Embed Size (px)

Citation preview

8/8/2019 May 2010 Oppenheimer Report

http://slidepdf.com/reader/full/may-2010-oppenheimer-report 1/41

Oppenheimer & Co. Inc. does and seeks to do business with companies covered in its research repora result, investors should be aware that the firm may have a conflict of interest that could affect theobjectivity of this report. Investors should consider this report as only a single factor in making their investment decision. See "Important Disclosures and Certifications" section at the end of this report foimportant disclosures, including potential conflicts of interest. See "Price Target Calculation" and "Keyto Price Target" sections at the end of this report, where applicable.

May 12, 2010

HEALTHCARE/MANAGED CARE & OTHERHEALTHCARE SERVICES

Carl McDonald, CFA

James Naklicki, CFA

The Game Has Changed,

But Still Trying to Play by the Old Rules--MLR UpdateSUMMARY

There will be a negative impact on health plan earnings from the minimum medicaloss ratio requirements that take effect next year. The hit won't be enormous, aplans will reduce broker commissions and cut non-core SG&A to offset most of th

rebates, but we now anticipate earnings growth of just 3% next year for the largediversified plans. This has already been reflected in stock prices, as these stockare down an average of 13% since April 8, compared to a 2% loss in the S&P. Thbigger valuation issue, in our view, is that it has become harder for plans to improvmargins, making the industry more dependent on increasing risk membership grow operating earnings, which is a problem, because the industry has no volumgrowth.

KEY POINTS

s There are opportunities to improve margins, but only in those markets wibelow average profitability. Re-pricing can help, but this normally results imembership losses, further pressuring revenue, and there are often structurreasons why a plan is less profitable, like lack of scale, or a difficult hospita

system that won't negotiate a reasonable price.

s The unfortunate truth is that the current Administration simply doesn't like thhealth insurance industry, and it believes plans make too much money. It maynot be rational, and it may not be true, but this is the world that plans inhabiand it isn't going to change in 2010, 2011, or 2012.

s So whether it it through minimum loss ratios, premium rate oversight, or judaring plans to step out of line, it doesn't seem like the for-profit plans are gointo be allowed to earn the kind of margins they have historically.

s This is why we're hesitant to step into the group here despite the drop valuation. The stocks look cheap, but that assumes the current margin structu

survives. And while margins have fallen from peak levels, profit levels are stiabove historical averages.

s Moreover, we can't forget that the industry still faces a steep drop in earnings i2014 when reform is fully implemented, led by adverse selection in thindividual business, the commoditization of the small group product, Medicarmargin pressure, employers converting to lower profit self-funded arrangementsand small employers dropping coverage and pushing employees into thexchange.

EQUITY RESEARCH

INDUSTRY UPDATE

Oppenheimer & Co Inc. 300 Madison Avenue 4th Floor New York, NY 10017 Tel: 800-221-5588 Fax: 212-667-822

8/8/2019 May 2010 Oppenheimer Report

http://slidepdf.com/reader/full/may-2010-oppenheimer-report 2/41

2

Investment Thesis

This report updates our prior analysis on the impact that minimum medical loss ratios wil

have on the industry next year (see The Average Person Thinks He Isn’t – Minimum

Medical Loss Ratio Analysis , published on April 8, 2010) with 2009 data. The conclusion is

relatively unchanged from our prior analysis, which is that earnings in the group will be

negatively impacted by the minimum loss ratios, but that the bigger valuation issue for the

group is the effective cap on margins that plans will now operate under. For investors, we

think this skews the risk / reward dynamics of the industry, since it leaves shareholdersexposed to company mispricing and lower than expected earnings, but doesn’t allow

investors to benefit as much when plans price above cost trends, like they are doing now.

Of course, with the large diversified plans (Aetna, CIGNA, UnitedHealth, WellPoint) down

12.9% since the initial loss ratio report was issued (relative to a 2.2% decline in the S&P

500), the most frequent question we get these days is whether the bad news is

appropriately factored into valuations. The simple answer is that we’re still not ready to

own the diversified managed care plans. It’s kind of an odd situation for us, because these

are the times we normally like the managed care stocks the most.

The stocks have traded down a lot, sentiment is awful, and there’s very little interest in the

group, but we can’t get rid of the nagging feeling that the world has changed for the

managed care industry. The stocks all look cheap right now, but that assumes that thehistorical margin structure for the industry holds, and we’re not sure that will be the case

Margins for the group have fallen from peak levels, but they are still above average. And

we can’t avoid the fact that the current Administration doesn’t like the health insurance

industry, and it believes plans make too much money. It isn’t rational, and the health

insurance industry has a lower margin than almost every other industry, but that is the

environment that the managed care group now operates in, and there isn’t any hope of it

changing in 2010, 2011, or 2012. Even if Republicans take back the House in the

upcoming mid-term elections, it just means that things can’t get any worse legislatively for

the industry. It wouldn’t do anything to change the legislation on the books, or the

interpretation of how the legislative language should be implemented. The point here is

whether it is through minimum medical loss ratios, premium rate increase oversight, or

simply daring plans to step out of the line, it feels like this Administration is going to do

everything in their power to keep the for-profit health plans from earning the kind ofmargins they have enjoyed historically.

We also don’t like that every day we seem to come across a new negative for the industry

For example, there hasn’t been a lot of attention paid to the student health insurance

business, which is a product that will likely see a major drop in revenue and earnings now

that children are allowed to remain on their parents’ insurance until the age of 26. Today

most insurers cut off children from parents’ insurance at either 19 or 23. This isn’t a huge

deal, and the product won’t go away entirely, because many enrollees are internationa

students. But the business generated $470 million in premiums for Aetna in 2009, and had

a loss ratio of 83.3%, while United’s student business reported 2009 premiums of $390

million and a loss ratio of 71.0%. (In 2008, the loss ratio on Aetna’s student business was

around 75%, while United’s student loss ratio was 56%). Assuming the student business

falls by half in 2011 because of the new regulation, and that the SG&A ratio typically runs

about 15%, we estimate it will cost Aetna about $4 million in earnings ($0.01 per share)

while United will take a slightly larger hit, at more than $25 million ($0.01 per share).

Another example is the unexpected places that the minimum MLR requirements show up

For example, no one thinks about the impact that the minimum MLR will have on Centene

since it is predominantly a Medicaid plan. However, we often forget that Centene bought

an individual health insurance company, Celtic Insurance, back in 2008. In 2009, Celtic

had $40 million in premiums, and a medical expense of 61.8%. If we assume the company

can increase its MLR by 300 basis points through tax adjustments and shifting SG&A

Centene would have incurred a rebate of $6.2 million on the business in 2009, which

would have negatively impacted earnings by $0.09 per share. Again, it’s not enormous

but it’s just another headwind facing the industry next year.

HEALTHCARE

8/8/2019 May 2010 Oppenheimer Report

http://slidepdf.com/reader/full/may-2010-oppenheimer-report 3/41

We also don’t think the market fully appreciates the administrative complexity that health

reform will place on the industry, and the spending that will be incurred complying with al

the new reporting requirements plans will have to abide by. It’s difficult to size the tota

cost at this point, but the incremental spending will be another reason (in addition to the

shrinking commercial membership base) that will make it difficult for plans to show

meaningful improvements in operating expenses over the next couple years. For example

most people believe the large group market is essentially immune from the minimum MLR

requirements because most large groups are already operating close to or above the 85%

loss ratio requirement. That depends. One of the issues that needs to be clarified is how

to treat a large group that technically buys its health insurance in one state, and hasemployees in a number of states. For purposes of the MLR calculation, does the health

plan need an 85% MLR in each state, or only in aggregate? Perhaps more importantly, if

plans do need to track loss ratios by state, rather than by employer group, they will need

to create an entirely new administrative structure, or spend a lot of time re-working

existing systems to provide the required data.

There has been a lot of attention focused on premium rate increase issues at the state

level, particularly in California, but a lot less on the regulation of “excessive” rate increases

currently being discussed in tandem with the minimum MLR definition. The debate at the

NAIC on how to define an excessive rate increase is ongoing, but there is more discussion

than we’d like around the idea that rates above a certain amount should be considered

excessive. From our perspective, no rate increase should be considered excessive if the

underlying claims data supports it. In other words, if cost trends are rising 40%, then a40% premium increase is more than reasonable, whereas there is some discussion at the

NAIC about capping rates at a certain amount. In addition, there’s also been some debate

about whether plans will have the ability to adjust pricing for prior year issues. In othe

words, if a plan misprices a product, the following year it will adjust premium rates to

account for normal cost trend, as well as to make-up for the mispricing the prior year,

whereas the NAIC has discussed limiting the increase to cost trend only.

Moreover, we can’t forget that in addition to all the modest earnings challenges facing the

group in 2011, the bigger negative earnings impact actually hits in 2014 when reform is

fully implemented. It is still a few years away, of course, but at that point, plans will have to

deal with financial losses in the individual business because of adverse selection, the

commoditization of the small group product because of product standardization and

pricing transparency, Medicare margin pressure, employers converting to lower profit self-

funded arrangements because the health insurance industry tax only applies to fully

insured plans, and smaller employers dropping coverage entirely and pushing employees

into the exchange to take advantage of the subsidies offered by the government and the

lack of penalty for small employers that don’t offer coverage. The earnings drop the

industry is facing in 2014 will re-base industry earnings back to 2011/2012 levels, and tha

is one reason why more long-term long only investors have been reluctant to step into the

group.

In any event, the point of this report is to update our minimum medical loss ratio analysis

with 2009 statutory data. The conclusion is that while the calculated rebate amounts are

lower in 2009, each company would still have incurred a rebate last year. Said differently

even though many plans would have characterized 2009 as a pretty bad year, companies

would still have had to return money to customers because certain markets remained very

profitable. Since it appears that 2010 will be a far more favorable year from a medical lossratio perspective, as the flu has not been a factor, and plans are pricing above cost trend

our sense is that the rebate amounts will grow dramatically in 2010 performance. A few

highlights of the analysis:

• Our sense is that plans will be able to increase medical loss ratios by abou

300-500 basis points. This will be driven by shifting certain SG&A expenses into

medical expenses (100 basis points), but this will be limited to clearly defined

items, like nurse hotlines and disease management. We don’t think plans have

gotten much traction on including items like health care information technology

We also think plans will be able to deduct state and federal taxes (including

income taxes) from premiums (200-400 basis points). The adjustment for federa

HEALTHCAR

8/8/2019 May 2010 Oppenheimer Report

http://slidepdf.com/reader/full/may-2010-oppenheimer-report 4/41

4

income taxes is still being debated, and is the primary reason for the wide range

of our estimate.

• Depending on the interpretation, the minimum loss ratio has the potentia

to create significant administrative expenses for plans. As noted, if plans

aren’t allowed to aggregate large group loss ratios at the employer level, and are

instead required to calculate loss ratios on a state by state basis, it wil

necessitate significant changes to the systems used by plans, increasing

administrative spending. In other words, let's assume an employer like Delta

Airlines is a fully insured plan. The question is whether plans can report one lossratio for that account, or if they would have to report 50 separate state by state

loss ratios.

In addition, the mechanism for rebating premiums has the potential to create

significant administrative headaches. Plans would much prefer to rebate

premiums back to employer groups, rather than rebating premiums back to

individual customers. In many cases, the cost of administering and sending the

check would be more than the actual rebate amount.

Another lingering question is whether MLRs will be based on calendar years o

plan years. The industry likely favors a calendar year approach, since the

administrative complexity of tracking rebates based on plan years would be

staggering.

• Some plans are pushing for a rolling three-year average medical loss ratio

to be implemented immediately in 2011, and some would like to see broker

commissions excluded from premium revenue, at least initially, but the

NAIC doesn’t seem likely to recommend these changes. The legislation

specifically requires a single year MLR calculation in 2011, with rolling averages

implemented in 2014, so it seems difficult to simply ignore the legislative

language. In the case of broker commissions, the probability of adjusting the

MLR calculation is basically zero. The legislative language clearly allows fo

adjustments related to quality improvement measures and taxes, but nothing

else, so it seems to us that plans are wasting their time pushing for a broad

commission adjustment.

• It still isn’t clear how closely the HHS Secretary plans to follow the NAIC

recommendations. With all the attention focused on the deliberations of the

NAIC, it is often lost that they are simply making recommendations to HHS

rather than determining the definition and interpretation. For example, the NAIC

could recommend that federal income taxes be excluded from premiums, but the

HHS Secretary could very easily have a different interpretation. Plans have

deployed most of their efforts to lobbying the NAIC, whereas consume

advocates and some Democratic members of Congress have focused their

attention on the HHS Secretary.

• In addition, it isn’t clear whether state regulators will implement the reform

legislation language, or do their own thing. As per the legislation, individua

state regulators have the authority to implement even more stringent minimum

loss ratio requirements if they see fit. For example, it is within the power of state

regulators to require an 87% large group loss ratio (rather than the 85% cited in

the legislation) if they believe their market can sustain it.

• It’s important to point out again that we are relying on statutory entity data

because the loss ratio minimums will likely be calculated on a state by

state basis, the rebates we’ve calculated in this report are likely

understated by a material amount. For example, United’s Golden Rule

subsidiary reported 2009 premiums of $1.3 billion, with an overall loss ratio of

around 63%. However, Golden Rule writes business in all 50 states, and while

there are some large markets, like Florida ($307 million in premiums), Texas

($113 million in premiums), and Ohio ($74 million), there are many states tha

HEALTHCARE

8/8/2019 May 2010 Oppenheimer Report

http://slidepdf.com/reader/full/may-2010-oppenheimer-report 5/41

write under $10 million in premiums. A state by state look at Golden Rule medica

loss ratios would likely reveal a number of states with loss ratios well below the

consolidated 63%.

• The NAIC is in the midst of several concurrent processes. The mos

immediate concern is responding to the questions issued by HHS regarding both

minimum medical loss ratios as well as excessive premium rate increases. The

NAIC was careful in these responses to try and provide information, rather than

make any recommendations. The responses to these questions will be

submitted by the May 14, 2010 deadline.

After responding to the HHS questions, the NAIC will develop a set o

recommendations regarding how both the minimum MLR and excessive rate

increases should be implemented and defined. These recommendations, o

course, are of the greatest interest to investors, and the NAIC appears to be on

track to submit these recommendations to HHS by the June 1, 2010 deadline.

