Embed Size (px)

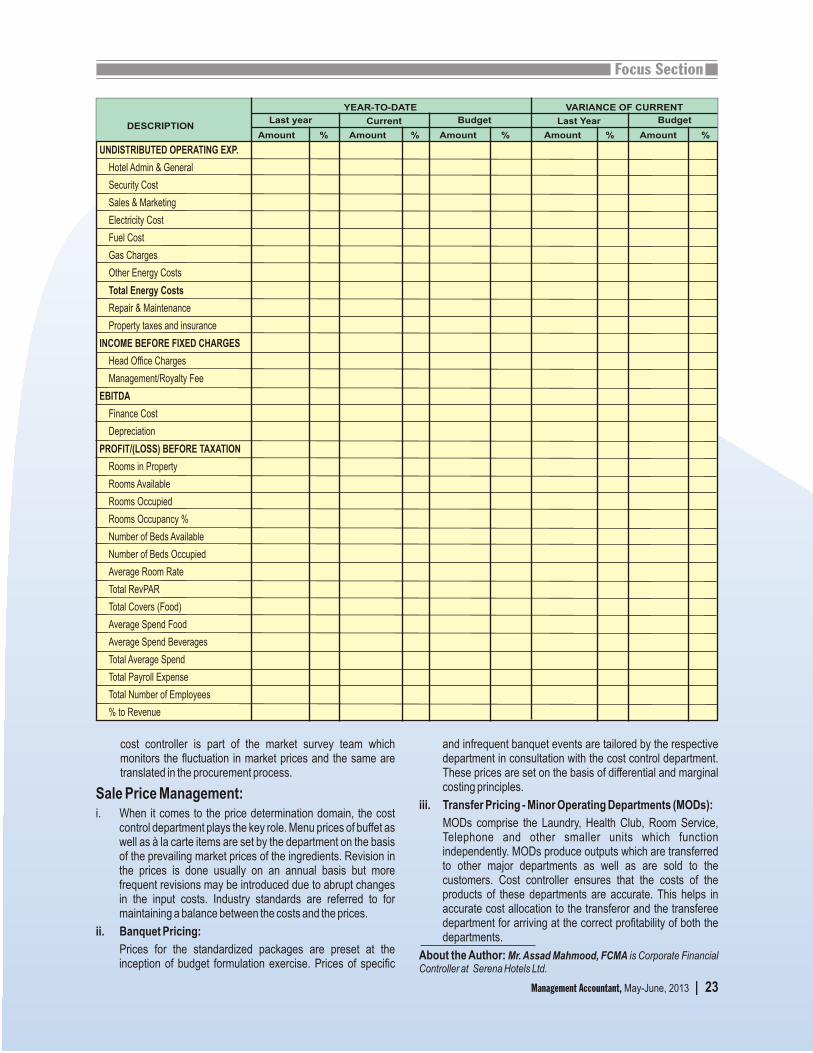

DESCRIPTION

cost audit

Citation preview

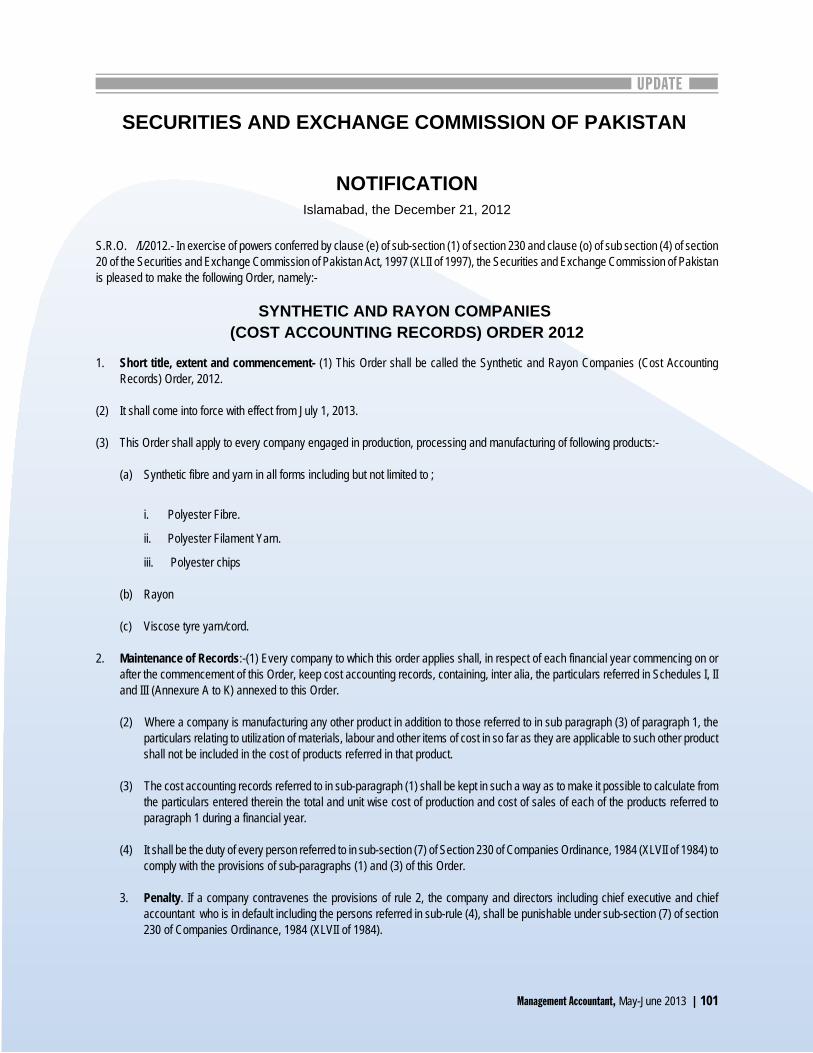

THE GAZETTE OF PAKISTAN

EXTRAORDINARYPUBLISHED BY COMMISSION

ISLAMABAD 2013

Part II

Statutory Notifications (S.R.O.)

SECURITIES AND EXCHANGE COMMISSION OF PAKISTAN

NOTIFICATION

Islamabad, the April 23, 2013

S.R.O. 343 /2013.— The following draft of Pharmaceuticals Industry (Cost Accounting Records) Order, 2013 which is proposed to be made in exercise of powers conferred by clause (e) of sub-section (1) of section 230 and clause (o) of sub section (4) of section 20 of theSecurities and Exchange Commission of Pakistan Act, 1997 (XLII of 1997) is hereby published for the information of all persons 1ike1y tobe affected thereby and notice is hereby given that the draft will be taken into consideration after thirty days of its publication in the OfficialGazette.

Any objection or suggestion which may be received from any person in respect of the said draft before the expiry of the said date shall beconsidered by the Securities and Exchange Commission of Pakistan.

PHARMACEUTICALS INDUSTRY (COST ACCOUNTING RECORDS) ORDER, 20131. Short title, application and commencement. - (1) This Order shall be called the Pharmaceutical Industry (Cost Accounting

Records) Order, 2013.

(2) This Order shall apply to every company, including a foreign company as defined under section 450 of the CompaniesOrdinance, 1984, which is engaged in the production, processing and manufacturing of pharmaceuticals products.

(3) It shall come into force with effect from July 1st 2013.

2. Maintenance of records.- (1) Every company to which this Order applies shall, in respect of each financial year commencing on orafter the commencement of this Order, keep cost accounting records, containing, inter-alia, the particulars specified in Schedule I, IIand III to this Order.

(2) The cost accounting records referred to in sub-paragraph (1) shall be kept in such a way as to make it possible to calculate fromthe particualrs entered thererin the cost of production and cost of sales of each of the formulation products referred to in sub-para (2) of para 1, during a financial year.

(3) Where a company is manufacturing any other product in addition to those referred to in sub- para (2) of para 1, the particularsrelating to the utilization of materials, labour and other items of cost in so far as they are applicable to such other product shall notbe included in the cost of product referred to in that para.

(4) It shall be the duty of every person referred to in sub-section (7) of section 230 of the Companies Ordinance, 1984 (XL VII of1984), to comply with the provisions of sub-paragraph (1) to (3) in the same manner as they are liable to maintain financialaccounts required under section 230 of the said Ordinance.

3. Penalty If a company contravenes the provisions of paragraph 3 the company and every officer thereof who is in default, including thepersons referred to in sub-paragraphs (4) of paragraph 2 shall be punishable under sub-section (7) of section 230 of the companiesOrdinance, 1984 (XL VII of 1984)

Man age ment Ac count ant, May- June 2013 | 65

UPDATE

SCHEDULE 1(See paragraph 2)

1. MATERIALS

(1) Direct Materials.-

(a) Adequate records shall be maintained showing receipts, issues and balances, both in quantities and values of each item of direct materials such as basic for manufacture, semi-basic manufacture, excipients, and pharmaceutical aids etc, required formanufacture of different types of formulations batch-wise. The basis on which the value of receipts, and issues have beencalculated shall be clearly indicated in the cost records maintained or if so desired by the company in a separate manual ofprocedures, if any, maintained by the company or in footnotes or separate explanatory notes to the cost statements for therelevant period. Such basis shall be applied consistently throughout the relevant period. The values shall include all directcharges upto works such as excise duty, sales tax, transport, freight, handling and transit insurance premium incurred for localmaterials. In case of imported materials, custom duty, sales tax, port charges, inland freight charges, sea freight and insurancecharges, and any other levies and charges, and any other levies and charges payable at the time of import shall be shownseparately and included to work out the landed cost. Separate record shall be maintained for imports of basic drugs from theparent company or third party suppliers in foreign country alongwith transfer prices.

(b) In case basic manufactures and semi-basic manufactures used as direct materials in the manufacture of formulations, which are being produced or processed by the company itself proper cost records shall be maintained so as to arrive at the cost of eachsuch item.

(c) Consumption reflected in cost records should correspond to the date recorded in the manufacturing records under the samenomenclature as maintained under the Drugs Rules, 1976.

(d) All issues of production and packing materials shall be reconciled with figures shown in Annexes of Schedule III, or in any otherform as thereto as possible. Any losses/surpluses arising as a result of physical verification of inventories and adjustmentsthereof shall be clearly indicated in the cost records.

(e) Record of purchase/supply contracts entered into with local and foreign suppliers including principals shall be maintainedshowing the rates at which various quantities of materials are to be acquired. The records shall indicate principal features ofeach contract particularly conditions relating to quantity, quality, price, and period of delivery, discount for transit loss and termsof payment including cash discounts. In case of basic drugs and chemicals, the chemical specifications, strength and technicalcontents should also be clearly indicated.

(f) Where some of the direct materials apart from basic manufactures and semi-basic manufactures are being produced orprocessed by the Company, separate records showing the cost of producing/processing such direct materials shall bemaintained in such detail as may enable the company to provide particulars required in the annexes of Schedule III.

(g) Any abnormal wastage of material whether in transit, storage or for any other reason shall be recorded separately indicating thestage at which such losses occurred and reasons thereof. The method of dealing with such losses in the calculation of costsshall also be indicated in the cost records. Normal wastage will be absorbed by the remaining material in itself. Realizable valueof any waste material recovered or sale proceeds of any process material shall be credited to the cost of such process to arrive at the net cost of formulation produced.

(h) If the quantity and value of materials consumed in a company are determined on any basis other than actuals for example atstandards, the method adopted shall be mentioned in cost records and followed consistently. The overall reconciliation of suchquantities and values of materials with the actuals shall be made at the end of the financial year explaining the reasons ofvariances. The treatment of such variances in determining the cost of items referred to in sub-para (2) of paragraph V shall beindicated in the cost records.

(h) The records shall be maintained in such details as may enable the company to readily provide data required in the variousAnnexes of Schedule III, in a verifiable state.

(2) Consumable Stores/Spares/Operating Supplies.-

(a) Record of each item of consumable stores/spares/operating supplies shall be maintained so as to show receipts, issues andbalances, both in quantities and values, required or actually used for the relevant cost centres. In case of consumable stores and small tools cost of which is insignificant, the company may if it so desires maintain such records for main group of such items.

(b) Cost of consumable stores shall include all direct charges incidental to procurement of each item up to the factory. The cost ofsuch stores/spares/operating supplies consumed shall be charged to relevant cost centre on the basis of actual consumption.

66 | Man age ment Ac count ant, May- June, 2013

UPDATE

The items issued for capital expenditure, such as additions to plant and machinery shall be shown under relevant heads and notin the cost statements of formulation.

(c) Wastage of consumable stores, whether in transit, storage or at any other point, shall be quantified and shown separately.Method of dealing with such losses in costing shall also be indicated in the cost records.

II. SALARIES AND WAGES(1) Adequate record shall be maintained to show the attendance of workers employed by the company whether on regular, temporary,

piece-rate basis or on contract basis, as the case may be, proper records shall also be maintained in respect of payment made forovertime work and production incentives whether in the shape of production bonus or incentives based on output given to the workers. Payment of any production bonus or incentive based on output given to the workers. Payment of any retirement benefits includingpension, provident fund, gratuity, old age benefits and any identifiable labour related expenses shall also be included in the labour cost of beneficiary cost centre/department. This will be done in a manner that labour cost is available for each cost centre and for eachformulation and batch so that all particulars required to fill in the Annexes of Schedule III are readily available and verifiable.

(2) Fair and reasonable allocation shall be made for wages paid to such direct labour as has been utilized in more than one department,between the various departments or cost centres and the basis of such allocation shall be consistently followed. Any wages paid foradditions to plant and machinery or other fixed assets shall be capitalized and excluded from the cost statements.

(3) Benefits paid to the employees other than covered in (a) above shall be worked out separately and shown in the cost statementdepartment-wise.

III. SERVICE DEPARTMENTSAdequate records shall be maintained showing expenses incurred for each Service Department, such as laboratory, testing house, animalhouse, transport, and quality control, these expenses have to be apportioned to other cost centres including service departments on anequitable basis. Where these service departments serve other products other than formulations suitable bases should be worked out sothat the share apportioned to formulations is worked out and applied consistently.

IV. UTILITIESAdequate record shall be maintained showing the quantity and cost of the following utilities and services both purchased/produced andutilized by different cost centres:

(i) Power(ii) Treated Water/Deionized water(iii) Refrigeration(iv) Compressed Air (if installed separately)(v) Effluent treatment(vi) Oxygen/Nitrogen Plants.(vii) Air Conditioning(viii) LPG(ix) Quality Control Department.(x) Others (to be specified).

The records shall be so maintained as to enable assessment of consumption or utilization of services by different departments, cost centres or manufacturing units. Allocation of cost shall be on the basis of actual consumption, or utilization, if possible, or on the basis of technicalestimates in the absence of actual measurement. In the case of fixed charges or fuel adjustment surcharges for electricity claimed by theutility company irrespective of the actual power consumed and if the amount payable as per actual consumption falls below the contractualminimum, the difference between the contractual minimum and the actual amount shall be treated as fixed period cost and transferred torelevant Annexes of Schedule III. Cost of service including power consumed in and chargeable to non-manufacturing departments, ifsignificant, shall be shown separately.

