Embed Size (px)

Citation preview

Disclaimer: The information contained in this document is intended only for use during the presentation and should not be disseminated or distributed to parties outside the presentation. Phillip Securities accepts no liability whatsoever with respect to the use of this document or its contents.

Phillip Securities Pte Ltd (A member of PhillipCapital) Co. Reg. No. 197201035Z © PhillipCapital 2014. All Rights Reserved. For internal circulation only.

1

Market StrategistsJoshua Tan, Head of Research

Kenneth Koh, Market & Equity Analyst

Soh Lin Sin, Macro Economist

Osama Bakhteyar, Research Assistant

SG & US Equity Analysts Lucas Tan, Real Estate

Wong Yong Kai, US Equities

Colin Tan, Telcos

Caroline Tay, Real Estate

Ben Ong, Financials

Richard Leow, Transport

By Phillip Securities ResearchMr. Chan Wai Chee, CEO

Jermaine Tock, Operations Exec

21st July 14, 8.15am/11.15am Morning Call/Webinar

Disclaimer: The information contained in this document is intended only for use during the presentation and should not be disseminated or distributed to parties outside the presentation. Phillip Securities accepts no liability whatsoever with respect to the use of this document or its contents.

Phillip Securities Pte Ltd (A member of PhillipCapital) Co. Reg. No. 197201035Z © PhillipCapital 2014. All Rights Reserved. For internal circulation only.

22

Disclaimer

This presentation is provided to you for general information only and does not constitute a recommendation, an offer or solicitation to subscribe for, purchase or sell the investment products mentioned herein. It does not have any regard to your specific investment objectives, financial situation and any of your particular needs. Accordingly, no warranty whatsoever is given and no liability whatsoever is accepted for any loss arising whether directly or indirectly as a result of you acting based on this information. Investments are subject to investment risks including the possible loss of the principal amount invested. The value of the units in any fund and the income from them may fall as well as rise. Access to services and your account may be affected by market conditions, system performance and other reasons.

The information contained in this presentation has been obtained from public sources which PSPL has no reason to believe are unreliable and any analysis, forecasts, projections, expectations and opinions (collectively the “Research”) contained in this presentation are based on such information and are expressions of belief only. PSPL has not verified this information and no representation or warranty, express or implied, is made that such information or Research is accurate, complete or verified or should be relied upon as such. Any such information or Research contained in this presentation is subject to change, and PSPL shall not have any responsibility to maintain the information or Research made available or to supply any corrections, updates or releases in connection therewith. In no event will PSPL be liable for any special, indirect, incidental or consequential damages which may be incurred from the use of the information or Research made available, even if it has been advised of the possibility of such damages.

You may wish to seek advice from a qualified financial adviser, pursuant to a separate engagement, before making a commitment to purchase any of the investment products mentioned. In the event that you choose not to seek advice from a qualified financial adviser, you should consider whether the investment product is suitable for you before proceeding to invest and we do not offer advice in this regard unless mandated to do so by way of a separate engagement.

You are advised to read the Conditions governing Phillip Securities Trading Accounts and the Risk Disclosure Statement carefully before investing in this product.

Disclaimer: The information contained in this document is intended only for use during the presentation and should not be disseminated or distributed to parties outside the presentation. Phillip Securities accepts no liability whatsoever with respect to the use of this document or its contents.

Phillip Securities Pte Ltd (A member of PhillipCapital) Co. Reg. No. 197201035Z © PhillipCapital 2014. All Rights Reserved. For internal circulation only.

3

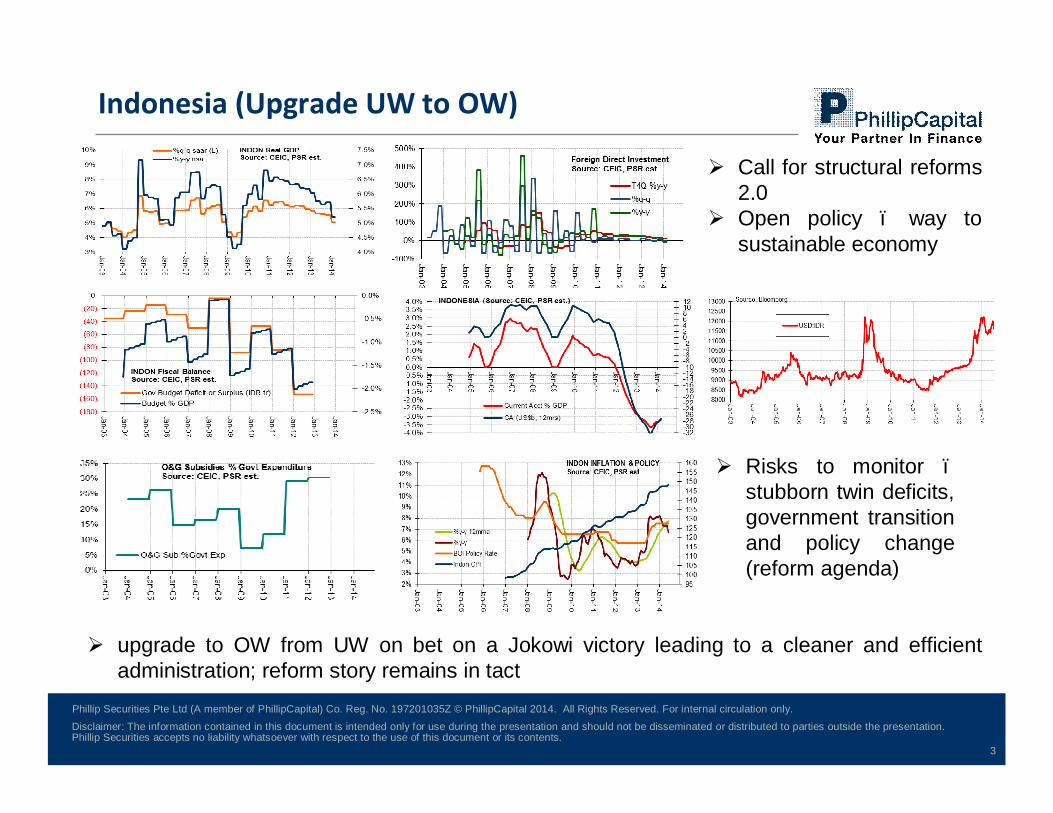

Indonesia (Upgrade UW to OW)

Ø Call for structural reforms 2.0

Ø Open policy – way to sustainable economy

Ø Risks to monitor –stubborn twin deficits, government transition and policy change (reform agenda)

Ø upgrade to OW from UW on bet on a Jokowi victory leading to a cleaner and efficient administration; reform story remains in tact

Disclaimer: The information contained in this document is intended only for use during the presentation and should not be disseminated or distributed to parties outside the presentation. Phillip Securities accepts no liability whatsoever with respect to the use of this document or its contents.

Phillip Securities Pte Ltd (A member of PhillipCapital) Co. Reg. No. 197201035Z © PhillipCapital 2014. All Rights Reserved. For internal circulation only.

4

Mutual Funds that proxy IndonesiaØAberdeen Indonesia EquityØFidelity Indonesia A USD

ETFs that proxy IndonesiaØLyxor Indonesia10US$x@ (P2Q)ØDBXT MSINDO 10US$x@ (KJ7)ØIshares MSCI Indonesia ETF (EIDO)ØMarket Vectors Indonesia Index ETF (IDX)

Indonesia (Upgrade UW to OW)

Ø JCI has rallied 18.65% year-to-date, currently trading at 20.49x P/E, slightly above its 52-weeks trailing P/E, and valued at 16.35x estimated 12-month earnings with a consensus earnings forecast growth to grow at 50.86% y-y.

Ø Post-election near term volatility. Investors may book gains into potential market rally post-election, but reforms agenda and timeline may limit market upside.

Disclaimer: The information contained in this document is intended only for use during the presentation and should not be disseminated or distributed to parties outside the presentation. Phillip Securities accepts no liability whatsoever with respect to the use of this document or its contents.

Phillip Securities Pte Ltd (A member of PhillipCapital) Co. Reg. No. 197201035Z © PhillipCapital 2014. All Rights Reserved. For internal circulation only.

