessing the regulation of investment advisers in developed jurisdictions, SEBI in its 2011 consultative paper had sought for invest-ment advisers to be regulated through a self regulatory organization. This intention was perhaps in line with experi-ences from jurisdictions such as the United States where FINRA claims that the SEC has struggled with resources for effective oversight of the investment adviser ecosystem – on average it apparently only manages to inspect the books of each investment adviser once in 11 years . However, to avoid any potential teething issues which a new self regula-tory organization may have, the IA Regulations provide for regulatory oversight by SEBI with the power to recognize a self regulatory organization for regulation of investment advisers at a later date.

Coming to the crux of the regulations, SEBI has defined “investment advice” as advice relating to investing in,

purchasing, selling or otherwise dealing in securities or investment products, and advice on an investment portfolio containing securities or investment products, whether writ-ten, oral or through any other means of communication for the benefit of the client and includes within its scope finan-cial planning. An investment adviser is defined as a person who for consideration is engaged in the business of provid-ing investment advice and includes any person who defines himself as an investment adviser, by whatever name called.

Three relevant points emerge from the definitions of invest-ment advice, investment advisers and the categories of persons exempt from registration requirements as invest-ment advisers:

• As part of the regulations, investment advice provided exclusively to foreign residents is exempt. Notably however, the regulations are silent on exemption on the basis of the underlying security for which advice is given – i.e. whether the security itself is foreign or domestic. All investment advice provided to Indian residents on domestic securities is covered under the IA Regulations. The broad definition of “securities” that may be borrowed from Section 2(h) of the Securities Contracts (Regulation) Act, 1956, implies that advice given to Indians on foreign securities is also covered under the regulations and investment advisers who provide investment advice to Indians on foreign securities may pos-sibly need to register themselves under the IA Regulations.

• Presently, portfolio managers (commonly known as wealth managers) are governed by the SEBI (Portfolio Managers) Regulations, 1993. The primary activities of portfolio man-agers typically involve administration or management of a portfolio of securities and rendering advice in relation

“These regulations are an important milestone in SEBI’s attempts to bring the Indian securities markets in line with global standards.”

EMPEA Legal & Regulatory Bulletin Spring 2013 11

to the portfolio of securities. To the extent that portfolio managers are involved primarily in providing investment advice and do not administer or manage their clients’ portfolio, SEBI’s intention appears to be to eventually regulate such persons under the IA Regulations.

• The IA Regulations are likely to have a significant impact on small independent investment advisers who were so far not regulated and who would now be caught under the net of the IA Regulations. The IA Regulations man-date an investment adviser to maintain an arm’s length relationship between its investment advisory activities and other activities and the smaller independent financial advisers may find it difficult to create different depart-ments for distribution and advisory.

• SEBI has also exempted a number of entities from manda-tory registration as an investment adviser. These include an insurance agent or broker offering advice solely for insurance products, a pension adviser advising on pen-sion products, a mutual fund distributor providing advice incidental to its primary activity, advocates, solicitors, law firms, chartered accounts, company secretaries, cost accountants, actuaries and fund managers of mutual funds and alternative investment funds, providing advice incidental to their primary activity.

In addition, stock brokers, portfolio managers and mer-chant bankers are also exempt; however, they would be required to comply with the general obligations of investment advisers as stated in the IA Regulations. These general obligations (applicable to all investment advisers and specifically also to stock brokers, portfolio managers and merchant bankers despite being exempt from regis-tration) require an investment adviser to act in a fiduciary capacity towards its clients, disclose all conflicts of inter-est when they arise, maintain an arm’s length relationship between activities as an investment adviser and other activities, maintain a high degree of confidentiality and critically, restricting receipt of consideration from any per-son other than the client being advised.

Maintaining an arm’s length relationship between activities as an investment adviser and other activities would entail creating information barriers between the investment advi-sory arm and other activities carried out by the same entity. In the Indian context, advisory functions are often housed in the same legal entity which also carries out broking/investment banking and other activities. It therefore remains to be seen if the mandated system of information barriers will be effective. Where two separate divisions of

an enterprise have been maintained, will such divisions be able to receive compensation in relation to the same prod-ucts – for investment advisory services from an investor and for other services (such as investment banking), from the product provider or issuer of the product?

Prior to the IA Regulations, there was no restriction on an investment adviser from receiving consideration from both the product provider and the client being advised, which often resulted in conflicts of interest. A restriction on receipt of consideration from any other person than the client being advised seeks to perhaps address this concern. While SEBI’s intentions seem to be to protect the interest of the investors, market practice in India is to the contrary. Typically investment advisers in India receive consideration from product providers and not the investors and, therefore, this restriction may impose additional costs on investors.

The IA Regulations also list a number of other responsi-bilities for investment advisers. A stock broker, for example, cannot invest in a contrary fashion in a security it has pro-vided advice for up to a period of 15 days (it must provide advance intimation to its client 24 hours in advance if it proposes to do so). Other responsibilities include maintain-ing risk profiling standards, comprehensive disclosures of all possible material information, maintaining a record of rationale through which the advice given was determined as well as determining full suitability of a client to the advice provided and record maintenance requirements.

“The IA Regulations are likely to have a significant impact on small independent investment advisers who were so far not regulated and who would now be caught under the net of the IA Regulations.”

© 2013 Emerging Markets Private Equity Association12

In terms of eligibility requirements, SEBI has prescribed qualification norms for an investment adviser. Capital adequacy for corporate investment advisers is approxi-mately US$50,000 (INR 2.5 million) and that of individuals or partnership firms is approximately US$2,000 (INR 0.1 million). An investment adviser must have a professional qualification or a post-graduate degree or diploma and also a minimum of five years previous experience in finan-cial markets. SEBI has also directed investment advisers to, within a period of two years from commencement of the IA Regulations, get certified through an appropriate course with the National Institute of Securities Market (“NISM”) (an autonomous public trust originally set up by SEBI to promote securities education) or any other accredited NISM course.