Note. - In case of self generation quantity of power generated and reasons for any under utilization of power generated capacity, shall bespecified and the relevant cost should be treated as fixed / period cost.

V. REPAIRS AND MAINTENANCEAdequate records showing expenditure incurred on workshop facilities for repairs and maintenance of plant and machinery in differentdepartments and cost centres shall be maintained on permanent basis. Details of costs incurred and the basis of allocation of repairs and

Man age ment Ac count ant, May- June 2013 | 67

UPDATE

maintenance expenditure to different departments or manufacturing units or cost centres shall be indicated. Cost of work of capital nature,of heavy repairs, and overhaul cost, benefit of which is likely to be spread over a period longer than the financial year, shall be shownseparately.

(i) If a separate maintenance team is working for a particular department the salaries, wages, cost of consumables, spares and toolsshould be charged as direct expense of that department.

(ii) If the maintenance services are utilized for other products such as basic manufactures and semi-manufactures also, the portionutilized for them should be segregated and charged thereto.

VI. MULTIPURPOSE VESSELS AND MACHINESWhen same vessels and machines are used for manufacturing of different formulations/drugs, formulations-wise and batch-wise costincurred may be charged accordingly. When composite machine hour rates are used for allocation of conversion costs, overheads andequipment usage, adequate records for machine hour’s utilization for different formulations and batches should be kept for properapportionment of cost. The variances between the actuals and the amount charged on the basis of predetermined standard rates shall beadjusted or arriving at the actual cost of production periodically and the year end.

VII. DEPRECIATION(1) Adequate records shall be maintained showing values and other particulars of fixed assets in respect of which depreciation is to be

provided. The records shall, inter-alia, indicate the cost of each item of asset, the date of its acquisition, amount of depreciationcharged for the relevant period, accumulated depreciation and the written down value of the assets.

(2) Basis on which depreciation is calculated and allocated to the various departments and or products/formulation shall be clearlyindicated in the records.

(3) Amount of depreciation chargeable to different departments, manufacturing units or cost centres, for the financial year shall bemeasured and disclosed in accordance with the in accordance with the company’s policy which shall be consistent with theAccounting and Financial Reporting Standards as applicable in Pakistan and shall relate to the plant and machinery and other fixedassets utilized in such departments or units or cost centres. The method once adopted shall be applied consistently.

VII. INSURANCE(1) Record shall be maintained showing insurance premium paid for the various risks covered for the assets and other interests of the

Company.

(2) Method of allocating insurance cost to the various cost centers shall be indicated in the cost records and followed consistently.

(3) Amount of depreciation chargeable to different, manufacturing units or cost centres, for the financial year shall be in accordance withthe provisions of the Fourth Schedule of the Companies Ordinance 1984, and shall relate to the plant and machinery and other fixedassets utilized in such departments or units or cost centres. The method once adopted shall be applied consistently.

IX. ROYALTY/TECHNOLOGY TRANSFER FEEAdequate record including technical agreements shall be maintained in respect of fee paid to the collaborators or technology suppliers onrecurring or non-recurring basis, party-wise. The basis of charging such amounts to the beneficiating formulations shall be indicated in thecost records.

X. OTHER OVERHEADSAdequate records showing the amounts comprising the manufacturing overhead expenses other than those already mentioned and detailsof apportionment thereof to the various departments or processes or cost centres, shall be maintained. The factory overheads shallinclude, among other items, indirect labour cost alongwith share of labour related cost such as fringe benefits, other labour and staff welfare expenses, and establishment expenses of manufacturing of items referred in paragraph 2. If products other than formulations are alsobeing produced in the factory, adequate bases should be developed to apportion the overhead cost equitably.

X. CONVERSION COSTAdequate record shall be maintained for bifurcating conversion cost for each formulation batch-wise into fixed and variable factors forcompiling the different Annexes of Schedule III.

68 | Man age ment Ac count ant, May- June, 2013

UPDATE

X. QUALITY CONTROL EXPENSESIn case certain formulations require continuous or periodic checks by the quality control department, as to the formula strength conformingto the standards laid down by the Government or industry, necessary records shall be maintained so that the expenses incurred on thequality control department are prorated to the formulations/batches concerned. Adequate records shall be maintained of rejectedformulation/batches. Expenses incurred on quality control built in within the cost of a certain department shall be charged as directdepartmental expense.

X. RESEARCH AND DEVELOPMENT EXPENSESResearch and development expenses incurred by the research and development department shall be broken down by the nature andactivity, e.g., development of new products, improvement of manufacturing processes, design and development of new plant facilities,market research for existing and new products shall be maintained separately. The benefit of some of these expenses might extend to more than one accounting cycle in which case these expenses shall be treated in accordance with the Accounting and Financial ReportingStandards as applicable in Pakistan. In other case the bases of pro-ration of the expenses to the formulations, batch-wise shall be indicated in the cost records.

X. INTER-DEPARTMENTAL TRANSFERSProper records shall be maintained showing the quantity and cost of formulation transferred to other departments/units of the company forfurther processing, mixing or self-consumption. Such transfers shall ordinarily be affected at cost and shall be disclosed in the cost records. If however, the transfer of formulation to other departments/units is made at a valuation other than cost, profit or loss arising out of suchtransfer shall be disclosed in the records.

X. WORK-IN-PROCESS AND FINISHED GOODS INVENTORIES.The method of valuation of work-in-process and the finished goods inventories shall be indicated in the cost records so as to reveal the costelements, which have been taken into account in such computation. The cost elements shall be related to the items referred to in therelevant annexes of Schedule III. The costing method adopted shall be consistently followed. Treatment of differences, if any, on physicalverification of stocks with book balances, shall also be indicated in the cost records.

X. PACKINGAdequate records shall be maintained showing all the receipts, issues and balances both in quantities and cost of various packing materials such as strips, ampoules, vials, bottles, cartons, boxes, labels, and literature for each item separately. Adequate records shall also bemaintained for wages and other expenses incurred in respect of different size of packs adopted for marketing of formulations separately.The details of various packing materials actually used and spoiled shall be maintained in respect of each formulation. Where anyformulation is repacked due to defective packing, details of such repacking for each pack shall be determined if repacking cost is significant. In case any packing materials are produced by the company, proper record showing the cost and manufacture of such items shall bemaintained. In case of export packing, separate records and additional packing cost shall be maintained.

X. EXPORT INCENTIVE/EXPENSESProper record of export incentive received from the Government and any additional expenses incurred will be accounted for suitably.

XVIII. COST STATEMENTSExport of formulations (if any) authorized shall be shown separately in cost statements for sale in the local market.

XIX. ADJUSTMENT OF COST VARIANCEWhen the company maintains cost records on any basis other than actuals, such as standard costing, the records shall indicate theprocedure followed by the company in working out the actual cost of product under such system. The method followed for adjusting the cost variances in determining the actual cost of the product shall be indicated clearly in the cost records. The cost variances shall be shownagainst the relevant heads in the respective annexes of Schedule III. The reasons for variances in respect of materials shall inter-alia arefurnished separately for major materials. Variance analysis shall be made at least monthly/quarterly during the financial year and also atthe year-end. The reasons for variances shall be given in the cost reports.

Man age ment Ac count ant, May- June 2013 | 69

UPDATE

XX. SELLING AND DISTRIBUTION EXPENSESAdministration and selling and distribution expenses shall be recorded separately and bases developed for their apportionment to differentformulations, and/or products.

XXI. STATISTICAL STATEMENTS AND OTHER RECORDSCompanies may develop and adopt appropriate standards for use as a basis to evaluate performance. Alternatively formats/proceduresadopted by the industry in general should be maintained.

XXII. RECONCILIATION OF COST AND FINANCIAL ACCOUNTS(1) The cost records shall be periodically reconciled with the financial accounts to ensure accuracy if integrated accounts are not

maintained. Variations, if any, shall be clearly indicated and explained.

(2) The reconciliation shall be done in such a manner that the profitability of the different products, as per cost statements, is correctlyjudged and reconciled with the overall profits of the company from all of its activities.

(c) Adequate cost records shall be maintained in a manner so that the cost statements can be compiled.

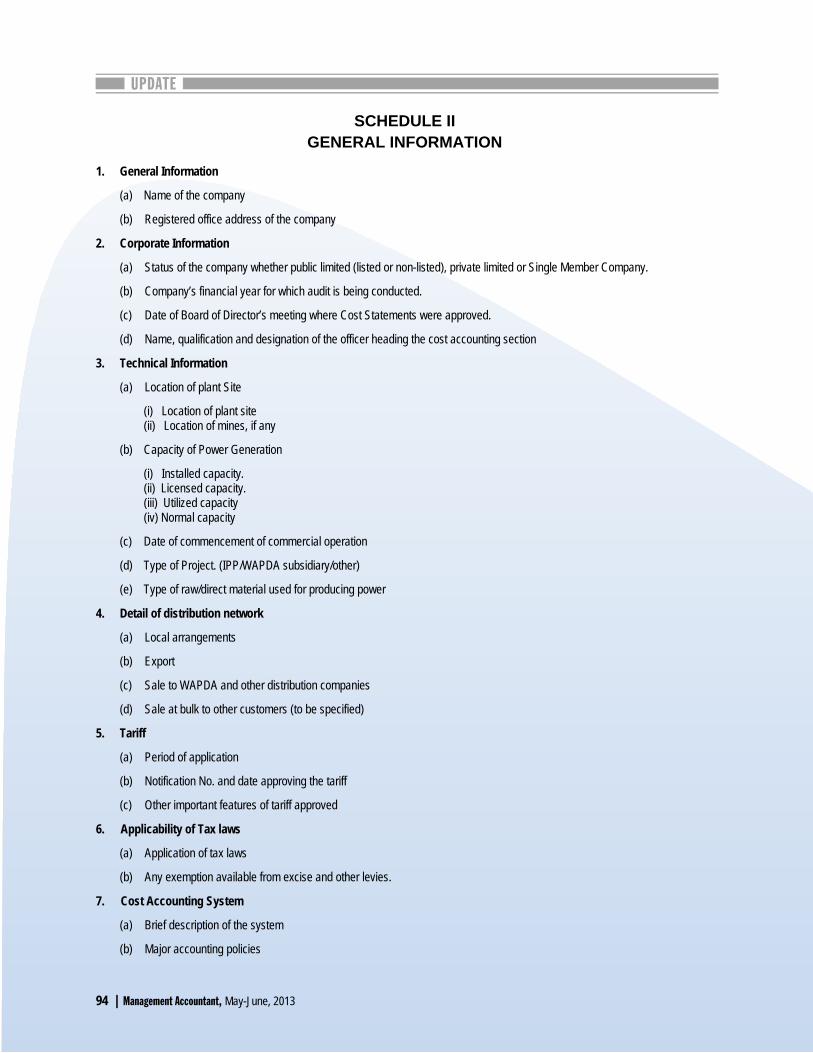

SCHEDULE IIGENERAL INFORMATION

1. Name of Company: _______________________________________________________________________________________

2. Address: ________________________________________________________________________________________________

3. Location of the Factory(s).(if more than one unit state the formulation/activities being manufactured/engaged in by each separately).

4. Date of Registration with the Central Licencing Board under the Drugs Act, 1976 (Act No. XXI of 1976) and Drugs (Licencing andAdvertising) Rules, 1976 {Rule No. 3(iii)}

5. Capacity of manufacturing: Current Year Previous Year Equipment:

(i) Tablets

(ii) Capsules

(iii) Syrups

(iv) Suspension

(v) Injections

(vi) Ointments

(vii) Creams

(viii) Powders

(ix) Others (Please specify)

6. Affiliation with foreign manufacturers, if any.

7. Please state if basic, semi-basic and Generic drugs which are also being manufactured.

8. Research and Development activity, if any.

70 | Man age ment Ac count ant, May- June, 2013

UPDATE

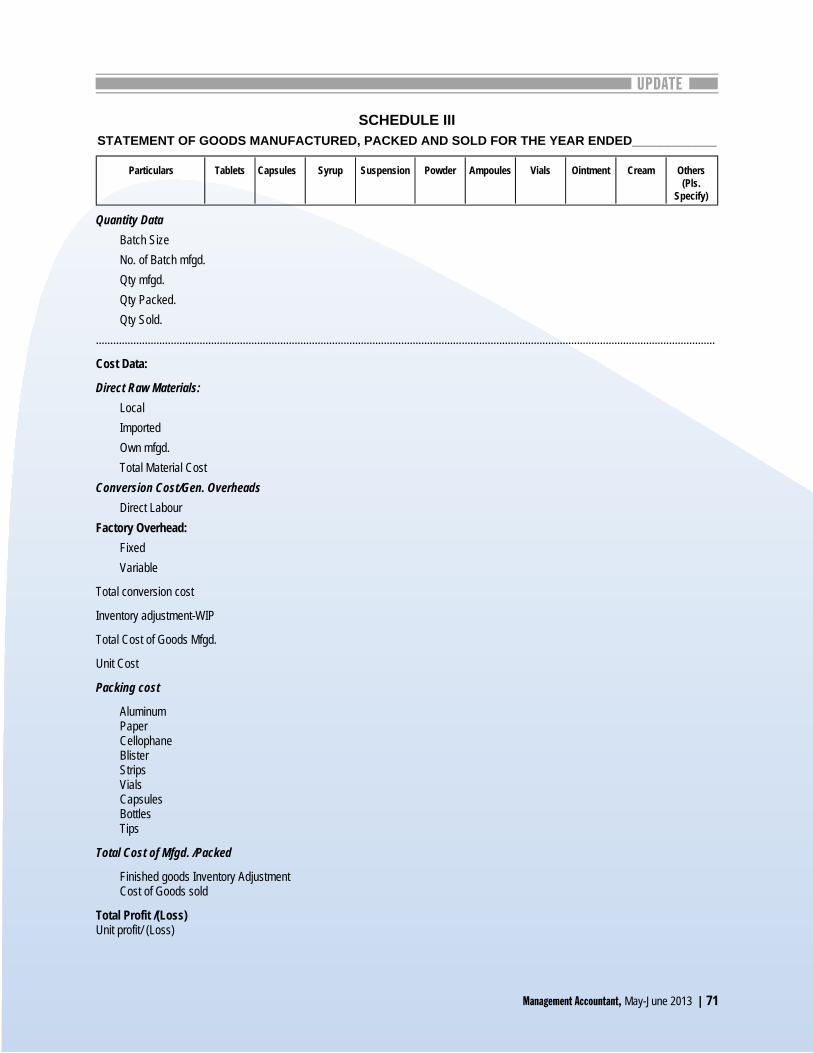

SCHEDULE IIISTATEMENT OF GOODS MANUFACTURED, PACKED AND SOLD FOR THE YEAR ENDED____________

Particulars Tablets Capsules Syrup Suspension Powder Ampoules Vials Ointment Cream Others(Pls.

Specify)

Quantity DataBatch SizeNo. of Batch mfgd.Qty mfgd.Qty Packed.Qty Sold.