5

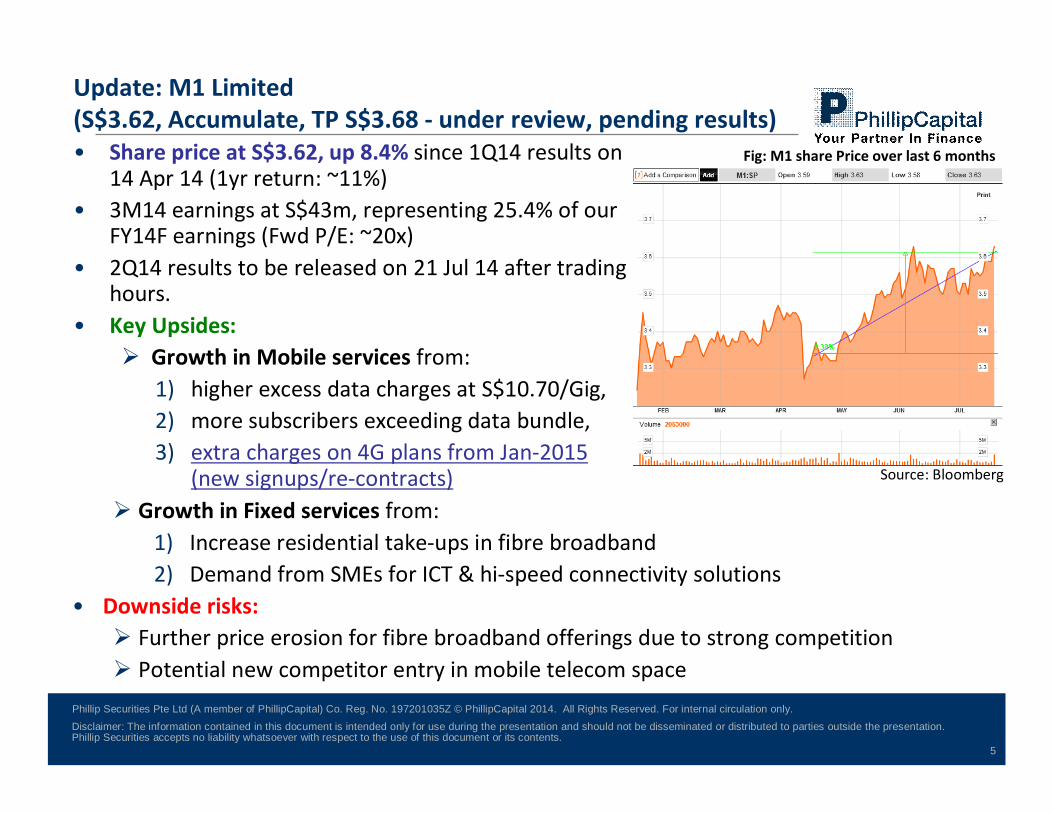

Update: M1 Limited (S$3.62, Accumulate, TP S$3.68 - under review, pending results)• Share price at S$3.62, up 8.4% since 1Q14 results on

14 Apr 14 (1yr return: ~11%) • 3M14 earnings at S$43m, representing 25.4% of our

FY14F earnings (Fwd P/E: ~20x)• 2Q14 results to be released on 21 Jul 14 after trading

hours.• Key Upsides: Ø Growth in Mobile services from:

1) higher excess data charges at S$10.70/Gig, 2) more subscribers exceeding data bundle, 3) extra charges on 4G plans from Jan-2015

(new signups/re-contracts) Source: Bloomberg

Fig: M1 share Price over last 6 months

Ø Growth in Fixed services from: 1) Increase residential take-ups in fibre broadband2) Demand from SMEs for ICT & hi-speed connectivity solutions

• Downside risks:Ø Further price erosion for fibre broadband offerings due to strong competitionØ Potential new competitor entry in mobile telecom space

Disclaimer: The information contained in this document is intended only for use during the presentation and should not be disseminated or distributed to parties outside the presentation. Phillip Securities accepts no liability whatsoever with respect to the use of this document or its contents.

Phillip Securities Pte Ltd (A member of PhillipCapital) Co. Reg. No. 197201035Z © PhillipCapital 2014. All Rights Reserved. For internal circulation only.

6

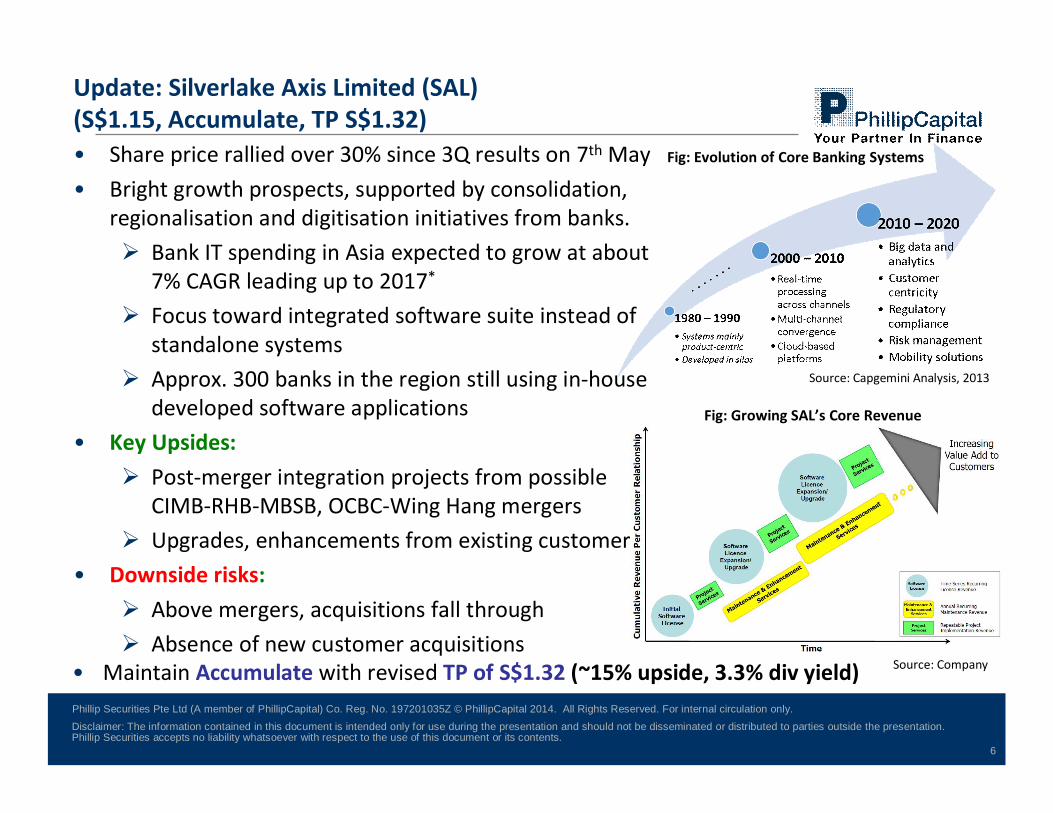

Update: Silverlake Axis Limited (SAL)(S$1.15, Accumulate, TP S$1.32)• Share price rallied over 30% since 3Q results on 7th May• Bright growth prospects, supported by consolidation,

regionalisation and digitisation initiatives from banks.Ø Bank IT spending in Asia expected to grow at about

7% CAGR leading up to 2017*

Ø Focus toward integrated software suite instead of standalone systems

Ø Approx. 300 banks in the region still using in-house developed software applications

• Key Upsides: Ø Post-merger integration projects from possible

CIMB-RHB-MBSB, OCBC-Wing Hang mergersØ Upgrades, enhancements from existing customers

• Downside risks: Ø Above mergers, acquisitions fall throughØ Absence of new customer acquisitions

• Maintain Accumulate with revised TP of S$1.32 (~15% upside, 3.3% div yield)

Source: Capgemini Analysis, 2013

Source: Company

Fig: Evolution of Core Banking Systems

Fig: Growing SAL’s Core Revenue

Disclaimer: The information contained in this document is intended only for use during the presentation and should not be disseminated or distributed to parties outside the presentation. Phillip Securities accepts no liability whatsoever with respect to the use of this document or its contents.

Phillip Securities Pte Ltd (A member of PhillipCapital) Co. Reg. No. 197201035Z © PhillipCapital 2014. All Rights Reserved. For internal circulation only.

