Embed Size (px)

Citation preview

MANUAL OF FINANCIAL RECORDS FOR

KANAWHA COUNTY SCHOOLS

7TH Edition

Budget, Finance and Accounting

Kanawha County Schools 200 Elizabeth Street

Charleston, West Virginia 25311

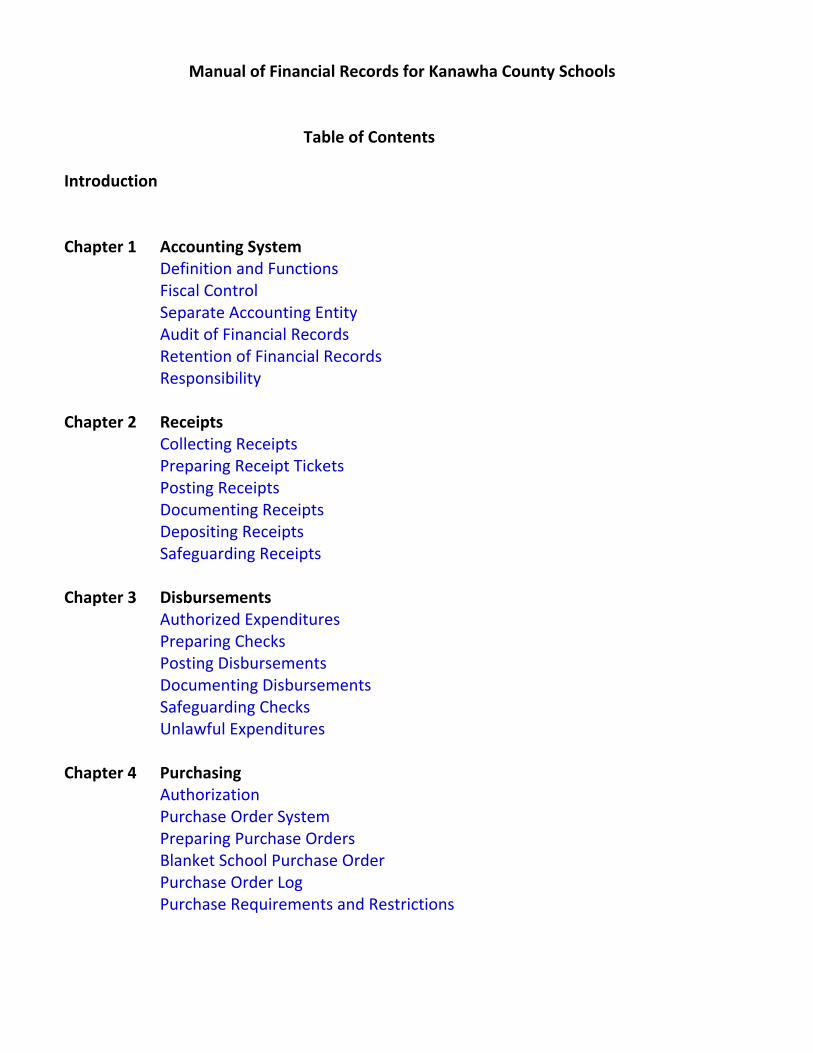

Manual of Financial Records for Kanawha County Schools Table of Contents Introduction Chapter 1 Accounting System Definition and Functions Fiscal Control Separate Accounting Entity Audit of Financial Records Retention of Financial Records Responsibility Chapter 2 Receipts Collecting Receipts Preparing Receipt Tickets Posting Receipts Documenting Receipts Depositing Receipts Safeguarding Receipts Chapter 3 Disbursements Authorized Expenditures Preparing Checks Posting Disbursements Documenting Disbursements Safeguarding Checks Unlawful Expenditures Chapter 4 Purchasing Authorization Purchase Order System Preparing Purchase Orders Blanket School Purchase Order Purchase Order Log Purchase Requirements and Restrictions

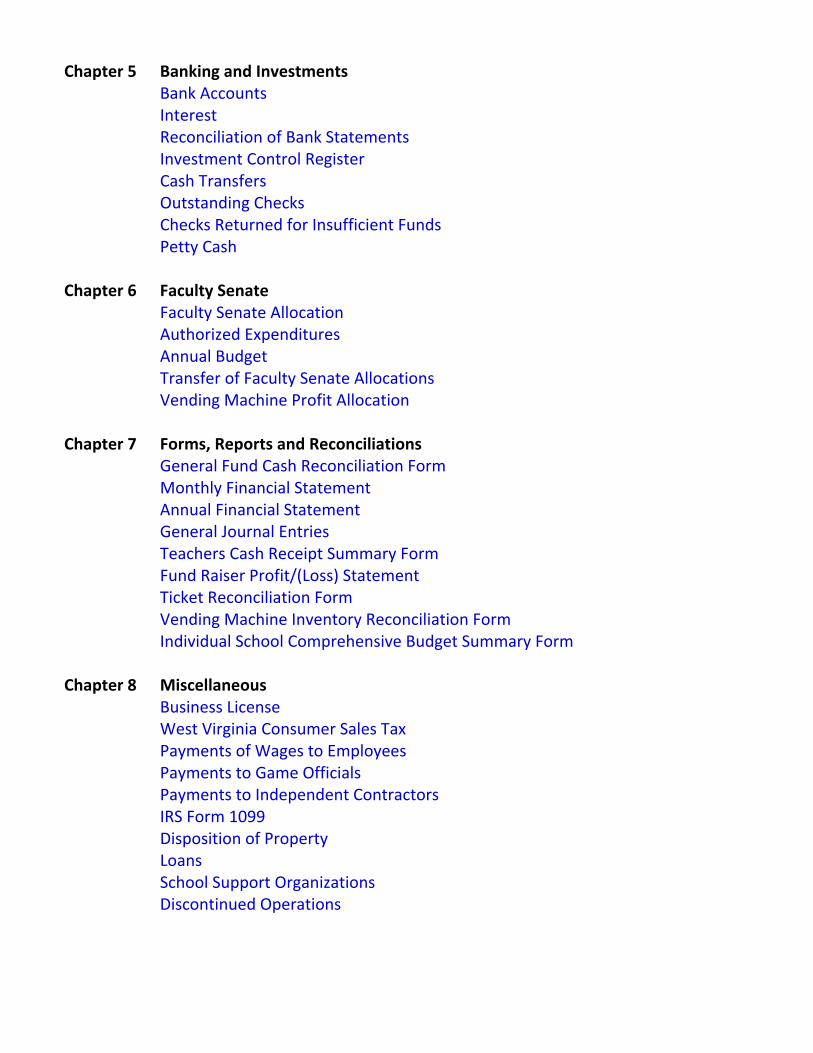

Chapter 5 Banking and Investments Bank Accounts Interest Reconciliation of Bank Statements Investment Control Register Cash Transfers Outstanding Checks Checks Returned for Insufficient Funds Petty Cash Chapter 6 Faculty Senate Faculty Senate Allocation Authorized Expenditures Annual Budget Transfer of Faculty Senate Allocations Vending Machine Profit Allocation Chapter 7 Forms, Reports and Reconciliations General Fund Cash Reconciliation Form Monthly Financial Statement Annual Financial Statement General Journal Entries Teachers Cash Receipt Summary Form Fund Raiser Profit/(Loss) Statement Ticket Reconciliation Form Vending Machine Inventory Reconciliation Form Individual School Comprehensive Budget Summary Form Chapter 8 Miscellaneous Business License West Virginia Consumer Sales Tax Payments of Wages to Employees Payments to Game Officials Payments to Independent Contractors IRS Form 1099 Disposition of Property Loans School Support Organizations Discontinued Operations

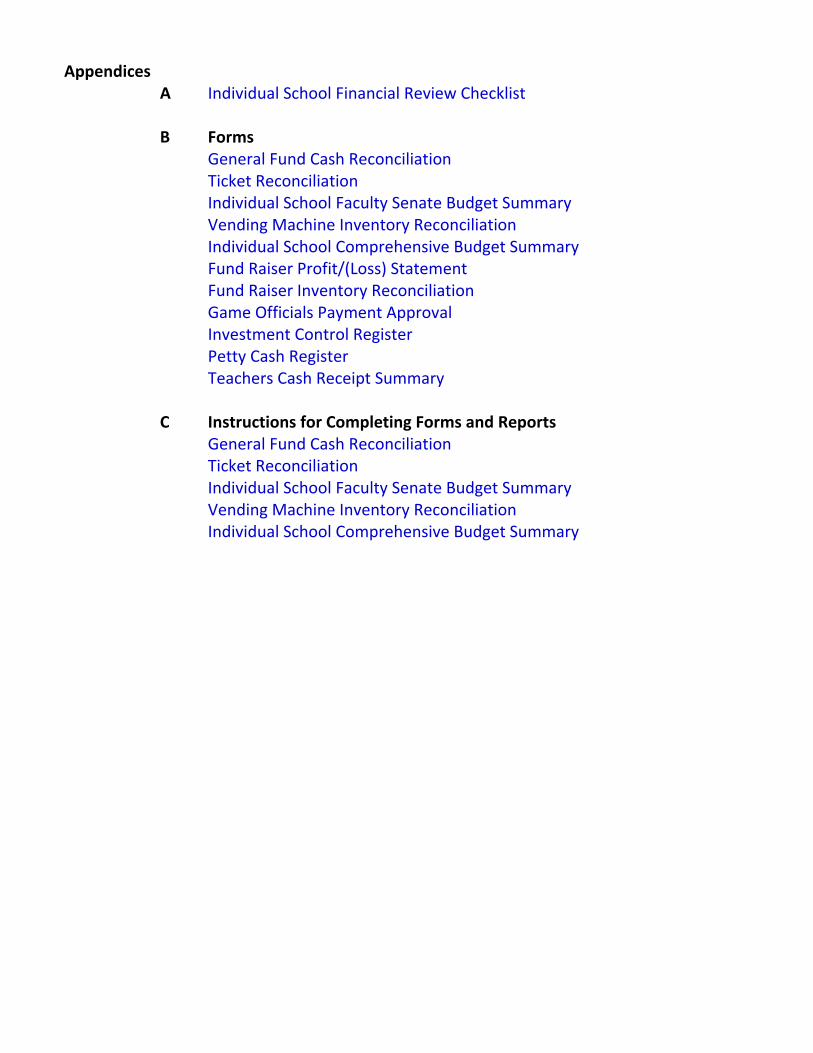

Appendices A Individual School Financial Review Checklist B Forms General Fund Cash Reconciliation Ticket Reconciliation Individual School Faculty Senate Budget Summary Vending Machine Inventory Reconciliation Individual School Comprehensive Budget Summary Fund Raiser Profit/(Loss) Statement Fund Raiser Inventory Reconciliation Game Officials Payment Approval Investment Control Register Petty Cash Register Teachers Cash Receipt Summary C Instructions for Completing Forms and Reports General Fund Cash Reconciliation Ticket Reconciliation Individual School Faculty Senate Budget Summary Vending Machine Inventory Reconciliation Individual School Comprehensive Budget Summary

Manual of Financial Records for Kanawha County Schools

Introduction

The purpose of this manual is to describe the minimum system of accounting practices and procedures that is to be followed by all schools under the authority of Kanawha Board of Education. This manual is supplemental to the Accounting Procedures Manual for the Public Schools in the State of West Virginia. This manual supersedes the one entitled Manual of Financial Records for Kanawha County Schools – Seventh Edition. This manual is an integral part of Kanawha County Board of Education Policy and Administrative Regulation D12. County boards of education, subject to the provisions of statute and the rules and regulations of the State Board of Education, have the authority and responsibility to require that records be kept of all receipts and disbursements of all funds collected or received by any principal, teacher, student, or other person connected with the school, to audit such funds, and to conserve such funds. All such funds so collected shall be deemed quasi-public moneys, and shall be expended for the benefit of the students of the school. Accountability over school money, which is deemed quasi-public money, is imperative. The Manual of Financial Records for Kanawha County Schools - Seventh Edition is designed to facilitate accountability over school money. Proper use of this manual will assist the school principal to achieve the following for his or her school:

Compliance with Policy Regulation 1224.1 of the West Virginia Board of Education.

Compliance with accreditation standards 2.2.3 and 2.2.4 of the West Virginia Board of Education.

Compliance with Policy Regulation D12 of the Kanawha County Board of Education.

Maintain fiscal control over the school.

Properly record, summarize and report the financial transactions of the school.

Protect the integrity of the financial records of the school. This manual is subject to future revisions, in whole or in part, by the Kanawha County Board of Education.

Manual of Financial Records for Kanawha County Schools

Chapter 1

Accounting System

Definition and Functions An accounting system is comprised of the forms, records, procedures and controls used to process financial date and produce reliable reports. An accounting system includes three basic functions:

1. The recording of transactions 2. 3. The summarizing of transactions

4. The reporting and interpreting of summary information

Fiscal Control Fiscal control is a plan of organization designed t safeguard assets, check the reliability of accounting records, promote operational efficiency and encourage adherence to prescribed policies. Good fiscal control is a key factor in the effective management of the school. Good fiscal control includes the following characteristics:

1. A plan of organization that provides appropriate segregation of duties.

2. A system of authorization and record procedures adequate to provide reasonable accounting control over assets, liabilities, revenues, and expenses.

3. Sound practices to be followed in the performance of duties.

4. Personnel of a quality commensurate with responsibilities.

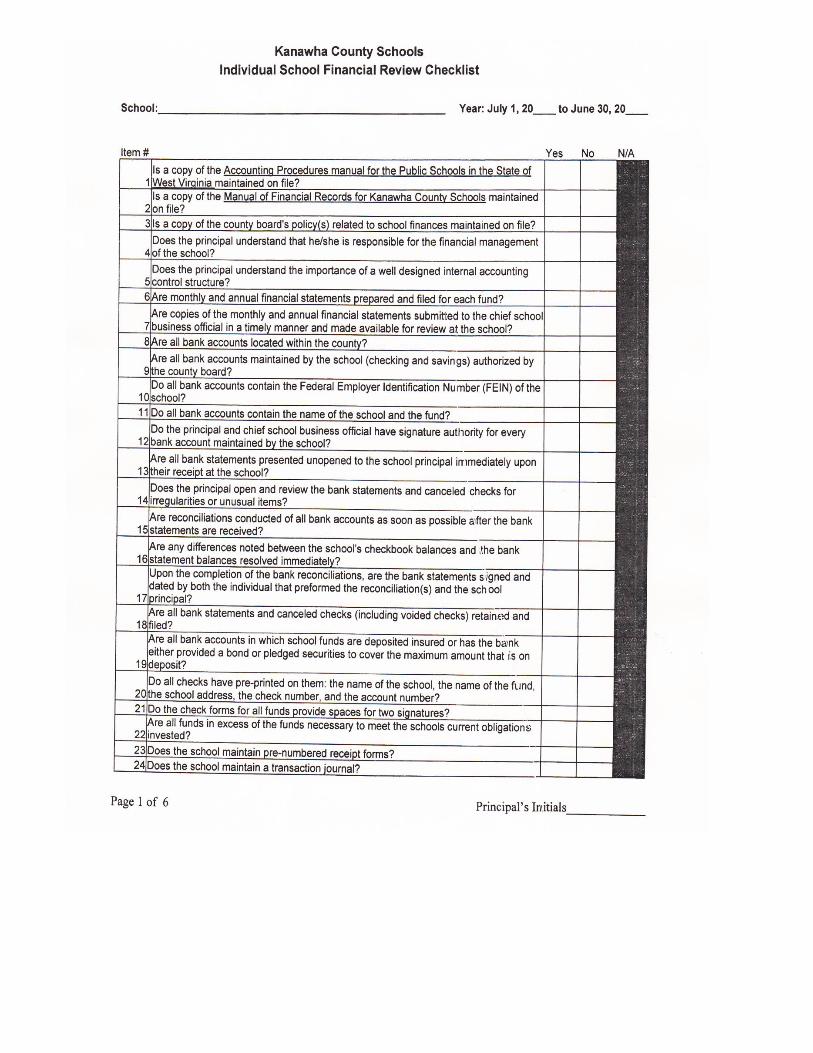

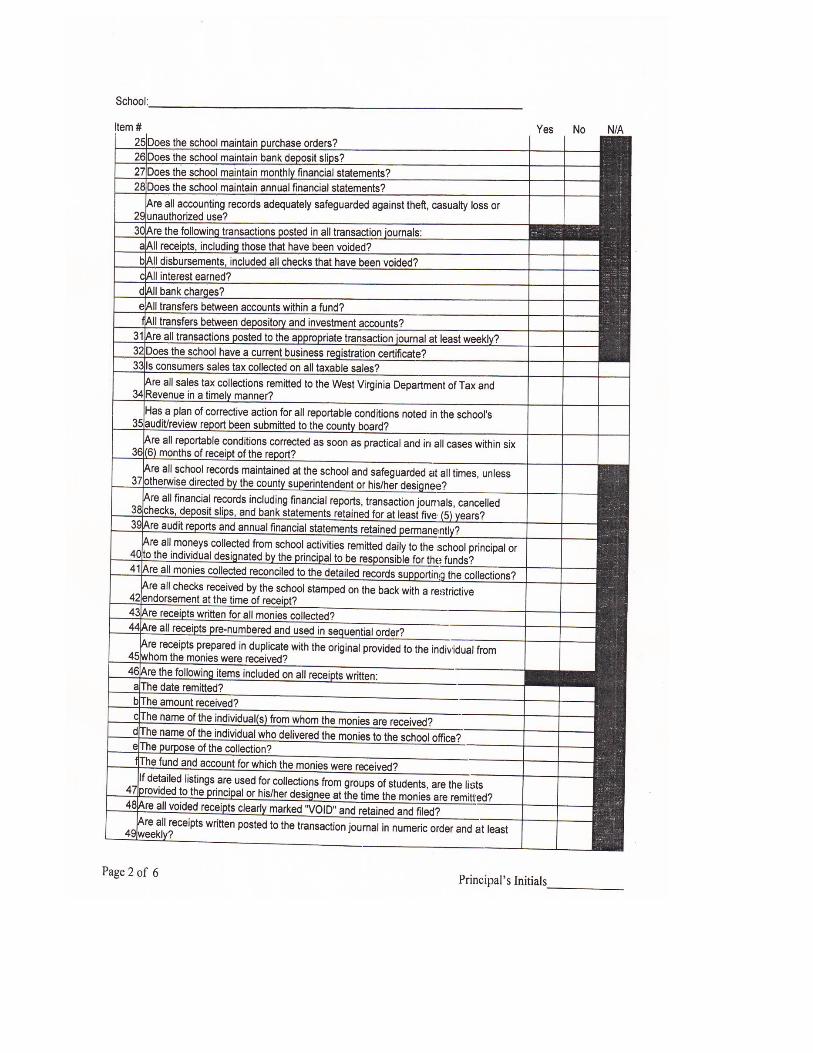

A fiscal control checklist is a series of questions designed to identify weaknesses in the administrative and accounting controls of the school. The Kanawha County Schools Individual School Financial Review Checklist is a fiscal control checklist that is worded so that “No” answers suggest undesirable practices relative to achieving good internal control. This checklist is located in Appendix A of this manual, and must be completed by the principal of each school on an annual basis.