• It is still unclear exactly what products will be subject to the minimum MLR

It is certain that individual, small group, and large group products will each

separately have to meet their respective minimum loss ratio on a state by state

basis. Less clear is whether things like limited benefit products, short-term

medical offerings, student health insurance, and the Federal Employees Health

Benefits Program (FEHBP) will also be subject to the minimum MLRs. Planswould prefer that these other products be excluded from the MLR calculation

with the exception of the FEHBP program. Because of they way that produc

operates, plans typically have a loss ratio of around 95%, so including it in the

calculation pushes up the large group loss ratio. This is a particularly important

question for Blue Cross plans, since they serve the majority of enrollees in the

FEHBP program.

In our analysis, we’ve excluded all of these other products from the rebate

calculation, with the exception of the student health insurance, which we’ve

included in the individual rebate calculation. While it is possible that student

health insurance is excluded entirely from the minimum MLR discussion, it is also

possible that it is counted as a large group product, since it is typically sold to

universities and there are generally more than 100 enrollees. In the latter caseplans would be subject to a minimum 85% MLR, which would put pressure on

what has historically been a very profitable business for plans. As noted earlier

we think the student health insurance business will be under significant pressure

next year because of the new provision allowing children to remain on their

parents’ insurance until the age of 26.

• Not surprisingly, the calculated rebates in 2009 are much lower than wha

we found looking at 2008 data. Aetna missed earnings several times in 2009

while WellPoint has frequently discussed the loss it incurred on its California

individual business. And many plans were vocal about the unexpected cos

increases experienced last year because of the flu season and the highe

penetration of COBRA members. But it is a bit of a disappointment that even in

what most plans believe was a bad year, each plan would have still incurred a

significant rebate. Financial results for the industry appear to be improving

significantly in 2010, so this means rebates will presumably be larger based on

the 2010 data.

The Earnings Impact

Since the ultimate amount of SG&A shifting and tax adjustment is still unknown, we are

presenting our data in the form of a scenario analysis to illustrate the potential rebates

plans could incur. In Exhibit 1, below, we’ve picked a spot estimate of a 500 basis poin

shift to give a sense of the potential earnings impact that plans would experience

assuming that plans did nothing else to offset the impact of the consumer rebates, like cu

HEALTHCAR

8/8/2019 May 2010 Oppenheimer Report

http://slidepdf.com/reader/full/may-2010-oppenheimer-report 6/41

6

broker commissions. In any event, after all those caveats, we estimate that rebates for the

average plan in the industry will negatively impact earnings by about 5% based on the

2009 data. Since 2010 earnings appear to be shaping up a lot better, it suggests that the

amount of rebates paid by plans will grow a lot as we head into 2011.

Exhibit 1: 2009 Rebates, Assuming 500 Basis Point Shift to MLR, andthat Rebates are Calculated at a Statutory Entity

Rebate, Assuming EPS 2011 % of

500 bp MLR Shift Impact EPS Total

Aetna $33,766,955 $0.05 $3.05 2%CIGNA $28,355,735 $0.07 $4.10 2%Humana $63,844,106 $0.24 $5.65 4%United $323,385,304 $0.19 $3.35 6%WellPoint $179,532,572 $0.27 $6.75 4%

Source: Company reports and Oppenheimer & Co. analysis.

Of course, as we noted above, the figures in Exhibit 1 assume the full impact of the rebate

falls to the bottom line. That's not reasonable, considering that plans do have othe

options. As we pointed out in a prior eHealth report (see EHTH: Disposing Of Medica

Waste-Health Reform Update, published on March 30, 2010), many plans are considering

reducing individual commissions in order to come into compliance with the new

regulations. In addition, whatever non-core SG&A that isn’t counted as medical expense

could be eliminated. For example, if nurse hotlines are ruled to be an administrative cost

they can simply be ended. Plans don't have to offer disease management programs, or

spend as much on health care IT as they do.

There are a couple points here. The first is that the ultimate earnings impact on plans wil

not be as dire as the raw numbers suggest. But the data also indicates that there will be

some impact on earnings in 2011 that will slow the industry’s earnings growth rate, and

will put pressure on consensus projections. In other words, even if plans can re-size their

administrative cost base, it is unlikely they will be able to do it fully for 2011 given the tigh

timeframe in which these regulations will likely be announced.

Company by Company Data

What follows is our company by company analysis of enrollment, premiums, and medica

expense broken down into individual, small group, and large group products, as well as

the other products sold by plans that aren’t subject to the minimum MLR requirements.

We'll start with WellPoint. In Exhibit 2, we’ve summarized WellPoint’s 2009 results, where

tracked down almost $31 billion of WellPoint’s commercial premiums. Almost $24 billion o

the premiums come from traditional individual, small group, and large group products

The balance comes from other products such as Medicare supplemental and FEHBP, bu

it is still unclear if these products will be counted in the minimum MLR calculations. We

estimate that WellPoint had something less than $44 billion in commercial premiums

overall in 2009, with the difference largely due to the premiums derived from WellPoint’sBlue Cross of California subsidiary. Because of the different California statutory filing, we

can’t derive profitability by product for the state. In any event, while WellPoint’s overal

commercial medical loss ratio appeared to be about 81.9%, the breakdown by produc

makes clear that loss ratios differ materially by product, as WellPoint’s individual loss ratio

was 75.3%, while its small group loss ratio was 81.4%, followed by a large group medica

loss ratio of 84.8%.

HEALTHCARE

8/8/2019 May 2010 Oppenheimer Report

http://slidepdf.com/reader/full/may-2010-oppenheimer-report 7/41

Exhibit 2: WellPoint Summary of 2009 Results by Product

Member Medical

Plan Lives Months PMPM Premiums Expense MLR

Individual 1,816,207 22,203,195 $192.70 $4,278,501,638 $3,223,119,439 75.3%

Small Group 2,132,580 26,565,602 $316.67 $8,412,636,472 $6,848,486,952 81.4%Large Group 2,859,619 35,001,440 $325.50 $11,393,036,704 $9,659,941,591 84.8%

Total 6,808,406 83,770,237 $287.50 $24,084,174,814 $19,731,547,982 81.9% Source: Company reports and Oppenheimer & Co. analysis.

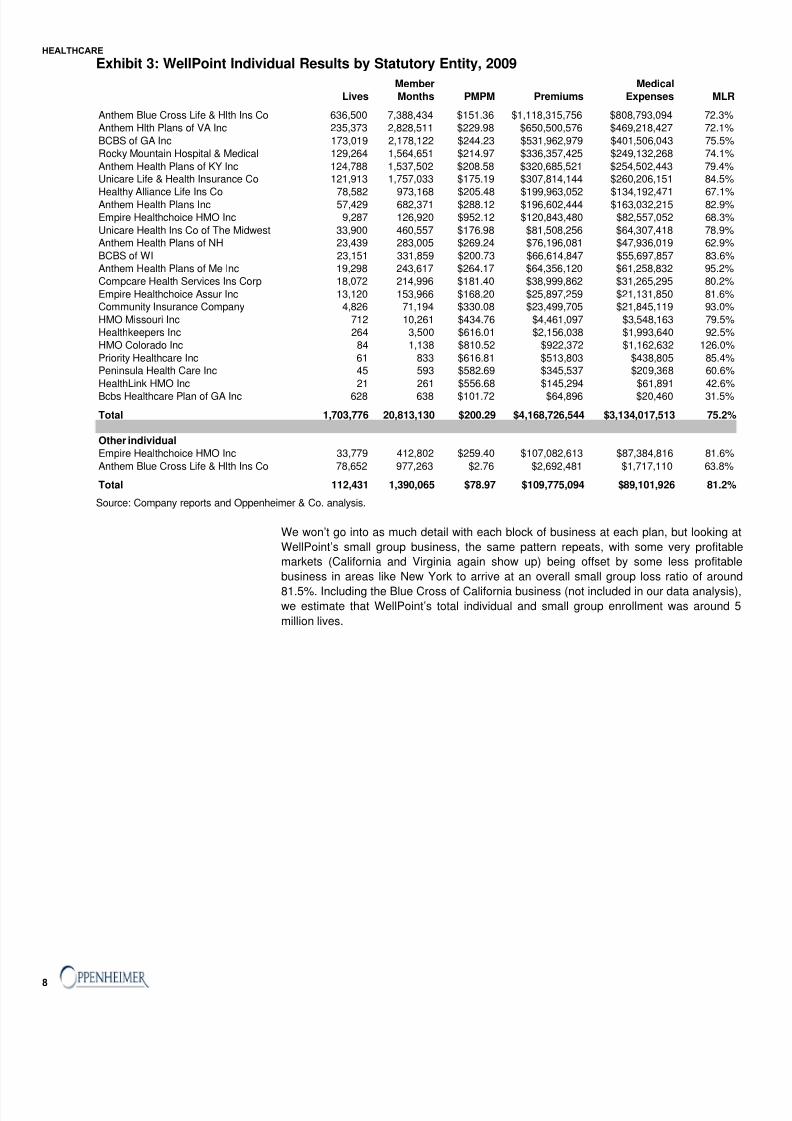

Our analysis tracked down 1.8 million individual lives at WellPoint in 2009, although if we

had been able to include the California data, WellPoint’s individual book would have been

over 2 million lives. From a statutory entity perspective, even if WellPoint was able to shift

500 basis points into its MLR, the company would have still incurred an individual rebate

in excess of $85 million in 2009. Looking at the data, a few things stand out. The first is

extraordinary profitability of a handful of markets. Specifically, the individual gross profits

from the Anthem Blue Cross Life & Health Insurance Company (California), Anthem o

Virginia, BCBS of GA Inc. and Rocky Mountain (Colorado) subsidiaries account over two

thirds of the individual gross profits in our analysis.

Second, WellPoint is one plan that would probably be heavily in favor of a state by state

interpretation, rather than a statutory entity look at minimum loss ratios, since it would beable to combine its presumably less profitable Blue Cross of California subsidiary with

Anthem Blue Cross Life & Health, which could significantly reduce its customer giveback

something it could also do with its multiple New York and Virginia entities. Third, WellPoin

has a number of individual markets that don't appear to be very profitable, and don't have

a lot of membership. These are the markets we would view as being most at-risk if

WellPoint decided to reduce its exposure to the individual business and pulled out of some

individual markets.

HEALTHCAR

8/8/2019 May 2010 Oppenheimer Report

http://slidepdf.com/reader/full/may-2010-oppenheimer-report 8/41

8

Exhibit 3: WellPoint Individual Results by Statutory Entity, 2009

Member MedicalLives Months PMPM Premiums Expenses MLR

Anthem Blue Cross Life & Hlth Ins Co 636,500 7,388,434 $151.36 $1,118,315,756 $808,793,094 72.3%Anthem Hlth Plans of VA Inc 235,373 2,828,511 $229.98 $650,500,576 $469,218,427 72.1%

BCBS of GA Inc 173,019 2,178,122 $244.23 $531,962,979 $401,506,043 75.5%Rocky Mountain Hospital & Medical 129,264 1,564,651 $214.97 $336,357,425 $249,132,268 74.1%

Anthem Health Plans of KY Inc 124,788 1,537,502 $208.58 $320,685,521 $254,502,443 79.4%Unicare Life & Health Insurance Co 121,913 1,757,033 $175.19 $307,814,144 $260,206,151 84.5%

Healthy Alliance Life Ins Co 78,582 973,168 $205.48 $199,963,052 $134,192,471 67.1%Anthem Health Plans Inc 57,429 682,371 $288.12 $196,602,444 $163,032,215 82.9%Empire Healthchoice HMO Inc 9,287 126,920 $952.12 $120,843,480 $82,557,052 68.3%

Unicare Health Ins Co of The Midwest 33,900 460,557 $176.98 $81,508,256 $64,307,418 78.9%Anthem Health Plans of NH 23,439 283,005 $269.24 $76,196,081 $47,936,019 62.9%

BCBS of WI 23,151 331,859 $200.73 $66,614,847 $55,697,857 83.6%Anthem Health Plans of Me Inc 19,298 243,617 $264.17 $64,356,120 $61,258,832 95.2%Compcare Health Services Ins Corp 18,072 214,996 $181.40 $38,999,862 $31,265,295 80.2%

Empire Healthchoice Assur Inc 13,120 153,966 $168.20 $25,897,259 $21,131,850 81.6%Community Insurance Company 4,826 71,194 $330.08 $23,499,705 $21,845,119 93.0%

HMO Missouri Inc 712 10,261 $434.76 $4,461,097 $3,548,163 79.5%Healthkeepers Inc 264 3,500 $616.01 $2,156,038 $1,993,640 92.5%HMO Colorado Inc 84 1,138 $810.52 $922,372 $1,162,632 126.0%

Priority Healthcare Inc 61 833 $616.81 $513,803 $438,805 85.4%Peninsula Health Care Inc 45 593 $582.69 $345,537 $209,368 60.6%

HealthLink HMO Inc 21 261 $556.68 $145,294 $61,891 42.6%

Bcbs Healthcare Plan of GA Inc 628 638 $101.72 $64,896 $20,460 31.5%

Total 1,703,776 20,813,130 $200.29 $4,168,726,544 $3,134,017,513 75.2%

Other individualEmpire Healthchoice HMO Inc 33,779 412,802 $259.40 $107,082,613 $87,384,816 81.6%

Anthem Blue Cross Life & Hlth Ins Co 78,652 977,263 $2.76 $2,692,481 $1,717,110 63.8%

Total 112,431 1,390,065 $78.97 $109,775,094 $89,101,926 81.2% Source: Company reports and Oppenheimer & Co. analysis.