7

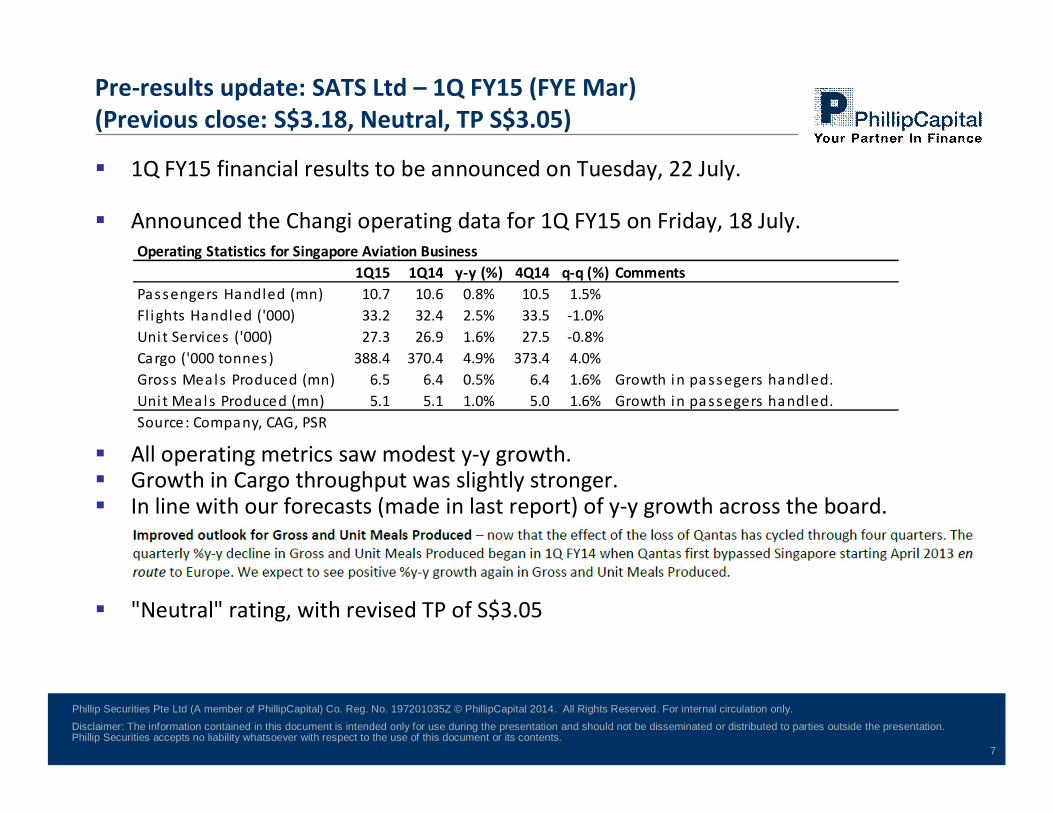

Pre-results update: SATS Ltd – 1Q FY15 (FYE Mar)(Previous close: S$3.18, Neutral, TP S$3.05)

§ 1Q FY15 financial results to be announced on Tuesday, 22 July.

§ Announced the Changi operating data for 1Q FY15 on Friday, 18 July.

§ All operating metrics saw modest y-y growth.§ Growth in Cargo throughput was slightly stronger.§ In line with our forecasts (made in last report) of y-y growth across the board.

§ "Neutral" rating, with revised TP of S$3.05

Operating Statistics for Singapore Aviation Business1Q15 1Q14 y-y (%) 4Q14 q-q (%) Comments

Passengers Handled (mn) 10.7 10.6 0.8% 10.5 1.5%Flights Handled ('000) 33.2 32.4 2.5% 33.5 -1.0%Unit Services ('000) 27.3 26.9 1.6% 27.5 -0.8%Cargo ('000 tonnes) 388.4 370.4 4.9% 373.4 4.0%Gross Meals Produced (mn) 6.5 6.4 0.5% 6.4 1.6% Growth in pa ssegers handled.Uni t Meals Produced (mn) 5.1 5.1 1.0% 5.0 1.6% Growth in pa ssegers handled.Source: Company, CAG, PSR

Disclaimer: The information contained in this document is intended only for use during the presentation and should not be disseminated or distributed to parties outside the presentation. Phillip Securities accepts no liability whatsoever with respect to the use of this document or its contents.

Phillip Securities Pte Ltd (A member of PhillipCapital) Co. Reg. No. 197201035Z © PhillipCapital 2014. All Rights Reserved. For internal circulation only.

8

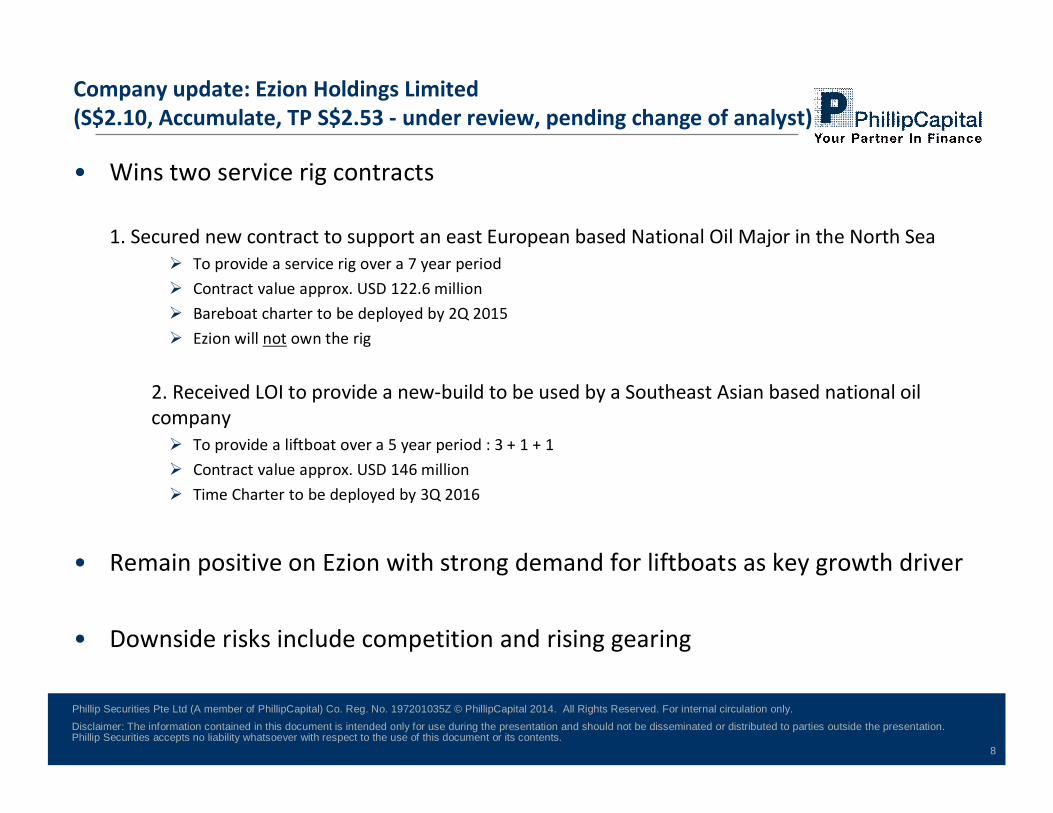

Company update: Ezion Holdings Limited (S$2.10, Accumulate, TP S$2.53 - under review, pending change of analyst)

• Wins two service rig contracts

1. Secured new contract to support an east European based National Oil Major in the North SeaØ To provide a service rig over a 7 year periodØ Contract value approx. USD 122.6 million Ø Bareboat charter to be deployed by 2Q 2015Ø Ezion will not own the rig

2. Received LOI to provide a new-build to be used by a Southeast Asian based national oil company Ø To provide a liftboat over a 5 year period : 3 + 1 + 1Ø Contract value approx. USD 146 million Ø Time Charter to be deployed by 3Q 2016

• Remain positive on Ezion with strong demand for liftboats as key growth driver

• Downside risks include competition and rising gearing

Disclaimer: The information contained in this document is intended only for use during the presentation and should not be disseminated or distributed to parties outside the presentation. Phillip Securities accepts no liability whatsoever with respect to the use of this document or its contents.

Phillip Securities Pte Ltd (A member of PhillipCapital) Co. Reg. No. 197201035Z © PhillipCapital 2014. All Rights Reserved. For internal circulation only.

9

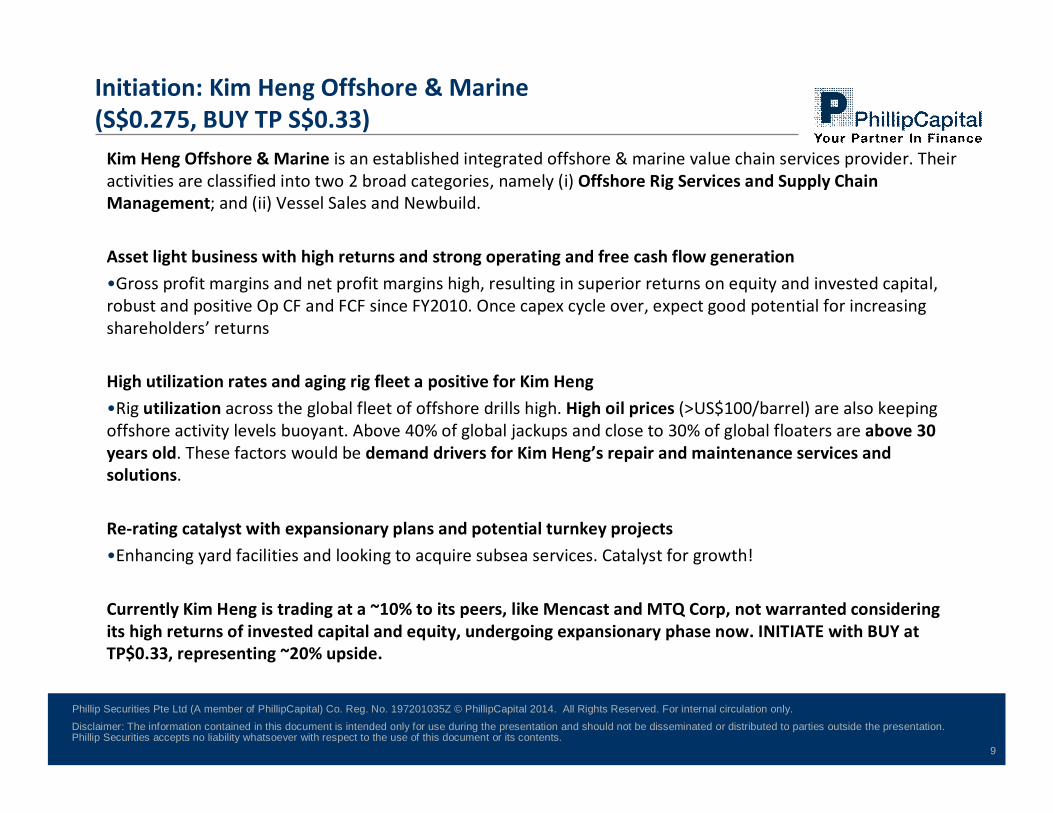

Kim Heng Offshore & Marine is an established integrated offshore & marine value chain services provider. Their activities are classified into two 2 broad categories, namely (i) Offshore Rig Services and Supply Chain Management; and (ii) Vessel Sales and Newbuild.

