Embed Size (px)

Citation preview

Measuring Inter-Industry Financial Transmission of Shocks

October 25th 2006

Daniel Paravisini

Columbia University GSB

Federal Deposit Insurance Corporation – CRF 2006 Fall Workshop

Work in Progress Report

Motivation Financial intermediaries may transmit real shocks

across industries Loan/equity losses weaken bank balance sheets and induce

decline in supply of credit (Holmstrom and Tirole (1997))

Natural experiment evidence: Peek and Rosengren (1997) Chava and Purnanandam (2006), Gan (2006)

Open questions: Cross section: Through which banks? Within banks: Change with bank characteristics (derivatives,

securitization)? Time series: Change with the business cycle, monetary policy?

This Presentation

Methodology to measure financial transmission more generally

Reduced form approach Compare firms that differ according to the

exposure of their lenders to shocks

Illustrate with application Measure the financial transmission of the

Telecoms defaults in 2002 (WorldCom, Adelphia)

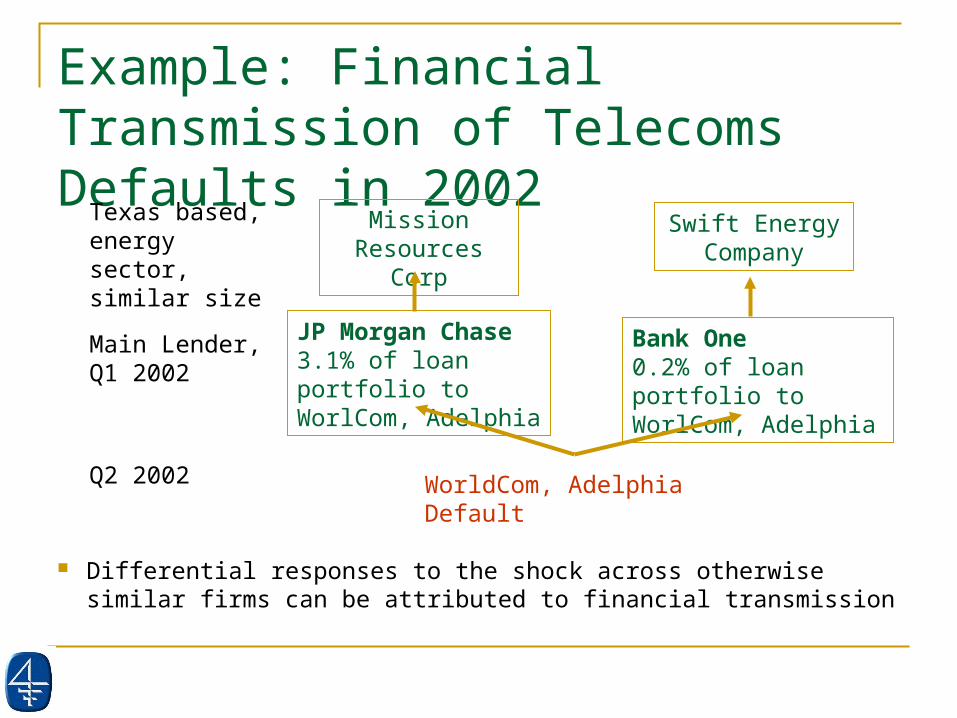

Example: Financial Transmission of Telecoms Defaults in 2002

Mission Resources Corp

Swift Energy Company

JP Morgan Chase 3.1% of loan portfolio to WorlCom, Adelphia

Bank One 0.2% of loan portfolio to WorlCom, Adelphia

Main Lender, Q1 2002

Texas based, energy sector, similar size

Differential responses to the shock across otherwise similar firms can be attributed to financial transmission

WorldCom, Adelphia DefaultQ2 2002

Main Potential Concerns Data requirements

Bank loan portfolio composition Link firms to their lenders

Dealscan

Sample: large banks, public firms Requires differences in bank exposures Hedging by banks and firms

Fraction of lending may overestimate exposure (credit derivatives, loans sales)

Multiple sources of capital

Potentially find no effect

Results from Telecoms Application Banks exposed to defaults reduce supply of

credit Firms experience a 3 percentage point decline in leverage

if their lenders had high exposure to WorldCom/Adelphia before defaults

Heterogeneity across banks Smaller/none for banks with larger use of credit derivatives

Roadmap

Data and variable definition Dealscan, Call Reports, Compustat Proxy for industry composition of loan portfolios Descriptive statistics

Application: transmission of Telecoms defaults Classify banks by exposure to Adelphia/Worldcom Classify firms by exposure of their lenders Firm level specification Results

