Embed Size (px)

Citation preview

McGill University Pension PlanSettlement Options Information Session

The presentation can be accessed online at: http://www.mcgill.ca/hr/pensions/mupp/sessions .

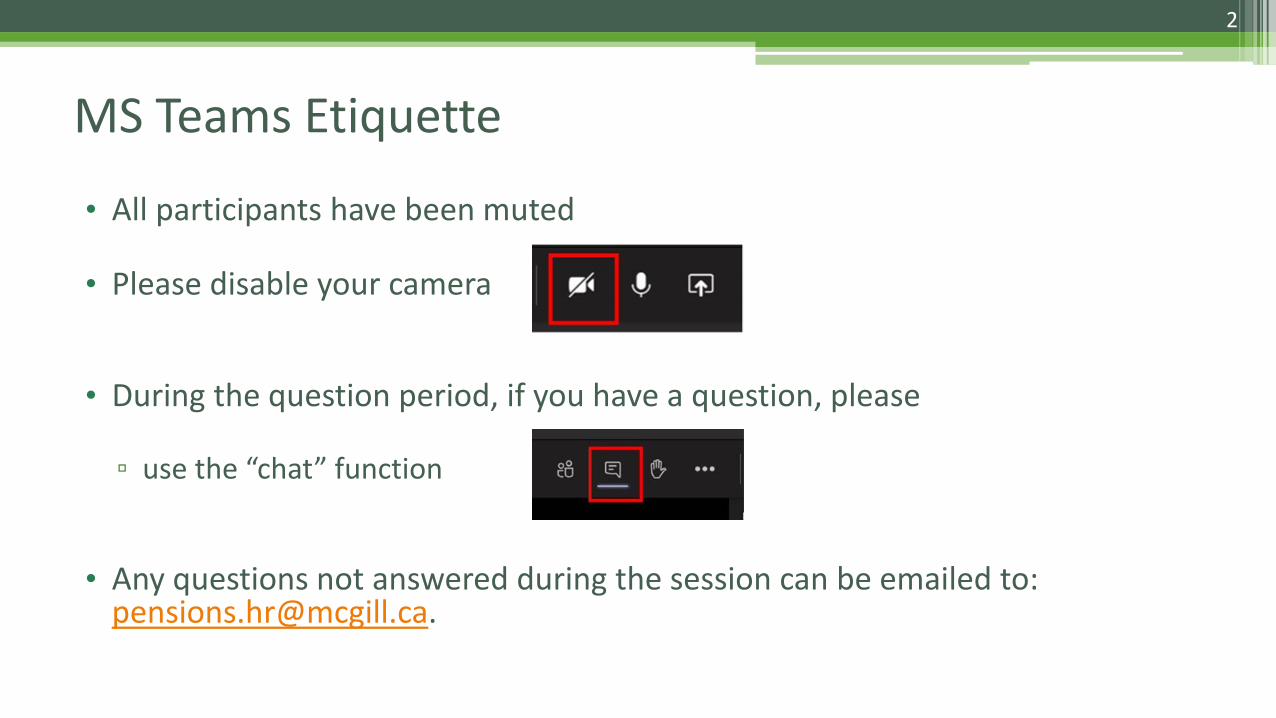

MS Teams Etiquette

• All participants have been muted

• Please disable your camera

• During the question period, if you have a question, please

▫ use the “chat” function

• Any questions not answered during the session can be emailed to: [email protected].

2

This presentation is intended to inform you about the McGill Pension Plan & the importance of integrating pension investment decisions to your financial management.

This is not financial advice & should not be taken as such. It is meant to alert you to the matters to look into.

Your individual needs & circumstances may not be adequately addressed by the info contained in this presentation.

3

Types of Pension Plans

• Pension is based on a formula tied to service & salary

Defined Benefit

• Retirement income is based on contributions, the investment return accumulated at retirement as well as market conditions

Defined Contribution

5

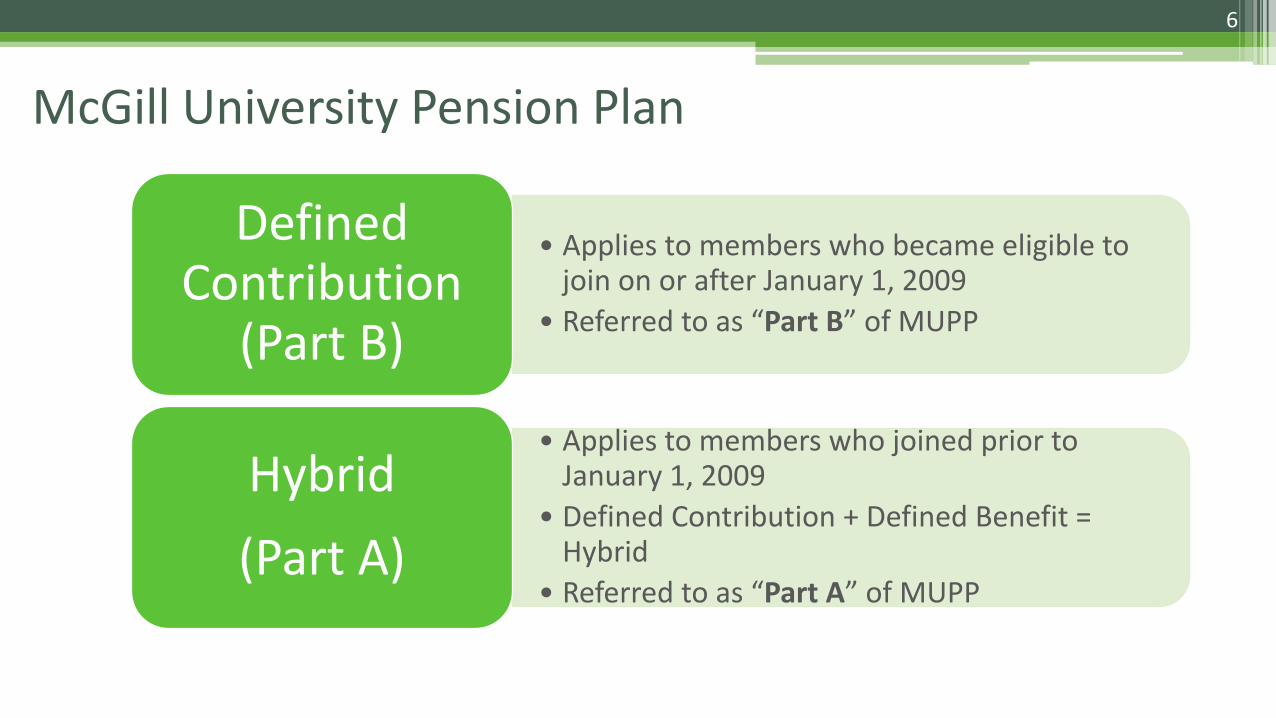

McGill University Pension Plan

• Applies to members who became eligible to join on or after January 1, 2009

• Referred to as “Part B” of MUPP

Defined Contribution

(Part B)

• Applies to members who joined prior to January 1, 2009

• Defined Contribution + Defined Benefit = Hybrid

• Referred to as “Part A” of MUPP

Hybrid(Part A)