Asset light business with high returns and strong operating and free cash flow generation•Gross profit margins and net profit margins high, resulting in superior returns on equity and invested capital, robust and positive Op CF and FCF since FY2010. Once capex cycle over, expect good potential for increasing shareholders’ returns

High utilization rates and aging rig fleet a positive for Kim Heng•Rig utilization across the global fleet of offshore drills high. High oil prices (>US$100/barrel) are also keeping offshore activity levels buoyant. Above 40% of global jackups and close to 30% of global floaters are above 30 years old. These factors would be demand drivers for Kim Heng’s repair and maintenance services and solutions.

Re-rating catalyst with expansionary plans and potential turnkey projects•Enhancing yard facilities and looking to acquire subsea services. Catalyst for growth!

Currently Kim Heng is trading at a ~10% to its peers, like Mencast and MTQ Corp, not warranted considering its high returns of invested capital and equity, undergoing expansionary phase now. INITIATE with BUY at TP$0.33, representing ~20% upside.

Initiation: Kim Heng Offshore & Marine(S$0.275, BUY TP S$0.33)

Disclaimer: The information contained in this document is intended only for use during the presentation and should not be disseminated or distributed to parties outside the presentation. Phillip Securities accepts no liability whatsoever with respect to the use of this document or its contents.

Phillip Securities Pte Ltd (A member of PhillipCapital) Co. Reg. No. 197201035Z © PhillipCapital 2014. All Rights Reserved. For internal circulation only.

Oil & Gas Industry:Exploration & Production

Wong Yong Kai

Investment Analyst

Phillip Securities Research

21 July 2014

Disclaimer: The information contained in this document is intended only for use during the presentation and should not be disseminated or distributed to parties outside the presentation. Phillip Securities accepts no liability whatsoever with respect to the use of this document or its contents.

Phillip Securities Pte Ltd (A member of PhillipCapital) Co. Reg. No. 197201035Z © PhillipCapital 2014. All Rights Reserved. For internal circulation only.

11

Different Types of Oil/Gas

§ Natural Gas – gaseous mixture of hydrocarbon compounds, primarily methane.

§ Crude Oil – mixture of hydrocarbons that exists in liquid phase in natural underground reservoirs and remains liquid at atmospheric pressure.

§ West Texas Intermediate (WTI) and Brent – two grades of crude oil used as benchmarks for oil pricing. WTI currently trading at ~$8/bbl discount to Brent.

§ WTI => US & Canada interior | Brent => Europe, Africa, Middle East

§ Natural Gas Liquids (NGLs) – non-crude oil liquids naturally found together with natural gas, and made up of lighter hydrocarbons (ethane and propane > 50%).

§ Shale Gas/Tight Oil refers to hydrocarbons produced from shale formation. NOT to be confused with shale oil, even though media uses the term loosely. Shale Oil = kerogen (non-crude oil) produced from sedimentary rocks.

Disclaimer: The information contained in this document is intended only for use during the presentation and should not be disseminated or distributed to parties outside the presentation. Phillip Securities accepts no liability whatsoever with respect to the use of this document or its contents.

Phillip Securities Pte Ltd (A member of PhillipCapital) Co. Reg. No. 197201035Z © PhillipCapital 2014. All Rights Reserved. For internal circulation only.

12

Different Types of Oil/Gas

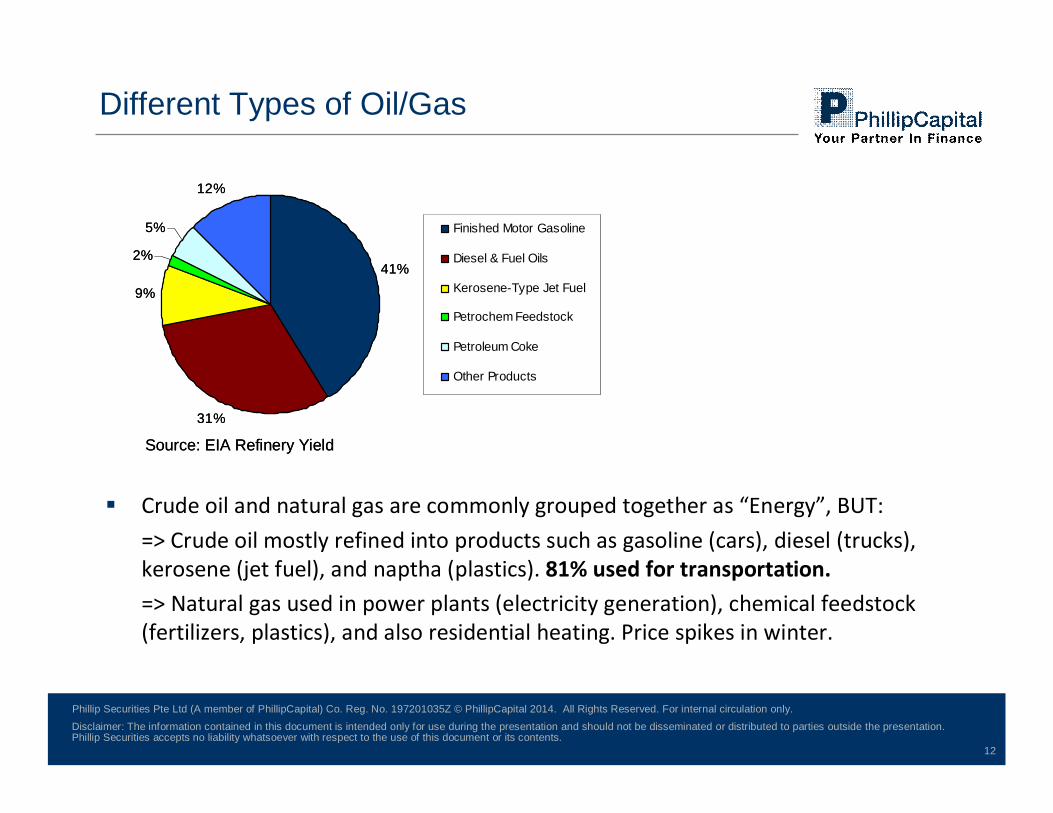

§ Crude oil and natural gas are commonly grouped together as “Energy”, BUT: => Crude oil mostly refined into products such as gasoline (cars), diesel (trucks), kerosene (jet fuel), and naptha (plastics). 81% used for transportation.=> Natural gas used in power plants (electricity generation), chemical feedstock (fertilizers, plastics), and also residential heating. Price spikes in winter.

41%

31%

9%

2%

5%

12%

Finished Motor Gasoline

Diesel & Fuel Oils

Kerosene-Type Jet Fuel

Petrochem Feedstock

Petroleum Coke

Other Products

Source: EIA Refinery Yield

41%

31%

9%

2%

5%

12%

Finished Motor Gasoline

Diesel & Fuel Oils

Kerosene-Type Jet Fuel

Petrochem Feedstock

Petroleum Coke

Other Products

Source: EIA Refinery Yield

Disclaimer: The information contained in this document is intended only for use during the presentation and should not be disseminated or distributed to parties outside the presentation. Phillip Securities accepts no liability whatsoever with respect to the use of this document or its contents.

Phillip Securities Pte Ltd (A member of PhillipCapital) Co. Reg. No. 197201035Z © PhillipCapital 2014. All Rights Reserved. For internal circulation only.

13

Resources vs Reserves

§ PROSPECTIVE RESOURCES– potentially recoverable + undiscovered accumulations.