Conclusions and next steps

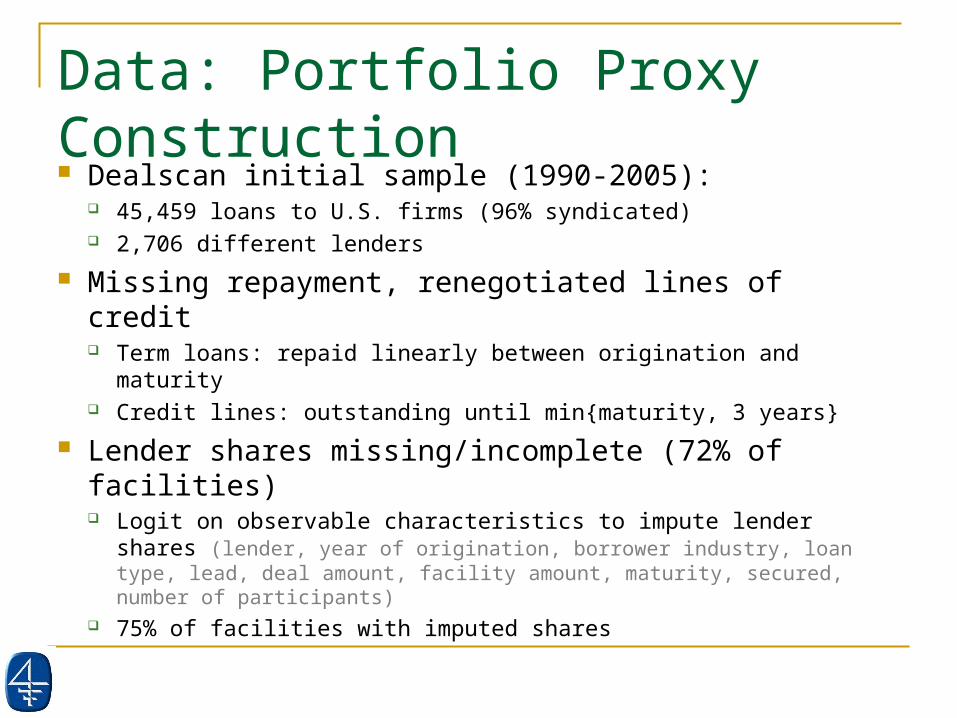

Data: Portfolio Proxy Construction Dealscan initial sample (1990-2005):

45,459 loans to U.S. firms (96% syndicated) 2,706 different lenders

Missing repayment, renegotiated lines of credit Term loans: repaid linearly between origination and maturity Credit lines: outstanding until min{maturity, 3 years}

Lender shares missing/incomplete (72% of facilities) Logit on observable characteristics to impute lender shares

(lender, year of origination, borrower industry, loan type, lead, deal amount, facility amount, maturity, secured, number of participants)

75% of facilities with imputed shares

Descriptive Statistics: Portfolio Proxy Calculate amount outstanding for every

firm/bank/quarter Implied by imputed lender shares and repayment schedule

by facility

Total outstanding by bank/quarter: Average 52.3% of C&I loans from Call Reports using the

1995 to 2004 sample

Substantial time series and cross sectional variation in industry composition of portfolios

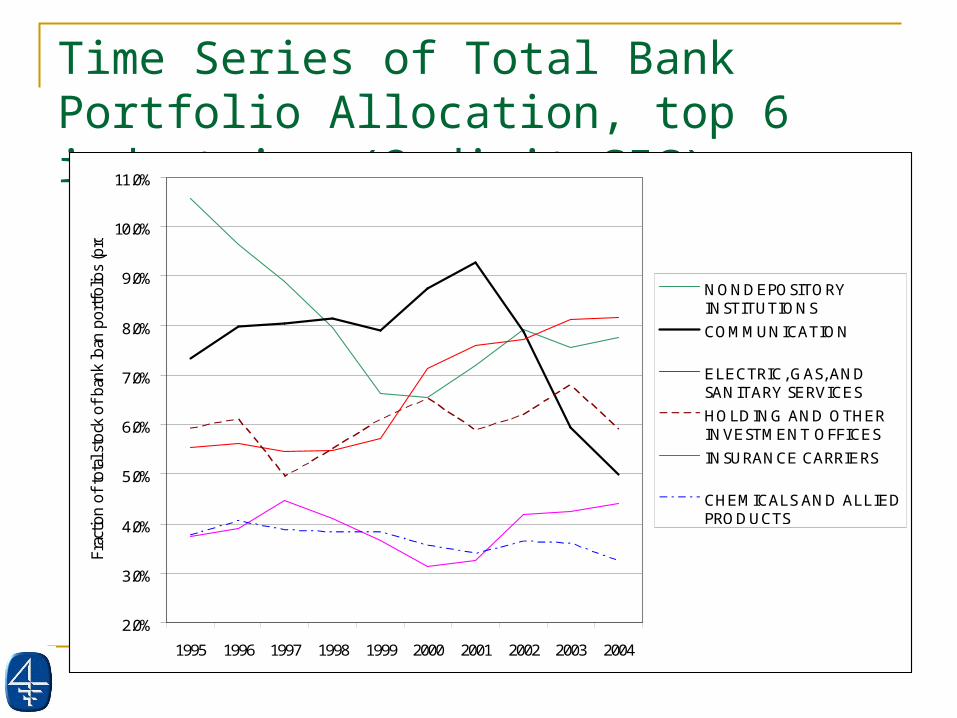

Time Series of Total Bank Portfolio Allocation, top 6 industries (2-digit SIC)

2.0%

3.0%

4.0%

5.0%

6.0%

7.0%

8.0%

9.0%

10.0%

11.0%

1995 1996 1997 1998 1999 2000 2001 2002 2003 2004

Frac

tion

of to

tal s

tock

of ba

nk lo

an p

ortfol

ios

(pro

xy)