6

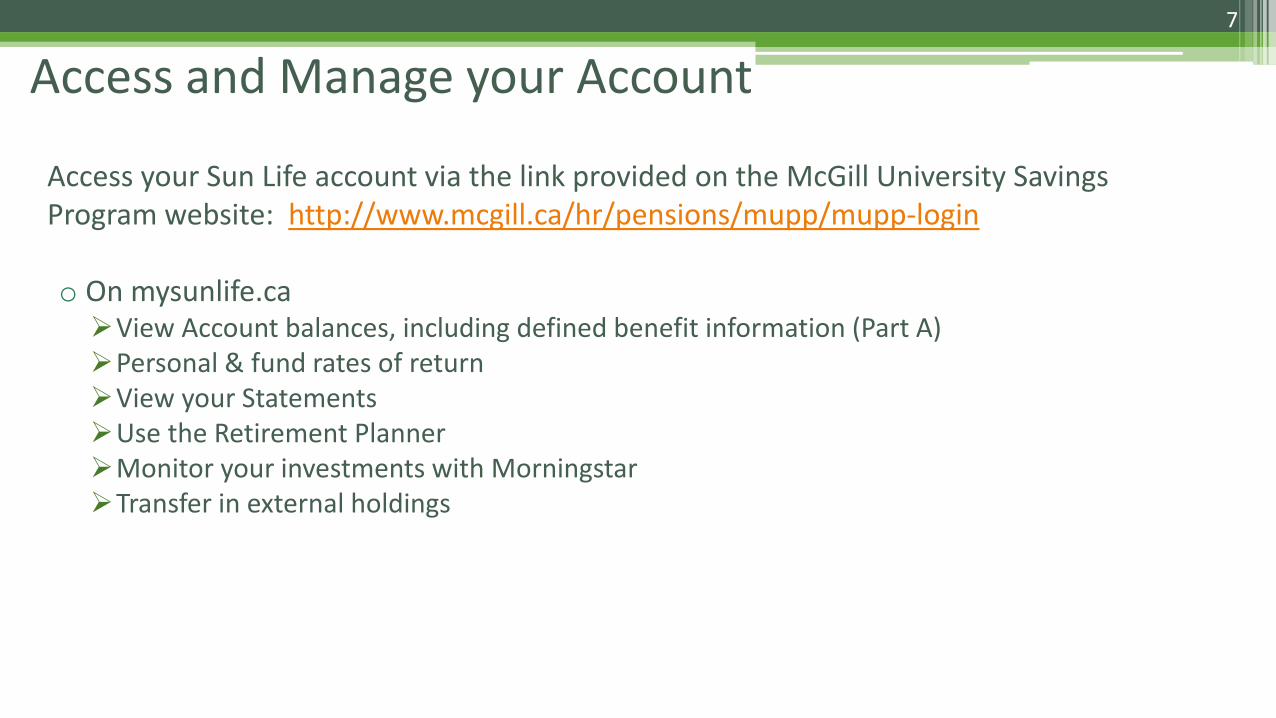

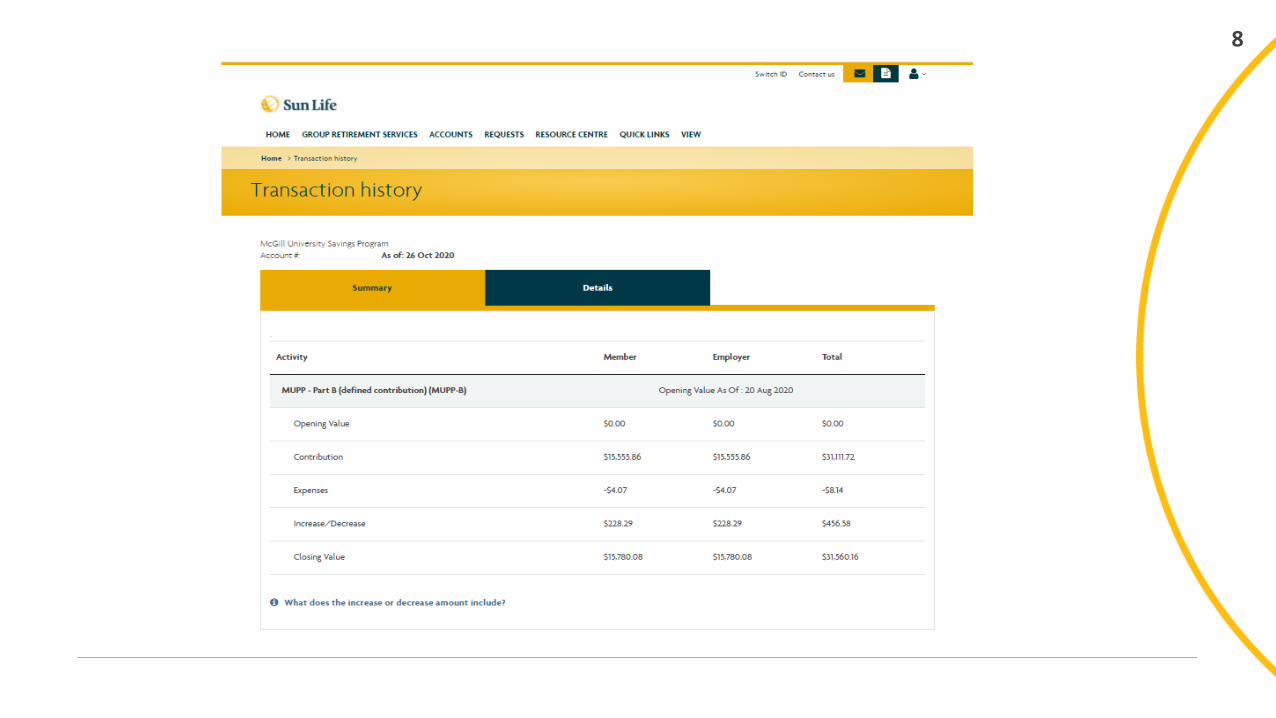

Access and Manage your Account

Access your Sun Life account via the link provided on the McGill University Savings Program website: http://www.mcgill.ca/hr/pensions/mupp/mupp-login

o On mysunlife.caView Account balances, including defined benefit information (Part A) Personal & fund rates of returnView your StatementsUse the Retirement Planner Monitor your investments with MorningstarTransfer in external holdings

7

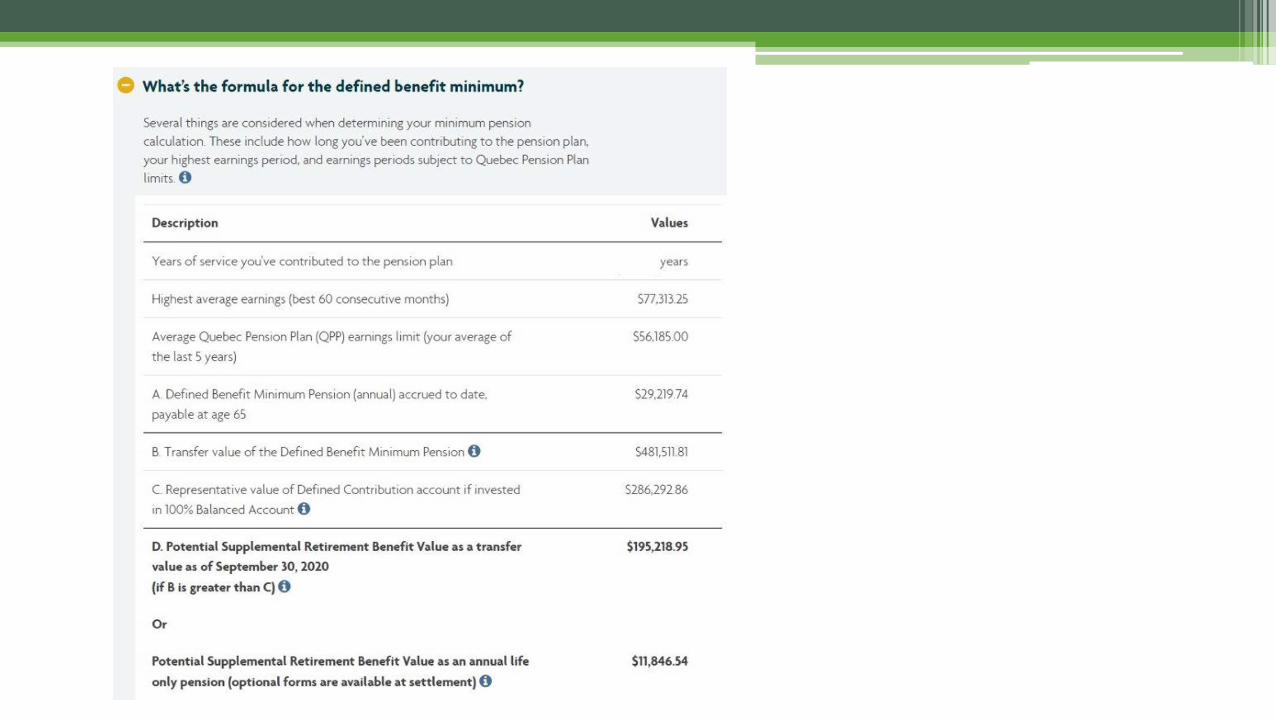

8

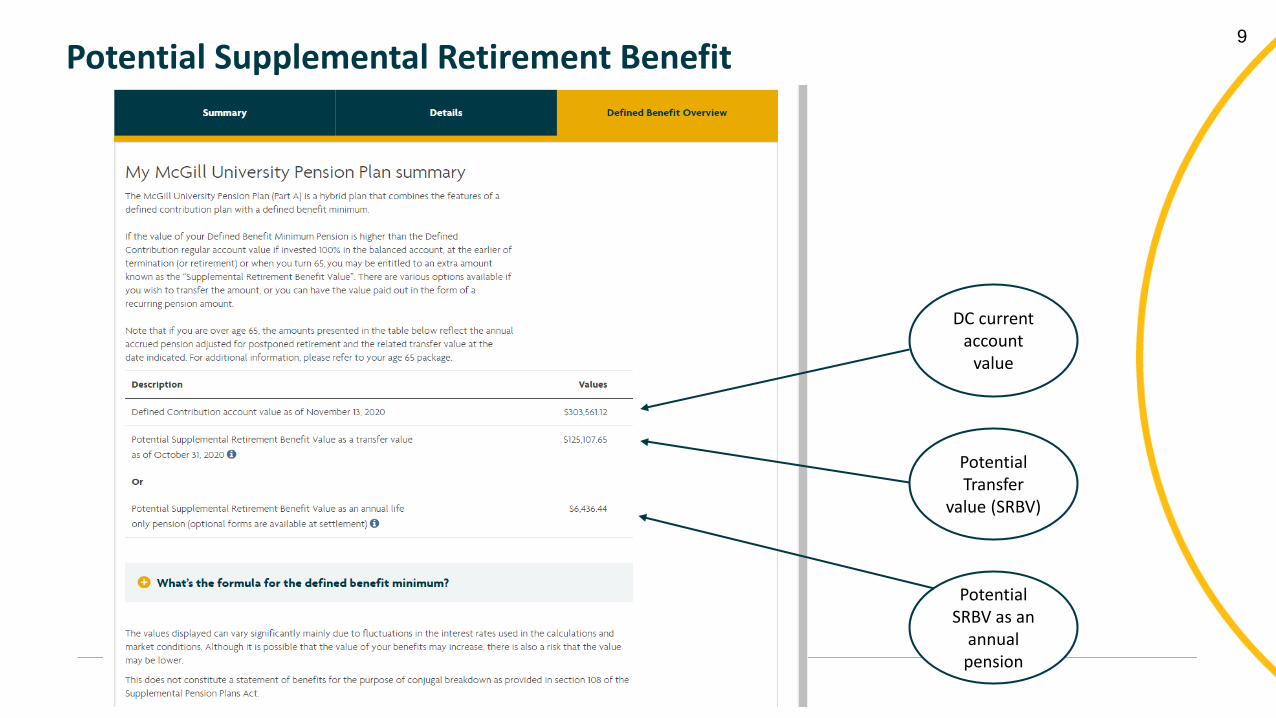

9

Potential SRBV as an

annual pension

Potential Transfer

value (SRBV)

DC current account

value

Potential Supplemental Retirement Benefit

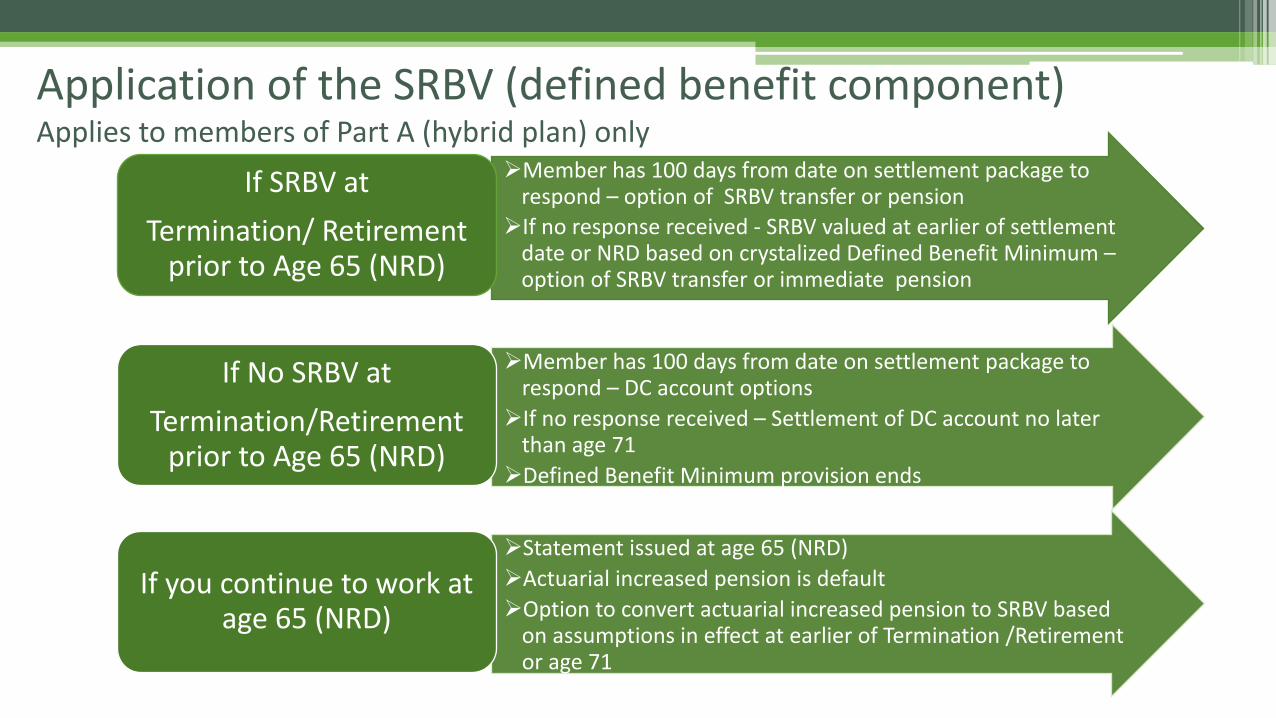

Member has 100 days from date on settlement package to respond – option of SRBV transfer or pensionIf no response received - SRBV valued at earlier of settlement

date or NRD based on crystalized Defined Benefit Minimum –option of SRBV transfer or immediate pension

