Embed Size (px)

Citation preview

THINK AHEAD. STAY AHEAD.

MARKET OUTLOOK:

WHAT’S NEW…WHAT’S THE RISK?

JANUARY 2017

Michael White, CFA

Portfolio Manager

1

-----------------------------------

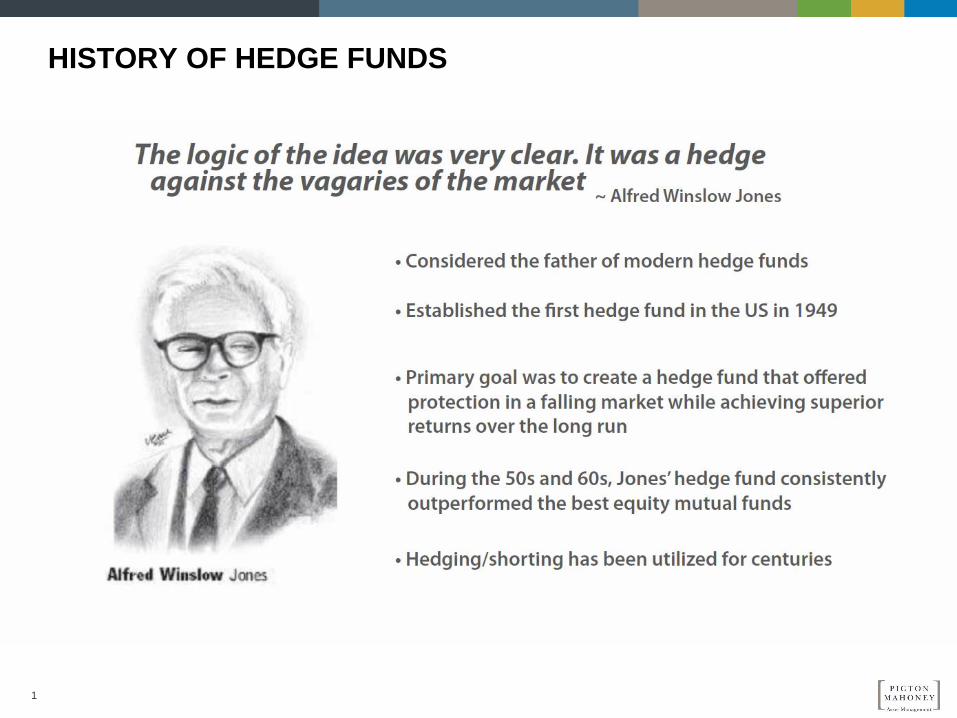

HISTORY OF HEDGE FUNDS

2

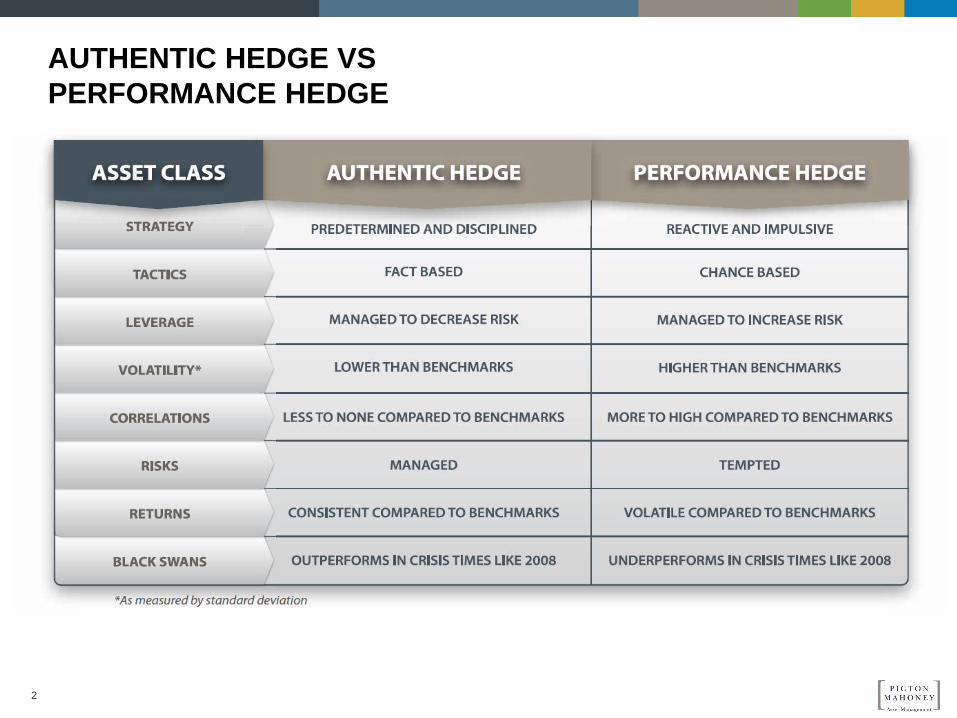

AUTHENTIC HEDGE VS

PERFORMANCE HEDGE

3

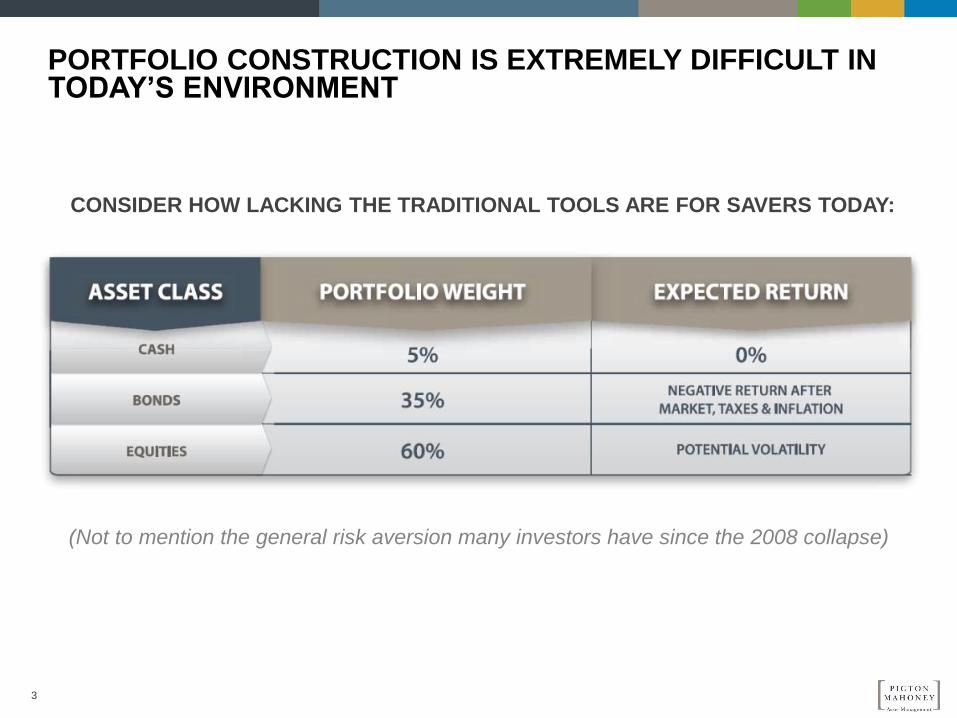

PORTFOLIO CONSTRUCTION IS EXTREMELY DIFFICULT IN TODAY’S ENVIRONMENT

CONSIDER HOW LACKING THE TRADITIONAL TOOLS ARE FOR SAVERS TODAY:

(Not to mention the general risk aversion many investors have since the 2008 collapse)

