Embed Size (px)

Citation preview

Mark WestPartner

21 August 2014

Possible tax loss credit (swap) scheme

30943335 2

Background - the concern

■Reflects considerations by;

□Grant Fawcett CEO Northern Gulf Resource Management Group

□Professor Flavio Menezes Head of School of Economics UQ

■Extraordinary circumstances have led to significant losses funded by significant debt

■Seeking an effective way to ‘access’ tax losses to assist viable businesses by way of debt reductions

■Aim of removing (reducing) debt from the agribusiness sector

30943335 3

What could a proposal involve?

■In summary :

□to allow ‘trading’ of tax losses (from primary production) with a bank in return for a reduction in their debt to the at bank

□the bank would be able to claim the loss against its taxable income

■Economic and tax issues

■Only losses from prior years

■Would need to be eligibility and integrity rules

30943335 4

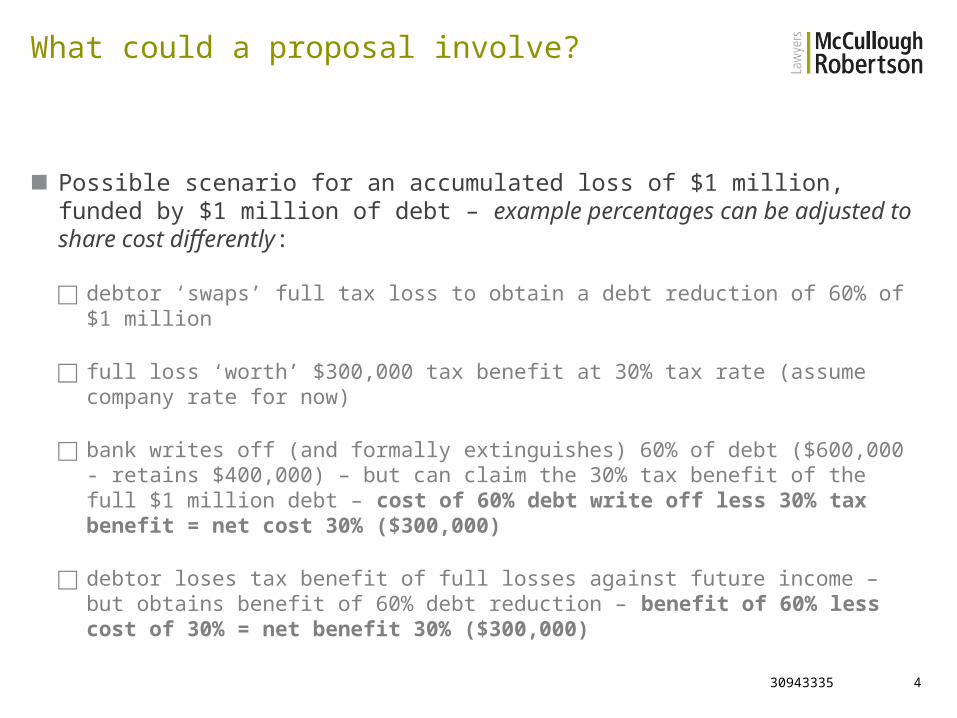

What could a proposal involve?

■Possible scenario for an accumulated loss of $1 million, funded by $1 million of debt – example percentages can be adjusted to share cost differently:

□debtor ‘swaps’ full tax loss to obtain a debt reduction of 60% of $1 million

□full loss ‘worth’ $300,000 tax benefit at 30% tax rate (assume company rate for now)

□bank writes off (and formally extinguishes) 60% of debt ($600,000 - retains $400,000) – but can claim the 30% tax benefit of the full $1 million debt – cost of 60% debt write off less 30% tax benefit = net cost 30% ($300,000)

□debtor loses tax benefit of full losses against future income – but obtains benefit of 60% debt reduction – benefit of 60% less cost of 30% = net benefit 30% ($300,000)

30943335 5

What could a proposal involve?