If SRBV atTermination/ Retirement

prior to Age 65 (NRD)

Member has 100 days from date on settlement package to respond – DC account optionsIf no response received – Settlement of DC account no later

than age 71Defined Benefit Minimum provision ends

If No SRBV atTermination/Retirement

prior to Age 65 (NRD)

Statement issued at age 65 (NRD)Actuarial increased pension is defaultOption to convert actuarial increased pension to SRBV based

on assumptions in effect at earlier of Termination /Retirement or age 71

If you continue to work at age 65 (NRD)

Application of the SRBV (defined benefit component)Applies to members of Part A (hybrid plan) only

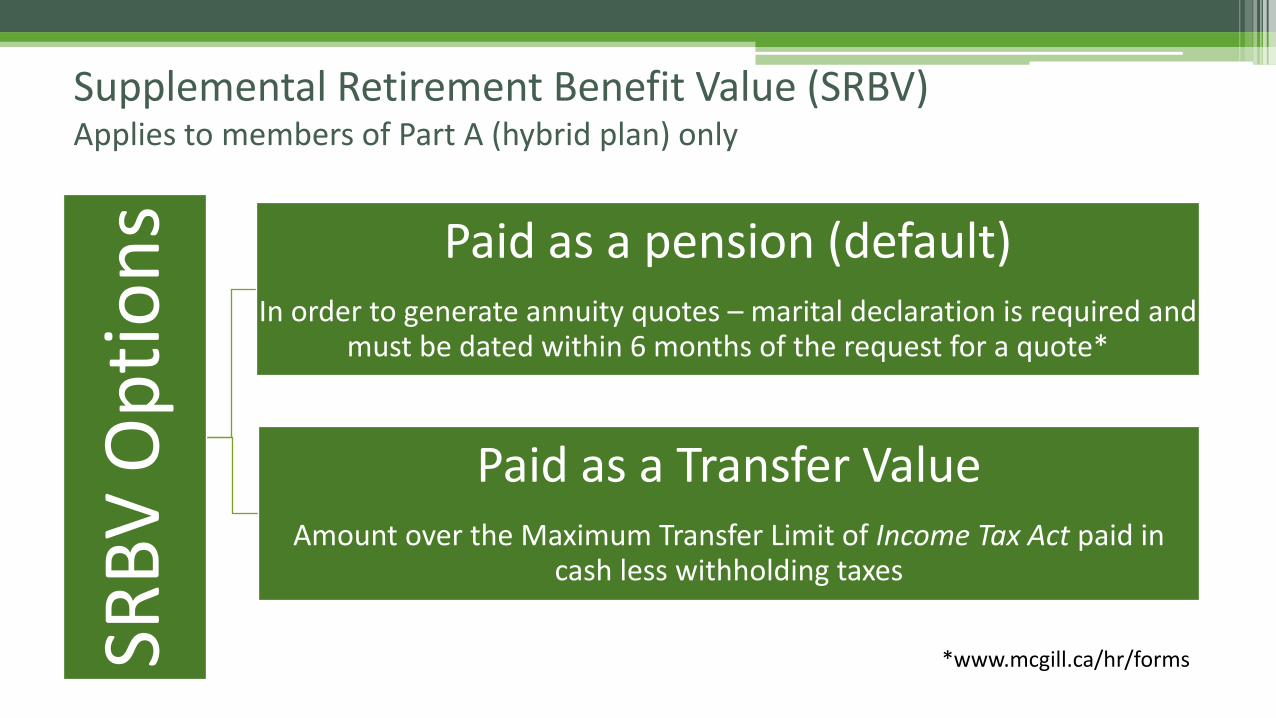

Supplemental Retirement Benefit Value (SRBV)Applies to members of Part A (hybrid plan) only

SRBV

Opt

ions

Paid as a Transfer ValueAmount over the Maximum Transfer Limit of Income Tax Act paid in

cash less withholding taxes

Paid as a pension (default)In order to generate annuity quotes – marital declaration is required and

must be dated within 6 months of the request for a quote*

*www.mcgill.ca/hr/forms

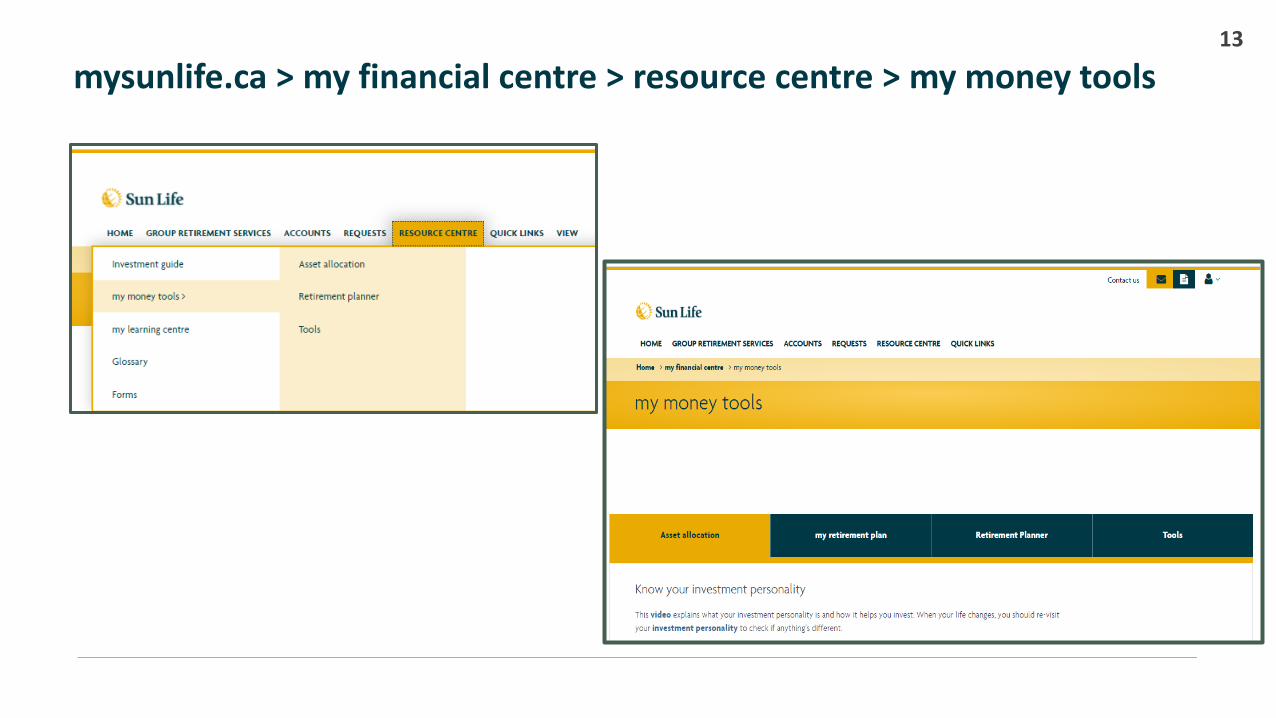

mysunlife.ca > my financial centre > resource centre > my money tools13

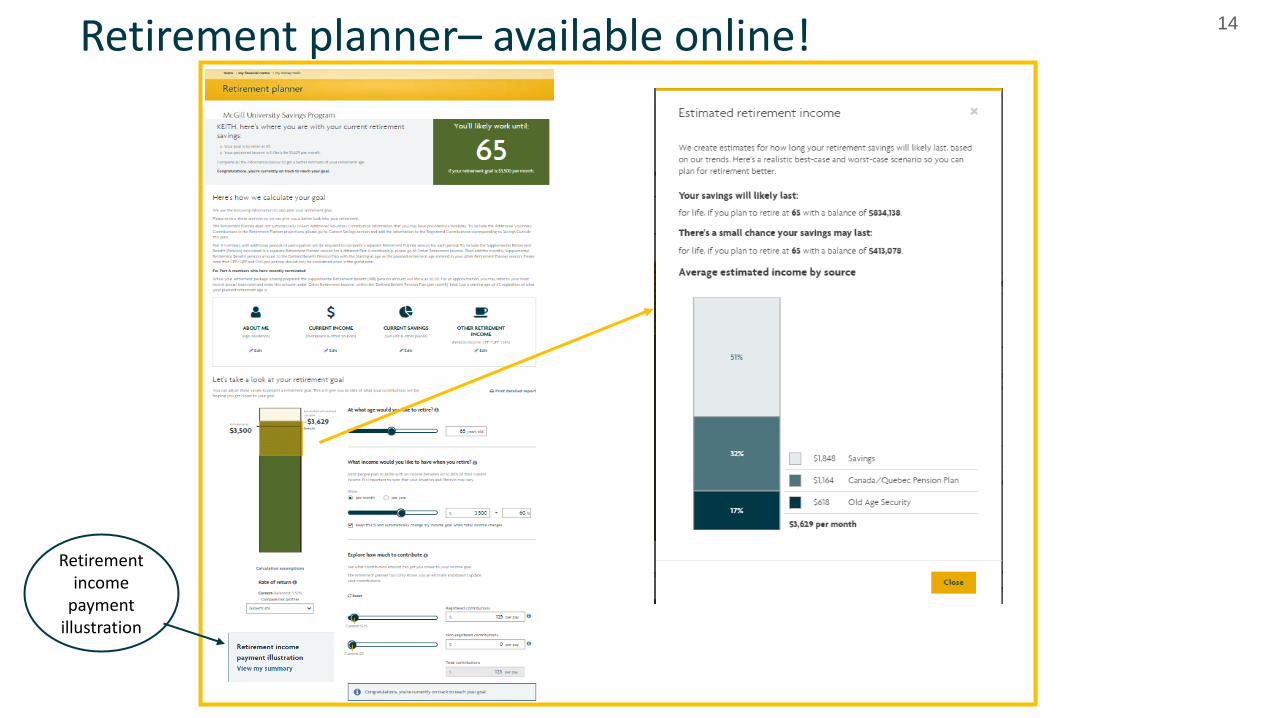

14Retirement planner– available online!

Retirement income

payment illustration

You can “retire” from the University without having to settle your MUPP holdings = deferred settlement

Ability to settle MUPP holdings:• Earliest of termination, retirement or if you continue to

work, the year in which you turn age 71 or• Latest: December 31st of the year in which you turn 71.

15

Retirement vs. Settlement

New Retirement/Termination: Statement and settlement package forwarded to you following notification of your retirement by your department via Workday and remittance of final pension contributions.

Previous Retirement/Termination or Members who turn age 71: Contact the Call Centre for the McGill University Savings Programs at 1-888-444-2023 to request a settlement package.

Settlement transactions: valued on 15th or last business day of the month.

16

How do I request settlement?

Please ask any questions you may have by “using the chat”

Any questions not answered during the session can be emailed to: [email protected].

18

A brief overview of settlement options. For more information, please sign up for a “Settlement Option Information Session”.