4

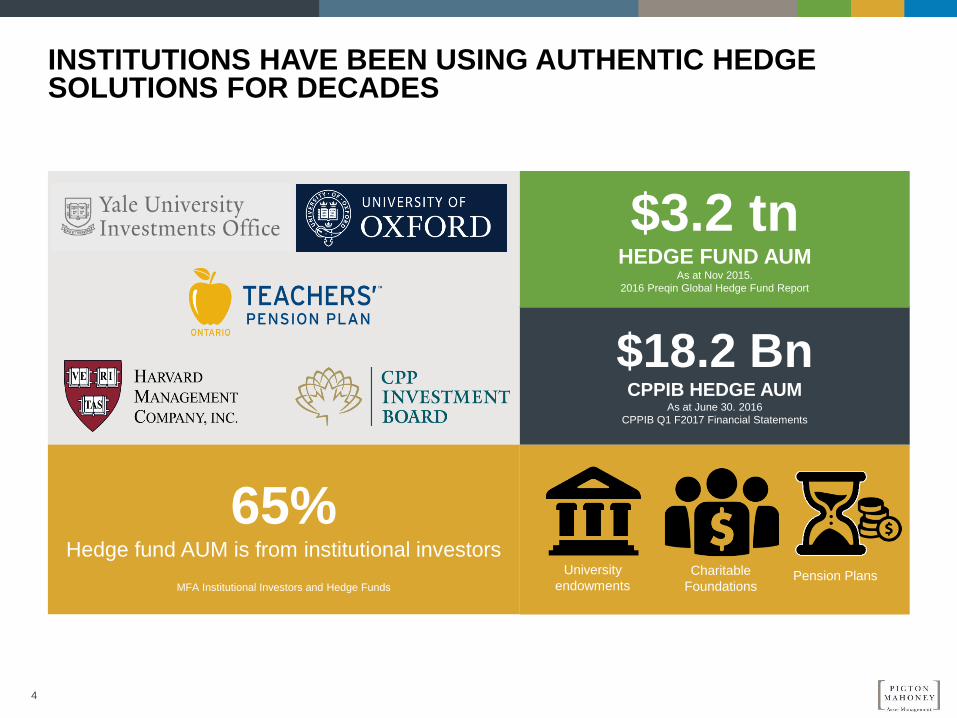

65%

Hedge fund AUM is from institutional investors

MFA Institutional Investors and Hedge Funds

INSTITUTIONS HAVE BEEN USING AUTHENTIC HEDGE SOLUTIONS FOR DECADES

$18.2 Bn CPPIB HEDGE AUM

As at June 30. 2016

CPPIB Q1 F2017 Financial Statements

$3.2 tn HEDGE FUND AUM

As at Nov 2015.

2016 Preqin Global Hedge Fund Report

University

endowments Charitable

Foundations Pension Plans

5

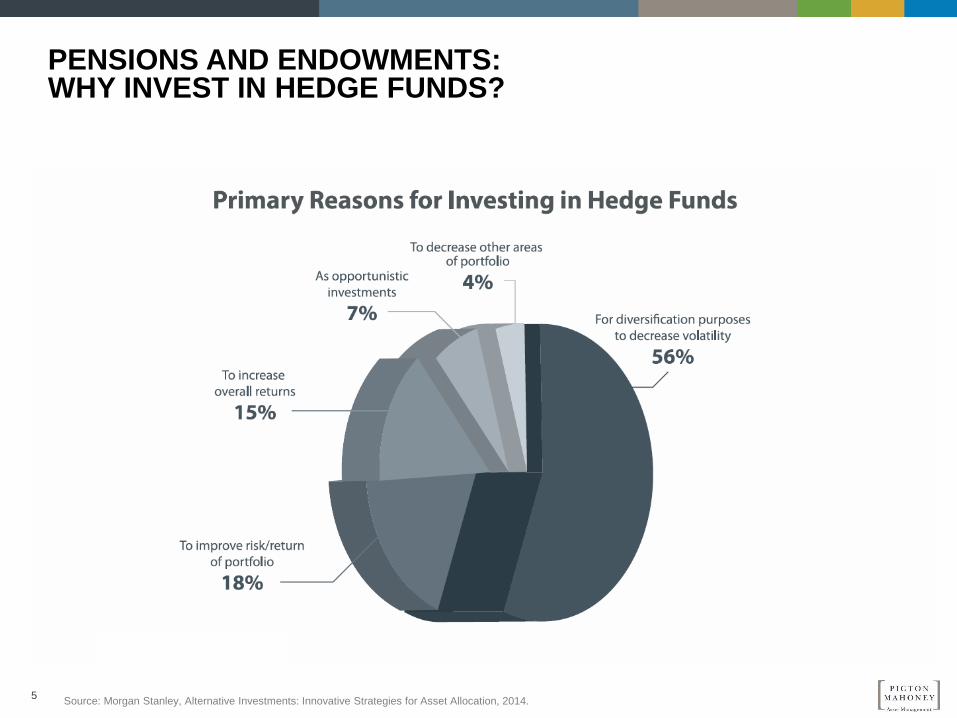

PENSIONS AND ENDOWMENTS: WHY INVEST IN HEDGE FUNDS?

Source: Morgan Stanley, Alternative Investments: Innovative Strategies for Asset Allocation, 2014.

6

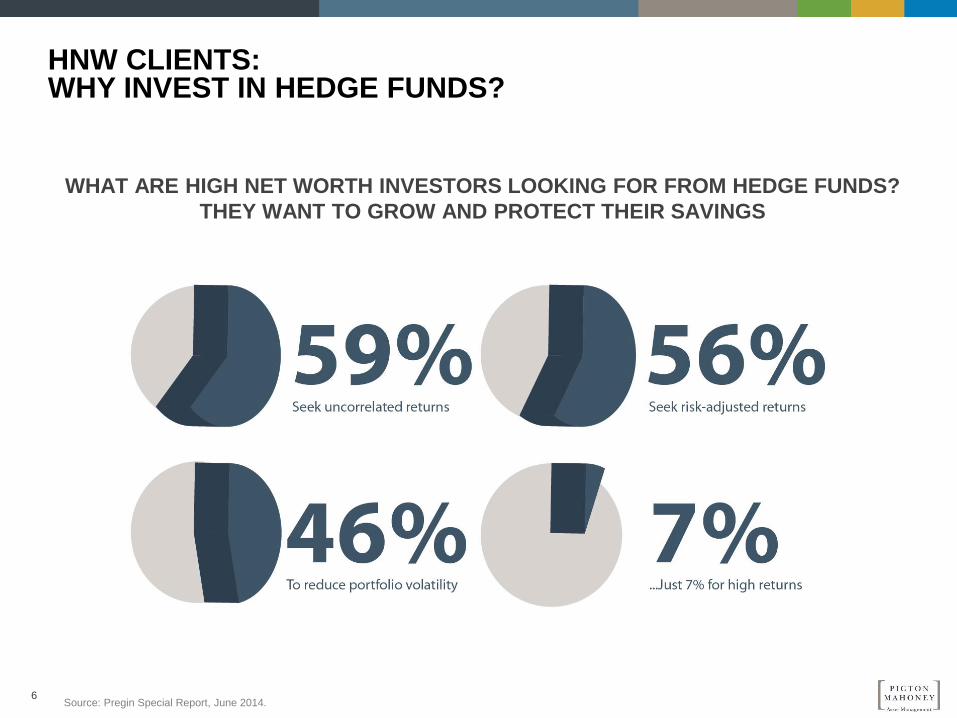

HNW CLIENTS: WHY INVEST IN HEDGE FUNDS?

