Embed Size (px)

DESCRIPTION

Discusses the limited role played by the Public Accounts Committees of Pakistan since independence. Analyzes reasons and raises questions about the about the accountability framework of Pakistan. The paper was written in late nineties but the analysis and recommendations made are still valid.

Citation preview

LEGISLATIVE OVERSIGHT IN PAKISTAN *

A Critical Review of the Accountability Framework

Muhammad Akram Khan# [email protected]

In developed democracies, the legislature oversees the performance of the executive through a mechanism of standing committees. The developing countries have also tried to emulate this pattern. We see that most of the developing democracies have provisions in their constitutions for setting up standing committees to review the operations of the executive departments and agencies. One of these standing committees is the Public Accounts Committee (PAC). The main function of the PAC is to hold the executive departments and agencies accountable for the proper management of resources authorized by the legislature in the annual budget. Within this broad framework each country has its own set of rules and procedures for the scope and functions of the PAC. In Pakistan we have PACs at the federal and provincial levels. They have been set up under various constitutions of the country since independence. The main objective of the present paper is to discuss the role played by the federal PAC in overseeing the performance of the executive. How effective has been this oversight? What are the difficulties, ambiguities and challenges in enforcing accountability by the legislature? What can be done to sharpen the legislative oversight ? The present paper aims at discussing these questions and making some tentative suggestions.

SCHEME OF THE PAPERThe first part of the paper will discuss the legislative framework under the Constitution of Pakistan 1973, for holding the executive accountable. It will introduce, briefly, the legal provisions regarding the formation and functions of the PAC. It will also throw light on the actual functioning of the federal PAC and how effective has it been? This will take us to the second part which analyzes the factors hampering the process of accountability in Pakistan. This part will also highlight the ambiguities in the concept and framework of accountability and the difficulties in enforcing under the existing legal framework. The third part will draw conclusions and make some suggestions for increasing the effectiveness of legislative oversight in Pakistan.

PART ONE

FRAMEWORK FOR OVERSIGHT OF FINANCIAL MANAGEMENT

# Former Deputy Auditor General of Pakistan.

1.1 Composition and Functions of the PACThe job of the PAC starts with the presentation of the reports of the Auditor- General to the legislature through President of Pakistan. The legislature refers these reports to the PAC. Under rules 183-184 of the Rules of Procedure and Conduct of Business in the National Assembly 1992, the composition and functions of the federal PAC are as under: “183 Composition: The Standing Committee on Public Accounts shall consist of not more than twelve members to be elected by the Assembly and the Minister for Finance shall be its member ex-officio.

“184 Functions:(1) The Committee shall examine the accounts showing the appropriation of sums granted by the Assembly for the expenditure of the government, the annual finance accounts of the government, the report of the Auditor-General of Pakistan and such other matters as the Minister for Finance may refer to it.“ (2) In scrutinizing the Appropriation accounts of the government and the reports of the Auditor-General of Pakistan thereon it shall be the duty of the Committee to satisfy itself:

1. that the moneys shown in the accounts as having been disbursed were legally available for, and applicable to the service or purpose to which they have been applied or charged;

2. that the expenditure conforms to the authority which governs it; and

3. that every re-appropriation has been made in accordance with the provisions made in this behalf under rules framed by the Ministry of Finance.

“(3) It shall also be the duty of the Committee:

1. to examine the statement of accounts showing the income and expenditure of state corporations, trading and manufacturing schemes, concerns and projects together with the balance sheets and statements of profit and loss accounts which the President may have required to be prepared or are prepared under the provisions of the statutory rules regulating the financing of a particular corporation trading or manufacturing scheme or concern or project and the report of the Auditor-General of Pakistan thereon;

2. to examine the statement of accounts showing the income and expenditure of autonomous and semi-autonomous bodies, the audit of which may be

conducted by the Auditor-General of Pakistan either under the directions of the President or under an Act of Majlis-e-Shoora (Parliament); and

3. to consider the report of the Auditor-General of Pakistan in cases where the President may have required him to conduct the audit of any receipts or to examine the accounts of stores and stocks.

“(4) If any money has been spent on any service during a financial year in excess of the amount granted by the Assembly for that purpose, the Committee shall examine with reference to the facts of each case the circumstances leading to such an excess and make such recommendation as it may deem fit.

“(5) The report of the Committee shall be presented within a period of one year from the date on which reference was made to it by the Assembly unless the Assembly, on a motion being made, directs that the time for the presentation of the report be extended to a date specified in the motion:

“Provided that extension in the time for the presentation of the report shall be asked for before the expiry of the time allowed under the rule.”

These rules specify the scope of the work of the PAC. The PAC is supposed to look into the legality and regularity of the income and expenditure of government departments along with the report of the Auditor-General on them. We shall argue in this paper that by itself it is a very narrow scope for the legislative oversight. Even within this narrow scope the performance of the PAC has not been enviable. We shall substantiate this assertion in the following discussion.

