Embed Size (px)

Citation preview

Matching Accounting and Financial Reporting to the Asset Life Cycle

Bob Mahaney, CPPSMgr, Program Accounting & FinanceMD Anderson Cancer Center

Who is in the room?

• New member this year

• First NES

Who else is in the room?

Type of Business– University– Contract Property/Federal– State/Local Government– Private

Learning Objectives

• Learn basics of asset accounting.

• Learn the accounting transactions associated with each phase of the asset live cycle.

• Use financial reports to benefit asset management.

Asset Accounting

Welcome to the land of debits & credits.

•OMG!

•Relax.– It’s just a new language.– It’s how management sees you.

Asset Accounting Law

• If you like physics…• Newton’s Third Law.• For every action, there is an equal and

opposite reaction.

• You will like asset accounting.• Accounting magic.• For every debit, there is an equal and

offsetting credit.• Debits always equal credits.

Basic Asset Life Cycle

Taken together, the steps or phases

experienced by an item of property from

acquisition through disposition.

NPMA Fundamentals of Personal Property Management, Glossary - Chapter 12, page 5

Budget

• Develop asset budget request.

• Submit budget request for approval.

• Receive approved asset budget.

Acquisition

• Process asset requisition.• Procurement issues asset PO.

• Asset received and tagged.– Hit our comfort zone here.

• Accounts Payable matches & pays invoice.

Add to Asset Registry

• Asset added to registry.

– Owning department established.– Useful life set.– Depreciation starts.

Asset In-Service

• What happens in this cycle.– Physical inventory.

– Depreciation.

– Transfers.

– Maintenance

Final Disposition

• Asset no longer providing acceptable level of service.

• Determine final dispostion.– Trade-in on new asset.– Sell.– Scrap.– Donate.

Back to Debits and Credits

• Basic accounting equation.

Assets = Liabilities + Owner Equity

Assets = Liabilities + Fund Balance

Financial Statements

• Income Statement

• Revenues

• Expenses

• Net Profit or Margin

Financial Statements

• Balance Sheet

• Assets

• Liabilities

• Owners Equity/Fund Balance

Income StatementAsset Revenues

• Revenue– Donated capital assets.

– Gain/loss on final disposition.

– Income from sale of non-capital assets.

Income StatementAsset Expenses

• Expense.– Cost of non-capital assets.

– Depreciation.

– Gain/loss on final disposition.

– Maintenance.

Balance SheetAssets

• Asset Section– Total cost of capital assets.– Pre-payments.

• Liabilities Section– Accumulated Depreciation.– Equipment Held in Trust.• Entity is the custodian but does not have title.

• Owners Equity/Fund Balance

Two Types of Assets

• Capital assets– Useful life greater than one year.– Meet capitalization threshold.

• Non-capital assets– Does not meet capital asset criteria.– Considered to be controlled, high risk, or

contractually required to track.

Non-Capital Assets

• Expensed when purchased

– Operating cost.– No additional accounting entries.– No gain or loss at final disposition.

Capital Assets

• Capitalized when purchased.

– Depreciation is operating cost.– Monthly depreciation entries.– Asset transfer between departments may

require journal entry.– Gain or loss is recorded at final

disposition.

Capital Asset Transactions

• Capitalized when purchased.

– Recorded on Balance Sheet.

– Exchange of assets.

• Give up asset (Cash)• Add asset (Capital Equipment)

Capital Asset Transactions

• Monthly– Depreciation expense.

• Activity driven

– Transfers between departments.

– Asset disposals.

Life Cycle Matching

• Accounting Transactions.

• Financial Statement Impact.