WHAT ARE HIGH NET WORTH INVESTORS LOOKING FOR FROM HEDGE FUNDS?

THEY WANT TO GROW AND PROTECT THEIR SAVINGS

Source: Pregin Special Report, June 2014.

7

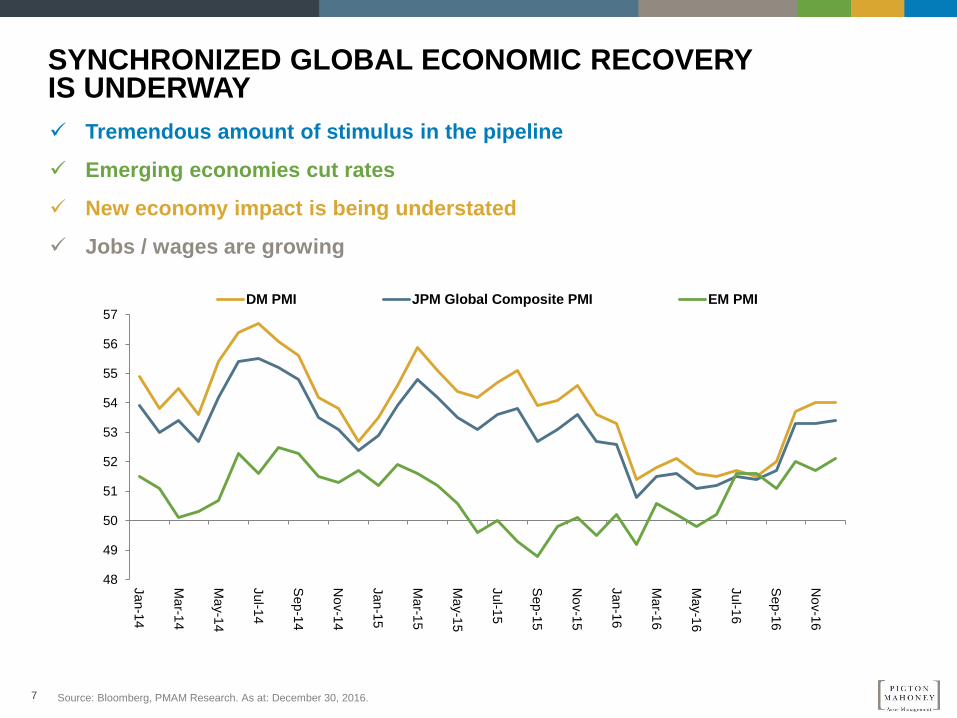

SYNCHRONIZED GLOBAL ECONOMIC RECOVERY IS UNDERWAY

Tremendous amount of stimulus in the pipeline

Emerging economies cut rates

New economy impact is being understated

Jobs / wages are growing

Source: Bloomberg, PMAM Research. As at: December 30, 2016.

48

49

50

51

52

53

54

55

56

57

Jan-1

4

Ma

r-14

Ma

y-1

4

Jul-1

4

Sep-1

4

No

v-1

4

Jan-1

5

Ma

r-15

Ma

y-1

5

Jul-1

5

Sep-1

5

No

v-1

5

Jan-1

6

Ma

r-16

Ma

y-1

6

Jul-1

6

Sep-1

6

No

v-1

6

DM PMI JPM Global Composite PMI EM PMI

8

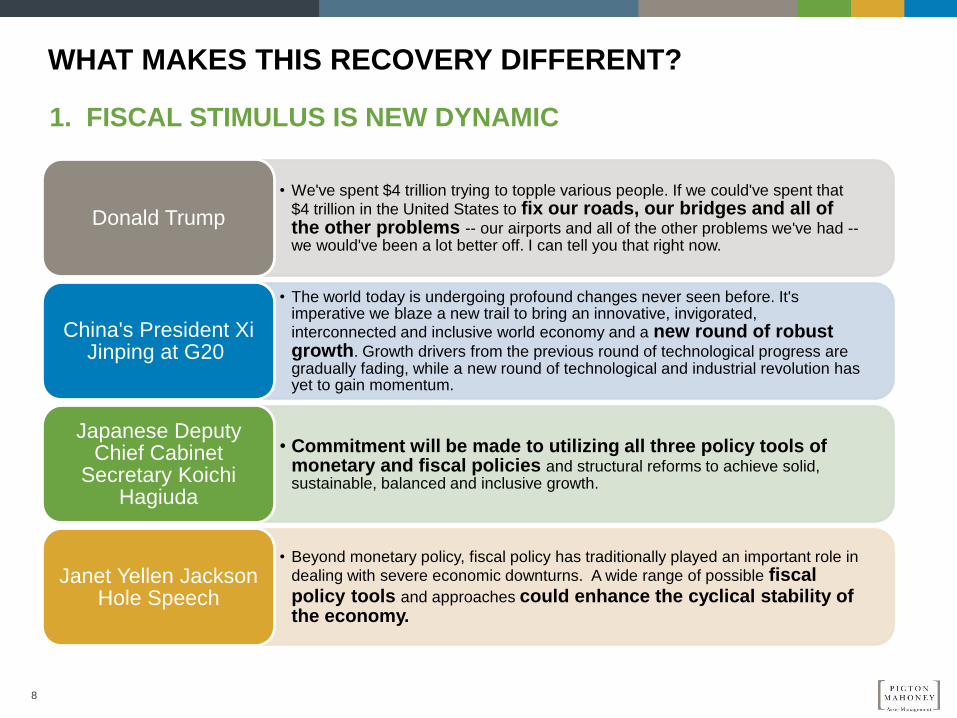

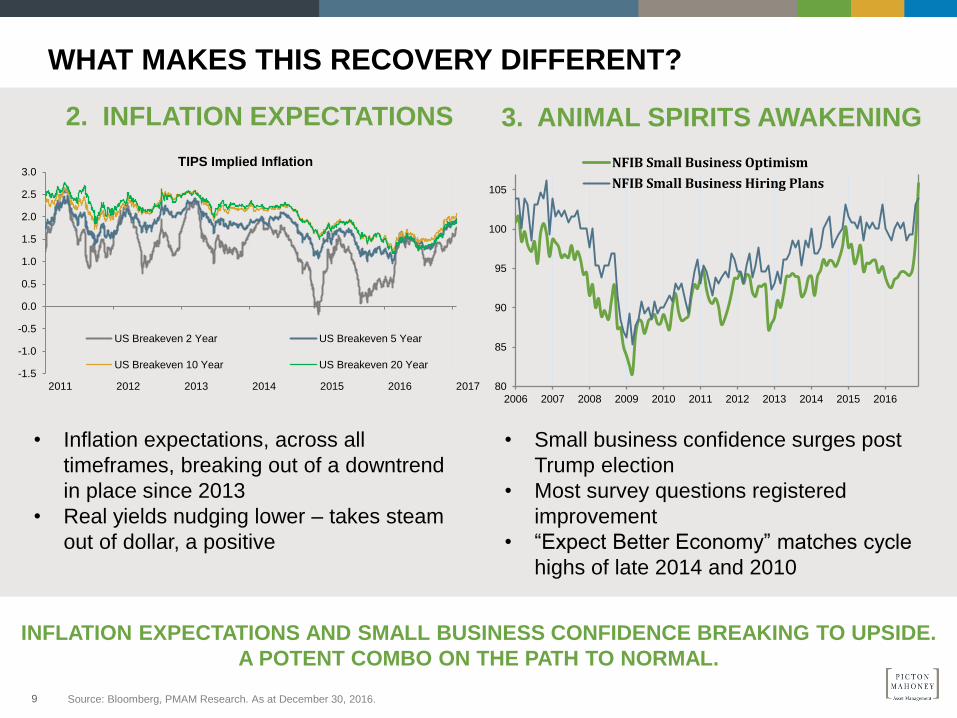

WHAT MAKES THIS RECOVERY DIFFERENT?

