Embed Size (px)

Citation preview

© 2

012

Tiet

o C

orpo

ratio

n

Market dynamics and Tieto value creation in 2012–2016Kimmo Alkio

© 2

012

Tiet

o C

orpo

ratio

nMacro trends

Social

Changing demographicsData explosionSocial networks

Economic

EfficiencyGlobalizationEcosystems

Technology

MobilityCloud

Big data

© 2

012

Tiet

o C

orpo

ratio

nIT industry drivers

Social

Changing demographicsData explosionSocial networks

Economic

EfficiencyGlobalizationEcosystems

Technology

MobilityCloud

Big data Efficient business transformation

Unlimited global opportunities

Ecosystems as innovation engine

Enterprise mobility & BYODCloud adoption

Intelligence everywhere and predictive analytics

Building information societyPower and value of

informationSocial enterprise

From information

and automation to innovation and

business transformation

© 2

012

Tiet

o C

orpo

ratio

n

Competitive Edge

Strong customer base ~800

Outsourcing-Software-Integration

Industry and customer process

insight

Industry products and IPR

Nordics as core

Global delivery scale

Leading PES capabilities

Tieto driving customers’ transformation

Expanding to provide full life-cycle

IT services

Reinforce industryexpertise

Focus on selected markets

Realize “full stack”opportunity with CSI

Industry specificsolution packaging

Growth in Nordics and selective expansion

MS automation and efficiency

Drive new business models e.g. SaaS

Expand PES global customer base

New technologies and alliances

Transformation services

Accelerate global delivery

© 2

011

Tie

to C

orpo

ratio

nAttractiveness of Nordics

Worlds 8th largest economy• 25 million inhabitants, GDP growth 1.5%• Stable financial, political and social environment• IT market size EUR 40 billion• Educated society

Customers value a trusted local partner• Demand for local culture and regulatory knowledge• Emphasize social responsibility and transparency• Customer process knowledge as a pre-requisite for IT

transformation partner

Technology innovation and adaptation• All Nordic countries among top 10 in internet penetration• Long track record of technology innovation• Appetite for embracing new services and technologies

© 2

012

Tiet

o C

orpo

ratio

nMarket drivers and opportunities

© 2

012

Tiet

o C

orpo

ratio

n

Market drivers

2010 2015 2020

New offering CAGR +25%

Basic offering CAGR -1 to -3%

Data doubles every 40 months

50 billion devices connected by 2020

Need for predictive analytics to become critical success factor

Mobility

Big Data Cloud

Social Media

500% wireless penetration is possible

Mobile connected devices to double by 2020

85% said Internet has positive effect on their social world

Online and offline worlds will accelerate changing behavior

Highly engaging virtual social world will dominate future workplaces

Multiple sources

© 2

012

Tiet

o C

orpo

ratio

n

Market drivers and opportunities

Mobility

Big Data Cloud

Social Media

• Eureka as enterprise and public crowd-sourcing solution (e.g. City of Helsinki, OP-Pohjola)

• Enterprise transformation with Social media and traditional intranet

• Proactive transformation with large infrastructure customers

• Industry specific cloud services (e.g. Lifecare)