1-1

Separate Accounting Entity Each school is considered to be a separate and distinct financial accounting entity. As such, a complete set of accounting records must be maintained for each school in which is recorded all financial activities of the school. Only financial activities of the school are to be recorded in the school’s accounting records. Personal transactions of the staff or other outside sources, such as coffee or flower fund collections are not to be recorded in the school’s accounting records. Schools are not legal entities and school personnel, including principals, do not have the statutory authority to enter into contracts or obligate money belonging to a county board of education. All money located in the depository accounts of the school must be owned and controlled by the school. The personal money of outside sources must not be intermingled with money that belongs to the school.

Fund Accounting A fund is a separate grouping of receipts and disbursements for specific activities. The school is permitted to have a General Fund. The General Fund is used to account for the general operations of the school. All financial activities of the school must be recorded in the General Fund. The following accounting records must be maintained for the General Fund:

Receipts Journal

Disbursements Journal

Pre-numbered Receipt Tickets

Pre- numbered Checks

Bank Deposit Slips

Cash Reconciliation Forms

Investment Control Registers

School Purchase Orders

Purchase Order Log

Monthly Financial Statements

Annual Financial Statements

The General Fund is divided into activity accounts that serve to classify receipts and expenditures by type. For example, the school’s General Fund might consist of the following activity accounts:

1-2

Office To account for the general activity of the school Clubs To account for the activity of student organizations

Faculty Senate – Teachers To account for the $100 portion of faculty senate funds allocated to each teacher

Faculty Senate – School To account for the $100 portion of faculty senate funds allocated to each teacher

Athletics To account for the activity of student athletics Each General Fund activity account could consist of several sub-accounts to more specifically classify receipts and expenditures. A sub-account is defined as a group or particular activity with a claim against the assets of the school without regard to the specific asset (checking, savings, certificate of deposit (CD), etc.) For example, the Clubs activity account might be divided into the following sub-accounts: Chemistry Club To account for activity of the Chemistry Club French Club To account for activity of the French Club Honor Society To account for activity of the Honor Society General Fund activity must be recorded utilizing the General Fund and Purchase Order Log software designed for Kanawha County Schools. Documentation manuals for this software may be obtained from the Information Systems Department.

Audit of Financial Records The financial records of the school will be audited on an annual basis. Criteria for an adverse opinion in the annual School Audit Report include the following findings:

Fraud in the financial management of the school

Gross negligence (i.e. – acting or omitting to act in a situation where there is a duty to act, not inadvertently, but willfully and intentionally with a conscious indifference to consequences) in the financial management of the school that results in the reprimand, suspension or termination of the guilty school employee

Negligence due to a negative net balance on an Annual Financial Statement

Negligence due to incomplete and/or unauditable financial records that result from a lack of fiscal control

Negligence due to the non-implementation of audit recommendations

1-3

Retention of Financial Records All school accounting records are considered property of the Kanawha County Board of Education. All financial records must be retained at the school for a period of five years. Annual financial statements, audit reports and responses to audit reports must be retained at the school permanently. The process of disposing of any financial records must be supervised by the principal to ensure complete destruction.

Responsibility The principal is responsible for the financial management of the school. The principal must ensure that all accounting records are maintained accurately and that all financial reports are submitted timely to the Kanawha County Board of Education.

1-4

Manual of Financial Records for Kanawha County Schools

Chapter 2

Receipts

Collecting Receipts All receipts collected by individuals for the school must be submitted daily to the school office. All checks submitted to the school must be made payable to the school. Checks that are made payable to individuals and are subsequently endorsed payable to the school should not be accepted. The total amount of money delivered to the school office must be reconciled to the detailed records that support the receipts. Certain types of receipts will require the school to maintain detailed records for each student (i.e. - patrol trip collections, yearbook sales, etc.).

Preparing Receipt Tickets Receipt tickets must be prepared for all receipts. Receipt tickets must be prepared at the time that the monies are received – not at the end of the day, or when a deposit is being prepared. Each receipt ticket must contain the following information:

The date of the receipt A pre-printed number The name of the remitter The amount of the receipt The form of payment (cash/check) A brief description of the receipt The name of the deliverer The signature of the preparer

Every receipt ticket must contain a valid signature. The use of electronic signatures is acceptable if the signature is password protected. Signature stamps or preprinted signatures are not allowed for use by the school. Receipt tickets must be pre-numbered and must be issued in numerical order.

2-1

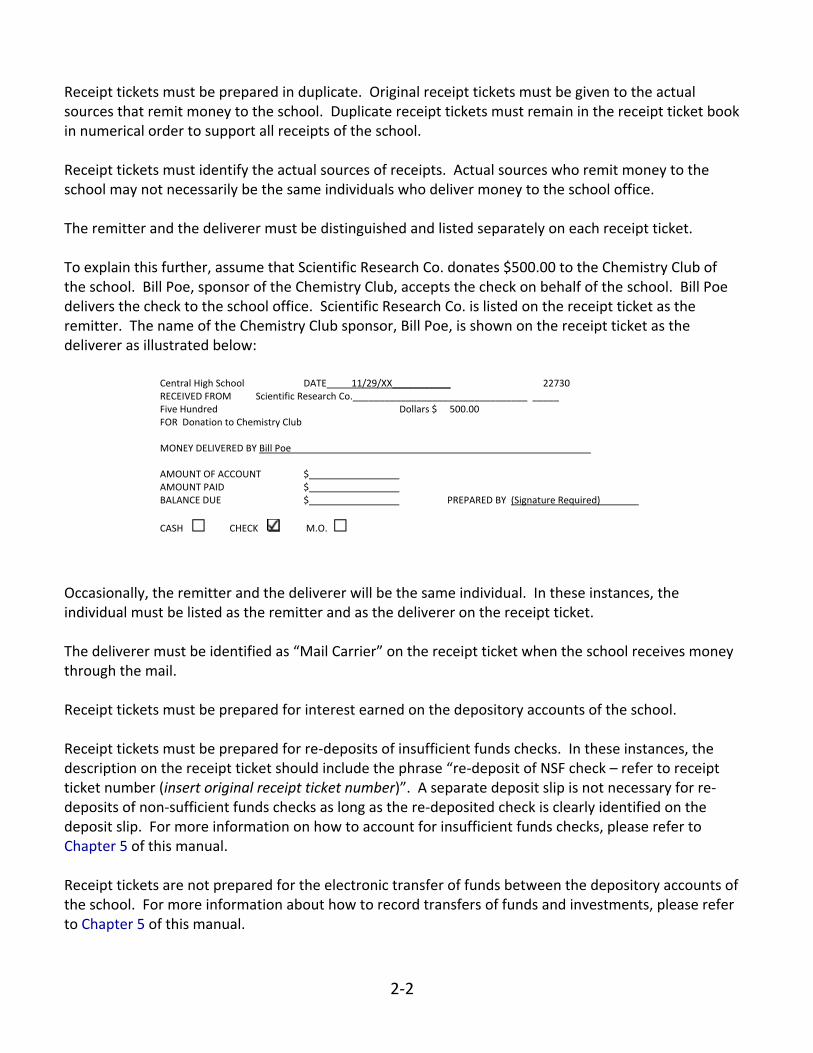

Receipt tickets must be prepared in duplicate. Original receipt tickets must be given to the actual sources that remit money to the school. Duplicate receipt tickets must remain in the receipt ticket book in numerical order to support all receipts of the school. Receipt tickets must identify the actual sources of receipts. Actual sources who remit money to the school may not necessarily be the same individuals who deliver money to the school office. The remitter and the deliverer must be distinguished and listed separately on each receipt ticket. To explain this further, assume that Scientific Research Co. donates $500.00 to the Chemistry Club of the school. Bill Poe, sponsor of the Chemistry Club, accepts the check on behalf of the school. Bill Poe delivers the check to the school office. Scientific Research Co. is listed on the receipt ticket as the remitter. The name of the Chemistry Club sponsor, Bill Poe, is shown on the receipt ticket as the deliverer as illustrated below:

Central High School DATE 11/29/XX___________ 22730 RECEIVED FROM Scientific Research Co._________________________________ _____ Five Hundred Dollars $ 500.00 FOR Donation to Chemistry Club MONEY DELIVERED BY Bill Poe AMOUNT OF ACCOUNT $ AMOUNT PAID $ BALANCE DUE $ PREPARED BY (Signature Required)

CASH □ CHECK M.O. □

Occasionally, the remitter and the deliverer will be the same individual. In these instances, the individual must be listed as the remitter and as the deliverer on the receipt ticket. The deliverer must be identified as “Mail Carrier” on the receipt ticket when the school receives money through the mail. Receipt tickets must be prepared for interest earned on the depository accounts of the school. Receipt tickets must be prepared for re-deposits of insufficient funds checks. In these instances, the description on the receipt ticket should include the phrase “re-deposit of NSF check – refer to receipt ticket number (insert original receipt ticket number)”. A separate deposit slip is not necessary for re-deposits of non-sufficient funds checks as long as the re-deposited check is clearly identified on the deposit slip. For more information on how to account for insufficient funds checks, please refer to Chapter 5 of this manual. Receipt tickets are not prepared for the electronic transfer of funds between the depository accounts of the school. For more information about how to record transfers of funds and investments, please refer to Chapter 5 of this manual.

2-2

The work “Void” must be written on the face of all receipt tickets not issued due to preparation errors. The original and all duplicate copies of voided receipt tickets must be retained.

Posting Receipts Receipt tickets must be posted daily to the receipts journal using the General Fund software for Kanawha County Schools. Bookkeeping errors are frequently the result of not posting receipt transactions promptly to the journal. Receipt tickets must be posted to the journal in numerical order. Receipt entries are posted to the journal from information listed on receipt tickets. Receipt tickets must be posted individually to the journal. Receipts must be classified to activity accounts in the journal based upon the nature of each receipt. Proper account classification may require that a receipt be posted to more than one activity account in the journal. The account classification breakdown must equal the total receipt amount. Documentation manuals with instructions for posting receipts using Kanawha County Schools General Fund software may be obtained from the Information Systems Department.

Documenting Receipts Cash is sometimes received from a group for a specific activity. In these instances, the group is listed as the remitter on the receipt ticket. For example, if a group of 25 fifth grade students had each paid $10.00 to take a field trip, then one receipt ticket would be issued with “Fifth Grade Students” listed as the remitter for $250.00. This eliminates the need to issue separate receipt tickets to individual students. Receipt tickets can only be issued to a group when the cash receipts are for the same purpose, are posted only to one activity account, and are remitted to the school office at the same time. Receipt tickets issued to a group rather than to an individual remitter must be supported by detailed documentation. Examples of detailed documentation to support receipt tickets include:

Teachers Cash Receipt Summary Form

Fund Raiser Profit/(Loss) Statement

Ticket Reconciliation Form Detailed instructions on how to complete each of these forms is included in Chapter 7 of this manual.

2-3

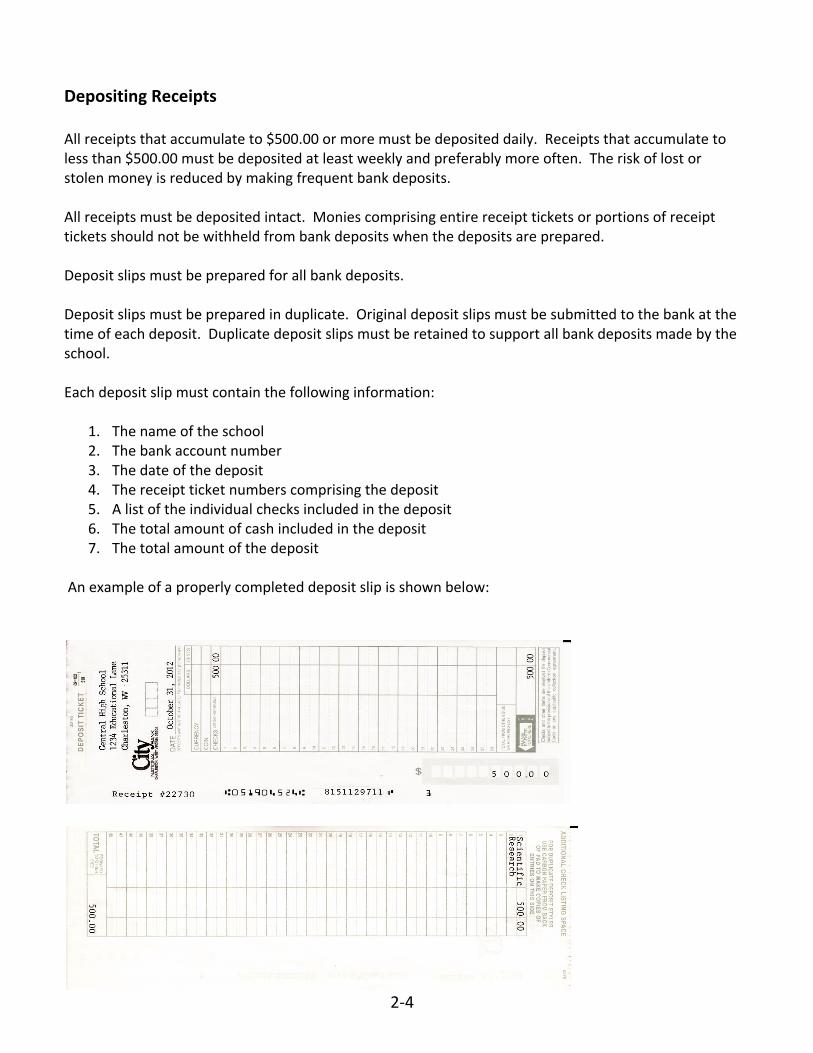

Depositing Receipts All receipts that accumulate to $500.00 or more must be deposited daily. Receipts that accumulate to less than $500.00 must be deposited at least weekly and preferably more often. The risk of lost or stolen money is reduced by making frequent bank deposits. All receipts must be deposited intact. Monies comprising entire receipt tickets or portions of receipt tickets should not be withheld from bank deposits when the deposits are prepared. Deposit slips must be prepared for all bank deposits. Deposit slips must be prepared in duplicate. Original deposit slips must be submitted to the bank at the time of each deposit. Duplicate deposit slips must be retained to support all bank deposits made by the school. Each deposit slip must contain the following information:

1. The name of the school 2. The bank account number 3. The date of the deposit 4. The receipt ticket numbers comprising the deposit 5. A list of the individual checks included in the deposit 6. The total amount of cash included in the deposit 7. The total amount of the deposit

An example of a properly completed deposit slip is shown below:

2-4

When preparing the bank deposit, the receipt tickets for the period (in consecutive order) should be added and the total noted in pencil on the last receipt ticket. The monies comprising the deposit should then be counted and listed on the deposit slip. The total of the receipt tickets should equal the total on the bank deposit slip. If there are differences, they should be resolved at this time to reduce the possibility of errors in preparing bank deposits. A restrictive endorsement must be stamped on the back of all checks received by the school. This restrictive endorsement must include the following information:

1. The words “For Deposit Only” 2. The name of the school 3. The name of the fund – (i.e. – General Fund) 4. The ban account number

The bank verification of the deposit must be retained and attached to the school’s copy of the deposit slip. Personal checks are prohibited to be cashed from the un-deposited receipts of the school. The risks of cash shortages and bank deposit errors increase if the school cashes the person checks of outside sources.

