Embed Size (px)

Citation preview

Master of Accounting

Program

Information Guide

2016

IMPORTANT DATES

Fall 2015 October 15 ............................. Deadline to apply to MAcc through OUAC

October 16 ............................. Deadline to complete LEARN Winter course selection quiz November 23 ......................... Quest course enrolment for Winter term opens

December 1 ........................... Deadline to submit Undergrad Intent to Graduate Form to Registrar’s Office December 10 ......................... Winter Term Fees Due

Winter 2016

January 4 ............................... Winter Term Lectures Begin January 29 ............................. Deadline to complete LEARN Spring course selection quiz February 15-19 ...................... Reading Week March 25 ............................... University closed – Good Friday

March 31 ............................... Winter Term Lectures End April 4-11 .............................. MAcc Examination Period

Spring 2016 April 25 ................................. Spring Term Fees Due

May 2 ..................................... Spring Term Lectures Begin May 23 ................................... University closed – Victoria Day July 1 ..................................... University closed – Canada Day July 21 ................................... Spring Term Lectures End July 22-July 29 ...................... MAcc Examination Period

Information contained in this Guide is subject to change.

Making Informed Decisions As a UW undergraduate accounting student considering the MAcc Program, you have many important decisions to make. This Guide provides you with most of the information you will need to make informed decisions about the program, but you should also attend the Program and Course Information sessions, speak to faculty who teach in these programs, and talk to alumni who have made these decisions in prior years. The new CPA qualification process contains multiple pathways to the Common Final Evaluation (CFE) and CPA designation, while still allowing some students to have the CA designation tagged onto their CPA if certain conditions are met. Most important, as CPA-Accredited programs, the UW undergraduate/MAcc degree combination still provides direct access to the CFE for successful graduates. Full details of the new pathways and CA tagging are provided in this Guide, so please be sure to read it thoroughly and carefully so that you understand all your options. As Directors of the MAcc program, we are keen to uphold its high standards and will provide you with whatever assistance you may need to make informed decisions. If you have questions about admission or course selection issues, you should direct them to Julie at the email address below. Any issues of a purely administrative or clerical nature should be directed to Kaitlyn Kraatz, the Graduate Studies Co-ordinator ([email protected]). All other queries can be directed to Greg at the address below.

Greg Berberich, CPA, CA, PhD Julie Robson, CPA, CA, MAcc CPA (Illinois) Director Associate Director, Admissions MAcc & Diploma Programs MAcc & Diploma Programs [email protected] [email protected]

MAcc Program Information Guide

Table of Contents Program Overview .................................................................................................................................... 1 Admission & Degree Requirements ......................................................................................................... 7 Course Information ................................................................................................................................. 12 Application & Course Selection ............................................................................................................. 49 Tuition and Scholarships ........................................................................................................................ 54 This PDF also contains numerous bookmarks to facilitate navigation through its contents.

Program Overview

1

PROGRAM OVERVIEW

The MAcc is a professional degree designed to combine the exploration of career interests with preparation for the CFE. Students with a specific career interest may select courses that provide them with a head start on this career. Students without a specific career interest may take courses in several practice areas to determine which careers they might like to pursue. All MAcc students must take five courses that develop the technical and enabling competencies needed to pass the CFE and obtain the CPA designation. The MAcc program is accredited by CPA Canada, so students who successfully complete the program may proceed directly to the September 2016 CFE.

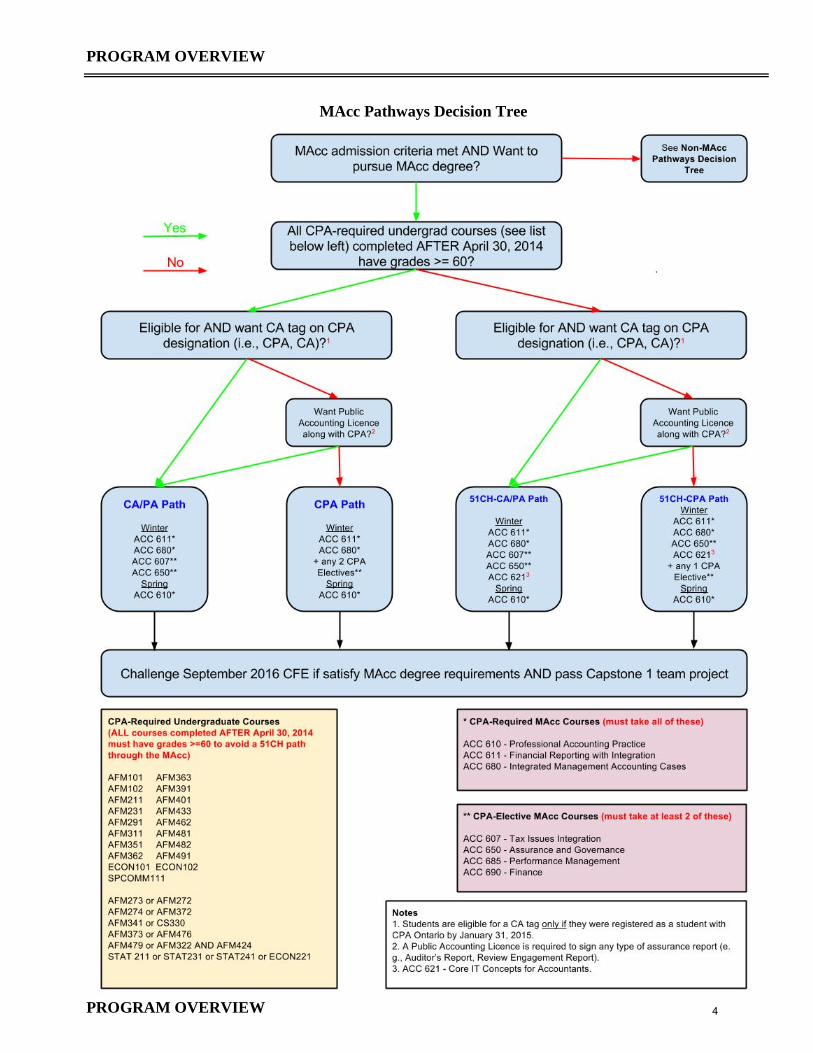

Career Paths The MAcc program is designed to combine professional accounting career interests with preparation for the CFE. Some students considering the MAcc program may have already identified a particular career path by the end of their undergraduate program, whereas others may still be uncertain about the accounting career they want to pursue. The MAcc program offers benefits to both groups. Students who have determined a particular career path can select courses that will develop the competencies required for success in their chosen career. Students considering a career as part of the management team of an organization can, for example, take courses that will expand their knowledge of contemporary management issues, assist them in designing and implementing incentive systems, improve their financial statement analysis competencies, or expand their ability to develop and execute profitable business models. Students who are less certain about their careers can select courses that will provide them with exposure to a variety of practice areas, such as forensic accounting, tax or business valuations, to determine the practice areas they would like to pursue upon completing the MAcc. The Course Information section of the Guide provides some guidance on selecting courses pertaining to specific designations and careers. MAcc Pathways to a CPA(,CA) Designation Within the MAcc program there are four distinct pathways to the CPA designation, with two of them also leading to a CA tag if you meet the criteria below. These pathways are described on the next page and the decision tree that follows will help you determine which of these pathways you are eligible to follow, along with the MAcc courses you must take for each pathway. Criteria Required for a CA Tag (all four criteria must be met by February 1, 2020) 1. Registered as CA Legacy student in good standing with CPA Ontario as at January 31, 2015. 2. Complete the 51-Credit-Hour-CA/Public Accounting or CA/Public Accounting pathway through the

MAcc (see next page for details on these pathways). 3. Demonstrate depth in the Assurance and Financial Reporting areas of the CPA Competency Map

when writing the CFE. 4. Complete 36 months of practical experience with an Approved Training Office.

2

PROGRAM OVERVIEW The 51-Credit-Hour Pathways Any MAcc student with a grade below 60 in any CPA-required undergraduate course completed after April 30, 2014 (see next page for list of courses) must follow one of the two 51CH pathways through the MAcc. All other MAcc students may follow one of the two other pathways in the next subsection. The 51-Credit-Hour-CA/Public Accounting (51CH-CA/PA) Pathway Students who fall in the above category must follow this pathway if they want to (1) be eligible for a Public Accounting Licence* or (2) be eligible for the CA tag (all other CA tag conditions must be met as well). The 51-Credit-Hour-CPA (51CH-CPA) Pathway Students who follow this pathway will be eligible for a CPA designation, but will not be eligible for either a Public Accounting Licence* or a CA tag. The CA/PA and CPA Pathways Students with grades of 60 or higher in all CPA-required undergraduate courses (see next page for list) may follow one of these two pathways: The CA/Public Accounting (CA/PA) Pathway Students must follow this pathway if they want to (1) be eligible for a Public Accounting Licence* or (2) be eligible for the CA tag (all other CA tag conditions must be met as well). The CPA Pathway Students who follow this pathway will be eligible for a CPA designation, but will not be eligible for either a Public Accounting Licence* or a CA tag. * A Public Accounting Licence is required to sign assurance reports such as audit or review engagement reports. It is not required to simply work as an auditor at a public accounting firm. Even students who do not follow a Public Accounting pathway to the CPA designation will be able to receive a Licence at a later date by fulfilling supplementary requirements to be set by the Public Accountants’ Council of Ontario.

3

PROGRAM OVERVIEW

MAcc Pathways Decision Tree

PROGRAM OVERVIEW 4

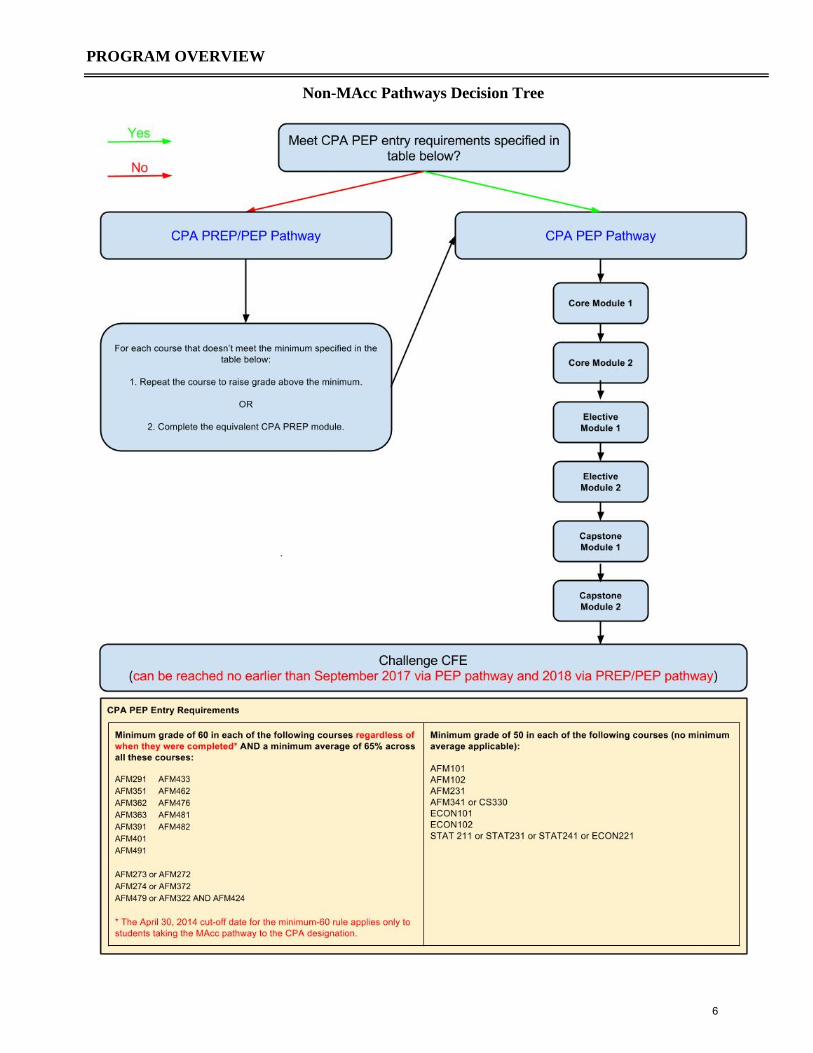

Non-MAcc Pathways to a CPA Designation For students who do not want to or are ineligible to complete the MAcc program, there are two pathways to the CPA designation, the CPA PEP pathway and the CPA PREP/PEP pathway. Neither of these pathways permit students to obtain the CA tag, and the PREP/PEP pathway also precludes students from obtaining a Public Accounting Licence. These pathways are described below and the decision tree on the next page will let you determine which of these pathways you are eligible to follow. CPA PEP Pathway Students who meet the entry criteria for the CPA Professional Education Program (PEP; see next page for criteria) may proceed directly to the first Core module of the program. Students eligible to follow this pathway could reach the CFE by September 2017. CPA PREP/PEP Pathway Students who do not meet the PEP entry criteria must first repeat applicable university courses or take the equivalent modules in the CPA Prerequisite Education Program (PREP). The PREP courses are cheaper and quicker, so they are the recommended option for students who must follow this pathway. Once the PEP entry criteria have been met, students may proceed to the first Core module of the PEP. Students who must follow this pathway will not be able to reach the CFE until 2018 at the earliest.

5

PROGRAM OVERVIEW

Non-MAcc Pathways Decision Tree

6

Admission & Degree Requirements

7

ADMISSION & DEGREE REQUIREMENTS Admission Requirements

Admission to the MAcc program requires ALL of the following: 1. Successful completion of one of the following University of Waterloo undergraduate degrees by no

later than February 1, 2016:

• Bachelor of Accounting and Financial Management • BMath Chartered Professional Accountancy Studies, or • BSc in Biotechnology Chartered Professional Accountancy Studies

2. Achievement of at least a 75% average (calculated with rounding) in the last two years of the undergraduate program above. This admission average is calculated using the grades obtained in all courses completed beginning in the 3A term and ending in the term immediately preceding commencement of the MAcc program. If a course has been repeated, grades from all attempts will be included in the calculation of this admission average.

3. Achievement of at least a 75% average (calculated with rounding) in the following set of courses. If a course has been repeated, the grade obtained in the student’s first attempt at the course will be included in the calculation of this admission average. Students who took any of the following courses at an institution other than UW must include with their MAcc application an official transcript from the other institution that provides details of the course(s) taken and the grade(s) received.

• AFM 311 • AFM 341 or CS 330 • AFM 351 • AFM 362 • AFM 363 • AFM 373 or AFM 476 • AFM 391 • AFM 401 • AFM 433 • AFM 462 • AFM 479 or AFM 322 and AFM 424 • AFM 481 • AFM 482 • AFM 491

For any pre-Class of 2016 students applying to the MAcc, the following set of courses will be used to determine your special admission average: AFM 331, AFM 341 or CS 330, AFM 361, AFM 391, AFM 401, AFM 431 or PHIL 215, AFM 451, AFM 461, AFM 471 or AFM 476, AFM 481, AFM 482, and AFM 491.

8

ADMISSION & DEGREE REQUIREMENTS Conditional Admission Offers Once all MAcc applications have been received and reviewed, conditional offers of admission will be made to all applicants meeting both of the following requirements: 1. Achievement of at least a 75% average (calculated with rounding) across all courses completed

between and including the student’s 3A term and the Spring 2015 term. Where a course has been repeated, grades from all attempts will be included in the calculation of this admission average.

2. Achievement of at least a 75% average across all courses in the list below that have been completed by the time of application to the program. Where a course has been repeated, the grade obtained in the student’s first attempt at the course will be included in the calculation of this admission average. Students who took any of the following courses at an institution other than UW must include with their MAcc application an official transcript from the other institution that provides details of the course(s) taken and the grade(s) received.

• AFM 311 • AFM 341 or CS 330 • AFM 351 • AFM 362 • AFM 363 • AFM 373 or AFM 476 • AFM 391 • AFM 401 • AFM 433 • AFM 462 • AFM 479 or AFM 322 and AFM 424 • AFM 481 • AFM 482 • AFM 491

Students who have not received a numerical grade in at least seven of these courses by the time of application will be deemed not to have met this requirement.

Any students who do not receive a conditional offer of admission will be considered for admission once all 4B grades are final.

9

ADMISSION & DEGREE REQUIREMENTS Degree Requirements To receive an MAcc degree, students must:

1. Achieve a grade of at least 60% in each MAcc course and a minimum overall average of 75% in all eight MAcc courses (calculated without rounding).

AND 2. Complete the online Graduate Academic Integrity Module (Graduate AIM).