.......................................................................................................................................................................................................................

Cost Data:

Direct Raw Materials:LocalImportedOwn mfgd.Total Material Cost

Conversion Cost/Gen. OverheadsDirect Labour

Factory Overhead:FixedVariable

Total conversion cost

Inventory adjustment-WIP

Total Cost of Goods Mfgd.

Unit Cost

Packing cost

AluminumPaperCellophaneBlisterStripsVialsCapsulesBottlesTips

Total Cost of Mfgd. /Packed

Finished goods Inventory AdjustmentCost of Goods sold

Total Profit /(Loss)Unit profit/ (Loss)

Man age ment Ac count ant, May- June 2013 | 71

UPDATE

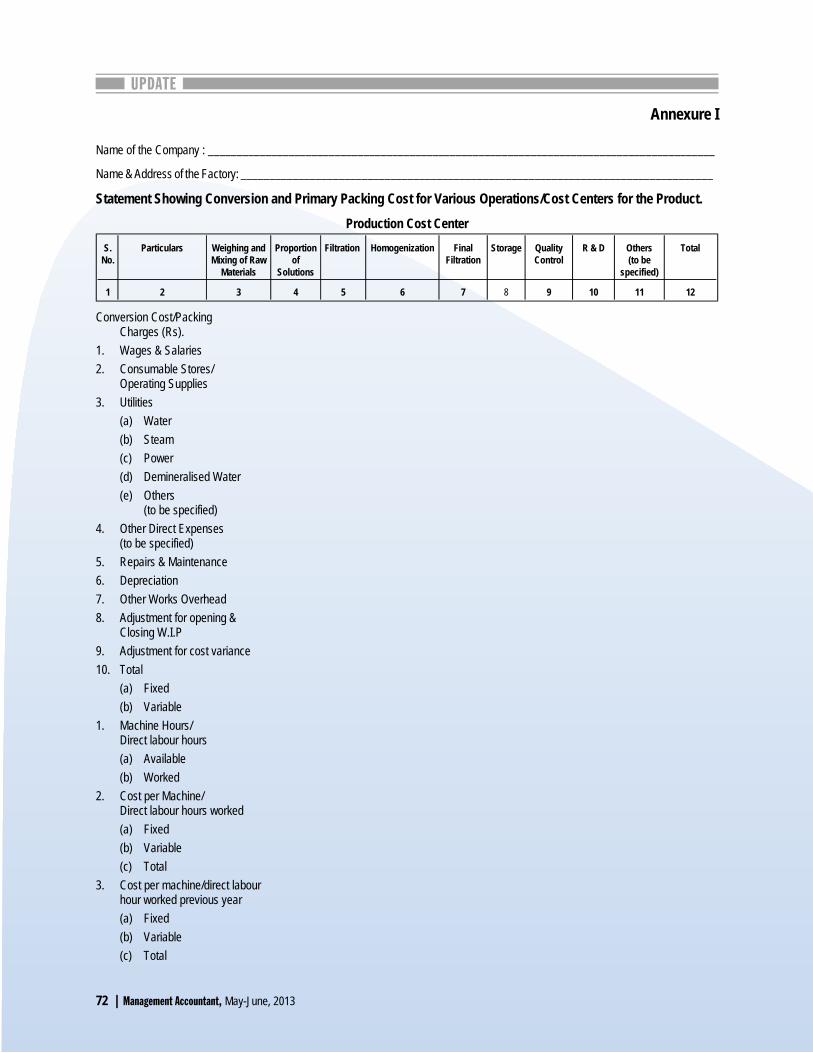

An nex ure I

Name of the Company : ________________________________________________________________________________________

Name & Address of the Factory: __________________________________________________________________________________

Statement Showing Conversion and Primary Packing Cost for Various Operations/Cost Centers for the Product.Production Cost Center

S.No.

Particulars Weighing andMixing of Raw

Materials

Proportionof

Solutions

Filtration Homogenization FinalFiltration

Storage QualityControl

R & D Others(to be

specified)

Total

1 2 3 4 5 6 7 8 9 10 11 12

Conversion Cost/PackingCharges (Rs).

1. Wages & Sala ries2. Consumable Stores/

Operating Supplies3. Utilities

(a) Water(b) Steam(c) Power(d) Demineralised Water(e) Others

(to be specified)4. Other Direct Expenses

(to be specified)5. Repairs & Maintenance6. Depreciation7. Other Works Overhead8. Adjustment for opening &

Closing W.I.P9. Adjustment for cost variance10. Total

(a) Fixed(b) Variable

1. Machine Hours/Direct labour hours(a) Available(b) Worked

2. Cost per Machine/Direct labour hours worked(a) Fixed(b) Variable(c) Total

3. Cost per machine/direct labourhour worked previous year(a) Fixed (b) Variable(c) Total

72 | Man age ment Ac count ant, May- June, 2013

UPDATE

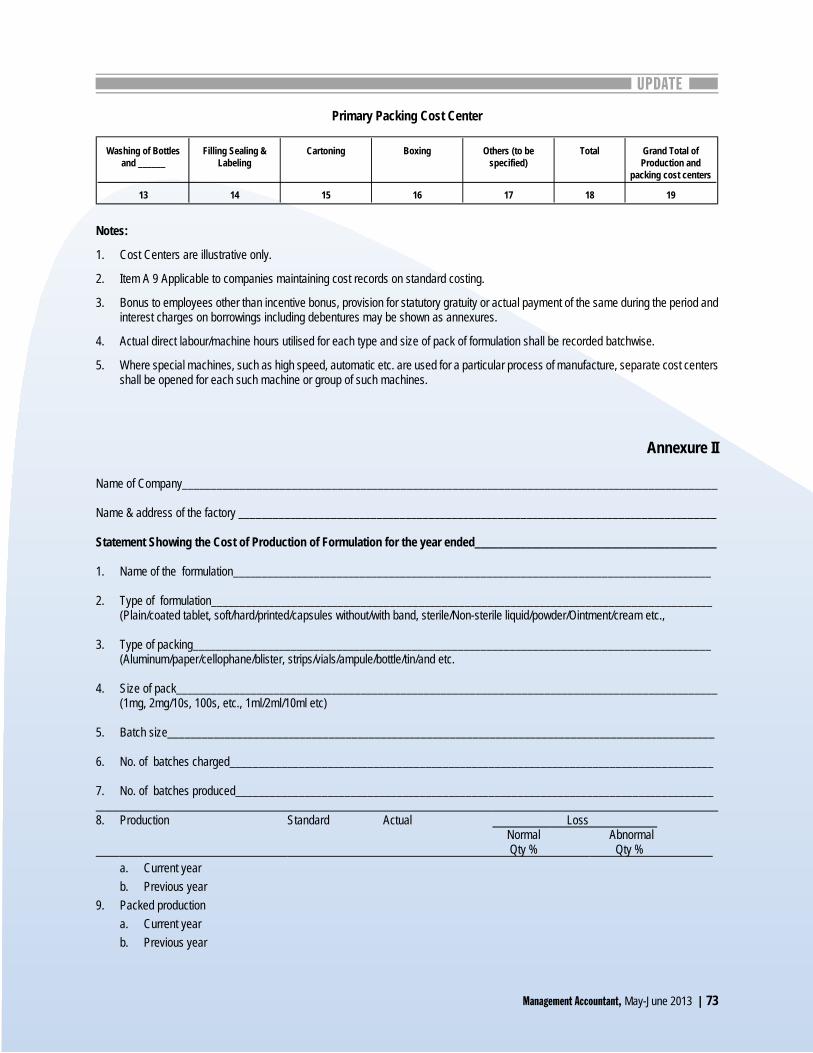

Primary Packing Cost Center

Washing of Bottlesand ______

Filling Sealing &Labeling

Cartoning Boxing Others (to bespecified)

Total Grand Total ofProduction and

packing cost centers

13 14 15 16 17 18 19

Notes:

1. Cost Centers are illustrative only.

2. Item A 9 Applicable to companies maintaining cost records on standard costing.

3. Bonus to employees other than incentive bonus, provision for statutory gratuity or actual payment of the same during the period andinterest charges on borrowings including debentures may be shown as annexures.

4. Actual direct labour/machine hours utilised for each type and size of pack of formulation shall be recorded batchwise.

5. Where special machines, such as high speed, automatic etc. are used for a particular process of manufacture, separate cost centersshall be opened for each such machine or group of such machines.

An nex ure II

Name of Company_____________________________________________________________________________________________

Name & address of the factory ___________________________________________________________________________________

Statement Showing the Cost of Production of Formulation for the year ended__________________________________________

1. Name of the formulation___________________________________________________________________________________

2. Type of formulation_______________________________________________________________________________________(Plain/coated tablet, soft/hard/printed/capsules without/with band, sterile/Non-sterile liquid/powder/Ointment/cream etc.,

3. Type of packing__________________________________________________________________________________________(Aluminum/paper/cellophane/blister, strips/vials/ampule/bottle/tin/and etc.

4. Size of pack______________________________________________________________________________________________(1mg, 2mg/10s, 100s, etc., 1ml/2ml/10ml etc)

5. Batch size_______________________________________________________________________________________________

6. No. of batches charged____________________________________________________________________________________

7. No. of batches produced___________________________________________________________________________________

8. Production Standard Actual Loss Normal Abnormal Qty % Qty %

a. Current yearb. Previous year

9. Packed productiona. Current yearb. Previous year

Man age ment Ac count ant, May- June 2013 | 73

UPDATE

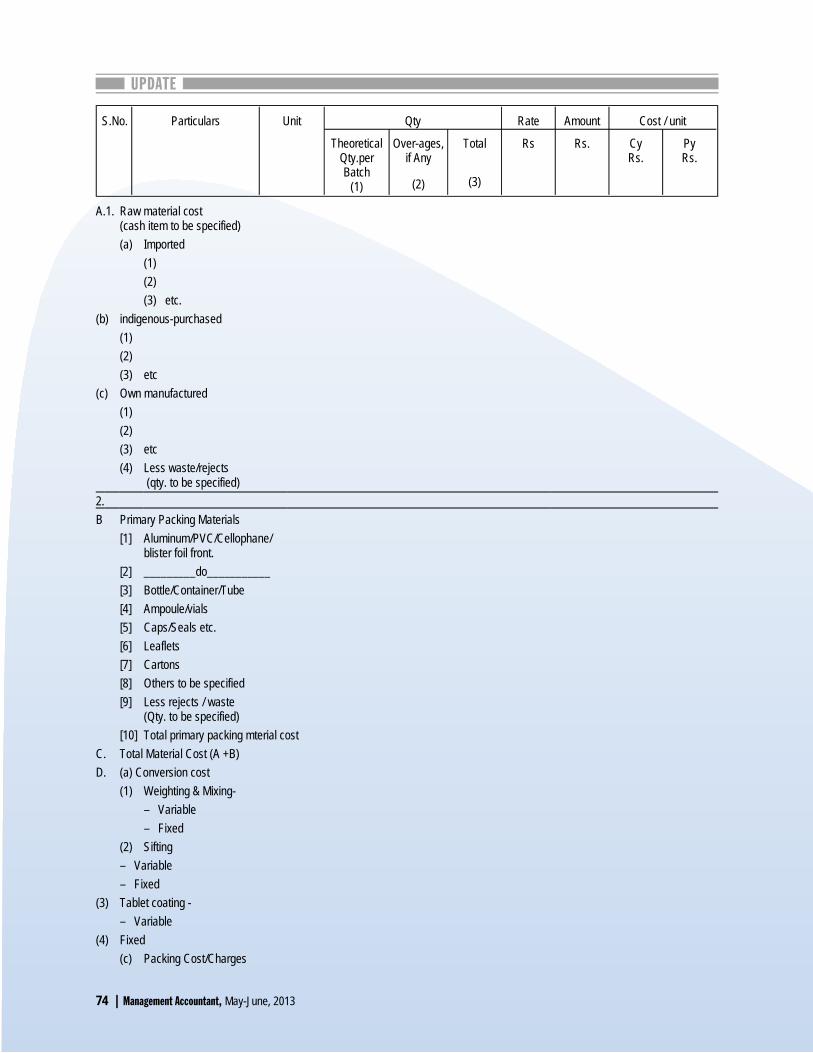

S.No. Particulars Unit Qty Rate Amount Cost / unit

TheoreticalQty.perBatch

(1)

Over-ages, if Any

(2)

Total

(3)

Rs Rs. CyRs.

PyRs.

A.1. Raw material cost(cash item to be specified)(a) Imported

(1)(2)(3) etc.

(b) indigenous-purchased(1) (2)(3) etc

(c) Own manufactured(1)(2)(3) etc(4) Less waste/rejects

(qty. to be specified)2.B Primary Packing Materials

[1] Aluminum/PVC/Cellophane/blister foil front.

[2] _________do___________[3] Bottle/Container/Tube[4] Ampoule/vials[5] Caps/Seals etc.[6] Leaflets[7] Cartons[8] Others to be specified[9] Less rejects / waste

(Qty. to be specified)[10] Total primary packing mterial cost

C. Total Material Cost (A +B)D. (a) Conversion cost

(1) Weighting & Mixing-– Variable– Fixed

(2) Sifting– Variable– Fixed

(3) Tablet coating -– Variable

(4) Fixed(c) Packing Cost/Charges

74 | Man age ment Ac count ant, May- June, 2013

UPDATE

(1) Strip Making -Variable Fixed

(2) Washing / sterilizing of bottles -VariableFixed

(3) Filling & sealing -VariableFixed

(4) Cartoning -(5) Others (to be specified)

Total Packing Cost(c) Other Expenses

(1) InspectionVariable Fixed

(2) Quality ControlVariable

(3) Testing -VariableFixed

(4) R & D -VariableFixed

4. Storage –VariableFixed

5. Others (to be specified)Total other expenses

G.1. Total cost [D(a) +D(c)] 2. Adjustment for opening & closing work in process 3. Adjustment for cost variances

(a) Raw material(b) Packing material(c) Conversion & packing charges(d) Total

4. Total Cost of Production.Notes: -1. This annexure shall be prepared for each type and size of packing (1 mg. 2mg./10s 1000s etc. 1ml./2ml./10ml.etc 5gm./ 10 gms etc. plain/

coated tablet soft / hard/ printed capsules, sterile/non sterile liquid/ powder, ointment/cream etc. in different packing of aluminum / paper /blister/strip vials/ampoule bottle/tin/jar etc. formulations separately.

2. The impact of foreign exchange gain/loss on the purchase of raw material from a foreign country or any other transaction may be disclosedseparately, if the impact of such gain or loss is 5% of total material cost;

3. The impact of subsidy/grant/incentive received shall be incorporated and disclosed separately. 4. Separate statement shall be prepared as above for export packing: -5. Item No.G.3 is applicable for companies following standard costing.6. The cost of raw material and packing material shall be based on actual consumption for each size and type of formulation.7. The abnormal loss, if nay, both in quantity and cost shall be own in a separate statement indicating the reason therefore.8. CY-Current year.