• We've spent $4 trillion trying to topple various people. If we could've spent that

$4 trillion in the United States to fix our roads, our bridges and all of the other problems -- our airports and all of the other problems we've had -- we would've been a lot better off. I can tell you that right now.

Donald Trump

• The world today is undergoing profound changes never seen before. It's imperative we blaze a new trail to bring an innovative, invigorated, interconnected and inclusive world economy and a new round of robust growth. Growth drivers from the previous round of technological progress are gradually fading, while a new round of technological and industrial revolution has yet to gain momentum.

China's President Xi Jinping at G20

• Commitment will be made to utilizing all three policy tools of monetary and fiscal policies and structural reforms to achieve solid, sustainable, balanced and inclusive growth.

Japanese Deputy Chief Cabinet

Secretary Koichi Hagiuda

• Beyond monetary policy, fiscal policy has traditionally played an important role in

dealing with severe economic downturns. A wide range of possible fiscal policy tools and approaches could enhance the cyclical stability of the economy.

Janet Yellen Jackson Hole Speech

1. FISCAL STIMULUS IS NEW DYNAMIC

INFLATION EXPECTATIONS AND SMALL BUSINESS CONFIDENCE BREAKING TO UPSIDE.

A POTENT COMBO ON THE PATH TO NORMAL.

• Inflation expectations, across all

timeframes, breaking out of a downtrend

in place since 2013

• Real yields nudging lower – takes steam

out of dollar, a positive

• Small business confidence surges post

Trump election

• Most survey questions registered

improvement

• “Expect Better Economy” matches cycle

highs of late 2014 and 2010

WHAT MAKES THIS RECOVERY DIFFERENT?

2. INFLATION EXPECTATIONS 3. ANIMAL SPIRITS AWAKENING

Source: Bloomberg, PMAM Research. As at December 30, 2016.

-1.5

-1.0

-0.5

0.0

0.5

1.0

1.5

2.0

2.5

3.0

2011 2012 2013 2014 2015 2016 2017

TIPS Implied Inflation

US Breakeven 2 Year US Breakeven 5 Year

US Breakeven 10 Year US Breakeven 20 Year

80

85

90

95

100

105

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

NFIB Small Business Optimism

NFIB Small Business Hiring Plans

9

10 Source: Bloomberg, Picton Mahoney Asset Management. As at December 31, 2016. Updated quarterly.

Atlanta Fed chart source: RBC Research. As at: April 30, 2016.

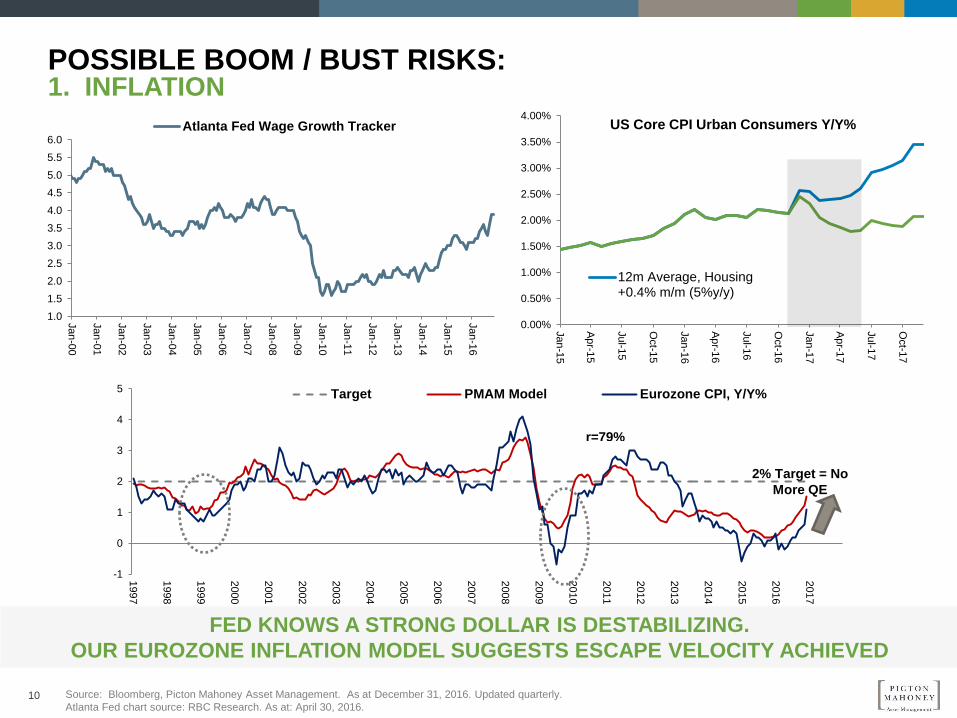

FED KNOWS A STRONG DOLLAR IS DESTABILIZING.

OUR EUROZONE INFLATION MODEL SUGGESTS ESCAPE VELOCITY ACHIEVED

0.00%

0.50%

1.00%

1.50%

2.00%

2.50%

3.00%

3.50%

4.00%

Jan

-15

Ap

r-15

Jul-1

5

Oct-1

5

Jan

-16

Ap

r-16

Jul-1

6

Oct-1

6

Jan

-17

Ap

r-17

Jul-1

7

Oct-1

7

US Core CPI Urban Consumers Y/Y%

12m Average, Housing+0.4% m/m (5%y/y)

-1

0

1

2

3

4

5

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

Target PMAM Model Eurozone CPI, Y/Y%

r=79%

2% Target = No

More QE

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

5.0

5.5

6.0

Jan

-00

Jan

-01

Jan

-02

Jan

-03

Jan

-04

Jan

-05

Jan

-06

Jan

-07

Jan

-08

Jan

-09

Jan

-10

Jan

-11

Jan

-12

Jan

-13

Jan

-14

Jan

-15

Jan

-16

Atlanta Fed Wage Growth Tracker

POSSIBLE BOOM / BUST RISKS: 1. INFLATION

11

Source: Bloomberg, PMAM Research. As at: Dec 30, 2016.

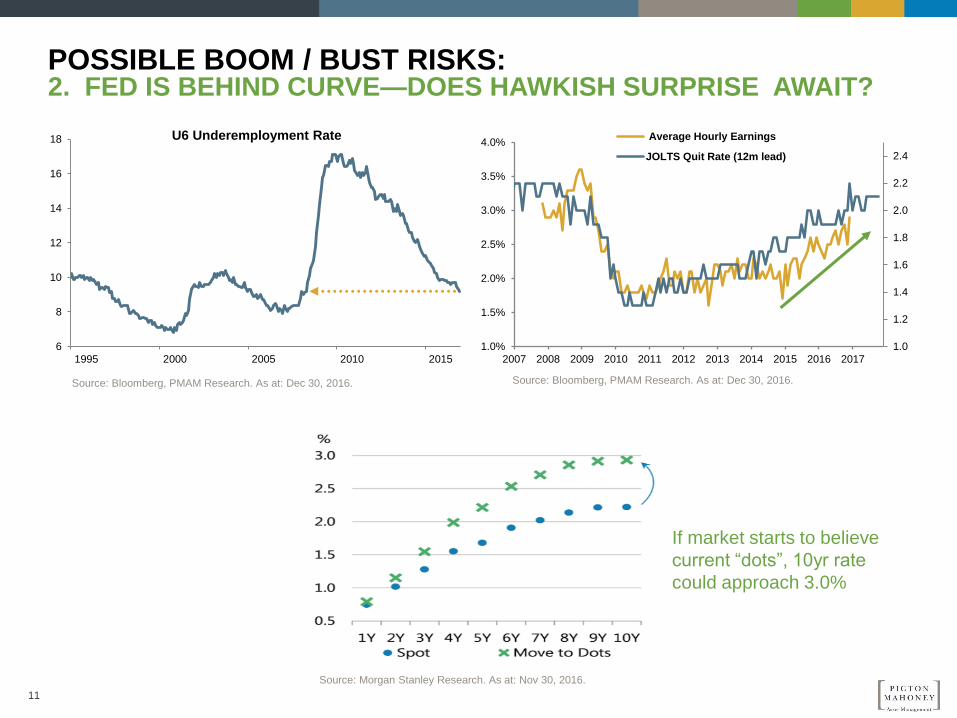

Source: Morgan Stanley Research. As at: Nov 30, 2016.