NONDEPOSITORYINSTITUTIONS

COMMUNICATION

ELECTRIC, GAS, ANDSANITARY SERVICES

HOLDING AND OTHERINVESTMENT OFFICES

INSURANCE CARRIERS

CHEMICALS AND ALLIEDPRODUCTS

0.05

.1.15

mea

n of

fsto

ck

NO

ND

EPO

SITO

RY IN

STIT

UTI

ON

S

CHEM

ICAL

S AN

D A

LLIE

D P

ROD

UCT

S

HO

LDIN

G A

ND

OTH

ER IN

VEST

MEN

T O

FFIC

ES

ELEC

TRO

NIC

& O

THER

ELE

CTRI

C EQ

UIP

MEN

T

INSU

RAN

CE C

ARRI

ERS

IND

UST

RIAL

MAC

HIN

ERY

AND

EQ

UIPM

ENT

FOO

D A

ND

KIN

DRE

D P

ROD

UCTS

COM

MUN

ICAT

ION

ELEC

TRIC

, GAS

, AN

D S

ANIT

ARY

SERV

ICES

0.05

.1.15

mea

n of

fsto

ck

HO

TELS

AN

D O

THER

LO

DG

ING

PLA

CES

WH

OLE

SALE

TRA

DE

- DUR

ABLE

GO

OD

S

BUSI

NES

S SE

RVIC

ES

INSU

RAN

CE C

ARRI

ERS

HO

LDIN

G A

ND

OTH

ER IN

VEST

MEN

T O

FFIC

ES

ELEC

TRIC

, GAS

, AN

D S

ANIT

ARY

SERV

ICES

COM

MUN

ICAT

ION

NO

ND

EPO

SITO

RY IN

STIT

UTIO

NS

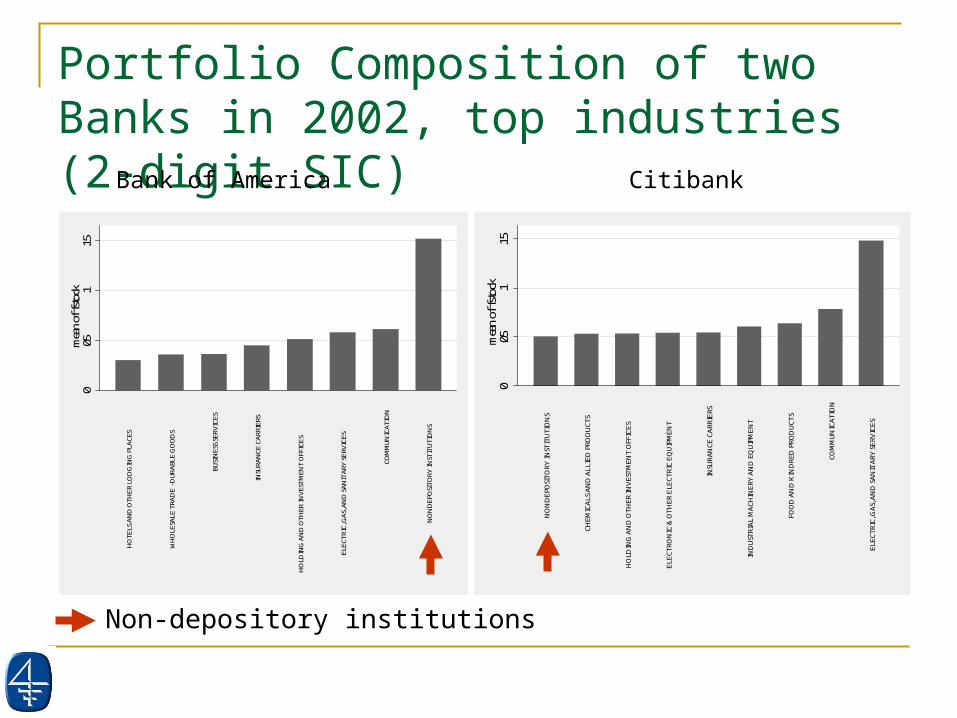

Portfolio Composition of two Banks in 2002, top industries (2-digit SIC)

