Embed Size (px)

Citation preview

© Reacfin 2019Reacfin’s Seasonal Breakfast – Nov.2019

Managing insurance companies in periods of recession

A discussion panel animated by F. Vangheluwe, Pr. F. Ducuroir, S. Mahy, J. Antunes Mendes & Dr. A. Lebègue

Brussels – 26 Nov. 2019

Please read the important disclaimer at the end of this presentation

IMPORTANT : This presentation is only the supporting document of an oral presentation. It is not intended to be exhaustive. Quoting or using this document on its own might be misleading. Furthermore, although the authors have been careful in the selection of their sources and assumptions, the authors cannot guarantee that all information in the document are exact or correct. As a result, these materials may not be used by anybody except their authors nor should they be relied upon in any way for any purpose other than as contemplated by a written agreement with Reacfin.

© Reacfin 2019Reacfin’s Seasonal Breakfast – Nov.2019

2

Welcome

Today’s discussion panel

Fréderic VangheluweIndependent expert

Management consultant

François DucuroirManaging Partner

Guest professor at UCLouvain

Samuel MahyDirector – Head of Non-Life Insurance

Certified actuary

Julien Antunes MendesManager – Life Insurance

Certified actuary

Adrien LebègueManager – Head of Risk & Finance

Certified actuary & PhD

© Reacfin 2019Reacfin’s Seasonal Breakfast – Nov.2019

3

Agenda

• Lessons from the 2007-2009 Great Recession

• Should we really fear a recession impacting European Insurances?

• Impact of recession on insurance companies

o Life

o Non-Life

o Investments, ALM and finance

• Case study

• Getting prepared to mitigating the adverse impacts of a recession

• Q&A and Contact details

© Reacfin 2019Reacfin’s Seasonal Breakfast – Nov.2019

4

Lessons from the 2007-2009 Great Recession

• 30 to 40 Mn people lost their jobs.

• About 10% of the US population lost their home.

• Dow Jones lost more than 50% in a few months.

• In the US, 20 Tn USD in assets value evaporated between 2007 and 2012 (stocks, real estate).

• UK lost 50% of its GDP in wealth over 18 months.

What happened some 10 years ago?

#of foreclosures in the US

Sources: Federal Reserve of NY, ECB, economicshelp.org

Unemployment rate in the US, UK and the Eurozone%

© Reacfin 2019Reacfin’s Seasonal Breakfast – Nov.2019

5

Lessons from the 2007-2009 Great Recession

A compounding combination of factors related to

– Liquidity Management

– US Mortgage market

– Regulations

– Financial innovations

– Globalization

– Systemic pro-cyclicality

– Moral Hazard

– Governance & governmental responses

– Risk Management

How was it possible?

© Reacfin 2019Reacfin’s Seasonal Breakfast – Nov.2019

6

Lessons from the 2007-2009 Great Recession

Diagnostic

– Did the system fail or did it actually work?

– Private or public?

– What about the next one?

Financial institutions need to

Develop a systematic “system vision”

Enable a “prospective vision”: plan contingent measures!

Embed a Risk culture: Train ! Train ! Train !

Key lessons learned

Don’t get fooled by numbersBlack swans do exist

© Reacfin 2019Reacfin’s Seasonal Breakfast – Nov.2019

7

Agenda

• Lessons from the 2007-2009 Great Recession

• Should we really fear a recession impacting European Insurances?

• Impact of recession on insurance companies

o Life

o Non-Life

o Investments, ALM and finance

• Case study

• Getting prepared to mitigating the adverse impacts of a recession

• Q&A and Contact details

© Reacfin 2019Reacfin’s Seasonal Breakfast – Nov.2019

8

Signs of a recession?

• Economic contraction (i.e. reduced economic activity) for a material period

• Typical metric: Decrease in GDP for 2 consecutive quarters or more

Rationale for a recession

Definition

Fundamental threats

• Global trade restrictions (e.g. US – Chine; US – EU, etc.) & economies suffering (e.g. GE)

• Upcoming regional barriers to free trade (e.g. Brexit)

• Credit & liquidity bubble as a result of low rates environment

• Persistent risks of economic instability in Europe (e.g. Italy, Greece)

Early warning indicator

• One of the most empirically accurate predictors of U.S recessions : inversion of the government bond yield curve

• Illustration: 3 Months vs. 10 Years US sovereign yields

Sources: Federal Reserve of NY

© Reacfin 2019Reacfin’s Seasonal Breakfast – Nov.2019

9

Signs of a recession?