If market starts to believe

current “dots”, 10yr rate

could approach 3.0%

Source: Bloomberg, PMAM Research. As at: Dec 30, 2016.

POSSIBLE BOOM / BUST RISKS: 2. FED IS BEHIND CURVE—DOES HAWKISH SURPRISE AWAIT?

6

8

10

12

14

16

18

1995 2000 2005 2010 2015

U6 Underemployment Rate

1.0

1.2

1.4

1.6

1.8

2.0

2.2

2.4

1.0%

1.5%

2.0%

2.5%

3.0%

3.5%

4.0%

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

Average Hourly Earnings

JOLTS Quit Rate (12m lead)

12 Source: Bloomberg, Picton Mahoney Asset Management. As at January 9, 2017.

50

150

250

350

450

550

650

201

1

201

2

201

3

201

4

201

5

201

6

201

7

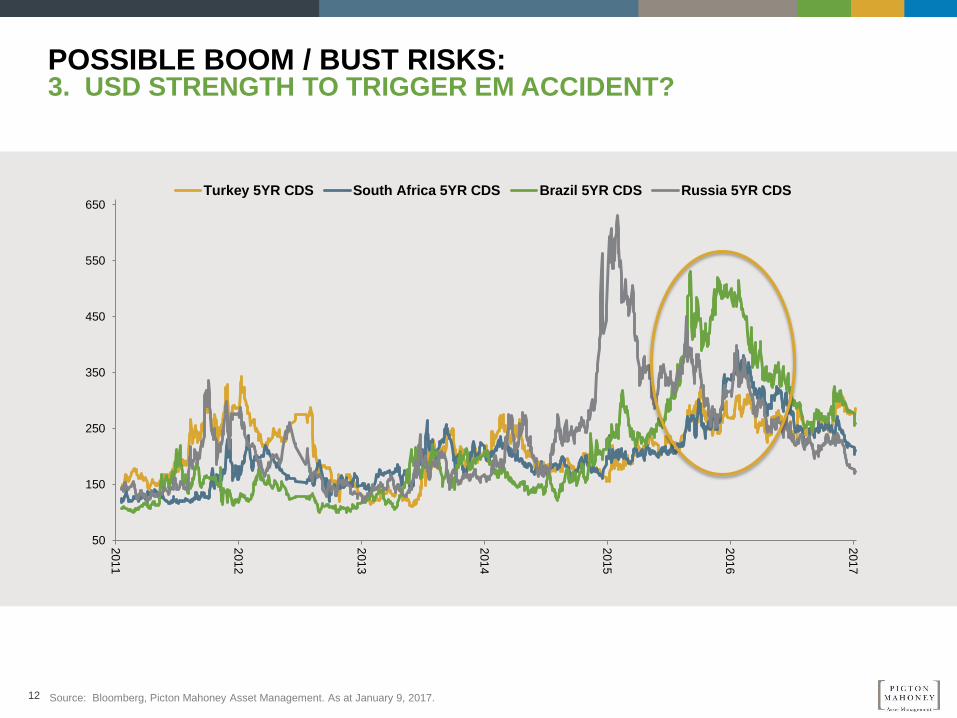

Turkey 5YR CDS South Africa 5YR CDS Brazil 5YR CDS Russia 5YR CDS

POSSIBLE BOOM / BUST RISKS: 3. USD STRENGTH TO TRIGGER EM ACCIDENT?

13

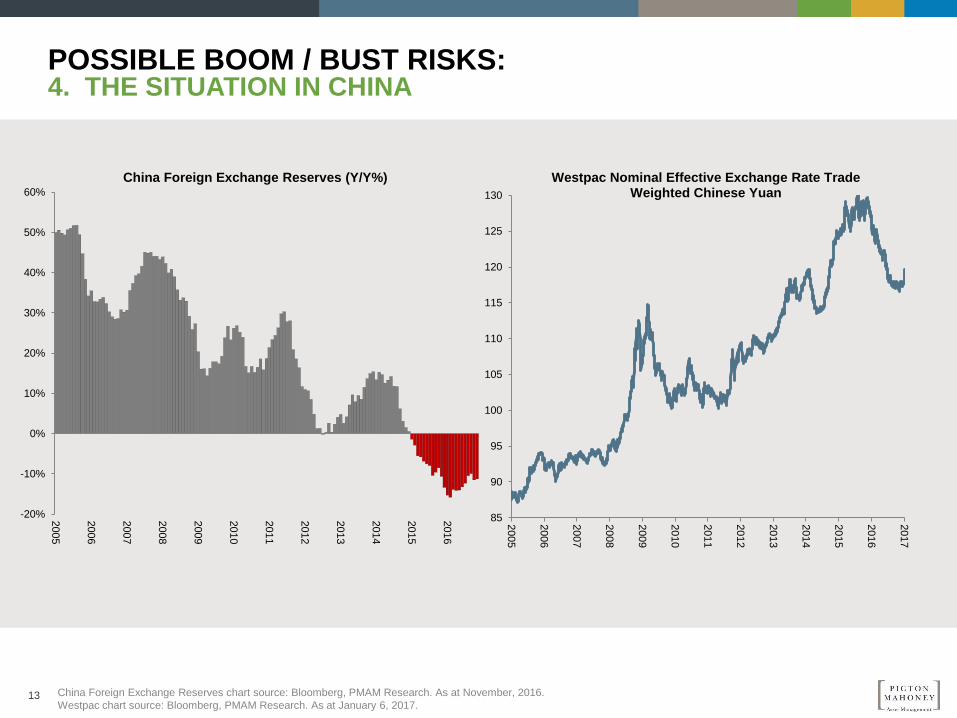

China Foreign Exchange Reserves chart source: Bloomberg, PMAM Research. As at November, 2016.

Westpac chart source: Bloomberg, PMAM Research. As at January 6, 2017.