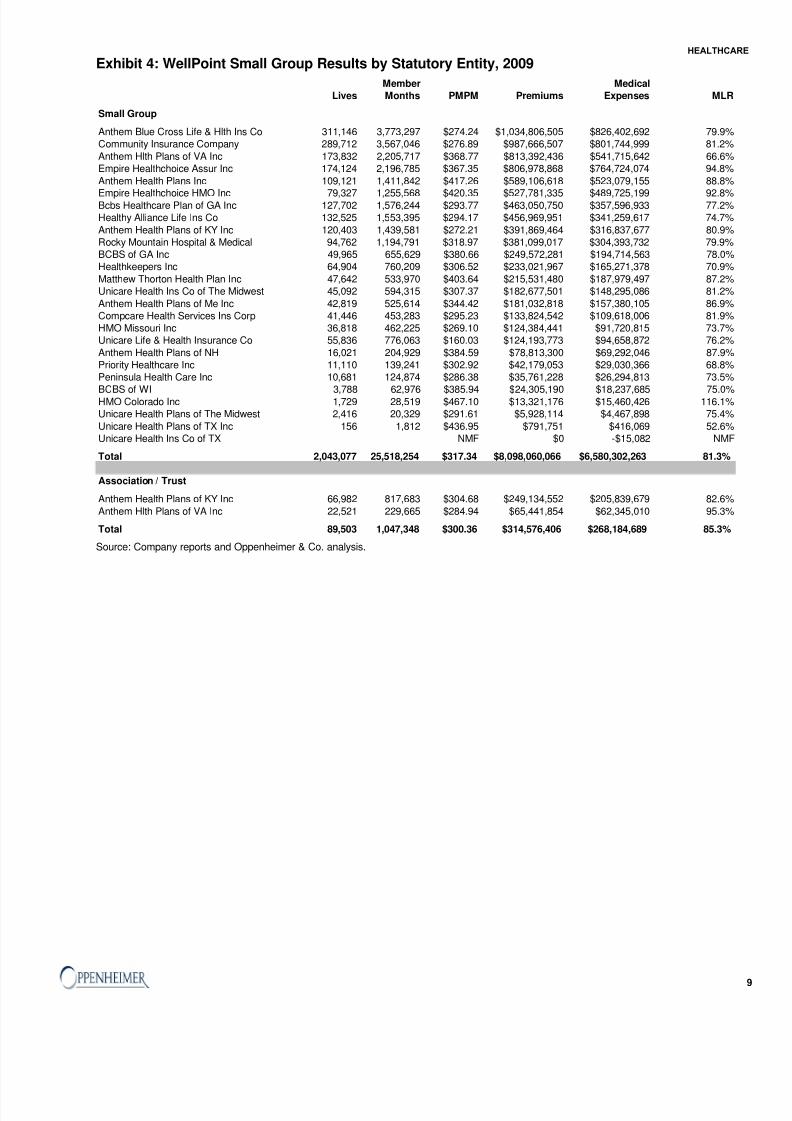

We won’t go into as much detail with each block of business at each plan, but looking at

WellPoint’s small group business, the same pattern repeats, with some very profitable

markets (California and Virginia again show up) being offset by some less profitable

business in areas like New York to arrive at an overall small group loss ratio of around

81.5%. Including the Blue Cross of California business (not included in our data analysis),we estimate that WellPoint’s total individual and small group enrollment was around 5

million lives.

HEALTHCARE

8/8/2019 May 2010 Oppenheimer Report

http://slidepdf.com/reader/full/may-2010-oppenheimer-report 9/41

Exhibit 4: WellPoint Small Group Results by Statutory Entity, 2009

Member Medical

Lives Months PMPM Premiums Expenses MLR

Small Group

Anthem Blue Cross Life & Hlth Ins Co 311,146 3,773,297 $274.24 $1,034,806,505 $826,402,692 79.9%Community Insurance Company 289,712 3,567,046 $276.89 $987,666,507 $801,744,999 81.2%Anthem Hlth Plans of VA Inc 173,832 2,205,717 $368.77 $813,392,436 $541,715,642 66.6%Empire Healthchoice Assur Inc 174,124 2,196,785 $367.35 $806,978,868 $764,724,074 94.8%Anthem Health Plans Inc 109,121 1,411,842 $417.26 $589,106,618 $523,079,155 88.8%

Empire Healthchoice HMO Inc 79,327 1,255,568 $420.35 $527,781,335 $489,725,199 92.8%Bcbs Healthcare Plan of GA Inc 127,702 1,576,244 $293.77 $463,050,750 $357,596,933 77.2%Healthy Alliance Life Ins Co 132,525 1,553,395 $294.17 $456,969,951 $341,259,617 74.7%Anthem Health Plans of KY Inc 120,403 1,439,581 $272.21 $391,869,464 $316,837,677 80.9%Rocky Mountain Hospital & Medical 94,762 1,194,791 $318.97 $381,099,017 $304,393,732 79.9%BCBS of GA Inc 49,965 655,629 $380.66 $249,572,281 $194,714,563 78.0%Healthkeepers Inc 64,904 760,209 $306.52 $233,021,967 $165,271,378 70.9%Matthew Thorton Health Plan Inc 47,642 533,970 $403.64 $215,531,480 $187,979,497 87.2%Unicare Health Ins Co of The Midwest 45,092 594,315 $307.37 $182,677,501 $148,295,086 81.2%Anthem Health Plans of Me Inc 42,819 525,614 $344.42 $181,032,818 $157,380,105 86.9%Compcare Health Services Ins Corp 41,446 453,283 $295.23 $133,824,542 $109,618,006 81.9%HMO Missouri Inc 36,818 462,225 $269.10 $124,384,441 $91,720,815 73.7%Unicare Life & Health Insurance Co 55,836 776,063 $160.03 $124,193,773 $94,658,872 76.2%Anthem Health Plans of NH 16,021 204,929 $384.59 $78,813,300 $69,292,046 87.9%Priority Healthcare Inc 11,110 139,241 $302.92 $42,179,053 $29,030,366 68.8%Peninsula Health Care Inc 10,681 124,874 $286.38 $35,761,228 $26,294,813 73.5%

BCBS of WI 3,788 62,976 $385.94 $24,305,190 $18,237,685 75.0%HMO Colorado Inc 1,729 28,519 $467.10 $13,321,176 $15,460,426 116.1%Unicare Health Plans of The Midwest 2,416 20,329 $291.61 $5,928,114 $4,467,898 75.4%Unicare Health Plans of TX Inc 156 1,812 $436.95 $791,751 $416,069 52.6%Unicare Health Ins Co of TX NMF $0 -$15,082 NMF

Total 2,043,077 25,518,254 $317.34 $8,098,060,066 $6,580,302,263 81.3%

Association / Trust

Anthem Health Plans of KY Inc 66,982 817,683 $304.68 $249,134,552 $205,839,679 82.6%Anthem Hlth Plans of VA Inc 22,521 229,665 $284.94 $65,441,854 $62,345,010 95.3%

Total 89,503 1,047,348 $300.36 $314,576,406 $268,184,689 85.3% Source: Company reports and Oppenheimer & Co. analysis.

HEALTHCAR

8/8/2019 May 2010 Oppenheimer Report

http://slidepdf.com/reader/full/may-2010-oppenheimer-report 10/41

10

Exhibit 5: WellPoint Large Group Results by Statutory Entity, 2009

Member Medical

Lives Months PMPM Premiums Expenses MLR

Large Group

Community Insurance Company 427,168 5,134,866 $312.67 $1,605,530,292 $1,412,451,513 88.0%

Anthem Health Plans Inc 308,715 3,765,128 $379.41 $1,428,511,843 $1,259,628,898 88.2%Anthem Blue Cross Life & Hlth Ins Co 360,252 4,274,311 $284.47 $1,215,925,607 $1,027,064,085 84.5%

Bcbs Healthcare Plan of GA Inc 252,809 3,054,670 $280.30 $856,213,244 $699,889,480 81.7%

Anthem Hlth Plans of VA Inc 152,927 2,002,480 $425.11 $851,283,871 $675,712,717 79.4%

BCBS of GA Inc 175,915 2,268,958 $309.54 $702,341,574 $604,085,050 86.0%Healthy Alliance Life Ins Co 165,896 1,853,050 $307.69 $570,167,870 $471,913,230 82.8%Anthem Health Plans of Me Inc 106,085 1,281,843 $412.17 $528,333,440 $472,976,576 89.5%

Anthem Health Plans of KY Inc 120,090 1,505,237 $309.39 $465,708,674 $381,657,260 82.0%

Empire Healthchoice HMO Inc 70,144 984,559 $429.29 $422,659,379 $338,330,181 80.0%

Unicare Life & Health Insurance Co 52,424 730,210 $499.24 $364,552,333 $326,230,630 89.5%

Rocky Mountain Hospital & Medical 92,288 1,100,024 $302.86 $333,152,526 $276,882,822 83.1%

Healthkeepers Inc 93,462 1,104,974 $301.08 $332,689,093 $276,336,819 83.1%

HMO Colorado Inc 68,303 815,990 $322.87 $263,458,857 $238,205,532 90.4%

Unicare Health Plans of The Midwest 61,430 781,597 $323.47 $252,819,505 $209,216,749 82.8%

Compcare Health Services Ins Corp 55,799 658,542 $338.91 $223,186,203 $199,370,510 89.3%

Matthew Thorton Health Plan Inc 34,529 426,066 $407.19 $173,490,811 $150,753,534 86.9%

HMO Missouri Inc 26,856 349,085 $301.38 $105,206,671 $84,112,744 80.0%

Anthem Health Plans of NH 17,405 237,283 $357.41 $84,806,913 $74,990,064 88.4%Priority Healthcare Inc 22,319 273,627 $281.92 $77,140,290 $58,445,090 75.8%

Unicare Health Ins Co of The Midwest 16,770 233,509 $217.36 $50,755,273 $40,671,273 80.1%

BCBS of WI 11,460 142,485 $344.08 $49,026,435 $42,538,996 86.8%Unicare Health Plans of TX Inc 10,933 139,515 $344.37 $48,044,912 $43,877,764 91.3%

Peninsula Health Care Inc 12,882 148,796 $284.81 $42,378,462 $32,493,285 76.7%

Total 2,716,861 33,266,805 $332.08 $11,047,384,078 $9,397,834,802 85.1%

Other comprehensive major medical

Empire Healthchoice Assur Inc 2,109,022 25,436,802 $168.98 $4,298,372,042 $3,850,175,356 89.6%

Community Insurance Company 125,237 1,520,516 $190.80 $290,109,196 $220,540,996 76.0%

Empire Healthchoice HMO Inc 17,521 214,119 $259.40 $55,543,430 $41,565,793 74.8%

Total 142,758 1,734,635 $199.27 $345,652,626 $262,106,789 75.8% Source: Company reports and Oppenheimer & Co. analysis.

HEALTHCARE

8/8/2019 May 2010 Oppenheimer Report

http://slidepdf.com/reader/full/may-2010-oppenheimer-report 11/41

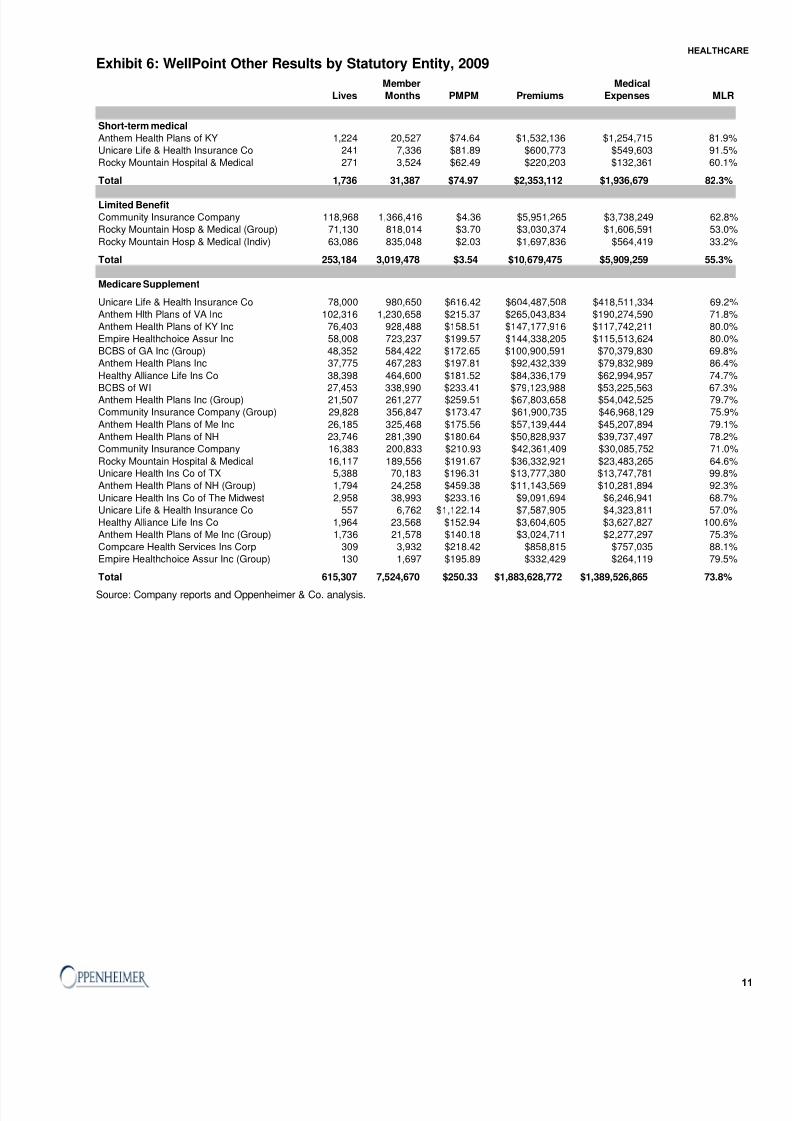

Exhibit 6: WellPoint Other Results by Statutory Entity, 2009

Member Medical

Lives Months PMPM Premiums Expenses MLR

Short-term medical

Anthem Health Plans of KY 1,224 20,527 $74.64 $1,532,136 $1,254,715 81.9%

Unicare Life & Health Insurance Co 241 7,336 $81.89 $600,773 $549,603 91.5%

Rocky Mountain Hospital & Medical 271 3,524 $62.49 $220,203 $132,361 60.1%

Total 1,736 31,387 $74.97 $2,353,112 $1,936,679 82.3%

Limited Benefit

Community Insurance Company 118,968 1,366,416 $4.36 $5,951,265 $3,738,249 62.8%

Rocky Mountain Hosp & Medical (Group) 71,130 818,014 $3.70 $3,030,374 $1,606,591 53.0%

Rocky Mountain Hosp & Medical (Indiv) 63,086 835,048 $2.03 $1,697,836 $564,419 33.2%

Total 253,184 3,019,478 $3.54 $10,679,475 $5,909,259 55.3%

Medicare Supplement

Unicare Life & Health Insurance Co 78,000 980,650 $616.42 $604,487,508 $418,511,334 69.2%

Anthem Hlth Plans of VA Inc 102,316 1,230,658 $215.37 $265,043,834 $190,274,590 71.8%

Anthem Health Plans of KY Inc 76,403 928,488 $158.51 $147,177,916 $117,742,211 80.0%