Bank of America

Non-depository institutions

Citibank

0.05

.1.15

mea

n of

fsto

ck

NO

ND

EPO

SITO

RY IN

STIT

UTI

ON

S

CHEM

ICAL

S AN

D A

LLIE

D P

ROD

UCT

S

HO

LDIN

G A

ND

OTH

ER IN

VEST

MEN

T O

FFIC

ES

ELEC

TRO

NIC

& O

THER

ELE

CTRI

C EQ

UIP

MEN

T

INSU

RAN

CE C

ARRI

ERS

IND

UST

RIAL

MAC

HIN

ERY

AND

EQ

UIPM

ENT

FOO

D A

ND

KIN

DRE

D P

ROD

UCTS

COM

MUN

ICAT

ION

ELEC

TRIC

, GAS

, AN

D S

ANIT

ARY

SERV

ICES

0.05

.1.15

mea

n of

fsto

ck

HO

TELS

AN

D O

THER

LO

DG

ING

PLA

CES

WH

OLE

SALE

TRA

DE

- DUR

ABLE

GO

OD

S

BUSI

NES

S SE

RVIC

ES

INSU

RAN

CE C

ARRI

ERS

HO

LDIN

G A

ND

OTH

ER IN

VEST

MEN

T O

FFIC

ES

ELEC

TRIC

, GAS

, AN

D S

ANIT

ARY

SERV

ICES

COM

MUN

ICAT

ION

NO

ND

EPO

SITO

RY IN

STIT

UTIO

NS

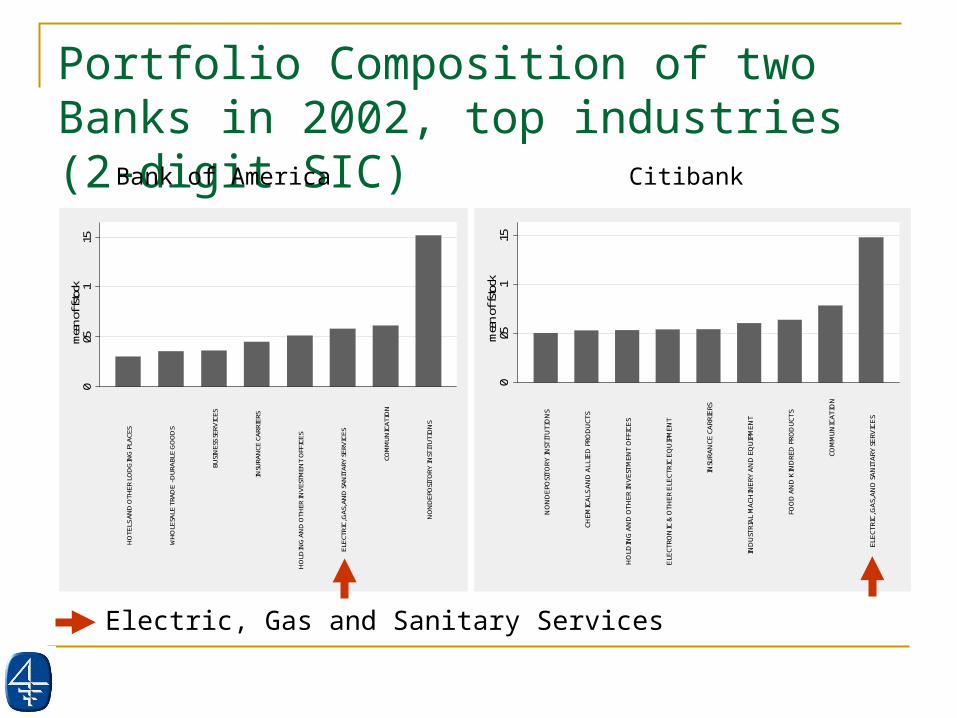

Portfolio Composition of two Banks in 2002, top industries (2-digit SIC)

Electric, Gas and Sanitary Services

Bank of America Citibank

Roadmap

Data and variable definition Dealscan, Call Reports, Compustat Proxy for industry composition of loan portfolios Descriptive statistics

Application: transmission of Telecoms defaults Classify banks by exposure to Adelphia/Worldcom Classify firms according to exposure of their lenders Firm level specification Results

Conclusions and next steps

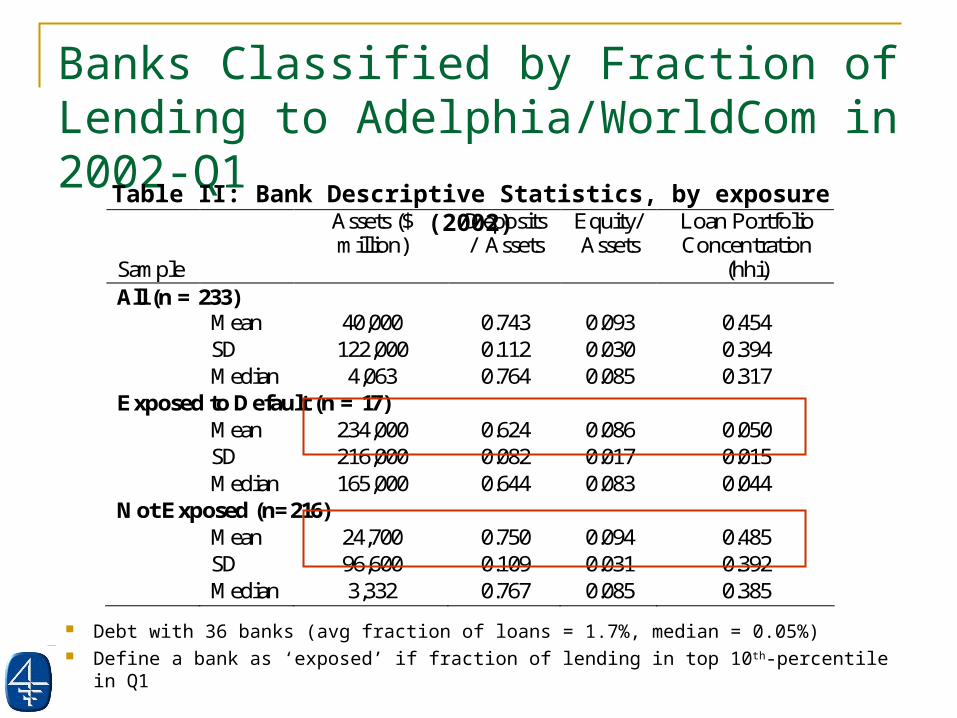

Banks Classified by Fraction of Lending to Adelphia/WorldCom in 2002-Q1

Debt with 36 banks (avg fraction of loans = 1.7%, median = 0.05%) Define a bank as ‘exposed’ if fraction of lending in top 10th-percentile in Q1

Sample

Assets ($ million)

Deposits/ Assets

Equity/ Assets

Loan Portfolio Concentration

(hhi) All (n = 233) Mean 40,000 0.743 0.093 0.454 SD 122,000 0.112 0.030 0.394 Median 4,063 0.764 0.085 0.317 Exposed to Default (n = 17) Mean 234,000 0.624 0.086 0.050 SD 216,000 0.082 0.017 0.015 Median 165,000 0.644 0.083 0.044 Not Exposed (n=216) Mean 24,700 0.750 0.094 0.485 SD 96,600 0.109 0.031 0.392 Median 3,332 0.767 0.085 0.385

Table II: Bank Descriptive Statistics, by exposure (2002)

Roadmap

Data and variable definition Dealscan, Call Reports, Compustat Proxy for industry composition of loan portfolios Descriptive statistics

Application: transmission of Telecoms defaults Classify banks by exposure to Adelphia/Worldcom Classify firms according to exposure of their lenders Firm level specification Results