At the conclusion of the winter term, a panel of SAF faculty is convened to conduct a review of each MAcc student whose cumulative average is below 75%. These students may be given the opportunity to proceed to the spring term if, in the opinion of the review panel, they have a reasonable prospect of achieving the degree requirements upon completion of the spring term. Any student who is deemed not to have a reasonable prospect of satisfying the degree requirements by the end of the spring term will be required to withdraw from the MAcc program. CFE Eligibility In accordance with the program’s accreditation agreement with CPA Canada and CPA Ontario, to be placed on the list of students eligible to proceed directly to the CFE, students must:

1. Satisfy the MAcc degree requirements above.

AND

2. Achieve a passing grade on the Capstone 1 team project completed as part of ACC 610 in the Spring term of the MAcc program.

It is therefore possible to satisfy MAcc degree requirements but still not be permitted to proceed directly to the CFE.

10

OTHER PROGRAM POLICIES Academic Integrity All MAcc students are subject to UW’s Academic Integrity policies, which can be found under Policy 71 at the UW Secretariat’s website. Missing Final Exams for Valid Reasons Students should note that while UW's examination policy does allow certain valid reason for missing a final examination, it does not automatically entitle a student to an alternate exam before the end of the program year (See UW’s Exam Regulations at the Registrar’s website for more information.). Because it is not possible to set, administer, and grade a deferred final exam by the end of the program year, completion of the MAcc degree requirements is effectively deferred by one year for any students missing a final exam for a valid reason. Section Assignments Students enrolled in courses with multiple sections must attend the section in which they are registered, unless they receive prior instructor approval to attend another section due to an acceptable, non-recurring conflict.

Communicating with Students All program-related email is sent to your @uwaterloo.ca address. If you wish to have email redirected to another address, please refer to the mail-forwarding guidelines at UW’s Official Student Email Address webpage.

11

Course Information

12

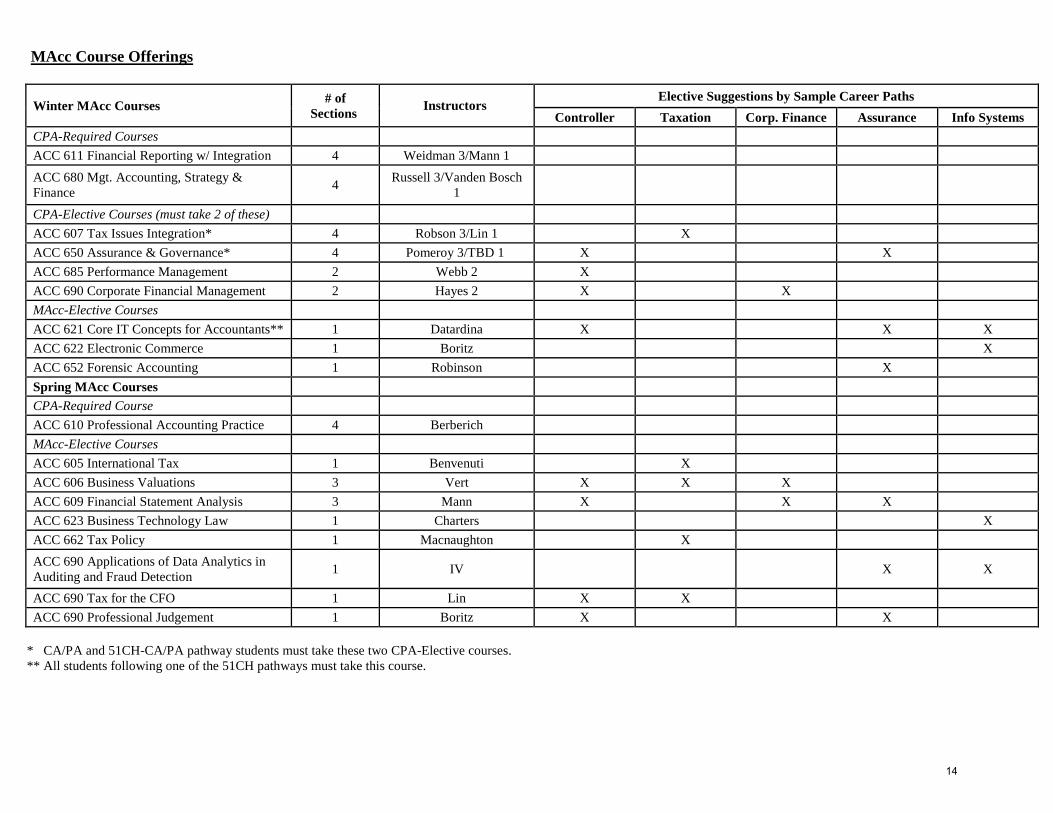

COURSE INFORMATION MAcc Courses Course offerings fall into three categories: CPA-Required Courses ACC 610 – Professional Accounting Practice ACC 611 – Financial Reporting with Integration ACC 680 – Management Accounting, Strategy and Finance All students pursuing a CPA designation must take these courses. CPA-Elective Courses ACC 607 – Tax Issues Integration ACC 650 – Assurance and Governance ACC 685 – Performance Management ACC 690 – Corporate Financial Management All students pursuing a CPA designation must take two of these courses and can take as many as three. Students following the CA/PA or 51CH-CA/PA pathway through the MAcc must take ACC 607 and ACC 650. Students following the 51CH-CPA pathway must take ACC 650. All other CPA students may choose any of the electives. MAcc-Elective Courses ACC 605 – International Tax ACC 606 – Business Valuations ACC 609 – Financial Statement Analysis ACC 621 – Core IT Concepts for Accountants ACC 622 – Electronic Commerce ACC 623 – Business Technology Law - IT Challenges & Opportunities ACC 652 – Forensic Accounting ACC 662 – Tax Policy ACC 690 – Applications of Data Analytics in Auditing and Fraud Detection ACC 690 – Professional Judgement ACC 690 – Tax for the CFO MAcc students who take two CPA-Elective courses must take three MAcc-Elective courses, while those who take three CPA-Elective courses must take two MAcc-Elective courses. All students following a 51CH pathway must take ACC 621, so they can take only two CPA-Elective courses. The table on the next page provides key details on these course offerings and also suggests which elective courses to consider if you are interested in a particular career path. The pages following the table provide descriptions of each course.

13

MAcc Course Offerings

Winter MAcc Courses # of Sections Instructors

Elective Suggestions by Sample Career Paths Controller Taxation Corp. Finance Assurance Info Systems

CPA-Required Courses ACC 611 Financial Reporting w/ Integration 4 Weidman 3/Mann 1 ACC 680 Mgt. Accounting, Strategy & Finance 4 Russell 3/Vanden Bosch

1

CPA-Elective Courses (must take 2 of these) ACC 607 Tax Issues Integration* 4 Robson 3/Lin 1 X ACC 650 Assurance & Governance* 4 Pomeroy 3/TBD 1 X X ACC 685 Performance Management 2 Webb 2 X ACC 690 Corporate Financial Management 2 Hayes 2 X X MAcc-Elective Courses ACC 621 Core IT Concepts for Accountants** 1 Datardina X X X ACC 622 Electronic Commerce 1 Boritz X ACC 652 Forensic Accounting 1 Robinson X Spring MAcc Courses CPA-Required Course ACC 610 Professional Accounting Practice 4 Berberich MAcc-Elective Courses ACC 605 International Tax 1 Benvenuti X ACC 606 Business Valuations 3 Vert X X X ACC 609 Financial Statement Analysis 3 Mann X X X ACC 623 Business Technology Law 1 Charters X ACC 662 Tax Policy 1 Macnaughton X ACC 690 Applications of Data Analytics in Auditing and Fraud Detection 1 IV X X

ACC 690 Tax for the CFO 1 Lin X X ACC 690 Professional Judgement 1 Boritz X X

* CA/PA and 51CH-CA/PA pathway students must take these two CPA-Elective courses. ** All students following one of the 51CH pathways must take this course.

14

CPA-Required Courses

15

ACC 610 Professional Accounting Practice

CPA-Required

Faculty: Greg Berberich and various Group Facilitators Term Offered: Spring

Career Relevance

This course is required for all students pursuing a CPA designation. It will be used to deliver CPA Canada’s Capstone 1 module and will also provide extensive exam-writing practice to prepare students for all three days of the CFE.

Course Overview and Objectives

Group Case Component (graded on Pass/Fail basis) The first day of the CFE consists of one large case featuring the same company that is the subject of CPA Canada’s Capstone 1 module, which consists solely of a major group case analysis with a related written report and oral presentation. One significant component of ACC 610 is the direct delivery of this Capstone module. Per CPA Canada’s Capstone 1 guidance, this module’s primary objectives are to: 1. Continue the development of candidates' enabling competencies,

particularly their teamwork and leadership, professional and ethical behaviour, problem-solving and decision-making, and communication competencies;

2. Simulate an authentic business problem, including gathering and evaluating relevant information, developing a written report, and preparing an oral presentation suitable for delivery to a board of directors or senior management team;

3. Prepare candidates for the Common Final Examination, particularly Day 1, which will draw on both the content and the skills developed in Capstone 1;

4. Continue the development of candidates' integration of technical competency areas;

and key aspects of the module include: • a significant written report that simulates a report to a board of directors

or team of senior executives • an oral team presentation that simulates a presentation to a board or

team of senior executives • structured time for questions and answers that simulates a question

period from a board or team of senior executives • individual reflections and peer evaluations. Each group will be assigned an outside facilitator who will provide guidance (not solutions!) as the group completes its work.

16

ACC 610

Professional Accounting Practice

Course Overview and Objectives (continued)

Individual Exam-Writing Component This component of the course will provide extensive opportunities to fine-tune the competencies required for success on the CFE. Its broad objectives are to: 1. Continue your development of the CPA Competency Map’s enabling

competencies, particularly your written communication and self-management competencies;

2. Continue the development of your ability to draw on and integrate knowledge from the CPA Competency Map’s six technical competency areas;

3. Prepare you for the various types of cases you will encounter across all three days of the CFE.

These objectives will be accomplished using weekly practice exam-writing sessions, in-class debriefing of cases, peer evaluations, and formal case examinations.

Course Materials

All required materials will be distributed via the course website. The CPA Handbook and Canadian Income Tax Act will also be important resources.

Proposed Course Evaluation and Workload

NOTE: The workload in this course will be very heavy. All work related to the Capstone 1 group project will be done outside of class time and the project will be much more challenging than any you’ve encountered before: “The case for Capstone 1 is unlike other cases that candidates would have seen in the CPA PEP [or university] due to its complexity and length, its increased focus on strategic analysis, its integrative nature, its requirement for external research, and the potential for increased ambiguity and lack of directedness for critical variables and assumptions.” (CPA Canada) In addition, the work required for the individual exam-writing component will be roughly equivalent to that of a standard MAcc course. You should therefore be prepared to work very hard in this course. Final grades in the course will likely be determined in the following manner: Component Evaluation Entry-Level Competency Diagnostic Examination Class Participation Core-Level Competency Diagnostic Examination

10% 20% 10%

Midterm Examination 30% Final Examination 30%

17

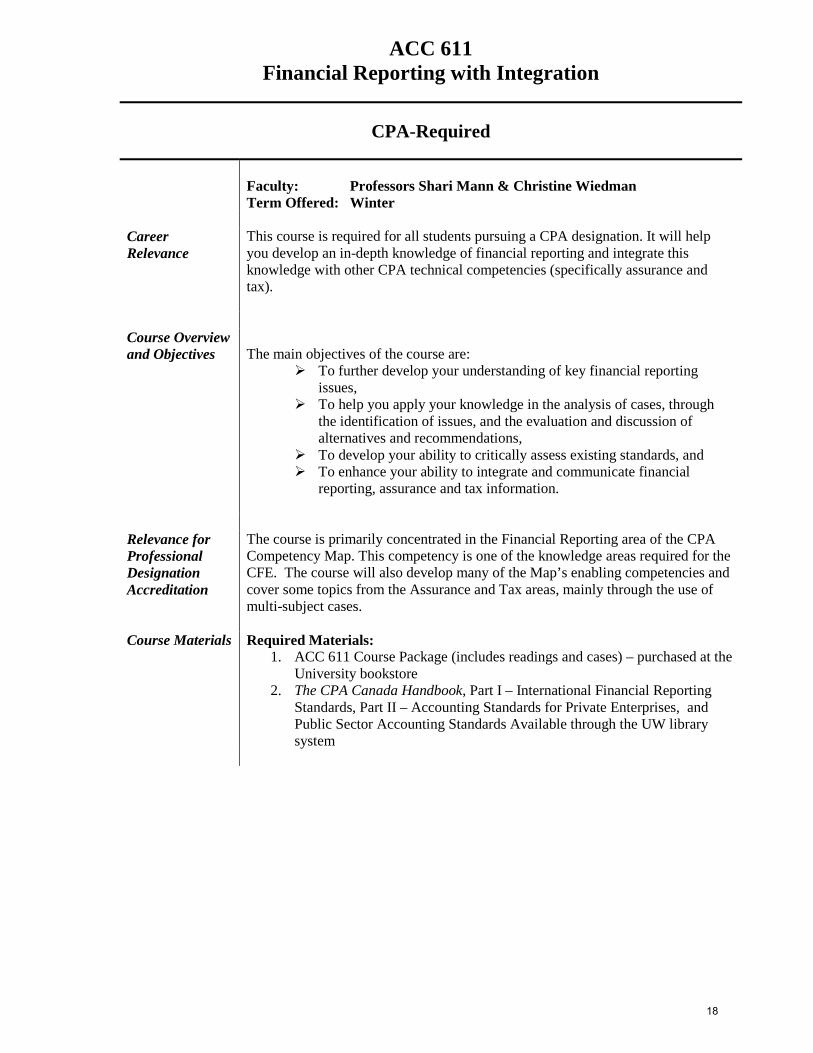

ACC 611 Financial Reporting with Integration

CPA-Required

Faculty: Professors Shari Mann & Christine Wiedman Term Offered: Winter

Career Relevance

This course is required for all students pursuing a CPA designation. It will help you develop an in-depth knowledge of financial reporting and integrate this knowledge with other CPA technical competencies (specifically assurance and tax).

Course Overview and Objectives

The main objectives of the course are:

To further develop your understanding of key financial reporting issues,

To help you apply your knowledge in the analysis of cases, through the identification of issues, and the evaluation and discussion of alternatives and recommendations,

To develop your ability to critically assess existing standards, and To enhance your ability to integrate and communicate financial

reporting, assurance and tax information.

Relevance for Professional Designation Accreditation

The course is primarily concentrated in the Financial Reporting area of the CPA Competency Map. This competency is one of the knowledge areas required for the CFE. The course will also develop many of the Map’s enabling competencies and cover some topics from the Assurance and Tax areas, mainly through the use of multi-subject cases.