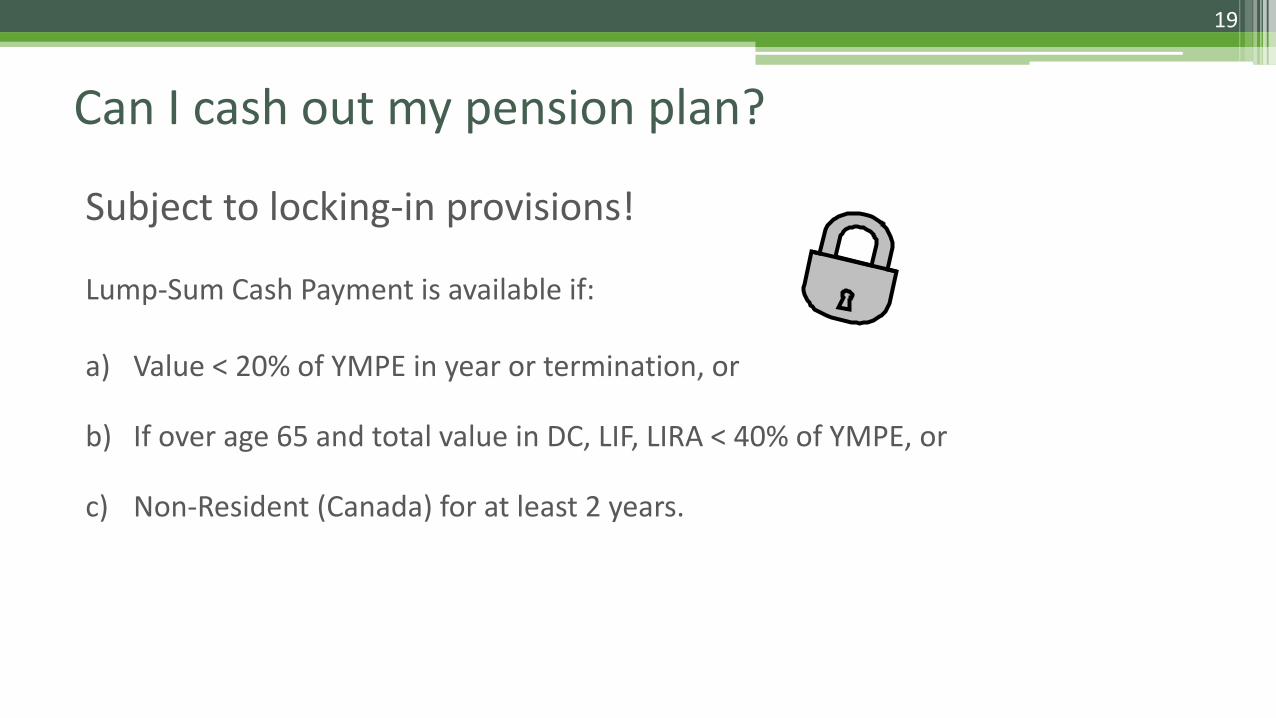

Subject to locking-in provisions!

Lump-Sum Cash Payment is available if:

a) Value < 20% of YMPE in year or termination, or

b) If over age 65 and total value in DC, LIF, LIRA < 40% of YMPE, or

c) Non-Resident (Canada) for at least 2 years.

19

Can I cash out my pension plan?

20

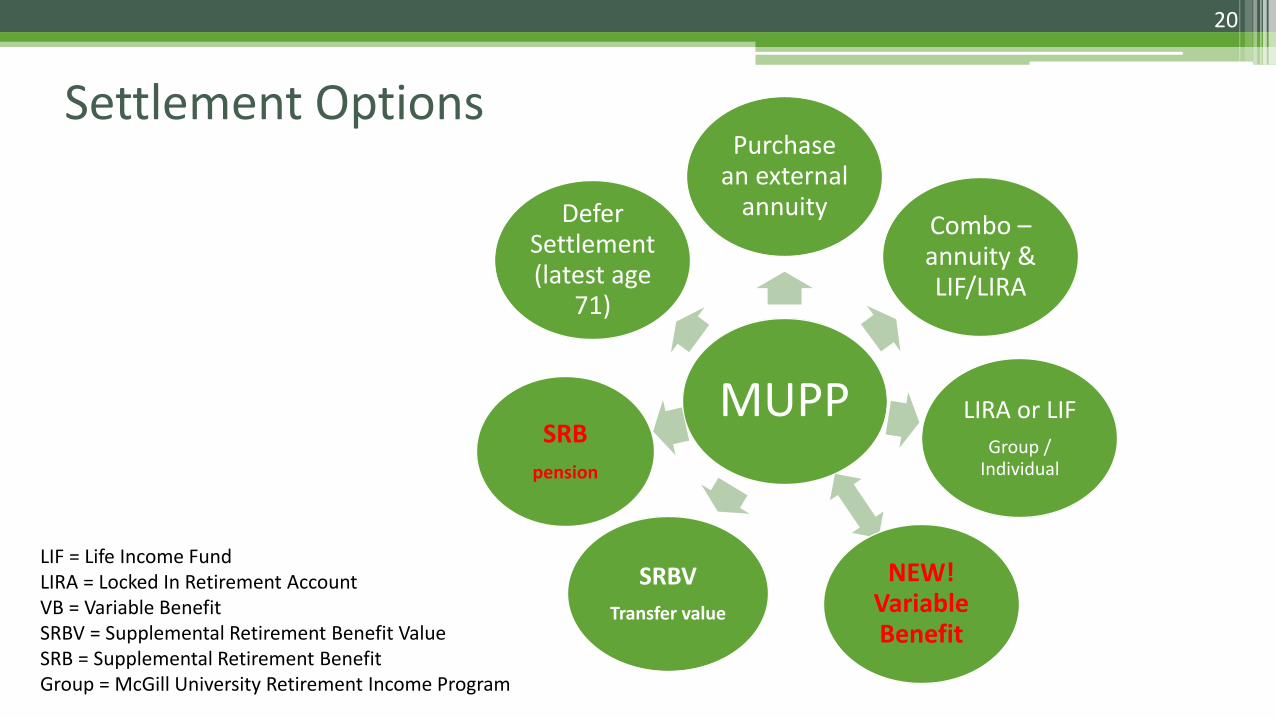

MUPP

Purchase an external

annuityCombo –annuity & LIF/LIRA

LIRA or LIFGroup /

Individual

NEW! Variable Benefit

SRBVTransfer value

SRB pension

Defer Settlement (latest age

71)

Settlement Options

LIF = Life Income FundLIRA = Locked In Retirement AccountVB = Variable BenefitSRBV = Supplemental Retirement Benefit ValueSRB = Supplemental Retirement BenefitGroup = McGill University Retirement Income Program

21

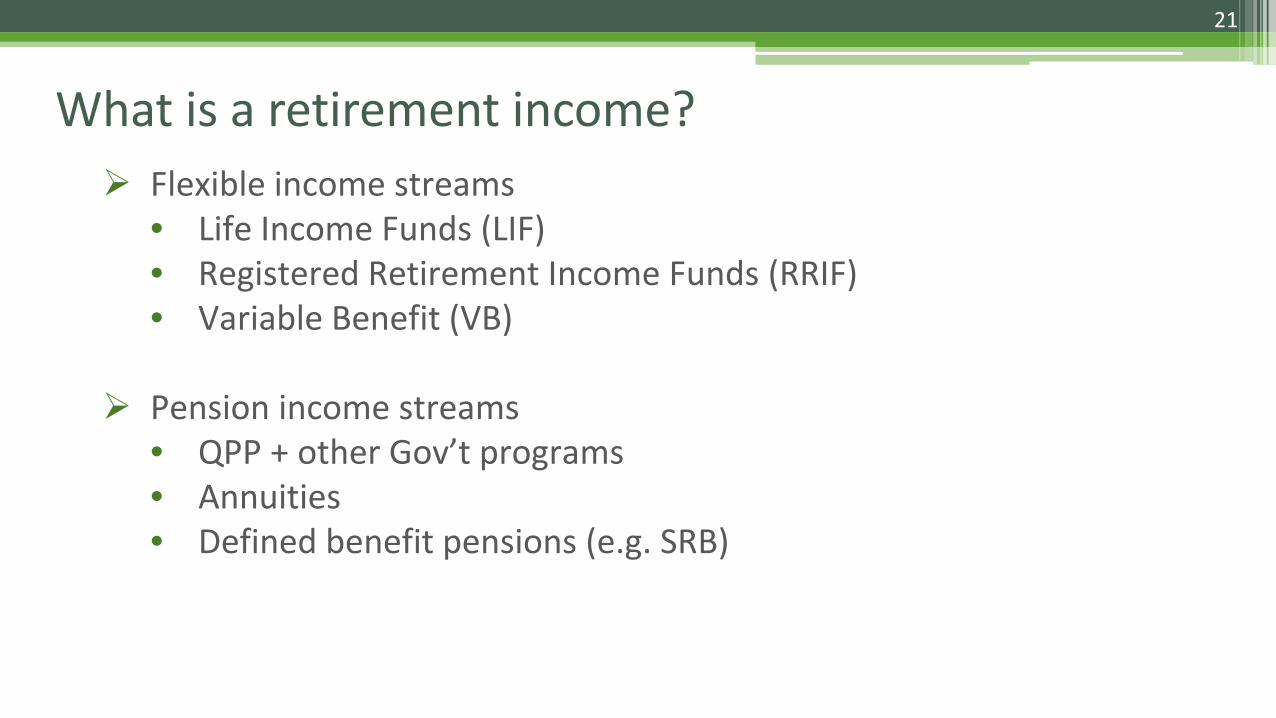

Flexible income streams • Life Income Funds (LIF)• Registered Retirement Income Funds (RRIF)• Variable Benefit (VB)

Pension income streams • QPP + other Gov’t programs• Annuities• Defined benefit pensions (e.g. SRB)

What is a retirement income?