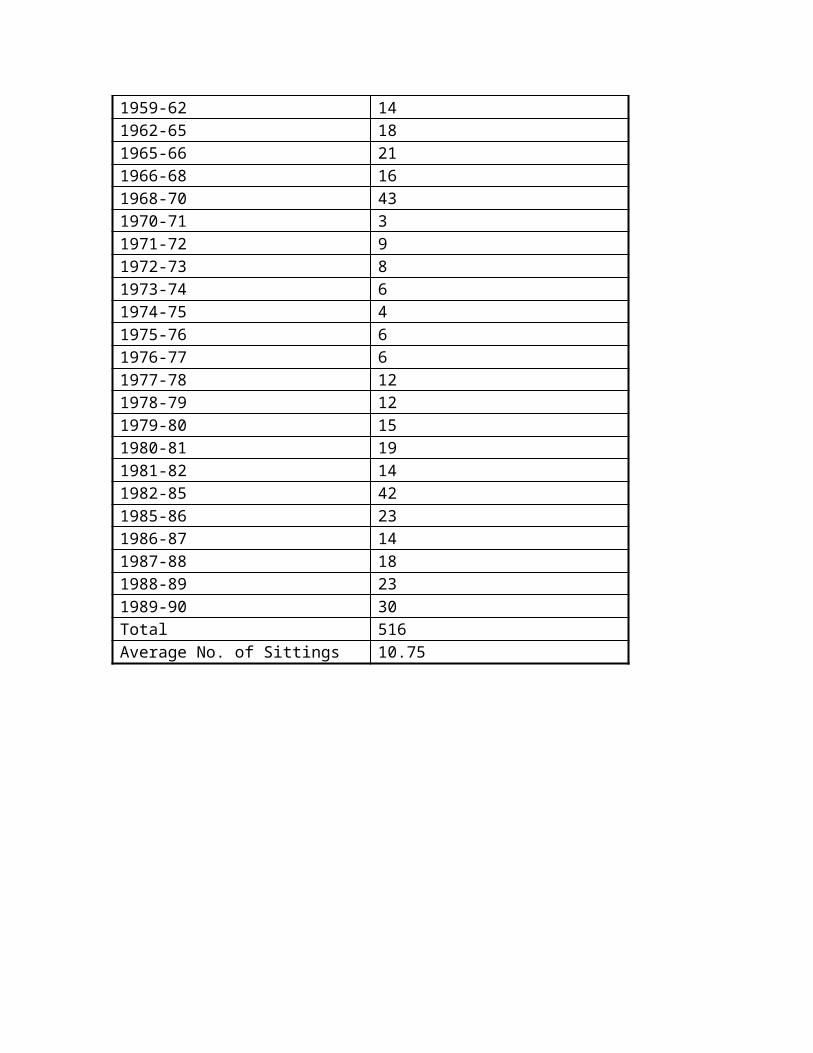

How Often Has The Federal PAC Examined The Accounts?The record of the PAC’s performance has not been very encouraging. There have been 16 years since 1947 when there was no federal PAC. ( see Exhibit 1). Even when a PAC was formed, it did not hold a session at all or when held it was not very quickly. Sometimes it took a PAC several years before it convened a session. As a whole during the last 48 years, the federal PAC lost 12.5 years in convening their first session after their formation. Even after the first session, the PAC lost a lot of time because it met quite sporadically and remained in session for a few days only. Exhibit 3 gives details of the sessions held by all the federal PACs since inception of the country. It shows that the PACs held a total of 516 session during the last 48 years with an average of about 11sessions per year. If we assume that each session was about 4 hours long, the average time devoted by the PAC for holding the executive accountable comes to 44 hours per annum. As a result, as of the date of writing (December 1996), the PAC had not completed the examination of Audit Reports on the accounts for 1989-90. It is already 5 years in arrears. Whenever the next PAC comes into being, it will have to clear the backlog of

these years plus it will have to examine the current audit reports. Until extraordinary measures are taken, it is not likely that the PAC shall be able to make up this loss. #

This shows that the legislature did not accord a very high priority to the formation of the PAC. We can well imagine the condition of accountability in the country when the highest forum of accountability spares less than 45 hours per year to hold the executive departments accountable. The PAC also did not consider its own work quite important. This is in clear contrast to the situation in developed democracies from where we have borrowed this institution. For example, in the UK the PAC remains in session almost throughout the year.

Exhibit 1PERIODS WHEN THERE WAS NO PAC IN EXISTENCE

(Months)No PACs for 10/54 to 04/58 18

10/58 to 03/60 17 12/62 to 11/65 35 01/67 to 03/67 02 03/69 to 06/70 15 12/71 to 08/72 08 01/77 to 03/78 14 10/81 to 08/82 10 01/85 to 08/85 07 06/88 to 03/89 09 08/90 to 05/92 21

2/93 to 10/95 32 11/96 to 12/96 (date of writing this paper

2

Total 191 months = about 16 years

# The condition of the provincial PACs is still more worrying. There has not been any PAC in the province of Sindh and Balochistan for the last two decades. The NWFP PAC is also behind the schedule for several years. The position of Punjab is not encouraging either.

Exhibit 2

TIME GAP BETWEEN DATE OF CONSTITUTION OF PACs AND THEIR IST MEETING( Months)

1st PAC did not meet at all 36 2nd PAC 17 3rd PAC 04 4th PAC 07 5th PAC 09 6th PAC 03 7th PAC 20 8th PAC 02 9th PAC 17 10th PAC 7 11th PAC 5 12th PAC 7 13th PAC 0 14th PAC 13 15th PAC 2 16th PAC 1

Total 150 months

Exhibit 3TIME DEVOTED BY THE PAC FOR THE EXAMINATION OF

AUDIT REPORTSYear of Account No. of Sittings1947-48 141948-49 141949-50 101950-51 131951-52 201952-53 201953-54 191954-57 171957-59 131959-62 141962-65 181965-66 211966-68 161968-70 431970-71 31971-72 91972-73 8