Retail Indian investors have long clamored for reliable, trustworthy and responsible investment advice. The SEBI-mandated definition of an investment adviser is sweeping and covers a wide range of intermediaries. Regardless of who it comes from, the general flavor of investment advice for Indian investors often doesn’t live up to the highest fidu-ciary standards. A product-pushing approach, a conscious overlook of customer understanding and an entrenched product-centric (rather than customer-centric) characteris-tic of financial counsel are all unfortunate, but real features of investment advice today. While trying to strike the right balance between getting the unregulated investment advis-ers within its fold and protecting the securities market in India, some may argue that the IA Regulations unwittingly overregulate the unorganized sector of investment advisers by imposing onerous conditions on compensation in addi-tion to other compliances and procedures to be followed. Effective implementation of the regulations will remain the biggest challenge and the industry hopes for a pragmatic approach by the regulator.

Disclaimer: This material should not be construed as professional legal advice and is intended solely as commentary on legal and regulatory developments affecting the private equity community in emerging markets. The views expressed in this bulletin are those of the authors and not necessarily those of their firms. If you would like to republish this bulletin or link to it from your website, please contact Holly Freedman at [email protected].

About the Authors

The co-author is a Partner at AZB & Partners, Advocates & Solicitors, India.

The co-author is an Associate at AZB & Partners, Advocates & Solicitors, India.

The co-author is a Partner at AZB & Partners, Advocates & Solicitors, India. Views expressed are personal

The co-author is an Associate at AZB & Partners, Advocates & Solicitors, India. Views expressed are personal

For more information on the FINRA story, please see: http://newsandinsight.thomsonreuters.com/Securities/News/2013/ 02_-_February/Exclusive__U_S__watchdog_backs_off_over_financial_ adviser_regulation/

“Effective implementation of the regulations will remain the biggest challenge and the industry hopes for a pragmatic approach by the regulator.”

EMPEA Legal & Regulatory Bulletin Spring 2013 13

Over recent years the US FATCA disclosure regime, designed to tackle tax avoidance by US taxpayers, has become all too familiar to financial institutions the world over. This article does not attempt to explain the rules and regulations in detail, as others have done, but instead considers some of the specific challenges it brings to the private equity world.

The Story So Far The US legislation known as the Foreign Account Tax Compliance Act (“FATCA”) and the US Regulations imple-menting it have the potential to impose a new 30% withholding tax on certain payments derived from US sources, if various reporting requirements are not met. That being said, the broad aims of FATCA were stated to be to address US tax non-compliance and to increase report-ing to the US Internal Revenue Service (“IRS”), and not to increase US tax revenues. FATCA withholding can therefore typically be prevented by agreeing to disclose information on account holders, as discussed further below.

However, focusing on the US withholding tax aspects can mask the global scope and significance of FATCA. Even for fund managers with no US investments or assets, non-com-pliance with FATCA may have commercial ramifications, as financial institutions are increasingly demanding FATCA compliance from those with whom they do business. A fund manager who manages no US investments is nonetheless likely, therefore, to find that investors and other financial institutions with which it deals, such as banks, custodians, etc. all demand FATCA compliance.

In short, FATCA is here to stay and it will require your attention.

Who Does FATCA Affect? FATCA applies differently to foreign financial institu-tions (“FFIs”) and non-financial foreign entities (“NFFEs”). Without going into the detailed definitions involved, the term FFI covers “investment entities” and potentially includes private equity fund entities, fund managers/advi-sors and private equity acquisition vehicles; this article therefore focuses on the position for FFIs.

FFIs that do not comply with FATCA are subject to 30% withholding on “withholdable payments”; which includes US source FDAP income and the gross proceeds of sale of property that could produce it. The US rules also require participating FFIs to operate “pass-thru” withholding where a payment is attributable to an underlying “withholdable

payment”. The pass-thru concept clearly takes FATCA beyond US territorial limits and is technically difficult to implement; given this, pass-thru withholding has been deferred until after 1 January 2017.

Complying with FATCAThe original compliance method set out in the US legisla-tion was for an FFI to become a “participating FFI” (“PFFI”) by entering into an “FFI Agreement” with the IRS. Pursuant to this FFI Agreement, the FFI agrees to a number of obli-gations including: (i) obtaining information in order to identify any “US account holders” (broadly, US citizens and entities owned by US citizens); (ii) reporting information on US accounts to the IRS; and (iii) withholding 30% of any pass-thru payment to “recalcitrant account holders” and FFIs that are not PFFIs, “deemed compliant”, or otherwise exempt (there being some narrowly drawn, low risk, cat-egories of FFI that are exempt from or deemed to comply with FATCA).

“Recalcitrant account holders” are those that either fail to comply with reasonable requests for identifying informa-tion, or fail to provide a waiver of foreign data protection laws enabling them to do so.

IGAsWhen FATCA was introduced, there was widespread con-cern as to its extra territorial scope and the practical aspects of compliance. These concerns included whether FFIs could legally comply with the requirements, for example, deduct-ing tax from relevant payments and disclosing an account holder’s details to the IRS, in particular given stringent data protection laws in many foreign jurisdictions.

It quickly became apparent that FATCA would not work as the US government had intended without the co-operation

FATCA Fun for Funds By Laura Charkin and Katy Webb, SJ Berwin LLP

“A fund manager who manages no US investments is nonetheless likely, therefore, to find that investors and other financial institutions with which it deals, such as banks, custodians, etc. all demand FATCA compliance.”

© 2013 Emerging Markets Private Equity Association14

of foreign governments. In light of this, the US government has developed “intergovernmental agreements” (“IGAs”) with certain “FATCA partner jurisdictions” in order to agree a common approach to implementation of FATCA. Two dif-ferent forms of model IGAs have been published; the UK led with entry into a “Model I” IGA, obliging UK FFIs to report information to the UK’s HM Revenue & Customs, which will be passed to the IRS, in exchange for reciprocal information reporting by the IRS. Under the “Model II” IGA (contem-plated by, amongst others, Japan), local FFIs are directed by the relevant foreign government to report directly to the IRS.