Course Materials Required Materials: 1. ACC 611 Course Package (includes readings and cases) – purchased at the

University bookstore 2. The CPA Canada Handbook, Part I – International Financial Reporting

Standards, Part II – Accounting Standards for Private Enterprises, and Public Sector Accounting Standards Available through the UW library system

18

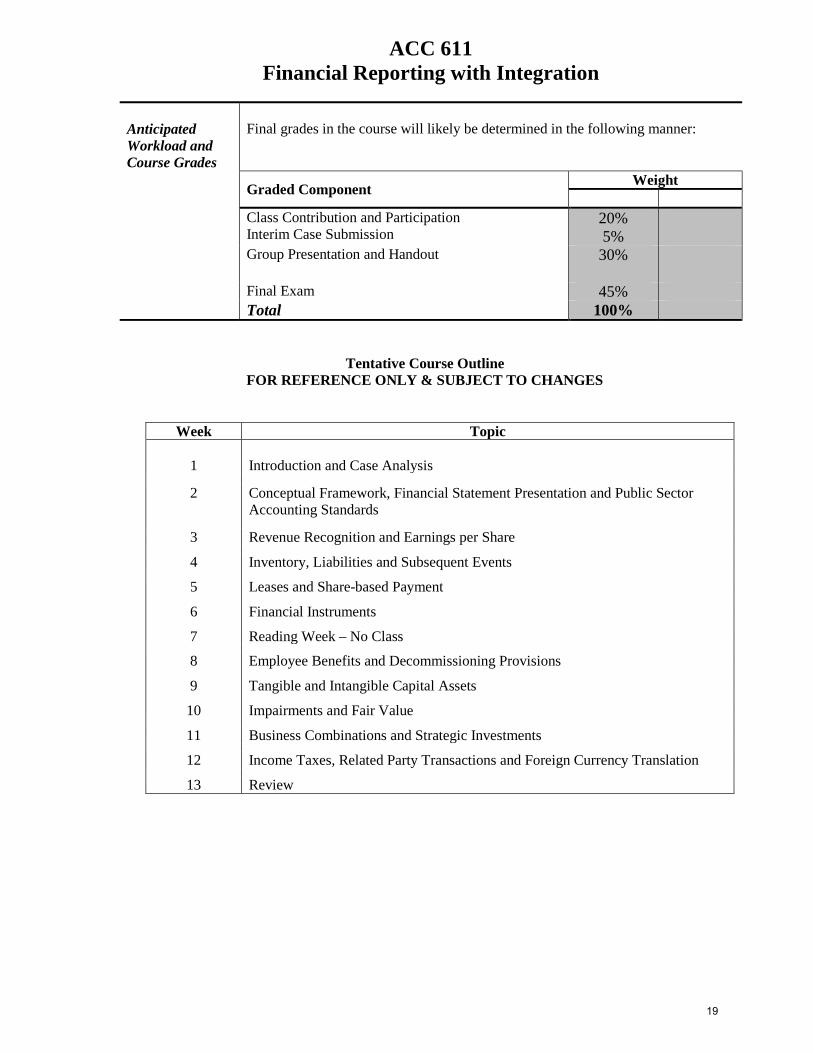

ACC 611 Financial Reporting with Integration

Anticipated Workload and Course Grades

Final grades in the course will likely be determined in the following manner:

Graded Component Weight

Class Contribution and Participation Interim Case Submission

20% 5%

Group Presentation and Handout 30% Final Exam 45% Total 100%

Tentative Course Outline FOR REFERENCE ONLY & SUBJECT TO CHANGES

Week Topic

1 Introduction and Case Analysis 2 Conceptual Framework, Financial Statement Presentation and Public Sector

Accounting Standards 3 Revenue Recognition and Earnings per Share 4 Inventory, Liabilities and Subsequent Events 5 Leases and Share-based Payment 6 Financial Instruments 7 Reading Week – No Class 8 Employee Benefits and Decommissioning Provisions 9 Tangible and Intangible Capital Assets 10 Impairments and Fair Value 11 Business Combinations and Strategic Investments 12 Income Taxes, Related Party Transactions and Foreign Currency Translation 13 Review

19

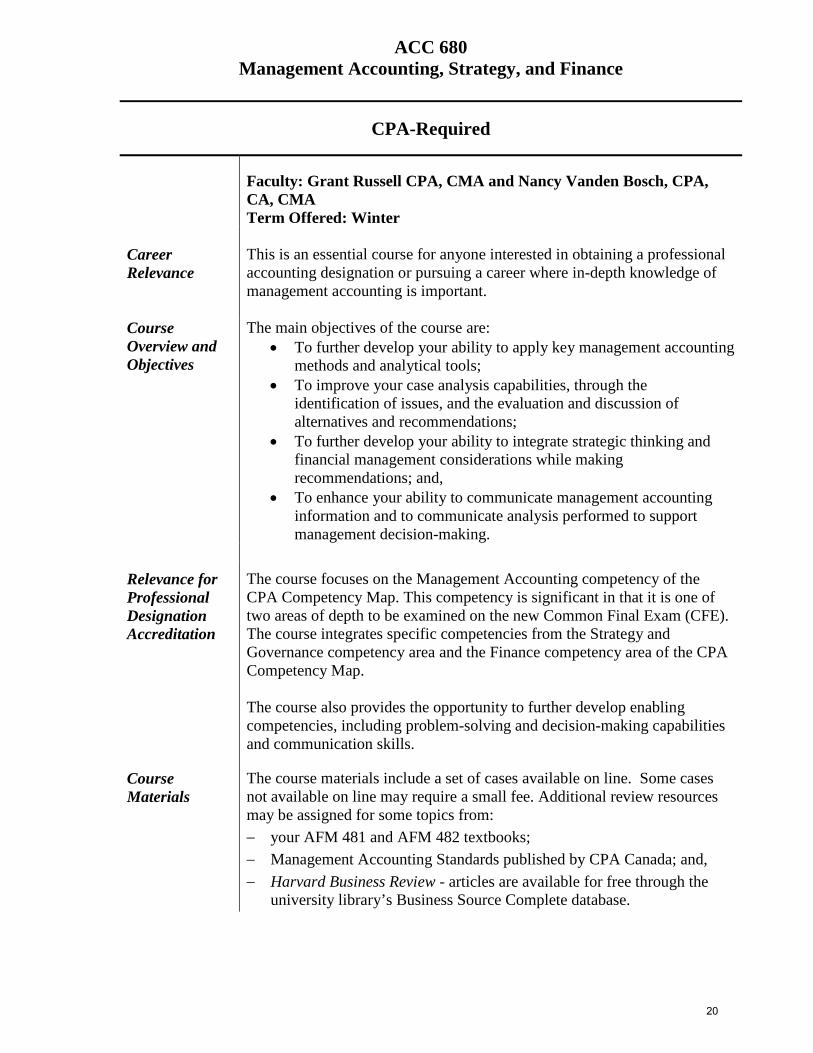

ACC 680 Management Accounting, Strategy, and Finance

CPA-Required

Faculty: Grant Russell CPA, CMA and Nancy Vanden Bosch, CPA, CA, CMA Term Offered: Winter

Career Relevance

This is an essential course for anyone interested in obtaining a professional accounting designation or pursuing a career where in-depth knowledge of management accounting is important.

Course Overview and Objectives

The main objectives of the course are: • To further develop your ability to apply key management accounting

methods and analytical tools; • To improve your case analysis capabilities, through the

identification of issues, and the evaluation and discussion of alternatives and recommendations;

• To further develop your ability to integrate strategic thinking and financial management considerations while making recommendations; and,

• To enhance your ability to communicate management accounting information and to communicate analysis performed to support management decision-making.

Relevance for Professional Designation Accreditation

The course focuses on the Management Accounting competency of the CPA Competency Map. This competency is significant in that it is one of two areas of depth to be examined on the new Common Final Exam (CFE). The course integrates specific competencies from the Strategy and Governance competency area and the Finance competency area of the CPA Competency Map. The course also provides the opportunity to further develop enabling competencies, including problem-solving and decision-making capabilities and communication skills.

Course Materials

The course materials include a set of cases available on line. Some cases not available on line may require a small fee. Additional review resources may be assigned for some topics from: − your AFM 481 and AFM 482 textbooks; − Management Accounting Standards published by CPA Canada; and, − Harvard Business Review - articles are available for free through the

university library’s Business Source Complete database.

20

ACC 680 Management Accounting, Strategy, and Finance

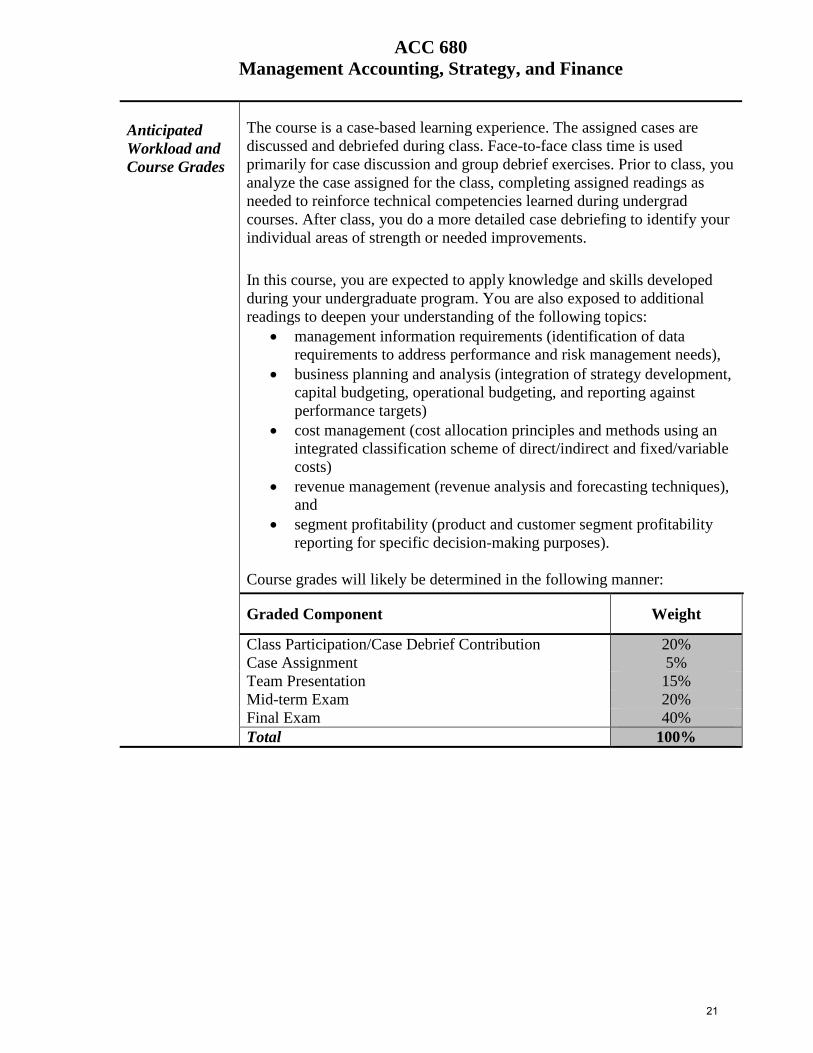

Anticipated Workload and Course Grades

The course is a case-based learning experience. The assigned cases are discussed and debriefed during class. Face-to-face class time is used primarily for case discussion and group debrief exercises. Prior to class, you analyze the case assigned for the class, completing assigned readings as needed to reinforce technical competencies learned during undergrad courses. After class, you do a more detailed case debriefing to identify your individual areas of strength or needed improvements.

In this course, you are expected to apply knowledge and skills developed during your undergraduate program. You are also exposed to additional readings to deepen your understanding of the following topics:

• management information requirements (identification of data requirements to address performance and risk management needs),

• business planning and analysis (integration of strategy development, capital budgeting, operational budgeting, and reporting against performance targets)

• cost management (cost allocation principles and methods using an integrated classification scheme of direct/indirect and fixed/variable costs)

• revenue management (revenue analysis and forecasting techniques), and

• segment profitability (product and customer segment profitability reporting for specific decision-making purposes).

Course grades will likely be determined in the following manner:

Graded Component Weight

Class Participation/Case Debrief Contribution Case Assignment

20% 5%

Team Presentation 15% Mid-term Exam 20% Final Exam 40% Total 100%

21

CPA-Elective Courses

22

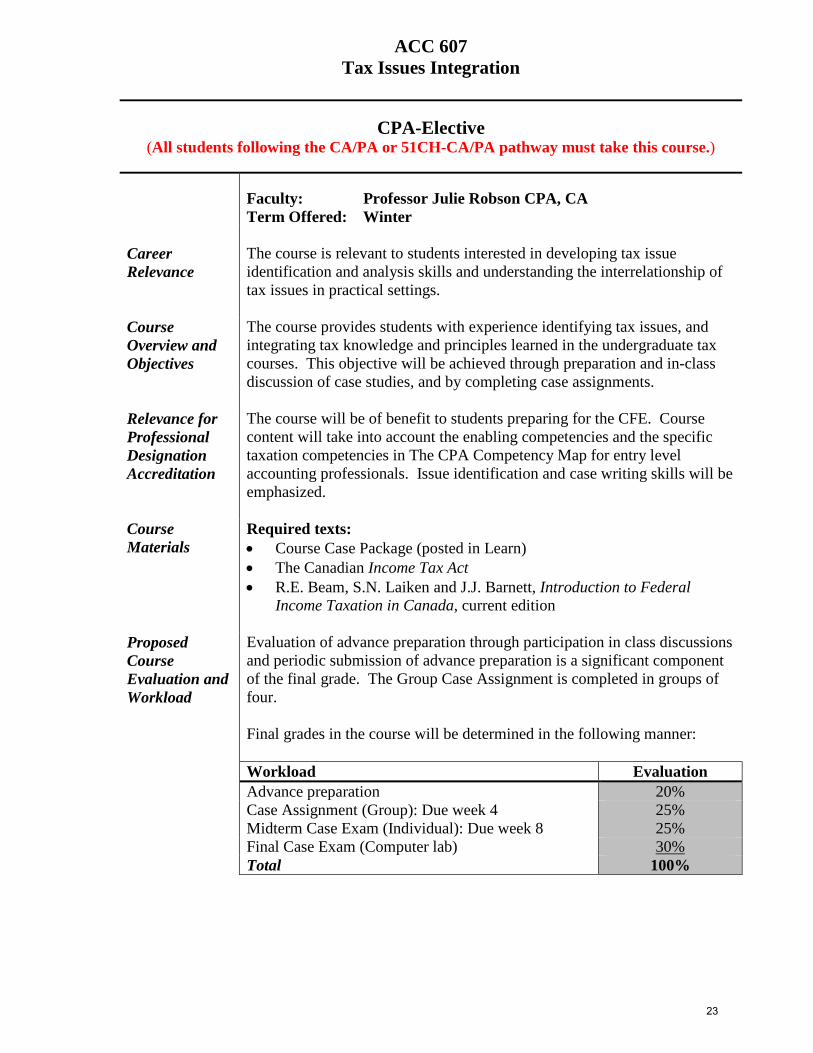

ACC 607 Tax Issues Integration

CPA-Elective (All students following the CA/PA or 51CH-CA/PA pathway must take this course.)

Faculty: Professor Julie Robson CPA, CA Term Offered: Winter

Career Relevance

The course is relevant to students interested in developing tax issue identification and analysis skills and understanding the interrelationship of tax issues in practical settings.

Course Overview and Objectives

The course provides students with experience identifying tax issues, and integrating tax knowledge and principles learned in the undergraduate tax courses. This objective will be achieved through preparation and in-class discussion of case studies, and by completing case assignments.

Relevance for Professional Designation Accreditation

The course will be of benefit to students preparing for the CFE. Course content will take into account the enabling competencies and the specific taxation competencies in The CPA Competency Map for entry level accounting professionals. Issue identification and case writing skills will be emphasized.

Course Materials

Required texts: • Course Case Package (posted in Learn) • The Canadian Income Tax Act • R.E. Beam, S.N. Laiken and J.J. Barnett, Introduction to Federal

Income Taxation in Canada, current edition

Proposed Course Evaluation and Workload

Evaluation of advance preparation through participation in class discussions and periodic submission of advance preparation is a significant component of the final grade. The Group Case Assignment is completed in groups of four. Final grades in the course will be determined in the following manner:

Workload Evaluation Advance preparation 20% Case Assignment (Group): Due week 4 25% Midterm Case Exam (Individual): Due week 8 25% Final Case Exam (Computer lab) 30% Total 100%

23

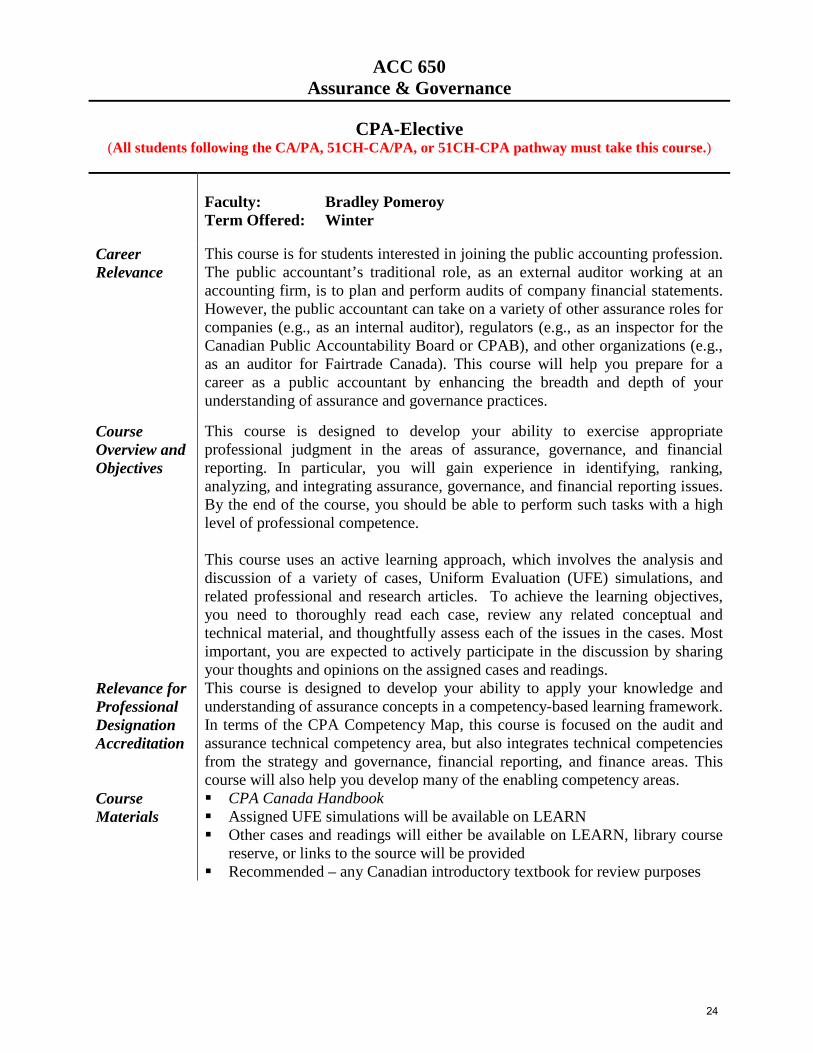

ACC 650 Assurance & Governance

CPA-Elective (All students following the CA/PA, 51CH-CA/PA, or 51CH-CPA pathway must take this course.)