POSSIBLE BOOM / BUST RISKS: 4. THE SITUATION IN CHINA

-20%

-10%

0%

10%

20%

30%

40%

50%

60%

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

China Foreign Exchange Reserves (Y/Y%)

85

90

95

100

105

110

115

120

125

130

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

Westpac Nominal Effective Exchange Rate Trade Weighted Chinese Yuan

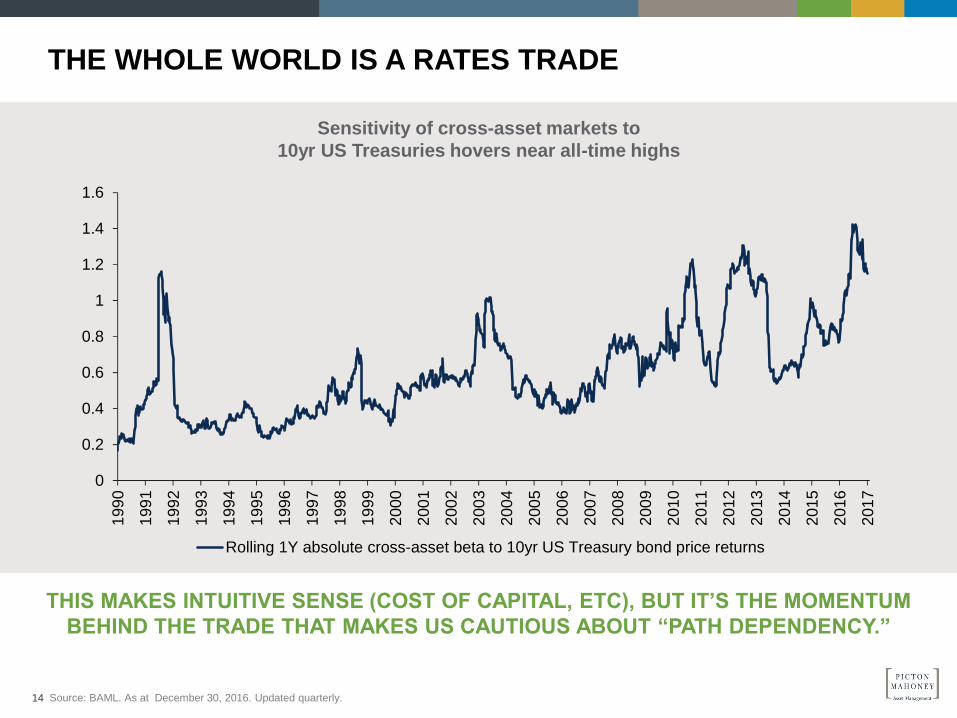

THIS MAKES INTUITIVE SENSE (COST OF CAPITAL, ETC), BUT IT’S THE MOMENTUM

BEHIND THE TRADE THAT MAKES US CAUTIOUS ABOUT “PATH DEPENDENCY.”

THE WHOLE WORLD IS A RATES TRADE

14 Source: BAML. As at December 30, 2016. Updated quarterly.

Sensitivity of cross-asset markets to

10yr US Treasuries hovers near all-time highs

0

0.2

0.4

0.6

0.8

1

1.2

1.4

1.6

199

0

199

1

199

2

199

3

199

4

199

5

199

6

199

7

199

8

199

9

200

0

200

1

200

2

200

3

200

4

200

5

200

6

200

7

200

8

200

9

201

0

201

1

201

2

201

3

201

4

201

5

201

6

201

7

Rolling 1Y absolute cross-asset beta to 10yr US Treasury bond price returns

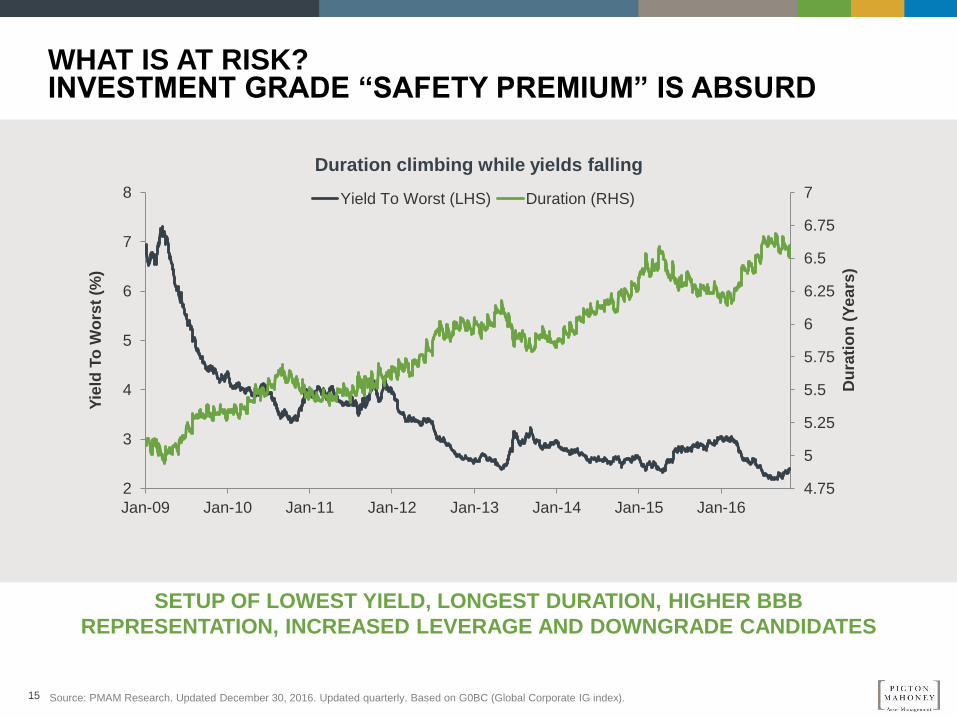

15 Source: PMAM Research. Updated December 30, 2016. Updated quarterly. Based on G0BC (Global Corporate IG index).

SETUP OF LOWEST YIELD, LONGEST DURATION, HIGHER BBB

REPRESENTATION, INCREASED LEVERAGE AND DOWNGRADE CANDIDATES

WHAT IS AT RISK? INVESTMENT GRADE “SAFETY PREMIUM” IS ABSURD

4.75

5

5.25

5.5

5.75

6

6.25

6.5

6.75

7

2

3

4

5

6

7

8

Jan-09 Jan-10 Jan-11 Jan-12 Jan-13 Jan-14 Jan-15 Jan-16

Du

rati

on

(Y

ea

rs)

Yie

ld T

o W

ors

t (%

)

Duration climbing while yields falling

Yield To Worst (LHS) Duration (RHS)

16

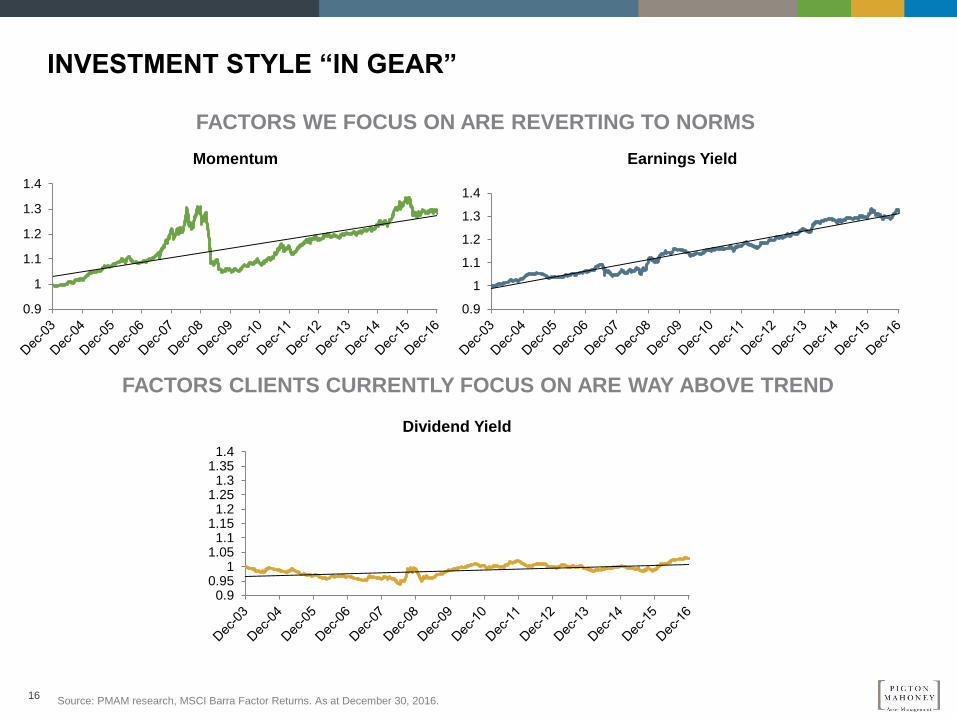

INVESTMENT STYLE “IN GEAR”

FACTORS WE FOCUS ON ARE REVERTING TO NORMS

FACTORS CLIENTS CURRENTLY FOCUS ON ARE WAY ABOVE TREND

Source: PMAM research, MSCI Barra Factor Returns. As at December 30, 2016.