The advantage for an FFI that is resident in an IGA juris-diction is that it can be registered as “deemed compliant” with FATCA, without having to enter into an FFI Agreement. The local FFI will still be obliged to register with the IRS to obtain a “GIIN” (or a Global Intermediary Identification Number) and will be under a domestic law obligation to obtain and provide information on its account holders. However, as a result of being registered deemed compliant with FATCA, the local FFI should not be subject to, nor have to deduct, FATCA withholding, provided the terms of the IGA are complied with.

Among the emerging markets, Mexico has already entered into an IGA and according to the US Treasury, India, Brazil and Russia are each exploring a FATCA intergovernmental engagement with the US.

Notably absent from the US Treasury’s published list of those countries engaged in FATCA discussions, is China. Interestingly, and albeit speaking in a personal capacity, it has been reported that the deputy director general in the legal affairs department of the People’s Bank of China commented that an internationally coordinated approach should replace FATCA and declined to comment on whether or not the Chinese government was likely to enter into IGA discussions with the US.

In addition, several offshore jurisdictions commonly used in fund and deal structures in the emerging markets, including Mauritius, are also in discussions with the US with a view to entering into an IGA and in particular, the governments of Guernsey and Jersey have announced their intention to enter into an IGA with the US.

So What Do I Do Now?As explained above, most fund managers are thought likely to decide to become and remain “FATCA compliant”. Indeed those resident in IGA jurisdictions are likely to find themselves obliged under their local laws to report investor information, irrespective of whether they would have had any withholding risk under the original FATCA rules.

Fund managers will need to determine, firstly, whether or not each vehicle in their fund and deal structures is subject to FATCA and/or an IGA and, secondly, whether it is a finan-cial institution as defined for these purposes.

This is not always straightforward; for example, if the fund vehicle is a limited partnership established in Jurisdiction A, with a managing general partner established in Jurisdiction B and a local investment advisor established in Jurisdiction C, thought will need to be given as to how mainstream FATCA and/or (potentially) three possible IGAs apply. Much of the relevant legislation in the different jurisdictions does not yet exist and it may be that more than one regime is applicable.

Trying to implement a common international approach to various key concepts, such as where an FFI should be viewed as belonging for these purposes, has its problems. The US looks primarily to the jurisdiction in which the entity is organized, whereas others may be more used to a central management and control based residency test. If you then consider applying these concepts to partnerships (which are typically not thought of as tax “resident” entities), you can get some idea of the difficulties being faced. If not dealt with, these mismatches could lead to FFIs subject to duplicate reporting (under two different regimes) or falling between the gaps, and not able to rely on an IGA at all.

There also remain various discrepancies between concepts and definitions used in the US Regulations and the IGAs, because the final form of the US Regulations came out after many IGAs had already been signed, and contained sub-stantial changes to the draft regulations they replaced. For example, in the US Regulations it is made clear that a fund manager and an investment advisor are each FFIs, whereas under the IGAs it is less clear whether or not investment advisors are FFIs.

Similarly, in respect of holding companies used in group structures (“HoldCos”), under the US Regulations, a HoldCo that is a member of a non-financial group is treated as an “excepted NFFE”, and should not, therefore, be subject to FATCA withholding. Whereas any HoldCo formed in con-nection with or availed of by a collective investment vehicle, including private equity funds, will be treated as an FFI. This concept is not as yet reflected in the model IGAs and so, at present, the position for deal HoldCos is unclear under the IGA regime. This creates uncertainty, for example, in deal finance documentation, where a lender may seek represen-tations as to the HoldCo’s FATCA/IGA status.

One helpful new concept in the US Regulations, which does not as yet appear in the model IGAs, is that of a “sponsoring FFI”. Broadly, under the US Regulations, a fund manager is permitted to perform the due diligence and reporting for all of the FFIs that it manages on a consolidated basis. In this

EMPEA Legal & Regulatory Bulletin Spring 2013 15

About the Authors

Laura Charkin is a Partner at SJ Berwin LLP

Katy Webb is an Associate at SJ Berwin LLP

Disclaimer: This material should not be construed as pro-fessional legal advice and is intended solely as commentary on legal and regulatory developments affecting the private equity community in emerging markets. The views expressed in this bulletin are those of the authors and not necessarily those of their firms. If you would like to republish this bulletin or link to it from your website, please contact Holly Freedman at [email protected].

regard, any “sponsored FFIs” will be registered as deemed compliant, as long as the sponsoring entity agrees to per-form their FATCA obligations. It would clearly be helpful to replicate this in the model IGAs (and related domestic implementing legislation), although whether any of the FATCA partner jurisdictions are prepared to implement this on a cross-IGA basis remains doubtful. The broader ques-tion here is whether all IGAs will be amended to incorporate new concepts from the US Regulations.

Next Steps for Fund ManagersFund managers will need to review their fund structures, categorize each vehicle in the structure and ascertain the relevant FATCA/IGA requirements. Fund managers should also start to categorize their investors in FATCA terms, con-sider what investor information is already held and what further information may be required in order to comply. It will also be necessary to conduct a legal review of exist-ing fund documentation and on-boarding procedures, to establish whether the fund manager has the power to obtain the required information from investors, or whether changes to the documentation are needed.

Fund managers should also consider whether to ask inves-tors questions as to residency and ownership, etc. in general terms, to future proof against the introduction of similar new regimes. The UK government has already approached its crown dependencies, such as BVI, Cayman, the Channel Islands and the Isle of Man, in this regard and other jurisdic-tions may follow suit.

