Embed Size (px)

Citation preview

8/6/2019 Long Term and Shrt Run relationship between Macroeconomic variables and stock market in India

http://slidepdf.com/reader/full/long-term-and-shrt-run-relationship-between-macroeconomic-variables-and-stock 1/48

1

University of Newcastle Upon Tyne

Business School

MSc. International Economics and Finance

IS THERE A LONG RUN EQUILIBRIUM AND SHORT RUN DYNAMIC RELATIONSHIP BETWEEN

MACROECONOMIC VARIABLES AND STOCK PRICES IN INDIA?

Supervisor: Dr. Simon Vicary

June 2010

8/6/2019 Long Term and Shrt Run relationship between Macroeconomic variables and stock market in India

http://slidepdf.com/reader/full/long-term-and-shrt-run-relationship-between-macroeconomic-variables-and-stock 2/48

2

Dedication

This dissertation is dedicated to my parents and sisters.

8/6/2019 Long Term and Shrt Run relationship between Macroeconomic variables and stock market in India

http://slidepdf.com/reader/full/long-term-and-shrt-run-relationship-between-macroeconomic-variables-and-stock 3/48

3

Acknowledgements

I would like to express my gratitude to my supervisor and personal tutor, Dr. Simon Vicary,

for his guidance and support throughout the dissertation work.

I would like to thank all my professors for their support all the year which was a great help

for me.

I would like to thank my parents for giving me motivation and determination to complete

this dissertation. I would also like to thank my friends for helping me out in small issues that

made this dissertation look better.

8/6/2019 Long Term and Shrt Run relationship between Macroeconomic variables and stock market in India

http://slidepdf.com/reader/full/long-term-and-shrt-run-relationship-between-macroeconomic-variables-and-stock 4/48

4

Abstract

Understanding the reasons for the changes in stock prices has always been

topic of interest among analysts and investors. This study aims at finding the

effects of changes in macroeconomic variables on stock prices in long run and

short run for Indian economy using Vector auto regression, impulse response,

forecast error variance decomposition and Granger Causality. Results show

that stock prices are not related to macroeconomic variable in long run or

short run. Only exception is Exchange Rate which affects stock prices in short

run. This study shows that stock prices are not much dependent on domestic

factors.

8/6/2019 Long Term and Shrt Run relationship between Macroeconomic variables and stock market in India

http://slidepdf.com/reader/full/long-term-and-shrt-run-relationship-between-macroeconomic-variables-and-stock 5/48

5

Table of Contents

Abstract.........................................................................................................................4

Table of Contents...........................................................................................................5

List of Figures.................................................................................................................6

List of Tables...................................................................................................................7

1.0 Introduction.....................................................................................................9

1.1 Development of Indian Economy....................................................9

2.0 Literature Review............................................................................................12

2.1 Chronological Review of Literature................................................13

3.0 Theoretical Framework...................................................................................19

(3.1) Inflation..........................................................................................19

(3.2) Exchange Rate................................................................................20

(3.3) Money Supply.................................................................................20

(3.4) Interest Rate...................................................................................21

(3.5) Industrial Production......................................................................21

4.0 Empirical Framework......................................................................................21

(4.1) Stationary and Non Stationary Data...............................................21

(4.2) Augmented Dickey Fuller................................................................22

(4.3) Engle Granger Cointegration Test...................................................23

(4.4) Granger Causality...........................................................................23

(4.5) Vector Auto Regression (VAR)........................................................24

(4.5.1) Variance Decomposition............................................26

8/6/2019 Long Term and Shrt Run relationship between Macroeconomic variables and stock market in India

http://slidepdf.com/reader/full/long-term-and-shrt-run-relationship-between-macroeconomic-variables-and-stock 6/48

6

(4.5.2) Impulse Response......................................................26

5.0 Tests and Results..............................................................................................26

6.0 Conclusion.........................................................................................................35

7.0 References........................................................................................................37

8.0 Appendix...........................................................................................................39

8/6/2019 Long Term and Shrt Run relationship between Macroeconomic variables and stock market in India

http://slidepdf.com/reader/full/long-term-and-shrt-run-relationship-between-macroeconomic-variables-and-stock 7/48

7

List of Figures

Figure 1............................................................................................................................10

Figure 2.............................................................................................................................30

Figure 3.............................................................................................................................30

Figure 4.............................................................................................................................30

Figure 5..............................................................................................................................30

Figure 6..............................................................................................................................30

8/6/2019 Long Term and Shrt Run relationship between Macroeconomic variables and stock market in India

http://slidepdf.com/reader/full/long-term-and-shrt-run-relationship-between-macroeconomic-variables-and-stock 8/48

8

List of Tables

Table 1.........................................................................................................................27

Table 2.........................................................................................................................27

Table 3..........................................................................................................................28

Table 4..........................................................................................................................28

Table 5..........................................................................................................................31

Table 6...........................................................................................................................31

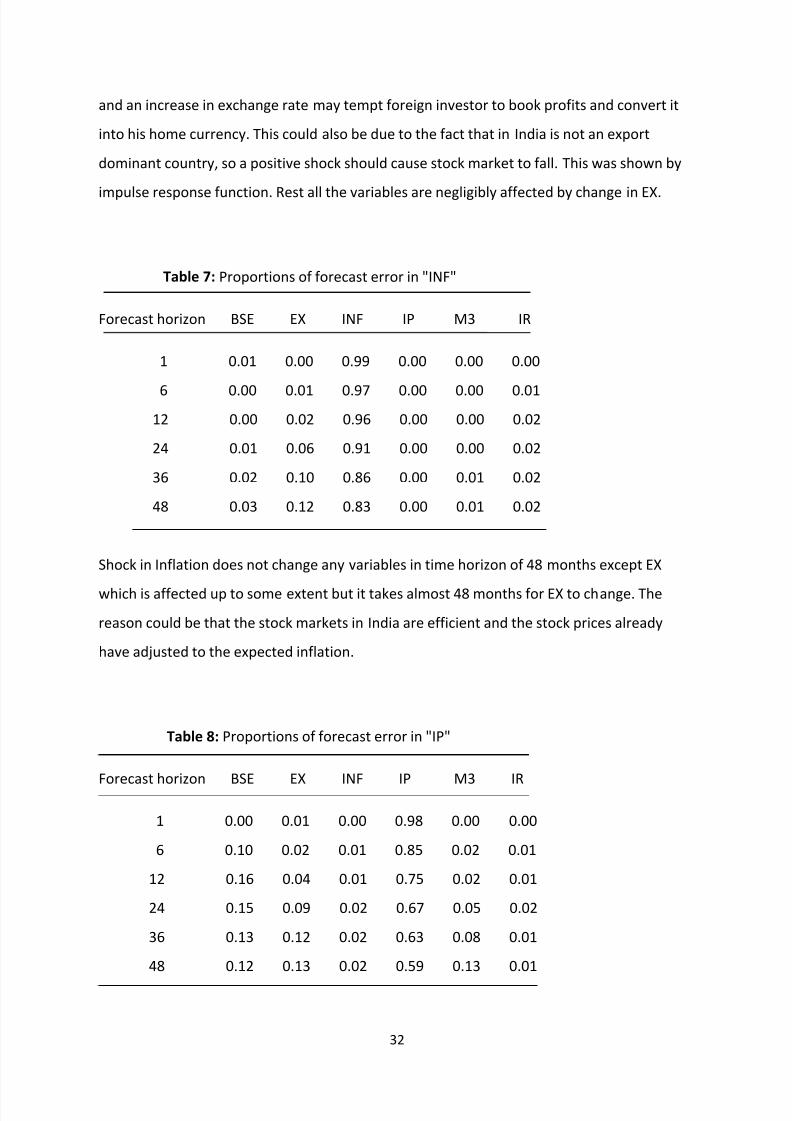

Table 7...........................................................................................................................32

Table 8...........................................................................................................................32

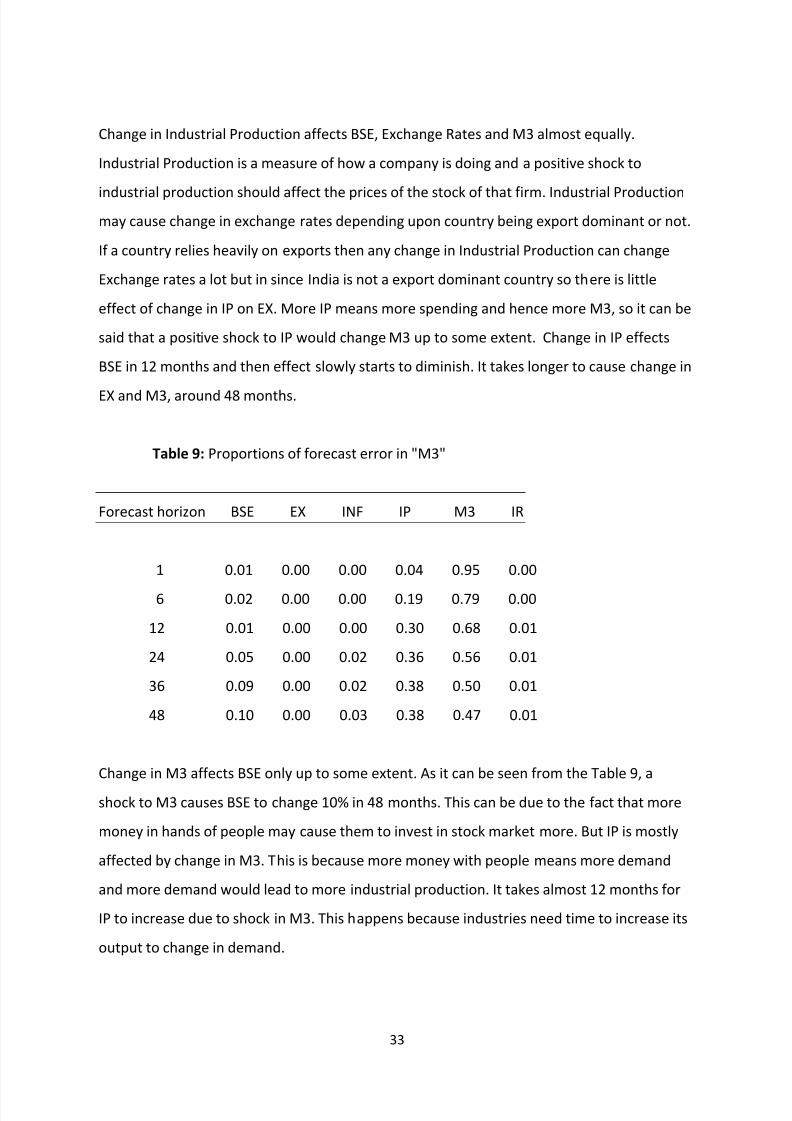

Table 9...........................................................................................................................33