PY- Previous year.

Man age ment Ac count ant, May- June 2013 | 75

UPDATE

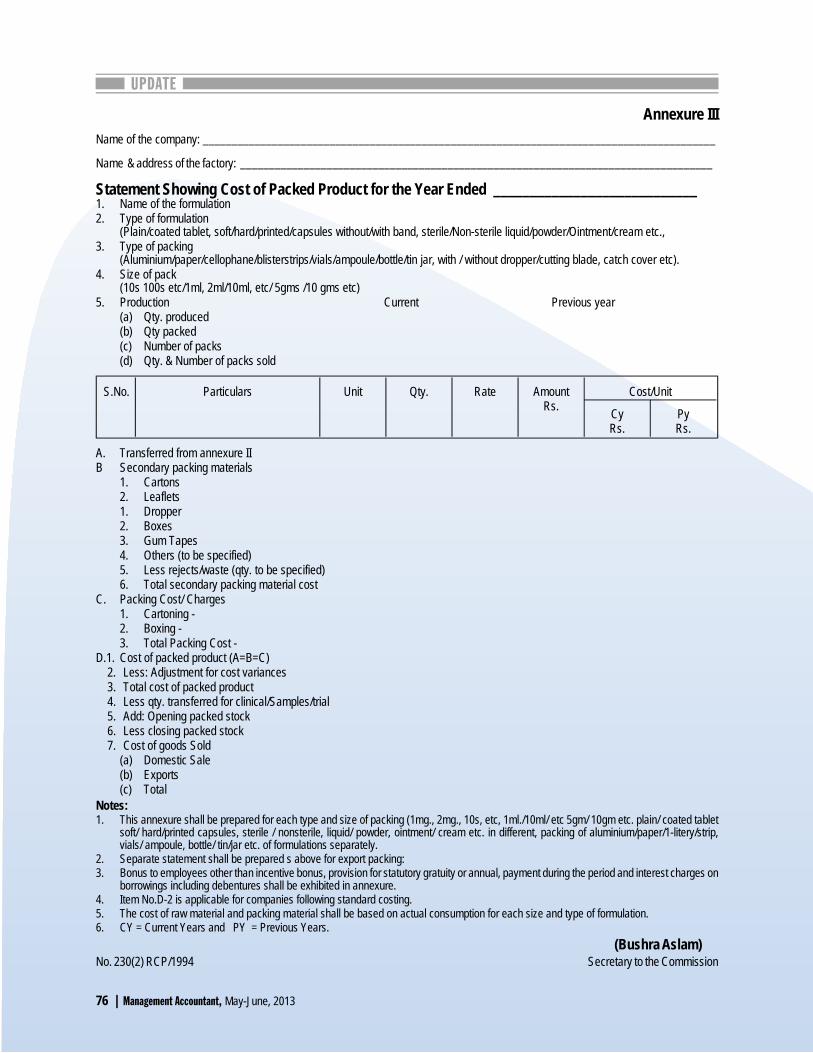

An nex ure IIIName of the company: _________________________________________________________________________________________

Name & address of the factory: __________________________________________________________________________________

Statement Showing Cost of Packed Product for the Year Ended ____________________________1. Name of the formulation2. Type of formulation

(Plain/coated tablet, soft/hard/printed/capsules without/with band, sterile/Non-sterile liquid/powder/Ointment/cream etc.,3. Type of packing

(Aluminium/paper/cellophane/blisterstrips/vials/ampoule/bottle/tin jar, with / without dropper/cutting blade, catch cover etc).4. Size of pack

(10s 100s etc/1ml, 2ml/10ml, etc/ 5gms /10 gms etc)5. Production Current Previous year

(a) Qty. produced(b) Qty packed(c) Number of packs(d) Qty. & Number of packs sold

S.No. Particulars Unit Qty. Rate AmountRs.

Cost/Unit

CyRs.

PyRs.

A. Transferred from annexure IIB Secondary packing materials

1. Cartons2. Leaflets1. Dropper2. Boxes3. Gum Tapes4. Others (to be specified)5. Less rejects/waste (qty. to be specified)6. Total secondary packing material cost

C. Packing Cost/ Charges1. Cartoning -2. Boxing -3. Total Packing Cost -

D.1. Cost of packed product (A=B=C) 2. Less: Adjustment for cost variances 3. Total cost of packed product 4. Less qty. transferred for clinical/Samples/trial 5. Add: Opening packed stock 6. Less closing packed stock 7. Cost of goods Sold

(a) Domestic Sale(b) Exports(c) Total

Notes:1. This annexure shall be prepared for each type and size of packing (1mg., 2mg., 10s, etc, 1ml./10ml/ etc 5gm/ 10gm etc. plain/ coated tablet

soft/ hard/printed capsules, sterile / nonsterile, liquid/ powder, ointment/ cream etc. in different, packing of aluminium/paper/1-litery/strip,vials/ ampoule, bottle/ tin/jar etc. of formulations separately.

2. Separate statement shall be prepared s above for export packing:3. Bonus to employees other than incentive bonus, provision for statutory gratuity or annual, payment during the period and interest charges on

borrowings including debentures shall be exhibited in annexure.4. Item No.D-2 is applicable for companies following standard costing.5. The cost of raw material and packing material shall be based on actual consumption for each size and type of formulation.6. CY = Current Years and PY = Previous Years.

(Bushra Aslam) No. 230(2) RCP/1994 Secretary to the Commission

76 | Man age ment Ac count ant, May- June, 2013

UPDATE

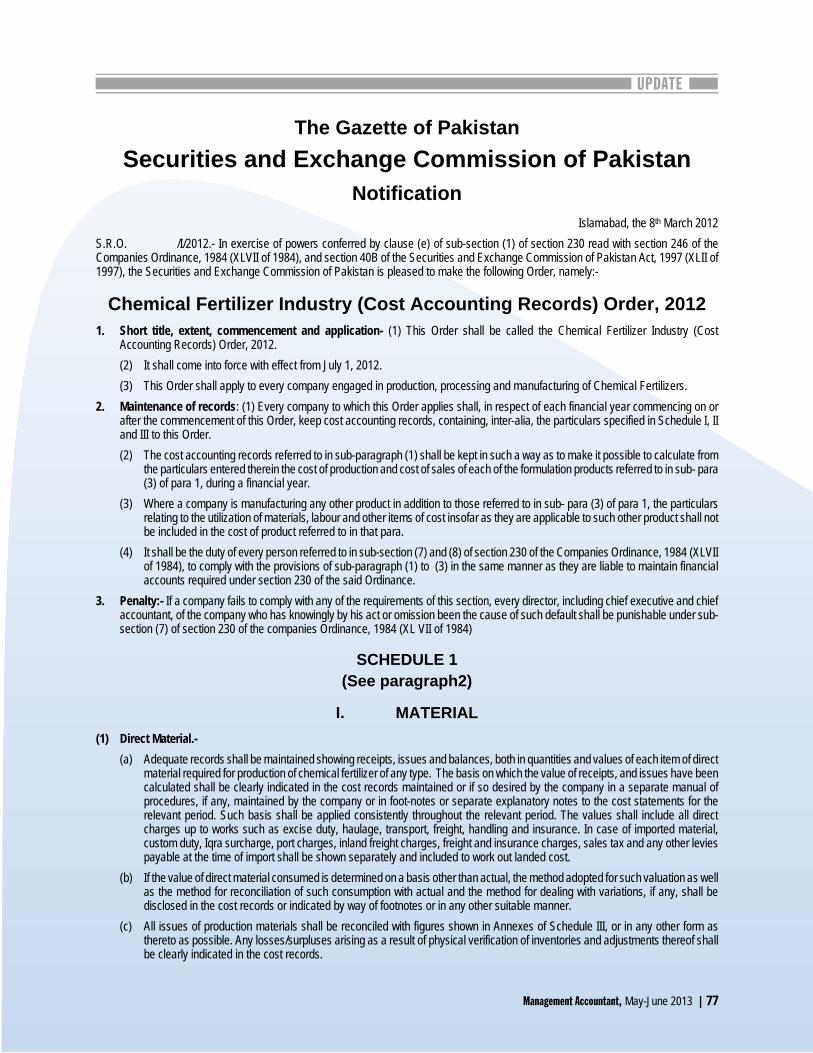

The Gazette of PakistanSecurities and Exchange Commission of Pakistan

NotificationIslamabad, the 8th March 2012

S.R.O. /I/2012.- In exercise of powers conferred by clause (e) of sub-section (1) of section 230 read with section 246 of theCompanies Ordinance, 1984 (XLVII of 1984), and section 40B of the Securities and Exchange Commission of Pakistan Act, 1997 (XLII of1997), the Securities and Exchange Commission of Pakistan is pleased to make the following Order, namely:-

Chemical Fertilizer Industry (Cost Accounting Records) Order, 20121. Short title, extent, commencement and application- (1) This Order shall be called the Chemical Fertilizer Industry (Cost

Accounting Records) Order, 2012.(2) It shall come into force with effect from July 1, 2012.(3) This Order shall apply to every company engaged in production, processing and manufacturing of Chemical Fertilizers.

2. Maintenance of records: (1) Every company to which this Order applies shall, in respect of each financial year commencing on orafter the commencement of this Order, keep cost accounting records, containing, inter-alia, the particulars specified in Schedule I, IIand III to this Order.(2) The cost accounting records referred to in sub-paragraph (1) shall be kept in such a way as to make it possible to calculate from

the particulars entered therein the cost of production and cost of sales of each of the formulation products referred to in sub- para(3) of para 1, during a financial year.

(3) Where a company is manufacturing any other product in addition to those referred to in sub- para (3) of para 1, the particularsrelating to the utilization of materials, labour and other items of cost insofar as they are applicable to such other product shall notbe included in the cost of product referred to in that para.

(4) It shall be the duty of every person referred to in sub-section (7) and (8) of section 230 of the Companies Ordinance, 1984 (XLVIIof 1984), to comply with the provisions of sub-paragraph (1) to (3) in the same manner as they are liable to maintain financialaccounts required under section 230 of the said Ordinance.

3. Penalty:- If a company fails to comply with any of the requirements of this section, every director, including chief executive and chiefaccountant, of the company who has knowingly by his act or omission been the cause of such default shall be punishable under sub-section (7) of section 230 of the companies Ordinance, 1984 (XL VII of 1984)

SCHEDULE 1(See paragraph2)

I. MATERIAL(1) Direct Material.-

(a) Adequate records shall be maintained showing receipts, issues and balances, both in quantities and values of each item of direct material required for production of chemical fertilizer of any type. The basis on which the value of receipts, and issues have beencalculated shall be clearly indicated in the cost records maintained or if so desired by the company in a separate manual ofprocedures, if any, maintained by the company or in foot-notes or separate explanatory notes to the cost statements for therelevant period. Such basis shall be applied consistently throughout the relevant period. The values shall include all directcharges up to works such as excise duty, haulage, transport, freight, handling and insurance. In case of imported material,custom duty, Iqra surcharge, port charges, inland freight charges, freight and insurance charges, sales tax and any other leviespayable at the time of import shall be shown separately and included to work out landed cost.

(b) If the value of direct material consumed is determined on a basis other than actual, the method adopted for such valuation as well as the method for reconciliation of such consumption with actual and the method for dealing with variations, if any, shall bedisclosed in the cost records or indicated by way of footnotes or in any other suitable manner.

(c) All issues of production materials shall be reconciled with figures shown in Annexes of Schedule III, or in any other form asthereto as possible. Any losses/surpluses arising as a result of physical verification of inventories and adjustments thereof shallbe clearly indicated in the cost records.

Man age ment Ac count ant, May- June 2013 | 77

UPDATE

(d) Record of purchase/supply contracts entered into with local and foreign suppliers as the case may be shall be maintainedshowing the rate at which various quantities of materials are to be acquired. The records shall indicate principal features of eachcontract particularly conditions relating to quantity, quality and, in case of catalysts showing their life, and in case of chemicalstheir strength and technical contents, price, period of delivery, discount for transit loss and terms of payment including cashdiscounts.

(e) Any abnormal wastage of material whether in transit, storage or for any other reason, shall be recorded separately indicating thestage at which such losses occur and reasons thereof. Method of dealing with such losses in the calculation of cost shall beindicated in the records. Normal wastages/losses due to shrinkage or evaporation etc. and gain due to elongation or absorptionof moisture etc. will be absorbed by the remaining material itself.

(f) Realizable value of any waste material, by-product or intermediary product recovered or sale proceeds of any process materialor intermediary product shall be credited to the cost of such process to arrive at the net cost of that particular process and finallythat of the fertilizer produced.

(g) The method adopted for the quantity and value of materials consumed in a company, if determined on a basis other than actual,shall be mentioned in cost records and it shall be followed consistently. The overall reconciliation of such quantities and values of materials with the actual shall be made at least quarterly during the financial year explaining the reasons for variances. Thetreatment of such variances in determining the cost of items referred to in paragraph 3 shall be indicated in the cost records.

(h) Where a material is acquired in exchange for other material or services supplied, the cost of material acquired is taken as thecost of material supplied or services provided plus other applicable cost such as freight.

(i) The forex component of imported material is converted at the rate on the date of the transaction. Any subsequent change in theexchange rate till payment or otherwise will not form part of the material cost.

(j) Self manufactured materials are valued at cost including Direct Material Cost, Direct Employee Cost, Factory overheads andshare of administrative overheads relating to production. Share of other administrative overheads, finance cost and marketingoverheads are excluded.

(k) The records shall be maintained in such detail as may enable the company to readily provide data as required in the various CostStatements prescribed in this Order in a verifiable state.

(2) Catalysts, Other Chemicals, Consumable Stores/Spares, etc:(a) Adequate record of each item of catalysts, chemicals, consumable stores/spares shall be maintained to show receipts, issues

and balances, both in quantities and values, required for production of chemical fertilizer and/or actually used for the relevantcost centers.

(b) Cost of catalysts, chemicals, consumable stores and spare parts shall include all direct charges incidental to procurement ofeach item up to the factory. The cost of such chemicals, stores/spares etc. consumed shall be charged to relevant cost centerson the basis of actual consumption as recorded in the Cost Statements. The items issued for capital expenditure, viz. asadditions to plant and machinery shall be shown under relevant heads and not in the cost statements of chemical fertilizer. Costof catalysts which are relatable to production over a period of time, is amortized over the production units benefited by such cost.Cost of material with life exceeding one year is included in the cost over useful life of the material.

(c) The basis of valuation of receipt and consumption of each item shall be indicated in the cost records and shall be consistentlyfollowed.

(d) Wastage of chemicals, consumable stores, spares whether in transit, storage or at any other point shall be quantified and shownseparately. Method of dealing with such losses in costing shall also be indicated in the cost records.