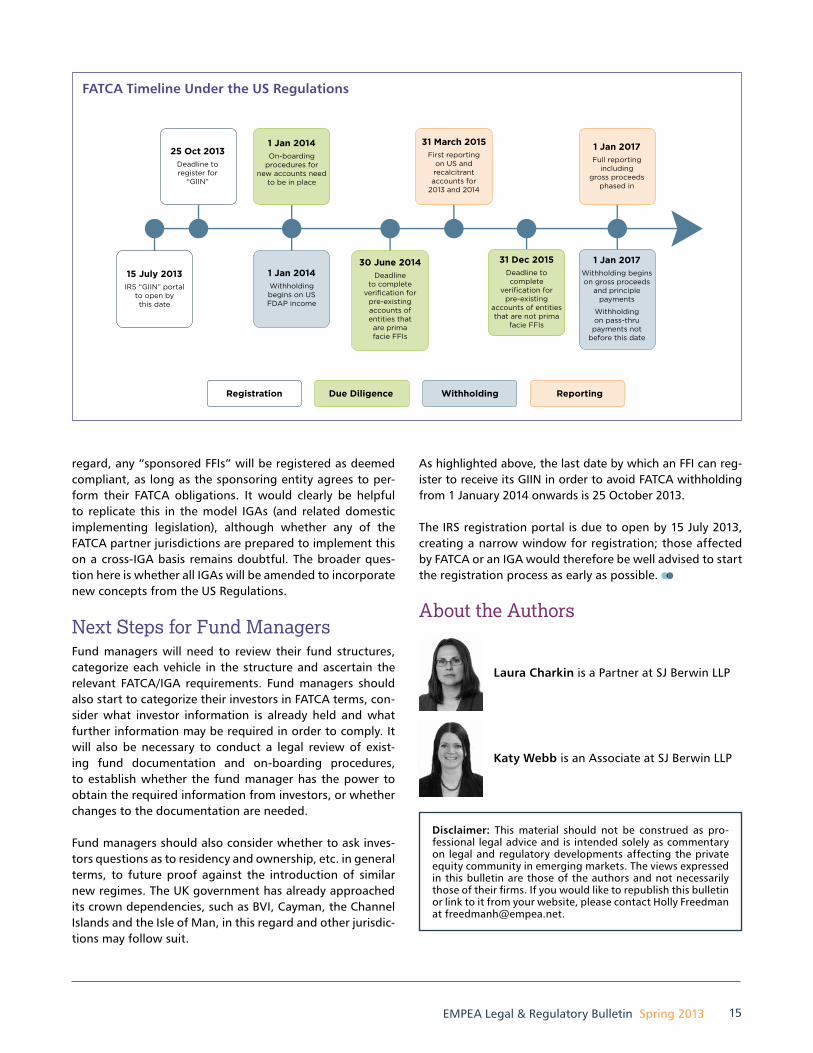

FATCA Timeline Under the US Regulations

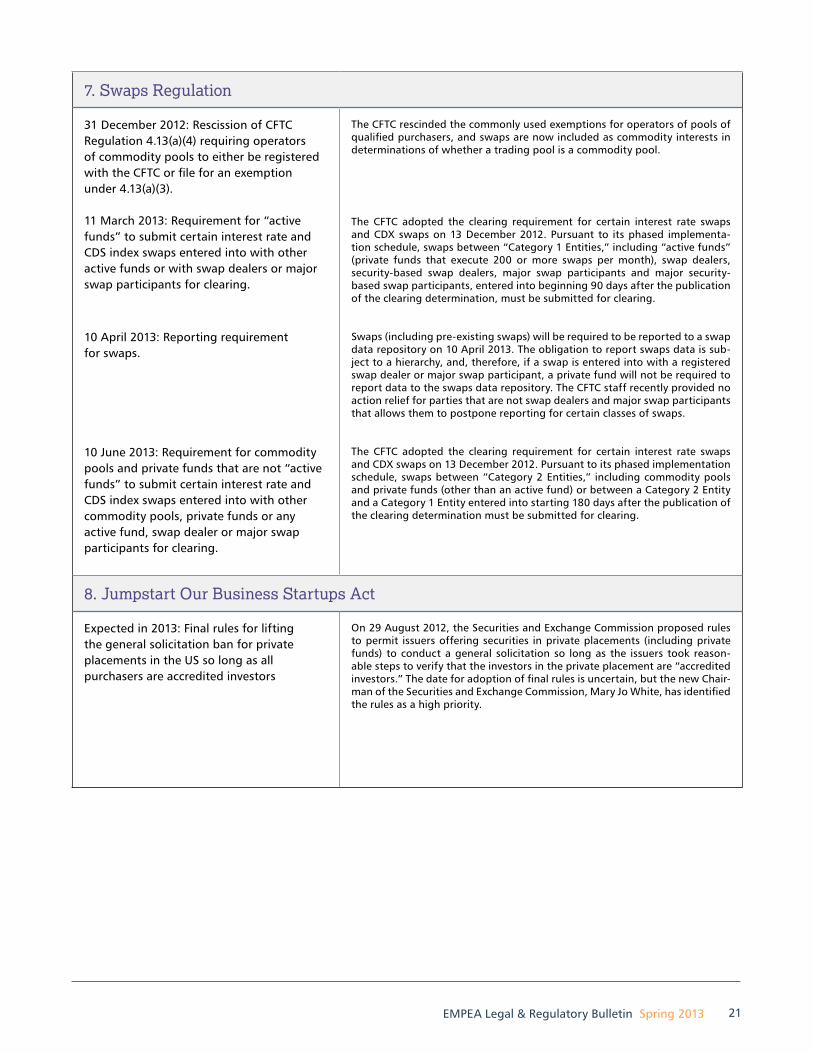

As highlighted above, the last date by which an FFI can reg-ister to receive its GIIN in order to avoid FATCA withholding from 1 January 2014 onwards is 25 October 2013.

The IRS registration portal is due to open by 15 July 2013, creating a narrow window for registration; those affected by FATCA or an IGA would therefore be well advised to start the registration process as early as possible.