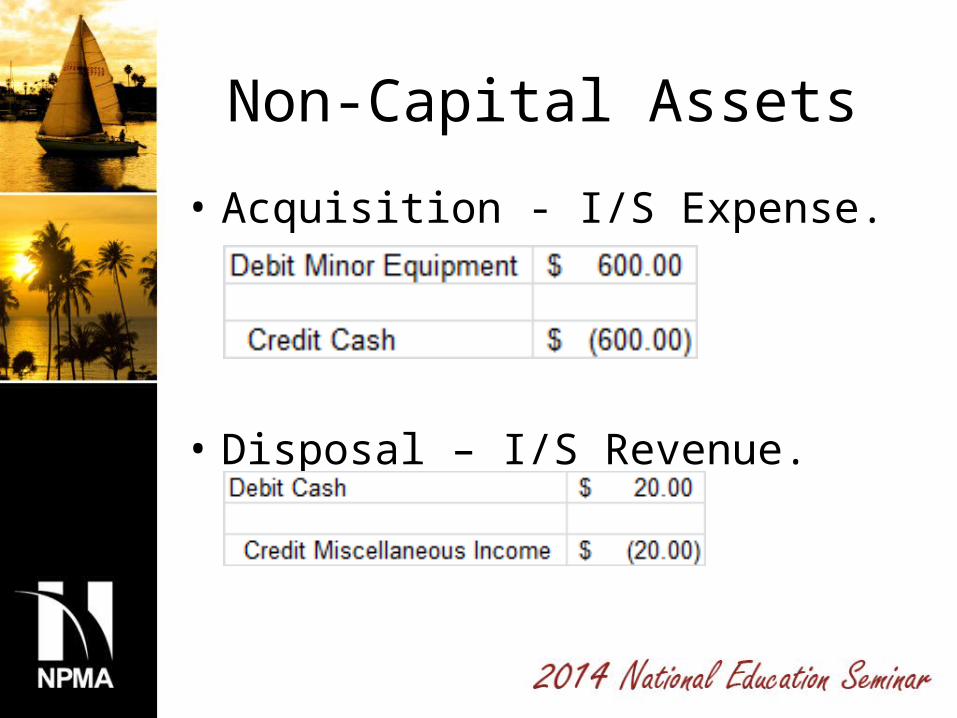

Non-Capital Assets

• Acquisition - I/S Expense.

• Disposal – I/S Revenue.

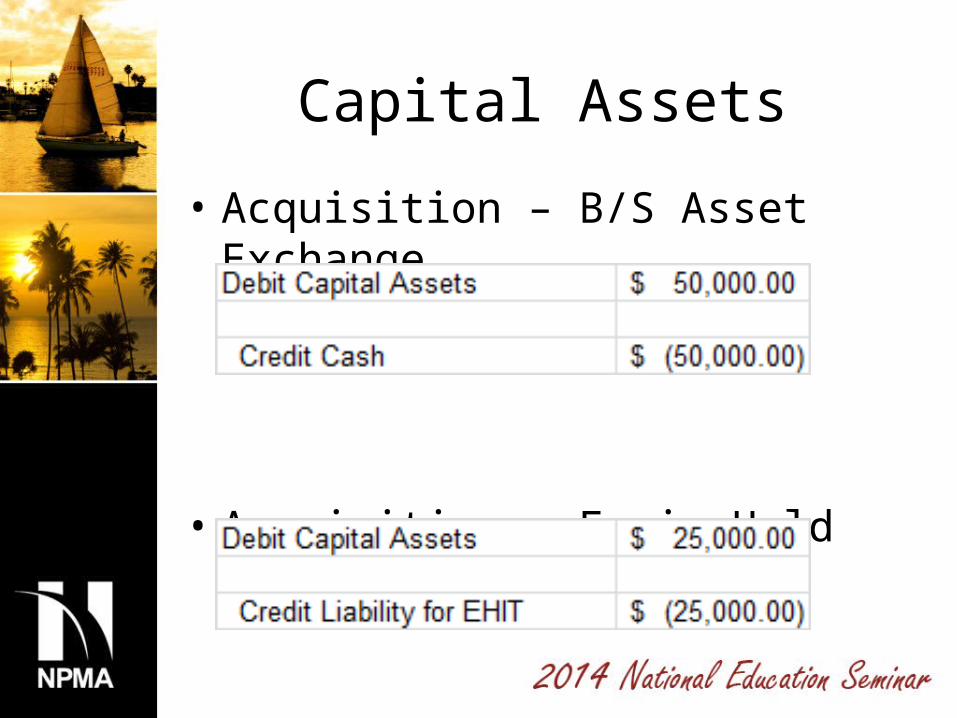

Capital Assets

• Acquisition – B/S Asset Exchange.

• Acquisition – Equip Held In Trust.