• Cloud integration as value driver

• Predictive analytics for transaction centric industries

• Unstructured data as a source of innovation

• Modernizing information management

• New services and user experiences across all industries

• Smart devices and applications with global PES customers

© 2

012

Tiet

o C

orpo

ratio

n

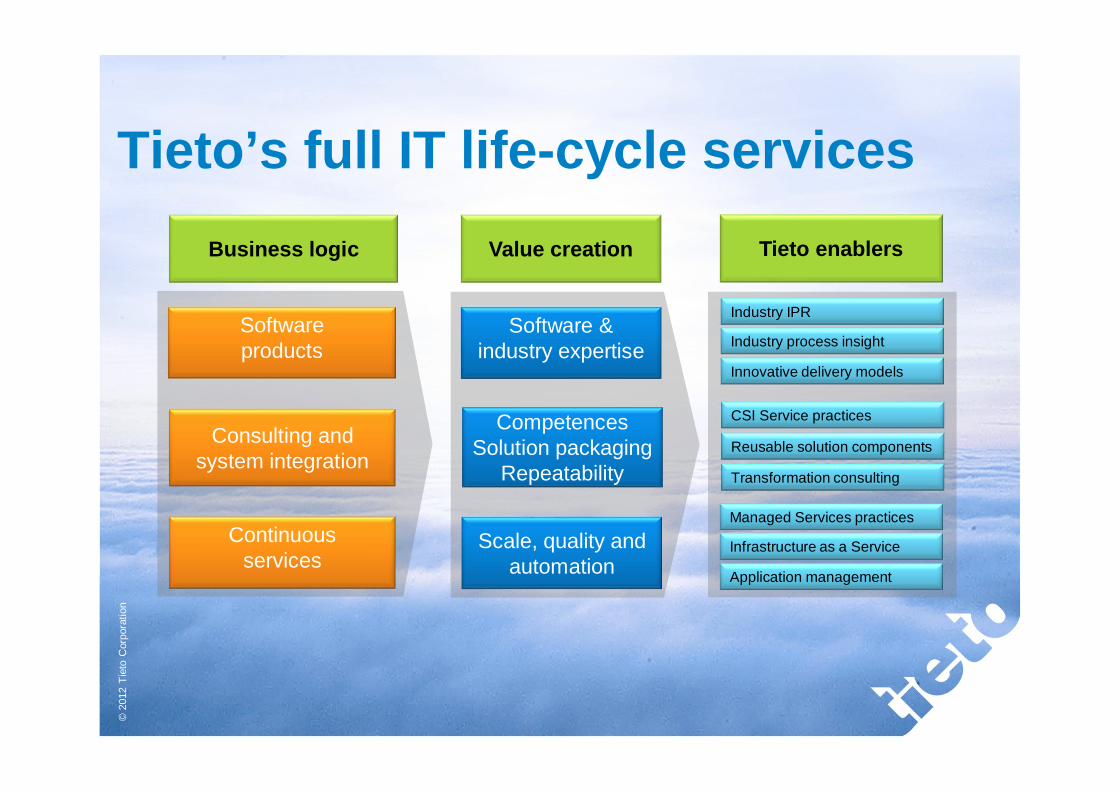

Tieto’s full IT life-cycle servicesBusiness logic Value creation Tieto enablers

Consulting and system integration

CSI Service practicesCompetencesSolution packaging

RepeatabilityReusable solution components

Transformation consulting

Software products

Software & industry expertise

Industry IPR

Industry process insight

Innovative delivery models

Continuous services

Scale, quality and automation

Managed Services practices

Infrastructure as a Service

Application management

© 2

012

Tiet

o C

orpo

ratio

n

Software products

Utilities

Oil & Gas

Software products

Manufacturing

Forest, pulp and paper

Software products

Healthcare and Welfare

Software products

Insurance

Transaction banking

Capital markets

Managed services

Financial Services

Public, Healthcare and Welfare

Manufacturing, Retail & Logistics

Telecom, Media and Energy

Consulting and System Integration

Business & Transformation ConsultingFront-end and AnalyticsEnterprise applicationsIT Solutions and System development