25 Oct 2013Deadline to register for

“GIIN”

1 Jan 2014On-boarding

procedures for new accounts need

to be in place

1 Jan 2014Withholding begins on US FDAP income

30 June 2014Deadline

to complete verification for

pre-existing accounts of entities that

are prima facie FFIs

31 March 2015First reporting

on US and recalcitrant accounts for

2013 and 2014

1 Jan 2017Full reporting

including gross proceeds

phased in

1 Jan 2017Withholding begins on gross proceeds

and principle payments

Withholding on pass-thru payments not

before this date

15 July 2013IRS “GIIN” portal

to open by this date

31 Dec 2015Deadline to complete

verification for pre-existing

accounts of entities that are not prima

facie FFIs

Registration Due Diligence Withholding Reporting

© 2013 Emerging Markets Private Equity Association16

On 24 August 2012, Minister of Finance Luc Frieden filed with Parliament Government Bill N° 6471 (“Bill”) on Alter-native Investment Fund Managers, transposing Directive 2011/61/EU (“AIFM Directive”), that was expected to pass into legislature in December 2012. On 4 March 2013, the Chamber of Commerce of Luxembourg approved the terms of the Bill and it is expected that the Bill will be enacted into law shortly, which would make Luxembourg the first mover to implement the Alternative Investment Fund Directive.

Changes to the environment of unregulated or semi-reg-ulated funds (e.g., SIFs, SICARs, etc.) will be profound by requiring, subject to exemption, that they be processed by a management company approved by the Commission de Surveillance du Secteur Financier, the Luxembourg financial sector regulator (“CSSF”). The AIFM Directive could argu-ably translate into tedious and expensive adaptations for alternative investment funds. On the basis of the terms of the Bill, pragmatism will prevail on the new operational requirements applicable to management companies.

This article aims to clarify the Luxembourg regulatory framework defining substance requirements for manage-ment companies, with an insight on changes to be expected and practical steps to be considered by managers to exploit the full potential of the transposition of the AIFM Direc-tive in Luxembourg, where, according to the report of the Association of the Luxembourg Fund Industry published on 29 January 2013, assets of Luxembourg domiciled funds hit €2.383trn at the end of 2012. Changes to the European regulatory framework though the AIFM Directive will have an impact on investors from emerging markets whose investments in Europe are channeled through Luxembourg, traditionally referred to as the Gateway to Europe (market-ing passport) and a vast array of emerging market funds, often located there alongside a fund in the United Kingdom.

What is an AIFM? According to the Bill, a management company (i.e., an AIFM) is a legal person whose activities are, on a regu-lar basis, portfolio management and/or risk management of one or more alternative investment funds (“AIFs”). The definition of AIF in the Bill is extremely broad and techni-cally includes any fund that would not be regulated by Directive 2009/65/EC of 13 July 2009 of the EU Parliament and of the Council on the coordination of laws, regula-tions and administrative provisions on undertakings for collective investments in transferable securities. There-fore, the Bill on AIFs and AIFMs remains very close to the terms of Article 4(1) of the AIFM Directive, which defines AIFs as collective investment undertakings, including investment compartments thereof which, (i) raise capital from a number of investors, with a view to investing it in accordance with a defined investment policy for the ben-efit of those investors and (ii) do not require authorization pursuant to Article 5 of Directive 2009/65/EC and AIFMs as any legal person whose regular business is managing one or more AIFs.

Given the very broad definition of AIFs under the Bill, many fund managers will be caught by the reform. There are limited exclusions, which reflect the terms of the exclusions provided in the Alternative Investment Fund Directive. These include holding companies, supra-national institutions, pension funds, securitization special purpose vehicles subject to the conditions set out in the Bill, employee participation schemes, insurance contracts, managers of funds, single investor structures where no investor is an AIF, family offices and managers of small AIFs which do not opt in the AIFM Directive to benefit from its advantages and with assets acquired with lever-age lesser than EUR 100 million or assets acquired with no leverage lesser than EUR 500 million.

Alternative Investment Fund Managers – Luxembourg’s Attractive Features on Substance and DelegationBy Alexandrine Armstrong-Cerfontaine and Jean-Noel Lequeue, SJ Berwin LLP

“Luxembourg is an international financial services center. It is the world leader in investment funds which are legal products and they channel international investments through Luxembourg into Europe.” H.E. Luc Frieden, Minister of Finance, Grand Duchy of Luxembourg

EMPEA Legal & Regulatory Bulletin Spring 2013 17

No Surprise on SubstanceBroadly, Luxembourg domestic law stipulates, as of today’s date, that a management company is considered Luxem-bourg resident if it has its statutory seat or its place of effective management in Luxembourg, which is fairly easy to satisfy. It is impossible to say today with certainty what the detailed requirements for AIFMs in Luxembourg will be for a management company to be approved by the CSSF and to what extent it may delegate its functions to third parties, but it is relatively easy to guess the core principles that will be applied by the CSSF.

A management company will have to seek authorization as an AIFM if it performs either of the two functions (i.e. portfolio management or risk management) for an AIF. The conditions for obtaining and keeping such authorization will be laid down in a circular to be issued by the CSSF after the Bill is passed into legislature. However, from a policy perspective, it is difficult to see why the Luxembourg regu-lator would adopt a different approach to the requirements it set out for management companies authorized to man-age UCITS funds with a European passport. This is because (i) the UCITS Directive and the AIFM Directive are virtually identical when addressing the conditions applicable to man-agement companies to be authorized, (ii) the Bill translates literally the terms of the AIFM Directive on such conditions and (iii) the AIFM Directive expressly provides that manage-ment companies which are already authorized under the UCITS regime should not be required, when applying for an AIFM license, to provide information or documents already provided under the UCITS regime.

Consequently, particular attention should be given by CSSF to the AIFM’s substance, i.e., its actual physical and economic presence in Luxembourg when designing organi-zational and operational requirements for AIFMs. Substance requirements applicable to management companies han-dling UCITS funds (“ManCos”) have recently been designed by the Luxembourg regulator to better capture the notion of substance in Regulation 10-04 as detailed in Circular 11/508, replaced and reinforced on 26 October 2012 by Circular 12/546 on the authorization and organization of Luxem-bourg ManCos. Circular 12/546 will come into force on 1 July 2013 and in terms of substance, the shape of the future of ManCos and AIFMs should very much look the same.

Sound Governance Requirements for Shareholder(s) and Directors of the Management CompanyGovernance requirements strengthen investor protection and are twofold. It is expected that the shareholders of AIFMs will have to show proof of (i) honesty and integrity

and transparency, as well as (ii) sufficient financial solid-ity for ensuring the company’s long-term equity needs. It is likely that potential conflict of interests will have to be tack-led when authorization will be requested from the CSSF.