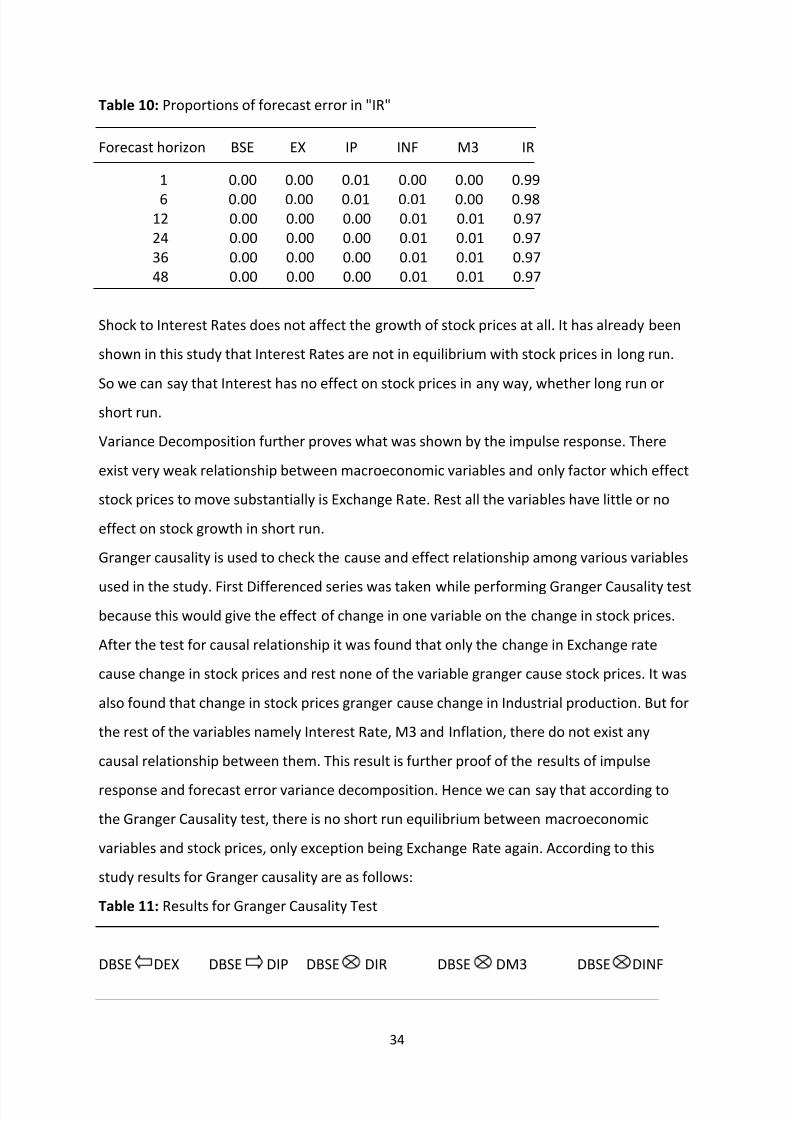

Table 10.........................................................................................................................34

Table 11.........................................................................................................................34

Table 12.........................................................................................................................39

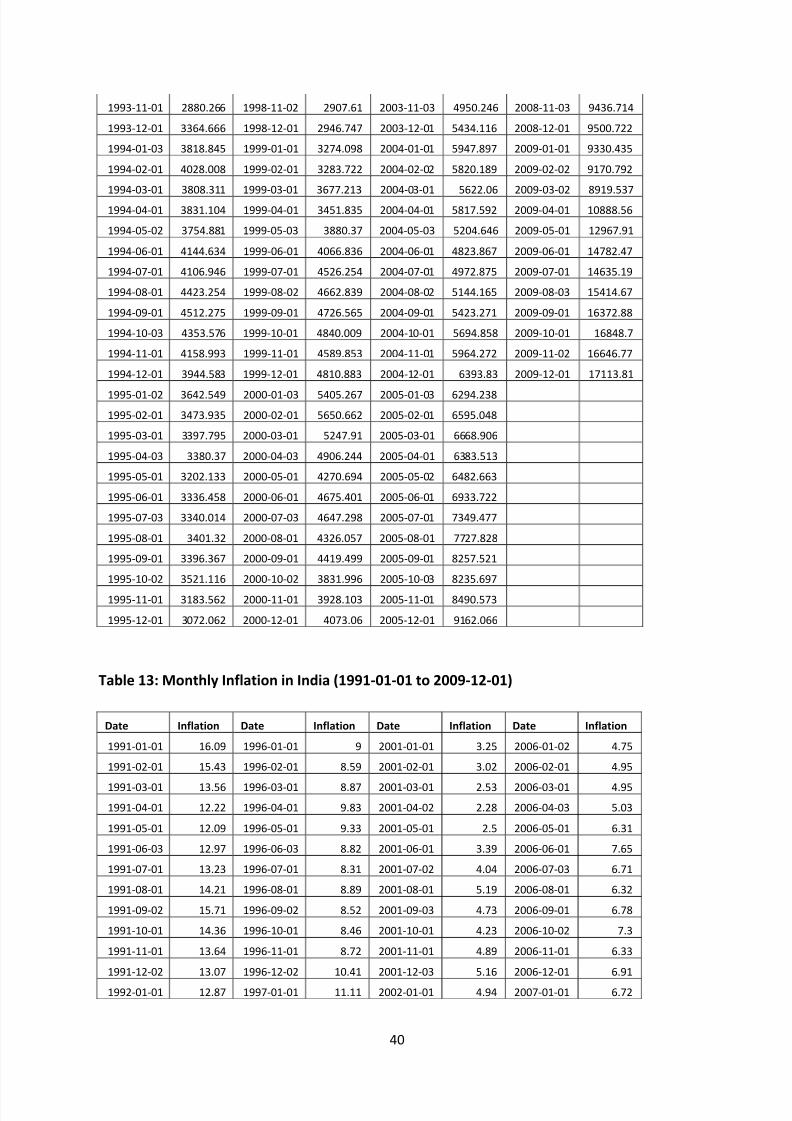

Table 13.........................................................................................................................40

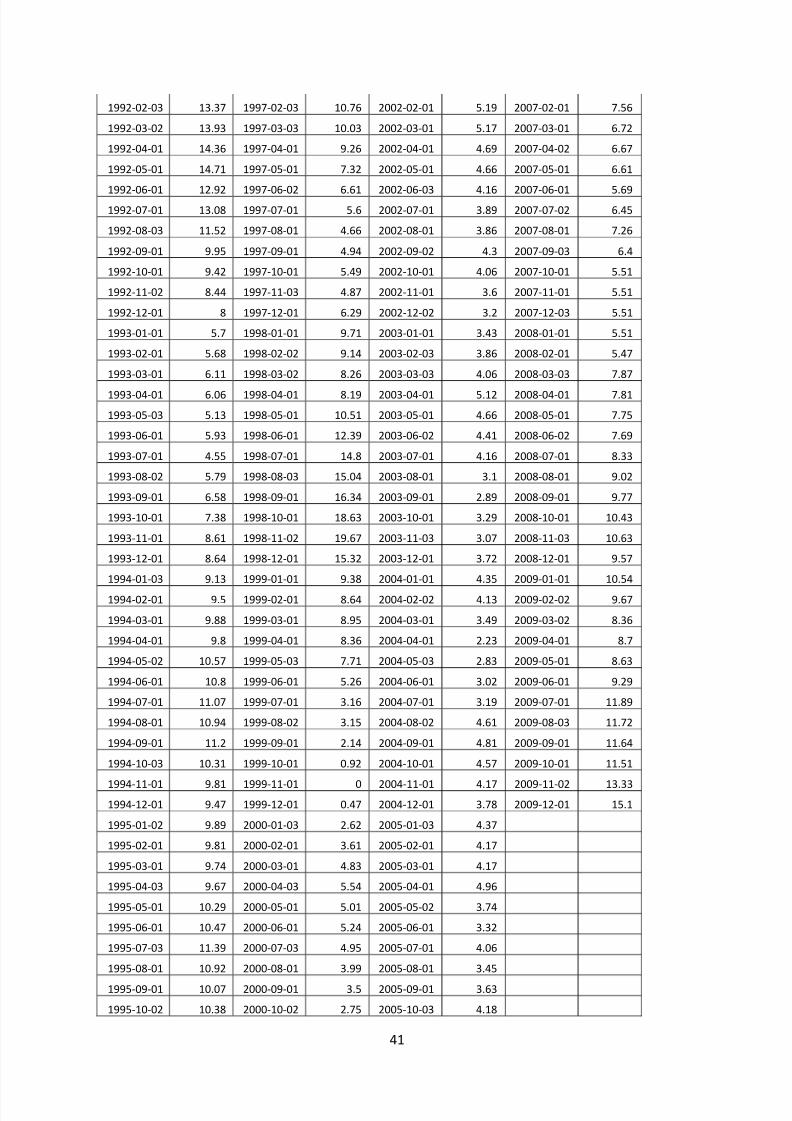

Table 14..........................................................................................................................42

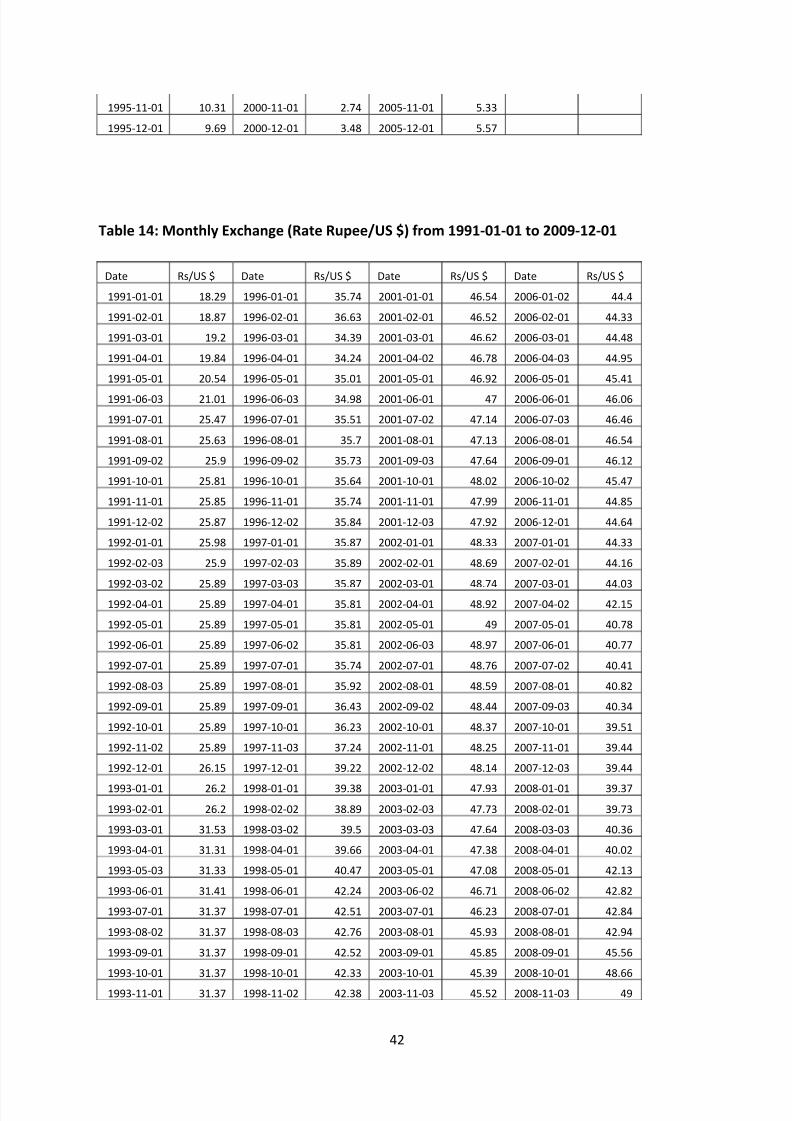

Table 15..........................................................................................................................43

Table 16..........................................................................................................................45

Table 17..........................................................................................................................46

8/6/2019 Long Term and Shrt Run relationship between Macroeconomic variables and stock market in India

http://slidepdf.com/reader/full/long-term-and-shrt-run-relationship-between-macroeconomic-variables-and-stock 9/48

9

(1) Introduction:

This dissertation is an attempt to study the long run equilibrium and short run dynamic

relationship of Indian Stock Market with its Macroeconomic variables during 1991 to 2009.

Reason for choosing this study was the fact that there had been very less research work

done on relationship between stock prices and macroeconomic variables for developing

countries, especially India, whereas one can find lot of work in this field for developed

economies like US, UK, Japan and other European economies. Most of the studies on this

topic, in relation to Indian economy, have been very limited in terms of number of variables

used in research. Some studies have been done on Indian economy but those were

concentrated on developing nations as a whole rather than looking specifically at India. I

could not find any research paper using five macroeconomic variables to find the

relationship between macroeconomic variables and stock prices in India. In this topic I am

trying to find whether a dynamic relationship between Indian stock market Growth and

macroeconomic variables exists in long run and short run. In emerging economies like India,

often the company information is late and of low standards which makes it difficult to

correctly evaluate the true value of company shares (Bekaert and Harvey 1998). Few

questions that need to be answered through this dissertation are

Is there long run equilibrium between Indian Stock Prices and its macroeconomic

variables?