1973-74 61974-75 41975-76 61976-77 61977-78 121978-79 121979-80 151980-81 191981-82 141982-85 421985-86 231986-87 141987-88 181988-89 231989-90 30Total 516Average No. of Sittings 10.75

PART TWO

AMBIGUITIES IN THE ACCOUNTABILITY FRAMEWORK

2.1 Can A Legislature Hold Government Of Its Majority Party Accountable Effectively? Ideally, the legislature is the supreme sovereign body in the country. It has the mandate from the people to oversee the government. The government is supposed to operate within the constitutional and legal framework and observe the rules of business authorized and approved by the legislature. The legislature, through a system of standing committees and special committees can review and control the executive departments and agencies. Theoretically, it makes a lot of sense. But in practice, the government is headed by the leader of the majority party in the House. The government enjoys the support of the majority of the members of the parliament. In this situation, it is politically inconvenient for the legislature to hold the government accountable or to restrain it from certain activities. The system becomes still weaker, if a certain standing committee has a majority of the members representing the government party. For example, in the case of PAC in Pakistan, most often the chairman of the federal PAC has been Finance Minister or some nominee of the ruling party. This is in contrast to the tradition in the developed countries where the chairman of the PAC is usually from the opposition benches. It shows that we have the institution but have not been able to develop it in its true spirit. The successive political governments have not found it convenient for themselves to appoint a member of the opposition party as chairman of the PAC.

2.2 Who Is Accountable? The Minister? Senior Public Servants Or Junior Functionaries? The public servants are frequently called upon by Ministers or Secretaries to twist rules or present the analysis in such manner that the desires of certain political parties or certain partisan interests are served. Public servants who have qualms about such actions feel that their careers will be affected if they refuse to carry out such orders. They feel very uncomfortable about it but cannot do much. They also know that in case they refuse or resist to obey illegal or border-line orders from their superiors, there will be many more like them who will volunteer to obey and carry out those orders. In this way, not only public interest is not served but the government servant who refuses to obey is discredited for being inefficient or tactless. The legal framework does not clearly specify the responsibility of different levels of authority and decision-making. In the PAC, the Ministers are not answerable, although a Secretary or a junior officer might have acted on the orders of the Minister. It is not clear that in a situation where a government servant receives orders from his superior in writing but those orders are not in conformity with the applicable rules what should he do. One can always take the position that he

obeyed those orders as were given by his superiors. In such situations what are the limits beyond which a subordinate should refuse to obey? And what is the protection of the subordinate? Examples of reprisals by different political governments against those officers who refused to carry out their illegal orders are in abundance. The stories about the sufferings of such innocent public servants teach a lesson to others. As a result the government officers tend to show weakness to save their skin as not every government servant is strong enough to stand up and refuse to obey illegal orders. In such a situation, what should a government servant do? But the other question is that if a government servant carries out the orders of his superior, who should be held accountable? This is particularly important, if the superior is also a Minister. A further complicating factor is when the superior officer or the Ministers issue illegal or improper orders orally. Should the government servant receiving orders insist on written orders and in such situations what is the protection of such government servants? Since, practically, the government servants do not feel protected, they either remain in a dilemma or they carry out such orders under duress. Later on in response to any inquiry into such matters, the government servants are unable to defend themselves. The officers or Ministers who issued oral orders are always in a position to back out from their orders. In such a scenario, the government servants, sometime, analyze that if they are forced to carry out illegal orders of their superiors why not derive some benefit for themselves. Thus the situations opens a gateway for corruption at lower levels as well. There is another dimension of this issue. The Ministers need support from the public officials working under them for making decisions. The public officials are conversant with rules and regulation and proper procedures for work. It is their responsibility to inform the Ministers about the regularity, legality and propriety of a proposal. They should make all efforts to advise the Minister about a proper course of action, leaving the right to take the final decision with the Minister. In this relationship, before we hold a Minister responsible for any wrong act or decision we must explore whether the Minister was appropriately informed by the public officials working under them about the legal or procedural aspects of the case. If the Minister took a decision in good faith and the staff working under them did not also inform them about the proper procedure or law in a particular case, it will be unfair to hold the Minister singly responsible for a wrong decision. The public officials working under them must also share the responsibility.

2.3 Who Should Accept The Responsibility Of An Irregularity In A Department? The Person Who Has Done The Misdeed, The Secretary Or The Minister?The government business is very complex and spread out in the entire country. It is being carried out in the field by all levels of functionaries including those at the bottom. Not everyone in the government is fully conscious of the department’s mission, policies, strategies and overall

objectives. Everyone is assigned a responsibility in his own limited sphere. When we are talking about the accountability of a person, ordinarily he will be responsible for the job assigned to him. Beyond that he is not answerable. Therefore, we need to clearly delineate the levels of responsibility. Individuals at each level must have their jobs specified and targets laid down. However, the secretary remains responsible for the overall success of the department’s programs. The Minister should be responsible for policy making, and getting necessary political support for his policies. Unfortunately, in real life all this is quite unclear. In case of a failure or a wrong act, usually there is a search for a scapegoat which ends up in roping in a low level functionary. The senior level public servants and Ministers never get the blame. As a result, it is common knowledge that whenever there is a question of accountability, it will be the bottom people who will get caught. This is so since the focus is on procedures and compliance to rules and not on results of the governmental programs. Also, there is little attention on job descriptions, planning, laying down of targets and monitoring of plans. As a result, the whole exercise of accountability remains restricted to observance of petty rules.