Safeguarding Receipts All un-deposited receipts of the school must be safeguarded against theft, casualty loss, and unauthorized use. Un-deposited receipts must be placed in safekeeping and be accessible only by authorized personnel.

2-5

Manual of Financial Records for Kanawha County Schools

Chapter 3

Disbursements Authorized Expenditures All moneys received by a school are considered quasi-public funds and are to be expended for the benefit of the students at the school. Expenditures of school money for private purposes are not permitted. Items for which quasi-public funds shall not be expended include flowers, gifts, banquets, or service awards for school employees and/or members of the general public. The purchase of flowers with General Fund monies is permitted in connection with the death or hospitalization of a student at the school. Schools and school clubs may not make contributions to charitable or private non-profit organizations unless a fundraiser is conducted specifically for that purpose. In these instances, the fundraiser purpose must be clearly stated when the fundraiser is conducted, and a separate activity account must be established in the General Fund to account for the fundraiser. The expenditure of General Fund money for food and drink is strictly limited to those items consumed during student-focused activities that involve the direct participation of the students of the school. The school is not allowed to use General Fund money to purchase food and drink items for the exclusive consumption by the public and /or employees of the Kanawha County Board of Education including members of the school staff. The school is permitted to reimburse the meal expenses of school staff members who travel for approved school related business. Kanawha County Board of Education Policies and Administrative Regulations Series: G47 contains more information regarding the reimbursement of travel expenses to employees. W. Va. Code §18-5-13 allows schools to expend money for student, parent, teacher and community recognition programs using monies generated through a fund-raiser or donation-soliciting activity. Prior to commencing the activity, the school must publicize that the activity will be for this purpose and must designate the monies generated for this purpose. Any money generated must be accounted for in a separate activity account in the General Fund and not co-mingled with other school monies.

Preparing Checks All disbursements must be made by check. The only exception is for petty cash expenditures. Petty cash procedures are explained in Chapter 5 of this manual.

3-1

Each check must contain the following information:

The date of the disbursement A pre-printed number The pre-printed name of the school The pre-printed name of the fund (i.e. – General Fund) The pre-printed words “Void After Six Months” The pre-printed bank account number The name of the payee The amount of the disbursement The manual signature of the principal An additional signature of an individual designated by the principal

Checks must be made payable to the individual or vendor to whom the payment is being made, not to another party that is subsequently making payment on behalf of the school. Two signatures are required on every check issued by the school. Both signatures cannot be by the same individual. One of the required signatures must be either that of the school principal or other individual(s) officially designated to act in the place of the principal in his/her continued absence. The second signature is to be that of an individual designated by the principal. The signing of blank checks is prohibited. The signing of blank checks increases the risk of the unauthorized use of money that belongs to the school. The principal must know the checking account balance before signing checks. The signing of checks without the knowledge of the checking account balance increases the risk of bank overdrafts. Checks are not permitted to be made payable to “Cash”. A check must be made payable to the principal if cash is needed by the school. All checks written to the principal must be supported by detailed documentation. Checks stubs must be filled out completely and kept up to date at all times. If computer checks are used rather than the traditional checkbook format, then duplicate copies or stubs or the computer checks must be retained and filed in numerical order. The word “Void” must be written on the face of all checks not issued due to preparation errors. All voided checks must be retained and not discarded. Voided checks should be attached to the check stub or to the duplicate copy of the check if computer checks are used. All voided checks must be entered in the disbursements journal with the description listed as “Void” and the amount listed as zero.

3-2

Cancelled checks (checks returned paid with the monthly bank statement) must be retained by the school. If a checkbook format is used, cancelled checks should be taped to the check stub in the checkbook after the bank statement is reconciled at the end of the month. If a computer check format is used, cancelled checks should be attached to the duplicate copy or stub of the computer check. If check images rather than actual cancelled checks are returned with the bank statement, an image of both sides of the check is required. If the check images cannot be easily attached to check stubs, the check stubs must be marked with the word “cancelled” and the bank statement date that the check was paid. This can be done through the use of a date and phrase rubber stamp. The check images must be retained by the school and filed with the bank statement.

Posting Disbursements Checks must be posted daily to the disbursements journal using the General Fund software for Kanawha County Schools. Bookkeeping errors are frequently the result of not posting disbursement transactions promptly to the journal. Checks must be posted to the journal in numerical order. Checks must be posted individually to the journal. Disbursements must be classified to activity accounts in the journal. Proper classification is based upon the nature of each disbursement. Proper account classification may require that a disbursement be posted to more than one account in the journal. The account classification breakdown must equal the total disbursement amount. Documentation manuals with instructions for posting disbursements using Kanawha County Schools General Fund software may be obtained from the Information Systems Department.

Documenting Disbursements All disbursement must be supported by detailed documentation. Detailed documentation consists of an invoice or receipt provided by the vendor. Detailed documentation must include the following:

3-3

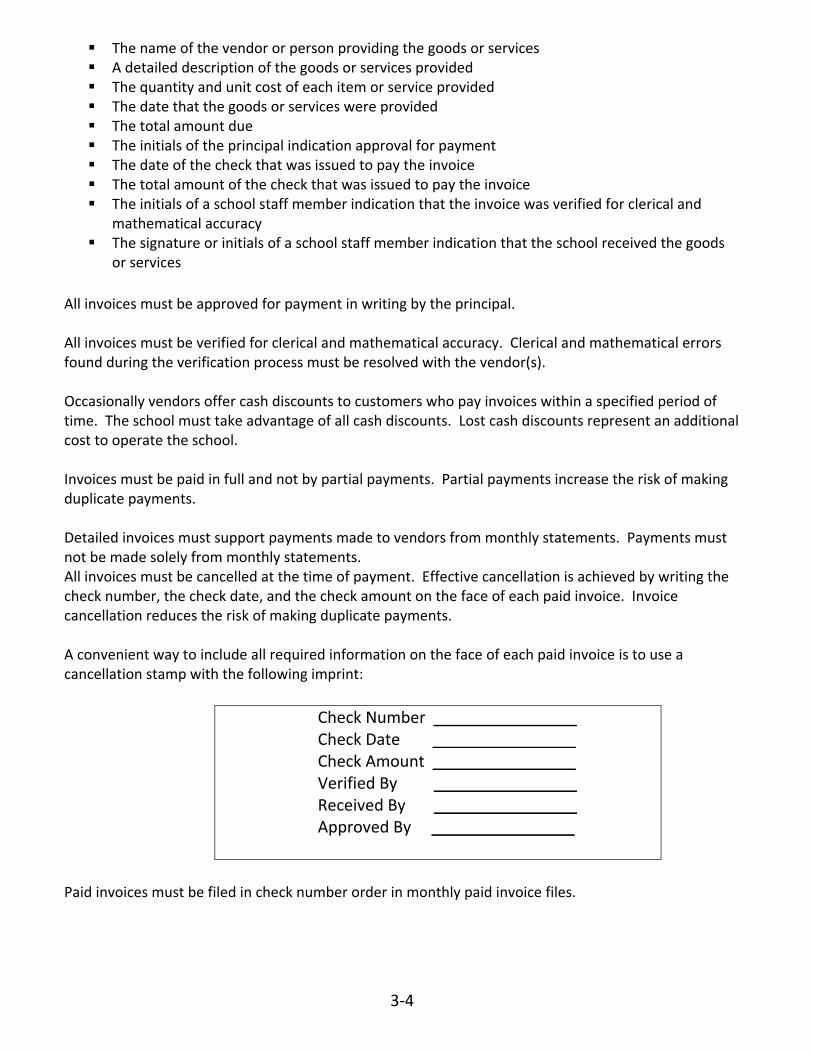

The name of the vendor or person providing the goods or services A detailed description of the goods or services provided The quantity and unit cost of each item or service provided The date that the goods or services were provided The total amount due The initials of the principal indication approval for payment The date of the check that was issued to pay the invoice The total amount of the check that was issued to pay the invoice The initials of a school staff member indication that the invoice was verified for clerical and

mathematical accuracy The signature or initials of a school staff member indication that the school received the goods

or services

All invoices must be approved for payment in writing by the principal. All invoices must be verified for clerical and mathematical accuracy. Clerical and mathematical errors found during the verification process must be resolved with the vendor(s). Occasionally vendors offer cash discounts to customers who pay invoices within a specified period of time. The school must take advantage of all cash discounts. Lost cash discounts represent an additional cost to operate the school. Invoices must be paid in full and not by partial payments. Partial payments increase the risk of making duplicate payments. Detailed invoices must support payments made to vendors from monthly statements. Payments must not be made solely from monthly statements. All invoices must be cancelled at the time of payment. Effective cancellation is achieved by writing the check number, the check date, and the check amount on the face of each paid invoice. Invoice cancellation reduces the risk of making duplicate payments. A convenient way to include all required information on the face of each paid invoice is to use a cancellation stamp with the following imprint:

Check Number ________________ Check Date ________________ Check Amount ________________ Verified By ________________ Received By ________________ Approved By ________________

Paid invoices must be filed in check number order in monthly paid invoice files.

3-4

Safeguarding Checks All checks must be safeguarded against theft, casualty loss, and unauthorized use. Checks must be placed in safekeeping and be accessible only by authorized personnel. Unlawful Expenditures All schools under the authority of the Kanawha County Board of Education are subject to West Virginia Code §11-8-26 which provides in part as follows: “…a local fiscal body shall not expend any money or incur obligations:

1. In a unauthorized manner: 2. For an unauthorized purpose; 3. In excess of the amount allocated to the fund in the levy order; 4. In excess of the funds available for current expense.”

All schools under the authority of the Kanawha County Board of Education are subject to West Virginia Code §11-8-29 which provides in part as follows:

“A person who in his official capacity negligently participates in the violations of section twenty-six (§11-8-26) of this article shall be personally liable, jointly and severally, for the amount illegally expended.”

All schools under the authority of the Kanawha County Board of Education are subject to West Virginia Code §11-8-31 which provides in part as follows:

“A person who in his official capacity willfully violates the provisions for the article shall be guilty of a misdemeanor and, upon conviction, shall be fined not more than five hundred dollars, or confined in jail not more than one year, or both. Upon conviction he shall also forfeit his office.”

The phrase “this article” refers to Article 11 of the West Virginia Code and thereby includes West Virginia code §11-8-26, West Virginia Code §11-8-29, and West Virginia Code §11-8-31.

3-5

Manual of Financial Records for Kanawha County Schools

Chapter 4

Purchasing

Authorization All purchases made by the school must be approved in writing by the principal. The school will not be responsible for purchases that are made without proper authorization. School staff members who make purchases on behalf of the school without proper authorization by the principal will be held personally responsible for the purchases.

Purchase Order System The primary objectives of school purchasing are as follows:

1. Obtain the maximum educational value for each school dollar spent 2. Maintain a system of internal control over all purchases made by the school

A School Purchase Order is a purchasing document that requisitions supplies, equipment and/or services directly from a specific vendor at predetermined quantities and costs. The School Purchase Order documents the approval of the principal for a purchase to be made on behalf of the school. A purchase order system is to be maintained at each school whereby all purchases of materials, equipment, supplies and services are made through a pre-numbered purchase order approved in writing by the principal or designee before the purchase is made. The purchase orders must be posted in numerical sequence to a Purchase Order Log. The purpose for maintaining a purchase order system at each school is to provide the principal with a means of maintaining control over purchases to ensure that funds are available before the purchase is made, and that unauthorized purchases are not made.

Preparing Purchase Orders Purchase orders must be prepared using the Purchase Order software for Kanawha County Schools. This software generates and prints pre-numbered purchase orders and also interfaces with the General Fund software to produce the Purchase Order log. The original copy of the purchase order should be issued to the vendor. The duplicate copy of the purchase order must be retained by the school, and filed in numerical order in a purchase order file.

4-1

Purchase orders must be prepared prior to the actual purchase being made. The only exception is for reimbursements from Faculty Senate funds to school staff members who have expended their personal funds on behalf of the school. Reimbursements such as these are subject to the approval of the principal and should be held to a minimum. All purchase orders must be approved in writing by the principal or his/her designee. Approval can only be made when sufficient funds are available to make the purchase. Descriptions and prices of items and services to be purchased must be as specific as possible to eliminate any confusion with the vendor. In some instances, when it is not possible to exactly specify the item or price, limitations should be used. For example, if a teacher wants to purchase items to prepare a new bulletin board display, but he/she does not now specifically what items will be purchased prior to visiting the vendor’s store, the purchase order could be prepared as follows:

Qty Description Price Total

1 Bulletin board materials for Ms. Smith’s $35.00 $35.00 classroom not to exceed $35.00

This type of description, although not specific to each item, limits Ms. Smith and the vendor to a purchase not exceeding $35.00 and only for bulletin board materials. These limitations help the principal to maintain control over purchases.

Blanket School Purchase Order A Blanket School Purchase Order is a purchasing document that requisitions items and/or services directly from an outside vendor for a specific period of time at estimated prices. Blanket school purchase orders eliminate the need to prepare individual school purchase orders for consistent and repetitive purchases from the same vendor on a regular basis. Blanket school purchase orders must only be issued to outside vendors who deliver items to the school on a regular week-to-week or month-to-month basis. The description on blanket school purchase orders must include an estimate of the total amount of purchases for the school year, and the contract conditions of the blanket school purchase order. The contract conditions of a blanket school purchase order must specify that the purchase order becomes void whenever the stated maximum limit is reached or at the end of the school year. If the maximum limit of a blanket school purchase is reached during the school year, then a new blanket school purchase order must be prepared for any remaining purchase from the vendor for the year.

4-2

Purchase Order Log A Purchase Order Log must be maintained to account for all school purchase orders issued during the school year. The Purchase Order Log must contain the following information:

School Name

School Year

Purchase Order Date

Vendor

Purchase Order Number

Purchase Order Amount

General Fund Activity Account

Date Paid

Check Number

Check Amount

Void Date (if applicable) School purchase orders are automatically posted to the Purchase Order Log when they are prepared using the Kanawha County Schools Purchase Order software. The Purchase Order Log must be printed and reviewed on a regular basis. A complete printed Purchase Order Log for the school year must be maintained in the financial records of the school.

Purchase Requirements and Restrictions No purchases may be made from a fund or activity account in excess of the funds currently available in that fund or activity account. Purchases may not be made which will obligate the funds of a subsequent year. The school is permitted to make purchases only from outside vendors that have been approved by the Kanawha County Schools Purchasing Department. These vendors have completed the vendor registration requirements with the Purchasing Department, and are included on the WVEIS vendor list. The school is to make purchases in consideration of cost, quality, and service. All reputable outside vendors must be considered for the business of the school. Any individual or organization that makes an unauthorized purchase on behalf of the school may incur a personal obligation to the outside vendor. No person is permitted to solicit or accept personal gratuities, favors, or anything of a monetary value as a result of purchases made by the school.

4-3

The school is not permitted to purchase supplies, equipment and/or services from any employee of or any member of the Kanawha County Board of Education. School personnel and all other individuals are prohibited to purchase items and/or services for personal use through the school or by the use of the school name. The school is not allowed to have any type of credit card in the name of the school with which to make purchases from various outside vendors. Some vendors require that the school be assigned an account number or account card that identifies the school’s account with that particular vendor. In these instances, the account card must be issued only to the principal. The schools must utilize any existing county or state purchasing contracts when making purchases from the General Fund. Purchases for $1,000.00 or more are subject to a competitive bidding process before authorization by the principal. The bidding process consists of obtaining bids (or prices) from at least three competitive vendors to ensure that the best price is obtained for the school. A file of all bid documentation must be maintained in the school’s records. If a purchase for $1,000.00 or more is made utilizing a current count or state purchasing contract price, then the contract number should be noted on the School Purchase Order. In these instances, it is not necessary for the school to obtain three competitive bids. The school is to plan purchases so that the scheduled delivery date coincides with the date the items and/or services are needed. All items and/or services must be counted and inspected upon delivery to the school. A cash refund or credit memo must be received from an outside vendor for items returned to that vendor by the school.

4-4

Manual of Financial Records for Kanawha County Schools

Chapter 5

Banking and Investments

Bank Accounts Every bank account must contain the name of the school, the name of the fund, and the school’s Federal Employer Identification number (FEIN). Bank signature cards for individuals that have signature authority on local bank accounts must be maintained current at all times. The principal must have signature authority for every account in which schools funds are deposited. In addition, the chief school business official of the county must also have signature authority on all accounts. This will ensure that the school has access to school funds in circumstances in which the principal and his/her designee, if applicable, are absent unexpectedly or for an extended period of time. The use of signature stamps to sign school checks is not acceptable. The school is permitted to have the following types of bank accounts:

1. Checking account 2. Savings account 3. Certificate(s) of Deposit

The school is permitted to have only one checking account. All checks must have the following information pre-printed on them:

the name of the school

the fund

the school address

the check number

the bank account number

the words “Void After Six Months”

two blank spaces for signatures.

The total of all bank accounts should be equal to the total of all activity sub-accounts All bank accounts must be interest bearing.