Empire Healthchoice Assur Inc 58,008 723,237 $199.57 $144,338,205 $115,513,624 80.0%

BCBS of GA Inc (Group) 48,352 584,422 $172.65 $100,900,591 $70,379,830 69.8%

Anthem Health Plans Inc 37,775 467,283 $197.81 $92,432,339 $79,832,989 86.4%

Healthy Alliance Life Ins Co 38,398 464,600 $181.52 $84,336,179 $62,994,957 74.7%

BCBS of WI 27,453 338,990 $233.41 $79,123,988 $53,225,563 67.3%Anthem Health Plans Inc (Group) 21,507 261,277 $259.51 $67,803,658 $54,042,525 79.7%

Community Insurance Company (Group) 29,828 356,847 $173.47 $61,900,735 $46,968,129 75.9%

Anthem Health Plans of Me Inc 26,185 325,468 $175.56 $57,139,444 $45,207,894 79.1%

Anthem Health Plans of NH 23,746 281,390 $180.64 $50,828,937 $39,737,497 78.2%

Community Insurance Company 16,383 200,833 $210.93 $42,361,409 $30,085,752 71.0%

Rocky Mountain Hospital & Medical 16,117 189,556 $191.67 $36,332,921 $23,483,265 64.6%Unicare Health Ins Co of TX 5,388 70,183 $196.31 $13,777,380 $13,747,781 99.8%

Anthem Health Plans of NH (Group) 1,794 24,258 $459.38 $11,143,569 $10,281,894 92.3%

Unicare Health Ins Co of The Midwest 2,958 38,993 $233.16 $9,091,694 $6,246,941 68.7%

Unicare Life & Health Insurance Co 557 6,762 $1,122.14 $7,587,905 $4,323,811 57.0%

Healthy Alliance Life Ins Co 1,964 23,568 $152.94 $3,604,605 $3,627,827 100.6%

Anthem Health Plans of Me Inc (Group) 1,736 21,578 $140.18 $3,024,711 $2,277,297 75.3%

Compcare Health Services Ins Corp 309 3,932 $218.42 $858,815 $757,035 88.1%

Empire Healthchoice Assur Inc (Group) 130 1,697 $195.89 $332,429 $264,119 79.5%

Total 615,307 7,524,670 $250.33 $1,883,628,772 $1,389,526,865 73.8% Source: Company reports and Oppenheimer & Co. analysis.

HEALTHCAR

8/8/2019 May 2010 Oppenheimer Report

http://slidepdf.com/reader/full/may-2010-oppenheimer-report 12/41

12

Exhibit 7: WellPoint Other Results by Statutory Entity Continued, 2009

Member MedicalLives Months PMPM Premiums Expenses MLR

FEHBP

Anthem Hlth Plans of VA Inc 268,378 3,199,062 $346.92 $1,109,814,630 $1,043,702,467 94.0%

BCBS of GA Inc 173,341 2,072,223 $410.63 $850,924,466 $787,893,093 92.6%Rocky Mountain Hospital & Medical 97,143 1,158,845 $411.23 $476,549,869 $450,954,037 94.6%

Empire Healthchoice Assur Inc 98,648 1,185,893 $378.52 $448,886,118 $421,003,134 93.8%BCBS of WI 54,394 655,569 $499.28 $327,310,781 $311,556,283 95.2%

Healthy Alliance Life Ins Co 49,198 590,330 $392.58 $231,753,646 $230,488,843 99.5%Anthem Health Plans of NH 31,834 383,045 $508.21 $194,666,590 $185,650,461 95.4%Anthem Health Plans Inc 32,105 385,697 $423.46 $163,328,445 $154,195,533 94.4%

Anthem Health Plans of Me Inc 34,331 414,545 $370.06 $153,407,588 $144,090,230 93.9%HMO Missouri Inc 21,215 257,599 $369.63 $95,216,115 $91,220,120 95.8%

Unicare Health Plans of The Midwest 8,384 106,542 $394.58 $42,039,427 $39,252,829 93.4%Unicare Health Ins Co of The Midwest 36 355 $45.20 $16,047 -$3,333 -20.8%Community Insurance Company 0 0 NMF -$602,581 $715,317 -118.7%

Total 869,007 10,409,705 $393.22 $4,093,311,141 $3,860,719,014 94.3%

Total commercial 8,547,640 104,755,477 $287.09 $30,074,147,314 $24,989,639,799 83.1%

Dental

Anthem Blue Cross Life & Hlth Ins Co 308,113 3,969,216 $41.20 $163,536,186 $100,693,600 61.6%

Anthem Blue Cross Life & Hlth (Indiv) 162,764 1,995,990 $28.65 $57,176,238 $29,234,331 51.1%Community Insurance Company (Group) 150,217 1,904,349 $23.56 $44,874,399 $32,089,528 71.5%

Anthem Health Plans Inc (Group) 69,056 882,978 $35.38 $31,241,792 $21,037,548 67.3%Empire Healthchoice Assur Inc (Group) 94,835 1,225,832 $23.07 $28,274,865 $20,895,804 73.9%

Unicare Life & Health Insurance Co (Group) 57,744 817,315 $30.44 $24,881,614 $16,794,060 67.5%

Compcare Health Services Ins Corp (Group) 45,068 563,235 $31.51 $17,746,574 $13,831,569 77.9%BCBS of WI (Group) 57,140 697,334 $24.05 $16,772,046 $11,380,937 67.9%Rocky Mountain Hospital & Medical (Group) 40,296 497,867 $30.61 $15,240,408 $10,504,521 68.9%Healthy Alliance Life Ins Co (Group) 46,586 567,190 $22.07 $12,517,200 $7,323,938 58.5%

BCBS of GA Inc (Group) 49,359 593,415 $20.12 $11,941,959 $8,025,090 67.2%

Anthem Health Plans of KY Inc (Group) 28,143 332,740 $30.46 $10,135,948 $7,439,427 73.4%Healthy Alliance Life Ins Co 22,678 268,055 $20.30 $5,442,612 $2,893,349 53.2%

Rocky Mountain Hosp & Medical (Indiv) 23,046 272,764 $19.87 $5,420,266 $2,696,425 49.7%Anthem Health Plans of KY Inc (Indiv) 31,016 366,709 $10.09 $3,701,905 $2,102,099 56.8%

Unicare Life & Health Insurance Co 14,261 215,755 $14.24 $3,071,446 $786,336 25.6%

Anthem Health Plans of Me Inc (Group) 7,955 86,275 $29.34 $2,531,006 $1,897,005 75.0%

BCBS of WI (Indiv) 7,016 87,162 $24.20 $2,109,109 $963,673 45.7%Anthem Health Plans of NH (Group) 4,289 55,079 $32.08 $1,766,939 $1,303,394 73.8%Onenation Ins Co (Group) 295 4,068 $36.47 $148,347 $57,875 39.0%

Total 1,219,877 15,403,328 $29.77 $458,530,859 $291,950,509 63.7%

Stop loss

Community Insurance Company 521,739 6,370,318 $10.72 $68,317,681 $62,162,749 91.0%Anthem Health Plans Inc $47,890,963 $40,604,042 84.8%Anthem Blue Cross Life & Hlth Ins Co 445,880 3,535,057 $12.94 $45,731,322 $46,861,819 102.5%

BCBS of GA Inc $34,880,756 $29,972,371 85.9%BCBS of WI 84,377 1,059,619 $18.48 $19,582,115 $17,554,818 89.6%

Rocky Mountain Hospital & Medical $15,815,780 $15,912,626 100.6%

Bcbs Healthcare Plan of GA Inc $10,578,946 $3,851,750 36.4%Anthem Health Plans of NH $3,667,144 $523,958 14.3%

Matthew Thorton Health Plan Inc $3,038,724 $1,447,984 47.7%

Anthem Health Plans of Me Inc $2,024,693 $587,205 29.0%HMO Colorado Inc $807,480 $515,508 63.8%

Total 1,051,996 10,964,994 $23.01 $252,335,604 $219,994,830 87.2% Source: Company reports and Oppenheimer & Co. analysis.

HEALTHCARE

8/8/2019 May 2010 Oppenheimer Report

http://slidepdf.com/reader/full/may-2010-oppenheimer-report 13/41

Exhibit 8: WellPoint Other Results by Statutory Entity Continued, 2009

Member MedicalLives Months PMPM Premiums Expenses MLR

Accident only

Anthem Life Ins Co 1,019,266 13,208,542 $0.84 $11,061,147 $4,412,091 39.9%

Unicare Life & Health Insurance Co 315,039 4,172,152 $1.53 $6,372,596 $3,735,796 58.6%

Anthem Blue Cross Life & Hlth (Group) 384,566 4,696,640 $0.90 $4,219,454 $1,164,522 27.6%Greater Georgia Life Insurance Co 159,207 1,958,004 $0.64 $1,243,473 $808,897 65.1%

Unicare Health Ins Co of The Midwest 9,662 128,852 $0.81 $104,318 $37,609 36.1%

Anthem Blue Cross Life & Hlth (Individ) 64,408 784,377 $0.10 $81,538 $1,519 1.9%Anthem Life & Disability Ins Co 1,445 6,037 $2.00 $12,068 $3,343 27.7%Anthem Life Ins Co 11 150 $1.12 $168 $0 NMF

Total 1,953,604 24,954,754 $0.93 $23,094,762 $10,163,777 44.0%

Disability (Short-term)

Anthem Life Ins Co (Group) 146,121 1,193,154 $18.62 $22,212,780 $13,764,223 62.0%

Unicare Life & Health Insurance Co (Group) 35,340 470,819 $12.97 $6,108,709 $4,934,134 80.8%Greater Georgia Life Insurance Co (Group) 22,978 289,340 $15.64 $4,526,372 $2,563,313 56.6%

Unicare Health Ins Co of The Midwest 43 528 $12.48 $6,592 $1,361 20.6%Anthem Life & Disability Ins Co (Group) 61 61 $15.54 $948 $678 71.5%

Total 204,543 1,953,902 $16.82 $32,855,401 $21,263,709 64.7%

Disability (Long-term)

Anthem Life Ins Co (Group) 122,751 1,465,318 $24.31 $35,618,024 $23,230,400 65.2%

Unicare Life & Health Insurance Co (Group) 41,790 517,628 $16.05 $8,305,436 $2,104,785 25.3%Greater Georgia Life Insurance Co (Group) 18,527 230,909 $15.82 $3,652,381 $4,698,310 128.6%Unicare Health Ins Co of The Midwest 11 145 $88.83 $12,881 $0 0.0%

Anthem Life & Disability Ins Co (Group) 165 557 $23.03 $12,825 $9,213 71.8%

Anthem Life Ins Co 29 372 $20.08 $7,471 $11,942 159.8%

Total 183,273 2,214,929 $21.49 $47,609,018 $30,054,650 63.1%

Long-term Care

Anthem Blue Cross Life & Hlth Ins Co 2,265 27,870 $202.07 $5,631,658 $6,852,808 121.7%

Healthy Alliance Life Ins Co 139 1,668 $62.24 $103,821 $483,691 465.9%Anthem Health Plans of VA Inc. 0 0 NMF $84,943 -$14,803 -17.4%

BCBS of WI 32 384 $162.73 $62,488 $83,751 134.0%

Unicare Health Ins Co of The Midwest 9 110 $197.82 $21,760 $8,470 38.9%Unicare Life & Health Insurance Co 18 248 $77.97 $19,337 -$23,444 -121.2%

Total 2,463 30,280 $195.64 $5,924,007 $7,390,473 124.8%

Other group care

American Imaging Management E Llc 81,641 1,061,661 $21.19 $22,497,919 $21,075,959 93.7%Anthem Blue Cross Life & Hlth Ins Co 304,542 3,357,573 $5.41 $18,152,376 $10,614,493 58.5%

Empire Healthchoice Assur Inc 5,917 70,917 $124.76 $8,847,860 $5,437,986 61.5%

Anthem Health Plans Inc 11,057 130,434 $37.75 $4,923,833 $1,650,978 33.5%Rocky Mountain Hospital & Medical 1,911 20,596 $232.03 $4,778,787 $3,171,052 66.4%

Anthem Health Plans of KY Inc 98,758 1,124,828 $3.99 $4,487,004 $2,853,522 63.6%

Anthem Health Plans of Me Inc 23,655 279,786 $4.96 $1,388,282 $659,824 47.5%

Anthem Health Plans of NH 3,546 39,645 $6.48 $256,777 $98,478 38.4%BCBS of WI 6,960 $169,520 $81,103 47.8%

Anthem Life Ins Co 3 36 $0 $18,782

Total 537,990 6,085,476 $10.76 $65,502,358 $45,662,177 69.7%

Total Specialty $885,852,009 $626,480,125 70.7%

Overall $30,959,999,323 $25,616,119,924 82.7% Source: Company reports and Oppenheimer & Co. analysis.

In the next exhibit, we lay out a scenario analysis of what WellPoint’s rebates would have

been had the minimum medical loss ratio requirements been in effect in 2008, depending

on how much in SG&A / premium taxes plans are able to shift into medical costs. Note

that we’re doing these calculations on a statutory entity basis (rather than state by state)

a treatment that probably has a more negative impact on WellPoint than any other plan. In

addition, we aren’t giving any credit to plans for their ability to reduce broker commissions

or eliminate other non-essential SG&A.