2.4 The System Of Responding To The Audit Observations After the auditors have completed their work, the auditees are requested by the Auditor-General’s department to respond to the audit observations. Subsequently, when the audit report is placed before the PAC, secretary of the executive department is present before the PAC to respond to the audit observations or to answer questions from the PAC. The system in vogue is that the present incumbent of an office answers the questions although the audit observation may relate to any of his predecessors. The concept is that the irregularity committed by anyone in the office was in his official capacity and not in his personal capacity. Therefore the office should respond to the audit observation. The present incumbent of the office has to respond to the audit observation and he feels compelled to defend the actions of his predecessors without looking into the merit of the case. There is a built-in culture of the civil service. Everyone is supposed to take care of his colleagues. In turn he will be taken care of . Thus there is a system of mutual cover-up. It often becomes very difficult for the PAC to arrive at truth in a given case.

2.5 Ministerial Responsibility Toward Audit ObservationsThe public servants respond to the audit observations or to directives of the PAC without reference to the their Minister. Do the Ministers have a responsibility in this regard? The present system presumes that the Ministers do not have any responsibility toward audit observations and directives of the PAC although it is not written specifically anywhere. If we make the Ministers responsible for their departments, then the final replies to the audit observations will have to be cleared with the Minister before they are laid

before the PAC. At present the responsibility of the Ministers toward audit observations of their departments is ambiguous.

2.6 Accountability for What? An important question is: Do we hold people accountable for their official conduct or do we also look into their private lives and lifestyles? Another important question relates to the role of media and anecdotal reports. What is the role and limits of public complaints or media stories about the ill-gotten wealth of certain functionaries or politicians? To what extent this forum should remain in vogue and who should investigate into such reports? How to reconcile the concepts of privacy and individual freedom with state monstrosity?

This question has serious ramifications for the scope of accountability as well as for personal freedom of individuals. If we argue that the individuals should be held accountable for their personal wealth and lifestyles, then we need to develop a framework for it. It should clearly say in which situation a person’s private wealth will be scrutinized? How will it link with the existing income tax and wealth tax laws? Do we need to bring in new laws or the existing ones need be elaborated? To which extent the investigation can go and who will carry out the investigation? How to ensure that the investigating agency itself does not blow its limits? These and host of other questions need to be answered before we accept the principle of accountability for one’s private wealth.

But at the same time if we ignore the private wealth and lifestyles of the individuals, we are shutting our eyes from a very vital area of corruption. The accountability process will remain restricted to compliance with certain rules and fulfillment of certain formalities while the corrupt persons will accumulate heaps of ill-gotten wealth. No one will trust this type of accountability. This question needs to be debated widely before a consensus emerges.

2.7 What Does Examination Mean?The rules of business of the PAC define the scope of examination by the PAC as under: The funds expended by the executive should be legally available i.e.

approved by the legislature. The expenditure should be sanctioned by the competent authority. All re-appropriations should be made according to the rules made by the

Ministry of Finance.These rules determine a narrow scope for the examination of the PAC. It is rule-focused and compliance-oriented. It does not refer to the objectives for which the legislature authorized a budget grant. Consequently, it is possible that an executive department has spent every penny according to the applicable rules but has not achieved the results intended by the expenditure.

Examples of such wasteful but rule-focused transactions abound in the government. During our audits we have found, for example, that a government college had only 26 students but 14 lecturers, all appointed with due authority and proper sanctions. In another case, we found that a malaria control program laboratory set up to collect blood samples was not able to test any sample as the pathologist required to do this job was not employed. Rest of the expenditure in the laboratory was quite according to the rules. The point we are making is that the present scope of examination by the PAC is very restrictive and cannot lead to any meaningful oversight by the legislature.

It also shows that with the passage of time our legislative institutions have not grown in line with developments in other parts of the world. In a large number of countries the legislators have found that accountability which focuses on compliance with rules is hardly meaningful. Consequently, in a large number of countries, the legislatures have authorized their Supreme Audit Institutions (SAIs) to examine the performance of the executive departments and agencies in the broader framework of economy, efficiency and effectiveness. In Pakistan, there does not exist any such authority for the Auditor- General. But the Auditor-General, taking an initiative on his own, introduced performance auditing of the government projects and programs. These audits have a record of mixed success. The PAC has also examined performance audit reports during the last several years. But there is no formal move for giving the Auditor-General the necessary mandate to examine the performance of the government departments in the light of economy, efficiency and effectiveness. Once the Auditor-General gets this authority, it will transform the focus of the PAC examination as well. From the present position where the PAC “also sees” to the position where the “PAC requires” performance auditing, there is a major change in the scope of the PAC’s own scope of examination. The executive departments will also extend ready cooperation to the Auditor-General in his performance audits. The PAC will also have more meaningful examination of the performance of the executive departments.

2.8 How to Measure the Results? Once we are talking about accountability we cannot ignore its wider implications. Accountability in a narrow sense may mean accounting, financially or otherwise, for the objectives to be achieved. This connotation of accountability may remain restricted to financial accounting or referring to certain outputs or quantities produced. But a wider connotation of accountability refers to the impact of government programs or the results achieved in the long run and the effects of these programs on the society. Once we conceive accountability in its wider sense, it introduces further complications in the concept. For one thing, it is not clear how to measure results in such cases. The other is: how to delineate the contribution of each agent in the achievement of certain results? Third: how to measure the future,

but as yet, invisible costs? These are complex questions. At the present stage of social development of our society, perhaps, we cannot meet the challenge of holding people accountable in its wider sense. But perhaps a beginning can be made.