Is there a short run causal relationship between variables?

How much one variable can be explained by innovation in other variable?

(1.1) Developments in Indian Economy

Economic reforms in India started in 1990-91 when India was struggling with its balance of

payments and high inflation due to increase in oil prices caused by Gulf war. Indian Stock

Markets experienced an era of high growth after the liberalization of Indian Economy in

8/6/2019 Long Term and Shrt Run relationship between Macroeconomic variables and stock market in India

http://slidepdf.com/reader/full/long-term-and-shrt-run-relationship-between-macroeconomic-variables-and-stock 10/48

10

1991. Indian economy was on the brink of bankruptcy as foreign reserves were almost

extinct in 1991 with inflation as high as 11% and economy was about to collapse. Then

finance minister and current Prime Minister of India Mr. Manmohan Singh took first step

towards liberalization by privatizing sectors like Telecom, Aviation, Banks etc. and openingup the gates for FDIs and FIIs in India and hence calling an end to high tax regime in India.

With more flow of foreign capital, the Indian stock markets saw its capitalization going up

exponentially. From the period between 1990 and 2010, Indian economy has grown at more

than 6% annually. Economic reforms helped boost sectors like Information Technology,

Pharmaceuticals, Telecom, Aviation, banking, textile and Real Estate which lead to more

private players playing important role in the economy. In 2009, seven Indian firms were

listed among the top 15 technology outsourcing companies in the world.

While the credit

rating of India was hit by its nuclear tests in 1998, it has been raised to investment level in

2007 by S&P and Moody's.

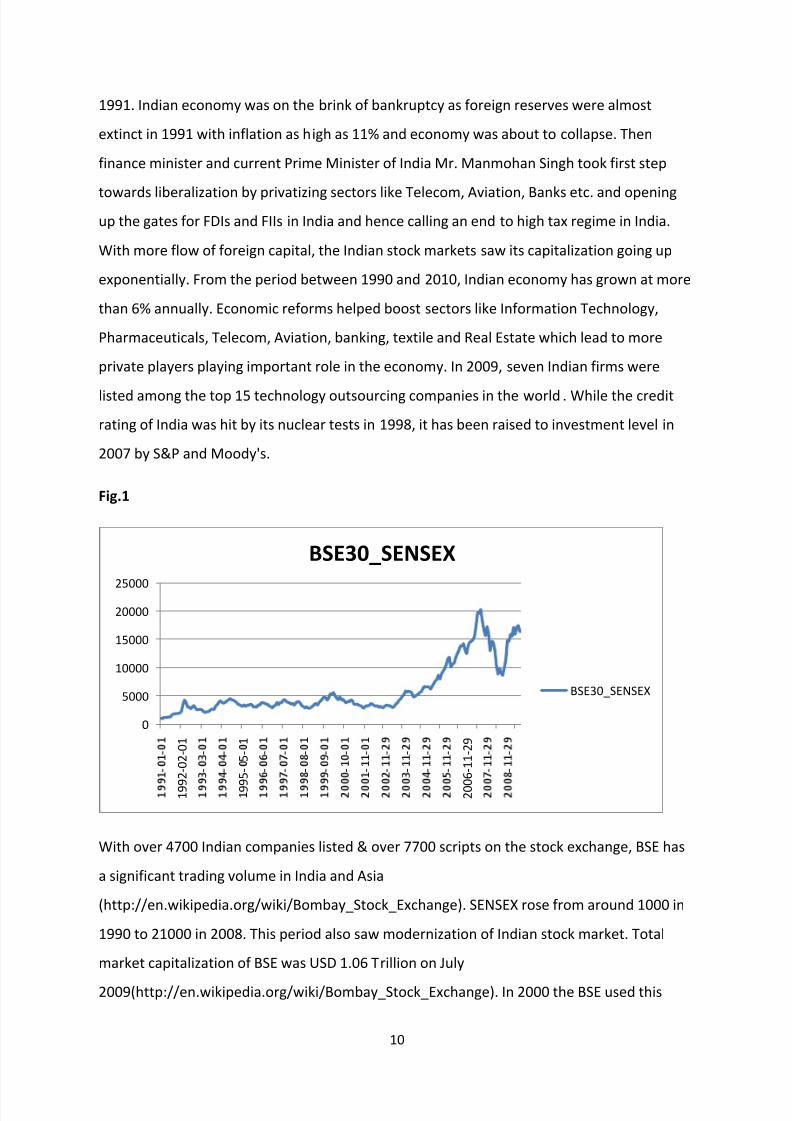

Fig.1

With over 4700 Indian companies listed & over 7700 scripts on the stock exchange, BSE has

a significant trading volume in India and Asia

(http://en.wikipedia.org/wiki/Bombay_Stock_Exchange). SENSEX rose from around 1000 in

1990 to 21000 in 2008. This period also saw modernization of Indian stock market. Total

market capitalization of BSE was USD 1.06 Trillion on July

2009(http://en.wikipedia.org/wiki/Bombay_Stock_Exchange). In 2000 the BSE used this

0

5000

10000

15000

20000

25000

-

-

1 9 9 2 - 0 2 - 0 1

-

-

-

-

9 9 5 -

5 -

1

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

2 0 0 6 - 1 1 - 2 9

-

-

-

-

BSE30_SENSEX

BSE30_SENSEX

8/6/2019 Long Term and Shrt Run relationship between Macroeconomic variables and stock market in India

http://slidepdf.com/reader/full/long-term-and-shrt-run-relationship-between-macroeconomic-variables-and-stock 11/48

11

index to open its derivatives market, trading Sensex futures contracts. The development of

Sensex options along with equity derivatives followed in 2001 and 2002, expanding the

BSE's trading platform. Historically an open-cry floor trading exchange, the Bombay Stock

Exchange switched to an electronic trading system in 1995. It took the exchange only fiftydays to make this transition. These changes lead to a very high growth in Sensex from 1997

and thereafter. But this period was marked by very high volatility in stock market due to

frenzied buying and selling by FIIs. As the Indian stock markets became more integrated

with world market, we saw international events and news affecting the stock prices to a

great extent. On 29th October 2007, Sensex crossed 20000 points ahead of US Federal

Reserve meeting. Stock markets in India saw highest single day gain of 2110.79 points after

the results of 15th general elections in which UPA government won with full majority

signalling a stable political environment ahead.

NSE is the other major stock exchange of India. NSE is the largest stock exchange in terms

of daily turnover and number of trades, for both equity and derivative trades. Main index of

NSE is SNP CNX Nifty. BSE and NSE jointly account for the most of the daily trading done in

India. In this study, BSE data has been used because BSE is still largest stock exchange in

terms of market capitalization and data for BSE was easily available. Furthermore, stockexchanges in India started modernizing after 1995. Today NSE and BSE trade in several

financial products like derivatives, currencies and equities. Very recently a new stock

exchange was started in India called United Stock Exchange. It aims to bring in trading of

Interest Rate Derivatives in India which is still not available in India. Generally Indian stock

markets have been far more volatile than other markets. BSE SENSEX moved from the level

of 1000 in 1991-92 to 21000 points in 2007. It was a 21 times return. But immense poverty

and slow pace of reforms pose a huge challenge in front of India. Still most of the 1.2 Billion

people of India are directly or indirectly dependent upon the agriculture for their living and

agriculture in India is totally dependent upon the seasonal rain. Though the industrial

production shows a double digit growth quarter on quarter but the agricultural growth still

lags around 1-2%. Bureaucratic obstacle makes it very difficult for foreign investments and

widespread corruption in government sector allows only rich and influential people to run

businesses. Internet penetration is still among the lowest in the world. Lack of government

8/6/2019 Long Term and Shrt Run relationship between Macroeconomic variables and stock market in India

http://slidepdf.com/reader/full/long-term-and-shrt-run-relationship-between-macroeconomic-variables-and-stock 12/48

12

spending on key sectors like infrastructure can cause India to lose the race to be an

economic superpower in future.

India has done remarkably well in few sectors. Information Technology has been the pillar of

the Indian growth story. BPOs and KPOs have become very common in every big city of

India. Most of the jobs are being off shored to India because of the availability of super

cheap labour. This is why India is now being called back office of the world. Another miracle

industry is Telecommunication Industry. With cheapest call rates, India is the fastest

growing telecom market of the world. India has maximum number of mobile users after

China. Healthcare has been another growth area for Indian economy.

India has become one of the most attractive investment destinations among the emerging

economies but the growth of the country will depend upon the future policies of the

government. It would be interesting to see how the changes in macroeconomic policies in

future will affect the stock market in India. According to World Bank estimates India would

need $ 1000Billion by 2015 for the development of its infrastructure. This opens further

opportunities for investment in India.

(2)Literature Review

Several studies have been done in the past on the relationship between stock Growth and

fundamental variables using different models and variables (for example Fama, 1965;

Granger and Morgerstern, 1963). There has been increased interest for research in this field

after development of co integration Techniques by Granger (1986) and Engle and Granger

(1987). It has been shown in some papers that the causal relation between stock Growth

and various macroeconomic variables exist in almost all the countries in long run but in

short run it may or may not exist.

Keywords used for locating these literatures were MACROECONOMIC VARIABLES, STOCK

PRICES, GROWTH, VECTOR AUTO CORRELATION, VAR, COINTEGRATION and INDIA. Firstly, I

started with looking for MACROECONOMIC and STOCK PRICES. I found lot of articles, many

of them were irrelevant. After reading few papers I found that my study would be based on

VAR and VECM models and I need to find more papers which were employing the

econometrics techniques like VAR and VECM. So I searched for VAR and COINTEGRATION

8/6/2019 Long Term and Shrt Run relationship between Macroeconomic variables and stock market in India

http://slidepdf.com/reader/full/long-term-and-shrt-run-relationship-between-macroeconomic-variables-and-stock 13/48

13

technique on EBSCO search. I got many relevant papers. Search criterion was filtered for

only PEER REVIEWED PAPERS. Term INDIA was also included in every search but I could not

find any relevant paper on Indian economy. This shows very little work has been done in this

field in Indian context. Database used was EBSCO.

Following literatures gives us an idea about studies on relationship between stock Growth

and macroeconomic variables of different countries. All studies have considered different

economic variables and used different econometric techniques to find the relationship

between macroeconomic variables and stock prices. These studies are listed in

chronological order of year of being published.

(2.1) CHRONOLOGICAL REVIEW OF LITERATURES:

An important study in this field was done by Abdulla (1993). Though this study was on US

economy which is not much related with the study on Indian economy but the methods

used in this study have been explained very well and makes it very easy for the reader to

reach a conclusion. All the inferences are very well supported by the theoretical arguments

and compared with the results obtained by previous studies. This study was aimed at finding

the fluctuations of US stock market using monthly data which was not often used in other

studies in US. Abdullah and Hayworth have emphasised on use of monthly data in place of

weakly and daily by explaining that use of daily and weekly data eliminates many the use of

many important variables from the study due to unavailability of the complete data. Model

used in this analysis is VAR estimation with tests for Granger Causality, Variance

Decomposition and sum of coefficient of the lag variables. VAR estimation and Granger

Causality Test were simple and same as done in numerous other studies. But test for error

variance decomposition was employed using two orders of variables to check the effect of

innovation in one variable on other variables. Order of selection of variables has been

discussed in detailed. Sum of coefficients of lag variables are not generally used in analysis

but in this study, the test gives some important outcomes which are according to the

theoretical studies on economy. Choice of variables in this study was another interesting

part; variables used were S&P, Trading Deficit, Budget Deficit, CPI, Money Supply, Short

Term Interest Rates and Long Term Interest Rates. Other important variables like Industrial

Production and Exchange Rates were not included into the study. All the processes of

8/6/2019 Long Term and Shrt Run relationship between Macroeconomic variables and stock market in India

http://slidepdf.com/reader/full/long-term-and-shrt-run-relationship-between-macroeconomic-variables-and-stock 14/48

14

testing are explained in detail which makes it easy to interpret the results. But there were

few short comings. This study doesn’t seem to distinguish very clearly about the short term

and long term impact of changes in macroeconomic variables on stock prices like use of

Cointegration techniques could have given clearer view of long run relationship betweenstock prices and macroeconomic variables. The final conclusion of the study was that stock

Growth are positively related to inflation and money supply and stock Growth are negatively

related to the trade deficit, budget deficit, long term interest rates and short term interest

rates. This work seems to be very precise and accurate at same time. Models seem to be

useful tools in analysis which can be used in my dissertation; I will need few more models to

test the consistency of my results though. This study doesn’t use any alternative model to

check the consistency of the results.