Faculty: Bradley Pomeroy Term Offered: Winter

Career Relevance

This course is for students interested in joining the public accounting profession. The public accountant’s traditional role, as an external auditor working at an accounting firm, is to plan and perform audits of company financial statements. However, the public accountant can take on a variety of other assurance roles for companies (e.g., as an internal auditor), regulators (e.g., as an inspector for the Canadian Public Accountability Board or CPAB), and other organizations (e.g., as an auditor for Fairtrade Canada). This course will help you prepare for a career as a public accountant by enhancing the breadth and depth of your understanding of assurance and governance practices.

Course Overview and Objectives

This course is designed to develop your ability to exercise appropriate professional judgment in the areas of assurance, governance, and financial reporting. In particular, you will gain experience in identifying, ranking, analyzing, and integrating assurance, governance, and financial reporting issues. By the end of the course, you should be able to perform such tasks with a high level of professional competence. This course uses an active learning approach, which involves the analysis and discussion of a variety of cases, Uniform Evaluation (UFE) simulations, and related professional and research articles. To achieve the learning objectives, you need to thoroughly read each case, review any related conceptual and technical material, and thoughtfully assess each of the issues in the cases. Most important, you are expected to actively participate in the discussion by sharing your thoughts and opinions on the assigned cases and readings.

Relevance for Professional Designation Accreditation

This course is designed to develop your ability to apply your knowledge and understanding of assurance concepts in a competency-based learning framework. In terms of the CPA Competency Map, this course is focused on the audit and assurance technical competency area, but also integrates technical competencies from the strategy and governance, financial reporting, and finance areas. This course will also help you develop many of the enabling competency areas.

Course Materials

CPA Canada Handbook Assigned UFE simulations will be available on LEARN Other cases and readings will either be available on LEARN, library course

reserve, or links to the source will be provided Recommended – any Canadian introductory textbook for review purposes

24

ACC 650 Assurance & Governance

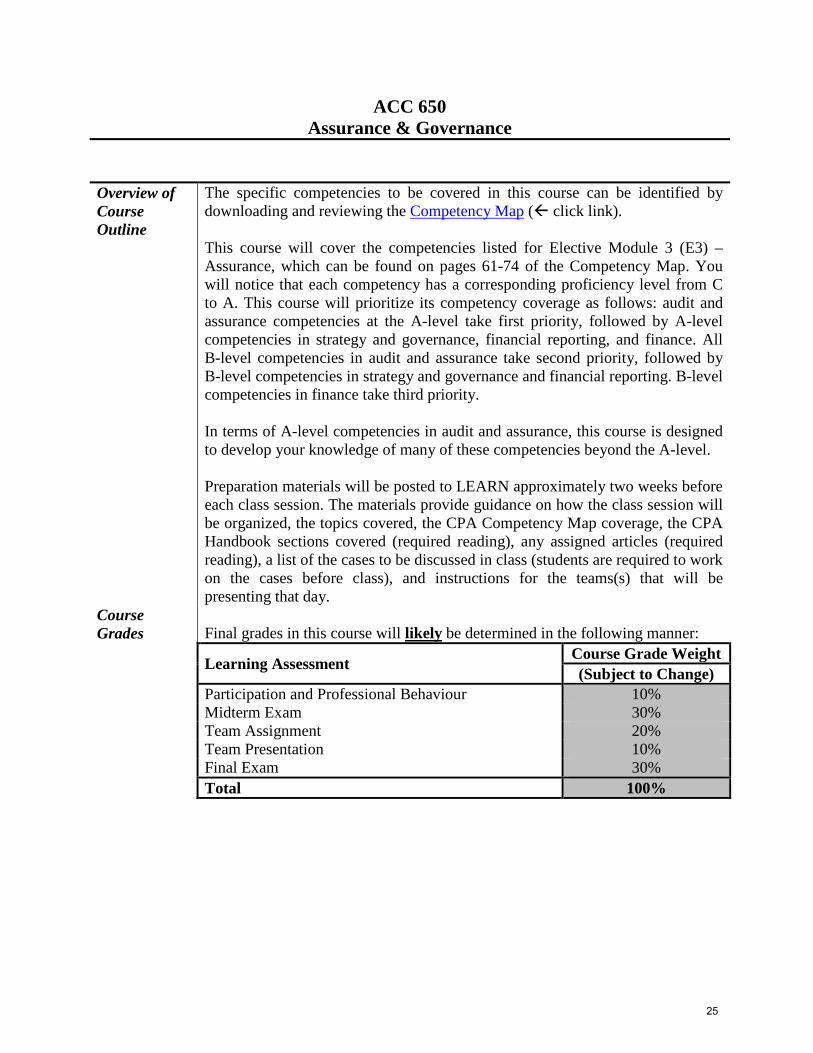

Overview of Course Outline

The specific competencies to be covered in this course can be identified by downloading and reviewing the Competency Map ( click link). This course will cover the competencies listed for Elective Module 3 (E3) – Assurance, which can be found on pages 61-74 of the Competency Map. You will notice that each competency has a corresponding proficiency level from C to A. This course will prioritize its competency coverage as follows: audit and assurance competencies at the A-level take first priority, followed by A-level competencies in strategy and governance, financial reporting, and finance. All B-level competencies in audit and assurance take second priority, followed by B-level competencies in strategy and governance and financial reporting. B-level competencies in finance take third priority. In terms of A-level competencies in audit and assurance, this course is designed to develop your knowledge of many of these competencies beyond the A-level. Preparation materials will be posted to LEARN approximately two weeks before each class session. The materials provide guidance on how the class session will be organized, the topics covered, the CPA Competency Map coverage, the CPA Handbook sections covered (required reading), any assigned articles (required reading), a list of the cases to be discussed in class (students are required to work on the cases before class), and instructions for the teams(s) that will be presenting that day.

Course Grades

Final grades in this course will likely be determined in the following manner:

Learning Assessment Course Grade Weight (Subject to Change)

Participation and Professional Behaviour 10% Midterm Exam 30% Team Assignment 20% Team Presentation 10% Final Exam 30% Total 100%

25

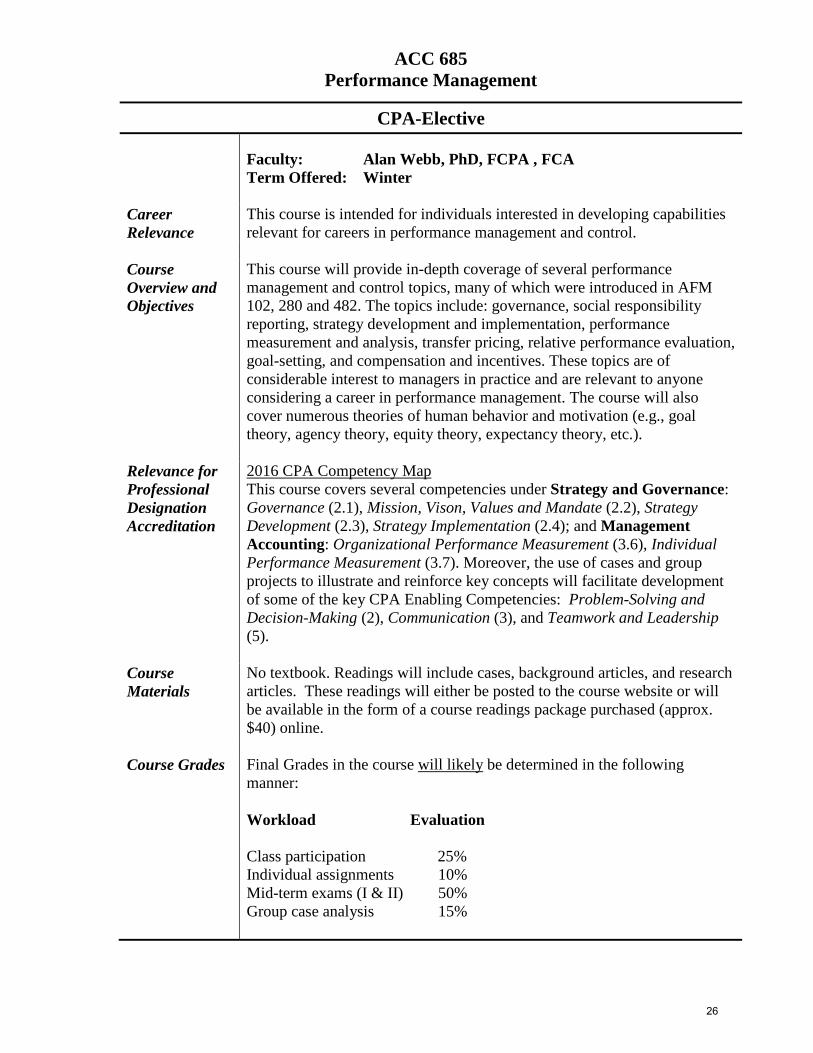

ACC 685 Performance Management

CPA-Elective

Faculty: Alan Webb, PhD, FCPA , FCA Term Offered: Winter

Career Relevance

This course is intended for individuals interested in developing capabilities relevant for careers in performance management and control.

Course Overview and Objectives

This course will provide in-depth coverage of several performance management and control topics, many of which were introduced in AFM 102, 280 and 482. The topics include: governance, social responsibility reporting, strategy development and implementation, performance measurement and analysis, transfer pricing, relative performance evaluation, goal-setting, and compensation and incentives. These topics are of considerable interest to managers in practice and are relevant to anyone considering a career in performance management. The course will also cover numerous theories of human behavior and motivation (e.g., goal theory, agency theory, equity theory, expectancy theory, etc.).

Relevance for Professional Designation Accreditation

2016 CPA Competency Map This course covers several competencies under Strategy and Governance: Governance (2.1), Mission, Vison, Values and Mandate (2.2), Strategy Development (2.3), Strategy Implementation (2.4); and Management Accounting: Organizational Performance Measurement (3.6), Individual Performance Measurement (3.7). Moreover, the use of cases and group projects to illustrate and reinforce key concepts will facilitate development of some of the key CPA Enabling Competencies: Problem-Solving and Decision-Making (2), Communication (3), and Teamwork and Leadership (5).

Course Materials

No textbook. Readings will include cases, background articles, and research articles. These readings will either be posted to the course website or will be available in the form of a course readings package purchased (approx. $40) online.

Course Grades Final Grades in the course will likely be determined in the following

manner: Workload Evaluation Class participation 25% Individual assignments 10% Mid-term exams (I & II) 50% Group case analysis 15%

26

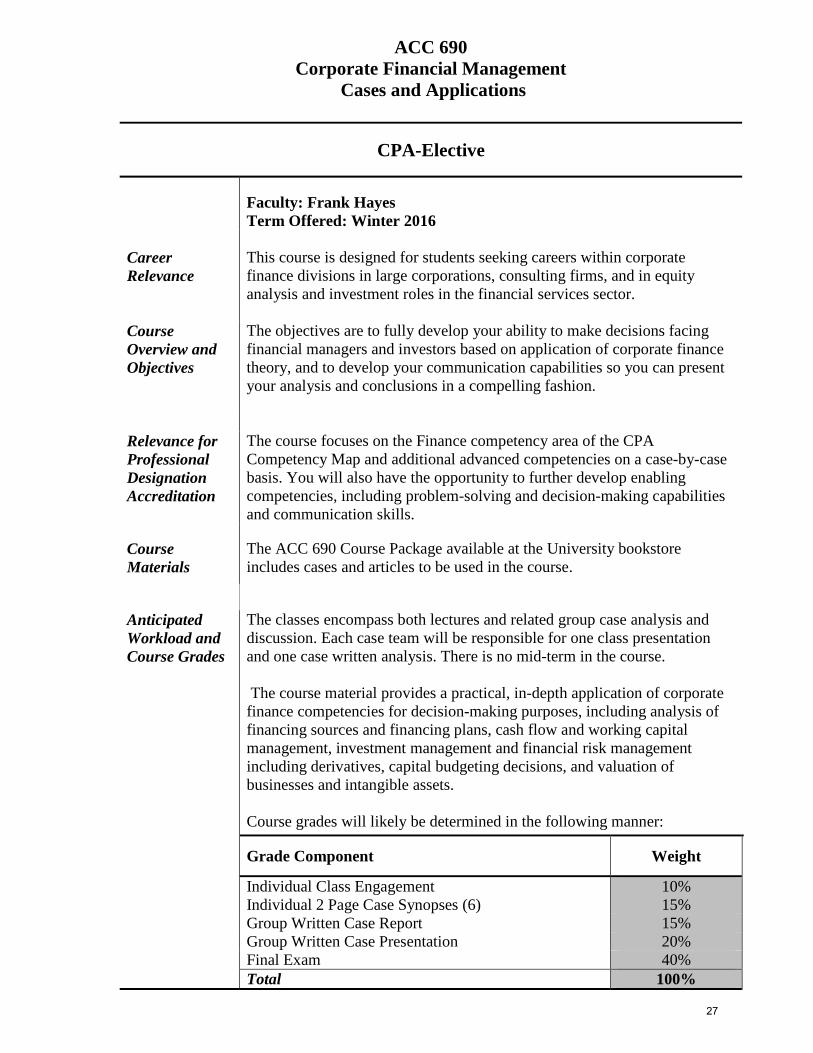

ACC 690 Corporate Financial Management

Cases and Applications

CPA-Elective

Faculty: Frank Hayes Term Offered: Winter 2016

Career Relevance

This course is designed for students seeking careers within corporate finance divisions in large corporations, consulting firms, and in equity analysis and investment roles in the financial services sector.

Course Overview and Objectives

The objectives are to fully develop your ability to make decisions facing financial managers and investors based on application of corporate finance theory, and to develop your communication capabilities so you can present your analysis and conclusions in a compelling fashion.

Relevance for Professional Designation Accreditation

The course focuses on the Finance competency area of the CPA Competency Map and additional advanced competencies on a case-by-case basis. You will also have the opportunity to further develop enabling competencies, including problem-solving and decision-making capabilities and communication skills.

Course Materials

The ACC 690 Course Package available at the University bookstore includes cases and articles to be used in the course.