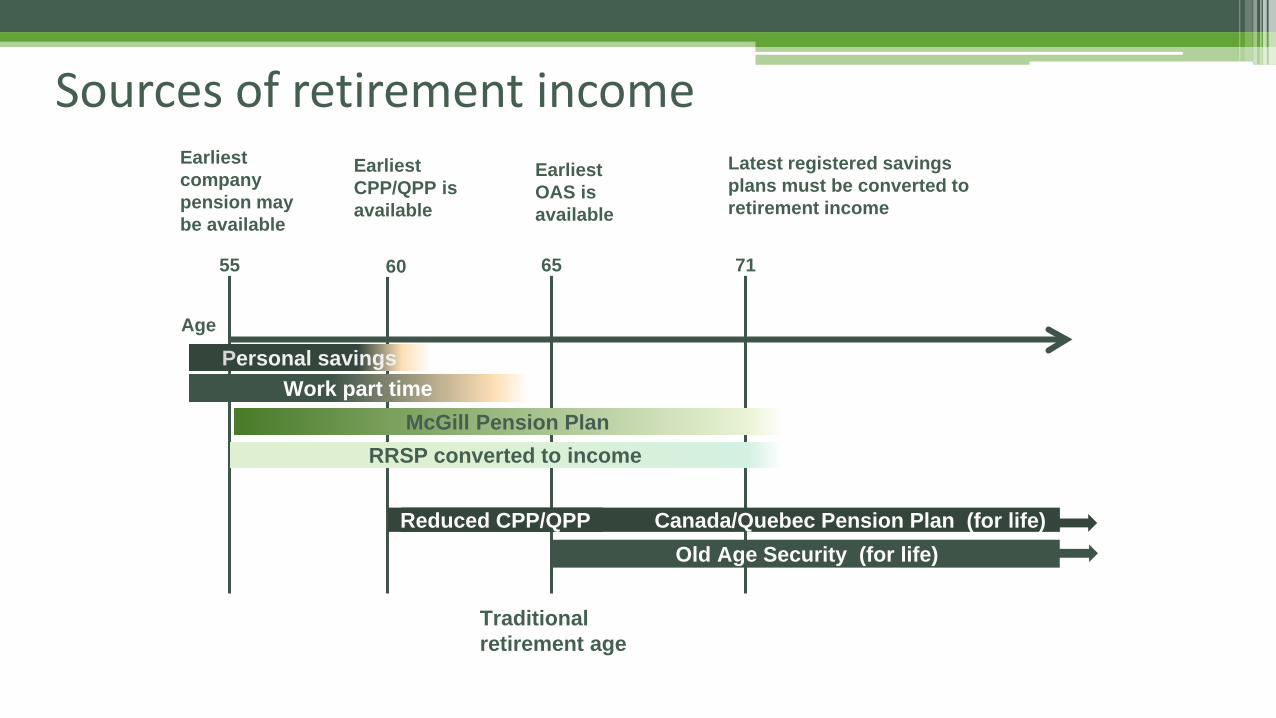

Age

55 60 65 71

Earliest company pension may be available

Earliest CPP/QPP is available

Traditional retirement age

Earliest OAS is available

Latest registered savings plans must be converted to retirement income

Personal savingsWork part time

McGill Pension PlanRRSP converted to income

Old Age Security (for life)Canada/Quebec Pension Plan (for life)Reduced CPP/QPP

Sources of retirement income

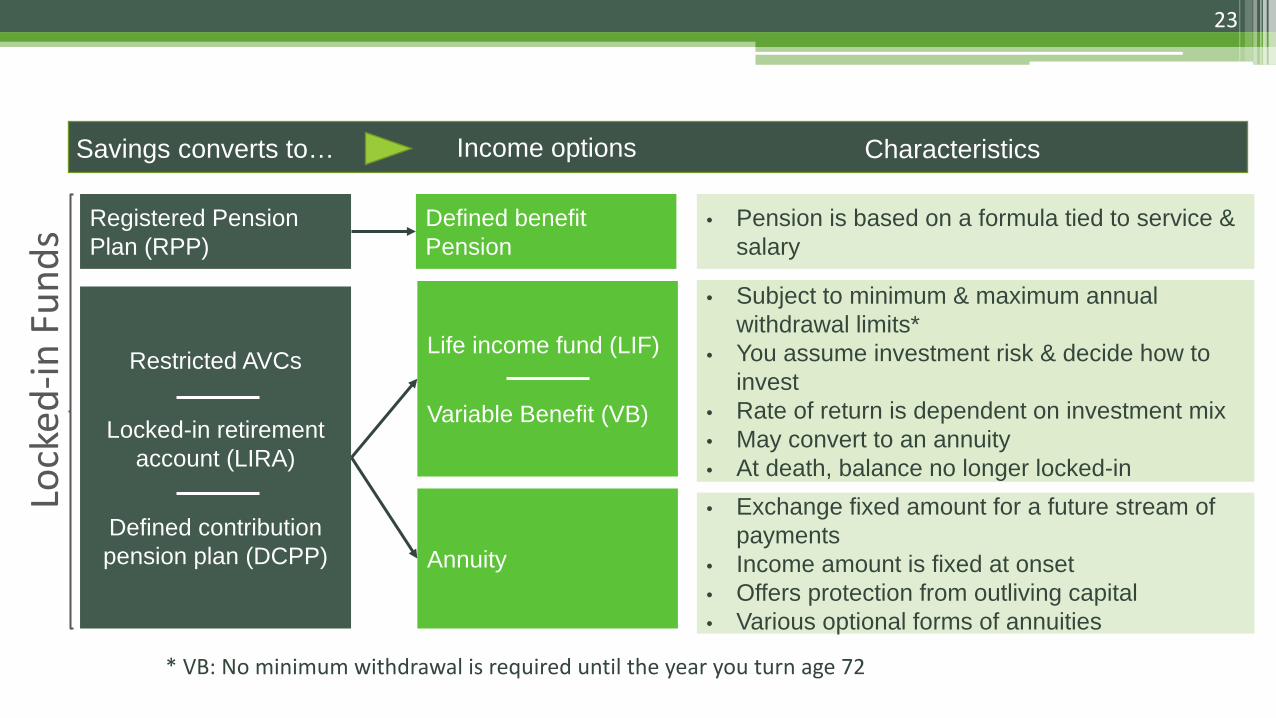

Savings converts to… Income options

Registered Pension Plan (RPP)

Defined benefit Pension

• Pension is based on a formula tied to service & salary

Restricted AVCs

Locked-in retirement account (LIRA)

Defined contribution pension plan (DCPP)

Life income fund (LIF)

Variable Benefit (VB)

• Subject to minimum & maximum annual withdrawal limits*

• You assume investment risk & decide how to invest

• Rate of return is dependent on investment mix• May convert to an annuity• At death, balance no longer locked-in

Lock

ed-in

Fun

ds

Characteristics

Annuity

• Exchange fixed amount for a future stream of payments

• Income amount is fixed at onset• Offers protection from outliving capital• Various optional forms of annuities

23

* VB: No minimum withdrawal is required until the year you turn age 72

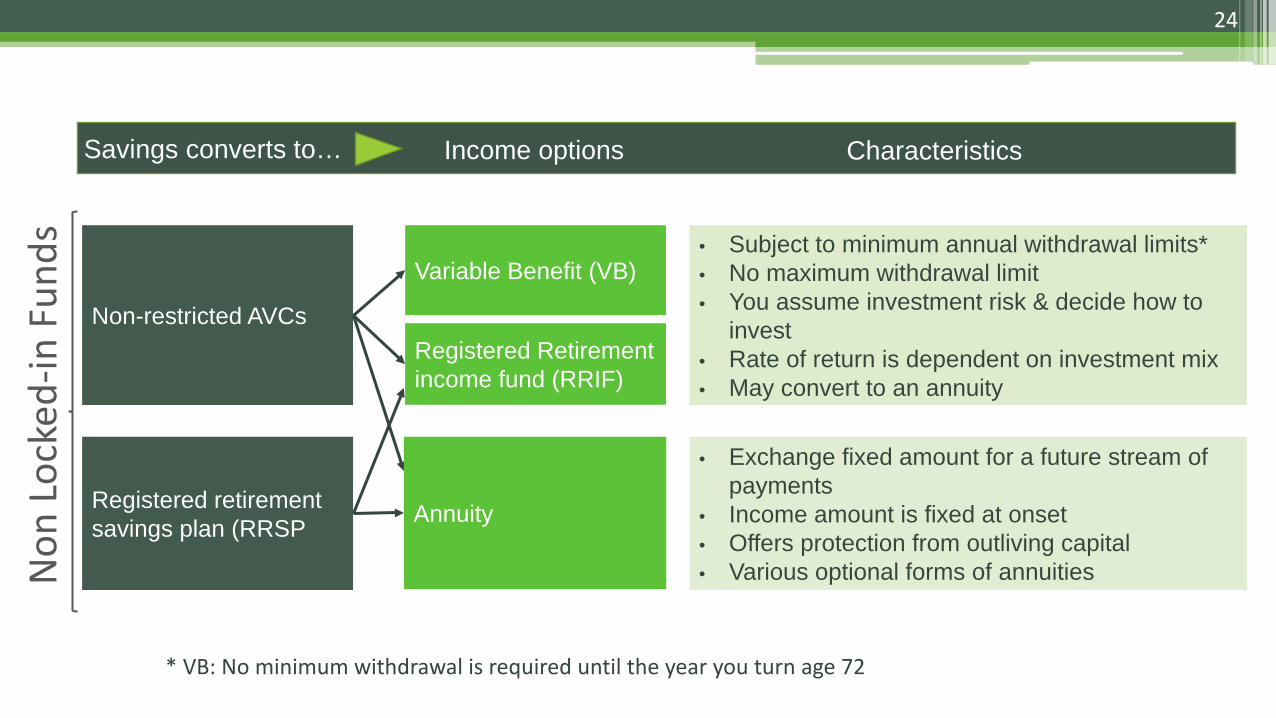

Savings converts to… Income options Characteristics

Non-restricted AVCs

Variable Benefit (VB)• Subject to minimum annual withdrawal limits*• No maximum withdrawal limit• You assume investment risk & decide how to

invest• Rate of return is dependent on investment mix• May convert to an annuity

Registered Retirement income fund (RRIF)

Non

Loc

ked-

in F

unds

Annuity

• Exchange fixed amount for a future stream of payments

• Income amount is fixed at onset• Offers protection from outliving capital• Various optional forms of annuities

Registered retirementsavings plan (RRSP

24

* VB: No minimum withdrawal is required until the year you turn age 72

Characteristics

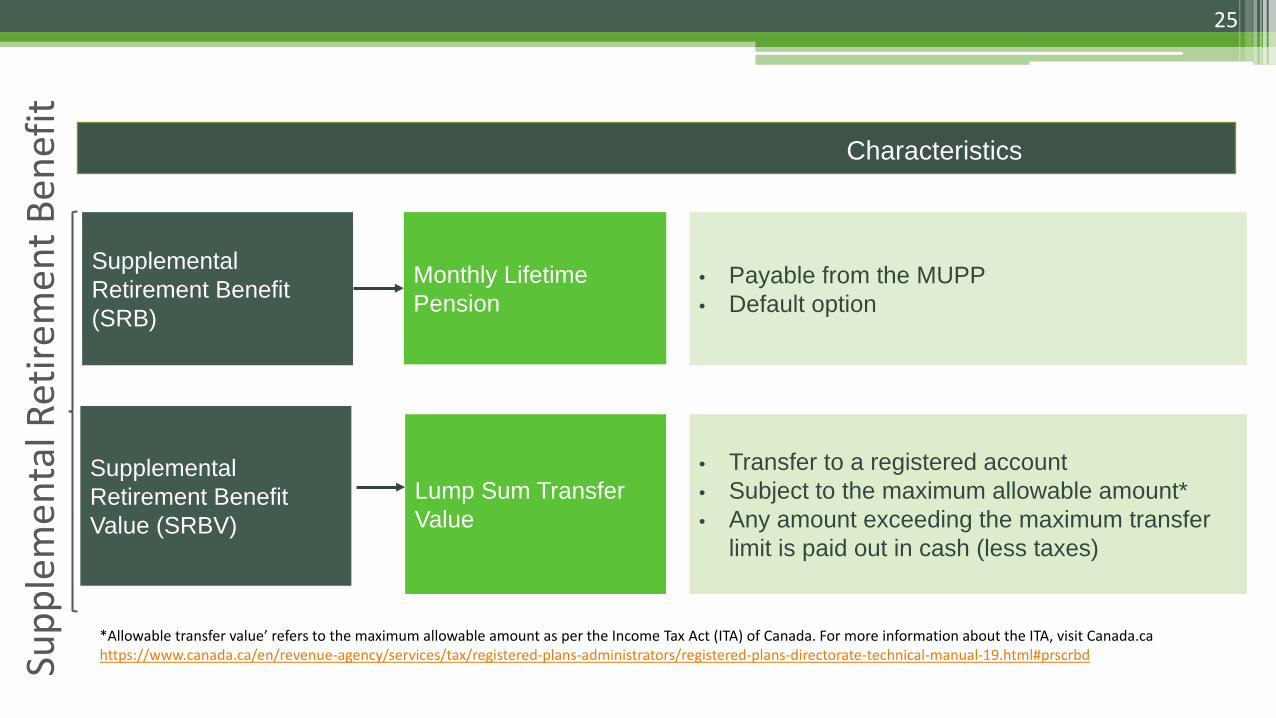

Supplemental Retirement Benefit Value (SRBV)