Korean stock market reacts in a different way than US and Japan stock markets to the

change in economic fundamentals. This was founded by Kwon (1999). This paper is very

relevant for my study because economic history of India and Korea has been similar in few

aspects in past 20 years. Both of the economies opened the gates for foreign investment in

1991 and since then both of the economies have seen substantial growth of stock markets

as well as their economy. His study found that stock markets are not the leading indicatorfor macroeconomic fundamentals and stock markets in US and other developed economies

were more efficient than Korean Stock Market. Two indices were used in research namely

KOSPI and SMLS. This was the first time that Cointegration technique was used to find the

relationship between stock Growth and macroeconomic variables in Korea. Unit Root

hypothesis used Augmented Dickey Fuller Test. VECM and Granger Causality were employed

to find causal relationship. Cointegration and VECM proved that there exists Cointegration

between stock prices and macroeconomic variables- Production Index, Trade balance,

Exchange Rate and Money Supply. There are few differences between Indian economy and

Korean economy that need to be considered while selecting variables for Indian economy

like Trade Balance is not a very important factor when it comes to Indian economy because

Indian economy, unlike Korea, is not a export oriented economy. This means that I can drop

Trade Balance from my study and I can rather take some other more relevant variable. This

study proves the existence of long run relationship and Cointegration between the

economic variables and stock prices. Not much has been done to find short run relationship

8/6/2019 Long Term and Shrt Run relationship between Macroeconomic variables and stock market in India

http://slidepdf.com/reader/full/long-term-and-shrt-run-relationship-between-macroeconomic-variables-and-stock 15/48

15

in this study. Techniques like variance decomposition and impulse response could have

been employed to get a clearer picture of the effects of change in one variable on other

variables. This is very basic and fundamental study but it gives very useful results which are

in accordance with the theoretical aspects of Korean economy. This study proves thatKorean stock market is very different from other stock markets of advanced economies like

US and Japan, and behaves more like other emerging economies which are more sensitive

to change in inflation and interest rates. This work provides a better understanding of

development in emerging economies than Moradoglu (2000). Results are more concrete

and according to the previous findings

A research done by Muradoglu (2000) was first research covering almost all the developing

nations at that time. It included 19 developing nations. Aim of the study was to find the

causal relationship between stock Growth and macroeconomic variables. He used data from

1976 to 1997 which is a fairly long period and can be considered for long run analysis.

Macroeconomic variables which he considered were Exchange rate, Interest Rate, Inflation

and Industrial Production. He reached different conclusions for different countries. This

predominantly showed that different emerging economies respond to the changes in

economic fundamentals and stock prices in different ways. In regard to India, the resultsshowed that real sector and domestic production in India followed the stock Growth. Also,

exchange rates were Granger caused by stock Growth in India. Study found that out of

nineteen countries only twelve countries had causal relationship with stock market. He

concluded that these 12 countries are the one where liberalization started earlier and

markets in these countries became more developed and much more integrated with the

international markets. This study gives a wide overview of many developing countries of the

world but there some major shortcomings which need to be considered. There has been use

of only Granger causality to find the inferences. Consistency of the results was not

established by the authors. This may lead to some wrong interpretation of real scenario.

Study didn’t tell much about how much one variable can be explained by innovation in other

variable.

Another study in this field was done by Ibhrahim (2003) on Malaysian Economy. This study

also tried to find the co movement of Malaysian stock prices with US and Japan Markets.

This is done basically because Malaysia depends upon its exports and imports heavily and

8/6/2019 Long Term and Shrt Run relationship between Macroeconomic variables and stock market in India

http://slidepdf.com/reader/full/long-term-and-shrt-run-relationship-between-macroeconomic-variables-and-stock 16/48

16

two most important trading partner of Malaysian economy are US and Japan. The method

of estimation used in this study was VAR analysis. He used Impulse Response and Variance

Decomposition to find the dynamic relationship between all the considered variables. Study

seems to give good insight shock in one variable and its effect on other variable while takingin account the effects on rest of the variables. For testing the Cointegration, the method

employed was Johansen (JJ) Cointegration which is considered to be more powerful test

than Engle-Granger test. Augmented Dickey Fuller Test was used for testing the unit roots.

Malaysian economy has many similarities with Indian economy. Both of the economies

started liberalization process during late 80s and early 90s. Both Indian and Malaysian

economies saw phase of very high growth rate after liberalisation and stock markets

responded with exponential growth. But there lies a very basic difference in the economic

framework of both the countries; while Malaysian economy is export oriented and depends

upon trading partners to a large extent, Indian economy, on the other hand, is driven by

high domestic consumption. So, though the techniques used in analysis of both the

economies can be same but we can’t expect same kind of relationship between various

variables as in case of Malaysian Economy. We can expect Malaysian stock prices to be

more sensitive towards variables like Exchange Rates, Industrial Production as these factors

directly influence the results of any firm. But from the perspective of Indian Economy, we

expect stock prices to be more integrated with factors like Inflation, Interest Rates.

Exchange rates are important in Indian context too. The results from this study revealed

some important facts about Malaysian Economy. There is a negative relationship between

the stock Growth and exchange rates. This shows that when value of Malaysian currency

goes up, the stock market too responds by an upward movement. This shows that though

Malaysia is export oriented economy, even then Malaysia depends upon its imports a lot.

Relationship between stock prices and CPI is negative which is different from what was

found in the recent studies for other countries. An interesting observation came up while

comparing the stock movement of Malaysia with US and Japanese counterpart. It was found

that Malaysian stock market is positively related with US and negatively related with Japan.

This seemed to be contradictory. I won’t discuss these results as co movement of stock

prices of different countries is not the part of this study. Results of this study are compared

by analysing them through Cointegrating Equation, Impulse Response function and VarianceDecomposition. All the three techniques present a consistent result and give a very good

8/6/2019 Long Term and Shrt Run relationship between Macroeconomic variables and stock market in India

http://slidepdf.com/reader/full/long-term-and-shrt-run-relationship-between-macroeconomic-variables-and-stock 17/48

17

understanding of dynamic relationship between various variables in long run and short run.

Most of the inferences are very well supported by the arguments on happenings in real

economy.

Patra (2006) identified that there exists both long run and short run relationship between

stock Growth and macroeconomic variables for Greek Stock Market. He used the data from

period 1990 to 1999. Variables used in his study were Stock Prices, Inflation, exchange rate,

money supply and trading volumes. He found that causality existed between all the

economic indicators except exchange rate. He attributed this kind of behaviour to the fact

that Greece joined EMU between this period. Various models were used to test the

consistency of the findings. These were Granger Causality, Co integration Techniques, ARCH

Model and Error Correction model (ECM). All the models proved that the results were

consistent. This study is very useful for understanding relationship between stock Growth

and macroeconomic indicators for emerging economies. Fundamental changes in Greek and

Indian economy happened during same period from 1990 and stock markets of both the

economies behaved in somewhat similar pattern during this period. His findings very well

support the real economic activities happening in Greece. Stock markets in Greece rose

sharply after 1997. Greek interest rates dropped a lot by 1997 and investors moved towardsstock market in order to get better Return. With Greece’s entry into Exchange Rate

Mechanism, the investors’ confidence on Greek Stock Market increased further and as a

result Greek stock market reached new peak in 1998. Similarly, Greece saw very high

inflation during 1990 to 1999 but with strong control on money supply by Greek

government the inflation dropped to 2.6% in 1999 from 19.5% in 1990. This boosted the

investors’ confidence further and led to rise in stock market. All these economic events are

according to the findings by Patra (2006). It was concluded in his study that Athens Stock

Exchange is inefficient as macroeconomic variables and trading volume can be good

predictors of the stock prices.

Ratanapakorn (2007) reaches different conclusion for US stock market. He used six

macroeconomic variables in his research namely Inflation, Money Supply, Exchange rates,

long term Interest rates, short term interest rates and Industrial Production. The study

8/6/2019 Long Term and Shrt Run relationship between Macroeconomic variables and stock market in India

http://slidepdf.com/reader/full/long-term-and-shrt-run-relationship-between-macroeconomic-variables-and-stock 18/48

18

showed that all the six macroeconomic variables do not Granger Caused stock prices in

short run but in the long run all the variables Granger Caused the stock prices. This finding

was very different from Patra (2006) for Athens Stock Exchange. Data used by Ratanapakorn

(2007) was from period 1975 to 1999. This is fairly long period under consideration ascompared to one used by Patra (2006). It may not be possible for Patra (2006) to do such

analysis because of lack of availability of data for Greece. In fact, this is the problem with

most of the developing economies of the world. Most of the data which is available starts

from time when liberalization started in that country; this may not be true for each and

every country though. Models that have been used in this study are Granger Causality Test,

Vector Error Correction Method (VECM), Augmented Dickey Fuller (ADF) Unit Root test,

GARCH-X which is an extension of GARCH model. Co integration results show that there is a

good degree of co integration between variables and stock prices. This indicates that there

can be an arbitrage opportunity considering the changes in the macroeconomic variables

will cause stock prices to change in the future. This research has used specific tools for

finding long term and short term relationships. It gives more detailed and more useful

conclusions at the end of the study. This research is very apt base for studying Indian

Economy. Greece economy is also a developing economy like the Indian economy and

Greece’s economy is not dependent upon exports like other emerging economies of the

world. So, the fundamentals of both the economies can be compared to establish a

theoretical reasoning and relevance of the results of econometric analysis.

After looking at all the above literatures, I found that lots of empirical work has been done

on finding relationship between macroeconomic indicators and stock prices for different

countries. Many researches have been done on emerging market economies too. These

studies on emerging economies can be a very good estimate for Indian economy as well but

there are few fundamental differences which need to be addressed. Indian economy is very

less dependent upon the trade and is predominantly a domestic consumption driven

economy. This means that variable used in analysis will be different for Indian economy and

importance of a variable will not be same as for other emerging economies. As far as use of

econometric models is concern, I think basic tests for unit root and Cointegration are must

in an empirical work of this type of study. Most of the literatures employ Vector Auto

Regression (VAR) based model and more recent study use VECM and extensions of GARCH

8/6/2019 Long Term and Shrt Run relationship between Macroeconomic variables and stock market in India

http://slidepdf.com/reader/full/long-term-and-shrt-run-relationship-between-macroeconomic-variables-and-stock 19/48

19

model. Another very important method which is used in almost all the study was Granger

causality test but there is two more tests which I think are more informative and gives a

clearer picture of long run and short run relationships; these methods are Variance

Decomposition and Impulse Response. Although not all the research works use these twomethods but they are employed very often to check the consistency of the results obtained

by other models. There is scope of doing univariate analysis too with multivariate analysis.

Univariate analysis can be used to forecast the price of stock prices and then it can be

compared with forecast of multivariate analysis to see if we get same or different result.

Amount of difference in the result can also tell us that macroeconomic indicators which we

chose are how much efficient in deciding the movement of stock prices. All these literatures

provide a very good base for understanding the methodologies to use. They also give

information regarding which model is how much efficient in reaching conclusion. There are

conflicting results in the literatures but they are probably due to the fact that the countries

used in the studies are different and they have different economic fundamentals.

(3) THEORETICAL FRAMEWORK

Economic Variables which will be used in this research are Inflation, Interest rates, exchange

rates, Industrial Production and Money Supply. These economic variables are supposed to

be important indicators of stock Growth (see Fama 1981; Chan et al., 1986; Smith and Sims,

1993, etc.). Understanding of the cause and effect relationship of various variables with

stock Growth is very important for framing the economic policies for a country.