Additional indicators

Sources: NY Fed, Baker, Bloom & Davis (Policyuncertainty.com)

• “Things in Europe appear to be much more bleak, and the odds for a recession there are much higher. Europe's export-reliant economies are at the center of trade and slowdown worries.“ Anneken Tappe, CNN Business, 19-Oct.2019

• “Key parts of the European economy are struggling – Germany, Italy and the U.K. amongst them – making renewed monetary easing and restarted QE unavoidable.“ Paul F. Gruenwald, S&P Global Ratings, 1-Oct.2019

• “Low interest rates fuel financial risk-taking by institutional investors such as European Insurers and pension fund. These exposures may act as an amplifier of shocks in case of recession” IMF, Presentation of the Global Financial Stability Report,

16-Oct-2019

European insurers could

be particularly impacted

NY Fed’s Recession Probability index European Economic Policy Uncertainty indices

Baker, Bloom & Davis “European Policy Uncertainty” IndexBased on # of press articles discussing Economic uncertainty

Purchasing Managers Indices

Standard & Poor’s Global Economics

DM = Developed markets; EM = Emerging Markets

© Reacfin 2019Reacfin’s Seasonal Breakfast – Nov.2019

10

Signs of a recession?

Some other signals are more mitigated

• Most European GDP’s are still growing and seem to recover from the “dip” observed in Q2 2019 (incl. some feared to be “at threat” ; e.g. U.K.)

• Markets’ worries w.r.t. some specific European economies seem to reduce (e.g. evolution of Italian and Greek CDS Spreads)

Sources: Office for Nationale Statistics (UK) www.ons.gov.uk, www.worldgovernmentbonds.com

• Central Bankers Quotes

o “With appropriate monetary policy, I don’t see any evidence right now that recession risks are elevated” Richard Clarida, Federal Reserve Vice

Chairman, 19-Oct-2019

o “We do not foresee the euro zone entering into recession but rather the bloc experiencing lower economic growth for a longer period. ” Luis de Guindos, Vice-President of the ECB, 4-Oct-2019

Italy’s 5y-CDS Spread

Greece’s 5y-CDS Spread

UK GDP Growth

© Reacfin 2019Reacfin’s Seasonal Breakfast – Nov.2019

11

Signs of a recession?

We may still have some time to prepare

Elevated Ratio of High-Yield Downgrades per Upgrade Preceded the recent recessions of 1990-1991 and 2001

Sources: Moody’s Analytics, “Next Recession May Lower 10-year Treasury Yield to Range of 0.5% to 1%”, Oct.3 2019

• During the Great Recession of 2007-2009, High-Yield downgrades however proved to be simultaneous with the economic contraction.

© Reacfin 2019Reacfin’s Seasonal Breakfast – Nov.2019

12

Agenda

• Lessons from the 2007-2009 Great Recession

• Should we really fear a recession impacting European Insurances?

• Impact of recession on insurance companies

o Life

o Non-Life

o Investments, ALM and finance

• Case study

• Getting prepared to mitigating the adverse impacts of a recession

• Q&A and Contact details

© Reacfin 2019Reacfin’s Seasonal Breakfast – Nov.2019

13

Impact of recession on insurance companies

Life insurance: Premiums & lapses

Sources: https://www.fanews.co.za/article/life-insurance/9/general/1202/looming-recession-will-impact-life-insurance-industry/3858

• Less premiums income

– New business sales will decrease, further affecting life insurance company profits

– Especially dropping sales of unit-linkedproducts as policyholders shun investment risk

– Due to unemployment, less group insurance income than expected

• Increase of lapses

– Liquidity issue: disposable income becomes a scarce commodity (due to increased unemployment, long-term diseases…) and insurance premiums are among the first items to face the ‘axe’ from household budgets

– Will lead to increased operating costs, potential need to increase operating staff negative impact on financial results

Illustrative case of a Belgian insurance company

© Reacfin 2019Reacfin’s Seasonal Breakfast – Nov.2019

14

Impact of recession on insurance companies

Health and pension

• Health: Increased disability claims

– Increased back and psychology claims showing a direct correlation to economic prosperity

– More fraudulent claims (at a moment where cost-cutting efforts may reducing the companies’ ability to detect and manage it)

• Pension & group insurances (Employee Benefits): Assets deteriorating

– For DB/DC group insurance contracts, legal guaranteed rate could be supported by sponsor causing however increased difficulty for the sponsor (pro-cyclical effect) & reputational risk for the insurer