Lump Sum TransferValue

• Transfer to a registered account• Subject to the maximum allowable amount*• Any amount exceeding the maximum transfer

limit is paid out in cash (less taxes)

Supp

lem

enta

l Ret

irem

ent B

enef

it

Monthly Lifetime Pension

• Payable from the MUPP• Default option

Supplemental Retirement Benefit (SRB)

25

*Allowable transfer value’ refers to the maximum allowable amount as per the Income Tax Act (ITA) of Canada. For more information about the ITA, visit Canada.cahttps://www.canada.ca/en/revenue-agency/services/tax/registered-plans-administrators/registered-plans-directorate-technical-manual-19.html#prscrbd

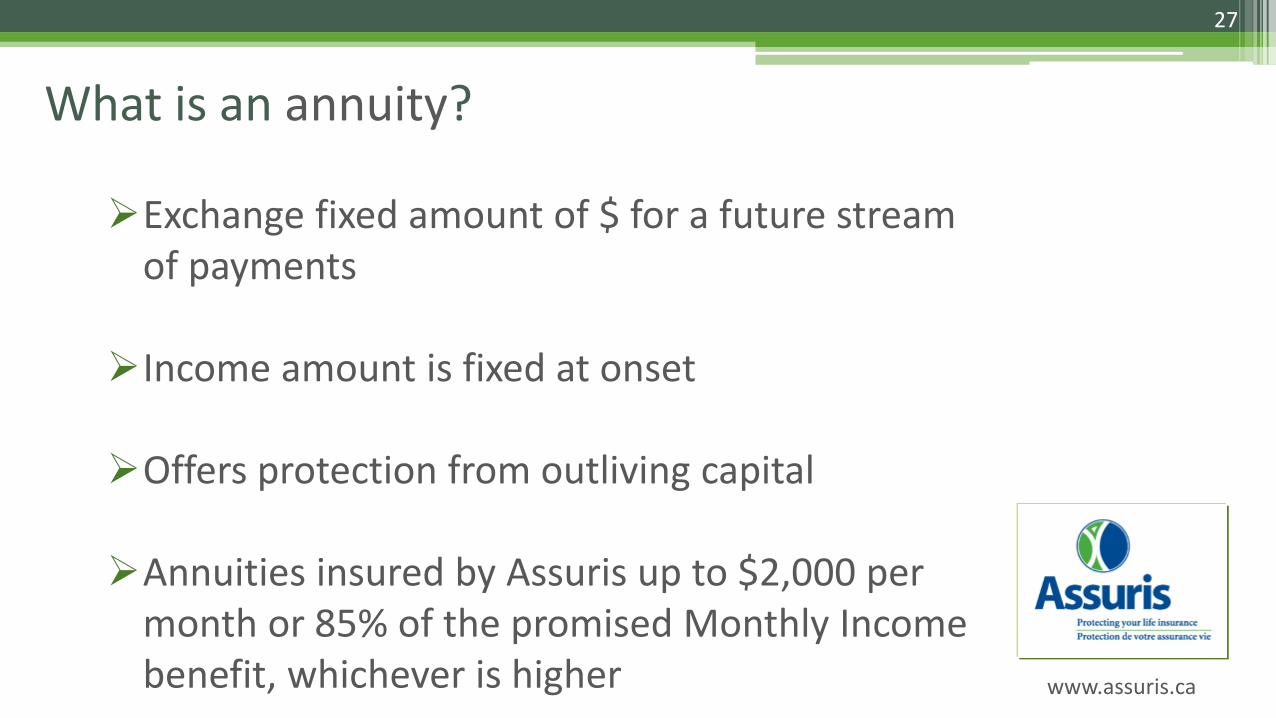

Exchange fixed amount of $ for a future stream of payments

Income amount is fixed at onset

Offers protection from outliving capital

Annuities insured by Assuris up to $2,000 per month or 85% of the promised Monthly Income benefit, whichever is higher

27

What is an annuity?

www.assuris.ca

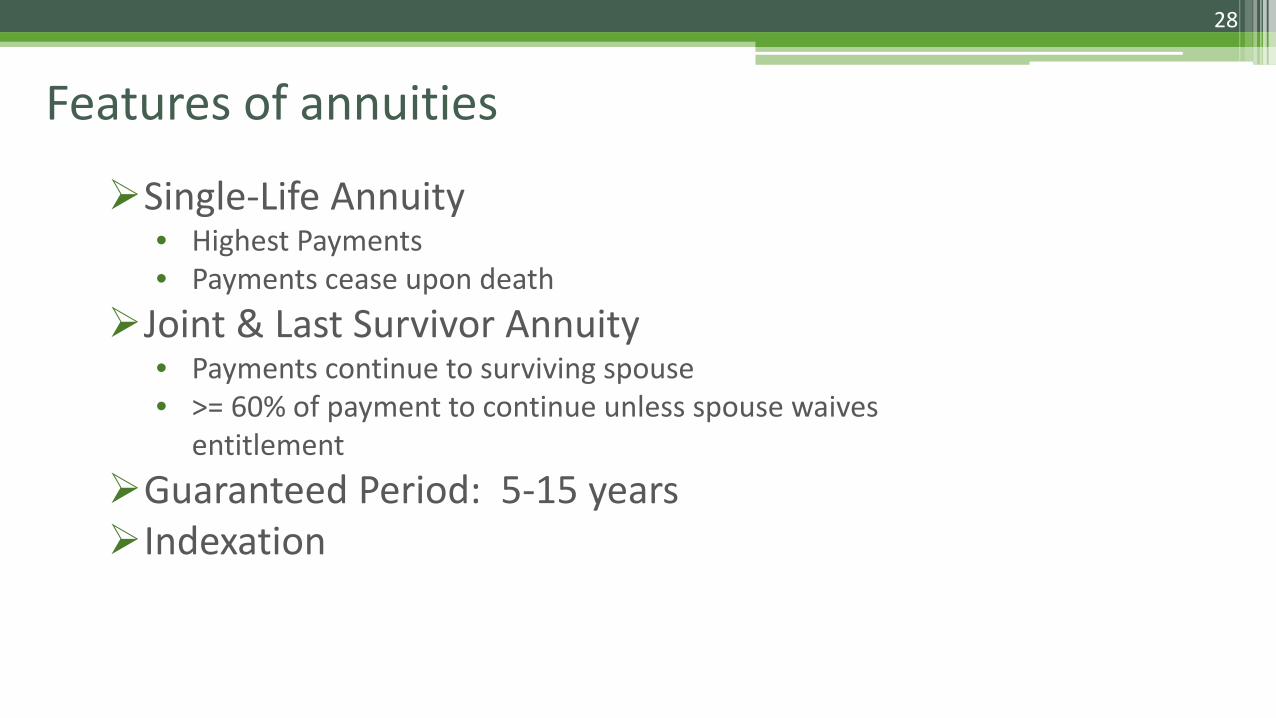

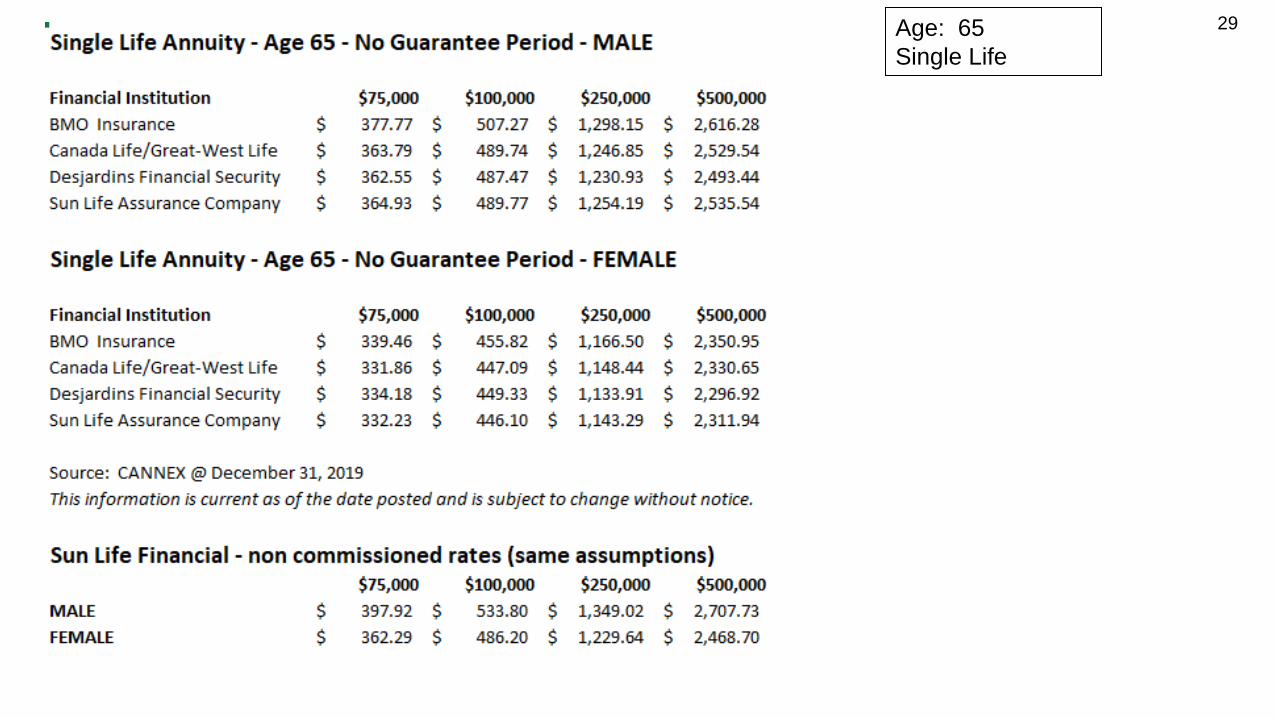

Single-Life Annuity• Highest Payments• Payments cease upon death

Joint & Last Survivor Annuity• Payments continue to surviving spouse• >= 60% of payment to continue unless spouse waives

entitlementGuaranteed Period: 5-15 yearsIndexation

28

Features of annuities

29Age: 65Single Life

31

What is a Supplemental Retirement Benefit (SRB)?