Interest Receipt tickets must be prepared to record the receipt of all interest to the bank accounts.

5-1

In most instances it is not possible to prepare the receipt ticket for interest within the same month that the interest was earned because of the time lag in receiving the bank statement that lists the interest amount. The receipt ticket should be prepared as soon as the bank statement is received and the interest amount is known. The receipt ticket must be dated on the day that it is written and not back dated to the previous month. Receipt tickets must be issued in numerical sequence. The practice of leaving a receipt ticket blank to record interest in the previous month is strictly forbidden.

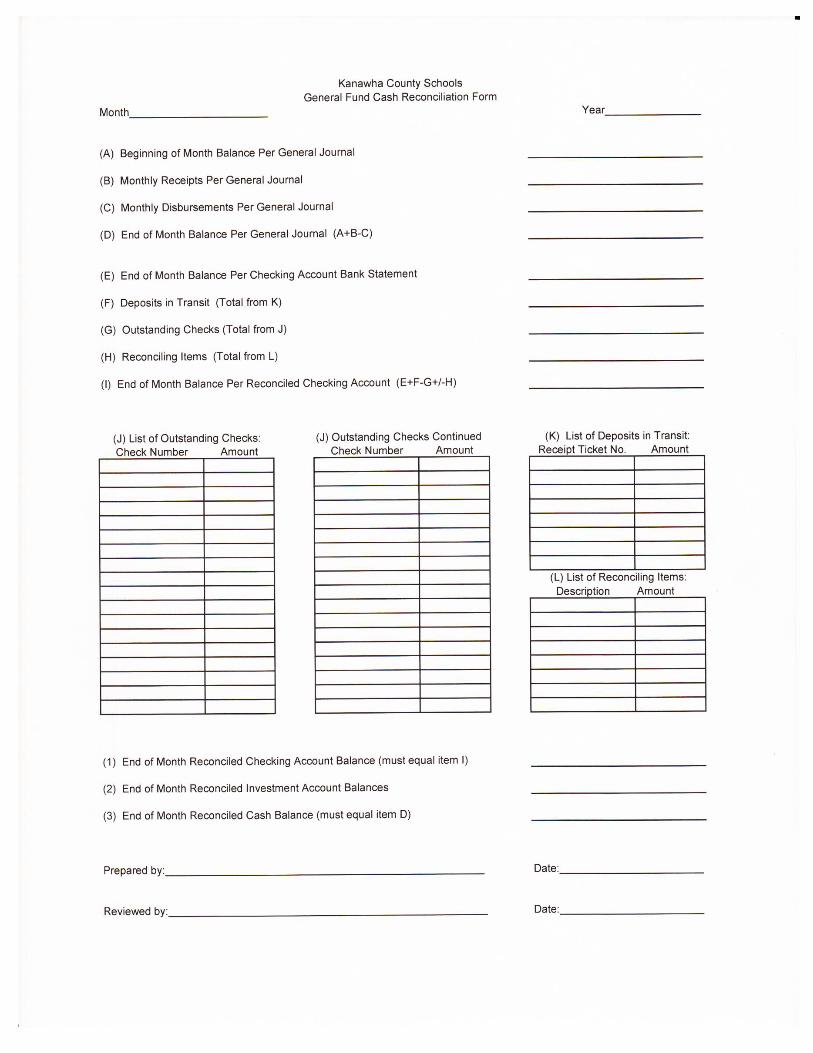

Reconciliation of Bank Statements The General Fund records must be reconciled to the corresponding bank statement(s) each month using the General Fund Cash Reconciliation form. The reconciliation should be prepared as soon as possible after the Bank statement(s) are received. The General Fund Cash Reconciliation form must be signed by the preparer and presented to the principal for review. The principal must review the General Fund Cash Reconciliation from and corresponding bank statement(s) for accuracy and any possible irregularities. The principal must sign the General Fund Cash Reconciliation form to indicate his/her review. Any differences between the bank statement(s) and the General Fund records must be resolved prior to issuing the Individual School’s Monthly Financial Statement. Detailed instructions on how to complete the General Fund Cash Reconciliation form are included in Chapter 7 and Appendix C of this manual. A blank copy of the General Fund Cash Reconciliation form is located in Appendix B of this manual.

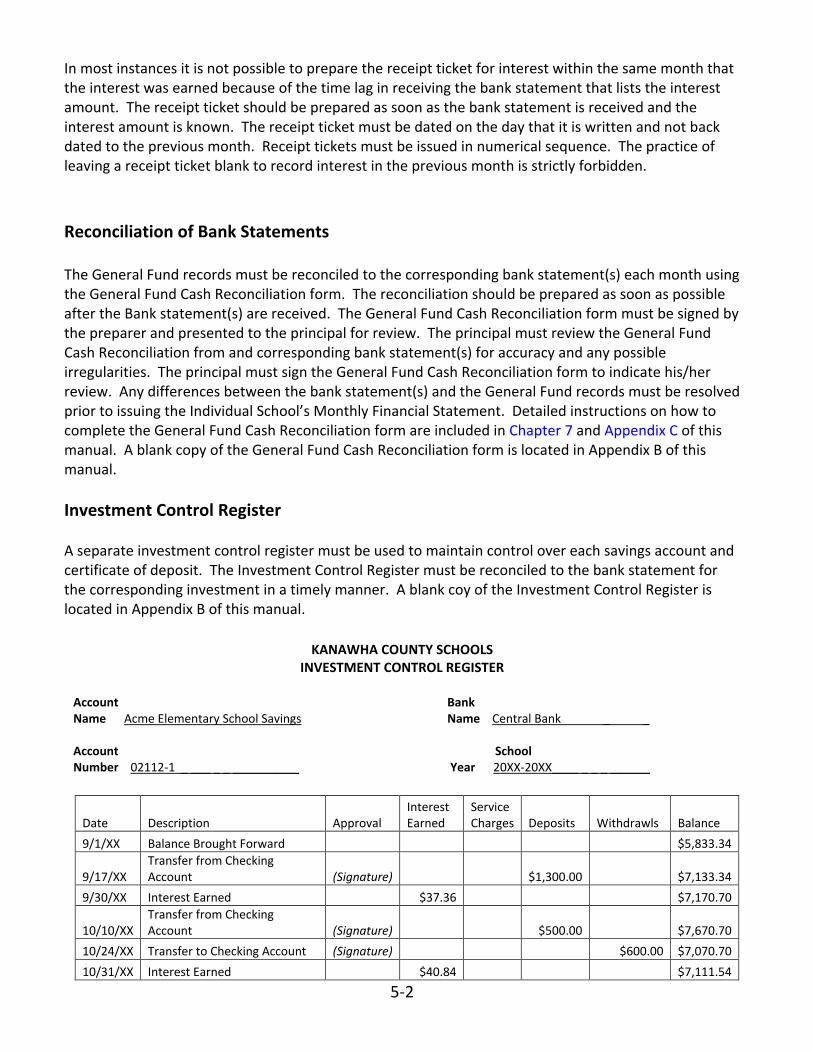

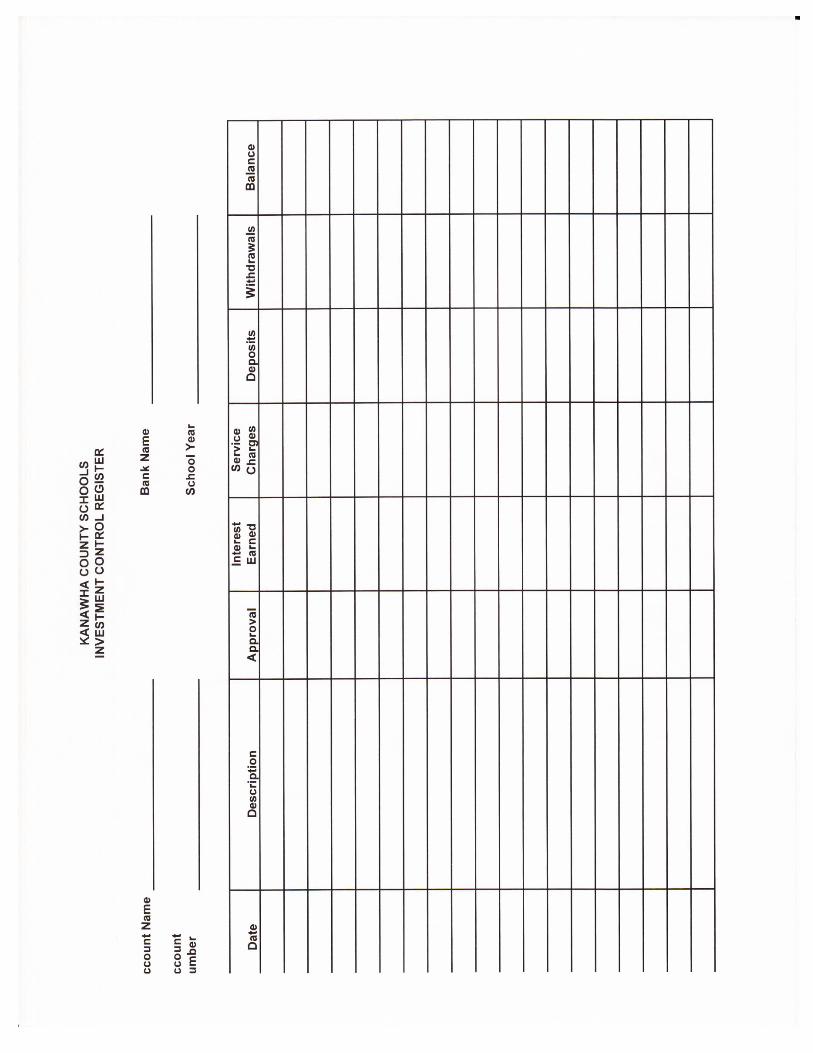

Investment Control Register A separate investment control register must be used to maintain control over each savings account and certificate of deposit. The Investment Control Register must be reconciled to the bank statement for the corresponding investment in a timely manner. A blank coy of the Investment Control Register is located in Appendix B of this manual.

KANAWHA COUNTY SCHOOLS

INVESTMENT CONTROL REGISTER

Account Bank Name Acme Elementary School Savings Name Central Bank _ _ Account School Number 02112-1 _ ___ _ _ __________ Year 20XX-20XX____ _ _ _ ______

5-2

Date Description Approval Interest Earned

Service Charges Deposits Withdrawls Balance

9/1/XX Balance Brought Forward $5,833.34

9/17/XX Transfer from Checking Account (Signature) $1,300.00 $7,133.34

9/30/XX Interest Earned $37.36 $7,170.70

10/10/XX Transfer from Checking Account (Signature) $500.00 $7,670.70

10/24/XX Transfer to Checking Account (Signature) $600.00 $7,070.70

10/31/XX Interest Earned $40.84 $7,111.54

Cash Transfers Transfers of cash between the General Fund checking account and General Fund investment accounts must be recorded in the General Fund software, as well as in the Investment Control Register(s). The method of recording the cash transfer in the General Fund software differs depending on how the transfer of money occurs. If the transfer of money to/from the General Fund checking account to/from an investment account is done electronically by the bank, then the transfer is recorded by using the Cash Transfer menu option in the General Fund software, no other entries are required. If the transfer of money from the General Fund checking account to an investment account is done by issuing a General Fund check, then the transfer is recorded by performing the following steps:

1. Post the check to the General Fund software through the Manual/Void check or Computer Check menu option to record the disbursement of funds from the checking account.

2. Prepare a General Fund receipt ticket for the check and post the receipt ticket to the General Fund software through the Receipt Entry menu option to record the receipt of money to the investment account. Deposit the check into the investment account.

If the transfer of money from an investment account to the General Fund checking account is done by receiving a check from the bank, then the transfer is recorded by performing the following steps:

1. Prepare a General Fund receipt ticket for the check and post the receipt ticket to the General Fund software through the Receipt Entry menu option to record the receipt of funds to the checking account. Include the check in the next bank deposit for the checking account.

2. Post a corresponding journal entry in the General Fund software through the Manual/Void Check or Computer Check menu option to record the corresponding disbursement of funds from the investment account.

Outstanding Checks Outstanding checks that become more than six months old must be written off. It is sometimes necessary to write off a check that has been lost and replace it with a new check. In these instances, it is prudent to first place a stop payment order on the original check with the bank. Issue the replacement check only after the stop payment order is in effect at the bank.

5-3

The proper procedure for writing off a check is to post a journal entry in the General Fund software through the Manual/Void Check or Computer Check menu. The journal entry is recorded as a negative disbursement amount. This reduces the total disbursements for the year and therefore does not overstate total disbursements on the Individual School’s Annual Financial Report. If a replacement check is necessary it should be issued in the normal manner. A notation that the check has been written off should be made on the supporting invoice/documentation. Replacement checks can be documented through copies of supporting documentation for the original check and a notation explaining the situation. A check is no longer listed as outstanding on the General Fund Cash Reconciliation Form after it has been written off in the General Journal.

Checks Returned for Insufficient Funds Occasionally checks received by the school from individuals for various school activities are returned by the bank for insufficient funds. The following procedures should be followed to properly record the returned check and the subsequent re-deposit of the funds:

1. Post a journal entry in the General Fund software through the Adjustment Entry menu to record the returned check. The journal entry should be posted as a negative adjustment entry dated on the day that the school received the notice from the bank.

2. If there is a ban charge associated with the returned check, post a journal entry for the charge amount in the General Fund software through the Adjustment Entry menu to record the bank charge. The journal entry should be posted as a negative adjustment entry dated on the day the school received the notice from the bank.

3. Contact the remitter of the check to attempt to collect the funds and/or ascertain if the check

can be re-deposited. When the funds are collected or the check is re-deposited, prepare a new receipt ticket for the check amount and the bank charge (if any). Note on the receipt ticket that the receipt is for a returned check. Identify the re-deposited amount separately on the bank deposit slip.

5-4

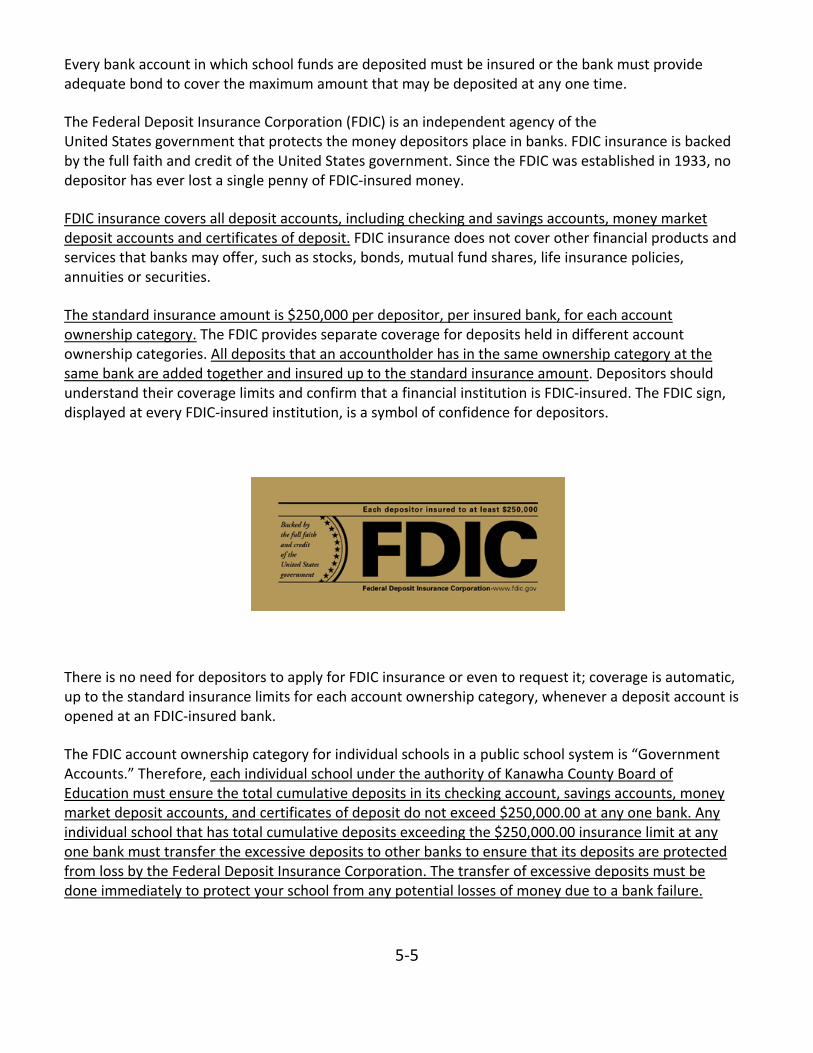

Every bank account in which school funds are deposited must be insured or the bank must provide adequate bond to cover the maximum amount that may be deposited at any one time.

The Federal Deposit Insurance Corporation (FDIC) is an independent agency of the United States government that protects the money depositors place in banks. FDIC insurance is backed by the full faith and credit of the United States government. Since the FDIC was established in 1933, no depositor has ever lost a single penny of FDIC-insured money.

FDIC insurance covers all deposit accounts, including checking and savings accounts, money market deposit accounts and certificates of deposit. FDIC insurance does not cover other financial products and services that banks may offer, such as stocks, bonds, mutual fund shares, life insurance policies, annuities or securities.