II. SALARIES AND WAGES(1) Adequate record shall be maintained to show the attendance of workers employed by the company whether on regular, temporary, or

on contract basis, as the case may be. Proper record shall also be maintained in respect of payment made for overtime work andproduction incentives whether in the shape of production bonus or incentives based on out-put given to the workers. Payment of anyretirement benefits including pension, provident fund, gratuity, old age benefits and any welfare expenses shall also be included in thelabour or factory overhead cost of beneficiary cost center/department. This will be done in a manner that labour cost is available foreach cost center or department and for each product whether intermediary, by-product or main product so that different CostStatements are filled properly and easily.

(2) Fair and reasonable allocation shall be made for wages paid to such direct labour as has been utilised in more than one department,between the various departments or cost centers and the basis of such allocation shall be consistently followed. Any wages paid foradditions to plant and machinery or other capitalised assets shall be capitalized and excluded from the cost statements of chemicalfertilizer.

78 | Man age ment Ac count ant, May- June, 2013

UPDATE

III. UTILITIES(1) Adequate records shall be maintained showing the quantity and cost of various utilities and services both purchased and produced as

detailed below and consumed and utilised by different cost centers:(a) Power(b) Steam(c) De-mineralised Water(d) Compressed Air (e) Others (to be specified)

(3) The records shall be maintained so as to enable assessment of consumption or utilization of services by different departments, costcenters or manufacturing units. Allocation of cost of utilization shall be on the basis of actual consumption, if possible, or on the basisof technical estimates in the absence of actual measurement. In the case of fixed charges or fuel adjustment surcharge for electricityclaimed by the utility company, irrespective of the actual power consumed and if the amount payable as per actual consumption fallsbelow the contractual minimum, the difference between the contractual minimum and the actual amount shall be treated as fixed orperiod cost and transferred to relevant Cost Statement. Cost of service including power and gas consumed in and chargeable to non-manufacturing departments, if significant, shall be shown separately.

Note: - In case of self generation quantity and reasons for underutilization shall be specified and the relevant cost should be treated asfixed/period cost. In case of natural gas separate records shall be maintained for use of gas as direct material and use of gas in utilityservices or for supply to housing colonies, if any. Moreover, Cost of utilities generated for sale to outside parties is arrived as Cost of selfgenerated utilities plus distribution cost plus share of administrative overheads plus marketing overheads.

IV. REPAIRS AND MAINTENANCEAdequate records showing expenditure incurred on workshop facilities for repairs and maintenance of plant and machinery in differentdepartments and cost centers shall be maintained on permanent basis. Details of cost determination and the basis of allocation of repairsand maintenance expenditure to different departments or manufacturing units or cost centers shall be indicated. Cost of work of capitalnature, of heavy repairs, and overhaul cost, benefit of which is likely to be spread over a period longer than one financial year, shall beshown separately. If a separate maintenance team is working for a particular department the salaries, wages, cost of consumables, sparesand tools should be charged as direct expense of that department. If the maintenance services are utilised for other products, the portionutilised for them shall be segregated and charged thereto.

V. DEPRECIATION(1) Adequate records shall be maintained showing values and other particulars of fixed assets in respect of which depreciation is to be

provided. The records shall inter-alia indicate the cost of each item of asset, details of revaluation of assets, if any, the date of itsacquisition, accumulated depreciation, the rate of depreciation and the depreciation charge, for the relevant period.

(2) Basis on which depreciation is calculated and allocated to the various departments and products shall be clearly indicated in therecords.

(3) Where small value items are written off fully at the time of purchase in financial accounts, the same may be generally adopted for costaccounts.

VI. INSURANCE(1) Record shall be maintained showing insurance premium paid for the various risks covered on the assets and other interests of the

company.(2) Method of allocating insurance cost to the various cost centers shall be indicated in the cost records and followed consistently.

VII. ROYALTY/TECHNOLOGY TRANSFER FEE Adequate record including technical agreements shall be maintained in respect of fee paid to the collaborators or technology suppliers onrecurring or non-recurring basis, party-wise. The basis of charging such amounts to the beneficiating formulations shall be indicated in thecost records.

VIII. OTHER OVERHEADSAdequate records showing the amounts comprising the manufacturing overhead expenses other than those already mentioned and detailsof apportionment thereof to the various departments or processes or cost centers, shall be maintained. The factory overheads shall include, among other items, indirect labour cost along with share of labour related cost such as fringe benefits, other labour and staff welfareexpenses, and establishment expenses of manufacturing of items referred to in paragraph 2. If products other than chemical fertilizersincluding salable by-products are also being produced in the factory, adequate bases should be developed to apportion the overhead costequitably.

Man age ment Ac count ant, May- June 2013 | 79

UPDATE

IX. QUALITY CONTROL EXPENSESIn case certain chemical fertilizers require periodic checks by the quality control department, as to the chemical strength conforming tostandards laid down by the Government or industry, necessary records shall be maintained so that the expenses incurred on the qualitycontrol department are collected and charged to the different products. Adequate records shall be maintained of rejected fertilizers,intermediary products and by-products. Expenses incurred on quality control built-in within a certain department shall be charged as directdepartmental expense.

X. JOINT PRODUCTSWhen more than one product arises from a process, the cost shall be allocated to the different products on some reasonable basis whichshall be consistently applied during the relevant period. The basis on which such joint costs are allocated to the different products arisingfrom a process shall be indicated in the cost records.

XI. TRANSFER TO THE NEXT PROCESSThe costs incurred in an intermediary process will be transferred proportionate to the quantity transferred to the next process.

XII. WORK-IN-PROCESS AND FINISHED GOODS INVENTORIESThe method of valuation of work-in-process and the finished goods inventories shall be indicated in the cost records so as to reveal the costelements which have been taken into account in such computation. The cost elements shall be related to the items referred to in therelevant Cost Statement. The costing method adopted shall be consistently followed. Treatment of differences, if any, on physicalverification of stocks with book balances, shall also be indicated in the cost records.

XIII. PACKINGAdequate records shall be maintained showing all the receipts, issues and balances both in quantities and cost of various packing materials such as strips, ampoules, vials, bottles, cartons, boxes, labels, and literature for each item separately. Adequate records shall also bemaintained for wages and other expenses incurred in respect of different size of packs adopted for marketing of formulations separately.The details of various packing materials actually used and spoiled shall be maintained in respect of each formulation. Where anyformulation is repacked due to defective packing, details of such repacking for each pack shall be determined if repacking cost is significant. In case any packing materials are produced by the company, proper record showing the cost and manufacture of such items shall bemaintained. In case of export packing, separate records and additional packing cost shall be maintained.

XIV. COST STATEMENTSDetailed and adequate cost statements shall be prepared for each type of fertilizer product, intermediary product and by-productseparately, as required vides Schedule III.

XV. ADJUSTMENT OF COST VARIANCE(1) When the company maintains cost records on any basis other than actual, such as standard costing, the records shall indicate the

procedure followed by the company in working out the actual cost of product under such system. The method followed for adjustingthe cost variances in determining the actual cost of the product shall be indicated clearly in the cost records. The cost variances shallbe shown against the relevant heads in the respective Cost Statement.

(2) The reasons for variances in respect of materials shall inter-alia be furnished separately for major materials. Variance analysis shallbe made quarterly during the financial year and also at the year-end. The reasons for variances shall be given in the cost records.

XVI. ADMINISTRATIVE EXPENSESAdministrative expenses may be split up on the basis of total factory cost of each salable product and/or cost of imported fertilizers if sold bythe company or any other basis adopted by the company. Such basis shall be clearly indicated in the cost records.

XVII. SELLING AND DISTRIBUTION EXPENSES(1) Selling and distribution expenses in respect of fertilizer shall be apportioned to different final products and salable by-products and

Intermediary-products on the basis of sales revenue or some other equitable basis which shall be indicated in the cost records andshall be followed consistently.

(2) If imported fertilizers are also sold by the Company, selling expenses shall be allocated on the basis of sales revenue or any otheracceptable basis that the company may adopt. However, the basis of allocation shall be consistently followed.

80 | Man age ment Ac count ant, May- June, 2013

UPDATE

XVIII. SELLING AND DISTRIBUTION EXPENSES(1) A common cost is the cost of operating a common facility, activity or service or that is shared by two or more cost objects.(2) The common cost is generally lower than the stand-alone individual cost to each cost object, had the facility not shared.(3) Common cost is therefore allocated to each cost object based on the individual costs of the cost object.

XIX. STATISTICAL STATEMENTS AND OTHER RECORDSCompanies may develop appropriate standards for use as a basis to evaluate performance. Alternately formats/procedures adopted by theindustry in general should be maintained.

XX. RECONCILIATION OF COST AND FINANCIAL ACCOUNTS(1) The cost records shall be periodically reconciled with the financial accounts to ensure accuracy if integrated accounts are not

maintained. Variations, if any, shall be clearly indicated and explained.(2) The reconciliation shall be done in such a manner that the profitability of the different products, as per cost statements, is correctly

judged and reconciled with the overall profits of the company from all of its activities.(3) Adequate cost records shall be maintained in a manner that the cost statements can be compiled.

SCHEDULE II

GENERAL INFORMATION1 Name of the Company.2 Date of Incorporation.3 Date of Board Meeting where Cost Statements were approved4 Name, qualification and designation of the officer heading the cost accounting section.5 Location of Registered Office.6 Location of Factory/Factories.7 Type/Types of Fertilizers being produced.8 Any salable by-products and mid-products.9 Any imported fertilizers being sold by the company.10 Intermediary products: Per Day Per Year M.Tonnes M.Tonnes

Designed CapacityInstalled CapacityCapacity UtilizedNo. of Days in the yearon which capacity is calculated

11 Main products:Designed CapacityInstalled CapacityCapacity UtilisedNo. of Days in the yearon which capacity is calculated

12 Foreign Technical Collaboration:Name of the Process/Inventor/Patent holder.

Man age ment Ac count ant, May- June 2013 | 81

UPDATE

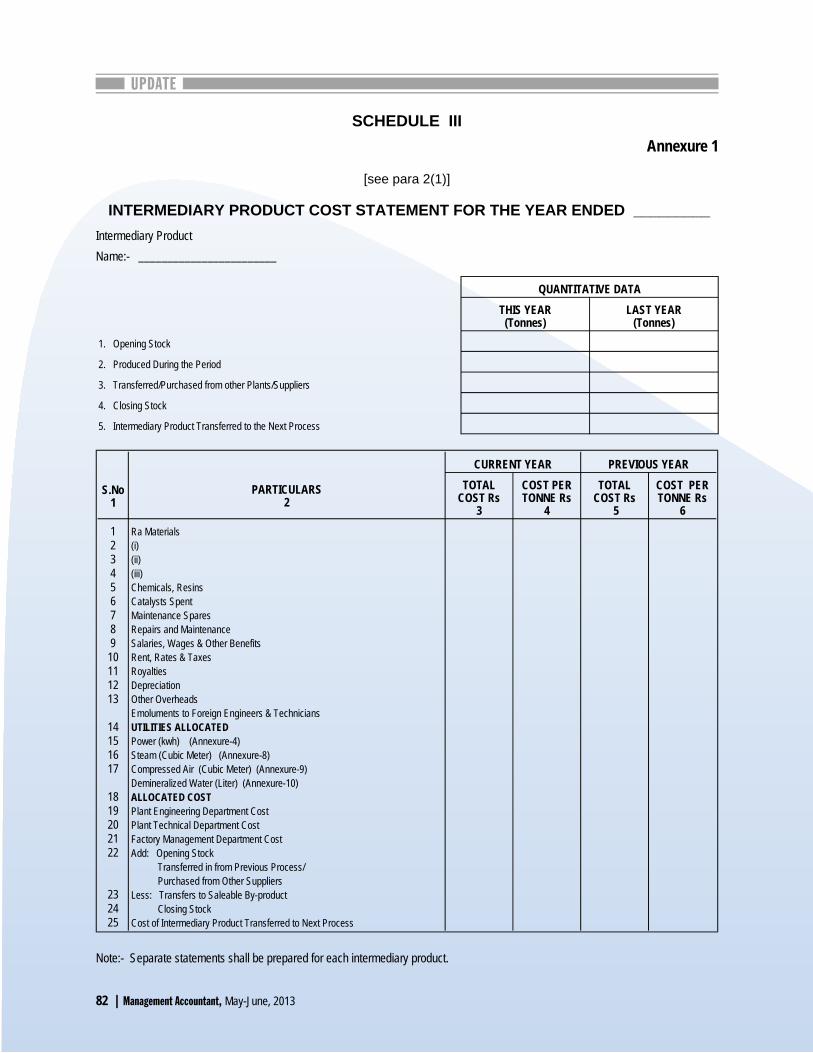

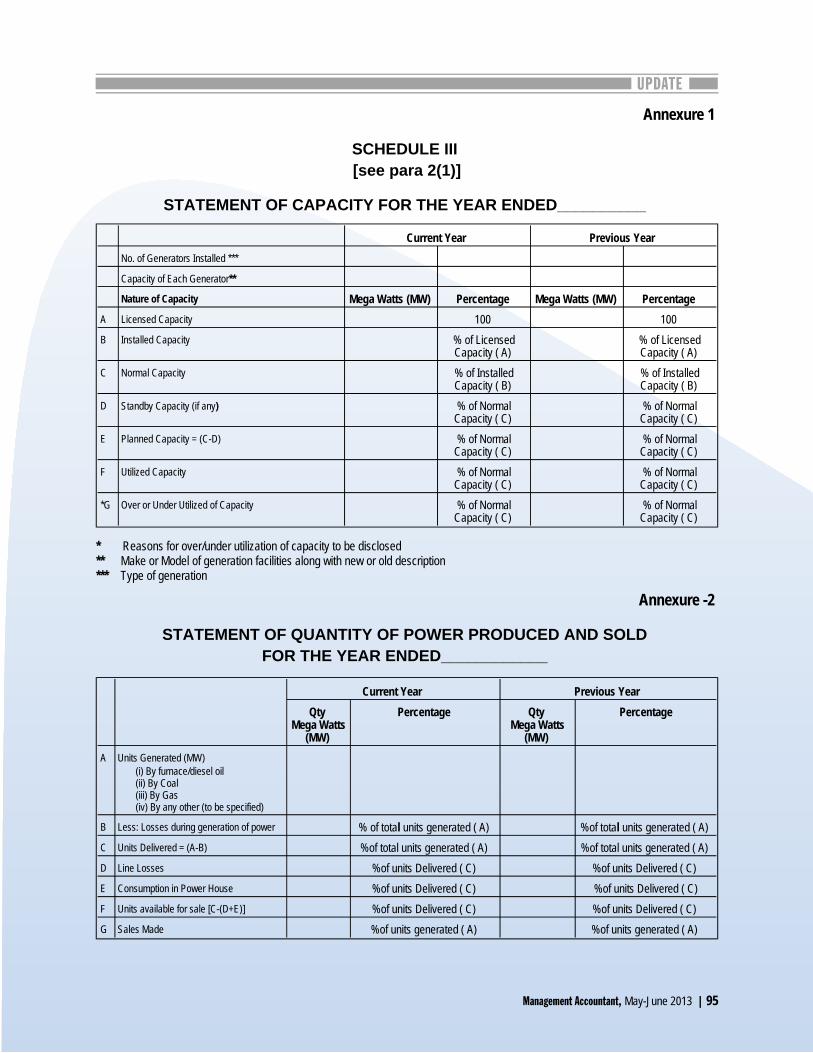

SCHEDULE IIIAn nex ure 1

[see para 2(1)]

INTERMEDIARY PRODUCT COST STATEMENT FOR THE YEAR ENDED _________Intermediary ProductName:- ________________________

QUANTITATIVE DATATHIS YEAR(Tonnes)

LAST YEAR(Tonnes)

1. Opening Stock

2. Produced During the Period

3. Transferred/Purchased from other Plants/Suppliers

4. Closing Stock

5. Intermediary Product Transferred to the Next Process

S.No1

PARTICULARS2

CURRENT YEAR PREVIOUS YEARTOTAL

COST Rs3

COST PERTONNE Rs

4

TOTALCOST Rs

5

COST PERTONNE Rs

6123456789

10111213

14151617

1819202122

232425

Ra Materials (i)(ii)(iii)Chemicals, ResinsCatalysts SpentMaintenance SparesRepairs and MaintenanceSalaries, Wages & Other BenefitsRent, Rates & TaxesRoyaltiesDepreciationOther OverheadsEmoluments to Foreign Engineers & TechniciansUTILITIES ALLOCATEDPower (kwh) (Annexure-4)Steam (Cubic Meter) (Annexure-8)Compressed Air (Cubic Meter) (Annexure-9)Demineralized Water (Liter) (Annexure-10)ALLOCATED COSTPlant Engineering Department Cost Plant Technical Department CostFactory Management Department Cost Add: Opening Stock Transferred in from Previous Process/ Purchased from Other SuppliersLess: Transfers to Saleable By-product Closing StockCost of Intermediary Product Transferred to Next Process

Note:- Separate statements shall be prepared for each intermediary product.