2.9 The Helplessness Of The PAC

The problem of delayed accountabilityOne of the frustrations of the PAC is that the audits are not completed

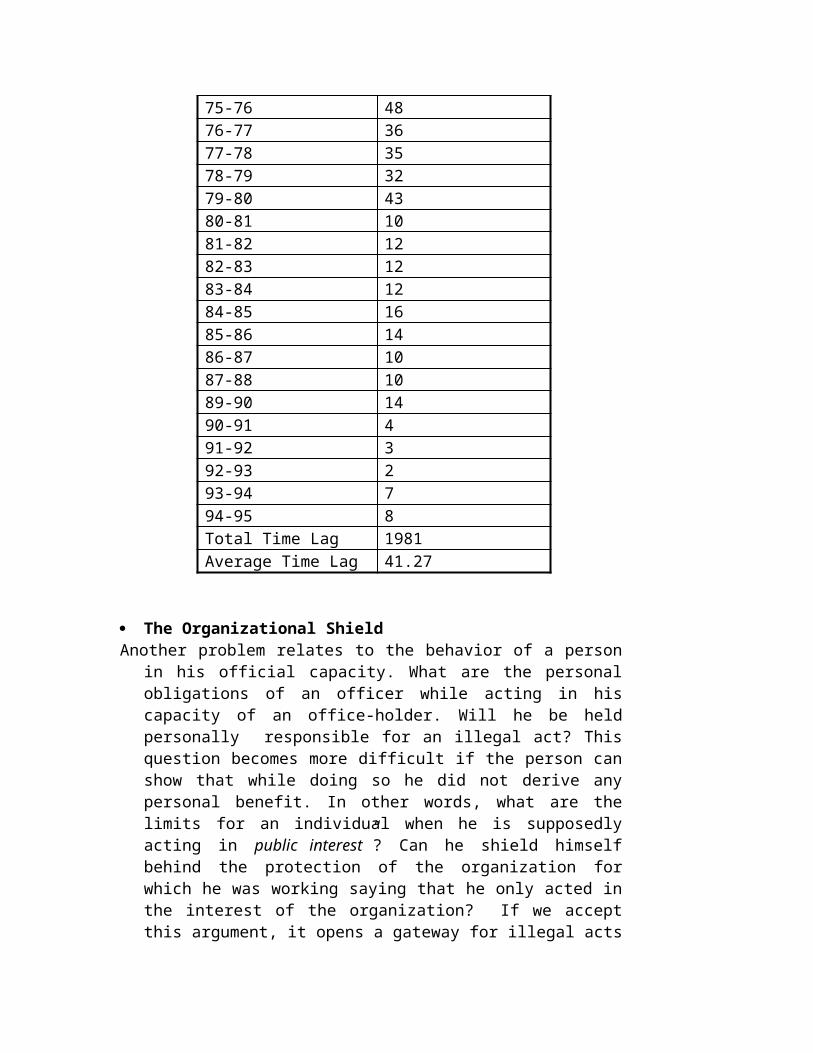

promptly and the audit reports are not placed before it within the same year. The Auditor-General has laid down 30the April as due date for finalizing and printing of the audit report each year. But hardly ever this date has been observed. If we look at the history of the audit reports, and measuring the delay from 30th April each year, we find that during the last 48 years the average delay in completing the audit reports has been 41 months (See Exhibit 4). This situation has an explanation also. The audits cannot be started until the accounts are closed. It takes a complete financial year to complete the audits and finalize the audit report. The finalization process entails sorting and sifting of the raw audit observations and seeking response of the departments. It usually takes several months. Then comes the stage of final approval by the Auditor-General and printing of the report. By the time the audit report is placed before the PAC, it is already quite late. Further delays occur due to time taken by the legislature in constituting the PAC and the by the PAC in convening a session. For example, as already pointed out, at present ( December 1996), the PAC has yet to examine the audit reports for 1989-90. All said and done, when the audit report comes up for discussion, it becomes very difficult to hold anyone responsible. The individuals responsible are retired, died or transferred or may have left the government job. Some of them even settle outside the country. All these factors make the accountability a very frustrating exercise. The PAC cannot handle this situation in an effective manner. It tries to get rid of such “dead issues” by forming sub-committees. It helps to sweep the issues under the carpet without attracting any blame.

The delay in the finalization of audit reports is a complicating phenomenon. It involves many factors. One is the absence of any legislative time table for the Auditor-General for finalizing the accounts and the audit reports. The Auditor-General has, out of his concern for good management and timeliness of the reports, laid down a time table for himself. But it has no legislative sanction. The other problems are lack of financial and human resources, outmoded auditing procedures, untrained and unqualified staff, non-cooperation of the auditees, delaying tactics of the controlling Ministries in responding to the audit reports, etc.

Exhibit 4

AUDIT REPORTSTIME LAG BETWEEN PERIOD OF ACCOUNTS AND

DATE ON WHICH REPORTS WERE PREPARED Months

47-48 5348-49 4149-50 4150-51 6551-52 5452-53 4853-54 5054-55 3855-56 6556-57 5357-58 6658-59 5459-60 8360-61 6761-62 5562-63 4863-64 3664-65 2465-66 5066-67 5467-68 5468-69 8869-70 7670-71 9671-72 8472-73 7673-74 6774-75 6775-76 4876-77 3677-78 3578-79 3279-80 4380-81 10 81-82 1282-83 1283-84 1284-85 16

85-86 1486-87 1087-88 10 89-90 14 90-91 491-92 392-93 293-94 794-95 8Total Time Lag 1981Average Time Lag 41.27

The Organizational ShieldAnother problem relates to the behavior of a person in his official capacity.