Settlement option if you are entitled to the SRBV arising from the defined benefit minimum provision

You may now select a monthly lifetime pension option, payable from the MUPP

Previously this additional amount was only payable at the time of settlement as a transfer to an authorized instrument

No action is needed until you are ready to settle

Please ask any questions you may have by “using the chat”

Any questions not answered during the session can be emailed to: [email protected].

34

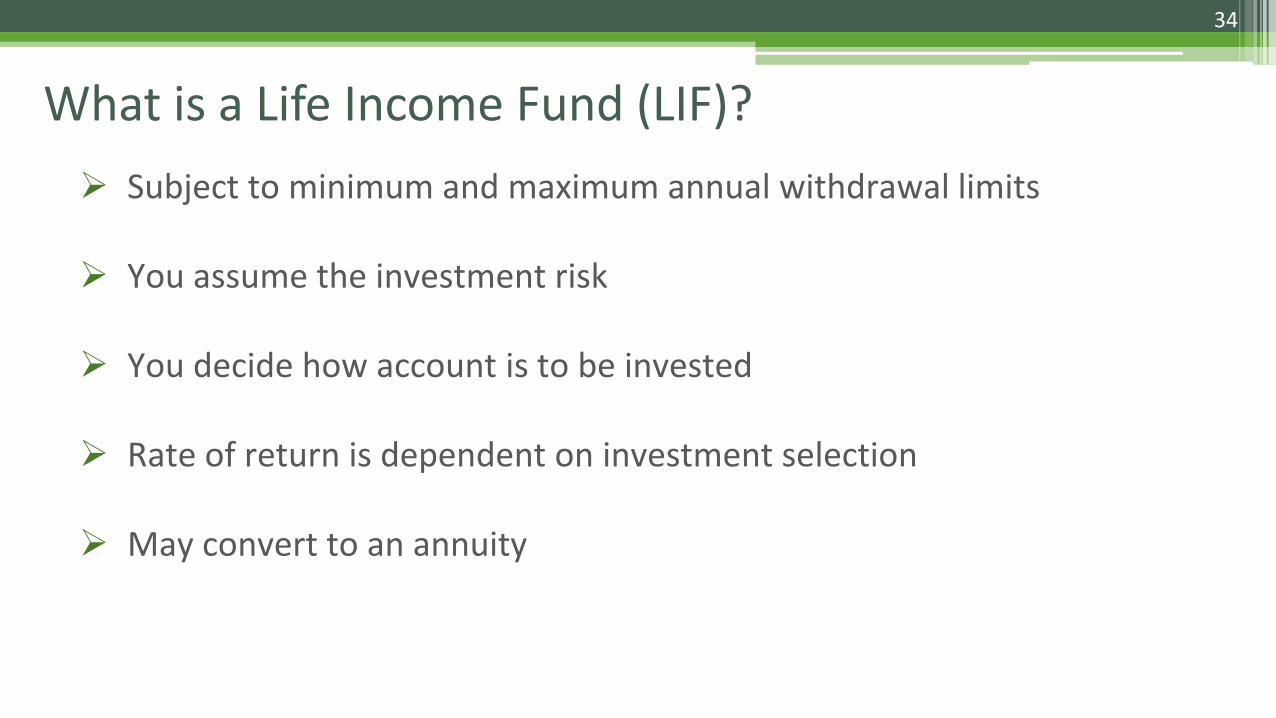

Subject to minimum and maximum annual withdrawal limits

You assume the investment risk

You decide how account is to be invested

Rate of return is dependent on investment selection

May convert to an annuity

What is a Life Income Fund (LIF)?

35

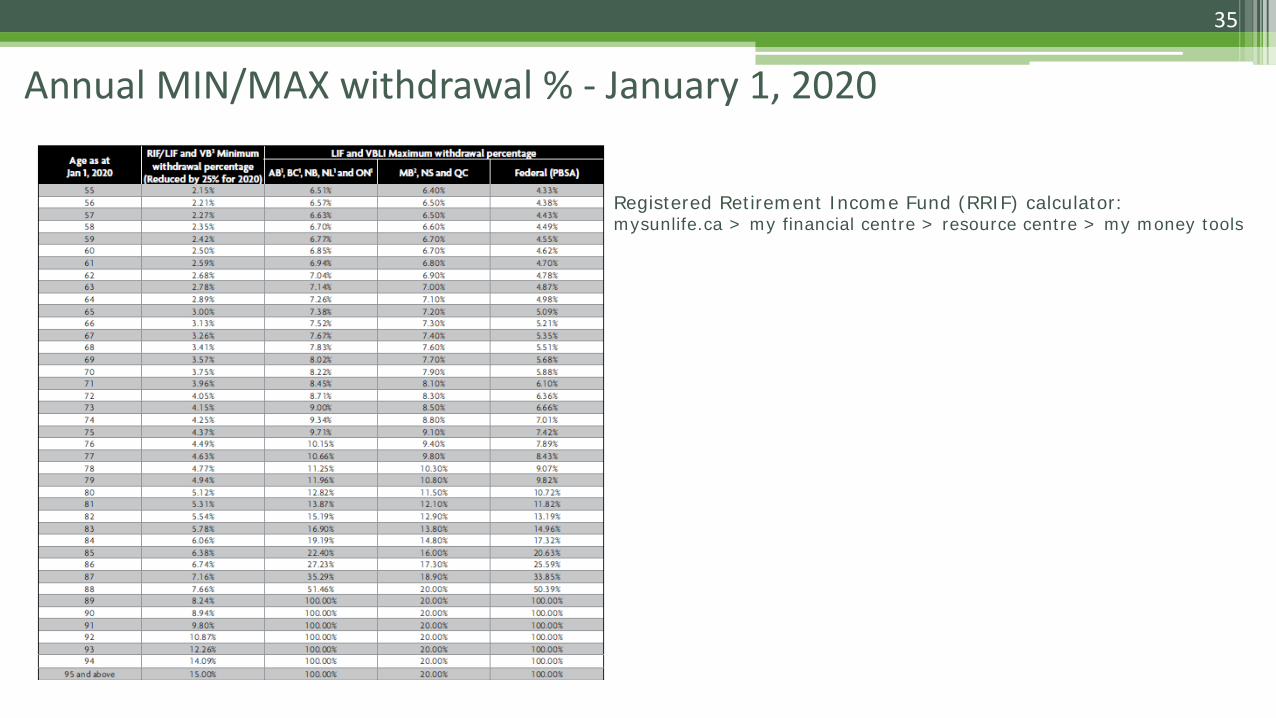

Annual MIN/MAX withdrawal % - January 1, 2020

Registered Retirement Income Fund (RRIF) calculator:mysunlife.ca > my financial centre > resource centre > my money tools

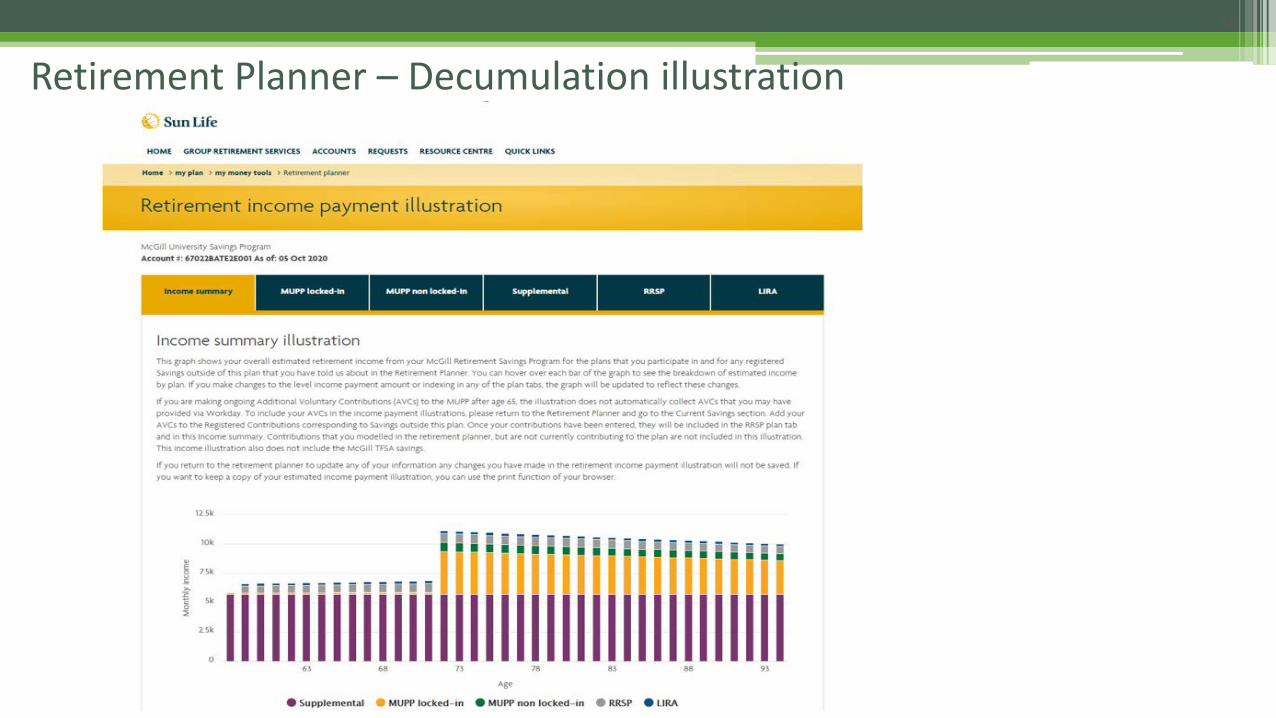

Retirement Planner – Decumulation illustration 36

Group LIF/RRIF38

Who is eligible?• Active Members (over age 65) and Inactive Members (55 or more) who have yet

to settle• Retired and/or terminated members who recently transferred out to LIF/RRIF

with a financial institution and whose funds continue to be administered under Quebec legislation

What are some of the advantages?• Access to RRIF for non-locked-in holdings• Easy to use website• Ability to transfer in external RRIFs/LIFs

What is a Variable Benefit?• A decumulation phase settlement option• Allows member to receive a life income type payment directly from the

McGill University Pension Plan (MUPP)• Member retains access to:▫ The investment lineup of the MUPP▫ Lower investment management fees as compared to retail products

Who is eligible for a Variable Benefit?• Inactive members of the MUPP who are 55 years or over;

• Active & inactive members of the MUPP who are 71 and who must convert their holdings into a retirement income prior to year-end

• Former members over age 55, who recently transferred out their holdings which continue to be administered under the Quebec Supplemental Pension Plans Act