– Less margin on Unit-Linked products because of lower fees taken on the value of the fund

Sources: https://www.fanews.co.za/article/life-insurance/9/general/1202/looming-recession-will-impact-life-insurance-industry/3858http://insurancethoughtleadership.com/how-life-insurers-prepare-for-recession/

© Reacfin 2019Reacfin’s Seasonal Breakfast – Nov.2019

15

Impact of recession on insurance companies

Non-Life: Impact on claims in P&C insurances

Driving cost of claims

upwards

• Fraud: increasing of the frequency and/or the severity of claims

– Increase in the number of fraudster/fraudulous claims

– Increase in the amounts falsely claimed

• Theft frequency increase

– Burglary tends to increase

– Car theft tend to increase

UK P&C fraud during the great recession

• Crisis lead to 30% rise in false claims

• Fraud claims reaching a level of 4% by value of the total general insurance claims amount of 2008

Source: ABI* Study 2009

Driving cost of claims Down-wards

• Some claims tend to decrease in line with economic activity.

– Eg. people drive less and the number of accidents in the construction and manufacturing sectors decline.

(*) Association of British insurers – source:https://www.telegraph.co.uk/finance/recession/5166522/Recession-sparks-rise-in-insurance-fraud.html

To limit the risk of increasing claims activity, attention should be paid in both development and settlement pattern

Workforce reductions in claims handling departments may prove counterproductive.

source: Insurance Europe

source: Insurance Europe

source: FBI - https://ucr.fbi.gov/

© Reacfin 2019Reacfin’s Seasonal Breakfast – Nov.2019

16

Impact of recession on insurance companies

• Insurance are private consumption contracts, so demand for non-compulsory P&C insurance is set to contract during recession as a result of slower economic activity (e.g. Damage motor insurances) .

• Reduced activity in Real Estate/construction depresses the engineering and property lines of business.

• Transport and credit insurers are negatively impacted by diminution of international trade.

Non-Life: Impact of a recession on revenues

Driving Revenue Down-wards

Sup-porting

revenues

• The effect of a recession on non-life insurance revenues varies materially for the different types of contracts.

• In most European jurisdictions, a set of insurance contracts are either legally compulsory (e.g. Third-Party Liability Motor insurance, Fire/property insurances, workers’ compensation, etc.) either contractually compulsory (e.g. Mortgages Outstanding balance insurance).

• Revenues related to such types of contracts will prove materially less impacted (if at all) by recession.

© Reacfin 2019Reacfin’s Seasonal Breakfast – Nov.2019

17

Impact of recession on insurance companies

Impact on reinsurers

• Increased probability of default (i.e. likelihood to downgrade) could increase insurers SCR(Default-Counterparty)

– Reinsurers increasingly rely on Cat-bonds market which could prove less accessible in times of recession

– However, reinsurers are currently well capitalized but make and increasing use of Hybrid Capital

Sources: S&P «Global Reinusrance Highlight 2011» & Aon «Reinsurance Market Outlook 2019»

Assessing the possible impact of reinsurers downgrades / defaults on

capital requirements

• Except for specialized “mono-liners”*, many reinsurers resisted relatively well the Great Recession yet some large diversified players were affected (e.g. Swiss Re, cut from AA- to A+ on 19-Feb-09)

(*) e.g. Channel Re cut from Aa3 to Baa1 on 4-Aug-2008 as largest client was monoliner bond-insurer MBIA

Evolution of Reinsurers

ratings during the Great Recession

Global reinsurer

capital

Catastrophe bond issuance

© Reacfin 2019Reacfin’s Seasonal Breakfast – Nov.2019

18

Impact of recession on insurance companies

Liquidity dry-up:

• Even the most liquid assets may suddenly see sudden sharp widening of their Bid-Ask spreads

• More bespoke instruments may virtually halt trading (e.g. CDO’s and other structured products during the great recession).