What are the personal obligations of an officer while acting in his capacity of an office-holder. Will he be held personally responsible for an illegal act? This question becomes more difficult if the person can show that while doing so he did not derive any personal benefit. In other words, what are the limits for an individual when he is supposedly acting in public interest”? Can he shield himself behind the protection of the organization for which he was working saying that he only acted in the interest of the organization? If we accept this argument, it opens a gateway for illegal acts which can be later defended in the name of the organization. But if we do not allow any flexibility, it leads to, sometimes, difficult or impossible situations if one has to follow the existing rules in letter. We cannot conceive any set of rules which can cover all possible situations. So the need for flexibility in the application of rules always remains. But the question is: where do you draw the line? How do you determine, in each case, that an individual while bending, twisting or violating the rules did in fact act in public interest? How to filter out those situations where people twisted the rules in their own interest?

Non-availability of InformationAnother scenario that clouds the process of accountability is the non-

availability of the information needed by the PAC. We have often seen the PAC helpless when some of its members ask a question from the executive and they do not have a ready answer. They promise to provide this information after collecting it from the field. According to the existing procedures, this information should be made available to the PAC within the time frame decided by the PAC. But the mechanism of follow-up of the PAC directives is quite weak and cumbersome. It is weak as the National Assembly Secretariat does not have any specific cell to provide support to the PAC. The officers of the Secretariat are too overburdened to pursue it vigorously. Moreover, the meetings of the PAC are not very

frequent. The turn of the same Ministry may come after several months. In the meantime the PAC forgets to recall what questions it had asked in the last session. The mechanism is cumbersome since the information provided by the executive must be independently verified by the Auditor-General before it is submitted to the PAC. It takes time. In brief, the PAC often finds itself with inadequate information and gradually forgets what it asked last time.

Secrecy of InformationWhat are the limits for the PAC to ask information from the government? Can some information be withheld from the PAC on the plea that it is classified or secret? These questions are important in view of the fact that government departments and agencies some time refuse to provide the information asked for by the PAC. A famous case is that of the refusal of the nationalized banks to provide list of those persons who got loans written off on the plea that banking laws do not allow to divulge such information. Similarly, some departments or agencies reply to the PAC that the existing rules do not permit making certain information public. The question arises: how can we complete the process of accountability when even the highest forum in the country cannot have access to certain information.

Technical Support to the PACThe PAC consists of politicians who are not conversant with the technical work of various departments and agencies. So far as the PAC focuses on the simple question of budgetary allocations and compliance of their limits, it is not much of a problem. But if we take into the broader concept of accountability as discussed in this paper, the needs of the PAC are much more. The broader concept of accountability requires reporting on the results achieved by the departments and authentication of those results by the audit. This takes the PAC to a more technical arena and the politicians will need technical support for a meaningful examination.

The PAC Report and the National AssemblyOnce the PAC has examined the accounts and the audit report, it compiles its report and recommendations for the consideration of the National Assembly. Practical experience is that the National Assembly hardly ever finds time to discuss the report of the PAC. It spends a few minutes in adopting the report without deliberating over it. This gives the message to the PAC that their work is not that important. As a result, the PAC members also feel that they need not spend much time on the whole exercise. If the National Assembly discusses the PAC report in greater detail, it will surely lend greater enthusiasm to the whole process of accountability.

2.10 Accountability On The Basis Of Hindsight Wisdom

Can we hold a person responsible for damaging public interest where he acted on the best information available to him at the time a decision was being made? In other words, can we hold some one responsible on the basis of information which became available after the event? The obvious answer is: No one should be held responsible on the basis of hindsight wisdom. But the question is: does the official record keeping or filing system keeps an elaborate and clear record of the context in which certain decisions are taken and about the amount of information available on that date? Since the system does not provide this information readily, when audit takes place the auditors call into question various decisions on grounds of propriety and fairness. At that time, it becomes difficult to show that the decisions were made on the basis of the best available information. Since the absence of a reliable proof for such an assertion exposes the executive officers to charges of impropriety, they often refuse to use their imagination and innovate in the public interest where it is obviously needed. There are no clear guidelines for such situations.

2.11 What Is Role Of The Legislature In Budget Formulation?PAC is the highest forum of accountability in the country but its role starts after the event. The annual budget is prepared by the Ministry of Finance on the basis of information provided by the executive departments and agencies. The budget is placed before the legislature for approval. The budget documents are written in a technical language and the time during which it has to be debated is so short that there is hardly any change which the legislature can make. As a result, the budget session of the National Assembly is a good debating session with little consequence for the budget proposals made by the Ministry of Finance. The legislature has to accept it as a fait accompli. How can the legislature exercise an effective control on the executive departments when it does not have a control on the formulation of their budgets? This question is being debated in many countries of the world. One of the suggestions is that the legislature should refer the budget proposals of each department to the respective standing committee for the department. The committee should examine the budget proposals in detail and consider the continuation or otherwise of the existing programs. This will link very effectively with our proposal for the introduction of a system of progress reporting by the departments for the legislature.* The departments will have the approval of the legislature for various programs after examination by the standing committee of the legislature. The budgets can also provide for physical targets to be achieved and the costs to be incurred for each component of the program. At the time of audit, these very targets will become the criteria of audit and the legislature will have the opportunity to examine the extent to which its approved targets have been achieved and at what cost.