Conclusions and next steps

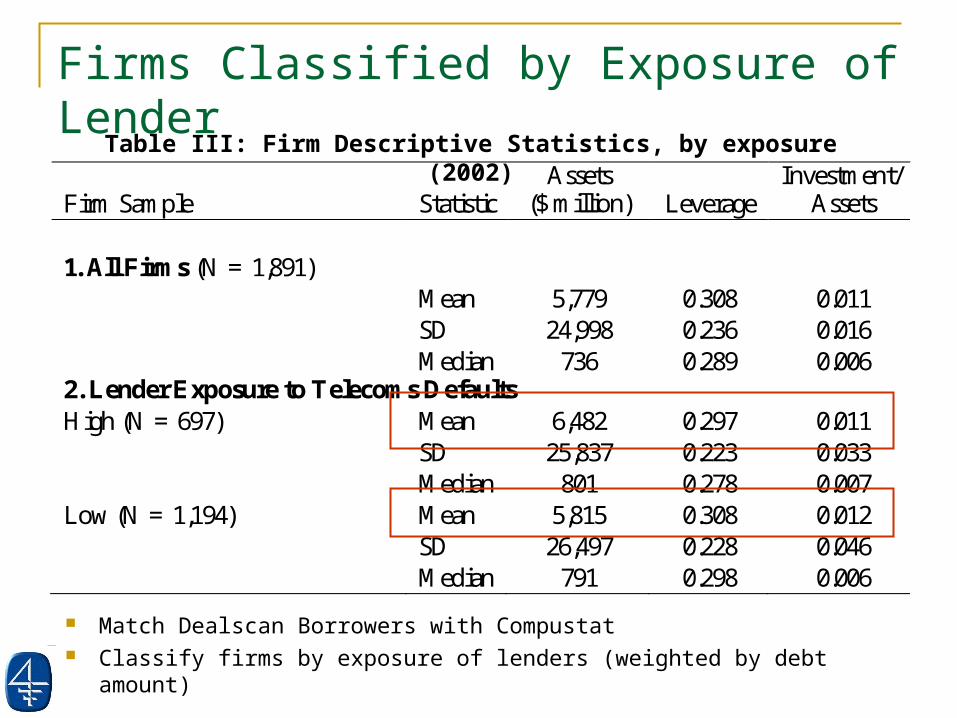

Firm Sample Statistic Assets

($ million) Leverage Investment/

Assets 1. All Firms (N = 1,891) Mean 5,779 0.308 0.011 SD 24,998 0.236 0.016 Median 736 0.289 0.006 2. Lender Exposure to Telecoms Defaults High (N = 697) Mean 6,482 0.297 0.011 SD 25,837 0.223 0.033 Median 801 0.278 0.007 Low (N = 1,194) Mean 5,815 0.308 0.012 SD 26,497 0.228 0.046 Median 791 0.298 0.006

Firms Classified by Exposure of Lender

Match Dealscan Borrowers with Compustat Classify firms by exposure of lenders (weighted by debt amount)

Table III: Firm Descriptive Statistics, by exposure (2002)

Roadmap

Data and variable definition Dealscan, Call Reports, Compustat Proxy for industry composition of loan portfolios Descriptive statistics

Application: transmission of Telecoms defaults Classify banks by exposure to Adelphia/Worldcom Classify firms by exposure of their lenders Firm level specification Results

Conclusions and next steps

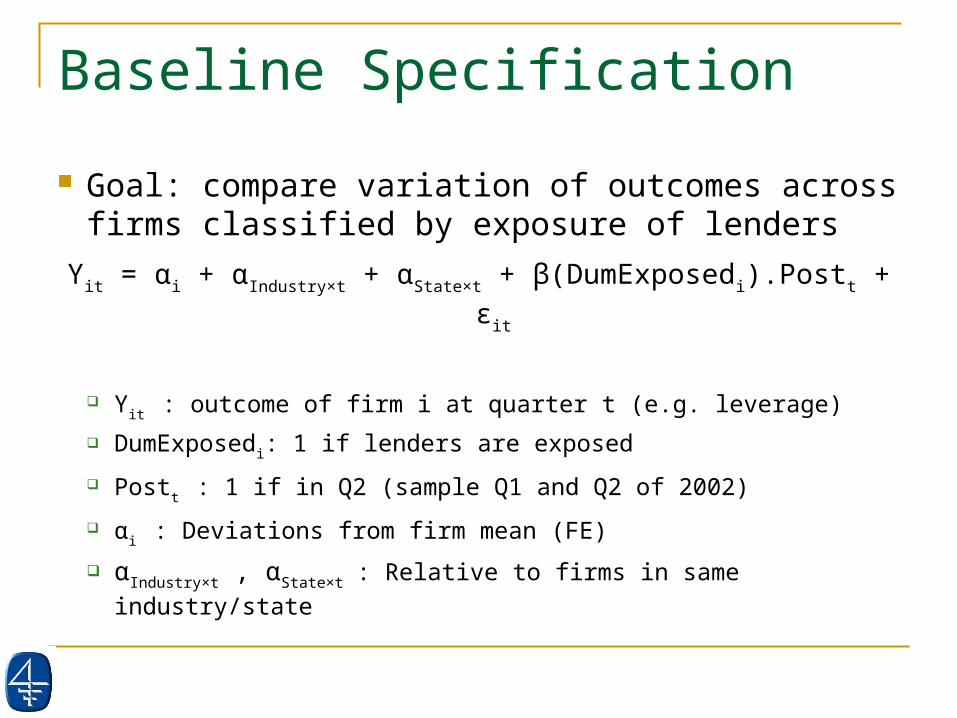

Baseline Specification

Goal: compare variation of outcomes across firms classified by exposure of lenders

Yit = αi + αIndustry×t + αState×t + β(DumExposedi).Postt + εit

Yit : outcome of firm i at quarter t (e.g. leverage)

DumExposedi: 1 if lenders are exposed

Postt : 1 if in Q2 (sample Q1 and Q2 of 2002)

αi : Deviations from firm mean (FE)