The board composition and role of its members will be strengthened. Members of the board of directors of the AIFM, for their part, or where a board member is a legal person, its representative, will have to demonstrate appro-priate professional experience (in addition to their good reputation) by having already exercised similar activities at a high level of responsibility and autonomy. The appreciation of what, in practice, constitutes a sufficient experience will require evidence that directors have (i) management skills and (ii) knowledge, skills and experience to understand the risks associated to the AIF’s activities and the type of assets in which the AIF invests.

Furthermore, the CSSF is expected to seek information from applicants for authorization on effective management. This criterion was set in practice by the CSSF and included in Circular 12/546 for ManCos. The AIFMs will be expected to devote sufficient time to perform their and the number of mandates of their directors, their activities other than as directors and geographical location will be considered by the CSSF.

Regarding the composition of the board of directors, there will have to be at least two directors, even if that is not expressly stated by the CSSF for UCITS. This is because it would be difficult to reconcile the existence of a single director with the conflict of interest rules, which prohibit, in particular, the plurality of office of the same manager with asset management responsibilities and risk control or internal audit and compliance functions.

Central Administration in LuxembourgThe management company will not be a plain administra-tive center with an administrative address in Luxembourg and the board will effectively have to manage the fund from Luxembourg with a decision making process and capacity to continuously monitor activities in Luxembourg. Therefore, at least half of the board of directors of the AIFM will be directors residing in Luxembourg or in a location that is close to Luxembourg as the AIFM’s directors will have to be able to exert adequate oversight and ensure that there is adequate control over delegated activities. Further-more, the premises of the management company will be, in addition to the decision-making center, an administrative center, with permanent compliance and risk control func-tions and include an IT center.

© 2013 Emerging Markets Private Equity Association18

What about Delegation?The delegation of functions for the operating parts of the management company is expected to reflect the terms of the AIFM Directive and nothing more, as opposed to other jurisdictions where the standards set out by the AIFM Direc-tive are considered as a minimum core on which to base rules on the decision-making processing and the organiza-tional structure of the AIFM.

The activities of an AIFM include portfolio management and risk management for the fund and these activities can be performed under a delegation arrangement with licensed asset managers or managers with regulatory approval within the EU or, in the case of a non-EU delegate, a delegate with regulatory supervision and co-operation agreements in place with Luxembourg. The activities of an AIFM may go much beyond these two core functions and include a vast array of other functions as provided in Annex 1, and these activities could be delegated as the AIFM may think fit. There is no limitation in Luxembourg to what an AIFM may choose to delegate, provided that delegation does not render the AIFM a “letter-box” entity. The AIFM will have to notify the CSSF in advance of delegation and the CSSF will assess whether delegation exceeds by an excessive margin the investment management functions done by the AIFM itself. This limitation to delegation implies that the CSSF will verify that the AIFM remains responsible for its activities and supervises its delegates. By analogy to ManCos, delegation may relate to AIFM’s basic func-tions (portfolio management and risk management) both to approved entities and according to strict monitoring and intervention procedures. Delegation may also relate to administrative functions, essentially the company’s accountancy, IT, risk control, compliance and internal audit functions. As for ManCos, AIFMs will have to keep inter-nal managers with the necessary skills for (i) supervising the AIFM’s contractors and (ii) assuming their duties (e.g., for ManCos, audits remain, even if delegated, a duty of an approved director).

The Shape of AIFMs in Luxembourg The regulatory framework on the substance of AIFMs based in Luxembourg is expected to adopt a sound and pragmatic approach to delegation in line with the AIFM Directive, both by the full transposition of the European directive into Luxembourg law and the resolute attitude of the Lux-embourg regulator on substance. The Luxembourg local accent on flexibility in terms of potential exemptions and delegations to which the industry is used should remain, leaving sufficient headroom for the development of funds and competitiveness of the financial arena. Therefore, it is expected that AIFMs in Luxembourg will be able to opti-mize business functions and processes, save costs and

use expertise in administration, risk, administration and/or specific markets or investments. The absence of “let-ter box” test should be satisfied by a Luxembourg AIFM if the decision making centre remains in Luxembourg, i.e., management of the AIFM has the skills and resources to supervise delegated tasks effectively. This flexibility, mixed together with the long lasted and well known appeal of Luxembourg for its funds structures with sharia-compliant instruments, should ensure that Luxembourg remains the platform of choice for investors in the EUA. More generally, the European passport mixed together with the approach in Luxembourg to remain close to the fund industry’s needs mean that the market expects Luxembourg to become a premier location for emerging markets funds managers to structure a European fund.

Now is the time for managers is to identify if delegation would add value to their operations and assess which ser-vice providers will be best placed to achieve their goals, as delegates (other than UCITS managers, MiFID discretionary managers, other AIFMs and non-EU managers authorized and supervised falling within the pool of co-operation agreements between Luxembourg and non-EU countries) will have to have an appropriate organizational structure and personnel with the necessary skills and expertise in the relevant functions considered for delegation.

About the Authors

Alexandrine Armstrong-Cerfontaine is a Partner at SJ Berwin LLP

Jean-Noel Lequeue is a Consultant at SJ Berwin LLP

Disclaimer: This material should not be construed as pro-fessional legal advice and is intended solely as commentary on legal and regulatory developments affecting the private equity community in emerging markets. The views expressed in this bulletin are those of the authors and not necessarily those of their firms. If you would like to republish this bulletin or link to it from your website, please contact Holly Freedman at [email protected].