HEALTHCAR

8/8/2019 May 2010 Oppenheimer Report

http://slidepdf.com/reader/full/may-2010-oppenheimer-report 14/41

14

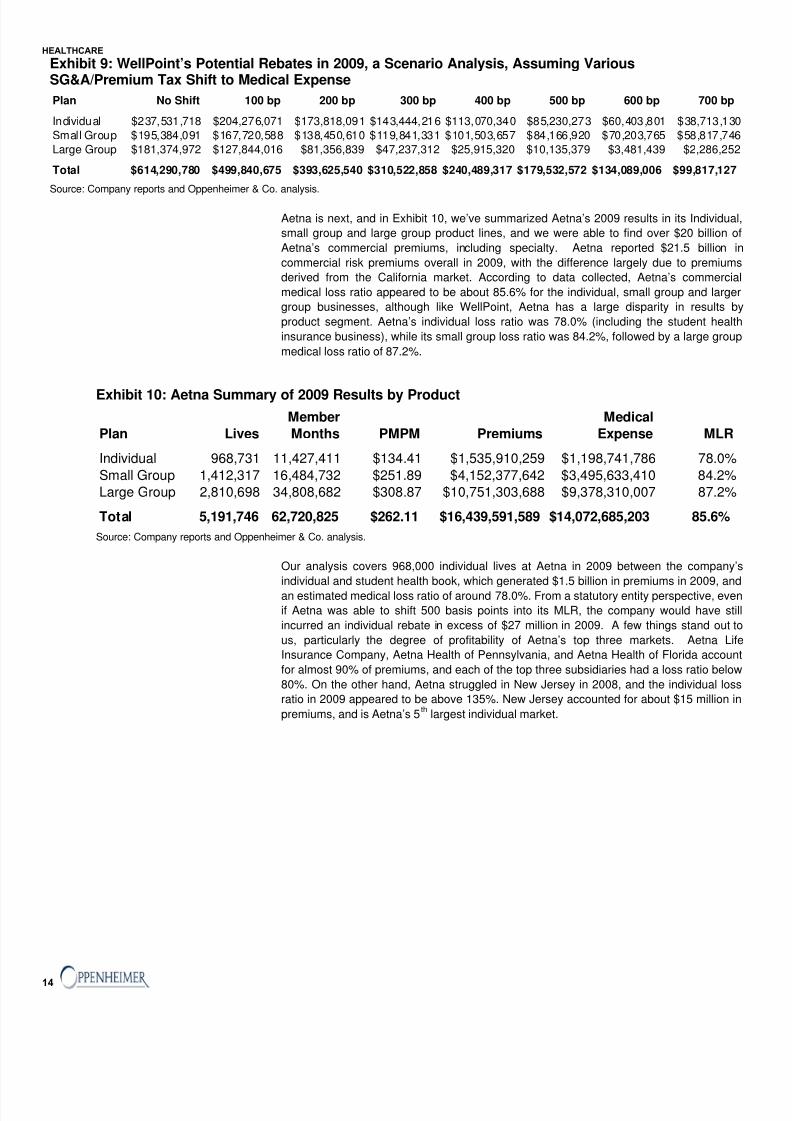

Exhibit 9: WellPoint’s Potential Rebates in 2009, a Scenario Analysis, Assuming VariousSG&A/Premium Tax Shift to Medical Expense

Plan No Shift 100 bp 200 bp 300 bp 400 bp 500 bp 600 bp 700 bp

Individual $237,531,718 $204,276,071 $173,818,091 $143,444,216 $113,070,340 $85,230,273 $60,403,801 $38,713,130Small Group $195,384,091 $167,720,588 $138,450,610 $119,841,331 $101,503,657 $84,166,920 $70,203,765 $58,817,746Large Group $181,374,972 $127,844,016 $81,356,839 $47,237,312 $25,915,320 $10,135,379 $3,481,439 $2,286,252

Total $614,290,780 $499,840,675 $393,625,540 $310,522,858 $240,489,317 $179,532,572 $134,089,006 $99,817,127 Source: Company reports and Oppenheimer & Co. analysis.

Aetna is next, and in Exhibit 10, we’ve summarized Aetna’s 2009 results in its Individual

small group and large group product lines, and we were able to find over $20 billion of

Aetna’s commercial premiums, including specialty. Aetna reported $21.5 billion in

commercial risk premiums overall in 2009, with the difference largely due to premiums

derived from the California market. According to data collected, Aetna’s commercia

medical loss ratio appeared to be about 85.6% for the individual, small group and larger

group businesses, although like WellPoint, Aetna has a large disparity in results by

product segment. Aetna’s individual loss ratio was 78.0% (including the student health

insurance business), while its small group loss ratio was 84.2%, followed by a large group

medical loss ratio of 87.2%.

Exhibit 10: Aetna Summary of 2009 Results by Product

Member MedicalPlan Lives Months PMPM Premiums Expense MLR

Individual 968,731 11,427,411 $134.41 $1,535,910,259 $1,198,741,786 78.0%

Small Group 1,412,317 16,484,732 $251.89 $4,152,377,642 $3,495,633,410 84.2%Large Group 2,810,698 34,808,682 $308.87 $10,751,303,688 $9,378,310,007 87.2%

Total 5,191,746 62,720,825 $262.11 $16,439,591,589 $14,072,685,203 85.6% Source: Company reports and Oppenheimer & Co. analysis.

Our analysis covers 968,000 individual lives at Aetna in 2009 between the company’s

individual and student health book, which generated $1.5 billion in premiums in 2009, and

an estimated medical loss ratio of around 78.0%. From a statutory entity perspective, even

if Aetna was able to shift 500 basis points into its MLR, the company would have stil

incurred an individual rebate in excess of $27 million in 2009. A few things stand out to

us, particularly the degree of profitability of Aetna’s top three markets. Aetna Life

Insurance Company, Aetna Health of Pennsylvania, and Aetna Health of Florida account

for almost 90% of premiums, and each of the top three subsidiaries had a loss ratio below

80%. On the other hand, Aetna struggled in New Jersey in 2008, and the individual loss

ratio in 2009 appeared to be above 135%. New Jersey accounted for about $15 million in

premiums, and is Aetna’s 5th

largest individual market.

HEALTHCARE

8/8/2019 May 2010 Oppenheimer Report

http://slidepdf.com/reader/full/may-2010-oppenheimer-report 15/41

Exhibit 11: Aetna Individual Results by Statutory Entity, 2009

Member MedicalIndividual Lives Months PMPM Premiums Expenses MLR

Aetna Life Insurance Co 359,541 4,047,278 $177.80 $719,620,244 $512,673,722 71.2%Aetna Health Inc PA Corp 36,490 477,613 $264.71 $126,429,380 $98,678,116 78.0%Aetna Health Inc FL Corp 44,443 555,888 $219.72 $122,137,375 $93,577,646 76.6%Aetna Health Inc NY Corp 8,218 102,207 $762.47 $77,930,135 $74,483,529 95.6%Aetna Health Inc NJ Corp 1,364 19,023 $811.46 $15,436,326 $20,781,713 134.6%Aetna Health Inc GA Corp 562 7,037 $504.14 $3,547,601 $4,927,103 138.9%

Aetna Health Inc TX Corp 86 1,114 $888.69 $989,999 $1,118,069 112.9%Aetna Health Inc 3 906 $357.44 $323,840 $79,651 24.6%Aetna Health Inc Co Corp 37 447 $715.78 $319,954 $1,010,328 315.8%Aetna Health Inc CT Corp 39 518 $567.11 $293,764 $263,843 89.8%Aetna Health Inc ME Corp 17 187 $905.72 $169,369 $326,680 192.9%Aetna Health of The Carolinas Inc 18 229 $634.74 $145,356 $282,977 194.7%Aetna Health Inc DE Corp 6 80 $382.73 $30,618 $37,897 123.8%

Total 450,824 5,212,527 $204.77 $1,067,373,961 $808,241,274 75.7%

Student

Aetna Life Insurance Co 517,907 6,214,884 $75.39 $468,536,298 $390,500,512 83.3% Source: Company reports and Oppenheimer & Co. analysis.

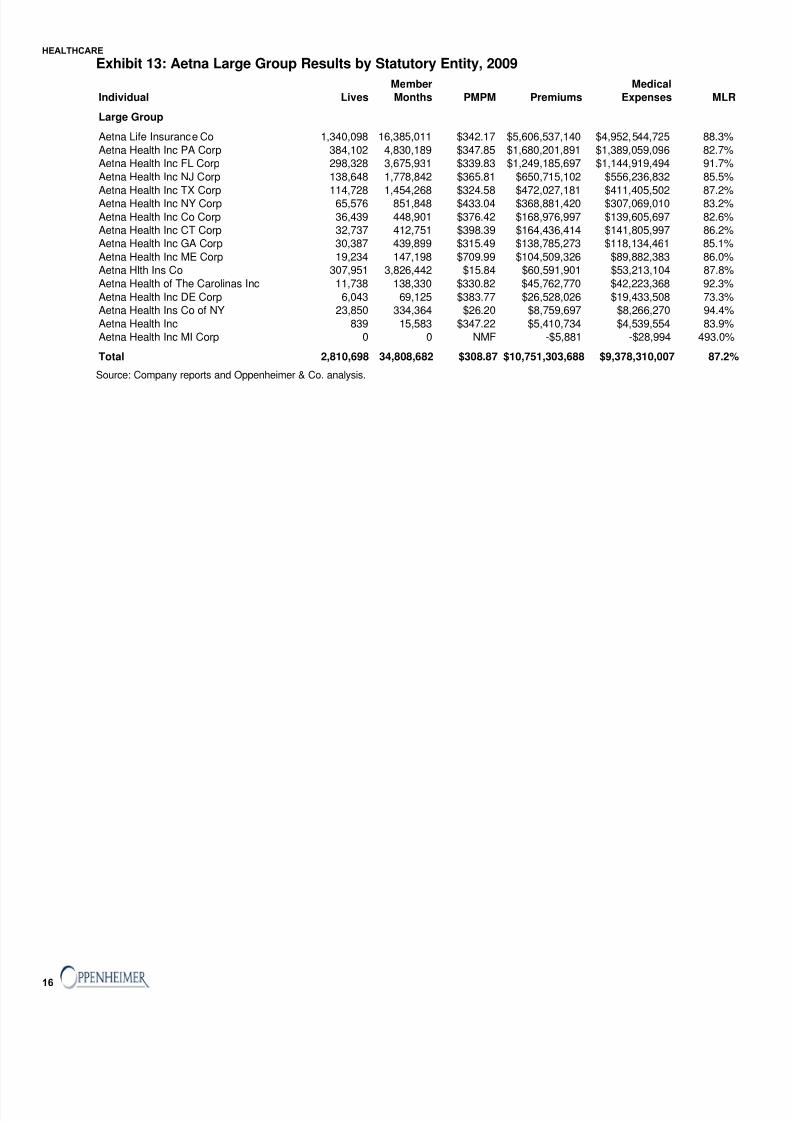

We won’t go into as much detail with each block of business at each plan, but looking atAetna’s small group business, the same pattern repeats, with some very profitable

markets (Florida and Texas) offset by some less profitable business in areas like Maryland

to arrive at an overall small group loss ratio of 79.4%. In the large group business, i

appears as though the company is producing a loss ratio substantially above the 85%

threshold, as only four of Aetna’s top ten large group markets had MLR’s below 85%.

Exhibit 12: Aetna Small Group Results by Statutory Entity, 2009

Member Medical

Individual Lives Months PMPM Premiums Expenses MLR

Small Group

Aetna Life Insurance Co 524,611 6,041,270 $306.68 $1,852,717,485 $1,582,377,988 85.4%Aetna Health Inc NJ Corp 157,941 1,970,254 $343.99 $677,740,318 $625,290,085 92.3%Aetna Health Inc PA Corp 190,389 2,232,034 $293.00 $653,984,981 $522,048,133 79.8%Aetna Health Inc FL Corp 127,899 1,630,551 $361.66 $589,707,409 $463,389,409 78.6%Aetna Health Inc GA Corp 48,451 533,422 $269.47 $143,739,061 $118,243,930 82.3%Aetna Health Inc TX Corp 28,491 319,085 $318.47 $101,618,484 $77,910,270 76.7%Aetna Health Inc CT Corp 18,024 174,418 $314.90 $54,924,593 $51,155,122 93.1%Aetna Health Inc NY Corp 5,371 60,766 $490.23 $29,789,113 $23,276,661 78.1%Aetna Hlth Ins Co 290,660 3,373,154 $5.91 $19,937,510 $10,746,354 53.9%Aetna Health Inc ME Corp 2,276 40,054 $415.40 $16,638,342 $12,227,818 73.5%Aetna Health of The Carolinas Inc 2,160 17,249 $303.67 $5,238,078 $4,120,210 78.7%Aetna Health Inc DE Corp 2,698 16,739 $310.07 $5,190,201 $3,730,581 71.9%Aetna Health Ins Co of NY 13,342 75,671 $14.05 $1,063,258 $1,203,808 113.2%Aetna Health Inc 4 65 $1,366.29 $88,809 -$86,959 -97.9%

Total 1,412,317 16,484,732 $251.89 $4,152,377,642 $3,495,633,410 84.2% Source: Company reports and Oppenheimer & Co. analysis.

HEALTHCAR

8/8/2019 May 2010 Oppenheimer Report

http://slidepdf.com/reader/full/may-2010-oppenheimer-report 16/41

16

Exhibit 13: Aetna Large Group Results by Statutory Entity, 2009

Member MedicalIndividual Lives Months PMPM Premiums Expenses MLR

Large Group

Aetna Life Insurance Co 1,340,098 16,385,011 $342.17 $5,606,537,140 $4,952,544,725 88.3%Aetna Health Inc PA Corp 384,102 4,830,189 $347.85 $1,680,201,891 $1,389,059,096 82.7%Aetna Health Inc FL Corp 298,328 3,675,931 $339.83 $1,249,185,697 $1,144,919,494 91.7%Aetna Health Inc NJ Corp 138,648 1,778,842 $365.81 $650,715,102 $556,236,832 85.5%Aetna Health Inc TX Corp 114,728 1,454,268 $324.58 $472,027,181 $411,405,502 87.2%Aetna Health Inc NY Corp 65,576 851,848 $433.04 $368,881,420 $307,069,010 83.2%Aetna Health Inc Co Corp 36,439 448,901 $376.42 $168,976,997 $139,605,697 82.6%Aetna Health Inc CT Corp 32,737 412,751 $398.39 $164,436,414 $141,805,997 86.2%Aetna Health Inc GA Corp 30,387 439,899 $315.49 $138,785,273 $118,134,461 85.1%Aetna Health Inc ME Corp 19,234 147,198 $709.99 $104,509,326 $89,882,383 86.0%Aetna Hlth Ins Co 307,951 3,826,442 $15.84 $60,591,901 $53,213,104 87.8%Aetna Health of The Carolinas Inc 11,738 138,330 $330.82 $45,762,770 $42,223,368 92.3%Aetna Health Inc DE Corp 6,043 69,125 $383.77 $26,528,026 $19,433,508 73.3%Aetna Health Ins Co of NY 23,850 334,364 $26.20 $8,759,697 $8,266,270 94.4%Aetna Health Inc 839 15,583 $347.22 $5,410,734 $4,539,554 83.9%Aetna Health Inc MI Corp 0 0 NMF -$5,881 -$28,994 493.0%

Total 2,810,698 34,808,682 $308.87 $10,751,303,688 $9,378,310,007 87.2% Source: Company reports and Oppenheimer & Co. analysis.

