Embed Size (px)

Citation preview

Management Presentation

March 2013

FORWARD LOOKING STATEMENTS

• This presentation about API Technologies Corp. (the “Company”) includes forward-looking statements within the meaning of the Private Securities Litigation Reform Act of 1995. All statements other than statements of historical fact, including statements regarding industry prospects or future results of the business, operations or financial position of API made in this presentation are forward-looking. We use words such as believe, expect, anticipate, intends, estimate, forecast, project, should and similar expressions to identify forward-looking statements. Forward-looking statements are based on management’s current expectations of our near-term results, based on current information available pertaining to us and are inherently uncertain. We wish to caution investors that any forward-looking statements made by or on our behalf are subject to uncertainties and other factors that could cause actual results to differ materially from such statements. These uncertainties and other risk factors include, but are not limited to: the affect of the unfavorable global, national and local economic results to differ materially from such statements. These uncertainties and other risk factors include, but are not limited to: the affect of the unfavorable global, national and local economic conditions on our customers and our businesses, the affect of the current economic crisis on our ability to effect our business plans and strategies, the changing political conditions in the United States and other countries, governmental laws and regulations, anticipated government budget changes, international trading and export restrictions, customer product acceptance, and access to capital markets, and foreign currency risks. These risks and uncertainties, as well as other risks and uncertainties could cause our actual results to differ significantly from management’s expectations. New factors emerge from time to time and it is not possible for management to predict all such factors, nor can it assess the impact of each such factor on the business or the extent to which any factor, or a combination of factors, may cause actual results to differ materially from those contained in any forward-looking statements. We assume no obligation to update or revise any forward-looking statements made herein or any other forward-looking statements we make, whether as a result of new information, future events, or otherwise.

2

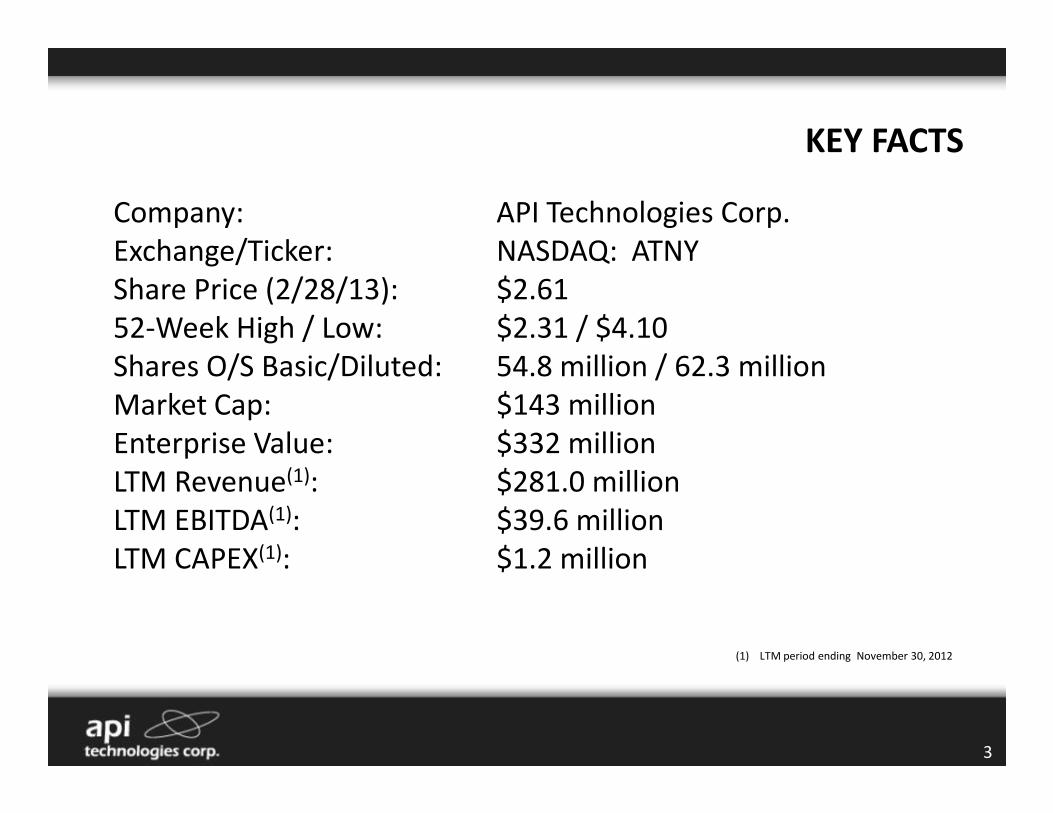

KEY FACTS

Company: API Technologies Corp.

Exchange/Ticker: NASDAQ: ATNY

Share Price (2/28/13): $2.61

52-Week High / Low: $2.31 / $4.10

Shares O/S Basic/Diluted: 54.8 million / 62.3 million

Market Cap: $143 millionMarket Cap: $143 million

Enterprise Value: $332 million

LTM Revenue(1): $281.0 million

LTM EBITDA(1): $39.6 million

LTM CAPEX(1): $1.2 million

(1) LTM period ending November 30, 2012

3

• Dominant RF/microwave, microelectronics, and

security technology provider in defense and

commercial high-reliability markets

– 90%+ sole/primary source with recurring revenue streams

– Broad portfolio of highly engineered technology products

INVESTMENT HIGHLIGHTS

– Alignment with growth areas of the Defense budget and

within high-reliability industrial markets

• Focus on revenue generation and profitability

– Target of 20% Adjusted EBITDA company wide

– Demonstrated ability to generate cash

4

• Provider of RF/microwave, microelectronics, and

security technologies for the defense, aerospace,

and commercial industries

• Founded in 1981; Re-launched the new API with

new vision in 2011

– Significant acquisition activity in 2011

Today, one of the largest “non-prime” provider of

COMPANY OVERVIEW

– Today, one of the largest “non-prime” provider of

RF/Microwave and microelectronics

• 2,200 employees world-wide

• 3,000 customers world-wide

• Revenue breakdown

– ~75% Domestic / 25% International

– ~60% Defense & Government / 40% Commercial

5

OUR MARKETS & CUSTOMERS

U.S. U.S. DoDDoD

45%

• Radar

• Military aircraft

Missile defense

Medical, Industrial & Medical, Industrial &

Commercial AerospaceCommercial Aerospace

22%

• Medical devices

• Commercial air

• Alt. Energy

Commercial & Commercial &

CommunicationsCommunications

22%

• Mobile devices

• Wireless

communications

Government & Government &

SecuritySecurity

11%

• Secure

communications

Secure access

6

LTM Ended November 30, 2012

• Missile defense

• SATCOM

• C4ISR

• UAVs

• Alt. Energy

• Downhole

• Transportation

communications

• Satellites

• Enterprise

systems

• Secure access

• Encryption

RF/Microwave & Microelectronics

38.4%

Electromagnetic Integrated Solutions (EIS)

18.6% 9.3%

Sensors Products

ATTRACTIVE PRODUCT PORTFOLIO

7

Power & Systems Solutions

5.6%

Secure Systems &Information Assurance (SSIA)

8.0%

Electronics Manufacturing Services (EMS)

21.0%

LTM-Ended November 30, 2012

SSC

Key:

Systems, Subsystems & Components (SSC) Segment SSIA Secure Systems & Information

Assurance (SSIA) Segment EMS Electronics Manufacturing Services (EMS) Segment

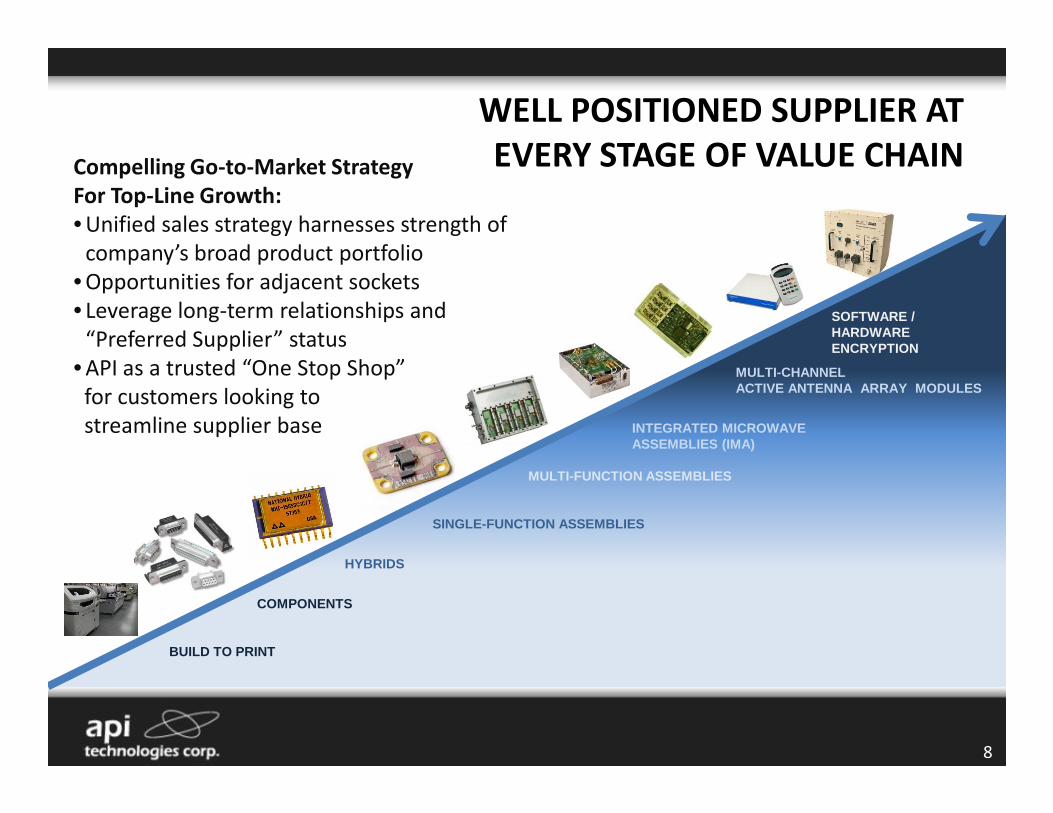

WELL POSITIONED SUPPLIER AT

EVERY STAGE OF VALUE CHAINCompelling Go-to-Market Strategy

For Top-Line Growth:

• Unified sales strategy harnesses strength of

company’s broad product portfolio

• Opportunities for adjacent sockets

• Leverage long-term relationships and

“Preferred Supplier” status

• API as a trusted “One Stop Shop”

for customers looking to MULTI-CHANNEL ACTIVE ANTENNA ARRAY MODULES

SOFTWARE / HARDWARE ENCRYPTION

8

for customers looking to

streamline supplier base

BUILD TO PRINT

COMPONENTS

HYBRIDS

SINGLE-FUNCTION ASSEMBLIES

MULTI-FUNCTION ASSEMBLIES

INTEGRATED MICROWAVE ASSEMBLIES (IMA)

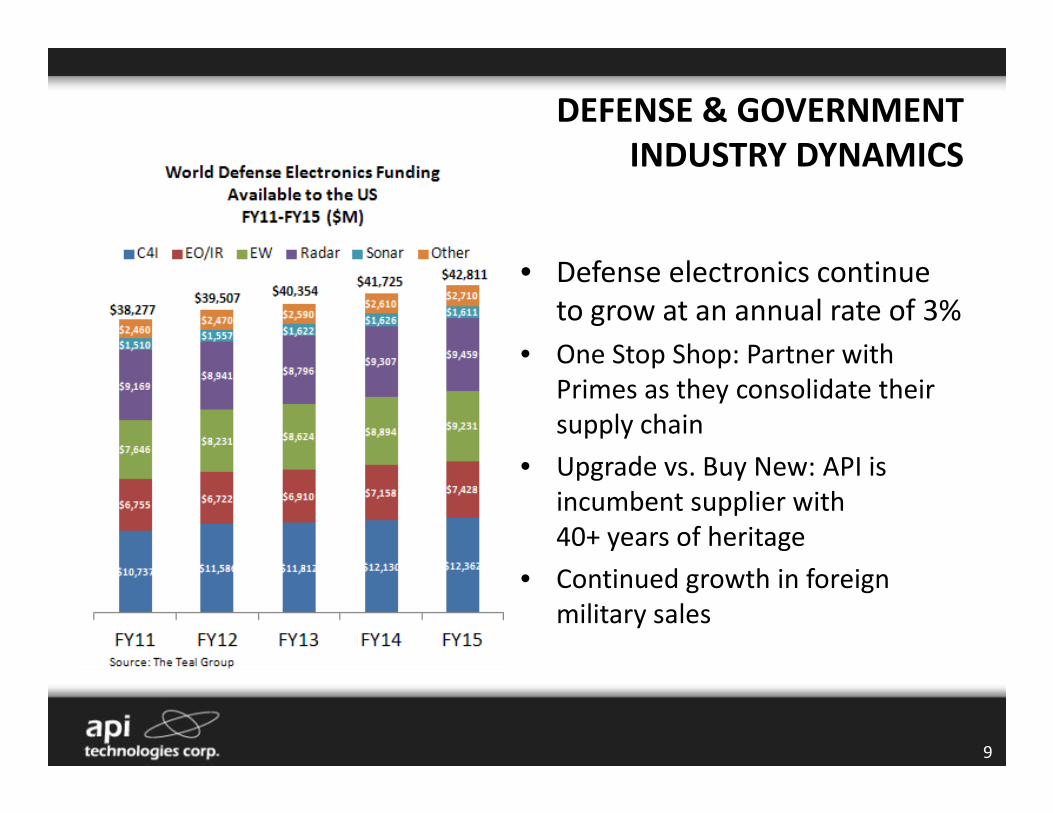

• Defense electronics continue

to grow at an annual rate of 3%

• One Stop Shop: Partner with

Primes as they consolidate their

supply chain

DEFENSE & GOVERNMENT

INDUSTRY DYNAMICS

supply chain

• Upgrade vs. Buy New: API is

incumbent supplier with

40+ years of heritage

• Continued growth in foreign

military sales

9

COMMERCIAL MARKET

INDUSTRY DYNAMICS

• Focus on high-reliability applications

• Non-defense niche applications aligned with growth markets

Key supplier to all major commercial airline

platforms

10

Commercial Aerospace

platforms

Sole/primary source supplier for medical and

industrial products and platformsMedical & Industrial

Expanding presence in energy markets

(oil and gas, alternative energy)