αIndustry×t , αState×t : Relative to firms in same industry/state

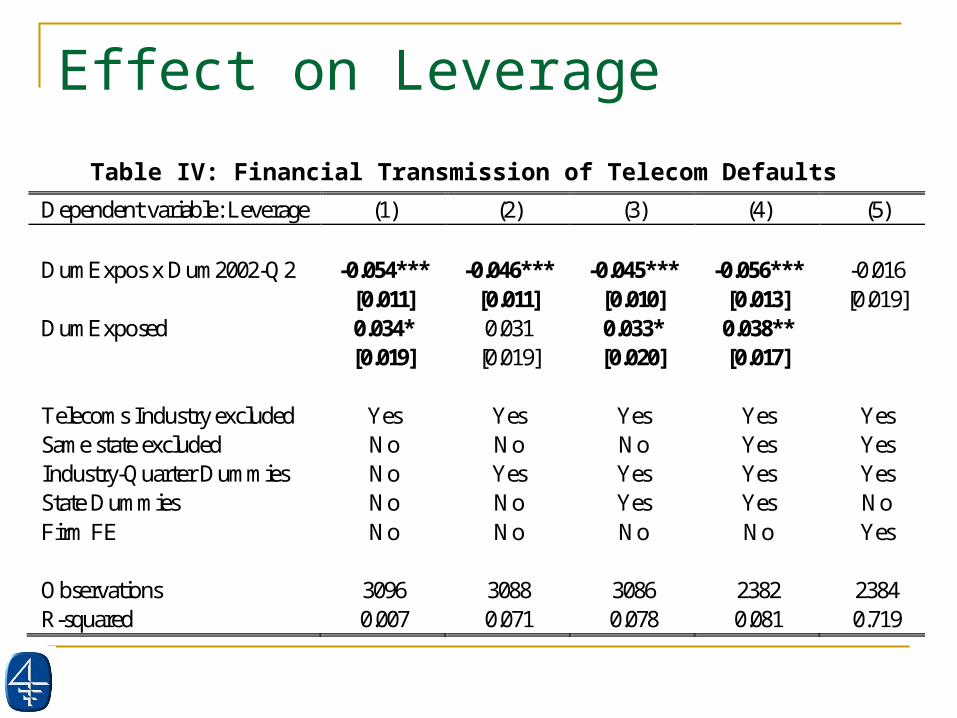

Effect on Leverage

Dependent variable: Leverage (1) (2) (3) (4) (5) DumExpos x Dum2002-Q2 -0.054*** -0.046*** -0.045*** -0.056*** -0.016 [0.011] [0.011] [0.010] [0.013] [0.019] DumExposed 0.034* 0.031 0.033* 0.038** [0.019] [0.019] [0.020] [0.017] Telecoms Industry excluded Yes Yes Yes Yes Yes Same state excluded No No No Yes Yes Industry-Quarter Dummies No Yes Yes Yes Yes State Dummies No No Yes Yes No Firm FE No No No No Yes Observations 3096 3088 3086 2382 2384 R-squared 0.007 0.071 0.078 0.081 0.719

Table IV: Financial Transmission of Telecom Defaults

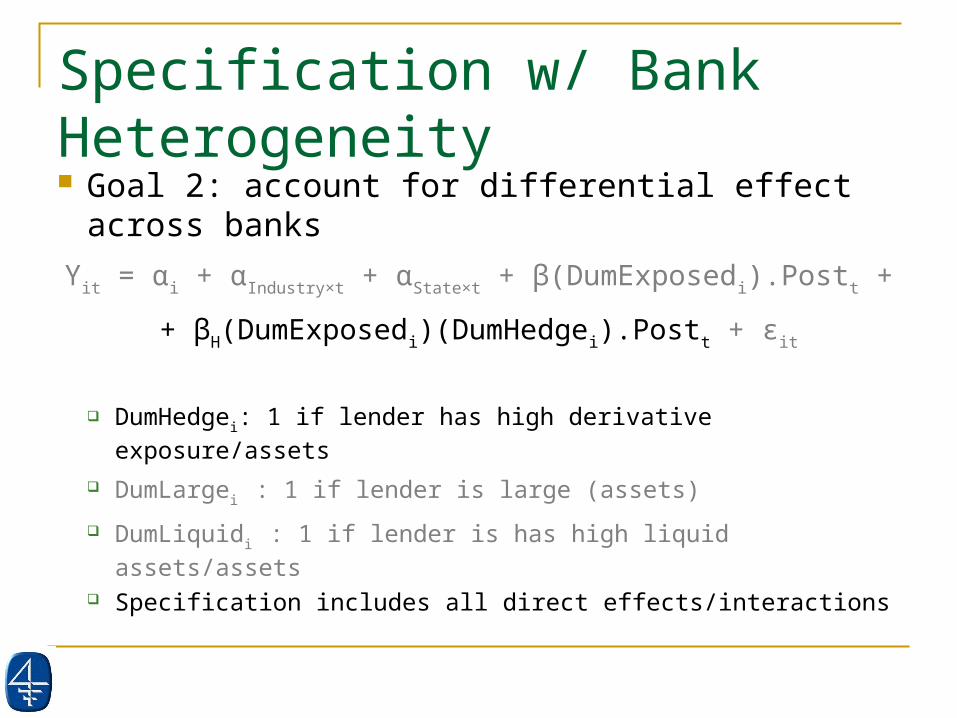

Specification w/ Bank Heterogeneity Goal 2: account for differential effect across banks

Yit = αi + αIndustry×t + αState×t + β(DumExposedi).Postt +

+ βH(DumExposedi)(DumHedgei).Postt + εit

DumHedgei: 1 if lender has high derivative exposure/assets

DumLargei : 1 if lender is large (assets)