(3.1) Inflation

Inflation has negative relationship with stock prices; this can be seen in various researches

like Malkiel (1979). Chaudhary (2001) found positive relationship between stock prices and

inflation in economies like Argentina, Chile, Mexico and Venezuela. Lee (1992) tried to

explain this relationship using VAR and VECM models for US. He found that stock prices do

not explain variation in inflation much but interest rates do explain the variation in inflation.

The relationship between stock prices and inflation has always been a debatable issue

8/6/2019 Long Term and Shrt Run relationship between Macroeconomic variables and stock market in India

http://slidepdf.com/reader/full/long-term-and-shrt-run-relationship-between-macroeconomic-variables-and-stock 20/48

20

among the researchers. Negative relationship between stock prices and Inflation may be

due to the fact that more inflation means that currency of that country losing its value

which may cause foreign investors to withdraw money from that country and move to some

other country. But this has not always been true. We can often seen period of high inflationand stock prices rise in emerging economies. India and China are the most recent example

to this. So, though some studies prove the negative relationship but we need to look into

the other factors also.

(3.2) Exchange rate

Exchange rate is also an important variable in this research. Exchange rates can affect the

profits of a company and hence, affect the price of its stock. Abdalla and Murinde (1997)

used Granger Causality and co integration test to find that there exists a unidirectional

causality between exchange rate and stock price in developing countries like India, Pakistan

and Korea. A study done by Granger, Huang and Yang (2000) on nine Asian countries

showed different results for different countries. Impact of Exchange Rates can be on either

side. If a country is export dominant then fall in exchange rate will cause stock prices to go

up as the firms will have more profitability from exchange rates but if a country is import

dominant then increase in exchange rates will cause firms to buy at higher prices, thus

reducing their profitability and resulting in fall of stock prices.

(3.3) Interest Rate

Interest Rates causes stock prices to move in opposite direction in both long and short run.

A decrease in interest rate may in increase the profitability of a company by reducing itscosts. This may result in rise in stock prices (Ratanapakorn, 2007). A study done by

Mukherjee and Naka (1995) shows that there is a direct relation between stock prices and

short term interest rates in Japan.

(3.4) Money Supply

8/6/2019 Long Term and Shrt Run relationship between Macroeconomic variables and stock market in India

http://slidepdf.com/reader/full/long-term-and-shrt-run-relationship-between-macroeconomic-variables-and-stock 21/48

21

M3 can be said to be the amount of money in hands of people in an economy. M3 gives us a

measure of action taken by Central Bank of a country to regulate the money supply in the

economy, RBI in case of India. How do these measures affect the stock prices? This can be

estimated by the help of the M3. Increase in money can cause stock market to move upbecause as the money supply increases, the interest rates will fall and this will raise the

stock prices. Also the fact, that increase in money supply will increase the expected inflation

and hence increase the discount rates which can cause stock prices to fall. This makes

money supply a debatable topic for researchers. Ratanapakorn, O. et al (2007).

(3.5) Industrial Production

Industrial Production is a measure of how an economy is doing. If industrial production of an

economy is increasing then its stock must move up as the valuation of the firms and

businesses in that economy goes up. If IP figures of an economy are good then stock

markets tend to give good Return.

(4) EMPIRICAL FRAMEWORK

In this research, variables used are monthly average prices of BSE (SENSEX), Inflation (INF),

Industrial Production (IP), Exchange Rate (EX), Interest Rates (IR) and Money Supply (MS).

Here inflation and IP represents goods market and IR and MS represent money market.

Econometric tests and models used are Augmented Dickey Fuller, Granger Causality, Engle-

Granger Cointegration Technique, VAR analysis using Impulse Response and Variance

Decomposition. These tests and models are explained below:

(4.1)Stationary and Non stationary Data: We must check stationarity of our time series

data before using it in our models. Data is considered to be non-stationary if its first three

moments namely mean, variance and covariance are not constant. If a time series is non

stationary then it moves away from its mean value, whereas if a series is stationary then it

comes back to mean value after going up or down. Non stationary data can be made

stationary by differencing it. But this doesn’t mean that first differenced series will be

stationary. We may need second or third or even more difference depending upon the data.

Hypothesis for testing stationarity is presence of Unit Root. A series with unit root present in

8/6/2019 Long Term and Shrt Run relationship between Macroeconomic variables and stock market in India

http://slidepdf.com/reader/full/long-term-and-shrt-run-relationship-between-macroeconomic-variables-and-stock 22/48

22

it is said to be non stationary and a series where no unit root is present is said to be a

stationary series.

Studies done in the past have found that if a unit root is present in a series then that will

lead to spurious regression. Spurious regression may cause wrong results as the results

show strong relationship between the variables which may not necessarily be the case. If

this happens then we may reach to a wrong or meaningless conclusion. There are many

methods to test unit roots:

Dickey Fuller

Augmented Dickey Fuller

Philips-Perron (PP) Test

In this paper ADF has been to use as this is the most commonly used unit root test by

econometricians.

(4.2)Augmented Dickey Fuller: ADF is the augmented form of Dickey Fuller Test. This test is

used for checking the presence of unit root. ADF is used for complicated time series data.

ADF is used in following type of models

∆ = + + −1 + 1∆−1 +⋯+ ∆− +

Where is a constant, is coefficient of time trend and p is the lag order of autoregressive

process. This means that ADF allows high order autoregressive processes. To find which

order to use in a ADF, we can do the regression and see which coefficients are significant or

alternatively we can use any of the information criterion like Akaike Information Criterion,

Bayesian information criterion or Hannan Quinn information criterion. Unit root test

hypothesis is:

0: = 0 Unit Root Present

0: < 0 No Unit Root

(4.3) Cointegration Theory and Engle Granger Cointegration Test: Two series are said to be

cointegrated if they have unit root present individually in each of them and their linear

8/6/2019 Long Term and Shrt Run relationship between Macroeconomic variables and stock market in India

http://slidepdf.com/reader/full/long-term-and-shrt-run-relationship-between-macroeconomic-variables-and-stock 23/48

23

combination has lower order of integration. This theory was developed first by Engle and

Granger (1987). If we have and as non stationary series of I(1) and on regressing on

:

= +

we find that ~ I(0) then these two series are said to be cointegrated of order one. This is

precisely the Engle Granger Test. Engle Granger Cointegration technique firstly requires a

Unit Root Test to check whether the considered series are stationary or not. This unit root

test can be performed using Augmented Dickey Fuller or Philips Perron (PP) test. Co

integration technique is used to find long term relationship between the macroeconomic

variables and stock Growth.

(4.4) Granger Causality: Engle and Granger (1987) said that in two series are cointegrated

then there must be some causality between them. If we have two series and and we

regress on its lag and the lags of variable, then if coefficient of the regression are

jointly significant then we say that granger causes . Granger causality is used to find

short run and long run causal relationship. It helps in understanding the relationship in 4

ways namely

Unidirectional causality from macroeconomic variables to stock Growth,

Unidirectional causality from stock return to macroeconomic variables,

Bidirectional causality,

No relationship.

To test the hypothesis that X granger causes Y we look at following regressions:

= 1−1 + 1−1 + (Unrestricted Regression)

= 2−1 + (Restricted Regression)

To test the null hypothesis that ‘X does not cause Y’ we perform a F-Test:

8/6/2019 Long Term and Shrt Run relationship between Macroeconomic variables and stock market in India

http://slidepdf.com/reader/full/long-term-and-shrt-run-relationship-between-macroeconomic-variables-and-stock 24/48

24

=

( −)( − )

( − )

Where n is the number of observations and k is the number of estimable parameters in each

regression.

To find the causal relationship between stock prices and macroeconomic variables following

equation has been used:

=

0 +

1

=1 −+

2

=1 −+

3

=1 −

+4

=13−+5

=1− +

If the coefficient of any of the lagged macroeconomic variable is jointly significant then we

can say that the variable Granger causes the stock return.

(4.5) Vector Auto Regression (VAR): In VAR equation for each variable explains the

evolution of that variable based on its own lag and lag of other variables which are included

in the model. This study uses 5 macroeconomic variables to model VAR. The equation for

VAR is given by:

= 0 +

=1 − +

Here, = 5 × 1

0 = 5 × 1 , = 5 × 5 ,

= 5 × 1

8/6/2019 Long Term and Shrt Run relationship between Macroeconomic variables and stock market in India

http://slidepdf.com/reader/full/long-term-and-shrt-run-relationship-between-macroeconomic-variables-and-stock 25/48

25

Vector Auto Regression (VAR) is used to find the relationships between various variables by

taking into account the feedback by other variables. Estimation based on VAR includes

endogenous as well as exogenous variables in the equation making it an important tool for

multivariate analysis.

It is very important for the order of integration of all the variables used in model to be

same. If variables are I(0) then it is said to be VAR at level. If variables are I(d) where d>0

then we have to add a error correction term into our model. This type of model is called

VECM (Vector error correction model). If variables are not cointegrated and are I(d) then we

have VAR at difference. While selecting the lags for the VAR model following three

Information Criterions have been employed:

Akaike Information Criterion: It was proposed by Hirotsugu Akaike in 1974. It is used to find

the goodness of fit of any econometric model. It basically tells us about the amount of

information lost while a model is being used to describe the reality. Generalized form of AIC

can be written as:

= 2 − 2ln ()

Where k is the number of parameters in the statistical model, L is maximised value of

likelihood function for the estimated model. AIC not only measures the goodness of a fit but

it also punishes for the increased number of estimated parameter. So it can be said that AIC

discourages the over fitting. Value assigned by the AIC is meant only to ranks the model and

find the best from different models. The value is nowhere used in our estimation or

Hypothesis at any point. Model with the least value of AIC is said to be the best model.

Bayesian Information Criterion or Schwartz Information Criterion: This criterion used forsame purpose but it penalizes more for including extra parameter in model than AIC. While

using maximum likelihood estimation for estimating a model, it is possible to increase the

likelihood by adding the parameters but this may lead to over fitting. By using BIC we can

resolve this problem because BIC introduces a penalty term. As in AIC, model with lower

value to BIC should be chosen.

Hannan Quinn Information Criterion: It is also the measure of goodness of fit like AIC and

BIC.

8/6/2019 Long Term and Shrt Run relationship between Macroeconomic variables and stock market in India

http://slidepdf.com/reader/full/long-term-and-shrt-run-relationship-between-macroeconomic-variables-and-stock 26/48

26

Two very useful methods of examining the properties of VAR are Variance Decomposition

and Impulse Response.

(4.5.1) Variance Decomposition is also known as forecast error variance decomposition. It

explains the amount of information that each variable contributes towards the change in

other variables. It tells how an exogenous shock in some variables contributes to the

forecast error variance of other variable. Order of selecting the variables is an important

issue in variance decomposition. We employ Cholesky Decomposition to decide the order of

the included variables.

(4.5.2) Impulse Response is basically the graphical representation of the change caused to

other variables by the shock or impulse in one variable. This is shock in error term of one

equation which propagates into the entire system. We can also say that, we trace the

response of endogenous variables to a ‘unit’ change of error term of a particular equation.

Numerous methods can be employed to know what kind of unit change we need to make

into the system but generally we make use of positive change of one standard deviation.

This change propagates into the system and changes the value of the dependent variables

for each time period.

All the data is collected from Datastream and PCgive statistical package will be used for

calculation. Data used for the analysis will be from 1991 to 2010 which is comparatively

short period for finding the long run relationship between the variables. For long run

analysis we should have data of past 30 years at least but due to unavailability of data

before 1991 we are restricted to consider data from 1991 only.