Energy

27.6%

7.6%

6.9%6.8%

3.7%1.9%%

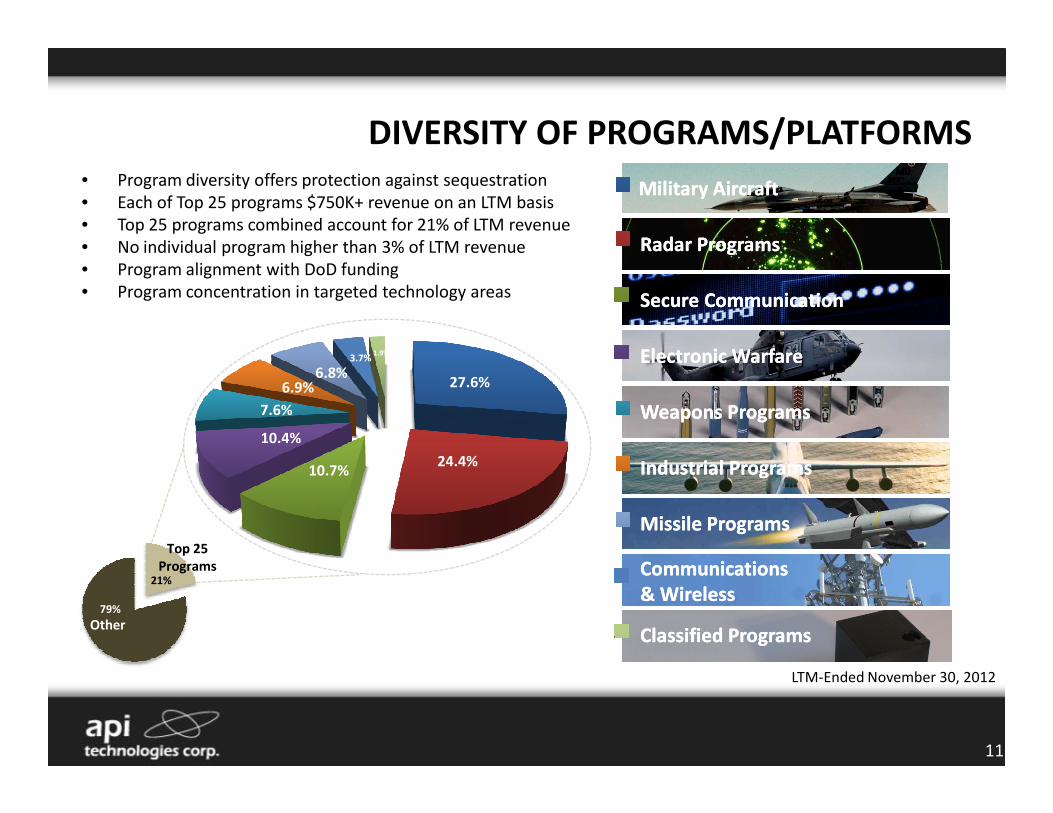

DIVERSITY OF PROGRAMS/PLATFORMS • Program diversity offers protection against sequestration

• Each of Top 25 programs $750K+ revenue on an LTM basis

• Top 25 programs combined account for 21% of LTM revenue

• No individual program higher than 3% of LTM revenue

• Program alignment with DoD funding

• Program concentration in targeted technology areas Secure CommunicationSecure Communication

Military AircraftMilitary Aircraft

Radar ProgramsRadar Programs

Electronic WarfareElectronic Warfare

Weapons ProgramsWeapons Programs

24.4%10.7%

10.4%

7.6%

LTM-Ended November 30, 2012

11

Missile ProgramsMissile Programs

Industrial ProgramsIndustrial Programs

Weapons ProgramsWeapons Programs

CommunicationsCommunications

& Wireless& Wireless

Classified ProgramsClassified ProgramsOther

21%

79%

Top 25

Programs

Other

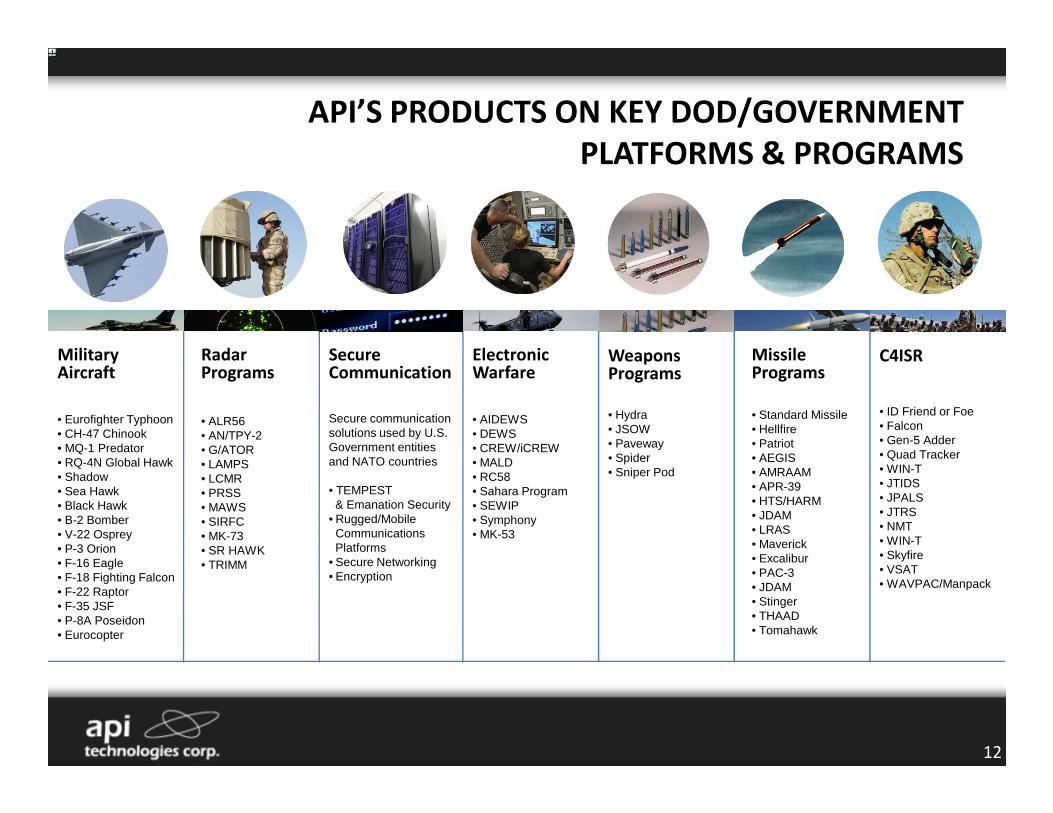

API’S PRODUCTS ON KEY DOD/GOVERNMENT

PLATFORMS & PROGRAMS

Secure Communication

Missile Programs

Military Aircraft

C4ISR

• ID Friend or Foe

RadarPrograms

ElectronicWarfare

WeaponsPrograms

12

Secure communication solutions used by U.S. Government entities and NATO countries

• TEMPEST& Emanation Security

• Rugged/Mobile CommunicationsPlatforms

• Secure Networking• Encryption

• Standard Missile• Hellfire• Patriot• AEGIS• AMRAAM• APR-39• HTS/HARM• JDAM• LRAS• Maverick• Excalibur• PAC-3• JDAM• Stinger• THAAD• Tomahawk