• (Non-cleared) derivatives may temporarily halt trading

Investments drivers

Bid-Ask spreads on US treasury bonds

Maturities:

source: Federal Reserve Bank of New-York

Credit spreads and Real Estate & Equity Markets:

• (Lower rated) spreads hikes on the fear of increasing PDs (however best rated liquid paper may act as safe haven)

• Increasing downgrades

• Increase in PD’s may trigger concurrent increases in LGDs (in particular for low rated paper – relation was more obvious in the past)

• Material drops in Real Estate and Equity prices Source: Mark-it iBoxx indices Source: Mark-it iBoxx indices Benchmarks: • Eurostoxx50 Total Return • iShares Emerging Markets

Corporate Bonds spreads (domestic US & EUR in %)

Equities Total Return(for €100 invested)

% %

Interest rates:

• To relaunch economy, central bankers may typically be inclined to limit IR rates increases at short term

US Dealer Repo Activity(USD Bn, rolling monthly average)

source: Federal Reserve Bank of New-York

© Reacfin 2019Reacfin’s Seasonal Breakfast – Nov.2019

19

Impact of recession on insurance companies

• Increasing default rates may trigger ALM mismatches

• Derivatives overlays

– Importance of cleared IRS:

• Are all contracts in the duration / convexity overlay cleared?

• Availability of cash to meet collateral requirements

– Forward bond sales :

• Are contracts collateralized by their underlying bonds?

• Have you defined a contingency plan in case of counterparty default?

– Other derivatives (e.g. ASW, Interest Rates options, Equity derivatives, etc.)

• Collateral usually governed by OTC CSA

• What if you downgrade?

• What does your contingency plan foresees in case of counterparty defaults?

– Expected increase in P&L volatility under IFRS as Hedge Accounting of “Macro Hedges” may prove less effective under distressed market conditions

Some ALM challenges

© Reacfin 2019Reacfin’s Seasonal Breakfast – Nov.2019

20

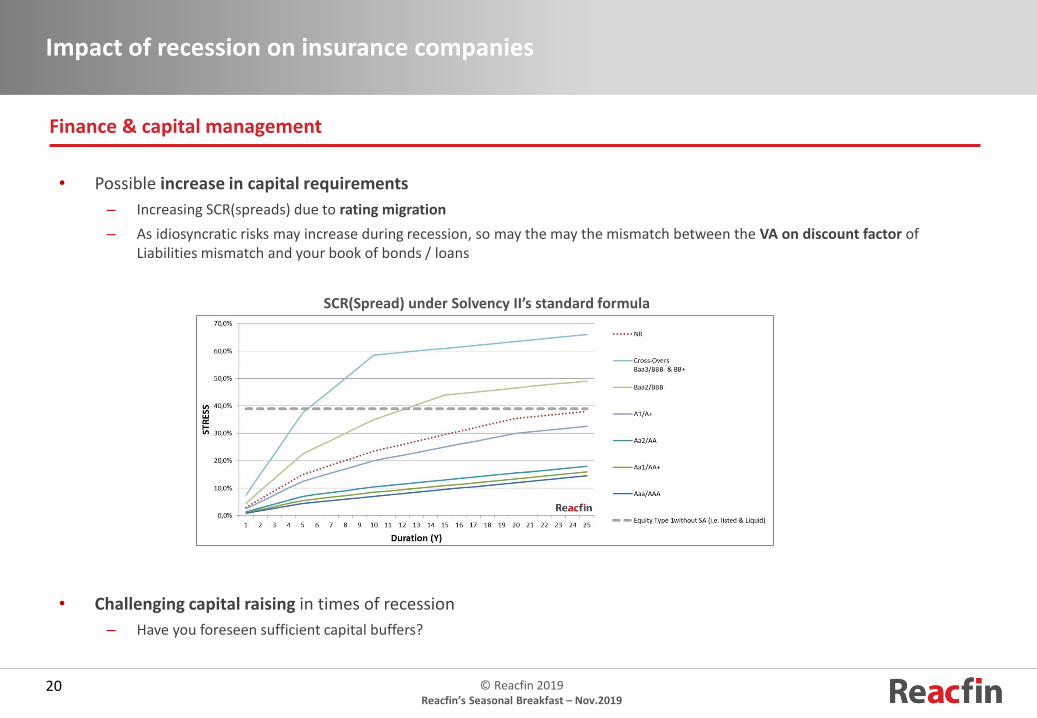

Impact of recession on insurance companies

• Possible increase in capital requirements

– Increasing SCR(spreads) due to rating migration

– As idiosyncratic risks may increase during recession, so may the may the mismatch between the VA on discount factor of Liabilities mismatch and your book of bonds / loans

• Challenging capital raising in times of recession

– Have you foreseen sufficient capital buffers?

Finance & capital management

SCR(Spread) under Solvency II’s standard formula

© Reacfin 2019Reacfin’s Seasonal Breakfast – Nov.2019

21

Agenda

• Lessons from the 2007-2009 Great Recession

• Should we really fear a recession impacting European Insurances?