Anticipated Workload and Course Grades

The classes encompass both lectures and related group case analysis and discussion. Each case team will be responsible for one class presentation and one case written analysis. There is no mid-term in the course. The course material provides a practical, in-depth application of corporate finance competencies for decision-making purposes, including analysis of financing sources and financing plans, cash flow and working capital management, investment management and financial risk management including derivatives, capital budgeting decisions, and valuation of businesses and intangible assets. Course grades will likely be determined in the following manner:

Grade Component Weight

Individual Class Engagement Individual 2 Page Case Synopses (6)

10% 15%

Group Written Case Report 15% Group Written Case Presentation 20% Final Exam 40% Total 100%

27

MAcc-Elective Courses

28

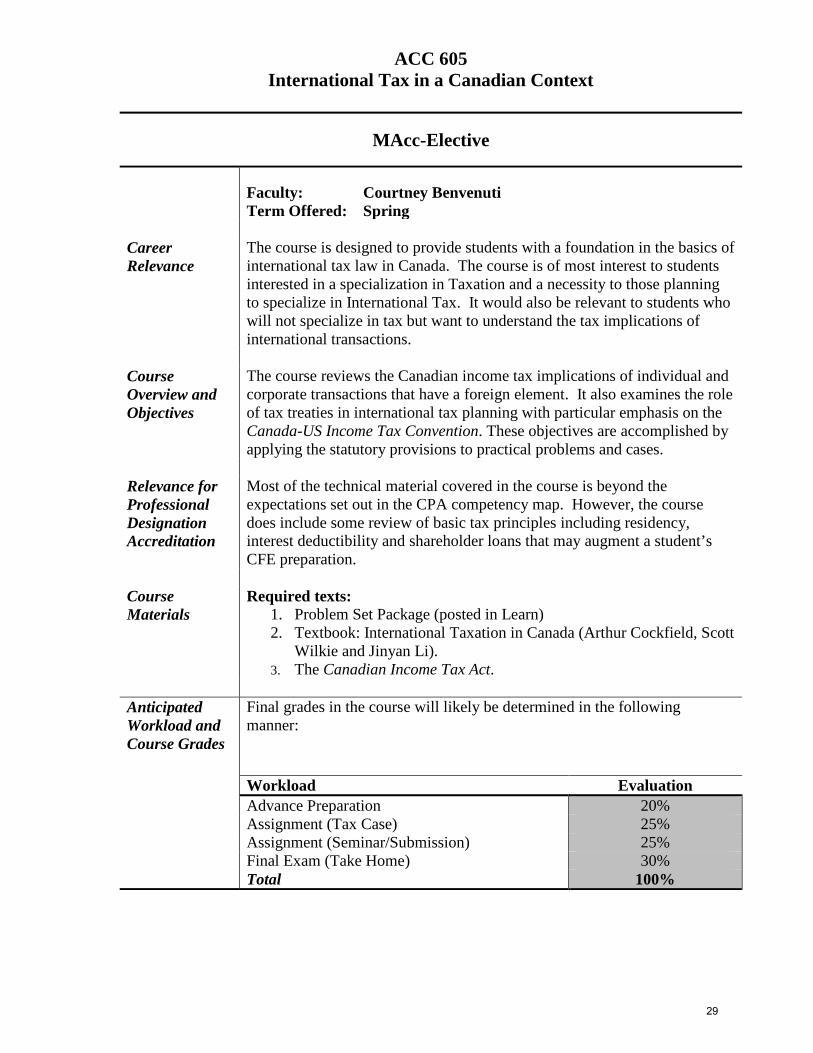

ACC 605 International Tax in a Canadian Context

MAcc-Elective

Faculty: Courtney Benvenuti Term Offered: Spring

Career Relevance

The course is designed to provide students with a foundation in the basics of international tax law in Canada. The course is of most interest to students interested in a specialization in Taxation and a necessity to those planning to specialize in International Tax. It would also be relevant to students who will not specialize in tax but want to understand the tax implications of international transactions.

Course Overview and Objectives

The course reviews the Canadian income tax implications of individual and corporate transactions that have a foreign element. It also examines the role of tax treaties in international tax planning with particular emphasis on the Canada-US Income Tax Convention. These objectives are accomplished by applying the statutory provisions to practical problems and cases.

Relevance for Professional Designation Accreditation

Most of the technical material covered in the course is beyond the expectations set out in the CPA competency map. However, the course does include some review of basic tax principles including residency, interest deductibility and shareholder loans that may augment a student’s CFE preparation.

Course Materials

Required texts: 1. Problem Set Package (posted in Learn) 2. Textbook: International Taxation in Canada (Arthur Cockfield, Scott

Wilkie and Jinyan Li). 3. The Canadian Income Tax Act.

Anticipated Workload and Course Grades

Final grades in the course will likely be determined in the following manner:

Workload Evaluation Advance Preparation 20% Assignment (Tax Case) 25% Assignment (Seminar/Submission) 25% Final Exam (Take Home) 30% Total 100%

29

ACC 606 Business Valuations

MAcc-Elective

Faculty: Professor Dave Vert CPA, CA, CBV Term Offered: Spring

Career Relevance

Some say a company is worth exactly what another person is willing to pay. Or is it? How about the value of the assets? Or profit? Is it the potential of the business? Or goodwill? Is it all or some of it? How do you arrive at that magic number? More importantly, who can provide that assessment? An accountant? A lawyer? A relative who just sold their business? The Chartered Business Valuator (CBV) is the pre-eminent designation for Canadian business valuation experts. More information on the CBV designation is available from the Canadian Institute of Chartered Business Valuators’ (CICBV) website at www.cicbv.ca.

Course Overview and Objectives

This course is intended to provide students with the educational equivalent of the CICBV’s Programme of Studies’ Introductory (Level I) and Intermediate (Level II) Business Valuation courses. Topics to be covered include role of the valuator, principles of valuation, valuation approaches and techniques, risk and growth considerations, determining rates of return, goodwill, minority and controlling interests, CICBV professional standards, etc.

Relevance for Professional Designation Accreditation

CBV Students completing this course are eligible for advanced standing in the CBV Programme of Studies for a period of 2 years following MAcc graduation. This advanced standing includes an exemption from completing the CICBV's Introductory Business Valuation (Level I) course and only having to challenge the CICBV's final exam for Intermediate Business Valuation (Level II) in order to proceed through the remainder of the CICBV's Programme. CICBV course examinations take place in March and September of each year. CPA The material covered in this course goes well beyond the expectations of CPA candidates and is not geared specifically towards preparation for the CPA's Common Final Exam. With regard to the CPA Competency Map, the concepts covered in this course have some relevance to the CPA Technical Competency areas. Specifically, there is a high degree of relevance under the Finance competency area with some modest integration with both the Financial Reporting and Taxation competency areas. Also, students will have the opportunity to further develop some of the skills set out in the CPA Enabling Competencies in the latter half of the course where both the in-class case problems and the final examination will have an increased emphasis on how valuation practitioners apply and communicate their knowledge in circumstances found in practice.

30

ACC 606 Business Valuations

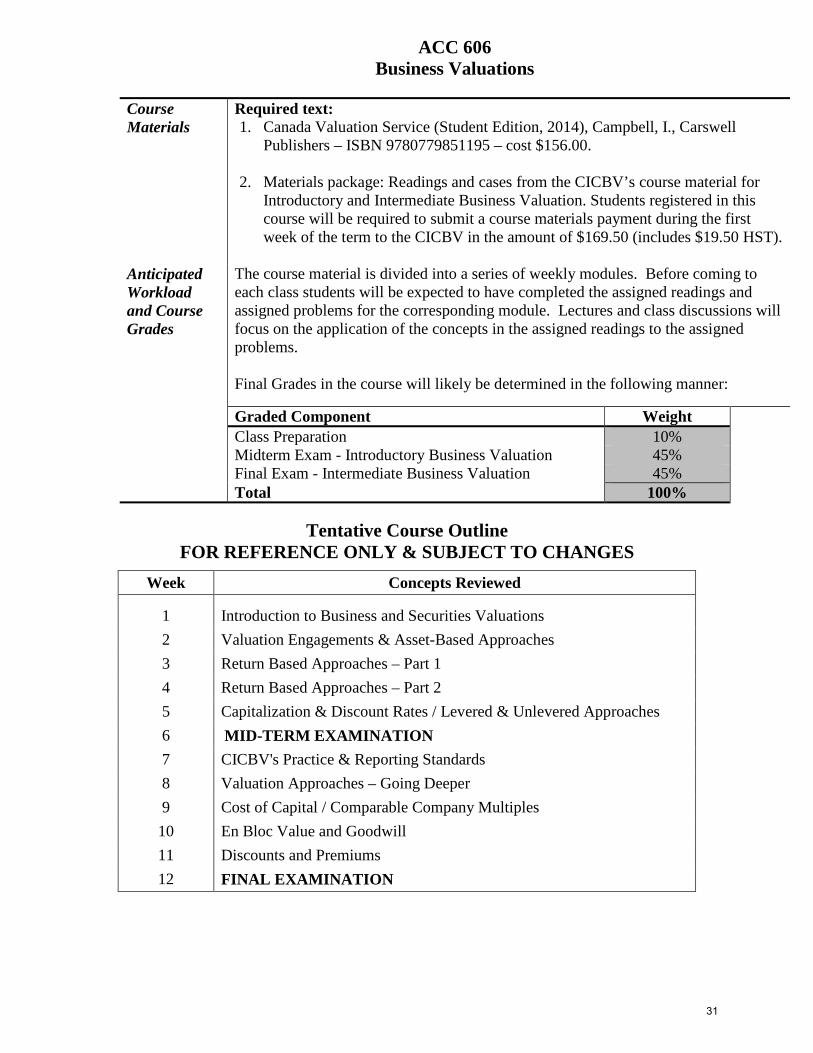

Course Materials

Required text: 1. Canada Valuation Service (Student Edition, 2014), Campbell, I., Carswell

Publishers – ISBN 9780779851195 – cost $156.00.

2. Materials package: Readings and cases from the CICBV’s course material for Introductory and Intermediate Business Valuation. Students registered in this course will be required to submit a course materials payment during the first week of the term to the CICBV in the amount of $169.50 (includes $19.50 HST).

Anticipated Workload and Course Grades

The course material is divided into a series of weekly modules. Before coming to each class students will be expected to have completed the assigned readings and assigned problems for the corresponding module. Lectures and class discussions will focus on the application of the concepts in the assigned readings to the assigned problems. Final Grades in the course will likely be determined in the following manner:

Graded Component Weight Class Preparation 10% Midterm Exam - Introductory Business Valuation 45% Final Exam - Intermediate Business Valuation 45% Total 100%

Tentative Course Outline FOR REFERENCE ONLY & SUBJECT TO CHANGES

Week Concepts Reviewed 1 Introduction to Business and Securities Valuations 2 Valuation Engagements & Asset-Based Approaches 3 Return Based Approaches – Part 1 4 Return Based Approaches – Part 2 5 Capitalization & Discount Rates / Levered & Unlevered Approaches 6 MID-TERM EXAMINATION 7 CICBV's Practice & Reporting Standards

8 Valuation Approaches – Going Deeper 9 Cost of Capital / Comparable Company Multiples 10 En Bloc Value and Goodwill 11 Discounts and Premiums 12 FINAL EXAMINATION

31

ACC 609 Financial Statement Analysis

MAcc-Elective

Faculty: Shari Mann, CPA, CA, Lecturer Term: Spring

Career Relevance Financial statement analysis is an essential skill for firm valuation in a

variety of occupations including investment management, corporate finance, commercial lending, and extension of credit. Since accounting information is used for valuation, both inside and outside the firm, valuation analysis should guide the accountant in providing accounting service. The accounting professional needs to understand how financial statements are used by investors and other stakeholders.

Course Overview and Objectives

This course is intended to improve your ability to analyze financial reports, with an emphasis on equity valuation. We will study accounting principles and their implications on the information presented in financial statements, and learn how to use that information in valuation models.

Relevance for Professional Accreditation

CPA/CFA The capabilities developed through this course are included in the: - CPA Candidates Competency Map in the Organizational

Effectiveness, Control and Risk Management, Finance, and Performance Measurement competency areas.

- CFA Institute’s Candidate Body of Knowledge within the knowledge required for Financial Reporting and Analysis and Equity Investments.

- While the course contents are not designed for the CFE or CFA exams, they are relevant as a body of knowledge. Students also have the opportunity to improve skills for problem-solving, decision-making, and communication.

Course Materials Text: To be announced Course package: Additional reading materials.

ACC 609 Financial Statement Analysis

32

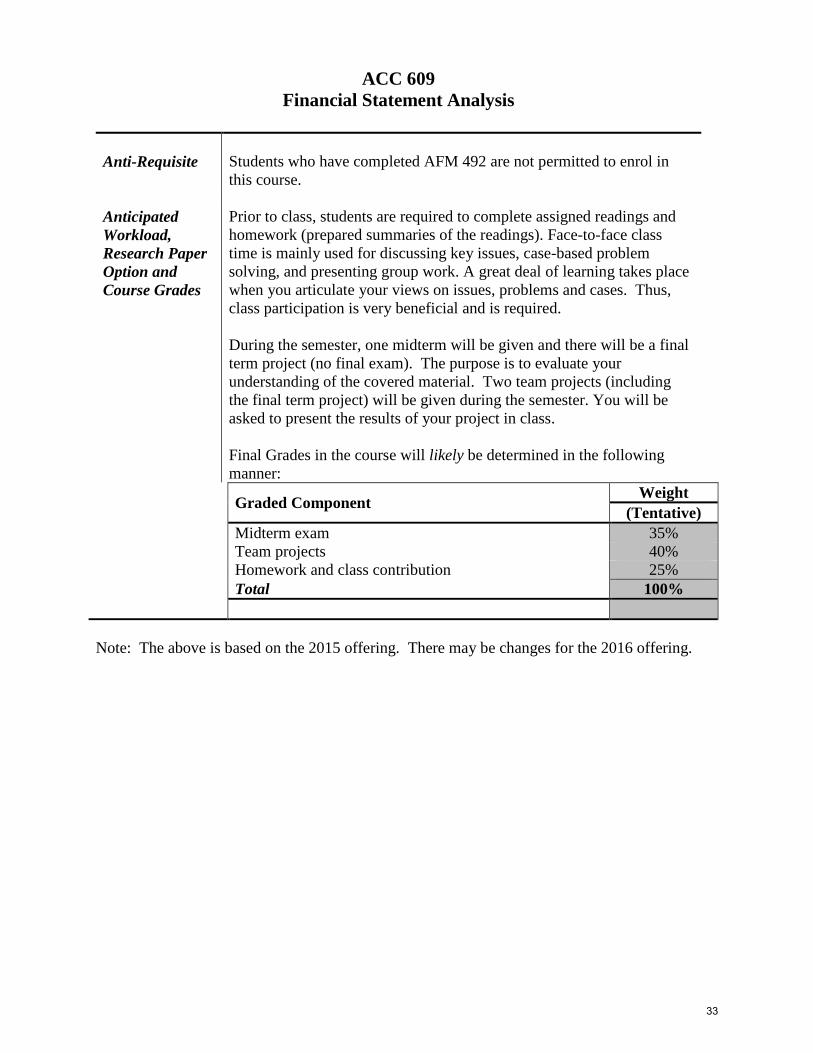

Graded Component Weight (Tentative)

Midterm exam 35% Team projects 40% Homework and class contribution 25% Total 100%

Note: The above is based on the 2015 offering. There may be changes for the 2016 offering.

ACC 609 Financial Statement Analysis

Anti-Requisite Students who have completed AFM 492 are not permitted to enrol in

this course. Anticipated Workload, Research Paper Option and Course Grades

Prior to class, students are required to complete assigned readings and homework (prepared summaries of the readings). Face-to-face class time is mainly used for discussing key issues, case-based problem solving, and presenting group work. A great deal of learning takes place when you articulate your views on issues, problems and cases. Thus, class participation is very beneficial and is required. During the semester, one midterm will be given and there will be a final term project (no final exam). The purpose is to evaluate your understanding of the covered material. Two team projects (including the final term project) will be given during the semester. You will be asked to present the results of your project in class. Final Grades in the course will likely be determined in the following manner:

33

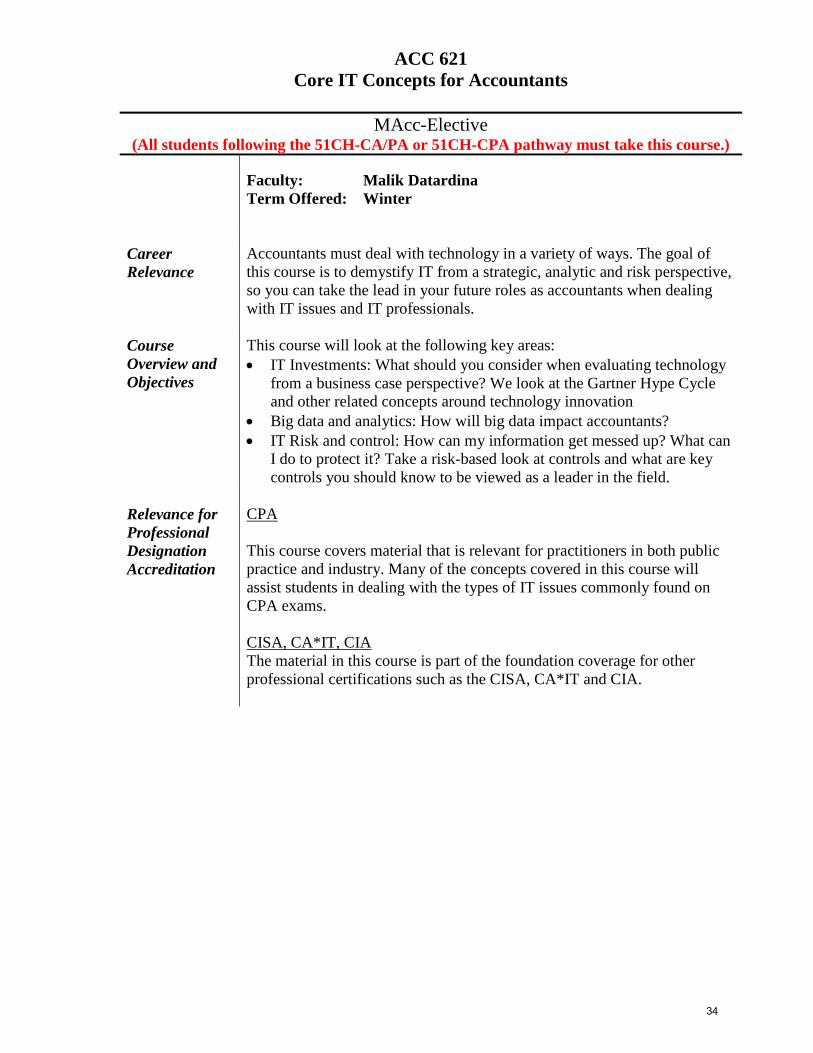

ACC 621 Core IT Concepts for Accountants

MAcc-Elective

(All students following the 51CH-CA/PA or 51CH-CPA pathway must take this course.)