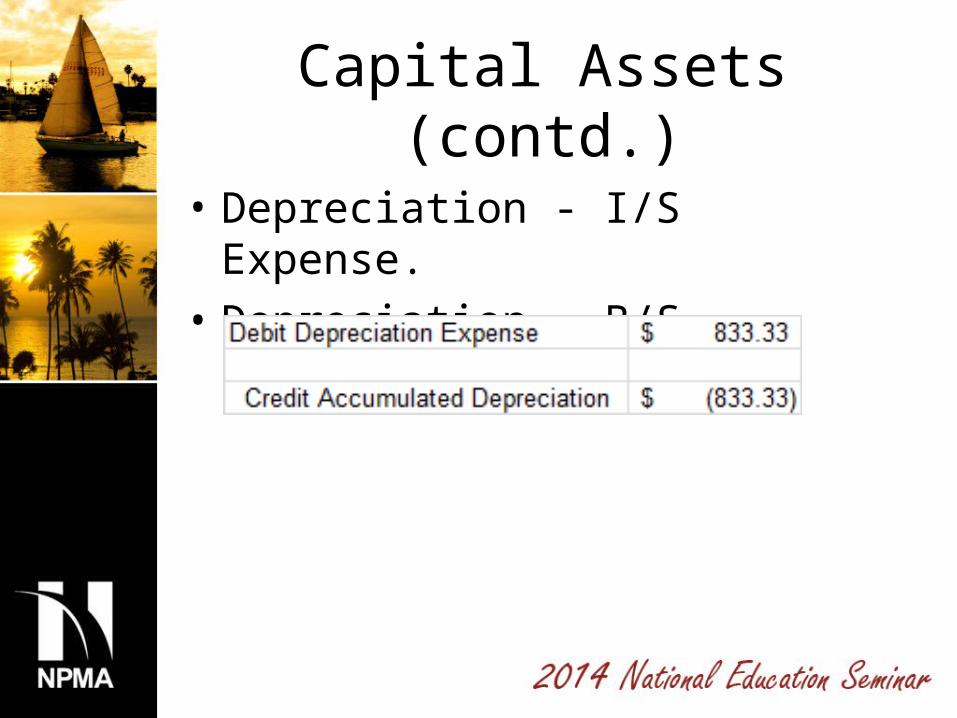

Capital Assets (contd.)

• Depreciation - I/S Expense.• Depreciation – B/S Liability.

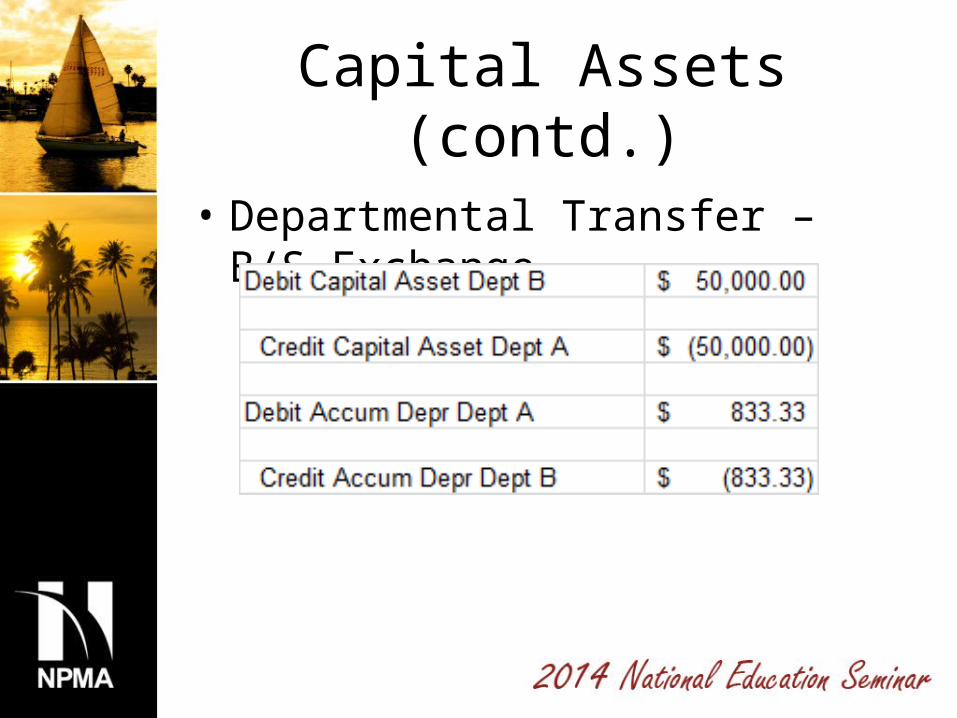

Capital Assets (contd.)

• Departmental Transfer – B/S Exchange.

Capital Assets (contd.)