The standard insurance amount is $250,000 per depositor, per insured bank, for each account ownership category. The FDIC provides separate coverage for deposits held in different account ownership categories. All deposits that an accountholder has in the same ownership category at the same bank are added together and insured up to the standard insurance amount. Depositors should understand their coverage limits and confirm that a financial institution is FDIC-insured. The FDIC sign, displayed at every FDIC-insured institution, is a symbol of confidence for depositors.

There is no need for depositors to apply for FDIC insurance or even to request it; coverage is automatic, up to the standard insurance limits for each account ownership category, whenever a deposit account is opened at an FDIC-insured bank.

The FDIC account ownership category for individual schools in a public school system is “Government Accounts.” Therefore, each individual school under the authority of Kanawha County Board of Education must ensure the total cumulative deposits in its checking account, savings accounts, money market deposit accounts, and certificates of deposit do not exceed $250,000.00 at any one bank. Any individual school that has total cumulative deposits exceeding the $250,000.00 insurance limit at any one bank must transfer the excessive deposits to other banks to ensure that its deposits are protected from loss by the Federal Deposit Insurance Corporation. The transfer of excessive deposits must be done immediately to protect your school from any potential losses of money due to a bank failure.

5-5

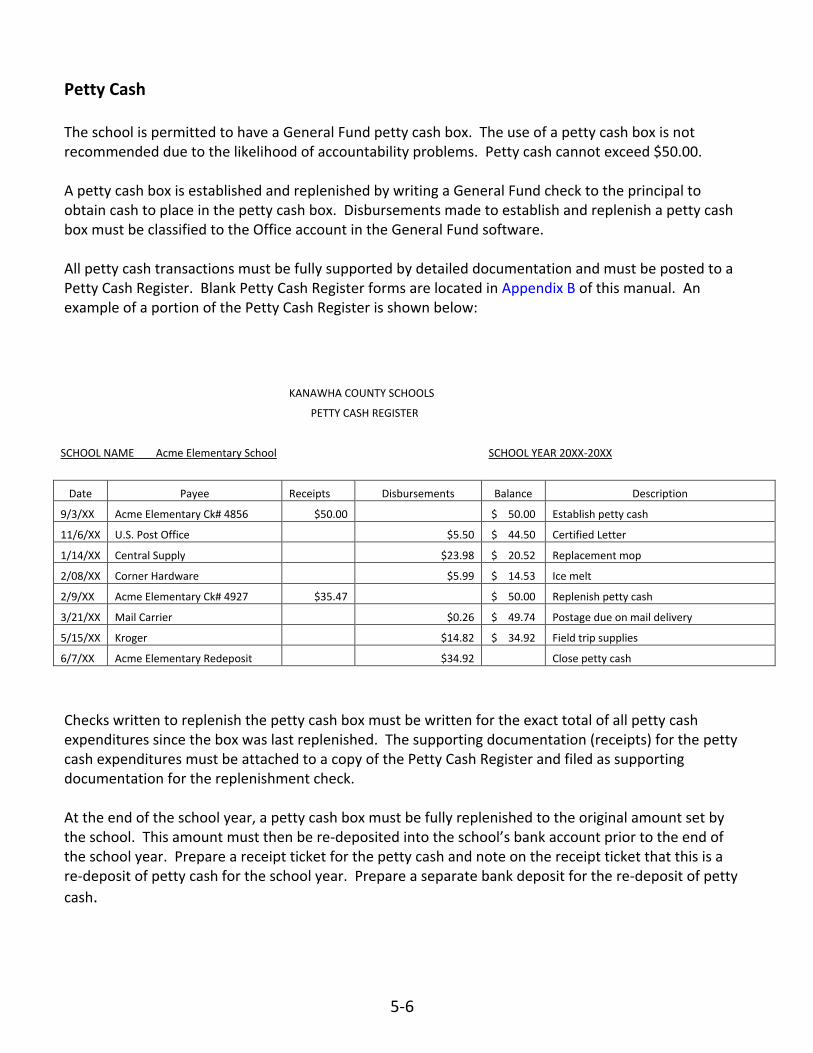

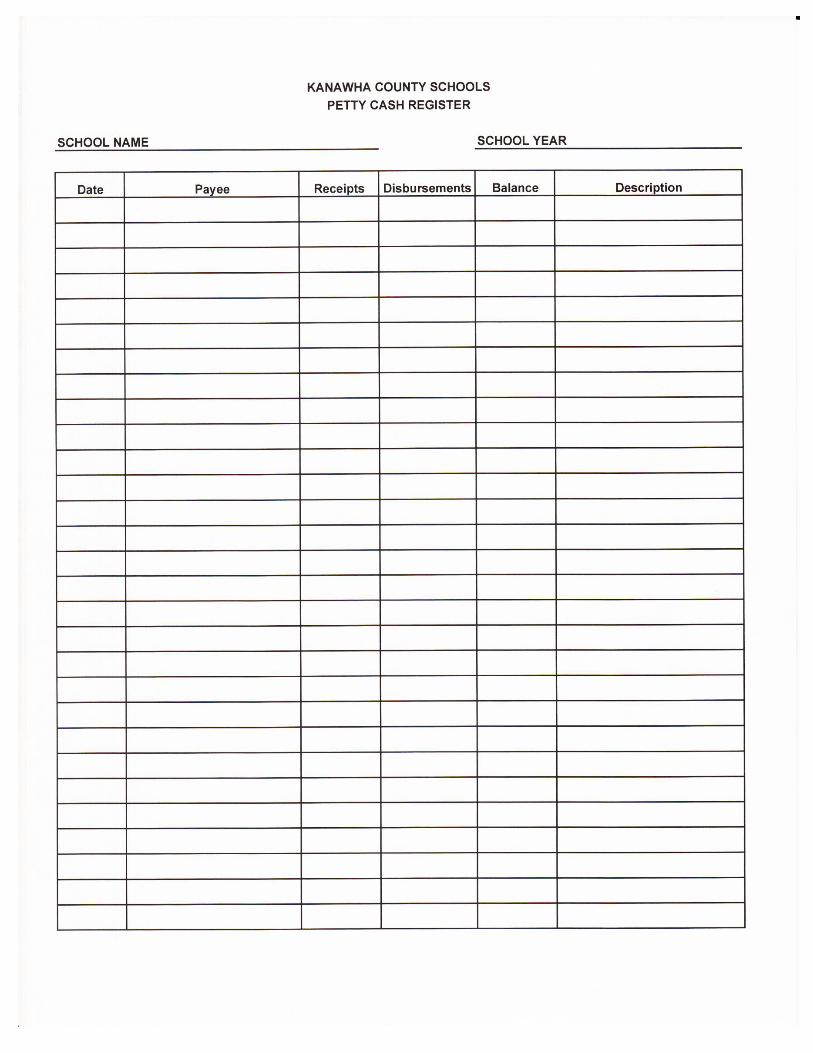

Petty Cash The school is permitted to have a General Fund petty cash box. The use of a petty cash box is not recommended due to the likelihood of accountability problems. Petty cash cannot exceed $50.00. A petty cash box is established and replenished by writing a General Fund check to the principal to obtain cash to place in the petty cash box. Disbursements made to establish and replenish a petty cash box must be classified to the Office account in the General Fund software. All petty cash transactions must be fully supported by detailed documentation and must be posted to a Petty Cash Register. Blank Petty Cash Register forms are located in Appendix B of this manual. An example of a portion of the Petty Cash Register is shown below:

KANAWHA COUNTY SCHOOLS

PETTY CASH REGISTER

SCHOOL NAME Acme Elementary School SCHOOL YEAR 20XX-20XX

Date Payee Receipts Disbursements Balance Description

9/3/XX Acme Elementary Ck# 4856 $50.00 $ 50.00 Establish petty cash

11/6/XX U.S. Post Office $5.50 $ 44.50 Certified Letter

1/14/XX Central Supply $23.98 $ 20.52 Replacement mop

2/08/XX Corner Hardware $5.99 $ 14.53 Ice melt

2/9/XX Acme Elementary Ck# 4927 $35.47 $ 50.00 Replenish petty cash

3/21/XX Mail Carrier $0.26 $ 49.74 Postage due on mail delivery

5/15/XX Kroger $14.82 $ 34.92 Field trip supplies

6/7/XX Acme Elementary Redeposit $34.92 Close petty cash

Checks written to replenish the petty cash box must be written for the exact total of all petty cash expenditures since the box was last replenished. The supporting documentation (receipts) for the petty cash expenditures must be attached to a copy of the Petty Cash Register and filed as supporting documentation for the replenishment check. At the end of the school year, a petty cash box must be fully replenished to the original amount set by the school. This amount must then be re-deposited into the school’s bank account prior to the end of the school year. Prepare a receipt ticket for the petty cash and note on the receipt ticket that this is a re-deposit of petty cash for the school year. Prepare a separate bank deposit for the re-deposit of petty

cash.

5-6

Manual of Financial Records for Kanawha County Schools

Chapter 6

Faculty Senate

Faculty Senate Allocation Annually, the faculty senate of the school will receive a legislative appropriation of $200 per each professional instructional personnel. These monies must be controlled by the faculty senate in accordance with the Manual of Financial Records for Kanawha County Schools – 7th Edition. The receipt and disbursement of all faculty senate money must be fully accounted for in the General Fund of the school. Two activity accounts must exist in the General Fund in order to fully account for all transactions that involve faculty senate money:

1. Faculty Senate – Teachers & Librarian 2. Faculty Senate – School

A $100 portion of each $200 unit of faculty senate allocation for each professional instructional personnel is to be allocated to the individual teacher, counselor, or librarian. This portion of faculty senate money is to be accounted for in the Faculty Senate – Teachers & Librarian activity account of the General Fund. The remaining $100 portion of each $200 unit of faculty senate allocation for each professional instructional personnel is to be allocated to the faculty senate of the school as a group. This portion of faculty senate money is to be accounted for in the Faculty Senate – School activity account of the General Fund. Sub-accounts can be established for each of these activity accounts to account for individual teacher allocations, if necessary.

Authorized Expenditures The $100 portion of each $200 unit of the faculty senate allocation accounted for in the Faculty Senate – School activity account of the General Fund must be expended only for academic materials, supplies or equipment. This portion of faculty senate allotment cannot be used for student travel, field trips, or incentive items to enhance student behavior or increase academic achievement.

6-1

The $100 portion of each $200 unit of the faculty senate allocation accounted for in the Faculty Senate – Teachers & Librarian activity account of the General Fund may be expended for academic materials, supplies or equipment which in the judgment of the individual teacher, counselor, or librarian will assist him/her in providing instruction. This includes expenditures for programs and materials that, in the opinion of the teacher, enhance student behavior, increase academic achievement, improve self-esteem and address the problems of students at risk. Faculty senate money can only be used for students within the school from which they are received. All purchases made by the faculty senate must be approved by the principal and supported by General Fund school purchase orders. All General Fund checks written for faculty senate expenditures must be fully supported by detailed vendor invoices or receipts. Expenditures which would cause an overdraft in a faculty senate activity account or sub-account are not permitted. The faculty senate of the school must closely monitor spending from faculty senate activity accounts to prevent overdrafts in these accounts. The faculty senate of the school must also closely monitor the spending of each individual teacher, counselor, and librarian to prevent overdrafts in individual sub-accounts. All expenditures of faculty senate money must be accounted for in the faculty senate activity accounts. Activity account transfers to/from faculty activity accounts to other activity accounts of the General Fund are not permitted. If an expenditure is to be made partially from a faculty senate activity account and partially from another General Fund activity account, then each account should be listed separately in the General Fund software when the disbursement is recorded.

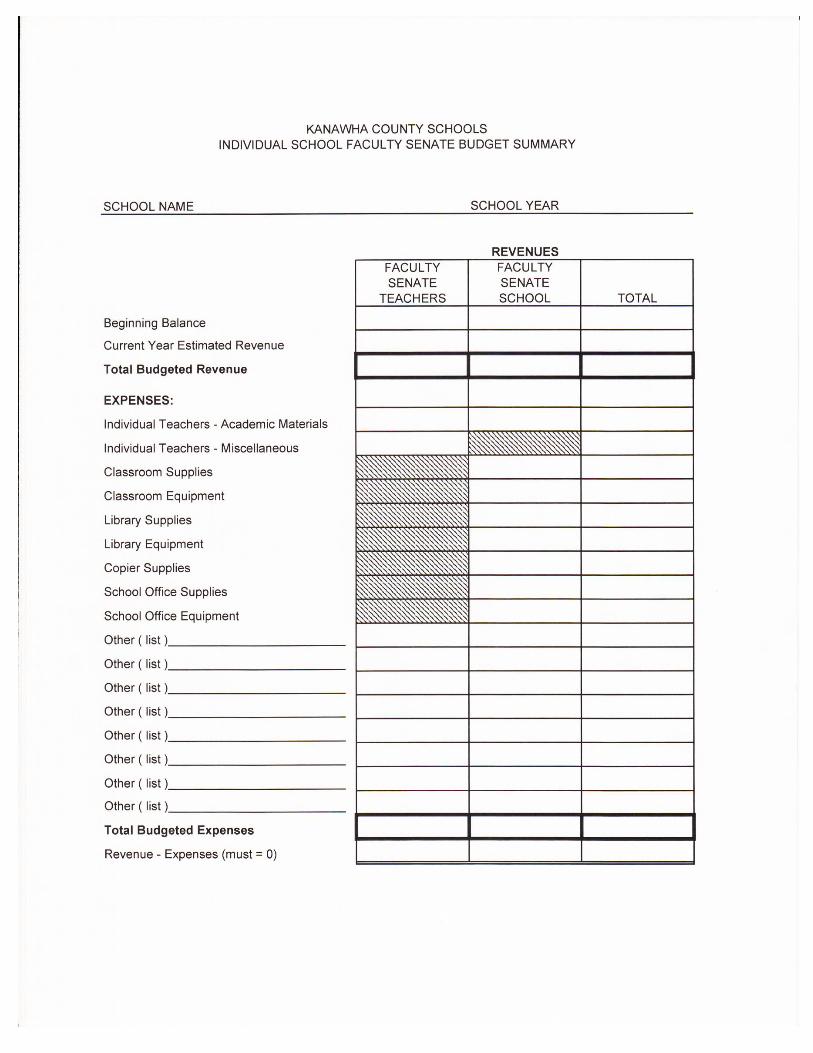

Annual Budget The faculty senate of the school is to prepare and approve an annual budget which reflects how the faculty senate monies are to be expended. This budget must be made a part of the minutes of the faculty senate meetings. The budget must be prepared and approved no later than the second regular faculty senate meeting for the school year. All expenditures of faculty senate funds must be in accordance with the faculty senate budget. The budget may be revised throughout the year if necessary provided that the revisions are approved by the membership and are clearly reflected in the minutes of the faculty senate meetings.

6-2

The budget for the current year cannot be prepared and/or approved in the previous year. The current year membership of the faculty senate must prepare and approve the budget for the current year. This includes the budgeting of any carryover money remaining from a previous year. All carryover funds (teacher and school portion of allocations) must be returned to the control of the faculty senate as a group at the beginning of the current school year. The faculty senate membership can then prepare and approve the budget which includes how the carryover monies will be allocated and expended. If the faculty senate membership votes to allow individuals to retain control of carryover money, then the budget for the current year should be prepared accordingly. The budget must be prepared using the Kanawha County Schools Individual School Faculty Senate Budget Summary form. The manually prepared version of the Individual School Faculty Senate Budget Summary form is located in Appendix B of this manual. Detailed instructions on how to complete this form are included in Appendix C of this manual.

Transfer of Faculty Senate Allocations Faculty senate allocations to a school for a specific individual must remain at that school even if the individual teacher, counselor, or librarian transfers to a different school. Faculty senate allocations are not to be transferred between faculty senates of different schools. The $100 portion of each $200 unit of faculty senate allocation which is accounted for in the Faculty Senate – School activity account must not be transferred to any other General Fund activity account including the Faculty Senate – Teachers & Librarian account during the school year. The $100 portion of each $200 unit of faculty senate allocation which is accounted for in the Faculty Senate – Teaches & Librarian activity account must not be transferred to any other General Fund activity account during the school year. If there is a previous school year carryover balance in the Faculty Senate – Teachers & Librarian activity account, and the approved budget includes returning that carryover balance to the faculty senate as a group, then a transfer to the Faculty Senate – School activity account can be made to comply with the approved budget.

6-3

Vending Machine Profit Allocation According to §18-2-6A of the West Virginia Code, seventy-five percent of the profits from soft drink sales and healthy beverages in all schools, regardless of the location of the machine, must be allocated by a majority vote of the faculty senate of the school. The remaining twenty-five percent of the profits from soft drink and healthy beverage sales is to be allocated for the purchase of necessary supplies by the school principal. A convenient way to determine the amount of soft drink and healthy beverage profits which will be allocated to the faculty senate is to set up a Soft Drinks – Faculty Senate sub account and a Soft Drinks – Supplies sub account under the Soft Drinks/Healthy Beverage or Snacks activity account. When profits from soft drink and healthy beverage sales are received, seventy-five percent of the profits should be posted to the Faculty Senate Soft Drink/Healthy Beverage sub account, and the remaining twenty-five percent should be posted to the Soft Drink/Healthy Beverage – Supplies sub account.