• Impact of recession on insurance companies

o Life

o Non-Life

o Investments, ALM and finance

• Case study

• Getting prepared to mitigating the adverse impacts of a recession

• Q&A and Contact details

© Reacfin 2019Reacfin’s Seasonal Breakfast – Nov.2019

22

Recession Case-Study

The illustrative insurer considered

• Insurer with a total balance-sheet of EUR 10Bn* (and ~20% unrealized capital gains)

– Own funds: ~15% of total Balance-Sheet

– Liabilities (~9y average lifetime): 50% of individual life (IL) contracts, 35% of group life (GL) contracts & 15% of Non-Life (NL) contracts

– Maturing liabilities are exactly replaced by new business with New Business shifting towards Non-Life (i.e. new production: 40% IL, 35% GL, 25% NL)

– Pattern of guaranteed returns on IL & GL and schedule of claims in NL typical* of mid-sized Belgian insurer

– Dividend policy: Paying 70% of net earnings (average corporate tax rate: 20%)

– Profit sharing (25%) applying on 40% of Individual Life contracts

– ALM strategy: Duration overlay per maturity buckets using 2, 5, 10, 15, 20, 25 & 30 years swaps

(*) based on Reacfin’s experience mid-sized Belgian

All assets are EUR denominated

© Reacfin 2019Reacfin’s Seasonal Breakfast – Nov.2019

23

Recession Case-Study

Market assumptions for the Base-Case i.e. our « No Recession » scenario

(*) The higher the spreads the higher PD’s & LGD’s

• Interest rates slowly pick-up in the coming years. Over long term, 30y rates reach 3% (i.e. 1% of ECB’s inflation target).

• Sovereign bonds spreads remain relatively stable for 5 years and pick-up slowly thereafter.

• Non-Financials Corp. Bonds spreads slowly increase*. Financials structurally pay a limited additional premium, compensated by adapted* PD & LGD assumptions. Residential Mortgage & corporate Loans pay additional illiquidity premium that is larger for loans with high LGDs (i.e. unsec. Corp. Loans vs. Collat. Corp.). Note that while we don’t display them here for clarity reason, in order to model rating transitions, all « full letter ratings » are calibrated in our model

• Average Net Return of Equities and Real estate pick-up slowly over time.

• Rating transition matrices as defined by latest Moody’s cohorts

• Time structure of spreads: constant as prevailing by end Q3 2019

• PD’s and LGD’s (linear) sensitivity** to spread (as observed for historical market implied parameters)

© Reacfin 2019Reacfin’s Seasonal Breakfast – Nov.2019

24

Recession Case-Study

Evolution of our illustrative insurer under Base-Case assumptions i.e. « No Recession »

• The decrease in Fair Value balance sheet that results from effect of increasing Interest rates is compensated by the FV of Off-Balance-sheet swaps

• The company is reasonably profitable but low rate environment weights profitability of Life Business and shift towards Non-Life is slow due to long maturity profiles of Life liabilities (which they progressively partly replace).

Net Interest Incomes vs. Operating Costs Profitability: Return on Equity (in Book Value)

Results from particular pattern in liabilities cash-flows (due to real-

life proxy used)

© Reacfin 2019Reacfin’s Seasonal Breakfast – Nov.2019

25

Recession Case-Study

Evolution of our illustrative insurer under Base-Case assumptions i.e. « No Recession »

• Our illustrative insurer is well capitalize (starting our scenario with a solvency ratio of about 175%)

• Solvency ratio drops to 140% in year 5 as a result of progressively increasing business in non-life while distributing most profits through dividends

• With its 5 % allocation in cash, the company has sufficient liquidities to meet all of pay-outs and its collateral requirements on swaps

© Reacfin 2019Reacfin’s Seasonal Breakfast – Nov.2019

26

Recession Case-Study

Decomposing the effect of a recession

(*) The higher the spreads the higher PD’s & LGD’s

• In the following slides we analyze the effect of a possible recession on our illustrative insurer

1. « Instant downgrades »:

• Effect of instantaneously downgrading fixed income assets (and increasing the related PD’s)

2. « Non Life claims increases »:

o Effect of fraud and increased claims frequency (in Non-Life only)

3. « Market risks in a Recession scenario »:

o Effect of a market evolution (along a « subprime Great Recession » like scenario but materially lighter in the amplitude of shocks– about half the impact)

© Reacfin 2019Reacfin’s Seasonal Breakfast – Nov.2019

27

Recession Case-Study

Effect of an “instant downgrade”

• We assume a limited downgrading impact: 10% of the fixed income instruments get downgrade by 1 rating letter which triggers limited set of impairments: on the downgraded instruments, impairments result in a reduction of book value of in average ~20%.