• Eurofighter Typhoon• CH-47 Chinook• MQ-1 Predator • RQ-4N Global Hawk• Shadow• Sea Hawk• Black Hawk• B-2 Bomber• V-22 Osprey• P-3 Orion• F-16 Eagle• F-18 Fighting Falcon• F-22 Raptor• F-35 JSF• P-8A Poseidon• Eurocopter

• ID Friend or Foe• Falcon• Gen-5 Adder• Quad Tracker• WIN-T• JTIDS• JPALS• JTRS• NMT• WIN-T• Skyfire• VSAT• WAVPAC/Manpack

• ALR56• AN/TPY-2• G/ATOR• LAMPS• LCMR• PRSS• MAWS• SIRFC• MK-73• SR HAWK• TRIMM

• AIDEWS• DEWS• CREW/iCREW• MALD• RC58• Sahara Program• SEWIP• Symphony• MK-53

• Hydra• JSOW• Paveway• Spider• Sniper Pod

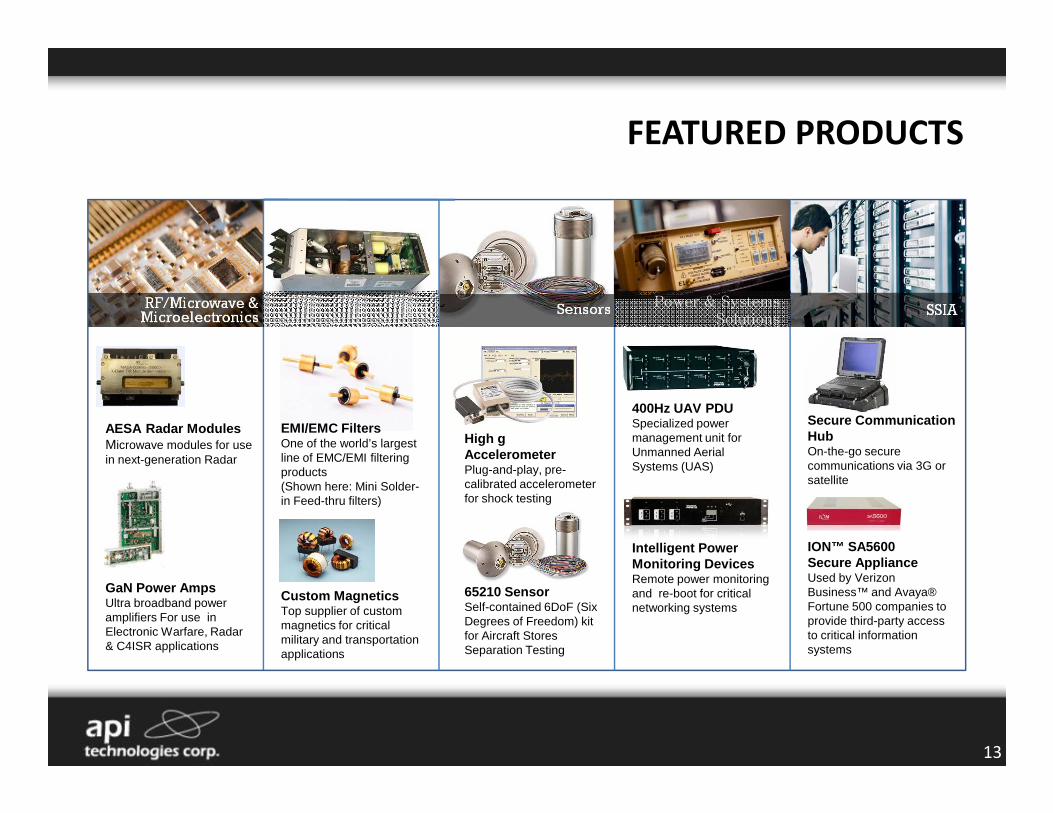

FEATURED PRODUCTS

400Hz UAV PDU

EISPower & Systems

Solutions

13

ION™ SA5600Secure ApplianceUsed by Verizon Business™ and Avaya® Fortune 500 companies to provide third-party access to critical information systems

Secure Communication HubOn-the-go secure communications via 3G or satellite

Intelligent Power Monitoring DevicesRemote power monitoring and re-boot for critical networking systems

400Hz UAV PDUSpecialized power management unit for Unmanned Aerial Systems (UAS)

High gAccelerometerPlug-and-play, pre-calibrated accelerometer for shock testing

65210 SensorSelf-contained 6DoF (Six Degrees of Freedom) kit for Aircraft Stores Separation Testing

EMI/EMC FiltersOne of the world’s largest line of EMC/EMI filtering products(Shown here: Mini Solder-in Feed-thru filters)

Custom MagneticsTop supplier of custom magnetics for critical military and transportation applications

GaN Power AmpsUltra broadband power amplifiers For use in Electronic Warfare, Radar & C4ISR applications