Faculty: Malik Datardina Term Offered: Winter

Career Relevance

Accountants must deal with technology in a variety of ways. The goal of this course is to demystify IT from a strategic, analytic and risk perspective, so you can take the lead in your future roles as accountants when dealing with IT issues and IT professionals.

Course Overview and Objectives

This course will look at the following key areas: • IT Investments: What should you consider when evaluating technology

from a business case perspective? We look at the Gartner Hype Cycle and other related concepts around technology innovation

• Big data and analytics: How will big data impact accountants? • IT Risk and control: How can my information get messed up? What can

I do to protect it? Take a risk-based look at controls and what are key controls you should know to be viewed as a leader in the field.

Relevance for Professional Designation Accreditation

CPA This course covers material that is relevant for practitioners in both public practice and industry. Many of the concepts covered in this course will assist students in dealing with the types of IT issues commonly found on CPA exams. CISA, CA*IT, CIA The material in this course is part of the foundation coverage for other professional certifications such as the CISA, CA*IT and CIA.

34

ACC 621 Core IT Concepts for Accountants

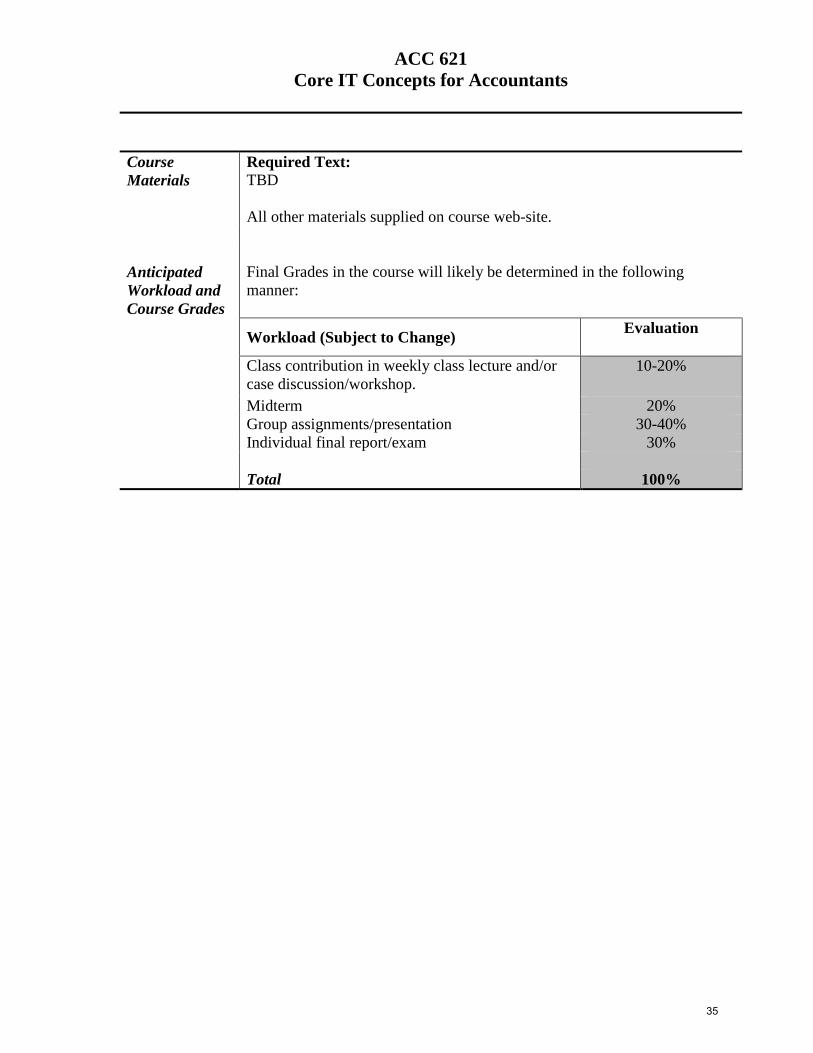

Course Materials

Required Text: TBD All other materials supplied on course web-site.

Anticipated Workload and Course Grades

Final Grades in the course will likely be determined in the following manner:

Workload (Subject to Change) Evaluation

Class contribution in weekly class lecture and/or case discussion/workshop.

10-20%

Midterm 20% Group assignments/presentation 30-40% Individual final report/exam 30% Total 100%

35

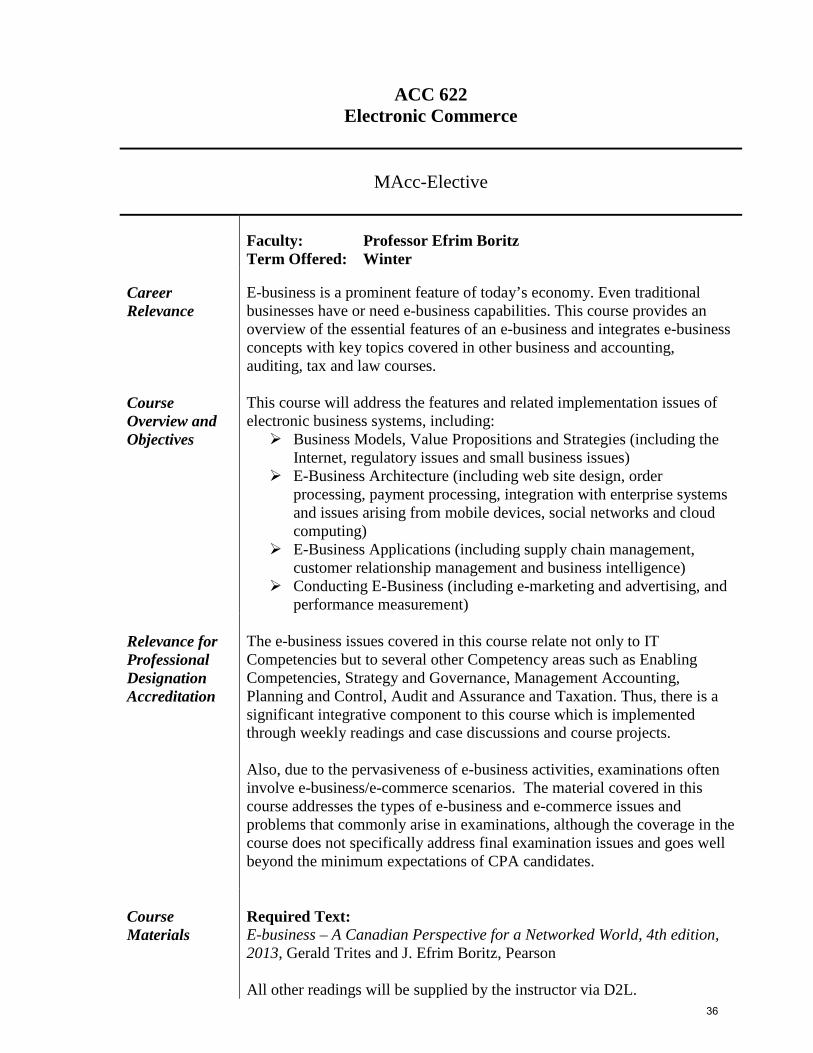

ACC 622 Electronic Commerce

MAcc-Elective

Faculty: Professor Efrim Boritz Term Offered: Winter

Career Relevance

E-business is a prominent feature of today’s economy. Even traditional businesses have or need e-business capabilities. This course provides an overview of the essential features of an e-business and integrates e-business concepts with key topics covered in other business and accounting, auditing, tax and law courses.

Course Overview and Objectives

This course will address the features and related implementation issues of electronic business systems, including: Business Models, Value Propositions and Strategies (including the

Internet, regulatory issues and small business issues) E-Business Architecture (including web site design, order

processing, payment processing, integration with enterprise systems and issues arising from mobile devices, social networks and cloud computing)

E-Business Applications (including supply chain management, customer relationship management and business intelligence)

Conducting E-Business (including e-marketing and advertising, and performance measurement)

Relevance for Professional Designation Accreditation

The e-business issues covered in this course relate not only to IT Competencies but to several other Competency areas such as Enabling Competencies, Strategy and Governance, Management Accounting, Planning and Control, Audit and Assurance and Taxation. Thus, there is a significant integrative component to this course which is implemented through weekly readings and case discussions and course projects. Also, due to the pervasiveness of e-business activities, examinations often involve e-business/e-commerce scenarios. The material covered in this course addresses the types of e-business and e-commerce issues and problems that commonly arise in examinations, although the coverage in the course does not specifically address final examination issues and goes well beyond the minimum expectations of CPA candidates.

Course Materials

Required Text: E-business – A Canadian Perspective for a Networked World, 4th edition, 2013, Gerald Trites and J. Efrim Boritz, Pearson All other readings will be supplied by the instructor via D2L.

36

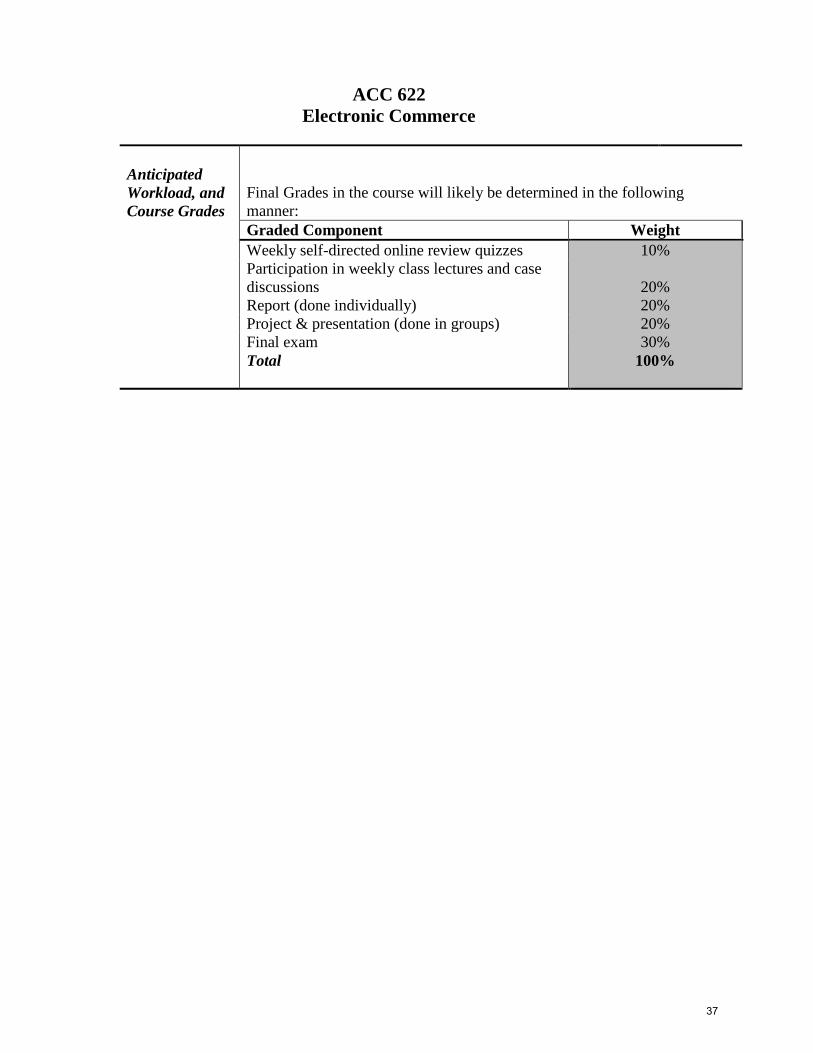

ACC 622 Electronic Commerce

Anticipated Workload, and Course Grades

Final Grades in the course will likely be determined in the following manner:

Graded Component Weight Weekly self-directed online review quizzes 10%

20% 20% 20% 30%

100%

Participation in weekly class lectures and case discussions Report (done individually) Project & presentation (done in groups) Final exam Total

37

ACC 623 Business Technology Law

IT Challenges & Opportunities

MAcc-Elective

Faculty: Professor Darren Charters Term Offered: Spring Delivery: Self learning with weekly topic intro/recap sessions

Career Relevance

This will be a particularly useful course for anyone contemplating a management career in a technology related sector of the economy or who, in a professional capacity, expects to work with such companies. However, the course still has relevance for those expecting to work in more traditional/conventional areas of the economy.

Course Overview and Objectives

Businesses operate in an environment proscribed as much by legal principles as by financial rules and performance expectations. The course will show students how legal issues of a technology oriented nature insinuate themselves into some key management activities, including those of both ‘old’ and ‘new’ economy businesses. It will provide an introduction to technology related legal issues that are relevant to business professionals and an examination of legal issues that create both obligations and opportunities for business. The course will address:

The legal environment for product development – focusing on core areas of intellectual property (IP) including patents, copyright, valuation of IP, and basic philosophical underpinnings of IP

Employee matters in technology focused business environment as well as traditional business confronting technology – including employees’ rights, privacy, appropriate company policies, etc.

Ecommerce legal issues – including privacy, consumer protection, electronic marketing, etc.

Providing products and services to third parties – including contract considerations in software licencing, IP licencing, etc.

CFE Relevance Course will provide useful background to information technology

competencies that are integrated throughout the competency map although not directly relevant to CFE.

Course Materials

Required Text: Courseware Package

38

ACC 623 Business Technology Law

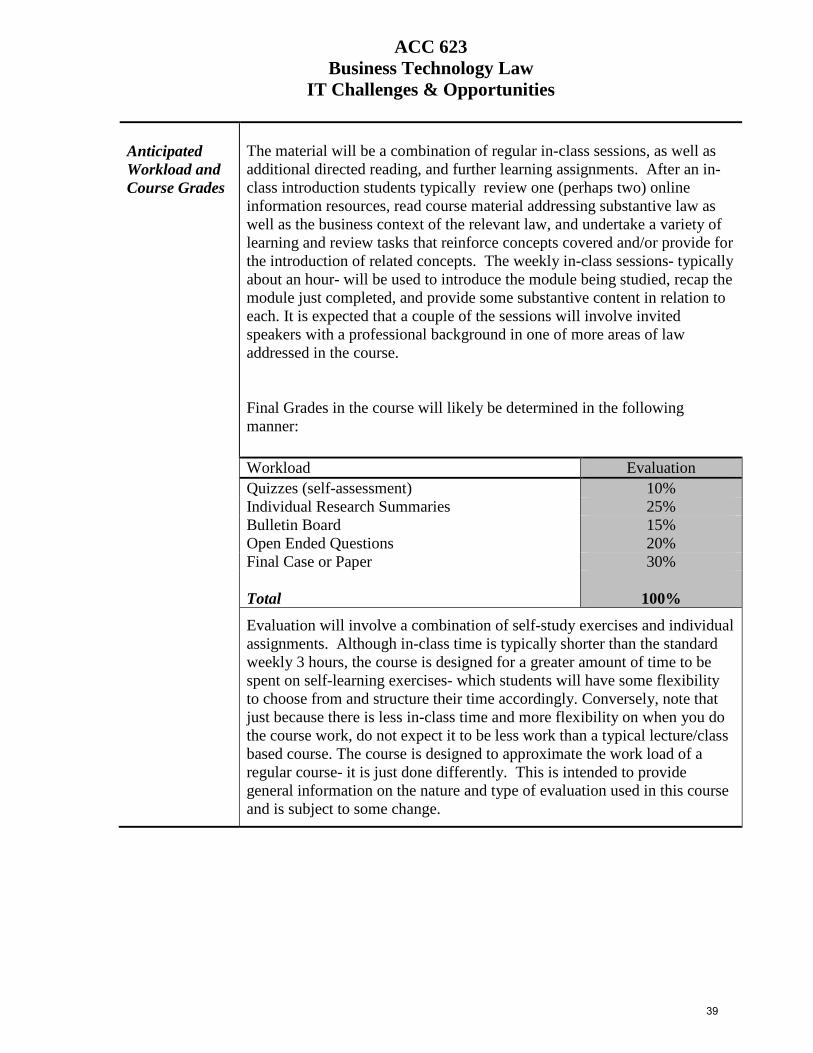

IT Challenges & Opportunities Anticipated Workload and Course Grades

The material will be a combination of regular in-class sessions, as well as additional directed reading, and further learning assignments. After an in-class introduction students typically review one (perhaps two) online information resources, read course material addressing substantive law as well as the business context of the relevant law, and undertake a variety of learning and review tasks that reinforce concepts covered and/or provide for the introduction of related concepts. The weekly in-class sessions- typically about an hour- will be used to introduce the module being studied, recap the module just completed, and provide some substantive content in relation to each. It is expected that a couple of the sessions will involve invited speakers with a professional background in one of more areas of law addressed in the course. Final Grades in the course will likely be determined in the following manner:

Workload Evaluation Quizzes (self-assessment) 10%

Individual Research Summaries 25% Bulletin Board 15% Open Ended Questions 20% Final Case or Paper 30% Total 100%

Evaluation will involve a combination of self-study exercises and individual assignments. Although in-class time is typically shorter than the standard weekly 3 hours, the course is designed for a greater amount of time to be spent on self-learning exercises- which students will have some flexibility to choose from and structure their time accordingly. Conversely, note that just because there is less in-class time and more flexibility on when you do the course work, do not expect it to be less work than a typical lecture/class based course. The course is designed to approximate the work load of a regular course- it is just done differently. This is intended to provide general information on the nature and type of evaluation used in this course and is subject to some change.