§ CONTINGENT RESOURCES– potentially but not currently commercially recoverable + known accumulations

§ PROVED RESERVES (1P)– commercially recoverable + known accumulations + 90% probability quantity > estimates

§ PROBABLE RESERVES (2P)– similar to 1P, but only 50% probability quantity > estimates

Disclaimer: The information contained in this document is intended only for use during the presentation and should not be disseminated or distributed to parties outside the presentation. Phillip Securities accepts no liability whatsoever with respect to the use of this document or its contents.

Phillip Securities Pte Ltd (A member of PhillipCapital) Co. Reg. No. 197201035Z © PhillipCapital 2014. All Rights Reserved. For internal circulation only.

14

Exploration Process

§ Crude oil often discovered near known producing areas; similar environment (heat, pressure) encourages formation, geology enables the entrapment.

§ Eagle Ford and Bakken plays each makes up 10% of US proved oil reserves.

§ Conventional reservoirs require sufficient depth for heat and pressure to turn hydrocarbons into crude oil, porous reservoir rocks for crude oil to accumulate over millenniums, and lastly impermeable layer of rocks on top of the porous formations to trap the oil and prevent it from escaping to the surface.

§ Low 10-15% chance of discovering oil in a location where oil has never been found, vs 50% or higher success rate where there is precedence.

§ Step 1: Bidding for concessions that grants rights to explore and produce.Step 2: Seismic study to reveal underground layers and map out oil reservoir.Step 3: Drilling to confirm presence of hydrocarbon, and estimate quantity.

Disclaimer: The information contained in this document is intended only for use during the presentation and should not be disseminated or distributed to parties outside the presentation. Phillip Securities accepts no liability whatsoever with respect to the use of this document or its contents.

Phillip Securities Pte Ltd (A member of PhillipCapital) Co. Reg. No. 197201035Z © PhillipCapital 2014. All Rights Reserved. For internal circulation only.

15

Production Rate

• No. of barrels of oil (bbl) or barrels of oil equivalent (boe) extracted per day.

• 1 bbl oil = 42 US gallons = 159 litres. After initial optimization and ramp-up, oil production will decline over time due to the gradual drop in pressure – unless various recovery techniques are utilized to sustain or increase production.

• 1 boe = Amount of energy released by burning 1 bbl oil = 5.8 x 106 BTU, and roughly equivalent to 6,000 cubic feet of natural gas (6 mcf).

• However, 1 bbl oil doesn’t sell for anywhere near the same price as 1 boe.

• As of 25 June 2014, WTI Crude Oil trades at $106.44/bbl, while NYMEX Natural Gas trades at $4.53/mcf (ie. $27.18/boe). Therefore, 1 bbl ≈ 4 boe in price.

Disclaimer: The information contained in this document is intended only for use during the presentation and should not be disseminated or distributed to parties outside the presentation. Phillip Securities accepts no liability whatsoever with respect to the use of this document or its contents.

Phillip Securities Pte Ltd (A member of PhillipCapital) Co. Reg. No. 197201035Z © PhillipCapital 2014. All Rights Reserved. For internal circulation only.

16

Enhanced Oil Recovery

Primary Oil Recovery• Natural pressure of the reservoir or gravity drives oil into the wellbore. This

pressure, combined with artificial lift techniques such as pumps, transports oil to the surface. 10% of the original oil in place is recovered this way.

Secondary Oil Recovery• As the pressure is relieved, less oil flows out by itself. Injection of water or gas

displaces the heavier oil and drives it to a production wellbore where it is brought to surface. 20-40% of the original oil in place is recovered this way.

Enhanced Oil Recovery (EOR)• By the time secondary techniques fail to induce more oil production, up to

70% of original oil is still underground. EOR (thermal steam or gas injection aims to lower viscosity and improve flow rate) has the potential to ultimately extract 30-60% of the original oil, but more costly than primary and secondary techniques and thus requires higher oil prices to achieve a reasonable ROI.

Disclaimer: The information contained in this document is intended only for use during the presentation and should not be disseminated or distributed to parties outside the presentation. Phillip Securities accepts no liability whatsoever with respect to the use of this document or its contents.

Phillip Securities Pte Ltd (A member of PhillipCapital) Co. Reg. No. 197201035Z © PhillipCapital 2014. All Rights Reserved. For internal circulation only.

17

Identifying Top Picks

Disclaimer: The information contained in this document is intended only for use during the presentation and should not be disseminated or distributed to parties outside the presentation. Phillip Securities accepts no liability whatsoever with respect to the use of this document or its contents.

Phillip Securities Pte Ltd (A member of PhillipCapital) Co. Reg. No. 197201035Z © PhillipCapital 2014. All Rights Reserved. For internal circulation only.

18

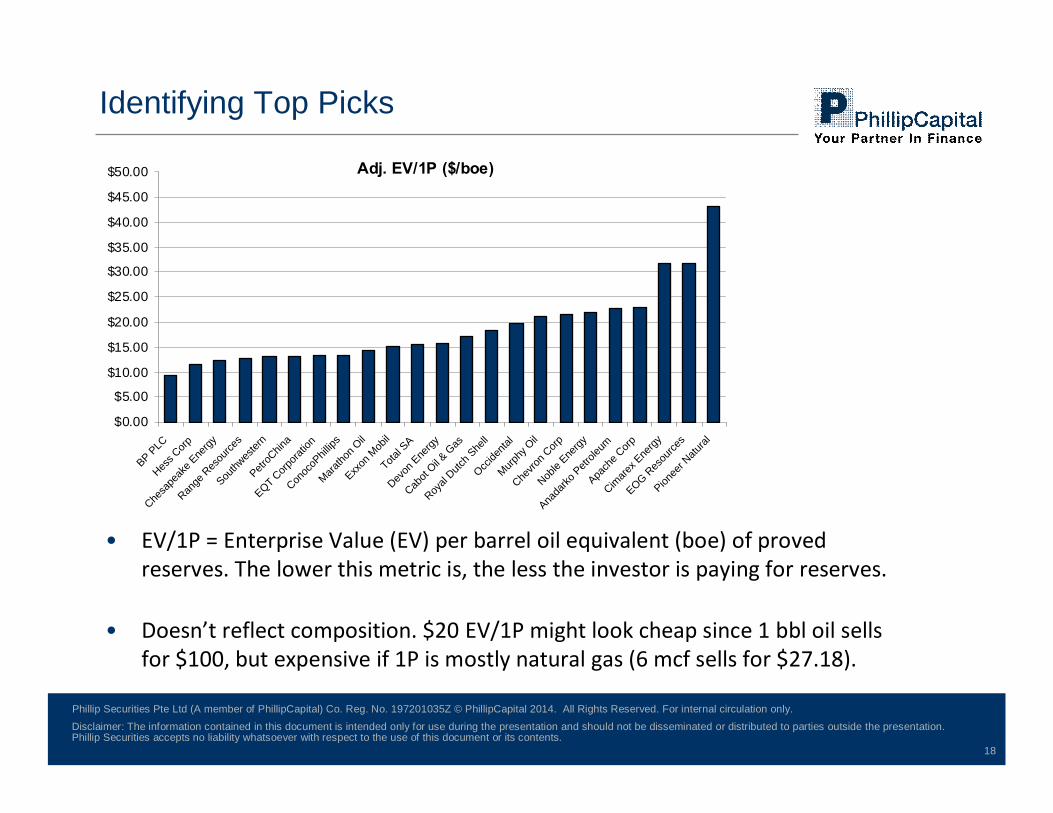

Identifying Top Picks

• EV/1P = Enterprise Value (EV) per barrel oil equivalent (boe) of proved reserves. The lower this metric is, the less the investor is paying for reserves.

• Doesn’t reflect composition. $20 EV/1P might look cheap since 1 bbl oil sells for $100, but expensive if 1P is mostly natural gas (6 mcf sells for $27.18).

Adj. EV/1P ($/boe)

$0.00

$5.00

$10.00

$15.00

$20.00

$25.00

$30.00

$35.00

$40.00

$45.00

$50.00

BP PLC

Hess C

orp

Chesa

peak

e Ene

rgy

Range

Res

ource

s

Southw

ester

n

PetroC

hina

EQT Corp

oratio

n

Conoc

oPhil

lips

Maratho

n Oil

Exxon

Mob

il

Total S

A

Devon

Ene

rgy

Cabot

Oil & G

as

Royal

Dutch S

hell

Occide

ntal

Murphy

Oil

Chevro

n Corp

Noble

Energy

Anada

rko P

etrole

um

Apach

e Corp

Cimare

x Ene

rgy

EOG Res

ource

s

Pionee

r Natu

ral

Disclaimer: The information contained in this document is intended only for use during the presentation and should not be disseminated or distributed to parties outside the presentation. Phillip Securities accepts no liability whatsoever with respect to the use of this document or its contents.

Phillip Securities Pte Ltd (A member of PhillipCapital) Co. Reg. No. 197201035Z © PhillipCapital 2014. All Rights Reserved. For internal circulation only.