82 | Man age ment Ac count ant, May- June, 2013

UPDATE

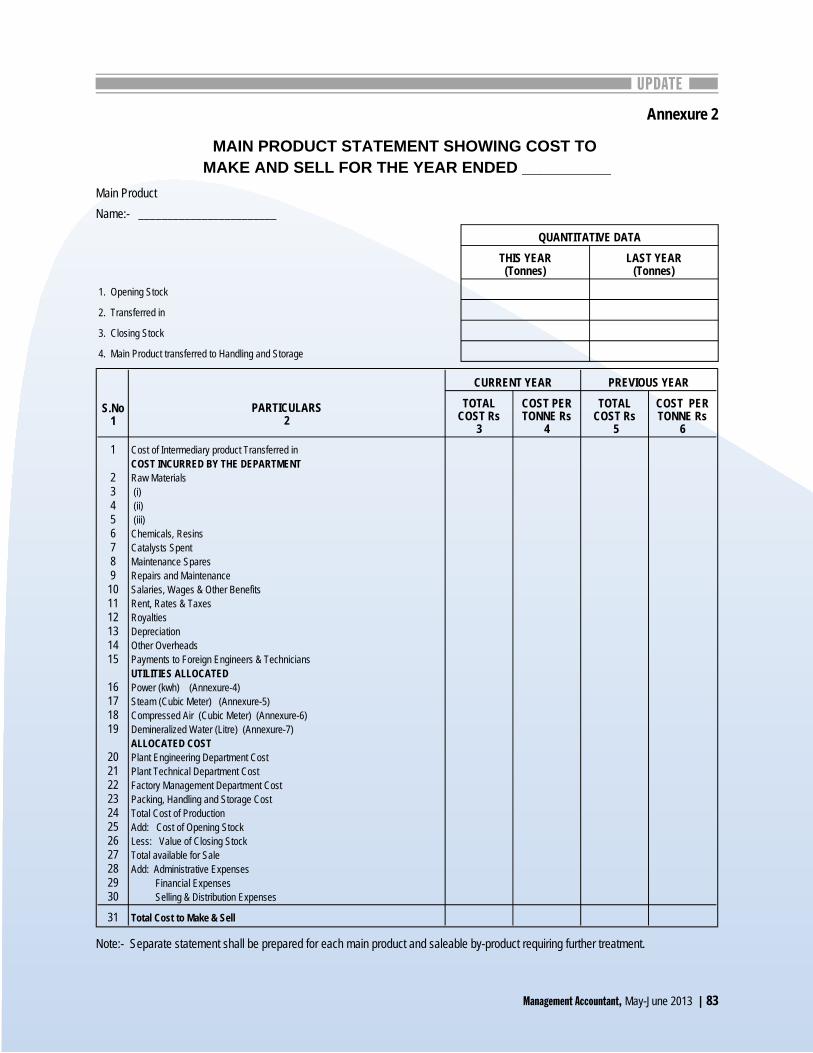

An nex ure 2

MAIN PRODUCT STATEMENT SHOWING COST TO MAKE AND SELL FOR THE YEAR ENDED __________

Main ProductName:- ________________________

QUANTITATIVE DATATHIS YEAR(Tonnes)

LAST YEAR(Tonnes)

1. Opening Stock

2. Transferred in

3. Closing Stock

4. Main Product transferred to Handling and Storage

S.No1

PARTICULARS2

CURRENT YEAR PREVIOUS YEARTOTAL

COST Rs3

COST PERTONNE Rs

4

TOTALCOST Rs

5

COST PERTONNE Rs

61

23456789

101112131415

16171819

2021222324252627282930

Cost of Intermediary product Transferred inCOST INCURRED BY THE DEPARTMENTRaw Materials (i) (ii) (iii)Chemicals, ResinsCatalysts SpentMaintenance SparesRepairs and MaintenanceSalaries, Wages & Other BenefitsRent, Rates & TaxesRoyaltiesDepreciationOther OverheadsPayments to Foreign Engineers & TechniciansUTILITIES ALLOCATEDPower (kwh) (Annexure-4)Steam (Cubic Meter) (Annexure-5)Compressed Air (Cubic Meter) (Annexure-6)Demineralized Water (Litre) (Annexure-7)ALLOCATED COSTPlant Engineering Department CostPlant Technical Department CostFactory Management Department CostPacking, Handling and Storage Cost Total Cost of ProductionAdd: Cost of Opening StockLess: Value of Closing StockTotal available for SaleAdd: Administrative Expenses Financial Expenses Selling & Distribution Expenses

31 Total Cost to Make & Sell

Note:- Separate statement shall be prepared for each main product and saleable by-product requiring further treatment.

Man age ment Ac count ant, May- June 2013 | 83

UPDATE

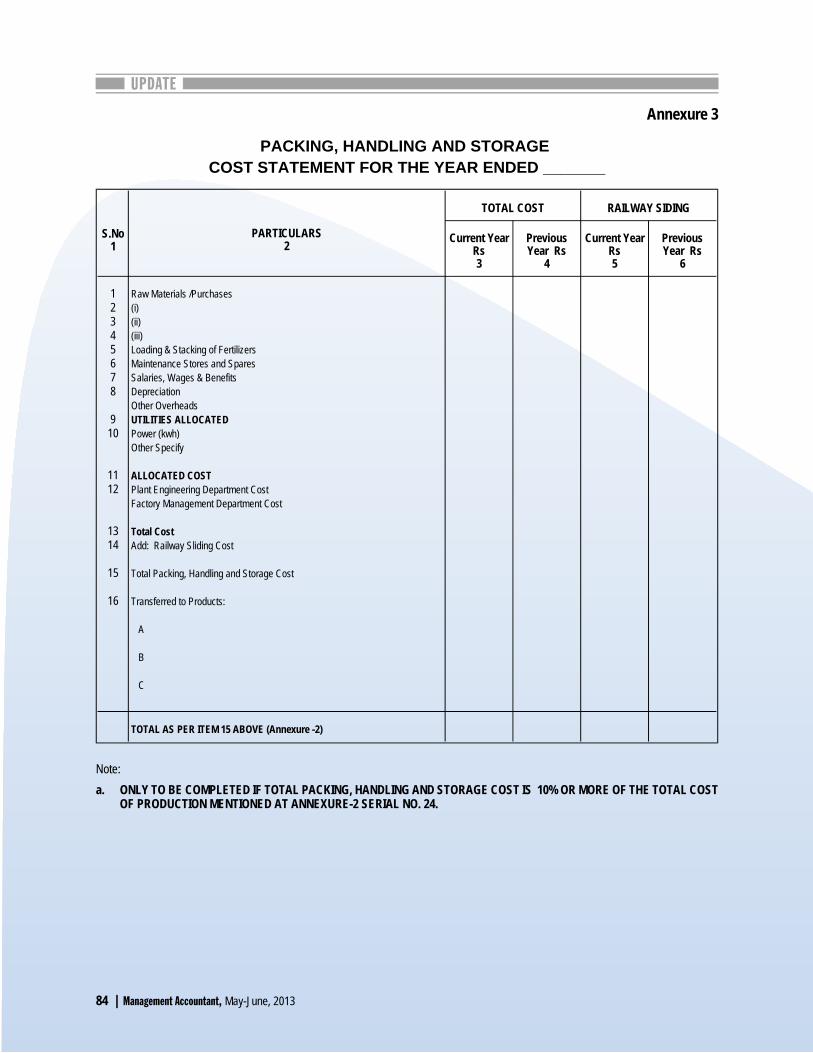

An nex ure 3

PACKING, HANDLING AND STORAGE COST STATEMENT FOR THE YEAR ENDED _______

S.No1

PARTICULARS2

TOTAL COST RAILWAY SIDING

Current YearRs3

PreviousYear Rs

4

Current YearRs5

PreviousYear Rs

6

12345678

910

1112

1314

15

16

Raw Materials /Purchases (i)(ii)(iii)Loading & Stacking of FertilizersMaintenance Stores and SparesSalaries, Wages & BenefitsDepreciationOther OverheadsUTILITIES ALLOCATEDPower (kwh) Other Specify

ALLOCATED COSTPlant Engineering Department Cost Factory Management Department Cost

Total CostAdd: Railway Sliding Cost

Total Packing, Handling and Storage Cost Transferred to Products:

A

B

C

TOTAL AS PER ITEM 15 ABOVE (Annexure -2)

Note:a. ONLY TO BE COMPLETED IF TOTAL PACKING, HANDLING AND STORAGE COST IS 10% OR MORE OF THE TOTAL COST

OF PRODUCTION MENTIONED AT ANNEXURE-2 SERIAL NO. 24.

84 | Man age ment Ac count ant, May- June, 2013

UPDATE

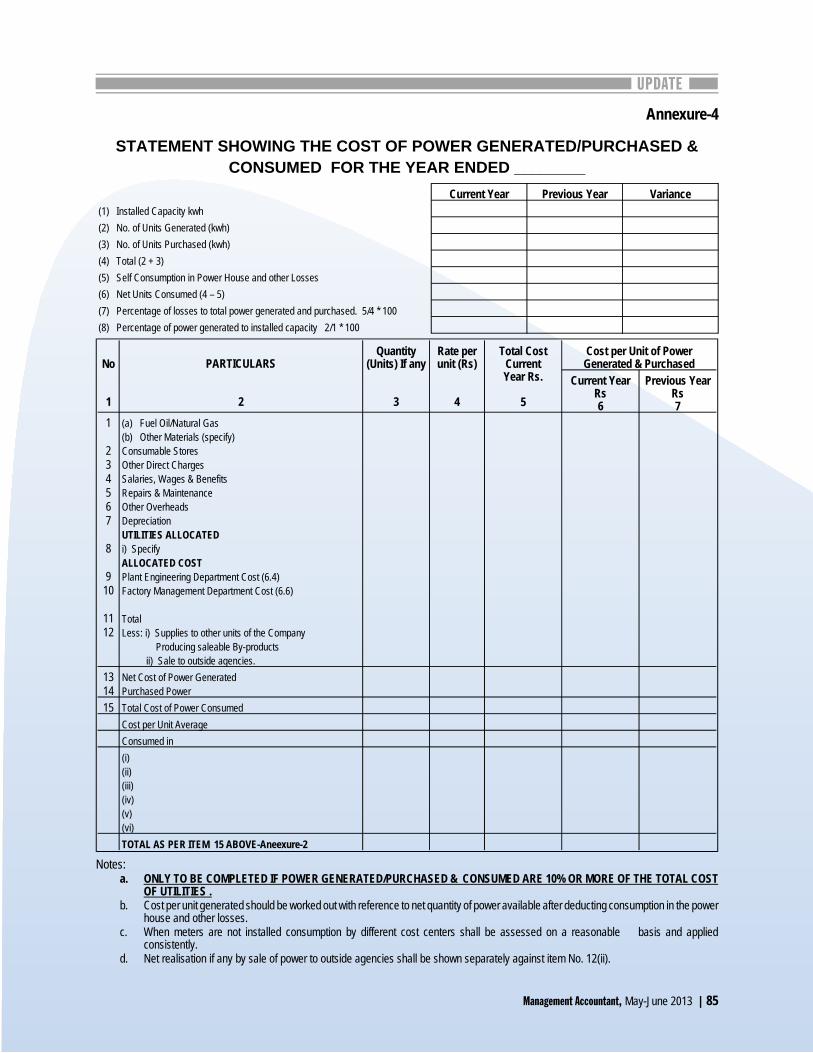

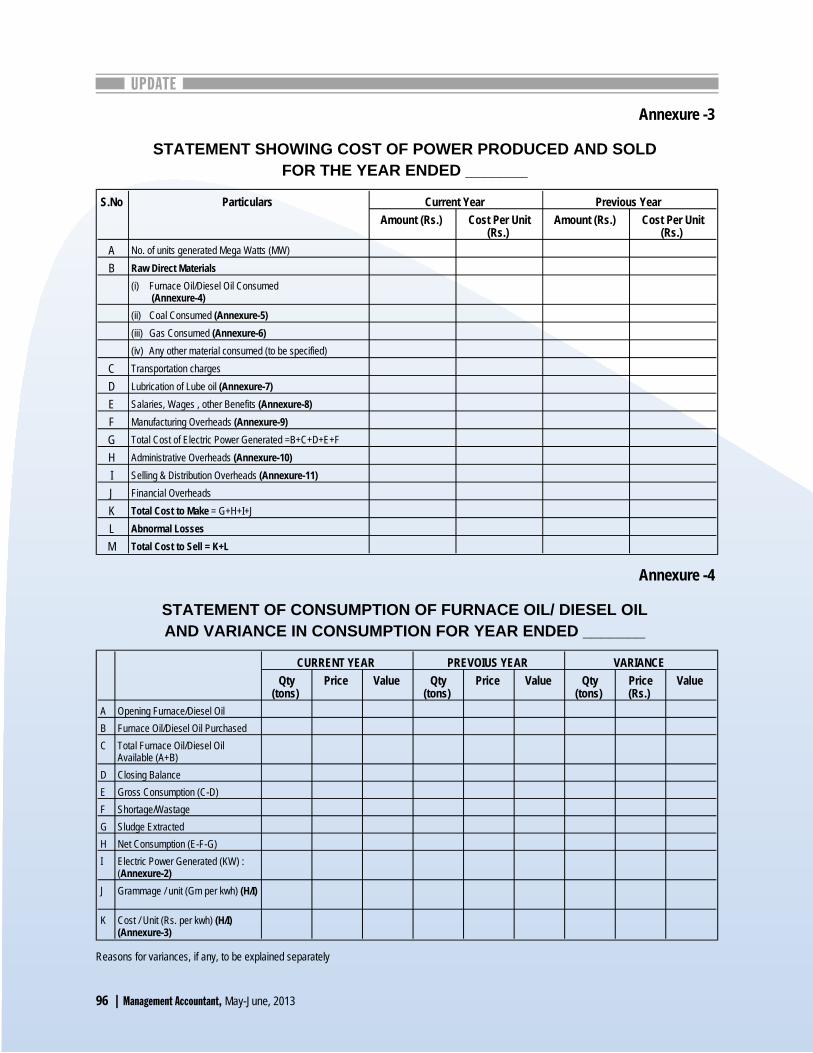

Annexure-4

STATEMENT SHOWING THE COST OF POWER GENERATED/PURCHASED &CONSUMED FOR THE YEAR ENDED ________

Current Year Previous Year Variance(1) Installed Capacity kwh(2) No. of Units Generated (kwh)(3) No. of Units Purchased (kwh)(4) Total (2 + 3)(5) Self Consumption in Power House and other Losses(6) Net Units Consumed (4 – 5)(7) Percentage of losses to total power generated and purchased. 5/4 * 100(8) Percentage of power generated to installed capacity 2/1 * 100

No

1

PARTICULARS

2

Quantity(Units) If any

3

Rate perunit (Rs)

4

Total CostCurrentYear Rs.