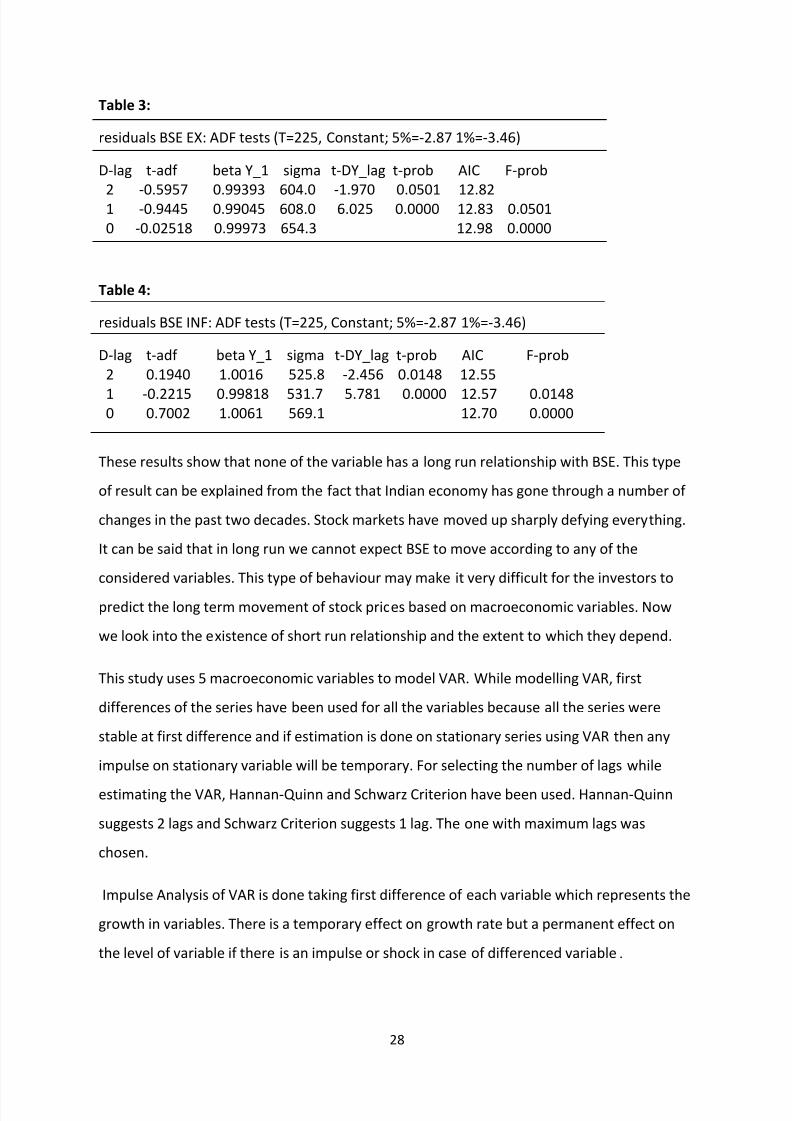

(5.0) Tests and Results

Test for stationarity of all the series used in our analysis namely BSE, INF, EX, IR, IP, M3 is

done using Augmented Dickey Fuller Test (ADF). The results show that all of the series

contain unit root except M3 and IP. So we conclude here that M3 and IP cannot be

cointegrated with other variables because for a series to be cointegrated with other series

should be at least integrated to first order, I(1) and hence, it can be said that M3 and IP has

no long run relationship with other variables. IP is stationary at 5% significance level but it is

8/6/2019 Long Term and Shrt Run relationship between Macroeconomic variables and stock market in India

http://slidepdf.com/reader/full/long-term-and-shrt-run-relationship-between-macroeconomic-variables-and-stock 27/48

27

non stationary at 10% significance level. We would not consider 10% level significance in

this study as this may lead to misguided results in the end. For rest of the variables, they are

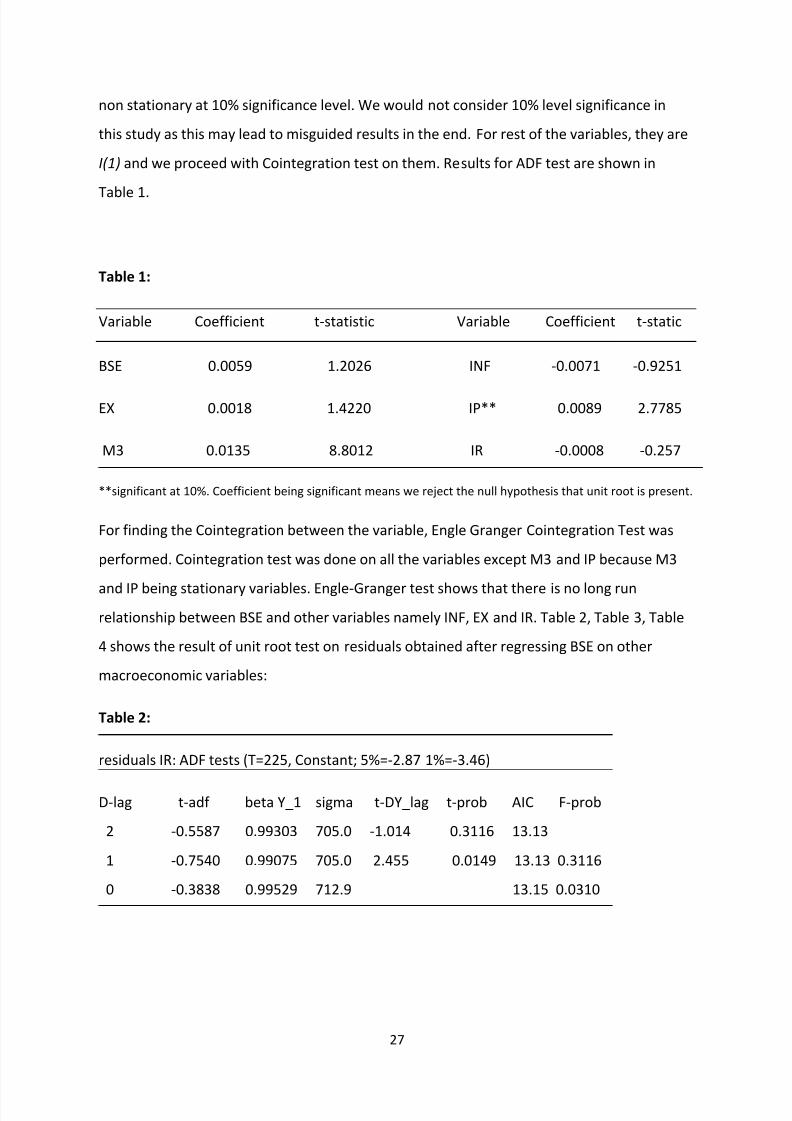

I(1) and we proceed with Cointegration test on them. Results for ADF test are shown in

Table 1.

Table 1:

Variable Coefficient t-statistic Variable Coefficient t-static

BSE 0.0059 1.2026 INF -0.0071 -0.9251

EX 0.0018 1.4220 IP** 0.0089 2.7785

M3 0.0135 8.8012 IR -0.0008 -0.257

**significant at 10%. Coefficient being significant means we reject the null hypothesis that unit root is present.

For finding the Cointegration between the variable, Engle Granger Cointegration Test was

performed. Cointegration test was done on all the variables except M3 and IP because M3

and IP being stationary variables. Engle-Granger test shows that there is no long run

relationship between BSE and other variables namely INF, EX and IR. Table 2, Table 3, Table

4 shows the result of unit root test on residuals obtained after regressing BSE on other

macroeconomic variables:

Table 2:

residuals IR: ADF tests (T=225, Constant; 5%=-2.87 1%=-3.46)

D-lag t-adf beta Y_1 sigma t-DY_lag t-prob AIC F-prob

2 -0.5587 0.99303 705.0 -1.014 0.3116 13.13

1 -0.7540 0.99075 705.0 2.455 0.0149 13.13 0.3116

0 -0.3838 0.99529 712.9 13.15 0.0310

8/6/2019 Long Term and Shrt Run relationship between Macroeconomic variables and stock market in India

http://slidepdf.com/reader/full/long-term-and-shrt-run-relationship-between-macroeconomic-variables-and-stock 28/48

28

Table 3:

residuals BSE EX: ADF tests (T=225, Constant; 5%=-2.87 1%=-3.46)

D-lag t-adf beta Y_1 sigma t-DY_lag t-prob AIC F-prob

2 -0.5957 0.99393 604.0 -1.970 0.0501 12.821 -0.9445 0.99045 608.0 6.025 0.0000 12.83 0.0501

0 -0.02518 0.99973 654.3 12.98 0.0000

Table 4:

residuals BSE INF: ADF tests (T=225, Constant; 5%=-2.87 1%=-3.46)

D-lag t-adf beta Y_1 sigma t-DY_lag t-prob AIC F-prob

2 0.1940 1.0016 525.8 -2.456 0.0148 12.55

1 -0.2215 0.99818 531.7 5.781 0.0000 12.57 0.01480 0.7002 1.0061 569.1 12.70 0.0000

These results show that none of the variable has a long run relationship with BSE. This type

of result can be explained from the fact that Indian economy has gone through a number of

changes in the past two decades. Stock markets have moved up sharply defying everything.

It can be said that in long run we cannot expect BSE to move according to any of the

considered variables. This type of behaviour may make it very difficult for the investors to

predict the long term movement of stock prices based on macroeconomic variables. Now

we look into the existence of short run relationship and the extent to which they depend.

This study uses 5 macroeconomic variables to model VAR. While modelling VAR, first

differences of the series have been used for all the variables because all the series were

stable at first difference and if estimation is done on stationary series using VAR then any

impulse on stationary variable will be temporary. For selecting the number of lags while

estimating the VAR, Hannan-Quinn and Schwarz Criterion have been used. Hannan-Quinn

suggests 2 lags and Schwarz Criterion suggests 1 lag. The one with maximum lags was

chosen.

Impulse Analysis of VAR is done taking first difference of each variable which represents the

growth in variables. There is a temporary effect on growth rate but a permanent effect on

the level of variable if there is an impulse or shock in case of differenced variable.

8/6/2019 Long Term and Shrt Run relationship between Macroeconomic variables and stock market in India

http://slidepdf.com/reader/full/long-term-and-shrt-run-relationship-between-macroeconomic-variables-and-stock 29/48

29

Innovations in growth of exchange rate, Inflation and Interest rates cause stock Growth to

fall of the stock prices and stock prices are set at a new level after the innovation.

In case of exchange rates and Inflation, the stock Growth take approximately 6 periods to

return to zero level, which means growth of stock prices become as they were before the

shock in 6 months. Negative effect of innovation in exchange rate on stock market is

according to the fact that India is an import dominant country and exchange rate should

have negative relationship with stock market. Shock in inflation can cause markets to go

down. This is according to the findings of Malkiel (1979).

Shock caused due to Interest Rates take even less time, 4 to 5 months, for stock Growth to

come back to zero line. Effect of an innovation in Interest rates is negative on stock Growth.

These inferences are according to the functioning of an economy and can be explained

theoretically. Increase in interest rates makes it costlier for investors and businesses to

borrow for investment. Hence they move to other low interest destinations.

An impulse on growth of Industrial Production and Money Supply cause stock growth to

increase for sometime but the level of stock prices increase permanently. It takes almost 6

to 7 months for stock Growth to come back to zero line. This is according to the predicted

theoretical behaviour because increase in Industrial Production and Money supply means

more profit for the firms and more money in hands of people to spend. Hence this should

lead to an increase in stock growth.