6-4

Manual of Financial Records for Kanawha County Schools Chapter 7

Forms, Reports and Reconciliations

General Fund Cash Reconciliation Form The General Fund Cash Reconciliation form must be prepared each month to reconcile the school’s bank account(s) to the General Fund financial records. The principal must review the General Fund Cash Reconciliation form and the accompanying bank statement(s). Both the preparer and the principal must sign the General Fund Cash Reconciliation form. The General Fund Cash Reconciliation form can be prepared manually or by utilizing Microsoft Excel. The manually prepared version of the General Fund Cash Reconciliation form is located in Appendix B of this manual. Detailed instructions for preparing the General Fund Cash Reconciliation form manually are located in Appendix C of this manual.

Monthly Financial Statement The Monthly Financial Statement is a summary of all General Fund activity of the school for the month. The Monthly Financial Statement must be prepared on or before the 10th working day of the month following the reported month. The General Fund Cash Reconciliation Form for the reported month must be completed prior to preparing the Monthly Financial Statement. Both the preparer and the principal must sign the Monthly Financial Statement. The Monthly Financial Statement must be prepared using the General Fund software. Documentation manuals for this software may be obtained from the Information Systems Department. The beginning book balance listed on the Monthly Financial Statement for the current month must agree to the ending book balance on the Monthly Financial Statement for the previous month. The ending book balance must include the total cash resources available in all depository accounts of the General Fund. All outstanding obligations must be listed on the Monthly Financial Statement. Outstanding obligations are unpaid bills and other liabilities for which the school has not yet received an invoice.

7-1

All receivables must be listed on the Monthly Financial Statement. Receivables are amounts due to the school from outside sources. All purchases of furniture or equipment that cost $1,000.00 or more must be listed on the Monthly Financial Statement. The school must retain the original copy of the Monthly Financial Statement in the financial records of the school. A copy of the Monthly Financial Statement must be submitted to the Accounting Department by the 10th of the following month, and a copy must be posted in the school office.

Annual Financial Report The Annual Financial Report is a summary of all General Fund activity of the school for the school year. The ending book balance listed on the current Annual Financial Report for the current school year must agree to the ending book balance listed on the Monthly Financial Statement for June of the current school year. Both the preparer and the principal must sign the Annual Financial Report. The Annual Financial Report must be prepared using the General Fund software. Documentation manuals for this software may be obtained from the Information Systems Department. The beginning book balance listed on the Annual Financial Report for the current school year must agree to the ending book balance on the Annual Financial Report for the previous year. The ending book balance must include the total cash resources available in all depository accounts of the General Fund. The school must not report a negative cash balance or a deficit net balance on the Annual Financial Report. In addition, a negative balance must not be reported for any activity account of the General Fund. To eliminate a deficit balance, transfers between activity accounts within the General Fund must be made before closing the books for the school year. All outstanding obligations must be listed on the Annual Financial Report. Outstanding obligations are unpaid bills and other liabilities for which the school has not yet been billed. All receivables must be listed on the Annual Financial Report. Receivables are amounts due to the school from outside sources. The school must retain the original copy of the Annual Financial Report in the financial records of the school. Two copies of the Annual Financial Report must be submitted to the Accounting Department during checkout, and one copy must be posted in the school office.

7-2

General Journal Entries Occasionally transactions of the General Fund must be recorded by the use of a general journal entry because no school check or receipt ticket was issued to reflect the transactions. In these instances, a general journal entry is posted to the General Fund software. Examples of the use of general journal entries include recording a bank charge for printing checks which was automatically deducted from the school’s bank account, or recording the charge for a check which was returned to the school for insufficient funds. All general journal entries must be posted to the General Fund software using the format JEXXX where XXX indicates the number of the general journal entry. General journal entries must be numbered beginning with 001 at the beginning of each year. General journal entries must be kept to a minimum and must be fully documented and approved by the principal. Documentation for general journal entries must be retained in the school’s financial records. A convenient way to document a general journal entry is to print the general journal entry from the General Fund software, and write a brief explanation on the printed page. The principal must approve the general journal entry by initialing the documentation.

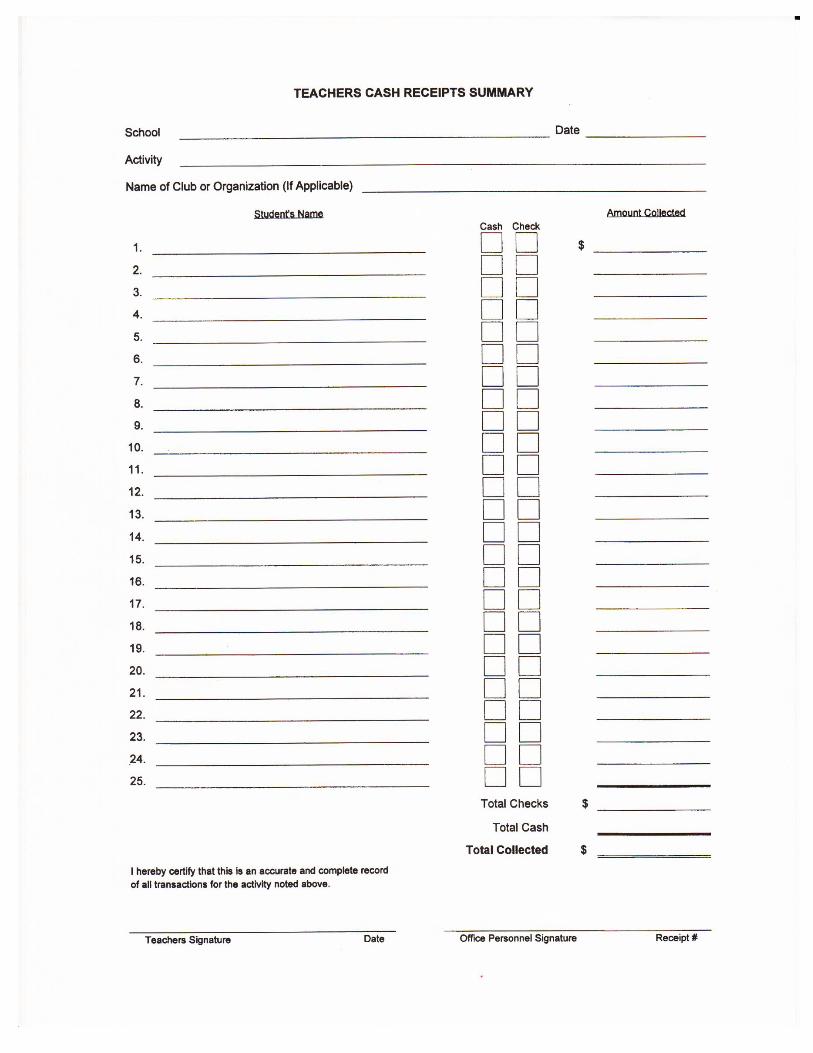

Teachers’ Cash Receipts Summary Form The Teachers’ Cash Receipts Summary form must be used when cash is collected from individual students by a teacher or other staff member and is subsequently remitted in total to the school office. The Teachers’ Cash Receipts Summary form provides a detailed accounting of monies remitted by each individual student, eliminates the need to write an individual receipt ticket to each student. A copy of the Teachers’ Cash Receipts Summary form must be submitted to the school office along with the monies collected. The individual responsible for collecting the monies must fully complete the Teachers’ Cash Receipts Summary form, including the total amount collected. Both the individual who collects the monies and the individual who receives it in the school office must sign the form. The General Fund receipt ticket number associated with the collection must be listed on the Teachers’ Cash Receipts Summary form. A copy of the Teachers’ Cash Receipts Summary form must be filed with the financial records of the school. A blank copy of the Teachers’ Cash Receipts Summary form is located in Appendix B of this manual.

7-3

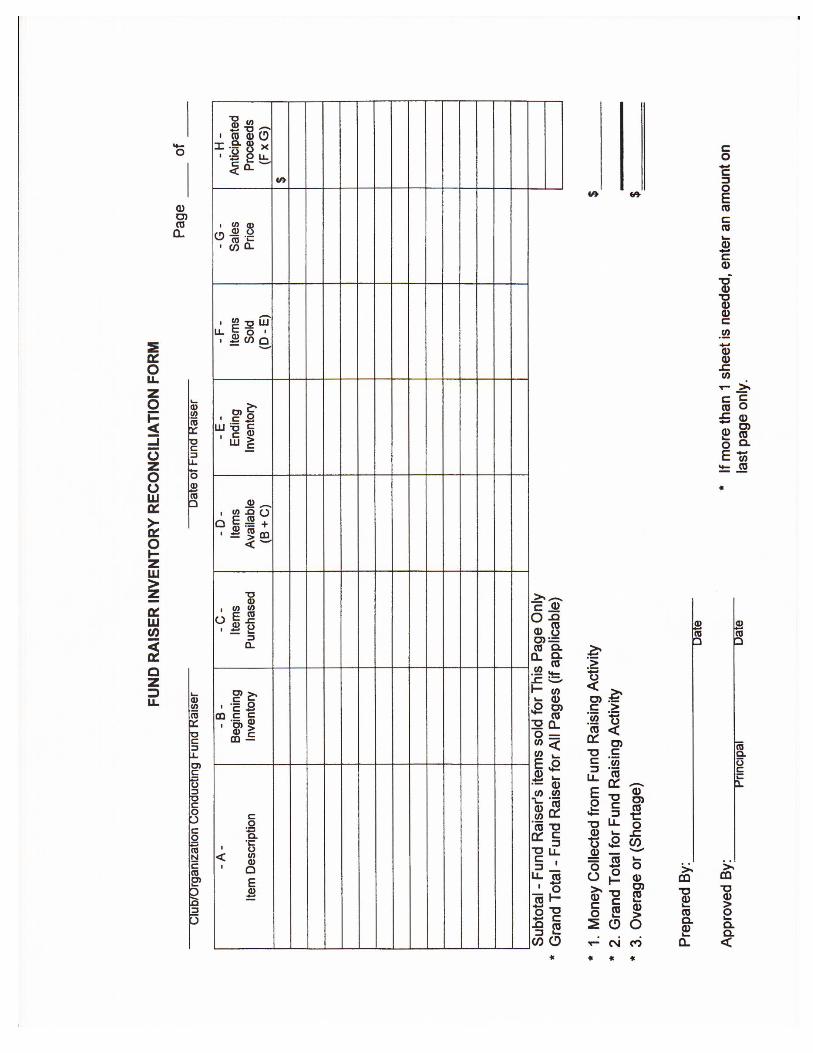

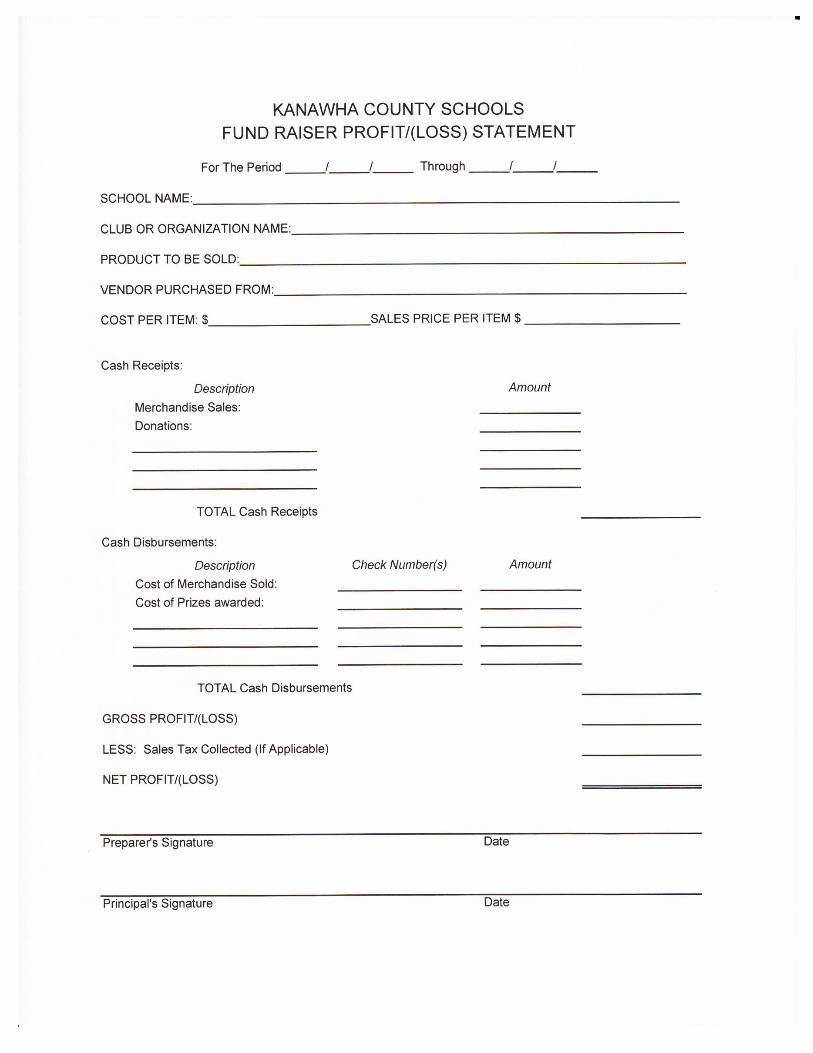

Fund Raiser Profit/(Loss) Statement The Fund Raiser Profit/(Loss) Statement must be completed to summarize an fund raising activity conducted by the school. A fund raising activity is defined as a school activity which will potentially generate a profit for the school or a specific school group or club. Typically a fundraiser involves purchasing and reselling some sort of inventory, however, some fundraisers (such as bake sales or car washes) might not require the purchase of inventories. Additional examples of fund raising activities include candy sales, sales of holiday items, and school pictures. The Fund Raiser Profit/(Loss) Statement contains a section to describe the fund raising activity, including the type of product sold, the cost of the item sold, and the sales price of the item. In instances where various items are sold with different costs and sales prices, it is permissible to indicate “various” in the product sold, item cost and sales price lines, and then attach a list of the items sold with the associated costs and sales prices. The Fund Raiser Profit/(Loss) Statement contains a section to list all cash receipts associated with the fund raiser. Any monies collected for the fund raiser must be listed in this section including any cash donations. Donations of products sold must be noted in the next section. General Fund receipt ticket numbers for the fund raiser cash receipts must be listed on the Fund Raiser Profit/(Loss) Statement. The Fund Raiser Profit/(Loss) Statement contains a section to list all cash disbursements associated with the fund raiser. Any monies expended for the fund raiser must be listed in this section, including the cost of prizes awarded to students for fund raiser participation. General Fund check numbers for the fund raiser cash disbursements must be listed on the Fund Raiser Profit/(Loss) Statement. If products sold for the fund raiser are donated and therefore there are no disbursements, then a description of the donation should be listed with the notation “donation” and zero in the amount column. A convenient way to determine receipts and disbursements associated with a specific fund raiser is to create a sub account in the General Fund software to account for the fund raising activity prior to the start of the fund raiser. As fund raiser transactions occur, they should be posted to the fund raiser sub account in the General Fund software. At the conclusion of the fund raiser, a report can be generated using the General Fund software listing all of the receipts and disbursements associated with the fund raiser. This report will be helpful in completing the cash receipts and cash disbursements sections of the Fund Raiser Profit/(Loss) Statement. Some fund raisers, such as concession stand sales, are ongoing over a period of time and necessitate stocking an inventory of merchandise to be sold. In these instances, it is necessary to complete a Fund Raiser Inventory Reconciliation Form to account for the merchandise, and to assist in the preparation of the Fund Raiser Profit/(Loss) Statement at the conclusion of the fund raiser.

7-4

The Fund Raiser Inventory Reconciliation Form must be prepared, at a minimum, each month after the sales and purchases for that month are complete. A physical inventory of merchandise must be taken each time the Fund Raiser Inventory Reconciliation Form is completed to determine if there is an overage or shortage for sales for the period. The Fund Raiser Inventory Reconciliation Form must be signed by both the preparer and the principal, and must be filed with the Fund Raiser Profit/(Loss) Statement. The Fund Raiser Profit/(Loss) Statement must be completed at the conclusion of the fund raiser and summarize all of the related Fund Raiser Inventory Reconciliation forms. Both the preparer and the principal must sign the Fund Raiser Profit/(Loss) Statement. All Fund Raiser Profit/(Loss) Statements must be filed with the financial records of the school. Fundraising activities must be covered by liability insurance. The school board’s Commercial General Liability Policy through the Board of Risk and Insurance Management (BRIM) generally includes elected or appointed officials, faculty members, employees, volunteers and student teachers acting within the scope of their duties, regardless of whether on school grounds. Blank copies of the Fund Raiser Profit/(Loss) Statement and the Fund Raiser Inventory Reconciliation Form are located in Appendix B of this manual.