EMPEA Legal & Regulatory Bulletin Spring 2013 19

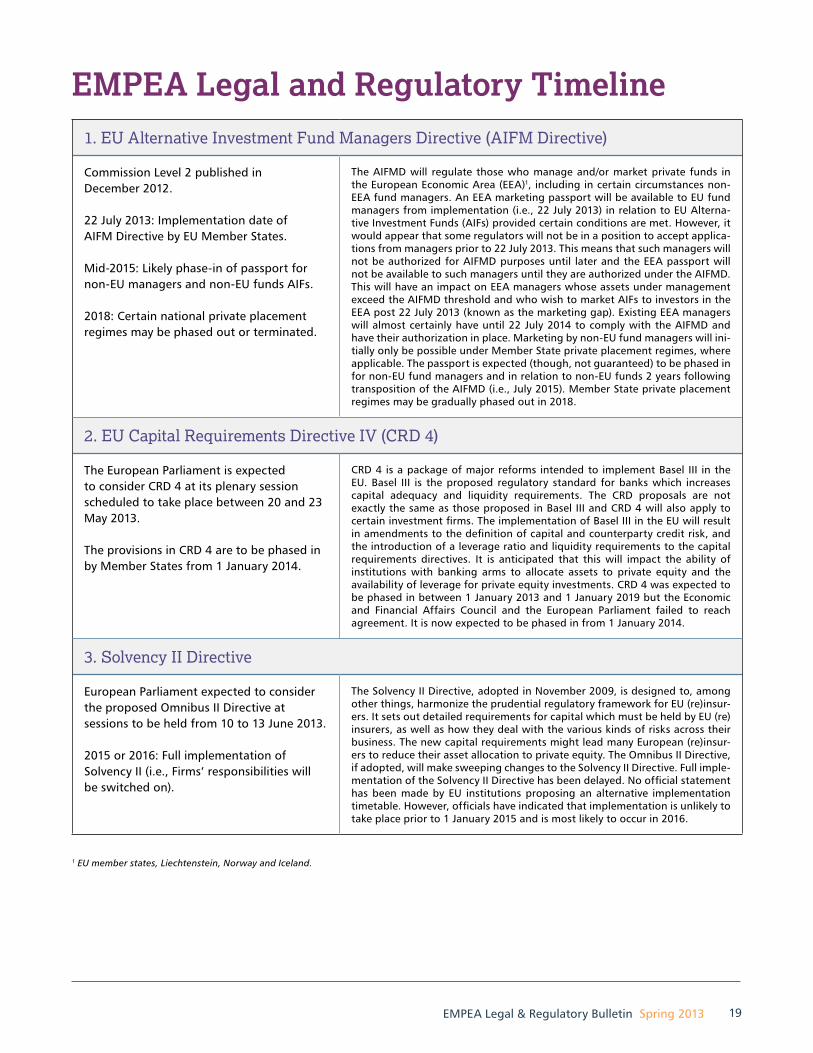

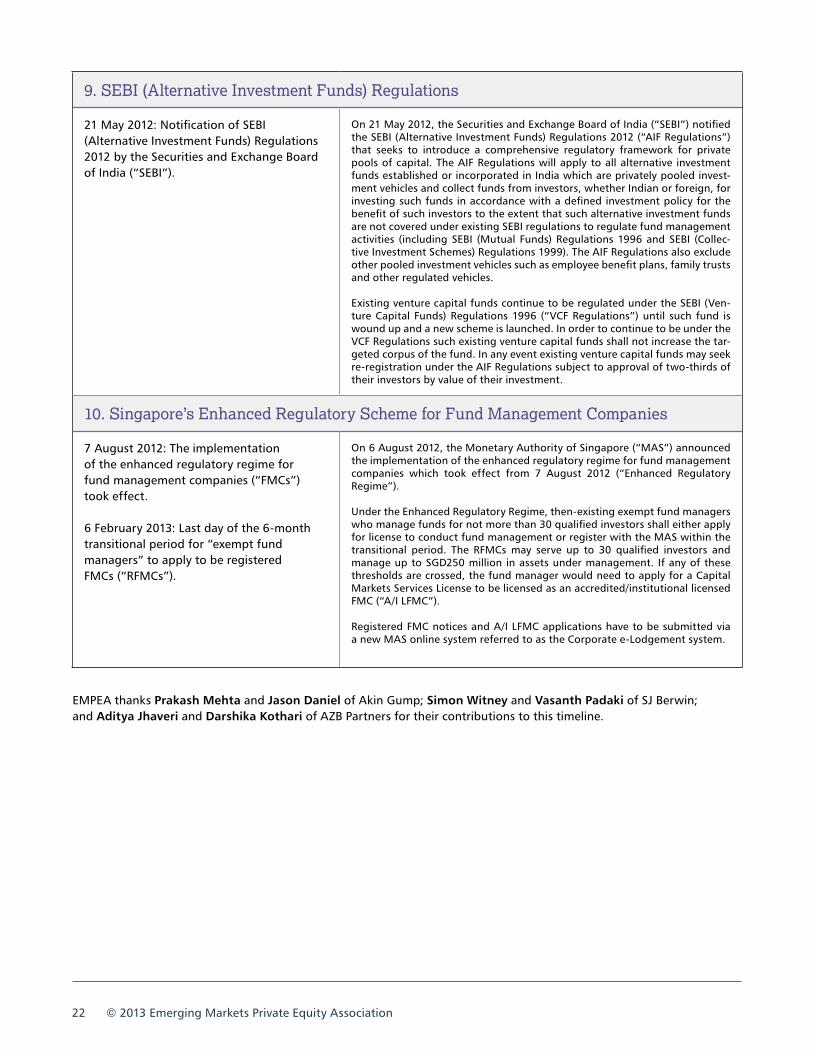

1. EU Alternative Investment Fund Managers Directive (AIFM Directive)

Commission Level 2 published in December 2012.

22 July 2013: Implementation date of AIFM Directive by EU Member States.

Mid-2015: Likely phase-in of passport for non-EU managers and non-EU funds AIFs.

2018: Certain national private placement regimes may be phased out or terminated.