These impulse responses gives us direction of the movement of stock prices with respect to

the shock in macroeconomic variables but the responses are of very small magnitude

(except for EX). So, based on these results, it can’t be said that there is a very strong

evidence of relationship between stock prices and macroeconomic variables. In fact, only EX

seem to be cause substantial movement in stock prices and rest other variables can be said

to have a negligible effect on stock growth. Results of Impulse response are show in figures

below:

8/6/2019 Long Term and Shrt Run relationship between Macroeconomic variables and stock market in India

http://slidepdf.com/reader/full/long-term-and-shrt-run-relationship-between-macroeconomic-variables-and-stock 30/48

30

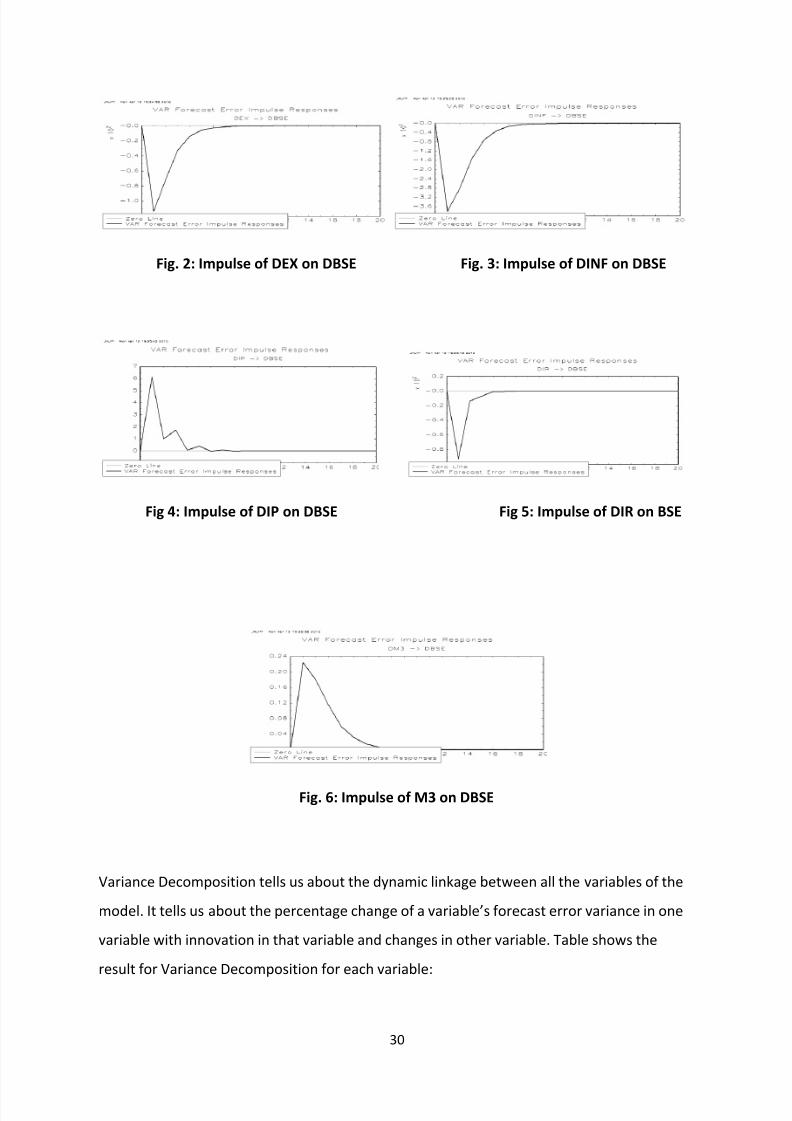

Fig. 2: Impulse of DEX on DBSE Fig. 3: Impulse of DINF on DBSE

Fig 4: Impulse of DIP on DBSE Fig 5: Impulse of DIR on BSE

Fig. 6: Impulse of M3 on DBSE

Variance Decomposition tells us about the dynamic linkage between all the variables of the

model. It tells us about the percentage change of a variable’s forecast error variance in one

variable with innovation in that variable and changes in other variable. Table shows the

result for Variance Decomposition for each variable:

8/6/2019 Long Term and Shrt Run relationship between Macroeconomic variables and stock market in India

http://slidepdf.com/reader/full/long-term-and-shrt-run-relationship-between-macroeconomic-variables-and-stock 31/48

31

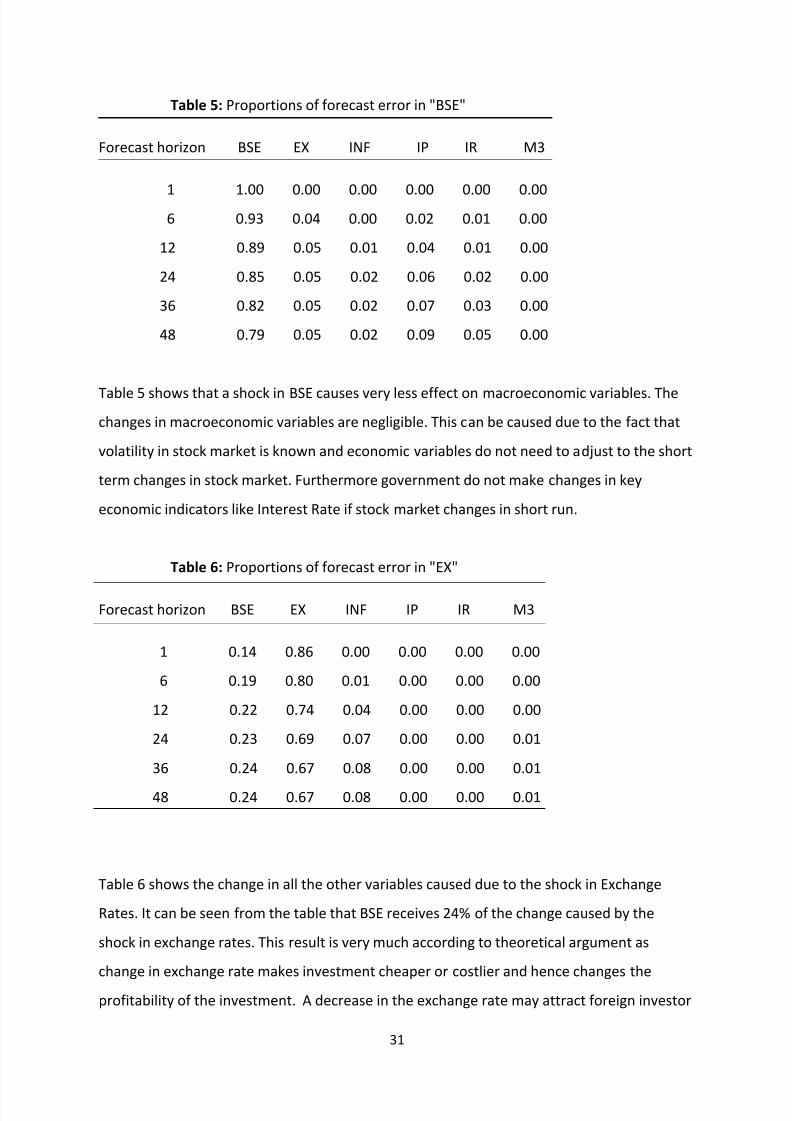

Table 5: Proportions of forecast error in "BSE"

Forecast horizon BSE EX INF IP IR M3

1 1.00 0.00 0.00 0.00 0.00 0.006 0.93 0.04 0.00 0.02 0.01 0.00

12 0.89 0.05 0.01 0.04 0.01 0.00

24 0.85 0.05 0.02 0.06 0.02 0.00

36 0.82 0.05 0.02 0.07 0.03 0.00

48 0.79 0.05 0.02 0.09 0.05 0.00

Table 5 shows that a shock in BSE causes very less effect on macroeconomic variables. The

changes in macroeconomic variables are negligible. This can be caused due to the fact that

volatility in stock market is known and economic variables do not need to adjust to the short

term changes in stock market. Furthermore government do not make changes in key

economic indicators like Interest Rate if stock market changes in short run.

Table 6: Proportions of forecast error in "EX"

Forecast horizon BSE EX INF IP IR M3

1 0.14 0.86 0.00 0.00 0.00 0.00

6 0.19 0.80 0.01 0.00 0.00 0.00

12 0.22 0.74 0.04 0.00 0.00 0.00

24 0.23 0.69 0.07 0.00 0.00 0.01

36 0.24 0.67 0.08 0.00 0.00 0.01

48 0.24 0.67 0.08 0.00 0.00 0.01

Table 6 shows the change in all the other variables caused due to the shock in Exchange

Rates. It can be seen from the table that BSE receives 24% of the change caused by the

shock in exchange rates. This result is very much according to theoretical argument as

change in exchange rate makes investment cheaper or costlier and hence changes the

profitability of the investment. A decrease in the exchange rate may attract foreign investor

8/6/2019 Long Term and Shrt Run relationship between Macroeconomic variables and stock market in India

http://slidepdf.com/reader/full/long-term-and-shrt-run-relationship-between-macroeconomic-variables-and-stock 32/48

32

and an increase in exchange rate may tempt foreign investor to book profits and convert it

into his home currency. This could also be due to the fact that in India is not an export

dominant country, so a positive shock should cause stock market to fall. This was shown by

impulse response function. Rest all the variables are negligibly affected by change in EX.

Table 7: Proportions of forecast error in "INF"

Forecast horizon BSE EX INF IP M3 IR

1 0.01 0.00 0.99 0.00 0.00 0.00

6 0.00 0.01 0.97 0.00 0.00 0.01

12 0.00 0.02 0.96 0.00 0.00 0.02

24 0.01 0.06 0.91 0.00 0.00 0.02

36 0.02 0.10 0.86 0.00 0.01 0.02

48 0.03 0.12 0.83 0.00 0.01 0.02

Shock in Inflation does not change any variables in time horizon of 48 months except EX

which is affected up to some extent but it takes almost 48 months for EX to change. The

reason could be that the stock markets in India are efficient and the stock prices already

have adjusted to the expected inflation.

Table 8: Proportions of forecast error in "IP"

Forecast horizon BSE EX INF IP M3 IR

1 0.00 0.01 0.00 0.98 0.00 0.00

6 0.10 0.02 0.01 0.85 0.02 0.01

12 0.16 0.04 0.01 0.75 0.02 0.01

24 0.15 0.09 0.02 0.67 0.05 0.02

36 0.13 0.12 0.02 0.63 0.08 0.01

48 0.12 0.13 0.02 0.59 0.13 0.01

8/6/2019 Long Term and Shrt Run relationship between Macroeconomic variables and stock market in India

http://slidepdf.com/reader/full/long-term-and-shrt-run-relationship-between-macroeconomic-variables-and-stock 33/48

33

Change in Industrial Production affects BSE, Exchange Rates and M3 almost equally.

Industrial Production is a measure of how a company is doing and a positive shock to

industrial production should affect the prices of the stock of that firm. Industrial Productionmay cause change in exchange rates depending upon country being export dominant or not.

If a country relies heavily on exports then any change in Industrial Production can change

Exchange rates a lot but in since India is not a export dominant country so there is little

effect of change in IP on EX. More IP means more spending and hence more M3, so it can be

said that a positive shock to IP would change M3 up to some extent. Change in IP effects

BSE in 12 months and then effect slowly starts to diminish. It takes longer to cause change in

EX and M3, around 48 months.

Table 9: Proportions of forecast error in "M3"

Forecast horizon BSE EX INF IP M3 IR

1 0.01 0.00 0.00 0.04 0.95 0.00

6 0.02 0.00 0.00 0.19 0.79 0.00

12 0.01 0.00 0.00 0.30 0.68 0.01

24 0.05 0.00 0.02 0.36 0.56 0.01

36 0.09 0.00 0.02 0.38 0.50 0.01

48 0.10 0.00 0.03 0.38 0.47 0.01

Change in M3 affects BSE only up to some extent. As it can be seen from the Table 9, a

shock to M3 causes BSE to change 10% in 48 months. This can be due to the fact that more

money in hands of people may cause them to invest in stock market more. But IP is mostly

affected by change in M3. This is because more money with people means more demand

and more demand would lead to more industrial production. It takes almost 12 months for

IP to increase due to shock in M3. This happens because industries need time to increase its

output to change in demand.

8/6/2019 Long Term and Shrt Run relationship between Macroeconomic variables and stock market in India

http://slidepdf.com/reader/full/long-term-and-shrt-run-relationship-between-macroeconomic-variables-and-stock 34/48

34

Table 10: Proportions of forecast error in "IR"

Forecast horizon BSE EX IP INF M3 IR

1 0.00 0.00 0.01 0.00 0.00 0.99

6 0.00 0.00 0.01 0.01 0.00 0.9812 0.00 0.00 0.00 0.01 0.01 0.97

24 0.00 0.00 0.00 0.01 0.01 0.97

36 0.00 0.00 0.00 0.01 0.01 0.97

48 0.00 0.00 0.00 0.01 0.01 0.97

Shock to Interest Rates does not affect the growth of stock prices at all. It has already been

shown in this study that Interest Rates are not in equilibrium with stock prices in long run.