AESA Radar ModulesMicrowave modules for use in next-generation Radar

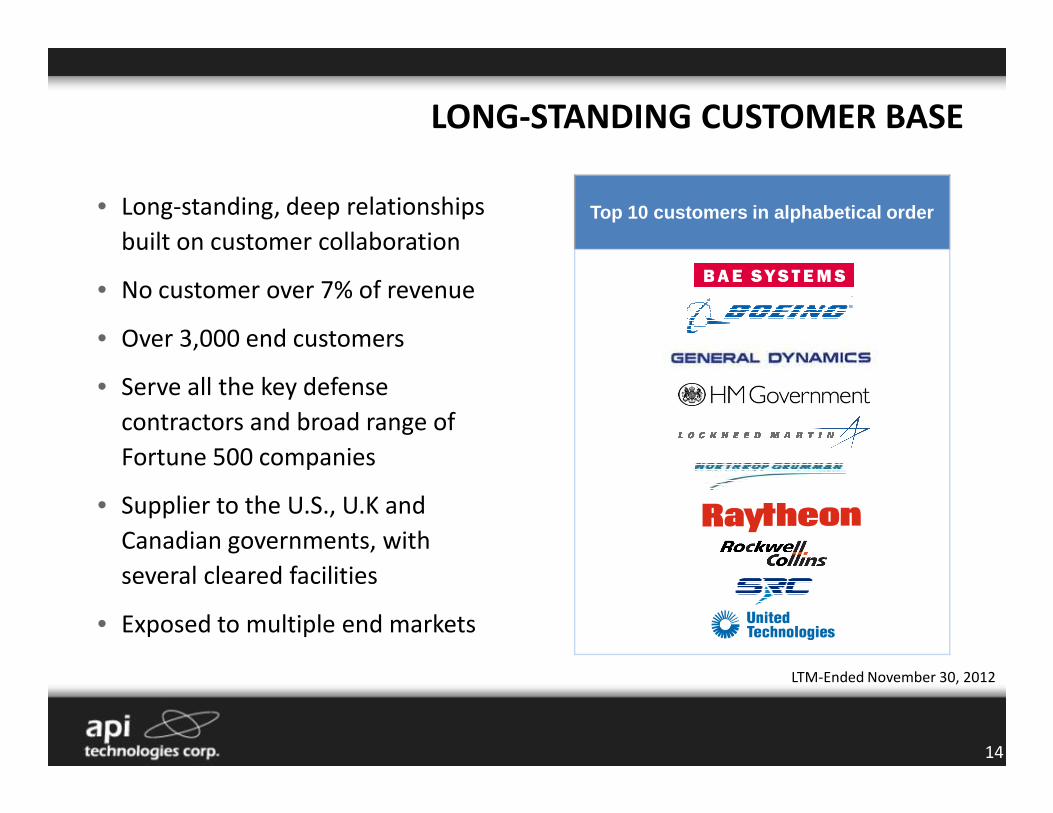

LONG-STANDING CUSTOMER BASE

• Long-standing, deep relationships

built on customer collaboration

• No customer over 7% of revenue

• Over 3,000 end customers

• Serve all the key defense

contractors and broad range of

Top 10 customers in alphabetical order

contractors and broad range of

Fortune 500 companies

• Supplier to the U.S., U.K and

Canadian governments, with

several cleared facilities

• Exposed to multiple end markets

14

LTM-Ended November 30, 2012

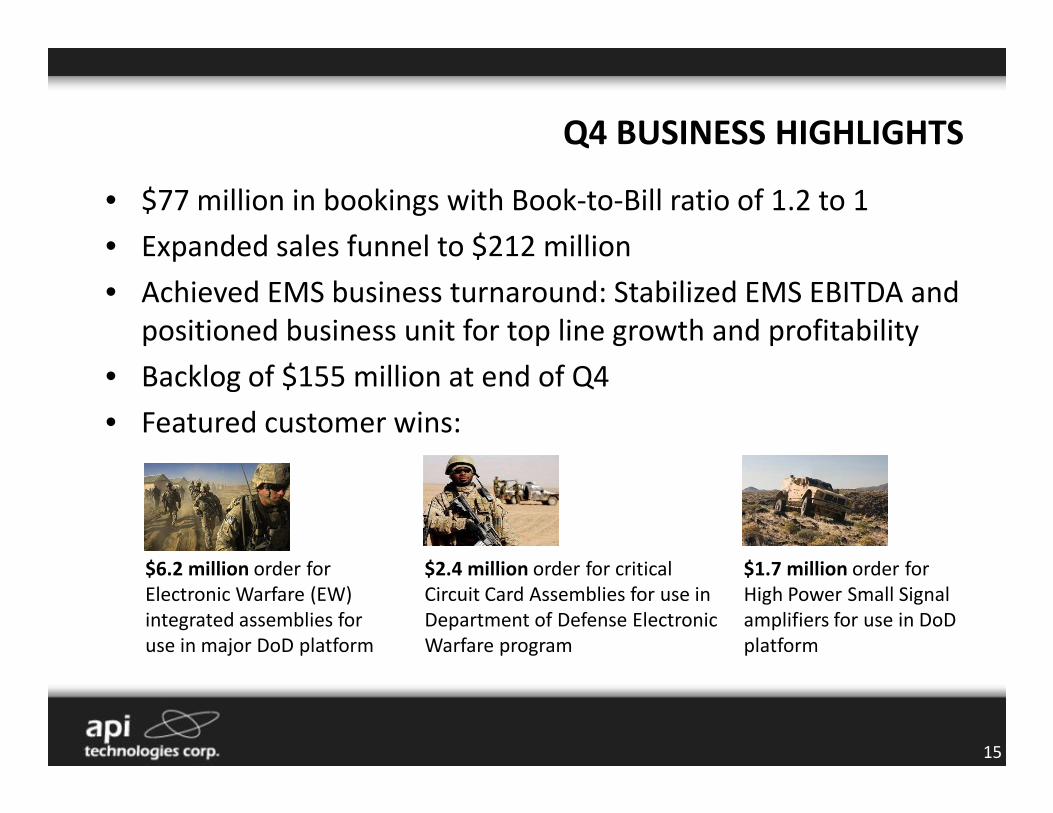

• $77 million in bookings with Book-to-Bill ratio of 1.2 to 1

• Expanded sales funnel to $212 million

• Achieved EMS business turnaround: Stabilized EMS EBITDA and

positioned business unit for top line growth and profitability

• Backlog of $155 million at end of Q4

• Featured customer wins:

Q4 BUSINESS HIGHLIGHTS

• Featured customer wins:

15

$6.2 million order for

Electronic Warfare (EW)