HEALTHCARE

8/8/2019 May 2010 Oppenheimer Report

http://slidepdf.com/reader/full/may-2010-oppenheimer-report 17/41

Exhibit 14: Aetna Other Results by Statutory Entity, 2009

Member MedicalIndividual Lives Months PMPM Premiums Expenses MLR

Medicare Supplement

Aetna Life Insurance Co 7,420 65,396 $164.84 $10,779,602 $9,071,468 84.2%

Total 7,420 65,396 $164.84 $10,779,602 $9,071,468 84.2%

FEHBP

Aetna Health Inc PA Corp 171,241 2,050,539 $366.05 $750,590,777 $645,307,719 86.0%Aetna Life Insurance Co 420,112 4,814,506 $58.61 $282,171,282 $255,812,778 90.7%

Aetna Health Inc NJ Corp 21,502 258,480 $460.89 $119,129,623 $106,798,039 89.6%Aetna Health Inc NY Corp 23,117 279,488 $424.75 $118,713,621 $103,908,703 87.5%Aetna Health Inc TX Corp 12,123 146,820 $414.58 $60,868,498 $55,674,162 91.5%

Aetna Health Inc GA Corp 11,817 144,398 $386.91 $55,868,344 $47,983,377 85.9%Aetna Health Inc CT Corp 971 11,314 $370.77 $4,194,943 $4,837,318 115.3%Aetna Health of The Carolinas Inc 938 10,147 $306.75 $3,112,566 $5,272,996 169.4%

Aetna Health Inc DE Corp 359 3,845 $360.31 $1,385,393 $1,050,197 75.8%Aetna Health Inc Co Corp 0 0 NMF $185,764 -$589,726 -317.5%Aetna Health Inc NMF $97,597 -$341,331 -349.7%

Total 662,180 7,719,537 $180.88 $1,396,318,408 $1,225,714,232 87.8%

Total commercial 5,861,346 70,505,758 $253.12 $17,846,689,599 $15,307,470,903 85.8%

Dental

Aetna Life Insurance Co 3,663,040 46,566,632 $24.15 $1,124,791,995 $884,211,265 78.6%

Aetna Dental Inc 323,044 5,461,053 $11.40 $62,282,437 $33,973,817 54.5%Aetna Dental Inc NJ Corp 188,492 2,306,247 $5.21 $12,004,344 $10,032,964 83.6%

Aetna Health Inc PA Corp 52,102 636,445 $18.54 $11,799,092 $8,952,607 75.9%

Aetna Health Inc GA Corp 52,043 650,112 $4.60 $2,988,430 $1,297,891 43.4%

Total 4,278,721 55,620,489 $21.82 $1,213,866,298 $938,468,544 77.3%

Stop loss

Aetna Life Insurance Co 1,986,724 23,840,638 $18.91 $450,814,679 $300,461,506 66.6%

Total 1,986,724 23,840,638 $18.91 $450,814,679 $300,461,506 66.6%

Accident only

Aetna Life Insurance Co. 2,992,694 35,912,328 $2.00 $71,661,493 $34,001,805 47.4%

Total 2,992,694 35,912,328 $2.00 $71,661,493 $34,001,805 47.4%

Disability (Short-term)

Aetna Life Insurance Co. 631,279 8,039,019 $17.73 $142,552,798 $107,230,113 75.2%

Total 631,279 8,039,019 $17.73 $142,552,798 $107,230,113 75.2%

Disability (Long-term)

Aetna Life Insurance Co. 2,098,325 26,137,603 $16.15 $422,052,098 $406,685,955 96.4%

Total 2,098,325 26,137,603 $16.15 $422,052,098 $406,685,955 96.4%

Long-term Care

Aetna Life Insurance Co. 76,413 1,071,357 -$16.03 -$17,177,220 -$29,806,900 173.5%

Other group care

Total Specialty $2,283,770,146 $1,757,041,023 76.9%

Overall $20,130,459,745 $17,064,511,926 84.8% Source: Company reports and Oppenheimer & Co. analysis.

HEALTHCAR

8/8/2019 May 2010 Oppenheimer Report

http://slidepdf.com/reader/full/may-2010-oppenheimer-report 18/41

18

The scenario analysis of what Aetna’s rebates would have been had the minimum medica

loss ratio requirements been in effect in 2009 is shown below. If the company could have

shifted 500 basis points of SG&A into the MLR, Aetna would have paid a rebate of $33

million under the new laws laid out in reform. Again, keep in mind that we aren’t giving

any credit to plans for their ability to reduce broker commissions or eliminate other non-

essential SG&A.

Exhibit 15: Aetna’s Potential Rebates In 2009, a Scenario Analysis, Assuming Various SG&A / Premium

Tax Shift to Medical ExpensePlan No Shift 100 bp 200 bp 300 bp 400 bp 500 bp 600 bp 700 bp

Individual $69,799,536 $60,114,428 $50,492,519 $42,071,704 $34,404,131 $27,204,690 $20,005,249 $12,805,808Small Group $20,391,865 $11,569,933 $7,381,146 $5,946,412 $5,191,901 $4,773,353 $4,354,804 $4,018,084

Large Group $52,792,343 $30,292,352 $8,738,438 $2,319,473 $2,054,193 $1,788,913 $1,523,633 $1,258,352

Total $142,983,744 $101,976,713 $66,612,103 $50,337,590 $41,650,225 $33,766,955 $25,883,686 $18,082,244 Source: Company reports and Oppenheimer & Co. analysis.

In the case of Humana, we‘ve summarized the company’s 2009 results in Exhibit 16. We

were able to track down $6.1 billion of Humana’s commercial premiums. Humana had a

total of $6.2 billion in commercial premiums overall in 2009. Humana’s commercia

medical loss ratio appeared to be about 83.1% in the individual, small group and large

group segments, and the breakdown by product makes clear that loss ratios diffematerially by product, as Humana’s individual loss ratio was 68.1% for the subsidiaries we

analyzed, while its small group loss ratio was 80.0%, followed by a large group medica

loss ratio of 88.2%.

Exhibit 16: Humana Summary of 2009 Results by Product

Member Medical

Plan Lives Months PMPM Premiums Expense MLR

Individual 382,412 4,368,359 $138.52 $605,085,496 $412,170,572 68.1%

Small Group 565,372 7,105,633 $299.48 $2,127,994,874 $1,703,155,307 80.0%Large Group 783,031 9,934,372 $306.10 $3,040,915,262 $2,683,218,711 88.2%

Total 1,730,815 21,408,364 $269.71 $5,773,995,632 $4,798,544,590 83.1% Source: Company reports and Oppenheimer & Co. analysis.

Our analysis covered 382,000 individual lives for Humana during 2009. These individua

members generated $605 million in premiums in 2009, and an estimated medical loss

ratio of around 68.1%. From a statutory entity perspective, even if Humana was able to

shift 500 basis points into its MLR, the company would have still incurred an individua

rebate in excess of $43 million in 2009, or $0.16 per share. Looking at the data, it appears

that Humana’s top subsidiary is extremely profitable. Humana Insurance Co. accounts fo

about 63% of the company’s individual premiums, and had a loss ratio of 68% during

2009, well below the threshold of 80% that will go into effect on January 1, 2011.

HEALTHCARE

8/8/2019 May 2010 Oppenheimer Report

http://slidepdf.com/reader/full/may-2010-oppenheimer-report 19/41

Exhibit 17: Humana Individual Results by Statutory Entity, 2009

Member Medical

Individual Lives Months PMPM Premiums Expenses ML

Humana Ins Co 241,548 2,745,342 $139.06 $381,766,173 $258,694,277 67.8%

Humana Health Insurance Co of FL Inc 81,609 950,649 $155.76 $148,076,760 $99,128,434 66.9%

Humana Health Benefit Plan of LA Inc 12,426 151,829 $193.15 $29,325,146 $21,756,956 74.2%Humana Health Plan Inc 18,269 234,806 $113.93 $26,752,412 $19,080,906 71.3%Humana Employers Health Plan GA Inc 13,467 133,827 $107.32 $14,361,935 $7,789,928 54.2%

Humana Medical Plan Inc 185 2,061 $749.74 $1,545,223 $2,005,235 129.8%

Humana Health Plan of Ohio Inc 102 1,257 $560.52 $704,573 $1,321,329 187.5%Humana Ins Co of KY 19 272 $775.33 $210,891 $425,572 201.8%

Humana Health Plan of TX Inc 3 36 $1,036.44 $37,312 $3,983 10.7%

Humana WI Health Org Ins Corp 1 12 $2,260.83 $27,130 $35,357 130.3%

Total 367,629 4,220,091 $142.84 $602,807,555 $410,241,977 68.1

Other Individual Business

Denticare Inc 11,879 111,894 $10.83 $1,212,078 $828,586 68.4%

Kanawha Insurance Co 2,904 36,374 $29.30 $1,065,863 $1,100,009 103.2%

Total 14,783 148,268 $15.36 $2,277,941 $1,928,595 84.7

Source: Company reports and Oppenheimer & Co. analysis.

Looking at Humana’s small group business, the loss ratio for was just above the 80%threshold, but there are variations among the subsidiaries. Humana Health Plan of Texas

had $170 million in premiums, and a loss ratio of just 70%. Humana Insurance, however

the company’s largest small group subsidiary, had a loss ratio of 81.8 %, in excess of the

threshold.

Exhibit 18: Humana Small Group Results by Statutory Entity, 2009

Member $0.63 Medical

Individual Lives Months PMPM Premiums Expenses MLR

Small Group

Humana Ins Co 274,794 3,495,719 $333.58 $1,166,114,745 $953,634,043 81.8%Humana Health Plan Inc 87,060 1,113,114 $247.00 $274,938,069 $215,948,938 78.5%

Humana Health Plan of TX Inc 64,102 722,875 $235.39 $170,154,160 $119,800,579 70.4%Humana Medical Plan Inc 33,593 444,590 $322.26 $143,274,983 $128,260,392 89.5%Humana Employers Health Plan GA Inc 36,090 417,333 $247.64 $103,347,153 $65,702,968 63.6%Humana Health Plan of Ohio Inc 26,583 330,723 $232.16 $76,782,133 $60,257,676 78.5%Humana Health Benefit Plan of LA Inc 15,934 194,180 $300.04 $58,262,229 $47,979,729 82.4%Humana WI Health Org Ins Corp 12,289 158,985 $283.65 $45,096,516 $39,366,948 87.3%Humana Health Insurance Co of FL Inc 3,613 56,264 $607.08 $34,156,913 $28,126,378 82.3%Cariten Insurance Co 5,898 85,277 $328.17 $27,985,336 $21,436,930 76.6%

Cariten Health Plan Inc 4,428 54,969 $277.05 $15,229,259 $11,891,238 78.1%Humana Benefit Plan of IL Inc 656 26,245 $409.96 $10,759,437 $9,469,621 88.0%Emphesys Ins Co 308 5,058 $281.26 $1,422,636 $915,647 64.4%Humana Ins Co of KY 24 301 $1,565.80 $471,305 $364,220 77.3%

Total 565,372 7,105,633 $299.48 $2,127,994,874 $1,703,155,307 80.0%

Association / Trust

Humana Medical Plan Inc 1,267 14,037 $316.95 $4,449,006 $4,475,098 100.6%Humana Ins Co 607 11,338 $174.33 $1,976,593 $1,988,618 100.6%Humana Health Insurance Co of FL Inc 438 5,023 $379.57 $1,906,598 $2,205,519 115.7%

Total 2,312 30,398 $274.10 $8,332,197 $8,669,235 104.0% Source: Company reports and Oppenheimer & Co. analysis.

HEALTHCAR

8/8/2019 May 2010 Oppenheimer Report

http://slidepdf.com/reader/full/may-2010-oppenheimer-report 20/41

20

Exhibit 19: Humana Large Group Results by Statutory Entity, 2009

Member $0.63 Medical

Individual Lives Months PMPM Premiums Expenses MLR

Large Group

Humana Ins Co 196,947 2,547,320 $316.28 $805,659,139 $751,069,845 93.2%Humana Health Plan Inc 149,470 2,005,040 $269.25 $539,847,414 $455,529,795 84.4%

Humana Medical Plan Inc 122,724 1,499,215 $328.39 $492,331,306 $441,341,813 89.6%Humana Health Plan of TX Inc 74,344 892,627 $235.10 $209,853,398 $173,224,486 82.5%

Humana WI Health Org Ins Corp 41,980 503,069 $409.08 $205,795,583 $185,502,476 90.1%Humana Health Plan of Ohio Inc 61,402 783,067 $262.62 $205,647,272 $169,383,535 82.4%

Humana Health Benefit Plan of LA Inc 41,624 513,435 $350.59 $180,003,914 $155,701,196 86.5%Humana Benefit Plan of IL Inc 17,065 231,614 $455.71 $105,549,041 $95,606,760 90.6%

Humana Health Insurance Co of FL Inc 17,428 229,350 $444.06 $101,845,266 $90,992,981 89.3%Humana Employers Health Plan GA Inc 34,790 409,133 $247.67 $101,329,472 $83,749,959 82.7%Cariten Health Plan Inc 14,190 178,395 $288.07 $51,390,656 $43,732,755 85.1%Cariten Insurance Co 10,512 138,595 $288.56 $39,992,306 $35,491,144 88.7%

Humana Ins Co of KY 512 2,745 $491.10 $1,348,061 $1,838,565 136.4%Emphesys Ins Co 43 767 $420.38 $322,434 $53,401 16.6%

Total 783,031 9,934,372 $306.10 $3,040,915,262 $2,683,218,711 88.2%

Source: Company reports and Oppenheimer & Co. analysis.