So we can say that Interest has no effect on stock prices in any way, whether long run or

short run.

Variance Decomposition further proves what was shown by the impulse response. There

exist very weak relationship between macroeconomic variables and only factor which effect

stock prices to move substantially is Exchange Rate. Rest all the variables have little or no

effect on stock growth in short run.

Granger causality is used to check the cause and effect relationship among various variables

used in the study. First Differenced series was taken while performing Granger Causality test

because this would give the effect of change in one variable on the change in stock prices.

After the test for causal relationship it was found that only the change in Exchange rate

cause change in stock prices and rest none of the variable granger cause stock prices. It was

also found that change in stock prices granger cause change in Industrial production. But for

the rest of the variables namely Interest Rate, M3 and Inflation, there do not exist any

causal relationship between them. This result is further proof of the results of impulse

response and forecast error variance decomposition. Hence we can say that according to

the Granger Causality test, there is no short run equilibrium between macroeconomic

variables and stock prices, only exception being Exchange Rate again. According to this

study results for Granger causality are as follows:

Table 11: Results for Granger Causality Test

DBSE DEX DBSE DIP DBSE DIR DBSE DM3 DBSE DINF

8/6/2019 Long Term and Shrt Run relationship between Macroeconomic variables and stock market in India

http://slidepdf.com/reader/full/long-term-and-shrt-run-relationship-between-macroeconomic-variables-and-stock 35/48

35

6.0 ConclusionThis dissertation is aimed to find the long run equilibrium and the short run dynamic

relationship between Indian stock prices and its macroeconomic variables. This study shows

that there is no long run equilibrium between macroeconomic variables and stock prices.

This means that in long run stock prices do not adjust for the change in macroeconomic

variables. This behaviour is very rare, not seen in many economies. Possible reason for such

behaviour can be the fact that Indian economy has been very volatile in past 20 years. None

of the variables have been stable in past. Another reason could be that data used in this

study is only 20 year old. A longer time frame could have shown much clearer picture of the

long run equilibrium between macroeconomic variables and stock prices but due to the

constraints of availability of data, only past 20 years were taken into consideration in this

study. Results of short run dynamic relationship between macroeconomic variables and

stock prices too show that macroeconomic variables affect Indian stock prices up to very

small extent. The only exception is Exchange Rate which can be said to have a short run

relationship with stock prices. Rest all the variables effect stock prices but very little.

Impulse response proves that EX, INF and IR cause BSE to change negatively and M3 and IP

change stock prices in same direction as the impulse. These results are further consolidated

by the outcomes from Forecast Error Variance Decomposition and Granger Causality. These

results show that Indian stock prices do not depend on macroeconomic variables. It can be

said that Indian stock market depends more on international events and other stock

markets than the domestic factors like macroeconomic situations. In recent years Indian

stock markets have become more integrated with stock markets of big economies like US

and UK. Due to this integration the markets are more affected by the broader events of

world economies than the domestic economy. Another reason for such results may be the

fact that Indian economy is driven mostly by domestic consumption and in the past 20 years

there has been a steep rise in Indian middle class which has caused domestic consumption

to increase multiple times. This phenomenon might have over shadowed the other

macroeconomic events. This also shows that it may be very difficult for government tocontrol stock prices from going down or up using macroeconomic variables and hence

8/6/2019 Long Term and Shrt Run relationship between Macroeconomic variables and stock market in India

http://slidepdf.com/reader/full/long-term-and-shrt-run-relationship-between-macroeconomic-variables-and-stock 36/48

36

government would be left with options such as applying cap on amount of foreign indirect

investments into the country. In past, Indian government have in fact capped many sectors

from foreign direct investments and foreign indirect investments.

Further study in this field may to look into the specific sectors of Indian economy and see if stock prices, of these sectors, are affected by the change in macroeconomic variables.

Another direction of study may be to include other factors which can affect stock prices like

US stock exchange prices, crude oil price, etc.

8/6/2019 Long Term and Shrt Run relationship between Macroeconomic variables and stock market in India

http://slidepdf.com/reader/full/long-term-and-shrt-run-relationship-between-macroeconomic-variables-and-stock 37/48

37

7.0 References:

Abdalla, I. S. A. and Murinde, V. (1997) Exchange rate and stock price interactions in

emerging financial markets: evidence on India, Korea, Pakistan and the Philippines,

Applied Financial Economics, 7, 25 –35.

Abdullah, D.A. and S.C. Hayworth, Macroeconomics of stock price fluctuations. Quarterly

Journal of Business & Economics, 1993. 32(1): p. 50.

Bekaert, G., et al., Distributional characteristics of emerging market returns and asset

allocation. Journal of Portfolio Management, 1998. 24(2): p. 102-+.

Chen, N. F., Roll, R. and Ross, S. (1986) Economic forces and the stock market , Journal of

Business, 59, 383 –403.

Choudhary, T. (2001) Inflation and rates of return on stocks: evidence from high inflation

countries, Journal of International Financial Markets, Institutions and Money, 11, 75 –96.

Engle, R. and Granger, C. W. S. (1987) Cointegration and error correction: representation

estimation and testing, Econometrica, 55, 251 –76.

Fama, E. (1981) Stock return, real activity, inflation and money , American Economic

Review, 65, 269 –82.

Fama, E., The behaviour of stock market prices, Journal of Business, 1965, 38, p. 34 –105.

Granger, C. W. and Morgerstern, O., Spectral Analysis of New York stock market prices,

Kyklos, 1963, 16, p.1 –27.

8/6/2019 Long Term and Shrt Run relationship between Macroeconomic variables and stock market in India

http://slidepdf.com/reader/full/long-term-and-shrt-run-relationship-between-macroeconomic-variables-and-stock 38/48

38

Granger, C. W., Huang, B. N. and Yang, C. W. (2000) A bivariate causality between stock

prices and exchange rates: evidence from recent Asian flu, The Quarterly Review of

Economics and Finance, 40, 337 –54.

Granger, C. W., Some recent developments in the concept of causality , Journal of

Econometrics, 1986, 39, p. 194 –211.

Ibrahim, M.H., MACROECONOMIC FORCES AND CAPITAL MARKET INTEGRATION. Journal

of the Asia Pacific Economy, 2003. 8(1): p. 19.

Kwon, C.S. and T.S. Shin, Cointegration and causality between macroeconomic variables

and stock market returns. Global Finance Journal, 1999. 10(1): p. 71.

Malkiel, B (1979), the capital formation problem in the, United States, Journal of Finance,

34, p. 291 –306.

Muradoglu, G., F. Taskin, and I. Bigan, Causality Between Stock Returns and

Macroeconomic Variables in Emerging Markets. Russian & East European Finance &

Trade, 2000. 36(6): p. 33.

Patra, T. and S. Poshakwale, Economic variables and stock market returns: evidence from

the Athens stock exchange. Applied Financial Economics, 2006. 16(13): p. 993-1005.

Ratanapakorn, O. and S.C. Sharma, Dynamic analysis between the US stock returns and

the macroeconomic variables. Applied Financial Economics, 2007. 17(5): p. 369-377.

Smith, K. and Sims, A. (1993) Stock market performance and macroeconomic variables,

Applied Financial Economics, 3, 55 –60.

8/6/2019 Long Term and Shrt Run relationship between Macroeconomic variables and stock market in India

http://slidepdf.com/reader/full/long-term-and-shrt-run-relationship-between-macroeconomic-variables-and-stock 39/48

39

8.0 Appendix:

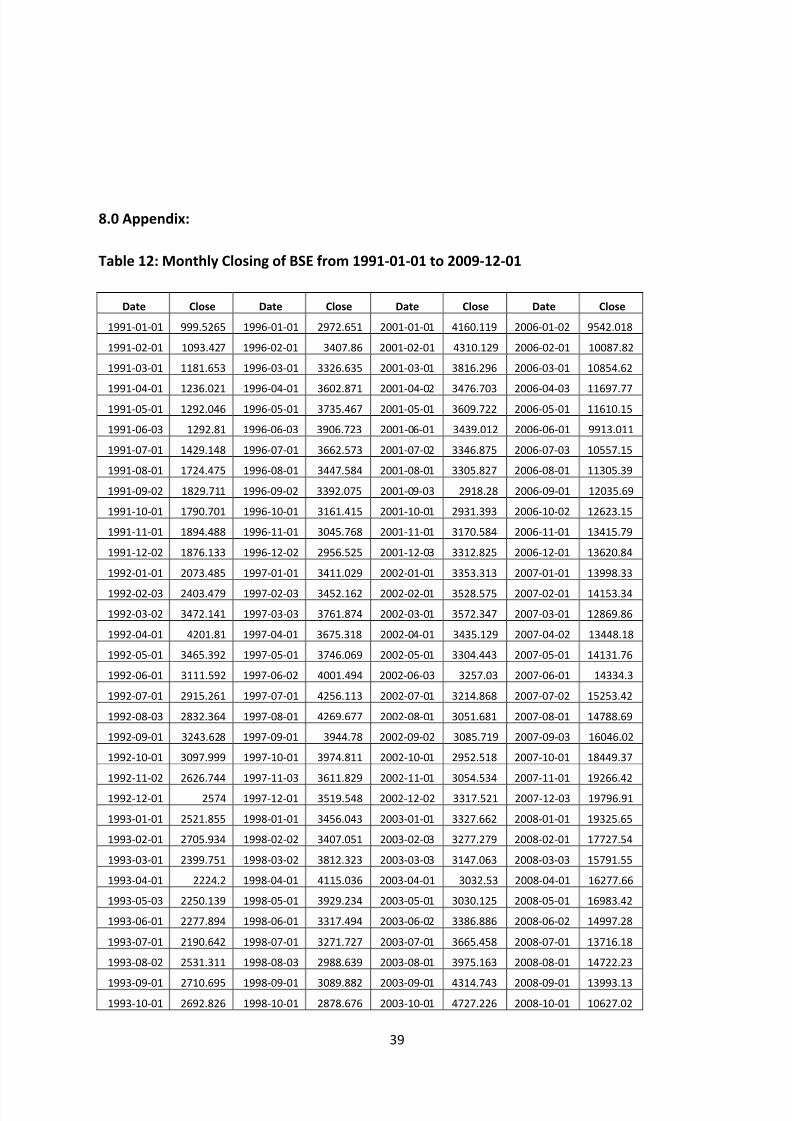

Table 12: Monthly Closing of BSE from 1991-01-01 to 2009-12-01

Date Close Date Close Date Close Date Close

1991-01-01 999.5265 1996-01-01 2972.651 2001-01-01 4160.119 2006-01-02 9542.018

1991-02-01 1093.427 1996-02-01 3407.86 2001-02-01 4310.129 2006-02-01 10087.82

1991-03-01 1181.653 1996-03-01 3326.635 2001-03-01 3816.296 2006-03-01 10854.62

1991-04-01 1236.021 1996-04-01 3602.871 2001-04-02 3476.703 2006-04-03 11697.771991-05-01 1292.046 1996-05-01 3735.467 2001-05-01 3609.722 2006-05-01 11610.15

1991-06-03 1292.81 1996-06-03 3906.723 2001-06-01 3439.012 2006-06-01 9913.011

1991-07-01 1429.148 1996-07-01 3662.573 2001-07-02 3346.875 2006-07-03 10557.15

1991-08-01 1724.475 1996-08-01 3447.584 2001-08-01 3305.827 2006-08-01 11305.39

1991-09-02 1829.711 1996-09-02 3392.075 2001-09-03 2918.28 2006-09-01 12035.69

1991-10-01 1790.701 1996-10-01 3161.415 2001-10-01 2931.393 2006-10-02 12623.15

1991-11-01 1894.488 1996-11-01 3045.768 2001-11-01 3170.584 2006-11-01 13415.79

1991-12-02 1876.133 1996-12-02 2956.525 2001-12-03 3312.825 2006-12-01 13620.84