Shared Infrastructure Services

Application ManagementCloud services

Customer specific infrastructure Services

TCM

eBankingCBS

Life insurance

CardSuite

Probroker

Abasec

PaymentSuiteLean

TIPPTIPS

Powergrid / NAM

CAB / WMS

AMI

Energy Components

ForumLifecare

E3

Tieto’s product and service offeringProduct EngineeringServices

Network InfrastructureSolutions

ConnectedLife Solutions

© 2012 Tieto Corporation

Proven expertise in Nordic industries

© 2

012

Tiet

o C

orpo

ratio

n

Value creation in 2012–2016

© 2

012

Tiet

o C

orpo

ratio

n

Value creation and Total shareholder return in 2012–2016

TSR above peer

groupaverage*

CSI

Competitivecost structure

Healthy operative cash flow

Selectiveexpansions

Quality

PES

Business mix

Growth

Profit improvement

Cash flow

Shareholder value

Attractive dividend yield

Optimal capital structure

Transformationservices

Offshoring and automation

*EPS growth and TSR as targets in the Long-Term Incentive Programme 2012–2015

© 2

010

Tiet

o C

orpo

ratio

n

Offsetting factors

Value creation

Simplification

Customer value

Future growth

• Simplified organization, practices and cost structure

• Optimizing for profit outside Nordics

• Initiate transformation programs with key customers towards new full life-cycle services

• Global delivery and MS automation

• Launch focused industry repeatable services (cloud, analytics)

• Enable PES to pursue global opportunities

• Inflation• Price erosion• Revenue cannibalization• Macro economic uncertainty

2012-2013

• Continue driving to a benchmarked cost structure

• Consider bolt-on acquisitions

• Expanding transformation services to the 800 customer base

• Expand customer base with new services

• Global delivery

• Identify future markets for growth and launch spearhead industry packages

• PES global expansion

• Inflation• Price erosion• Revenue cannibalization• Macro economic uncertainty• Saturation of outsourcing

2014-2015

• Prepare organization for possible M&A and integrations

• Launch repeatable full life-cycle IT services in future growth markets

• Global delivery• PES recognized as a

global player

• Expand in new markets for IT services

• Inflation• Price erosion• Revenue

cannibalization• Macro economic

uncertainty• Competition

~2016

© 2

012

Tiet

o C

orpo

ratio

nThis provides an opportunity for revenue growth and improved profitability

Growth

Tieto focus

•Transformation and CSI•MS Automation•Competitive cost structure•PES global expansion•Global delivery

Size of the bubble represents revenue in 2012 and 2016 (M€)

Tieto target profitability 2016

Average market growth

EBIT

%

Tieto 2012

Tieto 2016

© 2

012

Tiet

o C

orpo

ratio

n

Tieto target profitability 2016

Average market growth

MS 2012

MS 2016

Managed Services

Tieto target profitability 2016

Consulting and integration

Application Management

CSI 2012

Consulting and System Integration

Tieto target profitability 2016

Average market growth

IP 2012

IP 2016

Average market growth

Tieto target profitability 2016

PES 2012

PES 2016

Product Engineering ServicesIndustry Products

Average market growth

CSI 2016

© 2

012

Tiet

o C

orpo

ratio

nOur long-term journey proceeds as planned

2012Build the foundation

2013-2014Expand servicescope

2015-2016Focus onfuture growth

• Transition to industry driven structure• Accelerate Consulting and System Integration

expansion and Managed Services automation• Implement competitive cost structure• Focus on 2012 operating plan

• Expand full life-cycle IT services in core markets• Qualify and build future core markets• Product Engineering Services pursues growth globally

• Seek growth in and beyond core markets

• Consider strategic inorganic opportunities

© 2

012

Tiet

o C

orpo

ratio

n

Leading IT transformation partner in Nordics

Innovation and technology adaptation

Full life-cycle IT services with industry and customer process insight

High quality and repeatable solutions driving future growth

Attractive shareholder valueExpansion to new markets and PES globally

Focus on successful strategy execution

© 2

012

Tiet

o C

orpo

ratio

n

Organization structure

New MarketsKolbjørn Haarr

Financial ServicesPer Johanson

Public,Healthcareand WelfareSatu Kiiskinen(as of 1 Jan 2013)

Manufacturing,Retail andLogisticsAri Järvelä

Telecom, Media, Energy and UtilitiesEva Gidlöf

CFO, Lasse Heinonen

ProductEngineeringServicesAntti Vasara

CEOKimmo Alkio

Consulting and System IntegrationHenrik Sund

Managed ServicesAri Karppinen

HR, Katariina Kravi

© 2

012

Tiet

o C

orpo

ratio

n