HEALTHCARE

8/8/2019 May 2010 Oppenheimer Report

http://slidepdf.com/reader/full/may-2010-oppenheimer-report 21/41

Exhibit 20: Humana Other Results by Statutory Entity, 2009

Member MedicalIndividual Lives Months PMPM Premiums Expenses MLR

Medicare Supplement

Humana Ins Co 26,153 266,512 $150.85 $40,203,673 $35,524,918 88.4%Kanawha Insurance Co 1,276 18,021 $252.47 $4,549,842 $3,108,211 68.3%

Humana Ins Co of KY 1,646 16,779 $145.95 $2,448,835 $2,135,338 87.2%Humana Health Benefit Plan of LA Inc 525 6,060 $204.55 $1,239,566 $981,575 79.2%

Humana Health Insurance Co of FL Inc 279 3,348 $67.52 $226,058 $183,870 81.3%Humana Ins Co of NY 111 522 $180.82 $94,386 $105,294 111.6%Humana Health Plan Inc 2 33 $279.76 $9,232 $3,512 38.0%

Total 29,992 311,275 $156.68 $48,771,592 $42,042,718 86.2%

Limited Benefit

Compbenefits - Group 1,661,122 19,933,969 $2.05 $40,879,398 $39,090,817 95.6%Compbenefits Ins Co 425,206 5,297,032 $6.93 $36,715,650 $22,725,506 61.9%

The Dental Concern Inc 86,495 768,081 $7.47 $5,738,605 $4,148,998 72.3%Humana Ins Co 63,809 814 $3,882.34 $3,160,227 $1,855,962 58.7%Kanawha Insurance Co 7,886 89,010 $15.92 $1,417,405 $523,851 37.0%

Humana Ins Co of KY 7,181 73,460 $4.80 $352,485 $290,436 82.4%Humana Health Benefit Plan of LA Inc 2,359 28,416 $6.17 $175,405 $60,219 34.3%Compbenefits - Individual 1,142 13,199 $8.82 $116,407 $394,479 338.9%

Total 2,255,200 26,203,981 $3.38 $88,555,582 $69,090,268 78.0%

FEHBP

Humana Health Plan Inc 22,987 279,855 $383.67 $107,371,182 $95,215,359 88.7%

Humana Health Plan of TX Inc 14,498 176,422 $380.45 $67,120,431 $63,556,336 94.7%Humana Medical Plan Inc 8,741 105,093 $327.65 $34,434,044 $32,607,236 94.7%Humana Ins Co 2,445 28,097 $337.88 $9,493,350 $8,052,174 84.8%Compbenefits Co 10,879 125,285 $65.03 $8,147,692 $3,527,951 43.3%Humana Health Plan of Ohio Inc 1,490 17,945 $246.86 $4,429,977 $7,526,320 169.9%Humana Employers Health Plan GA Inc 1,463 16,183 $255.23 $4,130,405 $4,154,708 100.6%

Compbenefits Dental Inc 17,684 199,777 $18.96 $3,788,475 $2,053,353 54.2%Denticare Inc 10,188 117,987 $19.65 $2,318,792 $649,262 28.0%Humana Benefit Plan of IL Inc 1,696 20,433 $94.25 $1,925,790 $1,960,980 101.8%

Humana Health Insurance Co of FL Inc 473 5,430 $304.15 $1,651,529 $2,652,141 160.6%

Humana Health Benefit Plan of LA Inc 260 3,056 $273.24 $835,020 $680,285 81.5%American Dental Plan of NC Inc 1,470 16,411 $28.40 $466,054 $268,913 57.7%

American Dental Providers of AR Inc 392 4,532 $24.27 $109,988 $50,705 46.1%

Total 94,666 1,116,506 $220.53 $246,222,729 $222,955,723 90.6%

Total commercial 1,843,002 22,718,275 $271.31 $6,163,599,791 $5,139,373,939 83.4%

Dental - Individual

Humanadental Ins Co 55,138 608,256 $28.70 $17,456,888 $10,709,198 61.3%Compbenefits Co 115,476 1,355,558 $7.29 $9,886,196 $9,145,069 92.5%Kanawha Insurance Co 5,770 72,258 $28.82 $2,082,451 $1,680,720 80.7%Compbenefits Dental Inc 16,734 179,066 $9.62 $1,722,599 $1,357,060 78.8%Denticare Inc 11,879 111,894 $10.83 $1,212,078 $828,586 68.4%

The Dental Concern Inc 3,571 38,970 $24.84 $967,981 $669,626 69.2%American Dental Plan of NC Inc 3,231 18,775 $15.02 $281,983 $282,129 100.1%American Dental Providers of AR Inc 176 2,269 $9.27 $21,044 $16,107 76.5%

Total 211,975 2,387,046 $14.09 $33,631,220 $24,688,495 73.4% Source: Company reports and Oppenheimer & Co. analysis.

HEALTHCAR

8/8/2019 May 2010 Oppenheimer Report

http://slidepdf.com/reader/full/may-2010-oppenheimer-report 22/41

22

Exhibit 21: Humana Other Results by Statutory Entity, 2009

Member MedicalIndividual Lives Months PMPM Premiums Expenses MLR

Dental - Group

Humanadental Ins Co 859,894 10,246,458 $27.11 $277,759,322 $189,236,665 68.1%Compbenefits Ins Co 379,895 4,783,247 $18.94 $90,583,854 $67,675,258 74.7%Compbenefits Co 717,875 8,716,433 $7.94 $69,215,402 $43,155,028 62.3%

The Dental Concern Inc 69,212 836,970 $18.79 $15,726,808 $11,221,596 71.4%Denticare Inc 258,997 1,713,207 $8.93 $15,302,167 $9,886,861 64.6%

Compbenefits Dental Inc 78,478 934,103 $11.14 $10,408,707 $7,638,917 73.4%Kanawha Insurance Co 11,480 137,760 $27.22 $3,750,486 $2,905,552 77.5%Humana Ins Co of KY 8,691 111,171 $19.68 $2,187,725 $1,147,161 52.4%

Dental Concern Ltd 3,455 45,288 $15.54 $703,671 $412,324 58.6%Humana Ins Co 47 581,085 $0.10 $58,442 $542,433 928.2%

American Dental Plan of NC Inc 417 5,197 $10.24 $53,197 $46,028 86.5%American Dental Providers of AR Inc 225 2,679 $11.76 $31,508 $27,295 86.6%

Total 2,388,666 28,113,598 $17.28 $485,781,289 $333,895,118 68.7%

382,412 605,085,496 412,170,572 68.1%Stop loss

Humana Ins Co 216,320 2,595,840 $19.97 $51,826,657 $43,784,443 84.5%Kanawha Insurance Co 324,289 1,618,446 $21.02 $34,022,115 $30,365,669 89.3%Humana Ins Co of KY 111,821 1,341,852 $9.23 $12,386,878 $11,468,555 92.6%

Humana Health Insurance Co of FL Inc $3,897,966 $3,494,612 89.7%

Humana Health Benefit Plan of LA Inc $1,478,340 $1,170,262 79.2%Total 111,821 1,341,852 $77.22 $103,611,956 $90,283,541 87.1%

Specified Disease

Kanawha Insurance Co (Individual) 72,386 828,813 $14.74 $12,218,501 $12,349,672 101.1%Kanawha Insurance Co (Group) 18,308 181,695 $4.99 $906,731 $94,749 10.4%

Total 90,694 1,010,508 $12.99 $13,125,232 $12,444,421 94.8%

Accident only

Humana Ins Co 435 1,201 $2,816.04 $3,382,068 $671,600 19.9%Kanawha Insurance Co 16,741 162,425 $14.35 $2,330,613 $703,437 30.2%

Kanawha Insurance Co (Group) 16,945 20,827 $33.60 $699,883 $81,682 11.7%Humana Ins Co of KY 0 0 NMF $293,234 $1,791,151 610.8%

Total 34,121 184,453 $36.36 $6,705,798 $3,247,870 48.4%

Disability (Short-term)

Kanawha Insurance Co (Individual) 36,381 431,482 $37.34 $16,113,659 $11,759,392 73.0%Kanawha Insurance Co (Group) 24,624 311,371 $20.40 $6,352,654 $3,553,914 55.9%Humana Ins Co 6,476 86,488 $22.04 $1,906,624 $604,284 31.7%

Humana Ins Co of KY 357 4,485 $24.76 $111,065 $36,845 33.2%

Total 67,838 833,826 $29.36 $24,484,002 $15,954,435 65.2%

Disability (Long-term)

Kanawha Insurance Co 36,971 443,654 $12.95 $5,745,459 $3,397,713 59.1%Humana Ins Co 4,035 48,420 $41.38 $2,003,550 $5,165,366 257.8%

Humanadental Ins Co 161 1,932 $21.86 $42,229 $325,663 771.2%

Total 41,167 494,006 $15.77 $7,791,238 $8,888,742 114.1%

Long-term Care

Kanawha Insurance Co 36,243 437,802 $122.25 $53,519,513 $124,404,469 232.4%

Other group care

Kanawha Insurance Co 4,017 426,025 $0.33 $139,458 $1,425 1.0%

Total Specialty $731,067,647 $615,737,111 84.2%

Overall 6,894,667,438 5,755,111,050 83.5% Source: Company reports and Oppenheimer & Co. analysis.

HEALTHCARE

8/8/2019 May 2010 Oppenheimer Report

http://slidepdf.com/reader/full/may-2010-oppenheimer-report 23/41

In the next exhibit, we lay out a scenario analysis of what Humana’s rebates would have

been had the minimum medical loss ratio requirements been in effect in 2008, depending

on how much in SG&A / premium taxes plans are able to shift into medical costs. In

addition, we aren’t giving any credit to plans for their ability to reduce broker commissions

or eliminate other non-essential SG&A. Assuming a 500 basis points shift, Humana would

have incurred a hit of nearly $64 million.

Exhibit 22: Humana’s Potential Rebates in 2009, a Scenario Analysis, Assuming Various SG&A /

Premium Tax Shift to Medical ExpensePlan No Shift 100 bp 200 bp 300 bp 400 bp 500 bp 600 bp 700 bp

Individual $73,942,383 $67,927,065 $61,911,746 $55,896,428 $49,881,110 $43,865,792 $37,906,822 $32,184,755Small Group $39,945,845 $33,242,544 $28,416,516 $25,384,025 $22,523,007 $19,773,768 $17,024,528 $14,275,289Large Group $16,508,816 $7,996,783 $2,825,257 $210,995 $207,771 $204,546 $201,322 $198,098

Total $130,397,043 $109,166,392 $93,153,520 $81,491,449 $72,611,888 $63,844,106 $55,132,672 $46,658,141 Source: Company reports and Oppenheimer & Co. analysis.