39

ACC 652

Forensic Accounting

MAcc-Elective

Faculty: Professor Linda Robinson Term Offered: Winter

Career Relevance

This course is particularly relevant if you want to sharpen your skills for detecting financial fraud or corruption for your clients or employer. If you are planning a career in audit, either internal or external, or plan to run your own business this course will heighten your understanding of fraud risk factors that will assist with your assessment of the organization’s susceptibility to fraud. This course is also relevant to you if you are considering a career as a Forensic Accountant. You will learn how to conduct an investigation, how to gather evidence, and how to pursue areas of recovery.

Course Overview and Objectives

The purpose of this course is to expand on your understanding of fraud and fraud related topics which you learned in previous auditing courses. This introductory course in forensic accounting will cover a variety of topics including:

Nature and types of fraud Who commits fraud and why Red flags you should be aware of Types of financial statement manipulation Fraud detection Illegal Acts Money Laundering Computer forensics Interviewing techniques

In addition to the topics above, the class will discuss financial fraud cases that occurred in Canada, the US, and around the world over the past ten years. Discussions will center on how the fraud happened and what could have been done to prevent, detect, and deter the fraud.

Relevance for Professional Designation Accreditation

Situations involving financial statement fraud concepts have arisen on past professional exams. However, the material covered in this course goes well beyond the expectations of CPA candidates and is not geared specifically towards the CPA examination. With regard to the CPA Competency Map, the concepts covered in this course have relevance to many of the Assurance competency area. Issues related to the Financial Reporting and Management Accounting competency areas will also be addressed as it relates to evaluation of information.

Course Materials

Required Text: Courseware package purchased at the University bookstore.

40

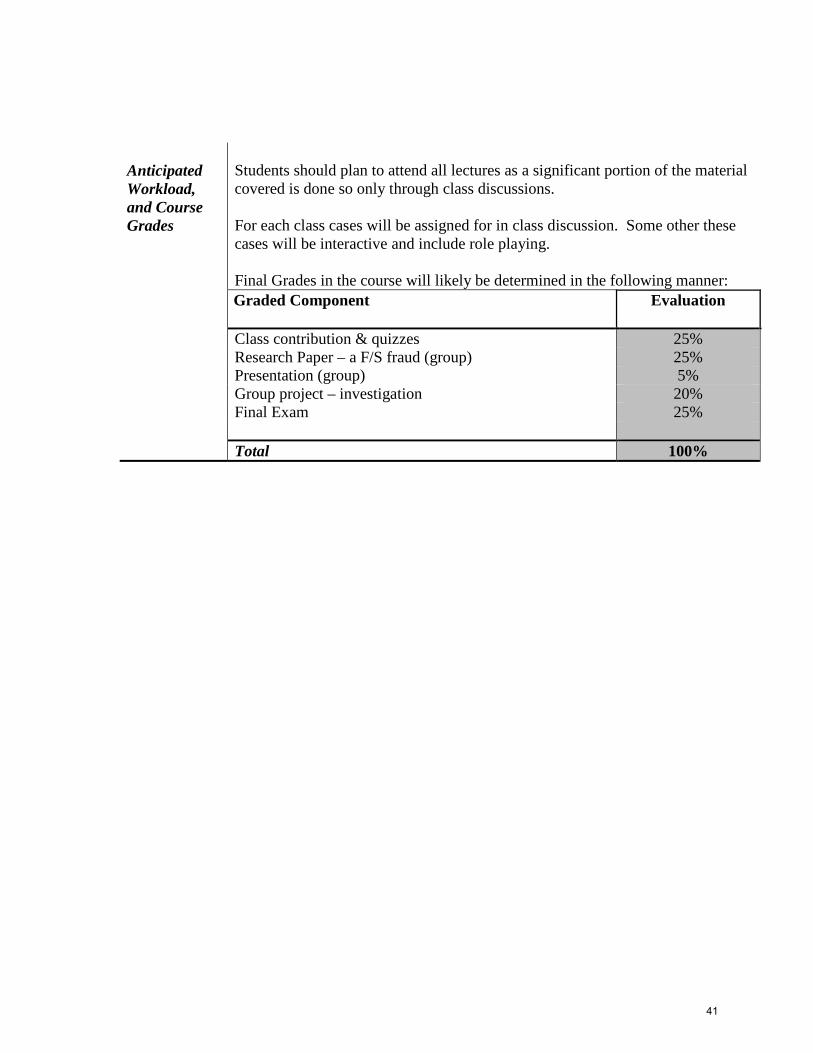

Anticipated Workload, and Course Grades

Students should plan to attend all lectures as a significant portion of the material covered is done so only through class discussions. For each class cases will be assigned for in class discussion. Some other these cases will be interactive and include role playing. Final Grades in the course will likely be determined in the following manner:

Graded Component

Evaluation

Class contribution & quizzes 25% Research Paper – a F/S fraud (group) 25% Presentation (group) 5% Group project – investigation 20% Final Exam 25% Total 100%

41

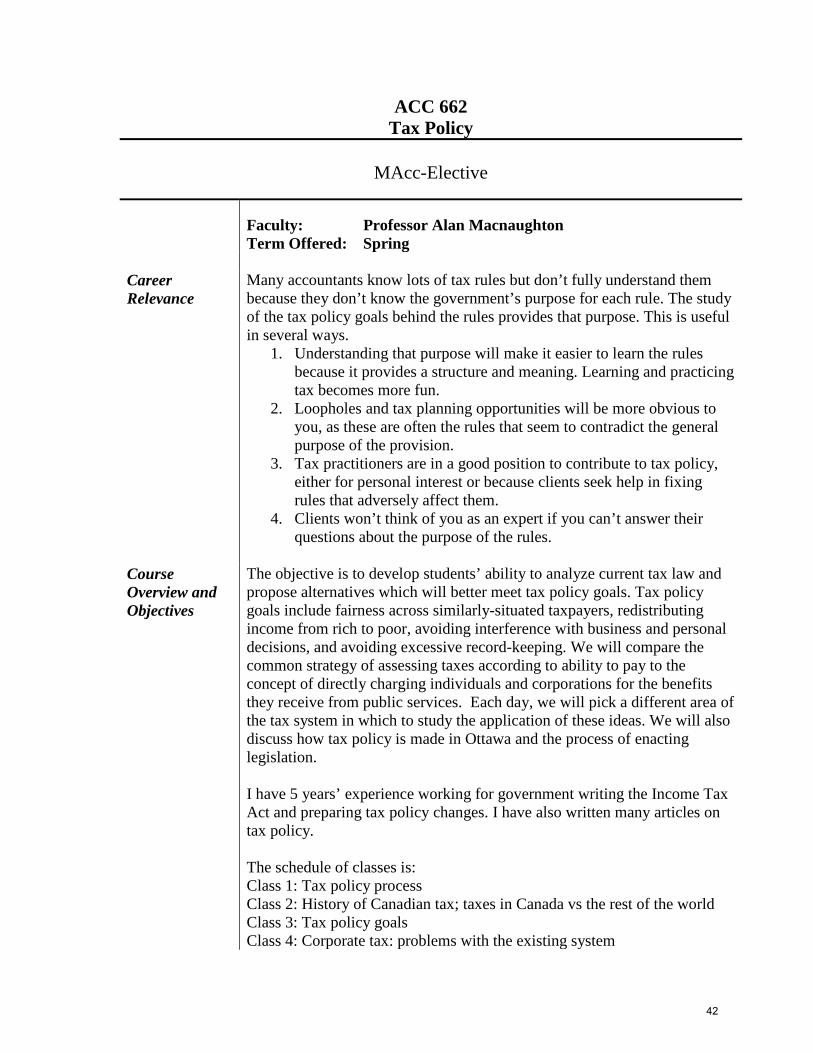

ACC 662 Tax Policy

MAcc-Elective

Faculty: Professor Alan Macnaughton Term Offered: Spring

Career Relevance

Many accountants know lots of tax rules but don’t fully understand them because they don’t know the government’s purpose for each rule. The study of the tax policy goals behind the rules provides that purpose. This is useful in several ways.

1. Understanding that purpose will make it easier to learn the rules because it provides a structure and meaning. Learning and practicing tax becomes more fun.

2. Loopholes and tax planning opportunities will be more obvious to you, as these are often the rules that seem to contradict the general purpose of the provision.

3. Tax practitioners are in a good position to contribute to tax policy, either for personal interest or because clients seek help in fixing rules that adversely affect them.

4. Clients won’t think of you as an expert if you can’t answer their questions about the purpose of the rules.

Course Overview and Objectives

The objective is to develop students’ ability to analyze current tax law and propose alternatives which will better meet tax policy goals. Tax policy goals include fairness across similarly-situated taxpayers, redistributing income from rich to poor, avoiding interference with business and personal decisions, and avoiding excessive record-keeping. We will compare the common strategy of assessing taxes according to ability to pay to the concept of directly charging individuals and corporations for the benefits they receive from public services. Each day, we will pick a different area of the tax system in which to study the application of these ideas. We will also discuss how tax policy is made in Ottawa and the process of enacting legislation. I have 5 years’ experience working for government writing the Income Tax Act and preparing tax policy changes. I have also written many articles on tax policy. The schedule of classes is: Class 1: Tax policy process Class 2: History of Canadian tax; taxes in Canada vs the rest of the world Class 3: Tax policy goals Class 4: Corporate tax: problems with the existing system

42

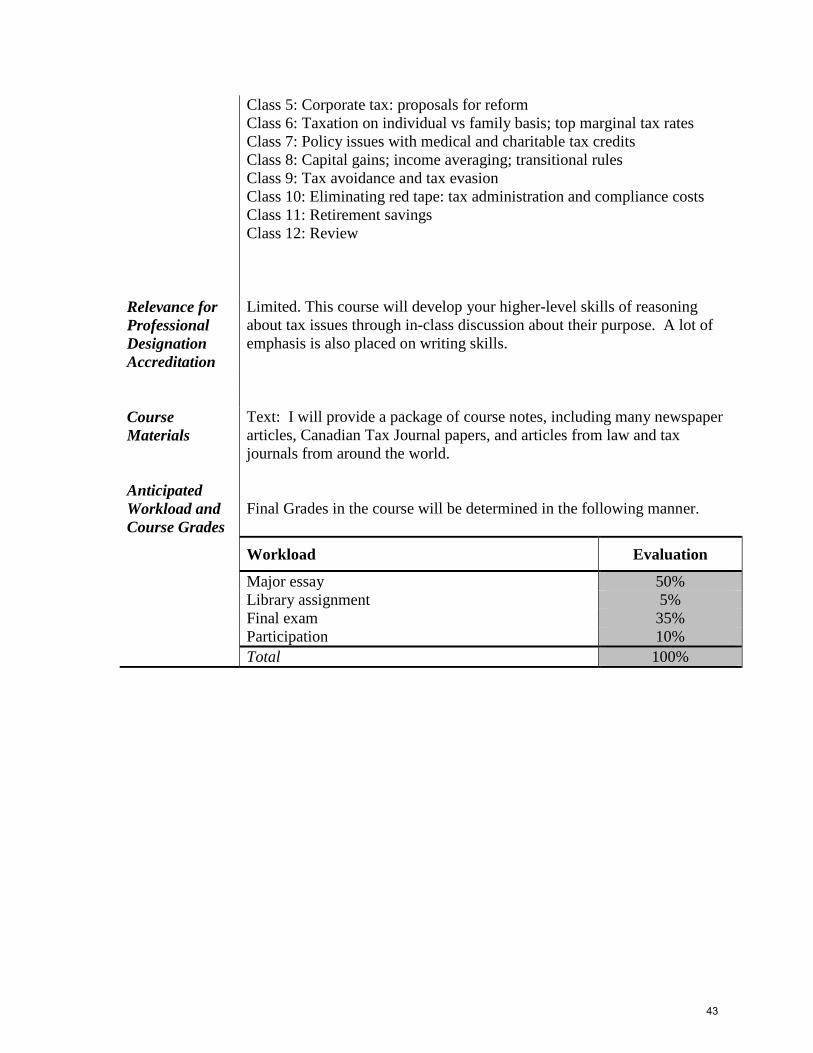

Class 5: Corporate tax: proposals for reform Class 6: Taxation on individual vs family basis; top marginal tax rates Class 7: Policy issues with medical and charitable tax credits Class 8: Capital gains; income averaging; transitional rules Class 9: Tax avoidance and tax evasion Class 10: Eliminating red tape: tax administration and compliance costs Class 11: Retirement savings Class 12: Review

Relevance for Professional Designation Accreditation

Limited. This course will develop your higher-level skills of reasoning about tax issues through in-class discussion about their purpose. A lot of emphasis is also placed on writing skills.

Course Materials Anticipated Workload and Course Grades

Text: I will provide a package of course notes, including many newspaper articles, Canadian Tax Journal papers, and articles from law and tax journals from around the world. Final Grades in the course will be determined in the following manner.

Workload Evaluation

Major essay 50% Library assignment 5% Final exam 35% Participation 10% Total 100%

43

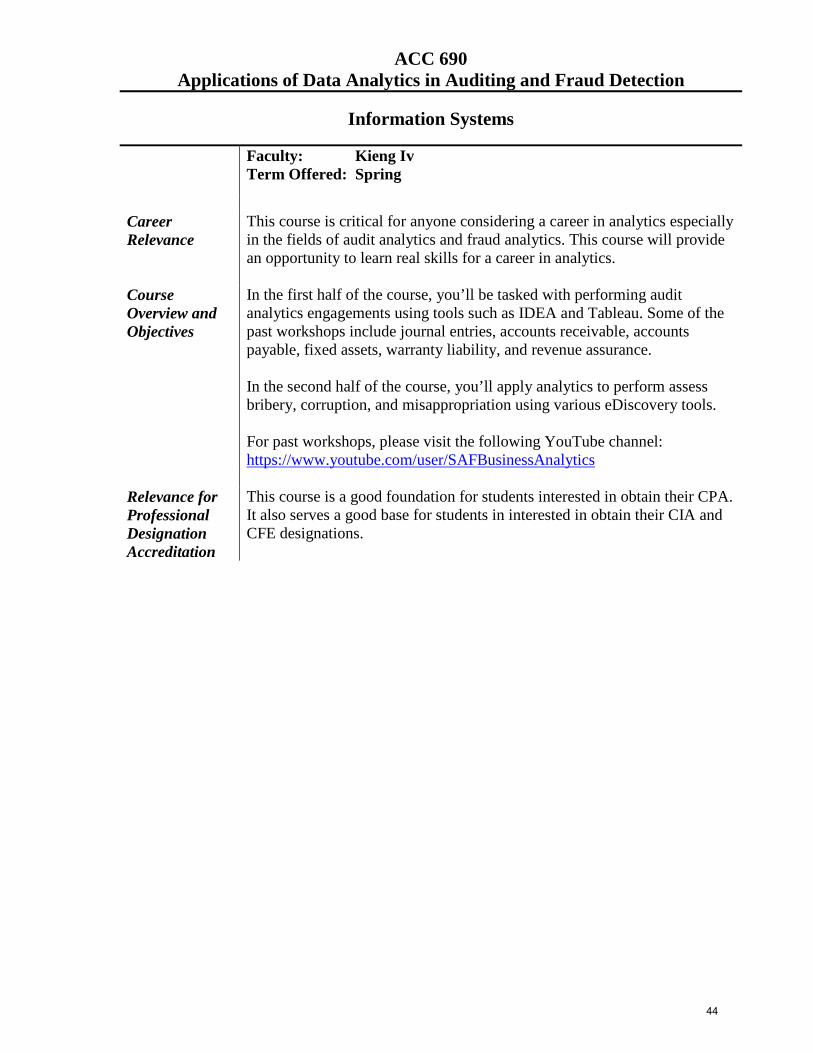

ACC 690 Applications of Data Analytics in Auditing and Fraud Detection

Information Systems

Faculty: Kieng Iv

Term Offered: Spring

Career Relevance

This course is critical for anyone considering a career in analytics especially in the fields of audit analytics and fraud analytics. This course will provide an opportunity to learn real skills for a career in analytics.