0.9

1

1.1

1.2

1.3

1.4

Momentum

0.9

1

1.1

1.2

1.3

1.4

Earnings Yield

0.90.95

11.05

1.11.15

1.21.25

1.31.35

1.4

Dividend Yield

17

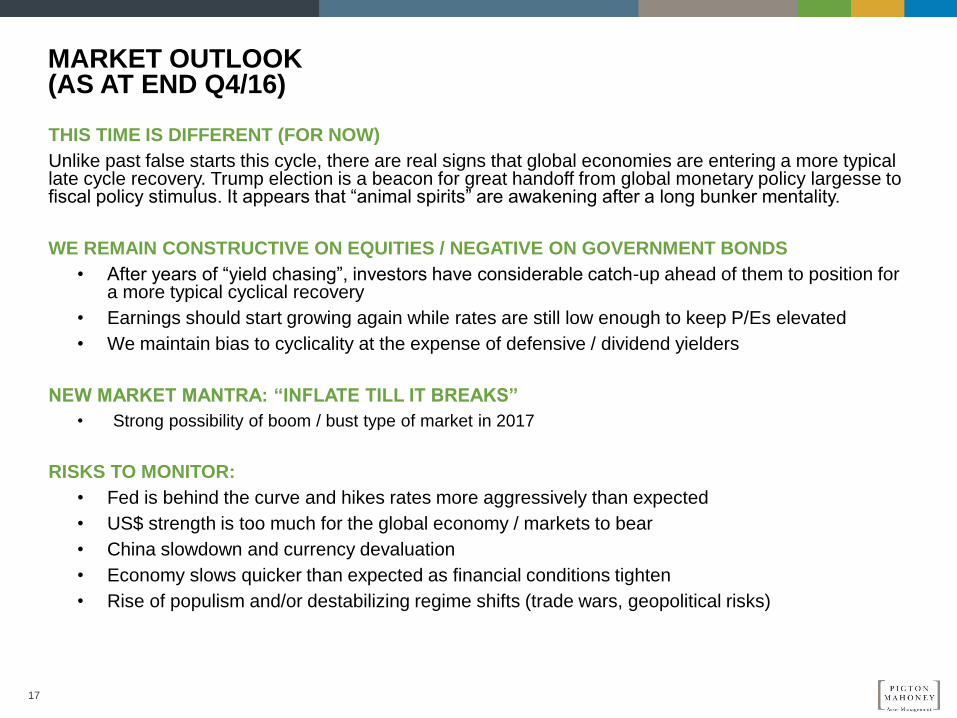

MARKET OUTLOOK (AS AT END Q4/16)

THIS TIME IS DIFFERENT (FOR NOW)

Unlike past false starts this cycle, there are real signs that global economies are entering a more typical late cycle recovery. Trump election is a beacon for great handoff from global monetary policy largesse to fiscal policy stimulus. It appears that “animal spirits” are awakening after a long bunker mentality.

WE REMAIN CONSTRUCTIVE ON EQUITIES / NEGATIVE ON GOVERNMENT BONDS

• After years of “yield chasing”, investors have considerable catch-up ahead of them to position for a more typical cyclical recovery

• Earnings should start growing again while rates are still low enough to keep P/Es elevated

• We maintain bias to cyclicality at the expense of defensive / dividend yielders

NEW MARKET MANTRA: “INFLATE TILL IT BREAKS”

• Strong possibility of boom / bust type of market in 2017

RISKS TO MONITOR:

• Fed is behind the curve and hikes rates more aggressively than expected

• US$ strength is too much for the global economy / markets to bear

• China slowdown and currency devaluation

• Economy slows quicker than expected as financial conditions tighten

• Rise of populism and/or destabilizing regime shifts (trade wars, geopolitical risks)

18

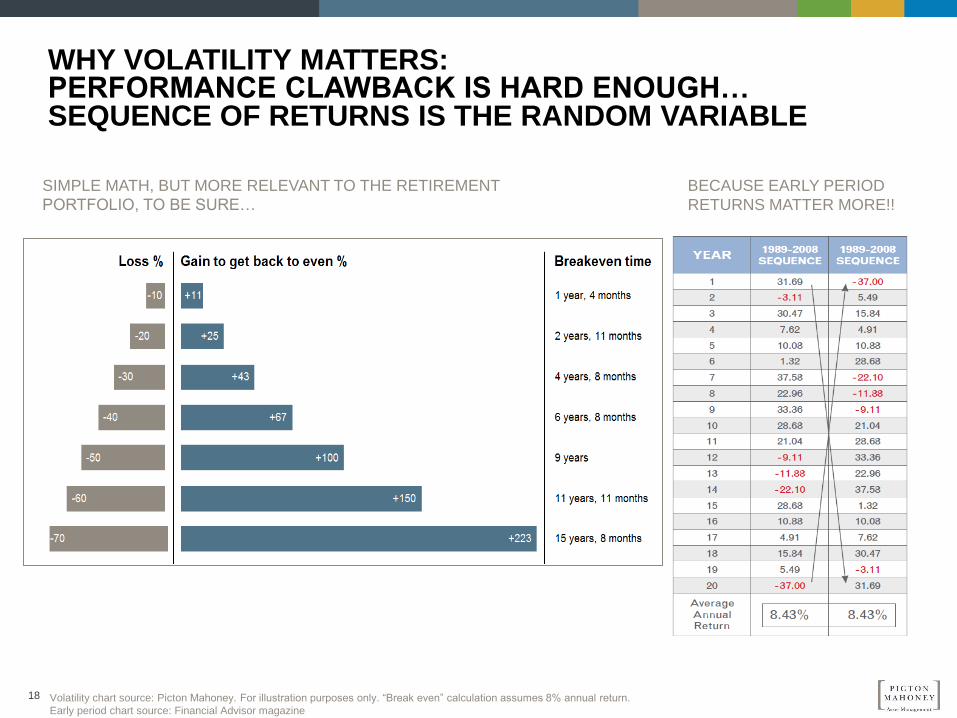

WHY VOLATILITY MATTERS: PERFORMANCE CLAWBACK IS HARD ENOUGH… SEQUENCE OF RETURNS IS THE RANDOM VARIABLE

-10

SIMPLE MATH, BUT MORE RELEVANT TO THE RETIREMENT

PORTFOLIO, TO BE SURE…

-20

-30 +43

-40 +67

-50 +100

-60 +150

-70 +223

BECAUSE EARLY PERIOD

RETURNS MATTER MORE!!

Volatility chart source: Picton Mahoney. For illustration purposes only. “Break even” calculation assumes 8% annual return.