DumLiquidi : 1 if lender is has high liquid assets/assets

Specification includes all direct effects/interactions

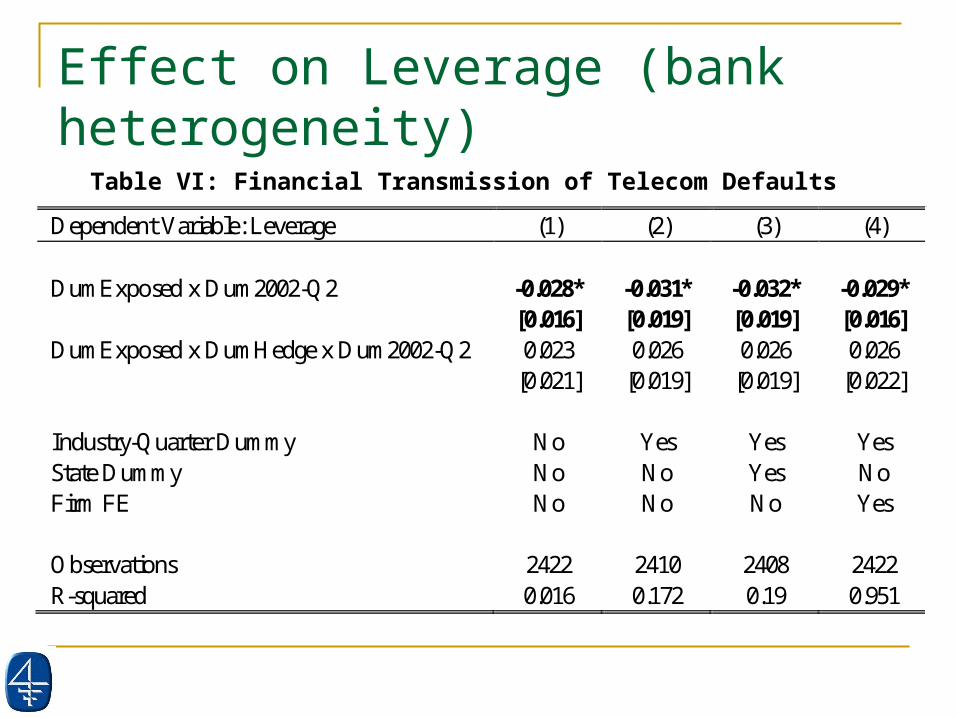

Effect on Leverage (bank heterogeneity)

Table VI: Financial Transmission of Telecom Defaults

Dependent Variable: Leverage (1) (2) (3) (4) DumExposed x Dum2002-Q2 -0.028* -0.031* -0.032* -0.029* [0.016] [0.019] [0.019] [0.016] DumExposed x DumHedge x Dum2002-Q2 0.023 0.026 0.026 0.026 [0.021] [0.019] [0.019] [0.022] Industry-Quarter Dummy No Yes Yes Yes State Dummy No No Yes No Firm FE No No No Yes Observations 2422 2410 2408 2422 R-squared 0.016 0.172 0.19 0.951

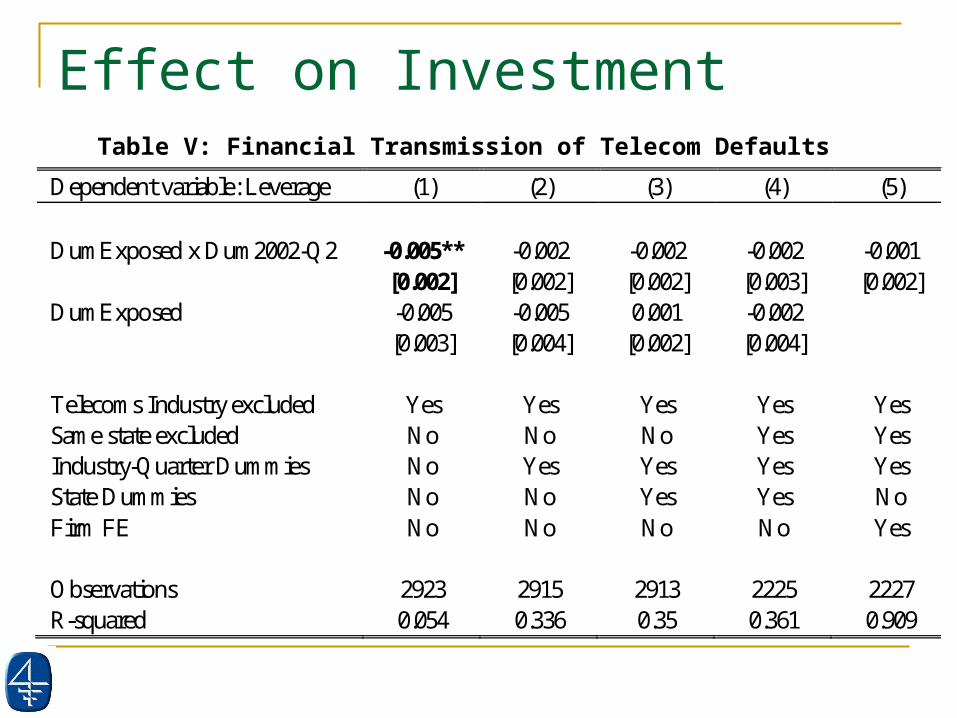

Effect on Investment

Dependent variable: Leverage (1) (2) (3) (4) (5) DumExposed x Dum2002-Q2 -0.005** -0.002 -0.002 -0.002 -0.001 [0.002] [0.002] [0.002] [0.003] [0.002] DumExposed -0.005 -0.005 0.001 -0.002 [0.003] [0.004] [0.002] [0.004] Telecoms Industry excluded Yes Yes Yes Yes Yes Same state excluded No No No Yes Yes Industry-Quarter Dummies No Yes Yes Yes Yes State Dummies No No Yes Yes No Firm FE No No No No Yes Observations 2923 2915 2913 2225 2227 R-squared 0.054 0.336 0.35 0.361 0.909