19

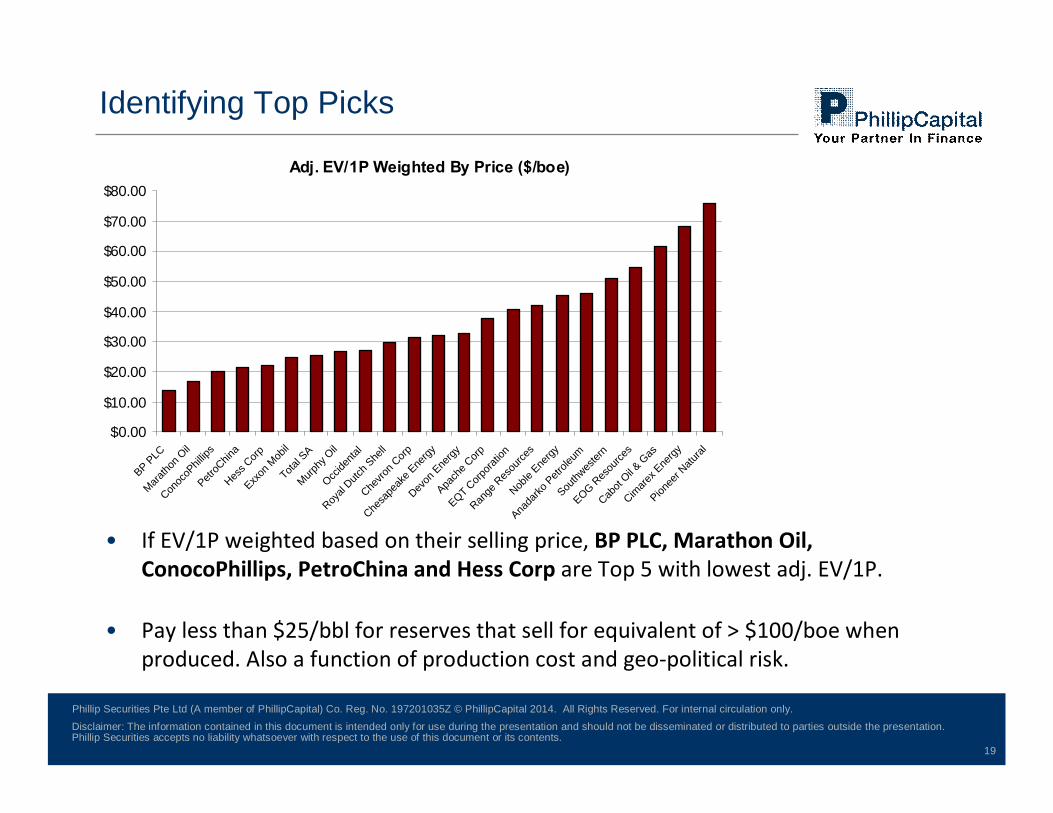

Identifying Top Picks

• If EV/1P weighted based on their selling price, BP PLC, Marathon Oil, ConocoPhillips, PetroChina and Hess Corp are Top 5 with lowest adj. EV/1P.

• Pay less than $25/bbl for reserves that sell for equivalent of > $100/boe when produced. Also a function of production cost and geo-political risk.

Adj. EV/1P Weighted By Price ($/boe)

$0.00

$10.00

$20.00

$30.00

$40.00

$50.00

$60.00

$70.00

$80.00

BP PLC

Maratho

n Oil

Conoc

oPhil

lips

PetroC

hina

Hess C

orp

Exxon

Mob

il

Total S

A

Murphy

Oil

Occide

ntal

Royal

Dutch S

hell

Chevro

n Corp

Chesa

peak

e Ene

rgy

Devon

Ene

rgy

Apach

e Corp

EQT Corp

oratio

n

Range

Res

ource

s

Noble

Energy

Anada

rko P

etrole

um

Southw

ester

n

EOG Res

ource

s

Cabot

Oil & G

as

Cimare

x Ene

rgy

Pionee

r Natu

ral

Disclaimer: The information contained in this document is intended only for use during the presentation and should not be disseminated or distributed to parties outside the presentation. Phillip Securities accepts no liability whatsoever with respect to the use of this document or its contents.

Phillip Securities Pte Ltd (A member of PhillipCapital) Co. Reg. No. 197201035Z © PhillipCapital 2014. All Rights Reserved. For internal circulation only.

20

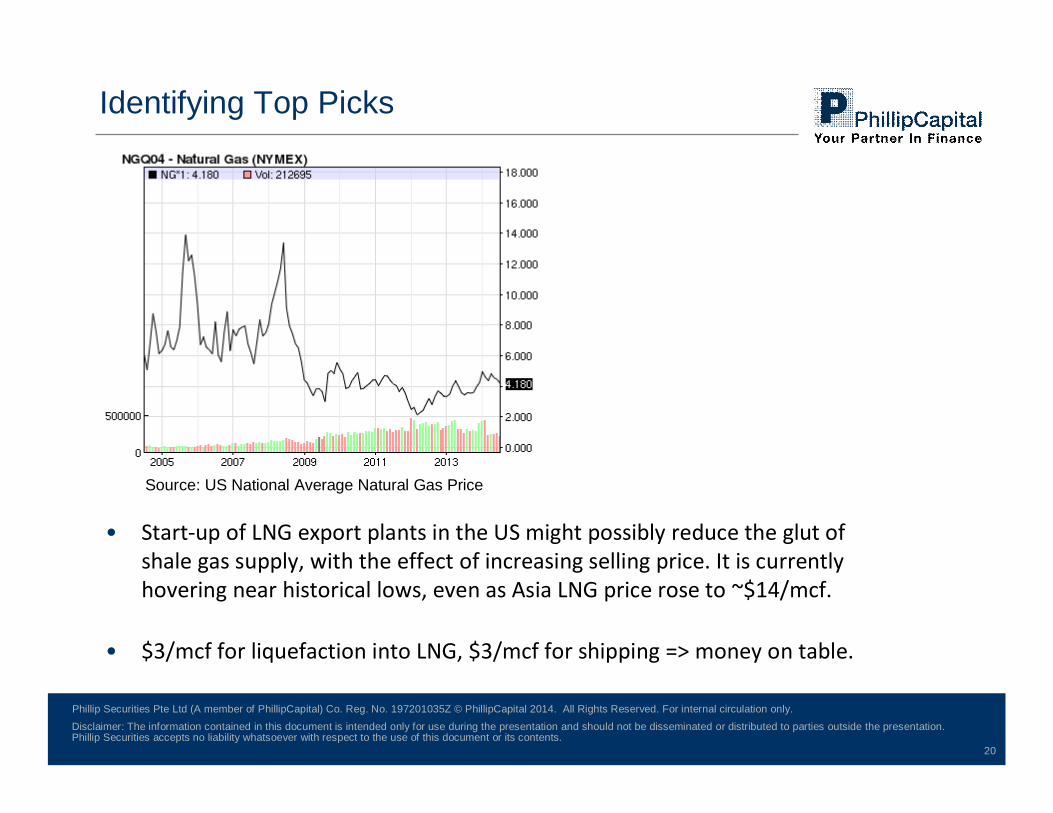

Identifying Top Picks

• Start-up of LNG export plants in the US might possibly reduce the glut of shale gas supply, with the effect of increasing selling price. It is currently hovering near historical lows, even as Asia LNG price rose to ~$14/mcf.

• $3/mcf for liquefaction into LNG, $3/mcf for shipping => money on table.

Source: US National Average Natural Gas Price

Disclaimer: The information contained in this document is intended only for use during the presentation and should not be disseminated or distributed to parties outside the presentation. Phillip Securities accepts no liability whatsoever with respect to the use of this document or its contents.

Phillip Securities Pte Ltd (A member of PhillipCapital) Co. Reg. No. 197201035Z © PhillipCapital 2014. All Rights Reserved. For internal circulation only.