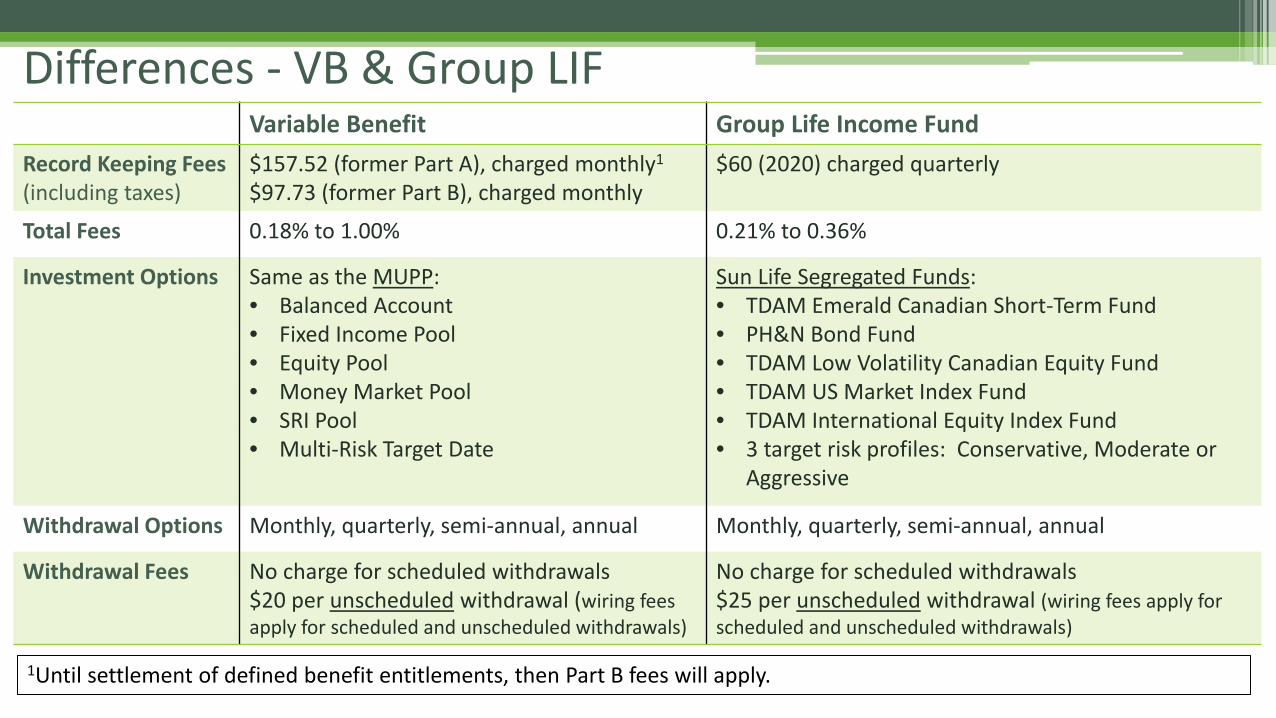

Differences - VB & Group LIFVariable Benefit Group Life Income Fund

Record Keeping Fees(including taxes)

$157.52 (former Part A), charged monthly1

$97.73 (former Part B), charged monthly$60 (2020) charged quarterly

Total Fees 0.18% to 1.00% 0.21% to 0.36%

Investment Options Same as the MUPP:• Balanced Account• Fixed Income Pool• Equity Pool• Money Market Pool• SRI Pool• Multi-Risk Target Date

Sun Life Segregated Funds:• TDAM Emerald Canadian Short-Term Fund• PH&N Bond Fund• TDAM Low Volatility Canadian Equity Fund• TDAM US Market Index Fund• TDAM International Equity Index Fund• 3 target risk profiles: Conservative, Moderate or

Aggressive

Withdrawal Options Monthly, quarterly, semi-annual, annual Monthly, quarterly, semi-annual, annual

Withdrawal Fees No charge for scheduled withdrawals$20 per unscheduled withdrawal (wiring fees apply for scheduled and unscheduled withdrawals)

No charge for scheduled withdrawals$25 per unscheduled withdrawal (wiring fees apply for scheduled and unscheduled withdrawals)

1Until settlement of defined benefit entitlements, then Part B fees will apply.

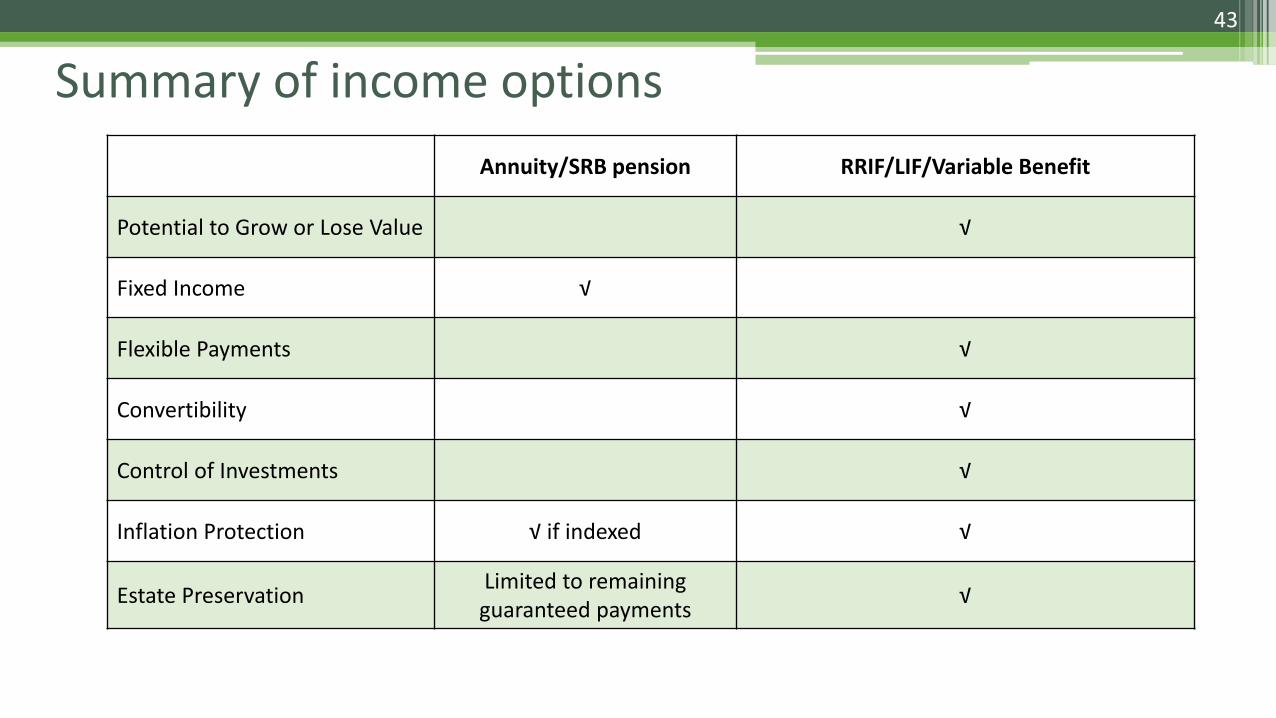

Summary of income options43

Annuity/SRB pension RRIF/LIF/Variable Benefit

Potential to Grow or Lose Value √

Fixed Income √

Flexible Payments √

Convertibility √

Control of Investments √

Inflation Protection √ if indexed √

Estate Preservation Limited to remaining guaranteed payments √

Other preferential arrangements – LIF & annuities

44

Sun Life Financial1-855-864-5989 between8:00 a.m. and 8:00 p.m ESTevery business dayWebsite: www.sunlife.ca

For more information: http://www.mcgill.ca/hr/pensions/mupp/settlement

45

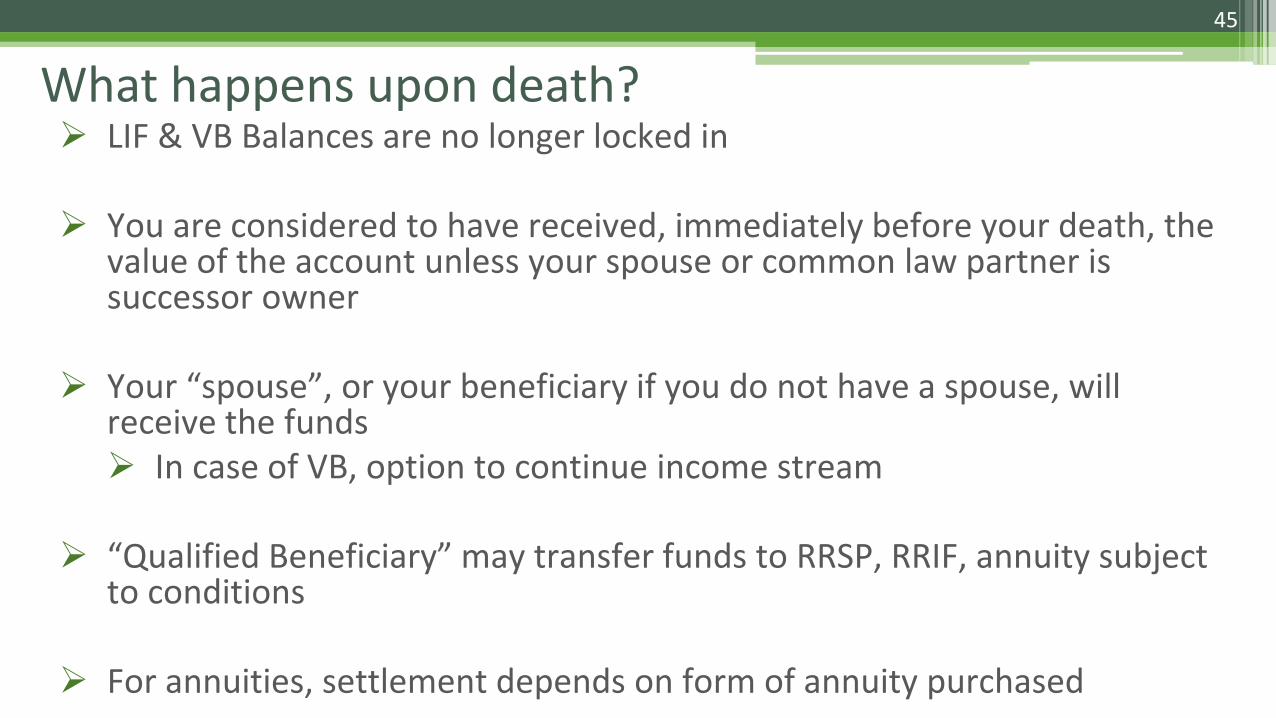

LIF & VB Balances are no longer locked in

You are considered to have received, immediately before your death, the value of the account unless your spouse or common law partner is successor owner

Your “spouse”, or your beneficiary if you do not have a spouse, will receive the funds In case of VB, option to continue income stream

“Qualified Beneficiary” may transfer funds to RRSP, RRIF, annuity subject to conditions

For annuities, settlement depends on form of annuity purchased

What happens upon death?

Topics include:

The risks associated with the payout phase of retirement• Cash flow, inflation & purchasing power, rates of return, longevity

The settlement options available How to review your investment strategy What are your sources of income during retirement and which should be

withdrawn first

***Highly recommended that you have previously attended a Settlement Options or Retirement Information Session

To Register: http://www.mcgill.ca/hr/pensions/mupp/sessions

46

Decumulation Session – to be scheduled in early 2021

Please ask any questions you may have by “using the chat”

Any questions not answered during the session can be emailed to: [email protected].