Table V: Financial Transmission of Telecom Defaults

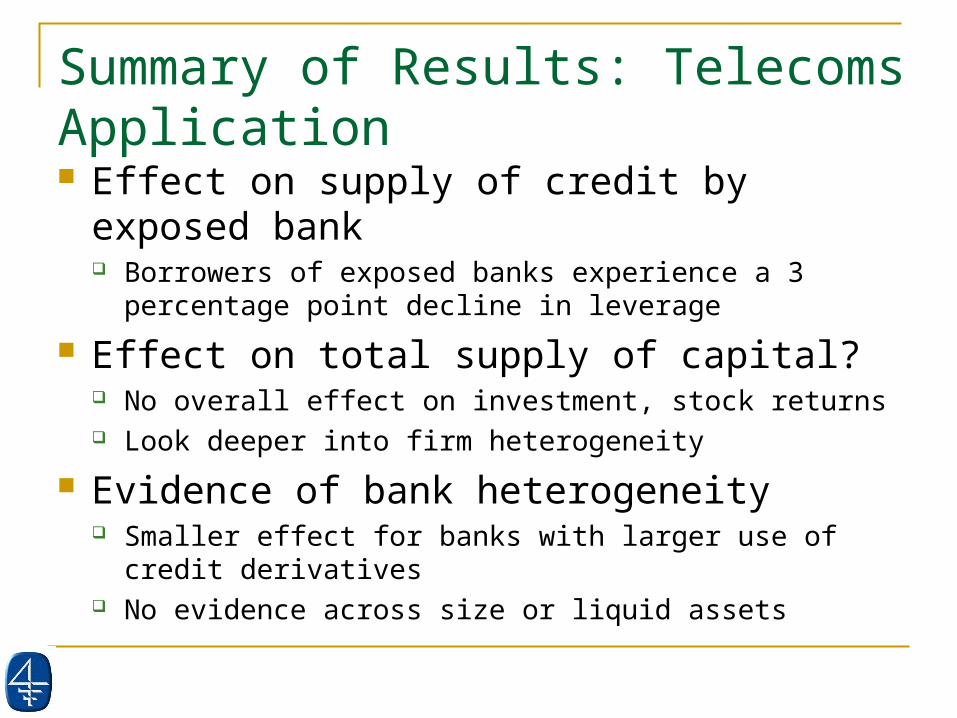

Summary of Results: Telecoms Application Effect on supply of credit by exposed bank

Borrowers of exposed banks experience a 3 percentage point decline in leverage

Effect on total supply of capital? No overall effect on investment, stock returns Look deeper into firm heterogeneity

Evidence of bank heterogeneity Smaller effect for banks with larger use of credit derivatives No evidence across size or liquid assets

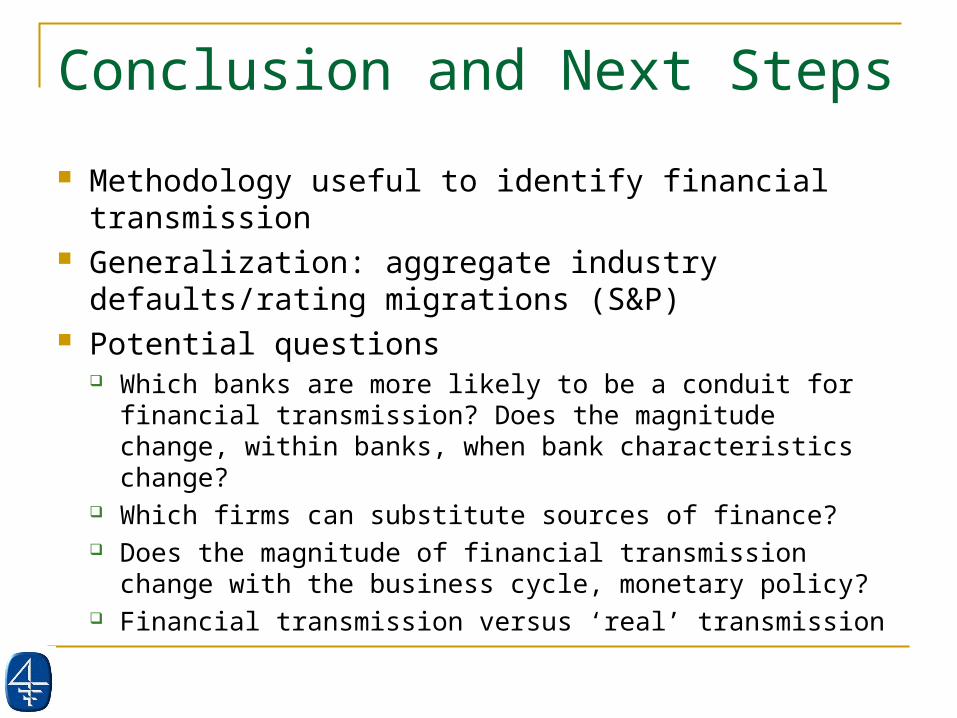

Conclusion and Next Steps

Methodology useful to identify financial transmission Generalization: aggregate industry defaults/rating

migrations (S&P) Potential questions

Which banks are more likely to be a conduit for financial transmission? Does the magnitude change, within banks, when bank characteristics change?

Which firms can substitute sources of finance? Does the magnitude of financial transmission change with

the business cycle, monetary policy? Financial transmission versus ‘real’ transmission

![GSB 550 RE GSB 550-2 - bosch-pt.co.kr0/user_manual_20024_2609140164.pdf · GSB 550 RE GSB 550-2 PROFESSIONAL ... [rpm] 2 500/3 000 0–3 000 0–3 000 Impact rate, max. [bpm]](https://img.pdfslide.net/doc/110x75/5b8439157f8b9a784a8bdcf8/gsb-550-re-gsb-550-2-bosch-ptcokr-0usermanual20024-gsb-550-re-gsb-550-2.jpg)