• Such downgrade has 2 effects for the Solvency Ratio in T0 (which decreases by ~5% from 175% to about 170%):

– A reduction in Fair Value as downgraded assets (as we compute their discounted cash-flows considering a somewhat higher discount rate)

– An increase in SCR(Market Risks) triggered by the increase in SCR(spreads)

SCR Market

Base Case

Downgraded

-1,9%

+3,8%

© Reacfin 2019Reacfin’s Seasonal Breakfast – Nov.2019

28

Recession Case-Study

Increased fraud & claims frequency in P&C insurance combined with the “downgrading” effect

• Let us now assume that for P&C insurance the cost of sinistrality increases as a result of an increase fraud and in claims frequency (related to more cases of theft, etc.)

• We assume such impact on claims frequency remains limited (~ halving the margin before operating costs on 40% of the policies)

• We consider here the case where scenario’s for market risk drivers remain unchanged

Projected Solvency Ratio

• Our illustrative insurer remains sufficiently capitalized to conduct its activities under normal market conditions

• The 150% « Pillar 2 threshold » is breached earlier, more materially and for a longer period

© Reacfin 2019Reacfin’s Seasonal Breakfast – Nov.2019

29

Recession Case-Study

Market’s risk drivers assumptions for the Recession scenario

(*) Net of Opex, Capex, tax and vacancies

• Our scenario is inspired by the dynamics observed during the « Great Recession » crisis (between 2006 & 2013) but shocks applied are milder (~half)

• For credit instruments, the dynamics of PD’s, LGD’s and transition matrices are defined in accordance to the linear dependency observed over long term periods (2003-2015), considering previous missions data & proxies for less liquid assets

%

%

%

%

%

%

© Reacfin 2019Reacfin’s Seasonal Breakfast – Nov.2019

30

Recession Case-Study

Profitability during Recession

• We consider here the combined effect of our “Recession Scenario” for market’s risk drivers, downgrading assumptions and the assumed increase in the cost of P&C claims.

Income & costs RoE

Our illustrative insurer becomes rapidly loss making

© Reacfin 2019Reacfin’s Seasonal Breakfast – Nov.2019

31

Recession Case-Study

Evolution of own funds (FV) & Solvency Ratio during Recession

• Incurred losses come eating away own funds (in particular under Solvency II’s Fair Value measures)

• During the second half of our simulated recession, our illustrative insurer breaches its 100% Solvency Ratio (i.e. “SCR limit”) limit and by the end of crisis period it probably comes close to (or breaches) it’s MCR limit

© Reacfin 2019Reacfin’s Seasonal Breakfast – Nov.2019

32

Recession Case-Study

Possible problems with cash and collateral requirements

• As our scenario portrays a situation where future swap rates remain lower for some years (i.e. even further than the forwards implied in swap valuations), the fair value of our Off-Balance Sheet derivatives (i.e. swaps) is affected.

• Defaults of fixed income instruments further impact the expected duration match, which at time trigger the closing of additional swaps

• As a result, the collateral requirements at standard clearing houses (we use here LCH assumptions), also increase materially and quickly exceed the available cash for our insurer (including right during the crisis when liquidities have possibly become a scarce resource)

For an insurer (in particular one with much exposure to illiquid assets and few high quality repo-able bonds), the crisis could become, not only a solvency & profitability problem, but also a liquidity issue (i.e. insurers could end-up having “bankers’ problems)

© Reacfin 2019Reacfin’s Seasonal Breakfast – Nov.2019

33

Recession Case-Study

Management actions to cope with the profitability issue during the crisis

• In the case of our “unprepared” illustrative insurer, to cope with its profitability problem, the management will likely have no other alternative than cutting costs massively.

• We simulate here the effect on of ROE of cutting operating costs from and average 85 bps over liabilities to 64 bp (i.e. ~ 25% cost cutting)

• Even so our illustrative insurer becomes non-profitable at the peak of the problem

• High Gain Question: Is it really reasonable to cut costs when your most in trouble? What side-effects on your ability to manage fraud, retain clients, act fast enough, etc.