21

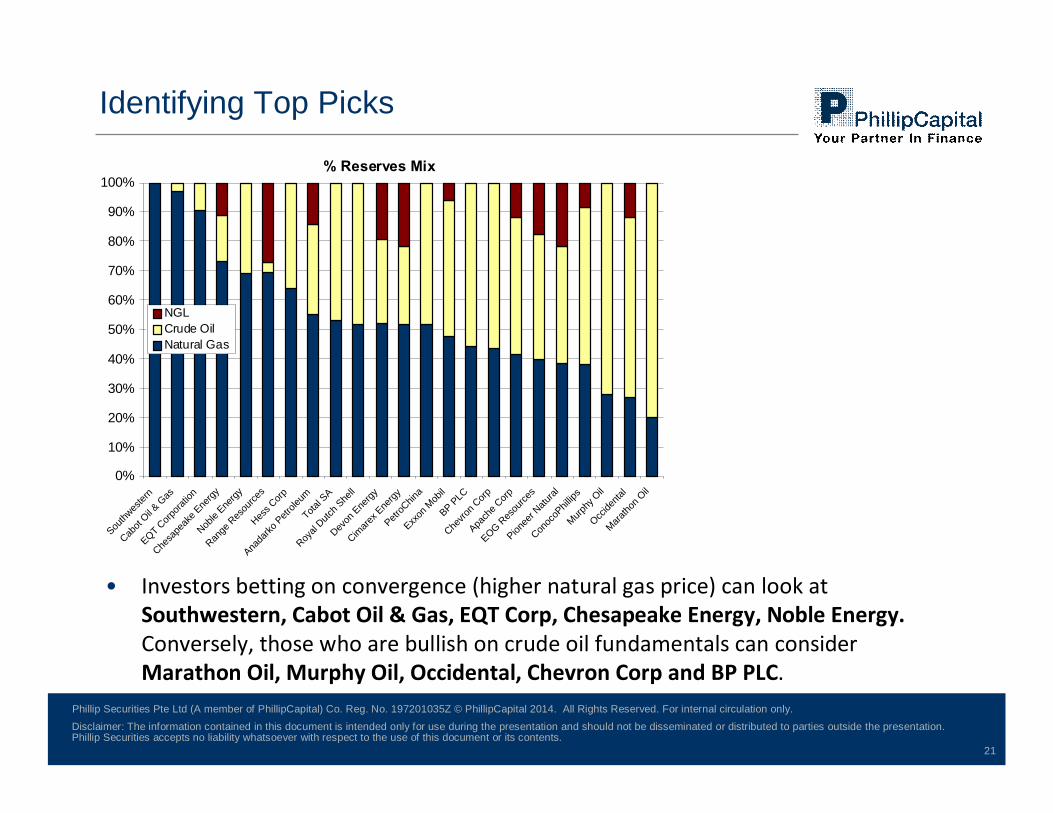

Identifying Top Picks

• Investors betting on convergence (higher natural gas price) can look at Southwestern, Cabot Oil & Gas, EQT Corp, Chesapeake Energy, Noble Energy. Conversely, those who are bullish on crude oil fundamentals can considerMarathon Oil, Murphy Oil, Occidental, Chevron Corp and BP PLC.

% Reserves Mix

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Southw

ester

n

Cabot

Oil & G

as

EQT Corp

oratio

n

Chesa

peak

e Ene

rgy

Noble

Energy

Range

Res

ource

s

Hess C

orp

Anada

rko P

etrole

um

Total S

A

Royal

Dutch S

hell

Devon

Ene

rgy

Cimare

x Ene

rgy

PetroC

hina

Exxon

Mob

il

BP PLC

Chevro

n Corp

Apach

e Corp

EOG Res

ource

s

Pionee

r Natu

ral

Conoc

oPhil

lips

Murphy

Oil

Occide

ntal

Maratho

n Oil

NGLCrude OilNatural Gas

Disclaimer: The information contained in this document is intended only for use during the presentation and should not be disseminated or distributed to parties outside the presentation. Phillip Securities accepts no liability whatsoever with respect to the use of this document or its contents.

Phillip Securities Pte Ltd (A member of PhillipCapital) Co. Reg. No. 197201035Z © PhillipCapital 2014. All Rights Reserved. For internal circulation only.

22

Identifying Top Picks

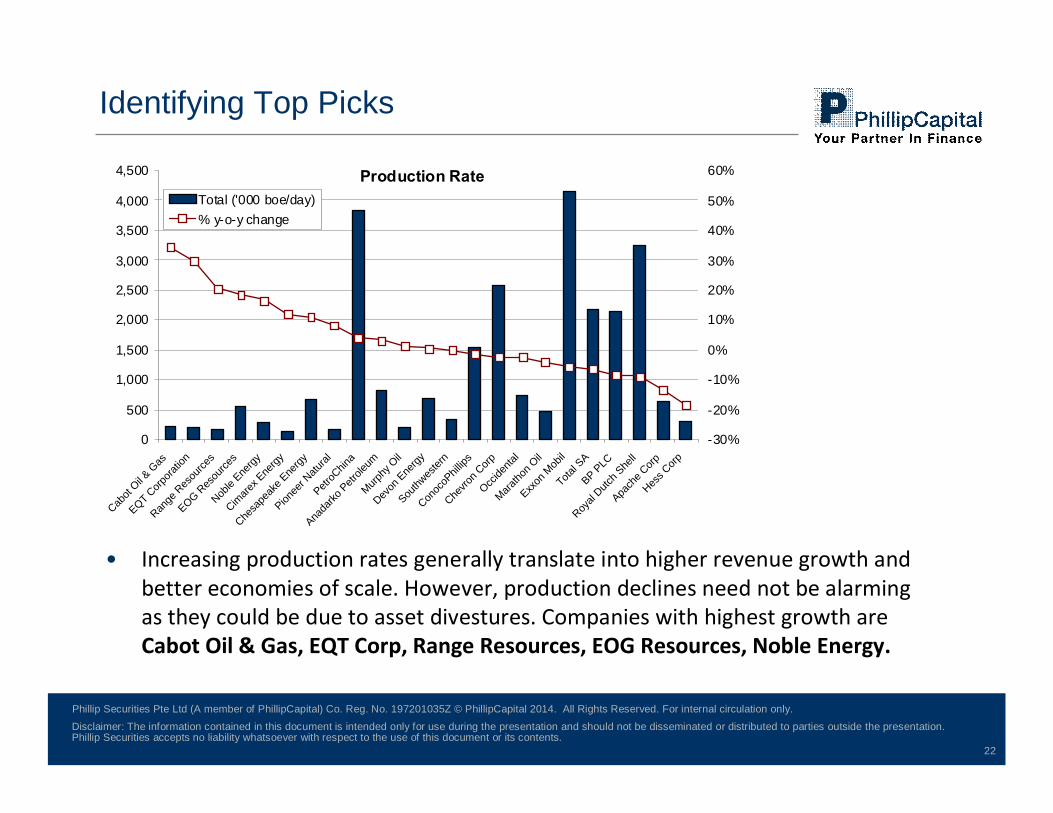

• Increasing production rates generally translate into higher revenue growth and better economies of scale. However, production declines need not be alarming as they could be due to asset divestures. Companies with highest growth are Cabot Oil & Gas, EQT Corp, Range Resources, EOG Resources, Noble Energy.

Production Rate

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

4,500

Cabot

Oil & G

as

EQT Corp

oratio

n

Range

Res

ource

s

EOG Res

ource

s

Noble

Energy

Cimare

x Ene

rgy

Chesa

peak

e Ene

rgy

Pionee

r Natu

ral

PetroC

hina

Anada

rko P

etrole

um

Murphy

Oil

Devon

Ene

rgy

Southw

ester

n

Conoc

oPhil

lips

Chevro

n Corp

Occide

ntal

Maratho

n Oil

Exxon

Mob

il

Total S

A

BP PLC

Royal

Dutch S

hell

Apach

e Corp

Hess C

orp-30%

-20%

-10%

0%

10%

20%

30%

40%

50%

60%

Total ('000 boe/day)% y-o-y change

Disclaimer: The information contained in this document is intended only for use during the presentation and should not be disseminated or distributed to parties outside the presentation. Phillip Securities accepts no liability whatsoever with respect to the use of this document or its contents.

Phillip Securities Pte Ltd (A member of PhillipCapital) Co. Reg. No. 197201035Z © PhillipCapital 2014. All Rights Reserved. For internal circulation only.