5

Cost per Unit of PowerGenerated & Purchased

Current YearRs6

Previous YearRs7

1

234567

8

910

1112

(a) Fuel Oil/Natural Gas(b) Other Materials (specify)Consumable StoresOther Direct ChargesSalaries, Wages & BenefitsRepairs & MaintenanceOther OverheadsDepreciationUTILITIES ALLOCATEDi) SpecifyALLOCATED COSTPlant Engineering Department Cost (6.4)Factory Management Department Cost (6.6)

TotalLess: i) Supplies to other units of the Company Producing saleable By-products ii) Sale to outside agencies.

1314

Net Cost of Power GeneratedPurchased Power

15 Total Cost of Power ConsumedCost per Unit AverageConsumed in(i)(ii)(iii)(iv)(v)(vi)TOTAL AS PER ITEM 15 ABOVE-Aneexure-2

Notes:a. ONLY TO BE COMPLETED IF POWER GENERATED/PURCHASED & CONSUMED ARE 10% OR MORE OF THE TOTAL COST

OF UTILITIES .b. Cost per unit generated should be worked out with reference to net quantity of power available after deducting consumption in the power

house and other losses.c. When meters are not installed consumption by different cost centers shall be assessed on a reasonable basis and applied

consistently.d. Net realisation if any by sale of power to outside agencies shall be shown separately against item No. 12(ii).

Man age ment Ac count ant, May- June 2013 | 85

UPDATE

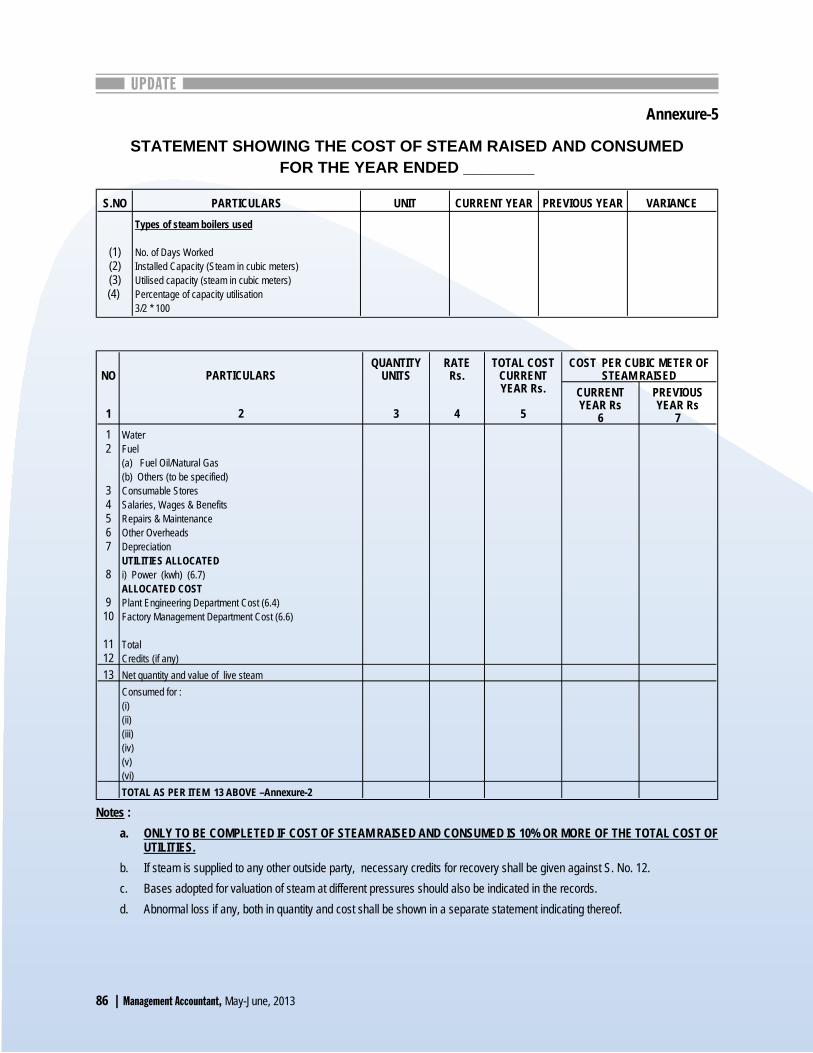

Annexure-5

STATEMENT SHOWING THE COST OF STEAM RAISED AND CONSUMEDFOR THE YEAR ENDED ________

S.NO PARTICULARS UNIT CURRENT YEAR PREVIOUS YEAR VARIANCE

(1)(2)(3)(4)

Types of steam boilers used

No. of Days WorkedInstalled Capacity (Steam in cubic meters)Utilised capacity (steam in cubic meters)Percentage of capacity utilisation3/2 * 100

NO

1

PARTICULARS

2

QUANTITYUNITS

3

RATERs.

4

TOTAL COSTCURRENTYEAR Rs.

5

COST PER CUBIC METER OFSTEAM RAISED

CURRENTYEAR Rs

6

PREVIOUSYEAR Rs

712

34567

8

910

1112

WaterFuel(a) Fuel Oil/Natural Gas(b) Others (to be specified)Consumable StoresSalaries, Wages & BenefitsRepairs & MaintenanceOther OverheadsDepreciationUTILITIES ALLOCATEDi) Power (kwh) (6.7)ALLOCATED COSTPlant Engineering Department Cost (6.4)Factory Management Department Cost (6.6)

TotalCredits (if any)

13 Net quantity and value of live steamConsumed for :(i)(ii)(iii)(iv)(v)(vi)TOTAL AS PER ITEM 13 ABOVE –Annexure-2

Notes : a. ONLY TO BE COMPLETED IF COST OF STEAM RAISED AND CONSUMED IS 10% OR MORE OF THE TOTAL COST OF

UTILITIES.b. If steam is supplied to any other outside party, necessary credits for recovery shall be given against S. No. 12.c. Bases adopted for valuation of steam at different pressures should also be indicated in the records.d. Abnormal loss if any, both in quantity and cost shall be shown in a separate statement indicating thereof.

86 | Man age ment Ac count ant, May- June, 2013

UPDATE

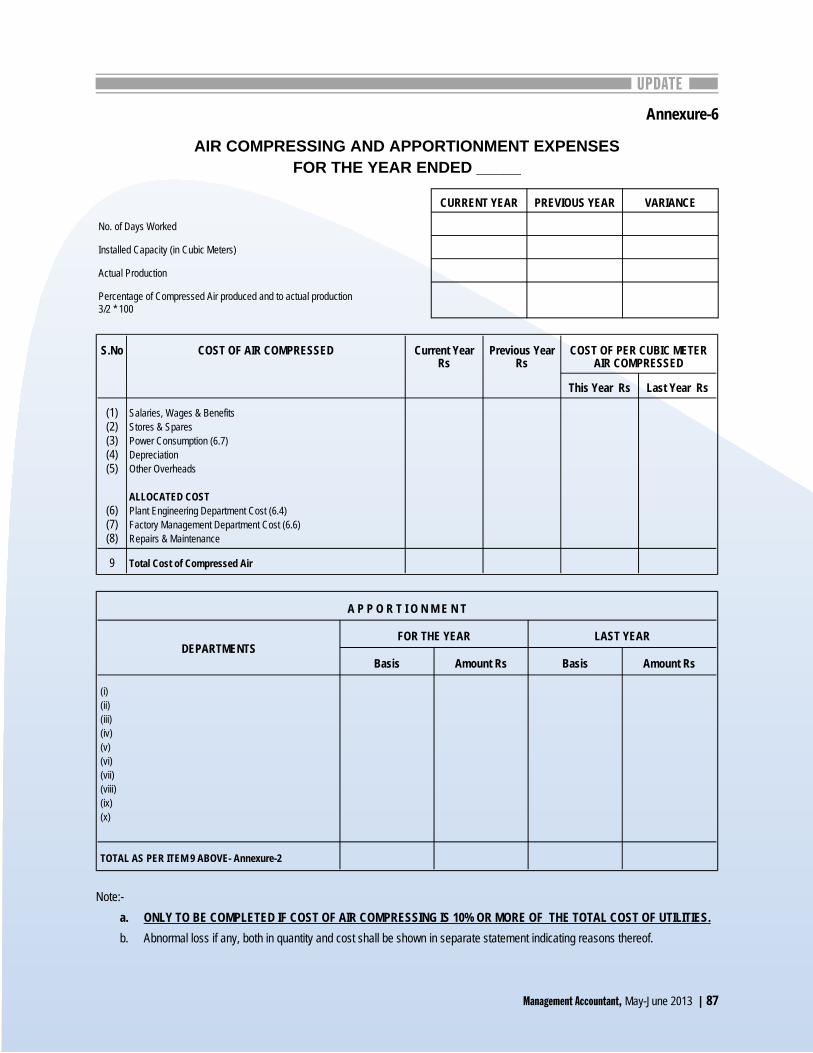

Annexure-6

AIR COMPRESSING AND APPORTIONMENT EXPENSESFOR THE YEAR ENDED _____

CURRENT YEAR PREVIOUS YEAR VARIANCE

No. of Days Worked

Installed Capacity (in Cubic Meters)

Actual Production

Percentage of Compressed Air produced and to actual production3/2 * 100

S.No COST OF AIR COMPRESSED Current YearRs

Previous YearRs

COST OF PER CUBIC METERAIR COMPRESSED

This Year Rs Last Year Rs

(1)(2)(3)(4)(5)

(6)(7)(8)

Salaries, Wages & BenefitsStores & SparesPower Consumption (6.7)DepreciationOther Overheads

ALLOCATED COSTPlant Engineering Department Cost (6.4)Factory Management Department Cost (6.6)Repairs & Maintenance

9 Total Cost of Compressed Air

A P P O R T I O N M E N T

DEPARTMENTSFOR THE YEAR LAST YEAR

Basis Amount Rs Basis Amount Rs

(i)(ii)(iii)(iv)(v)(vi)(vii)(viii)(ix)(x)

TOTAL AS PER ITEM 9 ABOVE- Annexure-2

Note:- a. ONLY TO BE COMPLETED IF COST OF AIR COMPRESSING IS 10% OR MORE OF THE TOTAL COST OF UTILITIES.b. Abnormal loss if any, both in quantity and cost shall be shown in separate statement indicating reasons thereof.

Man age ment Ac count ant, May- June 2013 | 87

UPDATE

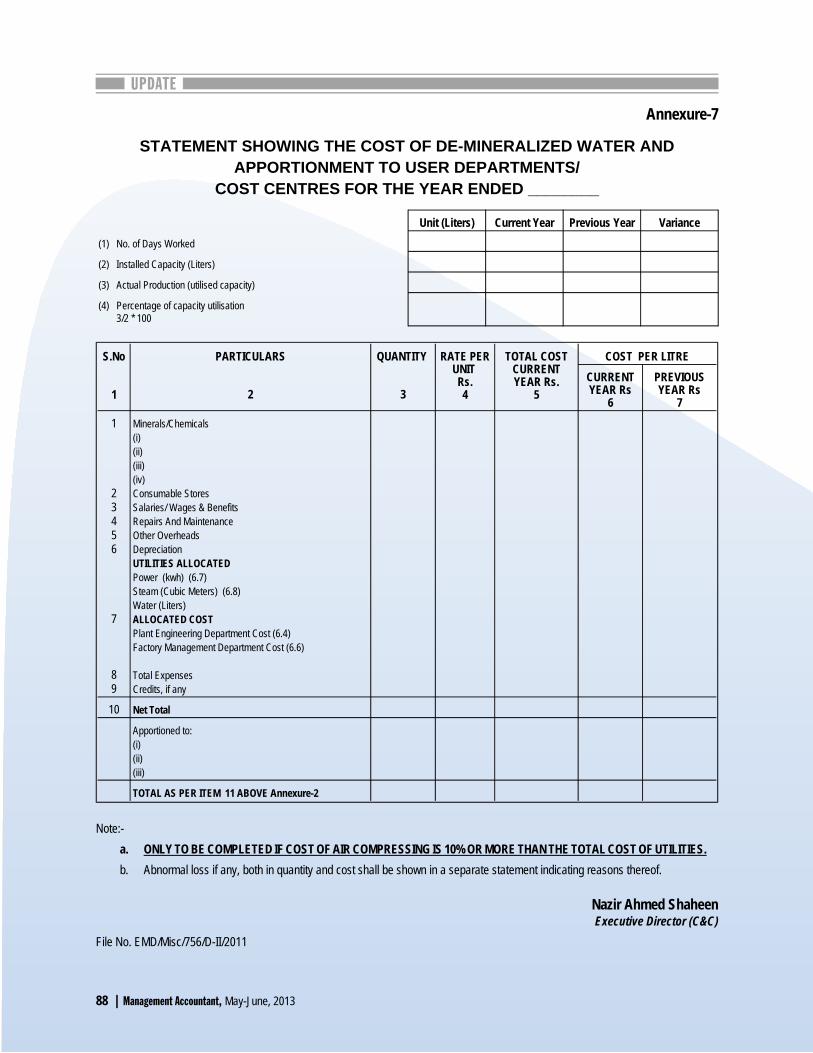

Annexure-7

STATEMENT SHOWING THE COST OF DE-MINERALIZED WATER ANDAPPORTIONMENT TO USER DEPARTMENTS/

COST CENTRES FOR THE YEAR ENDED ________

Unit (Liters) Current Year Previous Year Variance(1) No. of Days Worked

(2) Installed Capacity (Liters)

(3) Actual Production (utilised capacity)

(4) Percentage of capacity utilisation3/2 * 100

S.No

1

PARTICULARS

2

QUANTITY

3

RATE PERUNIT Rs.4

TOTAL COSTCURRENTYEAR Rs.