integrated assemblies for

use in major DoD platform

$1.7 million order for

High Power Small Signal

amplifiers for use in DoD

platform

$2.4 million order for critical

Circuit Card Assemblies for use in

Department of Defense Electronic

Warfare program

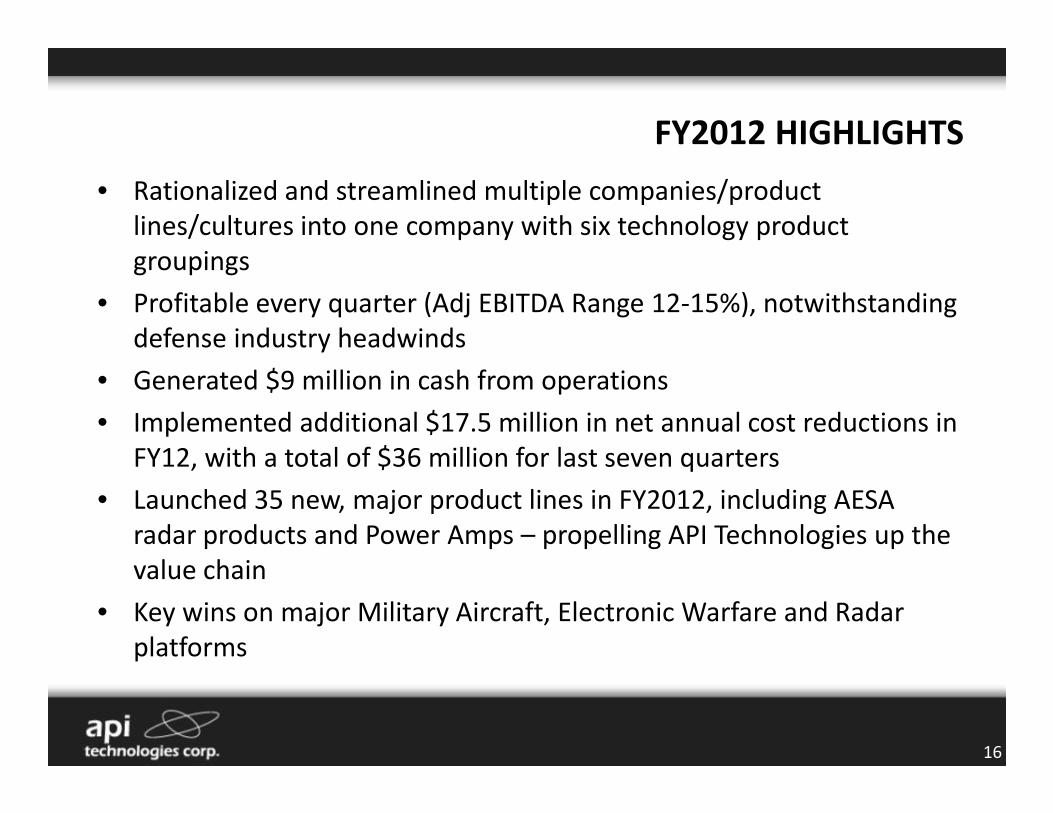

• Rationalized and streamlined multiple companies/product

lines/cultures into one company with six technology product

groupings

• Profitable every quarter (Adj EBITDA Range 12-15%), notwithstanding

defense industry headwinds

• Generated $9 million in cash from operations

• Implemented additional $17.5 million in net annual cost reductions in

FY2012 HIGHLIGHTS

• Implemented additional $17.5 million in net annual cost reductions in

FY12, with a total of $36 million for last seven quarters

• Launched 35 new, major product lines in FY2012, including AESA

radar products and Power Amps – propelling API Technologies up the

value chain

• Key wins on major Military Aircraft, Electronic Warfare and Radar

platforms

16

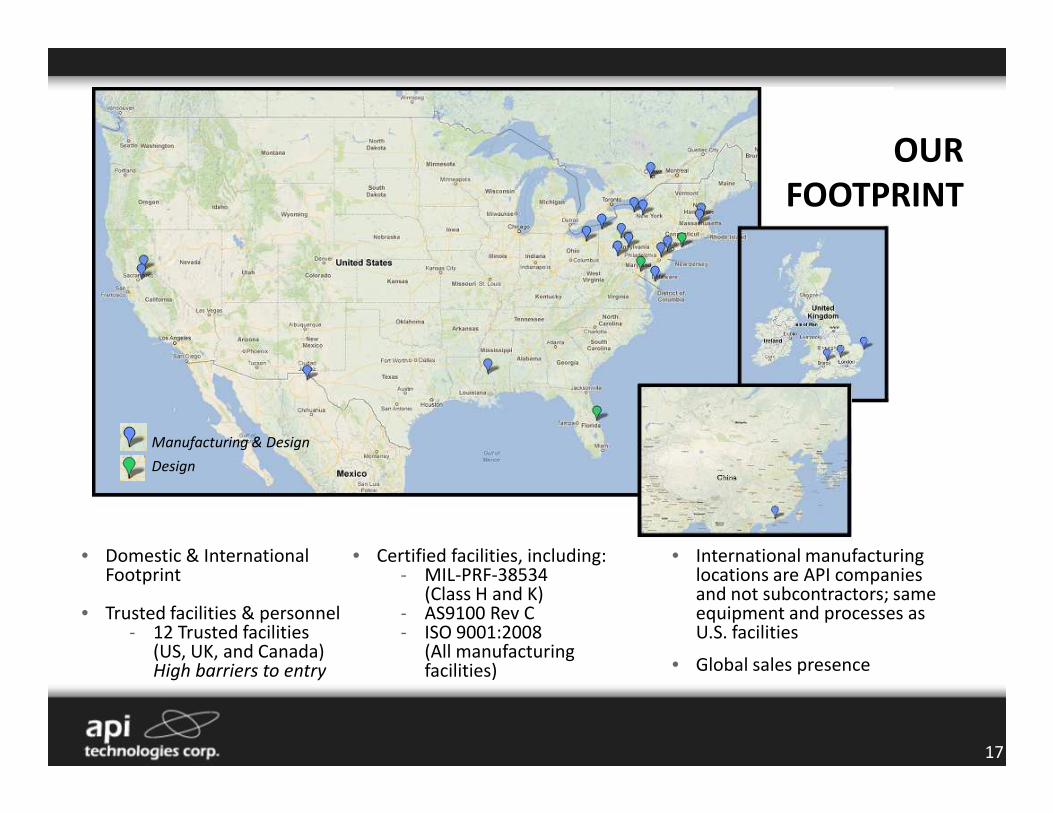

OUR

FOOTPRINT

• Certified facilities, including:- MIL-PRF-38534

(Class H and K)- AS9100 Rev C- ISO 9001:2008

(All manufacturing facilities)

17

Manufacturing & Design

Design

• Domestic & International Footprint

• Trusted facilities & personnel- 12 Trusted facilities

(US, UK, and Canada) High barriers to entry

• International manufacturing locations are API companies and not subcontractors; same equipment and processes as U.S. facilities