23

Identifying Top Picks

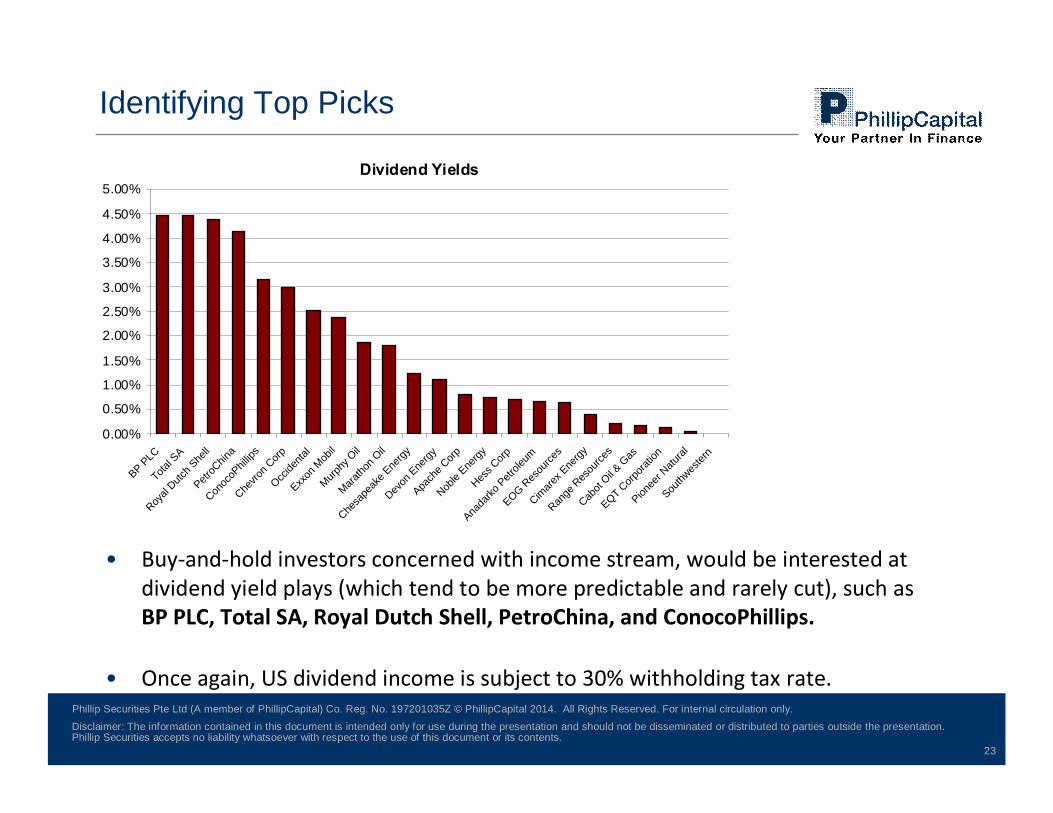

• Buy-and-hold investors concerned with income stream, would be interested at dividend yield plays (which tend to be more predictable and rarely cut), such as BP PLC, Total SA, Royal Dutch Shell, PetroChina, and ConocoPhillips.

• Once again, US dividend income is subject to 30% withholding tax rate.

Dividend Yields

0.00%

0.50%

1.00%

1.50%

2.00%

2.50%

3.00%

3.50%

4.00%

4.50%

5.00%

BP PLC

Total S

A

Royal

Dutch S

hell

PetroC

hina

Conoc

oPhil

lips

Chevro

n Corp

Occide

ntal

Exxon

Mob

il

Murphy

Oil

Maratho

n Oil

Chesa

peak

e Ene

rgy

Devon

Ene

rgy

Apach

e Corp

Noble

Energy

Hess C

orp

Anada

rko P

etrole

um

EOG Res

ource

s

Cimare

x Ene

rgy

Range

Res

ource

s

Cabot

Oil & G

as

EQT Corp

oratio

n

Pionee

r Natu

ral

Southw

ester

n

Disclaimer: The information contained in this document is intended only for use during the presentation and should not be disseminated or distributed to parties outside the presentation. Phillip Securities accepts no liability whatsoever with respect to the use of this document or its contents.

Phillip Securities Pte Ltd (A member of PhillipCapital) Co. Reg. No. 197201035Z © PhillipCapital 2014. All Rights Reserved. For internal circulation only.

24

Ending Remarks

Disclaimer: The information contained in this document is intended only for use during the presentation and should not be disseminated or distributed to parties outside the presentation. Phillip Securities accepts no liability whatsoever with respect to the use of this document or its contents.

Phillip Securities Pte Ltd (A member of PhillipCapital) Co. Reg. No. 197201035Z © PhillipCapital 2014. All Rights Reserved. For internal circulation only.

25

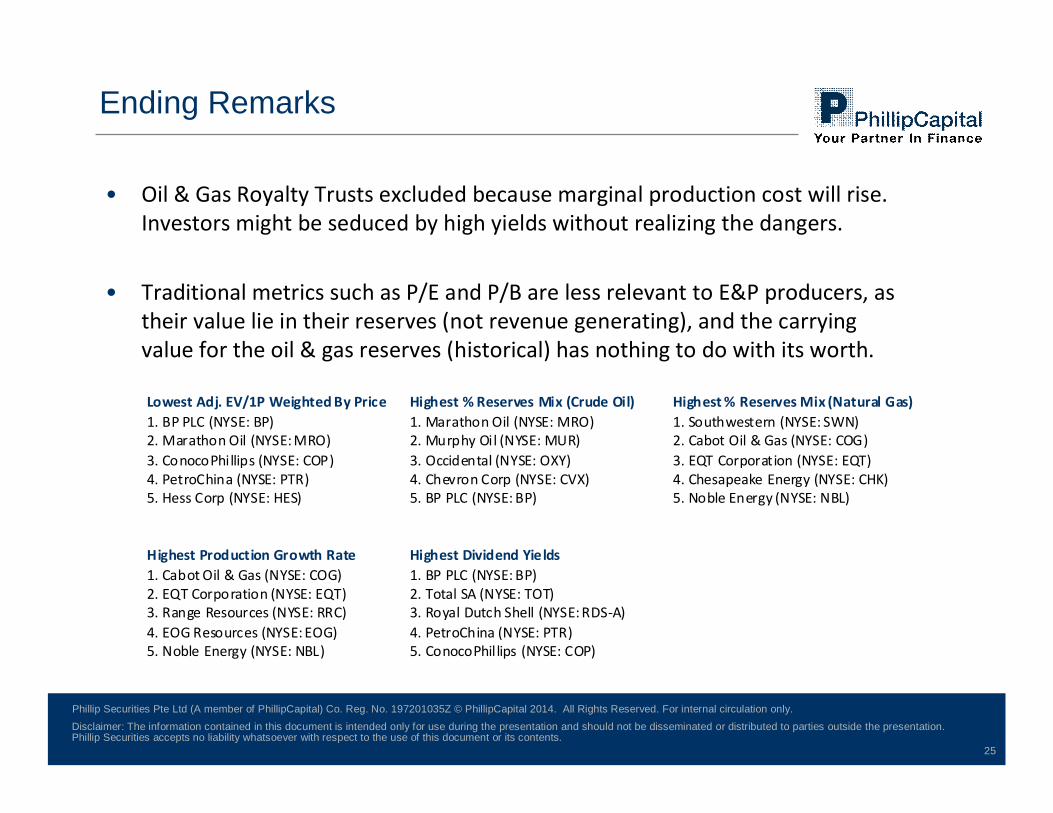

Ending Remarks

• Oil & Gas Royalty Trusts excluded because marginal production cost will rise. Investors might be seduced by high yields without realizing the dangers.

• Traditional metrics such as P/E and P/B are less relevant to E&P producers, as their value lie in their reserves (not revenue generating), and the carrying value for the oil & gas reserves (historical) has nothing to do with its worth.

Lowest Adj. EV/1P Weighted By Price Highest % Reserves Mix (Crude Oil) Highest % Reserves Mix (Natural Gas)1. BP PLC (NYSE: BP) 1. Marathon Oil (NYSE: MRO) 1. Southwestern (NYSE: SWN)2. Marathon Oil (NYSE: MRO) 2. Murphy Oil (NYSE: MUR) 2. Cabot Oil & Gas (NYSE: COG)3. ConocoPhillips (NYSE: COP) 3. Occidental (NYSE: OXY) 3. EQT Corporation (NYSE: EQT) 4. PetroChina (NYSE: PTR) 4. Chevron Corp (NYSE: CVX) 4. Chesapeake Energy (NYSE: CHK) 5. Hess Corp (NYSE: HES) 5. BP PLC (NYSE: BP) 5. Noble Energy (NYSE: NBL)

Highest Production Growth Rate Highest Dividend Yields1. Cabot Oil & Gas (NYSE: COG) 1. BP PLC (NYSE: BP)2. EQT Corporation (NYSE: EQT) 2. Total SA (NYSE: TOT)3. Range Resources (NYSE: RRC) 3. Royal Dutch Shell (NYSE: RDS-A)4. EOG Resources (NYSE: EOG) 4. PetroChina (NYSE: PTR) 5. Noble Energy (NYSE: NBL) 5. ConocoPhillips (NYSE: COP)

Disclaimer: The information contained in this document is intended only for use during the presentation and should not be disseminated or distributed to parties outside the presentation. Phillip Securities accepts no liability whatsoever with respect to the use of this document or its contents.

Phillip Securities Pte Ltd (A member of PhillipCapital) Co. Reg. No. 197201035Z © PhillipCapital 2014. All Rights Reserved. For internal circulation only.

26

Market StrategistsJoshua Tan, Head of Research

Kenneth Koh, Market & Equity Analyst

Soh Lin Sin, Macro Economist

Osama Bakhteyar, Research Assistant

SG & US Equity Analysts Lucas Tan, Real Estate

Wong Yong Kai, US Equities

Colin Tan, Telcos

Caroline Tay, Real Estate

Ben Ong, Financials

Richard Leow, Transport

By Phillip Securities ResearchMr. Chan Wai Chee, CEO

Jermaine Tock, Operations Exec

Ask Questions!

![[XLS] · Web view201407. 201407. 201407. 201407. 201407. 201407. 201407. 201407. 201407. 201407. 201407. 201407. 201407. 201407. 201407. 201407](https://img.pdfslide.net/doc/110x75/5aab066c7f8b9a9c2e8b68d5/xls-view201407-201407-201407-201407-201407-201407-201407-201407-201407.jpg)