RoE considering 85bp operating costs RoE considering 64bp operating costs

© Reacfin 2019Reacfin’s Seasonal Breakfast – Nov.2019

34

Recession Case-Study

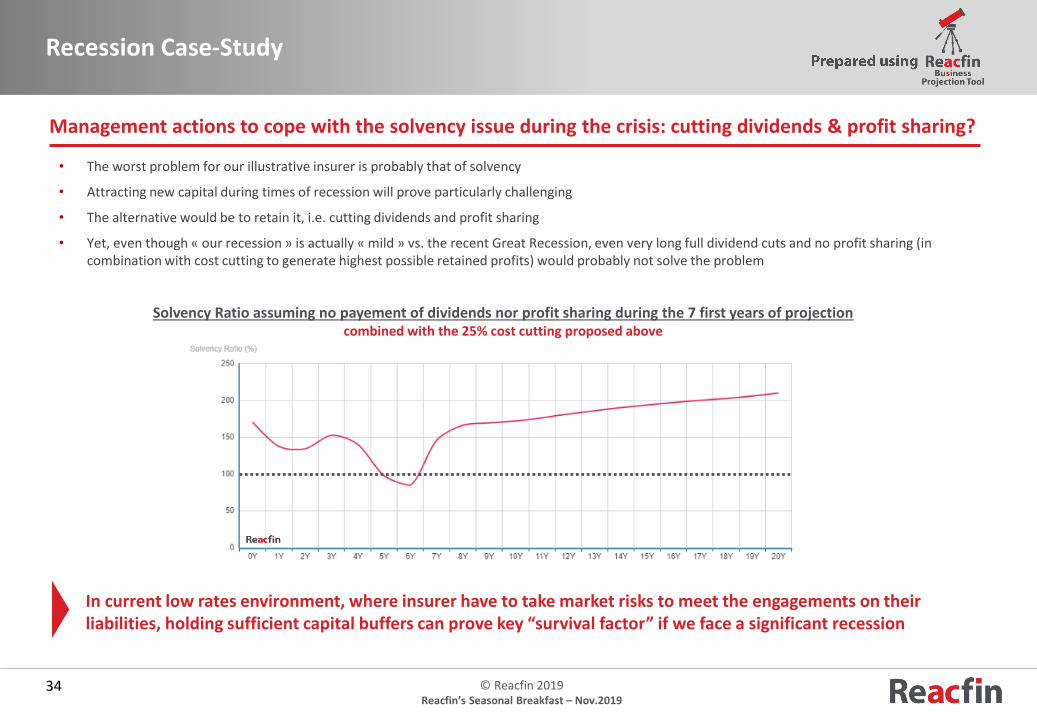

Management actions to cope with the solvency issue during the crisis: cutting dividends & profit sharing?

• The worst problem for our illustrative insurer is probably that of solvency

• Attracting new capital during times of recession will prove particularly challenging

• The alternative would be to retain it, i.e. cutting dividends and profit sharing

• Yet, even though « our recession » is actually « mild » vs. the recent Great Recession, even very long full dividend cuts and no profit sharing (in combination with cost cutting to generate highest possible retained profits) would probably not solve the problem

In current low rates environment, where insurer have to take market risks to meet the engagements on their liabilities, holding sufficient capital buffers can prove key “survival factor” if we face a significant recession

Solvency Ratio assuming no payement of dividends nor profit sharing during the 7 first years of projectioncombined with the 25% cost cutting proposed above

© Reacfin 2019Reacfin’s Seasonal Breakfast – Nov.2019

35

Agenda

• Lessons from the 2007-2009 Great Recession

• Should we really fear a recession impacting European Insurances?

• Impact of recession on insurance companies

o Life

o Non-Life

o Investments, ALM and finance

• Case study

• Getting prepared to mitigating the adverse impacts of a recession

• Q&A and Contact details

© Reacfin 2019Reacfin’s Seasonal Breakfast – Nov.2019

36

Getting prepared to mitigating the adverse impacts of a recession

What tactical “Quick-Wins” can you envisage now at teams & departments level?

• Reducing “Best Estimates” leakage & other modeling inefficiencies

• Optimizing your hedging programs & strengthen your collateral management

• Improve your data quality assessment and risk reporting capabilities through automation

• Can you facilitate the redemptions of some expensive legacy liabilities (e.g. Life) through lapses?

• Ensure regulatory required prospective self-assessments (e.g. ORSA) can truly be used for contingent management

• Raising risk awareness through dedicated trainings across the organization

ExamplesNot exhaustive

• Life & Non-Life liabilities modeling improvement support

• Recent collateral management improvement missions

• Development & assessment of contingent hedging / risk mitigation strategies (incl. pricing, contingent decisions, efficiency measurements, etc.)