Course Overview and Objectives

In the first half of the course, you’ll be tasked with performing audit analytics engagements using tools such as IDEA and Tableau. Some of the past workshops include journal entries, accounts receivable, accounts payable, fixed assets, warranty liability, and revenue assurance. In the second half of the course, you’ll apply analytics to perform assess bribery, corruption, and misappropriation using various eDiscovery tools. For past workshops, please visit the following YouTube channel: https://www.youtube.com/user/SAFBusinessAnalytics

Relevance for Professional Designation Accreditation

This course is a good foundation for students interested in obtain their CPA. It also serves a good base for students in interested in obtain their CIA and CFE designations.

44

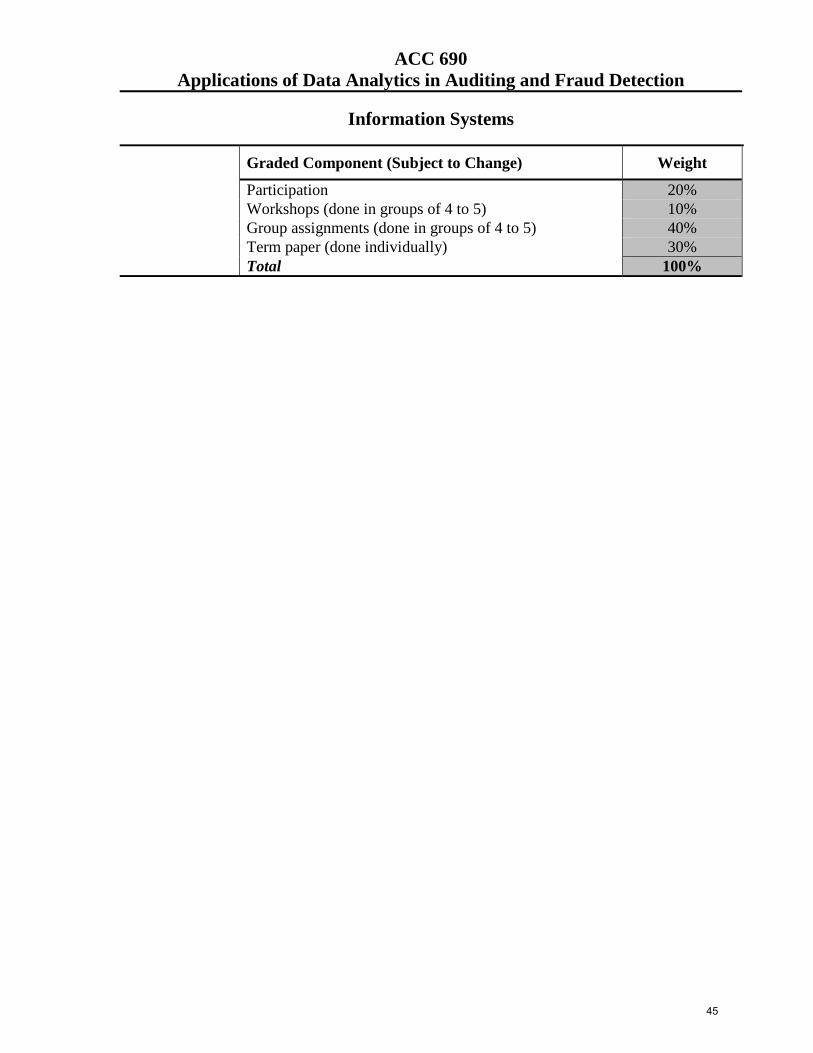

ACC 690 Applications of Data Analytics in Auditing and Fraud Detection

Information Systems

Graded Component (Subject to Change) Weight

Participation 20% Workshops (done in groups of 4 to 5) 10% Group assignments (done in groups of 4 to 5) 40% Term paper (done individually) 30% Total 100%

45

ACC 690 Professional Judgment

Other

Faculty: Professor Efrim Boritz Term Offered: Spring

Career Relevance

Sound professional judgment is a hallmark of a competent professional. The exercise of professional judgment has been studied in fields as diverse as medicine, law, psychology and accounting. Knowledge about the strengths and weaknesses of professional judgment can help professional accountants and financial managers understand and deal effectively with complex issues that require the application of professional judgment. Thus, this course has high career relevance to all aspiring professional accountants and financial managers.

Course Overview and Objectives

This course will consider the exercise of professional judgment in accounting, auditing and finance. There is a significant integrative component to this course which is implemented through weekly readings and discussions. We will strive to understand the barriers to the effective exercise of professional judgment by reviewing the professional and academic research that has been conducted about professional judgment. We will read and discuss some of the classic studies in the field. We will also perform some simulations of methods used to learn about professional judgment. A number of cases involving accounting and auditing judgments will be used to illustrate key concepts Unlike some courses that focus solely on technical aspects of judgment such as cognition and knowledge, we will also address the values underpinning the concept of professionalism and the codes of conduct established to guide professional behaviour in the accounting, auditing and finance domains.

Relevance for Professional Designation Accreditation

The material covered in this course relates to the professional competencies expected of all professionals. Due to the pervasiveness of professional judgment, professional examinations often address this topic indirectly; but there is no doubt that understanding the key elements underpinning the sound exercise of professional judgement is essential to all professionals.

Course Materials

All course materials will be supplied on D2L.

Prerequisites None Anticipated Workload and Course Grades

Final Grades in the course will likely be determined in the following manner:

Workload Evaluation Participation in weekly lectures and case discussions 30% Assignment 1 (individual) 20% Assignment 2 (in teams of 2-3, includes presentation) 30% Final Exam 20% 100%

46

ACC 690 Topics: Tax for the CFO

MAcc-Elective

Faculty: David Lin Term Offered: Spring

Career Relevance

The course is designed to provide students with a foundation of tax concepts that will be relevant to industry practitioners. This course will be of most interest to students interested in developing an understanding of tax reporting and related accounting issues and will be relevant to both students who will and will not specialize in Taxation.

Course Overview and Objectives

This course investigates tax and related accounting issues found in the tax provision on the financial statements to deepen the understanding of the impact of tax on accounting. It will also address tax risk management and other tax topics relevant for the industry professional. These objectives are accomplished by applying concepts discussed in class, statutory tax provisions, and the CPA Canada Handbook (as applicable) to practical problems and cases. Other tax topics described above that are scheduled for coverage in this course include Canadian-Controlled Private Corporation status, tax considerations in executive compensation, tax considerations in acquisitions and divestitures, government incentives, tax audits, and Canada Revenue Agency’s new risk-based audit approach.

Relevance for Professional Designation Accreditation

Limited - most of the concepts covered in the course will be beyond the expectations of students as described in the CFE Candidates’ Competency Map. This course is intended to provide students with an understanding of tax topics relevant for industry practice.

Course Materials

1. Course readings posted in Learn 2. The Canadian Income Tax Act 3. The CPA Canada Handbook, Part I – International Financial

Reporting Standards and Part II – Accounting Standards for Private Enterprises (available through UW Library)

47

ACC 690 Topic: Tax for the CFO

Anticipated Workload and Course Grades

Final grades in the course will likely be determined in the following manner:

Workload Evaluation Class Preparation & Participation 10%

25% 25% 40%

100%

Assignment (Tax Reporting) Assignment (Other Tax Topics) Final Exam Total

48

Application & Course Selection

49

APPLICATION & COURSE SELECTION Application Process 1. Applying to the MAcc program is done online via the link available at the Graduate Studies

Office’s Apply Online website. Please note that access to this website will be temporarily unavailable due to maintenance from October 4 to October 8, 2015. Please note the following regarding the online application:

It must be submitted by Thursday, October 15, 2015 at 5pm. Students who took any of the 14 courses in the MAcc admission basket at an institution

other than UW must include with their application an official transcript from the other institution that provides details of the course(s) taken and the grade(s) received.

Payment of the $100.00 application fee can be made by credit card or a cheque payable to OUAC (mailing information is available on the online application form).

The "Professional Background" section should be left blank – do not complete using Co-op work experience.

Disregard the "Referee" section. Referees are not required and you should simply submit the application.

On-line submission is sufficient. It is not necessary to print and forward hard copies of the application to the School of Accounting and Finance.

2. Prior to entering the MAcc program, you must also signal your intention to graduate by completing

the form available via this link: Intention to Graduate – Undergraduate Studies. Please note the following: It must be submitted to the Registrar’s Office by December 1st, 2015. This form must be

completed during the 4B term to facilitate the review by the Undergraduate Officer of the status of your undergraduate degree requirements.

The "Expected Graduation Ceremony" is June 2016 – It is important that you specify June (not October), even if you do not attend the June ceremony. This is to ensure your official academic record reflects conferral of your undergraduate degree by next spring in order for you to be eligible for the 2016 CFE.

50

APPLICATION & COURSE SELECTION Course Selection Process Quest Enrolment You will use the standard Quest enrolment process to select your courses. Students who receive a conditional admission offer will be able to enroll in Winter courses beginning November 23rd. Enrolment in specific sections and MAcc-Elective courses is first-come-first-served, so eligible students should enroll on this date to enhance their chance of access. Students who do not receive a conditional offer will not be able to enroll in courses until their admissibility is determined at the end of the 4B term. Access to all CPA-Required and CPA-Elective courses is guaranteed, so students who do not receive a conditional offer need not worry about access to these courses. The Spring Quest enrolment date will be announced during the Spring Course Information session in January. When enrolling in courses, you may not:

• Enroll in six hours of back-to-back classes • Enroll in more than two classes held on the same day

Any students who violate these restrictions will have their schedule unilaterally adjusted by the Associate Director, who also reserves the right to re-assign students to another section of the same course to overcome any class size or other logistical issues. Course Selection Quizzes To help us identify potential scheduling issues in advance of Quest enrolment, we will ask you to complete a LEARN course-selection quiz for each term. The Winter quiz will be due on Friday, October 16th and the Spring quiz on Friday, January 29th. You will be able to change your course selections when enrolling on Quest, but we ask that you be virtually certain of your selections when submitting the quizzes so we can address potential issues well in advance of the enrolment dates. You should attend both course information sessions to ensure you have full information about all elective courses prior to completing the quizzes and enrolling in courses. MAcc Pathways and Course Selection The table on the next page presents the course selection requirements and options for students in each of the four MAcc pathways. See the MAcc Pathways Decision Tree to determine the pathway that applies to you. Note that the 51CH pathways apply only to students who receive a grade less than 60 in any of the CPA-required undergraduate courses completed after April 30, 2014, so at the time you select your Winter MAcc courses you will not know if you fall into this category because the 4B term will be in progress. Before selecting your Winter courses, use the decision tree to determine whether you want to follow the CA/PA or CPA pathway and then select your Winter courses according to the table below. If, at the conclusion of the 4B term, you gain admission to the MAcc program but receive a grade less than 60 in one or more of the CPA-required courses you took in 4B, then we will contact you to request that you switch your Winter course selections to satisfy one of the 51CH pathways in the table.

51

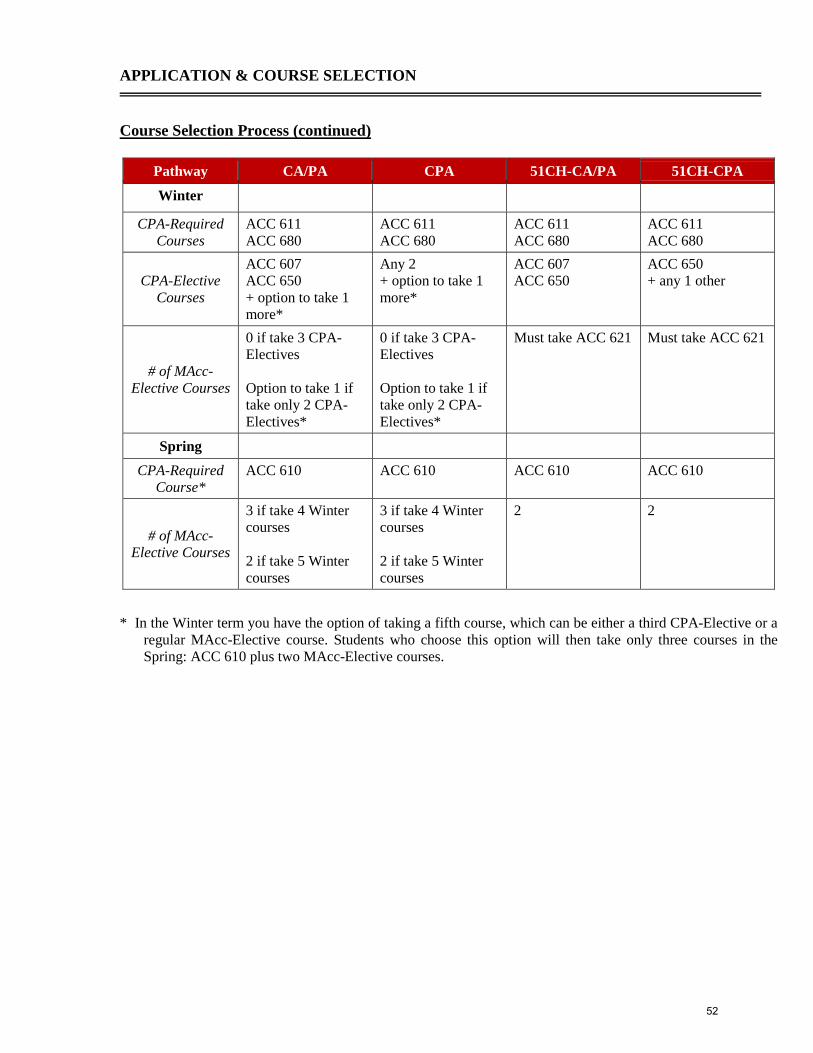

APPLICATION & COURSE SELECTION Course Selection Process (continued)

Pathway CA/PA CPA 51CH-CA/PA 51CH-CPA

Winter

CPA-Required Courses

ACC 611 ACC 680

ACC 611 ACC 680

ACC 611 ACC 680

ACC 611 ACC 680

CPA-Elective Courses

ACC 607 ACC 650 + option to take 1 more*

Any 2 + option to take 1 more*

ACC 607 ACC 650

ACC 650 + any 1 other

# of MAcc-Elective Courses

0 if take 3 CPA-Electives Option to take 1 if take only 2 CPA-Electives*

0 if take 3 CPA-Electives Option to take 1 if take only 2 CPA-Electives*

Must take ACC 621 Must take ACC 621

Spring

CPA-Required Course*

ACC 610 ACC 610 ACC 610 ACC 610

# of MAcc-Elective Courses

3 if take 4 Winter courses 2 if take 5 Winter courses

3 if take 4 Winter courses 2 if take 5 Winter courses

2 2

* In the Winter term you have the option of taking a fifth course, which can be either a third CPA-Elective or a regular MAcc-Elective course. Students who choose this option will then take only three courses in the Spring: ACC 610 plus two MAcc-Elective courses.

52

APPLICATION & COURSE SELECTION Course Selection Process (continued) Over-Subscribed MAcc-Elective Courses

Where the demand for an MAcc-Elective course exceeds the available space, students who do not gain access will have to monitor Quest to determine if any space opens up. Course Changes You will be able to make course changes on Quest up until the end of the first week of classes each term. Your ability to make course changes will depend on whether there is room in your requested course or section and whether there are any scheduling conflicts with your other courses. You should therefore carefully consider your initial course choices prior to enrolling in them so the need for changes later is minimized. Attendance at the course information sessions is an important step in this process. We reserve the right to switch students between sections in their chosen courses to eliminate any conflicts or other scheduling issues that may arise. Cancelled Courses MAcc courses with minimal enrolment may be cancelled.

53

Tuition & Scholarships

54

TUITION AND SCHOLARSHIPS