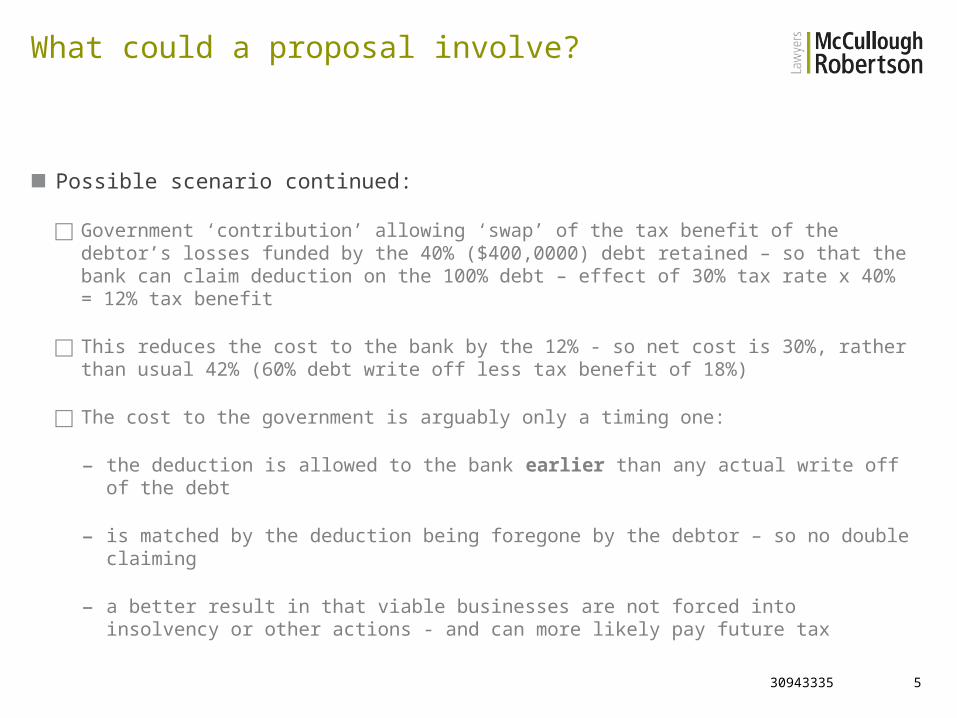

■Possible scenario continued:

□Government ‘contribution’ allowing ‘swap’ of the tax benefit of the debtor’s losses funded by the 40% ($400,0000) debt retained – so that the bank can claim deduction on the 100% debt – effect of 30% tax rate x 40% = 12% tax benefit

□This reduces the cost to the bank by the 12% - so net cost is 30%, rather than usual 42% (60% debt write off less tax benefit of 18%)

□The cost to the government is arguably only a timing one:

– the deduction is allowed to the bank earlier than any actual write off of the debt

– is matched by the deduction being foregone by the debtor – so no double claiming

– a better result in that viable businesses are not forced into insolvency or other actions - and can more likely pay future tax

30943335 6

Issues

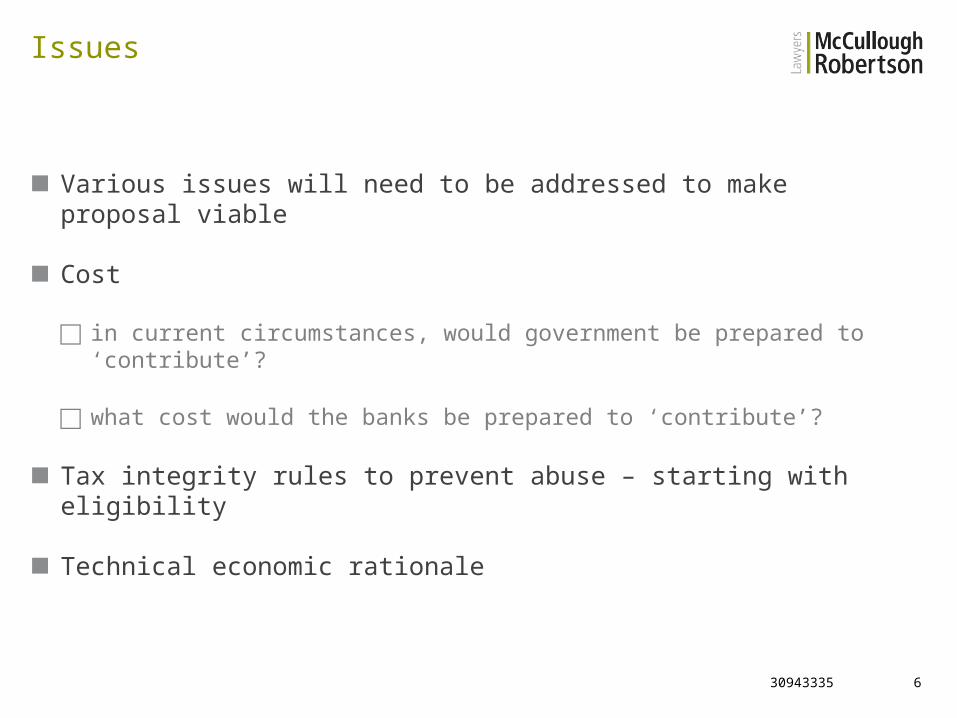

■Various issues will need to be addressed to make proposal viable

■Cost

□in current circumstances, would government be prepared to ‘contribute’?

□what cost would the banks be prepared to ‘contribute’?

■Tax integrity rules to prevent abuse – starting with eligibility

■Technical economic rationale

30943335 7

Contact

Mark WestPartnerT +61 7 3233 8871 (Brisbane)T +61 2 9270 8620 (Sydney)E [email protected]

Disclaimer: This presentation covers legal and technical issues in a general way. It is not designed to express opinions on specific cases. This presentation is intended for information purposes only and should not be regarded as legal advice. Further advice should be obtained before taking action on any issue dealt with in this presentation.