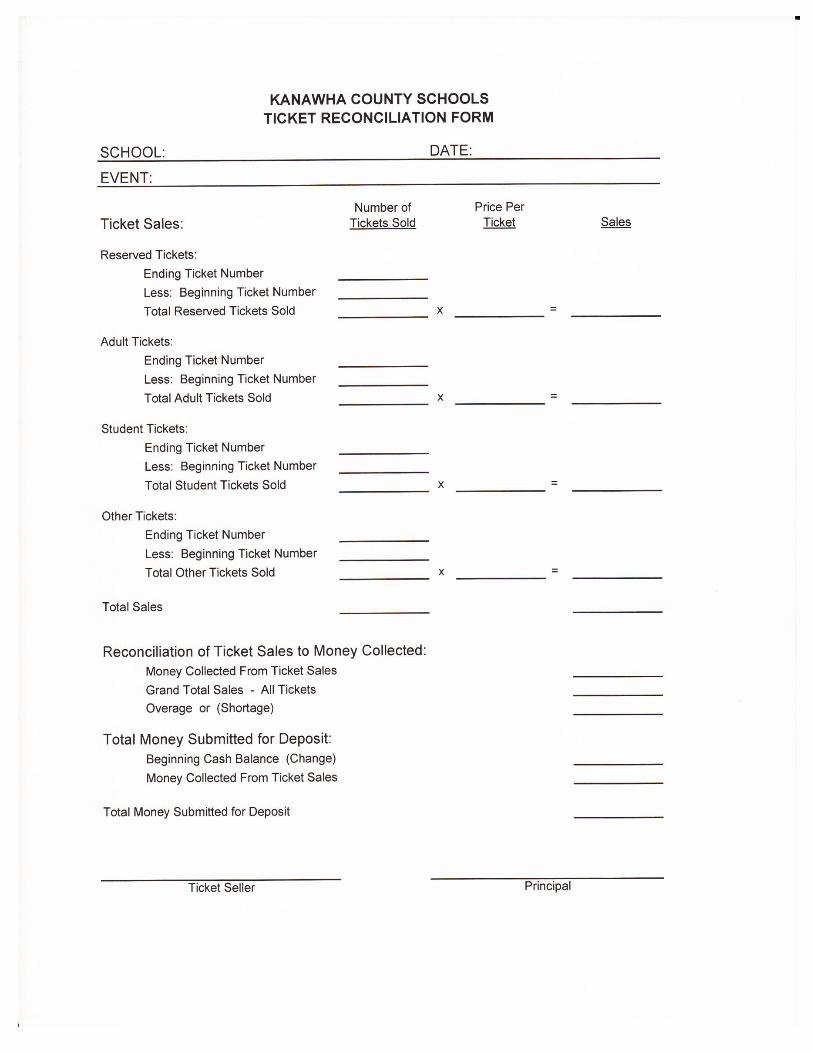

Ticket Reconciliation Form The school is required to sell tickets for any event (athletic or otherwise) for which there is a charge for admission. Tickets must be pre-numbered and issued in sequence. A Ticket Reconciliation Form must be completed by each ticket seller to summarize ticket sales for each event. Different ticket stock must be used for each type of ticket (student, adult, advance sales) so that total tickets sold can be reconciled to total cash collected. Unused ticket stock must be stored in a secure area and issued to ticket sellers prior to each event. The beginning ticket number for each type of ticket must be listed on the Ticket Reconciliation Form prior to the event. Whenever practical, separate individuals should be used to sell and collect the tickets and no individual should be used more than five times per year. Disbursements are not allowed to be made from the cash collections of school sponsored events. All cash proceeds from ticket sales of school sponsored events must be deposited intact into the school checking account. At the conclusion of the event, ticket sellers must submit Ticket Reconciliation forms to the school office along with the cash collected from the ticket sales. Ticket Reconciliation forms must be signed by the ticket seller(s) and by the principal. Ticket Reconciliation forms must be filed with the financial records of the school. A blank copy of the Ticket Reconciliation Form is located in Appendix B of this manual. Detailed instructions for preparing a Ticket Reconciliation Form are located in Appendix C of this manual.

7-5

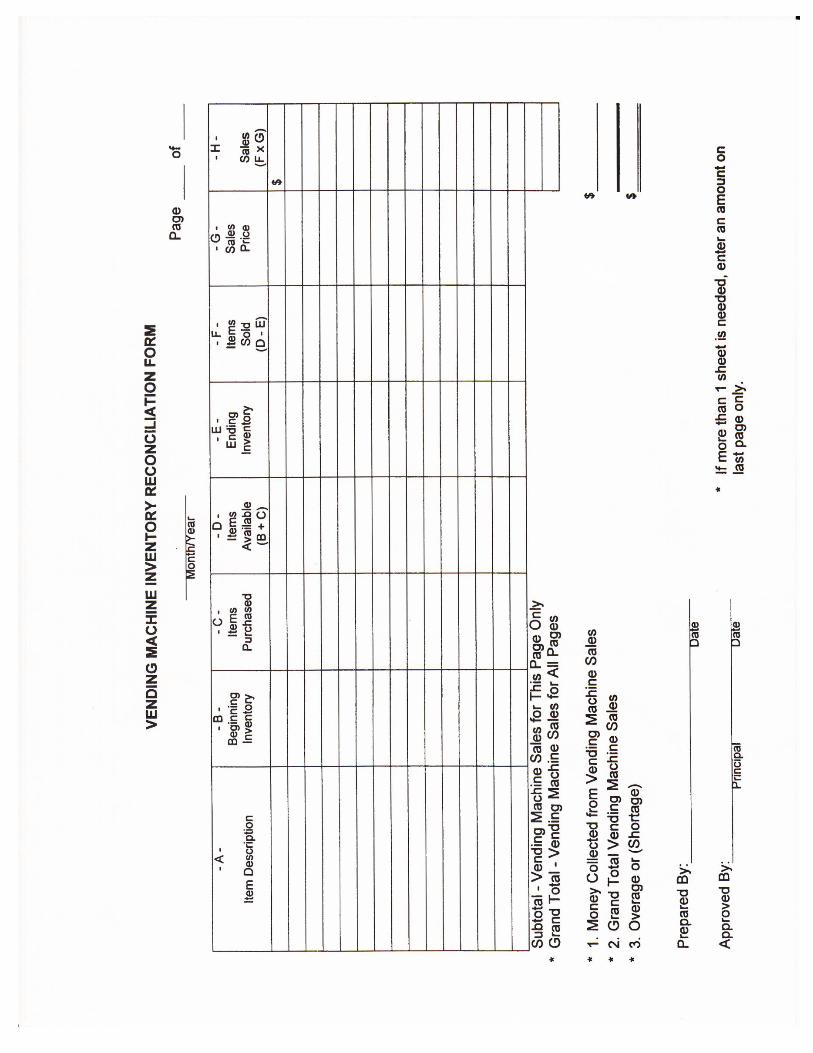

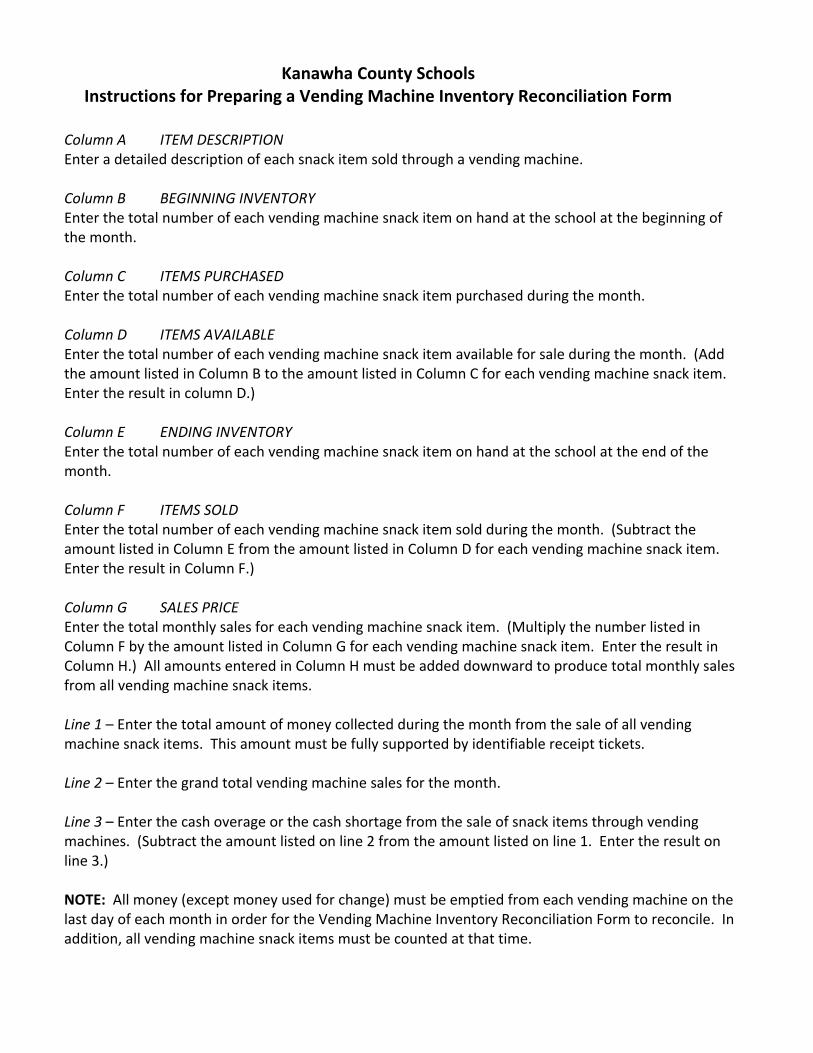

Vending Machine Inventory Reconciliation Form The school must ensure that inventory in all vending machines (snack, soft drink, healthy beverage or other) is properly accounted for in the financial records of the school. The preferred method of accounting for vending machine inventory is to utilize a full service vendor who has exclusive control of stocking inventory in the vending machines. With this method the vendor must provide reports to the school detailing the sales and commissions resulting from vending machine sales. In the event that a county contract exists for vending machine vendors, the school must utilize the county contract. Another method of accounting for vending machine inventory is for the school to be responsible for stocking inventory in the vending machines. With this method, the school must complete a Vending Machine Inventory Reconciliation Form which provides detailed information about vending machine inventory, sales, and profits. A blank copy of the Vending Machine Reconciliation Form is located in Appendix B of this manual. Detailed instructions for preparing a Vending Machine Inventory Reconciliation Form are located in Appendix C of this manual.

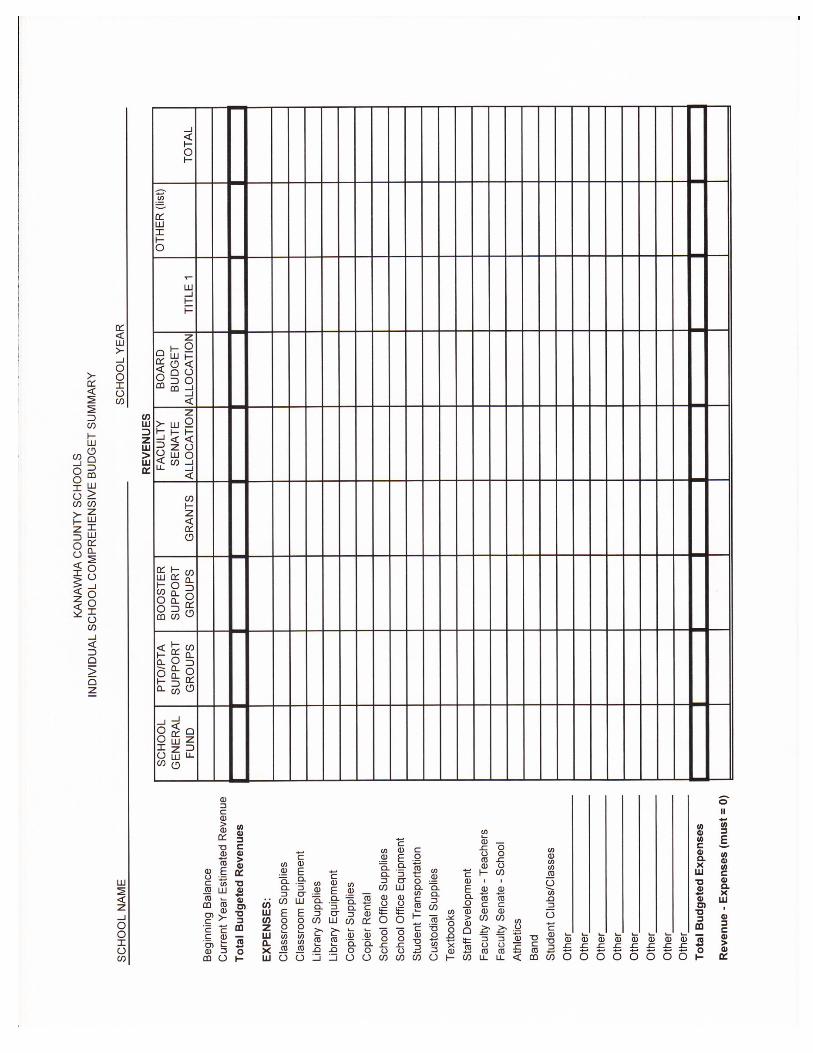

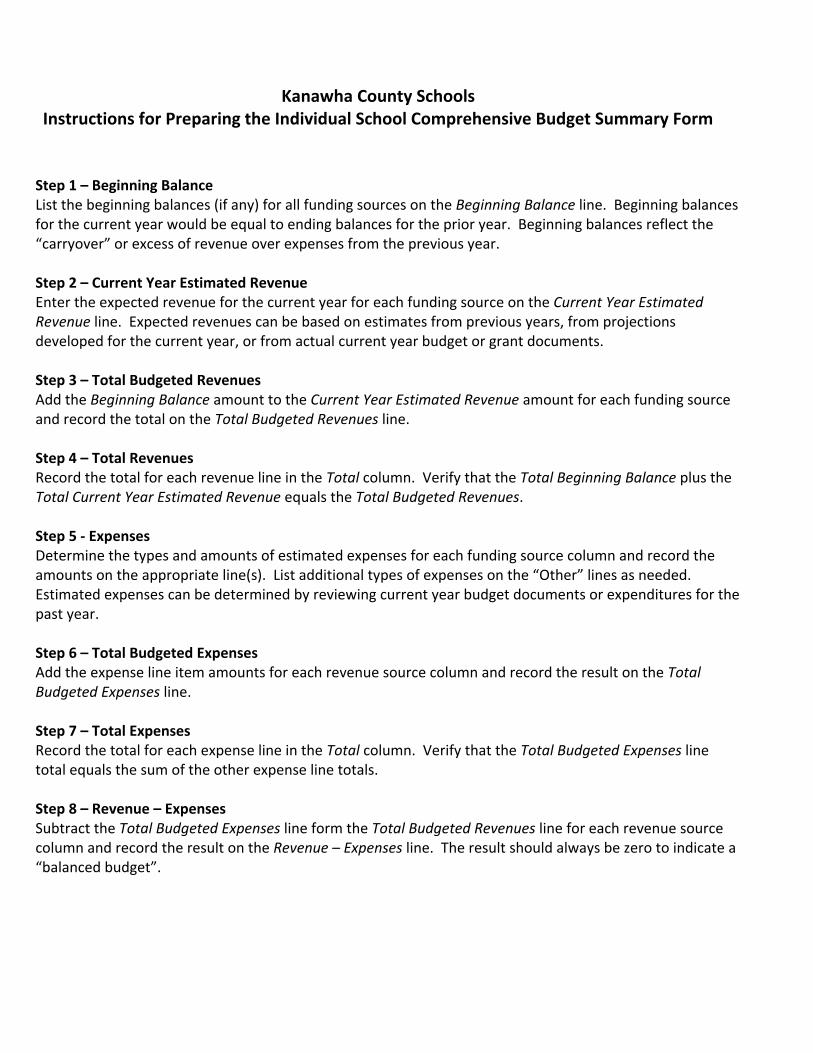

Individual School Comprehensive Budget Summary Form The Individual School Comprehensive Budget Summary Form is a required component of the school’s Unified School Improvement Plan. All funding sources available to the school for the school year are summarized on the Individual School Comprehensive Budget Summary Form, and are classified by funding source. All anticipated expenses of the school for the school year are summarized and classified by expense type. The principal must use historical data as well as short and long term plans outlined in the school’s Unified School Improvement Plan to estimate revenues and expenses when preparing the Individual School Comprehensive Budget Summary Form. The Individual School Comprehensive Budget Summary form must be filed with the school’s Unified School Improvement Plan, and a copy of the Individual School Comprehensive Budget Summary Form must be submitted each year to the Office of the Deputy Superintendent at the beginning of the each school year. The Individual School Comprehensive Budget Summary Form can be prepared manually or by utilizing Microsoft Excel. . The manually prepared version of the Individual School Comprehensive Budget Summary Form is located in Appendix B of this manual. Detailed instructions for preparing the Individual School Comprehensive Budget Summary Form are located in Appendix C of this manual.