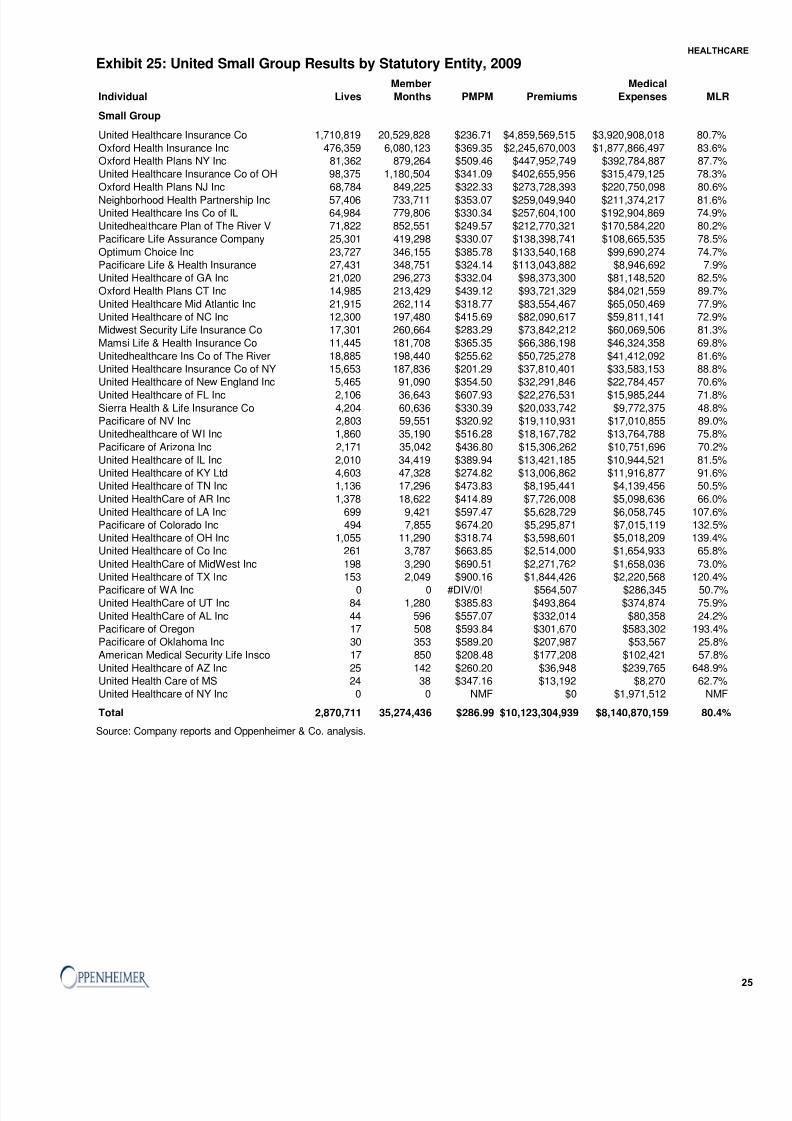

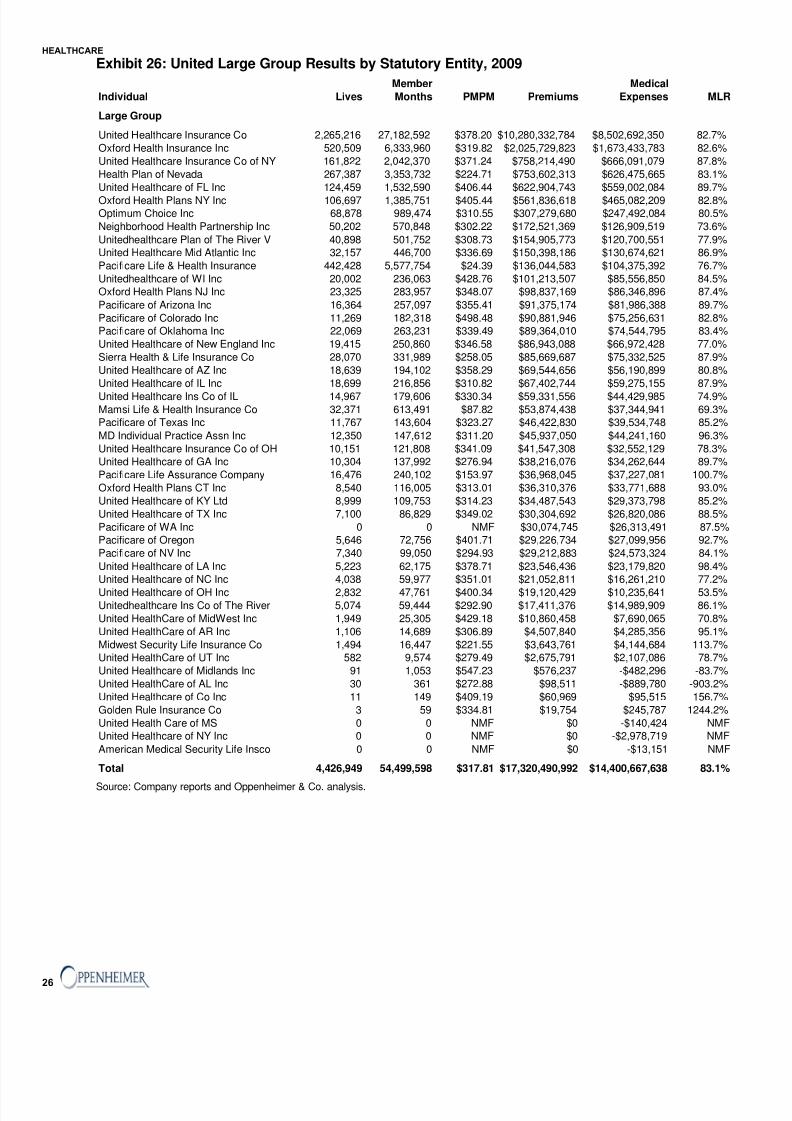

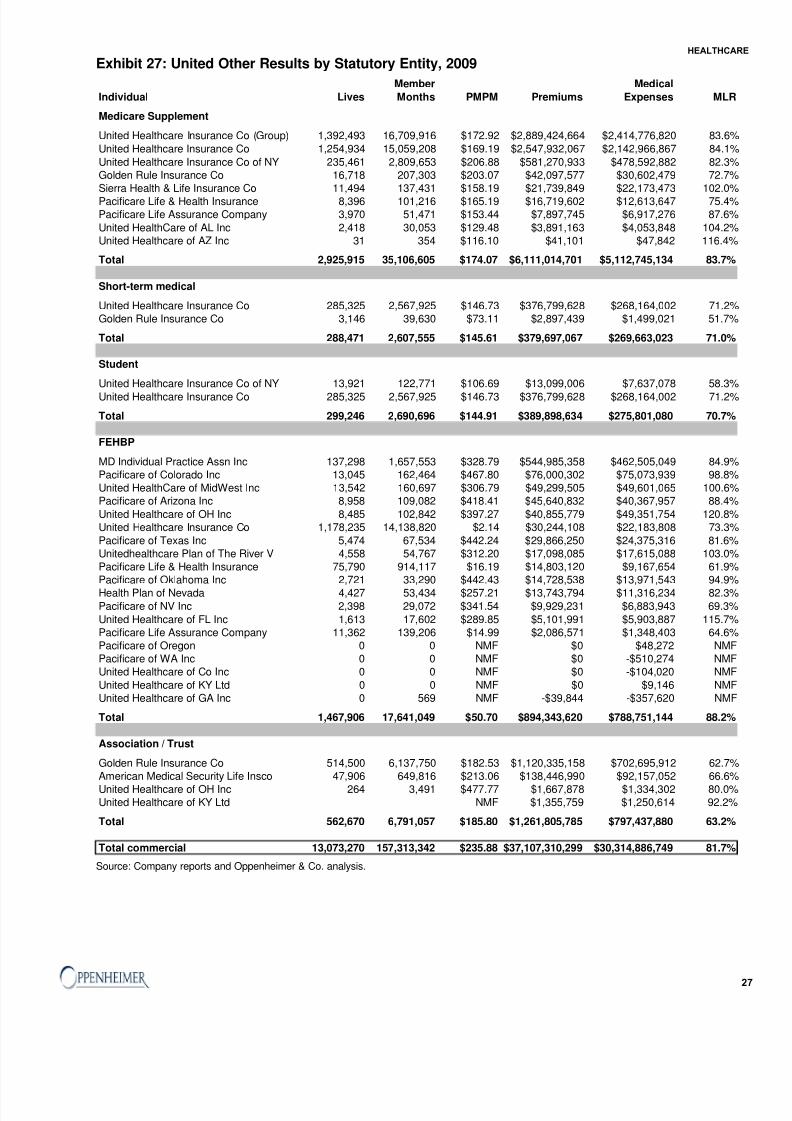

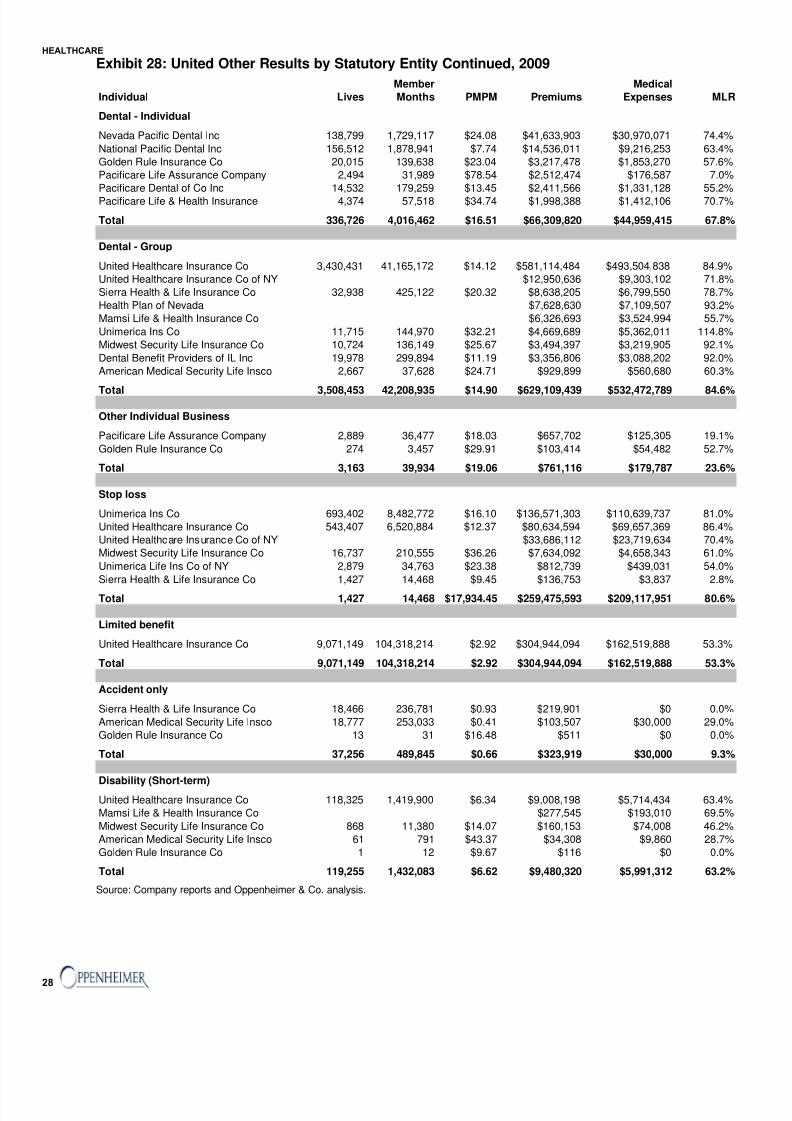

In Exhibit 23, we’ve summarized United’s results for 2009. We were able to account fo

$37 billion of the company’s commercial premiums. United’s overall commercial medica

loss ratio appeared to be about 81.4%, driven by an individual loss ratio of 70.2%, a smal

group loss ratio of 80.4%, and a large group medical loss ratio of 83.1%. That said

premiums for the individual represent just 5-6% of total commercial premiums, with largegroup accounting for the largest portion of the total revenue.

Exhibit 23: United Summary of 2009 Results by Product

Member Medical

Plan Lives Months PMPM Premiums Expense MLR

Individual 797,235 9,533,337 $198.18 $1,889,321,462 $1,326,568,358 70.2%

Small Group 2,870,711 35,274,436 $286.99 $10,123,304,939 $8,140,870,159 80.4%

Large Group 4,426,949 54,499,598 $317.81 $17,320,490,992 $14,400,667,638 83.1%

Total 8,094,895 99,307,371 $295.38 $29,333,117,393 $23,868,106,155 81.4% Source: Company reports and Oppenheimer & Co. analysis.

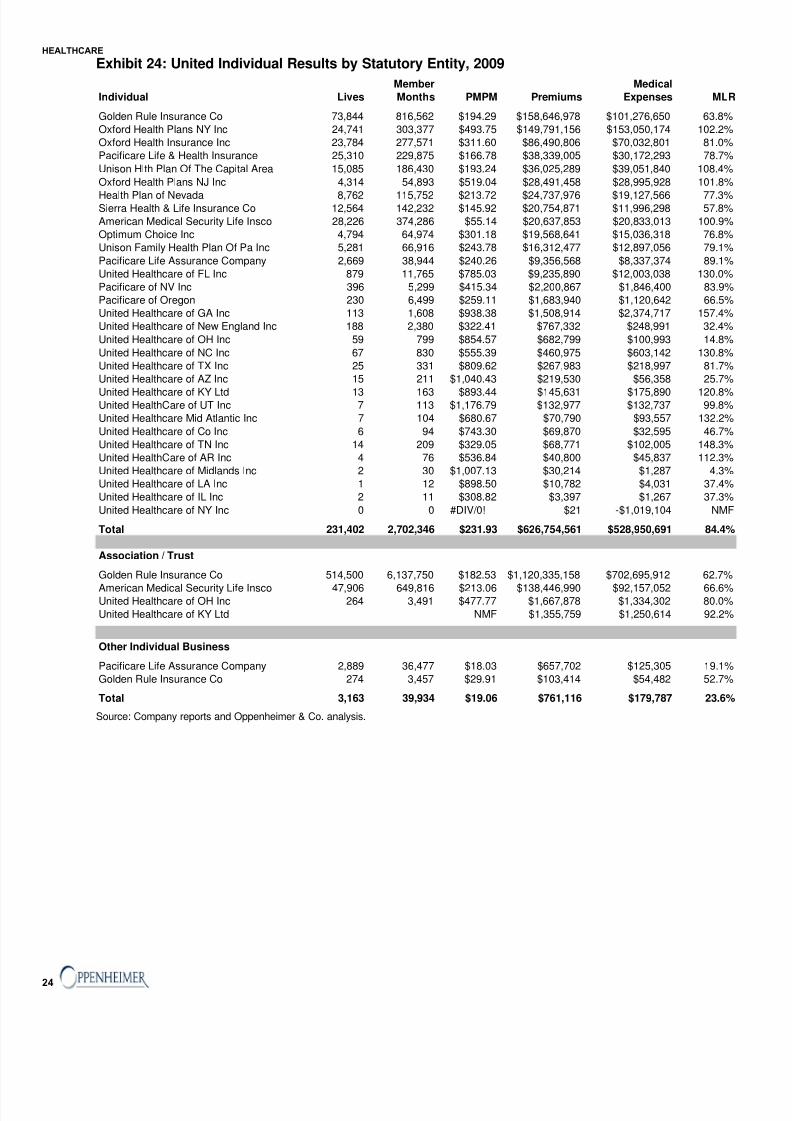

Our individual analysis shown below includes roughly 797,000 student health insurance

lives, along with the significant amount of business that Golden Rule writes through its

trust / association product. United’s individual product had a loss ratio of 70.2%

suggesting that even if United is able to shift significant SG&A to its medical expense, it

will still incur a large rebate. In particular, the company’s Golden Rule was quite profitable

in 2009.

HEALTHCAR

8/8/2019 May 2010 Oppenheimer Report

http://slidepdf.com/reader/full/may-2010-oppenheimer-report 24/41

24

Exhibit 24: United Individual Results by Statutory Entity, 2009

Member Medical

Individual Lives Months PMPM Premiums Expenses MLR

Golden Rule Insurance Co 73,844 816,562 $194.29 $158,646,978 $101,276,650 63.8%

Oxford Health Plans NY Inc 24,741 303,377 $493.75 $149,791,156 $153,050,174 102.2%

Oxford Health Insurance Inc 23,784 277,571 $311.60 $86,490,806 $70,032,801 81.0%

Pacificare Life & Health Insurance 25,310 229,875 $166.78 $38,339,005 $30,172,293 78.7%

Unison Hlth Plan Of The Capital Area 15,085 186,430 $193.24 $36,025,289 $39,051,840 108.4%

Oxford Health Plans NJ Inc 4,314 54,893 $519.04 $28,491,458 $28,995,928 101.8%

Health Plan of Nevada 8,762 115,752 $213.72 $24,737,976 $19,127,566 77.3%Sierra Health & Life Insurance Co 12,564 142,232 $145.92 $20,754,871 $11,996,298 57.8%

American Medical Security Life Insco 28,226 374,286 $55.14 $20,637,853 $20,833,013 100.9%

Optimum Choice Inc 4,794 64,974 $301.18 $19,568,641 $15,036,318 76.8%

Unison Family Health Plan Of Pa Inc 5,281 66,916 $243.78 $16,312,477 $12,897,056 79.1%

Pacificare Life Assurance Company 2,669 38,944 $240.26 $9,356,568 $8,337,374 89.1%

United Healthcare of FL Inc 879 11,765 $785.03 $9,235,890 $12,003,038 130.0%

Pacificare of NV Inc 396 5,299 $415.34 $2,200,867 $1,846,400 83.9%

Pacificare of Oregon 230 6,499 $259.11 $1,683,940 $1,120,642 66.5%

United Healthcare of GA Inc 113 1,608 $938.38 $1,508,914 $2,374,717 157.4%

United Healthcare of New England Inc 188 2,380 $322.41 $767,332 $248,991 32.4%

United Healthcare of OH Inc 59 799 $854.57 $682,799 $100,993 14.8%

United Healthcare of NC Inc 67 830 $555.39 $460,975 $603,142 130.8%

United Healthcare of TX Inc 25 331 $809.62 $267,983 $218,997 81.7%

United Healthcare of AZ Inc 15 211 $1,040.43 $219,530 $56,358 25.7%

United Healthcare of KY Ltd 13 163 $893.44 $145,631 $175,890 120.8%United HealthCare of UT Inc 7 113 $1,176.79 $132,977 $132,737 99.8%