The AIFMD will regulate those who manage and/or market private funds in the European Economic Area (EEA)1, including in certain circumstances non-EEA fund managers. An EEA marketing passport will be available to EU fund managers from implementation (i.e., 22 July 2013) in relation to EU Alterna-tive Investment Funds (AIFs) provided certain conditions are met. However, it would appear that some regulators will not be in a position to accept applica-tions from managers prior to 22 July 2013. This means that such managers will not be authorized for AIFMD purposes until later and the EEA passport will not be available to such managers until they are authorized under the AIFMD. This will have an impact on EEA managers whose assets under management exceed the AIFMD threshold and who wish to market AIFs to investors in the EEA post 22 July 2013 (known as the marketing gap). Existing EEA managers will almost certainly have until 22 July 2014 to comply with the AIFMD and have their authorization in place. Marketing by non-EU fund managers will ini-tially only be possible under Member State private placement regimes, where applicable. The passport is expected (though, not guaranteed) to be phased in for non-EU fund managers and in relation to non-EU funds 2 years following transposition of the AIFMD (i.e., July 2015). Member State private placement regimes may be gradually phased out in 2018.

2. EU Capital Requirements Directive IV (CRD 4)

The European Parliament is expected to consider CRD 4 at its plenary session scheduled to take place between 20 and 23 May 2013.

The provisions in CRD 4 are to be phased in by Member States from 1 January 2014.

CRD 4 is a package of major reforms intended to implement Basel III in the EU. Basel III is the proposed regulatory standard for banks which increases capital adequacy and liquidity requirements. The CRD proposals are not exactly the same as those proposed in Basel III and CRD 4 will also apply to certain investment firms. The implementation of Basel III in the EU will result in amendments to the definition of capital and counterparty credit risk, and the introduction of a leverage ratio and liquidity requirements to the capital requirements directives. It is anticipated that this will impact the ability of institutions with banking arms to allocate assets to private equity and the availability of leverage for private equity investments. CRD 4 was expected to be phased in between 1 January 2013 and 1 January 2019 but the Economic and Financial Affairs Council and the European Parliament failed to reach agreement. It is now expected to be phased in from 1 January 2014.

3. Solvency II Directive

European Parliament expected to consider the proposed Omnibus II Directive at sessions to be held from 10 to 13 June 2013.

2015 or 2016: Full implementation of Solvency II (i.e., Firms’ responsibilities will be switched on).

The Solvency II Directive, adopted in November 2009, is designed to, among other things, harmonize the prudential regulatory framework for EU (re)insur-ers. It sets out detailed requirements for capital which must be held by EU (re)insurers, as well as how they deal with the various kinds of risks across their business. The new capital requirements might lead many European (re)insur-ers to reduce their asset allocation to private equity. The Omnibus II Directive, if adopted, will make sweeping changes to the Solvency II Directive. Full imple-mentation of the Solvency II Directive has been delayed. No official statement has been made by EU institutions proposing an alternative implementation timetable. However, officials have indicated that implementation is unlikely to take place prior to 1 January 2015 and is most likely to occur in 2016.

EMPEA Legal and Regulatory Timeline

1 EU member states, Liechtenstein, Norway and Iceland.

© 2013 Emerging Markets Private Equity Association20

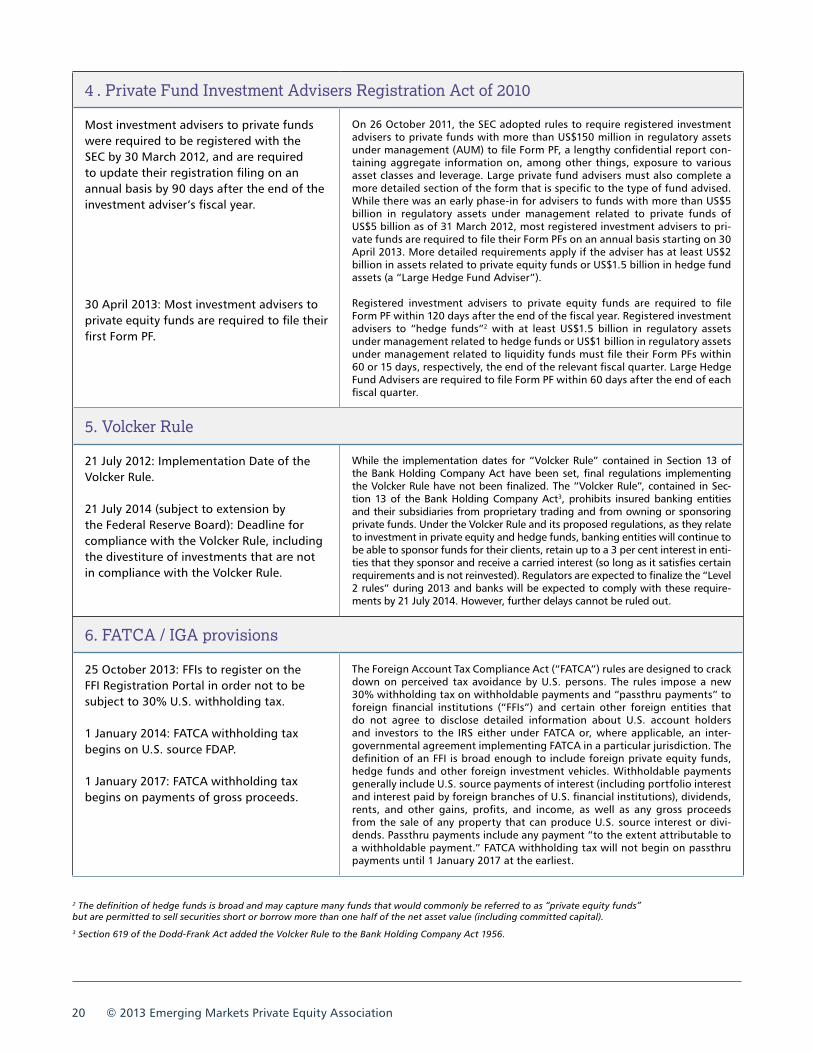

4 . Private Fund Investment Advisers Registration Act of 2010

Most investment advisers to private funds were required to be registered with the SEC by 30 March 2012, and are required to update their registration filing on an annual basis by 90 days after the end of the investment adviser’s fiscal year.

30 April 2013: Most investment advisers to private equity funds are required to file their first Form PF.