7-6

Manual of Financial Records for Kanawha County School

Chapter 8

Miscellaneous

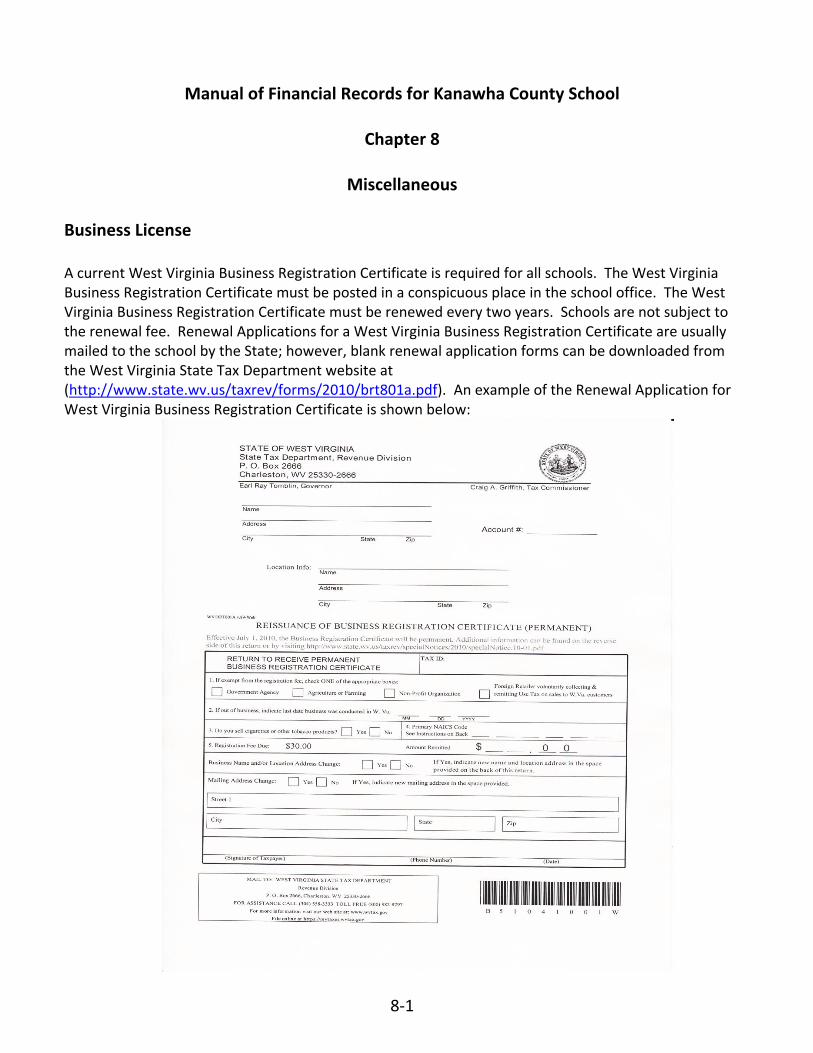

Business License A current West Virginia Business Registration Certificate is required for all schools. The West Virginia Business Registration Certificate must be posted in a conspicuous place in the school office. The West Virginia Business Registration Certificate must be renewed every two years. Schools are not subject to the renewal fee. Renewal Applications for a West Virginia Business Registration Certificate are usually mailed to the school by the State; however, blank renewal application forms can be downloaded from the West Virginia State Tax Department website at (http://www.state.wv.us/taxrev/forms/2010/brt801a.pdf). An example of the Renewal Application for West Virginia Business Registration Certificate is shown below:

8-1

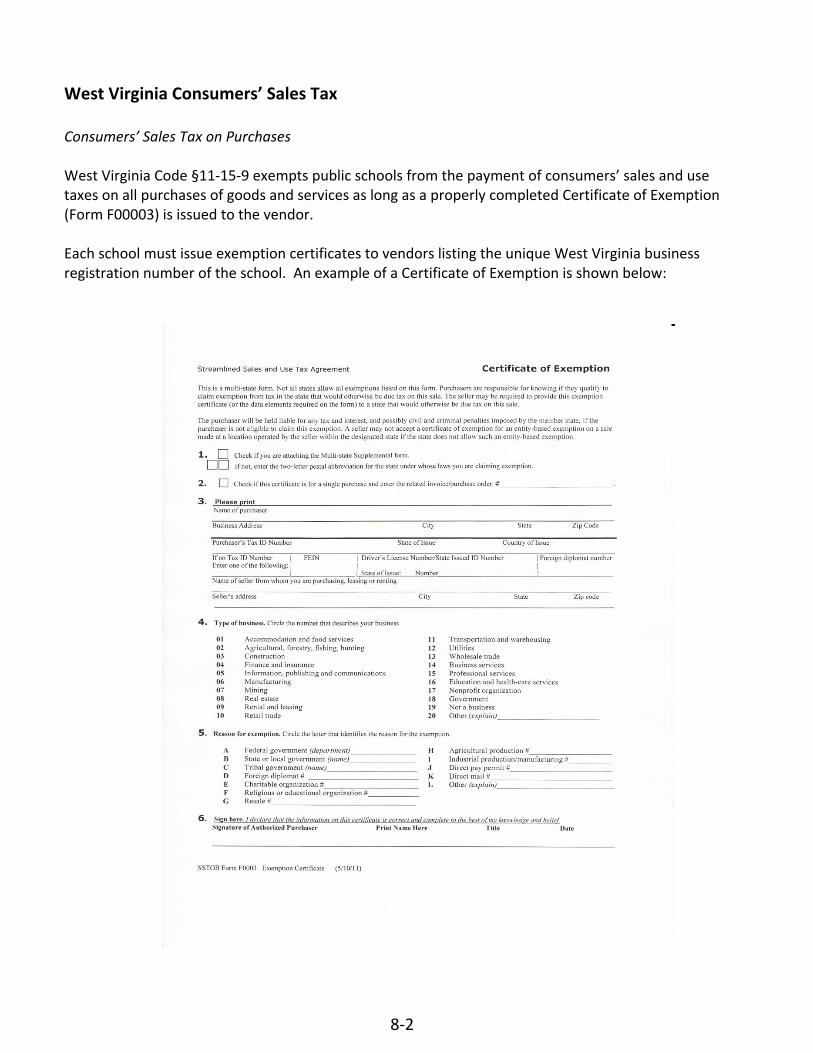

West Virginia Consumers’ Sales Tax Consumers’ Sales Tax on Purchases West Virginia Code §11-15-9 exempts public schools from the payment of consumers’ sales and use taxes on all purchases of goods and services as long as a properly completed Certificate of Exemption (Form F00003) is issued to the vendor. Each school must issue exemption certificates to vendors listing the unique West Virginia business registration number of the school. An example of a Certificate of Exemption is shown below:

8-2

Form WV/CST-580 can be downloaded from the West Virginia State Tax Department website at http://www.state.wv.us/taxrev/sst/f0003.pdf.

8-3

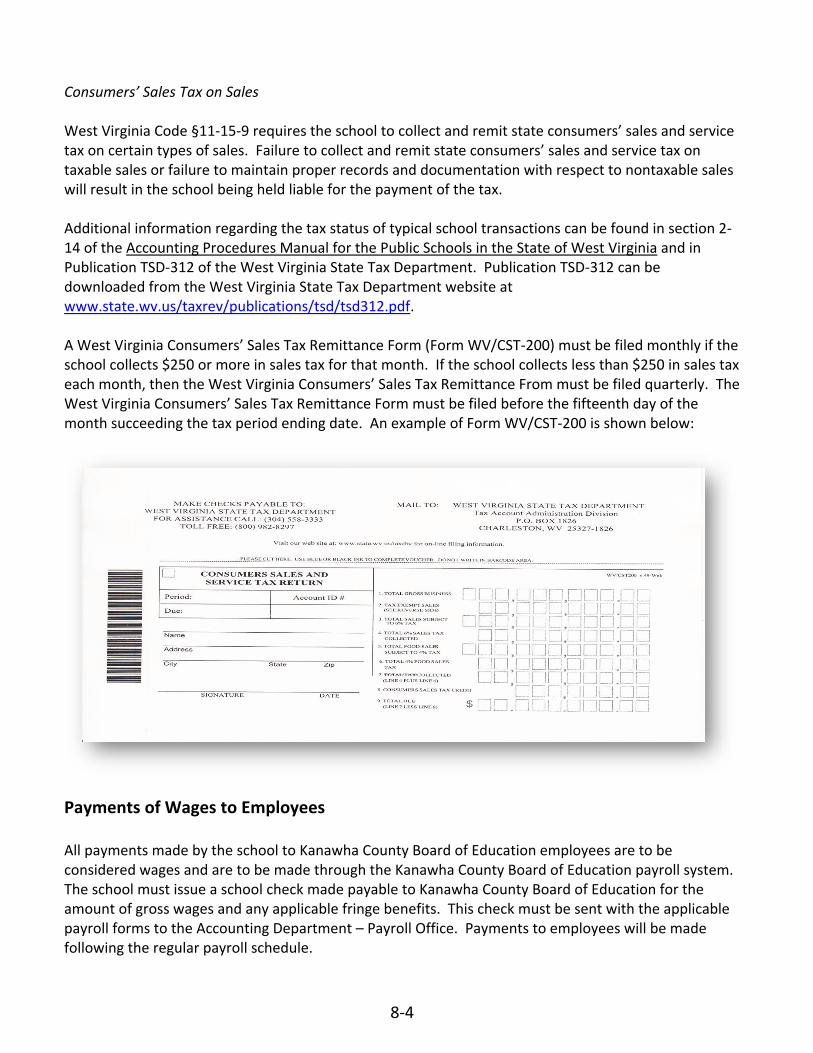

Consumers’ Sales Tax on Sales West Virginia Code §11-15-9 requires the school to collect and remit state consumers’ sales and service tax on certain types of sales. Failure to collect and remit state consumers’ sales and service tax on taxable sales or failure to maintain proper records and documentation with respect to nontaxable sales will result in the school being held liable for the payment of the tax. Additional information regarding the tax status of typical school transactions can be found in section 2-14 of the Accounting Procedures Manual for the Public Schools in the State of West Virginia and in Publication TSD-312 of the West Virginia State Tax Department. Publication TSD-312 can be downloaded from the West Virginia State Tax Department website at www.state.wv.us/taxrev/publications/tsd/tsd312.pdf. A West Virginia Consumers’ Sales Tax Remittance Form (Form WV/CST-200) must be filed monthly if the school collects $250 or more in sales tax for that month. If the school collects less than $250 in sales tax each month, then the West Virginia Consumers’ Sales Tax Remittance From must be filed quarterly. The West Virginia Consumers’ Sales Tax Remittance Form must be filed before the fifteenth day of the month succeeding the tax period ending date. An example of Form WV/CST-200 is shown below:

Payments of Wages to Employees All payments made by the school to Kanawha County Board of Education employees are to be considered wages and are to be made through the Kanawha County Board of Education payroll system. The school must issue a school check made payable to Kanawha County Board of Education for the amount of gross wages and any applicable fringe benefits. This check must be sent with the applicable payroll forms to the Accounting Department – Payroll Office. Payments to employees will be made following the regular payroll schedule.

8-4

These payments will be subject to all federal and state withholding deductions, and retirement deductions when applicable. The only exceptions are payments made to athletic officials as described in the following section.

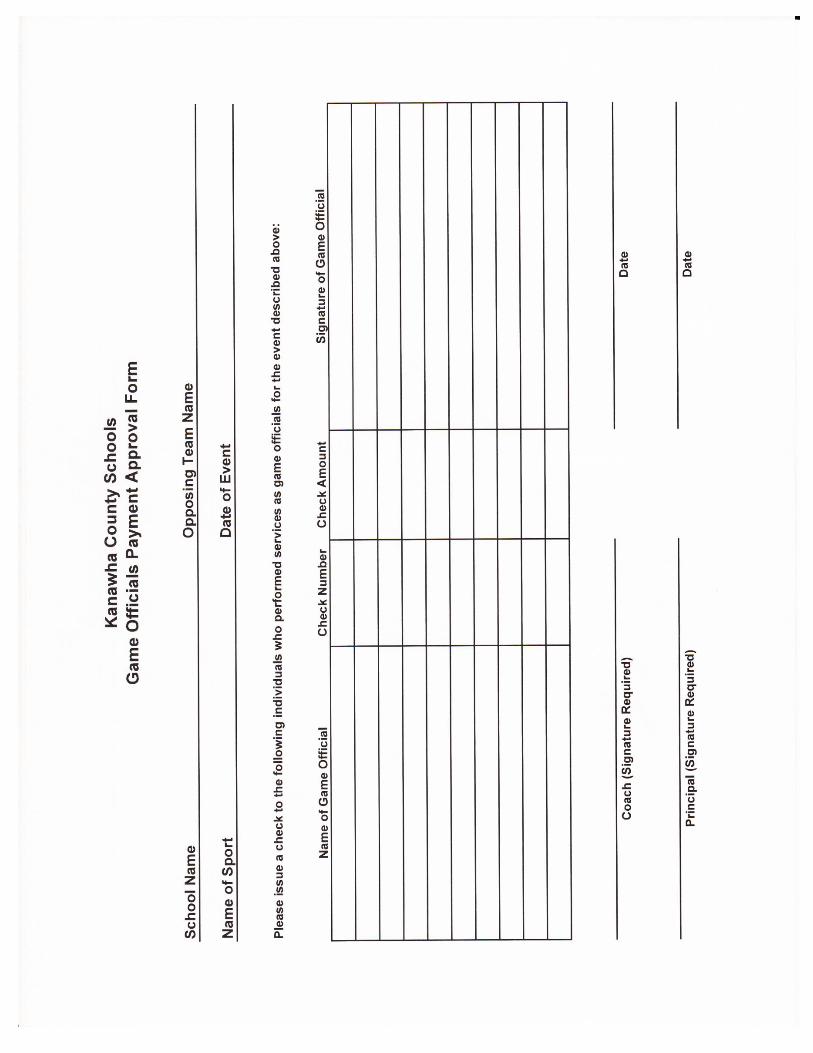

Payments to Game Officials The issuance of school checks as compensation to individuals who are employed by the Kanawha County Board of Education is only allowed in the specific situation whereby the employee performs services as a game official for an interscholastic athletic event sanctioned by the West Virginia Secondary Schools Activities Commission. All other employees who perform compensable services for the school must be paid through the Kanawha County Board of Education payroll system as described in the preceding section. Payments by a school to individuals who perform as game officials must be supported by a Game Officials Payment Approval Form. Game officials must complete an Internal Revenue Service Form W-9.

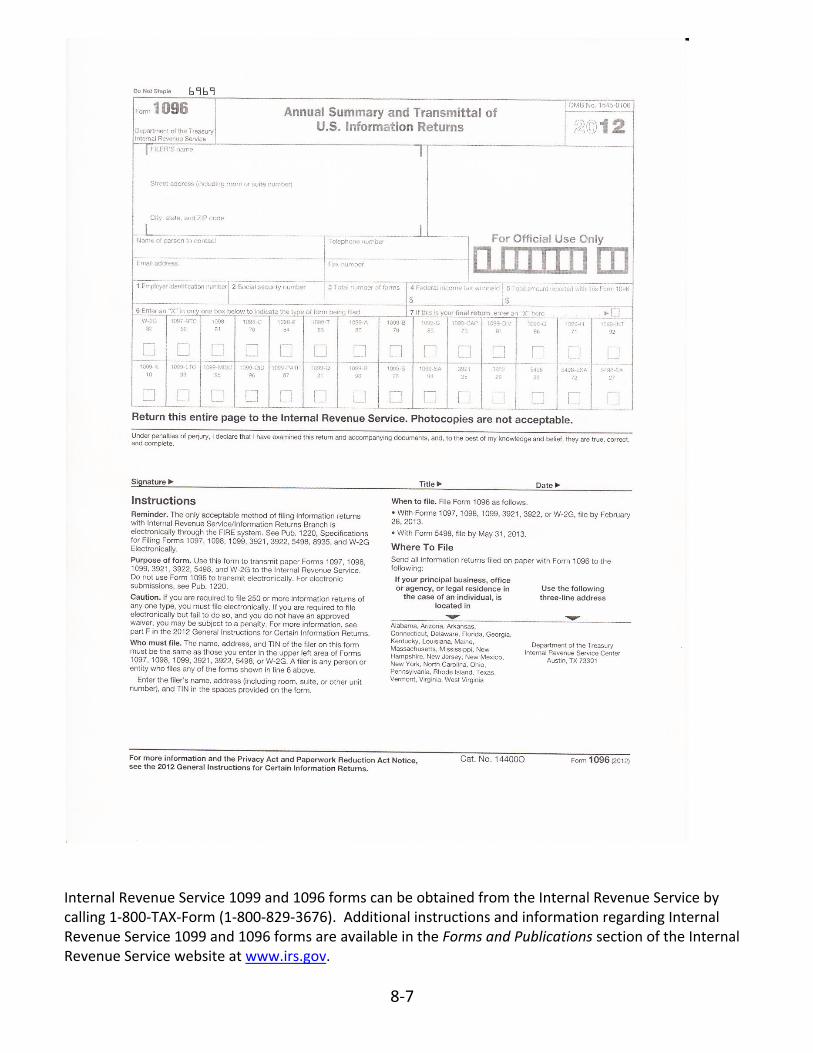

The Game Officials Payment Approval Form is included in Appendix B of this manual.