2.12 Relationship Of The Auditor-General And The Legislature* See para 3.8 of this paper.

Is the Auditor-General an officer of the legislature? Can the PAC order the Auditor-General to carry out certain investigations? Will it not injure the independence of the Auditor-General? The deeper question is: if the Auditor-General is independent, of whom is he independent? Of the executive or the legislature? or both?

There is no tradition in our country for the legislature and Auditor-General of talking to each other freely and frankly. The legislature has hardly ever approached the Auditor-General to carry out any special investigation. Nor has ever any MNA asked the Auditor-General to investigate into a certain matter. Same is also true for the Auditor-General. The Auditor-General does not have a free access to the legislature. His budget is controlled by the Ministry of Finance. His report is laid before the House by the President. He cannot approach the legislature freely on any matter of national concern. These are effective barriers to accountability. This is in sharp contrast to the developed democracies where the legislature or its individual members often request their Auditors-General to report on certain matters of national importance. For example, the General Accounting Office of the US publishes scores of such reports every year which were initiated and prepared in response to a request of a parliamentary committee or an MP. These reports present an independent and objective view by the Auditor-General.

2.13 Accountability of Non-government and Private Sector OrganizationsA complicating factor is that some of the public programs are being carried out by non-governmental agencies, such as private corporations, non-profit groups, and international organizations. Examples are educational institutions, hospitals or rural development programs. These organizations are supported by the government. The government support takes the form of subsidies, contracts, grants, cooperatives, joint venture, and various other public-private partnerships. The question is: how can we hold these organizations accountable in such a manner that we get the assurance that the objectives of the government are met? Sufficient instruments of accountability do not exist nor enough thought has been given by the legislature about this issue. The difficulty is that these organizations are independent of the government yet they are entrusted with implementation of the programs which normally the government would carry out by itself. Of these the accountability of the international organizations is the most complex area. Thus there is a conflict between accountability needs and independence of the organizations operating outside the government network.

PART THREE

CONCLUSIONS AND RECOMMENDATIONS

3.1 The concept and framework of accountability is ambiguous.Our main conclusion is that the system of legislative oversight in Pakistan is not fully developed. It has a narrow focus. The PAC is the only body which holds the executive departments accountable. But the system has several snags. For example, the PAC is not constituted quickly after the elected government comes into being. Once constituted it does not meet frequently. And if it meets, its focus is very narrow. Even then it does not get answers to all questions. Our main point is that the basic concept of accountability and the framework within which it operates is inadequate. It is clouded by ambiguities. Until the legislature clarifies its intent by further legislation, the question of accountability will remain evasive and it will not be possible to hold anyone accountable.

3.2 The legislature should enact the role of the Auditor General.The main tool of accountability is the audit done by the department of the Auditor General. It is a pity that there does not exist any law by the legislature which defines the role, functions and responsibility of the Auditor-General. The Auditor-General is being governed by a presidential order which can be modified by the government anytime it is unhappy from the Auditor-General. Most of the countries in the world have a statue passed by their legislatures on this subject. It is time that Pakistan also moves in this direction.

3.3 The concept of accountability should encompass reporting for results.The legislature should look into the whole question of accountability from a fresh angle. The government departments and agencies should not only be responsible for the financial management of resources but should also report to the legislature about the results achieved, output produced and services rendered. For this a reporting framework will have to be developed which should have two parts. Part one, applicable to all departments, should deal with the overall mission, activities, personnel, budget and objectives of the department. Part two should deal with the targets set for the current year. These targets should be approved at different levels by appointed authorities of the department. But the overall outputs of the departments should be approved by the legislature at the time of approving the budgets. The results produced by each department should also be approved by the legislature with reference to the approved targets for outputs and costs involved. The purpose is that the legislature should have an opportunity to judge for itself whether the promises made by the department at the time of budget approval have been met and whether these programs should be continued or not.

3.4 Accountability requires clear definition of delegation of authority.

The delegation of authority rules need to be elaborated further. They should clearly specify the responsibilities of Minsters, Secretaries and other levels of government.

3.5 The Ministerial responsibility should be defined clearly.The Minister in-charge of a Ministry should be made answerable for the performance of his department. He should appear before the PAC for responding to the audit reports. The present situation in which the precise responsibility of the Ministers and public servants is not clearly delineated is not conducive to accountability. In fact, the Minister’s personality is a role model for public servants. We cannot expect the public servants to behave ethically and lawfully if they find that their Minister is not keen to do so. The Ministers are supposed to operate within the authority given to them by the legislature. If they flout this authority implicitly or explicitly, it sets a bad example. But once we make the Ministers answerable before the PAC we can expect them to behave more responsibly. It is not to deny the Ministers the right to exercise political judgment in certain cases. It is possible that a Minister likes to set aside the technical analysis done by civil servants working under them in favor of political judgment. This privilege of the Ministers should remain intact. But in all such cases the basis of decision making should be made explicit by the Ministers.

3.6 The accountability framework should protect the honest government officials.The service conditions of government officials should be modified to give protection to those persons who act in public interest and refuse to obey the orders of their superiors. This is an intricate question and will require considerable research before we are able to define the limits of protection of such civil servants as this protection can also be misused.