Early period chart source: Financial Advisor magazine

19

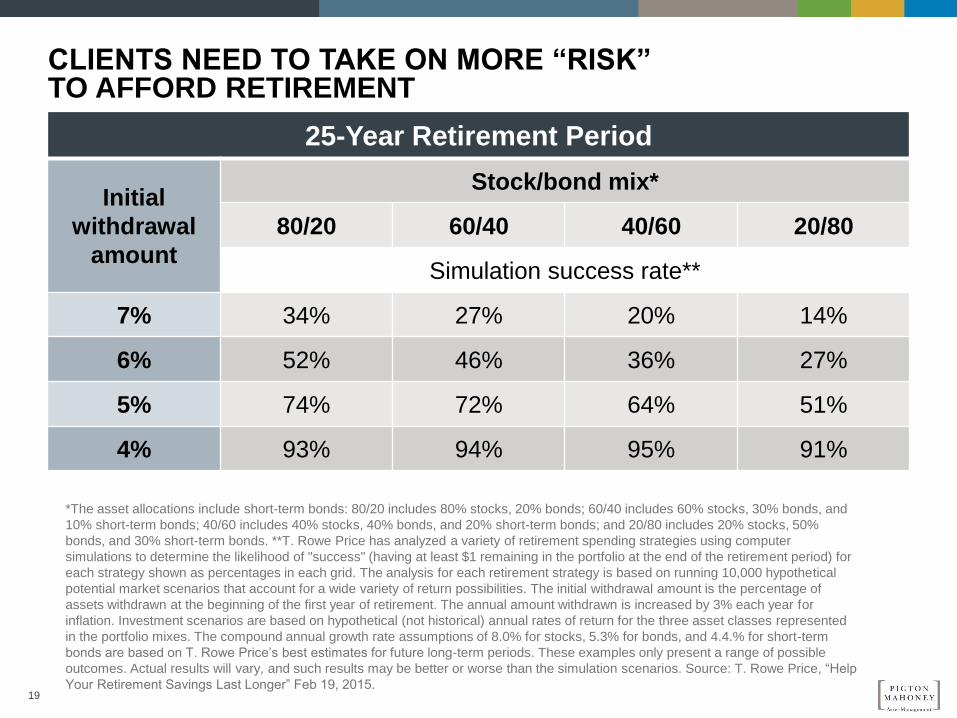

CLIENTS NEED TO TAKE ON MORE “RISK” TO AFFORD RETIREMENT

25-Year Retirement Period

Initial

withdrawal

amount

Stock/bond mix*

80/20 60/40 40/60 20/80

Simulation success rate**

7% 34% 27% 20% 14%

6% 52% 46% 36% 27%

5% 74% 72% 64% 51%

4% 93% 94% 95% 91%

*The asset allocations include short-term bonds: 80/20 includes 80% stocks, 20% bonds; 60/40 includes 60% stocks, 30% bonds, and

10% short-term bonds; 40/60 includes 40% stocks, 40% bonds, and 20% short-term bonds; and 20/80 includes 20% stocks, 50%

bonds, and 30% short-term bonds. **T. Rowe Price has analyzed a variety of retirement spending strategies using computer

simulations to determine the likelihood of "success" (having at least $1 remaining in the portfolio at the end of the retirement period) for

each strategy shown as percentages in each grid. The analysis for each retirement strategy is based on running 10,000 hypothetical

potential market scenarios that account for a wide variety of return possibilities. The initial withdrawal amount is the percentage of

assets withdrawn at the beginning of the first year of retirement. The annual amount withdrawn is increased by 3% each year for

inflation. Investment scenarios are based on hypothetical (not historical) annual rates of return for the three asset classes represented

in the portfolio mixes. The compound annual growth rate assumptions of 8.0% for stocks, 5.3% for bonds, and 4.4.% for short-term

bonds are based on T. Rowe Price’s best estimates for future long-term periods. These examples only present a range of possible

outcomes. Actual results will vary, and such results may be better or worse than the simulation scenarios. Source: T. Rowe Price, “Help

Your Retirement Savings Last Longer” Feb 19, 2015.

20

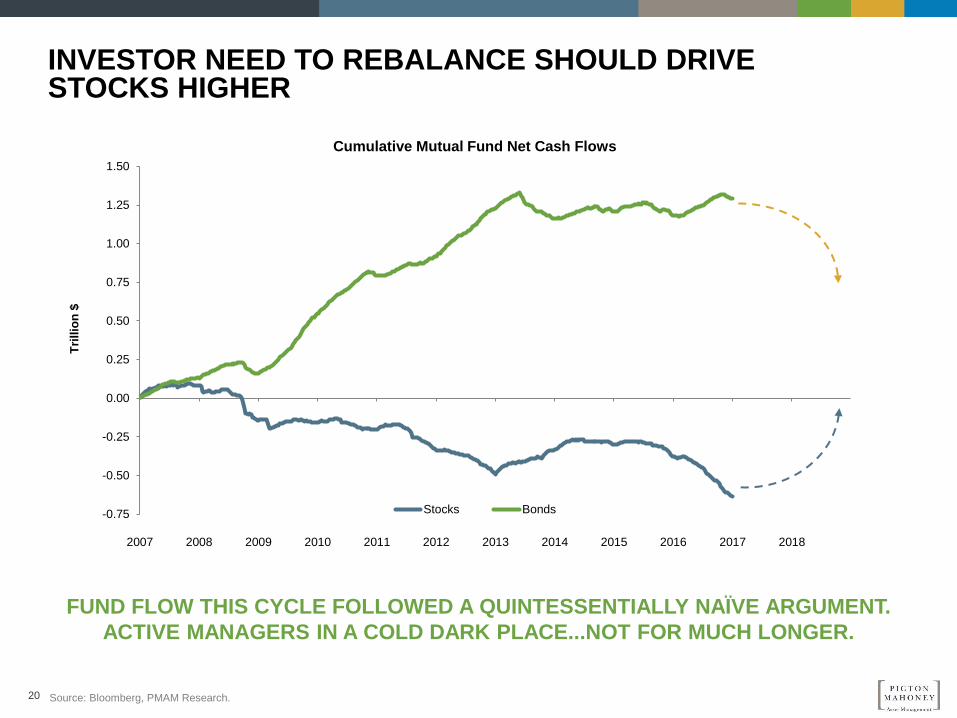

INVESTOR NEED TO REBALANCE SHOULD DRIVE STOCKS HIGHER

FUND FLOW THIS CYCLE FOLLOWED A QUINTESSENTIALLY NAÏVE ARGUMENT.

ACTIVE MANAGERS IN A COLD DARK PLACE...NOT FOR MUCH LONGER.

Source: Bloomberg, PMAM Research.

-0.75

-0.50

-0.25

0.00

0.25

0.50

0.75

1.00

1.25

1.50

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018

Tri

llio

n $

Cumulative Mutual Fund Net Cash Flows

Stocks Bonds

THINK AHEAD. STAY AHEAD.

This report is published by Picton Mahoney Asset Management (PMAM) on January 11, 2017. It is provided as a general source of information

and should not be considered personal investment advice or an offer or solicitation to buy or sell securities. The information contained in this

report has been obtained from sources believed reliable however the accuracy and/or completeness of the information is not guaranteed by

PMAM, nor does PMAM assume any responsibility or liability whatsoever. All opinions expressed are subject to change without notification

This report is confidential and for dealer use only. Any review, re-transmission, dissemination or other use of this information by persons or

entities other than the intended recipient is prohibited.

PMAM-FFMULTI-PPT-JAN-2017