• Global sales presence

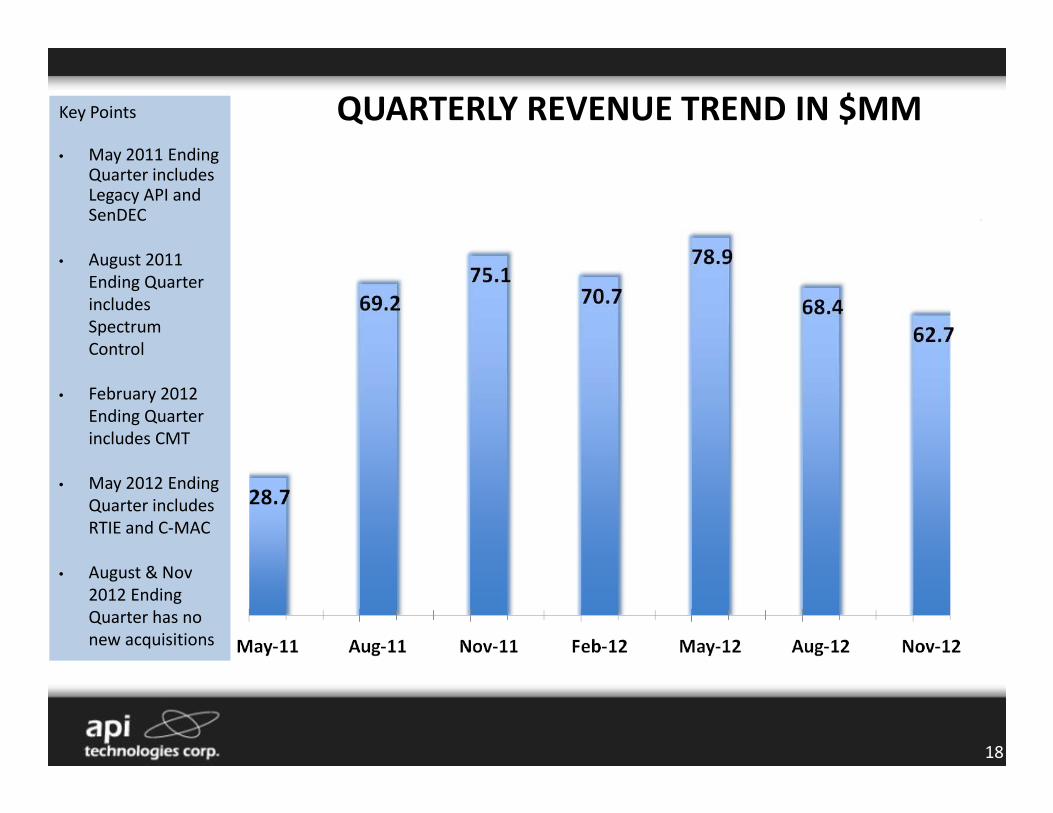

QUARTERLY REVENUE TREND IN $MMKey Points

• May 2011 Ending Quarter includes Legacy API and SenDEC

• August 2011

Ending Quarter

includes

Spectrum

Control

• February 2012

Ending Quarter

18

Ending Quarter

includes CMT

• May 2012 Ending

Quarter includes

RTIE and C-MAC

• August & Nov

2012 Ending

Quarter has no

new acquisitions

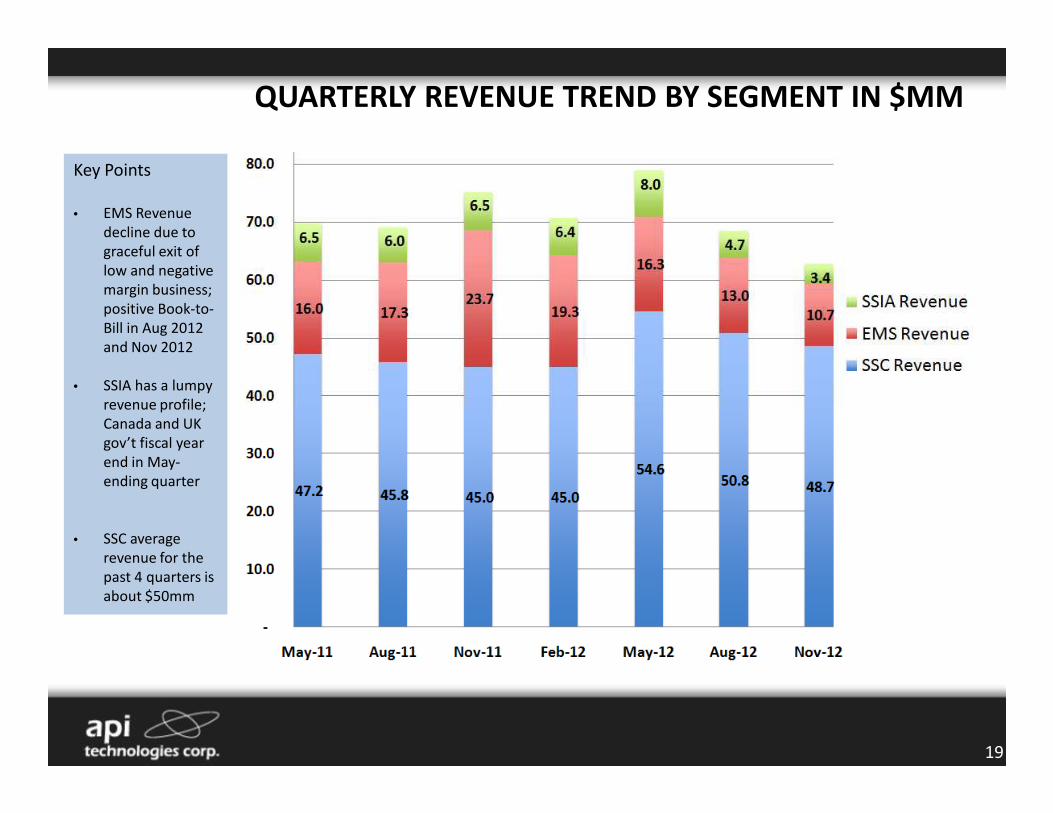

QUARTERLY REVENUE TREND BY SEGMENT IN $MM

Key Points

• EMS Revenue

decline due to

graceful exit of

low and negative

margin business;

positive Book-to-

Bill in Aug 2012

and Nov 2012

• SSIA has a lumpy

revenue profile;

19

revenue profile;