• Development of tools (incl. using AI) for data quality assessments, data flow lineage & Risk dashboard

Management actions to consider Reacfin’s support

Develop a systematic “system vision”

Enable a “prospective vision”

Embed a Risk culture

Lessons learned

• We propose Online and On-Site training programs

o Combining senior practitioners’ experience with the technical excellence of our academic roots

o Knowledge transfer across the different types of financial institutions (insurance, banks, AM, FMI’s, etc.)

o Our LMS platform allows training large pools of staff (some of our trainings are attended by several thousands employees)

• Life & Non-Life liabilities modeling improvement support

• We develop a large range of actuarial science solutions (e.g. ORSA toolkit, Competition analysis, etc.)

• We support many insurers in developing robust & actionable ORSA’s and contingency plans

© Reacfin 2019Reacfin’s Seasonal Breakfast – Nov.2019

37

Getting prepared to mitigating the adverse impacts of a recession

What business transformation could you consider at Corporate level?

Management actions to consider Reacfin’s support

• Strengthen your tools & processes you promptly estimate the various potential impacts of management decisions (considering capital, profitability, liquidity, etc. and the various related regulations/frameworks)?

• Beefing-up your company’s contingency plans and test it in real conditions regularly

• Introduce “Wrong Way Risk” in your risk assessments approach and ORSA

ExamplesNot exhaustive

(*) Reacfin’s experts (Pr. Jean Dessain & Pr. François Ducuroir) recently supported Belgian insurance companies to structure & issue Solvency II compliant hybrid instruments Read the slides of our May 2019 Seasonal Breakfast: «Hybrid Capital Instruments : Opportunities for larger and smaller financial Institutions », downloadable on our website www.reacfin.com [section « News & Publications » / « events »])

(**) Read our dedicated White Paper « Reacfin’s Strategic Digitalization Quick-Scan » (July 2018) by Pr. F. Ducuroir, Pr. A. Couloumy & Vidushi Gupta, downloadable on our website www.reacfin.com [section « News & Publications » / « White Paper »])

• Independent Business & Asset Allocation optimizations studies

• Prepare your Strategic Business Mix and Asset Allocation

• Would it be time to considerhybrid capital buffers?

• Prioritize how you strengthen your operations through digitalization

• Structuring & issuance support for Hybrid Capital instruments incl. loans

• Reacfin’s “Strategic Digitalization Quick-Scan & Prioritization” Methodology**

Develop a systematic “system vision”

Enable a “prospective vision”

Embed a Risk culture

Lessons learned

• Reacfin’s Business Projection tools

• Development and assessment of contingency plans

• Recent missions (incl. for large Financial Market Infrastructure companies) to identify, measure, report and mitigate main Wrong Way Risk exposures

Free demo on www.reacfin.com (see « Online Apps »)

© Reacfin 2019Reacfin’s Seasonal Breakfast – Nov.2019

38

Agenda

• Lessons from the 2007-2009 Great Recession

• Should we really fear a recession impacting European Insurances?

• Impact of recession on insurance companies

o Life

o Non-Life

o Investments, ALM and finance

• Case study

• Getting prepared to mitigating the adverse impacts of a recession

• Q&A and Contact details

© Reacfin 2019Reacfin’s Seasonal Breakfast – Nov.2019

39

Q&A and Contact details

Place de l’Université, 25B-1348 Louvain-la-Neuve (Belgium)

T +32 (0) 10 84 07 50

www.reacfin.com

Xavier MaréchalManaging Partner

+32 497 48 98 [email protected]

François DucuroirManaging Partner

+32 472 72 32 [email protected]

© Reacfin 2019Reacfin’s Seasonal Breakfast – Nov.2019

Place de l’Université 25B-1348 Louvain-la-Neuve

www.reacfin.com

Disclaimer:

The recipient of this document should treat all

information as strictly confidential and only in the

context stated below. Information may not be

disclosed to any third party without the prior join-

consent of Reacfin.

Estimates given in this presentation are based on our

current knowledge, they can be based upon our

previous experience within the Undertaking, as well as

taking into account similar projects in the same

context as the Undertaking, either locally, within

majority of the EU countries as well as overseas.

This presentation is only the supporting document of

a verbal presentation. Hence, it is not intended to be

exhaustive. Quoting or using this document on its own

might be misleading. As a result, these materials may

not be used by anybody except their authors nor

should they be relied upon in any way for any purpose

other than as contemplated by joint written

agreement with Reacfin.