5

COST PER LITRECURRENTYEAR Rs

6

PREVIOUSYEAR Rs

71

23456

7

89

Minerals/Chemicals(i)(ii)(iii)(iv)Consumable StoresSalaries/ Wages & BenefitsRepairs And MaintenanceOther OverheadsDepreciationUTILITIES ALLOCATEDPower (kwh) (6.7)Steam (Cubic Meters) (6.8)Water (Liters)ALLOCATED COSTPlant Engineering Department Cost (6.4)Factory Management Department Cost (6.6)

Total ExpensesCredits, if any

10 Net Total

Apportioned to:(i)(ii)(iii)

TOTAL AS PER ITEM 11 ABOVE Annexure-2

Note:-a. ONLY TO BE COMPLETED IF COST OF AIR COMPRESSING IS 10% OR MORE THAN THE TOTAL COST OF UTILITIES.b. Abnormal loss if any, both in quantity and cost shall be shown in a separate statement indicating reasons thereof.

Na zir Ah med Sha heenEx ecu tive Di rec tor (C&C)

File No. EMD/Misc/756/D-II/2011

88 | Man age ment Ac count ant, May- June, 2013

UPDATE

THE GAZETTE OF PAKISTAN SECURITIES AND EXCHANGE COMMISSION OF PAKISTAN

NOTIFICATION Is lama bad, the 26th March, 2012

S.R.O. 302-(I)/2012.- The fol low ing draft of Elec tric Power Gen era tion In dus try (Cost Ac count ing Re cords) Or der, 2012 which is pro posedto be made in ex er cise of pow ers con ferred by clause (e) of sub- section (1) of sec tion 230 read with sec tion 246 of the Com pa nies Or di -nance, 1984 (XLVII of 1984), and sec tion 40B of the Se cu ri ties and Ex change Com mis sion of Paki stan Act, 1997 (XLII of 1997) is herebypub lished for the in for ma tion of all per sons 1ike1y to be af fected thereby and no tice is hereby given that the draft will be taken into con sid -era tion af ter thirty days of its pub li ca tion in the Of fi cial Ga zette.

Any ob jec tion or sug ges tion which may be re ceived from any per son in re spect of the said draft bef ore the ex piry of the said date will be con -sid ered by the Se cu ri ties and Ex change Com mis sion of Paki stan.

ELECTRIC POWER GENERATION INDUSTRY(COST ACCOUNTING RECORDS) ORDER, 2012

1. Short ti tle, ex tent, com mence ment and ap pli ca tion.- (1) This Or der shall be called the Elec tric Power Gen era tion In dus try (CostAc count ing Re cords) Or der, 2012.

(2) It shall come into force with ef fect from July 1, 2012.

(3) This Or der shall ap ply to every com pany en gaged wholly or par tially in Gen era tion of Elec tric Power En ergy in Paki stan un derthe li cense(s) granted by the Na tional Elec tric Power Regu la tory Author ity (NEPRA) of Paki stan.

2. Main te nance of rec ords and in de pend ent audi tors’ as sur ance.- (1) Every com pany to which this Or der ap plies shall, in re spect ofeach fi nan cial year com menc ing on or af ter the com mence ment of this Or der, keep cost ac count ing rec ords, con tain ing, inter- alia, thepar ticu lars speci fied in Sched ule I, II and III to this Or der.

(2) The cost ac count ing rec ords re ferred to in sub- paragraph (1) shall be kept in such a way as to make it pos si ble to cal cu late fromthe par ticu lars en tered therein the cost of gen era tion and cost of sales of each of the gen era tion fa cil ity li censed by NEPRAre ferred to in sub- para (3) of para (1), dur ing a fi nan cial year.

(3) Where a com pany is en gaged in any other busi ness(es) in ad di tion to those re ferred to in sub- para (3) of para (1), the par ticu larsre lat ing to the utili za tion of ma te ri als, la bour and other items of cost in so far as they are ap pli ca ble to such other prod uct shall notbe in cluded in the cost of prod uct re ferred to in that para.

(4) It shall be the duty of every per son re ferred to in sub- section (7) of sec tion 230 of the Com pa nies Or di nance, 1984 (XL VII of1984), to com ply with the pro vi sions of sub- paragraph (1) to (3) in the same man ner as they are li able to main tain fi nan cialac counts re quired un der sec tion 230 of the said Or di nance.

3. Pen alty.- If a com pany con tra venes the pro vi sions of para 2 of this Or der, every di rec tor, in clud ing chief ex ecu tive and chiefac count ant, of the com pany who has know ingly by his act or omis sion been the cause of such de fault shall be pun ish able un der sub- section (7) of sec tion 230 of the com pa nies Or di nance, 1984 (XL VII of 1984)

(Na zir Ah med Sha heen) Ex ecu tive Di rec tor (C&C)

Man age ment Ac count ant, May- June 2013 | 89

UPDATE

SCHEDULE 1 (See para graph2)

I. MATERIAL

(1) Di rect Ma te rial.-

(a) Fol low ing raw/di rect ma te ri als are con sid ered as prime sources of en ergy in their re spec tive Elec tric Power Gen era tion pro cess:

(i) Fur nace Oil; (ii) Die sel Oil; (iii) Gas; (iv) Coal; (v) Wa ter; (vi) Wind; (vii) Steam; and (viii) Oth ers (to be speci fied)

(b) Ade quate rec ords shall be main tained for above ma te rial where ap pli ca ble for re ceipt, is sue and bal ances both in quan ti ties andval ues. The ba sis on which the value of re ceipt and is sue has been cal cu lated shall be in di cated clearly in the cost rec ordsmain tained or if so de sired by the com pany in a sepa rate man ual of pro ce dures, if any main tained by the com pany or in foot- notes or sepa rate ex plana tory notes to the cost state ments for the rele vant pe ri od. Such ba sis shall be ap plied con sis tently,through out the rele vant pe ri od.

(c) The val ues shall in clude all di rect charges upto plant site such as ex cise duty, haul age charges, trans port, freight, han dling andtran sit in sur ance pre mium in curred for lo cal pro cure ment.

(d) In case of im ported ma te ri als/sources of en ergy such as oils or coal, all im port charges, cus tom duty, port dues, ocean/air freight, in land freight, ma rine in sur ance and all other charges levi able and pay able at the time of im port, shall be shown sepa rately andin cluded to work out the landed cost of oils or coal.

(e) Where coal is raised from mines owned or taken on lease by the com pany, sepa rate rec ord show ing the cost of rais ing shall bemain tained in such de tail as may en able the com pany to es tab lish proper cost of the above re ferred ma te rial in cost rec ords.

(f) Ade quate rec ords shall be main tained to es tab lish the cor rect quan ti ties or vol ume of gas used. For as cer tain ment of value ofgas, all the ex penses in curred (all Gov ern ment dues lo cal or cen tral, and all other ex penses nec es sary to fetch the gas to plantsite) for the pro cure ment of gas at plant site, shall be shown sepa rately and in cluded to work out the cost of gas ac tu allycon sumed dur ing the pro cess.

(g) Proper rec ords shall be main tained show ing the quan tity and value of wast age, spoil age, re jec tion and losses of in putma te rial/fu els and con sum ables stores whether in tran sit, stor age, op era tions or at any other stage. The method fol lowed forad just ing the above losses as well as in come de rived from dis posal of re jected and waste ma te rial in clud ing spoil age, if any, inde ter min ing the cost of ac tivi ties shall be in di cated in cost rec ords.

(h) Re al iz able value of waste or by- product, if any, shall be cred ited to ar rive at the net cost of power pro duced

(i) Re cords shall be main tained in such de tail to en able the com pany to read ily pro vide data re quired in the vari ous Cost State ments pre scribed in this Or der in a veri fi able state.

(2) Lu bri ca tion oil con sump tion in en gines and tur bines.- Ade quate rec ords shall be main tained in re spect of all re ceipts, is sues andbal ances, both in quan ti ties and val ues. Sepa rate rec ord for regu lar con sump tion and rou tine oil change at stan dard hours of run shallbe main tained in the cost state ment as pre scribed in this Or der so that cost and quan ti ties may be veri fied with stan dards.

(3) Con sum able stores, small tools, ma chin ery spare parts, etc

(a) Ade quate rec ords shall be main tained to show the re ceipts, is sues and bal ances, both in quan ti ties and cost of each item ofcon sum able stores, small tools, ma chin ery spares.

(b) The cost of is sue of con sum able stores, small tools and ma chin ery spares shall be charged to the rele vant heads of ac countssuch as re pairs to plant and ma chin ery or re pairs to build ing. Ma te rial con sumed on capi tal works such as ad di tion to build ings,plant and ma chin ery and other as sets shall be shown un der the rele vant capi tal heads and not in the cost state ments of elec tricpower gen er at ing com pa nies.

90 | Man age ment Ac count ant, May- June, 2013

UPDATE

(c) Wast age of any con sum able stores whether in tran sit, stor age or in any other plant ac tiv ity shall be quan ti fied and shownsepa rately. Method of deal ing with such losses in cost ing shall also be in di cated in the cost rec ords. 4

II. INVENTORY (1) The in ven to ries shall be meas ured at the lower of cost and net re al is able value. Net re al iz able value is the es ti mated sell ing price in

the or di nary course of busi ness less the es ti mated costs of com ple tion and the es ti mated costs nec es sary to make the sale. The costof in ven to ries shall com prise all costs of pur chase, costs of con ver sion and other costs in curred in bring ing the in ven to ries to theirpres ent lo ca tion and con di tion.

(2) It shall also be dis closed that the cost of in ven to ries shall be as signed by us ing the first- in, first- out (FIFO) or weighted av er age costfor mula. An en tity shall use the same cost for mula for all in ven to ries hav ing a simi lar na ture and use to the en tity. For in ven to ries with a dif fer ent na ture or use, dif fer ent cost for mu las may be jus ti fied. How ever, the cost of in ven to ries of items that are not or di nar ilyin ter change able and goods or serv ices pro duced and seg re gated for spe cific proj ects shall be as signed by us ing spe cific iden ti fi ca tion of their in di vid ual costs.

III. SALARIES AND WAGES (1) Ade quate rec ords shall be main tained to show the at ten dance of work ers em ployed by the com pany whether on regu lar, tem po rary or

on con tract ba sis, as the case may be.

(2) Ade quate rec ord shall be main tained in re spect of pay ments made for over time in such man ner that la bour cost is avail able for eachcost cen ter.

(3) Proper rec ord shall be main tained in re spect of earn ings of all the em ploy ees, func tion or activity- wise, and the works on which theyare em ployed. The rec ord shall also in di cate the fol low ing sepa rately for each such func tion or ac tiv ity.-

(a) Di rect wages and sala ries (i) Regu lar sala ries/wages (ii) Con tract sala ries/wages (iii) Piece rate wages

(b) In di rect sala ries and wages (i) In cen tives (ii) Bo nuses (iii) Scheme based earn ings (iv) Over time (v) Gra tu ity or statu tory dues

(4) Fair and rea son able al lo ca tion shall be made for wages paid to such la bour as has been util ized in vari ous de part ments or cost cen ters and the ba sis of such al lo ca tion shall be fol lowed con stantly.

(5) Rea sons for idle time or lay off pay ments shall be re corded sepa rately and their treat ment in the cal cu la tions of cost of powerpro duced/gen er ated shall be in di cated in the cost state ments.

(6) Any wages paid for ad di tion to plant and ma chin ery or other fixed as sets shall be capi tal ized and ex cluded from the cost of powerpro duced/gen er ated.

(7) Bene fits paid to the em ploy ees other than cov ered in above para graphs shall be worked out sepa rately and shown in cost state ments,department- wise or cost cen ter wise.

IV. SERVICE DEPARTMENT

Ade quate rec ords shall be main tained show ing ex penses in curred for each serv ice de part ment e.g. work shop, labo ra tory, trans port andtest ing house etc. These ex penses shall be ap por tioned to other cost cen ters in clud ing serv ice de part ments on an eq ui ta ble ba sis. Wherethese serv ice de part ments serve other de part ments such as steam de part ment or fur nace oil han dling de part ment, suit able ba sis shall beworked out so that the ap por tion ment to other de part ments or to sale able prod ucts, is duly worked out and ap plied con sis tently.

V. UTILITIES

(1) Ade quate rec ords shall be main tained show ing the quan tity and cost of vari ous utili ties con sumed and util ized by dif fer entde part ments and cost cen ters.

Man age ment Ac count ant, May- June 2013 | 91

UPDATE

(2) Re cords shall be main tained to en able the as sess ment of con sump tion or utili za tion by serv ice de part ments. Al lo ca tion of cost shallbe made on the ba sis of ac tual con sump tion or on ba sis of tech ni cal es ti mates in the ab sence of ac tual meas ure ment.

(3) De tails shall be avail able to de ter mine the ac tual con sump tion by the power house. The cost of power con sumed by the com pany shall be shown sepa rately in cost state ments.

(4) Ap pro pri ate rec ords shall be main tained of pump ing, stor age and dis tri bu tion of wa ter to de ter mine the ac tual cost of wa ter used bythe dif fer ent cost cen ters e.g. cool ing tow ers, pu ri fi ers and by other serv ice de part ments. Ba sis of al lo cat ing the cost of wa ter amongstthe dif fer ent cost cen ters shall also be in di cated in the rec ords. 6

(5) Ade quate rec ords of cost of com pressed air shall be main tained. The al lo ca tion of cost of com pressed air to dif fer ent de part mentsshall be in di cated in the cost rec ords.

VI. REPAIR AND MAINTENANCE / WORKSHOP CHARGES

(1) Ade quate rec ords of ex pen di ture in curred on work shop fa cili ties pro vided for re pair and main te nance of plant and ma chin ery in costcen ters shall be main tained.

(2) Re cord of re pair and main te nance con tracts shall be main tained sepa rately. The ba sis of al lo ca tion of re pairs and main te nance todif fer ent cost cen ters shall be in di cated in the cost rec ords. Cost of work of capi tal na ture and/or of heavy re pairs and over hauls,bene fits of which are likely to spread over a longer pe ri od, shall be capi tal ized.

(3) If a sepa rate team is work ing for the main te nance of a par ticu lar cost cen tre, the sala ries/wages and cost of con sum ables, spare partsand tools shall be charged as di rect ex pense of that cost cen tre.

(4) If main te nance serv ices are util ized by other sale able items like waste, heat en ergy, the por tion util ized for them should be seg re gatedand charged thereto.

VII. DEPRECIATION