Canada and UK

gov’t fiscal year

end in May-

ending quarter

• SSC average

revenue for the

past 4 quarters is

about $50mm

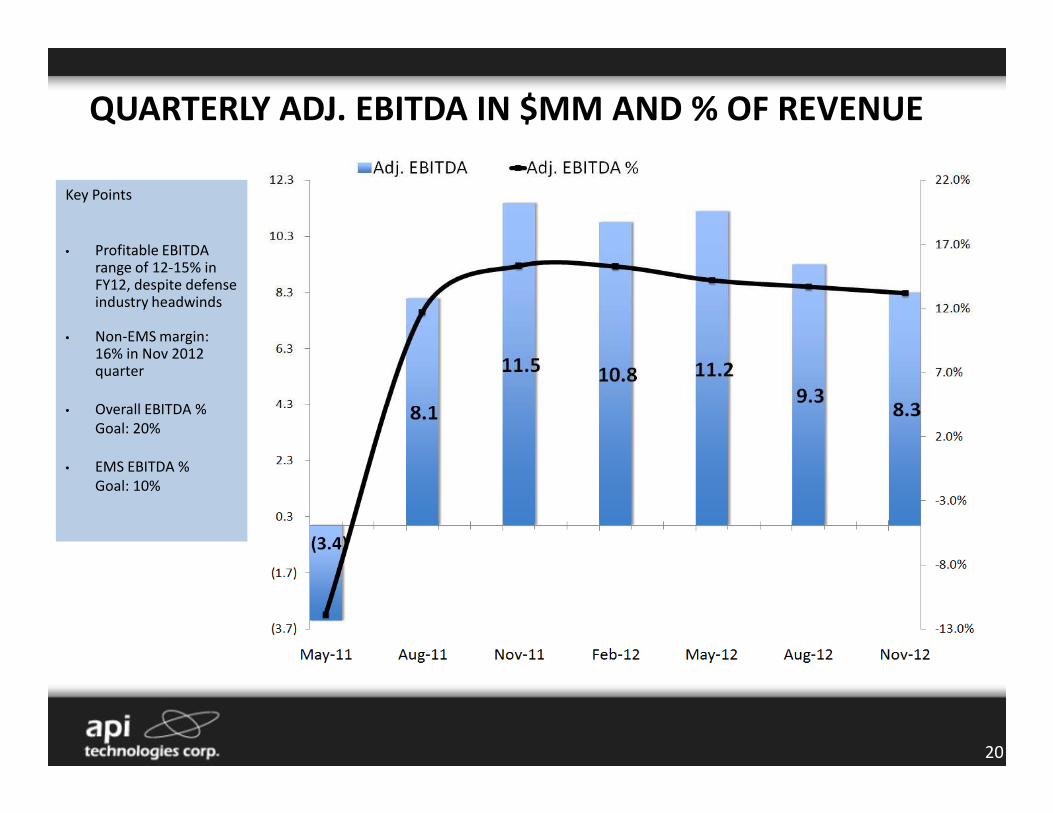

QUARTERLY ADJ. EBITDA IN $MM AND % OF REVENUE

Key Points

• Profitable EBITDA range of 12-15% in FY12, despite defense industry headwinds

• Non-EMS margin: 16% in Nov 2012 quarter

• Overall EBITDA %

20

• Overall EBITDA %

Goal: 20%

• EMS EBITDA %

Goal: 10%

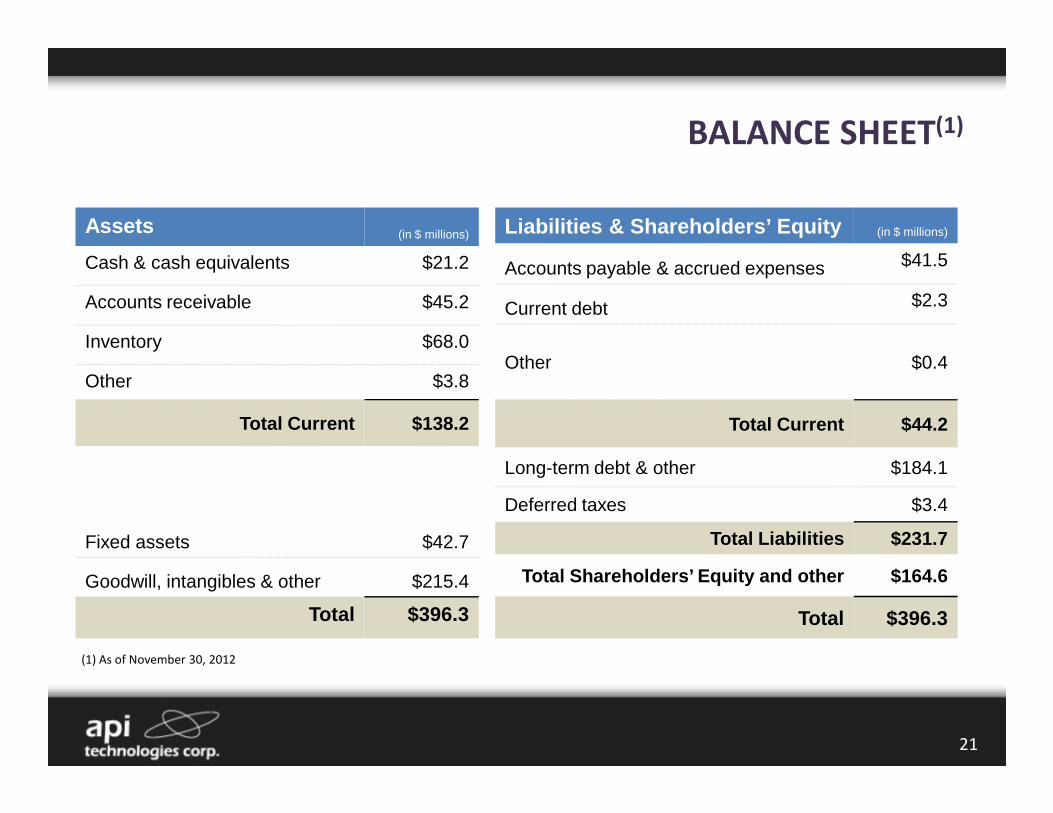

BALANCE SHEET(1)

Assets (in $ millions)

Cash & cash equivalents $21.2

Accounts receivable $45.2

Inventory $68.0

Other $3.8

Liabilities & Shareholders’ Equity (in $ millions)

Accounts payable & accrued expenses $41.5

Current debt $2.3

Other $0.4

Total Current $138.2

Fixed assets $42.7

Goodwill, intangibles & other $215.4

Total $396.3

Total Current $44.2

Long-term debt & other $184.1

Deferred taxes $3.4

Total Liabilities $231.7

Total Shareholders’ Equity and other $164.6

Total $396.3

(1) As of November 30, 2012

21

COMPANY LEADERSHIP

BEL LAZAR, President & Chief Executive Officer

• Over 25 years of experience in the defense, semiconductor and technology sectors

• Most recently served as the Senior Vice President of Operations at Microsemi Corporation

• Previously spent over 22 years at International Rectifier (NYSE: IRF) in expanding leadership and

general management roles, culminating as Vice President of the Company’s Aerospace &

Defense business unit

• Has completed over 12 acquisitions and over 25 consolidations within the Aerospace & Defense

electronics sectorelectronics sector

22

PHIL REHKEMPER, Executive Vice President & Chief Financial Officer• Joined API in April 2012• Brings to API more than 25 years of financial and strategic planning experience• Previously served as Vice President of Finance for International Rectifier (NYSE: IRF) and Chief

Financial Officer and Vice President of Finance for Alliance Fiber Optic Products

• Dominant RF/microwave, microelectronics, and

security technology provider in defense and

commercial high-reliability markets

– 90%+ sole/primary source with recurring revenue streams

– Broad portfolio of highly engineered technology products

INVESTMENT HIGHLIGHTS

– Alignment with growth areas of the Defense budget and

within high-reliability industrial markets

• Focus on revenue generation and profitability

– Target of 20% Adjusted EBITDA company wide

– Demonstrated ability to generate cash

23

ADDITIONAL SLIDES

24

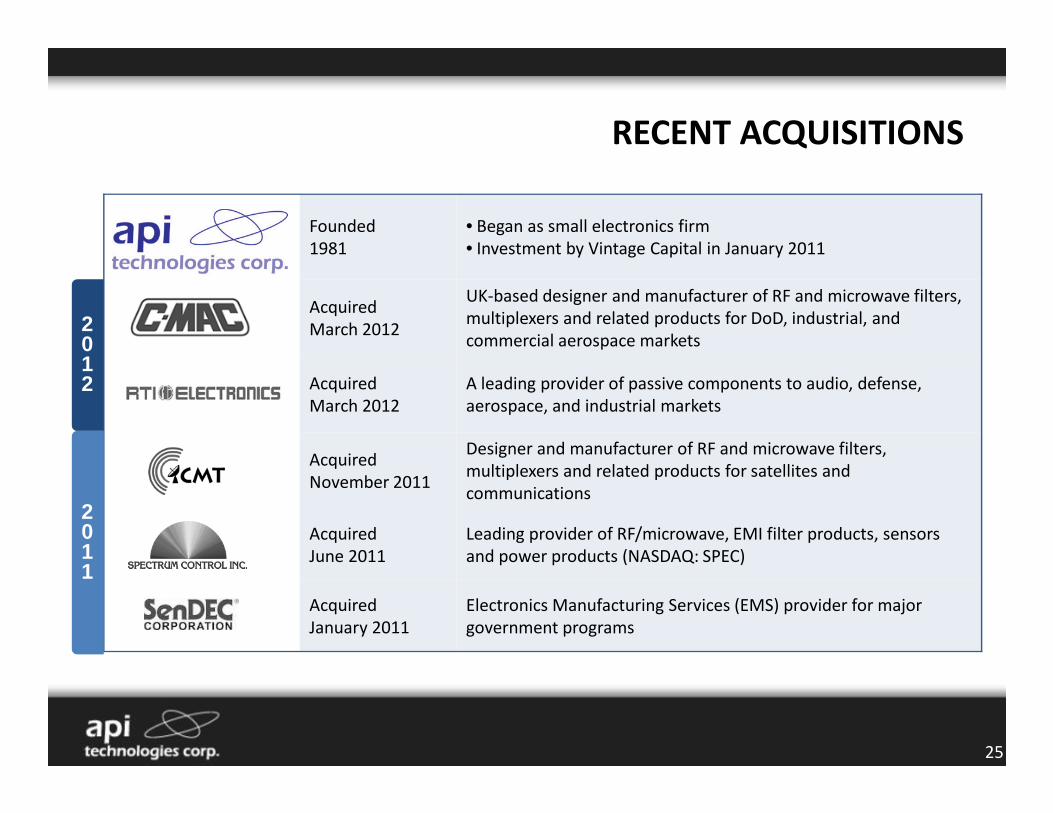

RECENT ACQUISITIONS

Founded

1981

• Began as small electronics firm

• Investment by Vintage Capital in January 2011

Acquired

March 2012

UK-based designer and manufacturer of RF and microwave filters,

multiplexers and related products for DoD, industrial, and

commercial aerospace markets

Acquired

March 2012

A leading provider of passive components to audio, defense,

aerospace, and industrial markets

2012

25

March 2012 aerospace, and industrial markets

Acquired

November 2011

Designer and manufacturer of RF and microwave filters,

multiplexers and related products for satellites and

communications

Acquired

June 2011

Leading provider of RF/microwave, EMI filter products, sensors

and power products (NASDAQ: SPEC)

Acquired

January 2011

Electronics Manufacturing Services (EMS) provider for major

government programs

2011