3.7 Accountability framework should empower public servants and define their limits clearly.An effective accountability framework requires that the public servants should get empowerment to make decisions and manage resources freely. They should have adequate resources to fulfill the task assigned to them. But empowerment does not mean there should be no controls. Internal controls will have to be in place. These controls should not be a means to obstruct the work but to help the public servants improve their performance.

3.8 The accountability of non-government and private organizations should also be defined.In cases where government programs or activities are entrusted to third parties, the capability of these parties should be carefully assessed before hand for the delivery of these programs.

There should be a clear agreement with the third parties carrying out government programs about their accountability. They should know before hand about the information they will have to provide to the government or such agencies as Auditor-General or other regulatory bodies.

The government should organize studies to examine the question of accountability of private and non-government organizations entrusted with carrying out of government programs. This research should culminate in the evolution of suitable accountability instruments which do not conflict with the independence of these organizations but at the same time provide necessary mechanism to hold them accountable.

3.9 Reporting framework for the departments should be developed.The legislature should make it obligatory on all government departments and agencies to generate information on the effectiveness of their programs. For this purpose a reporting framework will have to be developed.

3.10 There should be a reporting time table for the Auditor-General.The legislature should make it mandatory for the Auditor-General to follow a time table for completing the audits and issuing the audit report. In fact, the PAC should encourage the Auditor-General to issue audit reports on various departments throughout the year. A time table like, for example three months after an audit is completed, should be laid down for the report to be placed before the PAC. It will imply that the Auditor-General should agree with the legislature his annual plan for carrying out various audits and for laying down his reports before the PAC. This will create a sense of urgency both within the department of the Auditor-General as well in the executive departments and agencies.

3.11 The PAC should follow a time table enabling to complete the examination of Auditor-General’s reports on a current basis.The legislature should make it obligatory for the PAC to meet within a specified period after its constitution and keep on doing so until all backlog of the past audit reports is cleared and for the future it should finish its work for the current year during the same year. It will imply that the PAC will have to remain in session almost throughout the year.

3.12 The PAC should seek help from experts.The PAC should have the option of co-opting technical experts as advisors for reviewing the audit reports pertaining to any department or agency. It should also be possible for the PAC to associate such experts in the formal sessions of the PAC. They should have the right to cross-examine the executive departments on behalf of the PAC. This change in the procedures of the PAC will create a sense of seriousness among the executive departments about the replies they provide to the PAC.

3.13 The PAC should have its own secretariat.The PAC should be supported by a technical cell manned by the officers of the Auditor-General who should prepare necessary working papers, briefs and discussion material for the PAC. This cell should also be responsible for the follow-up work of the PAC. The cell can also provide support to various standing committees in the examination of budget proposals if the suggestion made in this paper is accepted.* Creating a secretariat for the PAC will detach it from the National Assembly secretariat where the PAC work remains a marginal activity at the moment.3.13 The PAC directives should be binding on the executive.At present the PAC makes recommendations for the executive departments and Ministries. The National Assembly should enact legislation and devise mechanism making it obligatory for the executive departments and Ministries to implement the directives of the PAC.

3.14 The Auditor-General should have free access to the legislature.The rules of business of the legislature should be amended to provide the Auditor-General a free access to the legislature. Similarly, the legislature should be encouraged to invite the Auditor-General to provide independent and objective assessments on issues of national interest. This will dismantle some of the barriers against effective accountability.

3.15 There should be no barriers for the legislature to receive information.The legislature needs to enact legislation to reiterate its right to receive any information it requires and all departments and agencies should be obliged to provide it. Of course, it will mean that the mode of providing information can be defined in such a manner that public interest is adequately safeguarded.

* See para 2.11 above.*

BIBLIOGRAPHY

AHSAN, M. NASEER, “Governance and the Legislative Audit Function,” Public Fund Digest, (11:1), 1996, pp. 9-14.

DESAUTELS, L. DENIS, “Reflections on Ethics and Accountability,“ Opinions, Ottawa, July 1994, pp. 1-8.

GORAYA, JAVED MUZAFFAR, “Audit: No Priority,” Horizon, 19 January 1993, pp. 1-5.

ICERMAN, RHODA C. & DAVID SINASON, “Government Accountability to the Public: The Dynamics of Accountability in the U.S.,” Public Fund Digest, (11:1), 1996, pp. 65-81.

MUIS, JULES W., “Accountability the 21st Century,” De Accountant, the Netherlands, November 1996, pp. 164-167.

POMERANZ, FELIX, “ Accountability: Its Importance to Democratic Society,” Public Fund Digest, (11:1), 1996, pp. 19-26.

PREMCHAND, A., Effective government Accounting, Washington: International Monetary Fund, 1995, 190 pp.

PREMCHAND, A., Public Expenditure Management, Washington: International Monetary Fund, 1993, 282 pp.

Report of the Public Accounts Committee on Finance Division 1981-1985, Islamabad: National Assembly Secretariat, 1986.

Rules of Procedure and Conduct of Business in the National Assembly, Islamabad: National Assembly Secretariat, 1992.

STAATS, ELMER B., “New Dimensions of Accountability in Government,” Public Fund Digest, (11:1), 1996, pp. 1-8.

STERN, ESTHER, Accountability Relationships in Program Delivery: A Canadian Perspective,“ Public Fund Digest, (11:1), 1996, pp. 43-54.

The Federal Public Accounts Committee in Pakistan, Islamabad: National Assembly Secretariat, 1985.