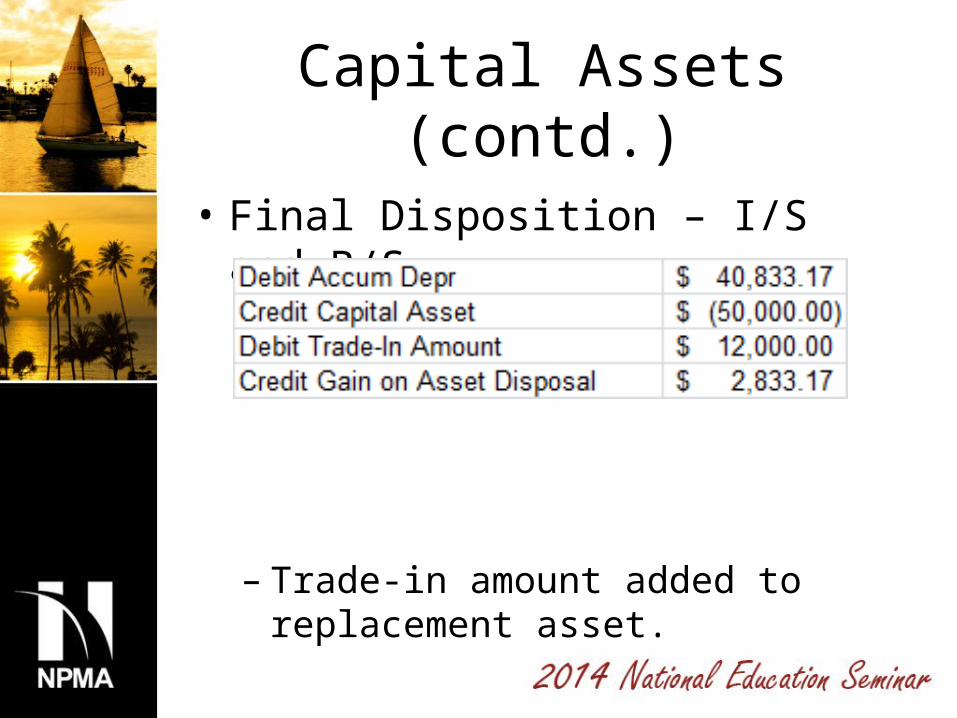

• Final Disposition – I/S and B/S.

– Trade-in amount added to replacement asset.

Financial Reports

• Snapshot of the financial results of an entity.

– Frequency – Annual and monthly.• Reporting at the entity level.• Reporting at department level.

• Can be your new best friend.

I/S Talks Revenues

• Revenue– Donated capital assets.

• Validate addition of donated capital assets.

– If you did not record any,

» Drill down and find the source of the dollars.

» Departments don’t tell you everything.

I/S Talks Revenues

• Revenue– Gain/loss on final disposition.

• Does this match registry disposals?– If not, drill to the dollars.

– Is the difference an omission or an accounting adjustment?

» You just need to know.

I/S Talks Revenues

• Revenue– Gain/loss on final disposition.

• Use departmental statements to highlight problematic departments.

– Is the loss missing assets?– Is the loss underutilization of assets?– Is the gain really a great deal?

I/S Talks Revenues

• Revenue– Income from sale of non-capital assets

• Did you sell any non-capital assets?

– If not, drill to the numbers.

• Does the amount look reasonable?

I/S Talks Expense

• Expense.– Cost of non-capital assets.

• Typically called Minor Equipment.• Difficult to track these results to asset

system.– Requires specific account numbers to track.– Most rely on asset system to identify the assets.

I/S Talks Expense (Contd)

• Expense.– Depreciation.

• Normally, a large number on the I/S.• If charged to department level, it has benefits

to asset management.– Departments will monitor assets closely.– Departments will report transfer with

promptness.– Departments will work to find missing assets.

I/S Talks Expense

• Expense.– Gain/loss on final disposition.

• Does this match registry disposals?– If not, drill to the dollars.

– Is the difference an omission or an accounting adjustment?

» You just need to know.

I/S Talks Expense

• Expense.

– Maintenance.

• Usually summarized at a high level.– Building– Equipment

• Frequently tracked in with PM software by Facilities.

B/S Talks Too

• Asset Section.

– Total cost of capital assets.• Presented by Type (Building, Equipment…).• Ties to AM sub-ledger balances.

– Sub-ledger?» The Asset Management system.

B/S Talks Too

• Asset Section.

– Pre-payments.• Vendor required down payment to build an

asset.• Not recorded in the AM system until asset.

received and invoices paid.• Good to monitor balance for changes.

B/S Talks Too

• Liability Section.

– Accumulated Depreciation.• Total depreciation expense for capital assets.• Balance ties to AM sub-ledger.

B/S Talks Too

• Liability Section.

– Equipment Held In Trust.• Total liability for equipment where entity is

custodian but does not have title.• Monitor balance for changes.

– Balance will change.

• Validate balance with Grants & Contracts at least annually.

Talking to Management

• Monitor I/S and B/S for opportunities.– Highlight value added by Asset

Management.

– Develop AM system reports to supplement financial report changes.

– Shine spotlight on non-compliant departments.

Final Thought

Focus management on the value of Asset Management.

•Get your NPMA certification.•Management likes certifications.

I’m a certified professional and bring “value

through professional asset management”.

Questions?

![CPPS Chapter 2[CompatibilityMode]](https://img.pdfslide.net/doc/110x75/577cc03c1a28aba7118f578b/cpps-chapter-2compatibilitymode.jpg)